Energy Prices Steal the Show FORECASTER - CANADA #1 BEST ... · The limited means of transporting...

8

COMMODITY TRENDS François Dupuis, Vice-President and Chief Economist • Carine Bergevin-Chammah, Economist • Mathieu D’Anjou, Senior Economist Desjardins, Economic Studies: 514-281-2336 or 1 866-866-7000, ext. 5552336 • [email protected] • desjardins.com/economics NOTE TO READERS: The letters k, M and B are used in texts and tables to refer to thousands, millions and billions respectively. IMPORTANT: This document is based on public information and may under no circumstances be used or construed as a commitment by Desjardins Group. While the information provided has been determined on the basis of data obtained from sources that are deemed to be reliable, Desjardins Group in no way warrants that the information is accurate or complete. The document is provided solely for information purposes and does not constitute an offer or solicitation for purchase or sale. Desjardins Group takes no responsibility for the consequences of any decision whatsoever made on the basis of the data contained herein and does not hereby undertake to provide any advice, notably in the area of investment services. The data on prices or margins are provided for information purposes and may be modified at any time, based on such factors as market conditions. The past performances and projections expressed herein are no guarantee of future performance. The opinions and forecasts contained herein are, unless otherwise indicated, those of the document’s authors and do not represent the opinions of any other person or the official position of Desjardins Group. Copyright © 2018, Desjardins Group. All rights reserved. CONTENTS Editorial ............................................................. 1 Energy ............................................................... 2 Base Metals ....................................................... 4 Precious Metals ................................................. 6 Other Commodities ........................................... 7 Tables ................................................................ 8 Except for energy, the commodity market has been looking fairly stable since our last publication in August (graph 1). Oil prices have shot up, as the market expects supply to tighten after U.S. sanctions on Iran come into effect in November. Other factors, such as the major oil producers’ limited spare capacity and the problems in Venezuela, fuelled this worry. The price of natural gas in the United States also started to pick up after spending several months below US$3.00/MMBTU (Million British Thermal Units). Industrial metals recovered slightly from their recent tumble, but remain much weaker than in the spring. Trade tensions between the United States and China as well as lower-than-expected Chinese demand continue to weigh on prices. The price of precious metals has sat virtually idle these past two months. The volatility that recently hit financial markets also had an impact on commodities. The price of oil fell after sharp increases, whereas gold prices regained momentum after a disappointing period. These effects should, however, be temporary. With a sustained favourable outlook for the global economy in 2019 (graph 2), monetary policy tightening could continue worldwide. Economic activity should also remain robust, which might help industrial metal prices. François Dupuis, Vice-President and Chief Economist Carine Bergevin-Chammah, Economist Energy Prices Steal the Show ECONOMIC STUDIES | OCTOBER 17, 2018 GRAPH 1 The spike in energy prices is due mainly to uncertainty surrounding oil supply Sources: Datastream and Desjardins, Economic Studies Bloomberg Commodity Index and its components Jan. 2018 = 100 80 90 100 110 120 130 JAN. FEB. MAR. APR. MAY. JUN. JUL. AUG. SEP. OCT. Index Energy Industrial metals Precious metals Cereals 2018 GRAPH 2 The growth outlook remains strong *Desjardins forecasts Sources: Desjardins, Economic Studies Real GDP growth* % annual change 0 1 2 3 4 5 6 7 8 Canada United States European Union China India World 2016 2017 2018* 2019* #1 BEST OVERALL FORECASTER - CANADA

Transcript of Energy Prices Steal the Show FORECASTER - CANADA #1 BEST ... · The limited means of transporting...

COMMODITY TRENDS

François Dupuis, Vice-President and Chief Economist • Carine Bergevin-Chammah, Economist • Mathieu D’Anjou, Senior Economist

Desjardins, Economic Studies: 514-281-2336 or 1 866-866-7000, ext. 5552336 • [email protected] • desjardins.com/economics

NOTE TO READERS: The letters k, M and B are used in texts and tables to refer to thousands, millions and billions respectively.IMPORTANT: This document is based on public information and may under no circumstances be used or construed as a commitment by Desjardins Group. While the information provided has been determined on the basis of data obtained from sources that are deemed to be reliable, Desjardins Group in no way warrants that the information is accurate or complete. The document is provided solely for information purposes and does not constitute an offer or solicitation for purchase or sale. Desjardins Group takes no responsibility for the consequences of any decision whatsoever made on the basis of the data contained herein and does not hereby undertake to provide any advice, notably in the area of investment services. The data on prices or margins are provided for information purposes and may be modified at any time, based on such factors as market conditions. The past performances and projections expressed herein are no guarantee of future performance. The opinions and forecasts contained herein are, unless otherwise indicated, those of the document’s authors and do not represent the opinions of any other person or the official position of Desjardins Group. Copyright © 2018, Desjardins Group. All rights reserved.

CONTENTSEditorial ............................................................. 1Energy ............................................................... 2

Base Metals ....................................................... 4Precious Metals ................................................. 6

Other Commodities ........................................... 7Tables ................................................................ 8

Except for energy, the commodity market has been looking fairly stable since our last publication in August (graph 1). Oil prices have shot up, as the market expects supply to tighten after U.S. sanctions on Iran come into effect in November. Other factors, such as the major oil producers’ limited spare capacity and the problems in Venezuela, fuelled this worry. The price of natural gas in the United States also started to pick up after spending several months below US$3.00/MMBTU (Million British Thermal Units). Industrial metals recovered slightly from their recent tumble, but remain much weaker than in the spring. Trade tensions between the United States and China as well as lower-than-expected Chinese demand continue to weigh on prices. The price of precious metals has sat virtually idle these past two months.

The volatility that recently hit financial markets also had an impact on commodities. The price of oil fell after sharp increases, whereas gold prices regained momentum after a disappointing period. These effects should, however, be temporary. With a sustained favourable outlook for the global economy in 2019 (graph 2), monetary policy tightening could continue worldwide. Economic activity should also remain robust, which might help industrial metal prices.

François Dupuis, Vice-President and Chief Economist

Carine Bergevin-Chammah, Economist

Energy Prices Steal the Show

ECONOMIC STUDIES | OCTOBER 17, 2018

GRAPH 1The spike in energy prices is due mainly to uncertainty surrounding oil supply

Sources: Datastream and Desjardins, Economic Studies

Bloomberg Commodity Index and its components

Jan. 2018 = 100

80

90

100

110

120

130

JAN. FEB. MAR. APR. MAY. JUN. JUL. AUG. SEP. OCT.

Index Energy Industrial metals Precious metals Cereals

2018

GRAPH 2The growth outlook remains strong

*Desjardins forecastsSources: Desjardins, Economic Studies

Real GDP growth*

% annual change

012345678

Canada United States EuropeanUnion

China India World

2016 2017 2018* 2019*

#1 BEST OVERALLFORECASTER - CANADA

ECONOMIC STUDIES

2OCTOBER 2018 | COMMODITY TRENDS

OIL

The second round of U.S. sanctions on Iran, slated to take effect on November 4, are aimed mainly at the energy sector, which created uncertainty as to the future availability of oil supply on the market. The U.S. administration expects the international community to eventually stop all imports of oil from Iran. However, Iran is a major exporter, with an average 2.1 million barrels per day (mbd) exported in 2017. Some countries have already begun scaling back their imports (graph 3), weakening Iranian oil production. Although India has already reduced its imports of Iranian oil, it nonetheless plans to import approximately 9 million barrels in November, according to Reuters. The ongoing crisis in Venezuela since 2016 is only adding pressure on the global oil supply, as the country produces roughly 1 mbd less than before the downturn. OPEC and Russia have, however, offset these losses by increasing their production by 0.7 mbd and 0.2 mbd, respectively, since the sanctions were announced in May. Saudi Arabia, the largest OPEC producer, also stated that it would be willing to bump up its production even more, bringing it from 10.5 mbd in September to 10.7 mbd in October. The significant growth in production since 2017 in Canada and the United States, among others, also kept the market fairly balanced, albeit with a slight deficit. Output in the United States continues to break records and is expected to

increase further in 2019 (graph 4), which would partly offset the effects of sanctions on Iran.

However, the uncertainty surrounding the availability of oil on the market after November and the possible exemptions for importing countries seems to have gotten the upper hand on the market. The price per barrel of WTI and Brent oil reached their peak recently since November 2014 (graph 5 on page 3). Prices came back down slightly, but remain relatively elevated. The widening gap between WTI and Brent prices also reflects this uncertainty, as the price of Brent tends to represent the price of European and Middle Eastern oil.

There is, however, a divergence in price trends in Canada, which caused the spread between the barrel price of WTI and WCS (Western Canadian Select) to hit a record. Canada is struggling to benefit from higher oil prices due to persistent bottlenecks in transport. Pipelines have reached their capacity, and rail transport is increasingly used. This mode of transportation is less effective and more expensive, but its capacity can be increased more quickly. The limited means of transporting oil from Western Canada are forcing producers to settle for lower prices.

EnergyThreats to Oil Supply Inflate Prices

FORECASTSThe recent rise in oil prices due to supply pressures have led us to revise slightly upward our forecasts for the price of a barrel of WTI (West Texas Intermediate) oil in the months to come. We are now expecting an average of US$68 a barrel in 2018 and US$72 in 2019. The sanctions on Iran, the growing U.S. output, the decisions of the Organization of the Petroleum Exporting Countries (OPEC) and the situation in Venezuela will have a significant impact on short‑term movements in oil prices. For natural gas, the low inventories could make its price sensitive to unseasonable temperatures.

GRAPH 3Countries are already preparing for U.S. sanctions on Iran’s energy sector to come into effect

Sources: Bloomberg and Desjardins, Economic Studies

Iranian oil exports

In millions of barrels/day

0.0

0.5

1.0

1.5

2.0

2.5

3.0

JAN. MAR. MAY. JUL. SEP. NOV. JAN. MAR. MAY. JUL. SEP.

Mill

iers

China India Europe Japan South Korea Others20182017

GRAPH 4U.S. production is increasing more quickly than expected

EIA: Energy Information Administration; STEO: Short-Term Energy OutlookSources: EIA and Desjardins, Economic Studies

EIA forecast for average oil production in the United States

In millions of barrels/day

9.5

10.0

10.5

11.0

11.5

12.0

January 2018 STEO April 2018 STEO October 2018 STEO

2018 forecast 2019 forecast

3OCTOBER 2018 | COMMODITY TRENDS

ECONOMIC STUDIES

Our forecasts for the price per barrel of WTI oil are currently US$68 on average for 2018 and US$72 for 2019. Despite the possibility that the trade disputes between China and the United States might reduce economic activity and therefore oil demand, we consider that risks to oil prices are more on the upside. We will continue to keep a close watch on the effect of the sanctions and on developments in the oil production of major producers. The tensions that emerged recently between Saudi Arabia and the United States could potentially bring more volatility to the market.

GASOLINE

Gas prices in the United States did not follow in the footsteps of oil prices, staying virtually unchanged since July at around US$2.90 a gallon (graph 6). Retailers and refineries seem hesitant to pass on the rise in oil prices to consumers. This means that consumers are not yet completely affected by the most recent increase, but this may be temporary.

NATURAL GAS

The price of natural gas has been trending upward since July and is currently sitting well above US$3.00/MMBTU, with inventories now at their lowest recorded level for the same period since 2005 (graph 7). Despite the spike in production, consumption has also risen sharply over the past year (graph 8). In addition, the United States has become a net exporter of natural gas since 2017. This explains the low inventories and seems to be behind the recent pressure on U.S. prices with less than a month left in the storage injection season. Low inventories could make the price more volatile and dependent on temperature.

GRAPH 8Natural gas production and consumption are posting a clear upward trend

Sources: Energy Information Administration and Desjardins, Economic Studies

Seasonally adjusted data – 12-month moving average

In billions of cubic feet

1,500

1,700

1,900

2,100

2,300

2,500

2,700

2002 2004 2006 2008 2010 2012 2014 2016 2018

Mill

iers

Consumption Marketed production

GRAPH 7The price of natural gas is beginning to respond to low inventories

MMBTU: Million British Thermal UnitsSources: Datastream and Desjardins, Economic Studies

Natural gas in the United States

In billions of cubic feet

0

1

2

3

4

5

6

-1,000

-500

0

500

1,000

2013 2014 2015 2016 2017 2018

Five-year average spread in stocks (left) Price (right)

US$/MMBTU

GRAPH 6Gas prices held steady despite a spike in oil prices

* Average WTI (West Texas Intermediate) and Brent prices.Sources: Datastream and Desjardins, Economic Studies

US$/barrel

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

25

35

45

55

65

75

85

2015 2016 2017 2018

Crude oil prices* (left)Gas prices in the United States (right)

US$/gallon

GRAPH 5As oil prices soar around the world, prices in Canada move in the opposite direction

WTI: West Texas Intermediate; WCS: Western Canadian SelectSources: Datastream, Bloomberg and Desjardins, Economic Studies

Oil prices

US$/barrel

0

20

40

60

80

100

120

2013 2014 2015 2016 2017 2018

WTI Brent WCS

ECONOMIC STUDIES

4OCTOBER 2018 | COMMODITY TRENDS

The LME index has hovered between 2,800 and 3,000 since August. It is currently up slightly from September at 3,000 (graph 9), but is still in negative territory compared with the start of 2018. The global economy remained strong, just like demand for industrial metals, as evidenced by the decline in inventories listed by the LME. We predict economic growth of 3.8% in 2018 and 2019, which is encouraging for the industrial metals market. Slightly weaker Chinese demand for metals has softened prices, however. In addition, the threat of protectionism sowed uncertainty on the markets and appears to be affecting the price of industrial metals. The tariffs and sanctions introduced this year by the Trump administration had a significant impact on markets. The Global Economic Policy Uncertainty Index developed by three economists has also seen an upward trend this year. This trend is even more pronounced if we consider the uncertainty directly related to U.S. trade policies (graph 10).

ALUMINIUM

The price of aluminum regained some ground lost since the easing of U.S. sanctions on Rusal, a Russian aluminum and alumina producer. A formal decision on Rusal’s fate is still pending, as its head negotiates with the United States. Aluminum is currently priced at about US$2,025 per tonne (graph 11 on page 5). The ongoing decline in inventories listed by the LME and

the marked increase in the price of alumina—the main ingredient in the production of aluminum—likely drove up aluminum prices. Alumina has had some difficulties lately due to disruptions in Brazilian production and sanctions imposed on Russia, among other factors. Its price rose from US$390 per tonne in January 2018 to US$520 recently. Considering that it takes two tonnes of alumina to produce one tonne of aluminum, the spike in the price of alumina is having a significant effect on aluminum production costs. The price of aluminum could therefore remain high, especially since global economic growth is expected to stay strong at least until late 2019. The final decision regarding sanctions on Rusal could also influence the price.

COPPER

The price of copper began to recover from its August and September slumps. It was recently around US$6,200 per tonne, 14% below its price from early 2018 (graph 12 on page 5). Problems in some emerging countries, lower Chinese demand for the metal, China‑U.S. trade conflicts and the mine union agreements in Chile all played a part in lowering copper prices. Global demand should, however, continue to be strong in 2018 and 2019, and the inventories listed by the LME are at their lowest since June 2016. These factors could raise the price of copper.

Base MetalsLittle Change Since Our Last Publication

FORECASTSThe prices of the main base metals we are monitoring inched up recently, but are not straying far from their August levels, despite ever-shrinking inventories. Some slowdown in Chinese demand and trade tensions have weighed on prices. The global economy is still robust, however, and should continue to be in 2019 as well. We therefore expect base metal prices to rise, which could bring the LME (London Metal Exchange) index to an average of 3,190 in 2018.

GRAPH 10Greater uncertainty abounds in 2018

Sources: policyuncertainty.com and Desjardins, Economic Studies

Index

0

200

400

600

800

1,000

2013 2014 2015 2016 2017 2018Global economic policy uncertaintyU.S. trade policy uncertainty

Indexed to 100 for the average between 1997 and 2016

GRAPH 9Metals prices have not recovered from their recent fall

LMEX: London Metal Exchange IndexSources: Datastream and Desjardins, Economic Studies

Index

5001,5002,5003,5004,5005,5006,5007,5008,500

5001,0001,5002,0002,5003,0003,5004,0004,5005,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

LMEX (left) Inventories of the six main metals (right)

In thousands of tonnes

5OCTOBER 2018 | COMMODITY TRENDS

ECONOMIC STUDIES

NICKEL

The price of nickel weakened since August and is now around 1 % lower than it was in January, at approximately US$12,500 per tonne (graph 13). However, the inventories listed by the LME are declining, and demand for this metal is expected to be strong in the coming years given its role in electric vehicle batteries, among other things. The downward trend in the price since June could therefore stop and even reverse.

ZINC

The price of zinc erased some of its losses and is now sitting at around US$2,650 per tonne (graph 14). Inventories have shrunk considerably over the past few years to their 2008 level, which is what has kept the price high. The International Lead and Zinc Study Group expects the zinc market to be in deficit in 2018 and 2019. The price of metal could therefore stay high, but it would be surprising for it to return to its 2018 peak on a sustained basis.

GRAPH 14Zinc prices and inventories

Sources: Datastream and Desjardins, Economic Studies

US$/tonne

100

300

500

700

900

1,100

1,300

1,2501,5001,7502,0002,2502,5002,7503,0003,2503,5003,750

2013 2014 2015 2016 2017 2018

Prices (left) Inventories (right)

In thousands of tonnes

GRAPH 13Nickel prices and inventories

Sources: Datastream and Desjardins, Economic Studies

US$/tonne

100

200

300

400

500

7,000

10,000

13,000

16,000

19,000

22,000

2013 2014 2015 2016 2017 2018

Prices (left) Inventories (right)

In thousands of tonnes

GRAPH 12Copper prices and inventories

Sources: Datastream and Desjardins, Economic Studies

US$/tonne

100

200

300

400

500

600

700

4,000

5,000

6,000

7,000

8,000

9,000

2013 2014 2015 2016 2017 2018

Prices (left) Inventories (right)

In thousands of tonnes

GRAPH 11Aluminum prices and inventories

Sources: Datastream and Desjardins, Economic Studies

US$/tonne

800

1,400

2,000

2,600

3,200

3,800

4,400

5,000

5,600

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2013 2014 2015 2016 2017 2018

Prices (left) Inventories (right)

In thousands of tonnes

ECONOMIC STUDIES

6OCTOBER 2018 | COMMODITY TRENDS

GOLD & SILVER

Another surge in the U.S. dollar in mid-August drove gold prices down below US$1,180 an ounce (graph 15). The U.S. dollar then fell slightly, but the strong emerging uptrend in bond yields also hurt the price of the yellow metal. Data on exchange-traded funds related to gold clearly show the reversal in investor sentiment at the end of spring (graph 16). While there is every indication that the Federal Reserve will continue its monetary tightening, the conditions for a lasting rebound in investor demand for gold in the coming quarters are not there. The recent stock market nosedive nonetheless helped the price

of the yellow metal rebound to around US$1,230 an ounce. Continued volatility on the markets could support some demand for gold, thus preventing a further drop in its price. The decline in silver prices since the beginning of 2018 is now close to 13%, compared to just under 6% for gold.

PLATINUM & PALLADIUM

Gold’s struggles continued to hurt other precious metals during the summer. The price of platinum fell to a new cyclical low of US$772 an ounce in early September before bouncing back recently to around US$840 an ounce (graph 17). For the time being, the drop in the South African currency seems to be limiting the negative effects that low platinum price, in U.S. dollars, might have on mining production. After retreating until mid-August, the price of palladium jumped more than 25% to a level slightly above the one at which it had started the year. The future seems rather uncertain for the price of palladium, as some observers see it exceeding the price of gold, while others doubt that it can stay above the price of platinum for long.

Precious MetalsThe Surge in Bond Yields is Not Helping the Situation

FORECASTSThe fairly strong U.S. dollar and the uptrend in bond yields do not suggest a lasting rise in gold prices in the coming quarters. We therefore predict gold prices to hold at around US$1,200 an ounce.

GRAPH 17Platinum and palladium prices

Sources: Datastream and Desjardins, Economic Studies

US$/ounce

400

500

600

700

800

900

1,000

1,100

1,200

700800900

1,0001,1001,2001,3001,4001,5001,6001,7001,800

2013 2014 2015 2016 2017 2018

Platinum (left) Palladium (right)

US$/ounce

GRAPH 16Investors have reduced their gold holdings in recent months

Sources: World Gold Council and Desjardins, Economic Studies

Gold held in exchange-traded funds

Monthly change in tonnes

-60

-40

-20

0

20

40

60

80

JAN. FEB. MAR. APR. MAY. JUN. JUL. AUG. SEP.2018

GRAPH 15Gold prices continue to be heavily influenced by movements in the U.S. dollar

Sources: Datastream and Desjardins, Economic Studies

Index

1,0001,0501,1001,1501,2001,2501,3001,3501,400

889092949698

100102104

2016 2017 2018

Trade-weighted U.S. dollar index (left) Gold prices (right)

US$/ounce

7OCTOBER 2018 | COMMODITY TRENDS

ECONOMIC STUDIES

FOREST PRODUCTS

This year has been particularly volatile for softwood lumber prices. After soaring to a peak of US$582/mbf (thousand board feet) at the end of spring, the benchmark lumber price plummeted and has even recently fallen below US$400/mbf (graph 18). The past few months have been confirmation that the record lumber prices were not sustainable and that they were mostly a reflection of rail congestion, which was causing shortages in some parts of the United States. Price moderation was therefore inevitable. The tumble in prices seems to have been magnified by some doubts as to the strength of demand for lumber, with disappointing U.S. residential market statistics in recent months. Rising mortgage rates are fuelling real estate sector worries (graph 19). The United States-Mexico-Canada Agreement (USMCA) might have also accentuated the decline in prices by rekindling hopes that tariffs on Canadian lumber exports would be lifted, but nothing has been settled there yet. While the economic context should remain favourable in North America, the drop in softwood lumber prices seems a bit exaggerated.

AGRICULTURAL COMMODITIES

Grain prices declined considerably in the last few weeks of summer, before climbing back slightly since the start of fall (graph 20). The price of wheat is still up by more than 15% compared with last year, as drought conditions in Europe pushed back production and lowered global inventories of this grain. The situation is different for corn and soybeans as favourable conditions in the United States and South America boosted crops. Despite that, global corn inventories continue to shrink as demand keeps growing rapidly. The U.S. administration’s recent decision to favor ethanol use suggests that demand for corn could remain robust. Global demand for soybeans also expanded, but not enough to prevent an increase in global inventories. The trade conflict between the United States and China continues to complicate things for U.S. farmers and is resulting in much lower soybean prices than a year ago. Now that the harvest season is drawing to a close in the northern hemisphere, grain prices should be less volatile.

Other CommoditiesPrices Continued to Decline

GRAPH 20Cereal prices

Sources: Datastream and Desjardins, Economic Studies

US$/bushel US$/bushel

7891011121314151617

2

3

4

5

6

7

8

9

2013 2014 2015 2016 2017 2018

Wheat (left) Corn (left) Soybeans (right)

GRAPH 18Forest product prices

tbf: thousand board feetSources: Datastream and Desjardins, Economic Studies

US$/tbf

8509009501,0001,0501,1001,1501,2001,2501,3001,3501,400

250

300

350

400

450

500

550

600

2013 2014 2015 2016 2017 2018

Softwood lumber (left) Pulp (right)

US$/tonne

GRAPH 19Are rising mortgage rates already curbing real estate activity in the United States?

Sources: Datastream and Desjardins, Economic Studies

U.S. mortgage rates

In %

2.5

3.0

3.5

4.0

4.5

5.0

5.5

2016 2017 2018

15 years 30 years

ECONOMIC STUDIES

8OCTOBER 2018 | COMMODITY TRENDS

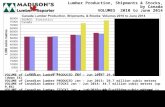

SPOT PRICE

Oct. 17 -1 month -3 months -6 months -1 year Higher Average Lower

IndexReuter-CRB (CCI) 420.9 5.6 3.7 -1.8 2.0 441.0 419.6 394.0Reuters/Jefferies CRB 199.7 5.3 4.5 0.2 8.4 206.4 194.5 183.4Bloomberg Commodity Index 87.0 5.9 5.1 -2.2 1.8 91.6 86.9 82.1Bank of Canada 443.0 -2.5 -12.4 -6.8 5.6 514.4 461.6 419.3

EnergyBrent oil (US$/barrel) 80.7 2.9 11.8 12.6 40.0 85.8 71.0 57.6WTI oil (US$/barrel) 71.9 4.5 5.7 8.2 38.7 77.4 65.0 51.3Gasoline (US$/gallon) 2.88 1.3 0.5 4.8 15.7 2.96 2.71 2.45Natural gas (US$/MMBTU) 3.24 15.1 18.2 18.3 9.4 3.63 2.88 2.55

Base metalsLMEX 2,978 4.0 0.4 -11.9 -9.2 3,500 3,214 2,820Aluminium (US$/tonne) 2,025 1.3 -2.0 -15.9 -4.3 2,541 2,142 1,960Copper (US$/tonne) 6,202 4.8 1.4 -9.2 -11.3 7,331 6,678 5,759Nickel (US$/tonne) 12,517 2.9 -6.5 -11.7 7.0 15,688 13,212 10,749Zinc (US$/tonne) 2,639 14.7 4.1 -15.9 -15.2 3,606 3,045 2,284

Precious metalsGold (US$/ounce) 1,228 2.0 0.0 -8.6 -4.3 1,359 1,278 1,179Silver (US$/ounce) 14.8 4.1 -6.4 -11.2 -13.8 17.5 16.2 14.1Platinum (US$/ounce) 842 5.1 2.1 -9.0 -9.3 1,020 900 772Palladium (US$/ounce) 1,084 10.4 18.5 8.2 10.1 1,129 995 849

Other commoditiesLumber (US$/tbf) 373 -15.4 -29.9 -24.5 -15.2 582 480 373Pulp (US$/tonne) 1,380 0.0 4.2 11.3 22.1 1,380 1,265 1,130Wheat (US$/bushel) 5.03 7.9 -1.9 7.5 19.2 5.73 4.79 4.13Corn (US$/bushel) 3.35 11.7 6.0 -3.2 6.3 3.78 3.33 2.91Soybean (US$/bushel) 8.16 8.2 1.1 -19.1 -13.5 10.33 9.12 7.45

CRB: Commodity Research Bureau; CCI: Continuous Commodity Index; WTI: West Texas Intermediate; MMBTU: Million British Thermal Units;LMEX: London Metal Exchange Index; tbf: thousand of board feetNOTE: Currency table base on previous day closure.

TABLE 1Commodities

VARIATION (%) LAST 52 WEEKS

2016 2017 2018f 2019f

Target: 68 Target: 72(range: 67 to 70) (range: 65 to 85)

Target: 2.95 Target: 3.15(range: 2.90 to 3.00) (range: 2.65 to 3.95)

Target: 1,265 Target: 1,210(range: 1,260 to 1,280) (range: 1,125 to 1,325)

Target: 3,190 Target: 3,300(range: 3,150 to 3,250) (range: 2,900 to 3,900)

TABLE 2Commodities prices: History and forecasts

ANNUAL AVERAGE

WTI oil (US$/barrel) 43 51

LMEX index—base metals 2,375 2,969

f: forecasts; WTI : West Texas Intermediate; MMBTU : Million British Thermal Units; LMEX : London Metal Exchange IndexSources: Datastream and Desjardins, Economic Studies

Natural gas Henry Hub(US$/MMBTU)

2.55 3.02

Gold (US$/ounce) 1,248 1,259