Energy efficiency optimization economic value driver?

22

THE CARBON OPPORTUNITY FIRM Energy efficiency optimization – economic value driver? Conference: “Kyoto Protocol as a financial tool for implementing energy efficiency projects” Yekaterinburg, 6 - 7 April 2011 April 6, 2011

Transcript of Energy efficiency optimization economic value driver?

THE CARBON OPPORTUNITY FIRM

Energy efficiency optimization – economic value driver? Conference: “Kyoto Protocol as a financial tool for implementing energy efficiency projects”

Yekaterinburg, 6 - 7 April 2011

April 6, 2011

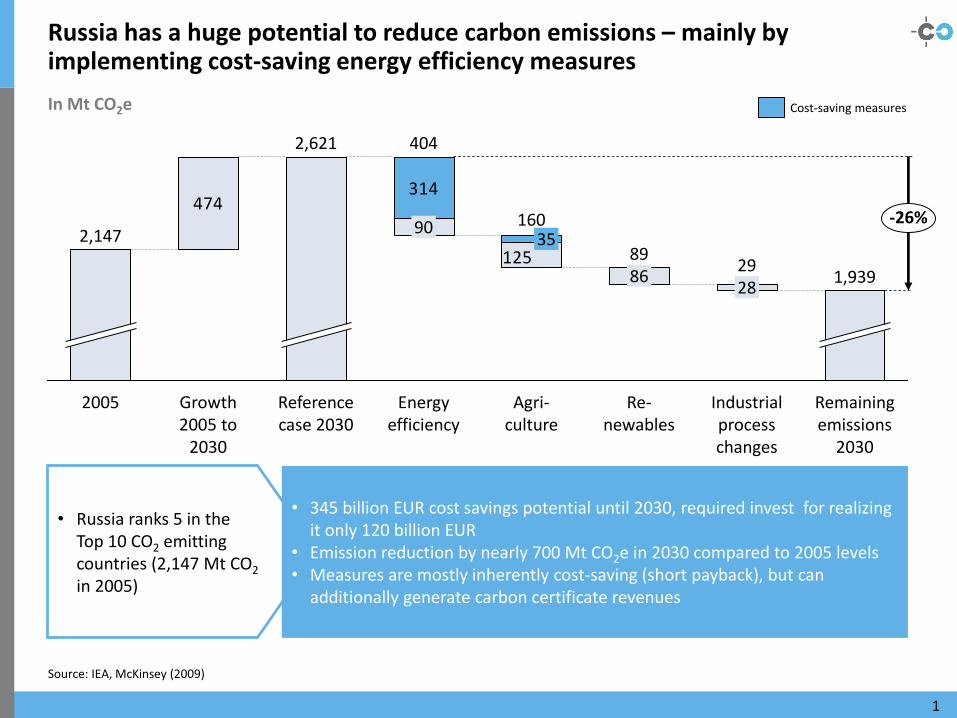

Russia has a huge potential to reduce carbon emissions – mainly by implementing cost-saving energy efficiency measures

In Mt CO2e

Source: IEA, McKinsey (2009)

1

125

474314

2,621

Growth 2005 to

2030

2005

2,147

Remaining emissions

2030

Industrial process changes

29 28

Re- newables

89 86

Agri- culture

160

Energy efficiency

404

90

Reference case 2030

35

1,939

-26%

• Russia ranks 5 in the Top 10 CO2 emitting countries (2,147 Mt CO2 in 2005)

• 345 billion EUR cost savings potential until 2030, required invest for realizing it only 120 billion EUR

• Emission reduction by nearly 700 Mt CO2e in 2030 compared to 2005 levels • Measures are mostly inherently cost-saving (short payback), but can

additionally generate carbon certificate revenues

Cost-saving measures

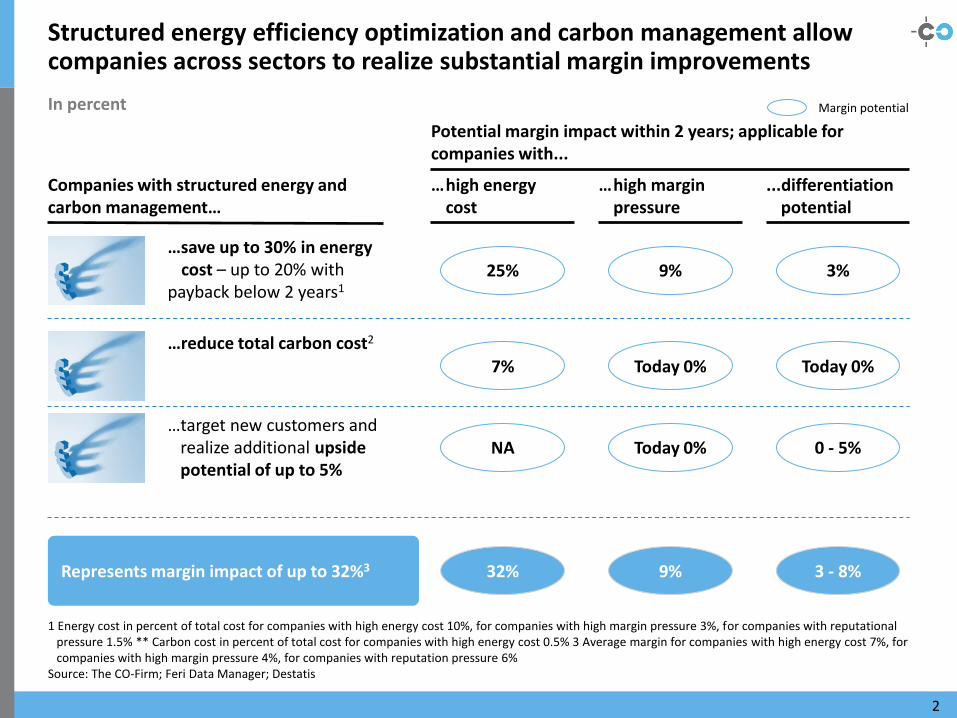

Structured energy efficiency optimization and carbon management allow companies across sectors to realize substantial margin improvements

1 Energy cost in percent of total cost for companies with high energy cost 10%, for companies with high margin pressure 3%, for companies with reputational pressure 1.5% ** Carbon cost in percent of total cost for companies with high energy cost 0.5% 3 Average margin for companies with high energy cost 7%, for companies with high margin pressure 4%, for companies with reputation pressure 6%

Source: The CO-Firm; Feri Data Manager; Destatis

Companies with structured energy and carbon management…

In percent

…save up to 30% in energy cost – up to 20% with payback below 2 years13

…reduce total carbon cost2

…target new customers and realize additional upside potential of up to 5%

Potential margin impact within 2 years; applicable for companies with...

Represents margin impact of up to 32%3

… high energy cost

… high margin pressure

...differentiation potential

25% 9% 3%

7% Today 0% Today 0%

NA Today 0% 0 - 5%

32% 9% 3 - 8%

Margin potential

2

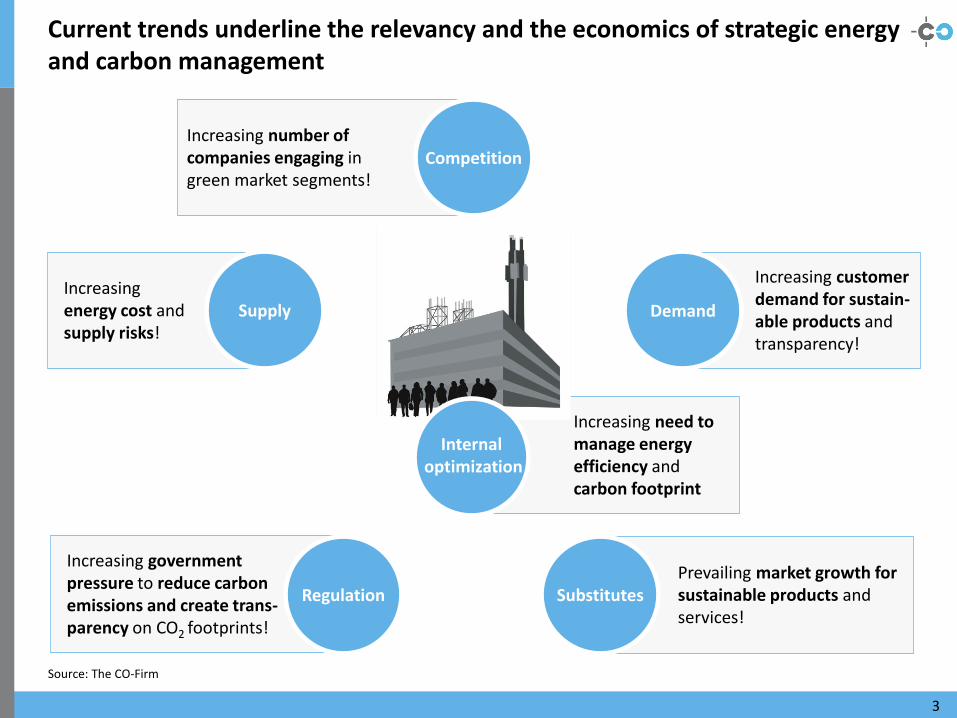

Increasing need to manage energy efficiency and carbon footprint

Current trends underline the relevancy and the economics of strategic energy and carbon management

Source: The CO-Firm

3

Demand

Internal optimization

Supply

Competition

Regulation

Increasing government pressure to reduce carbon emissions and create trans-parency on CO2 footprints!

Increasing energy cost and supply risks!

Increasing number of companies engaging in green market segments!

Increasing customer demand for sustain-able products and transparency!

Substitutes Prevailing market growth for sustainable products and services!

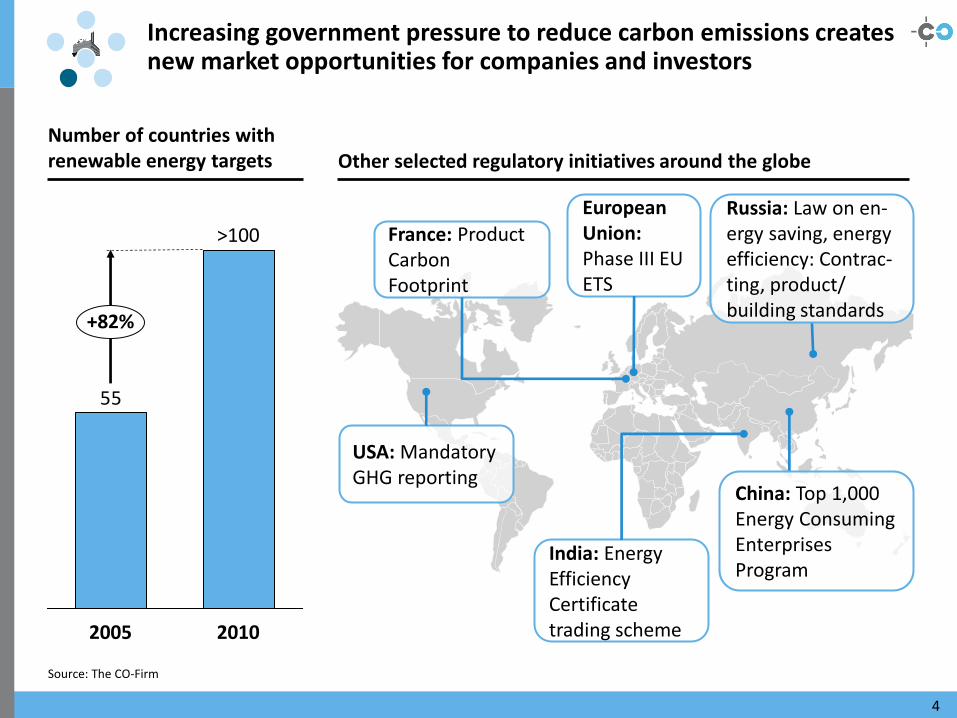

Increasing government pressure to reduce carbon emissions creates new market opportunities for companies and investors

Source: The CO-Firm

4

55

2005 2010

+82%

>100

Number of countries with renewable energy targets Other selected regulatory initiatives around the globe

China: Top 1,000 Energy Consuming Enterprises Program

India: Energy Efficiency Certificate trading scheme

France: Product Carbon Footprint

USA: Mandatory GHG reporting

European Union: Phase III EU ETS

Russia: Law on en-ergy saving, energy efficiency: Contrac-ting, product/ building standards

Increasing energy cost and supply risks create pressure to improve energy efficiency across regions

Source: The CO-Firm; Destatis; IEA World Energy Outlook 2009; EIA; IEA Energy Prices and Statistics 2010

5

0

50

100

150

200

250

300

350

400

450

2000 2002 2004 2006 2008 2010

USA Gas

USA Electricity

Russia Gas

Russia Electricity

Gas and electricity price development in Russia and USA [Index 2001 = 100]

Price Index for Electricity / Gas CAGR

21%

12%

4%

Energy price development In USD/t cement

8,3

8,8

17,1

10,8

11,6

22,4

12,9

15,8

28,7

+68%

Electricity

Coal

EXAMPLE: CEMENT INDUSTRY INDIA

-1%

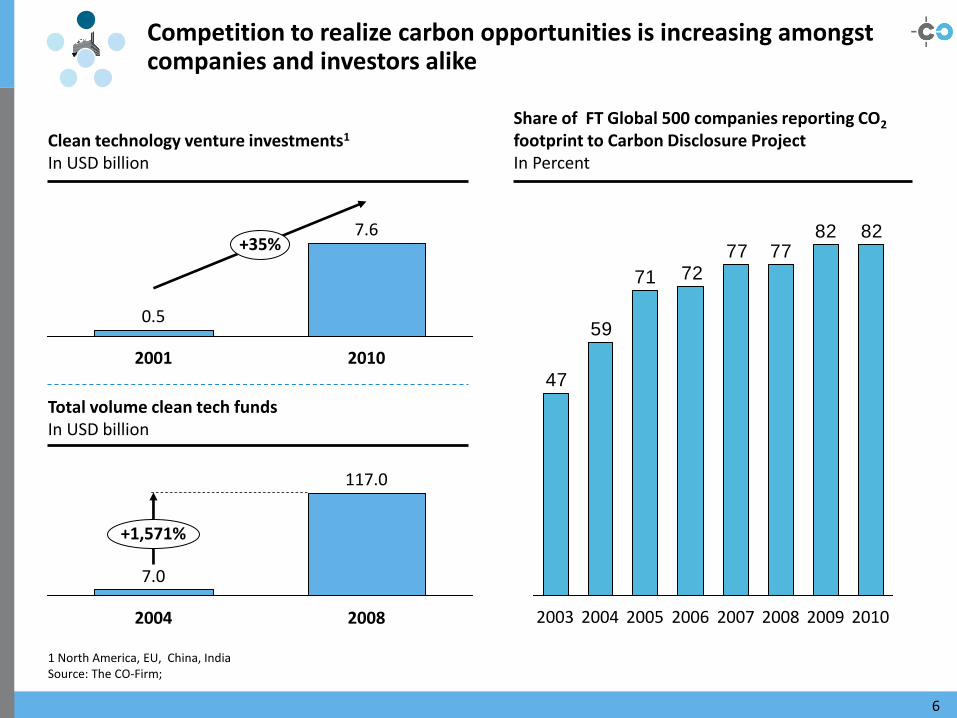

Competition to realize carbon opportunities is increasing amongst companies and investors alike

1 North America, EU, China, India Source: The CO-Firm;

6

7.6 +35%

2001 2010

0.5

Clean technology venture investments1

In USD billion

7.0

2004

117.0

2008

+1,571%

Total volume clean tech funds

In USD billion

Share of FT Global 500 companies reporting CO2

footprint to Carbon Disclosure Project In Percent

82827777

7271

59

47

2010 2007 2008 2009 2006 2003 2004 2005

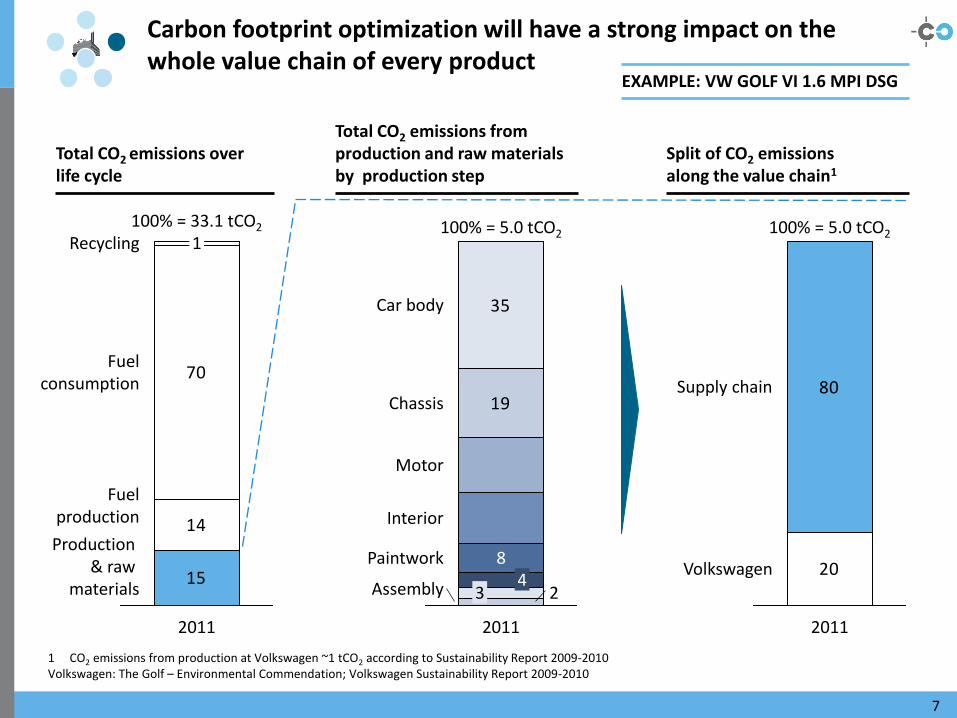

15

14

70

1

2011

100% = 33.1 tCO2

Recycling

Fuel consumption

Fuel production

Production & raw

materials

Carbon footprint optimization will have a strong impact on the whole value chain of every product

1 CO2 emissions from production at Volkswagen ~1 tCO2 according to Sustainability Report 2009-2010 Volkswagen: The Golf – Environmental Commendation; Volkswagen Sustainability Report 2009-2010

7

2

19

35

Assembly

Paintwork

Interior

Motor

Chassis

Car body

2011

100% = 5.0 tCO2

3 4

8

Total CO2 emissions over life cycle

Total CO2 emissions from production and raw materials by production step

Split of CO2 emissions along the value chain1

EXAMPLE: VW GOLF VI 1.6 MPI DSG

20

80Supply chain

Volkswagen

2011

100% = 5.0 tCO2

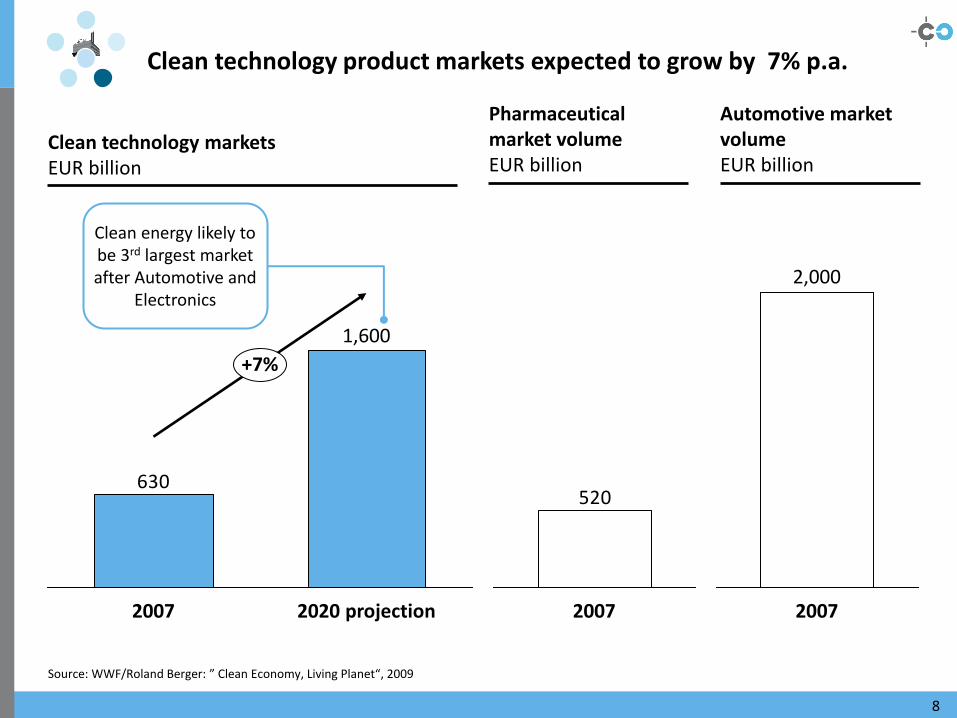

Clean technology product markets expected to grow by 7% p.a.

Source: WWF/Roland Berger: ” Clean Economy, Living Planet“, 2009

8

630

+7%

2020 projection

1,600

2007

Clean technology markets

EUR billion

2,000

2007

Automotive market volume

EUR billion

520

2007

Pharmaceutical market volume

EUR billion

Clean energy likely to be 3rd largest market after Automotive and

Electronics

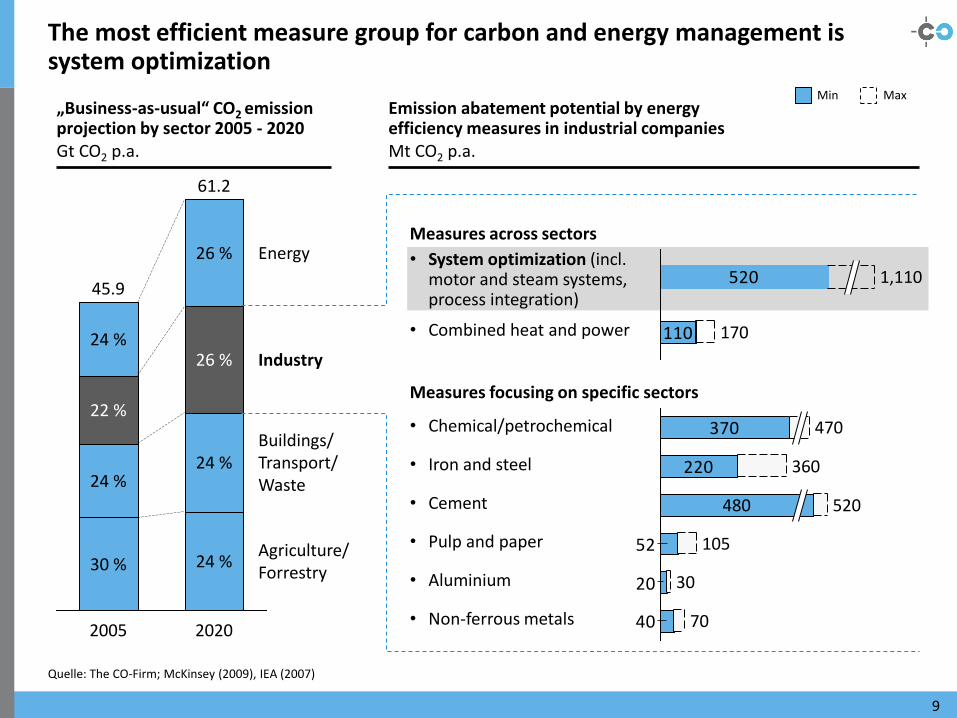

The most efficient measure group for carbon and energy management is system optimization

Quelle: The CO-Firm; McKinsey (2009), IEA (2007)

9

„Business-as-usual“ CO2 emission projection by sector 2005 - 2020 Gt CO2 p.a.

Measures across sectors

• System optimization (incl. motor and steam systems, process integration)

• Combined heat and power

Emission abatement potential by energy efficiency measures in industrial companies Mt CO2 p.a.

110

520 1,110

170

Agriculture/ Forrestry

Buildings/ Transport/ Waste

Industry

Energy

2020

61.2

24 %

24 %

26 %

26 %

2005

45.9

30 %

24 %

22 %

24 %

Min Max

Measures focusing on specific sectors

• Chemical/petrochemical

• Iron and steel

• Cement

• Pulp and paper

• Aluminium

• Non-ferrous metals 40

20

52

220

370

70

30

105

470

520 480

360

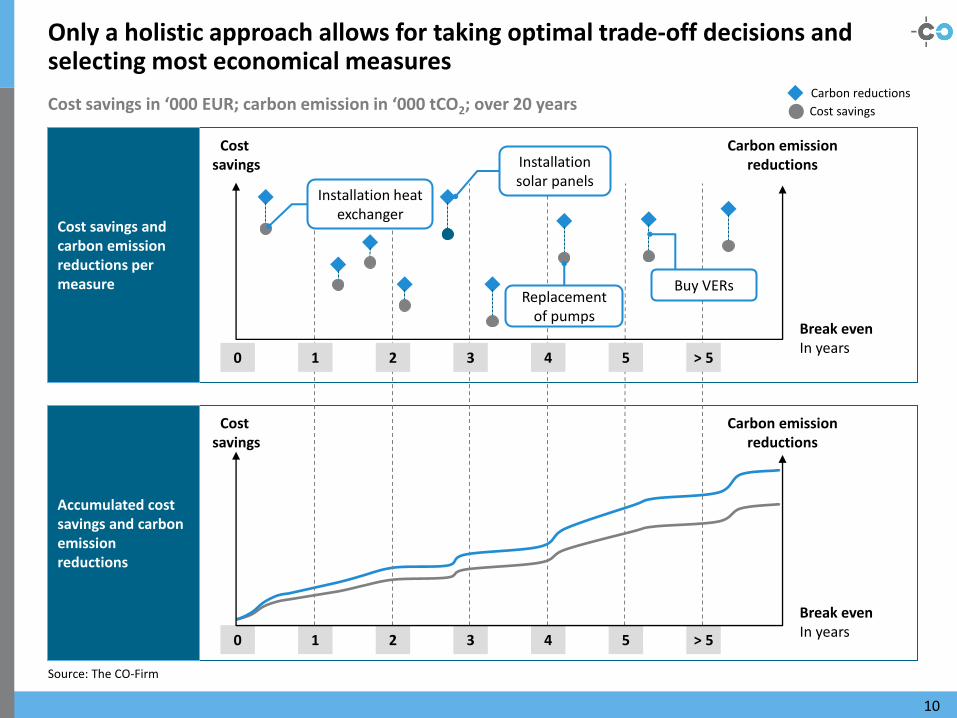

Only a holistic approach allows for taking optimal trade-off decisions and selecting most economical measures

Source: The CO-Firm

Carbon emission reductions

Break even In years

Cost savings

Cost savings in ‘000 EUR; carbon emission in ‘000 tCO2; over 20 years

Break even In years

Carbon reductions

Cost savings

Accumulated cost savings and carbon emission reductions

Cost savings and carbon emission reductions per measure

1 2 3 4 5 0 > 5

1 2 3 4 5 0 > 5

Installation solar panels

Buy VERs Replacement

of pumps

10

Carbon emission reductions

Cost savings

Installation heat exchanger

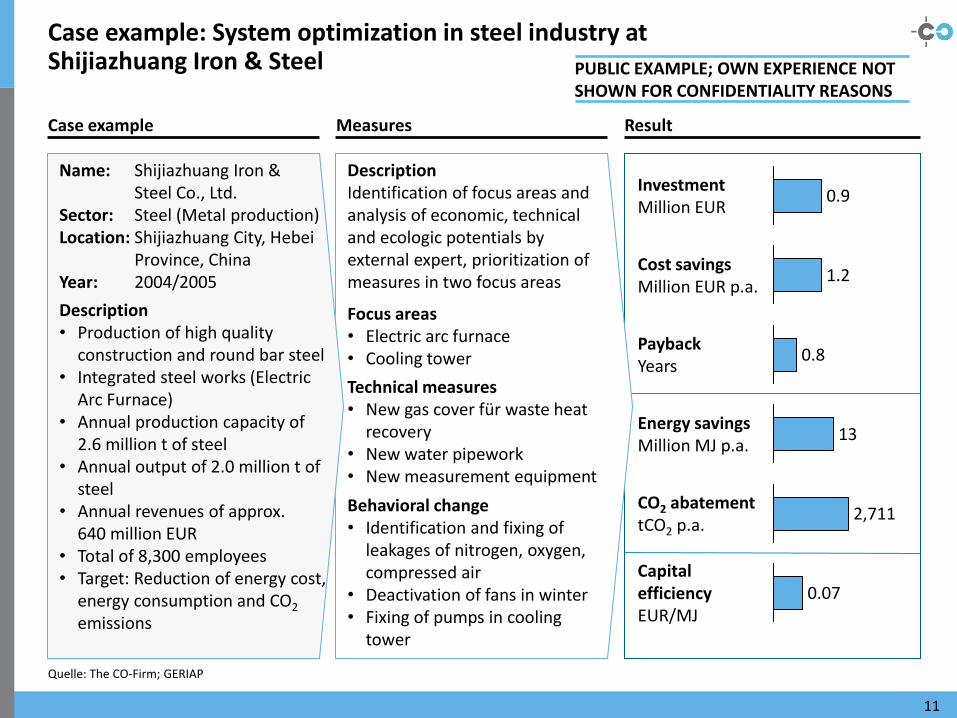

Case example: System optimization in steel industry at Shijiazhuang Iron & Steel

Quelle: The CO-Firm; GERIAP

11

Case example Measures

Name: Shijiazhuang Iron & Steel Co., Ltd.

Sector: Steel (Metal production) Location: Shijiazhuang City, Hebei

Province, China Year: 2004/2005

Description • Production of high quality

construction and round bar steel • Integrated steel works (Electric

Arc Furnace) • Annual production capacity of

2.6 million t of steel • Annual output of 2.0 million t of

steel • Annual revenues of approx.

640 million EUR • Total of 8,300 employees • Target: Reduction of energy cost,

energy consumption and CO2 emissions

Technical measures • New gas cover für waste heat

recovery • New water pipework • New measurement equipment

Behavioral change • Identification and fixing of

leakages of nitrogen, oxygen, compressed air

• Deactivation of fans in winter • Fixing of pumps in cooling

tower

Focus areas • Electric arc furnace • Cooling tower

Description Identification of focus areas and analysis of economic, technical and ecologic potentials by external expert, prioritization of measures in two focus areas

Result

Investment Million EUR

Cost savings Million EUR p.a.

Payback Years

Capital efficiency EUR/MJ

CO2 abatement tCO2 p.a.

Energy savings Million MJ p.a.

0.9

0.8

13

2,711

0.07

1.2

PUBLIC EXAMPLE; OWN EXPERIENCE NOT SHOWN FOR CONFIDENTIALITY REASONS

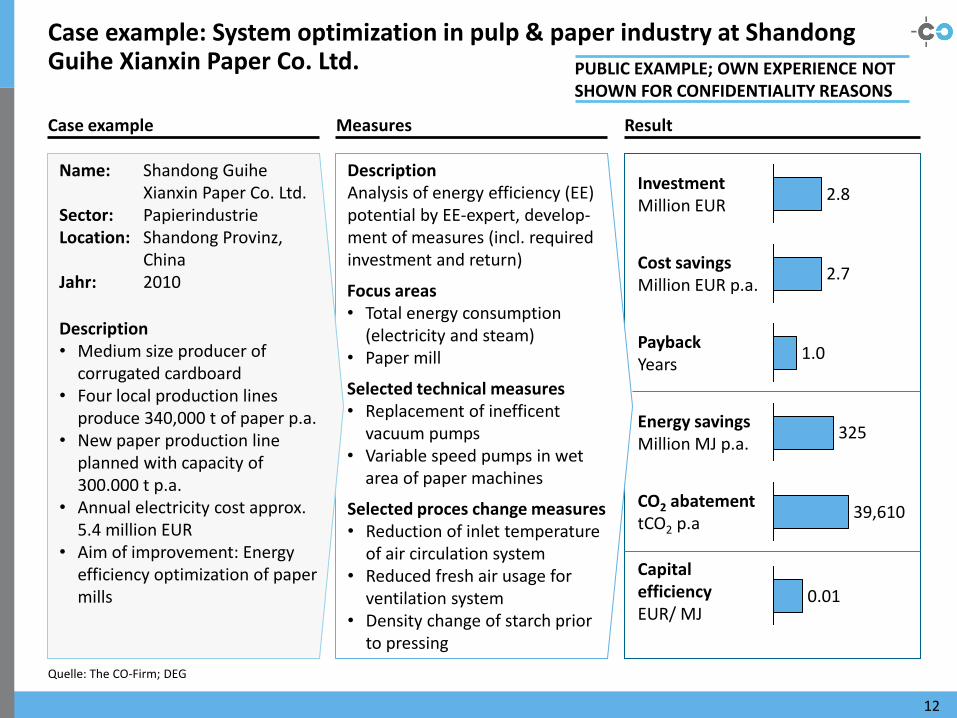

Case example: System optimization in pulp & paper industry at Shandong Guihe Xianxin Paper Co. Ltd.

Quelle: The CO-Firm; DEG

12

Investment Million EUR

Cost savings Million EUR p.a.

Payback Years

Capital efficiency EUR/ MJ

CO2 abatement tCO2 p.a

Energy savings Million MJ p.a.

2.8

1.0

325

39,610

2.7

0.01

Name: Shandong Guihe Xianxin Paper Co. Ltd.

Sector: Papierindustrie Location: Shandong Provinz,

China Jahr: 2010

Description • Medium size producer of

corrugated cardboard • Four local production lines

produce 340,000 t of paper p.a. • New paper production line

planned with capacity of 300.000 t p.a.

• Annual electricity cost approx. 5.4 million EUR

• Aim of improvement: Energy efficiency optimization of paper mills

Selected technical measures • Replacement of inefficent

vacuum pumps • Variable speed pumps in wet

area of paper machines

Selected proces change measures • Reduction of inlet temperature

of air circulation system • Reduced fresh air usage for

ventilation system • Density change of starch prior

to pressing

Focus areas • Total energy consumption

(electricity and steam) • Paper mill

Description Analysis of energy efficiency (EE) potential by EE-expert, develop-ment of measures (incl. required investment and return)

Case example Measures Result

PUBLIC EXAMPLE; OWN EXPERIENCE NOT SHOWN FOR CONFIDENTIALITY REASONS

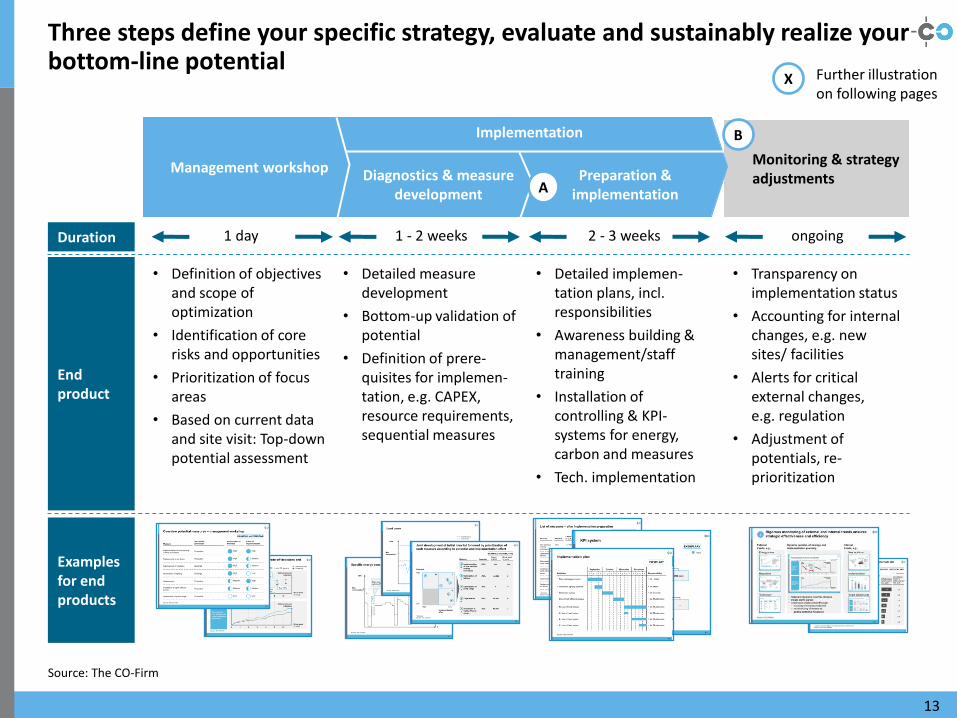

Examples for end products

End product

Duration

Three steps define your specific strategy, evaluate and sustainably realize your bottom-line potential

Source: The CO-Firm

Monitoring & strategy adjustments

1 day

• Definition of objectives and scope of optimization

• Identification of core risks and opportunities

• Prioritization of focus areas

• Based on current data and site visit: Top-down potential assessment

1 - 2 weeks 2 - 3 weeks ongoing

• Detailed measure development

• Bottom-up validation of potential

• Definition of prere-quisites for implemen-tation, e.g. CAPEX, resource requirements, sequential measures

• Detailed implemen-tation plans, incl. responsibilities

• Awareness building & management/staff training

• Installation of controlling & KPI-systems for energy, carbon and measures

• Tech. implementation

• Transparency on implementation status

• Accounting for internal changes, e.g. new sites/ facilities

• Alerts for critical external changes, e.g. regulation

• Adjustment of potentials, re-prioritization

13

Diagnostics & measure development

Preparation & implementation

Implementation

Management workshop

A

B

X Further illustration on following pages

Starting point for continuous

improvement

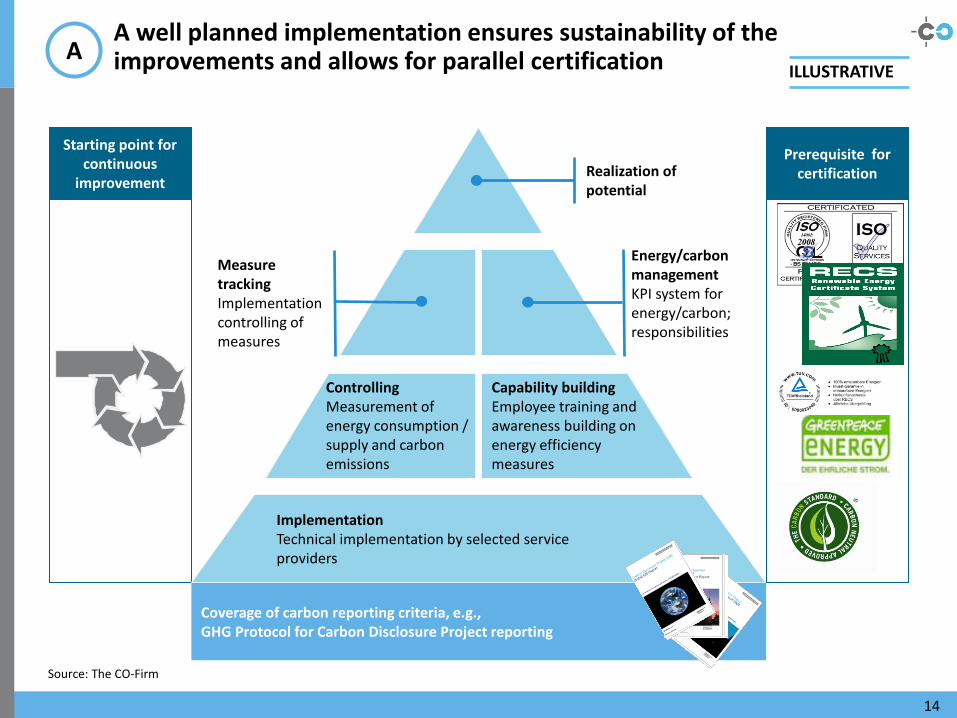

A well planned implementation ensures sustainability of the improvements and allows for parallel certification

Source: The CO-Firm

Realization of potential

Capability building Employee training and awareness building on energy efficiency measures

Controlling Measurement of energy consumption / supply and carbon emissions

Implementation Technical implementation by selected service providers

Energy/carbon management KPI system for energy/carbon; responsibilities

Measure tracking Implementation controlling of measures

Coverage of carbon reporting criteria, e.g., GHG Protocol for Carbon Disclosure Project reporting

14

A

Prerequisite for certification

ILLUSTRATIVE

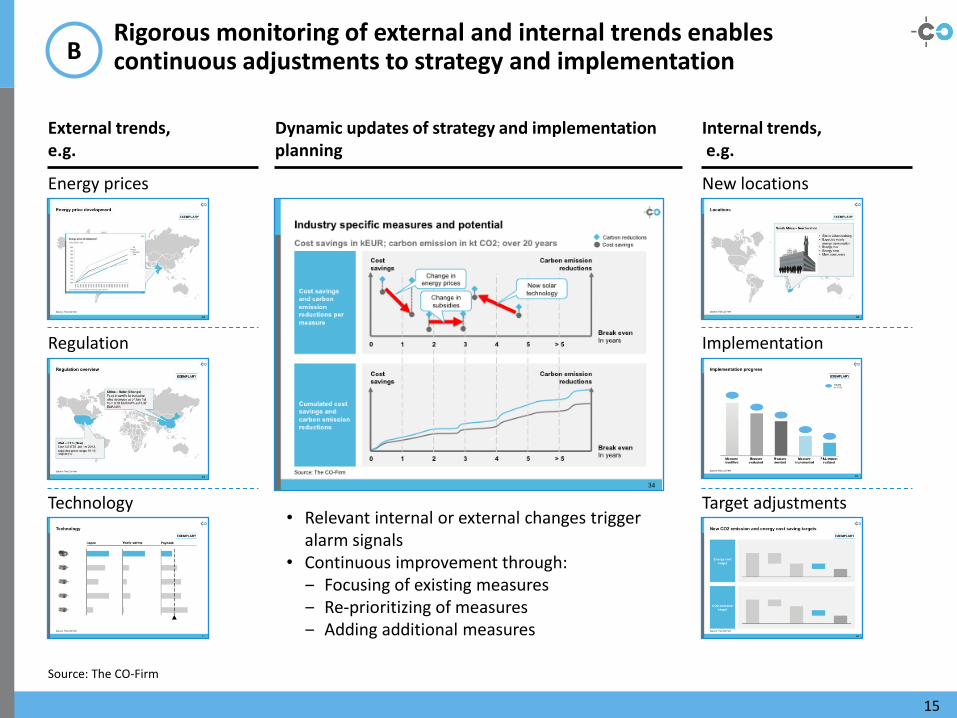

Rigorous monitoring of external and internal trends enables continuous adjustments to strategy and implementation

Source: The CO-Firm

External trends, e.g.

Internal trends, e.g.

Dynamic updates of strategy and implementation planning

• Relevant internal or external changes trigger alarm signals

• Continuous improvement through: ‒ Focusing of existing measures ‒ Re-prioritizing of measures ‒ Adding additional measures

15

B

Energy prices

Regulation

Technology

New locations

Implementation

Target adjustments

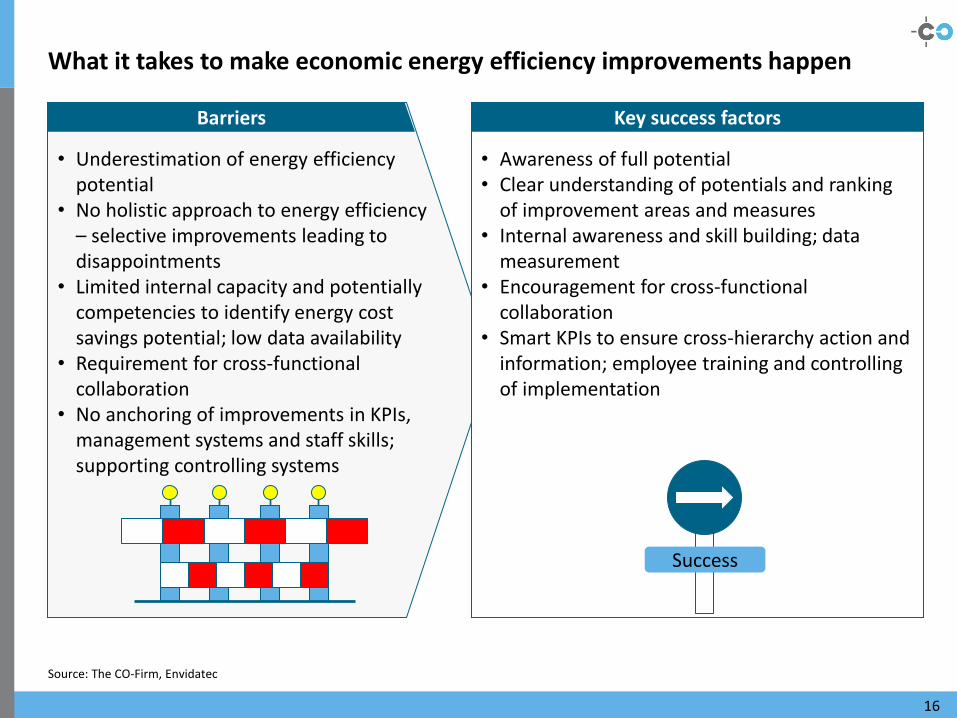

What it takes to make economic energy efficiency improvements happen

Source: The CO-Firm, Envidatec

• Underestimation of energy efficiency potential

• No holistic approach to energy efficiency – selective improvements leading to disappointments

• Limited internal capacity and potentially competencies to identify energy cost savings potential; low data availability

• Requirement for cross-functional collaboration

• No anchoring of improvements in KPIs, management systems and staff skills; supporting controlling systems

• Awareness of full potential • Clear understanding of potentials and ranking

of improvement areas and measures • Internal awareness and skill building; data

measurement • Encouragement for cross-functional

collaboration • Smart KPIs to ensure cross-hierarchy action and

information; employee training and controlling of implementation

Success

Barriers Key success factors

16

THE CARBON OPPORTUNITY FIRM

Your contact:

Dr. Nicole Röttmer

Mobile: +49 162 20 57 625

E-Mail: [email protected]

www.co-firm.com

Many thanks for your attention.

The Carbon Opportunity Firm – Vision

Source: The CO-Firm

18

Our clients realize their specific economic

opportunities from sustainable carbon action

The Carbon Opportunity Firm – What we do

Source: The CO-Firm

19

We support clients realizing sustainable business opportunities in the context of energy efficiency, renewable energy and CO2 certificates.

Detailed analysis of market potentials, business cases and trends across regions

Development of growth strategies

CO2 certificate strategies and project development, including network establishment of technology suppliers, investors and implementation partners

Training and workshops

We leverage our excellent team of consultants, internal databases on technologies, prices and regulation and an international network of strong partners.

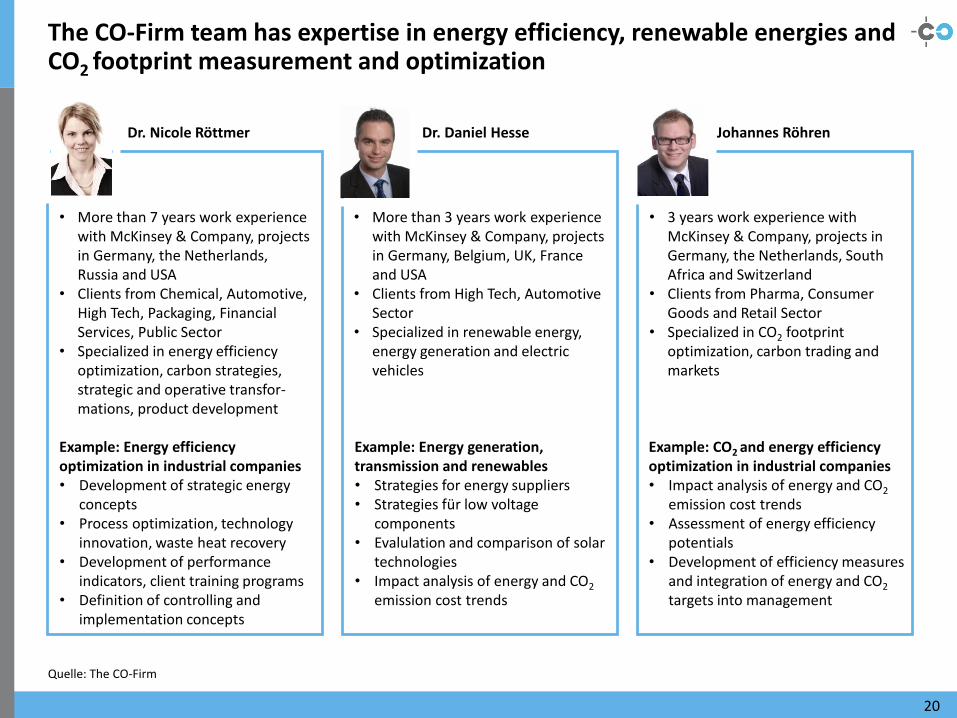

The CO-Firm team has expertise in energy efficiency, renewable energies and CO2 footprint measurement and optimization

Quelle: The CO-Firm

20

• More than 7 years work experience with McKinsey & Company, projects in Germany, the Netherlands, Russia and USA

• Clients from Chemical, Automotive, High Tech, Packaging, Financial Services, Public Sector

• Specialized in energy efficiency optimization, carbon strategies, strategic and operative transfor-mations, product development

Dr. Nicole Röttmer Dr. Daniel Hesse Johannes Röhren

Example: Energy efficiency optimization in industrial companies • Development of strategic energy

concepts • Process optimization, technology

innovation, waste heat recovery • Development of performance

indicators, client training programs • Definition of controlling and

implementation concepts

Example: Energy generation, transmission and renewables • Strategies for energy suppliers • Strategies für low voltage

components • Evalulation and comparison of solar

technologies • Impact analysis of energy and CO2

emission cost trends

• More than 3 years work experience with McKinsey & Company, projects in Germany, Belgium, UK, France and USA

• Clients from High Tech, Automotive Sector

• Specialized in renewable energy, energy generation and electric vehicles

• 3 years work experience with McKinsey & Company, projects in Germany, the Netherlands, South Africa and Switzerland

• Clients from Pharma, Consumer Goods and Retail Sector

• Specialized in CO2 footprint optimization, carbon trading and markets

Example: CO2 and energy efficiency optimization in industrial companies • Impact analysis of energy and CO2

emission cost trends • Assessment of energy efficiency

potentials • Development of efficiency measures

and integration of energy and CO2 targets into management

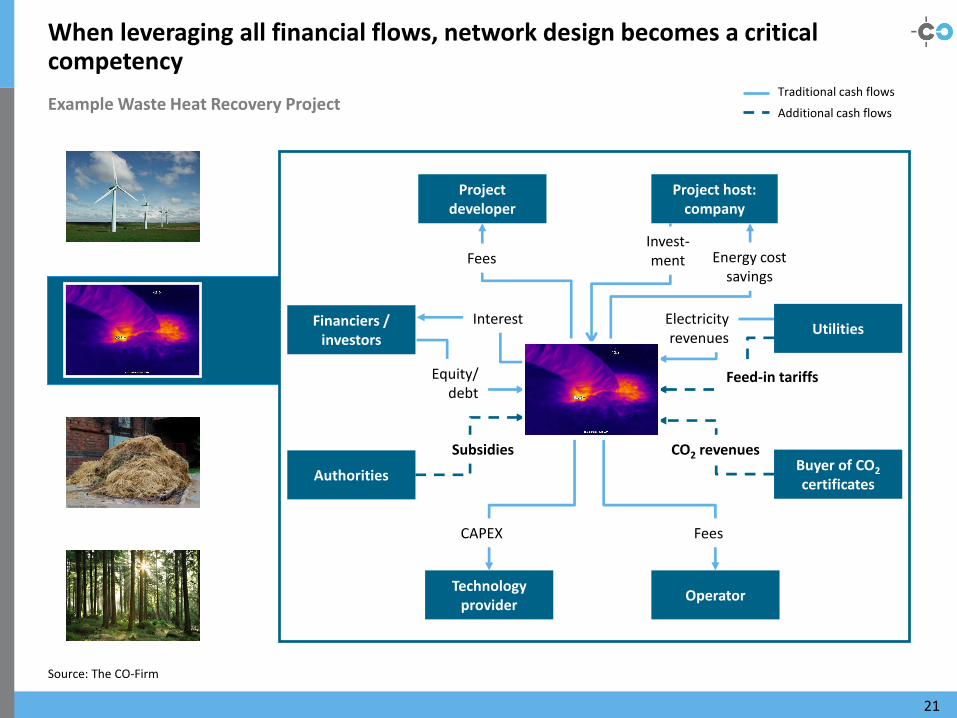

When leveraging all financial flows, network design becomes a critical competency

Example Waste Heat Recovery Project

21

Technology provider

Operator

Project developer

Financiers / investors

Authorities

Utilities

Buyer of CO2 certificates

Project host: company

Energy cost savings

Fees

Equity/ debt

Interest

Subsidies

Feed-in tariffs

Electricity revenues

CO2 revenues

Fees CAPEX

Traditional cash flows

Additional cash flows

Invest-ment

Source: The CO-Firm