Economics for Leaders I have with me at this EFL program a new Dell Vostro 13 Notebook computer. It...

33

Economics for Leaders I have with me at this EFL program a new Dell Vostro 13 Notebook computer. It has 13” screen, DVD drive, 500 GB hard drive, 4 GB Ram, i5 processor, windows 7, internal wireless, etc. Questions: It is mine . How much money would you give me for the computer? (You have until the end of the week to come up with the cash) ________ I have applied for a grant to study cigarette tax policies across the different states of the United States. To perform this project punctually, I will probably have to hire some research assistants. This work will have to be performed during the next 30 days. (at your home) The work will include data collection, research, and data coding. Questions: 2.How many hours would you work total over that time period? (next 30 days) if I paid you $35 per hour

-

Upload

abner-perkins -

Category

Documents

-

view

219 -

download

2

Transcript of Economics for Leaders I have with me at this EFL program a new Dell Vostro 13 Notebook computer. It...

Economics for Leaders

I have with me at this EFL program a new Dell Vostro 13 Notebook computer. It has 13” screen, DVD drive, 500 GB hard drive, 4 GB Ram, i5 processor, windows 7, internal wireless, etc.Questions:

It is mine. How much money would you give me for the computer? (You have until the end of the week to come up with the cash) ________

I have applied for a grant to study cigarette tax policies across the different states of the United States. To perform this project punctually, I will probably have to hire some research assistants. This work will have to be performed during the next 30 days. (at your home) The work will include data collection, research, and data coding.Questions:

2.How many hours would you work total over that time period?(next 30 days) if I paid you $35 per hour

3. I will probably undertake the project even if I do not get thegrant. How many hours would you be willing to work if I paid you $10 per hour?

Economics for Leaders

Economics for Leaders

Lesson 2: Opportunity Cost & Incentives

Economics for Leaders

Economic Reasoning Principle #1: People choose, and individual choices are the source of social outcomes.

Scarcity necessitates choices

Economics for Leaders

How Do You Know When

Scarcity Forces You to CHOOSE

Something Is Scarce?

SCARCITY CHOICE

Economics for Leaders

Economic Reasoning Principle # 2: Choices impose costs; people receive benefits and incur costs when they make decisions.

The cost of a choice is the value of the next-best alternative foregone.

Economics for Leaders

Opportunity Cost: the value of the next best or

foregone alternative

Think: “next-best”

Economics for Leaders

Opportunity Cost =the value of the

Next-Best Alternative

– What are the considered alternatives?• What would you do – not what could you

do?• What does the decision-maker perceive

to be the benefits of each alternative?

Economics for Leaders

Opportunity Cost Analysis

What was the 1st decision you made this morning?

Economics for Leaders

Opportunity Cost Analysis

Alternatives: Get Up Now Don’t Get Up Now

Perceived Benefits

Choice

Opp. Cost

Benefits Refused

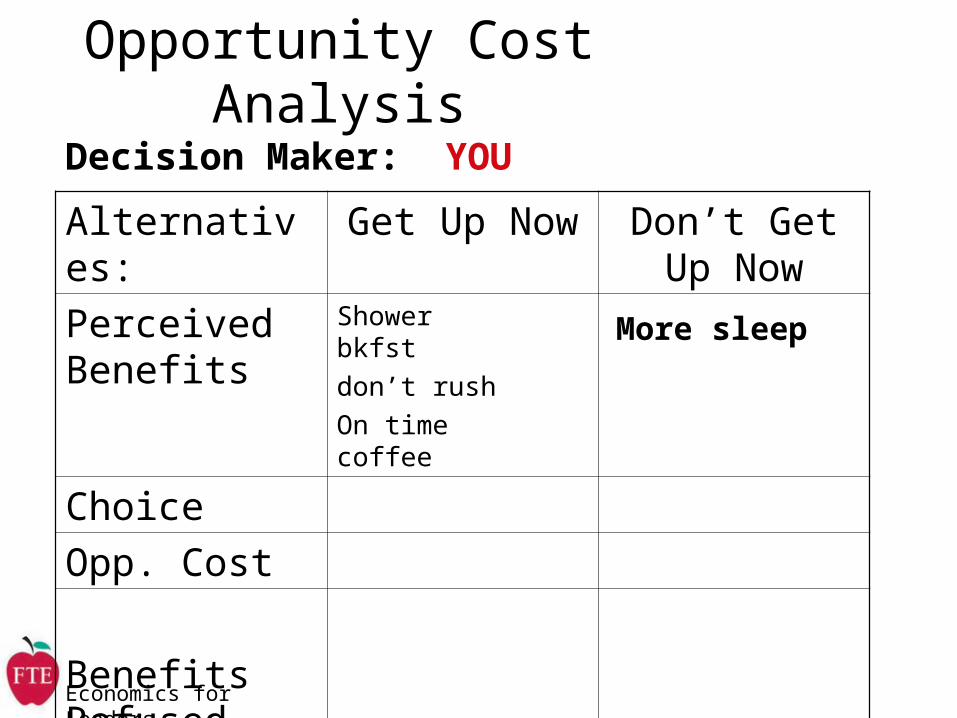

Decision Maker: YOU

Economics for Leaders

Opportunity Cost Analysis

Alternatives: Get Up Now Don’t Get Up Now

Perceived Benefits

Shower bkfst don’t rushOn time coffee

Choice

Opp. Cost

Benefits Refused

Decision Maker: YOU

More sleep

Economics for Leaders

Opportunity Cost Analysis

Alternatives: Get Up Now Don’t Get Up Now

Perceived Benefits

Shower bkfst don’t rushOn time coffee

Choice X

Opp. Cost

Benefits Refused

Decision Maker: YOU

More sleep

X

Economics for Leaders

Choosing is Refusing

Every time we choose we pay a cost.

Economics for Leaders

People’s Choices are always RATIONAL

Rational choice = choosing the alternative that has the greatest excess of benefits over costs.If ALL choices are rational, then the challenge is to understand the decision-maker’s perception of costs and benefits.

Economics for Leaders

Economics for Leaders

Characteristics of Cost

Costs are the results of ACTIONSCosts are TO people; things have no costAll costs lie in the FUTURE (past costs are “sunk” costs)Costs are frequently not monetary (although we may value them in dollar terms)

Economics for Leaders

What Determines YourOpportunity Cost?

AlternativesTastes and preferences (values)Rules of the Game--Institutions

Economics for Leaders

Do Gov’t actions have opportunity costs?

Government DebtEconomic Stimulus PackageWar in IraqLimiting Carbon EmissionsUniversal Healthcare

All alternatives have cost and benefitsIndividuals perceive the value of costs and benefits differently

Economics for Leaders

Should weShould weAllocate?Allocate? ration? ration?

Given that we MUST ration, what is the best mechanism?

Back to Scarcity: What’s the Question? (And what does

opportunity cost have to do with it?)

Economics for Leaders

Allocating/Rationing DVDs

Economics for Leaders

Methods of Rationing Scarce Methods of Rationing Scarce Goods and ServicesGoods and Services

pricesprices

command command (someone decides)(someone decides)

majority rulemajority rule

contestscontests

by forceby force

votingvoting

first-come-first-first-come-first-servedserved

sharing equallysharing equally

lotterylottery

personal personal characteristicscharacteristics

need or meritneed or merit

Economics for Leaders

Why is price rationing the most common method of allocating scarce goods, services, and resources in our economy?

1.1. The outcome is clearThe outcome is clear

2.2. Individuals can affect the outcome based Individuals can affect the outcome based on their desire for the producton their desire for the product

3.3. It directs resources to their most highly It directs resources to their most highly valued usesvalued uses

4.4. Individuals’ power and freedom is Individuals’ power and freedom is enhancedenhanced

5.5. It provides incentives for both consumers It provides incentives for both consumers and producers to reduce scarcity.and producers to reduce scarcity.

Economics for Leaders

Where do Prices Come From?

The market interaction of buyers and sellers in open and competitive markets!

Economics for Leaders

Prices: POWERFUL Incentives

When prices change, opportunity costs change –that’s an incentive!Both consumers and producers react to prices in ways that help us to deal with scarcity.

Economics for Leaders

Economic Reasoning Principle # 3: People respond to incentives in predictable ways.

Choices are influenced by incentives, the rewards that encourage and the punishments that discourage actions. When incentives change, behavior changes in predictable ways.

Economics for Leaders

When incentives (Prices) change, behavior changes in predictable

ways.

When prices go up consumers demand a larger/smaller quantity?

Demand

The willingness and ability to purchase goods and services at various prices.

Economics for Leaders

When incentives (Prices) change, behavior changes in predictable

ways.

When prices go up consumers demand a larger/smaller quantity?

SmallerWhen prices go down consumers demand a larger/smaller quantity?

LargerAlways?Law of Demand P Q

Economics for Leaders

When incentives (Prices) change, behavior changes in predictable

ways.

When prices go up producers supply a larger/smaller quantity?

Supply

Producers willingness and ability to produce goods and services at various prices.

Economics for Leaders

When incentives (Prices) change, behavior changes in predictable

ways.

When prices go up producers supply a larger/smaller quantity?

LargerWhen prices go down producers supply a larger/smaller quantity?

SmallerAlways?Law of Supply P Q

Economics for Leaders

What does Opportunity Cost have to do with supply and demand?

Everything!

Economics for Leaders

Choices are made at the Margin

Our only choice is the next choiceOur only choice is the next choice

Marginal = additional, next, a little Marginal = additional, next, a little more or a little lessmore or a little less

Economics for Leaders

How much should we do?

WorkPlayStudySleepBuySell

Economics for Leaders

As long as the marginal benefit is greater than the marginal cost you should continue the activity

MB=MC

Economics for Leaders

The “Big Ideas” from Lesson 2:

1. Scarcity forces us to choose and every choice has an opportunity cost.

2. When opportunity costs change, incentives change, and choices change.

3. Because costs lie in the future, the important costs and benefits occur at the margin.

4. Money price rations goods in markets.5. Consumers and producers respond to

changes in price in predictable ways.