European Electricity Market between Liberalisation and Climate Protection Dr. Markus Blesl,...

21

European Electricity Market between Liberalisation and Climate Protection Dr. Markus Blesl, Dipl.-Ing. Uwe Remme, Dr. Ulrich Fahl 23.06.2004 International Energy Workshop, Paris

-

date post

22-Dec-2015 -

Category

Documents

-

view

218 -

download

3

Transcript of European Electricity Market between Liberalisation and Climate Protection Dr. Markus Blesl,...

European Electricity Market between Liberalisation and Climate Protection

Dr. Markus Blesl, Dipl.-Ing. Uwe Remme, Dr. Ulrich Fahl

23.06.2004International Energy Workshop,

Paris

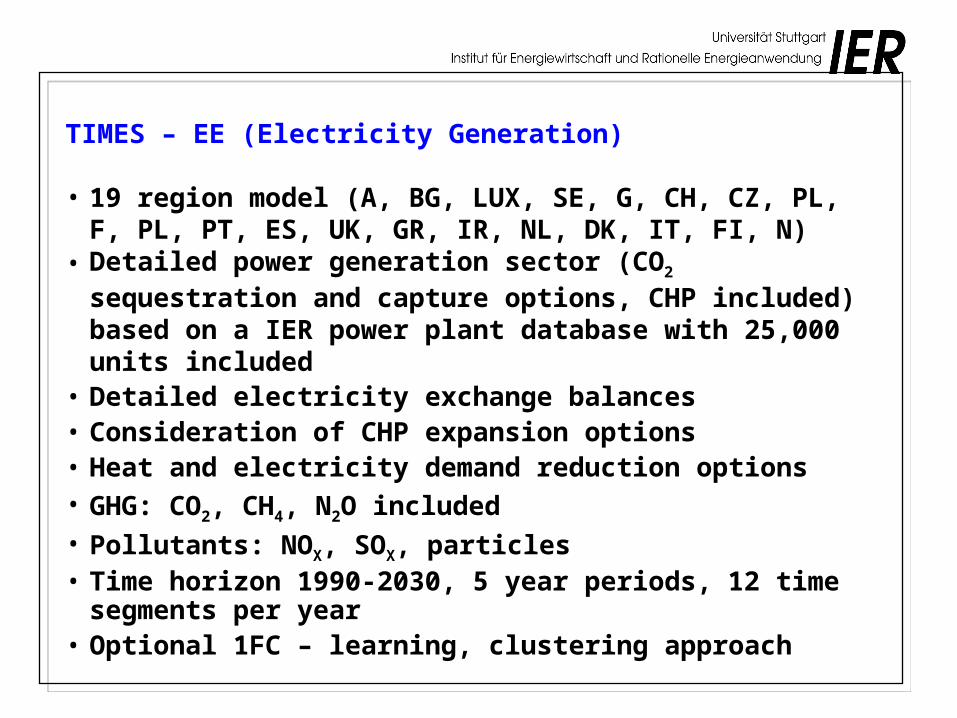

TIMES – EE (Electricity Generation)

• 19 region model (A, BG, LUX, SE, G, CH, CZ, PL, F, PL, PT, ES, UK, GR, IR, NL, DK, IT, FI, N)

• Detailed power generation sector (CO2 sequestration and capture options, CHP included) based on a IER power plant database with 25,000 units included

• Detailed electricity exchange balances• Consideration of CHP expansion options• Heat and electricity demand reduction options • GHG: CO2, CH4, N2O included• Pollutants: NOX, SOX, particles• Time horizon 1990-2030, 5 year periods, 12 time segments per

year• Optional 1FC – learning, clustering approach

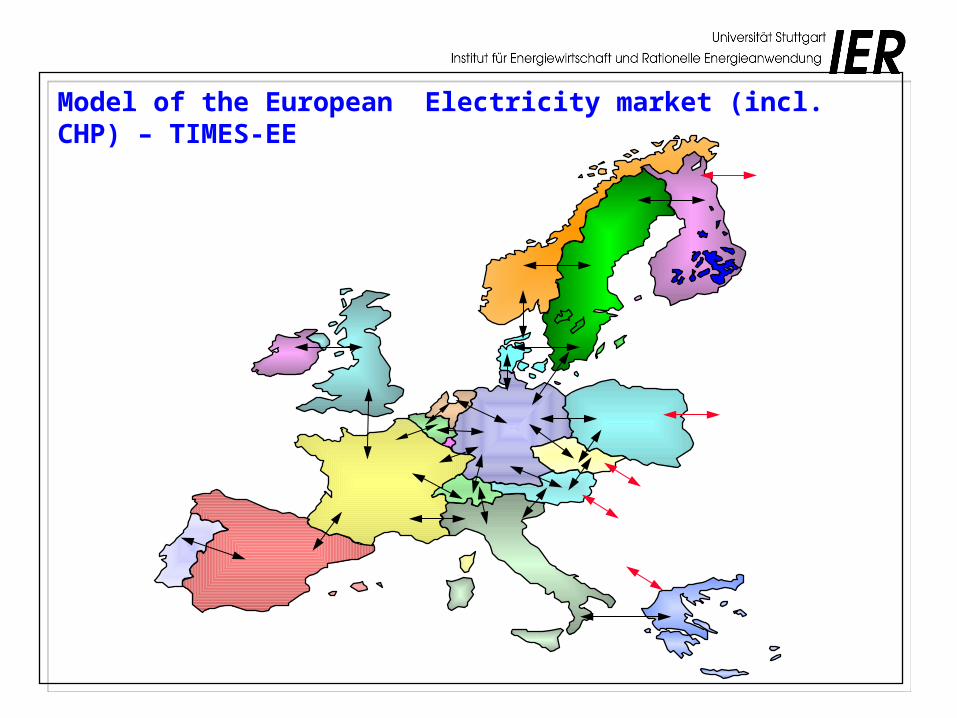

Model of the European Electricity market (incl. CHP) – TIMES-EE

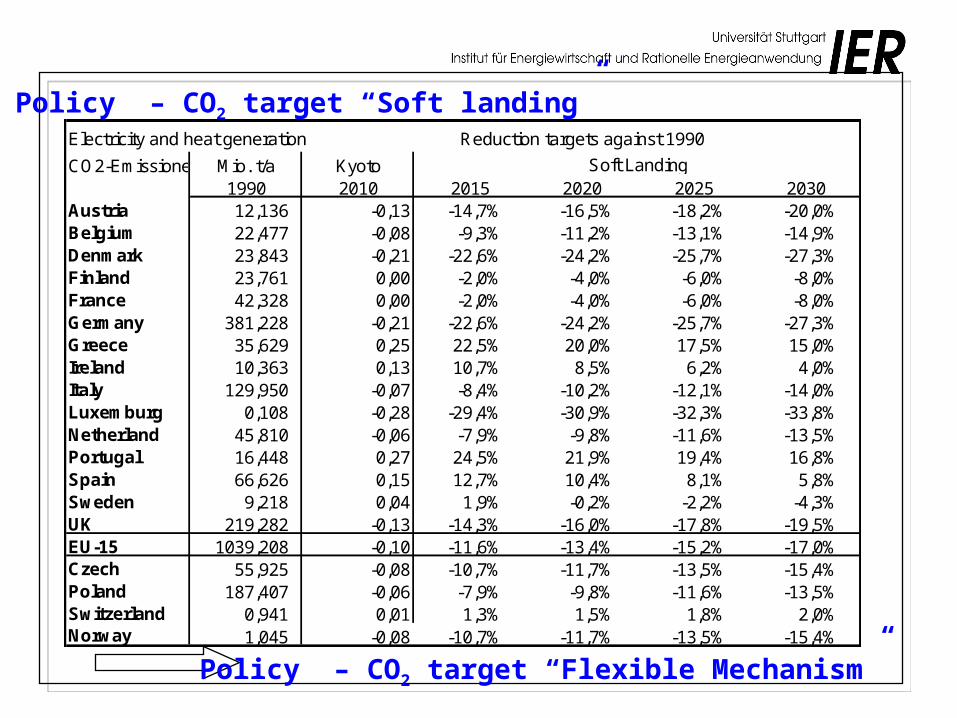

Policy – CO2 target “Soft landing” Electricity and heat generation Reduction targets against 1990

CO2-Emissionen Mio. t/a Kyoto1990 2010 2015 2020 2025 2030

Austria 12,136 -0,13 -14,7% -16,5% -18,2% -20,0% Belgium 22,477 -0,08 -9,3% -11,2% -13,1% -14,9% Denmark 23,843 -0,21 -22,6% -24,2% -25,7% -27,3% Finland 23,761 0,00 -2,0% -4,0% -6,0% -8,0% France 42,328 0,00 -2,0% -4,0% -6,0% -8,0% Germany 381,228 -0,21 -22,6% -24,2% -25,7% -27,3% Greece 35,629 0,25 22,5% 20,0% 17,5% 15,0% Ireland 10,363 0,13 10,7% 8,5% 6,2% 4,0% Italy 129,950 -0,07 -8,4% -10,2% -12,1% -14,0% Luxemburg 0,108 -0,28 -29,4% -30,9% -32,3% -33,8% Netherland 45,810 -0,06 -7,9% -9,8% -11,6% -13,5% Portugal 16,448 0,27 24,5% 21,9% 19,4% 16,8% Spain 66,626 0,15 12,7% 10,4% 8,1% 5,8% Sweden 9,218 0,04 1,9% -0,2% -2,2% -4,3% UK 219,282 -0,13 -14,3% -16,0% -17,8% -19,5% EU-15 1039,208 -0,10 -11,6% -13,4% -15,2% -17,0% Czech 55,925 -0,08 -10,7% -11,7% -13,5% -15,4% Poland 187,407 -0,06 -7,9% -9,8% -11,6% -13,5% Switzerland 0,941 0,01 1,3% 1,5% 1,8% 2,0% Norway 1,045 -0,08 -10,7% -11,7% -13,5% -15,4%

Soft Landing

Policy – CO2 target “Flexible Mechanism”

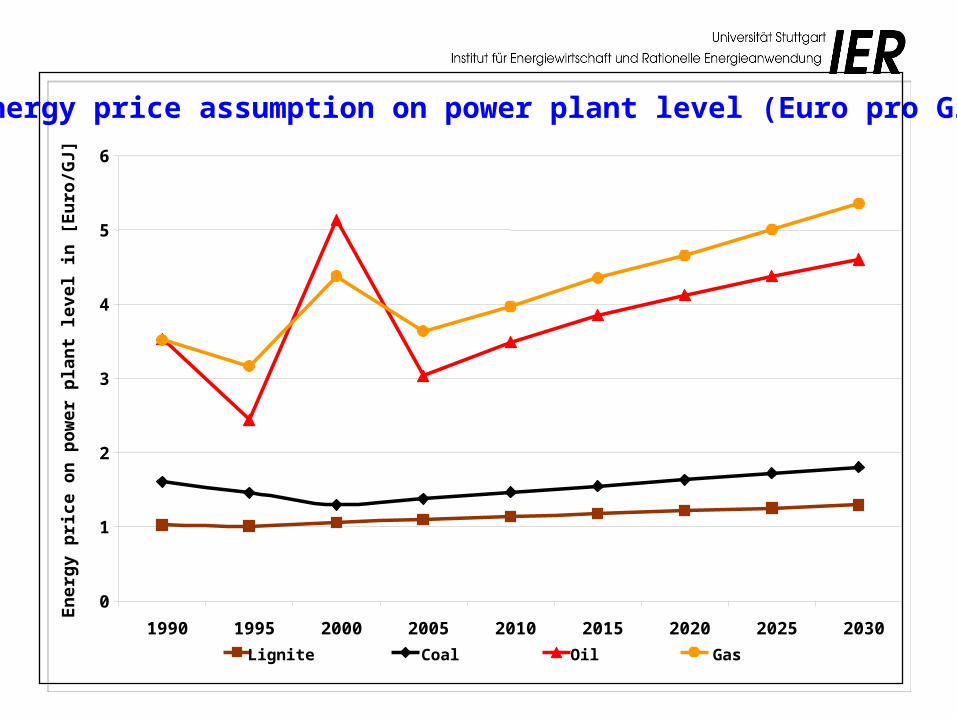

Energy price assumption on power plant level (Euro pro GJ)

0

1

2

3

4

5

6

1990 1995 2000 2005 2010 2015 2020 2025 2030

En

erg

y p

rice

on

po

wer

pla

nt

leve

l in

[E

uro

/GJ]

Lignite Coal Oil Gas

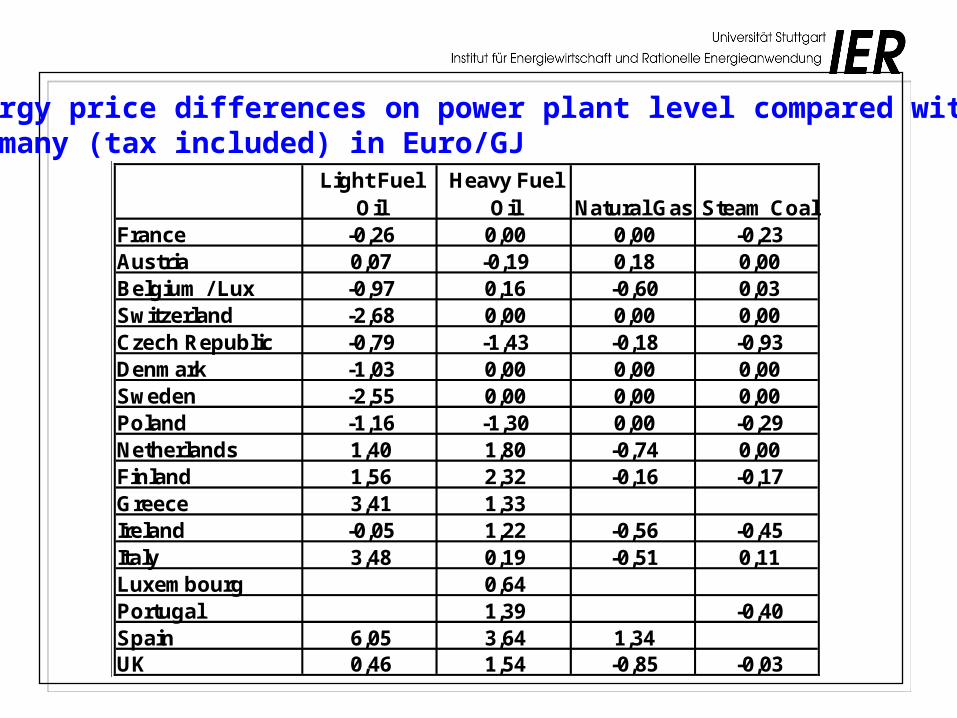

Energy price differences on power plant level compared with Germany (tax included) in Euro/GJ

Light Fuel Oil

Heavy Fuel Oil Natural Gas Steam Coal

France -0,26 0,00 0,00 -0,23Austria 0,07 -0,19 0,18 0,00Belgium / Lux -0,97 0,16 -0,60 0,03Switzerland -2,68 0,00 0,00 0,00Czech Republic -0,79 -1,43 -0,18 -0,93Denmark -1,03 0,00 0,00 0,00Sweden -2,55 0,00 0,00 0,00Poland -1,16 -1,30 0,00 -0,29Netherlands 1,40 1,80 -0,74 0,00Finland 1,56 2,32 -0,16 -0,17Greece 3,41 1,33Ireland -0,05 1,22 -0,56 -0,45Italy 3,48 0,19 -0,51 0,11Luxembourg 0,64Portugal 1,39 -0,40Spain 6,05 3,64 1,34UK 0,46 1,54 -0,85 -0,03

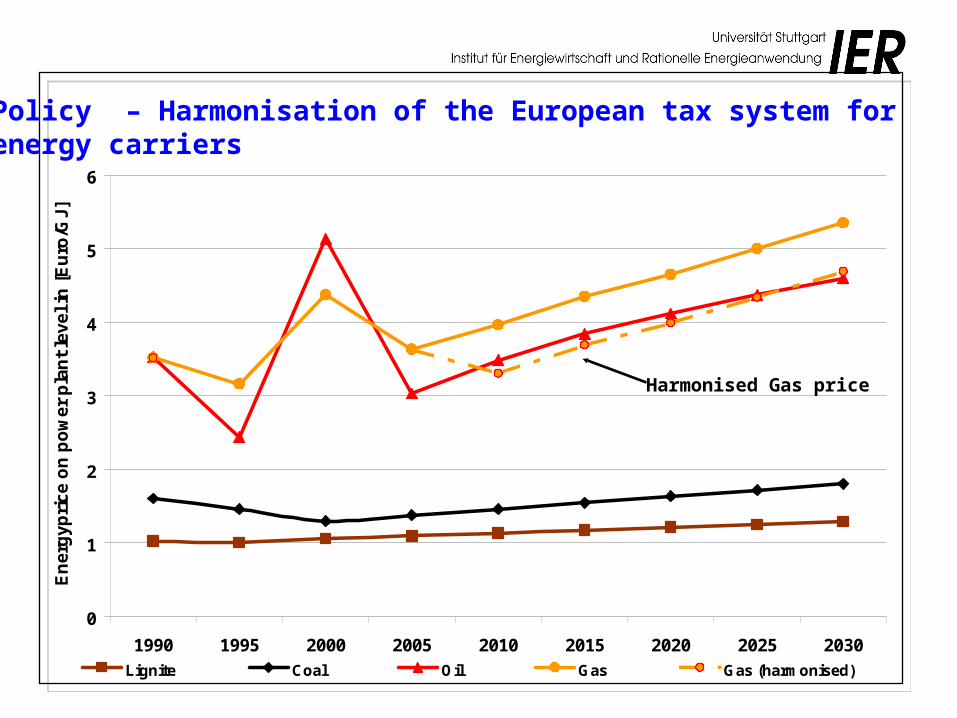

Policy – Harmonisation of the European tax system for energy carriers

0

1

2

3

4

5

6

1990 1995 2000 2005 2010 2015 2020 2025 2030

En

erg

yp

ric

e o

n p

ow

er

pla

nt

lev

el

in [

Eu

ro/G

J]

Lignite Coal Oil Gas Gas (harmonised)

Harmonised Gas price

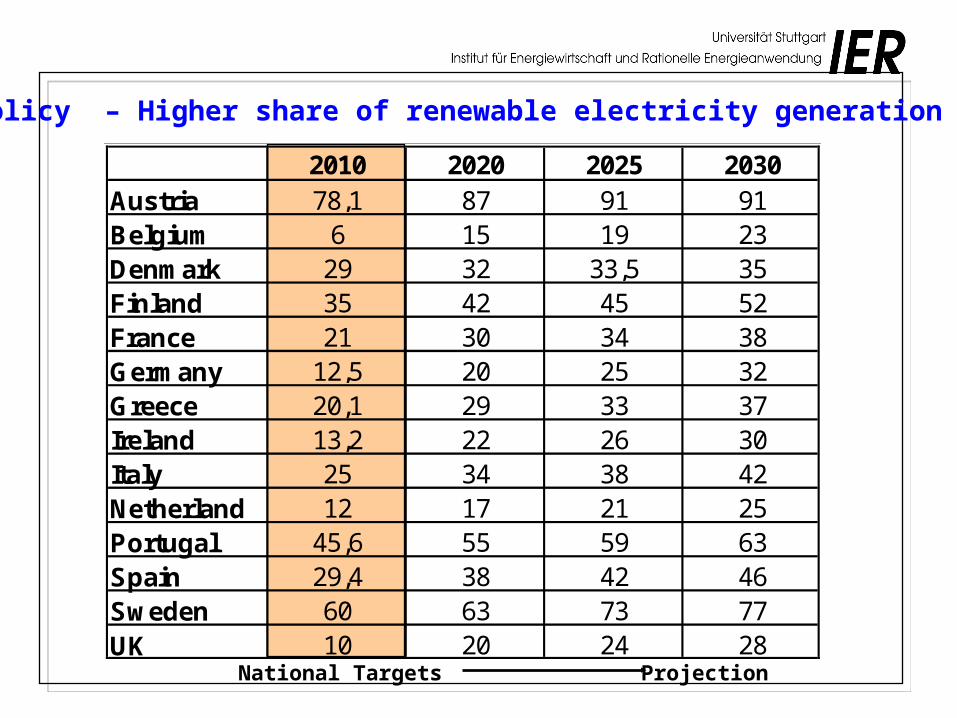

Policy – Higher share of renewable electricity generation

2010 2020 2025 2030Austria 78,1 87 91 91Belgium 6 15 19 23Denmark 29 32 33,5 35Finland 35 42 45 52France 21 30 34 38Germany 12,5 20 25 32Greece 20,1 29 33 37Ireland 13,2 22 26 30Italy 25 34 38 42Netherland 12 17 21 25Portugal 45,6 55 59 63Spain 29,4 38 42 46Sweden 60 63 73 77UK 10 20 24 28

Projection National Targets

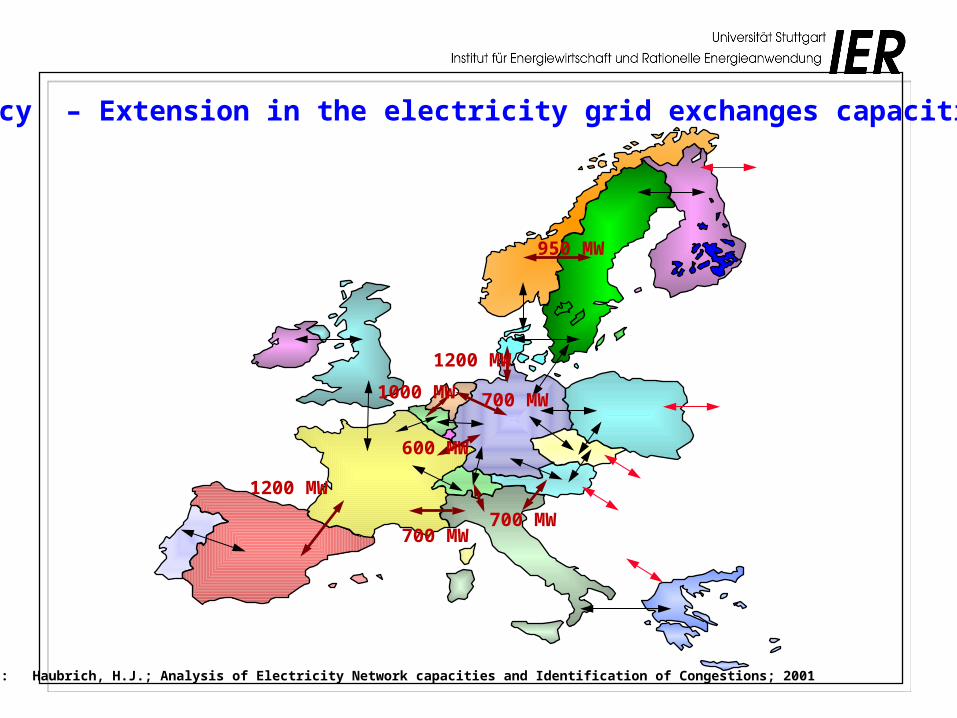

Policy – Extension in the electricity grid exchanges capacities

1200 MW

700 MW

600 MW

1000 MW

1200 MW

950 MW

700 MW

700 MW

Source: Haubrich, H.J.; Analysis of Electricity Network capacities and Identification of Congestions; 2001

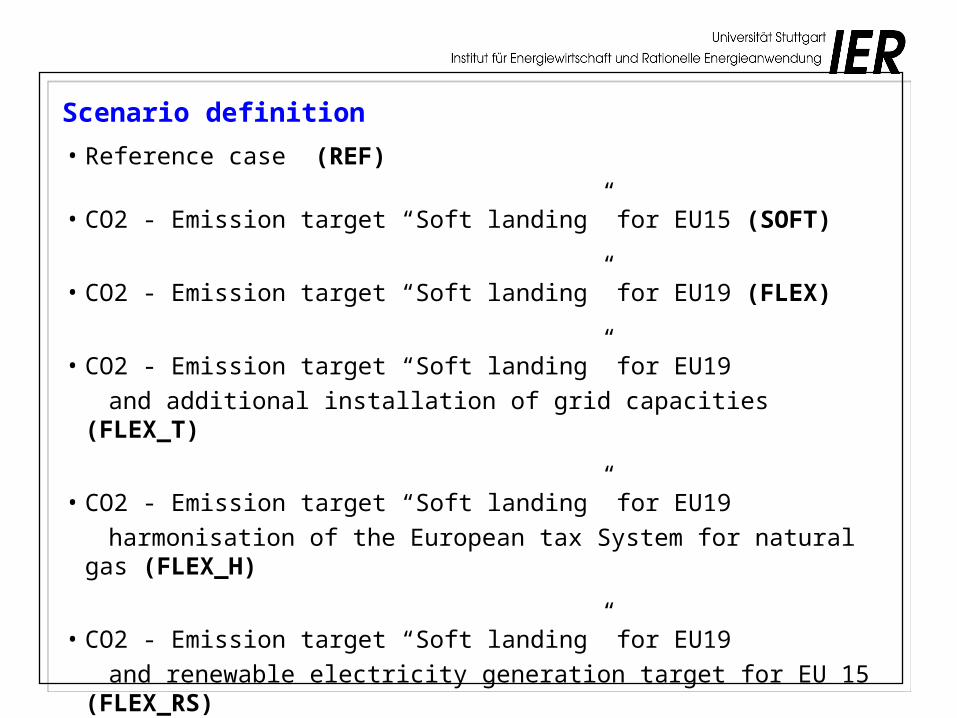

Scenario definition

• Reference case (REF)

• CO2 - Emission target “Soft landing” for EU15 (SOFT)

• CO2 - Emission target “Soft landing” for EU19 (FLEX)

• CO2 - Emission target “Soft landing” for EU19

and additional installation of grid capacities (FLEX_T)

• CO2 - Emission target “Soft landing” for EU19

harmonisation of the European tax System for natural gas (FLEX_H)

• CO2 - Emission target “Soft landing” for EU19

and renewable electricity generation target for EU 15 (FLEX_RS)

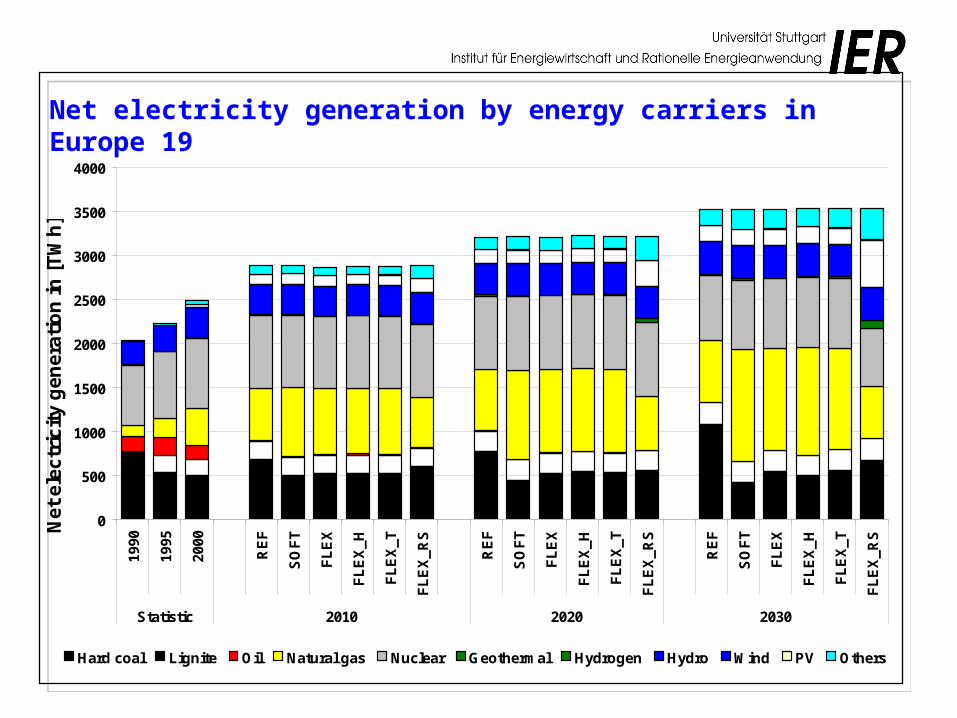

Net electricity generation by energy carriers in Europe 19

0

500

1000

1500

2000

2500

3000

3500

4000

1990

1995

2000

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

Statistic 2010 2020 2030

Ne

t e

lec

tric

ity

ge

ne

rati

on

in [

TW

h]

Hard coal Lignite Oil Natural gas Nuclear Geothermal Hydrogen Hydro Wind PV Others

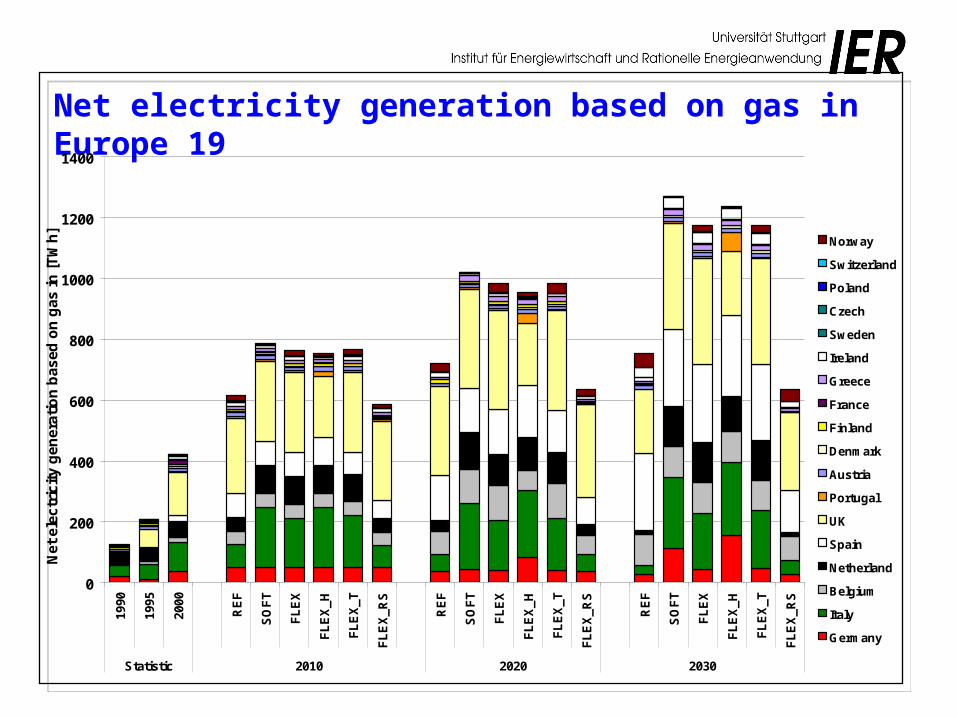

Net electricity generation based on gas in Europe 19

0

200

400

600

800

1000

1200

1400

1990

1995

2000

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

Statistic 2010 2020 2030

Net

ele

ctr

icit

y g

en

era

tio

n b

as

ed

on

ga

s i

n [

TW

h]

Norway

Switzerland

Poland

Czech

Sweden

Ireland

Greece

France

Finland

Denmark

Austria

Portugal

UK

Spain

Netherland

Belgium

Italy

Germany

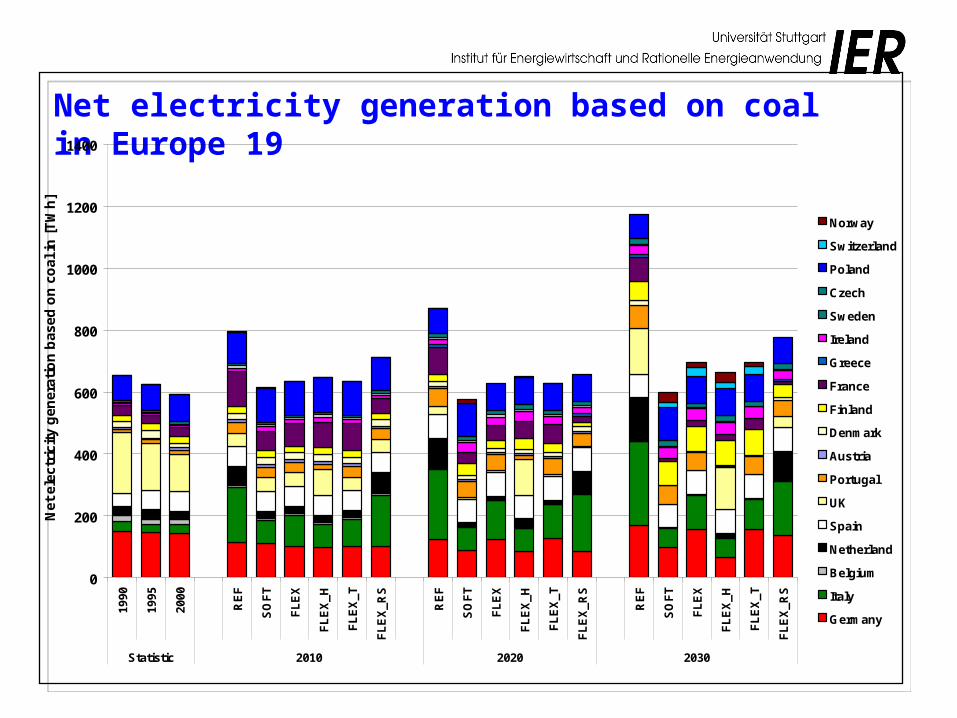

Net electricity generation based on coal in Europe 19

0

200

400

600

800

1000

1200

1400

1990

1995

2000

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

Statistic 2010 2020 2030

Net

ele

ctri

city

gen

erat

ion

bas

ed o

n c

oal

in

[T

Wh

]

Norway

Switzerland

Poland

Czech

Sweden

Ireland

Greece

France

Finland

Denmark

Austria

Portugal

UK

Spain

Netherland

Belgium

Italy

Germany

-250

-200

-150

-100

-50

0

50

100

150

200

250

1990

1995

2000

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

Statistic 2010 2020 2030

Ele

ctri

city

exc

han

ge

in [

TW

h]

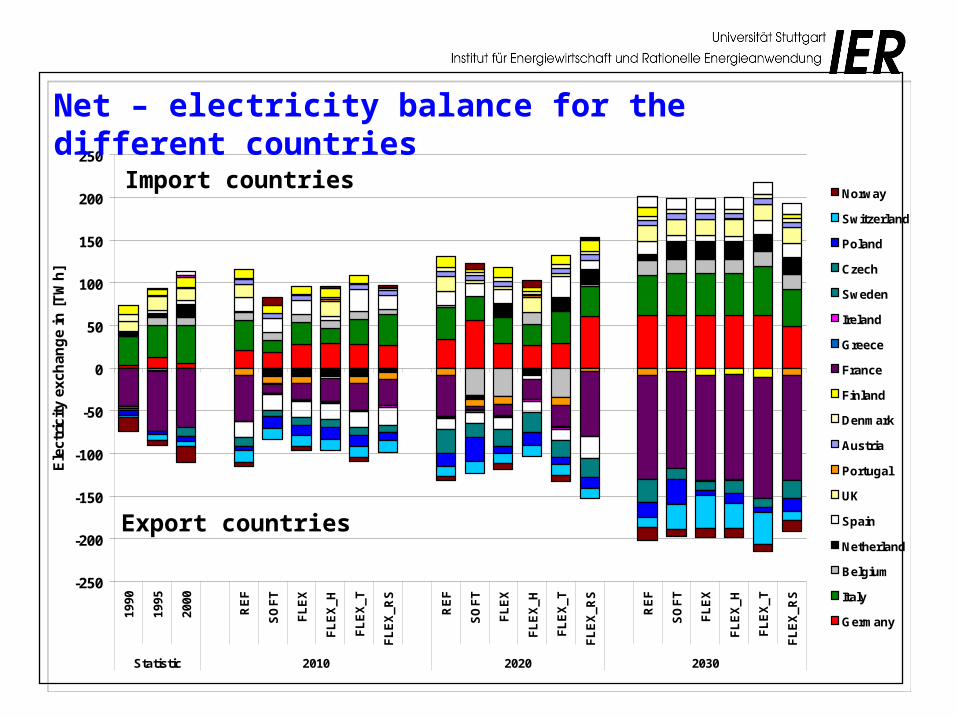

Norway

Switzerland

Poland

Czech

Sweden

Ireland

Greece

France

Finland

Denmark

Austria

Portugal

UK

Spain

Netherland

Belgium

Italy

Germany

Net – electricity balance for the different countries

Import countries

Export countries

-100

-50

0

50

100

150

200S

OF

T

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_RS

2010 2020 2030

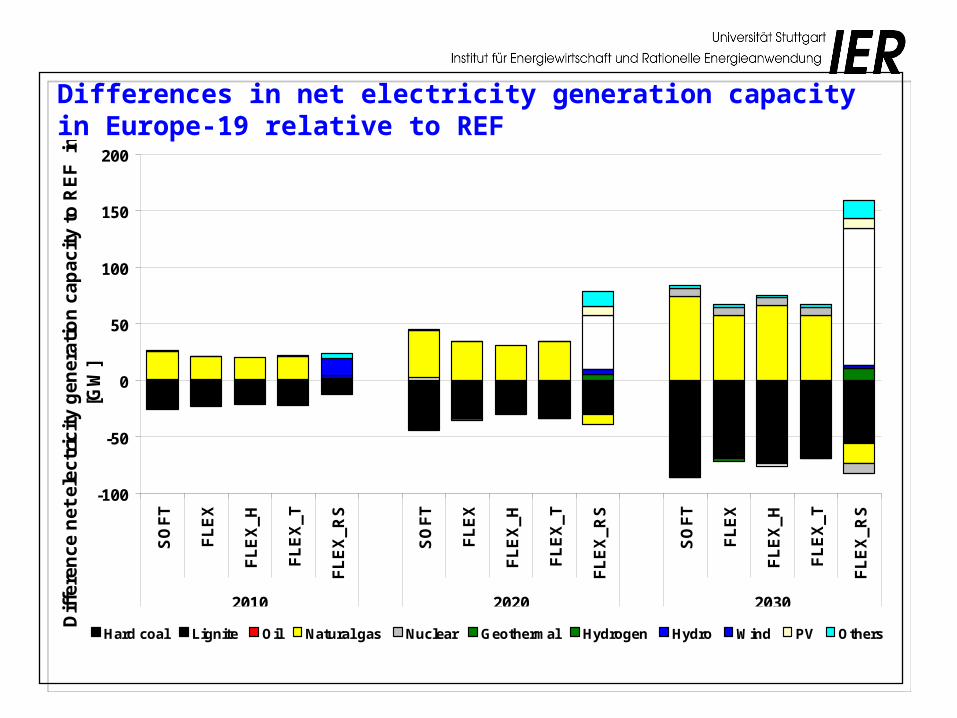

Dif

fere

nc

e n

et

ele

ctr

icit

y g

en

era

tio

n c

ap

ac

ity

to

RE

F i

n

[GW

]

Hard coal Lignite Oil Natural gas Nuclear Geothermal Hydrogen Hydro Wind PV Others

Differences in net electricity generation capacity in Europe-19 relative to REF

14,0

19,0

24,0

29,0

34,0

39,0

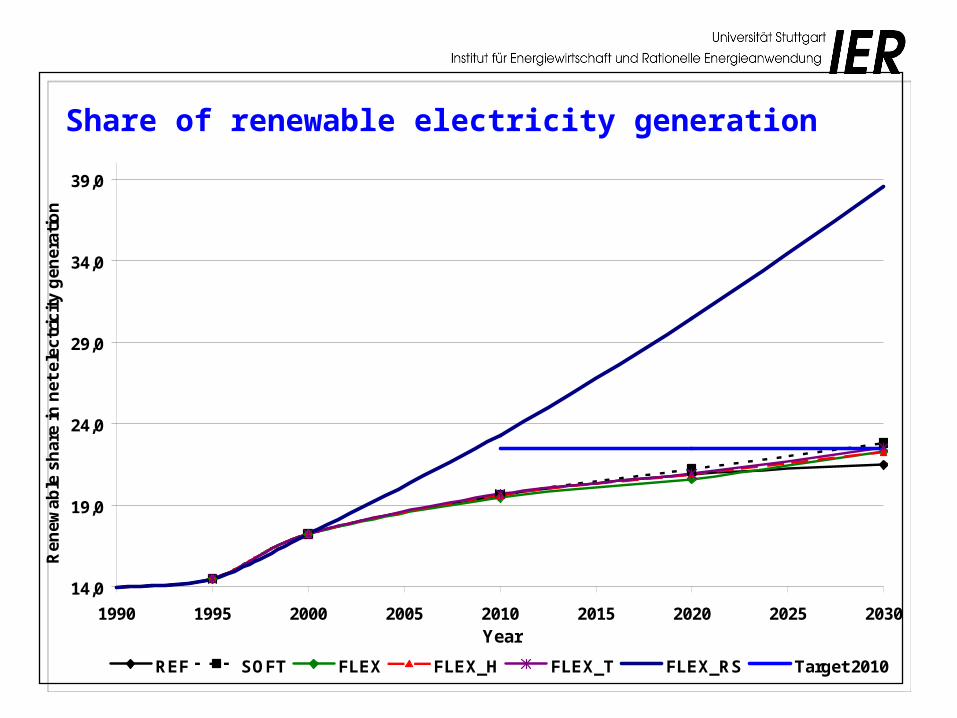

1990 1995 2000 2005 2010 2015 2020 2025 2030Year

Ren

ewa

ble

sh

are

in n

et e

lec

tric

ity

ge

ner

atio

n

REF SOFT FLEX FLEX_H FLEX_T FLEX_RS Target 2010

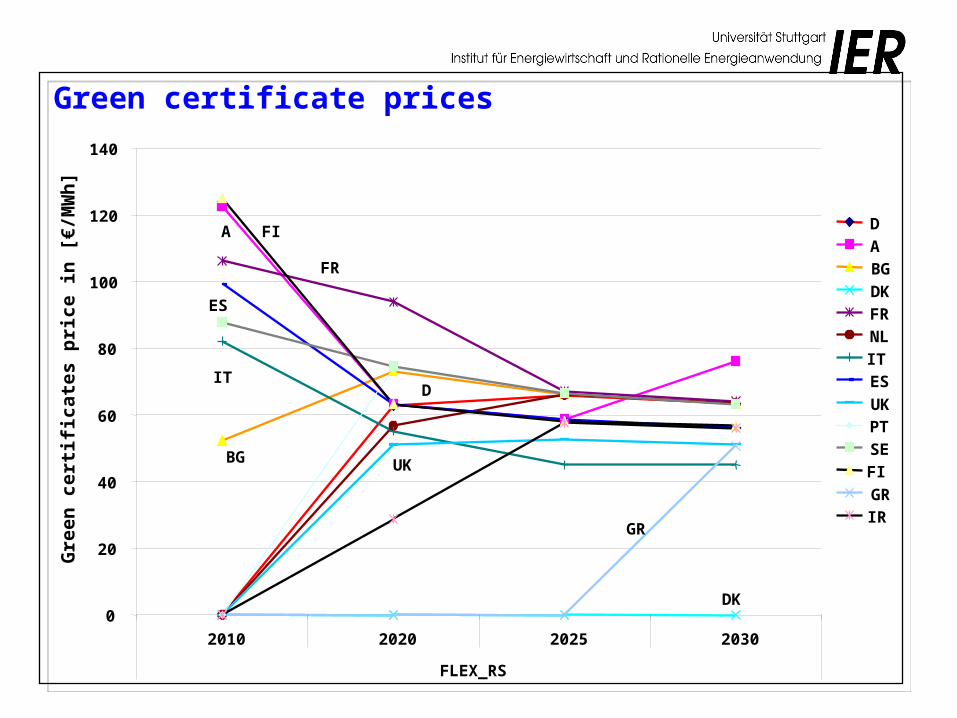

Share of renewable electricity generation

0

20

40

60

80

100

120

140

2010 2020 2025 2030

FLEX_RS

Gre

en c

erti

fica

tes

pri

ce i

n [

€/M

Wh

]

D

A

BG

DK

FR

NL

IT

ES

UK

PT

SE

FI

GR

IRGR

DK

FI

FR

A

D

Green certificate prices

UKBG

IT

ES

CO2 Emission in the different scenarios in EU 15

790

890

990

1090

1190

1290

1990 1995 2000 2005 2010 2015 2020 2025 2030Year

CO

2-E

mis

sio

n e

lect

rici

ty a

nd

hea

t g

ener

atio

n i

n [

Mio

. t

CO

2]

REF SOFT FLEX FLEX_H FLEX_T FLEX_RS Target EU15

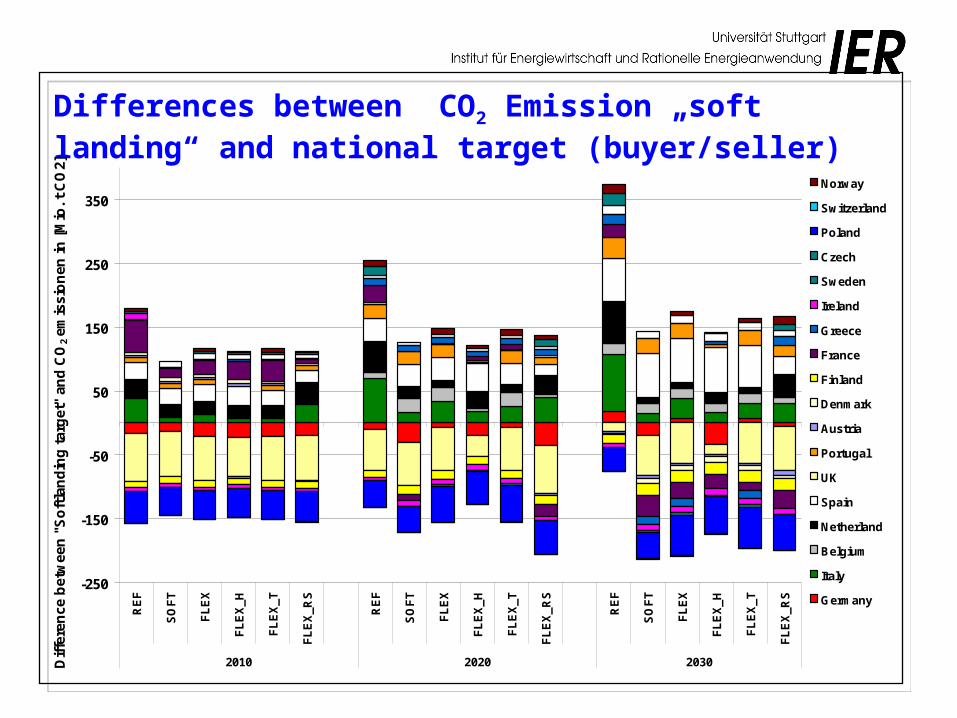

Differences between CO2 Emission „soft landing“ and national target (buyer/seller)

-250

-150

-50

50

150

250

350

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_R

S

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_R

S

RE

F

SO

FT

FL

EX

FL

EX

_H

FL

EX

_T

FL

EX

_R

S

2010 2020 2030Dif

fere

nce

bet

wee

n "

So

ftla

nd

ing

tar

get

" an

d C

O2 em

issi

on

en i

n [

Mio

. t

CO

2]

Norway

Switzerland

Poland

Czech

Sweden

Ireland

Greece

France

Finland

Denmark

Austria

Portugal

UK

Spain

Netherland

Belgium

Italy

Germany

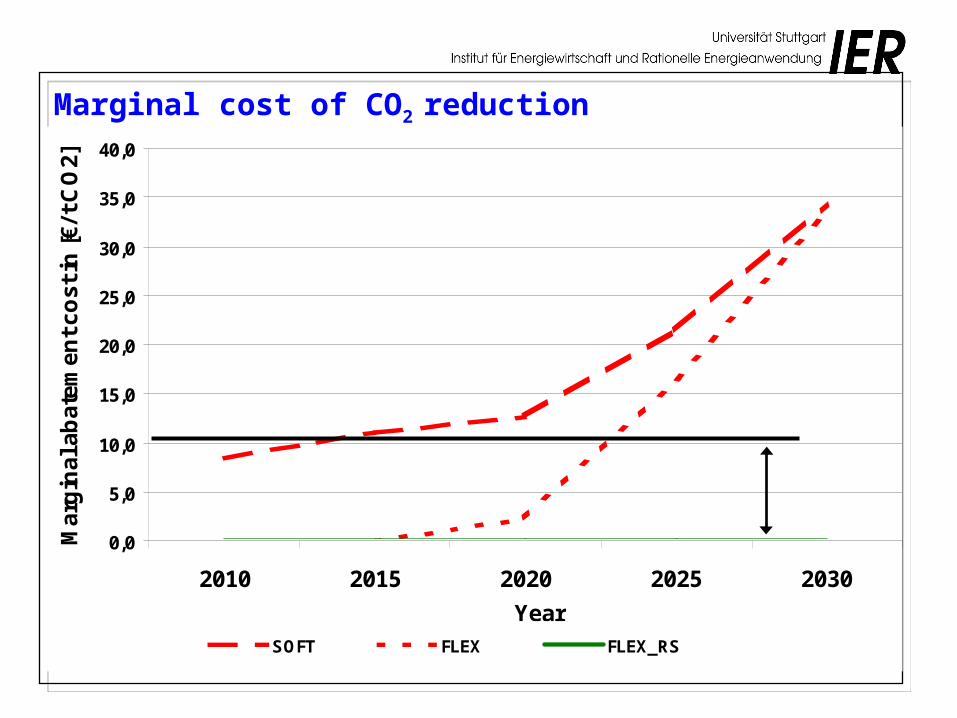

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

2010 2015 2020 2025 2030

Year

Ma

rgin

al a

ba

tem

en

t c

os

t in

[€

/ t C

O2

]

SOFT FLEX FLEX_RS

Marginal cost of CO2 reduction

Conclusions• The differences between Kyoto – target and the emissions of the

electricity and heat sector are not so big.

• If all European countries will include in the emission trading the certificate prices fall especially because of the hot air from Poland.

• Under the energy carrier price assumptions, the harmonisation of the European energy tax system influences the electricity capacities which will be installed in the different countries.

• The total amount of electricity exchange will be on the same level if there will be investments in additional net capacities between the countries. But the price for peak-load electricity fall and the national net imports balances will change.

• With the national targets for renewable electricity automatically the Kyoto-target will be achieved.

• With a common electricity market, a free certificate market, a harmonised tax system the European emission reduction and the national renewable targets can be achieved in the most cost-effective manner leading to the lowest electricity prices.

![CEEH Workshop Roskilde, February 6, 2008 The Pan European NEEDS-TIMES model SIXTH FRAMEWORK PROGRAMME [6.1] [ Sustainable Energy Systems] Markus Blesl.](https://static.fdocuments.us/doc/165x107/56649e635503460f94b5f558/ceeh-workshop-roskilde-february-6-2008-the-pan-european-needs-times-model.jpg)