En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

36

Banco Sabadell BoAML Banki ng & Insurance CEO Conference Jaime Guardi ola, Consejero Delegado October 5 th , 2011

Transcript of En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 1/35

Banco Sabadell

BoAML Banking & Insurance CEOConference

Jaime Guardiola, Consejero DelegadoOctober 5th, 2011

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 2/35

2

Disclaimer

Banco Sabadell cautions that this presentation may contain forward looking statements with respect to thebusiness. financial condition. results of operations. strategy. plans and objectives of the Banco Sabadell Group.While these forward looking statements represent our judgement and future expectations concerning the

development of our business. a certain number of risks. uncertainties and other important factors could cause

actual developments and results to differ materially from our expectations. These factors include. but are notlimited to. (1) general market. Macroeconomic. governmental. political and regulatory trends. (2) movements inlocal and international securities markets. currency exchange rate. and interest rates. (3) competitive pressures.(4) technical developments. (5) changes in the financial position or credit worthiness of our customers. obligorsand counterparts. These risk factors could adversely affect our business and financial performance published inour past and future filings and reports. including those with the Spanish Securities and Exchange Commission(Comisión Nacional del Mercado de Valores).

Banco Sabadell is not nor can it be held responsible for the usage. valuations. opinions. expectations ordecisions which might be adopted by third parties following the publication of this information.

Financial information by business areas is presented according to GAAP as well as internal Banco Sabadellgroup´s criteria as a result of which each division reflects the true nature of its business. These criteria do not

follow any particular regulation and can include forecasts and subjective valuations which could represent

substantial differences should another methodology be applied.

The distribution of this presentation in certain jurisdictions may be restricted by law. Recipients of thispresentation should inform themselves about and observe such restrictions.

These slides do not constitute or form part of any offer for sale or subscription of or solicitation or invitation ofany offer to buy or subscribe to any securities nor shall they or any one of them form the basis of or be relied onin connection with any contract or commitment whatsoever.

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 3/35

3

1. Economic environment

2. Liquidity and funding

3. Commercial activity4. Asset quality and real estate

Index

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 4/35

4

1. Economicenvironment

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 5/35

5

-30

-20

-10

0

10

2006 2007 2008 2009 2010 2011

4Q10 1Q11 2Q11

GDP (% chg. QoQ) 0.2 0.4 0.2

Private consumption 0.3 -0.1 0.6

Inv. capital equipment 1.2 0.0 0.3

Inv. construction -3.1 -2.8 -0.9

Exports 3.9 5.8 -1.9

GDP (% chg. YoY) 0.6 0.9 0.7

Spain's economy has stabilised

Sources: INE and European Commission

Industrial output(% chg. YoY)

Consumer confidence(level)

-50

-40

-30

-20

-10

0

2006 2007 2008 2009 2010 2011

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 6/35

6

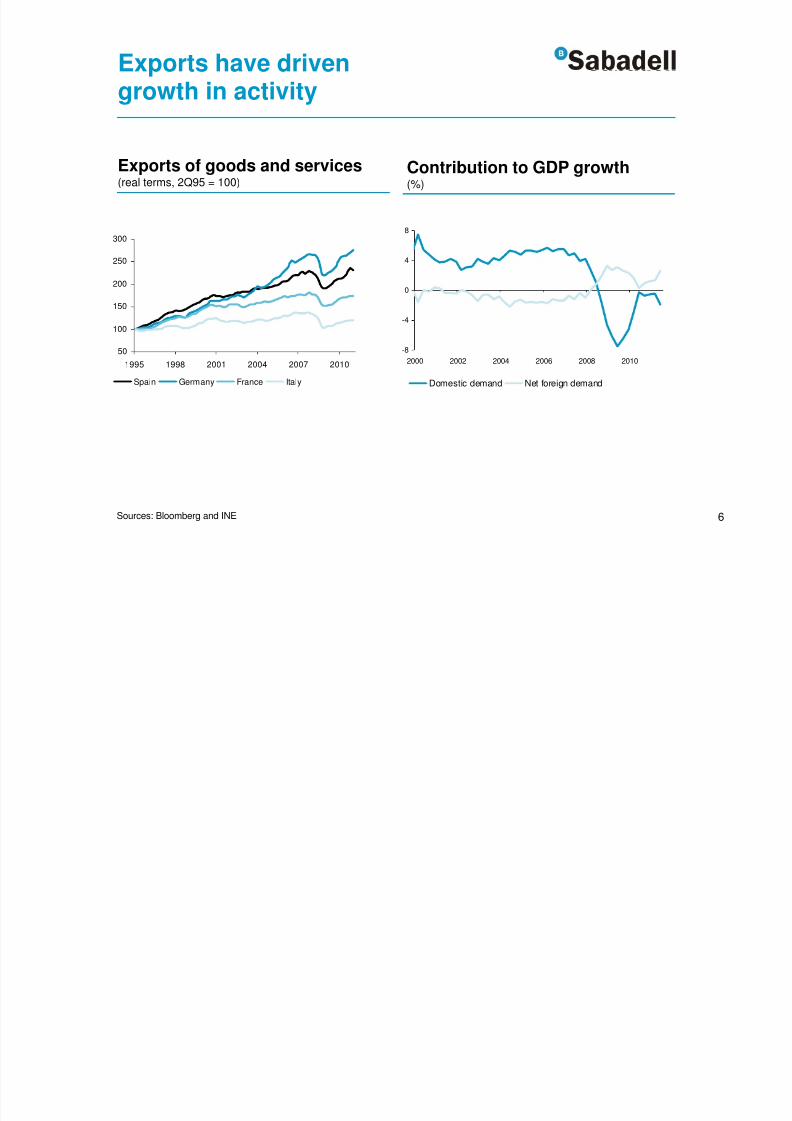

-8

-4

0

4

8

2000 2002 2004 2006 2008 2010

Domestic demand Net foreign demand

Sources: Bloomberg and INE

Exports of goods and services(real terms, 2Q95 = 100)

50

100

150

200

250

300

1995 1998 2001 2004 2007 2010

Spain Germany France Italy

Exports have driven

growth in activity

Contribution to GDP growth(%)

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 7/35

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 8/35

50

55

60

65

7075

80

85

90

95

2 0 1 0

2 0 1 1

2 0 1 2

2 0 1 3

2 0 1 4

2 0 1 5

2 0 1 6

2 0 1 7

2 0 1 8

2 0 1 9

2 0 2 0

2 0 2 1

2 0 2 2

2 0 2 3

2 0 2 4

2 0 2 5

8

3

4

5

6

2000 2002 2004 2006 2008 2010

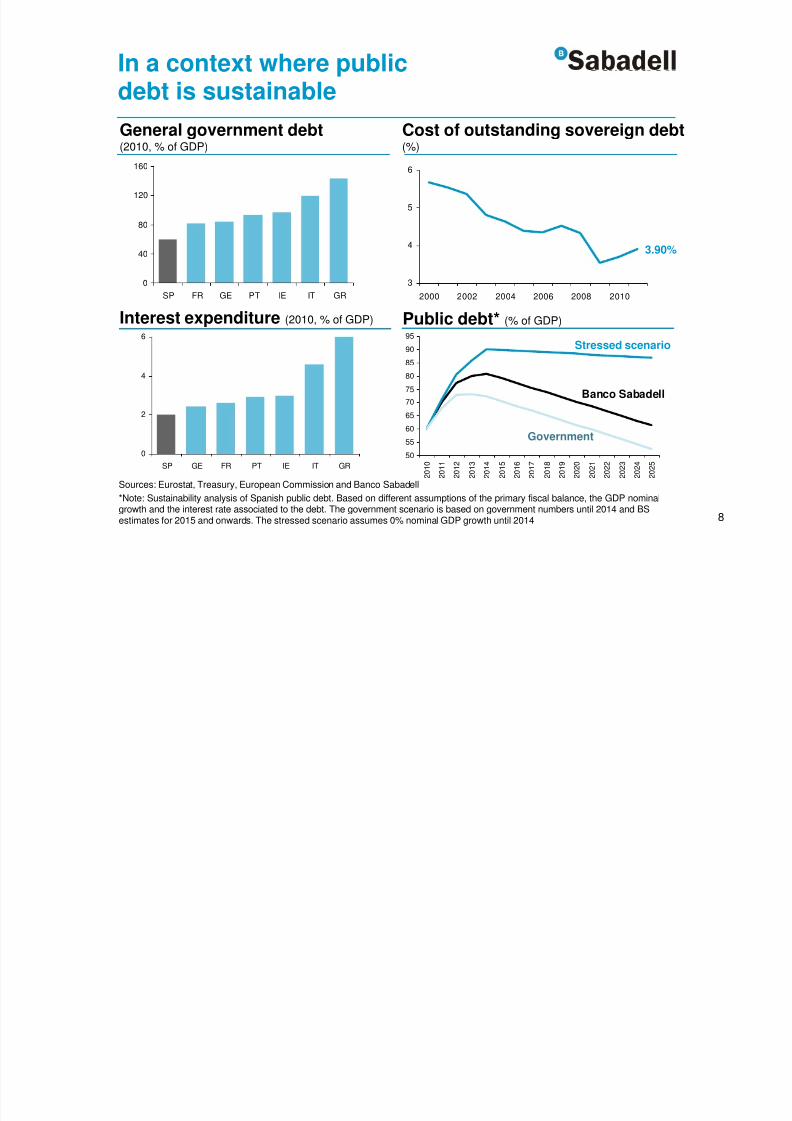

0

40

80

120

160

SP FR GE PT IE IT GR

3.90%

0

2

4

6

SP GE FR PT IE IT GR

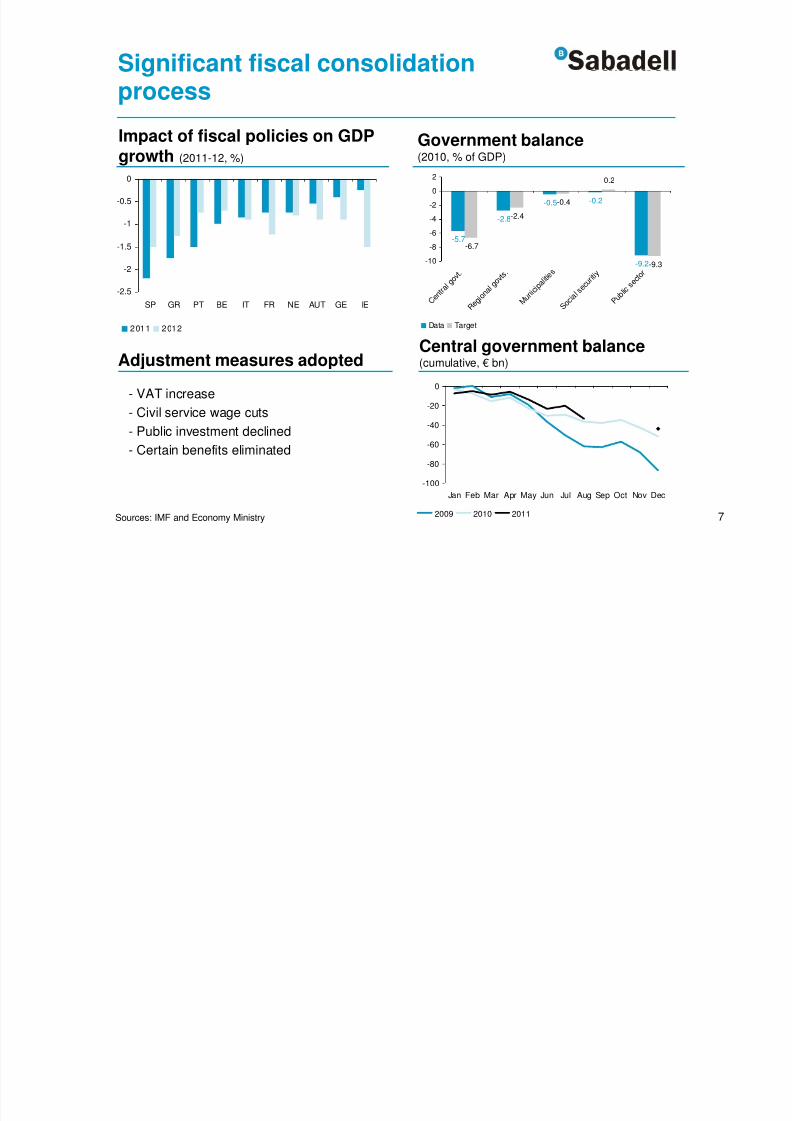

In a context where public

debt is sustainable

Sources: Eurostat, Treasury, European Commission and Banco Sabadell*Note: Sustainability analysis of Spanish public debt. Based on different assumptions of the primary fiscal balance, the GDP nominalgrowth and the interest rate associated to the debt. The government scenario is based on government numbers until 2014 and BSestimates for 2015 and onwards. The stressed scenario assumes 0% nominal GDP growth until 2014

Public debt* (% of GDP)

General government debt(2010, % of GDP)

Cost of outstanding sovereign debt(%)

Interest expenditure (2010, % of GDP)

Stressed scenario

Banco Sabadell

Government

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 9/35

9

Progress is being made with

structural reforms

Progress in structural reformsFiscal governance reform

• Law tying spending to medium-termeconomic growth

• Budget stability enshrined inConstitution, limiting the structuraldeficit

• Greater transparency in regionalgovernments' fiscal information

• Labour market and pension systemreform

• Measures to reduce the paperwork for

creating companies

• Restructuring of the financial systemand greater transparency in financialsystem exposure to construction and

real estate development

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 10/35

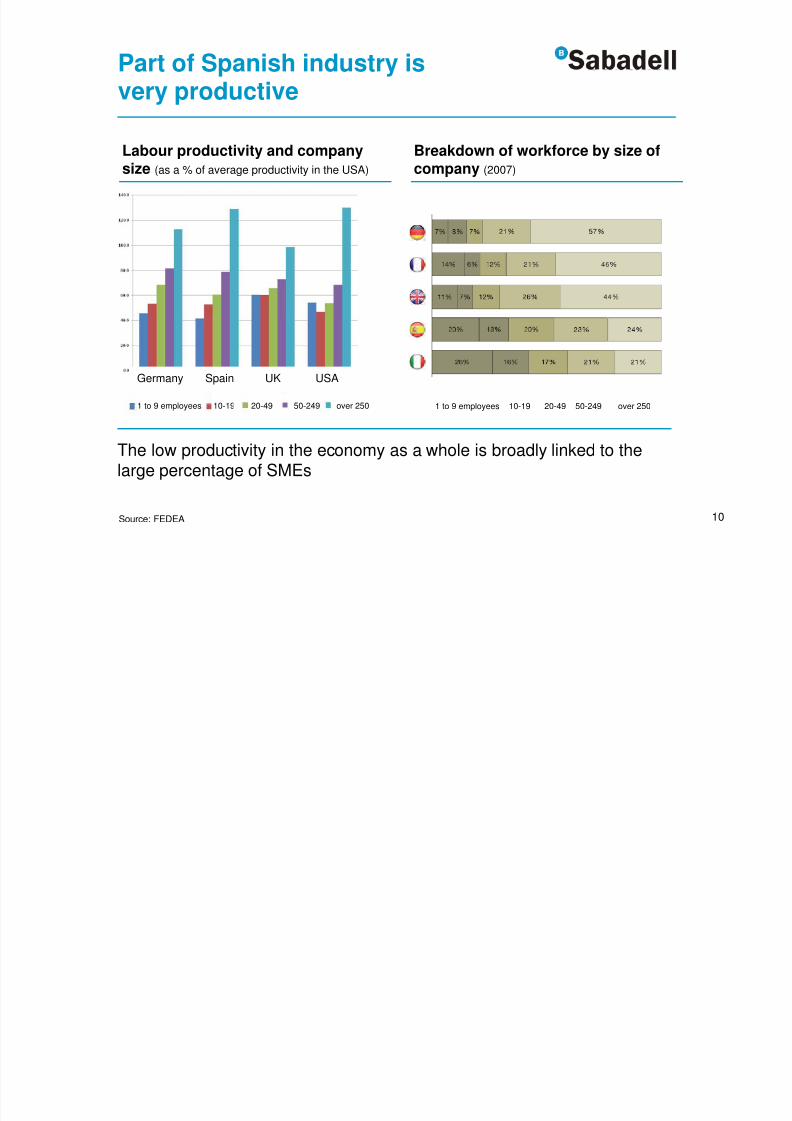

10Source: FEDEA

Labour productivity and companysize (as a % of average productivity in the USA)

The low productivity in the economy as a whole is broadly linked to thelarge percentage of SMEs

Breakdown of workforce by size ofcompany (2007)

Germany Spain UK USA

Part of Spanish industry is

very productive

1 to 9 employees 10-19 20-49 50-249 over 2501 to 9 employees 10-19 20-49 50-249 over 250

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 11/35

11

95

97

99

101

103

105

107

109

dic-07 jun-08 d ic-08 jun-09 d ic-09 jun-10 d ic-10

Spain Eurozone

Real labour productivity per capitain Spain (2000 = 100)

Improvement in the behaviour of

productivity and unit labour costs

Labour costs in Spain(% chg. YoY)

99

101

103

105

107

109

2000 2002 2004 2006 2008 2010

-1

0

1

2

3

45

6

2001 2003 2005 2007 2009 2011

100

102

104

106

108

2007 2008 2008 2009 2009 2010 2010

Spain Eurozone

Unit labour costs(Dec. 07 = 100)

Sources: INE, Eurostat and Bank of Spain

Real labour productivity percapita (Dec. 07 = 100)

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 12/35

12

40

45

50

55

60

65

S p a i n

G e r m

a n y

B e l g i u m

S w e d

e n

A u s t r i a

I r e l a n

d

F r a n

c e U K I t a l y

G r e e

c e

H o l l a

n d

P o r t u

g a l

Spanish companies are gradually refocusing their exports on marketswith greater growth potential

Sources: Goldman Sachs and COMTRADE

*Note: Index of price elasticity of exports (Goldman Sachs). Indicates how skewed a country exports are towards price inelastic goods.The higher the score on the index, the smaller the impact on export performance related to price changes. A higher score indicates thatnon-price factors dominate exports.

Exports' price sensitivity* Share of services exports (2000=100)

60

80

100

120

140

2000 2002 2004 2006 2008 2010

Spain GermanyUnited States France

Competitive position of

Spanish companies

Lower pricesensitivity

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 13/35

13

2. Liquidity andfunding

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 14/35

14

The challenging environment in

Europe increases concerns …Corporate Bond Holdings of USPrimary Dealers (USD bn)

Financial CDS 5Y in Europe(basis points)

ECB: Public Debt holdings underthe security market program (€ bn)

Stock exchange(Jan11 = 100)

Sources: Morgan Stanley, ECB and Bloomberg

0

100

200

300

400

500

600

2007 2008 2009 2010 2011Senior Subordinated

0

20

40

60

80

100

120

140

160

May-10 Aug-10 Nov-10 Feb-11 May-11 Aug-11

60

80

100

120

Jan-11 Mar-11 May-11 Jul-11 Sep-11

US (S&P500) Germany (DAX)

Spain (IBEX) Brazil (BOVESPA)

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 15/35

15

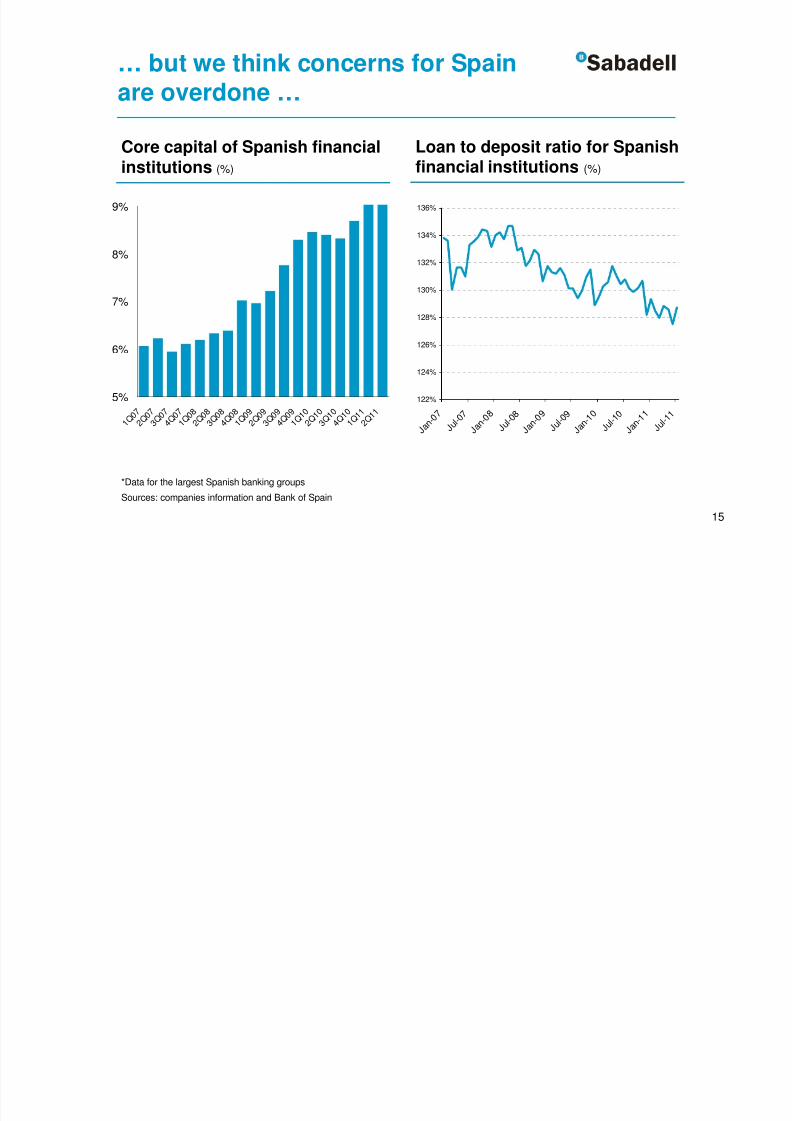

… but we think concerns for Spain

are overdone …

5%

6%

7%

8%

9%

1 Q 0 7

2 Q 0 7

3 Q 0 7

4 Q 0 7

1 Q 0 8

2 Q 0 8

3 Q 0 8

4 Q 0 8

1 Q 0 9

2 Q 0 9

3 Q 0 9

4 Q 0 9

1 Q 1 0

2 Q 1 0

3 Q 1 0

4 Q 1 0

1 Q 1 1

2 Q 1 1

*Data for the largest Spanish banking groups

Sources: companies information and Bank of Spain

Core capital of Spanish financialinstitutions (%)

Loan to deposit ratio for Spanishfinancial institutions (%)

122%

124%

126%

128%

130%

132%

134%

136%

J a n - 0 7

J u l - 0

7

J a n - 0 8

J u l - 0

8

J a n - 0 9

J u l - 0

9

J a n - 1 0

J u l - 1

0

J a n - 1 1

J u l - 1

1

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 16/35

16

ECB and central banks net liquidityprovision for European financial

institutions (as % of total assets)

0

2

4

6

8

10

12

14

2007 2008 2009 2010 2011

0

5

10

15

20

25

Ireland Portugal Spain

Germany Italy France

Greece (rhs)

ECB net liquidity provision andtotal assets in the European

context (€ bn and %)

… in light of fundamentals

Source: ECB, July & August 2011 data

ECB and

central

banks

liquidity

provision

as % of

total

liquidity

provision

Total

domestic

assets

as % of

total

domestic

assetsGermany 58 10% 8,001 25%

France 29 5% 7,979 25%

Italy 85 14% 3,848 12%

Spain 81 14% 3,553 11%

Greece 112 19% 502 2%

Portugal 46 8% 570 2%Ireland 154 26% 1,377 4%

Total 596 32,154

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 17/35

17

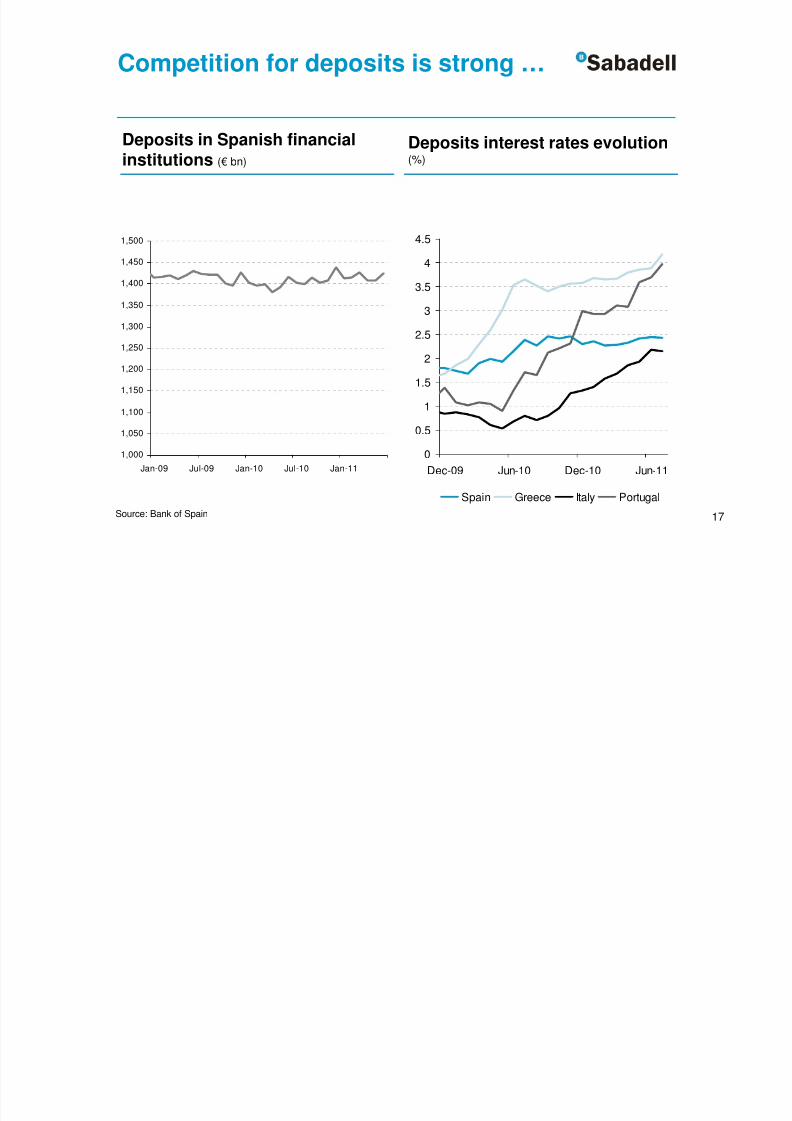

Competition for deposits is strong …

Deposits in Spanish financialinstitutions (€ bn)

1,000

1,050

1,100

1,150

1,200

1,250

1,300

1,350

1,400

1,450

1,500

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11

Deposits interest rates evolution(%)

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Dec-09 Jun-10 Dec-10 Jun-11

Spain Greece Italy Portugal

Source: Bank of Spain

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 18/35

18

… but BS has managed to increase itsdeposit base in the last quarters

BS deposit market share(%)

BS deposits evolution(€ m)

30,000

35,000

40,000

45,000

50,000

55,000

4Q08 1Q09 2Q09 3Q09 4Q091Q0102Q10 3Q10 4Q10 1Q11 2Q11

Total Deposits Acquisition BG New Deposits

2009 +€ 2.0bn

2010 +€ 6.3bn(excl. BG)

2011 YTD+€ 1.6bn

2

2.2

2.4

2.6

2.8

3

3.2

3.4

3.6

3.8

J u n - 0

7

O c t - 0

7

F e b -

0 8

J u n - 0

8

O c t - 0

8

F e b -

0 9

J u n - 0

9

O c t - 0

9

F e b -

1 0

J u n - 1

0

O c t - 1

0

F e b -

1 1

J u n - 1

1

Source: Bank of Spain

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 19/35

19

Most of our deposit base has

maturities over one year …

BS back book deposits by maturity(%)

BS deposit base by segment(%)

SMEs and

Corporates

41%

Retailers and

self-employed

8%

Other sectors

5%

Public sector

3%

Individuals

43%

9%

7%

37%

48%

Term deposit over 12 months

Term deposit 12 months

Term deposit 6 months

Term deposit 3 months

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 20/35

20

… giving us more margin to actively

manage spreads

Product jun-10 jun-11 Var YoY jun-10 jun-11 Var YoY

Credits 233 264 +31 174 223 +49Loans 156 247 +91 156 194 +38

Mortgages to individuals 81 116 +35 74 78 +4

Leasing 161 206 +45 97 113 +16

Commercial loans 242 290 +48 267 309 +42

Confirming 184 225 +41 168 237 +69

Forfaiting 263 225 -38 183 215 +32

Total loans 168 230 +62 134 157 +23

Term deposit 1 month 104 86 -18 86 69 -17

Term deposit 3 months 157 103 -54 99 69 -30

Term deposit 6 months 220 107 -113 121 113 -8

Term deposit 12 months 210 109 -101 165 160 -5

Term deposit 18 months 194 160 -34 163 191 +28

Term deposit 2 years 219 176 -43 160 204 +44

Term deposits 3 years 198 179 -19 89 134 +45

Deposits 182 116 -66 149 157 +8

Front book spreads Back book spreads

In basis points

Jun-10 Jun-11 Jun-10 Jun-11

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 21/35

21

3. Commercial activity

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 22/35

22

Attracting new clients…

Monthly new individual customers Monthly new company customers

0

5,000

10,000

15,000

20,000

25,000

30,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2010 2011

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2010 2011

Target 2011: 290,000

new customers

Target 2011: 50,000

new customers

Performance in line with CREA targets

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 23/35

23

… and growing market shares in

individuals …

Total sight deposits

3.88%

4.29%

Jun. 10

Jun. 11

+41 bps

2.06%

2.52%

Jun. 10

Jun. 11

Payrolls

+46 bps

Credit card invoicing (quarterly)

3.20%

2.74%Jun. 10

Jun. 11

+46 bps

2,94%

3.51%

Jun. 10

Jun. 11

+57 bps

1 Including cheques, transfers, SEPA transfers, receivables and promissory notes

Transactionality1

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 24/35

24

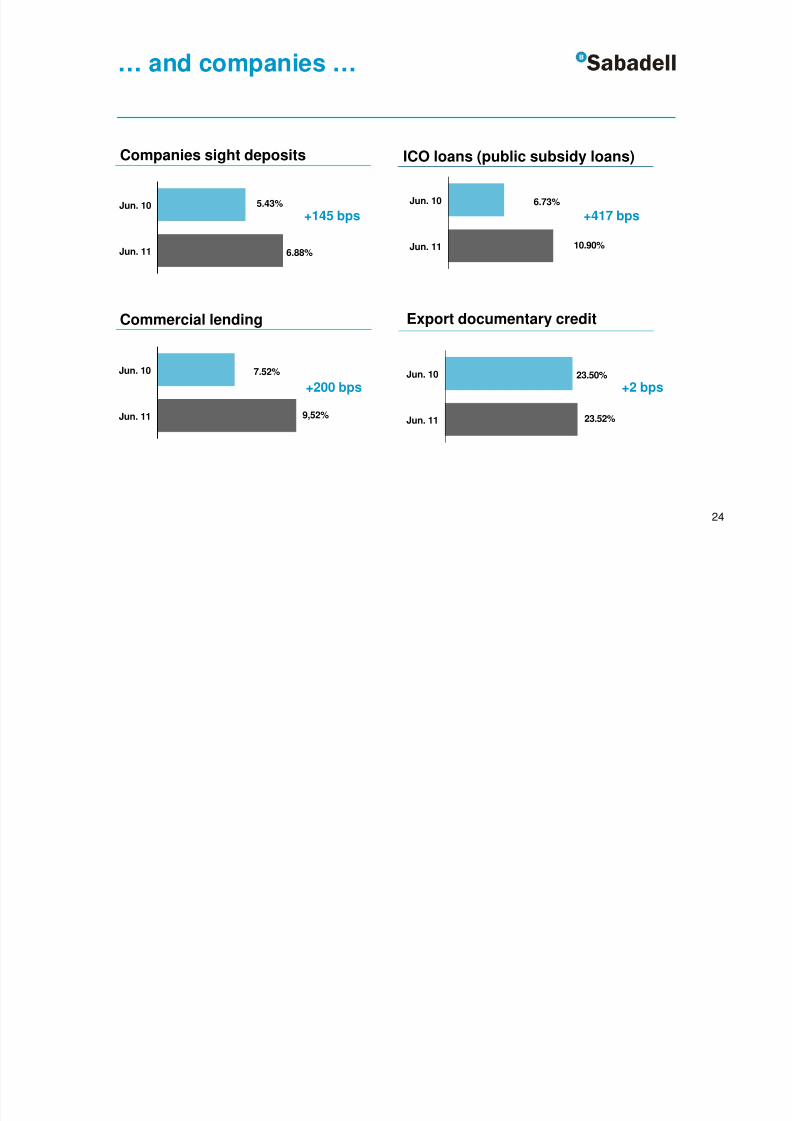

… and companies …

5.43%

6.88%

Jun. 10

Jun. 11

+145 bps

Commercial lending

23.50%

23.52%

Jun. 10

Jun. 11

+2 bps

6.73%

10.90%

Jun. 10

Jun. 11

+417 bps

7.52%

9,52%

Jun. 10

Jun. 11

+200 bps

Companies sight deposits ICO loans (public subsidy loans)

Export documentary credit

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 25/35

25

… holding up volumes in a

difficult environmentBS customer funds evolution

1 Including BG in 2010

2 Excluding repos, including preference shares and mandatory convertible bond placed in the retail network

Euros in million

Jun-10 Dec-10 Jun-11

% Var.

YoY

% Var. YoY

proforma1

On-balance sheet customer funds2

41,212 49,374 51,055 23.9% 10.7%Fix-term deposits 24,191 30,092 31,456 30.0% 15.7%

Sight deposits 16,021 18,285 18,600 16.1% 3.8%

Off-balance sheet funds 17,908 18,834 18,563 3.7% -2.1%Mutual funds 8,532 8,853 8,613 0.9% -6.8%

Pension funds 2,777 3,016 2,903 4.6% -6.6%

Third party insurance products 5,434 5,727 5,691 4.7% 4.4%

Gross loans to customers ex repos 65,356 73,058 72,309 10.6% -0.8%

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 26/35

26

4. Asset quality andreal estate

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 27/35

27

Slow negative trend persists …

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

9 0 9 1 9 2 9 3 9 4 9 5 9 6 9 7 9 8 9 9 0 0 0 1 0 2 0 3 0 4 0 5 0 6 0 7 0 8 0 9 1 0

J u n - 1

1

System NPL BS NPL

NPL ratio of Banco Sabadell vs.the system (%)

Real estate over total loans(%)

Source: Bank of Spain and annual reports

System BS

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

1 Q 0 7 2 Q

0 7 3 Q

0 7 4 Q

0 7 1 Q

0 8 2 Q

0 8 3 Q

0 8 4 Q

0 8 1 Q

0 9 2 Q

0 9 3 Q

0 9 4 Q

0 9 1 Q

1 0 2 Q

1 0 3 Q

1 0 4 Q

1 0 1 Q

1 1

4.28%

3.43%

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 28/35

28

… but manageable at the

provisioning level

Euros in million

Resilient pre-provision result has allowed forsignificant provisions to be taken through the P&L

BS pre-provision profit and cost of risk evolution(€ m)

*

* Including tax recoveries of € 99.1 m

2008 2009 2010 jun-11

Pre-provision profit 1.114,6 1.325,5 1.136,3 659,1

Total provisions -879,7 -837,7 -968,1 -545,5

Extraordinary items 650,7 83,6 296,1 102,8

Net profit 673,8 522,5 380,0 165,4

Cost of risk (bps) 136 129 133 151

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 29/35

29

Ramping up sales effort of RE

assets on bank’s balancesheet

Solvia sales force givesincentives to sell off balance

sheet RE assets

RE Credit portfolio

70-80 new hires of real estate

professionals

Regional credit risk officersworking side by side with REprofessionals to evaluate risk and

advising customers

RE risk arising from credit and asset exposures

RE Assetson and off BS

Adopting a more global approach to

managing RE risk …

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 30/35

30

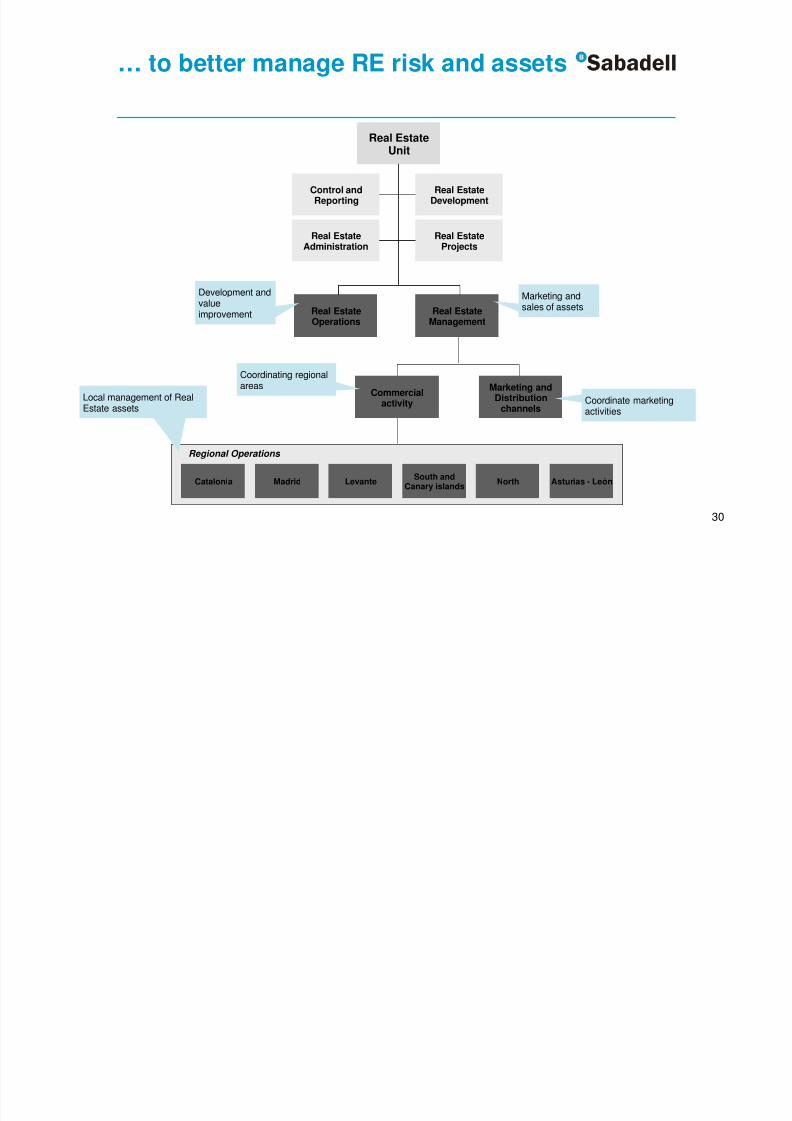

… to better manage RE risk and assets

Real EstateUnit

Real Estate

Development

Real EstateProjects

Real EstateOperations

Real EstateManagement

Control and

Reporting

Real EstateAdministration

Marketing and

Distributionchannels

Commercialactivity

Development andvalueimprovement

Marketing andsales of assets

Coordinate marketingactivities

Regional Operations

Catalonia Madrid Levante NorthSouth and

Canary islandsAsturias - León

Local management of RealEstate assets

Coordinating regionalareas

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 31/35

Finishedproperty

Land underdevelopment

Land Total %

% in

Barcelona /

Madrid

1st residence 922 966 537 2,424 67% 42%

2nd residence 168 123 37 328 9%

Industrial 151 36 143 330 9% 72%

Commercial 117 204 45 366 10% 64%

Hotels 80 35 13 128 4%

Other 22 2 1 25 1%

Gross portfolio 1,459 1,366 776 3,601 100% 48%

Provisions 320 443 269 1,032 29%

Net portfolio 1,139 923 507 2,569

31

67% of the portfolio is first residence

BS real estate portfolio breakdown(€ m)

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 32/35

32

2009 2010 1Q11 2Q11

Sales price 42 174 48 71

Pre-provision cost1

55 228 67 95

Discount to pre-provision costs 23% 24% 27% 25%

Provisions built up 12% 23% 29% 23%

% of sales price not covered by provisions 11% 1% -1% 2%

Real estate assets are sold at pricesin line with current book value

BS real estate asset sales evolution(€ m and %)

Sales target for 2011: € 400 million2

1 Including acquisition, development, and any transaction costs related to the sale of the asset2

Pre-provision cost

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 33/35

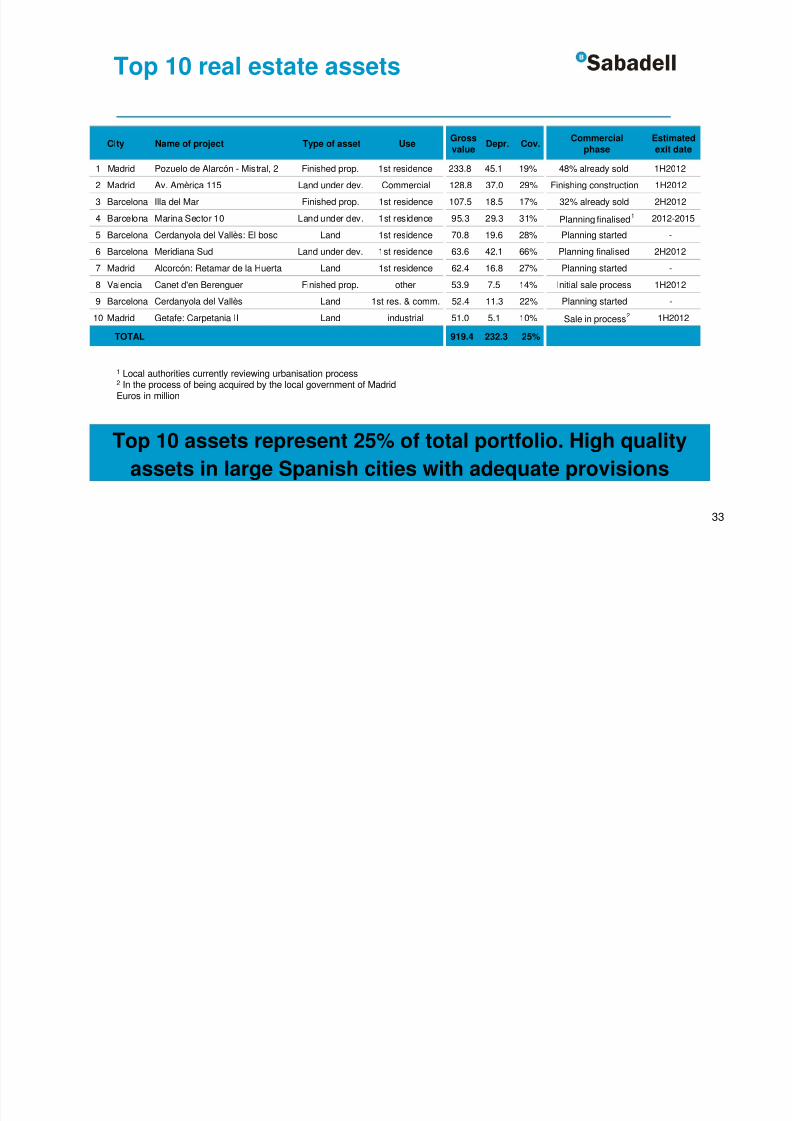

City Name of project Type of asset UseGross

valueDepr. Cov.

Commercial

phase

Estimated

exit date

1 Madrid Pozuelo de Alarcón - Mistral, 2 Finished prop. 1st residence 233.8 45.1 19% 48% already sold 1H2012

2 Madrid Av. Amèrica 115 Land under dev. Commercial 128.8 37.0 29% Finishing construction 1H2012

3 Barcelona Illa del Mar Finished prop. 1st residence 107.5 18.5 17% 32% already sold 2H2012

4 Barcelona Marina Sector 10 Land under dev. 1st residence 95.3 29.3 31% Planning finalised1 2012-2015

5 Barcelona Cerdanyola del Vallès: El bosc Land 1st residence 70.8 19.6 28% Planning started -

6 Barcelona Meridiana Sud Land under dev. 1st residence 63.6 42.1 66% Planning finalised 2H2012

7 Madrid Alcorcón: Retamar de la Huerta Land 1st residence 62.4 16.8 27% Planning started -

8 Valencia Canet d'en Berenguer Finished prop. other 53.9 7.5 14% Initial sale process 1H2012

9 Barcelona Cerdanyola del Vallès Land 1st res. & comm. 52.4 11.3 22% Planning started -

10 Madrid Getafe: Carpetania II Land industrial 51.0 5.1 10% Sale in process2 1H2012

TOTAL 919.4 232.3 25%

33

Top 10 real estate assets

Top 10 assets represent 25% of total portfolio. High quality

assets in large Spanish cities with adequate provisions

1 Local authorities currently reviewing urbanisation process2 In the process of being acquired by the local government of Madrid

Euros in million

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 34/35

34

Outlook 2011-2012

Lower volumes

Better net interest income due to lower rates thanforecasted

Satisfactory fees evolution

Provisioning behaviour according to expectations

8/3/2019 En Presentation Merrill Lynch Oct2011 Presentation Banco Sabadell (1)

http://slidepdf.com/reader/full/en-presentation-merrill-lynch-oct2011-presentation-banco-sabadell-1 35/35

35