Evidence on a Social Demand Theory of Corporate Social ... · We examine how local stakeholder...

55

1 Evidence on a Social Demand Theory of Corporate Social Responsibility Lixiong Guo † and Zhiyan Wang ‡ Culverhouse College of Business University of Alabama October 2018 ABSTRACT We examine how local stakeholder demand for CSR revealed by nonprofit organizations’ annual spending is associated with firms’ CSR policy and the relation between CSR and firm value. Using a novel data on nonprofit organizations in the U.S., we find that CSR ratings of firms vary positively with local nonprofit sector spending in their headquarters’ metropolitan statistical areas (MSAs) over time. This relation holds for both the overall CSR rating and CSR rating in each dimension. Our results are not driven by geographic or firm heterogeneity. Futher tests show that the association is unlikely to be driven by time-varying local omitted variables either. We also find that local nonprofit spending alters the relation between firm value and CSR in the positive direction, and CSR ratings of well-governed firms are more responsive to changes in local nonprofit spending than that of poorly-governed firms. Overall, our paper provides important evidence on a social demand-driven explanation of CSR which reconciles several mixed findings in the CSR literature. Our findings also suggest that the nonprofit sector plays a crucial role in revealing social demand on CSR and that shareholders benefit from responding to revealed social demand. Keywords: Nonprofit, Corporate Social Responsibility, Societal Demand, Firm Value, Institutional Impact JEL Classification: G30, G34, H40, M14 † Lixiong Guo is an Assistant Professor of Finance with the University of Alabama. Address: Culverhouse College of Commerce, University of Alabama, 222 Alston Hall, 361 Stadium Drive, Tuscaloosa, Alabama, 35487-0224. Office Phone: 205.348.2912. Email: [email protected]. ‡ Zhiyan Wang is a Ph.D. student of Finance at the University of Alabama. Email: [email protected]

Transcript of Evidence on a Social Demand Theory of Corporate Social ... · We examine how local stakeholder...

1

Evidence on a Social Demand Theory of Corporate Social Responsibility

Lixiong Guo† and Zhiyan Wang‡

Culverhouse College of Business

University of Alabama

October 2018

ABSTRACT

We examine how local stakeholder demand for CSR revealed by nonprofit organizations’

annual spending is associated with firms’ CSR policy and the relation between CSR and firm

value. Using a novel data on nonprofit organizations in the U.S., we find that CSR ratings of

firms vary positively with local nonprofit sector spending in their headquarters’ metropolitan

statistical areas (MSAs) over time. This relation holds for both the overall CSR rating and

CSR rating in each dimension. Our results are not driven by geographic or firm heterogeneity.

Futher tests show that the association is unlikely to be driven by time-varying local omitted

variables either. We also find that local nonprofit spending alters the relation between firm

value and CSR in the positive direction, and CSR ratings of well-governed firms are more

responsive to changes in local nonprofit spending than that of poorly-governed firms. Overall,

our paper provides important evidence on a social demand-driven explanation of CSR which

reconciles several mixed findings in the CSR literature. Our findings also suggest that the

nonprofit sector plays a crucial role in revealing social demand on CSR and that shareholders

benefit from responding to revealed social demand.

Keywords: Nonprofit, Corporate Social Responsibility, Societal Demand, Firm Value,

Institutional Impact

JEL Classification: G30, G34, H40, M14

† Lixiong Guo is an Assistant Professor of Finance with the University of Alabama. Address: Culverhouse College of Commerce,

University of Alabama, 222 Alston Hall, 361 Stadium Drive, Tuscaloosa, Alabama, 35487-0224. Office Phone: 205.348.2912.

Email: [email protected]. ‡ Zhiyan Wang is a Ph.D. student of Finance at the University of Alabama. Email: [email protected]

2

“The opinions and actions of International NGOs, Charities, Think Tanks and

Foundations are driving the CSR and sustainability agenda across the world.”

― Ipsos MORI

1. Introduction

Should companies have social responsibilities? The debate on this question has ebbed and

flowed over decades. Proponents of Friedman’s view assert that the only legitimate objective of

companies is to make profits for shareholders (e.g., Berle and Means, 1932; Friedman, 1970;

Sundaram and Inkpen, 2004). Yet, recent trend shows that businesses, especially large

corporations, are increasingly allocate significant portion of company resources to a variety of

sustainability3 , philanthropy4 , and corporate social initiatives5 . Many companies report their

corporate social responsibilities (CSR) engagements in their annual report and advertise them on

their corporate websites. Why do more and more companies voluntarily spend on stakeholder

interests? Do CSR activities add value to shareholders or are they simply a new form of managerial

private benefits? These are questions of intensive research and debate in the current CSR literature.

Several explanations are offered in the existing CSR literature. The “doing-well-by-doing-

good” view argues that firms engage in CSR to increase profitability and firm value (e.g. El Ghoul

et al., 2011; Albuquerque, Durnev and Koskinen, 2013; Flammer, 2015). The agency view argues

that CSR is a form of managerial private benefits. These two explanations have opposite value

3 The US spending on 29 sustainability initiatives will double to $60bn in 2014 from $28bn in 2010, according to a new

report from Verdantix. See at https://www.businesswire.com/news/home/20101006005109/en/ Verdantix-Forecasts-Sustainable-

Business-Spending-Double-60. 4 National Philanthropic Trust reports that US corporations donated 20.77 billion to charity – an increase of 8.0 % from

2016. See at https:// www.nptrust.org/philanthropic-resources/charitable-giving-statistics/. 5 According to the 2017 KPMG International Survey of Corporate Responsibility Reporting, nearly 93% of Global Fortune

250 companies and 75% of the largest 100 companies published CSR reports. See at https://assets.kpmg.com/

content/dam/kpmg/be/pdf/2017/kpmg-survey-of-corporate-responsibility-reporting-2017.pdf

3

implications for CSR. Other papers leave out the value question and explain CSR from legal

original or local culture norms. All these explanations have some shortcomings in explaining two

important observations about CSR. The first is that there is a recent rise in CSR engagements. The

second is that empirical evidence on the relation between CSR and firm value is at most mixed

(Margolis and Walsh, 2003). For example, the agency view is inconsistent with the time trend in

CSR because corporate governance is improving in the recent time periods. The “doing-well-by-

doing-good” view begs the question of what have changed so it is more valuable to engage in CSR

now than before. The legal original view obviously cannot explain the time trend in CSR because

firms’ legal origins in general do not change over time. The local norm view although can

potentially explain the time trend but they mainly focus on the impact on the supply of CSR. These

papers either do not give predictions on the value impact or provide inconclusive empirical

evidence on it.

In this paper, we provide a framework to understand CSR based on local demand for CSR.

Fundamentally, CSR is a “social good” that firms supply to stakeholders and thus the supply of

profit-maximizing CSR should essentially hinge on stakeholder demands. We argue and most

importantly provide evidence that local demand not only can explain cross-sectional and time-

series variations in CSR activities but also can reconcile the mixed evidence on the relation

between CSR and firm value. Since CSR activities consume corporate resources that could

otherwise be put into direct productive use, we expect that firms with an aim to maximize

shareholder value would vary their CSR engagements with local social demand. Similarly, the

relation between CSR and firm value also depends on local social demand. CSR initiatives are

more likely to add to firm value when the social demand for CSR is high and vice versa.

4

The key to our paper, this is also what distinguishes our paper from other papers, is how to

measure local social demand for CSR. Stakeholders’ demand on social issues are multidimensional

and diffused. We require a measure that aggregates diffused demand and also is most likely to be

felt and sensed by a firm’s decision makers. Binding to local society, firms are likely to seek and

acquire demand information revealed by local community and institutions, such as local nonprofits.

Local nonprofits can unite and reveal stakeholder demands on corporate social responsibility for

several reasons. First, the nonprofit sector is formed to serve the public interests (Hansmann, 1980)

and to advance social causes for population with broad interests. Therefore, their preferences and

demands are closely aligned with stakeholders. For instance, environment nonprofit prevents

environmental degradation for local community, employee nonprofit promotes welfare for

employees, consumer nonprofit protects the interests of customers, etc. Second, seeking to meet

various societal demands, the nonprofit sector unites groups with shared demands, publicize their

demands to the public, mobilizes all social constitutes, especially corporations, to engage in those

social causes. A 2015 report by Urban Institute showed that in 2013, US nonprofit sector spent

2.10 trillion to promote social causes. As a response in 2014, corporations donated 17.77 billion

to the nonprofit sector 6 and spent 60 billion on sustainability management 7 to meet societal

demands on CSR. Third, the nonprofit sector reveals demands on CSR separately for different

stakeholders, as CSR spans multiple categories that benefit different stakeholders.

Prior research suggests the importance of connections between local nonprofits and firms,

which facilitates the spread of information on both sides of CSR (Galaskiewicz, 1985; Marquis,

6 For the information on U.S. nonprofit sector, See https://www.urban.org/research/publication/

nonprofit-sector-brief-2015-public-charities-giving-and-volunteering 7 The US spending on 29 sustainability initiatives will double to $60bn in 2014 from $28bn in 2010, according to a new

report from Verdantix. See at https://www.businesswire.com/news/home/20101006005109/en/ Verdantix-Forecasts-Sustainable-

Business-Spending-Double-60.

5

Glynn and Davis, 2007), especially when firms have nonprofit-connected firm decision makers

(Ostrower, 1995), collaborative relationship (Wymer and Samu, 2003), partnership (Seitanidi and

Crane, 2009). Firms can also acquire demand-side information on CSR from nonprofit activities,

such as fundraising campaign, advocacy, and media coverage, and then incorporate these demand

information into CSR supply. Marquis, Glynn and Davis (2007) claim that local nonprofits serve

to put corporations directly in touch with social needs and thus the connectedness between local

nonprofits and corporations induces higher levels of corporate social actions. Similarly, Campbell

(2007) argue that the nonprofits deliver stakeholder demands directly to corporations by many

tactics (e.g., appealing to corporations, organizing demonstrations against corporations, and

mobilizing media campaigns).

Based on the previous work, we use local nonprofits spending as the proxy for local social

demand for CSR. Since nonprofit organizations play the role of aggregating stakeholder demands

and disseminating demand information for corporate social responsibility, their spending is a more

tangible measure of local social demand for CSR that can be relatively more easily sensed and felt

by local firm top executives than other local measures of social norm or prosocial attitude used in

existing studies.

Using a novel data on US nonprofit organizations, we find that firms’ annual overall CSR

ratings vary positively with annual spending of nonprofit organizations in the firms’ headquarter

metropolitan statistical area (MSA) 8 . When we further divide nonprofit organizations into

subgroups whose social causes best match a particular CSR dimension, we find that nonprofit

spending in a particular CSR dimension mainly affects firms’ CSR ratings in that dimension. In

8 The metropolitan statistical area hs been used as a unit of analysis to capture community-based geographical heterogeneity in

many existant studies (See Marquis, 2003; Stuart and Sorenson, 2003; Marquis, Glynn and Davis, 2007; Brown et al., 2008;

McGuire et al., 2012; Dougal, Parsons and Titman 2015; Cohen, Gurun and Malloy, 2017).

6

all our regressions, we control for MSA, industry and year fixed effects. Our results are also robust

to controlling for firm and year fixed effects. Hence, our findings are not driven by time-invariant

geographic, industry or firm differences. These findings provide strong support to our main

hypothesis that local social demand for CSR drives local firms’ CSR supply.

However, an important empirical challenge in interpreting this relation as evidence of

social demand drives changes in CSR supply remains because a time-varying omitted variable at

the MSA level could still drive our result. To overcome this concern, we take several approaches.

First, we group MSAs into CSAs (Combined Statistical Areas9) and control for CSA*Year fixed

effects. The reasoning is that neighbouring MSAs are likely to share similar social and economic

conditions, by controlling for CSA*Year fixed effects, we mitigate endogeneity concern over a

time-varying omitted variable that is related to local social and economics conditions. We find our

results remain significant after including the CSA*Year fixed effects. Second, we estimate an

instrumental variable regression. The instrument we choose is local nonprofit organizations’

investment income. It is reasonable to assume that nonprofit organizations hold diversified

portfolios of investments as sophisticated investors should do. Under this assumption, variations

in nonprofit organizations’ investment income should mostly be exogenous to changes in local

social and economic conditions and thus satisfy the exclusion condition of a valid instrument. On

the other hand, nonprofit spending is likely to be positively related to their spending. Our IV

regression results continue to show a statistically significant relation between local firms’ CSR

ratings and local nonprofit spending. Third, we break up MSAs into states and re-estimate our

models. Given that many MSAs spin multiple states, our approach could potentially break up the

9 Combined statistical areas (CSA) consist of two or more adjacent metropolitan and micropolitan statistical areas that have

substantial employment interchange. The metropolitan and micropolitan statistical areas that combine to create a CSA retain

separate identities within the larger CSA. See https://www.census.gov/geo/reference/webatlas/csa.html

7

chain between geographical omitted variables and nonprofit spending and firm’s CSR policy.

Lastly, we show that spending by nonprofit organizations on social causes related to a particular

CSR dimension mainly affects local firms’ CSR ratings in that dimension. For example, spending

by the environmental nonprofit group in a year is only positively assocaited with local firms’ CSR

performance in the environmental category in that year. It is difficult to reconcile this level of

precision in the relation between nonprofit spending and local firms’ CSR activities with an omittd

MSA level variable driving the relation we document. It is easier to conceive a local omitted

variable that would drive the overall level of nonprofit spending and local firms’ overall CSR

rating but obviously such a variable cannot explain our CSR subcategory results.

Our argument for the role of local social demand in affecting CSR also has implications

for the relation between CSR and firm value. In theory, meeting social demand can help increase

employee and customer satisfaction and build valuable social capital (Lins, Servaes and Tamayo,

2017). Hence, changes in firms’ CSR policy driven by the desire to meet stakeholder demand for

CSR are likely to indirectly benefit shareholders. To allow for the possibility that not all CSR

engagements are initiated to meet social demand, for example, some could be driven by managerial

preferences, we include both a firm’s CSR and its interaction with nonprofit spending in a

regression of the firm’s Tobin’s Q on explanatory variables. The coefficeint on CSR iteself is

negative and statistically significant, suggesting that CSR engagements that are not initiated to

meet social demand decrese firm value. However, the coefficeint on the interaction term is positive

and statistically significant, suggesting that high local demand as proxied by high local nonprofit

spending alters the negative relation between firm value and CSR in the positvie direction. In

unreported results, we find that a firm’s CSR rating is positively related to its Tobin’s Q in a

regression without the interaction of CSR and nonprofit spending. Our result shows that nonprofit

8

spending is an important variable that distinguishes good CSRs and bad CSRs from the

shareholders’ point of view. This result also suggests that social demand cannot explain all CSR

engagements in all firms. If CSR engagements during periods of high social demand are value

increasing, then we expect firms with better governance to be more likely to increase their CSR

rating during these periods. Consistent with this, we find that well-governed firms’ CSR policy is

more sensitive to local demand changes than that of poorly-governed firms even though the former

on average spend less on CSR than the latter.

Our paper provides novel and important evidence on a demand-side explanation of CSR

activities. Our findings suggest that firms’ CSR supply is partially driven by social demand

revealed by local nonprofits. Although not all CSR spending seems to create value for shareholders,

suggesting that some CSR activities are probably a form of managers’ private benefits of control,

local demand-induced CSR spending seems to benefit shareholders and well-governed firms are

more likely to choose to meet this demand as a way to maximize shareholder wealth.

In addition, we also provide important evidence on how stakeholder demand on CSR

subcategories revealed by local nonprofits drive firms CSR performance in those ratings. Prior

studies have not been able to explain why the same firm supply differently in different CSR

subcategory and adjust those subcategory ratings differently over time. For instance, why

democratic firms spend significantly more in environment, but not human rights, community and

so on (Di Giuli and Kostovetsky, 2014). Our detailed measure of nonprofit spending allows us to

link specific stakeholder demand to firms’ performance in the corresponding CSR subcategory.

Two recent studies also examine local determinants of CSR. Attig and Brockman (2017)

find that local prosocial attitude as proxied by the fraction of residents in the firm’s headquarter

state making charitable donations are positively associated with the CSR rating of firms

9

headquartered in that state. Jha and Cox (2015) find that altruism inclination in a firm’s headquarter

state is positively correlated with the firm’s CSR ratings. Since these papers do not control for

state fixed effects, the relation they document could be driven by omitted geographic differences

other than the main explanatory variable they try to proxy. Our paper is also related to Servaes and

Tamayo (2013) in that we both argue that the relation between CSR and firm value is conditional.

We also control for the proper fixed effects to address model misspecification issues in other

existing studies. However, Servaes and Tamayo (2013) use stakeholder awareness of firms’ CSR

engagements as the conditional variable and thus implicitly assume uniform demand for CSR. In

contrast, we conditional on local demand and provide evidence that demand for CSR is not uniform.

Lastly, this paper also complements the literature that examines social and economic

impacts of the nonprofit sector.

The remainder of this paper proceeds as follows. Section 2 discusses related literature and

institutional background. Section 3 describes the data, variables and empirical methods. Section 4

presents our main results, robustness tests, CSA time varying specification, state-level results, and

sub-category results. Section 5 shows details on nonprofit functions and effects. Section 6

discusses potential mechanisms on our main results. Section 7 concludes.

2. Related Literature and Institutional Background

2.1. Related Literature

With the rising attention of academics, business, and policymakers on corporate social

responsibility (Carroll, 2009), several fundamental questions of intense debates are that why

companies engage in corporate social responsibility and whether CSR engagements are in

shareholders’ interests.

10

Several explanations are offered in the existing CSR literature. The traditional view

(“doing-well-by-doing-good” view) argues that firms engage in CSR to increase profitability and

firm value (e.g. El Ghoul et al., 2011; Albuquerque, Durnev and Koskinen, 2013; Flammer, 2015).

The agency view argues that CSR is a reflection of managerial social preferences (Cronqvist and

Yu, 2017) or a form of managerial private benefits (Masulis and Reza, 2015). The normative

arguments leave out the value question and explain CSR from normative roots, such as legal origin

(Liang and Renneboog, 2017), social norms (Dyck et al., 2015) and prosocial attitudes (Attig and

Brockman, 2017). Although these explanations have some success in explaining CSR, they eschew

three important observations about CSR. The first is that there is a recent rise in CSR engagements.

The second is that empirical evidence on the relation between CSR and firm value is at most mixed

(Margolis and Walsh, 2003). The third is that CSR engagement levels differ among firms. For

example, the traditional view suffers from mixed evidence on the relation between CSR and firm

value. The agency view is inconsistent with the time trend in CSR because corporate governance

is improving recently. The legal origin view obviously cannot explain the time trend in CSR

because firms’ legal origins in general do not change over time. The local norm view although can

potentially explain the time trend but they mainly focus on the impact on the supply of CSR. These

papers either do not give predictions on the value impact or provide inconclusive empirical

evidence on it.

To investigate the rational and recent trend of CSR, we provide a framework to understand

CSR based on local stakeholder demand for CSR. We argue and most importantly provide

evidence that local stakeholder demand not only can explain cross-sectional and time-series

variations in CSR activities but also can reconcile the mixed evidence on the relation between CSR

and firm value. Since we study how local stakeholder demand proxied by local nonprofit spending

11

affect CSR and the relation between CSR and firm value, our study seem to be relevant to several

recent studies (e.g., Jha and Cox, 2015; Husted, Jamali and Saffar, 2016), especially Attig and

Brockman’s work (2017). However, our study differs in many ways.

First, they study how state-based norms affect CSR. Given that social norms evolve

incrementally, they find cross-states evidence. While our work studies how the nonprofit sector

affect corporations’ CSR policy through social demand channel. To separate institutional effects

from location-based factors, we control for MSA fixed effects in all our tests. Second, their results

neither have identifications on the relation, nor control for state fixed effects and state

fundamentals such as state GDP. We apply a series of plausible identification strategies to ensure

the direction going from nonprofit spending to CSR. Third, neither prosocial attitude nor social

norms have explicit explanations on CSR subcategories, while nonprofit spending has a consistent

and separate explanation on each category. Fourth, their results on firm value implications are self-

conflicting, while our results are consistent with conditional effect on firm value (Servaes and

Tamayo, 2013) that well explain the mixed findings in prior literature. Lastly, we investigate how

corporate governance react to stakeholder demand on CSR and the implication on the relation

between CSR and firm value.

2.2. Institutional Background

The nonprofit sector is formed to serve the public benefit other than the pursuit or

accumulation of profits for owners or members (Hansmann, 1980; Zimmer, 1993; Adelino,

Lewellen and Sundaram, 2015). It has long been documented that the nonprofit, as the third largest

sector in U.S. economy, plays a crucial role in the social and economic well-being of the United

States. A 2015 report by Urban Institute showed that in 2013, US nonprofit sector employed over

12

14.4 million people or 10.6 percent of total employment and contributed 905.9 billion or 5.4

percent of the total GDP to the economy. More importantly, the nonprofit sector spent a total of

2.10 trillion to provide public goods, advocate social causes, advance social welfare, and inspire

civic involvement. As a response, the general public of the U.S. donated 358.38 billion to the

nonprofit sector and volunteered 8.7 billion hours in the nonprofit sector in 201410. Meantime,

corporations donated 17.77 billion to the nonprofit sector and spent 60 billion on sustainability

management to advance a variety of environmental and social causes in line with the nonprofit

sector.

Given the amount of attention and money corporations give to social initiatives under such

a social context, it is natural to ask whether and how the nonprofit sector drives a firm’s CSR

policy. According to a 2014 IPSOS MORI global online survey, most respondents view that the

opinions of NGOs can directly shape how a company, and its activities, are perceived by the

broader stakeholder community and the public, shape how an organization’s sustainability strategy

is received and directly influence their wider corporate reputation11. Nonprofit organizations can

drive CSR through direct and indirect channels. The direct way is to impose pressure on

corporations to behave socially responsible. Campbell (2007) argue that “corporations will be

more likely to act in socially responsible ways if there are any private and independent nonprofit

in their environment who monitor their behaviors and, when necessary mobilize to change it.” The

indirect way is to influence corporations through primary stakeholders in local community.

Salamon et al. (2000) point out that nonprofit organizations potentially perform an expressive and

10 For the information on U.S. nonprofit sector, See https://www.urban.org/research/publication/

nonprofit-sector-brief-2015-public-charities-giving-and-volunteering 11 Ipsos MORI run a global online survey to ask adults their views on the relationship between large corporations and global

Non-Government Organizations. See https://www.ipsos.com/ipsos-mori/en-uk/delicate-relationship-between-worlds-biggest-

ngos-and-multinational-corporations

13

representational role for community constituents to express their interests and values. In line with

this representational role, both anecdotal evidence and empirical evidence show that nonprofit

organizations work on behalf of stakeholders and influence corporate social performance through

delivering stakeholder demands to corporations (e.g., Doh and Teegen, 2002; Vasi and King, 2012;

Helmig, Spraul and Ingenhoff, 2016).

3. Data and Methodology

To examine the effects of nonprofit organizations on local firms’ CSR policy, we construct

a data set that links nonprofit spending to their local firms’ CSR activities. In this section, we

describe our sample and outline our empirical methods and identification strategies.

3.1. CSR Data

Our sample consists of an unbalanced panel of the largest 3,000 publicly traded U.S.

companies, during the period 2003 – 2009. We start with CSR ratings over the period 2003 – 2009

from the MSCI ESG Database, previously known as the KLD STATS database. This database

contains annual ratings on 13 dimensions in the largest 3,000 publicly traded companies since

2003. Within each dimension, KLD provides a number of strength indicators and concern

indicators. If a firm has particular strength or concern in the area represented by the indicator, the

strength or concern indicator gets a value of one and zero otherwise. We only count community,

diversity, employee relations, environment, human rights, and product as components of CSR, as

other dimensions are widely considered to be outside the domain of CSR (Di Giuli and

Kostovetsky, 2014; Cronqvist and Yu, 2017). The six dimensions totally contain 56 different

indicators. For each firm-year observation in our sample, we calculate CSR raw score for each

dimension by subtracting total concerns from total strengths within each dimension, then we sum

14

up CSR raw scores across six dimensions to yield the aggregate CSR raw score. We further

standardize CSR raw scores to CSR indexes ranging from -1 to 1 for each dimension and from -6

to 6 for total six dimensions. Accordingly, a higher CSR index indicates a higher performance in

CSR and vice versa.

3.2. Nonprofit Data

Nonprofit organizations refer to 501(c) organizations or nongovernmental organizations.

They are formed to serve the public benefit other than the pursuit or accumulation of profits for

owners or members (Hansmann, 1980; Zimmer, 1993; Adelino, Lewellen and Sundaram, 2015).

Therefore, we utilize annual disclosure information required by Internal Revenue Service on all

U.S. 501(c) organizations from National Center for Charitable Statistics Database. According

to Title 26 of the United States Code § 501, there are 29 types of 501(c) organizations. For the

purpose of this study, we only include 501(c)(3) organizations and 501(c)(4) organizations, which

are public charity/interest organizations and social advocacy/welfare organizations, respectively.

The reason that we include these two types of organizations is that they both aim to serve

the general public through similar approaches such as public education, awareness, advocacy,

lobbying and so on. The only difference between the two is that 501(c)(3) organizations are limited

by IRS to political donation, but 501(c)(4) organizations are not. Considering political donation is

outside scope of nonprofit impact on corporations, we view the two types of organizations as the

same entity to influence corporations concerning corporate social performance.

The NCCS database was produced annually since 1989 and combine descriptive

information and financial variables of all 501(c) organizations with more than $25,000 in gross

receipts. All 501(c) organizations with less than $25,000 in gross receipts are not required to file

15

reports to IRS due to their small volume, short longevity, and negligible impact. As a result, our

sample consists of all 501(c)(3) and 501(c)(4) organizations that have more than $25,000 annual

income and operate on a regular basis.

To investigate whether and how these nonprofit groups affect the sub-category ratings of

corporate social responsibility, we match each sub-category rating to the corresponding nonprofit

group. To do so, first, we primarily follow National Taxonomy of Exempt Entities Core Codes

(NTTE-CC) system12 commonly used by IRS, NCSS and academic papers (e.g., Kelly and Lewis,

2009) to classify all 501(c)(3) and 501(c)(4) organizations into nonprofit subgroups. Second, since

NTEE-CC system doesn’t specify employee-related groups, we complement our procedures by

searching nonprofit organization’s name with a list of keywords.

Category “Community” comprises of two aspects of corporate socioeconomic performance.

The first is corporate donations to the nonprofit sector such as general cash giving, innovative

giving programs and other giving activities, which is influenced by active philanthropy and

volunteer nonprofit group. The second is the community economic impact, which is related to the

community development group. Thus, we include “Philanthropy and Volunteering” group (NTEE-

T) and “Community Improvement” group (NTEE-S). Category “Environment” contains a bunch

of environment externalities indicators such as pollution, recycling, and waste, so we use the entire

“Environment” group (NTEE-C), which includes pollution control subgroup, clean energy

subgroup and other environment protection subgroups. Category “Human Rights” covers a number

of human rights compliance indicators inside and outside the United States. As a result, we include

both “International Human Rights” group (NTEE-Q70) and “Civil Rights” group (NTEE-R).

12 For the information on NTEE system, See at http://nccs.urban.org/classification/national-taxonomy-exempt-entities

16

Category “Product” consists of two major aspects of the product. The first is a firm’s

compliance with industrial standards, including marketing/contracting compliance, marketplace

trust and other compliances, which largely hinge on industry associations and business leagues.

The second is product issues such as product quality, safety, fraud and so on, which is directly

related to consumer interests. Based on these two aspects of product category, we include

“Business and Industry” group (NTEE-S40), which contain all business industry-related nonprofit

organizations such as chambers of commerce, business leagues, industry association and so on.

We also include “Consumer Protection” group (NTEE-W90), which include all kinds of consumer

protection organizations such as consumer watch, consumer union, etc.

Category “Diversity” gauges a firm’s social actions in recruitment, employee

promotion/benefits and supply chain to address equality rights of four population groups: women,

minority, disabled and LGBTQ. Corporations should have more awareness and demand pressure

if they reside in a region with more nonprofit organizations that advocate those equality rights. We

thus include all women groups, minority groups, disabled groups and LGBTQ groups in human

service (NTEE-P), international human rights (NTEE-Q), and civil rights (NTEE- R).

Category “Employee” includes a series of employee welfare indicators such as profit

sharing, retirement benefits, health and safety improvement and so forth. It is well-documented

that labor unions (commonly known as 501(c)(5) organizations) have longstanding effects on firms

concerning employee rights and benefits (e.g. Freeman, 1981, 1982, 1984; Buchmueller, Dinardo

and Valletta, 2002; Budd and McCall, 2004). Distinguishing from the literature on labor union,

this paper studies the effects of public charity (501(c)(3)) and advocacy (501(c)(4)) nonprofit on

local firms’ employee benefits performance through channels like public awareness, education,

advocacy and other community-wide impacts. Given that there is no classified employee group in

17

NTEE-CC system, we apply keyword searching methods, which have been used in many studies

of finance literature (e.g. Ahern and Sosyura, 2015; Hwang and Kim, 2017). We construct a list of

keywords indicating employee-related public charity and advocacy organizations as follows:

“employee”, “labor”, “laborer”, “worker”, “work”, “working” and “workplace” compounding

with “right”, “benefit”, “welfare”, “justice”, “assistance”, and “alliance”. To further provide more

details on our sample nonprofit organizations, we sort our sample nonprofit organizations in each

category by total spending and list the top 10 organizations in Table 1.

[Insert TABLE 1 Here]

Using location identifiers of each nonprofit organization, we classify all sample nonprofit

organizations both at the state level and at metropolitan statistical area (MSA) level. We then

aggregate all nonprofit financial data at MSA level and State level to construct a measure of

nonprofit group impact in each MSA and State. More specifically, we use aggregated total expense,

program expense, fundraising expense, special-events expense, and legislative expense of a local

nonprofit group to proxy the group’s impact on the corresponding category of CSR in the local

area.

3.3. Control Variables

Using CUSIP and Ticker identifiers, we match firm-level CSR data with other firm-level

accounting data that is from Compustat. We obtain zip code identifier of firm headquarters from

Compustat and then associate them with MSA identifier13 . CEO characteristics data is from

13 United States Department of Labor provides the link files between geographical identifiers, like ZIP and MSA. See at

https://www.dol.gov/owcp/regs/feeschedule/fee/fee11/fs11_gpci_by_msa-ZIP.xls

18

Execucomp, and board characteristics are from ISS. Annual estimates of GDP at both MSA level

and state level are from Federal Reserve Economic Data (FRED).

3.4. Descriptive Statistics and Univariate Tests

After merging firm-level CSR data, local nonprofit data and control variables, we obtain a

sample of 4196 unique firms located in 282 metropolitan statistical areas and 51 states. Panel A of

Table 2 presents summary statistics on our nonprofit variables, CSR variables, firm characteristics

and other control variables. The average CSR-related nonprofit groups spend $ 1.43 billion across

MSAs per year and $ 2.5 billion across states per year to advance social causes in our sample.

MSAs in our sample have a median GDP growth rate of 2 percent per year while states in our

sample have a median GDP growth rate of 4 percent per year. Our CSR score has a mean of -0.187

and a median of -0.2 while subcategory CSR scores are centered at zero and exhibit less variation.

Panel B of Table 2 shows results of univariate analysis of CSR score. We split our sample

into subsamples by our independent variables: state-level nonprofit total expense and MSA-level

nonprofit total expense. The t-statistics for differences indicate that firms headquartered in areas

where CSR-related nonprofit groups spending is above the sample median have higher CSR scores

than firms located in areas where CSR-related nonprofit groups spending is below the sample

median. These findings provide preliminary support to our main hypothesis.

[Insert TABLE 2 Here]

3.5. Empirical Strategies

19

To examine the effects of nonprofit organizations on local firms, we estimate a baseline

model in which we regress firms’ CSR scores on their local nonprofit group spending, along with

firm-level controls, metropolitan statistical area level controls, and several fixed effects. The model

can be expressed as follows:

𝐶𝑆𝑅𝑖,𝑙,𝑘,𝑡 = 𝛼 + 𝛽1𝑁𝑜𝑛𝑝𝑟𝑜𝑓𝑖𝑡 𝑆𝑝𝑒𝑛𝑑𝑖𝑛𝑔𝑙,𝑡 + 𝛽2𝐹𝑖,𝑡 + 𝛽3𝐿𝑙,𝑡 + 𝛾𝑙 + 𝛿𝑡 + 𝜃𝑘 + 𝜖𝑖,𝑙,𝑘,𝑡 (1)

Where the subscripts i, l, k and t refer to firm, MSA, industry and time, respectively; CSR

score is a firm-level corporate social responsibility measure; Nonprofit spending is MSA-level

aggregated nonprofit spending. F is a vector of firm characteristics. L includes a vector of MSA

variables; , , and denote MSA, year and 2-digit SIC industry fixed effects, respectively, and

refers to error term. Heteroskedasticity-robust errors are clustered by firm and MSA.

The issue of endogeneity is a major concern for most studies in CSR literature. As we study

the real effects of nonprofit organizations on local firms, our analysis is also subjected to potential

omitted variables, like CSR policy of local peers (Cao, Liang and Zhan, 2015) and other MSA-

level characteristics. We conduct a series of tests to alleviate these concerns.

First, although we cannot include MAS*Year fixed effects because they will take away all

the variations, we group MSAs into different geographic regions, which we call Combined

Statistical Areas (CSAs), and allow each region to have its own time trend by including CSA*Year

fixed effects. If our results are driven by an omitted variable at the CSA level, then including

CSA*Year fixed effects should render our main results insignificant.

Second, we take an instrumental variable (IV) approach, using nonprofit investment

income as an exogenous variation for nonprofit spending. Independent of governments and other

institutions, most nonprofit organizations are self-governed, therefore, their spending primarily

depends on their incomes, that is, investment income, a major component of individual nonprofit

revenue, are very likely to affect nonprofit spending. We find that our IV is significantly positively

20

related to nonprofit spending and pass the Cragg-Donald F-test for weak instrument (Cragg and

Donald, 1993). The exclusion condition for a valid IV requires that nonprofit investment income

not affect local firms’ CSR policy in our sample, other than through nonprofit spending and other

control variables in our regression. This condition is likely to be met because nonprofit investment

income, assuming they hold diversified portfolios as most sophisticated investors do, to a great

extent, should mainly vary with the broader economy and thus be exogenous to local factors.

Using the IV, we estimate 2SLS regressions as follows:

In the first stage:

𝑁𝑜𝑛𝑝𝑟𝑜𝑓𝑖𝑡 𝑆𝑝𝑒𝑛𝑑𝑖𝑛𝑔𝑙,𝑡 = 𝛼 + 𝛽1𝑁𝑜𝑛𝑝𝑟𝑜𝑓𝑖𝑡 𝐼𝑛𝑐𝑜𝑚𝑒𝑙,𝑡 + 𝛽2𝐹𝑖,𝑡 + 𝛽3𝐿𝑙,𝑡 + 𝛾𝑙 + 𝛿𝑡 + 𝜃𝑘 + 𝜖𝑖,𝑙,𝑘,𝑡 (2)

In the second stage:

𝐶𝑆𝑅𝑖,𝑙,𝑘,𝑡 = 𝛼 + 𝛽1𝑁𝑜𝑛𝑝𝑟𝑜𝑓𝑖𝑡 𝑆𝑝𝑒𝑛𝑑𝑖𝑛𝑔𝑙,𝑡̂ + 𝛽2𝐹𝑖,𝑡 + 𝛽3𝐿𝑙,𝑡 + 𝛾𝑙 + 𝛿𝑡 + 𝜃𝑘 + 𝜖𝑖,𝑙,𝑘,𝑡 (3)

Third, we aggregate nonprofit spending to the state level and re-estimate the relation

between nonprofit spending and CSR at the state level. Since many MSAs span multiple states, if

a MSA level omitted variable drive our results, then we expect our results be weakened when the

aggregation to state level breaks up MSAs and combines parts of different MSAs into one

observation.

Lastly, we break local nonprofit spending into sub-spending that correspond to the KLD

CSR rating subcategories based on nonprofit organizations’ mission objectives and test whether

nonprofit spending in a particular CSR category mainly affect local firms’ CSR ratings in that

category. For example, whether environmental nonprofit spending only affects environmental

performance of local firms, rather than other aspects of corporate social performance. The idea is

that if some omitted time-varying local variable drives the general level of nonprofit spending and

CSR in a MSA, then we should find nonprofit spending in any CSR category to be significantly

related to CSR in other categories. If this is not true, then to explain our results by omitted variables,

21

the omitted variable has to only affect one CSR category but not others and each MSA needs to

have several such omitted variables that are independent of each other. Obviously, a very

complicated theory is needed to rationalize the existence of these omitted variables, which casts

seriously doubt on the omitted variable explanation.

4. Results

In this section, we present our results on the effects of nonprofit spending on local firms’

CSR policy as well as other firm-level and MSA-level characteristics, and we employ several

identification strategies to confirm the causality of the effects.

4.1. Main Results

Panel A of Table 3 reports the results from OLS regressions of local firms’ CSR policy on

CSR-related nonprofit expense. Column (1) performs a univariate regression. In column (2), we

control for firm size, cash flow, firm leverage and payout policy as proven to be important

determinants of firm’s CSR policy in prior studies (Udayasankar, 2008; Kubik, Scheinkman and

Hong, 2011; Cheung, Hu and Schwiebert, 2016); In column (3), we add return on asset and market

to book value to capture firm value and profitability characteristics, which could account for

economic incentives of CSR policy. In column (4), we add MSA level GDP growth to capture

MSA economic fundamental. In column (5), we control for firm fixed effects and year fixed effects

to address firm heterogeneity. Most specifications include Fama-French 49 industry fixed effects,

metropolitan statistical areas fixed effects and year fixed effects.

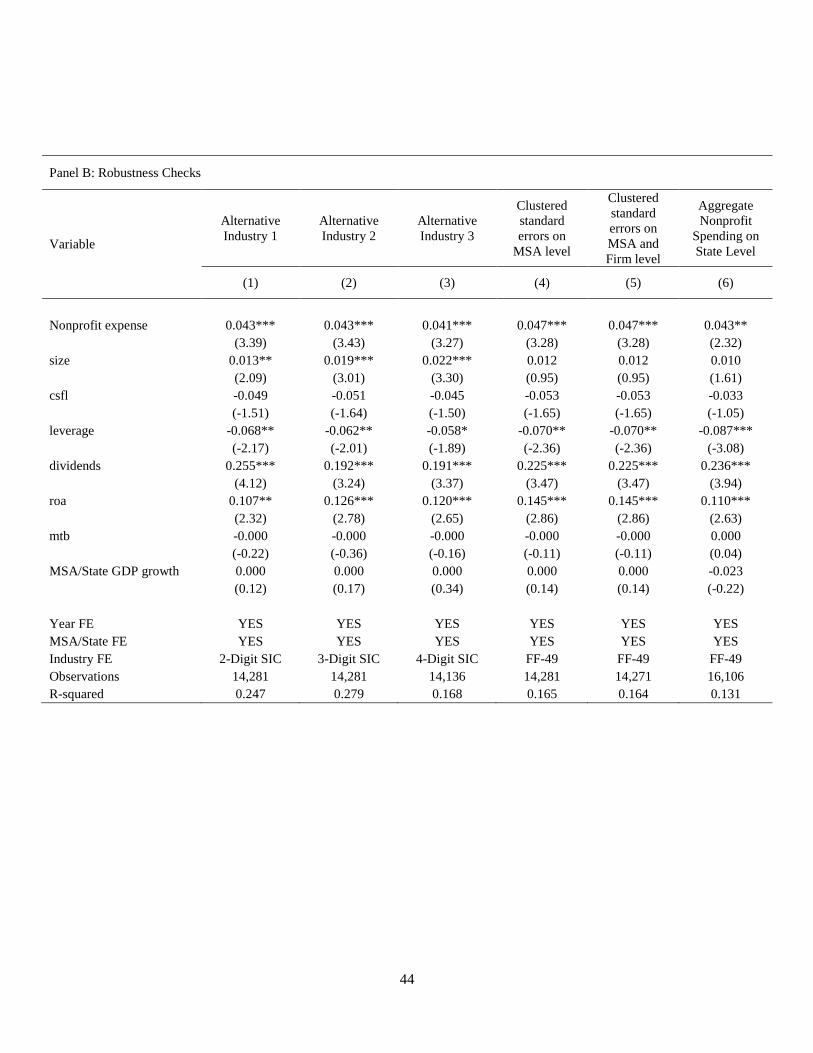

In Panel B of Table 3, we estimate OLS models with alternative industry definitions

including 2-digit SIC industry classification in Column (1), 3-digit SIC industry classification in

22

Column (2), and 4-digit SIC industry classification in Column (3), with clustering standard errors

on MSA level in Column (4), and with double clustering standard errors on MSA level and firm

level in Column (5), and aggregating nonprofit spending on state level in column (6). All

specifications control for firm characteristics, MSA-level characteristics, industry fixed effects,

MSA fixed effects, and year fixed effects. Panel C shows the results from OLS regressions

controlling CSA*Year Fixed effects. Panel D of Table 3 estimates 2SLS IV regression using

nonprofit investment income as an instrument variable for nonprofit spending and report the results

of the first stage in column (1) and the results of the second stage in column (2).

[Insert TABLE 3 Here]

Two notes stand out in our baseline results. First, all coefficient estimates of nonprofit

expense on CSR score in all specifications are positive and statistically significant, ranging from

0.042 to 0.047. This effect is three times larger than firm size effect, that is, 1% increase in

nonprofit expense leads to an approximate 12 % standard deviation increase in CSR score. Second,

our models control for time fixed effects, MSA fixed effects, firm fixed effects, alternative industry

definitions and standard errors clustering and obtain consistent positive relation between local

nonprofit spending and CSR. This suggests that our results are not driven by MSA level, industry

level and firm level heterogeneity, thereby strongly supporting our hypothesis that local nonprofit

spending drives CSR. To further alleviate endogeneity concerns, we take several the following

actions.

4.2. Controlling Combined Statistical Areas Time Trend

23

Considering that our results could be driven by some time-varying omitted variables, we

group MSAs into CSAs (Combined Statistical Areas) and control for CSA*Year fixed effects. The

reasoning is that neighbouring MSAs are likely to share similar social and economic conditions,

by controlling for CSA*Year fixed effects, we mitigate endogeneity concern over a time-varying

omitted variable that is related to local social and economics conditions. In Panel C, we control for

year and CSA fixed effects, CSA*year fixed effects and CSR*year fixed effects and industry fixed

effects. The relation between local nonprofit spending and CSR is still positively significant, while

the coefficient estimates decrease from 0.047 (column 4 of Panel A) to 0.009 (column 2 of Panel

C). The decrease of the estimates is a result of extracting large amount of nonprofit spending

variation. In short, after controlling for time-varying fixed effects, our results are still consistent

with our hypothesis that local nonprofit spending drives CSR. This suggests that our results are

not driven by some MSA-level time-varying omitted variables.

4.3. IV Estimation Results

In Panel D, we take an instrumental variable (IV) approach, using nonprofit investment

income as an exogenous variation for nonprofit spending. For the relevance condition, nonprofit

spending is likely to be positively related to their spending. In column 1 of Panel D, we find that

the Cragg-Donald F-tests statistics is 668.866, which reject the null hypothesis of weak instruments

and suggest that our IV is strongly correlated with our endogenous variable. On the other hand,

although there is no test for exclusion condition, it is reasonable to assume that nonprofit

organizations hold diversified portfolios of investments as sophisticated investors should do.

Under this assumption, variations in nonprofit organizations’ investment income should mostly be

exogenous to changes in local social and economic conditions and thus satisfy the exclusion

24

condition of a valid instrument. In column 2 of Panel D reports a positive association between

local nonprofit spending and CSR with a coefficient estimate of 0.066, which is consistent with

our baseline OLS result with a coefficient estimate of 0.047 (column 4 of Panel A). These results

further identify the relation is going from local nonprofit spending to CSR.

4.4. State Level Results

Given the fact that many MSAs cross multiple states, we are able to cross-verify the results

on MSA level with the results on state level. The idea is that if our results are caused by some

MSA level omitted variables, then we are unlikely to obtain the consistent results on state level.

In column (6) of Panel B, the relation between state-level nonprofit spending and CSR is positive

and statistically significant and the coefficient estimate of state-level nonprofit expense is 0.043.

These results are consistent with our predictions and mitigates concerns that our results are driven

by omitted variables at a given geographical level.

4.5. CSR Sub-Category Results

Corporate social responsibility spans many aspects of corporate environmental/social

performance, but most nonprofit organizations specialize in one type of social cause. Therefore,

presumably, a specific type of nonprofit organizations should only affect the corresponding aspect

of CSR. In this section, we exploit our detailed nonprofit organization data and test this hypothesis.

In Table 4, we estimate baseline specifications by replacing the dependent variable “CSR score”

with six sub-dimension scores and independent variable “nonprofit expense” with six sub-group

nonprofit spending, respectively.

25

[Insert TABLE 4 Here]

Table 4 reports the results from OLS regressions of separate effects of nonprofit expense

on subcategories of CSR. From column (1) to column (6), the dependent variables are community

score, diversity score, employee relation score, environment score, human rights score and product

score, respectively. It is worth noting that a specific nonprofit group only has positive and

statistically significant effect on the corresponding ratings of CSR. For example, community-

related nonprofit group only has positive and statistically significant effect on community score of

CSR. This effect is also larger than firm size effect, that is, a 1% increase in community-related

nonprofit spending leads to an 12% standard deviation increase in community index. The

explanation is intuitive that community-related nonprofit group, like Gifts in Kind International,

Silicon Valley Community Foundation and others, is a major advocate of social philanthropy and

community involvement, and it can stimulate corporate community engagement through activities

such as advocacy, fundraising campaign, partnership, etc.

Similarly, employee-related nonprofit group only affects employ relation score of KLD

CSR. Distinguishing from the well-documented effects of labor unions (commonly known as

501(c)(5) organizations) on employers’ stakeholder engagement (e.g. Freeman, 1981, 1982, 1984;

Buchmueller, Dinardo and Valletta, 2002; Budd and McCall, 2004), this effect captures how

501(c)(3) and 501(c)(4) organizations shape community-wide expectations, isomorphism and

pressure (Marquis, Glynn and Davis, 2007) on local firms’ employee welfare through a variety of

advocacy activities. The similar results are found on separate effects of nonprofit expense on

diversity performance, environment preservation, human rights protection and product quality.

26

Taken together, all our main results are consistent with the hypothesis that local firms’ CSR

policy is partially driven by local nonprofit spending, rather than geographical, industry, firm

heterogeneity and other omitted variables.

5. Nonprofit Functions and Effects

5.1. Nonprofit Sub-Spending Results

So far, we have shown that the nonprofit sector can affect local firms’ CSR policy, but

through which social functions are still not clear. The nonprofit sector advances social causes,

shapes societal preferences and reveals social demand on CSR through a variety of social activities

such as program/service, education, advocacy, campaigns, lobbying, and litigation and so on. To

provide evidence on these nonprofit sub-expense effects, we split nonprofit total expense into

several parts. Specifically, we use special-event expense and fundraising expense to proxy

“advocacy effect”, since both special-events and fundraising campaigns serve the same purpose of

improving public awareness and inducing public support as advocacy usually is defined. We use

program expense to represent “service and education effect”. We finally use legislative expense to

proxy “lobbying effect”.

[Insert TABLE 5 Here]

Panel A of Table 5 shows the results from OLS regressions of CSR score on different

expense proxies. All sub-expenses have statistically significant and positive effects on CSR.

Notably, advocacy (fundraising and special-events) drives the main part of nonprofit effects, with

27

program service effect and lobbying effect at the second places. This finding is consistent with

Salamon, Hems and Chinnock's work (2000), which claims that among all functions of the

nonprofit sector, few are more critical than advocacy to represent alternative perspectives and press

them on public and private decision makers. More importantly, this advocacy effect suggests that

local nonprofit organizations can affect CSR by increasing public awareness, affecting societal

preferences and revealing social demand. In addition, political expense has no effect on CSR,

which is not surprising because political expense is used for political campaigns, not to advance

social causes and reveal social demand. This exactly supports our conjecture that local nonprofit

affect CSR through social preferences and demand channel.

5.2. The Realization of Nonprofit Effects

In our main tests, we use the contemporaneous spending by nonprofit organizations to

examine its effect on local firms’ CSR performance. We essentially assume that nonprofit

spending has an immediate effect on firms. However, in some cases, it may take the firms some

time implement changes in their CSR policy. In Panel B of Table 5, we estimate the relation

between nonprofit spending and local firms’ CSR performance over different lags. In column (5),

the point estimate of nonprofit expense from OLS regressions is 0.044 in the current year and

attenuates to 0.023 in the following year. The results are consistent with prior studies that some

CSR ratings are flexible to adjust while some are not. For example, ratings in community

involvement, employee welfare and human rights can be adjusted immediately when firms face an

increase of demand pressure. However, ratings in environment may need more time to adjust when

firms need to upgrade or replace equipment, production line and so on.

28

6. Channels

6.1. Revealed social demand for CSR

Local nonprofit organizations can arouse societal awareness and preferences on social

causes, likely revealing social demand for CSR. Meeting such social demand could bring indirect

benefits to firms and hence enhances firm value. To test this channel, we interact nonprofit

spending and firm’s CSR performance and see whether adjusting CSR to the variation of nonprofit

spending has positive effects on firm value, measured by Tobin’s q.

[Insert TABLE 6 Here]

Our results are reported in Table 6. Two results are worth looking at. First, we find a

significant and negative relation between CSR ratings and firm performance, measured by Tobin’s

q, Industry-adjusted Tobin's q and MSA-adjusted Tobin's q. Our results show that CSR on average

is costly and hurts firm value at the expense of shareholders, but when social demand on CSR

increases, responding this call enhances firm performance, which is consistent with the view that

CSR enhances firm value only under certain conditions in several recent studies (e.g., Servaes and

Tamayo, 2013; Lins, Servaes and Tamayo, 2017). The effect of nonprofit spending on the CSR-

value relation is also economically significant. In column (1), for firms located in MSAs with

nonprofit spending 15.815 (1% quantile of the distribution), increasing CSR by one standard

deviation (0.38) leads to a decrease of 0.02 in Tobin’s Q. For firms located in MSAs with nonprofit

spending 19.967 (the median of the distribution), increasing CSR by one standard deviation (0.38)

leads to an increase of 0.07 in Tobin’s Q. The overall difference is 0.09, which is substantial given

the mean of Tobin’s Q is 2.06.

29

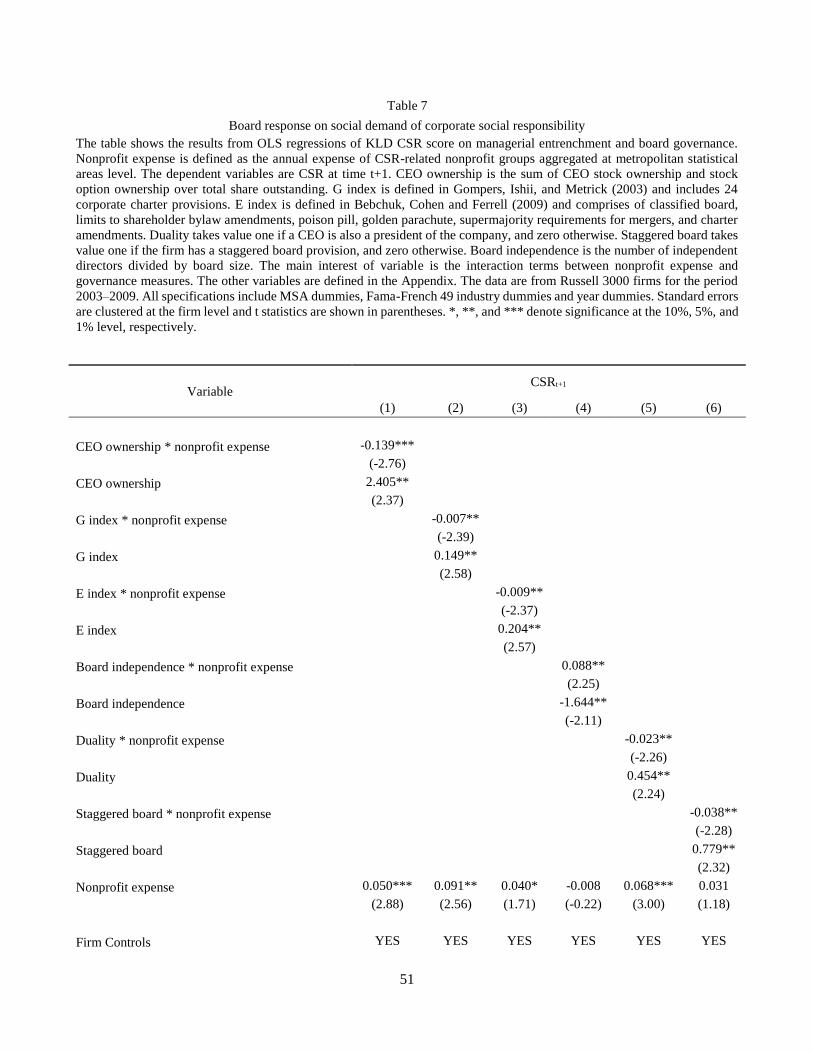

6.2 Governance on institutional impact for CSR

Given the significantly economic effects of nonprofit expense on the relation between CSR

and firm value, it is crucial to see what kind of companies are responsive to this institutional call

on CSR. Previous literature provides some conflicting views on the relation between corporate

governance and CSR. For example, Masulis and Reza (2015) argue that corporate philanthropy is

a result of weak governance and thus is an agency problem. On the contrary, Ferrell, Liang and

Renneboog (2016) show that well governed firms engage more in CSR. To join this conversation,

we employ a number of entrenchment and governance indices and investigate whether well-

governed firms are more responsive to CSR call.

Our results are reported in Table 7. We include CEO ownership and CEO duality as

measures of CEO entrenchment and contain G-index, E-index, staggered board, board

independence as measures of board governance. Two important points stand out. First, the

significant coefficients on these indices indicate that better governed and less entrenched firms

invest significantly less in CSR. For example, higher CEO ownership, dual CEO, higher G-index,

higher E-index, staggered board, lower board independence leads to higher engagement of CSR.

Second, the interaction between governance measures and nonprofit expense indicate that when

face an increase in institutional pressure on CSR, better-governed firms increase engagement in

CSR. The magnitudes of these joint effects are large. For example, based on model (3), for firms

in MSAs with nonprofit spending 15.815 (1% quantile of the distribution), increasing E-index by

one standard deviation (1.094) on average leads to an increase in 0.06 in CSR score. For firms in

MSAs with nonprofit spending 19.967 (the median of the distribution), increasing E-index by one

30

standard deviation (1.094) on average leads to an increase of 0.02 in CSR score. The overall

difference is 0.04 and this is relatively large given the mean of CSR is -0.187.

These results are particularly consistent with the relations between CSR and firm value in

table 6. That is, in general, in line with shareholder interests, better-governed firms invest less in

CSR because CSR alone decreases firm value. However, when facing an increase in social demand

on CSR, better-governed firms are more responsive to meet this call given investing CSR adds

value to firm performance. Overall, our results indicate that CSR, as a public good, is provided by

private sector (corporations) through a financially strategic mechanism, which is based on varying

social demand on CSR, measure by nonprofit spending. Our findings explain the “agency view”

(e.g., Cheng, Hong and Shue, 2013; Masulis and Reza, 2015) that poorly-governed firms on

average invest more in CSR. Also, it provides new evidence on the “good-governed view” (Ferrell,

Liang and Renneboog, 2016), showing that better-governed firms engage CSR under certain

conditions.

6.3. Managerial Social Preferences on CSR

A number of recent studies show that CEOs influenced by personal experience in social

life formalize particular preferences that possibly affect corporate outcomes. For example, CEOs

imprint personal leverage preference on the firms they manage (Cronqvist, Makhija and Yonker,

2012), pilot CEOs employ risky corporate policy (Cain and McKeon, 2016) and enhance

innovation (Sunder, Sunder and Zhang, 2017), military CEOs manage their firms with better ethics

(Benmelech and Frydman, 2015), CEOs shaped by their daughters engage more in corporate social

responsibility (Cronqvist and Yu, 2017) and so on. Residing in an area with high nonprofit impact,

managers are exposed more to civic life, obtain more education on social causes, face more

31

demand on social initiatives, and therefore are more likely to formalize strong social preference in

their utility functions. On the other hand, under the same community isomorphism (Marquis,

Glynn and Davis, 2007), important corporate insiders, such as employees, creditors, investors, and

customers are very likely to share the similar views and demand on CSR, and thus managers are

likely to face lower resistance and maybe greater support for CSR spending when local nonprofit

organizations are pushing for more social changes.

7. Conclusion

In this paper, we test how local demand for CSR revealed by local nonprofit organizations’

spending drives a firm’s CSR policy and its effect on shareholder wealth. Using nonprofit

organization data in the U.S. and KLD CSR data, we find local demand for CSR can explain the

time-series variations in firms’ CSR ratings overtime with each MSA area and reconcile the mixed

findings on the relation between CSR and firm performance. Specifically, we find that CSR ratings

of firms headquartered in a MSA vary positively with local nonprofit organizations’ spending. The

results hold for both the overall CSR ratings and CSR ratings by subcategory. Our results are

robust to controlling for year, MSA industry or firm fixed effects and various time-varying firm

and MSA characteristics. We also control for CSA*year fixed effects and use nonprofit investment

income as an IV for nonprofit spending confirms the relation between nonprofit spending and CSR

goes from nonprofit spending to CSR. Additional tests for addressing the endogeneity concern

also confirm the causal relation. We further find that increases in firm CSR ratings with local

nonprofit spending are positively related to firm value. Well-governed firms are more responsive

to local demand than poorly-governed firms in their CSR policy. Our results suggest that local

social demand for CSR revealed by local nonprofit organizations is an important determinant of a

32

firm’ CSR policy. Not all CSR spending increases firm value, only those that are done to meet

stakeholders’ demand do. Our paper provides important empirical evidence that is consistent with

a body of prior theoretical studies (e.g., McWilliams and Siegel, 2001; Campbell, 2007; Marquis,

Glynn and Davis, 2007; Benabou and Tirole, 2010), suggesting that local nonprofit sector plays a

crucial role in increasing societal awareness, shaping societal preferences and revealing social

demand on corporate social responsibility.

33

References

Adelino, M., Lewellen, K. and Sundaram, A. (2015) ‘Investment Decisions of Nonprofit Firms:

Evidence from Hospitals’, The Journal of Finance. Wiley/Blackwell (10.1111), 70(4), pp. 1583–

1628. doi: 10.1111/jofi.12234.

Ahern, K. R. and Sosyura, D. (2015) ‘Rumor Has It: Sensationalism in Financial Media’, The

Review of Financial Studies. Oxford University Press, 28(7), pp. 2050–2093. doi:

10.1093/rfs/hhv006.

Albuquerque, R. A., Durnev, A. and Koskinen, Y. (2013) ‘Corporate Social Responsibility and

Firm Risk: Theory and Empirical Evidence’. Available at:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2291334 (Accessed: 23 June 2018).

Attig, N. and Brockman, P. (2017) ‘The Local Roots of Corporate Social Responsibility’,

Journal of Business Ethics. Springer Netherlands, 142(3), pp. 479–496. doi: 10.1007/s10551-

015-2757-3.

Benabou, R. and Tirole, J. (2010) ‘Individual and corporate social responsibility’, Economica.

doi: 10.1111/j.1468-0335.2009.00843.x.

Benmelech, E. and Frydman, C. (2015) ‘Military CEOs’, Journal of Financial Economics.

North-Holland, 117(1), pp. 43–59. doi: 10.1016/J.JFINECO.2014.04.009.

Berle, A. A. and Means, G. C. (1932) The Modern Corporation and Private Property, New York

Macmillan. doi: 10.2307/3475545.

Brown, J. R. et al. (2008) ‘Neighbors Matter: Causal Community Effects and Stock Market

Participation’, The Journal of Finance. Wiley/Blackwell (10.1111), 63(3), pp. 1509–1531. doi:

10.1111/j.1540-6261.2008.01364.x.

Buchmueller, T. C., Dinardo, J. and Valletta, R. G. (2002) ‘Union Effects on Health Insurance

Provision and Coverage in the United States’, ILR Review. SAGE PublicationsSage CA: Los

Angeles, CA, 55(4), pp. 610–627. doi: 10.1177/001979390205500403.

Budd, J. W. and McCall, B. P. (2004) ‘Unions and Unemployment Insurance Benefits Receipt:

Evidence from the Current Population Survey’, Industrial Relations. Wiley/Blackwell (10.1111),

43(2), pp. 339–355. doi: 10.1111/j.0019-8676.2004.00332.x.

Cain, M. D. and McKeon, S. B. (2016) ‘CEO Personal Risk-Taking and Corporate Policies’,

Journal of Financial and Quantitative Analysis. Cambridge University Press, 51(01), pp. 139–

164. doi: 10.1017/S0022109016000041.

Campbell, J. L. (2007) ‘Why would corporations behave in socially responsible ways? an

institutional theory of corporate social responsibility’, Academy of Management Review.

Academy of Management Briarcliff Manor, NY 10510 , 32(3), pp. 946–967. doi:

10.5465/amr.2007.25275684.

Cao, J., Liang, H. and Zhan, X. (2015) ‘Peer Effects of Corporate Social Responsibility’, SSRN

Electronic Journal. doi: 10.2139/ssrn.2634100.

34

Carroll, A. B. (2009) A History of Corporate Social Responsibility. Edited by A. Crane et al.

Oxford University Press. doi: 10.1093/oxfordhb/9780199211593.003.0002.

Cheng, I.-H., Hong, H. and Shue, K. (2013) Do Managers Do Good with Other People’s

Money? Cambridge, MA. doi: 10.3386/w19432.

Cheung, A. W., Hu, M. and Schwiebert, J. (2016) ‘Corporate social responsibility and dividend

policy’, Accounting & Finance. Edited by T. Smith. Wiley/Blackwell (10.1111). doi:

10.1111/acfi.12238.

Clarkson, M. E. (1995) ‘A Stakeholder Framework for Analyzing and Evaluating Corporate

Social Performance’, Academy of Management Review. Academy of Management Briarcliff

Manor, NY 10510 , 20(1), pp. 92–117. doi: 10.5465/amr.1995.9503271994.

Cohen, L., Gurun, U. G. and Malloy, C. (2017) ‘Resident Networks and Corporate Connections:

Evidence from World War II Internment Camps’, The Journal of Finance. Wiley/Blackwell

(10.1111), 72(1), pp. 207–248. doi: 10.1111/jofi.12407.

Cragg, J. G. and Donald, S. G. (1993) ‘Testing Identifiability and Specification in Instrumental

Variable Models’, Econometric Theory. Cambridge University Press, 9(02), p. 222. doi:

10.1017/S0266466600007519.

Cronqvist, H., Makhija, A. K. and Yonker, S. E. (2012) ‘Behavioral consistency in corporate

finance: CEO personal and corporate leverage’, Journal of Financial Economics. North-Holland,

103(1), pp. 20–40. doi: 10.1016/J.JFINECO.2011.08.005.

Cronqvist, H. and Yu, F. (2017) ‘Shaped by their daughters: Executives, female socialization,

and corporate social responsibility’, Journal of Financial Economics. North-Holland, 126(3), pp.

543–562. doi: 10.1016/J.JFINECO.2017.09.003.

Doh, J. P. and Guay, T. R. (2006) ‘Corporate Social Responsibility, Public Policy, and NGO

Activism in Europe and the United States: An Institutional-Stakeholder Perspective’, Journal of

Management Studies. Wiley/Blackwell (10.1111), 43(1), pp. 47–73. doi: 10.1111/j.1467-

6486.2006.00582.x.

Doh, J. P. and Teegen, H. (2002) ‘Nongovernmental organizations as institutional actors in

international business: theory and implications’, International Business Review. Pergamon,

11(6), pp. 665–684. doi: 10.1016/S0969-5931(02)00044-6.

Dougal, C., Parsons, C. A. and Titman, S. (2015) ‘Urban Vibrancy and Corporate Growth’, The

Journal of Finance. Wiley/Blackwell (10.1111), 70(1), pp. 163–210. doi: 10.1111/jofi.12215.

Dyck, I. J. A. et al. (2015) ‘Do Institutional Investors Drive Corporate Social Responsibility?

International Evidence’, SSRN Electronic Journal. doi: 10.2139/ssrn.2708589.

Ferrell, A., Liang, H. and Renneboog, L. (2016) ‘Socially responsible firms’, Journal of

Financial Economics. North-Holland, 122(3), pp. 585–606. doi: 10.1016/j.jfineco.2015.12.003.

Flammer, C. (2015) ‘Does Corporate Social Responsibility Lead to Superior Financial

Performance? A Regression Discontinuity Approach’, Management Science. INFORMS ,

61(11), pp. 2549–2568. doi: 10.1287/mnsc.2014.2038.

35

Freeman, R. B. (1981) ‘The Effect of Unionism on Fringe Benefits’, ILR Review. SAGE

PublicationsSage CA: Los Angeles, CA, 34(4), pp. 489–509. doi:

10.1177/001979398103400401.

Freeman, R. B. (1982) ‘Union Wage Practices and Wage Dispersion within Establishments’, ILR

Review. SAGE PublicationsSage CA: Los Angeles, CA, 36(1), pp. 3–21. doi:

10.1177/001979398203600101.

Freeman, R. B. (1984) ‘Longitudinal Analyses of the Effects of Trade Unions’, Journal of Labor

Economics. University of Chicago Press , 2(1), pp. 1–26. doi: 10.1086/298021.

Friedman, M. (1970) ‘The social responsibility of business is to increase its profit’, New York

Times Magazine.

Galaskiewicz, J. (1985) Social organization of an urban grants economy : a study of business

philanthropy and nonprofit organizations. Academic Press.

Galaskiewicz, J. (1997) ‘An Urban Grants Economy Revisited: Corporate Charitable

Contributions in the Twin Cities, 1979-81, 1987-89’, Administrative Science Quarterly. Sage

Publications, Inc.Johnson Graduate School of Management, Cornell University, 42(3), p. 445.

doi: 10.2307/2393734.

Gao, W., Ng, L. and Wang, Q. (2011) ‘Does Corporate Headquarters Location Matter for Firm

Capital Structure?’, Financial Management. Wiley/Blackwell (10.1111), 40(1), pp. 113–138.

doi: 10.1111/j.1755-053X.2010.01136.x.

El Ghoul, S. et al. (2011) ‘Does corporate social responsibility affect the cost of capital?’,

Journal of Banking & Finance. North-Holland, 35(9), pp. 2388–2406. doi:

10.1016/J.JBANKFIN.2011.02.007.

Di Giuli, A. and Kostovetsky, L. (2014) ‘Are red or blue companies more likely to go green?

Politics and corporate social responsibility’, Journal of Financial Economics. North-Holland,

111(1), pp. 158–180. doi: 10.1016/J.JFINECO.2013.10.002.

Hansmann, H. B. (1980) ‘The Role of Nonprofit Enterprise’, The Yale Law Journal. The Yale

Law Journal Company, Inc., 89(5), p. 835. doi: 10.2307/796089.

Helmig, B., Spraul, K. and Ingenhoff, D. (2016) ‘Under Positive Pressure’, Business & Society.

SAGE PublicationsSage CA: Los Angeles, CA, 55(2), pp. 151–187. doi:

10.1177/0007650313477841.

Henderson, D. and Institute of Economic Affairs (Great Britain) (2001) Misguided virtue : false

notions of corporate social responsibility. Institute of Economic Affairs. Available at:

https://iea.org.uk/publications/research/misguided-virtue-false-notions-of-corporate-social-

responsibility (Accessed: 22 June 2018).

Hill, C. W. L. and Jones, T. M. (1992) ‘STAKEHOLDER-AGENCY THEORY’, Journal of

Management Studies. Wiley/Blackwell (10.1111), 29(2), pp. 131–154. doi: 10.1111/j.1467-

6486.1992.tb00657.x.

36

Husted, B. W., Jamali, D. and Saffar, W. (2016) ‘Near and dear? The role of location in CSR

engagement’, Strategic Management Journal. Wiley-Blackwell, 37(10), pp. 2050–2070. doi:

10.1002/smj.2437.

Hwang, B.-H. and Kim, H. H. (2017) ‘It pays to write well’, Journal of Financial Economics.

North-Holland, 124(2), pp. 373–394. doi: 10.1016/J.JFINECO.2017.01.006.

Jha, A. and Cox, J. (2015) ‘Corporate social responsibility and social capital’, Journal of

Banking & Finance, 60, pp. 252–270. doi: 10.1016/j.jbankfin.2015.08.003.

Kelly, D. and Lewis, A. (2009) ‘Human service sector nonprofit organization’s social impact’,

Business Strategy Series. Emerald Group Publishing Limited, 10(6), pp. 374–382. doi:

10.1108/17515630911005664.

Kubik, J. D., Scheinkman, J. A. and Hong, H. G. (2011) ‘Financial Constraints on Corporate

Goodness’, SSRN Electronic Journal. doi: 10.2139/ssrn.1784357.

Liang, H. and Renneboog, L. (2017) ‘On the Foundations of Corporate Social Responsibility’,

The Journal of Finance. Wiley/Blackwell (10.1111), 72(2), pp. 853–910. doi:

10.1111/jofi.12487.

Lins, K. V., Servaes, H. and Tamayo, A. (2017) ‘Social Capital, Trust, and Firm Performance:

The Value of Corporate Social Responsibility during the Financial Crisis’, The Journal of

Finance. Wiley/Blackwell (10.1111), 72(4), pp. 1785–1824. doi: 10.1111/jofi.12505.

Margolis, J. D., Elfenbein, H. A. and Walsh, J. P. (2009) ‘Does it Pay to Be Good...And Does it

Matter? A Meta-Analysis of the Relationship between Corporate Social and Financial

Performance’, SSRN Electronic Journal. doi: 10.2139/ssrn.1866371.

Margolis, J. D. and Walsh, J. P. (2003) ‘Misery Loves Companies: Rethinking Social Initiatives

by Business’, Administrative Science Quarterly. SAGE Publications, 48(2), p. 268. doi:

10.2307/3556659.

Marquis, C. (2003) ‘The Pressure of the Past: Network Imprinting in Intercorporate

Communities’, Administrative Science Quarterly. SAGE Publications, 48(4), p. 655. doi:

10.2307/3556640.

Marquis, C., Glynn, M. A. and Davis, G. F. (2007) ‘Community isomorphism and corporate

social action’, Academy of Management Review. Academy of Management Briarcliff Manor,

NY 10510 , 32(3), pp. 925–945. doi: 10.5465/amr.2007.25275683.

Masulis, R. W. and Reza, S. W. (2015) ‘Agency Problems of Corporate Philanthropy’, Review of

Financial Studies. Oxford University Press, 28(2), pp. 592–636. doi: 10.1093/rfs/hhu082.

McGuire, S. T. et al. (2012) ‘Does Local Religiosity Impact Corporate Social Responsibility?’,

SSRN Electronic Journal. doi: 10.2139/ssrn.1926387.

McWilliams, A. and Siegel, D. (2001) ‘Corporate Social Responsibility: A Theory of the Firm

Perspective’, The Academy of Management Review. Academy of Management, 26(1), p. 117.

doi: 10.2307/259398.

37

Orlitzky, M., Schmidt, F. L. and Rynes, S. L. (2003) ‘Corporate Social and Financial

Performance: A Meta-Analysis’, Organization Studies, 24(3), pp. 403–441. doi:

10.1177/0170840603024003910.

Ostrower, F. (1995) Why the wealthy give : the culture of elite philanthropy. Princeton

University Press. Available at: https://press.princeton.edu/titles/5769.html (Accessed: 18

September 2018).

Pirinsky, C. and Wang, Q. (2006) ‘Does Corporate Headquarters Location Matter for Stock

Returns?’, The Journal of Finance. Wiley/Blackwell (10.1111), 61(4), pp. 1991–2015. doi: