Financial Services Risk and Regulation - PwC · investment decisions and risk management. •...

12

Financial Services Risk and Regulation Regulatory updates newsletter December 2019

Transcript of Financial Services Risk and Regulation - PwC · investment decisions and risk management. •...

Financial Services Risk and Regulation

Regulatory updates newsletterDecember 2019

Regulatory Updates Newsletter — December 2019 PwC · 2

Executive

Summary

Managing ML/TF risks

associated with virtual

assets and virtual asset

service providers

SFC survey

findings on ESG,

climate change

and asset

management

Basel Committee report

on open banking and

application

programming interfaces

(APIs)

SFC circular on streamlined

requirements for eligible

exchange traded funds

adopting a master-feeder

structure

Basel Committee consultation on

credit valuation adjustment risk

and guiding principles on sectoral

countercyclical capital buffer

Guideline on

Medical

Insurance

Business

LIBOR

Reform

Updates

Other

Regulatory

Updates

Glossary

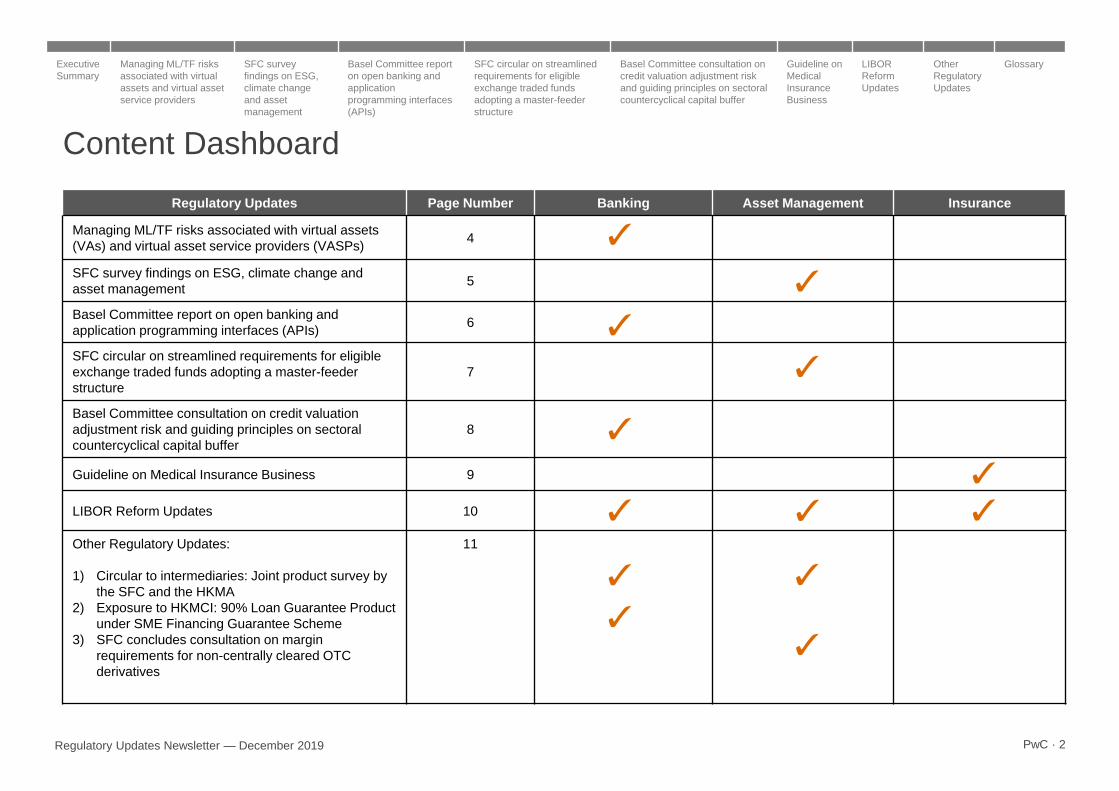

Content Dashboard

Regulatory Updates Page Number Banking Asset Management Insurance

Managing ML/TF risks associated with virtual assets

(VAs) and virtual asset service providers (VASPs)4

SFC survey findings on ESG, climate change and

asset management5

Basel Committee report on open banking and

application programming interfaces (APIs)6

SFC circular on streamlined requirements for eligible

exchange traded funds adopting a master-feeder

structure

7

Basel Committee consultation on credit valuation

adjustment risk and guiding principles on sectoral

countercyclical capital buffer

8

Guideline on Medical Insurance Business 9

LIBOR Reform Updates 10

Other Regulatory Updates:

1) Circular to intermediaries: Joint product survey by

the SFC and the HKMA

2) Exposure to HKMCI: 90% Loan Guarantee Product

under SME Financing Guarantee Scheme

3) SFC concludes consultation on margin

requirements for non-centrally cleared OTC

derivatives

11

Emily Lam

Partner

+852 2289 1247

PwC HK FS Risk and

Regulation

“As 2019 comes to a close, we discuss the

regulatory developments shaping the financial

services industry in Hong Kong. With this

newsletter, we will continue to keep you up to

speed with significant regulatory

developments across the financial services

industry.”

Regulatory Updates Newsletter — December 2019 PwC · 3

2019 has been a landmark year for

financial services regulations in Hong

Kong. We witnessed the first batch of

eight virtual banking licences issued, the

new regulatory regime for insurance

intermediaries came into operation and

the SFC provided guidance to

management companies of SFC-

authorised unit trusts and mutual funds on

enhanced disclosures for SFC authorised

green or ESG funds, amongst others.

The regulators kept the momentum up in

the month of December with several

important announcements. For instance,

the SFC announced waiving the annual

licensing fees for the financial year of

2020/21 in order to relieve the regulatory

cost burden on the securities and futures

industry having taken into account the

current challenging market environment.

In addition, LIBOR Reform has emerged

throughout the year on regulatory and risk

agendas. We have seen HKMA take

proactive actions during the year through

its circulars in March and October and

more recently issuing a survey to collect

information on the progress made by AIs

in their preparation to transition to

alternative reference rates. The survey,

requires responses by 23 December 2019.

It is encouraging to see increasing

awareness amongst banks in Hong Kong

which are starting to prioritise preparatory

work for the LIBOR transition.

Apart from these announcements, we

have discussed the following regulatory

updates in this edition of the newsletter:

• The HKMA has issued guidance to AIs

and stored value facility (SVF)

licensees in relation to recent updates

by the FATF to its Recommendation

15, which clarify the businesses and

activities that the FATF requirements

apply in the case of VAs and VASPs.

• The SFC released a report to present

the key findings of the industry-wide

survey to understand how and to what

extent licensed asset management

firms and leading institutional asset

owners consider ESG risks.

• The Basel Committee issued a report

on open banking and application

programming interfaces (APIs) that

monitors the evolving trend of open

banking observed in Basel Committee

member jurisdictions and discusses

the implications of these developments

on banks and banking supervision.

• The SFC issued a circular on

streamlined requirements for eligible

exchange traded funds adopting a

master-feeder structure.

• Moreover, the Basel Committee

launched a consultation on credit

valuation adjustment risk and issued

guiding principles on sectoral

countercyclical capital buffer.

• The IA has published GL31 –

Guideline on Medical Insurance

Business. The principal function of the

guideline is to regulate and supervise

the insurance industry for the

protection of existing and potential

policy holders.

• LIBOR Reform Updates: FCA

launched a consultation on extending

the senior managers regime to

benchmark administrators, ISDA letter

to FSB OSSG on pre-cessation issues,

and ISDA issued December 2019

Benchmark Fallbacks Supplemental

Consultation.

We also discuss other regulatory updates

such as the joint circular to intermediaries

by the SFC and the HKMA on product

survey. For further details on these

developments, please refer to the

following sections in this publication.

Emily Lam

FS Risk and Regulation

+852 2289 1247

Executive Summary

Executive

Summary

Managing ML/TF risks

associated with virtual

assets and virtual asset

service providers

SFC survey

findings on ESG,

climate change

and asset

management

Basel Committee report

on open banking and

application

programming interfaces

(APIs)

SFC circular on streamlined

requirements for eligible

exchange traded funds

adopting a master-feeder

structure

Basel Committee consultation

on credit valuation adjustment

risk and guiding principles on

sectoral countercyclical

capital buffer

Guideline on

Medical

Insurance

Business

LIBOR

Reform

Updates

Other

Regulatory

Updates

Glossary

Regulatory Updates Newsletter — December 2019 PwC · 4

AIs and SVF licensees must keep

abreast of international and local

developments to maintain an up-to-

date understanding of risks

The HKMA has issued a guidance to AIs

and stored value facility (SVF) licensees

in relation to recent updates by the FATF

to its Recommendation 15, which clarify

the businesses and activities that the

FATF requirements apply in the case of

VAs and VASPs.

FATF member jurisdictions have put in

place or are implementing regulatory

regimes for VASPs in response to the

international development. For example,

the SFC has recently announced a

framework allowing a VA trading

platform operator to opt-in to its

regulation.

Therefore, increasingly there may be

more VASPs which are licensed or

registered in Hong Kong or other

jurisdictions, and subject to AML/CFT

regulation and supervision in line with

the FATF Recommendations. Some

VASPs may be in the process of

applying for licensing or registration.

Key highlights of the guidance are:

• Following the risk-based approach,

when AIs and SVF licensees

establish and maintain business

relationships with VASPs, appropriate

risk assessments should be

conducted to differentiate the risks of

individual VASPs, recognising that

there is no “one-size-fits-all”.

• Depending on the nature of

relationship, AIs and SVF licensees

may undertake additional customer

due diligence measures, including

• the collection of sufficient

information to adequately

understand the nature of the

VASP’s business

• determining from publicly

available information whether

the VASP are licensed or

registered, and subject to

AML/CFT supervision; and

• assessing the AML/CFT

controls of the VASP as

appropriate.

• The extent of customer due diligence

measures should be commensurate

with the assessed ML/TF risks of the

VASP.

• In line with the FATF standards,

before an AI and / or SVF licensee

offers any new products relating to

VAs, it should undertake ML/TF risk

assessment.

Managing ML/TF risks associated with virtual assets (VAs) and virtual

asset service providers (VASPs)

Hokee Fu

Partner

+852 2289 2721

Executive

Summary

Managing ML/TF risks

associated with virtual

assets and virtual asset

service providers

SFC survey

findings on ESG,

climate change

and asset

management

Basel Committee report

on open banking and

application

programming interfaces

(APIs)

SFC circular on streamlined

requirements for eligible

exchange traded funds

adopting a master-feeder

structure

Basel Committee consultation

on credit valuation adjustment

risk and guiding principles on

sectoral countercyclical

capital buffer

Guideline on

Medical

Insurance

Business

LIBOR

Reform

Updates

Other

Regulatory

Updates

Glossary

Regulatory Updates Newsletter — December 2019 PwC · 5

PwC was engaged as a consultant to

conduct the survey and analyse the

findings for the SFC

From March to September 2019, the SFC

conducted an industry-wide survey to

understand how and to what extent

licensed asset management firms and

leading institutional asset owners

consider environmental, social and

governance (ESG) risks, particularly

those relating to climate change. The

issued report presents the key findings

and discusses the way forward.

The survey forms part of the SFC’s

Strategic Framework for Green Finance,

published in September 2018.

Key survey findings are:

• Consideration of ESG factors,

including climate change: Of the

firms surveyed, 83% (660) of those

actively involved in asset management,

considered at least one environmental,

social and governance factor in order

to understand a company’s investment

potential and facilitate better

investment decisions and risk

management.

• Governance and oversight: To

improve the financial performance of

investment portfolios and satisfy client

demand, 35% of the 660 asset

management firms which considered

ESG factors have implemented a

consistent approach to systemically

integrate ESG factors in their

investment and risk management

processes, rather than doing so on an

ad-hoc basis.

• Investment management: Asset

management firms which systemically

integrate ESG factors most often use

investment strategies such as

negative and exclusionary screening,

corporate engagement, shareholder

action and ESG integration.

• Risk management: Those asset

management firms which systemically

integrate ESG factors have put in

place risk management controls, such

as incident monitoring mechanisms to

flag major ESG incidents, so that

portfolio managers adjust investment

portfolios as appropriate.

• Disclosure: Although 660 asset

management firms reported giving

general consideration to ESG factors,

a majority, 68%, indicated that

information about their own ESG

practices was not available.

• Market trends: Survey results also

show that asset management firms of

various sizes, including small firms in

terms of AUM, have ESG investment

processes relating to research and

portfolio management.

To help firms move forward and more

closely align the SFC’s regulatory regime

with global standards, the SFC intends to

deliver three outcomes in the near term:

• To set expectations of asset

management firms in areas such as

governance and oversight, investment

management, risk management and

disclosure, focusing on environmental

risks with an emphasis on climate

change;

• To provide practical guidance, best

practices and training in collaboration

with the industry and relevant

stakeholders to enhance the capacity

of asset management firms to meet

the SFC’s expectations; and

• To establish an industry group to

exchange views amongst the SFC and

experts in environmental and climate

risks, as well as sustainable finance.

SFC survey findings on ESG, climate change and asset management

Sammie Leung

Partner

+852 2289 3188

Executive

Summary

Managing ML/TF risks

associated with virtual

assets and virtual asset

service providers

SFC survey

findings on ESG,

climate change

and asset

management

Basel Committee report

on open banking and

application

programming interfaces

(APIs)

SFC circular on streamlined

requirements for eligible

exchange traded funds

adopting a master-feeder

structure

Basel Committee consultation

on credit valuation adjustment

risk and guiding principles on

sectoral countercyclical

capital buffer

Guideline on

Medical

Insurance

Business

LIBOR

Reform

Updates

Other

Regulatory

Updates

Glossary

Regulatory Updates Newsletter — December 2019 PwC · 6

Basel Committee report on open banking and application programming

interfaces (APIs)Open banking brings potential benefits but also risks and

challenges to customers, banks and the banking system

The report on open banking and application programming

interfaces (APIs) monitors the evolving trend of open banking

observed in Basel Committee member jurisdictions and

discusses the implications of these developments for banks

and banking supervision. It builds upon the findings of the

Committee's Sound Practices paper on "Implications of fintech

developments for banks and bank supervisors".

The key findings of open banking frameworks and related

challenges identified for banks and bank supervisors are:

• Traditional banking is evolving into open banking

• Open banking frameworks vary across jurisdictions in

terms of stage of development, approach and scope

• Data privacy laws can provide a foundation for an open

banking framework

• Multi-disciplinary features of open banking may require

greater regulatory coordination

Some key challenges identified for banks and supervisors are:

• Adapting to the potential changes in business models

• Ensuring data and cyber security in an open banking

framework

• Some of the challenges hindering the development of APIs

to share customer -permissioned data include the time and

cost to build and maintain APIs and the lack of commonly

accepted API standards

• Oversight of third parties can be limited, especially in cases

where banks have no contractual relationship with the third

party, or where the third party itself has no regulatory

authorisation

• Assigning liability in the event of financial loss, or in the

event of erroneous sharing or loss of sensitive data, is

more complex with open banking, as more parties are

involved

• Banks may face reputational risk, even in jurisdictions

where there are established liability rules

Gary Ng

Partner

+852 2289 2967

Brian Yiu

Partner

+852 2289 1934

Executive

Summary

Managing ML/TF risks

associated with virtual

assets and virtual asset

service providers

SFC survey

findings on ESG,

climate change

and asset

management

Basel Committee report

on open banking and

application

programming interfaces

(APIs)

SFC circular on streamlined

requirements for eligible

exchange traded funds

adopting a master-feeder

structure

Basel Committee consultation

on credit valuation adjustment

risk and guiding principles on

sectoral countercyclical

capital buffer

Guideline on

Medical

Insurance

Business

LIBOR

Reform

Updates

Other

Regulatory

Updates

Glossary

Regulatory Updates Newsletter — December 2019 PwC · 7

SFC circular on streamlined requirements for eligible exchange traded

funds adopting a master-feeder structure

Carlyon Knight-Evans

Partner

+852 2289 2711

carlyon.knight-

Helen Li

Partner

+852 2289 2741

Executive

Summary

Managing ML/TF risks

associated with virtual

assets and virtual asset

service providers

SFC survey

findings on ESG,

climate change

and asset

management

Basel Committee report

on open banking and

application

programming interfaces

(APIs)

SFC circular on streamlined

requirements for eligible

exchange traded funds

adopting a master-feeder

structure

Basel Committee consultation

on credit valuation adjustment

risk and guiding principles on

sectoral countercyclical

capital buffer

Guideline on

Medical

Insurance

Business

LIBOR

Reform

Updates

Other

Regulatory

Updates

Glossary

The SFC is prepared to consider

authorising an index tracking feeder

ETF that invests in an overseas-listed

master ETF without SFC

authorisation on a case-by-case basis

Currently, index tracking exchange

traded fund (ETF) adopting a master-

feeder structure is permitted under the

Code on Unit Trusts and Mutual Funds

(UT Code) provided that both the feeder

ETF and the master ETF are authorized

by the SFC. Recently, the SFC has

received a number of requests to allow

more flexibility in the master-feeder ETF

structure so that an SFC-authorized

feeder ETF may invest its assets in an

overseas-listed master ETF without SFC

authorization. This would facilitate the

development of ETF product line-up in a

more cost-effective manner, offering

more investment choices to investors.

In response to the requests received, the

SFC has proposed the following

requirements under which it would

consider authorising such a feeder ETF.

The master ETF should, at a minimum,

meet the following key requirements:

• The master ETF must be a scheme

regulated in a recognized jurisdiction

managed by a management company

in an acceptable inspection regime or

a scheme eligible under a mutual

recognition of funds arrangement;

• The master ETF, together with its

management company and

trustee/custodian, must have a good

compliance record with the rules and

regulations of its home jurisdiction

and (in the case of master ETF) the

listing venue;

• The master ETF must have a fund

size of not less than USD 1 billion

and a track record of more than 5

years at the time of the feeder ETF’s

listing on the Stock Exchange of

Hong Kong;

• The master ETF must adopt physical

replication of the underlying index

through either a full replication or a

representative sampling strategy; and

• The master ETF’s engagement in

securities financing transactions

should not exceed 50% of its total net

asset value unless there are

comparable safeguards and

disclosure.

In addition, the feeder ETF should meet

the following requirements:

• The feeder ETF must be a Hong

Kong-domiciled ETF authorized by

the SFC;

• The feeder ETF must be managed by

a management company which is

licensed or registered for Type 9

regulated activity and has a good

compliance record;

• The management company of the

feeder ETF should report to the SFC

as soon as practicable if the master

ETF ceases to comply with the

requirements set out in this circular

and take appropriate remedial action

to promptly rectify the situation; and

• The management company of the

feeder ETF should put in place

appropriate arrangements to inform

Hong Kong investors of any material

change to, or event that has a

significant adverse impact on, the

master ETF in a timely manner.

Regulatory Updates Newsletter — December 2019 PwC · 8

The consultation is open for

comments till 25 February 2020

Improvements to the capital framework

to better capture credit valuation

adjustment (CVA) risk is one of the key

elements of the Basel Committee's

overall efforts to reform global regulatory

standards in response to the global

financial crisis.

This consultation document proposes a

set of targeted adjustments to the CVA

risk framework issued in December 2017.

These revisions aim to align relevant

parts of the revised CVA risk framework

with the Minimum capital requirements

for market risk published in January

2019 as well as Capital requirements for

bank exposures to central counterparties.

In addition, the Committee seeks

feedback on a possible adjustment to the

overall calibration of capital

requirements calculated under the CVA

standardised and basic approaches.

The proposed standards text has been

prepared in a new modular format that

adopts the style of the Basel framework .

In addition, the BCBS issued the Basel

III standard which includes a

countercyclical capital buffer (CCyB)

regime. National authorities can

implement a CCyB requirement to

ensure that the banking system has an

additional buffer of capital to protect

against potential future losses related to

downturns in the credit cycle.

Sectoral countercyclical capital buffer

(SCCyB) is a useful complement to the

CCyB. The impact of a SCCyB would

depend on a bank's exposure to a

targeted credit segment (eg, residential

real estate loans). Targeted tools such

as the SCCyB may be effective to aid in

building resilience early and in a specifc

manner, to more efficiently minimise

unintended side effects, and may be

used more flexibly than broad-based

tools.

These guiding principles are intended to

support the implementation of a SCCyB

on a consistent basis across jurisdictions.

The guiding principles are not included in

the Basel standards and are only

applicable for those jurisdictions that

choose to implement them on a

voluntarily basis.

Also, to help ensure a consistent

implementation of the new local IRRBB

framework, the HKMA has issued

answers to some additional FAQs. All

AIs not exempted from the new local

IRRBB framework are encouraged to

make reference to these FAQs for their

IRRBB compliance. The HKMA has also

included an updated version of the

spreadsheet containing calculation

examples for the completion of the

IRRBB return.

One of the key highlights of the FAQs is

that AIs must assess Credit Spread Risk

in the Banking Book (CSRBB) for items

at fair value, that is, for example, debt

securities. It is the AI’s responsibility to

develop a suitable methodology for

CSRBB.

In addition, the HKMA issued a circular

titled ‘Market Risk Capital Requirements:

Local Implementation Timeline’. The

standards on Minimum Capital

Requirements for Market Risk issued by

the Basel Committee on 14 January

2019 are scheduled to be implemented

by national supervisors by 1 January

2022. According to the latest BCBS

timetable, banks would be required to

calculate their market risk based on the

new standards from 1 January 2022.

Basel Committee consultation on credit valuation adjustment risk and

guiding principles on sectoral countercyclical capital buffer

Brian Yiu

Partner

+852 2289 1934

Executive

Summary

Managing ML/TF risks

associated with virtual

assets and virtual asset

service providers

SFC survey

findings on ESG,

climate change

and asset

management

Basel Committee report

on open banking and

application

programming interfaces

(APIs)

SFC circular on streamlined

requirements for eligible

exchange traded funds

adopting a master-feeder

structure

Basel Committee consultation

on credit valuation adjustment

risk and guiding principles on

sectoral countercyclical

capital buffer

Guideline on

Medical

Insurance

Business

LIBOR

Reform

Updates

Other

Regulatory

Updates

Glossary

Regulatory Updates Newsletter — December 2019 PwC · 9

Guideline on Medical Insurance Business

This Guideline shall take effect from 23 September 2020

Pursuant to section 133(1) of the Insurance Ordinance (Cap.

41), the IA has published GL31 – Guideline on Medical

Insurance Business.

The principal function of the guideline is to regulate and

supervise the insurance industry for the protection of existing

and potential policy holders. In addition, it aims to protect its

function to promote and encourage the adoption of proper

standards of conduct and sound and prudent business practices

by authorized insurers and proper standards of conduct by

licensed insurance intermediaries.

This guideline also takes account Insurance Core Principles,

Standards, Guidance and Assessment Methodology (“ICP”)

promulgated by the International Association of Insurance

Supervisors, in particular ICP 19 which stipulates that the

conduct of the business of insurance should ensure that

customers are treated fairly, both before a contract is entered

into and through to the point at which all obligations under a

contract have been satisfied.

This guideline applies to all authorized insurers underwriting

medical insurance business, and all licensed insurance

intermediaries carrying on regulated activities in respect of

medical insurance business.

GL31 applies to all medical insurance businesses, including

individual and group businesses, certified plans under the

Voluntary Health Insurance Scheme (“VHIS”) and any other

types of medical insurance business.

This Guideline provides guidance on the standards and

practices which are expected to be met in order to ensure fair

treatment of customers across all aspects of medical insurance

business.

The areas covered in this guideline are:

• Responsibilities of board of directors, controllers and senior

management;

• Product design;

• Sales process;

• Claims handling;

• After-sales service;

• Complaints handling;

• Proper handling of customers’ personal data; and

• VHIS-compliant policies

Billy Wong

Partner

+852 2289 1259

Executive

Summary

Managing ML/TF risks

associated with virtual

assets and virtual asset

service providers

SFC survey

findings on ESG,

climate change

and asset

management

Basel Committee report

on open banking and

application

programming interfaces

(APIs)

SFC circular on streamlined

requirements for eligible

exchange traded funds

adopting a master-feeder

structure

Basel Committee consultation

on credit valuation adjustment

risk and guiding principles on

sectoral countercyclical

capital buffer

Guideline on

Medical

Insurance

Business

LIBOR

Reform

Updates

Other

Regulatory

Updates

Glossary

Regulatory Updates Newsletter — December 2019 PwC · 10

UK’s Financial Conduct Authority (FCA)

launched a consultation on extending the

senior managers regime to benchmark

administrators

The Senior Managers Regime (SMR) will

come into force for firms that only administer

benchmarks on 7 December 2020. This

consultation explains how FCA proposes to:

• not apply the Certification Regime to

benchmark administrators

• categorise benchmark administrators

under the SMR as ‘Core’ firms initially, with

the option of subsequent waivers

• require them to allocate up to 4 Senior

Manager Functions, depending on their

governance structure

• require them to apply the Conduct Rules to

almost all their employees.

Additionally, after 9 December 2019, the

existing Approved Persons Regime will no

longer apply to firms authorised under FSMA,

and will only apply to Appointed

Representatives. The consultation proposes

some consequential changes to our rules to

make this clear.

The consultation is open for comments until

28 February 2020.

ISDA letter to FSB OSSG on pre-cessation

issues

ISDA has submitted a letter to the Financial

Stability Board’s Official Sector Steering

Group (FSB OSSG) on pre-cessation triggers

for derivatives fallbacks. The communication

is in response to a letter sent by the FSB

OSSG to ISDA in November 2019.

The key highlights of the letter are:

• ISDA is currently on track to finalise the

substantive portion of its work to develop

permanent cessation fallbacks by the end

of 2019, and to facilitate implementation

during the first half of 2020.

• On November 15, 2019, ISDA released the

results of a third successful industry

consultation on the adjustment

methodologies for permanent cessation

fallbacks rates.

• Based on strong majorities, this concluded

that the adjustments should use a

compounded setting in arrears rate with a

spread adjustment calculated as the

median of the historical differences

between the IBOR and the corresponding

RFR over a five-year lookback period.

• Bloomberg expects to commence

publication of indicative fallback rates

based on these adjustments at the

beginning of 2020.

• ISDA will shortly issue a brief

supplemental consultation to confirm the

suitability of these adjustments for

fallbacks in derivatives referencing euro

LIBOR and EURIBOR.

• Upon completion of this consultation in the

first quarter of 2020, ISDA will publish the

Supplement to the 2006 ISDA Definitions

containing the fallbacks and will open for

adherence a protocol to include these

fallbacks in existing derivatives.

• The amendments to new and existing

derivatives contracts will take effect

approximately three months later, in the

second quarter of 2020.

• Based on feedback and support from

market participants, ISDA believes that the

new documentation will provide a critical

backstop in contracts that continue to

reference LIBOR or another key IBOR if

and when that IBOR ceases.

ISDA issued December 2019 Benchmark

Fallbacks Supplemental Consultation

ISDA issued the Supplemental Consultation

on Spread and Term Adjustments, including

Final Parameters thereof, for Fallbacks in

Derivatives Referencing EUR LIBOR and

EURIBOR, as well as other less widely used

IBORs.

This consultation seeks input on the approach

for addressing certain issues associated with

adjustments that would apply to €STR if

fallbacks in EURIBOR or EUR LIBOR take

effect, including the final parameters for these

adjustments. It also asks about adjustments

that could apply if fallbacks take effect in less

widely used IBORs.

The deadline for responses to the consultation

is January 21, 2020.

LIBOR Reform Updates

Ilka Vazquez

Partner

+852 2289 6565

Amy Yeung

Partner

+852 2289 1245

Ian Farrar

Partner

+852 2289 2313

Executive

Summary

Managing ML/TF risks

associated with virtual

assets and virtual asset

service providers

SFC survey

findings on ESG,

climate change

and asset

management

Basel Committee report

on open banking and

application

programming interfaces

(APIs)

SFC circular on streamlined

requirements for eligible

exchange traded funds

adopting a master-feeder

structure

Basel Committee consultation

on credit valuation adjustment

risk and guiding principles on

sectoral countercyclical

capital buffer

Guideline on

Medical

Insurance

Business

LIBOR

Reform

Updates

Other

Regulatory

Updates

Glossary

PwC · 11

Circular to intermediaries: Joint product survey by

the SFC and the HKMA

The SFC and the HKMA will jointly launch an annual

survey on the sale of non-exchange traded investment

products by LCs and registered institutions (RIs)

licensed or registered for Type 1 or 4 regulated activity.

The first joint annual survey will cover the period from 1

January to 31 December 2020.

The survey will enable the SFC and the HKMA to better

understand market trends, identify risks associated with

the selling activities of intermediaries and coordinate

their responses to address areas of common concern.

The survey covers the sale of non-exchange traded

investment products, such as collective investment

schemes, debt securities, structured products, swaps

and repos, to individual professional investors1, certain

corporate professional investors (where intermediaries

cannot rely on a waiver of the suitability obligation) and

investors other than professional investors.

Transactions by institutional professional investors and

corporate professional investors for which

intermediaries have been exempted from the suitability

obligation are outside the scope of this survey.

Intermediaries are expected to submit completed

questionnaires to the SFC electronically in the first

quarter of 2021 for the first reporting period (1 January

to 31 December 2020).

Exposure to HKMCI: 90% Loan Guarantee Product

under SME Financing Guarantee Scheme

On 16 December 2019, the HKMC Insurance Limited

("HKMCI") announced the introduction of a 90% Loan

Guarantee Product under the SME Financing Guarantee

Scheme (“90% Guarantee Scheme”) with effect from 16

December 2019.

The HKMA issued a letter to confirm that the above has

been approved for the purposes of Banking (Exposure

Limits) Rules (“BELR”) Rule 57(1)(d) in respect of an

AI’s exposure to the HKMCI arising from the provisions

of the guarantee by the HKMCI under the 90%

Guarantee Scheme. Accordingly, for the exposure to the

HKMCI arising from any loan to an SME which is

covered by the HKMCI guarantee under the 90%

Guarantee Scheme, the amount so covered is deducted

from the AI's exposures to the HKMCI.

For capital adequacy calculation purposes, AIs

participating in the 90% Guarantee Scheme should

follow the relevant requirements set out in the Banking

(Capital) Rules (“BCR”) for calculating the risk-weighted

amount of their related exposures to the HKMCI under

the Scheme.

SFC concludes consultation on margin

requirements for non-centrally cleared OTC

derivatives

The SFC released consultation conclusions on

proposals to impose margin requirements for non-

centrally cleared over-the-counter (OTC) derivatives.

The proposals will be adopted with some amendments

and clarifications. A licensed corporation which is a

contracting party to a non-centrally cleared OTC

derivative transaction entered into with an authorized

institution, a licensed corporation or another defined

entity would be required to exchange margin with the

counterparty if the notional amount of their outstanding

non-centrally cleared OTC derivatives exceeds specified

thresholds.

The initial margin requirements will be phased in starting

from 1 September 2020, which is also the date the

variation margin requirements will take effect.

Regulatory Updates Newsletter — December 2019

Other Regulatory Updates

Executive

Summary

Managing ML/TF risks

associated with virtual

assets and virtual asset

service providers

SFC survey

findings on ESG,

climate change

and asset

management

Basel Committee report

on open banking and

application

programming interfaces

(APIs)

SFC circular on streamlined

requirements for eligible

exchange traded funds

adopting a master-feeder

structure

Basel Committee consultation

on credit valuation adjustment

risk and guiding principles on

sectoral countercyclical

capital buffer

Guideline on

Medical

Insurance

Business

LIBOR

Reform

Updates

Other

Regulatory

Updates

Glossary

PwC · 12Regulatory Updates Newsletter — December 2019

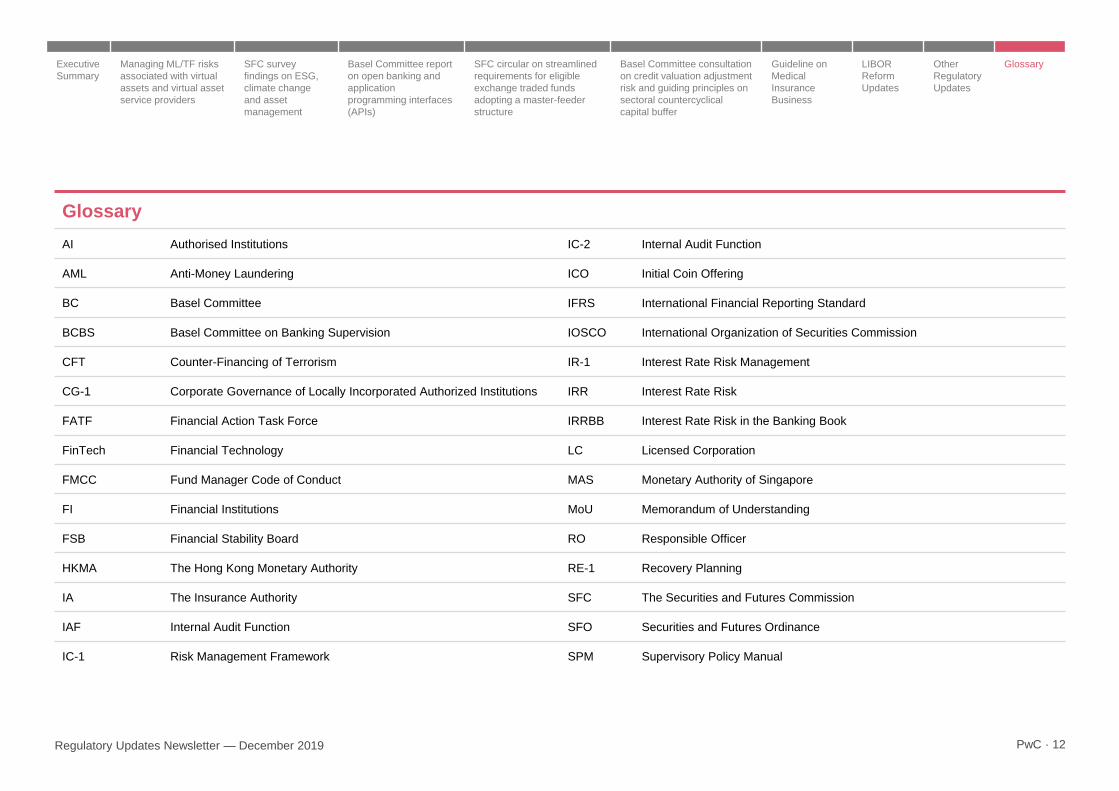

Glossary

AI Authorised Institutions IC-2 Internal Audit Function

AML Anti-Money Laundering ICO Initial Coin Offering

BC Basel Committee IFRS International Financial Reporting Standard

BCBS Basel Committee on Banking Supervision IOSCO International Organization of Securities Commission

CFT Counter-Financing of Terrorism IR-1 Interest Rate Risk Management

CG-1 Corporate Governance of Locally Incorporated Authorized Institutions IRR Interest Rate Risk

FATF Financial Action Task Force IRRBB Interest Rate Risk in the Banking Book

FinTech Financial Technology LC Licensed Corporation

FMCC Fund Manager Code of Conduct MAS Monetary Authority of Singapore

FI Financial Institutions MoU Memorandum of Understanding

FSB Financial Stability Board RO Responsible Officer

HKMA The Hong Kong Monetary Authority RE-1 Recovery Planning

IA The Insurance Authority SFC The Securities and Futures Commission

IAF Internal Audit Function SFO Securities and Futures Ordinance

IC-1 Risk Management Framework SPM Supervisory Policy Manual

Executive

Summary

Managing ML/TF risks

associated with virtual

assets and virtual asset

service providers

SFC survey

findings on ESG,

climate change

and asset

management

Basel Committee report

on open banking and

application

programming interfaces

(APIs)

SFC circular on streamlined

requirements for eligible

exchange traded funds

adopting a master-feeder

structure

Basel Committee consultation

on credit valuation adjustment

risk and guiding principles on

sectoral countercyclical

capital buffer

Guideline on

Medical

Insurance

Business

LIBOR

Reform

Updates

Other

Regulatory

Updates

Glossary