EXPLORING CHARITABLE GIFT ANNUITIES - …raymondjamescharitable.org/pdfs/Exploring Charitable Gift...

12

Enjoy an immediate partial tax deduction and a lifetime of annuity income. EXPLORING CHARITABLE GIFT ANNUITIES

Transcript of EXPLORING CHARITABLE GIFT ANNUITIES - …raymondjamescharitable.org/pdfs/Exploring Charitable Gift...

Enjoy an immediate partial tax deduction and a lifetime of annuity income.

EXPLORING CHARITABLE GIFT ANNUITIES

The Raymond James Charitable Endowment Fund does not issue

gift annuities in AL, AR, CA, HI, MD, ND, NJ, NY, WA and WI.

1

EXPLORING CHARITABLE GIFT ANNUITIES

PROVIDING FOR NOW AND IN THE FUTURE

You care deeply about charitable giving and creating a legacy for future generations.

Yet you rely on investment income to supplement your lifestyle or provide for those

you care about. The Raymond James Charitable Endowment Fund’s Charitable Gift

Annuity is one of the easiest ways to establish a plan for giving that will also provide

a lifetime of reliable annuity payments.

According to the American Council on Gift Annuities, gift annuity donors are

typically retirees seeking to increase their income through the security of guaranteed

payments while minimizing taxes. To help determine if a charitable gift annuity may

be right for you, consider the following questions.

Have the interest rates on your CDs and other fixed-income investments

declined, and would you like to increase your cash flow?

6Do you own appreciated stock or mutual fund shares that you’ve considered

selling to reinvest the proceeds into a vehicle that will generate more income –

but do not want to incur capital gains taxes?

6Are you interested in receiving fixed income that is unaffected

by interest rates and/or stock prices?

6Would you like to receive reliable income for the rest of your life?

6Would you like income payouts that will continue to go to a surviving

spouse without the expense and delay of probate?

If these are the kinds of questions you’ve been considering, read on to learn

more about how a charitable gift annuity works and how it can benefit you.

2

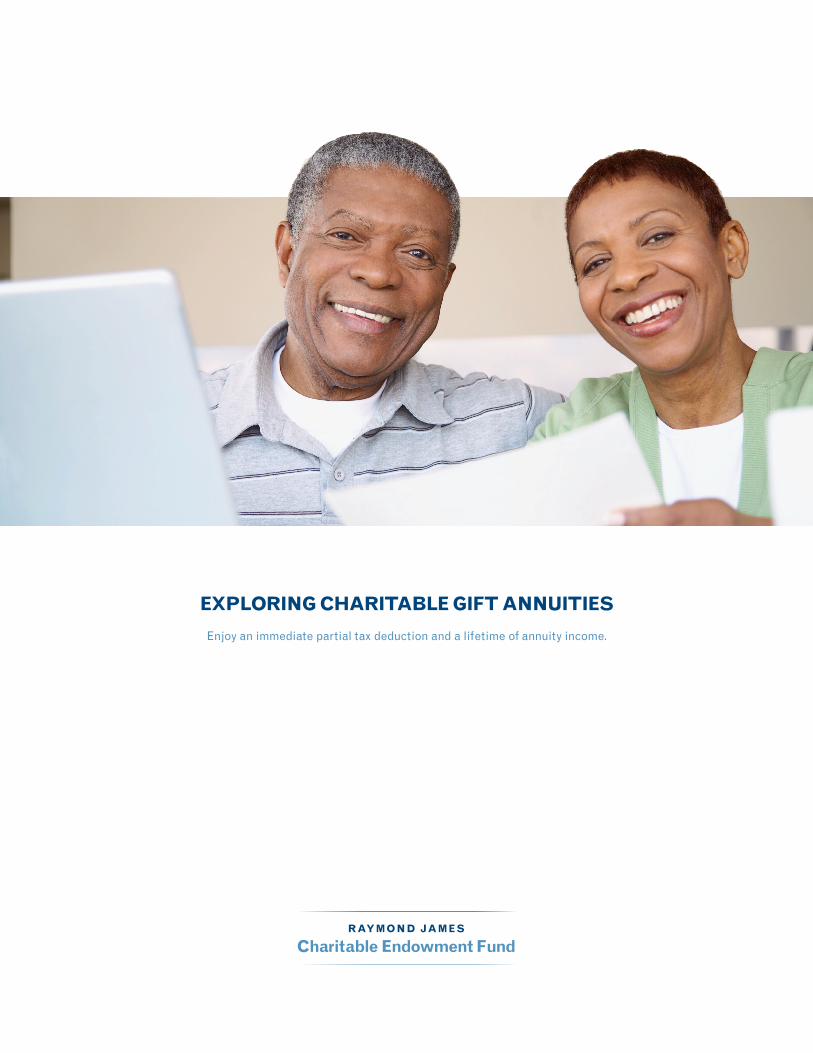

EXPLAINING A CHARITABLE GIFT ANNUITY

A charitable gift annuity is a simple contract between a donor and the

Raymond James Charitable Endowment Fund (RJCEF). A donation to the

RJCEF positions your gift for two purposes:

1. It will pay one or two “annuitants” a fixed sum either monthly, quarterly, semi-annually or annually for life.

2. Upon the death of the last annuitant, the remaining account balance will be distributed to the approved charity of your choice or transferred to the RJCEF Donor Advised Fund to be advised by the person of your choice, or pay to one or more charities of your selection over time.

DONOR BENEFITS

6An immediate partial

tax deduction

6Income stream for up to two beneficiaries until they pass

away (you may include yourself)

6 Spread out capital gains

taxes over annuitants’ life expectancy (ideal for highly

appreciated assets)

6Partial taxes on annuity

income received (depending on contribution source)

6 Gift creates a lasting legacy

for your wealth

DONOR

RAYMOND JAMES CHARITABLE GIFT ANNUITY

RAYMOND JAMES DONOR ADVISED

FUNDANNUITANTSCHARITY

Payments

Contribution of Cash or Securities

Income Tax Charitable Deduction

Remainder

EXPLORING CHARITABLE GIFT ANNUITIES

3

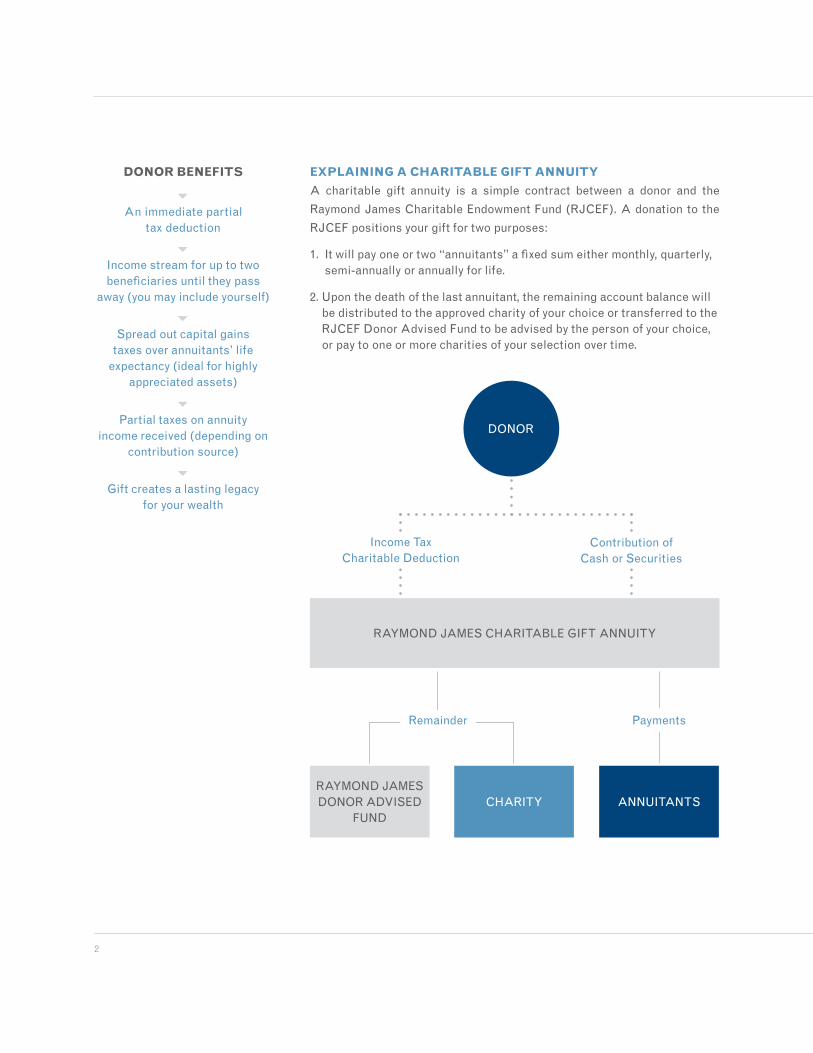

CHOOSING THE STRATEGY THAT MEETS YOUR OBJECTIVES

Charitable gift annuities are often compared to donor advised funds and pooled income funds. Although

somewhat similar, there are key differences, as detailed in the accompanying comparison table.

RJCEF ComparisonDonor Advised

FundPooled Income

FundsCharitable Gift

Annuity

Income to donor No Yes Yes

Income payout determined by N/A Investment yield ACGA rates – increases with age

Cash income N/A Varies with yield Fixed

Reduction in taxable estate Yes Yes Yes

Capital gains tax savings Yes Yes Gain recognized over annuitant’s life

Income tax deduction Yes / full Yes / partial Yes / partial

Grants to charity Yes / immediately

After death of last beneficiary

After death of last annuitant

Initial gift (minimum) $10,000 $20,000 $50,000

Subsequent gifts $500 $5,000 Not allowed

FLEXIBILITY

The direction of a charitable organization can change with leadership, financial or legal troubles,

or just through the passing of time. With a traditional gift annuity, your irrevocable gift cannot be

withdrawn and placed with another charity should you have a change of heart or the charity changes

its mission. However, with the Raymond James Charitable Endowment Fund’s Charitable Gift

Annuity, you have the flexibility to change the ultimate charitable beneficiary at any time you wish.

4

GETTING STARTED

You must be at least 55 years old and able to contribute a minimum, irrevocable gift

of $50,000 to establish a gift annuity. You are never too old to create an account. In

fact, the older you are, the higher your annuity payouts will be. There is no maximum

contribution amount, however, you cannot add to a gift annuity after it has been

opened. If you wish to make additional contributions, you can establish separate

charitable gift annuities.

To get started, review the Raymond James Charitable Endowment Fund’s Charitable

Gift Annuity Disclosure Brochure. Then, simply fill out and submit a charitable gift

annuity application, along with your contribution check or appropriate security

transfer form. Mail these documents to:

Raymond James Charitable Endowment Fund

P.O. Box 14407

St. Petersburg, FL 33733-4407

EXPLORING CHARITABLE GIFT ANNUITIES

5

6

INVESTING

A portion of each charitable gift annuity will be invested in a commercial annuity

contract with a large insurance company. The balance of each account will be

invested in one of three objectives based on your recommendations:

BALANCED – seeks to balance the generation of income, preservation of

capital and growth of capital

GROWTH WITH INCOME – seeks to emphasize the growth of capital over the

generation of income

GROWTH – seeks long-term capital appreciation; income may or may not be

sought and will always be secondary

There can be no guarantee that any objective will be met.

You may request to change the investment objective up to four times per

calendar year. Requests will be considered by the Raymond James Charitable

Endowment Fund Board during their regularly scheduled quarterly meetings.

The Raymond James Charitable Gift Annuity is not considered an

“investment,” but a charitable contribution. In addition, the annuity rates

offered by a charitable gift annuity will not be as high as those offered

by commercial annuity contracts. However, if you take into account the

cash flow the gift annuity will provide, the partial tax deduction, the tax

sheltering effect of annuity income streams and the potential to spread out

capital gains taxes, gift annuities can provide an attractive benefit.

You should consider the investment objectives, risks, and charges and expenses of mutual funds

carefully. The prospectus contains this and other information about mutual funds. The prospectus is

available from your financial advisor and should be read carefully.

6

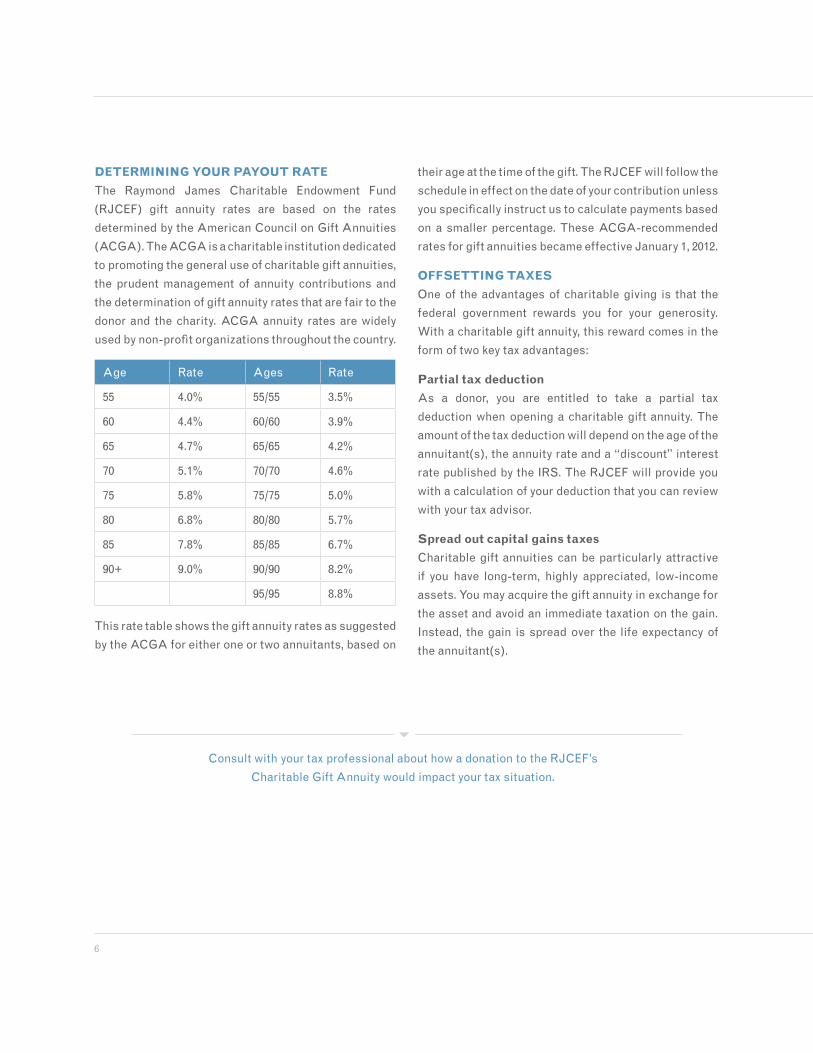

DETERMINING YOUR PAYOUT RATE

The Raymond James Charitable Endowment Fund

(RJCEF) gift annuity rates are based on the rates

determined by the American Council on Gift Annuities

(ACGA). The ACGA is a charitable institution dedicated

to promoting the general use of charitable gift annuities,

the prudent management of annuity contributions and

the determination of gift annuity rates that are fair to the

donor and the charity. ACGA annuity rates are widely

used by non-profit organizations throughout the country.

Age Rate Ages Rate

55 4.0% 55/55 3.5%

60 4.4% 60/60 3.9%

65 4.7% 65/65 4.2%

70 5.1% 70/70 4.6%

75 5.8% 75/75 5.0%

80 6.8% 80/80 5.7%

85 7.8% 85/85 6.7%

90+ 9.0% 90/90 8.2%

95/95 8.8%

This rate table shows the gift annuity rates as suggested

by the ACGA for either one or two annuitants, based on

their age at the time of the gift. The RJCEF will follow the

schedule in effect on the date of your contribution unless

you specifically instruct us to calculate payments based

on a smaller percentage. These ACGA-recommended

rates for gift annuities became effective January 1, 2012.

OFFSETTING TAXES

One of the advantages of charitable giving is that the

federal government rewards you for your generosity.

With a charitable gift annuity, this reward comes in the

form of two key tax advantages:

Partial tax deduction

As a donor, you are entitled to take a partial tax

deduction when opening a charitable gift annuity. The

amount of the tax deduction will depend on the age of the

annuitant(s), the annuity rate and a “discount” interest

rate published by the IRS. The RJCEF will provide you

with a calculation of your deduction that you can review

with your tax advisor.

Spread out capital gains taxes

Charitable gift annuities can be particularly attractive

if you have long-term, highly appreciated, low-income

assets. You may acquire the gift annuity in exchange for

the asset and avoid an immediate taxation on the gain.

Instead, the gain is spread over the life expectancy of

the annuitant(s).

Consult with your tax professional about how a donation to the RJCEF’s

Charitable Gift Annuity would impact your tax situation.

6

EXPLORING CHARITABLE GIFT ANNUITIES

7

SAMPLE CASE STUDY

Elaine Cole, a 75-year-old widow, needs to increase her

income. Years ago she and her husband purchased stock

worth $2,000. Its value has appreciated to $50,000, but

it only pays a 2% annual dividend. If she sold the stock,

Elaine would have to pay a significant amount of capital

gains tax. At her age, if she opens a charitable gift annuity

with the RJCEF, she will receive 5.8% annually on her

$50,000. As a result of making the gift, she is entitled to an

income tax charitable deduction of $20,640.50 (deduction

amount will vary over time). She will receive an annual

annuity payment of $2,900. Furthermore, approximately

84.4% of each annuity payment will be “tax advantaged”

for the next 12 years – a combination of tax-free payments

and long-term capital gain.

SIMPLIFYING THE WAY YOU GIVE

A charitable gift annuity provides a simple way to

exchange an irrevocable gift of $50,000 or more in cash

or marketable securities for a fixed sum of income paid

either monthly, quarterly, semi-annually or annually for life

– which may be split between two income beneficiaries.

Upon the death of the last annuitant, the remaining

account balance will either be distributed to the approved

charity you’ve selected or transferred to the RJCEF

Donor Advised Fund to be advised by the person of your

choice or distributed to one or more charities of your

choice over time. In short, a charitable gift annuity is one

of the simplest ways to create a lasting philanthropic

legacy while still receiving income from the same asset.

Raymond James provides all administration and reporting services, including the documentation you

need to calculate and support income tax deductions, in order to keep you apprised of account activity.{ }

8

6

THOMAS WALROND

Senior Vice President and

Chief Operating Officer,

Private Client Group,

Raymond James & Associates, Inc.

ERIK FRULAND

Chief Operating Officer,

Asset Management Services,

Raymond James Financial

NICOLE JOHNSON, DrPH, MA, MPH

Executive Director,

Bringing Science Home;

Founder, Students with Diabetes,

University of South Florida

FRANCES Z. NEU

Vice President, Institutional Advancement,

St. Petersburg College and Executive Director,

St. Petersburg College Foundation

THOMAS WILKINS, Chairman

Music Director, The Omaha Symphony Orchestra;

Principal Conductor, The Hollywood Bowl Orchestra;

and Youth and Family Concerts Conductor,

The Boston Symphony Orchestra

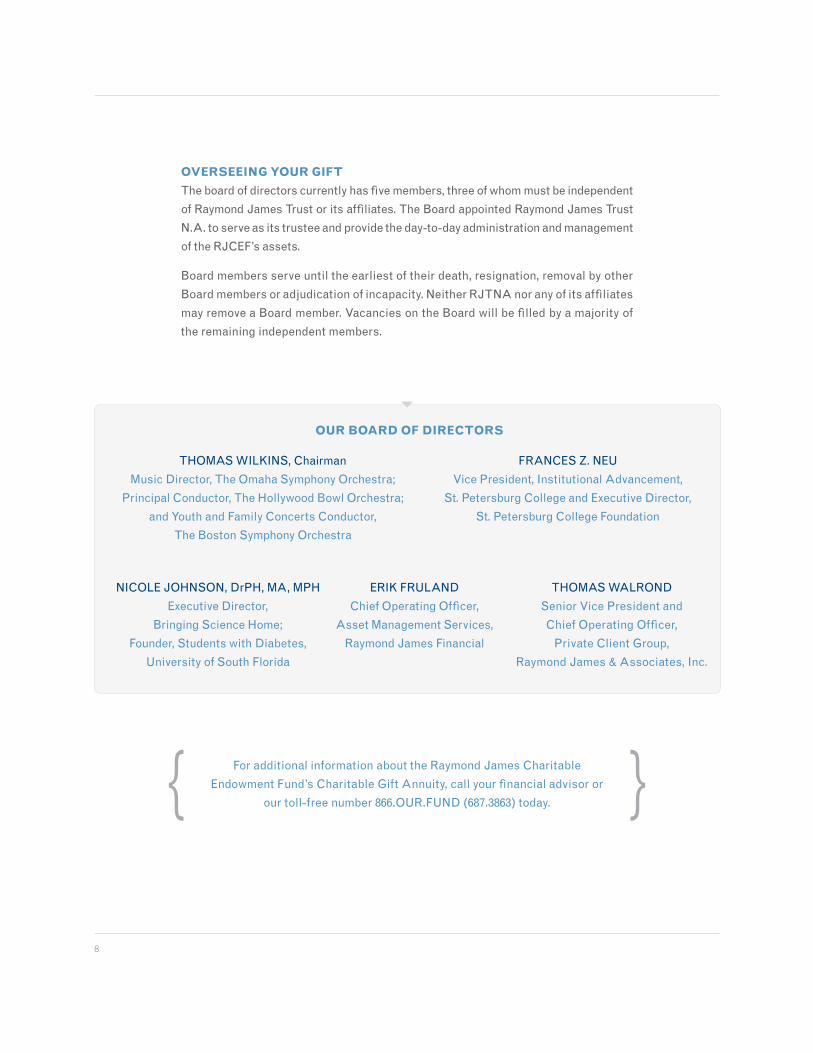

OUR BOARD OF DIRECTORS

OVERSEEING YOUR GIFT

The board of directors currently has five members, three of whom must be independent

of Raymond James Trust or its affiliates. The Board appointed Raymond James Trust

N.A. to serve as its trustee and provide the day-to-day administration and management

of the RJCEF’s assets.

Board members serve until the earliest of their death, resignation, removal by other

Board members or adjudication of incapacity. Neither RJTNA nor any of its affiliates

may remove a Board member. Vacancies on the Board will be filled by a majority of

the remaining independent members.

For additional information about the Raymond James Charitable

Endowment Fund’s Charitable Gift Annuity, call your financial advisor or

our toll-free number 866.OUR.FUND (687.3863) today.{ }

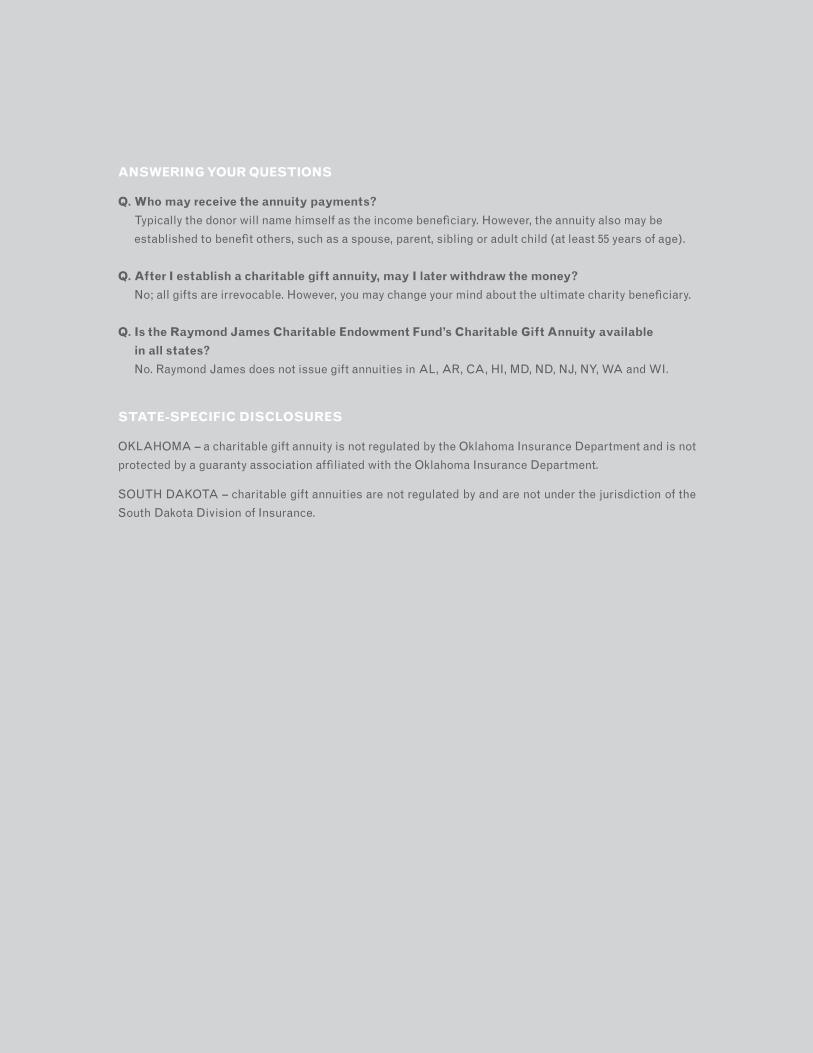

ANSWERING YOUR QUESTIONS

Q. Who may receive the annuity payments?

Typically the donor will name himself as the income beneficiary. However, the annuity also may be

established to benefit others, such as a spouse, parent, sibling or adult child (at least 55 years of age).

Q. After I establish a charitable gift annuity, may I later withdraw the money?

No; all gifts are irrevocable. However, you may change your mind about the ultimate charity beneficiary.

Q. Is the Raymond James Charitable Endowment Fund’s Charitable Gift Annuity available

in all states?

No. Raymond James does not issue gift annuities in AL, AR, CA, HI, MD, ND, NJ, NY, WA and WI.

STATE-SPECIFIC DISCLOSURES

OKLAHOMA – a charitable gift annuity is not regulated by the Oklahoma Insurance Department and is not

protected by a guaranty association affiliated with the Oklahoma Insurance Department.

SOUTH DAKOTA – charitable gift annuities are not regulated by and are not under the jurisdiction of the

South Dakota Division of Insurance.

TRUSTEE: RAYMOND JAMES TRUST

RAYMOND JAMES CHARITABLE ENDOWMENT FUND

P.O. BOX 14407 // ST. PETERSBURG, FL 33733-4407 // TOLL-FREE: 866.OUR.FUND (687.3863) // FAX: 727.567.8040

MYFAMILYFOUNDATION.ORG

Florida Registration #CH11828

A copy of the official registration and financial information may be obtained from the division of consumer services by calling

toll-free (800-435-7352) within the state. Registration does not imply endorsement, approval or recommendation by the state.

©2014 Raymond James Trust, N.A., is a subsidiary of Raymond James Financial, Inc. TRUST-0055CGA-0614_CGA BRO FKS/EG 6/14

GIVING. SIMPLIFIED.