Bladex's 4Q15 Conference Call Presentation

22

4Q15 Earnings Results February 19, 2016

-

Upload

bladex -

Category

Investor Relations

-

view

4.756 -

download

3

Transcript of Bladex's 4Q15 Conference Call Presentation

4Q15 Earnings Results February 19, 2016

Color

Scheme

234 93 46

109 179 63

235 235 235

0 75 141

253 185 36

Accent

Color

31 179 179

192 0 0

The information presented herein is based on reported un-audited

results for the year ended December 31, 2015, which have been

prepared following International Financial Reporting Standards

(“IFRS”) in adherence to a mandate for licensed Banks supervised by

the Superintendency of Banks of Panama, as the Bank completes its

transition from its previous accounting standard, US-GAAP. The Bank

has applied the provisions of IFRS 1 in presenting its financial results.

The Bank´s transition date is January 1, 2014, for which it has

prepared its opening consolidated statement of financial position under

IFRS as of that date, with comparative information provided as of

December 31, 2014 and December 31, 2015.

2

I. Transition to IFRS

• Basis of Consolidation: Previous GAAP established a variable interest entity (VIE) model and, for non-VIE, a voting

interest model. IFRS defines, and focuses on control as the basis for consolidation regardless of the form of the

investee, with the effect that Bladex’s former investment in the Bladex Asset Management Unit did not meet IFRS

consolidation criteria.

• Allowance for credit losses & impairment of investment securities: Under previous GAAP, allowances were based

on an incurred credit loss model. Under IFRS, and with the early-adoption of the IFRS 9 standard, the determination of

deterioration or improvement in the credit quality is based on forward-looking expected credit losses (over a 12-month

period or life-time, depending on the stage of impairment). The expected credit loss model is applied to a broader range

of debt instruments, including bonds.

• Hedging Derivatives: Previous GAAP allowed certain methods to simplify the determination of the effectiveness of

hedging relationships. Under IFRS, the level of ineffectiveness is determined for each transaction, and recorded in the

consolidated statement of income.

• Variable Compensation in Stock: Under previous GAAP, the straight-line attribution method was used to recognize

the compensation cost of awards with vesting periods. Under IFRS, recognition follows an accelerated amortization

pattern over the vesting period.

• Foreign Exchange Gains or Losses and Cumulative Translation Differences: While recorded in Other

Comprehensive Income under previous GAAP in the case of certain assets, IFRS prescribes recognition in the

consolidated statement of income. Upon first-time adoption, IFRS 1 allows a reset of cumulative translation differences

to zero as at the transition date.

Overall transition effects fairly limited, mainly due to the Bank’s

focused business model and short-dated book of business

Main effects on Bladex’s Financial Statements

3

III. Financial Performance Overview

• Net Income of $104.0 million, up +2% YoY from higher revenues, lower expenses and non-core gains from the

participation in investment funds, partially offset by higher provision and impairment loss for expected credit

losses on loans and investment securities (+$6.5 million).

• Business Net Income of $99.0 million (flat YoY).

• +3% increase in average Commercial Portfolio to $7.1 billion.

• +3% increase in Net Interest Income on 4% growth in average loans balances, as lending rates and average

funding costs remained stable.

• Fee income from the letter of credit business and loan structuring activities rises to $19.2 million (+10% YoY).

7 syndicated/club deal transactions successfully executed in 2015.

• Expenses drop -3% YoY, with Business Efficiency Ratio improving to 31%, Overall Efficiency Ratio to 30%.

• NIM at 1.84% (-4 bps YoY), mainly from higher average liquidity balances in the asset mix.

• Reserve coverage ratio increased 11 bps to 1.33% from 1.22% on higher expected credit losses. Non-

performing loan ratio increased temporarily to 0.78% on isolated exposure in Oil & Gas sector, with reduction to

0.42% on pre-payments received subsequent to date of close.

• Net Income of $23.2 million (-38%QoQ, -35% YoY), mainly from swing in results from particpation in investment

funds, and provision for, and impairment loss from, expected credit losses on loans and investment securities,

respectively.

• Business Net Income of $25.3 million (-17% QoQ, -16% YoY).

• Average Commercial Portfolio balances grew to $7.2 billion (+1%QoQ, -1%YoY).

• +2% QoQ increase in Net Interest Income on higher lending rates (+10 bps) and higher average loan balances

(+2%). -2% YoY decrease attributable to increased average funding costs (+16 bps) on higher average funding

tenors, with partial offset by increase in average loan balances (+1%) and lending rates (+10 bps).

• Fee income & other income (-6% QoQ, +9% YoY). QoQ decrease attributable to lower fees from syndicated

transactions, partially offset by higher net gain on sale of loans at amortized cost. YoY increase mainly

attributable to commissions from Letters of Credit and contingency business.

• NIM at 1.90% (+7 bps QoQ, -2 bps YoY) due to higher average balances and lending rates, offsetting increased

average funding costs from higher average funding tenors and LIBOR rates.

• Board declared $0.385 quarterly dividend per share.

Year 2015

$104.0 MM Net Income

(+2% YoY)

11.0% ROAE

10.4% Business ROAE

4Q15

$23.2 MM Net Income

(-38% QoQ, -35% YoY)

9.5% ROAE

10.4% Business ROAE

4

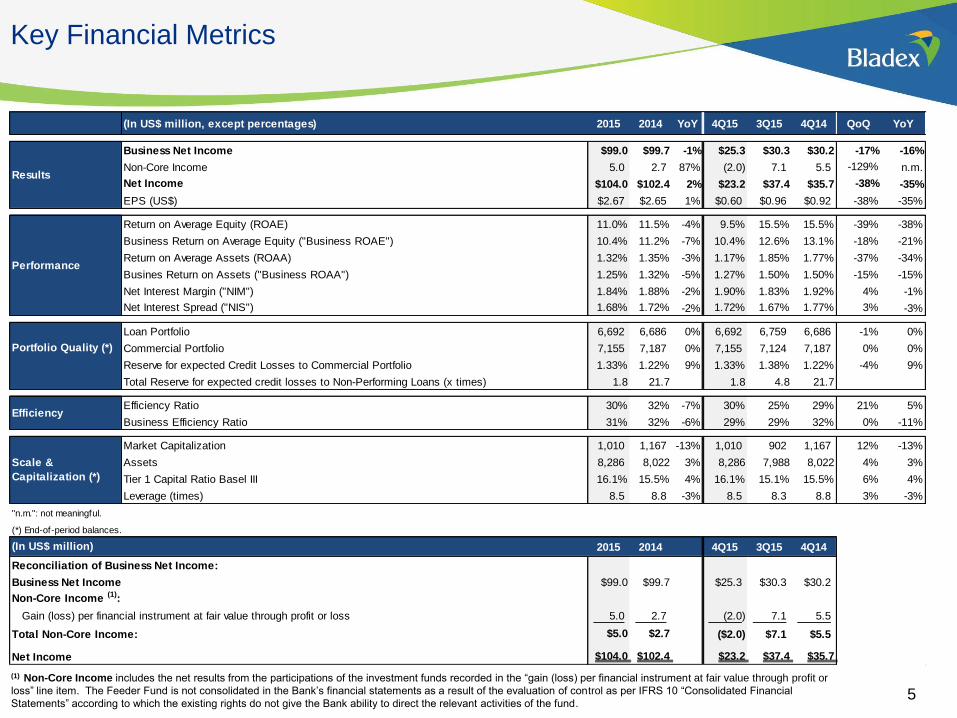

Key Financial Metrics

5

(1) Non-Core Income includes the net results from the participations of the investment funds recorded in the “gain (loss) per financial instrument at fair value through profit or

loss” line item. The Feeder Fund is not consolidated in the Bank’s financial statements as a result of the evaluation of control as per IFRS 10 “Consolidated Financial

Statements” according to which the existing rights do not give the Bank ability to direct the relevant activities of the fund.

(In US$ million, except percentages) 2015 2014 YoY 4Q15 3Q15 4Q14 QoQ YoY

Business Net Income $99.0 $99.7 -1% $25.3 $30.3 $30.2 -17% -16%

Non-Core Income 5.0 2.7 87% (2.0) 7.1 5.5 -129% n.m.

Net Income $104.0 $102.4 2% $23.2 $37.4 $35.7 -38% -35%

EPS (US$) $2.67 $2.65 1% $0.60 $0.96 $0.92 -38% -35%

Return on Average Equity (ROAE) 11.0% 11.5% -4% 9.5% 15.5% 15.5% -39% -38%

Business Return on Average Equity ("Business ROAE") 10.4% 11.2% -7% 10.4% 12.6% 13.1% -18% -21%

Return on Average Assets (ROAA) 1.32% 1.35% -3% 1.17% 1.85% 1.77% -37% -34%

Busines Return on Assets ("Business ROAA") 1.25% 1.32% -5% 1.27% 1.50% 1.50% -15% -15%

Net Interest Margin ("NIM") 1.84% 1.88% -2% 1.90% 1.83% 1.92% 4% -1%

Net Interest Spread ("NIS") 1.68% 1.72% -2% 1.72% 1.67% 1.77% 3% -3%

Loan Portfolio 6,692 6,686 0% 6,692 6,759 6,686 -1% 0%

Commercial Portfolio 7,155 7,187 0% 7,155 7,124 7,187 0% 0%

Reserve for expected Credit Losses to Commercial Portfolio 1.33% 1.22% 9% 1.33% 1.38% 1.22% -4% 9%

Total Reserve for expected credit losses to Non-Performing Loans (x times) 1.8 21.7 1.8 4.8 21.7

Efficiency Ratio 30% 32% -7% 30% 25% 29% 21% 5%

Business Efficiency Ratio 31% 32% -6% 29% 29% 32% 0% -11%

Market Capitalization 1,010 1,167 -13% 1,010 902 1,167 12% -13%

Assets 8,286 8,022 3% 8,286 7,988 8,022 4% 3%

Tier 1 Capital Ratio Basel III 16.1% 15.5% 4% 16.1% 15.1% 15.5% 6% 4%

Leverage (times) 8.5 8.8 -3% 8.5 8.3 8.8 3% -3%

"n.m.": not meaningful.

(*) End-of-period balances.

2015 2014 4Q15 3Q15 4Q14

Reconciliation of Business Net Income:

Business Net Income $99.0 $99.7 $25.3 $30.3 $30.2

Non-Core Income (1):

Gain (loss) per financial instrument at fair value through profit or loss 5.0 2.7 (2.0) 7.1 5.5

Total Non-Core Income: $5.0 $2.7 ($2.0) $7.1 $5.5

Net Income $104.0 $102.4 $23.2 $37.4 $35.7

Results

Portfolio Quality (*)

Efficiency

Scale &

Capitalization (*)

(In US$ million)

Performance

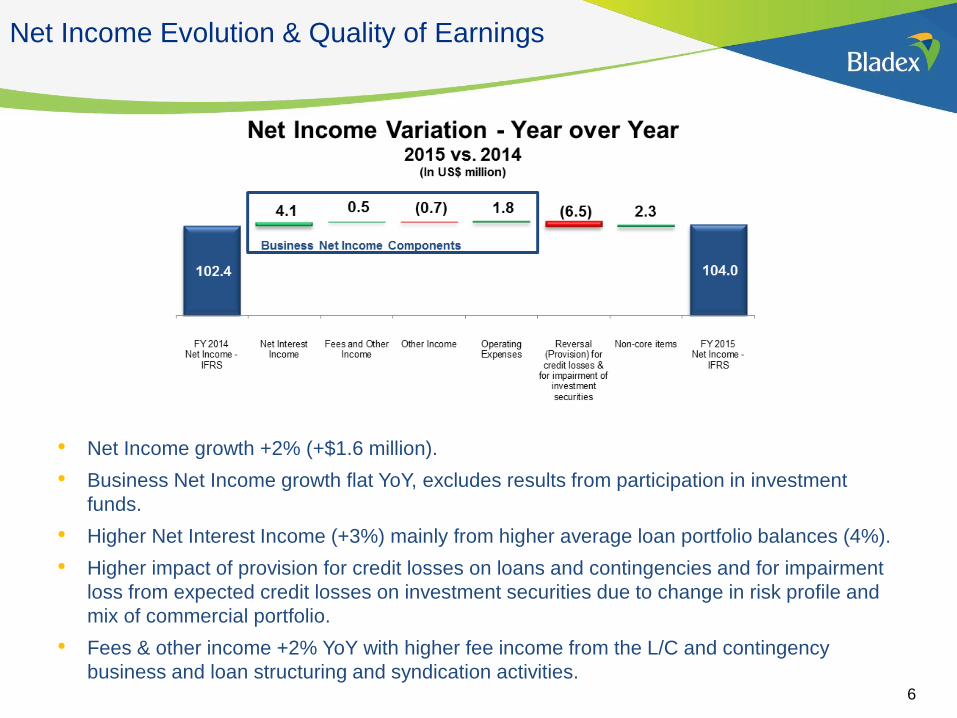

Net Income Evolution & Quality of Earnings

• Net Income growth +2% (+$1.6 million).

• Business Net Income growth flat YoY, excludes results from participation in investment

funds.

• Higher Net Interest Income (+3%) mainly from higher average loan portfolio balances (4%).

• Higher impact of provision for credit losses on loans and contingencies and for impairment

loss from expected credit losses on investment securities due to change in risk profile and

mix of commercial portfolio.

• Fees & other income +2% YoY with higher fee income from the L/C and contingency

business and loan structuring and syndication activities. 6

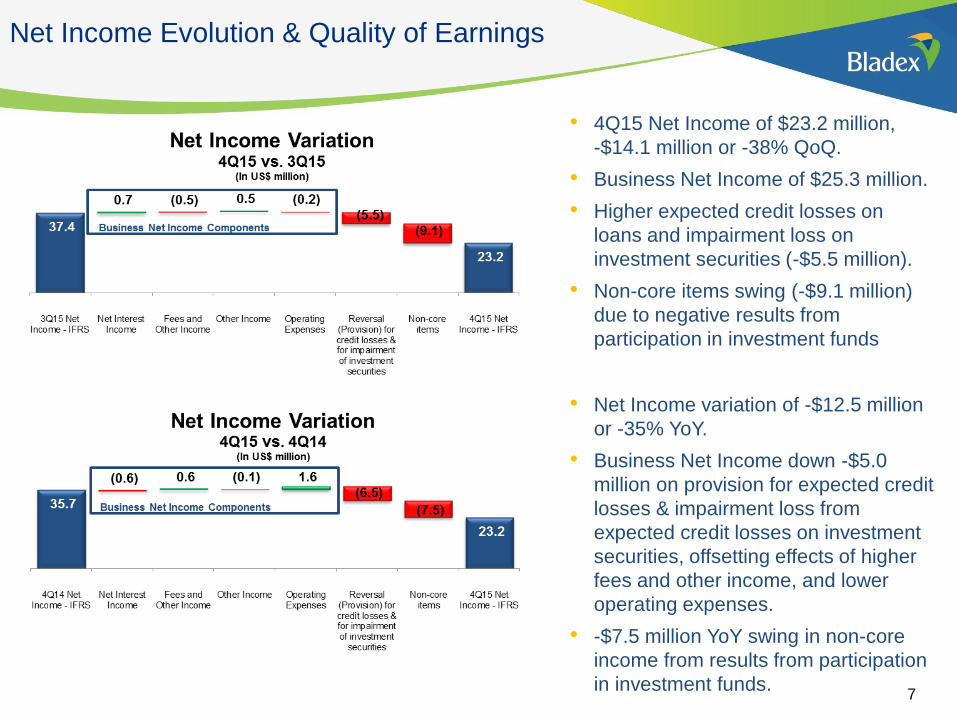

Net Income Evolution & Quality of Earnings

• 4Q15 Net Income of $23.2 million,

-$14.1 million or -38% QoQ.

• Business Net Income of $25.3 million.

• Higher expected credit losses on

loans and impairment loss on

investment securities (-$5.5 million).

• Non-core items swing (-$9.1 million)

due to negative results from

participation in investment funds

• Net Income variation of -$12.5 million

or -35% YoY.

• Business Net Income down -$5.0

million on provision for expected credit

losses & impairment loss from

expected credit losses on investment

securities, offsetting effects of higher

fees and other income, and lower

operating expenses.

• -$7.5 million YoY swing in non-core

income from results from participation

in investment funds. 7

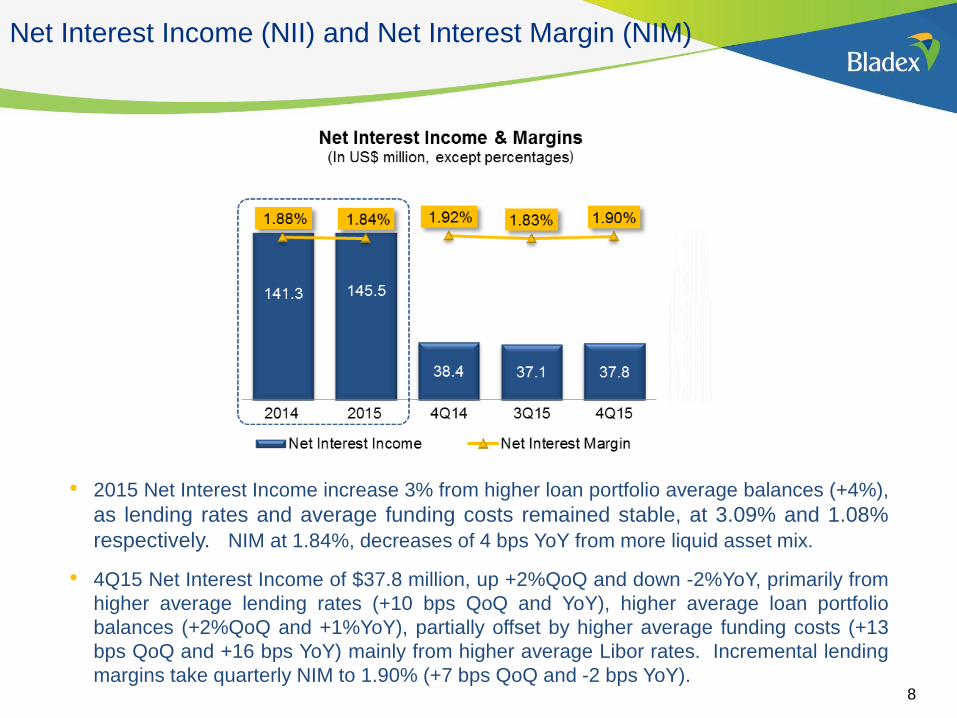

Net Interest Income (NII) and Net Interest Margin (NIM)

• 2015 Net Interest Income increase 3% from higher loan portfolio average balances (+4%),

as lending rates and average funding costs remained stable, at 3.09% and 1.08%

respectively. NIM at 1.84%, decreases of 4 bps YoY from more liquid asset mix.

• 4Q15 Net Interest Income of $37.8 million, up +2%QoQ and down -2%YoY, primarily from

higher average lending rates (+10 bps QoQ and YoY), higher average loan portfolio

balances (+2%QoQ and +1%YoY), partially offset by higher average funding costs (+13

bps QoQ and +16 bps YoY) mainly from higher average Libor rates. Incremental lending

margins take quarterly NIM to 1.90% (+7 bps QoQ and -2 bps YoY). 8

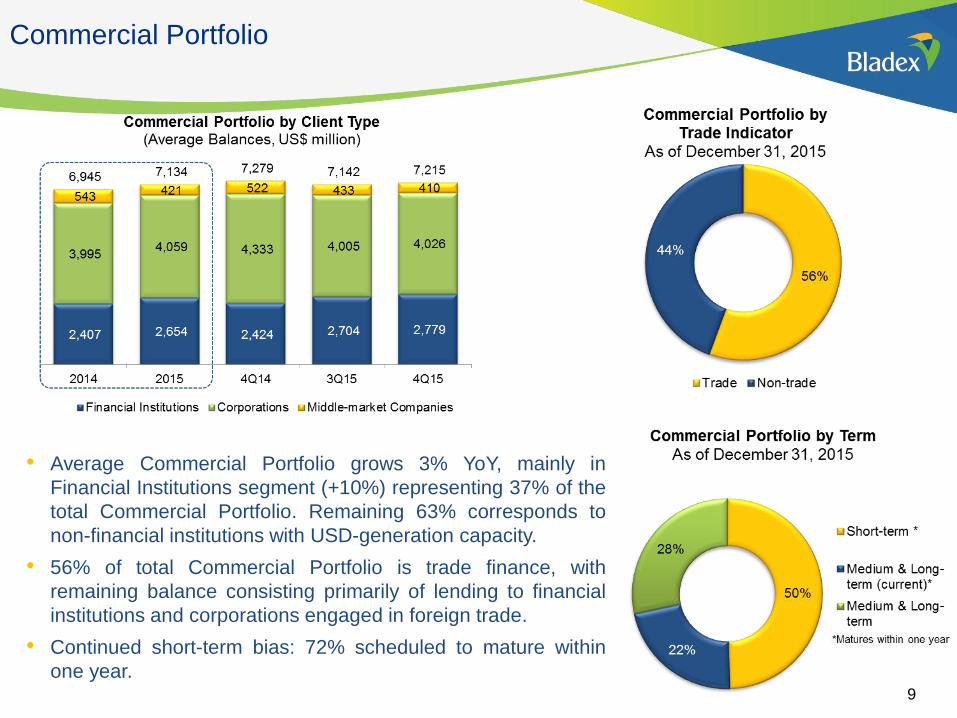

Commercial Portfolio

• Average Commercial Portfolio grows 3% YoY, mainly in

Financial Institutions segment (+10%) representing 37% of the

total Commercial Portfolio. Remaining 63% corresponds to

non-financial institutions with USD-generation capacity.

• 56% of total Commercial Portfolio is trade finance, with

remaining balance consisting primarily of lending to financial

institutions and corporations engaged in foreign trade.

• Continued short-term bias: 72% scheduled to mature within

one year. 9

Commercial Portfolio Exposure By Country and By Industry

• Broadly diversified across countries & industries.

• Brazil exposure at 23% of Commercial Portfolio, down from 25% in 3Q2015 (-2 ppts.

QoQ), and from 28% in 4Q2014 (-5 ppts. YoY).

• Growth focus shifted primarily to Central American & Caribbean Region (+4 ppts. QoQ

and +8 ppts. YoY).

• Exposure to financial institutions at 39%, unchanged from prior quarter (+3 ppts. YoY).

Overall exposure to Oil and Gas industry reduced to 12%, -3 ppts.YoY and -1ppts. QoQ. 10

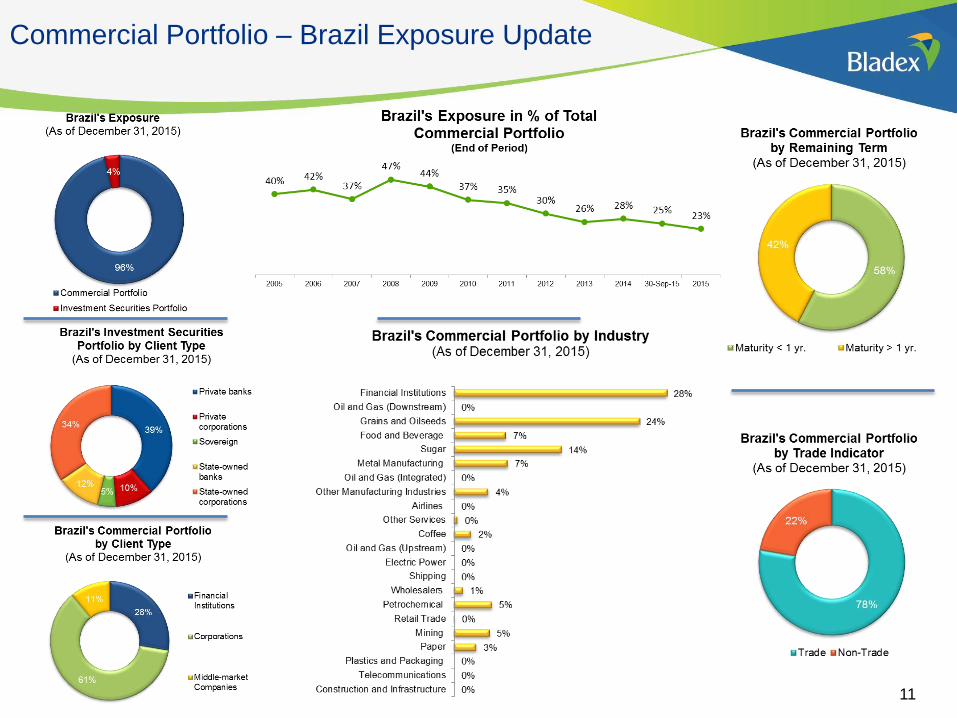

Commercial Portfolio – Brazil Exposure Update

11

Upstream Integrated Downstream

Clients primarily focused on

Exploration

Production

Clients focused on:

Full Value chain,

from Upstream to

Downstream

Clients primarily focused on

Refining

Storage

Distribution

Oil & Gas Exposure Analysis

Bladex Outlook Negative Stable Positive

Rationale for Outlook • Lower prices/margins

• Reduced cash flows

• Reduced investment

• Upstream impact mitigated by

positive outlook in

downstream activities

• Better refining margins

• Cost efficiency gains

Bladex Credit Exposure:

• Includes Commercial

Portfolio + Treasury Portfolio

(nominal values).

* Y/E 2015 Update:

• Total duration of 8 months

• 7.1% is related to Treasury

Portfolio.

• 88% of Bonds are sovereign

risk (Brazil, Chile, Colombia,

Mexico, Trinidad & Tobago).

• $176MM

• 2% of Total Credit Portfolio

• 18% of O&G Exposure

• Increase in credit

risk/impairment in securities

• Concerted lender actions

• Mitigating factors:

Diversification in Gas

More Competitive Cost

Base

Pre-payment of longer

dated disbursed loans

50% of exposure is

contingent only (SBLCs)

• $373MM

• 5% of Total Credit Portfolio

• 39% of O&G Exposure

• Import/export transactions

• Mitigating factors:

Strategic relevance / quasi-

gov´t entities

Local fuel price regimes

not tied to crude price

evolution

• $412MM

• 6% of Total Credit Portfolio

• 43% of O&G Exposure

• Import transactions

• Mitigating factors:

Strategic relevance / quasi-

gov´t entities

Local fuel price regimes

not tied to crude price

evolution

Bladex exposure continues downward trend, with bias towards

quasi-sovereigns and Integrated/Downstream market spectrum 12

Oil & Gas Credit Exposure

Year Credit Exposure

(USD MM) % / Bladex Credit

Exposure

2015* 961 13%

2014 1,117 15%

2013 1,206 17%

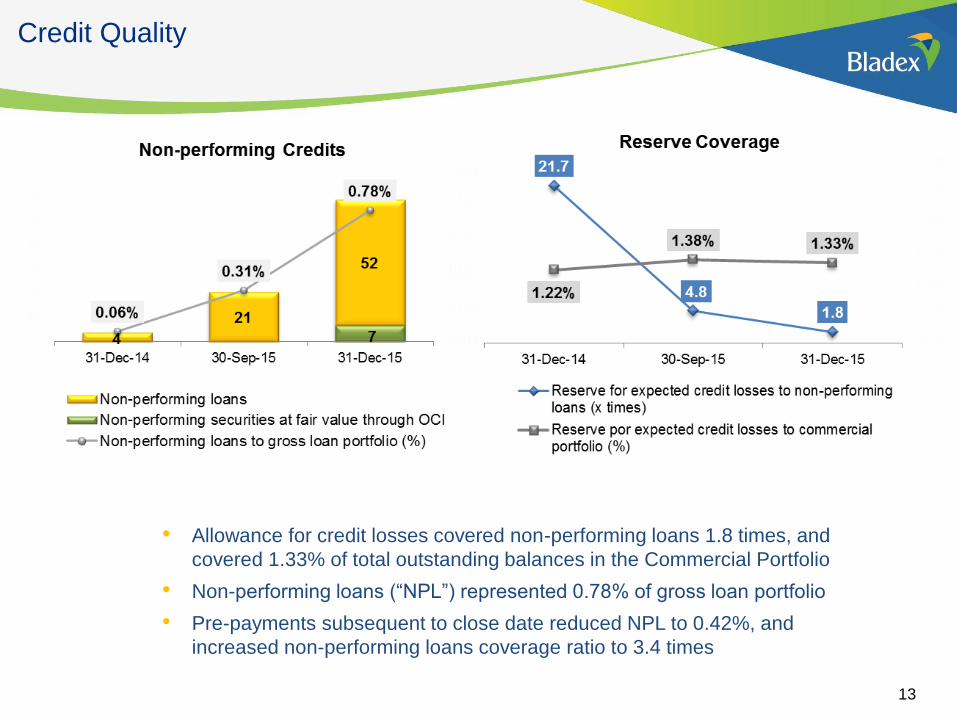

Credit Quality

• Allowance for credit losses covered non-performing loans 1.8 times, and

covered 1.33% of total outstanding balances in the Commercial Portfolio

• Non-performing loans (“NPL”) represented 0.78% of gross loan portfolio

• Pre-payments subsequent to close date reduced NPL to 0.42%, and

increased non-performing loans coverage ratio to 3.4 times

13

Off-balance Sheet Assets & Commission

and Intermediation Income

• Fees & Other Income increase 2% YoY, with higher fee

income from higher commissions from the L/C and

contingency business, and fees from structuring and

syndication activities, partially offset by lower loan

distribution activity in the secondary markets.

• 7 syndicated/club deal transactions totaling $612

million executed in 2015. Solid pipeline of prospective

transactions for 2016.

• 6% QoQ decrease mostly from lower loan structuring

and distribution fees, offsetting increased gain on sale

of loans. Income from letters of credit and

contingencies business remained relatively stable QoQ. 14

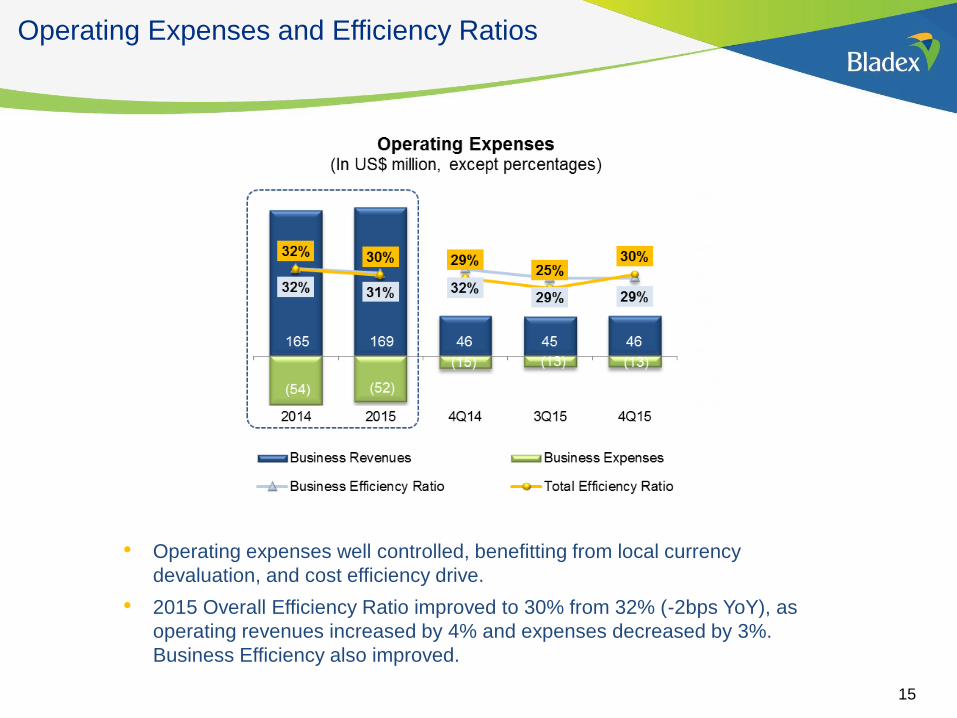

Operating Expenses and Efficiency Ratios

• Operating expenses well controlled, benefitting from local currency

devaluation, and cost efficiency drive.

• 2015 Overall Efficiency Ratio improved to 30% from 32% (-2bps YoY), as

operating revenues increased by 4% and expenses decreased by 3%.

Business Efficiency also improved.

15

ROAE and Capitalization

• QoQ ROAE drop attributable to losses from

participation in investment funds and higher

provision for expected credit losses on loans

and off-balance sheet financial instruments

and impairment losses from expected credit

losses on investment securities.

• 2015 ROAE fairly stable at 11.0% compared

to 11.5% in 2014

• Tier 1 Basel III capitalization strengthens to

16.1% with reduction of RWA

16

Shareholder Returns

•Bladex’s stock price performance

down 10% in 2015, outperforming

most indices (e.g. MSCI Latam,

IBOV). Total Shareholder Return

-9% for twelve trailing months.

•Attractive stock valuation at 9.7x

(P/EPS) and 1.0x (P/BV) at Y/E

2015.

•Stable dividend with yield well in

excess of 5%.

17

Questions & Answers

18

Appendix

19

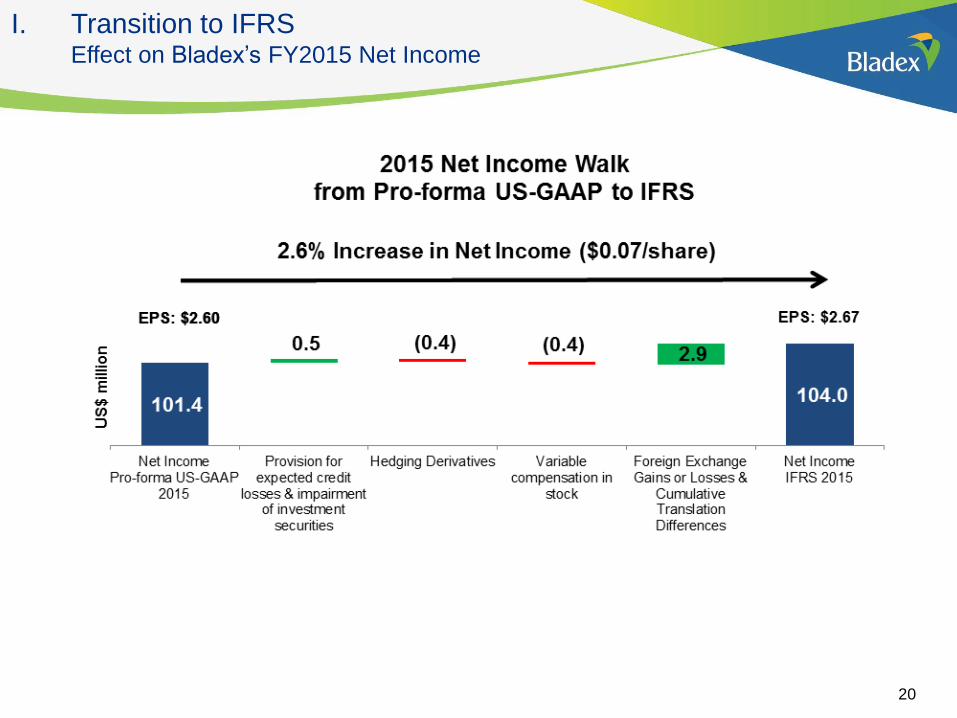

I. Transition to IFRS Effect on Bladex’s FY2015 Net Income

20

I. Transition to IFRS Effect on Bladex’s Statement of Financial Position

21

Thank You!

22