Feasibility Study on the Establishment of an Online Portal ...

76

Feasibility Study on the Establishment of an Online Portal for Trading in Freight Services (e-freightex) in East Africa Final Report – July 2013 Volume I Upper Quartile LLP

Transcript of Feasibility Study on the Establishment of an Online Portal ...

Feasibility Study on the Establishment of an Online Portal for Trading in Freight Services (e-freightex) in

East Africa

Final Report – July 2013

Volume I

Upper Quartile LLP

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 2

Contents ACRONYMS ......................................................................................................................... 6

EXECUTIVE SUMMARY ....................................................................................................... 8

1. INTRODUCTION .......................................................................................................... 13

1.1 Commissioned Project .............................................................................................. 13

1.2 Project Background .................................................................................................. 13

1.3 Project Objectives ..................................................................................................... 14

1.4 Failed Attempts ......................................................................................................... 14

1.5 Study Work Plan ....................................................................................................... 14

1.6 Structure of the Draft Report ..................................................................................... 15

2. E-FREIGHTEX MARKET ............................................................................................. 16

2.1 Introduction ............................................................................................................... 16

2.2 Types of E-Freightex's .............................................................................................. 16

2.2.1 Type 1: Quotation Engine E-Freightex .................................................................. 16

2.2.2 Type 2: Matching Engine E-Freightex ................................................................... 17

2.2.3 Type 3: Matching Engine E-Freightex with Aggregate Reporting .......................... 17

2.2.4 Type 4: Mature Freightex with Advanced Features ............................................... 18

2.3 Synergies Between other platforms .......................................................................... 19

2.3.1 Introduction ........................................................................................................... 19

2.3.2 Single Window Information for Trade (SWIFT) ...................................................... 19

2.3.3 Transport Observatory .......................................................................................... 19

2.3.4 Integrated Border Management ............................................................................. 20

2.3.5 Other Freight Studies ............................................................................................ 20

2.4 Key Freight Project Issues and Challenges ............................................................... 21

3. EAST AFRICA’S VOLUME AND TRADE DIRECTION ................................................. 23

3.1 Trade Performance ................................................................................................... 23

3.2 Top Exports and Imports ........................................................................................... 23

3.3 Intra-Regional Trade ................................................................................................. 24

3.4 East Africa Container Port Traffic of the Region ........................................................ 25

3.5 Import-Export Cargo Time in the Region ................................................................... 25

3.6 Import-Export Cost of a Container in the Region ....................................................... 27

3.7 Freight Distribution .................................................................................................... 29

4. WORKSHOPS AND STAKEHOLDERS’ CONSULTATIONS OUTCOMES ................. 30

4.1 Inception Workshop .................................................................................................. 30

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 3

4.1.1 General ................................................................................................................. 30

4.1.2 Key Outcomes of the Inception Workshop ............................................................. 30

4.2 Stakeholders’ Consultation Workshops ..................................................................... 31

4.2.1 Selection of E-Freightex Type ............................................................................... 31

4.2.2 Expected Impacts of E-Freightex Portal ................................................................ 32

4.2.3 Operation and Management of E-Freightex Portal ................................................ 32

4.3 Stakeholder Validation Workshop ............................................................................. 33

5. OPTIONEERING .......................................................................................................... 34

5.1 Introduction ............................................................................................................... 34

5.2 Methodology ............................................................................................................. 34

5.2.1 Overview ............................................................................................................... 34

5.2.2 Qualitative Assessment ......................................................................................... 34

5.3 Outcome of Optioneering .......................................................................................... 38

6. DESIGN OF E-FREIGHTEX ......................................................................................... 39

6.1 Business Process Management (BPM) - As Is .......................................................... 39

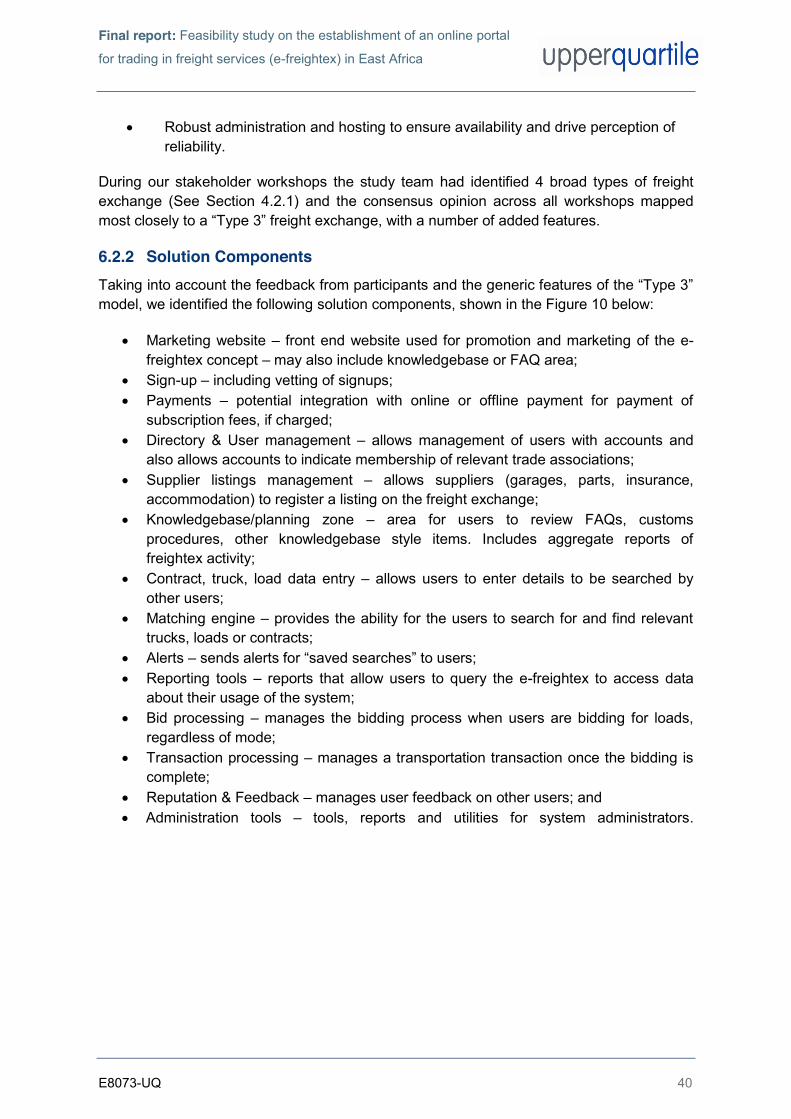

6.2 Solution Components for To-Be ................................................................................ 39

6.2.1 Key Requirements ................................................................................................. 39

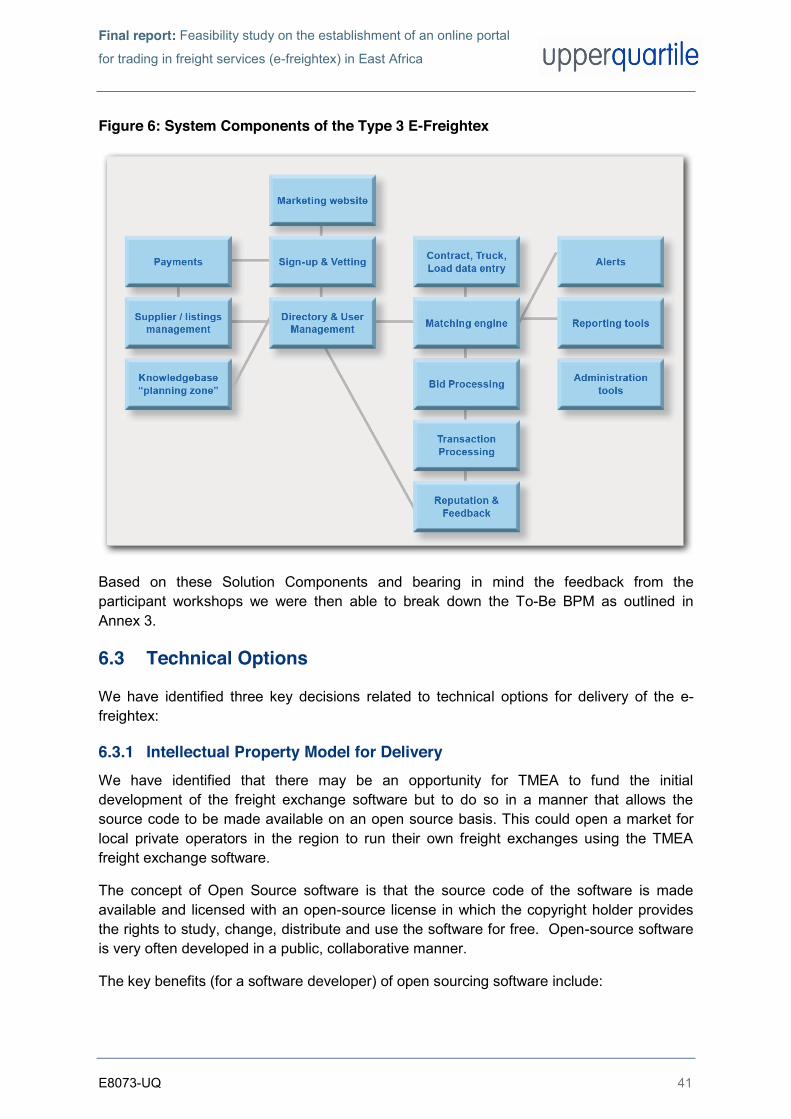

6.2.2 Solution Components ............................................................................................ 40

6.3 Technical Options ..................................................................................................... 41

6.3.1 Intellectual Property Model for Delivery ................................................................. 41

6.3.2 Deployment and Development Technology Choices ............................................ 43

6.3.2.1 Deployment Technologies ................................................................................. 43

6.3.2.2 Development Technologies ............................................................................... 44

6.3.3 Hosting .................................................................................................................. 44

6.3.3.1 Scaling and Volume Predictions ........................................................................ 45

6.3.3.2 Availability and Disaster Recovery ..................................................................... 46

6.4 IT Capacity Requirements & Interventions Required ................................................. 46

6.4.1 Hosting Infrastructure in the Region ...................................................................... 46

6.4.2 Reliability of Local Connectivity ............................................................................. 47

6.4.3 Lack of General IT skills ........................................................................................ 47

6.4.4 Consolidating freight statistics from across the region ........................................... 48

6.5 Proposed Solution .................................................................................................... 48

6.5.1 Buy vs Build .......................................................................................................... 48

6.5.2 Proposed solution for feasibility study purposes .................................................... 51

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 4

6.6 Cost Estimates.......................................................................................................... 51

6.6.1 Software Development Costs ................................................................................ 51

6.6.2 Other initial development costs ............................................................................. 52

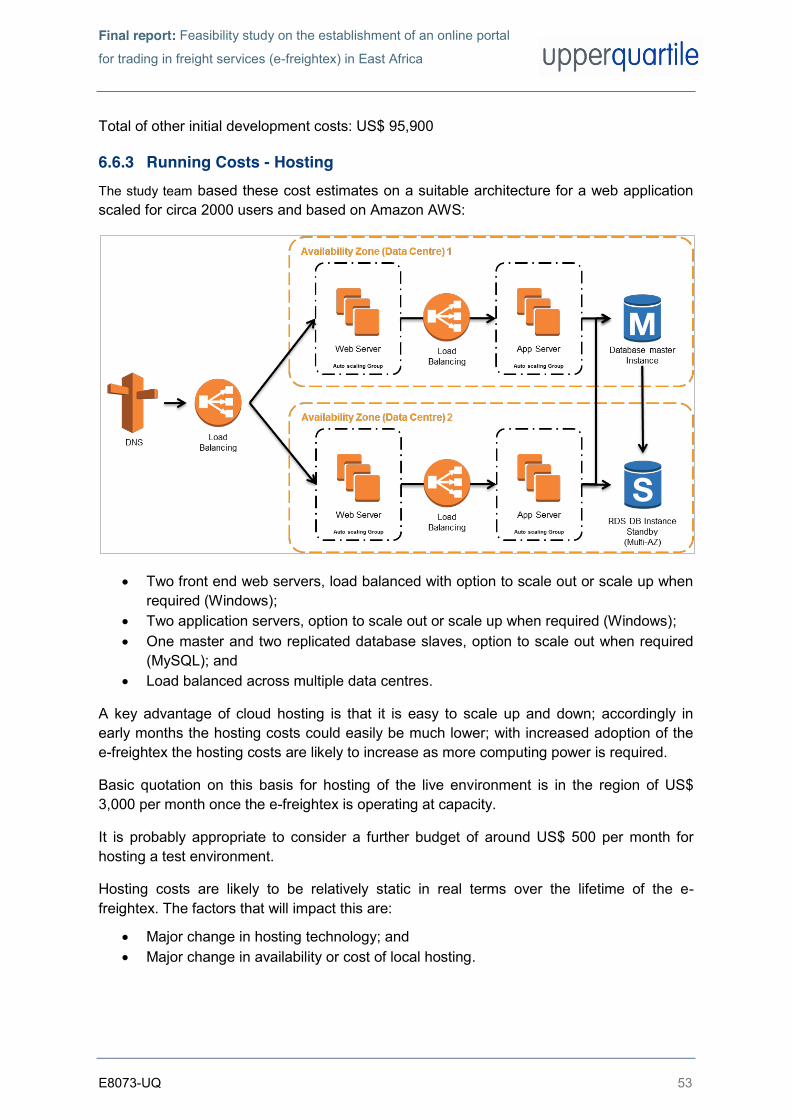

6.6.3 Running Costs - Hosting ....................................................................................... 53

6.6.4 Running Costs – Administration Staff and Equipment Costs ................................. 54

6.6.5 Running Costs – Software Support and Maintenance ........................................... 54

6.6.6 Running Costs - Management & Admin overheads ............................................... 54

6.6.7 Payment Transactions Cost .................................................................................. 56

6.6.8 Overall Cost Summary .......................................................................................... 56

7. THE VALUE FOR MONEY CASE ................................................................................ 58

7.1 Container Demand Forecasts ................................................................................... 58

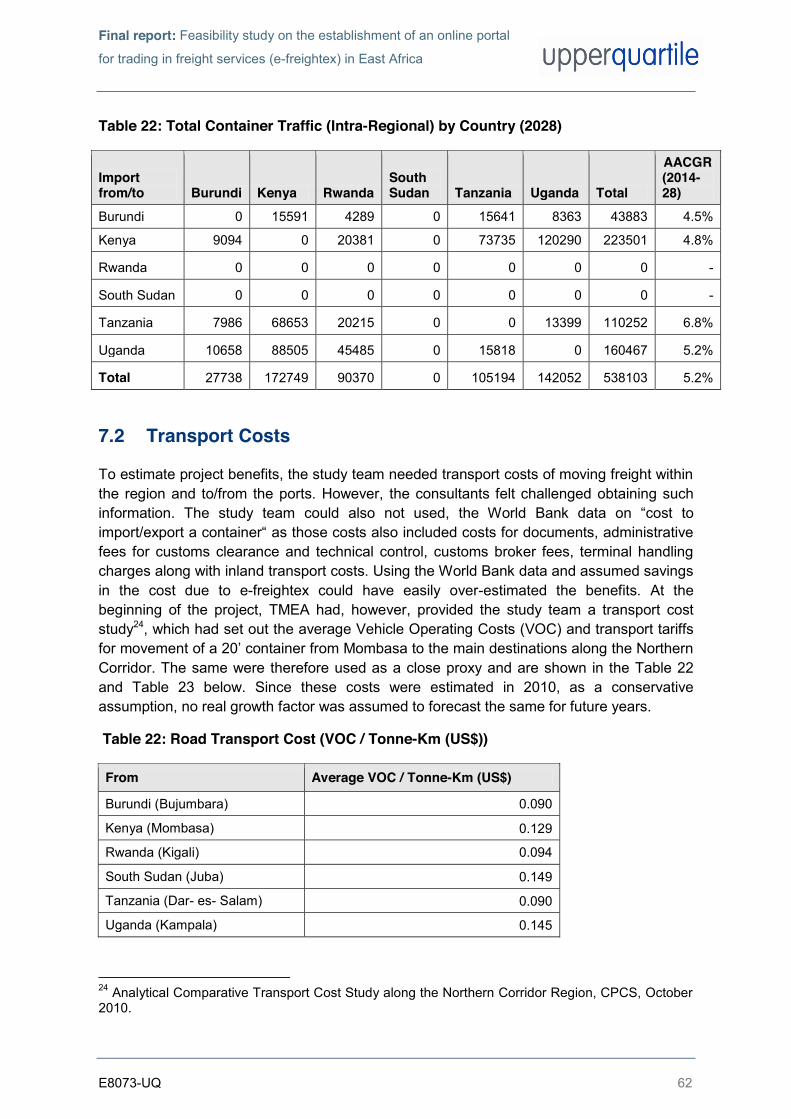

7.2 Transport Costs ........................................................................................................ 62

7.3 The Value for Money Case ....................................................................................... 63

7.3.1 Introduction ........................................................................................................... 63

7.3.2 Options Assessment ............................................................................................. 63

7.3.3 Definition of Scenarios .......................................................................................... 63

7.3.4 Appraisal Period .................................................................................................... 63

7.3.4 Project Costs ......................................................................................................... 64

7.3.5 Monetised Benefits of the Project .......................................................................... 64

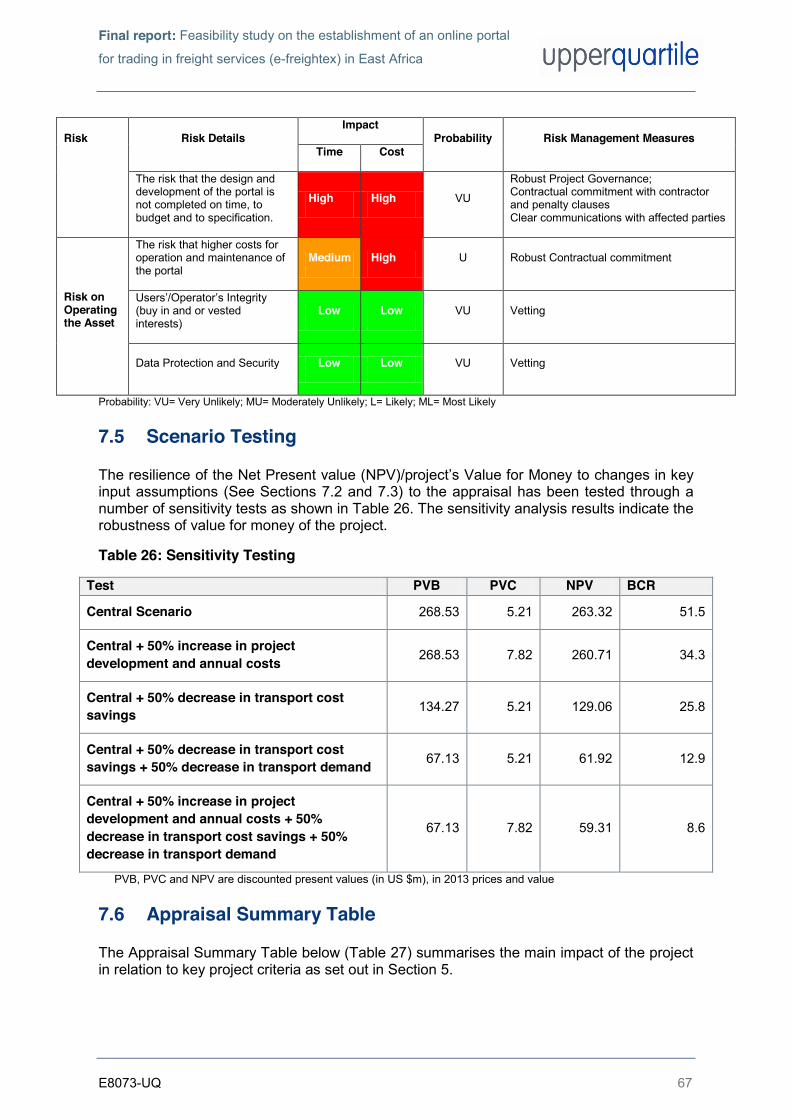

7.4 Risk Assessment ...................................................................................................... 65

7.4.1 Introduction ........................................................................................................... 65

7.4.2 Risk Assessment ................................................................................................... 65

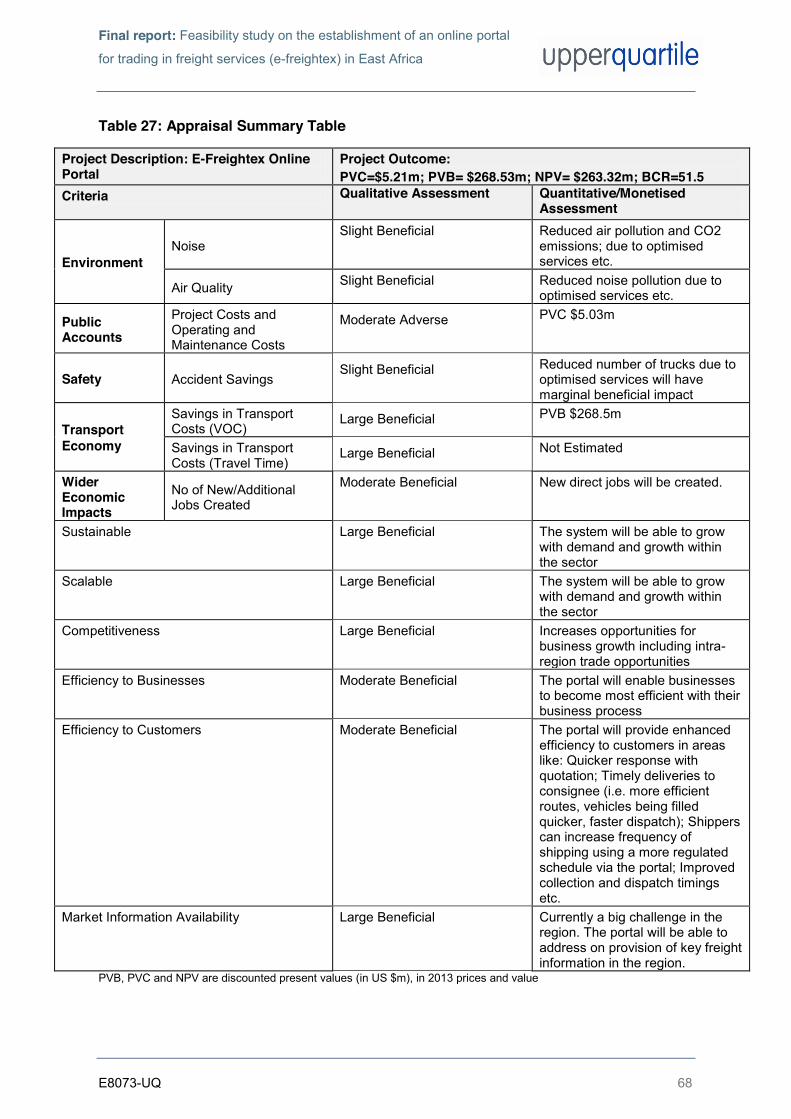

7.5 Scenario Testing ....................................................................................................... 67

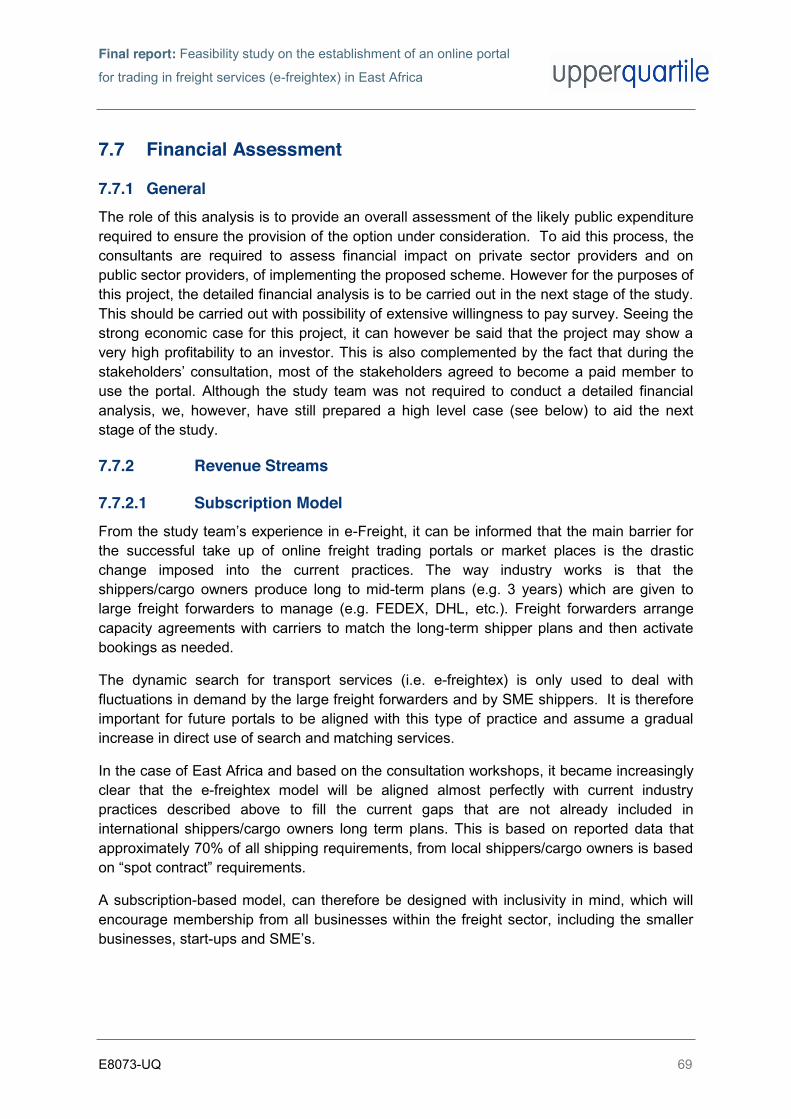

7.6 Appraisal Summary Table ......................................................................................... 67

7.7 Financial Assessment ............................................................................................... 69

7.7.1 General ................................................................................................................. 69

7.7.2 Revenue Streams ................................................................................................ 69

7.7.2.1 Subscription Model ............................................................................................ 69

7.7.2.2 Fee-based Model ............................................................................................... 73

7.7.2.3 Advertising Revenues ........................................................................................ 73

7.8 E-Freightex Ownership, Management and Regulation Options ................................. 74

7.8.1 Options for Ownership, Management and Regulation of e-freightex ...................... 74

8. CONCLUSIONS AND RECOMMENDATIONS ............................................................. 76

8.1 Conclusions .............................................................................................................. 76

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 5

8.2 Recommendations .................................................................................................... 76

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 6

ACRONYMS ABADT - Association Burundaise des Agences en Douaneet Transitaires,

Burundi ACOBU - Chambre Sectorielle des Commercants du Burundi/Service Chamber ADR - Association des Agences en Douane du Rwanda AFAB - Association des femmes d'affaires du Burundi ATIB - International Transporters Association of Burundi B2B - Business to Business B2C - Business to Consumer BPM - Business Process Mapping C&F - Clearing and Forwarding CCTTFA - Central Corridor Transit Transport Facilitation Agency CCS - Consultative Committee of Stakeholders EAC - East African Community EATTA - East Africa Tea Trade Association FEAFFA - Federation of East African Freight Forwarders Associations FEARTA - Federation of East Africa Road Transport Association FPEAK - Fresh Produce Exporters Association of Kenya IT - Information and Technology KAM - Kenya Association of Manufacturers KIFWA - Kenya International freight & Warehousing Association KEPSA - Kenya Private Sector Alliance KSAA - Kenya Ships Agents Association KENTRADE - Kenya Trade Network Agency KPA - Kenya Ports Authority KSC - Kenya Shippers Council KTA - Kenya Transporters Association Ministry of Trade - Rwanda Ministry of Trade NCTTCA - Northern Corridor Transit Transport Coordination Authority NTB - Non Tariff Barrier RDB - Rwanda Development Board RLDTA - Regional Lorry Drivers and Transporters Association RTA - Road Transport Association RVR - Rift Valley Railways TAFFA - Tanzania Freight Forwarders Association TATOA - Tanzania Truck Owners Association TPA - Tanzania Port Authority TSC - Tanzania Shippers Council TMEA - Trade Mark East Africa ToR - Terms of Reference UCIFA - Uganda Clearing Industry and Forwarding Association UCTOA - Uganda Commercial Trucker Owners Association

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 7

UFFA - Uganda Freight Forwarders Association UNTA - Uganda National Transporters Alliance USC - Uganda Shippers Council UTA - Uganda Transporters Alliance US$ - United States Dollar UQ - Upper Quartile

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 8

EXECUTIVE SUMMARY

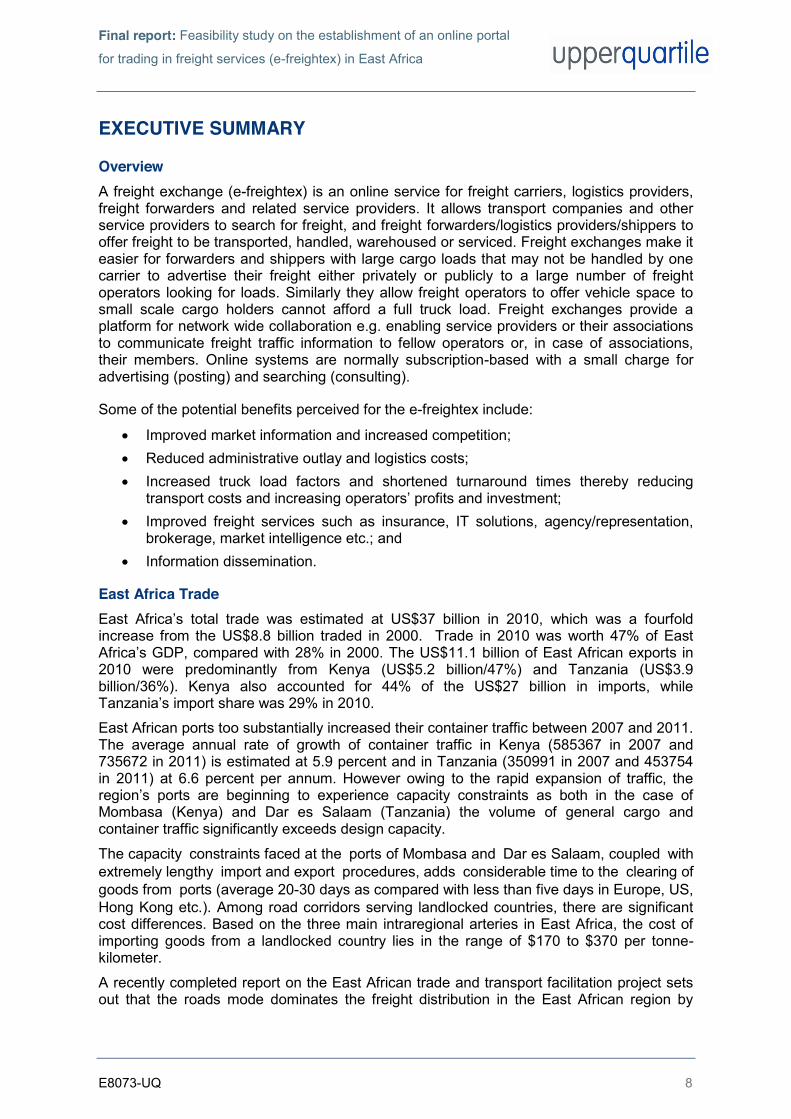

Overview A freight exchange (e-freightex) is an online service for freight carriers, logistics providers, freight forwarders and related service providers. It allows transport companies and other service providers to search for freight, and freight forwarders/logistics providers/shippers to offer freight to be transported, handled, warehoused or serviced. Freight exchanges make it easier for forwarders and shippers with large cargo loads that may not be handled by one carrier to advertise their freight either privately or publicly to a large number of freight operators looking for loads. Similarly they allow freight operators to offer vehicle space to small scale cargo holders cannot afford a full truck load. Freight exchanges provide a platform for network wide collaboration e.g. enabling service providers or their associations to communicate freight traffic information to fellow operators or, in case of associations, their members. Online systems are normally subscription-based with a small charge for advertising (posting) and searching (consulting).

Some of the potential benefits perceived for the e-freightex include:

Improved market information and increased competition; Reduced administrative outlay and logistics costs; Increased truck load factors and shortened turnaround times thereby reducing

transport costs and increasing operators’ profits and investment;; Improved freight services such as insurance, IT solutions, agency/representation,

brokerage, market intelligence etc.; and Information dissemination.

East Africa Trade East Africa’s total trade was estimated at US$37 billion in 2010, which was a fourfold increase from the US$8.8 billion traded in 2000. Trade in 2010 was worth 47% of East Africa’s GDP, compared with 28% in 2000. The US$11.1 billion of East African exports in 2010 were predominantly from Kenya (US$5.2 billion/47%) and Tanzania (US$3.9 billion/36%). Kenya also accounted for 44% of the US$27 billion in imports, while Tanzania’s import share was 29% in 2010.

East African ports too substantially increased their container traffic between 2007 and 2011. The average annual rate of growth of container traffic in Kenya (585367 in 2007 and 735672 in 2011) is estimated at 5.9 percent and in Tanzania (350991 in 2007 and 453754 in 2011) at 6.6 percent per annum. However owing to the rapid expansion of traffic, the region’s ports are beginning to experience capacity constraints as both in the case of Mombasa (Kenya) and Dar es Salaam (Tanzania) the volume of general cargo and container traffic significantly exceeds design capacity.

The capacity constraints faced at the ports of Mombasa and Dar es Salaam, coupled with extremely lengthy import and export procedures, adds considerable time to the clearing of goods from ports (average 20-30 days as compared with less than five days in Europe, US, Hong Kong etc.). Among road corridors serving landlocked countries, there are significant cost differences. Based on the three main intraregional arteries in East Africa, the cost of importing goods from a landlocked country lies in the range of $170 to $370 per tonne-kilometer.

A recently completed report on the East African trade and transport facilitation project sets out that the roads mode dominates the freight distribution in the East African region by

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 9

carrying 80% of the regional ton-km. Pipelines carry 10%, which is followed by rail (8%) and air transport (2%).

Stakeholder Consultations The participants were presented with 4 types based on the complexity of a freight exchange:

Type 1 – Quotation engine, simplest form of freight exchange, allows buyers to find sellers (generally regarded by participants as too simplistic);

Type 2 – Matching engine to allow buyers and sellers to find each other; Type 3 – As Type 2, with additional aggregate reporting services; and Type 4 – As Type 3, with additional value-added features (generally regarded by

participants as a good “end goal” but likely more complex than necessary to derive the key benefits of the freight exchange concept)

During the stakeholders’ consultation stage, 83.5% of the total stakeholders of the region preferred Type 3 to be taken forward to the next stage of the study; followed by 12.5% showing preference for Type 4; and the remaining 5% voting for Type 1 e-freightex system.

When stakeholders were asked that what percentage of transport costs reduction do they envisage the e-freightex portal can generate; 73.9% of those who voted thought it could reduce the transport costs by 5%; 21.7% thought that the development of e-freightex portal could reduce the transport costs by 10%; and the remaining 4.4% thought the costs savings will be higher than 10%.

Optioneering A preliminary appraisal of each e-freightex type was designed to show the broad impacts of a range of criteria on them. The information derived from the exercise helped UQ and TMEA to identify the preferred type of e-freightex. It was concluded that Type 3 e-freightex (Matching Engine E-Freightex with Aggregate Reporting) was ranked first among the other types of e-freightex’s; and was clearly the most preferred type of e-freightex.

E-Freightex Design The study team assessed the requirements and functions for the e-freightex system including business processes, system development and hosting requirements. The study team also undertook the schematic design of the e-freightex system showing key components of the e- freightex system.

The study team found out that a key decision which will need to be made by the operator in the next stage of implementation of the e-freightex is whether to “build or buy” the e-freightex system software.

For the purposes of the feasibility study the consultants have assumed that the operator would make a “Build” decision because:

It provides maximum flexibility in terms of addressing requirements;

It maximises ownership and therefore control of the overall e-freightex solution, potentially with a positive impact on sustainability; and

It is definitely do-able (the study team do not know if any third parties want to sell or license their freight exchange software).

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 10

Figure E.1: Buy vs Build options

Project Costs The project development cost for the e-freightex portal was estimated at circa US$ 0.45m (2013 prices). The operational cost was estimated at circa US$ 0.6m per annum.

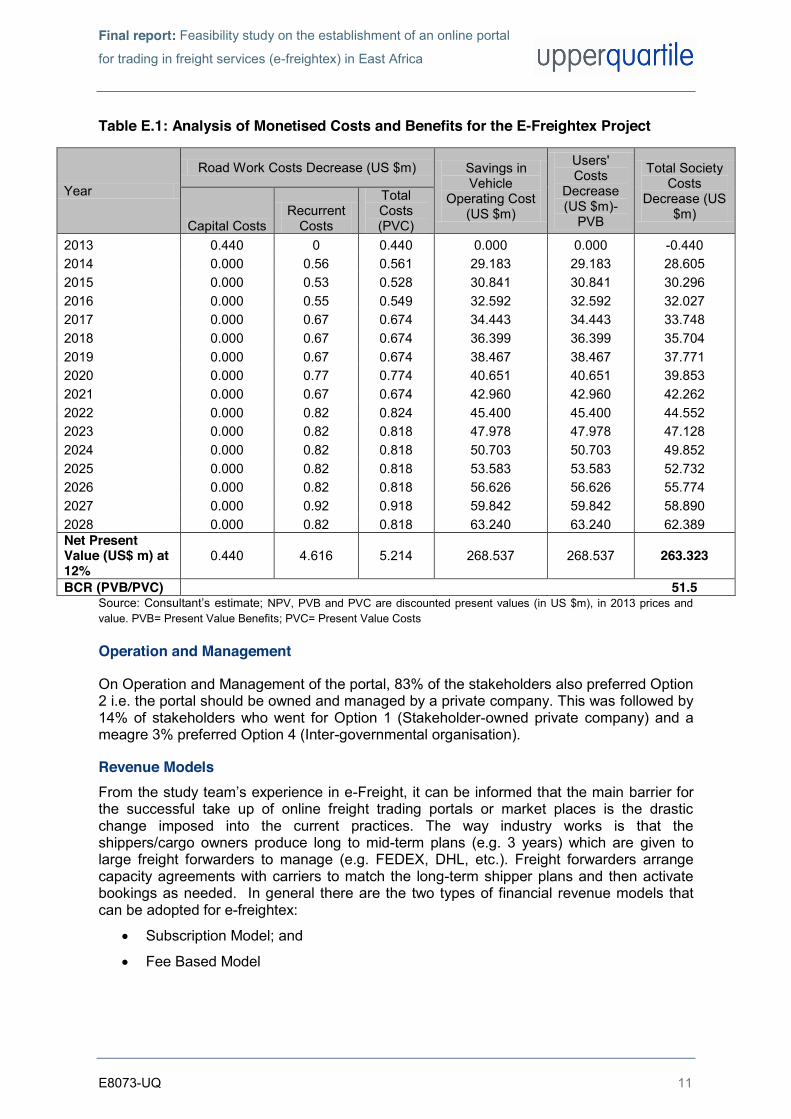

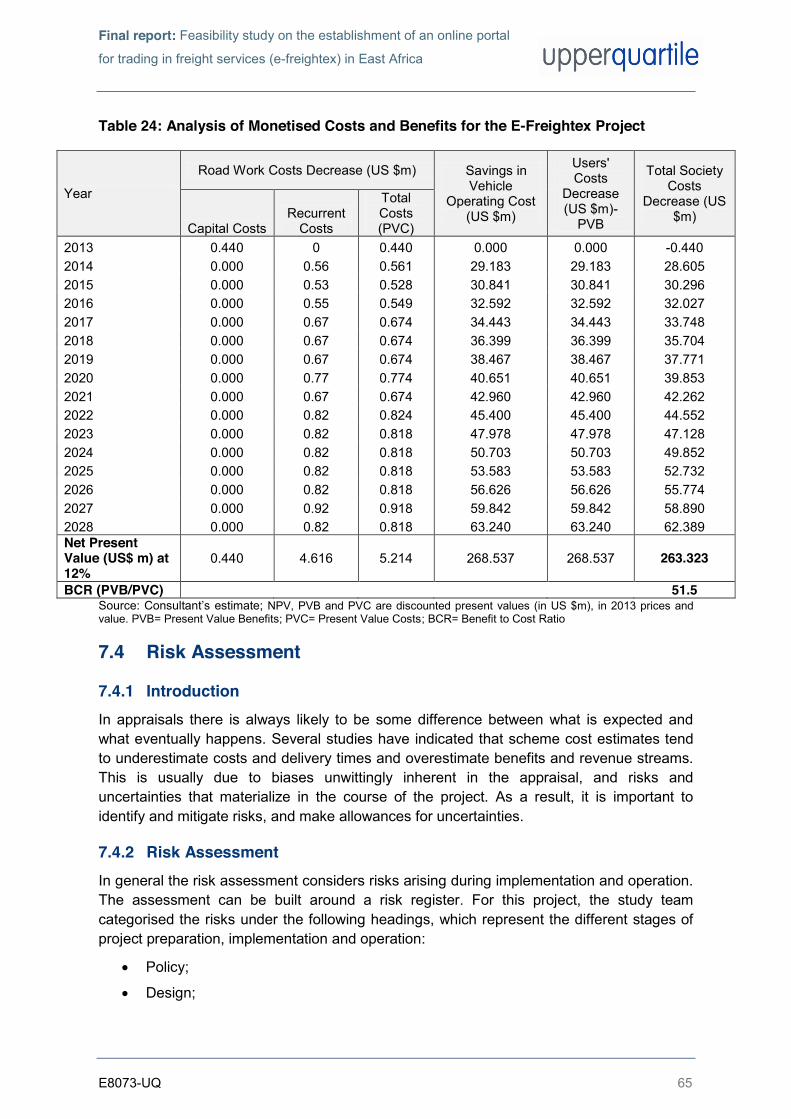

The Value for Money Case Table E.1 below summarise the costs and benefits and show that the Net Present Value (NPV) of the project is estimated at US$ 263.0m. This large positive value indicates that the benefits for the scheme considerably outweigh the costs i.e. the scheme offers a very high value for money to the taxpayer.

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 11

Table E.1: Analysis of Monetised Costs and Benefits for the E-Freightex Project

Year

Road Work Costs Decrease (US $m) Savings in Vehicle

Operating Cost (US $m)

Users' Costs

Decrease (US $m)-

PVB

Total Society Costs

Decrease (US $m)

Capital Costs Recurrent

Costs

Total Costs (PVC)

2013 0.440 0 0.440 0.000 0.000 -0.440 2014 0.000 0.56 0.561 29.183 29.183 28.605 2015 0.000 0.53 0.528 30.841 30.841 30.296 2016 0.000 0.55 0.549 32.592 32.592 32.027 2017 0.000 0.67 0.674 34.443 34.443 33.748 2018 0.000 0.67 0.674 36.399 36.399 35.704 2019 0.000 0.67 0.674 38.467 38.467 37.771 2020 0.000 0.77 0.774 40.651 40.651 39.853 2021 0.000 0.67 0.674 42.960 42.960 42.262 2022 0.000 0.82 0.824 45.400 45.400 44.552 2023 0.000 0.82 0.818 47.978 47.978 47.128 2024 0.000 0.82 0.818 50.703 50.703 49.852 2025 0.000 0.82 0.818 53.583 53.583 52.732 2026 0.000 0.82 0.818 56.626 56.626 55.774 2027 0.000 0.92 0.918 59.842 59.842 58.890 2028 0.000 0.82 0.818 63.240 63.240 62.389 Net Present Value (US$ m) at 12%

0.440 4.616 5.214 268.537 268.537 263.323

BCR (PVB/PVC) 51.5 Source: Consultant’s estimate;; NPV, PVB and PVC are discounted present values (in US $m), in 2013 prices and value. PVB= Present Value Benefits; PVC= Present Value Costs

Operation and Management

On Operation and Management of the portal, 83% of the stakeholders also preferred Option 2 i.e. the portal should be owned and managed by a private company. This was followed by 14% of stakeholders who went for Option 1 (Stakeholder-owned private company) and a meagre 3% preferred Option 4 (Inter-governmental organisation).

Revenue Models From the study team’s experience in e-Freight, it can be informed that the main barrier for the successful take up of online freight trading portals or market places is the drastic change imposed into the current practices. The way industry works is that the shippers/cargo owners produce long to mid-term plans (e.g. 3 years) which are given to large freight forwarders to manage (e.g. FEDEX, DHL, etc.). Freight forwarders arrange capacity agreements with carriers to match the long-term shipper plans and then activate bookings as needed. In general there are the two types of financial revenue models that can be adopted for e-freightex:

Subscription Model; and

Fee Based Model

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 12

For the purposes of this feasibility study the consultants have followed the predominant model in the industry and chosen to follow a subscription model rather than one based on transaction fees.

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

!

E8073-UQ 13

1. INTRODUCTION

1.1 Commissioned Project

TradeMark East Africa (TMEA) commissioned Upper Quartile (UQ) to carry a feasibility study on the establishment of an online portal for trading in freight services (e-freightex) in East Africa in March 2013. Along with setting out a number of specific tasks to successfully achieve the outputs of this study, the study’s Terms of Reference (ToR) also set out a challenging timeframe to achieve the same. The whole study was aimed to be finished in circa fourteen weeks starting from end March/beginning of April 2013.

1.2 Project Background

A freight exchange (e-freightex) is an online service for freight carriers, logistics providers, freight forwarders and related service providers. It allows transport companies and other service providers to search for freight, and freight forwarders/logistics providers/shippers to offer freight to be transported, handled, warehoused or serviced. Freight exchanges make it easier for forwarders and shippers with large cargo loads that may not be handled by one carrier to advertise their freight either privately or publicly to a large number of freight operators looking for loads. Similarly they allow freight operators to offer vehicle space to small scale cargo holders cannot afford a full truck load. Freight exchanges provide a platform for network wide collaboration e.g. enabling service providers or their associations to communicate freight traffic information to fellow operators or, in case of associations, their members. Online systems are normally subscription-based with a small charge for advertising (posting) and searching (consulting).

Discussions on the development of an e-freightex online portal in East Africa have been ongoing since 2005. While regional stakeholder groups have indicated broad support for the concept, capacity constraints have meant that there has been limited partner activity in this area in the period. However, more recently, renewed interest in the concept has been intimated to TMEA from private sector organisations and through the two corridor authorities in the region. It is within this context that TMEA has agreed to support the development and implementation of an e-freightex portal.

The commissioning of this study to assess the feasibility of the concept can be viewed as a major step in taking this support forward. The outputs of the feasibility study were assumed to be a key strategic resource to guide future decisions on the costs, specification, and implementation of the finalised e-freightex solution. As such, the outputs of the feasibility study would play a key role in ensuring that TMEA, regional stakeholders, and the wider economy gains the maximum potential benefits and improved linkages from the implementation of the e-freightex portal. Some of the potential benefits perceived for the e-freightex include:

• Improved market information and increased competition; • Reduced administrative outlay and logistics costs; • Increased truck load factors and shortened turnaround times thereby reducing

transport costs and increasing operators’ profits and investment (See sections 3.5 and 3.6);

• Improved freight services such as insurance, IT solutions, agency/representation, brokerage, market intelligence etc.; and

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 14

brokerage, market intelligence etc.; and Information dissemination.

1.3 Project Objectives

The objective of the study is twofold:

To carry out scoping and appraisal work for the development of an online portal for trading in freight services in East Africa; and

To propose appropriate interventions for its implementation. TMEA also regarded that the study will also help to elicit questions such as whether there is enough demand for such a service and why some private sector attempts failed in developing the online portal.

1.4 Failed Attempts

As set out above discussions on developing an e-freightex portal have been going on since around 2005. In February 2006, three leading industry organisations (KIFWA, KTA and KAM), the Northern Corridor’s Authority (TTCA) and a supporting team of specialists from USAID East Africa’s Trade Hub programme held consultations to discuss ways of establishing an online B2B platform (e-freightex) to support e- commerce in freight services in East Africa. Although the promoters reached a loose agreement to promote the initiative but, due to limited capacity, could not take the idea forward beyond that stage. No other major developments have taken place in this area except one or two failed attempts by private entrepreneurs. During the course of the study, the study team met one of those entrepreneurs and sought his views on the project and the reasons for the previous failed attempt. The three key reasons that the concept could not take off beyond a certain point are as follows:

Technology constraint, including e.g. the lack of advancement in information technology in the region ten years back. It should also be noted that, in real terms, the same was also quite expensive to adopt then;

Lack of understanding and vision as the private entrepreneur was unable to make the key stakeholders understand and appreciate the project concept including its potential benefits; and finally

Lack of enthusiasm and support shown by the stakeholders.

1.5 Study Work Plan

To achieve the objectives of the study, UQ developed a work plan comprising the following high-level tasks:

Mobilization and Inception; Inception Workshop; Stakeholder’s Consultation Workshops; Progress Report; E-Freightex Feasibility Analysis; Draft Final Report;

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

! ! ! !

E8073-UQ 15

• Final Report.

1.6 Structure of the Draft Report

The reminder of this report is structured as follows:

• Section 2 presents different types of e-freightex portals and sets out key challenges and issues of developing such projects;

• Section 3 provides a snapshot of East Africa’s trade;

• Section 4 details out outcomes of inception workshop and stakeholders’ workshops;

• Section 5 sets out optinoneering exercise undertaken for the four types of e-freightex portals;

• Section 6 presents detailed information on e-freightex design including information on BPM “As is” and “To be”;

• Section 7 presents the value for money case of the project including potential options on management, operation and regulation of the e-freightex portal; and finally

• Section 8 sets out conclusions and recommendations of the study.

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 16

2. E-FREIGHTEX MARKET

2.1 Introduction A freight exchange (freightex) is a real-time service where:

Transporters, freight forwarders, shipping agents and rail road operators etc. can list the availability of capacity to transport loads via several modes of transport;

Load providers who have a requirement to transport goods to a consignee can add/list loads, freight and cargo to the system, providing the opportunity for transport providers to make offers or bid on the listing, providing competitive pricing to Load providers;

Freight exchanges (freightex) provide a platform that allows carriers to communicate freight traffic information to other operators;

Freight can be advertised privately or publicly to participants that are looking for loads, and vehicle space can be advertised to participants looking to make shipments;

Vehicle operators add vehicles to the system that are available to transport a load; and

Load providers add loads, freight and cargo to the system that are looking for a vehicle to move the goods.

2.2 Types of E-Freightex's For the purposes of this study UQ identified four types of e-freightex solutions, of increasing complexity:

2.2.1 Type 1: Quotation Engine E-Freightex This is the simplest type of e-freightex that acts as a freight shipping quotation engine and allows buyers to find sellers e.g. e-Freight1 (US).

The key features of this type of freightex include:

Price comparison is available to all participants for a range of destinations and for a range of services (e.g. driver assistance, hazardous materials, time/date restrictions, Full truck load (FTL) vs Less-than truck load (LTL), etc.);

Multiple carriers can provide quotation algorithms for their standard shipping rates to/from a range of destinations (e.g. freight terminals etc.) or based on distance etc.; and

Shippers are presented with a range of carrier options and must establish contact and negotiate with carriers (or book shipment via the Freightex).

Perceived benefits of this type of freightex include:

Improved market awareness of carrier shipping rates;

Reduces barriers to entry for new market participants;

1 http://www.efreight.com/

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 17

Improved market efficiency regarding FTL/LTL loads;

Replaces manual estimation with automated shipping quotes; and

Likely to reduce effective shipping costs.

2.2.2 Type 2: Matching Engine E-Freightex This is a more complex freightex type that provides a matching service i.e. allows buyers and sellers to find each other. Examples include RightNowLoads2 (US) or Teleroute3 (EU).

The key features of this type of freightex include:

Carriers can enter specific space availability details for specific journeys (origin -> destination) with specific truck types and/or other restrictions;

Carriers can search for "backhaul" (return) loads as well as outbound; and

When matched with a load, carriers can bid on the load. Carriers and shippers need to contact each other to negotiate and agree terms.

Perceived benefits of this type of freightex (over and above Type 1 freightex) include:

Matching service proactively alerts carriers to load opportunities;

Freightex holds more accurate information regarding freight movements;

Enables route planning by carriers;

Simplifies process for bespoke pricing on specific journeys or for loads with specific requirements; and

Supports more open communication between shippers and carriers by providing a single hub for interactions.

2.2.3 Type 3: Matching Engine E-Freightex with Aggregate Reporting This is basically a Type 2 Freightex but with additional aggregate reporting services e.g. 123Loadboard4. The relatively simple statistics presented on this type are useful confidence-building numbers to encourage new participants to use the Freightex. In addition to this, it is also possible to include a richer set of statistics (popular destinations, total mileage, load types, etc.), which would be useful for all participants in gauging the success and usefulness of the Freightex.

Perceived benefits of this type of freightex (over and above Type 2 freightex) include:

Provision of statistics builds confidence for new participants and demonstrates that the Freightex is being used; and

2 http://www.rightnowloads.com/search.php?one=IL&two=FL&Submit2.x=66&Submit2.y=17&Submit2=Submit 3 http://freights.teleroute.com/#/from/Great-Britain/to/Great-Britain 4 http://www.123loadboard.com/signup/how-it-works/stats.aspx

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 18

Stats can be used to support aggregate reporting of freight activity across the area covered by the Freightex.

It should be noted that as a Type 3 e-freightex matures towards becoming a Type 4 e-freightex (See Section 2.2.4), it is common to see additional features being added in accordance with operator’s and users’ needs/requirements/preferences – such as:

Multi-user accounts (e.g. GetLoaded5);

Participant ratings and "top rated" carriers etc.; and

Mobile apps for use by shippers and carriers to allow searches and matches to be performed "on the move".

2.2.4 Type 4: Mature Freightex with Advanced Features As a Type 3 freightex matures over time, it will evolve into a “Type 4” freightex. With usage and increasing user experience it can be expected that the operator and users will want to improve the utility of the freightex with a range of value-added features (e.g. GetLoaded6). Typical features of this type of mature freightex would include:

Integration with third-party Transportation Management System (TMS) solutions as well as simplified upload of load and truck availability via email, File Transfer Protocol (FTP) and other mechanisms;

Advertising for related services (common examples are invoice factoring, software, insurance, asset financing, routing solutions);

Built-in invoice factoring and payment clearance (e.g. Transite case study7);

Industry specialisms (Livestock8, Vehicle transport9); and

Multi-modal quotes (e.g. intermodal shipping quotes provided by Canadian rail operator CN10).

It should be noted that in the case of GetLoaded the features on offer to freightex users vary depending on their subscription level and include options for alerts, matching, directory entries, multi-load searches, routing and tolls information and a variety of other features. There are also a number of similar freightexs with active user communities/forums (e.g. Livestock Network11) where participants were able to discuss issues, ask peers for advice etc.

Perceived benefits of this type of freightex (over and above Type 3 freightex) include:

Supports development of the community of participants;

Provides opportunities for supporting industries to participate in success of Freightex;

Improves utility of Freightex service to participants; 5 http://www.getloaded.com/ 6 http://www.getloaded.com/ 7 http://transite.com/news/Pergo_casestudy.pdf 8 http://www.livestocknetwork.com/ 9 http://www.carloadusa.com/ 10 http://www.cn.ca/en/our-business/prices-tariffs-transit-times 11 http://www.livestocknetwork.com/

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 19

Increases integration of Freightex with day-to-day freight operations; and

Provides opportunities to generate revenue from Freightex operation.

2.3 Synergies Between other platforms

2.3.1 Introduction A number of existing/proposed initiatives in East Africa (including those initiated by TMEA) were also reviewed briefly as part of this study. A description of a selected sample of these is provided below.

2.3.2 Single Window Information for Trade (SWIFT) The Single Window Information for Trade (SWIFT) is aimed to allow cross-border traders to access, apply for and submit regulatory documents, such as customs declarations, certificates of origin and applications for import/export permits, at a single location. Key initiatives include:

Tea Board of Kenya - TMEA signed an Memorandum of Understanding (MoU) with Tea Board of Kenya (TBK) in 2012 to develop an e-portal that would automate its business process, which touched on trade with regards to the application of various licenses and the workflow from initiation to the point where applications are either approved or rejected.

Rwanda Bureau of Standards - TMEA has also signed a Memorandum of Understanding (MoU) with the Rwanda Bureau of Standards (RBS) to provide an e-portal that would automate most of their internal processes with the exception of their laboratories as their had already purchased a separate system for this.

Expected results include: Increased Efficiency through time and cost savings;

Easier Access to standardised documents and other information at a single entry point; and

Increased compliance rates and reduces inaccurate documents.

Potential synergy areas with the e-freightex include:

Sharing of statistical and reporting information; and

Automated posting of load or contract opportunities to the e-freightex.

2.3.3 Transport Observatory The northern and central corridors are the primary transport networks linking the ports of Mombasa and Dar es Salaam to the landlocked countries of Uganda, Rwanda, South Sudan and Burundi. TMEA is supporting the corridor authorities to establish Transport Observatories (TOs) where collected data is analysed to map the various bottlenecks and identify the non-tariff barriers, with the aim of reducing transport-related costs. The delays identified by the TOs are analysed by cause, location, date and time, and parameters, such

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 20

as direction of travel, nationality of vehicles and types of cargo. The information is disseminated to partner states of the East African Community (EAC) to inform policy and decision-making that will reduce transport related costs. Expected results include:

Policy makers and the business community will improve their knowledge of corridor performance; and

Potential shorter transport times at less costs.

Potential synergy areas with the e-freightex project include:

Sharing of statistical information regarding freight movements; and

Transport-related costs.

2.3.4 Integrated Border Management Integrated Border Management (IBM) is a concept for establishing collaboration in the management of borders among agencies responsible for border controls. The framework is an essential tool for ensuring that a One-Stop Border Post (OSBP) becomes operational immediately when construction is completed. The essence of an OSBP is not the infrastructure and facilities but implementation of one-stop controls. Traffic stops at one side of the border only, which makes it easier for traders, transporters and the public in general to cross from one country to another.

IBM gives border agencies an opportunity to modernize their services and build their institutional capacity while enjoying new infrastructure and facilities. It will improve management of individual agencies and their standing in the local community, and will enable them to contribute to the regional integration agenda. Expected results include:

30% reduction in clearance times for passengers and transit goods; and

Better transparency and accountability at cross-border operations.

Potential synergy areas with the e-freightex project include:

Sharing of statistical information regarding freight movements; and

Transport-related costs.

2.3.5 Other Freight Studies A number of freight logistics studies have been completed or currently being commissioned (including by TMEA) in the region. The aim of these studies varied from analysing freight logistics chains and related markets in East Africa to transport costs of moving containers etc. The following key studies were reviewed:

Analytical Comparative Transport Cost Study along the Northern Corridor Region, prepared by CPCS;

Corridor Diagnostic Study of the Northern and Central Corridors of East Africa, prepared by Nathan Associates;

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 21

East Africa Freight Logistics Market Study, currently undertaken by CPCS;

Rwanda Integrated Trade Logistics Facilities Project, undertaken by Deloitte;

The ASSET Study by TMEA; and

Transport Prices and Costs in Africa, The World Bank.

Potential synergy areas with the commissioned e-freightex project include: freight logistics, Information dissemination, trade, transport-related costs etc.

2.4 Key Freight Project Issues and Challenges The study team sets out below key freight project issues, which involve multi-national stakeholders and policy changes at government level. It should be noted that the challenge of these issues is for countries and stakeholders to have an alignment of business processes with each other.

Stakeholder Identification and Needs Analysis – these systems need to be built with the needs of stakeholders in mind; if the wrong group of stakeholders is identified or their requirements not captured in sufficient detail then the project risks delivering functionality that is not required or that does not meet the needs of the participants.

Political Issues – Lack of co-operation and collaboration between countries, stakeholders, competitors and agencies. If these are lacking then the implementation of any kind of solutions that requires an integrated Business Process Model is a non-starter. For solutions to work there is an expectation to have consensus on ICT architecture, single template documents, base model for Business Processes and freight/logistics Government policies, regulations and legislations aligned between countries.

Competitors and Collaborative Working – Competitors are generally reluctant to share information relating to their business intelligence. Many feel that by collaborating via a portal/shared platform openly, they will expose their business intelligence about their business model, loads, type of contracts they undertake etc., and they will lose their competitive advantage. This issue must be considered when designing and presenting a draft ICT solution.

The Case for Change – there needs to be a compelling case for the reforms proposed by these systems. The following anecdote is taken from a case study on trade reform in Madagascar12, and could apply equally to public and private sector market participants: “Opposition to the reforms was widespread and came from many quarters. The private sector - resigned to the inefficiency and corruption in Customs - was reluctant to start paying the additional fees that the project would require and sceptical that such an ambitious and advanced solution would work in the Malagasy context. The 1,400-strong Customs service itself was also reluctant to change its

12 Kjartan Fjeldsted, 2009 Case study on trade reform in Madagascar, World Bank Publications

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 22

ways. Wedded to the old way of doing things, many customs agents also had a vested interest in existing arrangements, which brought steady revenues under the table.”

Technology Adoption – Even at the most basic level these projects have all depended on the willingness of participants to adopt the technologies being made available. Ease of use and simplicity of integration with existing business processes are high on the priority list for ensuring that technologies are used (provided that political issues can be overcome). Providing ubiquitous access methods for users (browser vs application, mobile vs desktop) are increasingly important and of course the robustness and uptime associated with online systems needs to be at an appropriately high level of service.

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 23

3. EAST AFRICA’S VOLUME AND TRADE DIRECTION

3.1 Trade Performance

East Africa’s total trade was estimated at US$37 billion in 2010, which was a fourfold increase (AACGR13 = 15% per annum) from the US$8.8 billion traded in 200014. Trade in 2010 was worth 47% of East Africa’s GDP, compared with 28% in 2000. The US$11.1 billion of East African exports in 2010 were predominantly from Kenya (US$5.2 billion/47%) and Tanzania (US$3.9 billion/36%). Kenya also accounted for 44% of the US$27 billion15 in imports, while Tanzania’s import share was 29% in 2010.

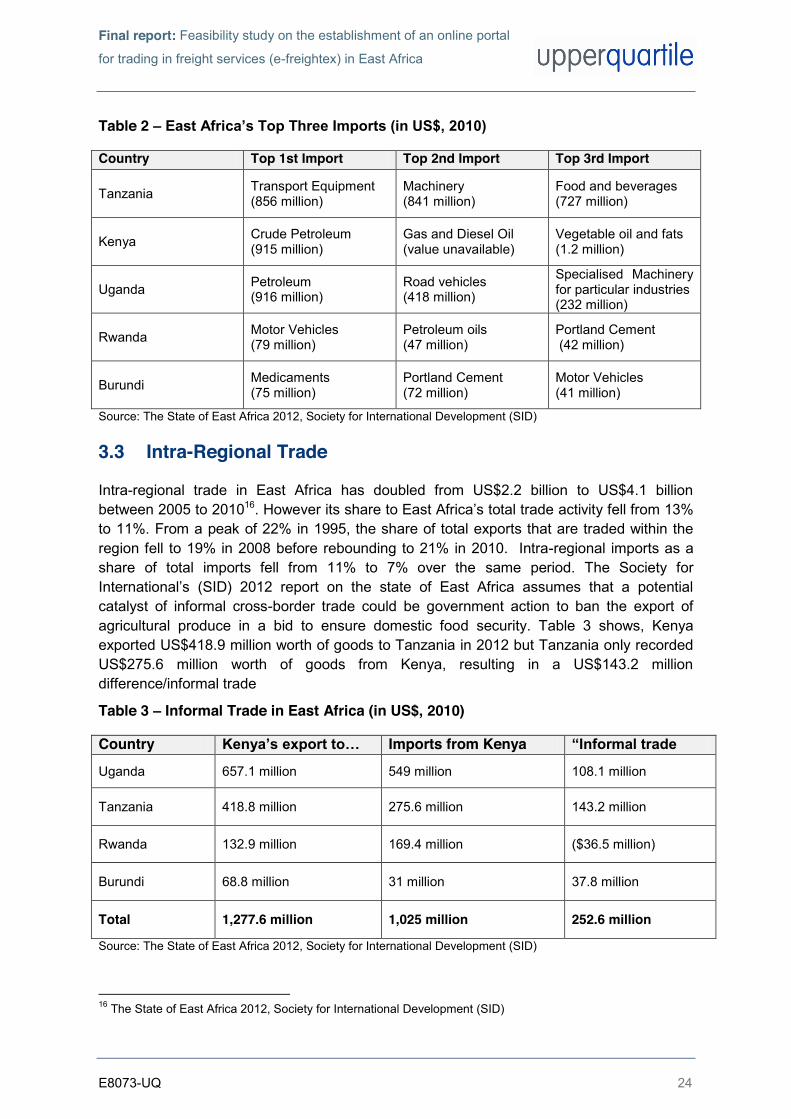

3.2 Top Exports and Imports

In 2010, the combined total of each of the five (Kenya, Tanzania, Uganda, Rwanda and Burundi) East African country’s top three exports was US$3.92 billion/36% of the region’s total exports. Agricultural products (tea, coffee, flowers, fish, tobacco and cashews) accounted for the majority of this, estimated to be US$2.7 billion of the top three exports. The balance US$1.2 billion of top three exports (as shown in Table 1 below) is made up almost entirely of gold.

Table 1 – East Africa’s Top Three Export Products (in US$, 2010)

Country Top 1st Export Top 2nd Export Top 3rd Export

Tanzania Gold (914 million)

Tobacco (121 million)

Cashews (118 million)

Kenya Tea (1.2 billion)

Cut flowers (312 million)

Coffee (150 million)

Uganda Coffee (283 million)

Fish and fish products (127 million)

Cellular telephones (79 million)

Rwanda Tin Ores (66 million)

Coffee (57 million)

Tea (34 million)

Burundi Coffee (275 million)

Gold (164 million)

Tea (23 million)

Source: The State of East Africa 2012, Society for International Development (SID)

The combined total of each of the five (Kenya, Tanzania, Uganda, Rwanda and Burundi) East African country’s top three imports was valued at US$6.5 billion (59% of total imports) in 2010. The major import categories were petroleum and related products (US$1.8 billion), vehicles and transport equipment (US$1.4 billion) and machinery (US$1.07 billion).

13 AACGR= Annual Average Compound Growth Rate 14 The State of East Africa 2012, Society for International Development (SID) 15 Numbers may not add up due to informal trade.

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 24

Table 2 – East Africa’s Top Three Imports (in US$, 2010)

Country Top 1st Import Top 2nd Import Top 3rd Import

Tanzania Transport Equipment (856 million)

Machinery (841 million)

Food and beverages (727 million)

Kenya Crude Petroleum (915 million)

Gas and Diesel Oil (value unavailable)

Vegetable oil and fats (1.2 million)

Uganda Petroleum (916 million)

Road vehicles (418 million)

Specialised Machinery for particular industries (232 million)

Rwanda Motor Vehicles (79 million)

Petroleum oils (47 million)

Portland Cement (42 million)

Burundi Medicaments (75 million)

Portland Cement (72 million)

Motor Vehicles (41 million)

Source: The State of East Africa 2012, Society for International Development (SID)

3.3 Intra-Regional Trade

Intra-regional trade in East Africa has doubled from US$2.2 billion to US$4.1 billion between 2005 to 201016. However its share to East Africa’s total trade activity fell from 13% to 11%. From a peak of 22% in 1995, the share of total exports that are traded within the region fell to 19% in 2008 before rebounding to 21% in 2010. Intra-regional imports as a share of total imports fell from 11% to 7% over the same period. The Society for International’s (SID) 2012 report on the state of East Africa assumes that a potential catalyst of informal cross-border trade could be government action to ban the export of agricultural produce in a bid to ensure domestic food security. Table 3 shows, Kenya exported US$418.9 million worth of goods to Tanzania in 2012 but Tanzania only recorded US$275.6 million worth of goods from Kenya, resulting in a US$143.2 million difference/informal trade

Table 3 – Informal Trade in East Africa (in US$, 2010)

Country Kenya’s export to… Imports from Kenya “Informal trade

Uganda 657.1 million 549 million 108.1 million

Tanzania 418.8 million 275.6 million 143.2 million

Rwanda 132.9 million 169.4 million ($36.5 million)

Burundi 68.8 million 31 million 37.8 million

Total 1,277.6 million 1,025 million 252.6 million

Source: The State of East Africa 2012, Society for International Development (SID)

16 The State of East Africa 2012, Society for International Development (SID)

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 25

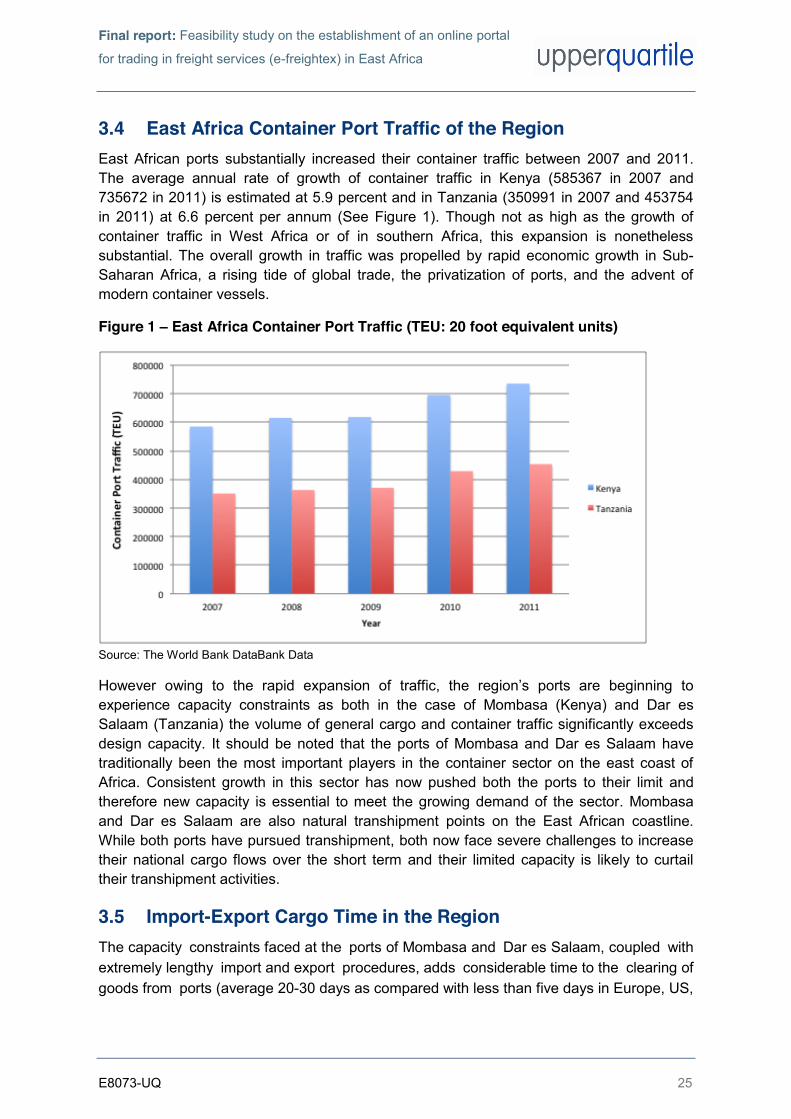

3.4 East Africa Container Port Traffic of the Region East African ports substantially increased their container traffic between 2007 and 2011. The average annual rate of growth of container traffic in Kenya (585367 in 2007 and 735672 in 2011) is estimated at 5.9 percent and in Tanzania (350991 in 2007 and 453754 in 2011) at 6.6 percent per annum (See Figure 1). Though not as high as the growth of container traffic in West Africa or of in southern Africa, this expansion is nonetheless substantial. The overall growth in traffic was propelled by rapid economic growth in Sub-Saharan Africa, a rising tide of global trade, the privatization of ports, and the advent of modern container vessels.

Figure 1 – East Africa Container Port Traffic (TEU: 20 foot equivalent units)

Source: The World Bank DataBank Data

However owing to the rapid expansion of traffic, the region’s ports are beginning to experience capacity constraints as both in the case of Mombasa (Kenya) and Dar es Salaam (Tanzania) the volume of general cargo and container traffic significantly exceeds design capacity. It should be noted that the ports of Mombasa and Dar es Salaam have traditionally been the most important players in the container sector on the east coast of Africa. Consistent growth in this sector has now pushed both the ports to their limit and therefore new capacity is essential to meet the growing demand of the sector. Mombasa and Dar es Salaam are also natural transhipment points on the East African coastline. While both ports have pursued transhipment, both now face severe challenges to increase their national cargo flows over the short term and their limited capacity is likely to curtail their transhipment activities.

3.5 Import-Export Cargo Time in the Region The capacity constraints faced at the ports of Mombasa and Dar es Salaam, coupled with extremely lengthy import and export procedures, adds considerable time to the clearing of goods from ports (average 20-30 days as compared with less than five days in Europe, US,

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 26

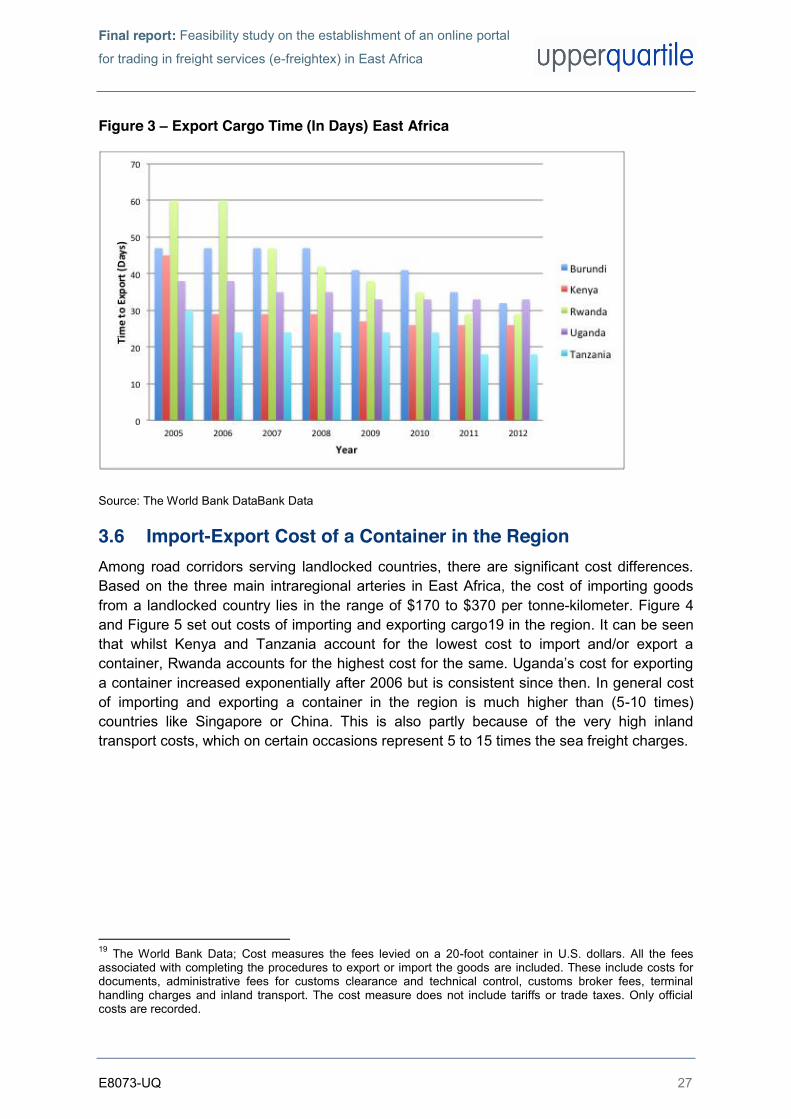

Hong Kong etc.)17. The long detention of goods in port has become a major obstacle to distribution. Detailed studies on importing goods along the northern corridor indicate that waiting times at ports account for a significant portion of the total time associated with transporting goods along the corridor. Figure 2 and Figure 3 set out time for importing and exporting cargo18 in the region.

Figure 2 – Import Cargo Time (In Days) East Africa

Source: The World Bank DataBank Data

17 East Africa’s Infrastructure A Continental Perspective, The World Bank, September 2011 18 The World Bank Data; Time is recorded in calendar days. The time calculation for a procedure starts from the moment it is initiated and runs until it is completed. If a procedure can be accelerated for an additional cost, the fastest legal procedure is chosen. It is assumed that neither the exporter nor the importer wastes time and that each commits to completing each remaining procedure without delay. Procedures that can be completed in parallel are measured as simultaneous. The waiting time between procedures--for example, during unloading of the cargo is included in the measure.

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 27

Figure 3 – Export Cargo Time (In Days) East Africa

Source: The World Bank DataBank Data

3.6 Import-Export Cost of a Container in the Region Among road corridors serving landlocked countries, there are significant cost differences. Based on the three main intraregional arteries in East Africa, the cost of importing goods from a landlocked country lies in the range of $170 to $370 per tonne-kilometer. Figure 4 and Figure 5 set out costs of importing and exporting cargo19 in the region. It can be seen that whilst Kenya and Tanzania account for the lowest cost to import and/or export a container, Rwanda accounts for the highest cost for the same. Uganda’s cost for exporting a container increased exponentially after 2006 but is consistent since then. In general cost of importing and exporting a container in the region is much higher than (5-10 times) countries like Singapore or China. This is also partly because of the very high inland transport costs, which on certain occasions represent 5 to 15 times the sea freight charges.

19 The World Bank Data; Cost measures the fees levied on a 20-foot container in U.S. dollars. All the fees associated with completing the procedures to export or import the goods are included. These include costs for documents, administrative fees for customs clearance and technical control, customs broker fees, terminal handling charges and inland transport. The cost measure does not include tariffs or trade taxes. Only official costs are recorded.

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 28

Figure 4 – Import Cost (US$ per container) of Cargo in East Africa

Source: The World Bank DataBank Data

Figure 5 – Export Cost (US$ per container) of Cargo in East Africa

Source: The World Bank DataBank Data

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 29

3.7 Freight Distribution A recently completed report on the East African trade and transport facilitation project sets out that the roads mode dominates the freight distribution in the East African region by carrying 80% of the regional ton-km. Pipelines carry 10%, which is followed by rail (8%) and air transport (2%).

On the rail side, the Tanzania Ports Authority’s 2009-10 Annual Report sets out that the poor performance of the two railway lines TRL (Tanzania Railway Limited) and TAZARA (Tanzania Zambia Railway Authority) had an adverse impact on the port’s overall performance. It sets out further that the percentage of container traffic handled by the rail as compared with road fell from 10% in 2008 to a 0.05% in 2009 even though it is expensive to send a container (long destined cargo) by road when compared with rail. Similar views were also echoed by Kenya Ports Authority, which sets out that there is poor off take by rail at Mombasa port and that the rail handles only 6% of the total containers handled at its container terminal.

For the pipelines freight, the major concern for the region and especially the land-locked countries has been security of supply of petroleum products, fuel prices and capacity of product transportation/distribution infrastructure. East and Central African countries are net importers of petroleum products i.e. refined petroleum products and crude oil processed at the Kenya Petroleum Refinery Ltd. The transportation/distribution of petroleum products in the region is by a network of the pipeline, railway, roads and (previously) lake transport systems. Out of these, the existing pipeline system in the region transports over 90% of the petroleum products consumed in Kenya and about 80% of the petroleum products consumed by the neighbouring countries of Uganda, Rwanda, Burundi, Northern Tanzania, Eastern DRC and Southern Sudan. The current pipeline system has experienced capacity constraints, which has led to oil marketers uplifting their products at Mombasa/Nairobi using the more costly road and rail options.

The bulk of the region’s air cargo traffic is handled by Kenya followed by smaller volumes by Tanzania and Uganda. Europe is the primary destination for the air cargo. Primary exports are counter-seasonal flowers and perishables, with relatively little return cargo. Kenya is a large exporter of flowers to the Netherlands; Nairobi is one of the three main airports in the region that handles air cargo traffic. In addition to exporting cut flowers, it handles strong domestic demand for imports shipped via air. Demand for Kenyan flowers is increasing, which has encouraged new entrants to the market, including Rwanda and Uganda. Seafood comprises the bulk of Tanzania’s exports to the European Union. Around two-thirds of the West Nile perch catch are shipped fresh by air. The fish are caught by fisherman as well as commercial fishing operations and then transferred via air to Mwanza or Nairobi.

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 30

4. WORKSHOPS AND STAKEHOLDERS’ CONSULTATIONS OUTCOMES

4.1 Inception Workshop

4.1.1 General The project’s inception workshop was held in Kenya (Mombasa) on 22 April 2013. The key purpose of the workshop was to raise awareness of the objectives and requirements of the project and to secure the buy-in of strategic stakeholders to support the study research and delivery. The following issues were discussed:

Background and Context – The study team introduced the study to the potential audience by providing them information on the background of the project. This discussion was aimed to ensure a mutual understanding between the consultant team and strategic stakeholders so that our work meets their needs.

Methodological Approach – The study team also discussed its proposed approach to delivering the project successful; and sought support from strategic stakeholders to identify and access relevant data and documentation.

In general the workshop was well received by the audience.

4.1.2 Key Outcomes of the Inception Workshop The key outcomes of the workshops were:

To establish a Focus Group for the study;

To identify key stakeholders for project’s stakeholders’ consultation process;; and

Finalisation of the programme for stakeholders’ consultation.

The Focus Group (See Annex 1) was selected to give as broad a range as possible of people who are in some way concerned with the associated issues of the project. Due to the tight time schedule of this project, it was conveyed that it might not be possible for the Focus Group to meet more than once during the course of the project. However the project team would keep them informed about the progress of the project via emails and telephone calls. Table 4 sets out the programme for stakeholders’ consultation process.

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 31

Table 4 – Programme for Stakeholders’ Consultation Workshop/s

Country/Town Date of Workshop

Venue/Schedule

Kenya (Pilot Workshop in Nairobi)

30 April 2013 9:00 am to 1:00 pm at Southern Sun Hotel in Nairobi

Kenya (Workshop in Mombasa)

2 May 2013 8:30 am to 1:00 pm at Whitesands Sarova Hotel in Mombasa

Rwanda (Workshop in Kigali)

2 May 2013 8:30 am to 1:00 pm at Hotel Mille Collines Hotel in Kigali

Tanzania (Workshop in Dar es Salam)

3 May 2013 9:00 am to 1:00 pm at Southern Sun Hotel in Dar es Salaam

Burundi (Workshop in Bujumbura)

3 May 2013 9:00 am to 1:00 pm at Roca Golf Hotel in Bujumbura

Uganda (Workshop in Kampala)

6 May 2013 9:00 am to 1:00 pm at Sheraton Hotel in Kampala

South Sudan 8 May 2013 Phone Interview/s

4.2 Stakeholders’ Consultation Workshops

4.2.1 Selection of E-Freightex Type In line with Section 2, the participants were presented with 4 types based on the complexity of a freight exchange:

Type 1 – Quotation engine, simplest form of freight exchange, allows buyers to find sellers (generally regarded by participants as too simplistic);

Type 2 – Matching engine to allow buyers and sellers to find each other; Type 3 – As Type 2, with additional aggregate reporting services; and Type 4 – As Type 3, with additional value-added features (generally regarded by

participants as a good “end goal” but likely more complex than necessary to derive the key benefits of the freight exchange concept)

During the stakeholders’ consultation stage, 83.5% of the total stakeholders of the region (circa 50 in total) preferred Type 3 to be taken forward to the next stage of the study; followed by 12.5% showing preference for Type 4; and the remaining 5% voting for Type 1 e-freightex system. The decision can be attributed to the following reasons:

It provides all the services of matching while “keeping it simple” during the period of introduction as the market gets used to the opportunities provided by the freight exchange;

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 32

It provides the aggregate market reporting that will improve the visibility of market information to all users – hence preferred to Type 2, which did not include these reports; and

It allows for the users to determine and prioritise future enhancements.

4.2.2 Expected Impacts of E-Freightex Portal When stakeholders were asked that what percentage of transport costs20 reduction do they envisage the e-freightex portal can generate; 73.9% of those who voted thought it could reduce the transport costs by 5%; 21.7% thought that the development of e-freightex portal could reduce the transport costs by 10%; and the remaining 4.4% thought the costs savings will be higher than 10%. The stakeholders also voiced their opinion on some other beneficial impacts that may include:

Increased competition;

Reducing the cost of shipping;

Reducing administration cost;

Small carrier can have access to more business and large contracts;

Larger shippers can get better rates and hence deliver cheaper goods and services to their end user customers and become more competitive on a global scale;

Optimizing capacity, by reducing voids on return journey;

More routes being serviced more frequently, shipping goods faster, reducing the loss of perishable goods; and

Increased timely deliveries.

4.2.3 Operation and Management of E-Freightex Portal The stakeholders were presented with the following four potential ownership and management options and were asked to vote for their preferred option:

Option 1: Stakeholder-owned private company - A private company owned by representatives from the region and company ownership will comprise of key stakeholders from the region including the revenue authorities, the importers, the EAC and forwarding agents (for profit);

Option 2: Outsourced to a private operator, with an oversight committee - A private operator run the e-freightex for profit but under oversight committee or board comprised of stakeholders (for profit);

Option 3: EAC Secretariat - EAC through an appointed committee would operate after being set up by a private company (Not for profit but self sustainable); and

Option 4: Inter-governmental organisation - Similar to the EAC owned and operated model but would involve government ownership where representatives

20 Transport costs were defined as a sum total of Fixed Costs (which includes, independently of vehicle usage, financing charges, depreciation of investment, wages, facilities, insurance, security, administrative overheads, taxes, profit margins etc.), Variable Costs (Fuel, subsistence, road user charges, occasional maintenance, tires, taxes etc.) and overheads (informal payments etc.).

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 33

seconded by each of the EAC member states manage the company (Not for profit but self sustainable).

83% of the stakeholders who voted preferred Option 2 i.e. the portal should be owned and managed by a private company. This was followed by 14% of stakeholders who went for Option 1 and a meagre 3% preferred Option 4.

Additional feedback included:

There should be a global tender and the project should be awarded to the best company;

Some stakeholders (including those from outside Kenya) felt that the portal could be based in Nairobi as it has higher technological experience as compared with other countries;

Stake holders also agreed that the actual data center for the portal can be based anywhere on the globe but there should be a balance between data security and the hosting cost of the data centre;

If the Option 2 goes ahead then the private operator should also be made accountable to an oversight committee made up of stakeholders form across all countries of the EAC. However, oversight committee should have a very straightforward role and does not need offices in each country.

Most of the stakeholders also conveyed a message that they are willing to pay a membership fee for the potential portal. However the same should offer them at the very least a good value for money and quality of service.

4.3 Stakeholder Validation Workshop The project’s stakeholder validation workshop was held in Rwanda (Kigali) on 26 June 2013. The key objectives of the workshop were as follows:

Update stakeholders on the project’s progress up to the submission of the draft final report of the project;

Solicit feedback from the stakeholders including their comments on the draft report; Agreeing upon potential changes; and Validating the project.

The key outcome of the workshop was that the stakeholders, who turned up quite in numbers, showed a lot of interest and enthusiasm for the project. Most of the stakeholders were keen to get on with the project and were seen asking questions on the next stage of the project. Key comments and observations were also noted from the stakeholders and the same were addressed during the writing up of this report.

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 34

5. OPTIONEERING

5.1 Introduction

This section sets out a preliminary appraisal of the proposed four types of e-freightexs (See Section 2). The assessment was designed to aid in the decision-making processes among the proposed types at this stage. Subsequently, a more complete Value for Money (VfM) analysis will be carried out for the preferred type of e-freightex.

5.2 Methodology

5.2.1 Overview A preliminary appraisal of each e-freightex type was designed to show the broad impacts of a range of criteria on them. The information derived from the exercise helped UQ and TMEA to identify the preferred type of e-freightex.

For the proposed e-freightexs types, the study team developed a matrix showing the ‘score’ of each type against a variety of criteria that could be useful in eliminating non-preferred types of e-freightex and selecting the preferred type of e-freightex. The following factors were considered when using this approach:

Since the scores are to be aggregated, we tried to arrange the ‘levels’ (e.g. Large Beneficial, Moderate Beneficial, Slight Beneficial, Neutral, Slight Adverse, Moderate Adverse, Large Adverse etc.) of each criterion in such a way that a given score for one criterion indicates the same order of importance as the same score for another;

The study team tried to avoid overlaps, i.e. where one criterion duplicates part of another; and most importantly

Since these assessments are inevitably subjective, it was born in mind that the robustness of the assessment system could only be improved if several people (with the relevant specialist knowledge) contributed to the process.

It should also be noted here that even after considering every possible factor for optioneering exercise, such a matrix, whilst being useful for sifting through types and for providing background information to go with the business case, could still not be used as a substitute for the business case of the preferred type. The same was subsequently addressed and a Value for Money section is presented in the latter part of this report.

5.2.2 Qualitative Assessment The qualitative assessment was designed to indicate the relative merits of the options considered. The methodology included the following steps:

Establishing the options/types of e-freightexs to be assessed;

Establishing the criteria to be assessed;

Designing the valuation system to be applied;

Assigning values to each criteria; and

Summarising and discussing outcomes.

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 35

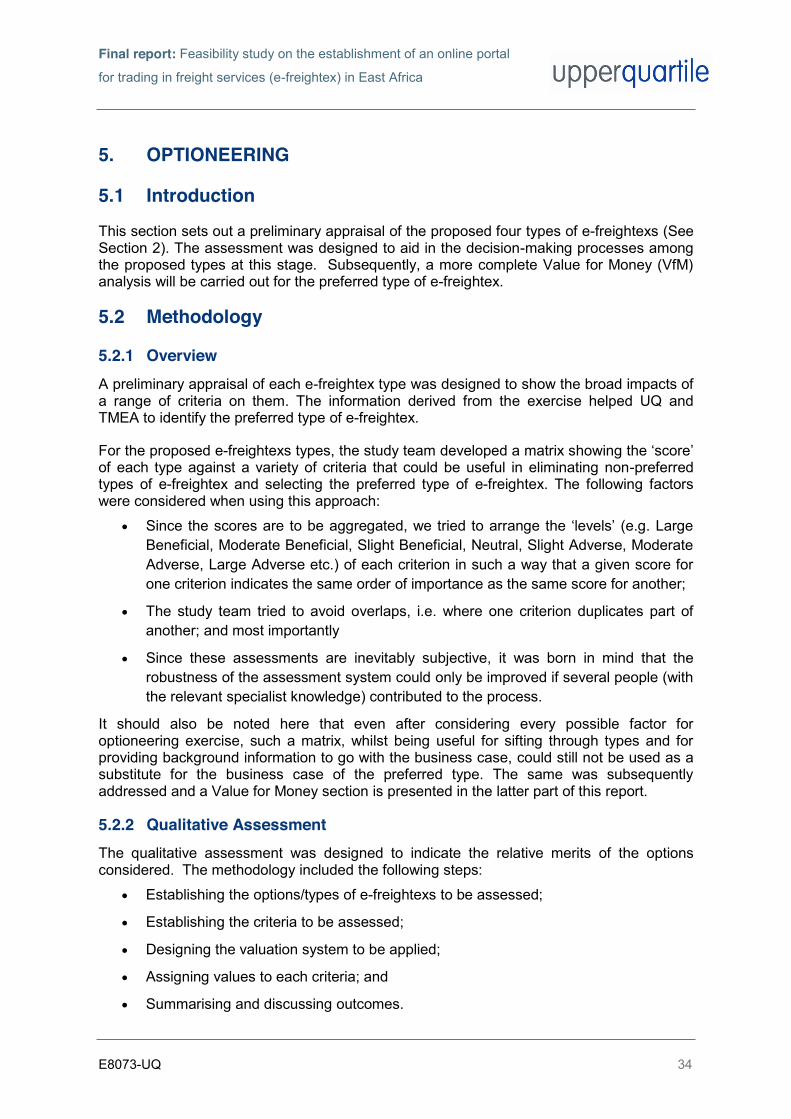

A qualitative assessment against fifteen (15) criteria was thus undertaken to illustrate the differences among the potential project options. As described above, this was only an initial assessment, based on little hard evidence, as the impacts had not been valued then. The four types of e-freightexs were assessed against the following criteria:

Environment;

Road Accidents;

Wider Economic Impacts (Jobs);

Capital Cost;

Sustainable;

Scalable;

Competitiveness;

Efficiency to Businesses;

Efficiency to Customers;

Market Information Availability;

Operating and Maintenance Cost;

Transport Costs;

Complexity;

Lead Time to Development; and

Commercial Disclosure.

Each type was valued for its impact on each criterion, on a system from -3 to +3. Scores could be interpreted as follows:

-3: Large Adverse;

-2: Moderate Adverse;

-1: Slight Adverse;

0: Neutral;

1: Slight Beneficial;

2: Moderate Beneficial;

3: Large Beneficial;

A matrix of option valuations as well as a summary of the relative ranking of the types to indicate any types that rank well according to many perspectives, and any that perform poorly is shown in Table 5 below.

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 36

Table 5: Optioneering of E-Freightexs

Criteria/ Types of E-Freightex Type 1 Type 2 Type 3 Type 4 Remarks

Environment 0 1 1 1 Reduced air pollution, noise pollution, CO2 emissions; due to optimised services etc.

Accidents 0 1 1 1 Reduced number of trucks due to optimised services will have marginal beneficial impact

Wider Economic Impacts (Jobs)

0 1 2 2 Creating jobs in the region (support staff for portal and multiplier effect)

Capital Cost -1 -2 -2 -3 Set up/development cost of the portal

Sustainable 0 1 3 2 Does the option have longevity (higher cost low sustainability

Scalable 0 3 3 3 Can the system grow with demand and growth within the sector

Competitiveness 1 2 3 3 Increases opportunities for business growth including intra-region trade opportunities

Efficiency to Businesses 0 1 2 3 Which type will enable businesses to become most efficient with their business process

Efficiency to Customers 0 1 2 3 Which option provides the most efficiency to customers in areas like: Quicker response with quotation; Timely deliveries to consignee (i.e. more efficient routes, vehicles being filled quicker, faster dispatch); Shippers can increase frequency of shipping using a more regulated schedule via the portal; Improved collection and dispatch timings etc.

Market Information Availability 1 2 3 3 -

Operating and Maintenance Cost

-1 -2 -2 -3 Operating and Maintenance Cost of running the portal

Final report: Feasibility study on the establishment of an online portal

for trading in freight services (e-freightex) in East Africa

E8073-UQ 37

Criteria/ Types of E-Freightex Type 1 Type 2 Type 3 Type 4 Remarks