EnerCom Conference - Amazon Web Services · 2014-08-18 · EnerCom Conference Rick Muncrief...

16

EnerCom Conference Rick Muncrief President & CEO, WPX Energy August 19, 2014

Transcript of EnerCom Conference - Amazon Web Services · 2014-08-18 · EnerCom Conference Rick Muncrief...

EnerCom Conference Rick Muncrief

President & CEO, WPX Energy

August 19, 2014

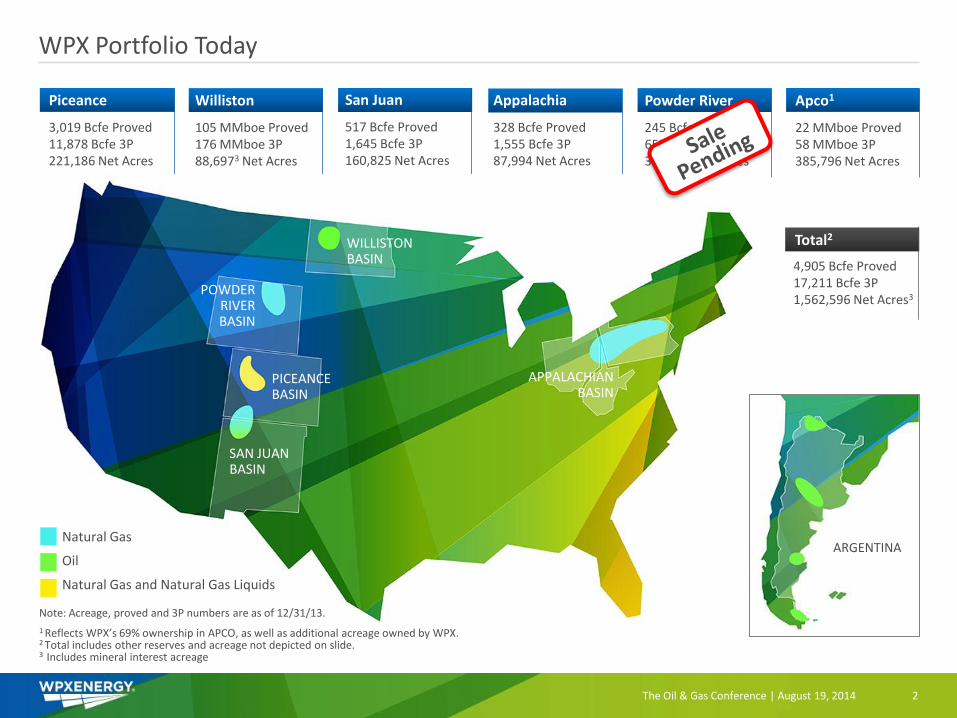

WPX Portfolio Today

The Oil & Gas Conference | August 19, 2014 2

Piceance

3,019 Bcfe Proved 11,878 Bcfe 3P 221,186 Net Acres

Williston

105 MMboe Proved 176 MMboe 3P 88,6973 Net Acres

Powder River

245 Bcfe Proved 657 Bcfe 3P 360,002 Net Acres

Apco1

22 MMboe Proved 58 MMboe 3P 385,796 Net Acres

Total Domestic

4,905 Bcfe Proved 17,211 Bcfe 3P 1,562,596 Net Acres3

Total2

San Juan

517 Bcfe Proved 1,645 Bcfe 3P 160,825 Net Acres

POWDER RIVER BASIN

PICEANCE BASIN

SAN JUAN BASIN

APPALACHIAN BASIN

WILLISTON BASIN

Natural Gas

Oil

Natural Gas and Natural Gas Liquids

Note: Acreage, proved and 3P numbers are as of 12/31/13.

1 Reflects WPX’s 69% ownership in APCO, as well as additional acreage owned by WPX. 2 Total includes other reserves and acreage not depicted on slide. 3 Includes mineral interest acreage

ARGENTINA

Appalachia

328 Bcfe Proved 1,555 Bcfe 3P 87,994 Net Acres

Industry Recognition and Awards

3 The Oil & Gas Conference | August 19, 2014

40+Awards

Innovation Colorado Oil and Gas

Drilling Innovation Award

Excellence Oil and Gas Investor

Best Discovery Award

Involvement Community Involvement

Award

2nd Quarter Highlights

Domestic oil production up 57% 2Q ’14 vs. 2Q ’13

► Domestic oil production grew 23% 2Q ’14 vs. 1Q ’14

Adjusted EBITDAX increased 40% 2Q ’14 vs. 2Q ’13

► Domestic oil revenue grew 60% quarter over quarter

Adding nearly 200 locations in the Williston

► Premium location adds in the highest quality rock in the play

Increasing San Juan Gallup spuds from 29 to 40

► ~40% increase in spuds without increasing rig count

Increased full year oil production guidance by 10%

4 The Oil & Gas Conference | August 19, 2014

Piceance Basin

5 The Oil & Gas Conference | August 19, 2014

More than 12,000 drillable locations

Excess infrastructure

Access to premium market

#1 Energy Producer in Colorado

Piceance Operations

Currently running 9 rigs

2nd quarter net production 691 MMcfe/d

► Natural gas 584 MMcf/d

► NGL 15.8 Mbbl/d

► Oil 2.0 Mbbl/d

Lowest-cost operator

► 34% less D&C capital cost1

► 57% less operating lifting cost2

State-of-the-art water management system

Successful Ryan Gulch 10-acre density

Exploratory efforts in the Niobrara

¹Utilizing data from eight 2012 Rulison field non-op wells 2Utilizing data from 215 Valley non-op wells – total well expense

6 The Oil & Gas Conference | August 19, 2014

Williston Basin

#1 Williston Producer in 1- and 2-year Cumulative Production1

7 The Oil & Gas Conference | August 19, 2014

10 years of drillable inventory

Operating 5 rigs 6-million-pound stimulations

¹Based on NDIC data for Middle Bakken laterals (7,500’ - 12,000’ ) drilled on 1,280 spacing units put on 1st sales since January 2011. Peer group includes companies with at least 20 wells with 365 days of production and 10 wells with 730 days of production as of 6/30/2014. WPX acquired Williston properties December 2010.

The Oil & Gas Conference | August 19, 2014 8

1-Yr and 2-Yr Cumulative Production per Well1 (Based on productive days)

Average 365-day cumulative production per well of 140.9 Mbo, 64% higher than the peer average

Average 730-day cumulative production per well of 224.2 Mbo, 62% higher than the peer average

WPX is #1 in Middle Bakken Cumulative Production

Peer 2-Yr Cumulative Production per Well

Peer 1-Yr Cumulative Production per Well

WPX 2-Yr Cumulative Production per Well

WPX 1-Yr Cumulative Production per Well

0.00

50,000.00

100,000.00

150,000.00

200,000.00

250,000.00

WP

X

ZAV

AN

NA

SLA

WSO

N

WH

ITIN

G

BU

RLI

NG

TON

QEP

EN

ERG

Y

SM E

NER

GY

MA

RA

THO

N

NEW

FIEL

D

CO

NTI

NEN

TAL

EOG

RES

OU

RC

ES

DEN

BU

RY

ON

SHO

RE

HES

S

OA

SIS

HU

NT

ZEN

ERG

Y

XTO

EN

ERG

Y

HR

C O

PER

ATI

NG

PET

RO

-HU

NT

MU

REX

PET

RO

LEU

M

OX

Y U

SA

SAM

SON

RES

OU

RC

ES

Peer 2-Yr Avg Peer 1-Yr Avg

¹Based on NDIC data for Middle Bakken laterals (7,500’ - 12,000’ ) drilled on 1,280 spacing units put on 1st sales since January 2011. Peer group includes companies with at least 20 wells with 365 days of production and 10 wells with 730 days of production as of 6/30/2014. WPX acquired Williston properties December 2010.

San Juan Basin

#1 Returns in the WPX Portfolio

9 The Oil & Gas Conference | August 19, 2014

Rapidly growing oil production

Diversified product mix

Over 30 years’ experience

0

10

20

30

40

50

60

70

0 100 200 300 400 500 600

Avg

Gro

ss C

um

ula

tive

Oil

Pro

du

ctio

n (

Mb

bl)

Days

2013 Spuds

2014 Spuds

13 Wells 15 Wells

San Juan Gallup 2014 Well Performance Exceeding 2013

The Oil & Gas Conference | August 19, 2014 10

Improving oil production from 2013 to 2014

► Average gross cumulative oil production grew by ~40%

► First 140 days of production

~40% Increase from 2013 to 2014

Strategic Review Process Underway

► Full-scale review of entire portfolio

► Multi-year strategy

► Measurable strategy

► Strategy to be unveiled this fall

11 The Oil & Gas Conference | August 19, 2014

Historical Commodity Snapshot

In recent years, oil and natural gas have been range bound

► Since 2011, 81% of days were over $90/bbl; 87% of days were under $105

► Since 2011, 81% of days were over $3/MBtu; 98% of days were under $5

WTI

$/b

bl

12 The Oil & Gas Conference | August 19, 2014

$1.00

$3.00

$5.00

$7.00

$9.00

$11.00

$13.00

$30.00

$50.00

$70.00

$90.00

$110.00

$130.00

$150.00

Jan

-07

M

ar-0

7

May

-07

Ju

l-0

7

Sep

-07

N

ov-

07

Ja

n-0

8

Mar

-08

M

ay-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

M

ar-0

9

May

-09

Ju

l-0

9

Sep

-09

N

ov-

09

Ja

n-1

0

Mar

-10

M

ay-1

0

Jul-

10

Se

p-1

0

No

v-1

0

Jan

-11

M

ar-1

1

May

-11

Ju

l-1

1

Sep

-11

N

ov-

11

Ja

n-1

2

Mar

-12

M

ay-1

2

Jul-

12

Se

p-1

2

No

v-1

2

Jan

-13

M

ar-1

3

May

-13

Ju

l-1

3

Sep

-13

N

ov-

13

Ja

n-1

4

Mar

-14

M

ay-1

4

Jul-

14

Natu

ral Gas $

/MB

tu

Oil

Gas

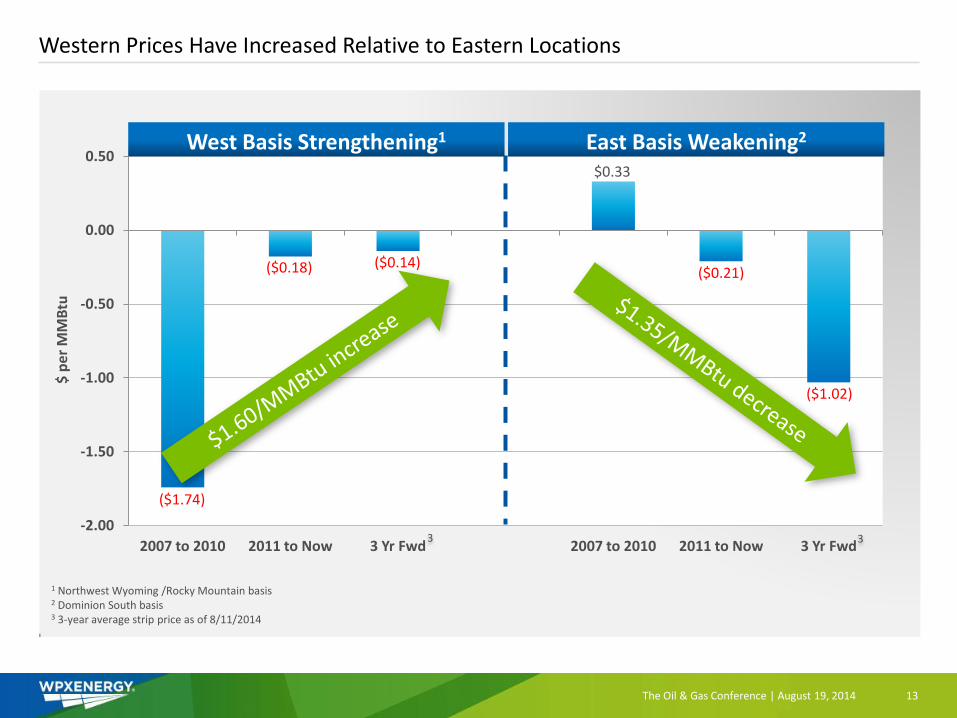

Western Prices Have Increased Relative to Eastern Locations

13 The Oil & Gas Conference | August 19, 2014

1 Northwest Wyoming /Rocky Mountain basis 2 Dominion South basis 3 3-year average strip price as of 8/11/2014

-2.00

-1.50

-1.00

-0.50

0.00

0.50

2007 to 2010 2011 to Now 3 Yr Fwd 2007 to 2010 2011 to Now 3 Yr Fwd

($1.74)

($0.18) ($0.14)

$0.33

($0.21)

($1.02)

West Basis Strengthening1 East Basis Weakening2

$ p

er M

MB

tu

3 3

Shifting to Pure Play E&P Mindset

“We are building one culture, one organization, one mission.”

14 The Oil & Gas Conference | August 19, 2014

More Nimble

View Asset Base in

New Way

Focus on Profitability

Greater Risk

Tolerance

WPX Long-Term Vision Coming Into Focus

The Oil & Gas Conference | August 19, 2014 15

Company Strategy

Integrity Scalability Identity

The Oil & Gas Conference | August 19, 2014 16