Federal Consolidated Return Regulations for Corporate Taxpayers

85

Federal Consolidated Return Regulations for Corporate Taxpayers Mastering Complex Rules and Guidance to Ensure Ongoing Compliance presents Today's panel features: Bart Stratton, Director, Mergers and Acquisitions Group, PricewaterhouseCoopers, Washington, D.C. Wayne Strasbaugh, Partner-In-Charge, Tax Group, Ballard Spahr, Philadelphia Marc Countryman, Principal, National Tax M&A - Transaction Advisory Services, Ernst & Young, Washington, D.C. Thursday, October 8, 2009 The conference begins at: 1 pm Eastern 12 pm Central 11 am Mountain 10 am Pacific The audio portion of this conference will be accessible by telephone only. Please refer to the dial in instructions emailed to registrants to access the audio portion of the conference. A Live 110-Minute Teleconference/Webinar with Interactive Q&A

Transcript of Federal Consolidated Return Regulations for Corporate Taxpayers

Federal Consolidated Return Regulations for Corporate Taxpayers

Mastering Complex Rules and Guidance to Ensure Ongoing Compliance

presents

Today's panel features:Bart Stratton, Director, Mergers and Acquisitions Group, PricewaterhouseCoopers, Washington, D.C.

Wayne Strasbaugh, Partner-In-Charge, Tax Group, Ballard Spahr, PhiladelphiaMarc Countryman, Principal, National Tax M&A - Transaction Advisory Services, Ernst & Young, Washington, D.C.

Thursday, October 8, 2009

The conference begins at:1 pm Eastern12 pm Central

11 am Mountain10 am Pacific

The audio portion of this conference will be accessible by telephone only. Please refer to the dial in instructions emailed to registrants to access the audio portion of the conference.

A Live 110-Minute Teleconference/Webinar with Interactive Q&A

Federal Consolidated Return Regulations For Corporate

Taxpayers Webinar

Oct. 8, 2009

Marc Countryman Bart StrattonErnst & Young [email protected] [email protected]

Wayne StrasbaughBallard Spahr

2

Today’s Program• Unified Loss Rule Sect. 1.1502-36, slides 3 through 15 (Marc

Countryman)• Final Inter-Company Obligation Regulations Sect. 1.1502-13(g), slides

16 through 30 (Marc Countryman)• Recent Guidance On Stock Elimination Transactions, slides 31

through 50 (Wayne Strasbaugh)• Related Party Debt Acquisitions And Sect. 165(g)(3) Worthless

Securities, slides 51 through 58 (Bart Stratton)• NOL Carryback Transactions And Sect. 382 Update, slides 59 through

62 (Bart Stratton)• Sect. 108(i)-Related Changes, slides 63 through 69 (Wayne

Strasbaugh)• Rev. Proc. 2009-37 And Consolidated Sect. 108(i), slides 70 through

72 (Bart Stratton)• Recent IRS Guidance On Separate Return Limitation Years, slides 73

through 84 (Wayne Strasbaugh)

3

Unified Loss Rule (§1.1502-36)

4

§1.1502-36: Unified Loss Rule

• Why is this the “unified” loss rule?– Non-economic loss– Duplicated loss

• When does the ULR apply?– Where there is a “transfer” of a “loss share” of “subsidiary” stock

§1.1502-36(a)(1).– “Transfer” – Basically a disposition, deconsolidation or

worthlessness– “Loss share” – Basis greater than value– “Subsidiary” stock – Stock of a member other than the common

parent

5

§1.1502-36: Unified Loss Rule (Cont.)

• What happens if the ULR applies?– Three rules apply sequentially:

1. Basis redetermination rule, §1.1502-36(b)2. Basis reduction rule, §1.1502-36(c)3. Attribute reduction rule, §1.1502-36(d)

6

§1.1502-36(b): Basis Redetermination Rule

• How does the basis redetermination rule apply?– Reallocates investment adjustments applied to members’ different bases in

shares of subsidiary (S) stock to “level out” the bases• Doesn’t change the aggregate amount of basis §1.1502-36(b)(1)(i)• Provides a specific method to reallocate positive and negative

investment adjustments to reduce basis disparity among shares §1.1502-36(b)(2)

• Backstops the two rules• Are there any exceptions?

– Two exceptions: §1.1502-36(b)(1)(ii)1. “Level” basis in S common stock, and no gain or loss in S preferred

stock2. All of S’ stock is disposed of or becomes worthless in one fully

taxable transaction

7

§1.1502-36(c): Basis Reduction Rule• How does the basis reduction rule apply?

– Reduces the basis of each transferred loss share (but not below value) by the lesser of:

1. The share’s net positive adjustment (NPA); and2. The share’s disconformity amount (DA) §1.1502-36(c)(2)

– This is the non-economic stock-loss component (only limits loss)• What are the “NPA” and “DA”?

– NPA is the sum of all investment adjustments reflected in the basis of the share (other than distributions), but can’t be less than zero §1.1502-36(c)(3)

– DA is any excess of the basis in the share over the share’s allocable portion (“vertical slice”) of the subsidiary’s net inside attribute amount (NIAA) §1.1502-36(c)(4)

• NIAA – Losses, basis and money, less liabilities §1.1502-36(c)(5)– Note: Special rules apply to determine NIAA, if S has lower-tier

subsidiaries.§1.1502-36(c)(6)

8

§1.1502-36(d): Attribute Reduction Rule• How does the attribute reduction rule apply?

– Reduces the S’ attributes by the attribute reduction amount (ARA) §1.1502-36(d)(2)(i)

– The ARA is the lesser of:1. The net stock loss (NSL); and2. S’ aggregate inside loss (AIL) §1.1502-36(d)(3)(i)

– The ARA is the amount of the loss duplication– This is the loss duplication component

• What are the “NSL” and “AIL”?– NSL is any excess of the aggregate basis in the transferred shares, over the

value of the transferred shares §1.1502-36(d)(3)(ii)– AIL is any excess of S’ net inside attribute amount, over the value of all of

S’ shares §1.1502-36(d)(3)(iii)– Note: Special rules apply to determine NIAA, if S has lower-tier

subsidiaries §1.1502-36(d)(5)

9

§1.1502-36(d): Attribute Reduction Rule (Cont.)

• Three forms of “relief” from attribute reduction:– Small duplication exception – Attribute reduction does not apply if the ARA

is less than 5% of the value of the transferred shares §1.1502-36(d)(2)(ii)– Reattribution of losses – May elect to reattribute losses that would otherwise

be subject to reduction §1.1502-36(d)(6)(i)– Elective stock basis reduction – May elect to reduce the basis of the

transferred loss shares to preserve attributes inside S §1.1502-36(d)(6)(i)• May combine reattribution and stock basis reduction elections §1.1502-

36(d)(6)(i)(C)• Provides a great deal of flexibility in addressing loss duplication• Made unilaterally on the selling group’s return for the year §1.1502-

36(e)(5)• Elections are irrevocable, but may make a protective election §1.1502-

36(d)(6)(ii)

10

ULR: Seller Issues• The common parent (P) should be thinking about:

– Is there a loss in the S stock after applying all other rules of law?• Consider the possible treatment of transaction costs as an offset

to purchase price (and presumably amount realized), or potentially an increase to stock basis

– Will any of the stock loss be eliminated as a result of the basis reduction rule (i.e., is any of the loss non-economic)?

– Do S (or any lower-tier subsidiaries) have any losses or deferred deductions that might be carried out of the group?

11

ULR: Seller issues (Cont.)– Are any of the S (or lower-tier subsidiary) losses or deductions

eligible for reattribution?• Would the losses otherwise be reduced?• If there are lower-tier subsidiaries, is there sufficient stock

basis?• Character, quality (SRLY, §382 limited, etc) and ability to

utilize vs. value to buyer are factors to consider

– What is the potential impact of the ULR on S’ (or any lower-tier subsidiaries’) other attributes (i.e., what will buyer be getting)?

• Impact might include lower-tier subsidiaries that remain in the group

12

ULR: Seller Issues (Cont.)– Are there any potential contingent adjustments to the purchase

price?• Relevant to how a reattribution or stock basis reduction

election is articulated

• Build flexibility into elections to accommodate possible subsequent adjustments (contingencies, audit adjustments, etc.)

– Did S (or any lower-tier subsidiaries) engage in any prior inter-company transactions with respect to stock of other members (as buyer or seller) that might invoke the ULR?Note: It is essential for P to model the potential tax impact of the ULR to determine

the available elections, impact, and other planning opportunities. Note: It is essential for P to model the potential tax impact of the ULR to determine the available elections, impact and other planning opportunities

13

ULR: Buyer Issues• Buyer should be thinking about:

– Will the selling group recognize a loss on the S stock after applying the basis redetermination rule and the basis reduction rule?

• This is something that the buyer previously might not have been concerned about (other than with respect to reattribution under old §1.1502-20(g))

– Can P reattribute any losses or deferred deductions from S (or any lower-tier subsidiaries)?

– What is the potential impact of the ULR on S’ (or any lower-tier subsidiaries’) other attributes (i.e., what will buyer be getting)?

14

ULR: Buyer Issues (Cont.)– What is the potential financial statement impact if S (or any lower-

tier subsidiaries) experiences a significant amount of attributereduction?

– It is critical that the buyer be thinking up-front about negotiating P’s elections to reattribute losses or deductions, or to reduce stock basis

• Buyer should be sure that any such elections contain the necessary flexibility to accommodate subsequent adjustments (contingencies, audit adjustments, etc.)

Note: It is essential for buyer to model the potential tax impact of the ULR to determine what it is buying, and the scope of potential elections it might want to negotiate

15

What Do P And Buyer Need To Know To Determine The Tax Treatment?

P

S1

Basis?

S3

S2

Investment adjustmenthistory?

NOLs and other

carryovers?

Basis in assets class by class, and liabilities?

SInvestment adjustment history?

Investment adjustment history?

Investmentadjustment

history?

Basis?

Basis?

NOLs and other carryovers?

NOLs and other

carryovers?

NOLs and other

carryovers?

Basis in assets class by class, and liabilities?

For each subsidiary, must know: –Basis in subsidiary stock–Prior investment adjustments to subsidiary stock basis (perhaps including in a prior group)–Subsidiary’s NOLs, capital loss carryovers and deferred deductions–Subsidiary’s basis in assets, class by class and asset by asset –Subsidiary’s liabilities (perhaps including contingent liabilities)

16

Final Intercompany Obligation Regulations [§1.1502-13(g)]

17

• Intercompany regulations first issued as final regulations in 1995

• Proposed regulations issued in 1998

• New proposed regulations issued in 2007

• New final regulations issued on Jan. 5, 2009– Effective for transactions occurring in consolidated return years

beginning on or after Dec. 24, 2008

Intercompany Obligation Regulations: History

18

General Applicability Of 2008 Intercompany Obligation Regulations

• An intercompany obligation becomes a non-intercompany obligation (“outbound transactions”)

• An intercompany obligation is assigned or extinguished within the group (“intragroup transactions”)

• A non-intercompany obligation becomes an intercompany obligation (“inbound transactions”)

19

Outbound And Intragroup Transactions: Deemed Satisfaction And Reissuance

(DSR)• Immediately before triggering transaction, inter-company obligation is:

– Deemed satisfied, generally for cash amount equal to the obligation’s FMV

– Deemed reissued for the cash amount used in the deemed satisfaction transaction

• “Reissued obligation” has the same terms as original

• DSR is separate from the triggering transaction

• DSR is for all federal income tax purposes

20

Deemed Satisfaction And Reissuance: Example (Outbound Transaction)

• Facts: B issues $100 note to S for $100; S later sells B’s note to X for $70 (the note’s FMV at time of sale)

• DSR treatment: B is deemed to (i) satisfy its $100 note with $70 and (ii) reissue a $100 note to S for $70; S sells B’s reissued $100 note to X for $70

P

B XS

P

X B S$100

$100 note

B’s note

$70

Actual transaction

$70 satisf.

$70

$100 Reissued note

$70

$100Reissued note

Transaction with DSR

21

Deemed Satisfaction And Reissuance: Example (Outbound Transaction), Cont.

• Tax consequences of deemed satisfaction– B has $30 CODI– S has $30 loss

• Tax consequences of deemed reissuance– B’s new note has stated redemption price at maturity of $100– B’s new note has issue price of $70– S’ basis in new note is $70

• Tax consequences of S’ sale of note to X– S has no gain or loss– $30 of OID is taken into account by B and X

22

Deemed Satisfaction And Reissuance: Example (Intragroup Transaction)

• Assume that in prior example, X was a member of the P group

• S’ sale of B’s note to X would be an intra-group transaction

• The same deemed satisfaction and reissuance transactions would occur

• The tax consequences would be modified by the general intercompany transaction regulations of Reg. §1.1502-13

23

Notable Exceptions To DSR For Intragroup Transactions

• Intercompany non-recognition transactions

• Intercompany extinguishment transactions

• Routine modification transactions

24

Exception For Inter-Company Non-Recognition Transactions

• DSR does not apply if:– The transaction is an intercompany exchange to which §361(a), sections

§§332 and 337(a), or §351 apply; and– The creditor and debtor recognize no amount of income, gain, deduction

or loss

• But, see special rule for intercompany §351 transactions in next slide

25

Special Rule For Intercompany §351 Transactions

• If the creditor assigns the intercompany obligation in a §351 transaction, the exception for inter-company non-recognition transactions generally does not apply (i.e., DSR does apply) if: – Transferor or transferee has a loss subject to limitation– Transferor or transferee has a special status (e.g., is a bank) that the other

member does not also have– A group member realizes CODI that is excluded under §108(a) in the tax year of

the exchange, and tax attributes of the transferor or transferee are reduced– Transferee has a non-member shareholder;– Transferee issues preferred stock to transferor in the assignment exchange; or– The stock of the transferee is disposed of within 12 months of the assignment

(special rules apply if stock of higher-tier members are disposed of and in cases of successive §351 transactions)

26

Exception For Intercompany Extinguishment Transactions

• DSR does not apply if: – All or part of the rights and obligations under the intercompany

obligation are extinguished in an intercompany transaction (other than an exchange or deemed exchange of an intercompany obligation for a newly issued intercompany obligation)

– The adjusted issue price of the obligation is equal to the creditor’s basis in the obligation; and

– The debtor’s corresponding item and the creditor’s intercompany item with respect to the obligation offset in amount

27

Exception For Routine Modification Transactions

• DSR does not apply if:– All of the rights and obligations under the intercompany obligation are

extinguished in an intercompany transaction that is an exchange (or deemed exchange) for a newly issued intercompany obligation; and

– The issue price of the newly issued obligation equals both:• The adjusted issue price of the extinguished obligation, and • The creditor’s basis in the extinguished obligation

28

Anti-Avoidance Rule: Tax Benefit Rule

• Tax benefit rule applies if intercompany assignment or extinguishment transaction is:

– Otherwise excepted from DSR under one of the three exceptions described previously (and one exception not described previously), and

– Engaged in with a view to secure a tax benefit that would not otherwise be enjoyed in a consolidated or separate return year

• If the tax benefit rule applies, then the assignment or extinguishment transaction triggers DSR

• “With a view” is low anti-avoidance standard

29

Notable Exception To DSR For Outbound Transactions

• Outbound subgroup exception

– Members of an inter-company obligation subgroup cease to be members• Bear a §1504(a)(1) relationship through a subgroup parent

– Neither the debtor nor the creditor recognizes any amounts with respect to the intercompany obligation

– Debtor and creditor are members of an intercompany obligation subgroup of another group immediately after

30

Outbound Subgroup Exception

P

B S$100 note

M

Intercompany obligation subgroup

P

B

S

$100 note

Intercompany obligation subgroup

XX

• P sells the M stock to X, or P sells the S stock to X

• No DSR in either case

$$ $$

31

Recent Guidance On Stock Elimination Transactions

32

Background• IT matching rules generally provide for inclusion/allowance of

matching items of income and deduction as if S and B were divisions of a single corporation

• Reg. § 1.1502-13(c)(6) provides that matching rule generally might require redetermination of inter-company items to be excluded from gross income or treated as non-capital, non-deductible amounts

• However, Reg. § 1.1502-13(c)(6) limits redetermination of income exclusion to situations in which:– Corresponding item is a deduction or loss that is permanently and

explicitly disallowed– Corresponding item is an unrealized loss on a distribution to a non-

member – The IRS determines income exclusion is consistent with the

purposes of the IT regulations and other applicable provisions of the Code and regulations (commissioner’s discretionary rule)

33

Examples Of NO Permanent And Explicit Disallowance

• Where Code or regulations provide that corresponding item is notrecognized (sections 332, 355(c)) – Member stock basis lost

• Where a related amount might be taken into account by B with respect to successor property (recovery of demolition costs capitalized under Sect. 280B)

• Where a related amount might be taken into account by another taxpayer (Sect. 267(d) non-recognition of gain for previously disallowed loss)

• Where a related amount might be taken into account as a deduction or loss (including as a carryforward and without regard to carryforwardexpiration)

• Where the corresponding item is reflected in the computation of any tax credit (including tax credit carryforwards)

34

IT Gain Triggered By Sect. 332Liquidation

P

BS

T T

$

21

Step 1 S sells T stock to B at a gain (intercompany item)Step 2 B liquidates T under Sect. 332 at no recognized gain or loss (corresponding item)

35

T.D. 9383 (March 6, 2008)• Provides relief for sections 332 and 355(c) transactions involving

member stock if:– Inter-company gain item belongs to common parent– Common parent holds member stock that produced intercompany

gain immediately before intercompany gain is taken into account– Stock basis is eliminated without recognition of gain or loss and

not reflected in basis of any successor asset– Group has not and will not derive any federal income tax benefit

from the original IT or from the redetermination of intercompanygain (including adjustments to stock basis)

– IT effects have not previously been reflected, directly or indirectly, in consolidated return

36

Reg. § 1.1502-13T(f)(7)(i) Example (7)

P

1

23

4

Spin-off Distribution

T1

ST

T1 T

37

Reg. § 1.1502-13T(f)(7)(i) Example (7) [Cont]

• S has basis of $40 in T stock and T stock has FMV of $100• STEP 1: S distributes stock of T to P under Sect. 301 in TY-1 (S has

inter-company gain item of $60 under Sect. 311(b). P has basis of $100in T stock)

• STEP 2: S distributes all of its remaining assets to P in complete liquidation under Sect. 332 in TY- 4 (P is successor person with respect to S’ intercompany gain item under Reg. § 1.1502-13(j)(2))

• STEP 3: T distributes T1 stock to P under Sect. 355 in TY-7 (P allocates $100 basis for T stock, $75 to T stock and $25 to T1 stock)

• STEP 4: T distributes all of its remaining assets, with FMV of $75 to P in complete liquidation under Sect. 332 in TY-9

38

Reg. § 1.1502-13T(f)(7)(i) Example (7) [Cont.]

• Analysis of STEP 4– Intercompany gain item belongs to P, and P holds the member

stock with eliminated stock basis – P has corresponding item of zero (no recognized gain or loss)

under Sect. 332– P has recomputed corresponding item of $45, $75 T stock basis

less $30 (allocated initial $40 T stock basis after Step 3)– P takes $45 of intercompany gain into account, but gain is

excluded from income because all prerequisites of Reg. § 1.1502-13T(c)(6)(ii)(C) are satisfied

39

T. D. 9383 Effective Dates

• Corresponding items taken into account on or after March 7, 2008

• Not applicable after March 3, 2011 unless adopted as final regulations

• Proposed regulations (REG-137573-07) intended to eliminate commissioner’s discretionary rule

40

Issues With T.D. 9383 Relief

• Sect. 332 liquidation must eliminate basis of member stock(deconsolidated members of affiliated group)

• Intercompany gain item must belong to common parent (order of tiered liquidations is important)

• Elimination of commissioner’s discretionary rule is controversial

41

T.D. 9458 (Sept. 3, 2009) –Background

• Reg. § 1.1502-13(f)(5)(ii) provides elective relief from matching and acceleration rules, where member stock basis is eliminated

• Requires member with eliminated stock basis to have been member throughout period beginning with IT and ending with stock elimination transaction

• Eligible transactions– Sect. 338(h)(10) and comparable transactions (election of Sect. 331

liquidation in lieu of deemed Sect. 332 liquidation)– Sect. 355 inter-company transactions (election of Sect. 311 inter-

company distribution treatment and FMV member stock basis determination in lieu of Sect. 358 basis determination)

– Actual Sect. 332 liquidations if liquidation-reincorporation (T.D. 9458 changes analysis)

42

Sect. 332 Liquidation Undone By Reg. § 1.1502-13(f) (5)(ii)(B) Election

P

BS

OldT

OldT

$

21

NewT

3

43

Sect. 332 Liquidation Do-Over

• STEP 1: S sells stock of Old T to B, creating an intercompany gain item with respect to Old T stock

• STEP 2: Old T distributes all of its assets in complete liquidation to B

• STEP 3: Not as part of the same plan as liquidation (recognizing its mistake?), B tries to undo by reincorporating T as New T

44

Sect. 332 Liquidations Before Oct. 25, 2007

• Election under former Reg. § 1.1502-13(f) (5)(ii)(B) permits transfer by B of substantially all assets of Old T to New T not otherwisepursuant to the same plan or arrangement as the Sect. 332 liquidation to be treated as pursuant to the same plan or arrangement, if: – B transfers assets to New T pursuant to a written plan, a copy of

which is attached to a timely filed original return (including extensions) for TY of T’s liquidation

– The transfer of the assets is completed within 12 months of the filing of that return

• Effect of election is to treat liquidation and asset transfer as Sect. 368(a) reorganization (liquidation-reincorporation) under step transaction principles of tax law

45

Sect. 332 Liquidations Before Oct. 25, 2007 (Cont.)

• End result of election under former Reg. § 1.1502-13(f) (5)(ii)(B) is that stock of New T is treated as successor asset to stock of New T under Reg. § 1.1502-13(j)(1), permitting matching (and deferral) to continue for intercompany item of gain with respect to T stock

• Appropriate adjustments are made to reflect any assets not transferred to New T as part of the same plan or arrangement. Such assets are treated as being acquired by New T but distributed to B immediately after the reorganization

46

T.D. 9361 (Oct. 24, 2007)

• Effective for transactions on or after Oct. 25, 2007

• Reg. § 1.368-2(k)(1) provides that a transaction otherwise qualifying as a reorganization under Sect. 368(a) is not disqualified or recharacterized as a result of subsequent downstream transfers of assets, so long as: – COBE is satisfied– Transferor’s tax existence does not terminate

47

Effect Of T.D. 9361 On Reg. § 1.1502-13(f) (5)(ii)(B) Election

• Step transaction liquidation-reincorporation is now treated as upstream Type C reorganization, with an asset drop under Sect. 368(a)(2)(C)

• Deemed step transaction liquidation-reincorporation by reason of election would apparently be similarly treated

• Stock of New T now takes basis under Sect. 362 (inside asset basis) rather than under Sect. 358 (Old T stock basis)

• Treatment of New T stock as successor asset to Old T stock and continuation of matching are no longer appropriate

48

T.D. 9458 Solution For Sect. 332 Liquidations On/After Oct. 25, 2007

• Election under new Reg. § 1.1502-13T(f) (5)(ii)(B) permits transfer by B of substantially all assets of Old T to New T not otherwise pursuant to the same plan or arrangement as the Sect. 332 liquidation to be treated as pursuant to the same plan or arrangement, if: – A direct transfer of substantially all the assets by Old T to New T

would qualify as Type D reorganization– B transfers asset to New T pursuant to a written plan entered into

before the due date for the group’s return (including extensions) for the tax year of T’s liquidation

– The transfer of the asset is completed within 12 months of the filing of the group’s return

– Effect of election is to treat liquidation and asset transfer as Type D reorganization, for all purposes

49

T.D. 9458 Solution For Sect. 332 Liquidations On/After Oct. 25, 2007

(Cont.)

• End result of election under new Reg. § 1.1502-13T(f) (5)(ii)(B) is that stock of New T is treated as successor asset to stock of New T under Reg. § 1.1502-13(j)(1), permitting matching (and deferral) to continue for intercompany item of gain with respect to T stock

• Appropriate adjustments are made to reflect any assets not transferred to New T. Such assets are treated as acquired by New T but distributed to B immediately after the reorganization

• Group effectively agrees to waive upstream reorganization treatment (including conformity to New T asset basis for stock of New T), with results virtually identical to those under former regulation

50

T.D. 9458 – Special Transitional Rule• For liquidations on or after Oct. 25, 2007, where group’s original tax

return filed before Nov. 3, 2009• Election under new Reg. § 1.1502-13t(f) (5)(ii)(b) may still be timely

made if– Written plan to transfer assets from B to New T entered into on or

before Nov. 3, 2009– Election statement is included on or with original or amended tax

return for TY of liquidation that is filed on or before Nov. 3, 2009 – Substantially all of the former assets of Old T are transferred to

New T within 12 months of the filing date for such original or amended return

• Note that any liquidation on or after Oct. 25, 2007 and before Nov. 3, 2009 may be undone under this special transitional rule (even ifelection originally overlooked)

51

Related Party Debt Acquisitions And

Sect. 165(g)(3) Worthless Securities

52

Related Party Debt Acquisitions

• Sect. 108(e)(4) provides that when debt is acquired by a related party, “to the extent provided in regulations,” the debt is deemed satisfied by the issuer for the amount paid by the related party

• Treasury Reg. Sect. 1.108-2(d)(2): A person is “related” to the debtor if they are related under either sections 267(b) or 707(b)(1) (generally >50% common ownership by value)

• Onerous attribution rules of Sect. 267(c)– Sect. 267(c)(1): Stock owned by a corporation or partnership is

treated as proportionately owned by its shareholders or partners– Sect. 267(c)(3): Individual who owns any stock in a corporation is

considered to own stock owned, directly or indirectly, by any ofhis partners

53

Related Party Debt Acquisitions (Cont.)

• Sect. 108(e)(4): Treats the acquisition of debt by a party related to the issuer as an acquisition of such indebtedness by the issuer itself

– Example: Issuer issues debt with an issue price of $100 and 5% interest. Due to market conditions, the value of the debt is less than $100. If the issuer goes out to repurchase its debt in the market for $95, it has COD income. If issuer sets up a NewCo to repurchase it, the debt is still outstanding. However, Sect. 108(e)(4) makes the issuer pick up COD income in this situation,and the debt is treated as reissued for $95

54

Consolidated Return Considerations

• Treasury. Reg. Sect. 1.1502-13(g)(5) – Non-intercompany debt becomes intercompany debt– Under final regulations effective 12/24/08, cash purchase model

applies to non-intercompany debt that becomes intercompany debt– Deemed satisfaction for cash at fair market value and immediate

reissuance for the same amount– Sect. 108(e)(4) does not apply when non-intercompany debt

becomes intercompany debt. Treasury Reg. Sect. 1.1502-13(g)(6)(i)(A)

55

Sect. 165(g)(3) Worthless Securities• Sect. 165(a) provides that there shall be allowed as a deduction any loss

sustained during the taxable year and not compensated for by insurance or otherwise

• Sect. 165(g)(1) provides that if any “security” which is a capital asset become worthless during the taxable year, the loss resulting therefrom shall be treated as a loss from the sale or exchange, on the last day of the taxable year, of a capital asset

• Sect. 165(g)(2) defines “security” to mean:– A share of stock in a corporation– A right to subscribe for, or to receive, a share of stock in a corporation; or– A bond, debenture, note or certificate or other evidence of indebtedness,

issued by a corporation or government or political subdivision thereof, with interest coupons or in registered form

56

Sect. 165(g)(3) Worthless Securities (Cont.)• Sect. 165(g)(3) provides ordinary loss treatment for worthless securities in

certain “affiliated” corporations• This provision is an exception to the general rule of Sect. 165(g)(1), which

mandates capital loss treatment for worthless securities that are capital assets• Ordinary loss treatment under Sect. 165(g)(3) is available only if the holder of

the security is a domestic corporation that satisfies a two-part test1) Ownership requirement – Sect. 1504(a)(2) control of the issuing

corporation (i.e., at least 80% of the total voting power and value of the issuer’s stock); and

2) Gross receipts requirement – More than 90% of the aggregate gross receipts for all taxable years must be from sources other than royalties, rents, dividends, interest, annuities and gains from sale or exchanges of stock and securities

57

Sect. 165(g)(3) Worthless Securities (Cont.)• Rev. Rul. 2003-125

– Allows a parent corporation a worthless security deduction when it elects to change the classification of its wholly-owned insolvent subsidiary to a single-member LLC

– States that loss with respect to parent’s related party debt instrument with its subsidiary is an ordinary deduction under Sect. 166

– Follows Rev. Rul. 70-489 (parent allowed section 165(g)(3) and Sect. 166 deductions on insolvency dissolution of wholly-owned subsidiary) and refutes FSA 200226004 (denied Sect. 165(g)(3) loss on CTB liquidation)

58

Sect. 165(g)(3) Worthless Securities (Cont.)• Recent noteworthy PLRs and TAMs

– TAM 200912021: Gross receipts test of Sect. 165(g)(3)(B) does not preclude the taxpayer from deducting an ordinary loss for the worthless stock of a wholly-owned operating company that never had gross receipts

– PLR 200924014: Software company whose gross receipts included mainly license fees attributable to computer software developed, manufactured and produced by the taxpayer found to be an operating company with active gross receipts

– PLR 200932018: Taxpayer was able to satisfy the gross receipts test by relying upon gross receipts that carried over to the subsidiary corporation pursuant to Sect. 381 following a series of transactions

59

NOL Carryback Changes And Sect. 382 Update

60

NOL Carryback Changes

• The American Recovery and Reinvestment Act of 2009 allows certain eligible small businesses (ESBs) to elect an increased NOL carrybackperiod for losses incurred in 2008

• An ESB is a corporation, partnership or sole proprietorship that meets a $15M gross receipts test (<$15M for the year of loss and <$15M for three-year period ending with the year of loss)

• Carryback period increased from two years to any whole number of years greater than two but less than six (i.e., three, four or five years)

• Rev. Proc. 2009-19 provides administrative guidance on the time and manner for making elections for this new provision

61

Sect. 382 – Update• The IRS has issued a series of taxpayer-favorable private letter rulings

addressing loss corporation mitigation of Sect. 382 by minimizing owner shifts related to investment advisors (IAs)– PLR 200747016: An IA should be treated as a 5% shareholder

unless the IA specifically states no one person or fund has economic interest of 5% or more, or information is acquired by the loss corporation to confirm that no one person or fund has economic ownership of 5% or more

– PLR 200806008: Taxpayers may rely upon the absence of Schedule 13D/G in determining the economic owners were not members of a group that constitutes as an “entity,” provided taxpayer has no actual knowledge to the contrary

– PLR 200902007: Taxpayers may use a stock surveillance company to help obtain evidence of existence or absence of 5% shareholders

62

Sect. 382 – Update (Cont.)• The IRS has also issued guidance on other Sect. 382 issues

– CCA 200926027• Taxpayer sought a ruling that it could carry back excess

recognized built-in losses in excess of Sect. 382 limitations to a pre-change year. IRS denied the ruling request, stating it was bound by Sect. 382(h)(4) and its legislative history

– Notice 2008-78• IRS states it intends to issue regulations under Sect. 382(l)(1)

that would provide exceptions to the general rule under Sect. 382(l)(1)(B)

• Contributions made during the two-year period prior to the change date are not presumed to be part of the plan, a principal purpose of which is to avoid or increase a Sect. 382 limitation

• Safe harbors

63

Sect. 108(i)-Related Changes

64

Code Sect. 108 Background

• Provides cancellation of debt (COD) income exclusions for subchapter C corporations for

• Bankruptcy (Title 11 cases)• Insolvency• Qualified farm indebtedness

• Tax cost is attribute reduction

65

New Sect. 108(i)

• Added by Sect. 1231 of ARRA

• Elective – Pre-empts COD exclusions – Eliminates need for attribute reduction

• Tax effect is deferral rather than exclusion

• Irrevocable

• Protective elections possible (Rev. Proc. 2009-37)

66

New Sect. 108(i) Elective Deferral

• To FIFTH taxable year for COD recognized in 2009 (2014 TY)

• To FOURTH taxable year for COD recognized in 2010 (2014 TY)

67

Cost Of Sect. 108(i) Deferral

• If new debt is issued in exchange for COD, amortization of any OID on the new debt created by COD is deferred for same five-year period (until 2014 TY)

• Deferred OID amortization is deducted ratably over five-year income inclusion (2014-2018)

• Election has no effect on holder

68

Election Available For COD From Reacquisition Of Applicable DI

• Applicable DI - Includes all DI issued by subchapter C corporations

• Reacquisition - Includes any acquisition of applicable DI by debtor or related person [Sect. 108(e)(4)]– For cash or (under Rev. Proc. 2009-37) other property – Involving the exchange of one DI for another DI (including

deemed exchange modifications under Reg. § 1.1001-3 – Involving the exchange of DI for stock or a contribution to capital– A complete COD– An indirect acquisition [Reg. § 1.108-2 (c)]

69

Acceleration Of All Deferred Income And OID Deductions

• Liquidation or sale of substantially all the assets of debtor (including in bankruptcy)

• Cessation of business by debtor

• “Similar circumstances”

70

Rev. Proc. 2009-37And

Consolidated Sect. 108(i)

71

Rev. Proc. 2009-37• The IRS recently released Rev. Proc. 2009-37 to provide detailed

guidance on the proper method for making the election under Sect.108(i). Further, the IRS provided clarity on several issues:

1) Partial elections are permitted (i.e., elect to defer only a portion of the COD income). Alternatively, a taxpayer can elect to aggregate its debt instruments and make only one election

2) Election can be made on an entity-by-entity basis3) Protective Sect. 108(i) elections4) COD income triggered by a related party acquisition can be

deferred5) Election does not defer CODI for purposes of determining

earnings and profits 6) Provides for 9100 relief procedures for making a late CODI

deferral election

72

Consolidated Sect. 108(i)• Consolidated return issues not addressed by Rev. Proc. 2009-37:

1) Stock basis adjustments under Treasury Reg. Sect. 1.1502-322) Application of the matching and acceleration rules in Treasury Reg. Sect.

1.1502-133) Impact of a subsequent liquidation of a debtor member4) Application of the deemed satisfaction/reissuance model of Treasury Reg.

Sect. 1.1502-13(g)5) Earnings and profits treatment under Treasury Reg. Sect.1.1502-336) Application of Sect. 108(i) to inter-company debt obligations

73

Recent IRS Guidance On Separate Return Limitation Years

74

Background

• Separate return limitation year rules (SRLY) apply when member joins group in transaction that is not Sect. 382 COO

• Generally limit utilization of member’s loss carryforwards to member’s contributions to CTI

• Situations where SRLY might apply– Creeping acquisitions by corporate LBO or MBO entity– Non-includible corporation common parent (such as foreign

corporation) combines two groups – Termination of 50-50 corporate joint ventures

75

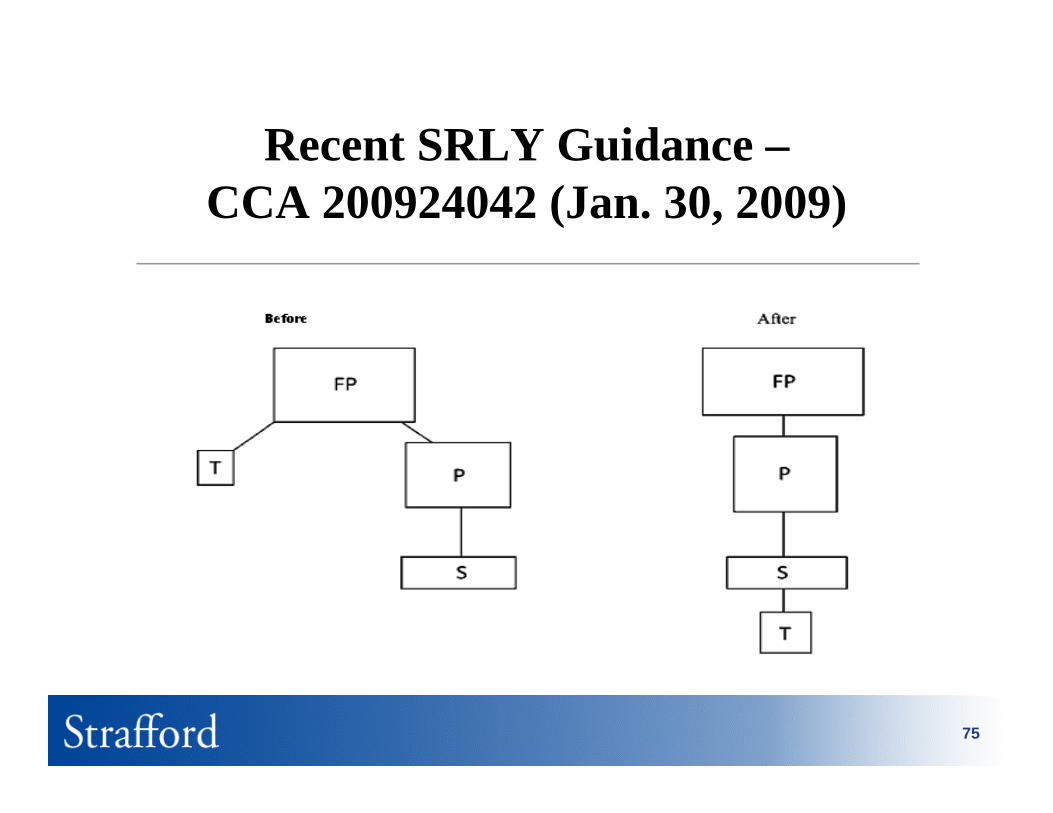

Recent SRLY Guidance –CCA 200924042 (Jan. 30, 2009)

76

Recent SRLY Guidance –CCA 200924042 (Jan. 30, 2009)

[Cont.]

• T is not member of P group in TY1 through TY3

• FP transfers T to S in TY4, and T joins P group

• S distributes T stock to P in TY8, and P sells T stock to purchaser

• A Sect. 338(h)(10) election is made for sale of T stock

• T is deemed to liquidate into P, and P succeeds to T NOL carryovers

77

CCA 200924042 (Cont.)

??[Deemed liquidated]9

??[Deemed liquidated]10

NoLossLoss8

NoProfitLoss7

NoProfitLoss6

YesProfitLoss5

NoProfitProfit4

NoLossLoss3

NoLossLoss2

NoLossLoss1

SRLY Carryover Deduction

CumulativeIncome RegisterCurrent Income Of T

Tax Year

78

CCA 200924042 – Taxpayer’s Position• Reg. § 1.1502-21(c)(1) (i): “General rule. -- Except as provided

in paragraph (g) of this section (relating to an overlap with section 382), the aggregate of the net operating loss carryoversand carrybacks of a member arising (or treated as arising) in SRLYs that are included in the CNOL deductions for all consolidated return years of the group under paragraph (a) of this section may not exceed the aggregate consolidated taxable income for all consolidated return years of the group determinedby reference to only the member's items of income, gain, deduction, and loss.”

• Reg. § 1.1502-21(f)(1): “In general. -- For purposes of this section, any reference to a corporation, member, common parent, or subsidiary, includes, as the context may require, a reference to a successor or predecessor, as defined in §1.1502-1(f)(4).”

79

CCA 200924042 – Taxpayer’s Position (Cont.)

• Reg. § 1.1502-1(f)(4): “Predecessor and successors. -- The term predecessor means a transferor or distributor of assets to a member (the successor) in a transaction … (i) to which section 381(a) applies [which includes a deemed Section 332 liquidation]”

• Therefore, either– Cumulative income register for TY9 and TY10 should include

separate contributions to consolidated taxable income of both P and T for pre-liquidation years; or

– Cumulative income for TY9 and TY10 should include only separate contributions to consolidated taxable income of P afterdeemed liquidation of T

80

CCA 200924042 – IRS Position

• Successor and predecessor definition qualified by “as the context may require,” and historical context of SRLY would limit to T’s income history

• Consideration of P’s pre-liquidation income history is in effect to allow a SRLY carryback contrary to Sect. 381

• Therefore, cumulative income register may include only pre-liquidation income of T and post-liquidation income of P

81

CCA 200901031 (June 15, 2006)• Background: Rev. Rul. 82-152, 1982-2 C.B. 205, holds that reverse merger of CP

transaction is functionally equivalent to the forward merger of CP in §1.1502-75(d)(2)(ii). CR Group continues

SH

OCP

NCP

SUB

SH

OCP

SH

NCP

OCP

82

CCA 200901031 (Cont.)• CCA addresses issue as to whether SRY carryforwards and carrybacks

are “SRLY-ied” for OCP or NCP• Reg. § 1.1502-1(f) (2) provides: “exceptions. -- The term separate

return limitation year (or SRLY) does not include:(i) A separate return year of the corporation which is the common parent for the consolidated return year to which the tax attribute is to be carried (except as provided in §1.1502-75(d)(2)(ii) and subparagraph (3) of this paragraph)” (lonely parent rule)

• Reg. §1.1502-75(d)(2)(ii)(last sentence) provides: “for purposes of applying paragraph (f)(2)(i) of §1.1502-1 to separate return years ending on or before the date on which the former parent ceases to exist, such former parent, and not the new common parent, shall be considered to be the corporation described in such paragraph”

83

CCA 200901031 (Cont.)

SRYloss CB

CRYcommon parent

CRYsubmember

SRYLoss CF

NCP

SRYloss CB

CRYsubmember

CRYcommonparent

SRYloss CF

OCP

TY 4TY 3TY 2TY 1

84

CCA 200901031- Holdings• OCP can carry forward SRY losses without SRLY limitation under

lonely parent rule, by reason of analogy to Reg. §1.1502-75(d)(2)(ii) (last sentence)

• SRY carryback losses of OCP are subject to SRLY limitation, because Reg. §1.1502-75(d)(2)(ii) does not contemplate continued existence of OCP after merger

• NCP can carry back SRY losses without SRLY limitation under basic lonely parent rule

• SRY carryforward losses of NCP are subject to SRLY limitation, because its status as CP under lonely parent rule for pre-merger years is pre-empted by OCP by reason of Reg. §1.1502-75(d)(2)(ii) (last sentence)