Europe & Israel 4Q15 Deals Done Review

51

Venture Capital in Europe & Israel Venture Investment Data: Fourth Quarter, 2015 Prepared by Gil Dibner Passo dello Stelvio, Italian-Swiss Border Second highest pass in Europe, at 2,757 m (9,045 ft) above sea level blog

-

Upload

gil-dibner -

Category

Technology

-

view

8.272 -

download

0

Transcript of Europe & Israel 4Q15 Deals Done Review

Venture Capital in Europe & IsraelVenture Investment Data: Fourth Quarter, 2015

Prepared by Gil Dibner

Passo dello Stelvio, Italian-Swiss BorderSecond highest pass in Europe, at 2,757 m (9,045 ft) above sea level blog

The data• Around the middle of last year, I decided I wasn’t happy with available data sources on VC

rounds in Europe & Israel, and that I’d need to build my own• The data in this report consists entirely of data I’ve gathered manually based on publically

available, free sources• No paid data sources or API calls were harmed in the making of this dataset, every

investment was manually classified• This allows analysis of some aspects of the data I consider important – aspects that don’t

appear in other data sources• Seed investment is still under-reported, but I got a bit better at capturing it in the fourth

quarter. Rounds smaller than $500K are generally excluded from this analysis• The analysis is limited to ICT categories and excludes life sciences• The analysis excludes Turkey and FSU countries• I’m converting EUR and GBP into USD using monthly average exchange rates

2@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

Quarterly pace of venture investment• For the first time since I

started collecting data, the total investment amounts in Europe & Israel decreased

• In 4Q15, Europe & Israel saw $2.856 billion flowing into 357 venture transactions

• While the number of accounted and recorded deals continued to rise, the total amount of investment dollars decreased to the lowest quarterly level in 2015, 12% below 3Q15 and just under 1% below 1Q15

3@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

1,703 1,916 2,873 3,139 3,248 2,856

122

204

270 271286

357

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

50

100

150

200

250

300

350

400

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

Amou

nt in

vest

ed (U

S $M

)

Num

ber

of in

vest

men

ts

VC Investments in Europe & Israel

Invested amount (US $M) Number of investments

Monthly pace of venture investment• During the fourth quarter of

2015, there were 357 venture investments in Europe &Israel totaling $2.9B

• Total investment volume showed a decrease in every month since September, though December’s especially low total likely reflects the seasonal slowdown

• Deal pace remained at 110-125 per month, higher than in any previous quarter

@gdibnerblog: yankeesabralimey 4Syndicate for European & Israeli Enterprise Companies

493

565

644

625 566

725

905

971

997

791

787

1,561

1,517

568

1,164

1,083

1,059

714

42 30 50 79 73 52 92 75 103 78 95 98 119 65 102 111 124 122

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

Num

ber

of in

vest

men

ts

VC Investments in Europe & Israel, July 2014 - December 2015

Invested amount (US $M) Number of investments

Mega-rounds skew the investment totals• This analysis breaks down VC

investments into brackets by size:• Seed (less than $2M)• Early venture ($2-8M)• Venture ($8-20M)• Growth ($20-100M)• Mega ($100M+)

• Three mega-rounds took place in Europe this quarter – all of them consumer-oriented businesses in the UK:

• Karhoo, a UK-based on-demand taxi app, raised $250M in October

• Deliveroo, a UK-based on-demand food delivery service, raised $100M in November

• Atom Bank, a UK-based challenger consumer bank, raised $128M in November

• Adjusting for mega-rounds, 4Q15 shows a decline compared to 3Q, but is the second highest quarter since 3Q14

5@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

248 349 285 354 368 507345312 556

716 567559539

935

1,154 8131,513 1,187

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

Amou

nt In

vest

ed (U

S $M

)

Pace of VC Investment in Europe and Israel

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8) Seed (.5-2)

Strong year-over-year growth• 4Q15 total investment volume

in Europe & Israel was up 48% over 4Q14 (excluding seed deals, where data is more spotty)

• Early venture volume grew by 45%

• Venture volume grew by 79%

• Growth volume grew by 27%

• Mega round volume nearly doubled, growing 91%

6@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

349 507

312

559

935

1,187250

478

0

500

1,000

1,500

2,000

2,500

3,000

Qtr4 Qtr4

2014 2015

Tota

l VC

inve

stm

ent (

US $

M)

VC investment volume in Europe and Israel by bracket

Mega (>100) Growth (20-100)Venture (8-20) Early Venture (2-8)

Number of investments, by bracket• Excluding seed deals, the

total number of VC investments per quarter was 223 in 4Q15, 24% higher than 3Q15

• All of this growth was in the early venture bracket of rounds under $8M, which grew 49% from 93 in 3Q15 to 139 in 4Q15

• All other categories were roughly flat in 4Q15 compared to 3Q15

7@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

6083 77 85 93

13930

26 4262 44

46

13

2633

26 38

35

3

1

6

6 4

3

0

50

100

150

200

250

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

Num

ber

of V

C in

vest

men

ts

VC investment volume in Europe and Israel by bracket

Mega (>100) Growth (20-100)Venture (8-20) Early Venture (2-8)

Corporate VC activity, by bracket• Excluding seed deals, the

total number of corporate VC investments was 42 in 4Q15, double the number of corporate VC investments in 3Q15

• Corporate VC activity in Europe & Israel hit the highest level since this data set was started

8@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

6 4 5

16

7

224

3

9

12

7

12

44

7

8

7

7

3

1

0

5

10

15

20

25

30

35

40

45

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

Num

ber

of V

C in

vest

men

ts

Corporate VC investment volume in Europe and Israel by bracket

Mega (>100) Growth (20-100)Venture (8-20) Early Venture (2-8)

Corporate VC activity, by country• During the fourth quarter of

2015, Israel saw the highest number of corporate VC investments, with 15

• The UK saw 7 corporate VC investments during that period

• Twelve other countries saw corporate VC activity across Europe, but at much lower levels

9@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

10

31 1 1 1 1 1 1 1 1

3

3

1 1 2 11

2

2 1 1

1

1

0

2

4

6

8

10

12

14

16

Israe

l

UK

Fran

ce

Spai

n

Germ

any

Swed

en

Norw

ay

Esto

nia

Finl

and

Switz

erla

nd

Belg

ium

Litua

nia

Aust

ria

Neth

erla

nds

Num

ber

of in

vest

men

ts

Number of corporate VC investments in Europe and Israel by bracket(4Q15)

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8)

Average round size• Previously, I presented this broken

down by bracket, but I think the data is more meaningful when taken in aggregate.

• This average excludes seed rounds and mega rounds, so it reflects all rounds done in Europe & Israel between $2M and $100M

• From February to June, average round sizes across all venture rounds were hovering between $10M and $12M

• The third quarter saw consistently higher average round sizes –between $13M and $14.5M on average

• In the fourth quarter, however, the trend reversed itself, with average round sizes dropping to $11M in October, $10.5M in November, and $9.2M in December

10@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

11.1

17.6

6.8

11.7 11.3

12.7

15.8

11.211.9

11.110.1

11.4

13.913.2 14.6

11.110.5

9.2

4

6

8

10

12

14

16

18

20

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

Amou

nt In

vest

ed (U

S $M

)

Average investment size in Europe and Israel(Round sizes of 2-100M)

Total venture investment by country, 4Q 2015• The UK again took the top

spot in 4Q15 with over $900M in total capital invested

• Israel took second place with just under $700M in venture capital investment

• Germany captured third place, with $341M, and France was a strong fourth place at $225M

11@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

922.0699.0

341.1224.7

112.0103.1

90.483.6

53.753.5

41.034.029.5

22.617.5

8.05.05.05.02.72.30.4

UKIsrael

GermanyFrance

SpainDenmark

SwitzerlandSwedenIrelandFinland

BelgiumIceland

LituaniaNetherlands

NorwayEstonia

BucharestAustria

ItalyPortugal

PolandCzech

0 100 200 300 400 500 600 700 800 900 1,000

Total VC investment volume by country, 4Q15 (US $M)

Total venture investment by country, 2015• When 2015 is looked at as a

whole, the UK took the top spot, at $3.3B

• Israel came in second with $2.8B

• Germany, France, and Sweden rounded out the top five

• Spain, Denmark, the Netherlands, and Ireland each saw over $200M in VC investment during 2015

12@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

3,335.32,786.6

1,921.61,167.9

950.8450.4

264.2242.3236.8

161.9146.0

122.955.142.538.235.635.429.529.324.612.6

UKIsrael

GermanyFrance

SwedenSpain

DenmarkNetherlands

IrelandFinland

SwitzerlandBelgiumEstonia

PortugalNorwayGreeceIceland

LituaniaItaly

PolandSlovenia

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000

Total VC investment volume by country, 2015 (US $M)(countries with over $10M in VC investment)

Total venture investment by country, 2015(excluding mega rounds)• When mega-rounds

($100M+) are excluded, Israel saw more VC investment than the UK in 2015

• Excluding mega-rounds, Germany was a solid third place with $1.3B raised in 2015, roughly half of Israel’s figure, but nearly twice France, which saw $853M

13@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

2,344.62,222.3

1,318.0852.9

424.8350.4

264.2242.3236.8

161.9146.0

122.955.142.538.235.635.429.529.324.612.6

IsraelUK

GermanyFrance

SwedenSpain

DenmarkNetherlands

IrelandFinland

SwitzerlandBelgiumEstonia

PortugalNorwayGreeceIceland

LituaniaItaly

PolandSlovenia

0 500 1,000 1,500 2,000 2,500

Total VC investment volume by country, 2015(Excludes mega-rounds, US $M, countries with over $10M in VC investment)

Total venture investment by country, 3Q14 to 3Q15• To get a better sense of VC

volumes in various countries, this analysis excludes mega-rounds

• Investment volumes increase in all of the top five markets

• Of the top five markets, only Israel showed an increase in 4Q compared to 3Q

14@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

315

567543

475

628

699

369

267

719

437

621

444

180

284

389

209

379341

29

163118

232279

225

74 12389

112140

84

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr40

100

200

300

400

500

600

700

800

Tota

l VC

inve

stm

ent (

US $

M)

Total VC investment, 3Q14 - 4Q15 (top 5 countries, excluding mega-rounds)

IsraelUKGermanyFranceSweden

Average venture round sizes, by region• This analysis excludes mega-

rounds and rounds less than $2M

• In 4Q, DACH companies raised the largest rounds on overage

• When we compare 4Q15 to 4Q14, the trend is mixed –round sizes in Israel, DACH, and the Nordics decreased, while other regions saw larger round sizes

• Overall, the trend towards round size convergence seems to be continuing

15@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

Benelux, 4.7 Benelux, 4.5

DACH, 14.9

DACH, 12.5

France, 8.2France, 9.2

Iberia, 7.2

Iberia, 9.4

Israel, 15.9

Israel, 11.5Nordic, 11.5

Nordic, 8.0UK & Ireland, 8.5

UK & Ireland, 11.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Qtr4 Qtr4

2014 2015

Aver

age

roun

d si

ze (U

S $M

)

Average investment size in Europe and Israel (rounds of $2-100M)

Total venture investment by region, 2015• When VC investments across

Europe are aggregated into regions, UK & Ireland, Israel, DACH, the Nordics, and France are the clear and consistent leaders

• Benelux, Iberia, Southern Europe, and Eastern Europe do produce meaningful VC investments, but the volumes are still low

16@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

UK & Ireland, 3,572.1, 29%

Israel, 2,786.6, 23%DACH, 2,073.9, 17%

Nordic, 1,541.5, 13%

France, 1,167.9, 10%

Iberia, 493.0, 4%

Benelux, 365.2, 3%

South. Eur., 78.3, 1%

East. Eur., 37.7, 0%

Total VC investment by region, 2015

Rounds by bracket & region• To get a better sense of deal

volume, this analysis excludes seed deals which are often poorly reported

• Excluding seed deals, Israel led in the number of announced deals, with 60 investments announced

• The UK & Ireland took second place with 45

• The Nordics took third place with 38, overtaking DACH with 34

17@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

3224

29

19 1610 7

1 1

17

11 3

10

2

12

11

76

5

4

2

3

0

10

20

30

40

50

60

70

Israel UK &Ireland

Nordic DACH France Benelux Iberia East. Eur. South. Eur.

Num

ber

of in

vest

men

ts

Number of investments in Europe and Israel by bracket, 4Q 2015

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8)

Investment by region, by bracket• When the three massive UK-

based mega-rounds are excluded, Israel takes first place in 4Q investment volume

• Excluding mega-rounds, the difference between UK & Ireland and DACH is not that great

18@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

120 83 85 85 64

226128 117

343

259224

191113

58

478

0

200

400

600

800

1,000

1,200

Israel UK &Ireland

DACH Nordic France Iberia Benelux East. Eur. South. Eur.

Tota

l am

ount

inve

sted

(US

$M)

Investment in Europe and Israel by bracket by region, 4Q 2015(ranked excluding mega-rounds)

Mega (>100) Growth (20-100) Venture (8-20) Early Venture (2-8) Seed (<2)

Participation rate of US VC firms, by bracket• US VC firms are increasingly

active in the European and Israeli VC markets

• Year to date, US VC firms participated in 14% of the venture rounds in Europe

• US VCs participated in only 5% of seed rounds, 9% of early venture rounds, and 22% of venture rounds

• As a company moves from bracket to bracket, the chance of US VC participation doubles with each bracket change

19@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

5% 9%22%

39%

68%

95% 91%78%

61%

32%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Seed (.5-2) Early Venture (2-8) Venture (8-20) Growth (20-100) Mega (>100)

Perc

enta

ge o

f rou

nds

Did US VC firms participate in European VC rounds? (2015)

No Yes

Rate of participation by US firms has recovered• US VC firm participation in

European & Israeli venture rounds dropped in 4Q15 to 17%, down from 21% in 3Q

• In fact, 4Q15 saw the lowest US VC participation rate since I started tracking the data in 3Q14

20@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

16%24% 20% 22% 21% 17%

84%76% 80% 78% 79% 83%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

Perc

enta

ge o

f Rou

nds

Did US VC firms participate in European VC rounds?(Excludes seed rounds, 3Q14-4Q15)

No Yes

Participation of US VC firms by country• In 4Q, US VCs firms were

active in 11 different European countries, down from 14 in 3Q

• US VC firms were most active in Israel, where they participated in 14 investment rounds out of 71 (20%)

• Germany saw 7 investments with US VC participation

• The UK saw 6 investments with US VC participation, down from 7 in 3Q

• In Ireland, 2 of 3 VC investments involved a US VC

21@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

147 6 3 2 2 2 2 1 1 10

10

20

30

40

50

60

70

80

Israe

l

Germ

any

UK

Spai

n

Irela

nd

Icel

and

Switz

erla

nd

Finl

and

Litua

nia

Belg

ium

Fran

ce

Num

ber

of V

C in

vest

men

ts

In which countries are US VCs most active?4Q, 2015

No US VC involved US VC involved

Participation of US VC firms by country• This chart shows US VC

activity within Europe throughout 2015

• The bulk of US VC activity is in Israel, the UK & Ireland, DACH, and the Nordics

22@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

Israel, 12 Israel, 14 Israel, 14 Israel, 14

UK & Ireland, 10

UK & Ireland, 13UK & Ireland, 9 UK & Ireland, 8

DACH, 8

DACH, 6

DACH, 4DACH, 9

Nordic, 2

Nordic, 3

Nordic, 5

Nordic, 5Iberia, 3

Iberia, 4 Iberia, 3Benelux, 5

France, 3

France, 2East. Eur., 2

South. Eur., 2

0

5

10

15

20

25

30

35

40

45

50

Qtr1 Qtr2 Qtr3 Qtr4

2015

Num

ber

of V

C in

vest

men

ts

Investments with US VC participation, 2015

South. Eur. East. Eur.

France Benelux

Iberia Nordic

DACH UK & Ireland

Israel

Dimension Categories Explanation/Example

1. Target market Consumer, SMB, Enterprise, Government, Telecom, OEM

What sort of customer does the company target?

2. Vertical marketAdtech, Communications, Data, Development, Durables, Education, Electronics, Employment, Energy, Fashion, Financial, Food, Gaming, Health, HMI, Industrial, Infrastructure, Lifestyle, Logistics, Marketing, Media, Productivity, Real Estate, Security, Sports, Storage, Transportation, Travel, Water

What type of problem does the company solve?

3. Business modelCommerce, Components, Content, Marketplace, SaaS, Semiconductors, Services, Software, Systems,

How does the company makemoney? What are customers paying for?

Segment descriptor Consumer + Travel + Marketplace AirBnB has built a travel-related marketplace for consumers

Three-dimensional approach to sector mapping

• Excluding mega-rounds, investment activity decreased in consumer and increased in enterprise in 4Q compared with 3Q

• Enterprise-oriented investments hit a new high of $1.1B in 3Q

• SMB-oriented and OEM-oriented investment volume both decreased compared to 3Q, but remained at elevated levels compared to previous quarters

24@gdibnerblog: yankeesabralimey

What target markets are attracting the most VC investment in Europe & Israel?

Syndicate for European & Israeli Enterprise Companies

475 595980 850

1,177906

494

798

953814

9071,112

78

133

121

153

275135

78

114

47106

182

150

0

500

1,000

1,500

2,000

2,500

3,000

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

Tota

l VC

inve

stm

ents

(US

$M)

European & Israeli venture financing by target market3Q14 to 4Q15 (excluding mega-rounds, US $M)

Series A

Government

Telecom

OEM

SMB

Enterprise

Consumer

• When Israel is excluded from the sample, 56% of all VC dollars in Europe went to consumer-oriented companies

• OEM-oriented companies continued to rise slightly in importance, accounting for 5% of all VC dollars in Europe

25@gdibnerblog: yankeesabralimey

Consumer investment leads Europe

Syndicate for European & Israeli Enterprise Companies

62%

36%

56% 63% 62% 56%

18%

49%

34% 22% 24% 32%

6%10% 4% 12% 8% 6%5%4% 2% 4% 5%6%8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

European venture financing by target market3Q14 to 4Q15 (excluding Israel, percent of US $M)

Government Telecom OEM SMB Enterprise Consumer

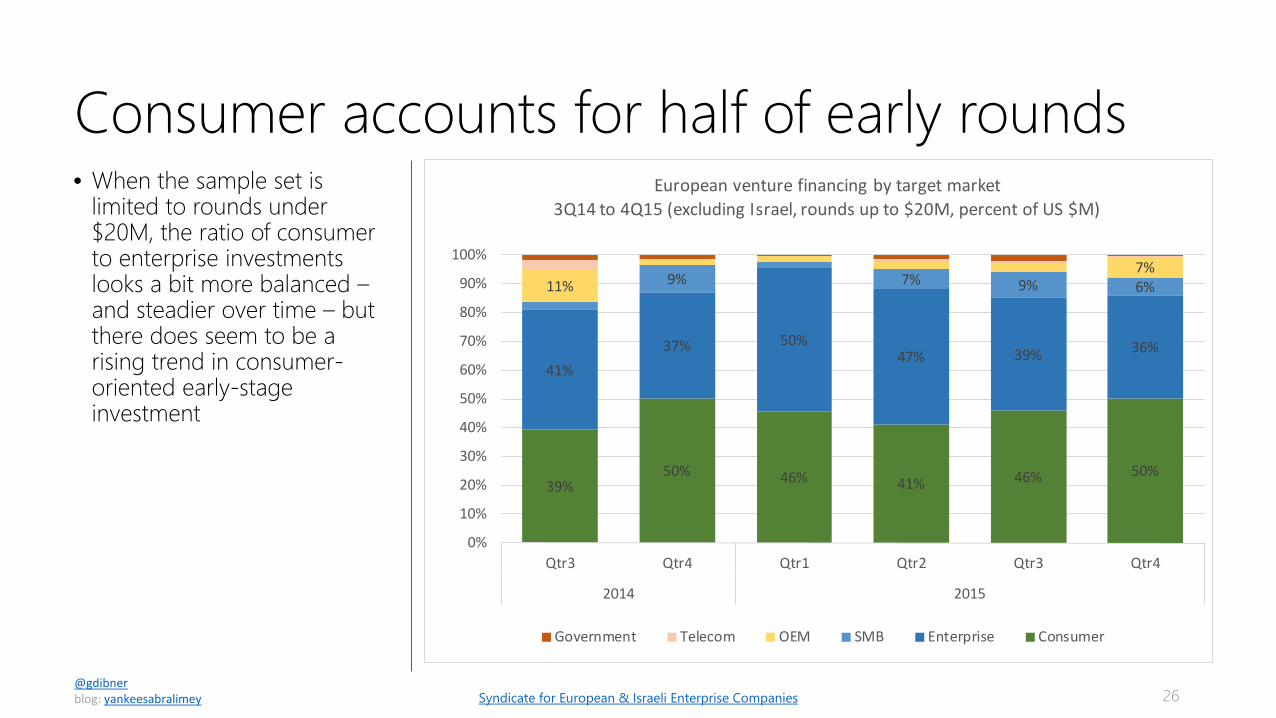

• When the sample set is limited to rounds under $20M, the ratio of consumer to enterprise investments looks a bit more balanced –and steadier over time – but there does seem to be a rising trend in consumer-oriented early-stage investment

26@gdibnerblog: yankeesabralimey

Consumer accounts for half of early rounds

Syndicate for European & Israeli Enterprise Companies

39%50% 46% 41% 46% 50%

41%37% 50%

47% 39% 36%

9% 7% 9% 6%11%7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

European venture financing by target market3Q14 to 4Q15 (excluding Israel, rounds up to $20M, percent of US $M)

Government Telecom OEM SMB Enterprise Consumer

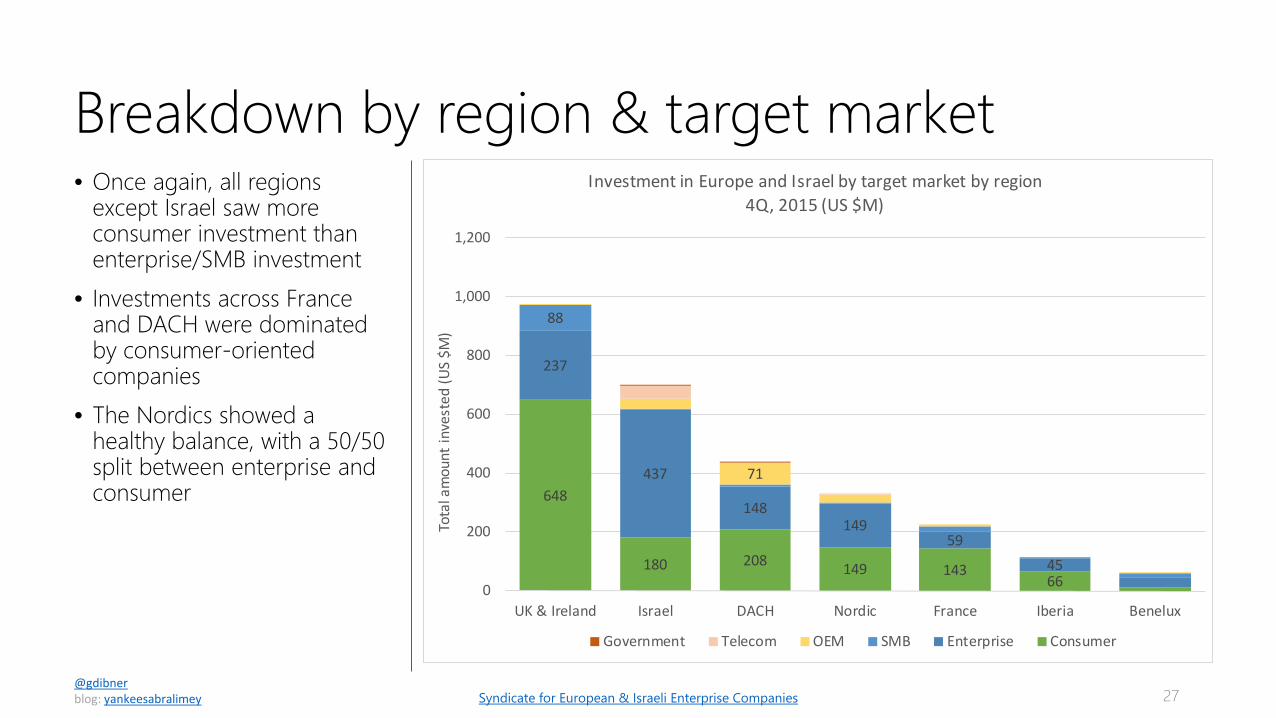

Breakdown by region & target market• Once again, all regions

except Israel saw more consumer investment than enterprise/SMB investment

• Investments across France and DACH were dominated by consumer-oriented companies

• The Nordics showed a healthy balance, with a 50/50 split between enterprise and consumer

27@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

648

180 208 149 14366

237

437

148149

5945

88

71

0

200

400

600

800

1,000

1,200

UK & Ireland Israel DACH Nordic France Iberia Benelux

Tota

l am

ount

inve

sted

(US

$M)

Investment in Europe and Israel by target market by region4Q, 2015 (US $M)

Government Telecom OEM SMB Enterprise Consumer

Distribution of investment rounds by country• Across Europe & Israel, 46%

of VC investment rounds were in consumer companies in 2015

• In DACH, 56% of rounds were into consumer companies, the highest proportion of any region except Iberia, where the number was 59%

• In UK, the number of consumer rounds was around 50% of the total

28@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

29%

41%

42%

47%

48%

50%

56%

59%

56%

47%

36%

39%

40%

39%

32%

27%

4%

14%

7%

8%

9%

7%

13%

8%

5%

3%

3%

1%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Israel

South. Eur.

Benelux

Nordic

France

UK & Ireland

DACH

Iberia

Investment in Europe and Israel by target market by country2015 (Number of investments)

Consumer Enterprise SMB OEM Telecom Government

Growth rounds by target market• From 4Q14 to 2Q15, there

was an upward trend towards consumer-oriented companies in growth investing, but this trend reversed itself in 3Q15 and continued into 4Q15

• For the first time, enterprise companies accounted for 50% of all growth rounds in Europe & Israel

29@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

56%

37%46%

56%43% 39%

25%

41%

46% 25%38% 50%

6% 7%

5%

9% 12%6% 11% 6% 7% 5%6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

Investment in Europe and Israel by target market(Rounds over $20M, number of investments)

Government Telecom OEM SMB Enterprise Consumer

• Marketing was the most popular vertical across Europe & Israel, with 33 investments in the category

• Security was second, with 25• Finance dropped to third

place, from first last quarter• Lifestyle (which is a catch-all

consumer category) took the fourth slot

• IT Infrastructure and health took the fourth and fifth slots

30@gdibnerblog: yankeesabralimey

Finance returned to being the top vertical

Syndicate for European & Israeli Enterprise Companies

Marketing, 33

Security, 25

Financial, 22

Lifestyle, 20Infrastructure, 17

Health, 17

Development, 16

Logistics, 16

Electronics, 16

Fashion, 14

Adtech, 13

Data, 13

Food, 12

Employment, 12

Education, 10Productivity, 10Social, 9Gaming, 9

Communications, 9Entertainment, 8Real Estate, 8Payments, 7Industrial, 7

Travel, 6SCM, 5

Energy, 5

European & Israeli venture financing by target market4Q 2015 (number of investments)

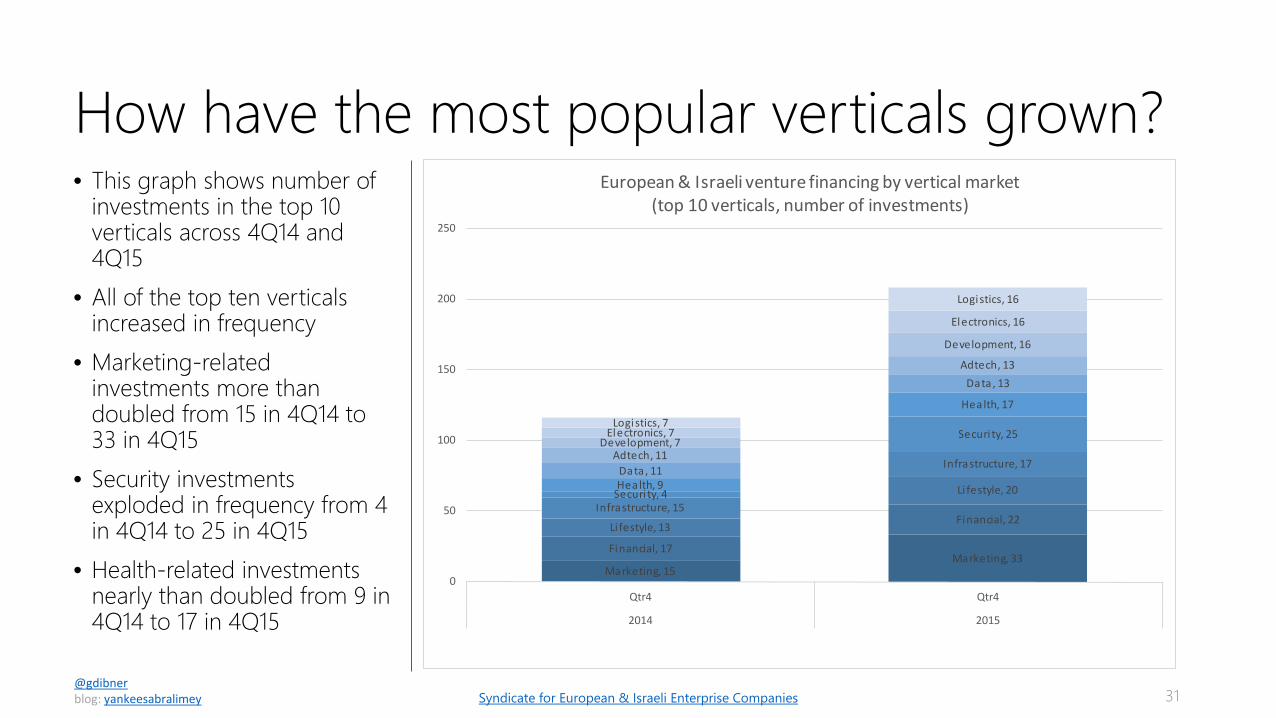

• This graph shows number of investments in the top 10 verticals across 4Q14 and 4Q15

• All of the top ten verticals increased in frequency

• Marketing-related investments more than doubled from 15 in 4Q14 to 33 in 4Q15

• Security investments exploded in frequency from 4 in 4Q14 to 25 in 4Q15

• Health-related investments nearly than doubled from 9 in 4Q14 to 17 in 4Q15

31@gdibnerblog: yankeesabralimey

How have the most popular verticals grown?

Syndicate for European & Israeli Enterprise Companies

Marketing, 15Marketing, 33

Financial, 17

Financial, 22Li festyle, 13

Li festyle, 20Infrastructure, 15

Infrastructure, 17

Securi ty, 4

Securi ty, 25

Health, 9

Health, 17

Data, 11

Data, 13

Adtech, 11

Adtech, 13

Development, 7

Development, 16

Electronics, 7

Electronics, 16

Logistics, 7

Logistics, 16

0

50

100

150

200

250

Qtr4 Qtr4

2014 2015

European & Israeli venture financing by vertical market(top 10 verticals, number of investments)

• Marketing was the most frequently funded vertical, with enterprise-oriented marketing taking the lion’s share within that category

• Security took second place with a heavy emphasis on enterprise security

• Finance dropped to third place, with most of the activity in the consumer finance space, followed by SMB finance

• IT infrastructure and health tech made strong showings

• Consumer lifestyle, electronics, and fashion also made the top ten verticals

32@gdibnerblog: yankeesabralimey

Which verticals for which segments?

Syndicate for European & Israeli Enterprise Companies

Fashion

Electronics

Logistics

Development

Health

Infrastructure

Lifestyle

Financial

Security

Marketing

0 5 10 15 20 25 30 35

European & Israeli venture financing by target market4Q, 2015 (number of investments, top 10 verticals)

Consumer

Enterprise

SMB

OEM

Telecom

Government

• This chart shows the ten most commonly funded verticals across Europe & Israel by quarter

• Marketing, security, and logistics, developer tooling show continued strength

• Health and adtech seem to have rebounded as areas of investor interest

33@gdibnerblog: yankeesabralimey

The most popular verticals in the past 12 months

Syndicate for European & Israeli Enterprise Companies

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

0

50

100

150

200

250

European & Israeli venture financing by vertical market(number of investments, top 10 verticals)

Marketing

Financial

Lifestyle

Infrastructure

Security

Adtech

Electronics

Health

Logistics

Development

• Lifestyle, which is admittedly a bit of a catch-all consumer category, continues to show tremendous strength in terms of VC volume

• Finance took the second place overall

• Health showed significant strength in 4Q

• Electronics (which typically means consumer electronics systems companies) seems to have rebounded

• Gaming, travel, and food-related categories whichedseem to be declining in 3Q, seemed to recover in 4Q

• Consumer-oriented logistics plays seem to be emerging as an important category for VC investment

34@gdibnerblog: yankeesabralimey

Consumer VC investment trends

Syndicate for European & Israeli Enterprise Companies

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

0

20

40

60

80

100

120

140

European & Israeli venture financing by consumer verticals(number of investments, top 10 verticals)

Lifestyle

Financial

Fashion

Gaming

Health

Travel

Social

Food

Logistics

Electronics

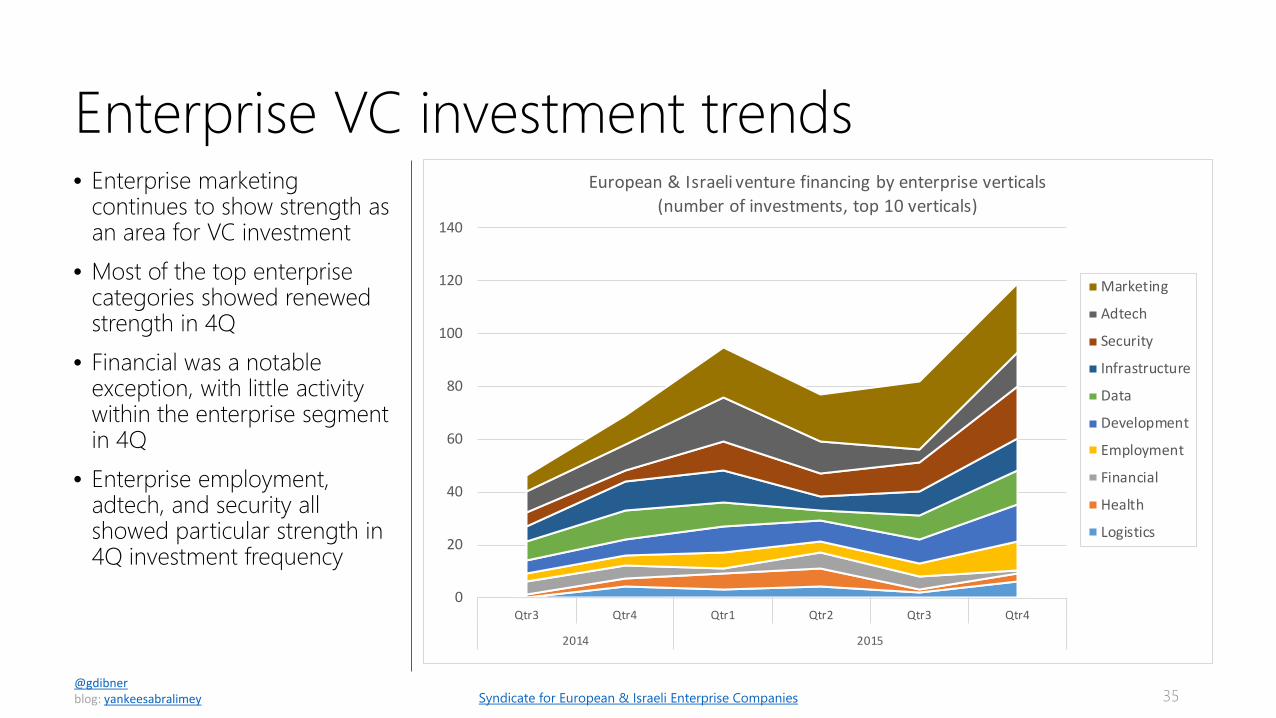

• Enterprise marketing continues to show strength as an area for VC investment

• Most of the top enterprise categories showed renewed strength in 4Q

• Financial was a notable exception, with little activity within the enterprise segment in 4Q

• Enterprise employment, adtech, and security all showed particular strength in 4Q investment frequency

35@gdibnerblog: yankeesabralimey

Enterprise VC investment trends

Syndicate for European & Israeli Enterprise Companies

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

0

20

40

60

80

100

120

140

European & Israeli venture financing by enterprise verticals(number of investments, top 10 verticals)

Marketing

Adtech

Security

Infrastructure

Data

Development

Employment

Financial

Health

Logistics

• Security retained the top spot in Israel, with 16 investments including 2 consumer-oriented investments

• Israel also saw 8 investments in IT infrastructure and 8 investments in the marketing vertical

• Communications and big data were the fourth and fifth most frequently funded categories

• Development tooling finally cracked the top ten, with 3 investments in 4Q

36@gdibnerblog: yankeesabralimey

A closer look at Israeli venture in 4Q15

Syndicate for European & Israeli Enterprise Companies

Fashion

Financial

Electronics

Logistics

Development

Data

Communications

Marketing

Infrastructure

Security

0 2 4 6 8 10 12 14 16 18

Israeli venture financing by target market4Q, 2015 (number of investments, top 10 verticals)

Consumer

Enterprise

SMB

OEM

Telecom

Government

• Throughout 2015, security, marketing, and infrastructure were the most frequently funded categories in Israel

• Communications, fintech, and adtech also made good showings

• Interestingly, enterprise development tools and consumer electronics are now strong emerging categories in Israel

37@gdibnerblog: yankeesabralimey

A closer look at Israeli venture in 2015

Syndicate for European & Israeli Enterprise Companies

Electronics

Development

Logistics

Productivity

Adtech

Financial

Communications

Infrastructure

Marketing

Security

0 5 10 15 20 25 30 35 40 45

Israeli venture financing by target market2015 (number of investments, top 10 verticals)

Consumer

Enterprise

SMB

OEM

Telecom

Government

• For the fourth quarter running, Fintech was the dominant category of investment in the UK, but this quarter the differential was much less than in 3Q

• Enterprise employment and enterprise marketing were also important categories

• As usual, consumer-oriented companies dominated most categories of VC funding across the UK

• Adtech and gaming did not crack the top ten

38@gdibnerblog: yankeesabralimey

UK VCs dialed back on fintech in 4Q…a bit

Syndicate for European & Israeli Enterprise Companies

Food

Lifestyle

Fashion

Development

Payments

Real Estate

Education

Security

Marketing

Employment

Social

Financial

0 1 2 3 4 5 6

UK venture financing by target market4Q, 2015 (number of investments, top verticals)

Consumer

Enterprise

SMB

OEM

• When 2015 is looked at as a whole, fintech was the standout category in the UK, with more than twice the investment numbers as the second most popular category

• Enterprise marketing was the second most frequently funded category by UK VCs

• Consumer fashion was the third most popular category

39@gdibnerblog: yankeesabralimey

UK VCs focused on fintech in 2015

Syndicate for European & Israeli Enterprise Companies

Adtech

Lifestyle

Security

Infrastructure

Payments

Education

Employment

Fashion

Marketing

Financial

0 5 10 15 20 25 30 35 40

UK venture financing by target market2015 (number of investments, top verticals)

Consumer

Enterprise

SMB

OEM

• The top three categories in German VC investment in 3Q15 were consumer lifestyle, consumer travel, and enterprise development tools

• In total, the top 10 categories in Germany generated 31 investments, 15 of which were in consumer companies

40@gdibnerblog: yankeesabralimey

The German VC market in 4Q15

Syndicate for European & Israeli Enterprise Companies

HMI

Adtech

Food

Communications

Energy

Logistics

SCM

Marketing

Fashion

Payments

Industrial

Health

Real Estate

Infrastructure

Financial

Electronics

Lifestyle

Travel

Development

0 1 2 3 4

German venture financing by target market4Q, 2015 (number of investments, top 10 verticals)

Consumer

Enterprise

SMB

OEM

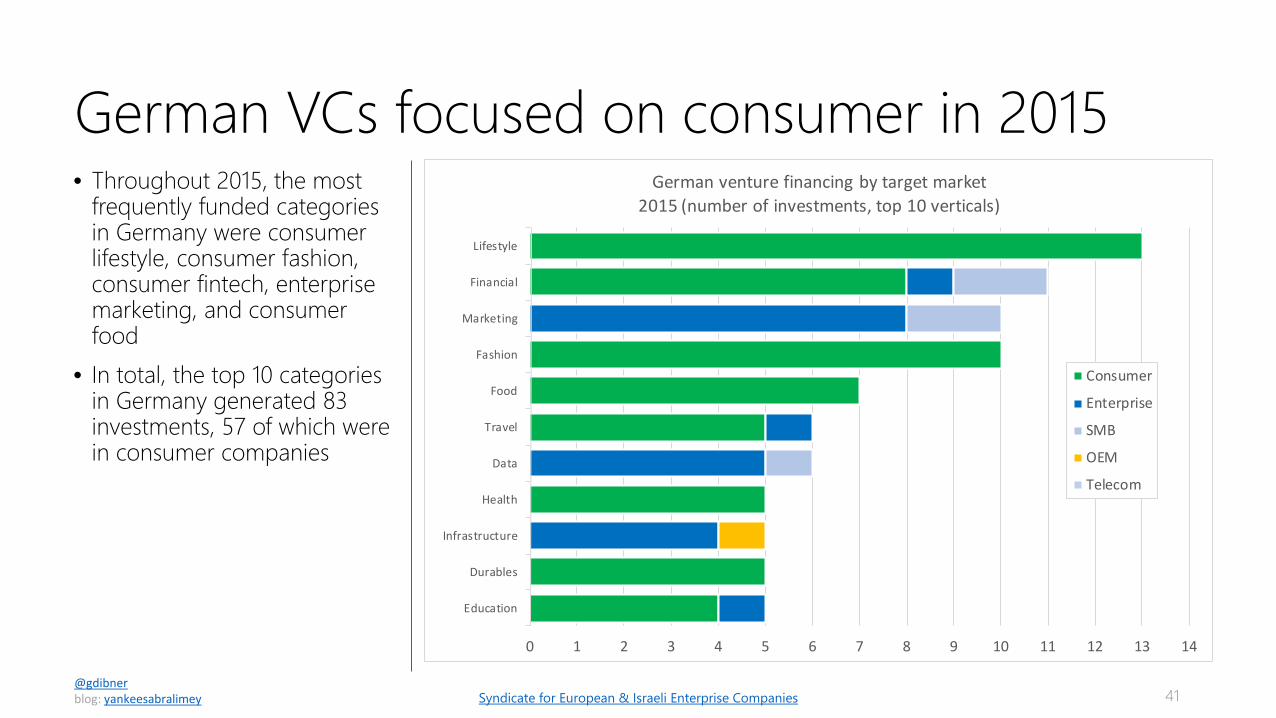

• Throughout 2015, the most frequently funded categories in Germany were consumer lifestyle, consumer fashion, consumer fintech, enterprise marketing, and consumer food

• In total, the top 10 categories in Germany generated 83 investments, 57 of which were in consumer companies

41@gdibnerblog: yankeesabralimey

German VCs focused on consumer in 2015

Syndicate for European & Israeli Enterprise Companies

Education

Durables

Infrastructure

Health

Data

Travel

Food

Fashion

Marketing

Financial

Lifestyle

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14

German venture financing by target market2015 (number of investments, top 10 verticals)

Consumer

Enterprise

SMB

OEM

Telecom

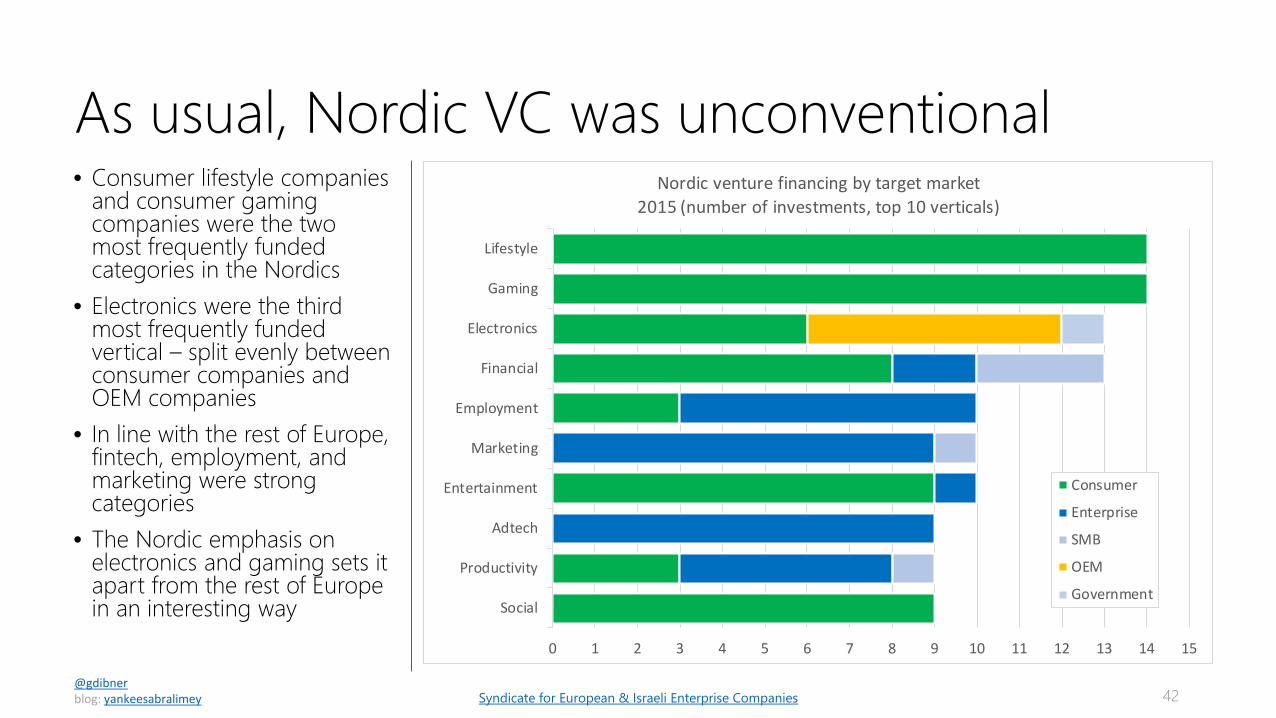

• Consumer lifestyle companies and consumer gaming companies were the two most frequently funded categories in the Nordics

• Electronics were the third most frequently funded vertical – split evenly between consumer companies and OEM companies

• In line with the rest of Europe, fintech, employment, and marketing were strong categories

• The Nordic emphasis on electronics and gaming sets it apart from the rest of Europe in an interesting way

42@gdibnerblog: yankeesabralimey

As usual, Nordic VC was unconventional

Syndicate for European & Israeli Enterprise Companies

Social

Productivity

Adtech

Entertainment

Marketing

Employment

Financial

Electronics

Gaming

Lifestyle

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Nordic venture financing by target market2015 (number of investments, top 10 verticals)

Consumer

Enterprise

SMB

OEM

Government

• As software eats the world, services are becoming an increasingly important business model for venture-backed startups

• This was certainly the case in 2015, with services taking 26% of the venture dollars invested in Europe & Israel

• SaaS emerged as the second most funded business model in 2015

• Commerce continues to be important, with 17% of the financing in 2015

• Marketplaces – business that serve a price discovery function – were 9%

43@gdibnerblog: yankeesabralimey

Services & SaaS dominated 2015

Syndicate for European & Israeli Enterprise Companies

Services, 2,331, 26%

SaaS, 1,969, 22%

Commerce, 1,497, 17%

Software, 1,343, 15%Marketplace, 768, 9%

Systems, 472, 5%

Media, 406, 4%

Components, 125, 1%

Semiconductors, 106, 1%

European & Israeli venture financing by target market2015 (in US $M) (excluding mega-rounds)

• SaaS jumped to a record-setting first place, at $655M in funding in 4Q15

• Services dropped to second with $480M

• Commerce took a major hit, dropping nearly 50% from 3Q

• Marketplaces recovered a bit in terms of investment volume

44@gdibnerblog: yankeesabralimey

In 4Q, SaaS set a record

Syndicate for European & Israeli Enterprise Companies

0

100

200

300

400

500

600

700

800

Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4

2014 2015

European & Israeli venture financing by business model(top five, in US $M, excluding mega-rounds)

Services

SaaS

Software

Commerce

Marketplace

US VCs focused on SaaS & services• Throughout 2015, US VC

interest was skewed heavily towards SaaS, Software & Services models

• Markets, commerce, and media investments also attracted US VC interest, but at much lower levels

45@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

47 43 32 15 12

259232

147

11995

72 80

0

50

100

150

200

250

300

350

SaaS Services Software Commerce Marketplace Media Systems Components Semiconductors

VC Investments in Europe & Israel2015 (number of investments)

No US VC involved US VC involved

• Enterprise marketing SaaS was by far the most popular segment for VC investment in 2015 with 72 investments across the region

• Consumer financial services were next, with 42 investments

• Enterprise security software was third, with 36 investments

46@gdibnerblog: yankeesabralimey

Enterprise marketing & consumer fintech

Syndicate for European & Israeli Enterprise Companies

0 10 20 30 40 50 60 70 80

Enterprise CRM SaaS

Consumer Travel Commerce

Enterprise Infrastructure SaaS

Enterprise Data Software

Consumer Education Services

Consumer Food Commerce

Consumer Gaming Software

Enterprise Employment SaaS

Enterprise Development SaaS

SMB Financial Services

Consumer Electronics Systems

Enterprise Adtech Services

Consumer Social Media

Consumer Lifestyle Commerce

Consumer Fashion Commerce

Enterprise Security Software

Consumer Financial Services

Enterprise Marketing SaaS

Number of VC investments

Investment in Europe & Israel by segment by country2015 (segments with 15 or more investments)

UK & Ireland IsraelNordic DACHFrance BeneluxIberia South. Eur.East. Eur.

• Across Europe & Israel, US VC firms invested in 74 enterprise companies, 49 consumer companies, 4 SMB companies, and 4 OEM-oriented companies

• Enterprise SaaS & Software attracted by far more US VC interest than any other space

47@gdibnerblog: yankeesabralimey

What business models attract US VC investments?

Syndicate for European & Israeli Enterprise Companies

0 5 10 15 20 25 30 35

Systems

Components

Semiconductors

Services

SaaS

SaaS

Systems

Software

Media

Marketplace

Commerce

Services

Services

Software

SaaS

OEM

SMB

Cons

umer

Ente

rpris

e

US VC Investments in Europe and Israel by end market, business model, & country, 2015 (excludes seed & mega-rounds)

Israel

UK & Ireland

DACH

Nordic

France

Iberia

Benelux

East. Eur.

South. Eur.

Show me the SaaS• The most popular category

by far for SaaS investments across the geography was marketing

• Development tools were the second most popular SaaS category

• Productivity SaaS applications came in third, with a focus on consumer and SMB offerings

• Employment SaaS was the fourth most frequently-funded category

48@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

0 10 20 30 40 50 60 70 80 90 100

ERP

Adtech

Health

Data

CRM

Infrastructure

Employment

Productivity

Development

Marketing

SaaS VC investment in Europe and Israelby vertical and target market, 2015 (top 10 verticals)

Consumer Enterprise Government SMB

Services investing in 2015• This graph shows the top ten

verticals within the services category in 2015 across Europe & Israel

• Financial services were far and away the most frequently funded category for VC investment in 2015 – mostly for consumers and SMBs

• Adtech was the second most funded services category in 2015

• Logistics and Education were the third and fourth place verticals

49@gdibnerblog: yankeesabralimey Syndicate for European & Israeli Enterprise Companies

0 10 20 30 40 50 60 70 80

Gaming

Employment

Health

Marketing

Infrastructure

Communications

Payments

Education

Logistics

Adtech

Financial

Services VC investment in Europe and Israelby vertical and target market, 2015 (top 10 verticals)

Consumer Enterprise SMB Telecom

Based in , I was previously a partner at . Before that, I helped run the

European seed program for . I moved to London after seven years in

during which I worked as a VC with and . I’m originally from .

My VC investments include and . Angel investments include and many more.

If you found this useful, I hope you’ll subscribe to my blog.50

Gil DibnerTo invest in the best European & Israeli enterprise startups,

consider backing me on here. Lots of exciting stuff in thepipeline – and you’ll be in pretty good company.