DMX Technologies Corporate Update - listed...

43

26th August 2008 The Fullerton Hotel, Singapore DMX Technologies Corporate Update

Transcript of DMX Technologies Corporate Update - listed...

26th August 2008

The Fullerton Hotel, Singapore

DMX Technologies

Corporate Update

2

Presentation Outline

DMX Business Segments

Business Realignment

Business Milestones

Financial Track Records

Digital Media

Infrastructure Enabling

Summary

Growth Strategy

Conclusion

Rights Issue

Use of Funds

3

Business Realignment: To Address Changing

Technological and Market Demands

In 2007, the Group realigned into two core businesses – the first intraditional Infrastructure Enabling and the second being Digital Media.

Infrastructure Enabling group comprises Infrastructure Solutions andManaged Services

Digital Media group comprises Digital Media solutions, MultimediaSoftware and New Media Content

Move was undertaken to update DMX!s successful traditional businessmodel in systems integration as well as to ensure DMX!s continuingrelevance to changing technological markets.

Business realignment equips DMX to leverage on growingopportunities in security, digital media market in China thuscreating long term value for customers and shareholders.

4

CATV

Telco

Broadcasters

MobilePortal

Digital

MediaMulti Media

Software

Groups Segments/Solutions

Customers

Digital MediaSolution

New Media

Content

Telco

Enterprises

Mobile

InfrastructureEnabling

InfrastructureSolution

Managed Services

DMX Business Segments

5

Business Milestones to-date 2008

Launch of Managed Service division; Vantage

Vantage secures MSSP deal with leading Chinese logistics player, Anji-TNT

Wins milestone Digital Media deal to develop world’s first IPTV entertainmentsystem for Keppel FELS

Implements first-ever “smartcard-less” Digitisation of Tai’An CATV in PRC

3 major CATV provincial wins - Inner Mongolia, Shaanxi and Hubei provinces

Forging strong strategic technological alliances:

Enhances Digital Media solution to create a non-stop fault tolerant IPTV solutionthrough strategic alliance with Stratus Technologies

Steps up Infrastructure Enabling capability by partnering with Silicon Valley-basedA10 Networks

Vantage enhances Managed Service capabilities with strategic partnership;

becomes Qualys certified reseller

6

Strong Technology Alliances

Infrastructure Enabling Digital Media

Financial Highlights

8

51.7

77.473.8

86.9

77.5

84.0

77.8

10

30

50

70

90

1H05 2H05 1H06 2H06 1H07 2H07 1H08

US$ Millions

1H08 Financial Highlights - Revenue

2H07 Revenue :

Reduced

infrastructure

business in Korea

and China

9

33.842.0

71.0

129.2

160.7 161.6

77.8

10

30

50

70

90

110

130

150

170

FY02 FY03 FY04 FY05 FY06 FY07 FY08 H1

US$ Millions

02-07 CAGR 30%02-07 CAGR 30%

Financial Track Records: Total Revenue

10

6.3

8.7 8.59.3

6.3

3.03.3

0

2

4

6

8

10

12

14

16

18

20

1H05 2H05 1H06 2H06 1H07 2H07 1H08

US$ Millions

1H08 Financial Highlights - Profits After Tax

1H08 Lower PAT:

US$2.7m increasein non operatingexpense ofamortisationand depreciation

11

3.9

5.2

8.9

15.1

17.8

9.3

3.3

0

2

4

6

8

10

12

14

16

18

20

FY02 FY03 FY04 FY05 FY06 FY07 FY08 H1

US$ Millions

02-07 CAGR 16%02-07 CAGR 16%

Financial Track Records: Net Profit after Tax

Lower NPAT in FY07caused by: -

1) Expansion plan inKorea notyielding desiredresults.

2) Additionalinvestments inmarketing andengineeringresources inDigital Media andMulti-MediaSoftware

CAGR before FY07 =36%

12

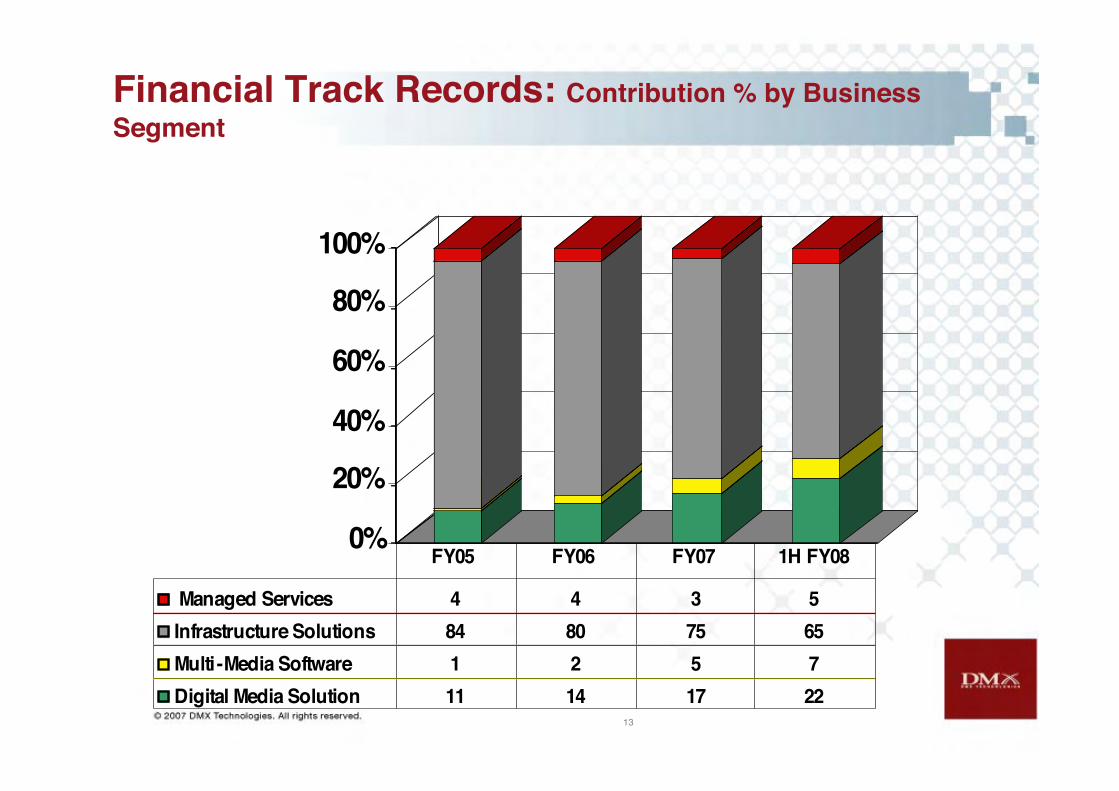

Financial Track Records: Contribution % by

Geography

0

20

40

60

80

100%

China 83 65 75 73 71

Non-China 17 35 25 27 29

FY04 FY05 FY06 FY07 1H FY08

13

Financial Track Records: Contribution % by Business

Segment

0%

20%

40%

60%

80%

100%

Managed Services 4 4 3 5

Infrastructure Solutions 84 80 75 65

Multi-Media Software 1 2 5 7

Digital Media Solution 11 14 17 22

FY05 FY06 FY07 1H FY08

14

Financial Track Records : Balance sheet

177.5172.9164.9101.6Nett Assets (US$ Million)

0.2720.2630.2660.179Nett Tangible Assets Per share(US cents)

0.3850.3750.3580.269Nett Assets Per share (US cents)

1H FY08FY 07FY 06FY 05

Strong Assets Backing

Low Debt Gearing Ratio

6.4%10.4%5.2%5.2%Debt to Equity

1H FY08FY 07FY 06FY 05

Digital Media Solution

Multi-media Software

New Media Content

Digital Media

16

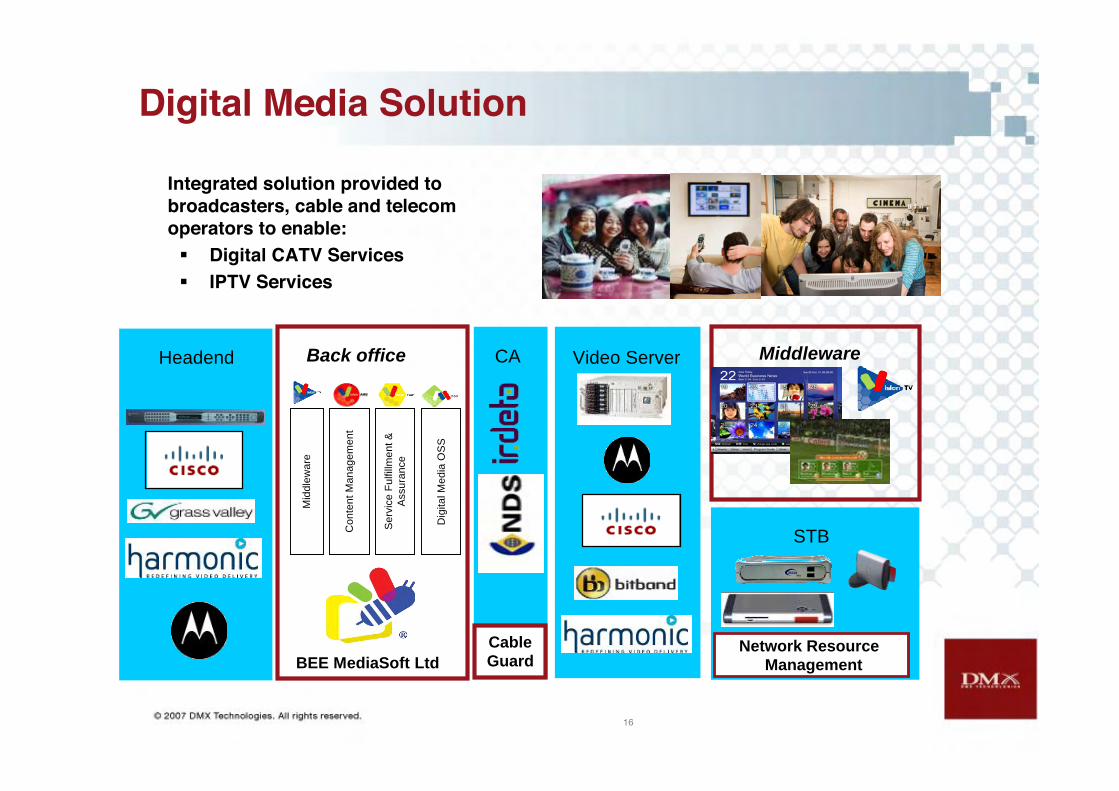

Digital Media Solution

Integrated solution provided to

broadcasters, cable and telecom

operators to enable:

! Digital CATV Services

! IPTV Services

Headend CA Video Server

STB

Mid

dle

wa

re

Co

nte

nt

Ma

na

ge

me

nt

Se

rvic

e F

ulfill

me

nt

&

Assu

ran

ce

Dig

ita

l M

ed

ia O

SS

Back office Middleware

Network Resource ManagementBEE MediaSoft Ltd

CableGuard

17

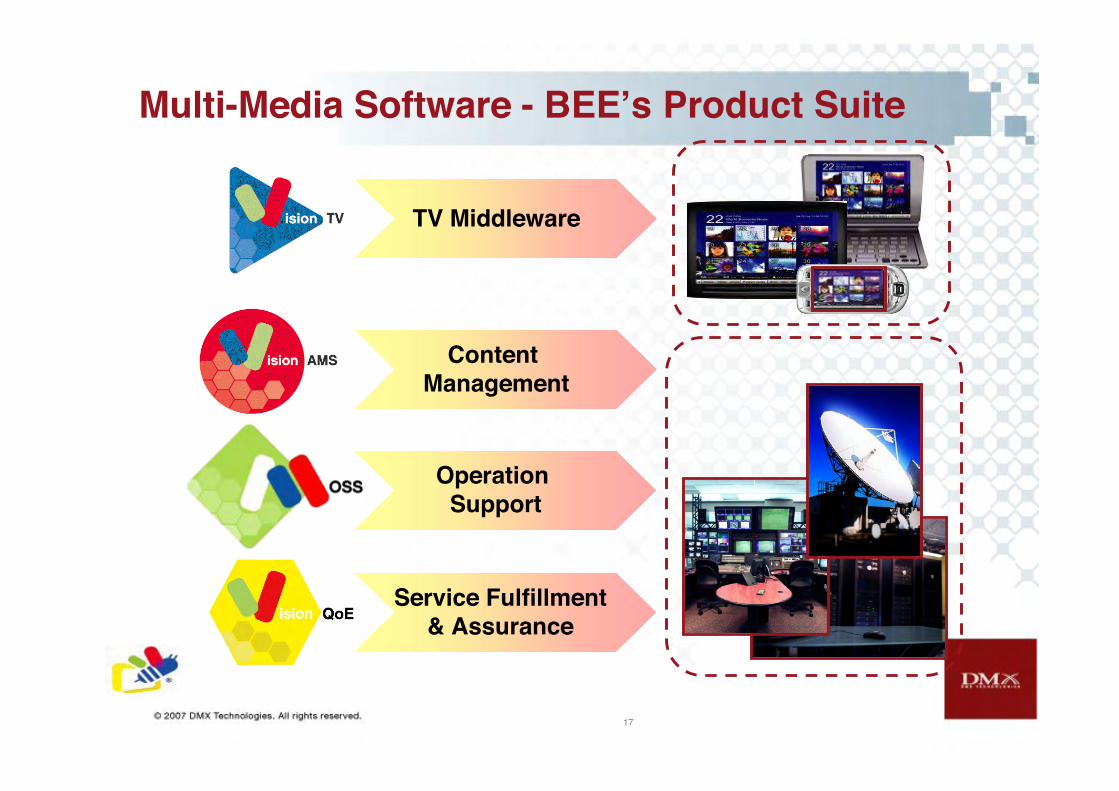

Multi-Media Software - BEE!s Product Suite

TV Middleware

Content

Management

Operation Support

Service Fulfillment

& Assurance

18

Approach to CATV market

IntegratedService

Management

Value AddedServices

Service Portfolio

Multi-stage digitization processMulti-stage digitization process

TV Middleware and

Back office

(Vision TV)

DigitalBroadcasting

• Add!l Service• Add!l Content• Add!l Mgt

Value AddedBusiness

• ISP• DVB-H• TVoD• …

• AdvertisementManagement

• Interactive TV• Databroadcasting

Stable Service Support Infrastructure

Serv

ice

Covera

ge

Cable Guard

& Network

Resource

Management

(NRM)

Customer Care &

Billing (MOSS)

19

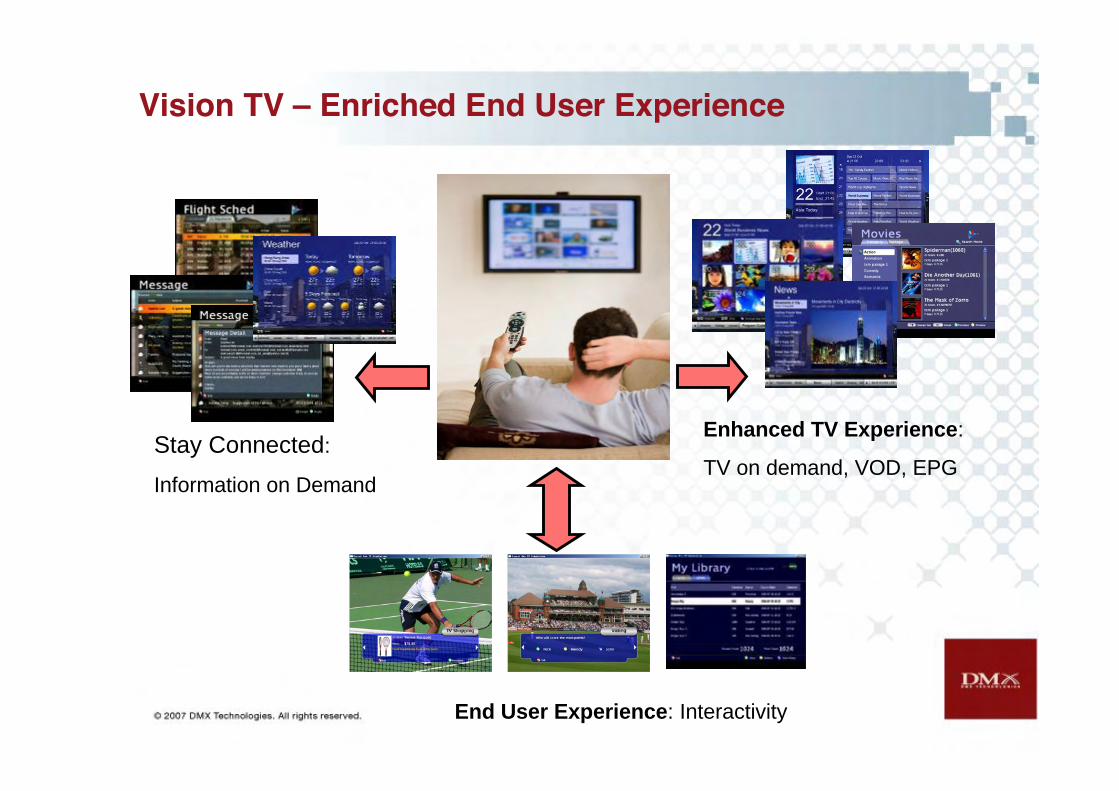

Vision TV – Enriched End User Experience

Enhanced TV Experience:

TV on demand, VOD, EPGStay Connected:

Information on Demand

End User Experience: Interactivity

20

Multi-Media Software - Competitive Advantage

True OPEN platform

Standard based technologies

Best of Breed approach

“Local” implementation capabilities

Beijing Gehua

Inner Mongolia

Shaanxi

Keppel Singapore

25

World’s most advance customer reference

A combination of professional Project Management

and Technologies

Our Digital Media business

World’s largest operators (by subscribers)

World’s first off-shore IPTV entertainment system

Asia’s first and largest smart-cardless CA

deployment

26

New Media Content

Creating a 360° value chain of content offeringacross CATV, Mobile and Internet platforms

27

CATV market in China - VOD Growth

Riding on the back China!s digitisation is demand for new interactiveservices on CATV

Consumers seek more choice and more convenience hence demand forservices like VOD.

The VOD service will offer a major opportunity to deliver much morecontent than traditional broadcast schedules.

In strategic discussions with all major studios to aggregate andredistribute content through it!s CATV partners that are launching VODservices.

28

Infrastructure Enabling

Infrastructure Solution

Managed Services

29

Infrastructure Solution

Infrastructure Solution

Information

Security SolutionNetwork

Integration

Telecom Operators

Enterprise

Broadband Services

Secured Online Business

Triple Play Services

30

Challenges in Infrastructure Solutions Market

Our traditional Infrastructure market has entered intoa mature phase - such as Korea, Hong Kong,Singapore.

Increasing competitive broadband market in China.

" Growth rate slowing to mid-teens.

" China Telcos looking at 3G as next step forward.

" Greater competition from Chinese manufacturers.

31

Opportunities in Infrastructure Solutions Market

Increasing requirements for security solutions.

" Market in APEJ was US$2.9 billion in 2006.

" Forecast 15% per annum growth till 2011; reaching US$5.8billion.

Value added services and application driven to increaseARPU and retain customers.

32

Steps taken in Infrastructure Solutions Market

Streamlined Korea operations" Staff and cost reduction

" Establishing market position in security solutions

Enhance focus on security solutions" Replicate successes within China

Complement Infrastructure Solutions withManaged Services" Established Managed Services Centre

" Work with Telecom operators to provide VAS to their end-users

33

Managed Services

Managed Security Services

! Proactive security devicesmanagement & monitoring

! Security devices performancemanagement & monitoring

! Security policy management! Security Incident handling! Security Scanning! Security Analysis! Review & reporting

Management Services

! Network maintenance &support

! Network performancemanagement

! Network Optimization

34

Opportunities - Managed Services

Drivers for Managed Security Services (MSS)

- Nature, volume and variety of threats on cyberspace

- Concerns over protection of data

- Legal liabilities and compliance with governmental

regulations

- Shortage of skilled security professionals

IDC forecasts MSS market to grow at CAGR of 17.4%

over five years to US$1 billion by 2012.

Summary

36

Growth Strategy

Expanding focus on high growth areas; digital CATV,security solutions and services while continuing thestronghold in Infrastructure Solutions

Creating robust recurring revenue through competitivesoftware and services

Leverage on technology alliances with vendors towiden business and geographical coverage

37

Robust Revenue Model

Recurring,

Scalable

Business

Model

1. P

roje

ct

2. Recurring

3. Upgrades

1. Projects

Traditional IT System Integration

Expansion

2. Recurring Revenues

Software Licensing

Subscriber Based Fees

Management Services

Managed Security Services

3. Upgrades

Back Office System Enhancement

Software Upgrades andmaintenance

38

Growth in multi-dimensions …

Customer

Equipment Vendors

Distributors

DMX Integration

Total Solution & Services Provider

Customer

TechnologyProvisioning

TechnologyAlliance

Coverage

Custo

mer

Penetr

ation

Rights Issue

40

Cash Flows Summary

Investments: Acquisitions -a) Lotun (FY04) – China Mobile and enterprise customersb) Packet Systems Group (FY05) – Geographical expansion

Capital Expenditure: Software Development -a) transform business model - project based to recurring basedb) tap on new business opportunities

US$M 1H08 1H07 FY07 FY06 FY05

Beginning Balance 40.0 45.6

45.6 23.8 32.9

Operating activities (0.8) (12.8) 9.4 (1.3) 3.1

Capex/Investments (7.1) (8.6) (22.1) (25.6) (14.7)

Financing activities (6.5) 5.6 6.2 47.4 2.4

Closing 26.4 30.1 40.0 45.6 23.8

41

Transaction Overview: Funding Requirements

Uses Investment Commentary

Development of DigitalMedia Group S$ 15mm

Digital media plays an important role in the transforming ofthe revenue model over the next 1-2 years.Continuous development of software to stay ahead andexpansion of the business to take advantage of currentopportunities.

Extend participation in digital media market. Tap onoperators to reach their consumers through end to endsolution and services offerings. Seek partners with expertisein content and advertising space.

Acquisition / JointVentures

S$ 15mm

S$ balanceWorking Capital

42

In Conclusion

Our business realignment is showing results –

Our Digital Media group is increasing momentum since late 2007to date with prominent customer wins, entry into new mediacontent, and strategic alliances

Our Managed Service business is also taking off with strategicalliances and prominent customer wins

The funds raised in the Rights Issue will accelerate the growthand maximise the opportunities for Digital Media

Thank you