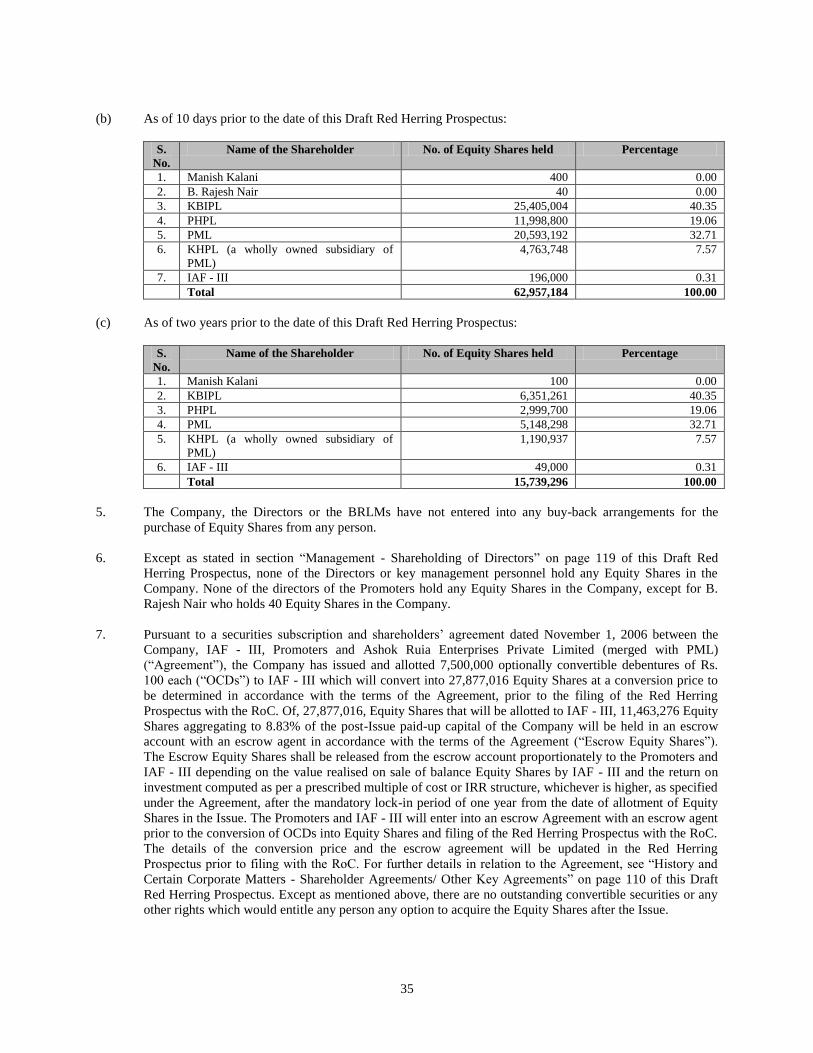

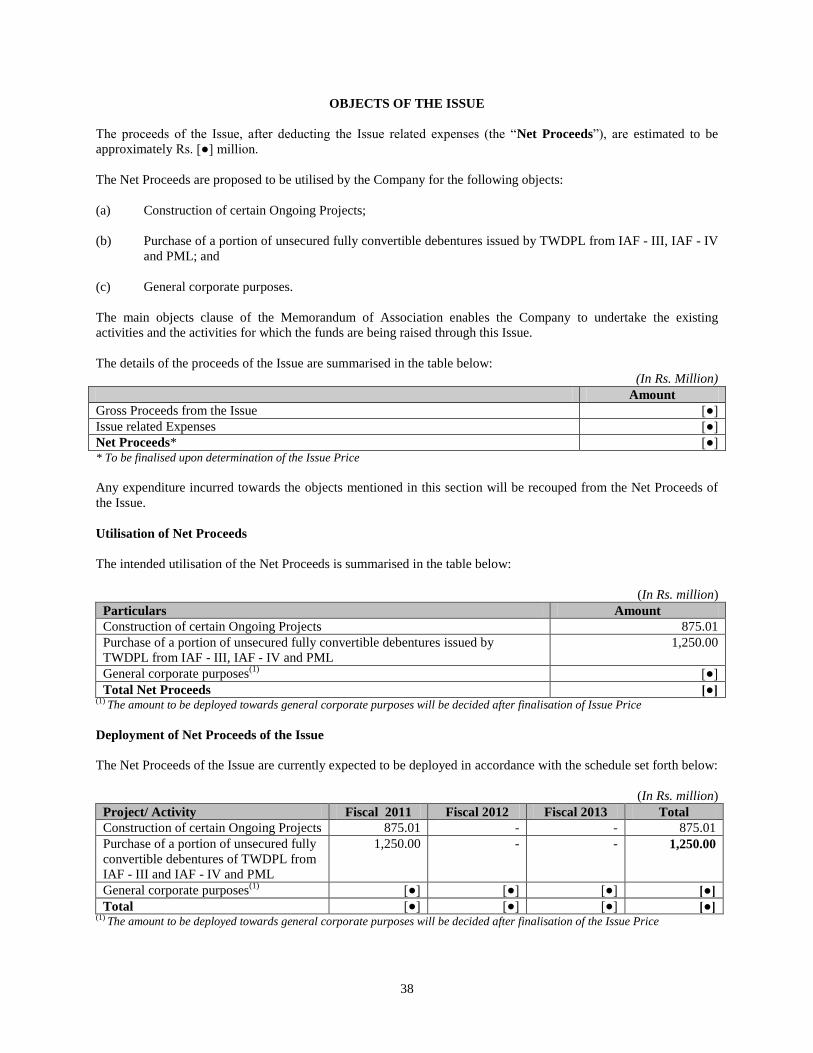

Entertainment World Developers Ltd.

424

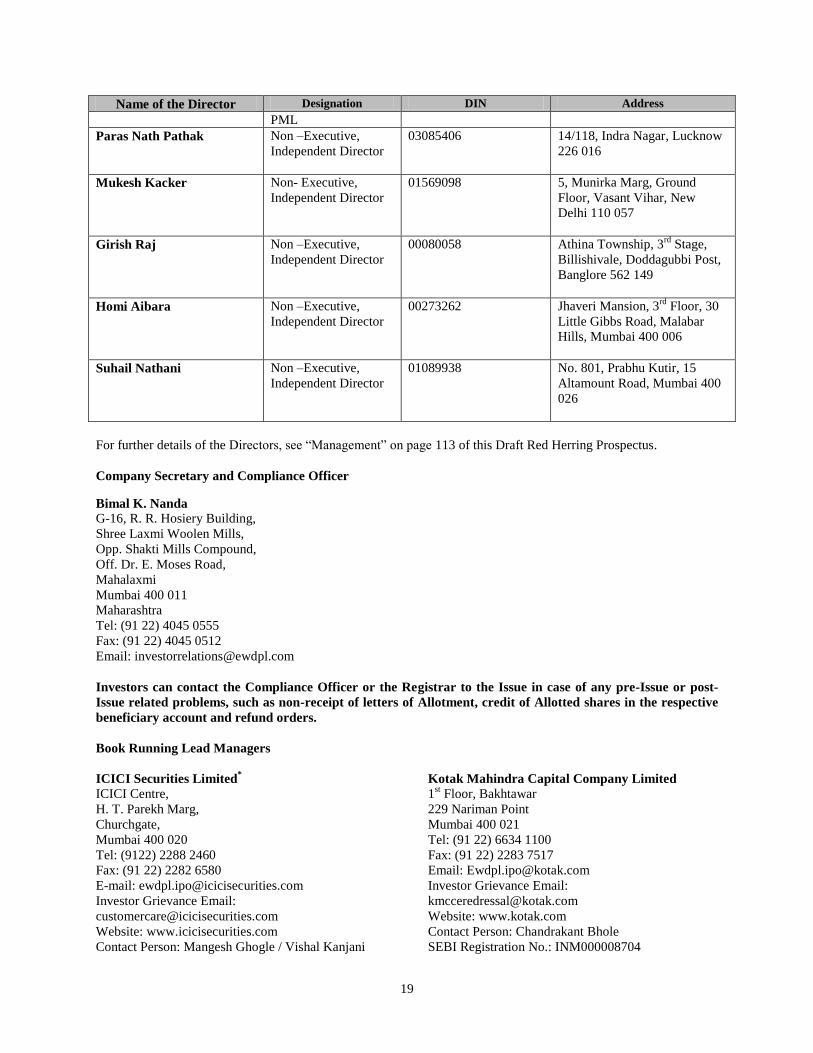

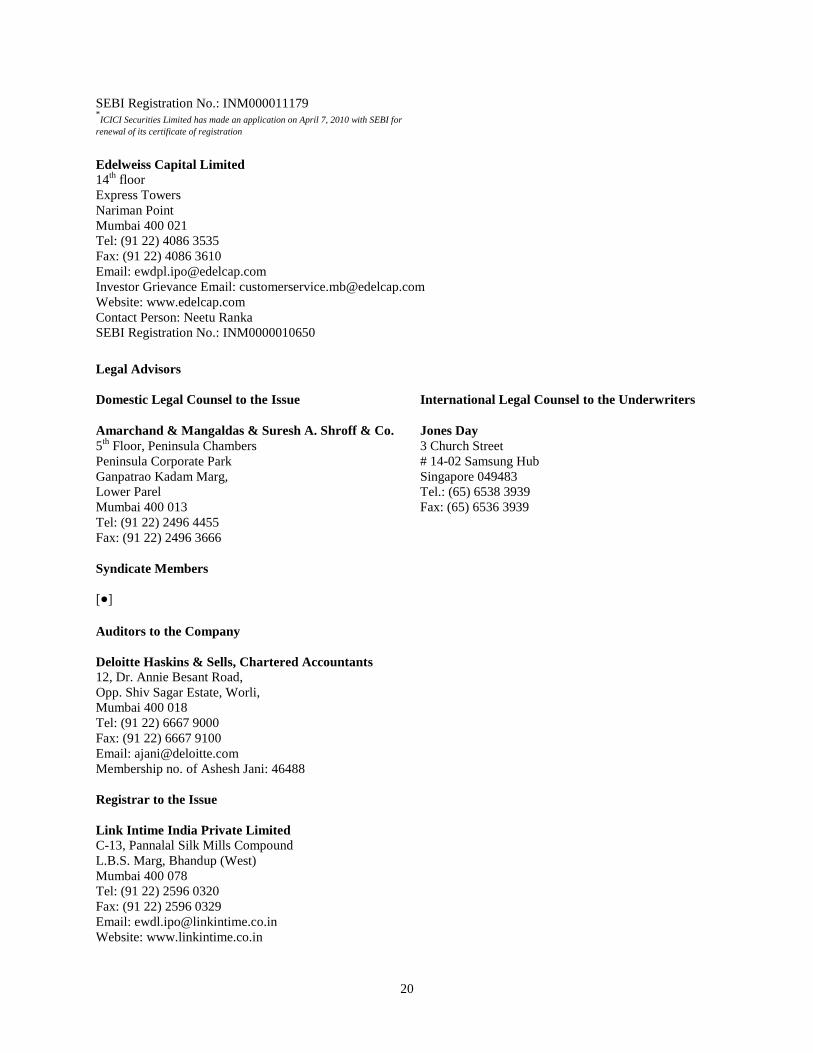

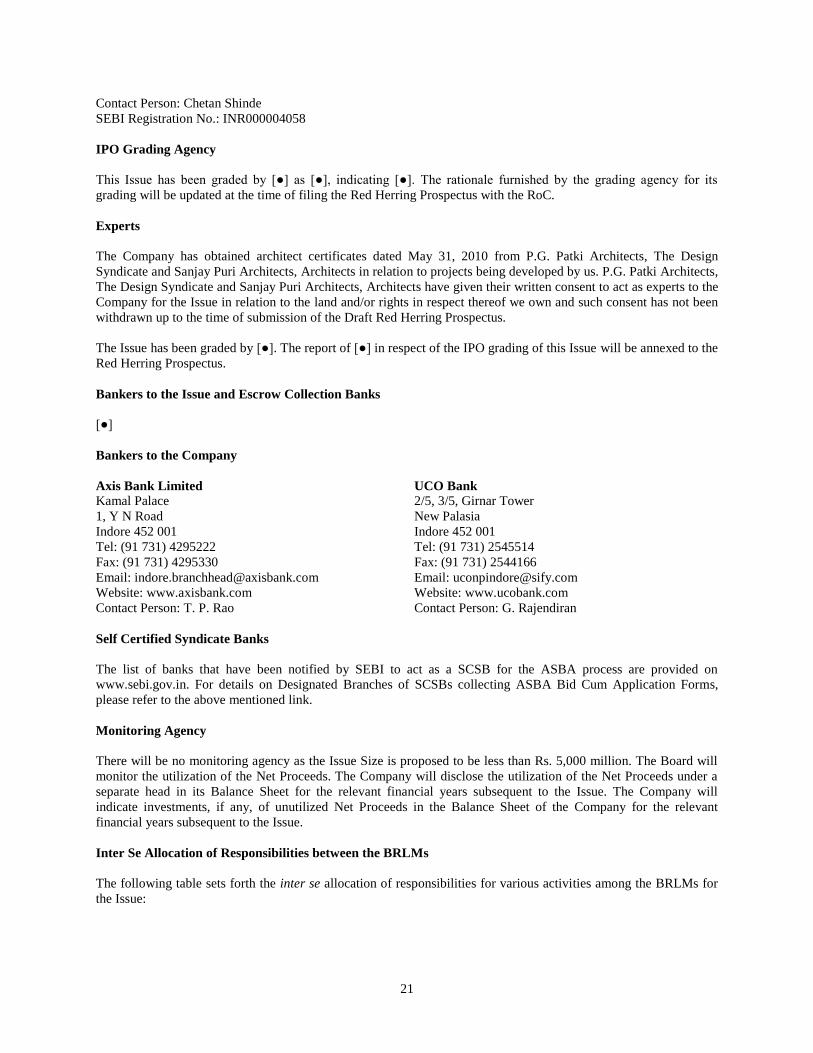

DRAFT RED HERRING PROSPECTUS Dated July 12, 2010 Please read section 60B of the Companies Act, 1956 (The Draft Red Herring Prospectus will be updated upon filing with the RoC) 100% Book Building Issue ENTERTAINMENT WORLD DEVELOPERS LIMITED The Company was incorporated on July 22, 1999 as ‘R.M.M. Construction Private Limited’ as a private limited company under the Companies Act, 1956, as amended (the “Companies Act”). The name of the Company was changed to ‘Entertainment World Developers Private Limited’ on February 28, 2003. The name of the Company was further changed to Entertainment World Developers Limited on conversion into a public limited company on February 5, 2010. For further details of changes in the name and registered office of the Company, see “History and Certain Corporate Matters” on page 106 of this Draft Red Herring Prospectus. Registered Office: G-16, R. R. Hosiery Building, Shree Laxmi Woolen Mills, Opp. Shakti Mills Compound, Off. Dr. E. Moses Road, Mahalaxmi, Mumbai 400 011 Corporate Office: 6 th Floor, Treasure Island, 11, M.G. Road, Tukoganj, Indore 452 001 Contact Person: Bimal K. Nanda, Company Secretary and Compliance Officer Tel: (91 22) 4045 0555; Fax: (91 22) 4045 0512; Email: [email protected]; Website: www.ewdpl.com Promoters of the Company: Manish Kalani, Kalani Brothers (Indore) Private Limited and Padma Homes Private Limited PUBLIC ISSUE OF 38,928,943 EQUITY SHARES OF Rs. 10 EACH (“EQUITY SHARES”) OF ENTERTAINMENT WORLD DEVELOPERS LIMITED (THE “COMPANY” OR THE “ISSUER” OR “EWDL”) FOR CASH AT A PRICE OF Rs. [l] PER EQUITY SHARE (INCLUDING A SHARE PREMIUM OF Rs. [l] PER EQUITY SHARE) AGGREGATING TO Rs. [l] MILLION (THE “ISSUE”). THE ISSUE WILL CONSTITUTE 30% OF THE POST-ISSUE PAID-UP CAPITAL OF THE COMPANY. THE FACE VALUE OF EQUITY SHARES IS Rs. 10 EACH. THE PRICE BAND AND THE MINIMUM BID LOT WILL BE DECIDED BY THE COMPANY IN CONSULTATION WITH THE BOOK RUNNING LEAD MANAGERS (“BRLMs”) AND WILL BE ADVERTISED AT LEAST TWO WORKING DAYS PRIOR TO THE BID/ISSUE OPENING DATE. In case of any revision to the Price Band, the Bid/Issue Period will be extended by three additional working days after such revision of the Price Band, subject to the Bid/ Issue Period not exceeding 10 working days. Any revision in the Price Band and the revised Bid/Issue Period, if applicable, will be widely disseminated by notification to the Bombay Stock Exchange Limited (“BSE”) and the National Stock Exchange of India Limited (“NSE”), by issuing a press release, and also by indicating the change on the website of the BRLMs and at the terminals of the other members of the Syndicate. In terms of Rule 19(2)(b)(i) of the Securities Contracts (Regulation) Rules, 1957 (“SCRR”), this is an issue for more than 25% of the post-Issue capital. The Issue is being made through the 100% Book Building Process wherein at least 50% of the Issue shall be allocated on a proportionate basis to Qualified Institutional Buyers (“QIB”) Bidders. 5% of the QIB Portion (excluding Anchor Investor Portion) shall be available for allocation on a proportionate basis to Mutual Funds only, and the remainder of the QIB Portion shall be available for allocation on a proportionate basis to all QIB Bidders, including Mutual Funds, subject to valid Bids being received at or above the Issue Price. Further, not less than 15% of the Issue shall be available for allocation on a proportionate basis to Non-Institutional Bidders and not less than 35% of the Issue shall be available for allocation on a proportionate basis to Retail Individual Bidders, subject to valid Bids being received at or above the Issue Price. If at least 50% of the Issue cannot be Allotted to QIBs, then the entire application money shall be refunded forthwith. Potential investors other than Anchor Investors may participate in this Issue through an Application Supported by Blocked Amount (“ASBA”) process providing details about the bank account which will be blocked by the Self Certified Syndicate Banks (“SCSBs”) for the same. For details, see “Issue Procedure” on page 332 of this Draft Red Herring Prospectus. RISK IN RELATION TO THE FIRST ISSUE This being the first public issue of the Company, there has been no formal market for the Equity Shares of the Company. The face value of the Equity Shares is Rs.10 and the Issue Price is [l] times of the face value. The Issue Price (has been determined and justified by the Company, and the BRLMs as stated under the section on “Basis for Issue Price” on page 45 of this Draft Red Herring Prospectus) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active or sustained trading in the Equity Shares or regarding the price at which the Equity Shares will be traded after listing. IPO GRADING This Issue has been graded by [l] as [l], indicating [l]. For details, see “General Information” on page 18 of this Draft Red Herring Prospectus. GENERAL RISKS Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in this Issue unless they can afford to take the risk of losing their investment. Investors are advised to read the risk factors carefully before taking an investment decision in this Issue. In taking an investment decision, investors must rely on their own examination of the Company and the Issue, including the risks involved. The Equity Shares offered in the Issue have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or adequacy of the contents. Specific attention of the investors is invited to “Risk Factors” on page xi of this Draft Red Herring Prospectus. ISSUER’S ABSOLUTE RESPONSIBILITY The Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Draft Red Herring Prospectus contains all information with regard to the Company and the Issue, which is material in the context of the Issue, that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which make this Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect. LISTING The Equity Shares offered through this Draft Red Herring Prospectus are proposed to be listed on the BSE and the NSE. We have received an ‘in-principle’ approval from each of the BSE and the NSE for the listing of the Equity Shares pursuant to the letters dated [l] and [l], respectively. For the purposes of the Issue, the Designated Stock Exchange shall be [l]. BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE ISSUE ICICI Securities Limited* ICICI Centre, H. T. Parekh Marg Churchgate, Mumbai 400 020 Tel: (91 22) 2288 2460 Fax: (91 22) 2282 6580 E-mail: [email protected] Investor Grievance Email: [email protected] Website: www.icicisecurities.com Contact Person: Mangesh Ghogle / Vishal Kanjani SEBI Registration No.: INM000011179 * ICICI Securities Limited has made an application on April 7, 2010 with SEBI for renewal of its certificate of registration Kotak Mahindra Capital Company Limited 1st Floor, Bakhtawar 229 Nariman Point, Mumbai 400 021 Tel: (91 22) 6634 1100 Fax: (91 22) 2283 7517 Email: [email protected] Investor Grievance Email: [email protected] Website: www.kotak.com Contact Person: Chandrakant Bhole SEBI Registration No.: INM000008704 Edelweiss Capital Limited 14th floor, Express Towers Nariman Point, Mumbai 400 021 Tel: (91 22) 4086 3535 Fax: (91 22) 4086 3610 Email: [email protected] Investor Grievance Email: [email protected] Website: www.edelcap.com Contact Person: Neetu Ranka SEBI Registration No.: INM0000010650 Link Intime India Private Limited C-13, Pannalal Silk Mills Compound L.B.S Marg, Bhandup (West) Mumbai 400 078 Tel: (91 22) 2596 0320 Fax: (91 22) 2596 0329 Email: [email protected] Website: www.linkintime.co.in Contact Person: Chetan Shinde SEBI Registration No.: INR000004058 BID/ ISSUE PROGRAMME * BID/ISSUE OPENS ON: [l] * BID/ISSUE CLOSES ON: [l] ** * The Company may consider participation by Anchor Investors. The Anchor Investor Bid/ Issue Period shall be one working day prior to the Bid/ Issue Opening Date. ** The Company may consider closing the Bid/Issue Period for QIBs one day prior to the Bid/Issue Closing Date.

-

Upload

adhavvikas -

Category

Documents

-

view

307 -

download

9

Transcript of Entertainment World Developers Ltd.

DRAFT RED HERRING PROSPECTUSDated July 12, 2010

Please read section 60B of the Companies Act, 1956(The Draft Red Herring Prospectus will be updated upon filing with the RoC)

100% Book Building Issue

ENTERTAINMENT WORLD DEVELOPERS LIMITEDThe Company was incorporated on July 22, 1999 as ‘R.M.M. Construction Private Limited’ as a private limited company under the Companies Act, 1956, as amended (the “Companies Act”). The name of the Company was changed to ‘Entertainment World Developers Private Limited’ on February 28, 2003. The name of the Company was further changed to Entertainment World Developers Limited on conversion into a public limited company on February 5, 2010. For further details of changes in the

name and registered office of the Company, see “History and Certain Corporate Matters” on page 106 of this Draft Red Herring Prospectus. Registered Office: G-16, R. R. Hosiery Building, Shree Laxmi Woolen Mills, Opp. Shakti Mills Compound, Off. Dr. E. Moses Road, Mahalaxmi, Mumbai 400 011

Corporate Office: 6th Floor, Treasure Island, 11, M.G. Road, Tukoganj, Indore 452 001Contact Person: Bimal K. Nanda, Company Secretary and Compliance Officer

Tel: (91 22) 4045 0555; Fax: (91 22) 4045 0512; Email: [email protected]; Website: www.ewdpl.com

Promoters of the Company: Manish Kalani, Kalani Brothers (Indore) Private Limited and Padma Homes Private Limited

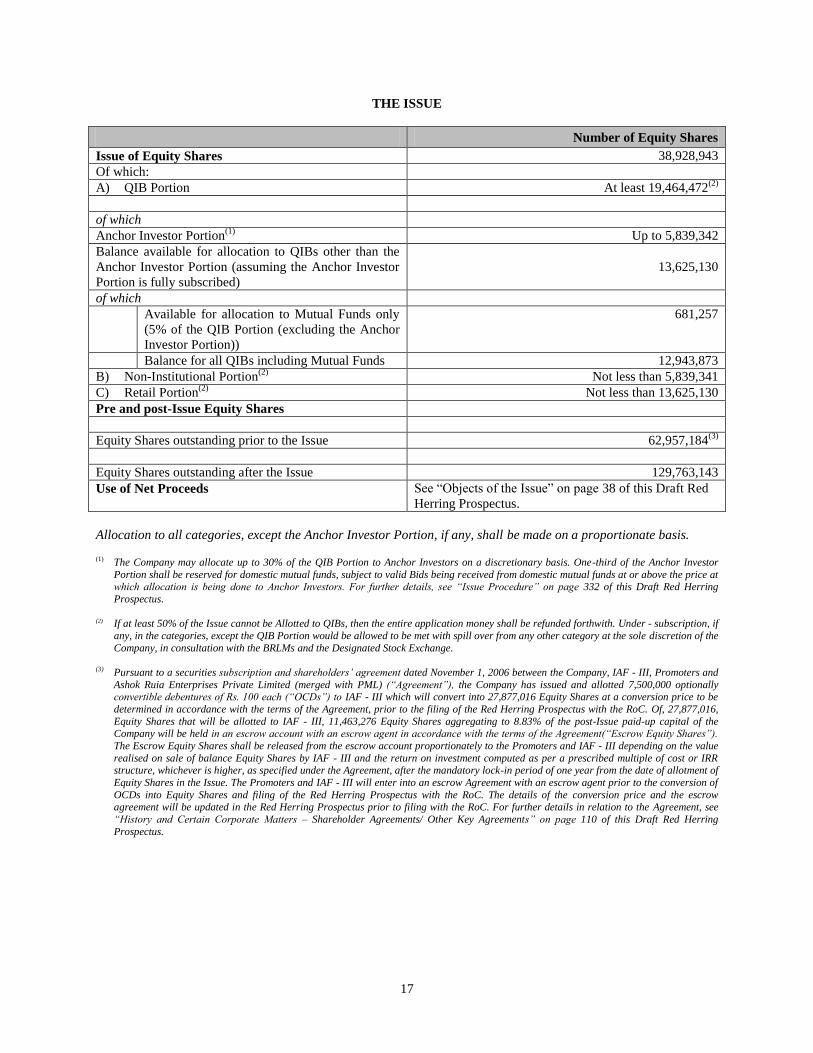

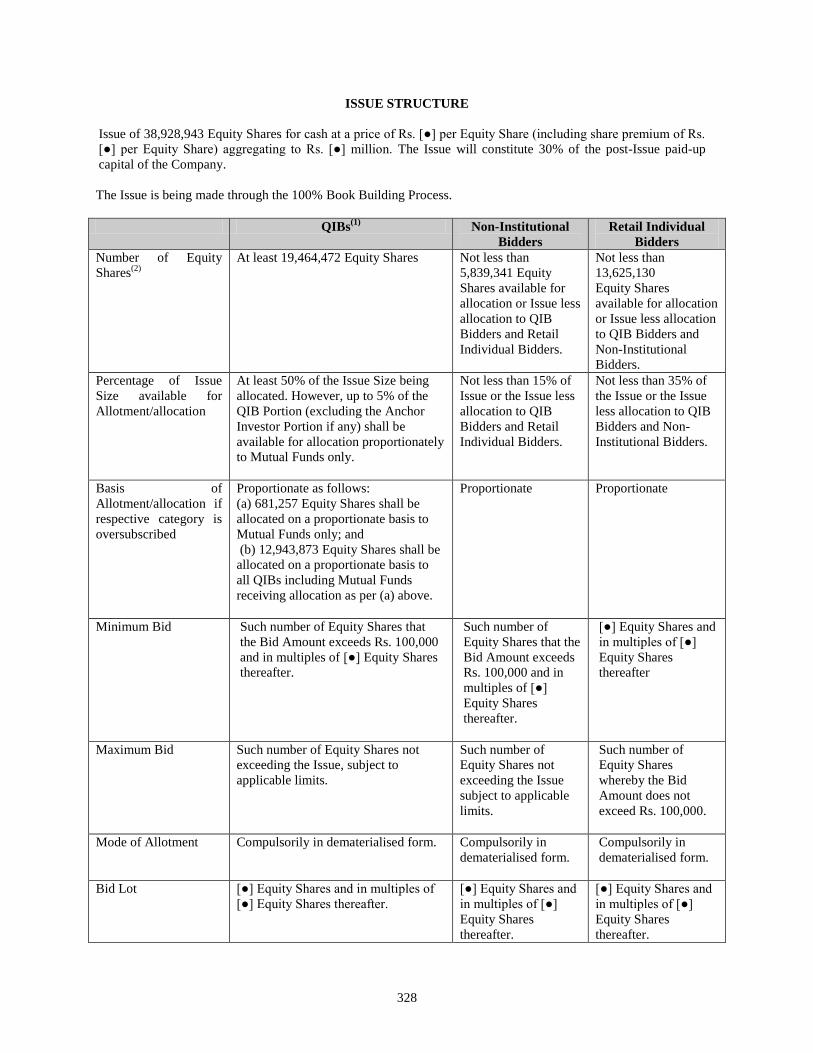

PUBLIC ISSUE OF 38,928,943 EQUITY SHARES OF Rs. 10 EACH (“EQUITY SHARES”) OF ENTERTAINMENT WORLD DEVELOPERS LIMITED (THE “COMPANY” OR THE “ISSUER” OR “EWDL”) FOR CASH AT A PRICE OF Rs. [l] PER EQUITY SHARE (INCLUDING A SHARE PREMIUM OF Rs. [l] PER EQUITY SHARE) AGGREGATING TO Rs. [l] MILLION (THE “ISSUE”). THE ISSUE WILL CONSTITUTE 30% OF THE POST-ISSUE PAID-UP CAPITAL OF THE COMPANY.

THE FACE VALUE OF EQUITY SHARES IS Rs. 10 EACH. THE PRICE BAND AND THE MINIMUM BID LOT WILL BE DECIDED BY THE COMPANY IN CONSULTATION WITH THE BOOK RUNNING LEAD MANAGERS (“BRLMs”) AND WILL BE ADVERTISED AT LEAST TWO WORKING DAYS

PRIOR TO THE BID/ISSUE OPENING DATE.

In case of any revision to the Price Band, the Bid/Issue Period will be extended by three additional working days after such revision of the Price Band, subject to the Bid/Issue Period not exceeding 10 working days. Any revision in the Price Band and the revised Bid/Issue Period, if applicable, will be widely disseminated by notification to the Bombay Stock Exchange Limited (“BSE”) and the National Stock Exchange of India Limited (“NSE”), by issuing a press release, and also by indicating the change on the website of the BRLMs and at the terminals of the other members of the Syndicate.

In terms of Rule 19(2)(b)(i) of the Securities Contracts (Regulation) Rules, 1957 (“SCRR”), this is an issue for more than 25% of the post-Issue capital. The Issue is being made through the 100% Book Building Process wherein at least 50% of the Issue shall be allocated on a proportionate basis to Qualified Institutional Buyers (“QIB”) Bidders. 5% of the QIB Portion (excluding Anchor Investor Portion) shall be available for allocation on a proportionate basis to Mutual Funds only, and the remainder of the QIB Portion shall be available for allocation on a proportionate basis to all QIB Bidders, including Mutual Funds, subject to valid Bids being received at or above the Issue Price. Further, not less than 15% of the Issue shall be available for allocation on a proportionate basis to Non-Institutional Bidders and not less than 35% of the Issue shall be available for allocation on a proportionate basis to Retail Individual Bidders, subject to valid Bids being received at or above the Issue Price. If at least 50% of the Issue cannot be Allotted to QIBs, then the entire application money shall be refunded forthwith. Potential investors other than Anchor Investors may participate in this Issue through an Application Supported by Blocked Amount (“ASBA”) process providing details about the bank account which will be blocked by the Self Certified Syndicate Banks (“SCSBs”) for the same. For details, see “Issue Procedure” on page 332 of this Draft Red Herring Prospectus.

RISK IN RELATION TO THE FIRST ISSUEThis being the first public issue of the Company, there has been no formal market for the Equity Shares of the Company. The face value of the Equity Shares is Rs.10 and the Issue Price is [l] times of the face value. The Issue Price (has been determined and justified by the Company, and the BRLMs as stated under the section on “Basis for Issue Price” on page 45 of this Draft Red Herring Prospectus) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active or sustained trading in the Equity Shares or regarding the price at which the Equity Shares will be traded after listing.

IPO GRADINGThis Issue has been graded by [l] as [l], indicating [l]. For details, see “General Information” on page 18 of this Draft Red Herring Prospectus.

GENERAL RISKSInvestments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in this Issue unless they can afford to take the risk of losing their investment. Investors are advised to read the risk factors carefully before taking an investment decision in this Issue. In taking an investment decision, investors must rely on their own examination of the Company and the Issue, including the risks involved. The Equity Shares offered in the Issue have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or adequacy of the contents. Specific attention of the investors is invited to “Risk Factors” on page xi of this Draft Red Herring Prospectus.

ISSUER’S ABSOLUTE RESPONSIBILITYThe Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Draft Red Herring Prospectus contains all information with regard to the Company and the Issue, which is material in the context of the Issue, that the information contained in this Draft Red Herring Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which make this Draft Red Herring Prospectus as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect.

LISTINGThe Equity Shares offered through this Draft Red Herring Prospectus are proposed to be listed on the BSE and the NSE. We have received an ‘in-principle’ approval from each of the BSE and the NSE for the listing of the Equity Shares pursuant to the letters dated [l] and [l], respectively. For the purposes of the Issue, the Designated Stock Exchange shall be [l].

BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE ISSUE

ICICI Securities Limited* ICICI Centre, H. T. Parekh Marg Churchgate, Mumbai 400 020Tel: (91 22) 2288 2460 Fax: (91 22) 2282 6580E-mail: [email protected] Grievance Email: [email protected]: www.icicisecurities.comContact Person: Mangesh Ghogle / Vishal KanjaniSEBI Registration No.: INM000011179* ICICI Securities Limited has made an application on April 7, 2010 with SEBI for renewal of its certificate of registration

Kotak Mahindra Capital Company Limited1st Floor, Bakhtawar 229 Nariman Point, Mumbai 400 021 Tel: (91 22) 6634 1100Fax: (91 22) 2283 7517Email: [email protected] Investor Grievance Email: [email protected]: www.kotak.comContact Person: Chandrakant BholeSEBI Registration No.: INM000008704

Edelweiss Capital Limited14th floor, Express TowersNariman Point, Mumbai 400 021Tel: (91 22) 4086 3535Fax: (91 22) 4086 3610Email: [email protected] Grievance Email: [email protected]: www.edelcap.comContact Person: Neetu RankaSEBI Registration No.: INM0000010650

Link Intime India Private Limited C-13, Pannalal Silk Mills CompoundL.B.S Marg, Bhandup (West)Mumbai 400 078Tel: (91 22) 2596 0320Fax: (91 22) 2596 0329 Email: [email protected]: www.linkintime.co.inContact Person: Chetan ShindeSEBI Registration No.: INR000004058

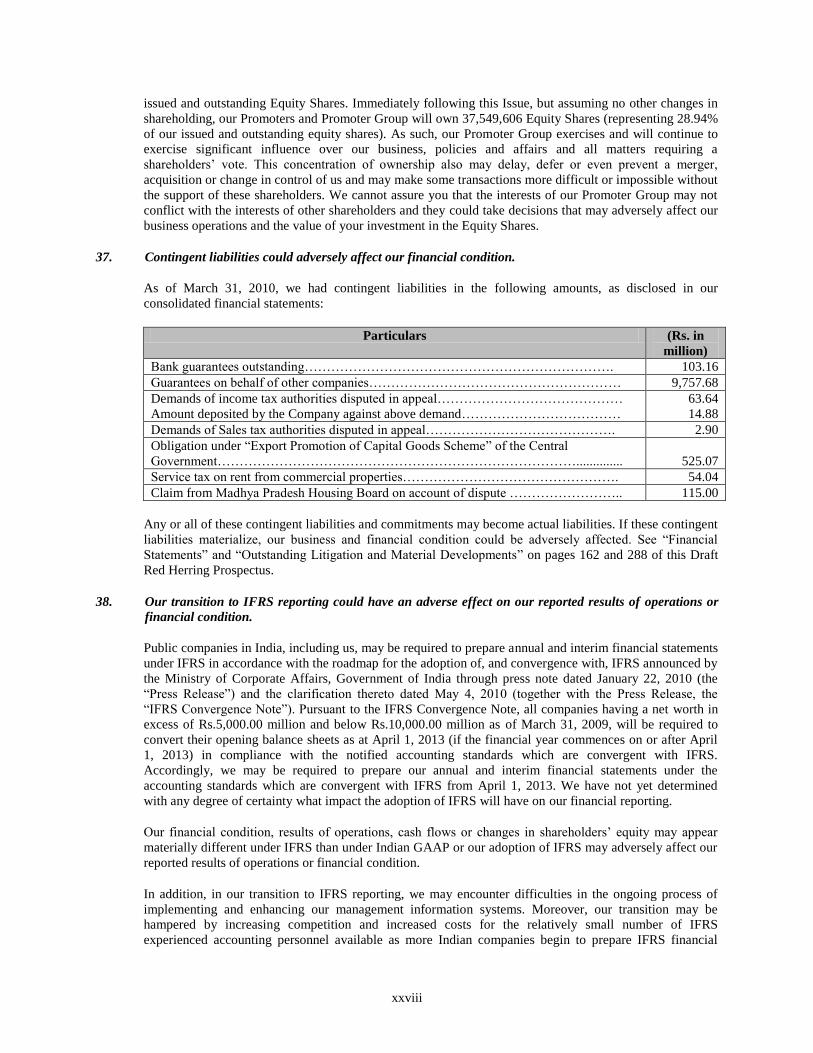

BID/ ISSUE PROGRAMME*

BID/ISSUE OPENS ON: [l] * BID/ISSUE CLOSES ON: [l] *** The Company may consider participation by Anchor Investors. The Anchor Investor Bid/ Issue Period shall be one working day prior to the Bid/ Issue Opening Date.** The Company may consider closing the Bid/Issue Period for QIBs one day prior to the Bid/Issue Closing Date.

TABLE OF CONTENTS

SECTION I: GENERAL ........................................................................................................................................... I DEFINITIONS AND ABBREVIATIONS .................................................................................................................... I PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA .................................................................... IX FORWARD-LOOKING STATEMENTS .................................................................................................................... X SECTION II: RISK FACTORS ................................................................................................................................. XI SECTION III: INTRODUCTION ............................................................................................................................... 1 SUMMARY OF INDUSTRY ..................................................................................................................................... 1 SUMMARY OF BUSINESS ..................................................................................................................................... 4 SUMMARY FINANCIAL INFORMATION ......................................................................................................... ....... 10 THE ISSUE .............................................................................................................................................................. 17 GENERAL INFORMATION ...................................................................................................................................... 18 CAPITAL STRUCTURE ........................................................................................................................................... 26 OBJECTS OF THE ISSUE ....................................................................................................................................... 38 BASIS FOR ISSUE PRICE ...................................................................................................................................... 45 STATEMENT OF TAX BENEFITS ........................................................................................................................... 48 SECTION IV: ABOUT THE COMPANY .................................................................................................................. 58 INDUSTRY OVERVIEW ........................................................................................................................................... 58 BUSINESS ............................................................................................................................................................... 76 REGULATIONS AND POLICIES ............................................................................................................................. 100 HISTORY AND CERTAIN CORPORATE MATTERS .............................................................................................. 106 MANAGEMENT........................................................................................................................................................ 113 SUBSIDIARIES AND JOINT VENTURE .................................................................................................................. 129 PROMOTERS AND PROMOTER GROUP ............................................................................................................. 149 GROUP COMPANIES .............................................................................................................................................. 155 RELATED PARTY TRANSACTIONS ...................................................................................................................... 160 DIVIDEND POLICY .................................................................................................................................................. 161 SECTION V: FINANCIAL INFORMATION .............................................................................................................. 162 FINANCIAL STATEMENTS ..................................................................................................................................... 162 MANAGEMENTS DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION ............... 266 FINANCIAL INDEBTEDNESS ................................................................................................................................. 286 SECTION VI: LEGAL AND OTHER INFORMATION ............................................................................................. 288 OUTSTANDING LITIGATION AND MATERIAL DEVELOPMENTS ........................................................................ 288 GOVERNMENT APPROVALS ................................................................................................................................. 295 OTHER REGULATORY AND STATUTORY DISCLOSURES ................................................................................ 314 SECTION VII: ISSUE INFORMATION .................................................................................................................... 325 TERMS OF THE ISSUE .......................................................................................................................................... 325 ISSUE STRUCTURE ............................................................................................................................................... 328 ISSUE PROCEDURE .............................................................................................................................................. 332 RESTRICTIONS ON FOREIGN OWNERSHIP OF INDIAN SECURITIES ............................................................. 361 SECTION VIII: MAIN PROVISIONS OF ARTICLES OF ASSOCIATION................................................................ 365 SECTION IX: OTHER INFORMATION ................................................................................................................... 380 MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION ....................................................................... 380 DECLARATION ....................................................................................................................................................... 382

i

SECTION I: GENERAL

DEFINITIONS AND ABBREVIATIONS

General Terms

Term Description

“EWDL”, “the Company” or the

“Issuer”

Unless the context otherwise indicates or implies, refers to Entertainment World

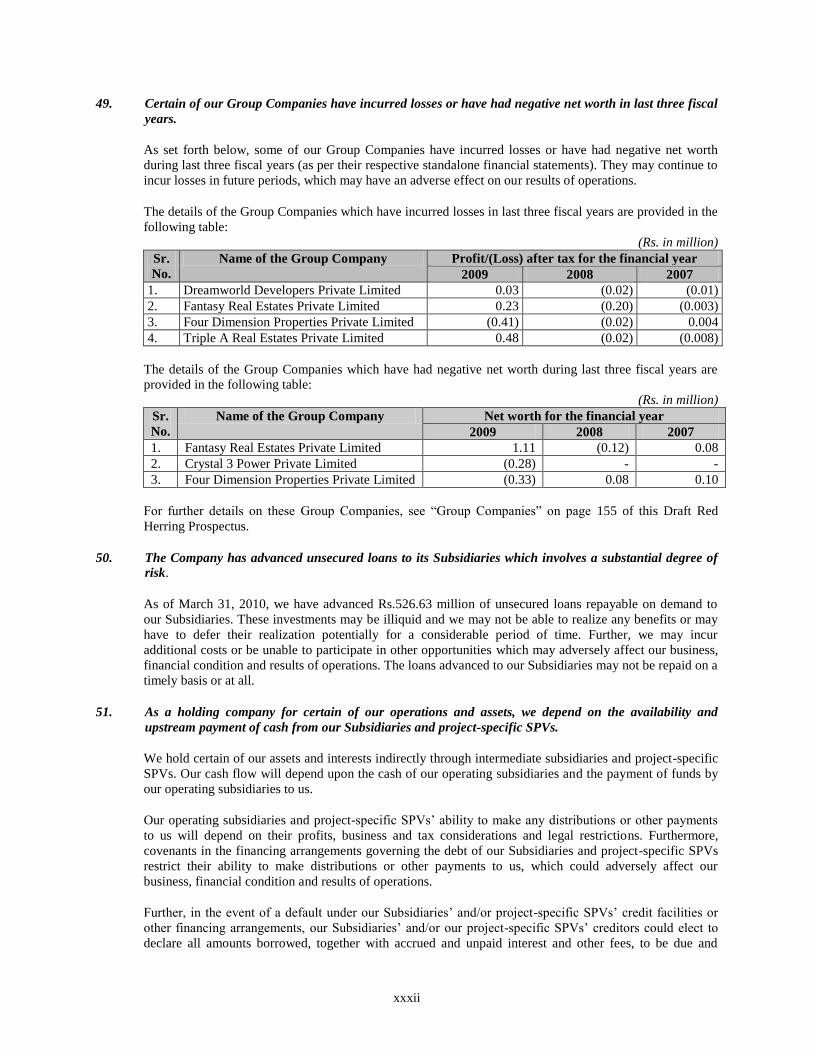

Developers Limited, a company incorporated under the Companies Act and

having its registered office at G-16, R. R. Hosiery Building, Shree Laxmi

Woolen Mills, Opp. Shakti Mills Compound, Off. Dr. E. Moses Road,

Mahalaxmi, Mumbai 400 011

“We”, “us” or “our” Unless the context otherwise requires, means the Company, its Subsidiaries and

joint venture

Joint Venture The joint venture of the Company as disclosed in “Subsidiaries and Joint

Venture” on page 129 of this Draft Red Herring Prospectus

Subsidiaries The subsidiaries of the Company as disclosed in “Subsidiaries and Joint

Venture” on page 129 of this Draft Red Herring Prospectus

Company Related Terms

Term Description

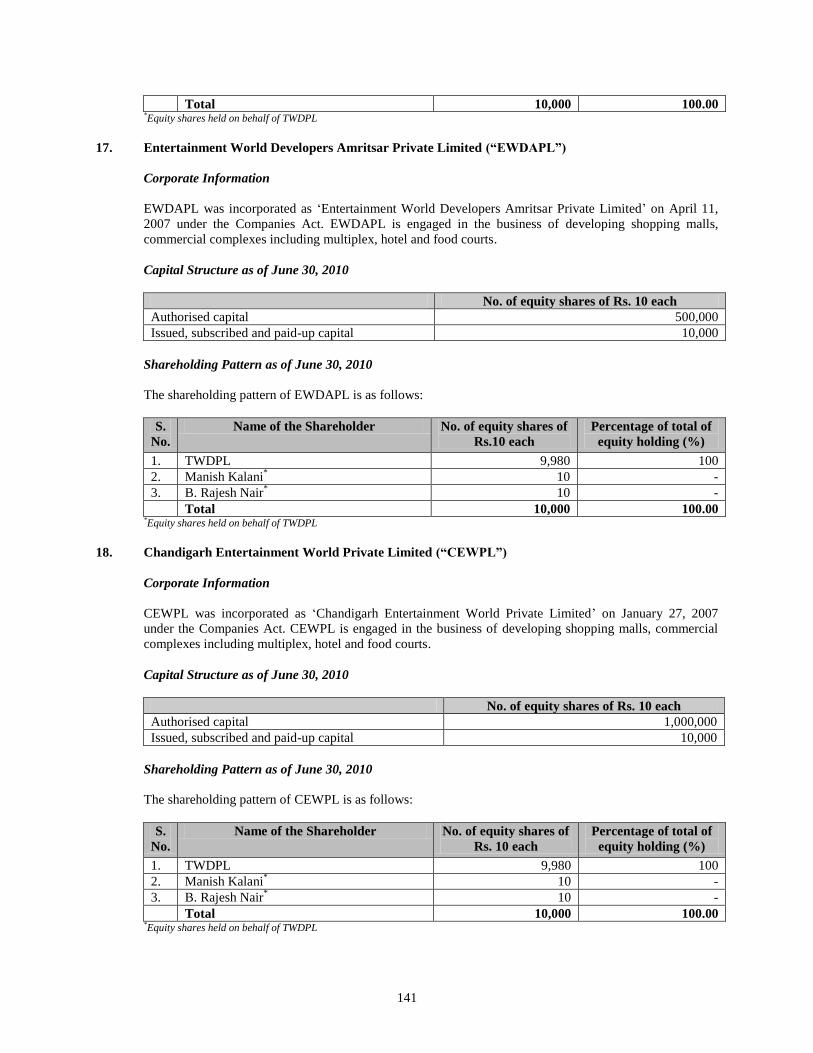

AEWDPL Annapoorna Entertainment World Developers Private Limited

Articles/Articles of Association Articles of Association of the Company

ATBPL Amaravati Treasure Bazaar Private Limited

Auditor The statutory auditor of the Company, Deloitte Haskins & Sells, Chartered

Accountants

BCCL The Baroda Commercial Corporation Limited

Board/Board of Directors The board of directors of the Company or a duly constituted committee thereof

CEO Chief Executive Officer

CEWPL Chandigarh Entertainment World Private Limited

Completed Projects Projects where construction has been completed and where the revenues of the

project have started

Corporate Office 6th

Floor, Treasure Island, 11, M. G. Road, Tukoganj, Indore 452 001

CRPL Cassandra Realty Private Limited

CTIPL Chandigarh Treasure Island Private Limited

Directors The director(s) of the Company, unless otherwise specified

DPPL Dazzling Properties Private Limited

EFSHPL EWDPL Five Star Hospitality Private Limited

ERHPL EWDPL Residential Holdings Private Limited

EWDAPL Entertainment World Developers Amritsar Private Limited

EWDBPL Entertainment World Developers Bijalpur Private Limited

Forthcoming Projects Projects in which the necessary legal documents relating to acquisition of land or

development rights have been executed, key land related approvals are being

obtained and management has prepared an initial design plan of the project or an

architect has been appointed and a detailed architect plan is in the process of

being prepared

Group Companies Companies, firms and ventures promoted by the Promoters, irrespective of

whether such entities are covered under section 370(1)(B) of the Companies Act

or not and disclosed in “Group Companies” on page 155 of this Draft Red

Herring Prospectus

IAF - III IDBI Trusteeship Services Limited (the merged entity after its merger with the

Western India Trustee and Executor Company Limited) in its capacity as trustee

of India Advantage Fund - III represented by its investment manager ICICI

Venture Funds Management Company Limited

ii

Term Description

IAF - IV IDBI Trusteeship Services Limited (the merged entity after its merger with the

Western India Trustee and Executor Company Limited) in its capacity as trustee

of India Advantage Fund - IV represented by its investment manager ICICI

Venture Funds Management Company Limited

ITMCPL Indore Treasure Market City Private Limited

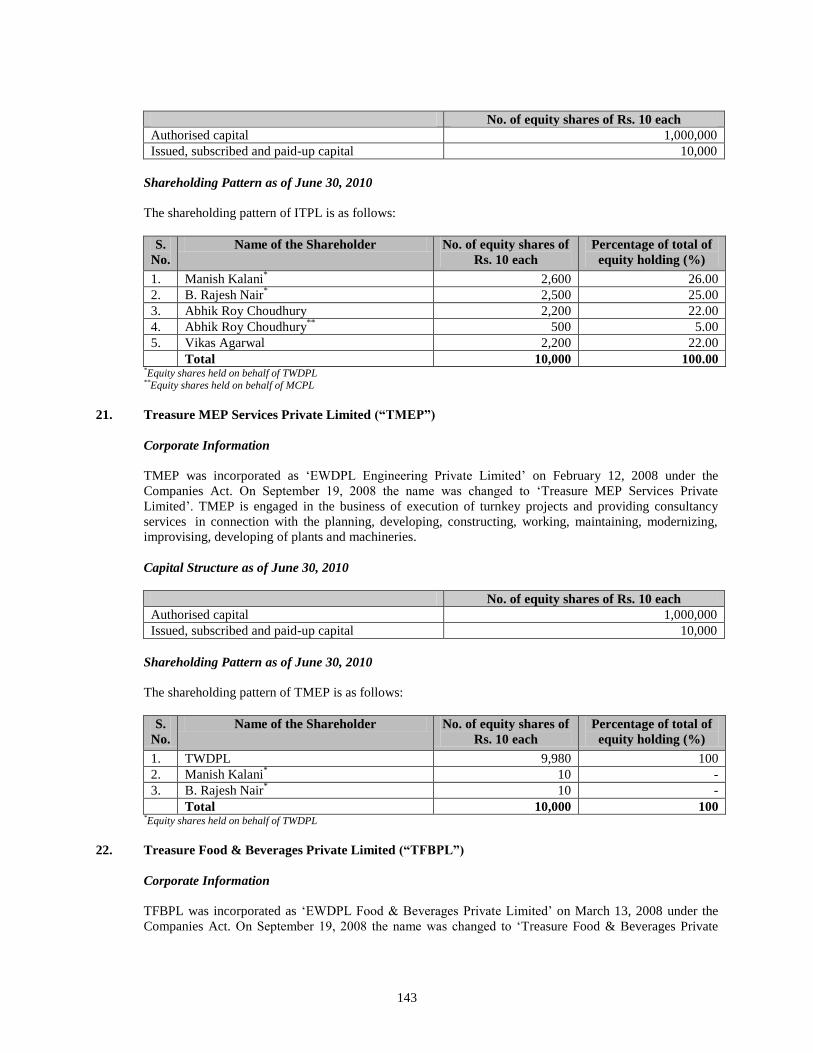

ITPL Intesys Technologies Private Limited

ITTPL Indore Treasure Town Private Limited

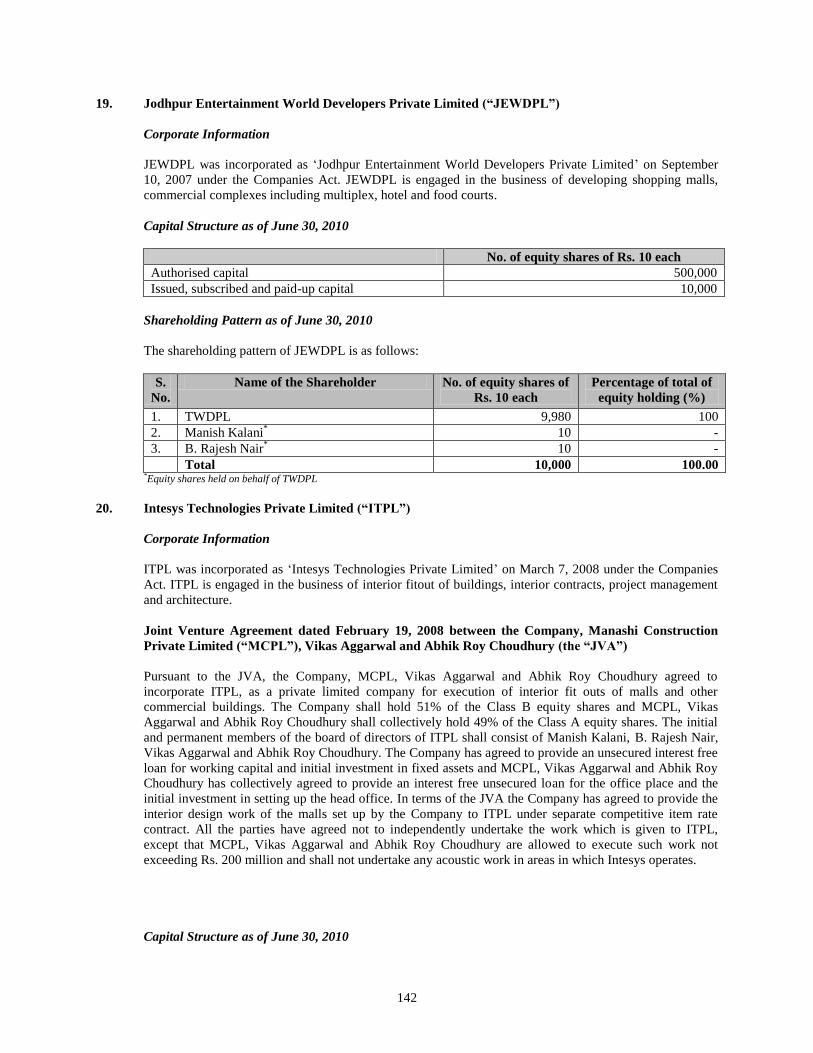

JEWDPL Jodhpur Entertainment World Developers Private Limited

JTIPL Jabalpur Treasure Island Private Limited

KBIPL Kalani Brothers (Indore) Private Limited

Memorandum/ Memorandum of

Association

Memorandum of Association of the Company, unless the context otherwise

specifies

MMDCPL Marvell Mall Development Company Private Limited

NMMCPL Naman Mall Management Company Private Limited

NTBPL Nanded Treasure Bazaar Private Limited

Ongoing Projects Projects in respect of which the necessary legal documents relating to the

acquisition of land or development rights have been executed by us and/ or key

land related approvals have been obtained and any one of the following activities

are being undertaken (not necessarily in the sequence set out herein): (a) on-site

construction of the project has commenced; (b) initial detailed design for civil

and landscaping is being undertaken and work has commenced on detailed

design; (c) project launch activity which includes the construction of a show

residence, sales office and other supporting infrastructure at the project site has

commenced; or (d) an architect has been appointed and a detailed concept design

has being prepared

PEWDPL Pune Entertainment World Developers Private Limited

PHPL Padma Homes Private Limited

PML The Phoenix Mills Limited

Promoters Manish Kalani, Kalani Brothers (Indore) Private Limited and Padma Homes

Private Limited

Promoter Group Unless the context otherwise requires, refers to such persons and entities

constituting the promoter group of the Company in terms of Regulation 2(zb) of

the SEBI Regulations and disclosed in “Promoters and Promoter Group” on page

149 of this Draft Red Herring Prospectus

Registered Office G-16, R. R. Hosiery Building, Shree Laxmi Woolen Mills, Opp. Shakti Mills

Compound, Off. Dr. E. Moses Road, Mahalaxmi, Mumbai 400 011

RTIPL Raipur Treasure Island Private Limited

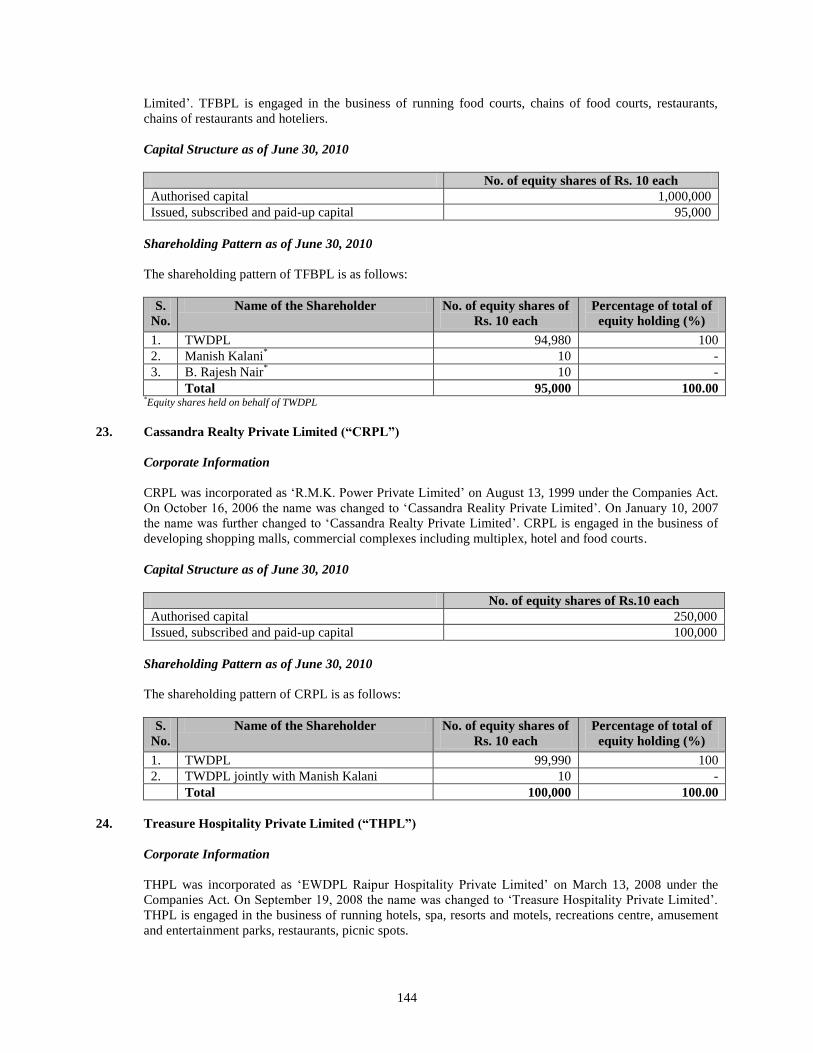

TFBPL Treasure Food & Beverages Private Limited

THPL Treasure Hospitality Private Limited

TMEP Treasure MEP Services Private Limited

TSPL Treasure Showcase Private Limited

TWCPL Treasure World Constructions Private Limited

TWDPL Treasure World Developers Private Limited

UTBPL Ujjain Treasure Bazaar Private Limited

UTMCPL Udaipur Treasure Market City Private Limited

WREPL Wanderland Real Estates Private Limited

Issue Related Terms

Term Description

Allotment/Allot/Allotted Unless the context otherwise requires, means the allotment of Equity Shares

pursuant to the Issue to the successful Bidders

Allottee A successful Bidder to whom the Equity Shares are Allotted

iii

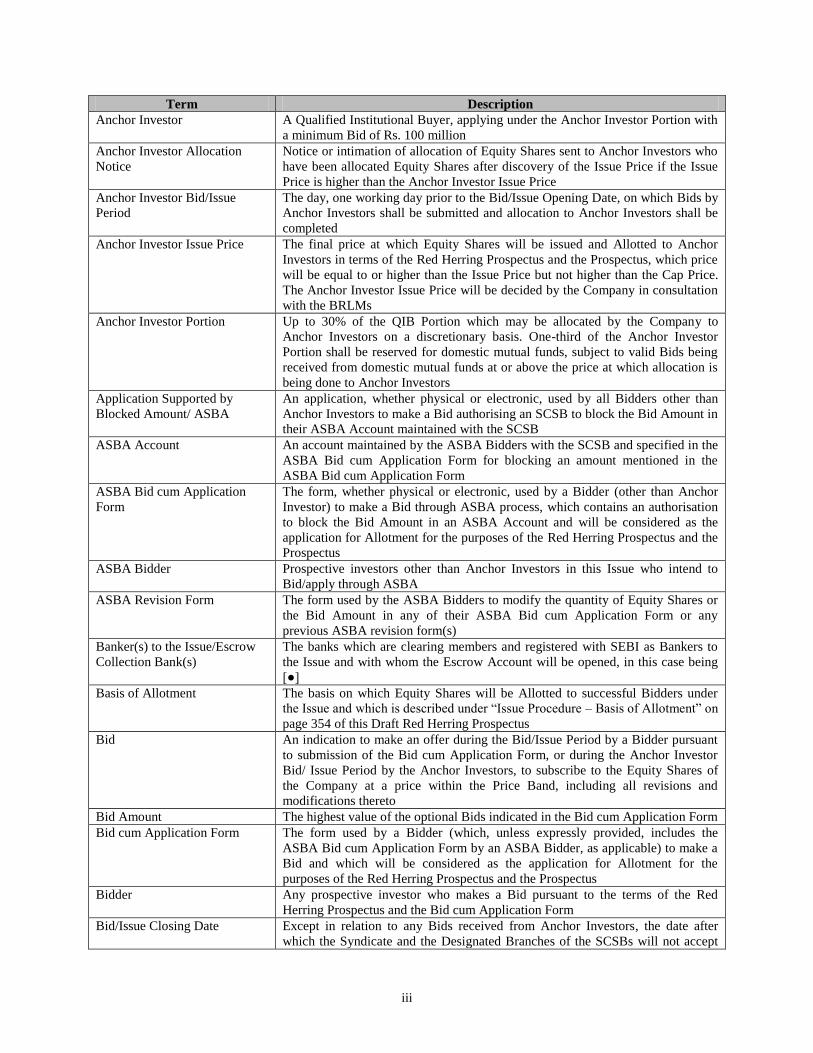

Term Description

Anchor Investor A Qualified Institutional Buyer, applying under the Anchor Investor Portion with

a minimum Bid of Rs. 100 million

Anchor Investor Allocation

Notice

Notice or intimation of allocation of Equity Shares sent to Anchor Investors who

have been allocated Equity Shares after discovery of the Issue Price if the Issue

Price is higher than the Anchor Investor Issue Price

Anchor Investor Bid/Issue

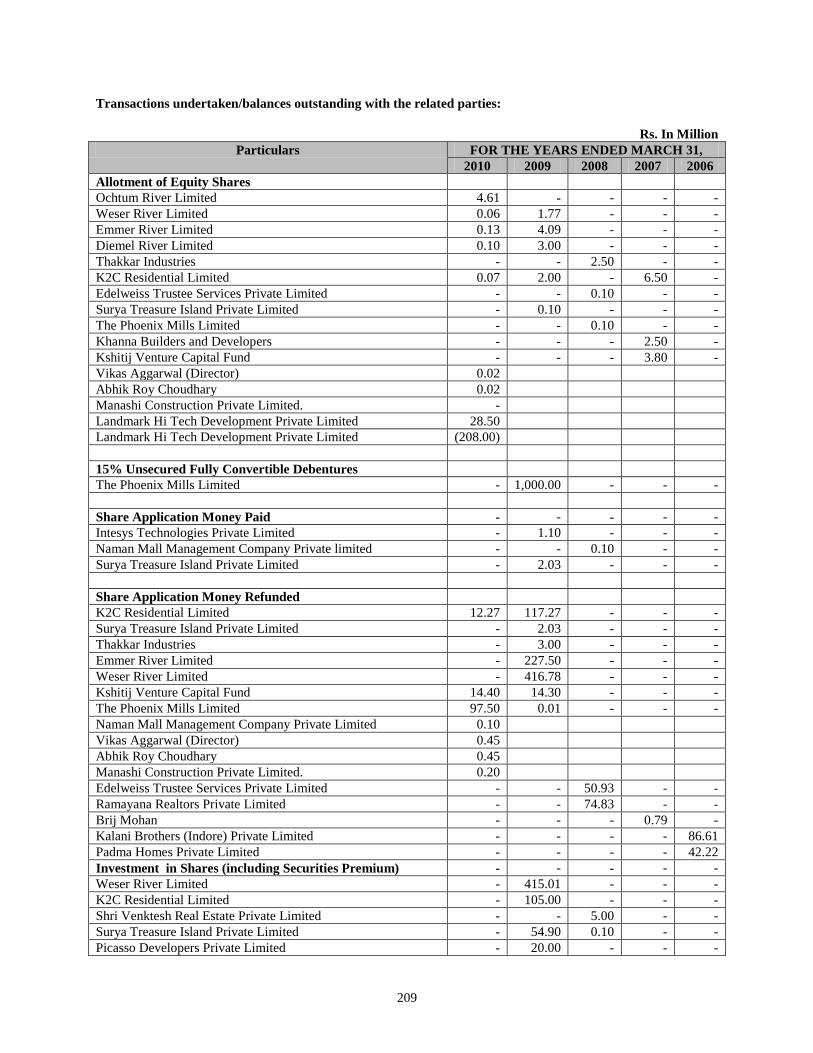

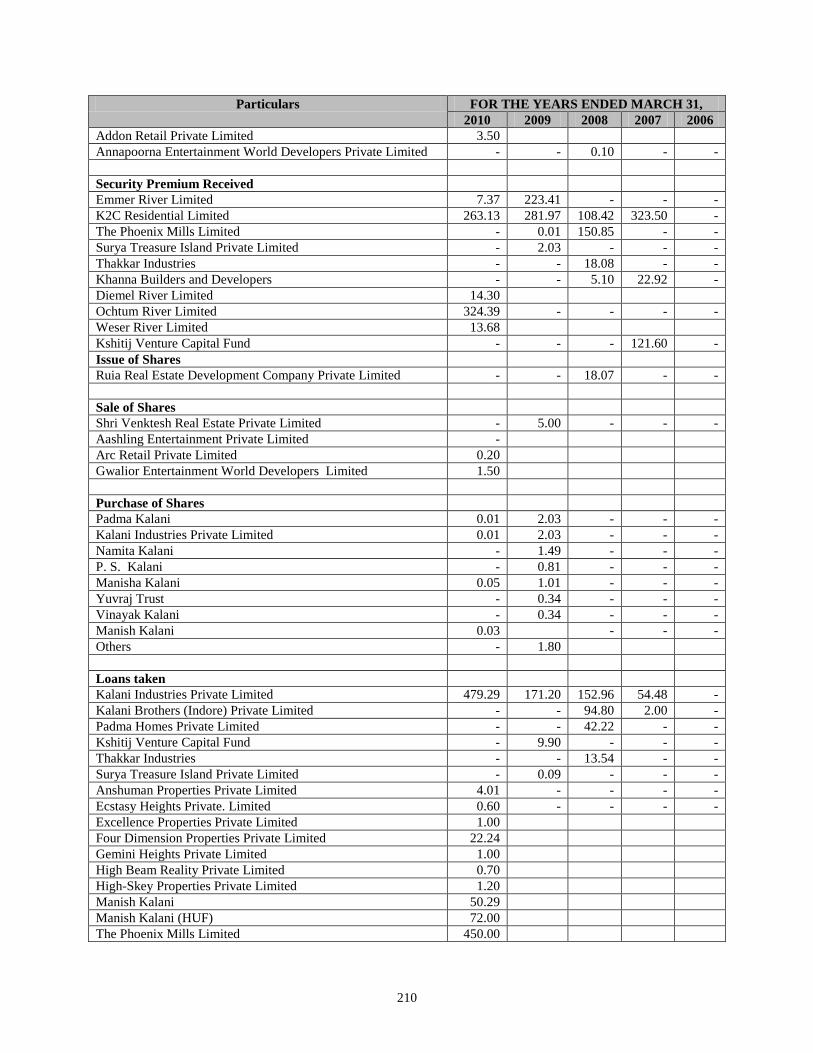

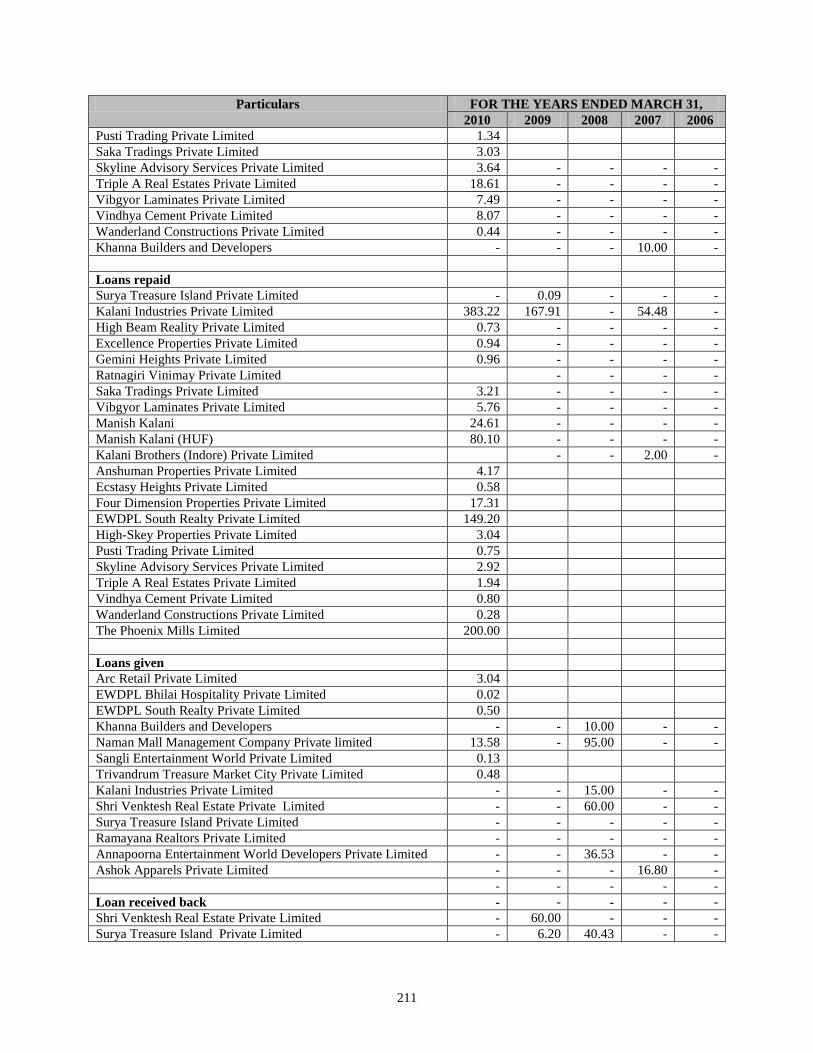

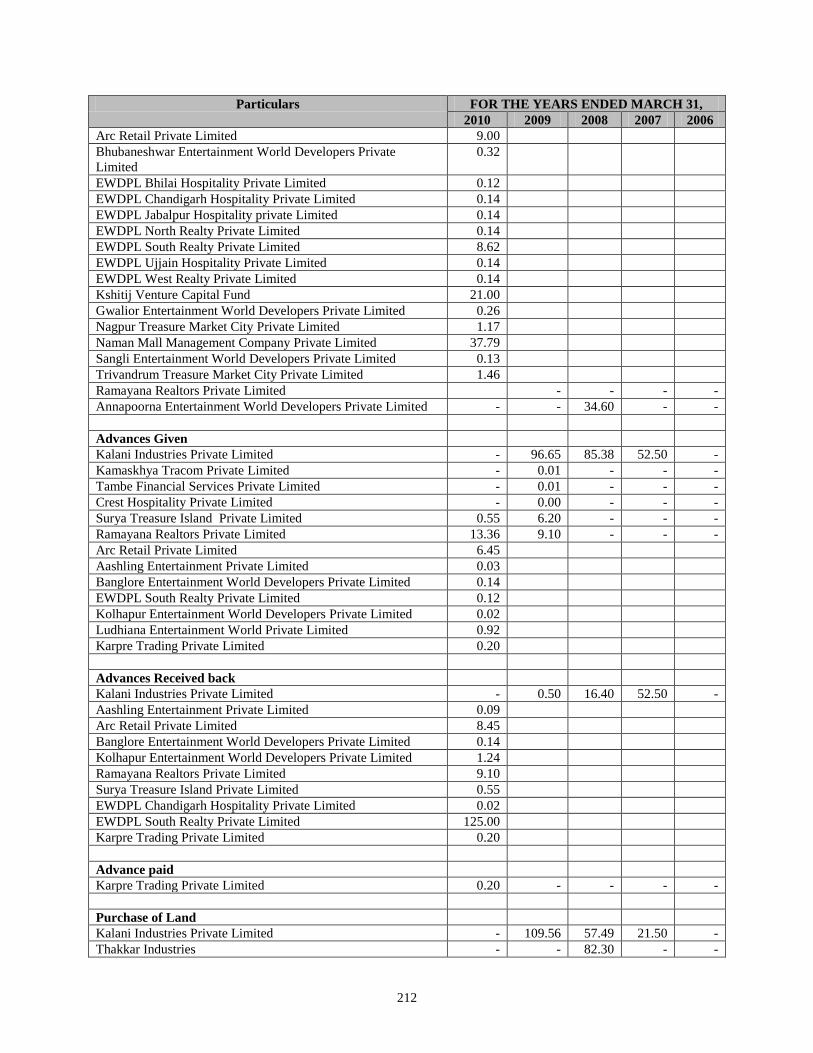

Period

The day, one working day prior to the Bid/Issue Opening Date, on which Bids by

Anchor Investors shall be submitted and allocation to Anchor Investors shall be

completed

Anchor Investor Issue Price The final price at which Equity Shares will be issued and Allotted to Anchor

Investors in terms of the Red Herring Prospectus and the Prospectus, which price

will be equal to or higher than the Issue Price but not higher than the Cap Price.

The Anchor Investor Issue Price will be decided by the Company in consultation

with the BRLMs

Anchor Investor Portion Up to 30% of the QIB Portion which may be allocated by the Company to

Anchor Investors on a discretionary basis. One-third of the Anchor Investor

Portion shall be reserved for domestic mutual funds, subject to valid Bids being

received from domestic mutual funds at or above the price at which allocation is

being done to Anchor Investors

Application Supported by

Blocked Amount/ ASBA

An application, whether physical or electronic, used by all Bidders other than

Anchor Investors to make a Bid authorising an SCSB to block the Bid Amount in

their ASBA Account maintained with the SCSB

ASBA Account An account maintained by the ASBA Bidders with the SCSB and specified in the

ASBA Bid cum Application Form for blocking an amount mentioned in the

ASBA Bid cum Application Form

ASBA Bid cum Application

Form

The form, whether physical or electronic, used by a Bidder (other than Anchor

Investor) to make a Bid through ASBA process, which contains an authorisation

to block the Bid Amount in an ASBA Account and will be considered as the

application for Allotment for the purposes of the Red Herring Prospectus and the

Prospectus

ASBA Bidder Prospective investors other than Anchor Investors in this Issue who intend to

Bid/apply through ASBA

ASBA Revision Form The form used by the ASBA Bidders to modify the quantity of Equity Shares or

the Bid Amount in any of their ASBA Bid cum Application Form or any

previous ASBA revision form(s)

Banker(s) to the Issue/Escrow

Collection Bank(s)

The banks which are clearing members and registered with SEBI as Bankers to

the Issue and with whom the Escrow Account will be opened, in this case being

[●]

Basis of Allotment The basis on which Equity Shares will be Allotted to successful Bidders under

the Issue and which is described under “Issue Procedure – Basis of Allotment” on

page 354 of this Draft Red Herring Prospectus

Bid An indication to make an offer during the Bid/Issue Period by a Bidder pursuant

to submission of the Bid cum Application Form, or during the Anchor Investor

Bid/ Issue Period by the Anchor Investors, to subscribe to the Equity Shares of

the Company at a price within the Price Band, including all revisions and

modifications thereto

Bid Amount The highest value of the optional Bids indicated in the Bid cum Application Form

Bid cum Application Form The form used by a Bidder (which, unless expressly provided, includes the

ASBA Bid cum Application Form by an ASBA Bidder, as applicable) to make a

Bid and which will be considered as the application for Allotment for the

purposes of the Red Herring Prospectus and the Prospectus

Bidder Any prospective investor who makes a Bid pursuant to the terms of the Red

Herring Prospectus and the Bid cum Application Form

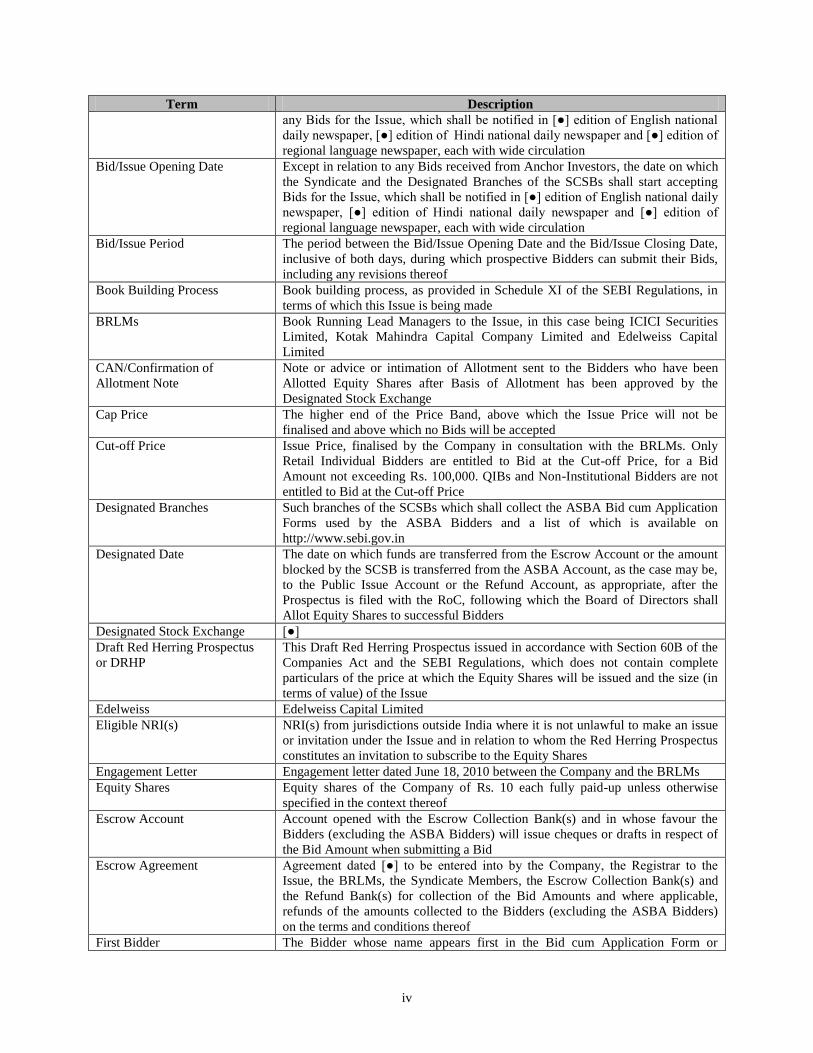

Bid/Issue Closing Date Except in relation to any Bids received from Anchor Investors, the date after

which the Syndicate and the Designated Branches of the SCSBs will not accept

iv

Term Description

any Bids for the Issue, which shall be notified in [●] edition of English national

daily newspaper, [●] edition of Hindi national daily newspaper and [●] edition of

regional language newspaper, each with wide circulation

Bid/Issue Opening Date Except in relation to any Bids received from Anchor Investors, the date on which

the Syndicate and the Designated Branches of the SCSBs shall start accepting

Bids for the Issue, which shall be notified in [●] edition of English national daily

newspaper, [●] edition of Hindi national daily newspaper and [●] edition of

regional language newspaper, each with wide circulation

Bid/Issue Period The period between the Bid/Issue Opening Date and the Bid/Issue Closing Date,

inclusive of both days, during which prospective Bidders can submit their Bids,

including any revisions thereof

Book Building Process Book building process, as provided in Schedule XI of the SEBI Regulations, in

terms of which this Issue is being made

BRLMs Book Running Lead Managers to the Issue, in this case being ICICI Securities

Limited, Kotak Mahindra Capital Company Limited and Edelweiss Capital

Limited

CAN/Confirmation of

Allotment Note

Note or advice or intimation of Allotment sent to the Bidders who have been

Allotted Equity Shares after Basis of Allotment has been approved by the

Designated Stock Exchange

Cap Price The higher end of the Price Band, above which the Issue Price will not be

finalised and above which no Bids will be accepted

Cut-off Price Issue Price, finalised by the Company in consultation with the BRLMs. Only

Retail Individual Bidders are entitled to Bid at the Cut-off Price, for a Bid

Amount not exceeding Rs. 100,000. QIBs and Non-Institutional Bidders are not

entitled to Bid at the Cut-off Price

Designated Branches Such branches of the SCSBs which shall collect the ASBA Bid cum Application

Forms used by the ASBA Bidders and a list of which is available on

http://www.sebi.gov.in

Designated Date The date on which funds are transferred from the Escrow Account or the amount

blocked by the SCSB is transferred from the ASBA Account, as the case may be,

to the Public Issue Account or the Refund Account, as appropriate, after the

Prospectus is filed with the RoC, following which the Board of Directors shall

Allot Equity Shares to successful Bidders

Designated Stock Exchange [●]

Draft Red Herring Prospectus

or DRHP

This Draft Red Herring Prospectus issued in accordance with Section 60B of the

Companies Act and the SEBI Regulations, which does not contain complete

particulars of the price at which the Equity Shares will be issued and the size (in

terms of value) of the Issue

Edelweiss Edelweiss Capital Limited

Eligible NRI(s) NRI(s) from jurisdictions outside India where it is not unlawful to make an issue

or invitation under the Issue and in relation to whom the Red Herring Prospectus

constitutes an invitation to subscribe to the Equity Shares

Engagement Letter Engagement letter dated June 18, 2010 between the Company and the BRLMs

Equity Shares Equity shares of the Company of Rs. 10 each fully paid-up unless otherwise

specified in the context thereof

Escrow Account Account opened with the Escrow Collection Bank(s) and in whose favour the

Bidders (excluding the ASBA Bidders) will issue cheques or drafts in respect of

the Bid Amount when submitting a Bid

Escrow Agreement Agreement dated [●] to be entered into by the Company, the Registrar to the

Issue, the BRLMs, the Syndicate Members, the Escrow Collection Bank(s) and

the Refund Bank(s) for collection of the Bid Amounts and where applicable,

refunds of the amounts collected to the Bidders (excluding the ASBA Bidders)

on the terms and conditions thereof

First Bidder The Bidder whose name appears first in the Bid cum Application Form or

v

Term Description

Revision Form or the ASBA Bid cum Application Form or the ASBA Revision

Form

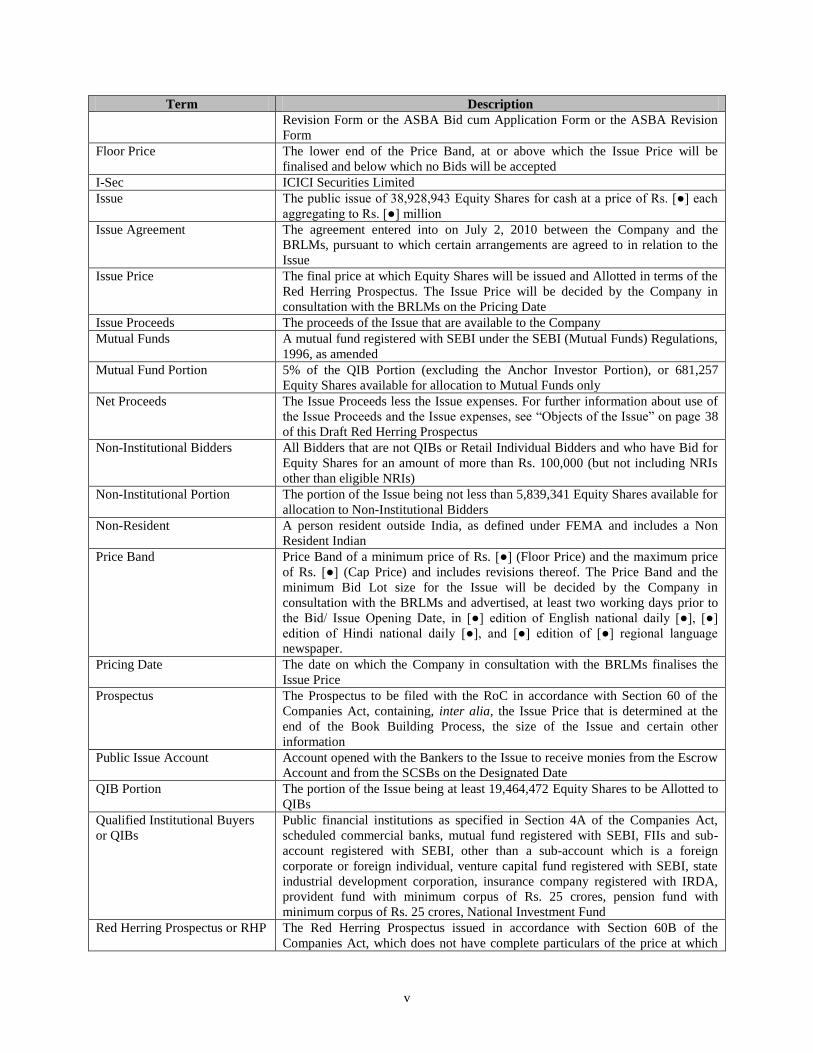

Floor Price The lower end of the Price Band, at or above which the Issue Price will be

finalised and below which no Bids will be accepted

I-Sec ICICI Securities Limited

Issue The public issue of 38,928,943 Equity Shares for cash at a price of Rs. [●] each

aggregating to Rs. [●] million

Issue Agreement The agreement entered into on July 2, 2010 between the Company and the

BRLMs, pursuant to which certain arrangements are agreed to in relation to the

Issue

Issue Price The final price at which Equity Shares will be issued and Allotted in terms of the

Red Herring Prospectus. The Issue Price will be decided by the Company in

consultation with the BRLMs on the Pricing Date

Issue Proceeds The proceeds of the Issue that are available to the Company

Mutual Funds A mutual fund registered with SEBI under the SEBI (Mutual Funds) Regulations,

1996, as amended

Mutual Fund Portion 5% of the QIB Portion (excluding the Anchor Investor Portion), or 681,257

Equity Shares available for allocation to Mutual Funds only

Net Proceeds The Issue Proceeds less the Issue expenses. For further information about use of

the Issue Proceeds and the Issue expenses, see “Objects of the Issue” on page 38

of this Draft Red Herring Prospectus

Non-Institutional Bidders All Bidders that are not QIBs or Retail Individual Bidders and who have Bid for

Equity Shares for an amount of more than Rs. 100,000 (but not including NRIs

other than eligible NRIs)

Non-Institutional Portion The portion of the Issue being not less than 5,839,341 Equity Shares available for

allocation to Non-Institutional Bidders

Non-Resident A person resident outside India, as defined under FEMA and includes a Non

Resident Indian

Price Band Price Band of a minimum price of Rs. [●] (Floor Price) and the maximum price

of Rs. [●] (Cap Price) and includes revisions thereof. The Price Band and the

minimum Bid Lot size for the Issue will be decided by the Company in

consultation with the BRLMs and advertised, at least two working days prior to

the Bid/ Issue Opening Date, in [●] edition of English national daily [●], [●]

edition of Hindi national daily [●], and [●] edition of [●] regional language

newspaper.

Pricing Date The date on which the Company in consultation with the BRLMs finalises the

Issue Price

Prospectus The Prospectus to be filed with the RoC in accordance with Section 60 of the

Companies Act, containing, inter alia, the Issue Price that is determined at the

end of the Book Building Process, the size of the Issue and certain other

information

Public Issue Account Account opened with the Bankers to the Issue to receive monies from the Escrow

Account and from the SCSBs on the Designated Date

QIB Portion The portion of the Issue being at least 19,464,472 Equity Shares to be Allotted to

QIBs

Qualified Institutional Buyers

or QIBs Public financial institutions as specified in Section 4A of the Companies Act,

scheduled commercial banks, mutual fund registered with SEBI, FIIs and sub-

account registered with SEBI, other than a sub-account which is a foreign

corporate or foreign individual, venture capital fund registered with SEBI, state

industrial development corporation, insurance company registered with IRDA,

provident fund with minimum corpus of Rs. 25 crores, pension fund with

minimum corpus of Rs. 25 crores, National Investment Fund

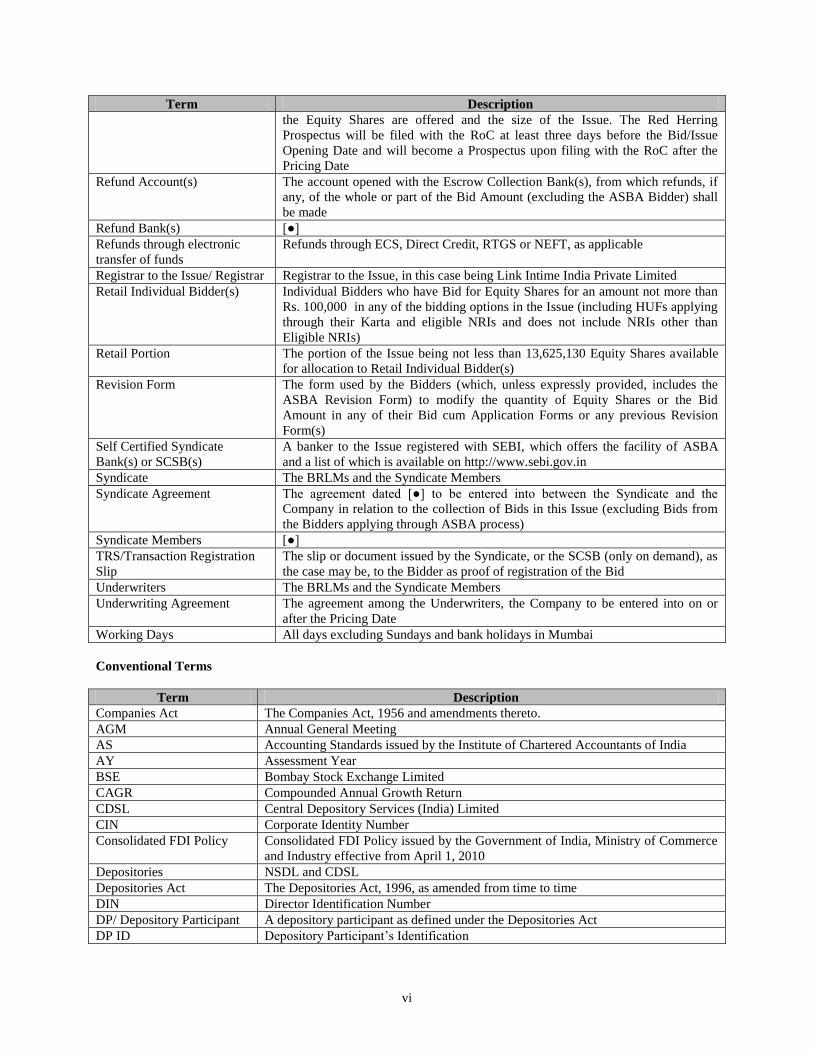

Red Herring Prospectus or RHP The Red Herring Prospectus issued in accordance with Section 60B of the

Companies Act, which does not have complete particulars of the price at which

vi

Term Description

the Equity Shares are offered and the size of the Issue. The Red Herring

Prospectus will be filed with the RoC at least three days before the Bid/Issue

Opening Date and will become a Prospectus upon filing with the RoC after the

Pricing Date

Refund Account(s) The account opened with the Escrow Collection Bank(s), from which refunds, if

any, of the whole or part of the Bid Amount (excluding the ASBA Bidder) shall

be made

Refund Bank(s) [●]

Refunds through electronic

transfer of funds

Refunds through ECS, Direct Credit, RTGS or NEFT, as applicable

Registrar to the Issue/ Registrar Registrar to the Issue, in this case being Link Intime India Private Limited

Retail Individual Bidder(s) Individual Bidders who have Bid for Equity Shares for an amount not more than

Rs. 100,000 in any of the bidding options in the Issue (including HUFs applying

through their Karta and eligible NRIs and does not include NRIs other than

Eligible NRIs)

Retail Portion The portion of the Issue being not less than 13,625,130 Equity Shares available

for allocation to Retail Individual Bidder(s)

Revision Form The form used by the Bidders (which, unless expressly provided, includes the

ASBA Revision Form) to modify the quantity of Equity Shares or the Bid

Amount in any of their Bid cum Application Forms or any previous Revision

Form(s)

Self Certified Syndicate

Bank(s) or SCSB(s)

A banker to the Issue registered with SEBI, which offers the facility of ASBA

and a list of which is available on http://www.sebi.gov.in

Syndicate The BRLMs and the Syndicate Members

Syndicate Agreement The agreement dated [●] to be entered into between the Syndicate and the

Company in relation to the collection of Bids in this Issue (excluding Bids from

the Bidders applying through ASBA process)

Syndicate Members [●]

TRS/Transaction Registration

Slip

The slip or document issued by the Syndicate, or the SCSB (only on demand), as

the case may be, to the Bidder as proof of registration of the Bid

Underwriters The BRLMs and the Syndicate Members

Underwriting Agreement The agreement among the Underwriters, the Company to be entered into on or

after the Pricing Date

Working Days All days excluding Sundays and bank holidays in Mumbai

Conventional Terms

Term Description

Companies Act The Companies Act, 1956 and amendments thereto.

AGM Annual General Meeting

AS Accounting Standards issued by the Institute of Chartered Accountants of India

AY Assessment Year

BSE Bombay Stock Exchange Limited

CAGR Compounded Annual Growth Return

CDSL Central Depository Services (India) Limited

CIN Corporate Identity Number

Consolidated FDI Policy Consolidated FDI Policy issued by the Government of India, Ministry of Commerce

and Industry effective from April 1, 2010

Depositories NSDL and CDSL

Depositories Act The Depositories Act, 1996, as amended from time to time

DIN Director Identification Number

DP/ Depository Participant A depository participant as defined under the Depositories Act

DP ID Depository Participant‟s Identification

vii

Term Description

EBITDA Earnings Before Interest, Tax, Depreciation and Amortisation

ECS Electronic Clearing Service

EGM Extraordinary General Meeting

EPS Earnings Per Share i.e., is calculated by dividing the net profit or loss for the period

attributable to equity shareholders by the weighted average number of equity shares

outstanding during the period.

FCNR Foreign Currency Non-Resident

FDI Foreign Direct Investment

FEMA

Foreign Exchange Management Act, 1999 read with rules and regulations thereunder

and amendments thereto

FEMA Regulations FEMA (Transfer or Issue of Security by a Person Resident Outside India)

Regulations 2000 and amendments thereto

FII(s) Foreign Institutional Investors as defined under SEBI (Foreign Institutional Investor)

Regulations, 1995, as amended, and registered with SEBI under applicable laws in

India

Financial Year/ Fiscal/ FY Unless stated otherwise, the period of 12 months ending March 31 of that particular

year

FIPB Foreign Investment Promotion Board

FVCI Foreign Venture Capital Investors

GDP Gross Domestic Product

GIR General Index Register

GoI/Government Government of India

HNI High Net Worth Individual

HUF Hindu Undivided Family

ICAI Institute of Chartered Accountants of India

IFRS International Financial Reporting Standards

Income Tax Act The Income Tax Act, 1961, as amended

Indian GAAP Generally Accepted Accounting Principles in India

LOI Letter of Intent

MCGM Municipal Corporation of Greater Mumbai

MHADA Maharashtra Housing Area Development Authority

Mn / mn Million

NA/ n.a. Not Applicable

National Investment Fund National Investment Fund set up by resolution no. F. No. 2/3/2005-DDII dated

November 23, 2005 of the Government of India published in the Gazette of India

NAV Net Asset Value

NEFT National Electronic Fund Transfer

NOC No Objection Certificate

NR Non-resident

NRE Account Non Resident External Account

NRI Non Resident Indian, being a person resident outside India, as defined under FEMA

and the FEMA Regulations

NRO Account Non Resident Ordinary Account

NSDL National Securities Depository Limited

NSE The National Stock Exchange of India Limited

OCB A company, partnership, society or other corporate body owned directly or

indirectly to the extent of at least 60% by NRIs including overseas trusts, in which

not less than 60% of beneficial interest is irrevocably held by NRIs directly or

indirectly as defined under the FEMA Regulations. OCBs are not allowed to invest

in this Issue.

p.a. Per annum

P/E Ratio Price/Earnings Ratio

PAN Permanent Account Number

viii

Term Description

PAT Profit After tax

PBT Profit Before tax

PIO Person of Indian Origin

PLR Prime Lending Rate

RBI The Reserve Bank of India

RoC The Registrar of Companies, Maharashtra located at 100, Everest, Marine Drive,

Mumbai 400 002

RONW Return on Net Worth

Rs./Rupees Indian Rupees

RTGS Real Time Gross Settlement

SCRA Securities Contracts (Regulation) Act, 1956, as amended

SCRR Securities Contracts (Regulation) Rules, 1957, as amended

SEBI The Securities and Exchange Board of India constituted under the SEBI Act, 1992,

as amended

SEBI Act Securities and Exchange Board of India Act 1992, as amended

SEBI Regulations SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009, as

amended

SEBI Takeover Regulations Securities and Exchange Board of India (Substantial Acquisition of Shares and

Takeovers) Regulations, 1997, as amended

SIA Secretariat for Industrial Assistance

SICA Sick Industries Companies (Special Provisions) Act, 1985

SPV Special Purpose Vehicle

Sq. Ft./ sq. ft. Square feet

Sq. Mts./ sq. mts. Square metres

State Government The government of a State of India

Stock Exchanges BSE and the NSE

UIN Unique Identification Number

US / United States United States of America

US GAAP Generally Accepted Accounting Principles in the United States of America

USD/US$ United States Dollars

Securities Act U.S. Securities Act, 1933, as amended

VCFs Venture Capital Funds as defined in and registered with SEBI under the SEBI

(Venture Capital Fund) Regulations, 1996, as amended

Technical/Industry Related Terms

Term Description

Developable Area The total construction area which we develop in each property, and includes carpet

area, wall area, common area, service and storage area, as well as other areas,

including car parking.

FSI Floor Space Index, which means the quotient of the ratio of the combined gross floor

area of all floors, excepting areas specifically exempted, to the total area of the plot

Leaseable Area Is calculated by the loading percentage (the percentage of a tenant‟s rent applied

towards a shopping center‟s common areas) of 10.00% to 60.00% of the carpet area

of the property, depending upon the use, and refers to the part of the Developable

Area that can be leased out to third parties

Saleable Area The part of the area relating to our economic interest in each property

ix

PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA

Financial Data

Unless stated otherwise, the financial data in this Draft Red Herring Prospectus is derived from the audited

consolidated and unconsolidated financial statements for the financial years ended March 31, 2010, 2009, 2008,

2007 and 2006, prepared in accordance with Indian GAAP and the Companies Act and restated in accordance with

the SEBI Regulations and included in this Draft Red Herring Prospectus. In this Draft Red Herring Prospectus, any

discrepancies in any table between the total and the sums of the amounts listed are due to rounding off. All decimals

have been rounded off to two decimals points.

Our fiscal year commences on April 1 and ends on March 31 of the next year, so all references to particular Fiscal,

unless stated otherwise, are to the 12 months period ended on March 31 of that year.

There are significant differences between Indian GAAP, US GAAP and IFRS. The Company has not attempted to

explain those differences or quantify their impact on the financial data included herein, and to the investors shall

consult their own advisors regarding such differences and their impact on the financial data. Accordingly, the degree

to which the Indian GAAP financial statements included in this Draft Red Herring Prospectus will provide

meaningful information is entirely dependent on the reader‟s level of familiarity with Indian accounting practices.

Any reliance by persons not familiar with Indian accounting practices on the financial disclosures presented in this

Draft Red Herring Prospectus should accordingly be limited.

Currency and Units of Presentation

All references to “Rupees” or “Rs.” are to Indian Rupees, the official currency of the Republic of India. All

references to “US$” or “USD” are to United States Dollars, the official currency of the United States of America.

In this Draft Red Herring Prospectus, the Company has presented certain information related to land in various units.

The conversion ratio of such units is as follows:

1 hectare = 2.47 acres

1 acre = 4,046.85 sq. mts.

1 acre = 43,560.00 sq. ft.

1 sq. mts. = 10.76 sq. ft.

Industry and Market Data

Unless stated otherwise, industry and market data used in this Draft Red Herring Prospectus has been obtained or

derived from publicly available information as well as industry publications and sources. Industry publications

generally state that the information contained in those publications has been obtained from sources believed to be

reliable but that their accuracy and completeness are not guaranteed and their reliability cannot be assured.

Accordingly, no investment decision should be made on the basis of such information. Although industry data used

in this Draft Red Herring Prospectus is reliable, it has not been independently verified.

The extent to which the market and industry data used in this Draft Red Herring Prospectus is meaningful depends

on the reader‟s familiarity with and understanding of the methodologies used in compiling such data.

x

FORWARD-LOOKING STATEMENTS

This Draft Red Herring Prospectus contains certain “forward-looking statements”. These forward-looking

statements generally can be identified by words or phrases such as “aim”, “anticipate”, “believe”, “expect”,

“estimate”, “intend”, “objective”, “plan”, “project”, “shall”, “will”, “will continue”, “will pursue” or other words or

phrases of similar import. Similarly, statements that describe the Company‟s strategies, objectives, plans or goals are

also forward-looking statements. All forward-looking statements are subject to risks, uncertainties and assumptions

about the Company that could cause actual results and property valuations to differ materially from those

contemplated by the relevant forward-looking statement.

Actual results may differ materially from those suggested by the forward-looking statements due to risks or

uncertainties associated with the expectations with respect to, but not limited to, regulatory changes pertaining to the

industries in India in which we have our businesses and our ability to respond to them, our ability to successfully

implement our strategy, our growth and expansion, technological changes, our exposure to market risks, general

economic and political conditions in India and which have an impact on our business activities or investments, the

monetary and fiscal policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange

rates, equity prices or other rates or prices, the performance of the financial markets in India and globally, changes

in domestic laws, regulations and taxes and changes in competition in our industry. Important factors that could

cause actual results to differ materially from our expectations include, but are not limited to, the following:

The performance of, and the prevailing conditions affecting, the real estate market in India generally;

development rights in respect of certain of our projects are subject to conditions, certain of which have not

been or may not be satisfied;

volatility in prices of, or shortages of, key building materials;

changes to the FSI/TDR regime;

financial stability of our tenants, in particular, our key tenants and our hotel and school operators;

changes to the slum rehabilitation schemes; and

difficulties in expanding our business into additional geographical markets in India.

For further discussion of factors that could cause the actual results to differ from the expectations, see “Risk

Factors”, “Business” and “Management‟s Discussion and Analysis of Financial Condition and Results of

Operations” on pages xi, 76 and 266 of this Draft Red Herring Prospectus, respectively. By their nature, certain

market risk disclosures are only estimates and could be materially different from what actually occurs in the future.

As a result, actual gains or losses could materially differ from those that have been estimated.

Forward-looking statements reflect the current views as of the date of this Draft Red Herring Prospectus and are not

a guarantee of future performance. Neither the Company, the Directors, the Underwriters nor any of their respective

affiliates have any obligation to update or otherwise revise any statements reflecting circumstances arising after the

date hereof or to reflect the occurrence of underlying events, even if the underlying assumptions do not come to

fruition. In accordance with SEBI requirements, the Company and the BRLMs will ensure that investors in India are

informed of material developments until the time of the grant of listing and trading permission by the Stock

Exchanges.

xi

SECTION II: RISK FACTORS

The risks and uncertainties described below together with the other information contained in this Draft Red Herring

Prospectus should be carefully considered before making an investment decision in the Equity Shares. The risks

described below are not the only ones relevant to the country, the industry in which we operate, or the Equity

Shares. Additional risks, not presently known to us or that we currently deem immaterial, may also impair our

business and operations. If any of the risks described below actually occur, our business, prospects, financial

condition and results of operations could suffer, the trading price of the Equity Shares could decline, and

prospective investors may lose all or part of their investment.

Prospective investors should pay particular attention to the fact that we are incorporated under the laws of India

and are subject to a legal and regulatory environment, which may differ in certain respects from that of other

countries.

This Draft Red Herring Prospectus also contains forward-looking statements that involve risk and uncertainties.

Our actual results could differ from those anticipated in these forward-looking statements as a result of certain

factors, including the considerations described below and elsewhere in this Draft Red Herring Prospectus. See

“Forward-Looking Statements” on page x of this Draft Red Herring Prospectus.

Unless specified or quantified in the relevant risk factors below, we are not in a position to quantify the financial or

other implication of any of the risks described in this section.

RISKS RELATING TO OUR BUSINESS

1. Most of our Ongoing Projects and Forthcoming Projects are still under development and have not

commenced operation; these projects are consequently exposed to a number of risks and uncertainties.

Most of our projects are still under development. The development of these new projects involves various

risks including, regulatory risks, financing risks and the risks that these projects may ultimately prove to be

unprofitable. These projects under development may pose significant challenges to our management,

administrative, financial and operational resources. We cannot provide any assurance that we will succeed

in any of these projects or that we will recover our investments. Any delay or failure in the development,

financing or operation of any of our new projects, or increase in their costs of development, is likely to

affect our business, prospects, financial condition and results of operations. We may be affected by the

development of our projects due to the following reasons:

the contractors and third parties hired to complete the projects may be unable to complete the

construction of the project on time, within budget or to the required specifications and standards;

delays in completion and commercial operation could increase the financing and other costs

associated with the construction and cause us to spend more capital than we anticipated for a

project;

we may be unable to obtain adequate capital or other financing at competitive rates to complete

construction of and to commence operations of these projects;

we may be unable to recover the amounts already invested in these projects if the assumptions

contained in the feasibility studies for these projects do not materialize.

While we expect most of the third parties for our projects to provide certain customary guarantees and

indemnities as to timely completion and cost overruns in the relevant construction contracts, these

guarantees and indemnities may not cover the entire amount of any cost overruns and we may be unable to

recover any or all amounts under such guarantees and indemnities. In addition, while we expect insurance

policies will be taken to cover natural disaster risks and other insurable risks, we cannot assure you that any

cost overruns or additional liabilities would be adequately covered by such insurance policies. As a result,

xii

we cannot assure you that our current or future projects under development will be completed, or, if

completed, will be completed on time or within budget.

2. We are dependent upon a few contractors and third party entities for the development of our projects,

and the inability or unwillingness of such third parties to provide their services to us on a timely and

cost-efficient basis may adversely affect our business and results of operations.

We undertake the management of our construction and fit out activity through Treasure MEP Services

Private Limited (“TMEP”) our wholly owned subsidiary and Intesys Technologies Private Limited

(“Intesys”), a Delhi based interior and fit-out specialist company in which we hold a 51.00% equity

interest. These companies in turn enter into agreements with other third parties and contractors such as

architects, engineers, and other suppliers of labor and materials to develop the property according to our

specifications and quality standards. The timing and quality of construction of the projects we develop

depends on the availability and skill of such third parties, as well as contingencies affecting them, including

labor and raw material shortages and industrial action such as strikes and lockouts. We may be unable to

identify appropriate experienced third parties and cannot assure you that skilled third parties will continue

to be available at reasonable rates and in the areas in which we undertake our projects, or at all. As a result,

we may be required to make additional investments or provide additional services to ensure the adequate

performance and delivery of contracted services. Any consequent delay in project execution could

adversely affect our profitability and reputation.

If such contractors or third party entities are unable to perform their contracts, including completing our

developments within the specifications, quality standards and time frames specified by us, at the estimated

cost, or at all, our business, reputation and results of operations could be adversely affected. While our

contractors provide us with back-to-back warranties, such warranties may be insufficient to cover our

losses and such losses could adversely affect our financial condition and results of operations. Further, we

cannot assure you that the services rendered by any of our independent construction contractors will always

be satisfactory or match our requirements for quality. We may therefore incur losses as a result of our

projects being delayed or disrupted or having to fund the repair of defective work or pay damages to

persons who have suffered losses as a result of such defective work. We have limited control over the cost,

availability or quality of their products or services, and as such the inability or unwillingness of other third-

party suppliers and sub-contractors to provide their products and services to us, including on a timely and

cost-efficient basis, may adversely affect our business and results of operations.

Further, the amount of property development in India has been significant in the recent past. As a result,

our contractors and other construction companies have had significant projects to complete and a

substantial backlog. If the services of these or other contractors do not continue to be available on terms

acceptable to us, or at all, our business and results of operations could be adversely affected. Additionally,

our operations may be affected by circumstances beyond our control such as work stoppages, labor

disputes, shortage of qualified skilled labor or lack of availability of adequate infrastructure.

Our joint venture partners, contractors and service providers may also face financial, legal or other

difficulties which may affect their ability to continue with a project. We may therefore be required to make

additional investments in the joint venture, provide extra funding or become liable for other obligations,

which could result in delays to our projects, reduced profits or, in some cases, significant losses.

3. The success of our future projects depends on our ability to identify properties in appropriate locations

to attract suitable businesses and customers.

Our ability to identify suitable new projects is fundamental to the growth of our business and involves

certain risks, including identifying and acquiring appropriate land, appealing to the tastes and needs of our

retail, residential, commercial and hospitality customers, understanding and responding to the requirements

of such customers and anticipating the changing trends in India. In identifying new projects, we also need

to take into account land use regulations, the land‟s location, including access and neighborhood, the land‟s

proximity to resources such as water and electricity and the availability and competence of third parties

such as architects, surveyors, engineers and contractors. We may not be as successful in identifying suitable

xiii

projects that meet market demand in the future. The failure to identify suitable projects and develop

properties that meet customer demand in a timely manner could result in loss or reduced profits. In

addition, it could reduce the number of projects we undertake and slow our growth.

In addition, we believe that in order to successfully operate retail developments we need to have the ability

to forecast demand, as well as enter into leasing arrangements with popular retailers. We believe that in

order to draw consumers away from traditional shopping environments, such as small local retail stores or

markets as well as from competing centers, we need to create demand for our retail developments where

customers can take advantage of a variety of consumer and retail options, such as large department stores,

in addition to amenities such as designer stores, comprehensive entertainment facilities, including

multiplexes, restaurants, bars, air conditioning and parking. Further, to help ensure our shopping centers‟

success, we must secure suitable anchor tenants and other retailers as they play a key role in generating

customer traffic. A decline in consumer and retail spending or a decrease in the popularity of the retailers‟

businesses could cause retailers to cease operations or experience significant financial difficulties that in

turn could harm our ability to continue to attract successful retailers and visitors to our projects.

4. There are criminal proceedings currently pending against one of the Promoters and certain Directors of

the Company.

There are criminal proceedings outstanding against one of our Promoters and certain Directors. A criminal

complaint has been filed by the State of Madhya Pradesh against the Promoter and Managing Director,

Manish Kalani and the Executive Director, B. Rajesh Nair in their capacity as directors of Naman Mall

Management Company Private Limited in relation to the death of a worker. A criminal complaint has been

filed by Mahesh Garg against Manish Kalani and others before the Director General of Police and

Superintendent of Police, Economic Offence Wing, Bhopal. Further, a complaint is pending against one of

the Directors, Mukesh Kacker in his capacity as the managing director of M.P Urja Vikas Nigam in relation

to alleged irregularities in the tender process for the supply of goods.

An adverse outcome in any or all of these criminal proceedings involving the Promoter or Directors could

have an adverse effect on their ability to serve our Company, as well as on our business, financial condition

and results of operations. We cannot assure you that any of these proceedings will be decided in favour of

the Directors, or that no further liability will arise out of these proceedings. For further details, see the

section “Outstanding Litigation and Material Developments” on page 288 of this Draft Red Herring

Prospectus.

5. There are outstanding legal proceedings involving our Company, our Subsidiaries, Directors and

Promoter.

There are outstanding legal proceedings involving our Company, our Subsidiaries, Directors and

Promoters. These proceedings are pending at different levels of adjudication before various courts,

tribunals, enquiry officers, appellate tribunals and arbitrators. A criminal complaint has also been filed

against Manish Kalani and B. Rajesh Nair, in relation to an accident at the construction site under the

Building and Other Construction Workers (Regulation of Employment & Condition of Service) Act, 1996,

in their capacity as directors of Naman Mall Management Company Private Limited. For further details,

see “Outstanding Litigation and Material Developments” on page 288 of this Draft Red Herring Prospectus.

In addition, further liability may arise out of these claims. Brief details of such outstanding litigation as of

the date of the Draft Red Herring Prospectus are as follows:

Litigation against the Company

Sr.

No.

Nature of cases No. of outstanding cases Amount Involved

(in Rs. million)

1. Civil proceedings 3 0.09

xiv

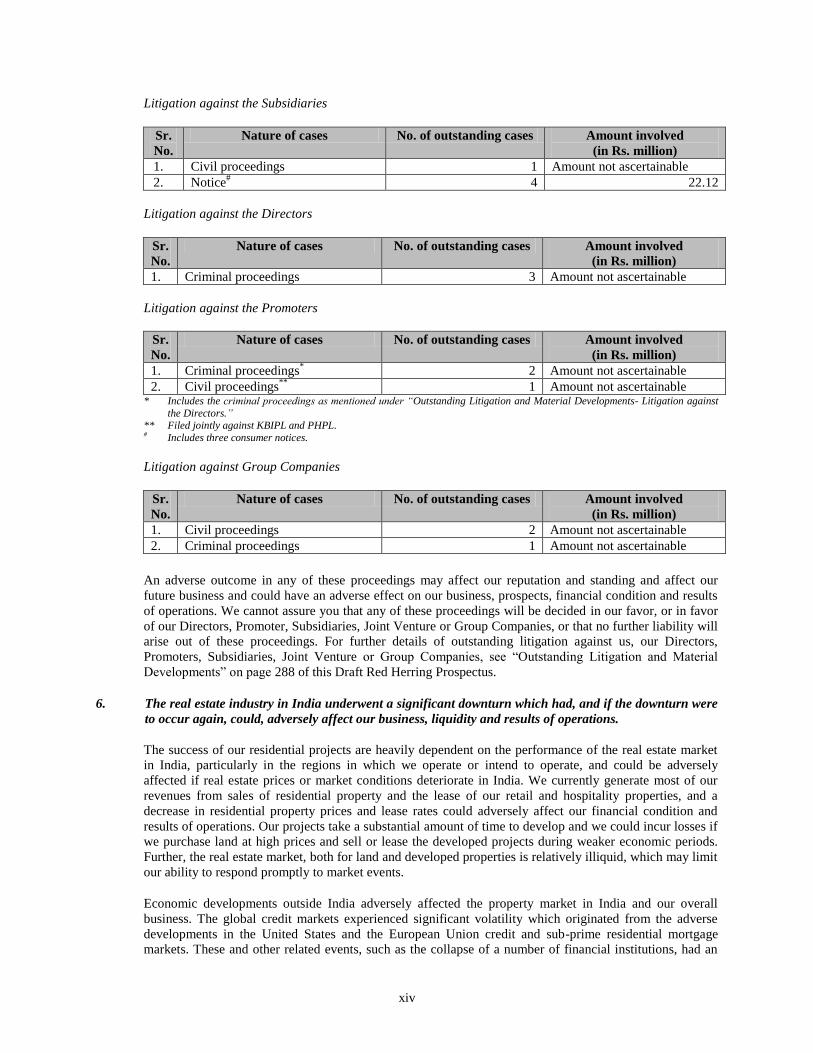

Litigation against the Subsidiaries

Sr.

No.

Nature of cases No. of outstanding cases Amount involved

(in Rs. million)

1. Civil proceedings 1 Amount not ascertainable

2. Notice#

4 22.12

Litigation against the Directors

Sr.

No.

Nature of cases No. of outstanding cases Amount involved

(in Rs. million)

1. Criminal proceedings 3 Amount not ascertainable

Litigation against the Promoters

Sr.

No.

Nature of cases No. of outstanding cases Amount involved

(in Rs. million)

1. Criminal proceedings* 2 Amount not ascertainable

2. Civil proceedings** 1 Amount not ascertainable

* Includes the criminal proceedings as mentioned under “Outstanding Litigation and Material Developments- Litigation against

the Directors.” ** Filed jointly against KBIPL and PHPL. # Includes three consumer notices.

Litigation against Group Companies

Sr.

No.

Nature of cases No. of outstanding cases Amount involved

(in Rs. million)

1. Civil proceedings 2 Amount not ascertainable

2. Criminal proceedings 1 Amount not ascertainable

An adverse outcome in any of these proceedings may affect our reputation and standing and affect our

future business and could have an adverse effect on our business, prospects, financial condition and results

of operations. We cannot assure you that any of these proceedings will be decided in our favor, or in favor

of our Directors, Promoter, Subsidiaries, Joint Venture or Group Companies, or that no further liability will

arise out of these proceedings. For further details of outstanding litigation against us, our Directors,

Promoters, Subsidiaries, Joint Venture or Group Companies, see “Outstanding Litigation and Material

Developments” on page 288 of this Draft Red Herring Prospectus.

6. The real estate industry in India underwent a significant downturn which had, and if the downturn were

to occur again, could, adversely affect our business, liquidity and results of operations.

The success of our residential projects are heavily dependent on the performance of the real estate market

in India, particularly in the regions in which we operate or intend to operate, and could be adversely

affected if real estate prices or market conditions deteriorate in India. We currently generate most of our

revenues from sales of residential property and the lease of our retail and hospitality properties, and a

decrease in residential property prices and lease rates could adversely affect our financial condition and

results of operations. Our projects take a substantial amount of time to develop and we could incur losses if

we purchase land at high prices and sell or lease the developed projects during weaker economic periods.

Further, the real estate market, both for land and developed properties is relatively illiquid, which may limit

our ability to respond promptly to market events.

Economic developments outside India adversely affected the property market in India and our overall

business. The global credit markets experienced significant volatility which originated from the adverse

developments in the United States and the European Union credit and sub-prime residential mortgage

markets. These and other related events, such as the collapse of a number of financial institutions, had an

xv

adverse effect on the availability of credit and the confidence of the financial markets globally, as well as in

India.

In light of these events, the real estate industry was significantly affected. An industry-wide softening of

demand for property resulted from a lack of consumer confidence, decreased affordability, decreased

availability of mortgage financing, and large supplies of resale and new inventories. Though the global

credit market and the Indian real estate market have recovered, economic turmoil may have other

unforeseen consequences, leading to uncertainty about future conditions in the real estate industry. We

cannot assure you that Government responses to the disruptions in the financial markets have restored

consumer confidence, stabilized the markets or increased liquidity and the availability of credit. Such

recurrence of the downturn would have an adverse effect on our business, liquidity and results of

operations.

7. Our business is heavily dependent on the availability of real estate financing in India and the failure to

obtain additional financing may adversely affect our ability to grow and our future profitability.

Our business and growth strategy is highly capital intensive, requiring substantial capital on acceptable

terms to develop and market our projects. The actual amount and timing of our future capital requirements

may also differ from estimates as a result of, among other things, unforeseen delays or cost overruns in

developing our projects, unanticipated expenses, regulatory changes and engineering design changes. See

“Management‟s Discussion and Analysis of Financial Condition and Results of Operations - Financial

Condition, Liquidity and Capital Resources - Capital Expenditures” and “Business - Strategies” on pages

283 and 80, respectively of this Draft Red Herring Prospectus. To the extent our capital expenditure

requirements exceed our available resources we will be required to seek additional debt or equity financing.

Additional debt financing could increase our interest cost and require us to comply with additional

restrictive covenants in our financing agreements. Additional equity financing could dilute our earnings per

share which could adversely affect our share price. In addition, the Indian regulations on foreign investment

in townships, housing, built-up infrastructure and construction and development projects impose significant

restrictions on us.

Our ability to obtain additional financing on favorable commercial terms, if at all, will depend on a number

of factors, including:

● our future financial condition, results of operations and cash flows;

● the amount and terms of our existing indebtedness;

● our credit rating;

● general market conditions for financing activities by real estate companies; and

● economic, political and other conditions in the markets where we operate.

Our attempts to consummate future financings may not be successful or be on favorable terms and failure

to obtain financing on terms favorable to us could have an adverse effect on our business prospects and

results of operations.

In addition, it is customary in the real estate business in which we operate to provide mobilization advances

in favor of third party contractors to secure obligations under contracts. We may not be able to continue

obtaining additional indebtedness or other access to capital in sufficient amounts to meet our business

requirements. If we are unable to incur sufficient additional indebtedness or have access to capital, our

ability to grow could be limited.

xvi