Exchange - Cboe · Page 2 February 4, 2011 Volume 39, Number 05 Chicago Board Options Exchange...

20

TRADING PERMIT INFORMATION FOR 01/27/2011 THROUGH 02/02/2011 Exchange Bulletin February 4, 2011 Volume 39, Number 05 The Bylaws and Rules of Chicago Board Options Exchange, Incorporated (“Exchange”), in certain specific instances, require the Exchange to provide notice to Exchange Trading Permit Holders. To satisfy this requirement, a copy of the Exchange Bulletin, including the Regulatory Bulletin, is delivered by e-mail or by hard copy free of charge to all effective Trading Permit Holders on a weekly basis. Trading Permit Holders are encouraged to receive the Exchange and Regulatory Bulletin and Information Circulars via e-mail. E-mail subscriptions may be obtained by submitting your name, firm if applicable, e-mail address, and phone number, to [email protected]. If you do sign up for e-mail delivery, please remember to inform the Registration Services Department of e-mail address changes. Sub- scriptions for hard copy delivery may be obtained by submitting your name, firm if any, mailing address and telephone number to: Chicago Board Options Exchange, Registration Services Department, 400 South LaSalle, Chicago, Illinois 60605, Attention: Bulletin Subscriptions. For access to the CBOE Trading Permit Holder Web Site, please also notify the Registration Services Department by sending an e-mail to [email protected] or by phone at 312-786-7449. Copyright © 2011 Chicago Board Options Exchange, Incorporated TRADING PERMIT APPLICATIONS RECEIVED FOR WHICH BULLETIN PUBLICATION IS REQUIRED Individual Applicants Daniel James Cashin Belvedere Trading, LLC 1255 S. State St., Unit 805 Chicago, IL 60605 Robert C. Sheehan GLP, LLC 320 Downing Road Riverside, IL 60546 Yasin A. Khan Belvedere Trading, LLC 1401 S. State St.. #1414 Chicago, IL 60605 TERMINATIONS Individuals Nominees: Termination Date Evan J. Miskella (BKY) 1/31/11 Belvedere Trading, LLC Nathan P. Campbell (NPC) 1/31/11 Belvedere Trading, LLC James Schroeder (FUD) 2/1/11 Toro Capital Management LLC Jeffrey S. Kerins (KER) 2/1/11 Ronin Capital, LLC Michael J. Hickey (HIX) 2/1/11 McLaughlin Capital, LLC Termination Date Matthew C. Friemel (DUK) 2/1/11 McLaughlin Capital, LLC Steven Stefancic (SSF) 2/2/11 G-Bar Limited Partnership TPH Organizations ST Capital LLC 2/1/11 Atlantic Trading Equities LLC 2/1/11 McLaughlin Capital, LLC 2/1/11 EFFECTIVE TRADING PERMIT HOLDERS Individuals Nominees: Effective Date Aurelio Picciuca (PIC) 1/31/11 CMCJL, LLC Type of Business to be Conducted: Proprietary Trading Permit Holder Jeffery I. Fried (FRE) 2/1/11 Gar Wood Securities, LLC Type of Business to be Conducted: Floor Broker Rodney D. Jennings (RDN) 2/2/11 Equitec Structured Products, LLC Type of Business to be Conducted: Floor Broker Thomas P. Tiernan (TJT) 2/2/11 Tibra Trading America LLC Type of Business to be Conducted: Market Maker Eric Donovan (DON) 2/2/11 Donovan, Schayer, & Massey Trading, LLC Type of Business to be Conducted: Market Maker

Transcript of Exchange - Cboe · Page 2 February 4, 2011 Volume 39, Number 05 Chicago Board Options Exchange...

TRADING PERMIT INFORMATION FOR 01/27/2011 THROUGH 02/02/2011

ExchangeBulletinFebruary 4, 2011 Volume 39, Number 05

The Bylaws and Rules of Chicago Board Options Exchange, Incorporated (“Exchange”), in certain specific instances, require the Exchange to provide notice to Exchange Trading Permit Holders. To satisfy this requirement, a copy of the Exchange Bulletin, including the Regulatory Bulletin, is delivered by e-mail or by hard copy free of charge to all effective Trading Permit Holders on a weekly basis.

Trading Permit Holders are encouraged to receive the Exchange and Regulatory Bulletin and Information Circulars via e-mail. E-mail subscriptions may be obtained by submitting your name, firm if applicable, e-mail address, and phone number, to [email protected]. If you do sign up for e-mail delivery, please remember to inform the Registration Services Department of e-mail address changes. Sub-scriptions for hard copy delivery may be obtained by submitting your name, firm if any, mailing address and telephone number to: Chicago Board Options Exchange, Registration Services Department, 400 South LaSalle, Chicago, Illinois 60605, Attention: Bulletin Subscriptions.

For access to the CBOE Trading Permit Holder Web Site, please also notify the Registration Services Department by sending an e-mail to [email protected] or by phone at 312-786-7449.

Copyright © 2011 Chicago Board Options Exchange, Incorporated

TRADING PERMIT APPLICATIONS RECEIVED FOR WHICH BULLETIN PUBLICATION IS REQUIRED

Individual Applicants

Daniel James CashinBelvedere Trading, LLC1255 S. State St., Unit 805Chicago, IL 60605

Robert C. SheehanGLP, LLC320 Downing RoadRiverside, IL 60546

Yasin A. KhanBelvedere Trading, LLC1401 S. State St.. #1414Chicago, IL 60605 TERMINATIONSIndividuals

Nominees: Termination Date

Evan J. Miskella (BKY) 1/31/11Belvedere Trading, LLC

Nathan P. Campbell (NPC) 1/31/11Belvedere Trading, LLC

James Schroeder (FUD) 2/1/11Toro Capital Management LLC

Jeffrey S. Kerins (KER) 2/1/11Ronin Capital, LLC

Michael J. Hickey (HIX) 2/1/11McLaughlin Capital, LLC

Termination Date

Matthew C. Friemel (DUK) 2/1/11McLaughlin Capital, LLC

Steven Stefancic (SSF) 2/2/11G-Bar Limited Partnership

TPH Organizations

ST Capital LLC 2/1/11

Atlantic Trading Equities LLC 2/1/11

McLaughlin Capital, LLC 2/1/11 EFFECTIVE TRADING PERMIT HOLDERSIndividuals

Nominees: Effective Date

Aurelio Picciuca (PIC) 1/31/11CMCJL, LLC Type of Business to be Conducted: Proprietary Trading Permit Holder

Jeffery I. Fried (FRE) 2/1/11Gar Wood Securities, LLC Type of Business to be Conducted: Floor Broker

Rodney D. Jennings (RDN) 2/2/11Equitec Structured Products, LLC Type of Business to be Conducted: Floor Broker

Thomas P. Tiernan (TJT) 2/2/11Tibra Trading America LLC Type of Business to be Conducted: Market Maker

Eric Donovan (DON) 2/2/11Donovan, Schayer, & Massey Trading, LLC Type of Business to be Conducted: Market Maker

Page 2 February 4, 2011 Volume 39, Number 05 Chicago Board Options Exchange

Research Circular #RS11-066February 2, 2011Compellent Technologies, Inc. (“CML”) Proposed Mergerwith Dell Inc. (“DELL”)

Research Circular #RS11-067February 2, 2011J.Crew Group, Inc. (“JCG”) Proposed Mergerwith Chinos Holdings, Inc.

Research Circular #RS11-068February 2, 2011Matrixx Initiatives, Inc. (“MTXX”)Tender Offer AMENDED and FURTHER EXTENDEDby Affiliates of H.I.G. Capital, LLC

Research Circular #RS11-069February 2, 2011*****UPDATE*****UPDATE*****UPDATE*****Central Pacific Financial Corp. (“CPF”)1-for-20 Reverse Stock SplitEx-Distribution Date: February 3, 2011

Research Circular #RS11-070February 3, 2011Five Star Quality Care, Inc. (“FVE”)To Move and Begin Trading on NYSEEffective Date: February 4, 2011

Research Circular #RS11-072February 3, 2011Banco Bradesco S.A. (“BBD & adj. BBD1/BBD2”)Cash Distribution in Lieu of RightsEx-Date: February 4, 2011

Research Circular #C2-RS11-010February 3, 2011Banco Bradesco S.A. (“BBD”)Cash Distribution in Lieu of RightsEx-Date: February 4, 2011

Research Circular #RS11-073February 3, 2010Penn Virginia GP Holdings, L.P. (“PVG”) Proposed Mergerwith Penn Virginia Resource Partners, L.P. (“PVR”)

Research Circular #RS11-074February 4, 2011Sonic Solutions (“SNIC & adj. SNIC1”) Exchange Offer by Sparta Acquisition Sub, Inc.

Research Circular #RS11-075February 4, 2011Genoptix, Inc. (“GXDX”)Tender Offer by GO Merger Sub, Inc.

RESEARCH CIRCULARS The following Research Circulars were distributed between January 28 and February 4, 2011. If you wish to read the entire document, please refer to the CBOE website at www.cboe.com and click on the “Trading Tools” Tab. New listings and series information is also available in the Trading Tools section of the website. For questions regarding information discussed in a Research Circular, please call The Options Clearing Corporation at 1-888-OPTIONS.

TPH Organizations

Gar Wood Securities, LLC 2/1/11Type of Business to be Conducted: Floor Broker

Research Circular #RS11-056January 28, 2011Whiting Petroleum Corporation ("WLL") 2-for-1 Stock SplitEx-Distribution Date: February 23, 2011

Research Circular #RS11-057January 28, 2011Woodward Governor Company (“WGOV”)Name and Underlying/Option Symbol Change to:Woodward, Inc. (“WWD”)Effective Date: January 31, 2011

Research Circular #RS11-058January 31, 2011*****UPDATE*****UPDATE*****UPDATE*****Central Pacific Financial Corp. (“CPF”)1-for-20 Reverse Stock SplitAnticipated Ex-Distribution Date: TO BE ANNOUNCED

Research Circular #RS11-059January 31, 2011Evergreen Solar, Inc. (“ESLRD/ESLR/ESLR1”)Stock Symbol Change to (“ESLR”)Effective Date: February 1, 2011

Research Circular #RS11-060January 31, 2011Applied Signal Technology, Inc. (“APSG”):Merger Completed -- Cash Settlement

Research Circular #RS11-061February 1, 2011Potash Corporation of Saskatchewan Inc. (“POT”) 3-for-1 Stock SplitEx-Distribution Date: February 25, 2011

Research Circular #C2-RS11-009February 1, 2011Potash Corporation of Saskatchewan Inc. (“POT”) 3-for-1 Stock SplitEx-Distribution Date: February 25, 2011

Research Circular #RS11-065February 2, 2011Eaton Corporation (“ETN”) 2-for-1 Stock SplitEx-Distribution Date: March 1, 2011

CHANGES IN TRADING FUNCTIONIndividuals Effective Date

Kurt J. Steib 2/1/11From: Nominee For ST Capital LLC; Market Maker To: Nominee For WSP Commodity Trading LLC; Market Maker

James D. Welch 2/1/11From: Nominee For Atlantic Trading Equities LLC; Market Maker To: Nominee For Atlantic Trading Indices LLC; Market Maker

February 4, 2011 Volume RB22, Number 5

______________________________________________________________________________

The Bylaws and Rules of Chicago Board Options Exchange, Incorporated (“Exchange”), in certain specific instances, require the Exchange to provide notice to Trading Permit Holders. The weekly Regulatory Bulletin is delivered to all effective Trading Permit Holders to satisfy this requirement. Copyright © 2011 Chicago Board Options Exchange, Incorporated.

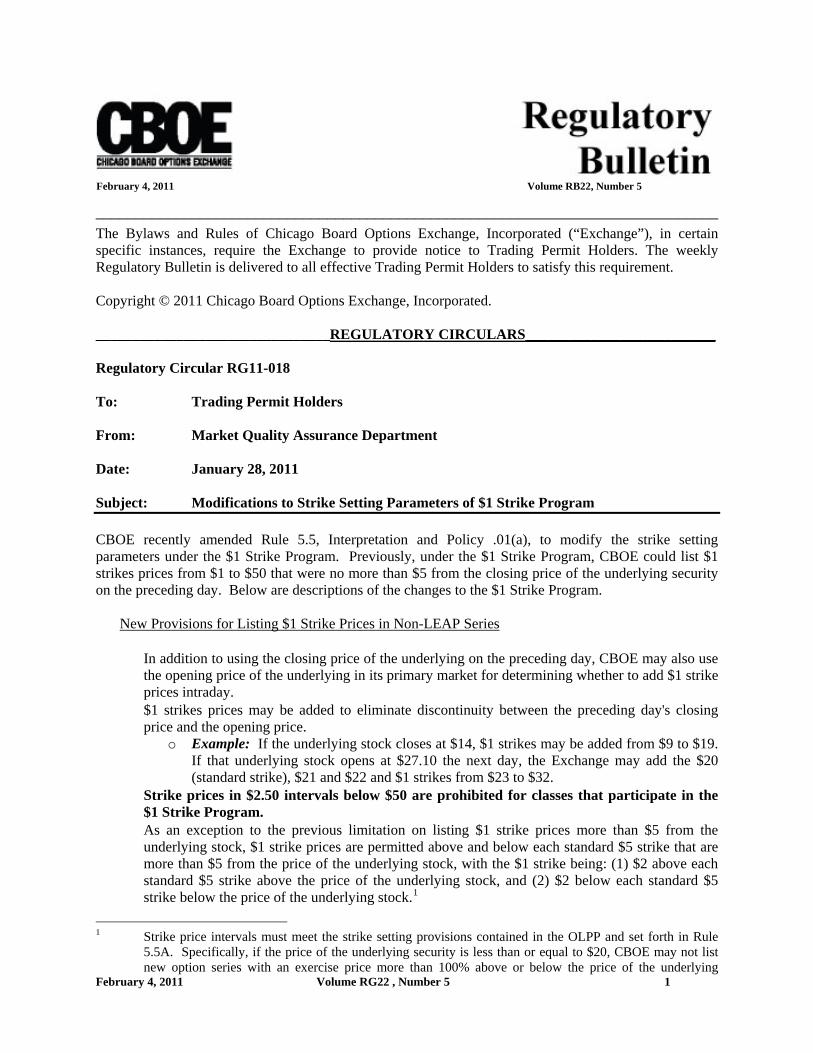

________________________________REGULATORY CIRCULARS__________________________ Regulatory Circular RG11-018 To: Trading Permit Holders From: Market Quality Assurance Department Date: January 28, 2011 Subject: Modifications to Strike Setting Parameters of $1 Strike Program CBOE recently amended Rule 5.5, Interpretation and Policy .01(a), to modify the strike setting parameters under the $1 Strike Program. Previously, under the $1 Strike Program, CBOE could list $1 strikes prices from $1 to $50 that were no more than $5 from the closing price of the underlying security on the preceding day. Below are descriptions of the changes to the $1 Strike Program.

New Provisions for Listing $1 Strike Prices in Non-LEAP Series

In addition to using the closing price of the underlying on the preceding day, CBOE may also use the opening price of the underlying in its primary market for determining whether to add $1 strike prices intraday.

$1 strikes prices may be added to eliminate discontinuity between the preceding day's closing price and the opening price.

o Example: If the underlying stock closes at $14, $1 strikes may be added from $9 to $19. If that underlying stock opens at $27.10 the next day, the Exchange may add the $20 (standard strike), $21 and $22 and $1 strikes from $23 to $32.

Strike prices in $2.50 intervals below $50 are prohibited for classes that participate in the $1 Strike Program.

As an exception to the previous limitation on listing $1 strike prices more than $5 from the underlying stock, $1 strike prices are permitted above and below each standard $5 strike that are more than $5 from the price of the underlying stock, with the $1 strike being: (1) $2 above each standard $5 strike above the price of the underlying stock, and (2) $2 below each standard $5 strike below the price of the underlying stock.1

February 4, 2011 Volume RG22 , Number 5 1

1 Strike price intervals must meet the strike setting provisions contained in the OLPP and set forth in Rule 5.5A. Specifically, if the price of the underlying security is less than or equal to $20, CBOE may not list new option series with an exercise price more than 100% above or below the price of the underlying

February 4, 2011 Volume RG22 , Number 5 2

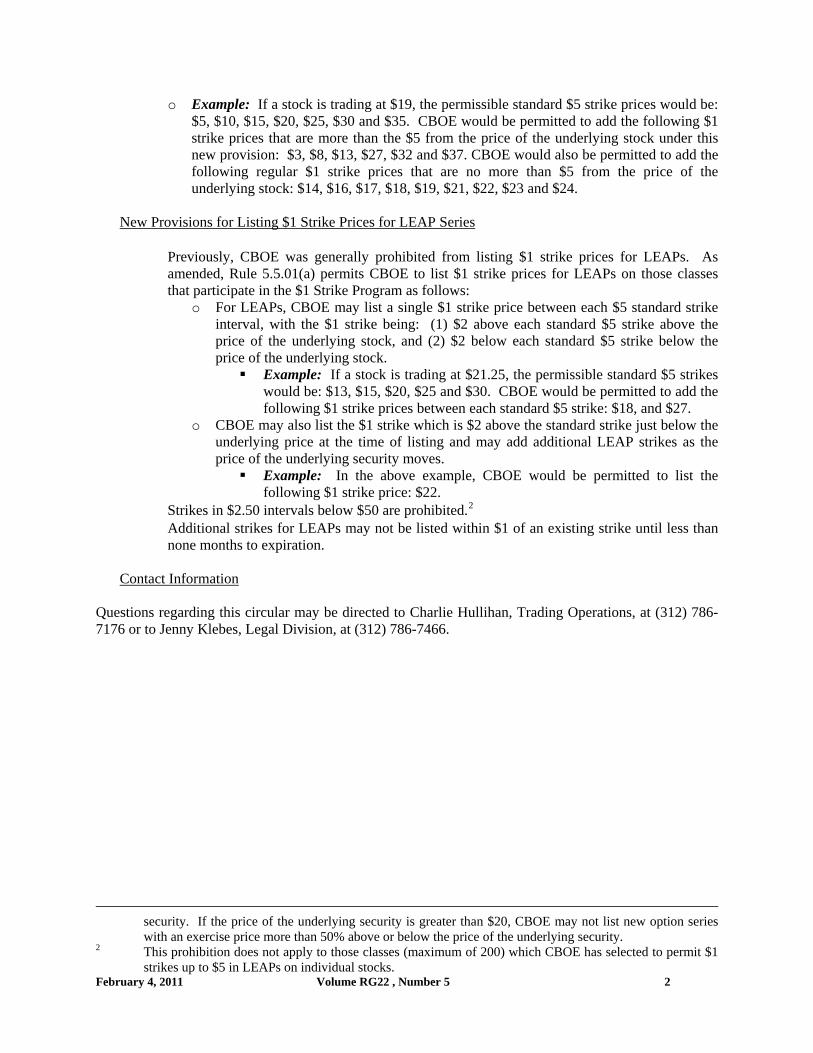

o Example: If a stock is trading at $19, the permissible standard $5 strike prices would be: $5, $10, $15, $20, $25, $30 and $35. CBOE would be permitted to add the following $1 strike prices that are more than the $5 from the price of the underlying stock under this new provision: $3, $8, $13, $27, $32 and $37. CBOE would also be permitted to add the following regular $1 strike prices that are no more than $5 from the price of the underlying stock: $14, $16, $17, $18, $19, $21, $22, $23 and $24.

New Provisions for Listing $1 Strike Prices for LEAP Series

Previously, CBOE was generally prohibited from listing $1 strike prices for LEAPs. As amended, Rule 5.5.01(a) permits CBOE to list $1 strike prices for LEAPs on those classes that participate in the $1 Strike Program as follows:

o For LEAPs, CBOE may list a single $1 strike price between each $5 standard strike interval, with the $1 strike being: (1) $2 above each standard $5 strike above the price of the underlying stock, and (2) $2 below each standard $5 strike below the price of the underlying stock. Example: If a stock is trading at $21.25, the permissible standard $5 strikes

would be: $13, $15, $20, $25 and $30. CBOE would be permitted to add the following $1 strike prices between each standard $5 strike: $18, and $27.

o CBOE may also list the $1 strike which is $2 above the standard strike just below the underlying price at the time of listing and may add additional LEAP strikes as the price of the underlying security moves. Example: In the above example, CBOE would be permitted to list the

following $1 strike price: $22. Strikes in $2.50 intervals below $50 are prohibited.2 Additional strikes for LEAPs may not be listed within $1 of an existing strike until less than

none months to expiration.

Contact Information Questions regarding this circular may be directed to Charlie Hullihan, Trading Operations, at (312) 786-7176 or to Jenny Klebes, Legal Division, at (312) 786-7466.

security. If the price of the underlying security is greater than $20, CBOE may not list new option series with an exercise price more than 50% above or below the price of the underlying security.

2 This prohibition does not apply to those classes (maximum of 200) which CBOE has selected to permit $1 strikes up to $5 in LEAPs on individual stocks.

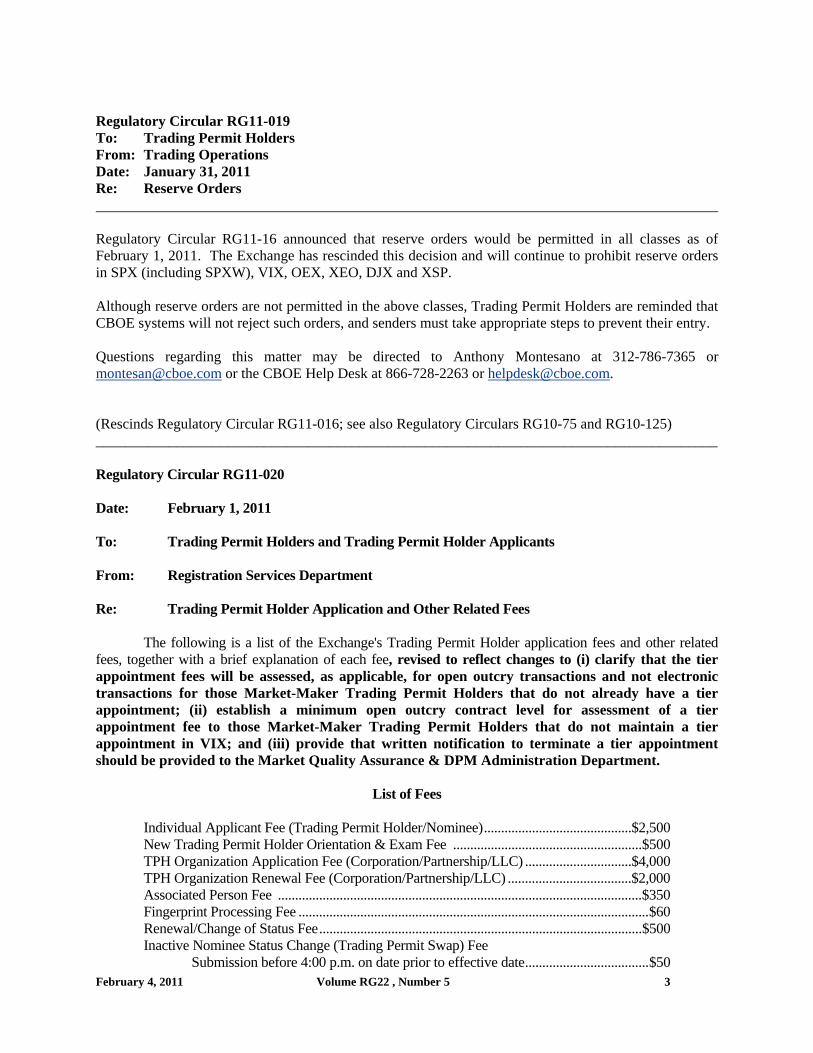

Regulatory Circular RG11-019 To: Trading Permit Holders From: Trading Operations Date: January 31, 2011 Re: Reserve Orders Regulatory Circular RG11-16 announced that reserve orders would be permitted in all classes as of February 1, 2011. The Exchange has rescinded this decision and will continue to prohibit reserve orders in SPX (including SPXW), VIX, OEX, XEO, DJX and XSP. Although reserve orders are not permitted in the above classes, Trading Permit Holders are reminded that CBOE systems will not reject such orders, and senders must take appropriate steps to prevent their entry. Questions regarding this matter may be directed to Anthony Montesano at 312-786-7365 or [email protected] or the CBOE Help Desk at 866-728-2263 or [email protected]. (Rescinds Regulatory Circular RG11-016; see also Regulatory Circulars RG10-75 and RG10-125) _____________________________________________________________________________________ Regulatory Circular RG11-020 Date: February 1, 2011 To: Trading Permit Holders and Trading Permit Holder Applicants From: Registration Services Department Re: Trading Permit Holder Application and Other Related Fees The following is a list of the Exchange's Trading Permit Holder application fees and other related fees, together with a brief explanation of each fee, revised to reflect changes to (i) clarify that the tier appointment fees will be assessed, as applicable, for open outcry transactions and not electronic transactions for those Market-Maker Trading Permit Holders that do not already have a tier appointment; (ii) establish a minimum open outcry contract level for assessment of a tier appointment fee to those Market-Maker Trading Permit Holders that do not maintain a tier appointment in VIX; and (iii) provide that written notification to terminate a tier appointment should be provided to the Market Quality Assurance & DPM Administration Department.

List of Fees Individual Applicant Fee (Trading Permit Holder/Nominee)...........................................$2,500 New Trading Permit Holder Orientation & Exam Fee .......................................................$500 TPH Organization Application Fee (Corporation/Partnership/LLC) ...............................$4,000 TPH Organization Renewal Fee (Corporation/Partnership/LLC) ....................................$2,000 Associated Person Fee ..........................................................................................................$350 Fingerprint Processing Fee ......................................................................................................$60 Renewal/Change of Status Fee..............................................................................................$500 Inactive Nominee Status Change (Trading Permit Swap) Fee Submission before 4:00 p.m. on date prior to effective date....................................$50 February 4, 2011 Volume RG22 , Number 5 3

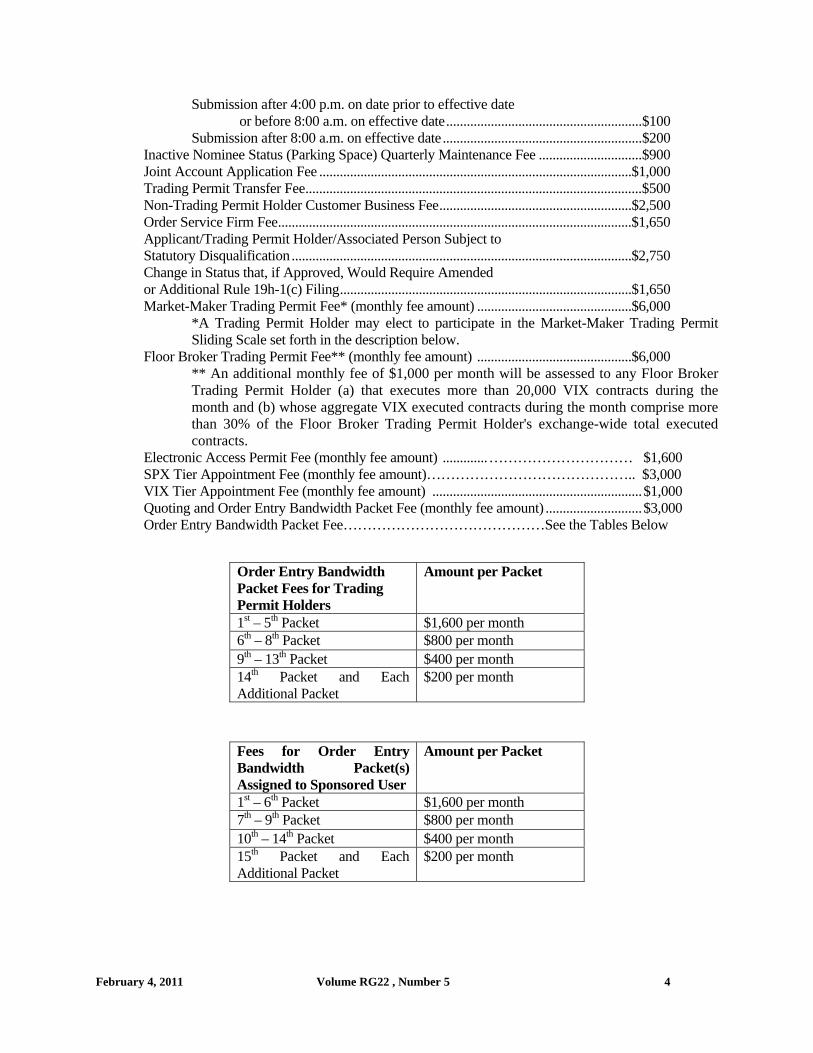

Submission after 4:00 p.m. on date prior to effective date or before 8:00 a.m. on effective date.........................................................$100 Submission after 8:00 a.m. on effective date..........................................................$200 Inactive Nominee Status (Parking Space) Quarterly Maintenance Fee ..............................$900 Joint Account Application Fee ...........................................................................................$1,000 Trading Permit Transfer Fee..................................................................................................$500 Non-Trading Permit Holder Customer Business Fee........................................................$2,500 Order Service Firm Fee.......................................................................................................$1,650 Applicant/Trading Permit Holder/Associated Person Subject to Statutory Disqualification ...................................................................................................$2,750 Change in Status that, if Approved, Would Require Amended or Additional Rule 19h-1(c) Filing.....................................................................................$1,650 Market-Maker Trading Permit Fee* (monthly fee amount) .............................................$6,000

*A Trading Permit Holder may elect to participate in the Market-Maker Trading Permit Sliding Scale set forth in the description below.

Floor Broker Trading Permit Fee** (monthly fee amount) .............................................$6,000 ** An additional monthly fee of $1,000 per month will be assessed to any Floor Broker Trading Permit Holder (a) that executes more than 20,000 VIX contracts during the month and (b) whose aggregate VIX executed contracts during the month comprise more than 30% of the Floor Broker Trading Permit Holder's exchange-wide total executed contracts.

Electronic Access Permit Fee (monthly fee amount) .............………………………… $1,600 SPX Tier Appointment Fee (monthly fee amount)…………………………………….. $3,000 VIX Tier Appointment Fee (monthly fee amount) .............................................................$1,000 Quoting and Order Entry Bandwidth Packet Fee (monthly fee amount) ............................$3,000 Order Entry Bandwidth Packet Fee……………………………………See the Tables Below

Order Entry Bandwidth Packet Fees for Trading Permit Holders

Amount per Packet

1st – 5th Packet $1,600 per month 6th – 8th Packet $800 per month 9th – 13th Packet $400 per month 14th Packet and Each Additional Packet

$200 per month

Fees for Order Entry

Bandwidth Packet(s) Assigned to Sponsored User

Amount per Packet

1st – 6th Packet $1,600 per month 7th – 9th Packet $800 per month 10th – 14th Packet $400 per month 15th Packet and Each Additional Packet

$200 per month

February 4, 2011 Volume RG22 , Number 5 4

ALL FEES ARE NON-REFUNDABLE

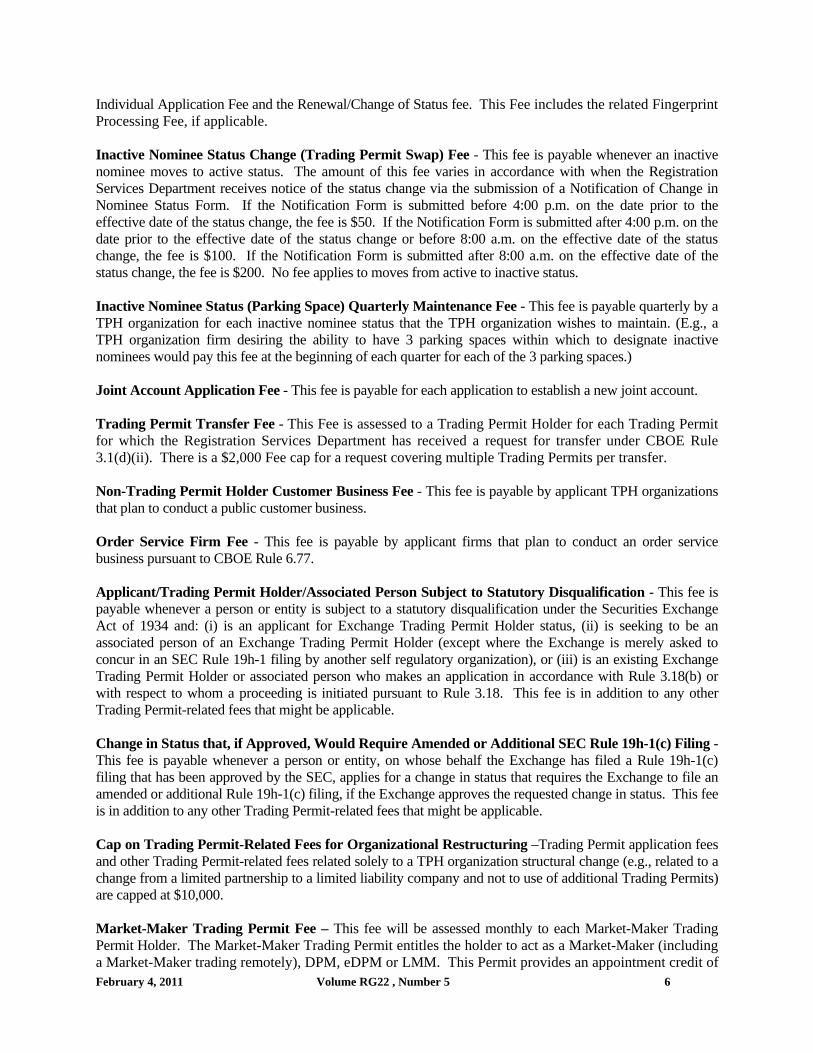

Individual Applicant Fee (Trading Permit Holder/Nominee) - This fee is payable by a new individual applicant for Trading Permit Holder status on the Exchange. The applicant’s Fingerprint Processing Fee is included as part of this fee. New Trading Permit Holder Orientation & Exam Fee - This fee is payable by each applicant seeking Trading Permit Holder status, which requires a trading function. TPH Organization Application Fee (Corporation/Partnership/LLC) - This fee is payable by an applicant that desires to be a TPH organization on the Exchange. This fee encompasses the TPH Organization Application and related documentation, one Nominee Individual Application Fee associated with the TPH Organization Application, and Associated Person(s) Fees that are part of this TPH Organization Application. TPH Organization Renewal Fee (Corporation/Partnership/LLC) - This fee is payable by a former trading firm member or TPH organization that reapplies for Trading Permit Holder status within 9 months of their membership or Trading Permit Status termination date and becomes an effective TPH organization within 1 year of their membership or Trading Permit Status termination date. This fee encompasses the TPH Organization Application and related documentation and one Nominee who is either (i) an existing individual Trading Permit Holder desiring to change Trading Permit Holder status or (ii) a former individual member or Trading Permit Holder who reapplies for Trading Permit Holder status within 9 months of their membership or Trading Permit Status termination date and becomes an effective Trading Permit Holder within 1 year of their membership termination date. Associated Person Fee - The Associated Person Fee is payable for the addition of certain individuals on a TPH organization’s Form BD. This fee includes the related Fingerprint Processing Fee. This Fee is payable by each executive officer, general partner, or LLC Manager. Additionally, this Fee is payable by each principal shareholder that has 5% or more direct ownership of a class of a voting security of a TPH organization corporation, limited partner who has the right to receive upon dissolution, or has contributed, 5% or more of the partnership's capital, and LLC member who has the right to receive upon dissolution, or has contributed, 5% or more of the LLC's capital. This Fee is also payable by any person classified as a “Control Person” of the TPH organization. Fingerprint Processing Fee - This Fee will be assessed for employees of Trading Permit Holders and any other individual requesting the Exchange to process a fingerprint, electronically or otherwise, excluding fingerprint requirements for Individual Applicants, individuals applying for Renewal/Change of Status, and Associated Persons subject to the Associated Person Fee set forth above. Renewal/Change of Status Fee - This fee is payable (i) by an existing individual Trading Permit Holder desiring to change Trading Permit Holder status or (ii) by a former individual Trading Permit Holder or former individual member who reapplies for Trading Permit Holder status within 9 months of their membership or Trading Permit Holder status termination date and becomes an effective Trading Permit Holder within 1 year of their membership or Trading Permit Holder status termination date. A former individual Trading Permit Holder or former individual member who reapplies for Trading Permit Holder status within 9 months of termination from membership or Trading Permit Holder status will be assessed the Renewal/Change of Status fee at the time of submission of the application. If that person becomes an effective Trading Permit Holder more than 1 year after their membership or Trading Permit Holder status termination date, the person will then be charged an additional fee equal to the difference between the

February 4, 2011 Volume RG22 , Number 5 5

Individual Application Fee and the Renewal/Change of Status fee. This Fee includes the related Fingerprint Processing Fee, if applicable. Inactive Nominee Status Change (Trading Permit Swap) Fee - This fee is payable whenever an inactive nominee moves to active status. The amount of this fee varies in accordance with when the Registration Services Department receives notice of the status change via the submission of a Notification of Change in Nominee Status Form. If the Notification Form is submitted before 4:00 p.m. on the date prior to the effective date of the status change, the fee is $50. If the Notification Form is submitted after 4:00 p.m. on the date prior to the effective date of the status change or before 8:00 a.m. on the effective date of the status change, the fee is $100. If the Notification Form is submitted after 8:00 a.m. on the effective date of the status change, the fee is $200. No fee applies to moves from active to inactive status. Inactive Nominee Status (Parking Space) Quarterly Maintenance Fee - This fee is payable quarterly by a TPH organization for each inactive nominee status that the TPH organization wishes to maintain. (E.g., a TPH organization firm desiring the ability to have 3 parking spaces within which to designate inactive nominees would pay this fee at the beginning of each quarter for each of the 3 parking spaces.) Joint Account Application Fee - This fee is payable for each application to establish a new joint account. Trading Permit Transfer Fee - This Fee is assessed to a Trading Permit Holder for each Trading Permit for which the Registration Services Department has received a request for transfer under CBOE Rule 3.1(d)(ii). There is a $2,000 Fee cap for a request covering multiple Trading Permits per transfer. Non-Trading Permit Holder Customer Business Fee - This fee is payable by applicant TPH organizations that plan to conduct a public customer business. Order Service Firm Fee - This fee is payable by applicant firms that plan to conduct an order service business pursuant to CBOE Rule 6.77. Applicant/Trading Permit Holder/Associated Person Subject to Statutory Disqualification - This fee is payable whenever a person or entity is subject to a statutory disqualification under the Securities Exchange Act of 1934 and: (i) is an applicant for Exchange Trading Permit Holder status, (ii) is seeking to be an associated person of an Exchange Trading Permit Holder (except where the Exchange is merely asked to concur in an SEC Rule 19h-1 filing by another self regulatory organization), or (iii) is an existing Exchange Trading Permit Holder or associated person who makes an application in accordance with Rule 3.18(b) or with respect to whom a proceeding is initiated pursuant to Rule 3.18. This fee is in addition to any other Trading Permit-related fees that might be applicable. Change in Status that, if Approved, Would Require Amended or Additional SEC Rule 19h-1(c) Filing - This fee is payable whenever a person or entity, on whose behalf the Exchange has filed a Rule 19h-1(c) filing that has been approved by the SEC, applies for a change in status that requires the Exchange to file an amended or additional Rule 19h-1(c) filing, if the Exchange approves the requested change in status. This fee is in addition to any other Trading Permit-related fees that might be applicable. Cap on Trading Permit-Related Fees for Organizational Restructuring –Trading Permit application fees and other Trading Permit-related fees related solely to a TPH organization structural change (e.g., related to a change from a limited partnership to a limited liability company and not to use of additional Trading Permits) are capped at $10,000. Market-Maker Trading Permit Fee – This fee will be assessed monthly to each Market-Maker Trading Permit Holder. The Market-Maker Trading Permit entitles the holder to act as a Market-Maker (including a Market-Maker trading remotely), DPM, eDPM or LMM. This Permit provides an appointment credit of February 4, 2011 Volume RG22 , Number 5 6

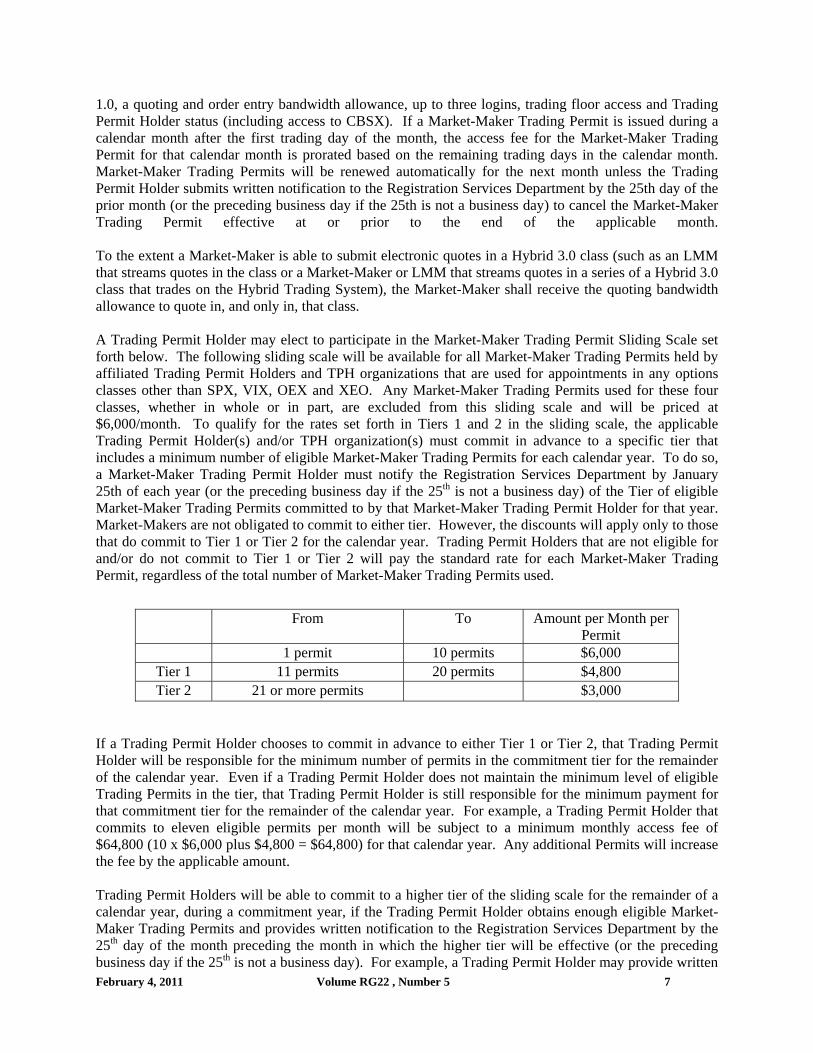

1.0, a quoting and order entry bandwidth allowance, up to three logins, trading floor access and Trading Permit Holder status (including access to CBSX). If a Market-Maker Trading Permit is issued during a calendar month after the first trading day of the month, the access fee for the Market-Maker Trading Permit for that calendar month is prorated based on the remaining trading days in the calendar month. Market-Maker Trading Permits will be renewed automatically for the next month unless the Trading Permit Holder submits written notification to the Registration Services Department by the 25th day of the prior month (or the preceding business day if the 25th is not a business day) to cancel the Market-Maker Trading Permit effective at or prior to the end of the applicable month. To the extent a Market-Maker is able to submit electronic quotes in a Hybrid 3.0 class (such as an LMM that streams quotes in the class or a Market-Maker or LMM that streams quotes in a series of a Hybrid 3.0 class that trades on the Hybrid Trading System), the Market-Maker shall receive the quoting bandwidth allowance to quote in, and only in, that class. A Trading Permit Holder may elect to participate in the Market-Maker Trading Permit Sliding Scale set forth below. The following sliding scale will be available for all Market-Maker Trading Permits held by affiliated Trading Permit Holders and TPH organizations that are used for appointments in any options classes other than SPX, VIX, OEX and XEO. Any Market-Maker Trading Permits used for these four classes, whether in whole or in part, are excluded from this sliding scale and will be priced at $6,000/month. To qualify for the rates set forth in Tiers 1 and 2 in the sliding scale, the applicable Trading Permit Holder(s) and/or TPH organization(s) must commit in advance to a specific tier that includes a minimum number of eligible Market-Maker Trading Permits for each calendar year. To do so, a Market-Maker Trading Permit Holder must notify the Registration Services Department by January 25th of each year (or the preceding business day if the 25th is not a business day) of the Tier of eligible Market-Maker Trading Permits committed to by that Market-Maker Trading Permit Holder for that year. Market-Makers are not obligated to commit to either tier. However, the discounts will apply only to those that do commit to Tier 1 or Tier 2 for the calendar year. Trading Permit Holders that are not eligible for and/or do not commit to Tier 1 or Tier 2 will pay the standard rate for each Market-Maker Trading Permit, regardless of the total number of Market-Maker Trading Permits used.

February 4, 2011 Volume RG22 , Number 5 7

From To Amount per Month per Permit

1 permit 10 permits $6,000 Tier 1 11 permits 20 permits $4,800 Tier 2 21 or more permits $3,000

If a Trading Permit Holder chooses to commit in advance to either Tier 1 or Tier 2, that Trading Permit Holder will be responsible for the minimum number of permits in the commitment tier for the remainder of the calendar year. Even if a Trading Permit Holder does not maintain the minimum level of eligible Trading Permits in the tier, that Trading Permit Holder is still responsible for the minimum payment for that commitment tier for the remainder of the calendar year. For example, a Trading Permit Holder that commits to eleven eligible permits per month will be subject to a minimum monthly access fee of $64,800 (10 x $6,000 plus $4,800 = $64,800) for that calendar year. Any additional Permits will increase the fee by the applicable amount. Trading Permit Holders will be able to commit to a higher tier of the sliding scale for the remainder of a calendar year, during a commitment year, if the Trading Permit Holder obtains enough eligible Market-Maker Trading Permits and provides written notification to the Registration Services Department by the 25th day of the month preceding the month in which the higher tier will be effective (or the preceding business day if the 25th is not a business day). For example, a Trading Permit Holder may provide written

notice to commit to Tier 1 effective July 1 for the remainder of the calendar year as long as the Trading Permit Holder obtains enough eligible Trading Permits and provides written notice by June 25th that the Trading Permit Holder would like to participate in the sliding scale starting in July for the remainder of that calendar year. Even if that Trading Permit Holder subsequently falls below the minimum number of eligible Market-Maker Trading Permits (in the committed calendar year), for the committed tier, the Trading Permit Holder will remain responsible for paying for the tier minimum for the remainder of the calendar year.

Trading Permit Holders will be responsible to pay for at least the minimum amount of eligible Market-Maker Trading Permits in the committed tier for the calendar year on a monthly basis unless the Trading Permit Holder entirely terminates as a Trading Permit Holder during the year. If a Trading Permit Holder combines, merges, or is acquired during the course of the calendar year, the surviving Trading Permit Holder will maintain responsibility for the committed number of eligible Market-Maker Trading Permits. Floor Broker Trading Permit Fee – This fee will be assessed monthly to each Floor Broker Trading Permit Holder. The Floor Broker Trading Permit entitles the holder to act as a Floor Broker. This Permit provides an order entry bandwidth allowance, up to three logins, trading floor access and Trading Permit Holder Status (including access to CBSX). If a Floor Broker Trading Permit is issued during a calendar month after the first trading day of the month, the access fee for the Floor Broker Trading Permit for that calendar month is prorated based on the remaining trading days in the calendar month. Floor Broker Trading Permits will be renewed automatically for the next month unless the Trading Permit Holder submits written notification to the Registration Services Department by the 25th day of the prior month (or the preceding business day if the 25th is not a business day) to cancel the Floor Broker Trading Permit effective at or prior to the end of the applicable month. An additional monthly fee of $1,000 per month will be assessed to any Floor Broker Trading Permit Holder (a) that executes more than 20,000 VIX contracts during the month and (b) whose aggregate VIX executed contracts during the month comprise more than 30% of the Floor Broker Trading Permit Holder's exchange-wide total executed contracts. Electronic Access Permit (EAP) Fee – This fee will be assessed monthly to each EAP Holder. The EAP entitles the holder to electronic access to the Exchange. Holders must be broker-dealers registered with the Exchange in one or more of the following capacities: (a) Clearing Trading Permit Holder; (b) TPH organization approved to transact business with the public; (c) Proprietary Trading Permit Holder; and (d) order service firm. This permit does not provide access to the trading floor. A Proprietary Trading Permit Holder is a Trading Permit Holder with electronic access to the Exchange to submit proprietary orders that are not Market-Maker orders (i.e. that are not M orders for the Proprietary Trading Permit Holder’s own account or an affiliated Market-Maker account). The EAP provides an order entry bandwidth allowance, up to three logins and Trading Permit Holder Status (including access to CBSX). If an EAP is issued during a calendar month after the first trading day of the month, the access fee for the EAP for that calendar month is prorated based on the remaining trading days in the calendar month. EAPs will be renewed automatically for the next month unless the Trading Permit Holder submits written notification to the Registration Services Department by the 25th day of the prior month (or the preceding business day if the 25th is not a business day) to cancel the EAP effective at or prior to the end of the applicable month. SPX Tier Appointment Fee – This fee will be assessed monthly to any Market-Maker Trading Permit Holder that either (a) has an SPX Tier Appointment at any time during a calendar month; or (b) conducts any open outcry transactions in SPX, including SPX Weeklys, at any time during a calendar month. Each SPX Tier Appointment may only be used with one designated Market-Maker Trading Permit. SPX Tier Appointments will be renewed automatically for the next month unless the Trading Permit Holder submits written notification to the Market Quality Assurance & DPM Administration Department by the February 4, 2011 Volume RG22 , Number 5 8

February 4, 2011 Volume RG22 , Number 5 9

last business day of the prior month to cancel the SPX Tier Appointment effective at or prior to the end of the applicable month. VIX Tier Appointment Fee – This fee will be assessed monthly to any Market-Maker Trading Permit Holder that either (a) has a VIX Tier Appointment at any time during a calendar month; or (b) trades at least 1,000 VIX options contracts in open outcry during a calendar month. Each VIX Tier Appointment may only be used with one designated Market-Maker Trading Permit. VIX Tier Appointments will be renewed automatically for the next month unless the Trading Permit Holder submits written notification to the Market Quality Assurance & DPM Administration Department by the last business day of the prior month to cancel the VIX Tier Appointment effective at or prior to the end of the applicable month. Quoting and Order Entry Bandwidth Packet Fee – This fee will be assessed monthly to Market-Maker Trading Permit Holders that have registered for a Quoting and Order Entry Bandwidth Packet. A Quoting and Order Entry Bandwidth Packet is available to Market-Maker Trading Permit Holders only and entitles the holder to a quoting and order entry bandwidth allowance and up to three additional logins, which may then be added onto the total bandwidth pool for a Market-Maker’s acronym(s) and Trading Permit(s). If a Quoting and Order Entry Bandwidth Packet is issued during a calendar month after the first trading day of the month, the fee for that calendar month is prorated based on the remaining trading days in the calendar month. Quoting and Order Entry Bandwidth Packets will be renewed automatically for the next month unless the Trading Permit Holder submits written notification to the Registration Services Department by the last business day of the prior month to cancel the Quoting and Order Entry Bandwidth Packet effective at or prior to the end of the applicable month. Order Entry Bandwidth Packet Fee - This fee will be assessed monthly to Trading Permit Holders that have registered for an Order Entry Bandwidth Packet. An Order Entry Bandwidth Packet is available to all Trading Permit Holders and entitles the holder to order entry bandwidth allowance and up to three additional logins. A Trading Permit Holder may also obtain and assign to a Sponsored User of the Trading Permit Holder one or more Order Entry Bandwidth Packets. In that event, the fees for the assigned bandwidth packet(s) are assessed to the Trading Permit Holder and the bandwidth packet(s) may be utilized solely by the Sponsored User (and not by the Trading Permit Holder or any other Sponsored User). If an Order Entry Bandwidth Packet is issued during a calendar month after the first trading day of the month, the fee for that calendar month is prorated based on the remaining trading days in the calendar month. Order Entry Bandwidth Packets will be renewed automatically for the next month unless the Trading Permit Holder submits written notification to the Registration Services Department by the last business day of the prior month to cancel the Order Entry Bandwidth Packet effective at or prior to the end of the applicable month. Any questions regarding this Regulatory Circular may be directed to Regina Millison at (312) 786-7452 or Stan Leimer at (312) 786-7299 in the Registration Services Department.

(Regulatory Circular RG11-001 Revised). _____________________________________________________________________________________

Regulatory Circular RG11-021 Date: February 1, 2011 To: Trading Permit Holders and Trading Permit Holder Organizations From: Finance and Administration Subject: Linkage Fees, Par Official Fees and CFLEX Cap ___________________________________________________________________________________ Effective February 7, 2011, CBOE will assess a fee of $0.35/contract for executions on an away exchange as a result of a linkage order sent by CBOE, where the original order received by CBOE was a public customer order of 100 contracts or greater. This represents a change from the current qualifying public customer order size of 500 or more contracts. Effective February 1, 2011, the Exchange will waive the Par Official Fees for any affiliated Trading Permit Holders that have ten or more Floor Broker Trading Permits throughout the calendar month. Currently, the CFLEX Surcharge Fee is $0.10/contract for all orders or origin types, however it is only charged up to the first 2,500 contracts per trade for public customers. Effective February 1, 2011, the cap of the first 2,500 contracts per trade will apply to all origin codes. Each of these changes is subject to SEC review.

__________________________ Questions can be directed to Don Patton at (312) 786-7026 ([email protected]), Colleen Laughlin at 312-786-8390 ([email protected]), John Mavindidze at (312) 786-7689 ([email protected]) or Cheryl Ahrens at 312-786-7450 ([email protected]).

February 4, 2011 Volume RG22 , Number 5 10

R U L E C H A N G E S APPROVED RULE CHANGE(S) The Securities and Exchange Commission (“SEC”) has approved the following change(s) to Exchange rules pursuant to Section 19(b) of the Securities Exchange Act of 1934 (the “Act”). Below, any additions to rule text are underlined and any deletions are [bracketed]. Copies are available on the CBOE public website at www.cboe.com/legal/effectivefiling.aspx. The effective date of the rule change is the date of approval unless otherwise noted. _________________________________________________________________________________ SR-CBOE-2010-106 Credit Option Margin Requirements On February 2, 2011, the SEC approved Rule Change File No. SR-CBOE-2010-106, which filing amends the margin requirements for Credit Options to be consistent with FINRA’s margin requirements for Credit Default Swaps. The margin requirements are established on a pilot basis to run on a parallel track with FINRA Rule 4240, which also operates on a pilot basis and is scheduled to expire on July 16, 2011. Any questions regarding the rule change may be directed to Jenny Klebes, Legal Division, at 312-786-7466. The rule text is shown below and the rule filing is available at https://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2010-106%20Amendment%201.pdf.

Rule 12.3—Margin Requirements RULE 12.3 (a) – (k) No changes. (l) Credit Options (1) Risk Monitoring Procedures and Guidelines

Trading Permit Holders are required to monitor the risk of customer and broker-dealer accounts with exposure to Credit Options and must implement and maintain a comprehensive written risk analysis methodology for assessing the potential risk to the Trading Permit Holder’s capital over a specified range of possible market movements over a specified time period. For purposes of complying with this rule, Trading Permit Holders must employ the risk monitoring procedures and guidelines set forth below in sub-paragraphs (i) through (viii) of this Rule 12.3(l)(1). The Trading Permit Holder must review, in accordance with the Trading Permit Holder’s written procedures, at reasonable periodic intervals, the Trading Permit Holder’s credit extension activities for consistency with the risk monitoring procedures and guidelines set forth in this Rule 12.3(l)(1), and must determine whether the data necessary to apply the risk monitoring procedures and guidelines is accessible on a timely basis and information systems are available to adequately capture, monitor, analyze and report relevant data, including:

(i) obtaining and reviewing the required account documentation and financial information necessary for assessing the amount of credit to be extended to customers and broker-dealers;

(ii) assessing the determination, review and approval of credit limits to each customer and broker-dealer, and across all customers and broker-dealers, engaging in Credit Option transactions;

(iii) monitoring credit risk exposure to the Trading Permit Holder from Credit Options, including the type, scope and frequency of reporting to senior management;

(iv) the use of stress testing of accounts containing Credit Option contracts in order to monitor market risk exposure from individual accounts and in the aggregate;

February 4, 2011 Volume RG22 , Number 5 11

(v) managing the impact of credit extended related to Credit Option contracts on the Trading Permit Holder’s overall risk exposure;

(vi) determining the need to collect margin from a particular customer or broker-dealer in addition to the amount required by this Rule 12.3(l), including whether such determination was based upon the credit worthiness of the customer or broker-dealer and/or the risk of the specific Credit Option contracts;

(vii) monitoring the credit exposure resulting from concentrated positions within both individual accounts and across all accounts containing Credit Option contracts: and

(viii) maintaining sufficient margin in each customer and broker-dealer account to protect against the default of the largest individual exposure in the account as measured by computing the largest maximum possible loss.

(2) Requiring Additional Margin. Trading Permit Holders shall, based on the risk monitoring procedures and guidelines required above, determine whether the margin required by this Rule 12.3(l) is adequate with respect to their customer and broker-dealer accounts and, where appropriate, increase such requirements.

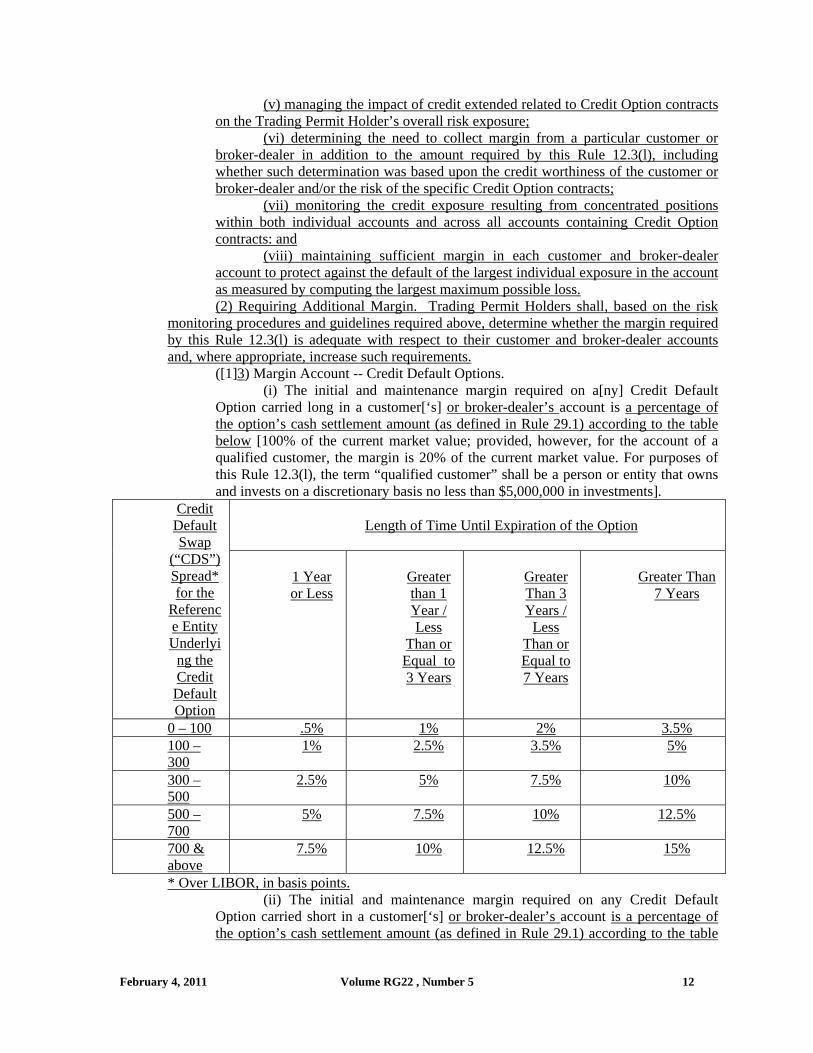

([1]3) Margin Account -- Credit Default Options. (i) The initial and maintenance margin required on a[ny] Credit Default

Option carried long in a customer[‘s] or broker-dealer’s account is a percentage of the option’s cash settlement amount (as defined in Rule 29.1) according to the table below [100% of the current market value; provided, however, for the account of a qualified customer, the margin is 20% of the current market value. For purposes of this Rule 12.3(l), the term “qualified customer” shall be a person or entity that owns and invests on a discretionary basis no less than $5,000,000 in investments].

Length of Time Until Expiration of the Option

Credit Default Swap

(“CDS”) Spread* for the

Reference Entity Underlyi

ng the Credit

Default Option

1 Year or Less

Greater than 1 Year / Less

Than or Equal to 3 Years

Greater Than 3 Years /

Less Than or Equal to 7 Years

Greater Than

7 Years

0 – 100 .5% 1% 2% 3.5% 100 – 300

1% 2.5% 3.5% 5%

300 – 500

2.5% 5% 7.5% 10%

500 – 700

5% 7.5% 10% 12.5%

700 & above

7.5% 10% 12.5% 15%

* Over LIBOR, in basis points. (ii) The initial and maintenance margin required on any Credit Default

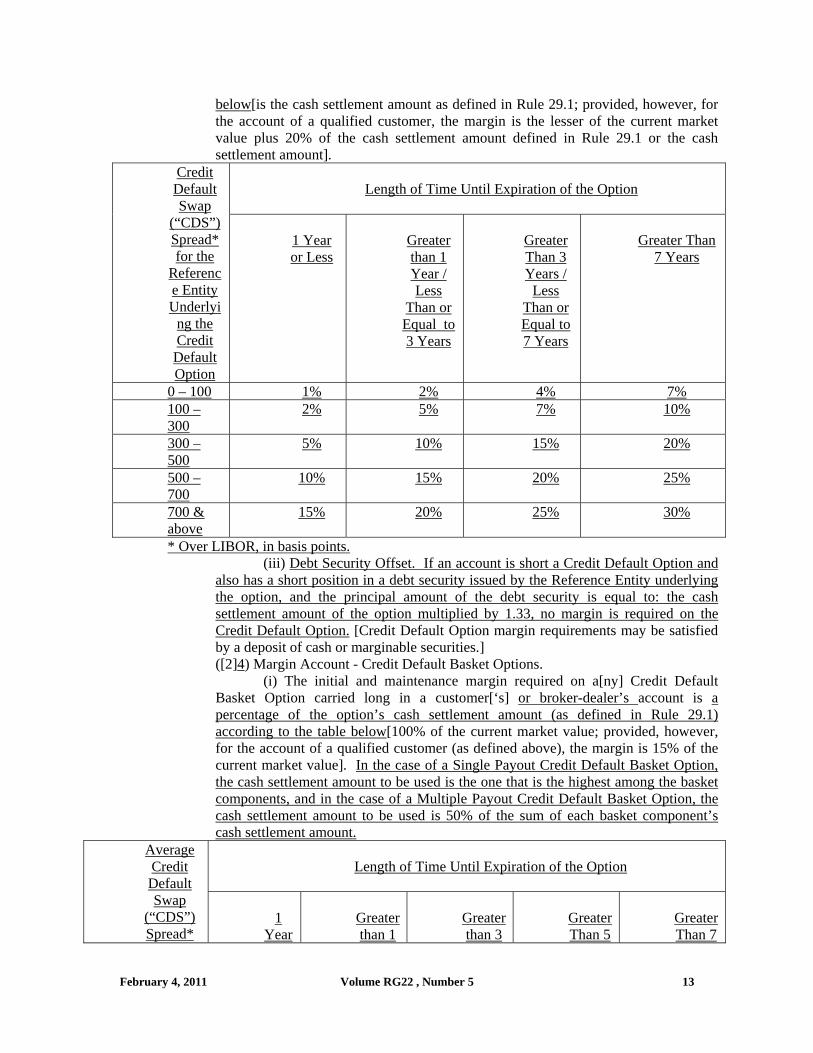

Option carried short in a customer[‘s] or broker-dealer’s account is a percentage of the option’s cash settlement amount (as defined in Rule 29.1) according to the table

February 4, 2011 Volume RG22 , Number 5 12

below[is the cash settlement amount as defined in Rule 29.1; provided, however, for the account of a qualified customer, the margin is the lesser of the current market value plus 20% of the cash settlement amount defined in Rule 29.1 or the cash settlement amount].

Length of Time Until Expiration of the Option

Credit Default Swap

(“CDS”) Spread* for the

Reference Entity Underlyi

ng the Credit Default Option

1 Year or Less

Greater than 1 Year / Less

Than or Equal to 3 Years

Greater Than 3 Years /

Less Than or Equal to 7 Years

Greater Than

7 Years

0 – 100 1% 2% 4% 7% 100 – 300

2% 5% 7% 10%

300 – 500

5% 10% 15% 20%

500 – 700

10% 15% 20% 25%

700 & above

15% 20% 25% 30%

* Over LIBOR, in basis points. (iii) Debt Security Offset. If an account is short a Credit Default Option and

also has a short position in a debt security issued by the Reference Entity underlying the option, and the principal amount of the debt security is equal to: the cash settlement amount of the option multiplied by 1.33, no margin is required on the Credit Default Option. [Credit Default Option margin requirements may be satisfied by a deposit of cash or marginable securities.] ([2]4) Margin Account - Credit Default Basket Options.

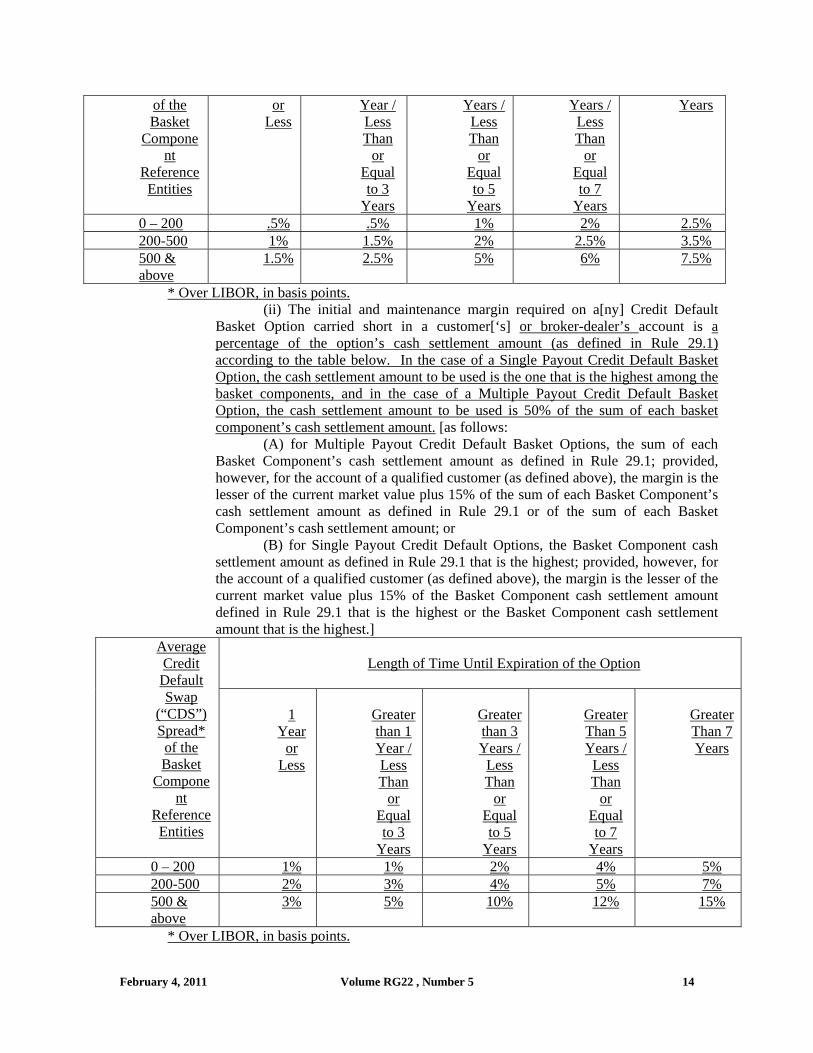

(i) The initial and maintenance margin required on a[ny] Credit Default Basket Option carried long in a customer[‘s] or broker-dealer’s account is a percentage of the option’s cash settlement amount (as defined in Rule 29.1) according to the table below[100% of the current market value; provided, however, for the account of a qualified customer (as defined above), the margin is 15% of the current market value]. In the case of a Single Payout Credit Default Basket Option, the cash settlement amount to be used is the one that is the highest among the basket components, and in the case of a Multiple Payout Credit Default Basket Option, the cash settlement amount to be used is 50% of the sum of each basket component’s cash settlement amount.

Length of Time Until Expiration of the Option

Average Credit Default Swap

(“CDS”) Spread*

1

Year

Greater than 1

Greater than 3

Greater Than 5

Greater Than 7

February 4, 2011 Volume RG22 , Number 5 13

of the Basket

Component

Reference Entities

or Less

Year / Less Than

or Equal to 3

Years

Years / Less Than

or Equal to 5

Years

Years / Less Than

or Equal to 7

Years

Years

0 – 200 .5% .5% 1% 2% 2.5% 200-500 1% 1.5% 2% 2.5% 3.5% 500 & above

1.5% 2.5% 5% 6% 7.5%

* Over LIBOR, in basis points. (ii) The initial and maintenance margin required on a[ny] Credit Default

Basket Option carried short in a customer[‘s] or broker-dealer’s account is a percentage of the option’s cash settlement amount (as defined in Rule 29.1) according to the table below. In the case of a Single Payout Credit Default Basket Option, the cash settlement amount to be used is the one that is the highest among the basket components, and in the case of a Multiple Payout Credit Default Basket Option, the cash settlement amount to be used is 50% of the sum of each basket component’s cash settlement amount. [as follows:

(A) for Multiple Payout Credit Default Basket Options, the sum of each Basket Component’s cash settlement amount as defined in Rule 29.1; provided, however, for the account of a qualified customer (as defined above), the margin is the lesser of the current market value plus 15% of the sum of each Basket Component’s cash settlement amount as defined in Rule 29.1 or of the sum of each Basket Component’s cash settlement amount; or

(B) for Single Payout Credit Default Options, the Basket Component cash settlement amount as defined in Rule 29.1 that is the highest; provided, however, for the account of a qualified customer (as defined above), the margin is the lesser of the current market value plus 15% of the Basket Component cash settlement amount defined in Rule 29.1 that is the highest or the Basket Component cash settlement amount that is the highest.]

Length of Time Until Expiration of the Option

Average Credit Default Swap

(“CDS”) Spread* of the Basket

Component

Reference Entities

1

Year or

Less

Greater than 1 Year / Less Than

or Equal to 3

Years

Greater than 3 Years /

Less Than

or Equal to 5

Years

Greater Than 5 Years /

Less Than

or Equal to 7

Years

Greater Than 7 Years

0 – 200 1% 1% 2% 4% 5% 200-500 2% 3% 4% 5% 7% 500 & above

3% 5% 10% 12% 15%

* Over LIBOR, in basis points.

February 4, 2011 Volume RG22 , Number 5 14

(5) Spreads. If an account is short a Credit Option and is also long a Credit Option with the same underlying Reference Obligation(s), and the long option is paid for in full, and the long option does not expire before the short option, no margin is required

([(iii)]6) Credit [Default Basket ]Option margin requirements may be satisfied by a deposit of cash or marginable securities.

(7) Concentrations. If, across all accounts, the maximum exposure in Credit Option contracts overlying any single Reference Entity exceeds the Trading Permit Holder’s tentative net capital, the Trading Permit Holder must deduct from net capital an amount equal to the aggregate margin requirement for all such accounts on the Credit Option contracts (including Credit Default Basket Options having the subject Reference Entity as a component) overlying such single Reference Entity, as specified in this Rule 12.3(l). This deduction from net capital may be reduced by the amount of excess margin held in all customer and broker-dealer accounts.

([3]8) Cash Account --Credit Default Options. A Credit Default Option carried short in a customer’s account is deemed a covered position, and eligible for the cash account, provided any one of the following either is held in the account at the time the option is written or is received into the account promptly thereafter:

(i) cash or cash equivalents equal to 100% of the cash settlement amount as defined in Rule 29.1; or

(ii) an escrow agreement. The escrow agreement must certify that the bank holds for the account of the customer as security for the agreement (A) cash, (B) cash equivalents, (C) one or more qualified equity securities, or (D) a combination thereof having an aggregate market value of not less than 100% of the cash settlement amount as defined in Rule 29.1 and that the bank will promptly pay the TPH organization the cash settlement amount in the event of a Credit Event as defined in Rule 29.1. ([4]9) Cash Account - Credit Default Basket Options. A Credit Default Basket

Option carried short in a customer’s account is deemed a covered position, and eligible for the cash account, provided any one of the following either is held in the account at the time the option is written or is received into the account promptly thereafter:

(i) For Multiple Payout Credit Default Basket Options, cash or cash equivalents equal to [100%] 50% of the sum of each Basket Component’s cash settlement amount as defined in Rule 29.1;

(ii) For Single Payout Credit Default Basket Options, cash or cash equivalents equal to 100% of the Basket Component cash settlement amount as defined in Rule 29.1 that is the highest; or

(iii) an escrow agreement. The escrow agreement must certify that the bank holds for the account of the customer as security for the agreement (A) cash, (B) cash equivalents, (C) one or more qualified equity securities, or (D) a combination thereof having an aggregate market value of not less than 100% of the sum of each Basket Component’s cash settlement amount as defined in Rule 29.1 in the case of Multiple Payout Credit Default Basket Option or 100% of the Basket Component cash settlement amount as defined in Rule 29.1 that is the highest in the case of a Single Payout Credit Default Basket Option and that the bank will promptly pay the TPH organization the cash settlement amount in the event of a Credit Event as defined in Rule 29.1. (10) Duration of the Credit Option Margin Pilot Program. The Credit Option Margin

Pilot Program shall be through July 16, 2011. * * * * *

February 4, 2011 Volume RG22 , Number 5 15

Rule 12.5—Determination of Value for Margin Purposes RULE 12.5. Positions in active securities, except security futures contracts, dealt in on a recognized exchange (including option contracts) shall, for margin purposes, be valued at current market value prices; provided that, whether or not dealt in on an exchange, only those options contracts on a stock or stock index, or a stock index warrant, having an expiration that exceeds 9 months, or a Credit Option as defined in Rule 29.1 [that is carried for the account of a qualified customer], and which are listed or guaranteed by the carrying broker-dealer, may be deemed to have market value for the purposes of Rule 12.3(c). Security futures contracts shall have no value for margin purposes. Positions in other securities shall be valued conservatively in the light of current market prices and the amount of anticipated realization upon a liquidation of the entire position. Substantial additional margin must be required in all cases where the securities carried are subject to unusually rapid or violent changes in value, or where the amount carried is such that they cannot be liquidated promptly.

* * * * * _________________________________________________________________________________ EFFECTIVE-ON-FILING RULE CHANGE(S) The following rule filings were submitted to the SEC “effective on filing,” and may have taken effect pursuant to Section 19(b)(3) of the Act. They will remain in effect barring further action by the SEC within 60 days after publication in the Federal Register. Below, any additions to rule text are underlined and any deletions are [bracketed]. Copies are available on the CBOE public website at www.cboe.org/legal/effectivefiling.aspx. _________________________________________________________________________________ SR-CBOE-2011-012 Weekly Option Series On January 31, 2011, the Exchange filed Rule Change File No. SR-CBOE-2011-012, which filing proposes to amend Rules 5.5 and 24.9 so that the Exchange may select fifteen (15) options classes on which Weekly options may be listed. Any questions regarding the rule change may be directed to Jenny Klebes, Legal Division, at 312-786-7466. The rule text is shown below and the rule filing is available at https://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2011-012.pdf.

Rule 5.5—Terms of Index Option Contracts RULE 5.5. (a) - (c) No change. (d) Short Term Option Series Program. After an option class has been approved for listing and trading on the Exchange, the Exchange may open for trading on any Thursday or Friday that is a business day (“Short Term Option Opening Date”) series of options on that class that expire on the Friday of the following business week that is a business day (“Short Term Option Expiration Date”). If the Exchange is not open for business on the respective Thursday or Friday, the Short Term Option Opening Date will be the first business day immediately prior to that respective Thursday or Friday. Similarly, if the Exchange is not open for business on the Friday of the following business week, the Short Term Option Expiration Date will be the first business day immediately prior to that Friday. Regarding Short Term Option Series:

(1) Classes. The Exchange may select up to [five] fifteen currently listed option classes on which Short Term Option Series may be opened on any Short Term Option Opening Date. In addition to the [five] fifteen-option class restriction, the Exchange also may list Short Term Option Series on any option classes that are selected by other securities

February 4, 2011 Volume RG22 , Number 5 16

exchanges that employ a similar program under their respective rules. For each option class eligible for participation in the Short Term Option Series Program, the Exchange may open up to twenty Short Term Option Series for each expiration date in that class.

(2) – (5) No change. (e) No change. . . . Interpretations and Policies: .01 - .18 No change.

* * * * * Rule 24.9—Terms of Index Option Contracts RULE 24.9. (a) General.

(1) Exercise Prices. No change. (2) Expiration Months. No change.

(A) Short Term Option Series Program. Notwithstanding the preceding restriction, after an index option class has been approved for listing and trading on the Exchange, the Exchange may open for trading on any Thursday or Friday that is a business day (“Short Term Option Opening Date”) series of options on that class that expire on the Friday of the following business week that is a business day (“Short Term Option Expiration Date”). If the Exchange is not open for business on the respective Thursday or Friday, the Short Term Option Opening Date will be the first business day immediately prior to that respective Thursday or Friday. Similarly, if the Exchange is not open for business on the Friday of the following business week, the Short Term Option Expiration Date will be the first business day immediately prior to that Friday. Regarding Short Term Option Series:

(i) Classes. The Exchange may select up to [five] fifteen currently listed option classes on which Short Term Option Series may be opened on any Short Term Option Opening Date. In addition to the [five] fifteen-option class restriction, the Exchange also may list Short Term Option Series on any option classes that are selected by other securities exchanges that employ a similar program under their respective rules. For each index option class eligible for participation in the Short Term Option Series Program, the Exchange may open up to twenty Short Term Option Series on index options for each expiration date in that class.

(ii) to (iv) No change. (B) No change.

(3) – (5) No change. (b) – (e) No change. …Interpretations and Policies: .01 - .11 No change.

_________________________________________________________________________________ SR-CBOE-2011-013 Fees Schedule On February 1, 2011, the Exchange filed Rule Change File No. SR-CBOE-2011-013, which filing proposes to amend the Fees Schedule and Trading Permit Fee Circular to (i) clarify that the tier appointment fees will be assessed, as applicable, for open outcry transactions and not electronic transactions for those Market-Maker Trading Permit Holders that do not already have a tier appointment; (ii) establish a minimum open outcry contract level for assessment of a tier appointment fee to those Market-Maker Trading Permit Holders that do not maintain a tier appointment in VIX; and (iii) clarify that written notification to terminate a tier appointment should be provided to the

February 4, 2011 Volume RG22 , Number 5 17

February 4, 2011 Volume RG22 , Number 5 18

Market Quality Assurance & DPM Administration Department. Any questions regarding the rule change may be directed to Kerry Adler, Legal Division, at 312-786-8093. The rule filing is available at https://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2011-013.pdf. _________________________________________________________________________________ SR-CBOE-2011-014 Fees Schedule On February 1, 2011, the Exchange filed Rule Change File No. SR-CBOE-2011-014, which filing proposes to waive the PAR Official Fees for Trading Permit Holders that maintain a minimum of ten Floor Broker Trading Permits throughout a calendar month. Any questions regarding the rule change may be directed to Kerry Adler, Legal Division, at 312-786-8093. The rule filing is available at https://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2011-014.pdf. _________________________________________________________________________________ SR-CBOE-2011-015 Fees Schedule On February 1, 2011, the Exchange filed Rule Change File No. SR-CBOE-2011-015, which filing proposes to amend the Fees Schedule to extend the cap on the CFLEX Surcharge Fee to all orders. Any questions regarding the rule change may be directed to Jaime Galvan, Legal Division, at 312-786-7058. The rule filing is available at https://www.cboe.org/publish/RuleFilingsSEC/SR-CBOE-2011-015.pdf. _________________________________________________________________________________