ERM and insurance risk management in P&C underwriting

18

ERM and insurance risk management in P&C underwriting David Ovenden, Towers Watson 26 – 27 September 2013, Brussels © 2013 Towers Watson. All rights reserved.

Transcript of ERM and insurance risk management in P&C underwriting

ERM and insurance risk management in P&C underwriting

David Ovenden, Towers Watson

26 – 27 September 2013, Brussels

© 2013 Towers Watson. All rights reserved.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Agenda

Introduction

Background and context

Material risks and risk drivers

Strategic engagement

Conclusions and reflections

towerswatson.com © 2013 Towers Watson. All rights reserved.2

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Introduction

towerswatson.com © 2013 Towers Watson. All rights reserved.

David OvendenDirector, RCS

London

David OvendenDirector, RCS

London

[email protected]@towerswatson.com

Phone. +44 207 8865106Mobile. +44 7908 1188855Phone. +44 207 8865106

Mobile. +44 7908 1188855

David OvendenDirector, RCS

London

Phone. +44 207 8865106Mobile. +44 7908 1188855

3

Risk Appetite

Technical Audit

Insurance Risk Framework

Performance Management

Pricing Committee

Deals Committee

Claims ManagementLarge Case Decisions

Background and contextAn underwriters perspective

© 2013 Towers Watson. All rights reserved.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

A definition of Insurance Risk

towerswatson.com © 2013 Towers Watson. All rights reserved.

The risk of loss due to actual experience being different than that assumed when an insurance product was designed and priced.

The likelihood that an insured event will occur, requiring the insurer to pay a claim.

The business risk associated with the act of providing insurance solutions.

The risk associated with undertaking insurance transactions.

5

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Who manages insurance risk

The Underwriters

Frontline Underwriters

Automated or systematic underwriting

Product or Portfolio Underwriters

Divisional Chief Underwriting Officers

Global CUOs

Insurance Risk Team

Technical Risk officers

Divisional Insurance Risk Director

Group Insurance Risk

Internal Audit

Group Internal audit

Internal Audit

A typical “three lines of defence model”.

towerswatson.com © 2013 Towers Watson. All rights reserved.6

Insurance RiskMaterial risks and risk drivers

© 2013 Towers Watson. All rights reserved.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Material Risks

l Characteristics of companies that have gone bustl A larger than life charismatic leaderl A product, process or methodology that is new to the marketl Results that are too good to be true, ultimately concealing:

– Systemic under pricing– Under reserving– Cashflow underwriting– Doctored accounts

l These characteristics are also applicable at product or portfolio levell Zero risk deals (not understanding the risk)l Systemic risks and lack of portfolio balance (sideways accumulations)l Failure to aggregate or correlate (lack of downside vision)l Management incentives and rewards (short termism)l IT developmentsl Not forgetting the favourite M&A or portfolio acquisition

towerswatson.com © 2013 Towers Watson. All rights reserved.

8

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Other Insurance risks I have encountered….

The price of beer is falling

towerswatson.com © 2013 Towers Watson. All rights reserved.

9

Keeping minutes but losing hoursEveryone is looking out of the back windowA positive decision not to do somethingBig data starts at homeConstructive tension is still tension“Could find nothing wrong”Don’t forget to milk the cowsLack of the hygiene

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Other Insurance Risks Print slide

l The price of beer is falling l do your exposure measure add up?

l Keeping minutes but losing hours l do you have the right balance of committees?

l Everyone is looking out of the back window l where are the forward looking metrics and assumptions?

l A positive decisions not to do something l is the organisation decisive?

l Big data starts at home l do you place enough value on your own data?

l Constructive tension is still tension l where is the P&L accountability?

l “Could find nothing wrong” l is the audit culture positive or corrosive?

l Don’t forget to milk the cows l high performing products need attention too?

l Lack of the hygiene l what are the hygiene factors for a line of business?

towerswatson.com © 2013 Towers Watson. All rights reserved.

10

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

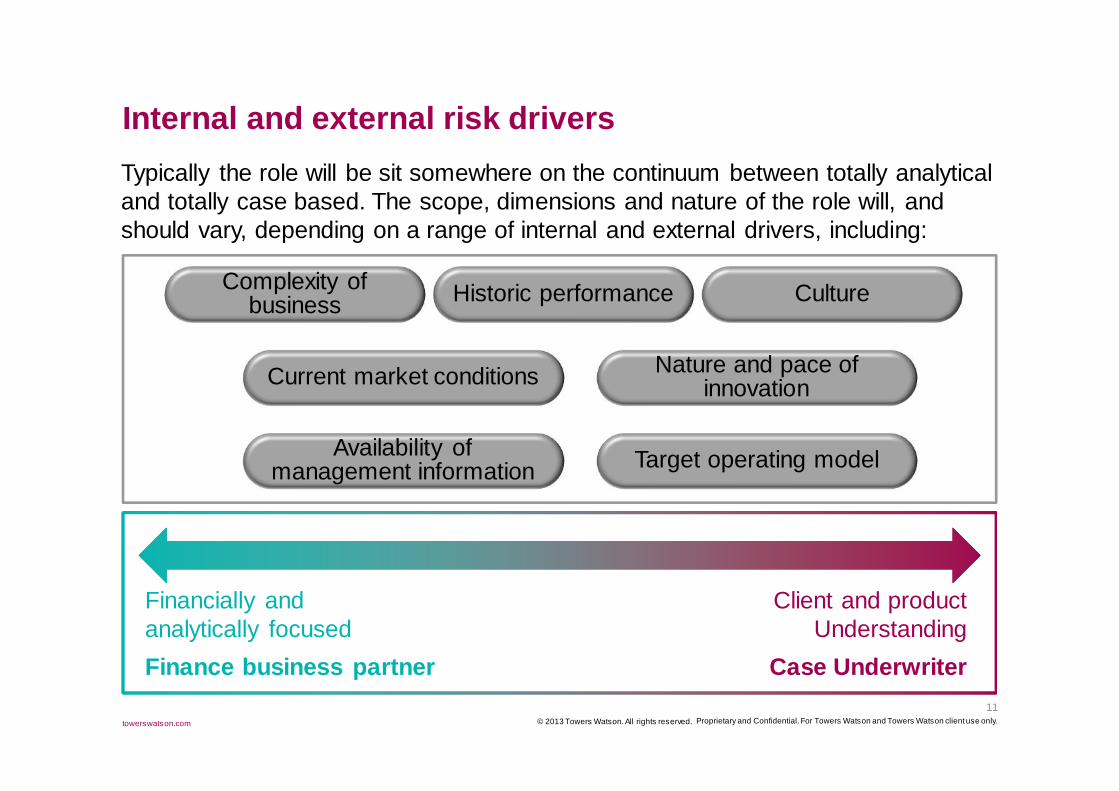

Internal and external risk drivers

towerswatson.com © 2013 Towers Watson. All rights reserved.

Financially and analytically focusedFinance business partner

Client and product Understanding

Case Underwriter

Typically the role will be sit somewhere on the continuum between totally analytical and totally case based. The scope, dimensions and nature of the role will, and should vary, depending on a range of internal and external drivers, including:

Complexity of business Historic performance Culture

Current market conditions Nature and pace of innovation

Availability of management information Target operating model

11

The role of the Insurance Risk Director Strategic engagement and cycle management

© 2013 Towers Watson. All rights reserved.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Insurance Risk Director and cycle management

towerswatson.com © 2013 Towers Watson. All rights reserved.

Financial, risk & capital

management

Business management

Portfolio Management

& Underwriting

Marketing &Distribution

Business restructuringPricing

Reserve surplus releases

Active management of finite resources

‘Worst performing cases’ reviews and

UW interventionCross-sell,

upsellDiscontinue/

run-off certain lines of business

Rate Action, basedTechnical price

Review actuarial reserves/DAC for

prudence

Efficiency improvement

programs

Segmentation, mixand cross subsidy

management

Advanced analytics and external data

Internal/external reinsurance and

frontingMarginal pricing

techniques

Robust financial forecasting and

planning

Retention management

programsProduct / Portfolio

redesignOptimisation of

marketing spendOther capital

raising/restructuring activity

Street Pricing and discounting strategies

ReinsuranceClaims

improvement programs

Product andchannel remediation

Commissionrestructuring

Purchase/sale of business/blocks

of businessUse of GLM

Accounting andtax optimisation

IT/Technology improvement

Technicalunderwritingstandards

New distribution channels

New businesses/markets

Optimisation techniques

Increasing Time —

Costs —

Com

plexity

Insurance Cycle Management

13

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Insurance Risk Director and cycle management

towerswatson.com © 2013 Towers Watson. All rights reserved.

Financial, risk & capital

management

Business management

Portfolio Management

& Underwriting

Marketing &Distribution

Business restructuringPricing

Reserve surplus releases

Active management of finite resources

‘Worst performing cases’ reviews and

UW interventionCross-sell,

upsellDiscontinue/

run-off certain lines of business

Rate Action, basedTechnical price

Review actuarial reserves/DAC for

prudence

Efficiency improvement

programs

Segmentation, mixand cross subsidy

management

Advanced analytics and external data

Internal/external reinsurance and

frontingMarginal pricing

techniques

Robust financial forecasting and

planning

Retention management

programsProduct / Portfolio

redesignOptimisation of

marketing spendOther capital

raising/restructuringactivity

Street Pricing and discounting strategies

ReinsuranceClaims

improvement programs

Product andchannel remediation

Commissionrestructuring

Purchase/sale of business/blocks

of businessUse of GLM

Accounting andtax optimisation

IT/Technology improvement

Technicalunderwritingstandards

New distribution channels

New businesses/markets

Optimisation techniques

Increasing Time —

Costs —

Com

plexity

Insurance Cycle Management

14

The role of the Insurance Risk DirectorConclusions and reflections

© 2013 Towers Watson. All rights reserved.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

The role of the Insurance Risk Director

towerswatson.com © 2013 Towers Watson. All rights reserved.

In common with the many senior appointment, the answer to what is the optimal scope for the role of Insurance Risk Directors role will vary across organisations, depending on the challenges faced, culture, performance, business complexity and target operating models.

However, there are key elements that should be addressed, with the exact method and therefore degree of engagement being constrained by organisational and external drivers. These include:

• Risk appetite • Strategy• Strategic initiatives • Performance management• Claims management • Technical audits• Planning • Large deals - case, portfolios, M&A• Portfolio pricing • Capital allocation and modelling• Data management & enrichment • New or material changes to product

16

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

The role of the Insurance Risk Director

012345

towerswatson.com © 2013 Towers Watson. All rights reserved.

Do you have the right balance in your day to day activity, given the company’s current performance, capabilities and ambition in the context of the market?

Below is a diagram where the blue zone represented the actual “zone of engagement” and the green represents the hindsight view of the same period.

17

Proprietary and Confidential. For Towers Watson and Towers Watson client use only. towerswatson.com © 2013 Towers Watson. All rights reserved.

18