Diverted Profits Tax the UK experience - Allen & Overy Slides.pdf · Diverted Profits Tax ......

27

© Allen & Overy 2016 Diverted Profits Tax – the UK experience Lydia Challen / Mark Middleditch / Ka Sen Wong Thursday 15 September 2016

Transcript of Diverted Profits Tax the UK experience - Allen & Overy Slides.pdf · Diverted Profits Tax ......

© Allen & Overy 2016

Diverted Profits Tax – the UK

experience Lydia Challen / Mark Middleditch / Ka Sen Wong

Thursday 15 September 2016

© Allen & Overy 2016

UK diverted profits tax (DPT or “Google” tax)

“ some of the largest companies in

the world, including those in the

tech sector, use elaborate

structures to avoid paying taxes

Chancellor of the Exchequer

”

“ contrived arrangements used to

shift profits away from the UK

Chief Secretary to the Treasury

” “ complex structures that

circumvent the international tax

rules on permanent establishment

and transfer pricing

Chief Secretary to the Treasury

”

“ a 25% tax on profits generated by

multinationals from economic

activity here in the UK which they

then artificially shift out of the

country

Chancellor of the Exchequer

”

© Allen & Overy 2016 3

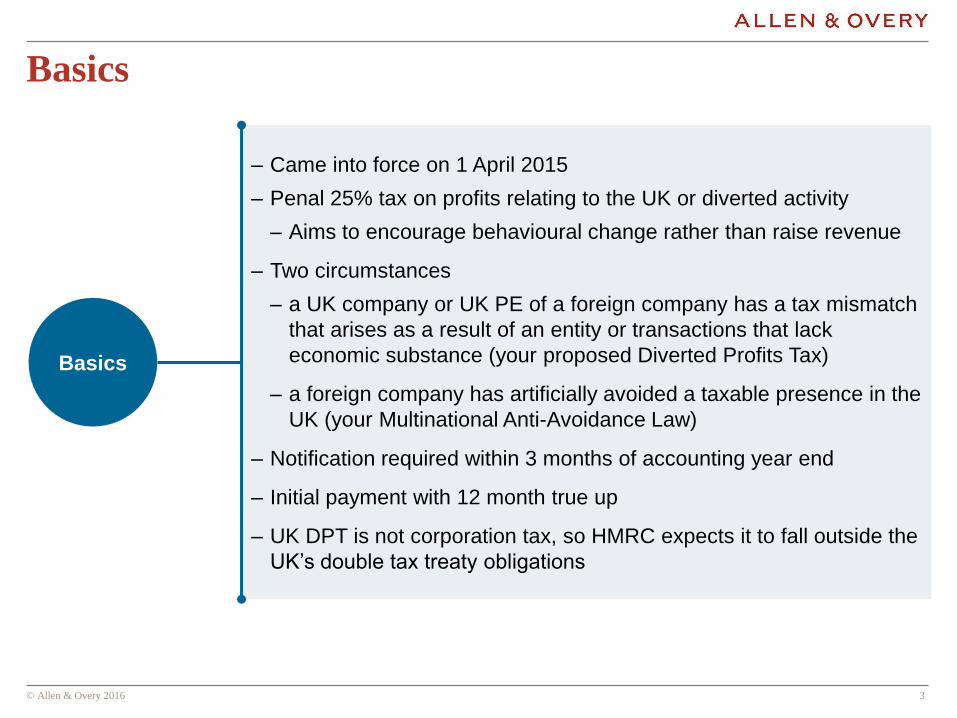

Basics

Basics

– Came into force on 1 April 2015

– Penal 25% tax on profits relating to the UK or diverted activity

– Aims to encourage behavioural change rather than raise revenue

– Two circumstances

– a UK company or UK PE of a foreign company has a tax mismatch

that arises as a result of an entity or transactions that lack

economic substance (your proposed Diverted Profits Tax)

– a foreign company has artificially avoided a taxable presence in the

UK (your Multinational Anti-Avoidance Law)

– Notification required within 3 months of accounting year end

– Initial payment with 12 month true up

– UK DPT is not corporation tax, so HMRC expects it to fall outside the

UK’s double tax treaty obligations

© Allen & Overy 2016 4

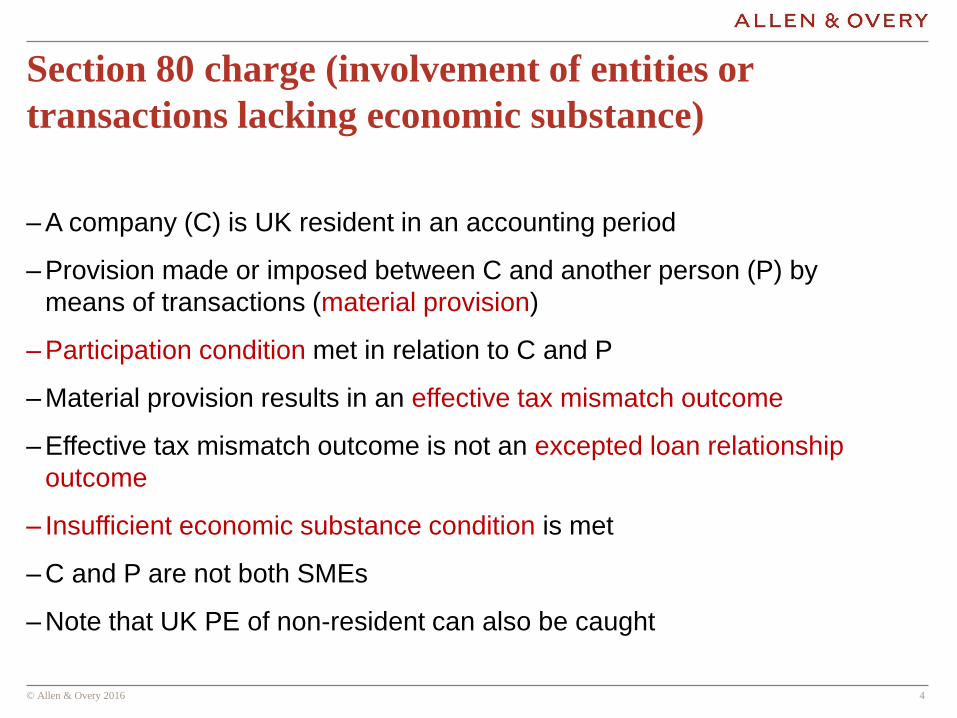

Section 80 charge (involvement of entities or

transactions lacking economic substance)

– A company (C) is UK resident in an accounting period

– Provision made or imposed between C and another person (P) by

means of transactions (material provision)

– Participation condition met in relation to C and P

– Material provision results in an effective tax mismatch outcome

– Effective tax mismatch outcome is not an excepted loan relationship

outcome

– Insufficient economic substance condition is met

– C and P are not both SMEs

– Note that UK PE of non-resident can also be caught

© Allen & Overy 2016 5

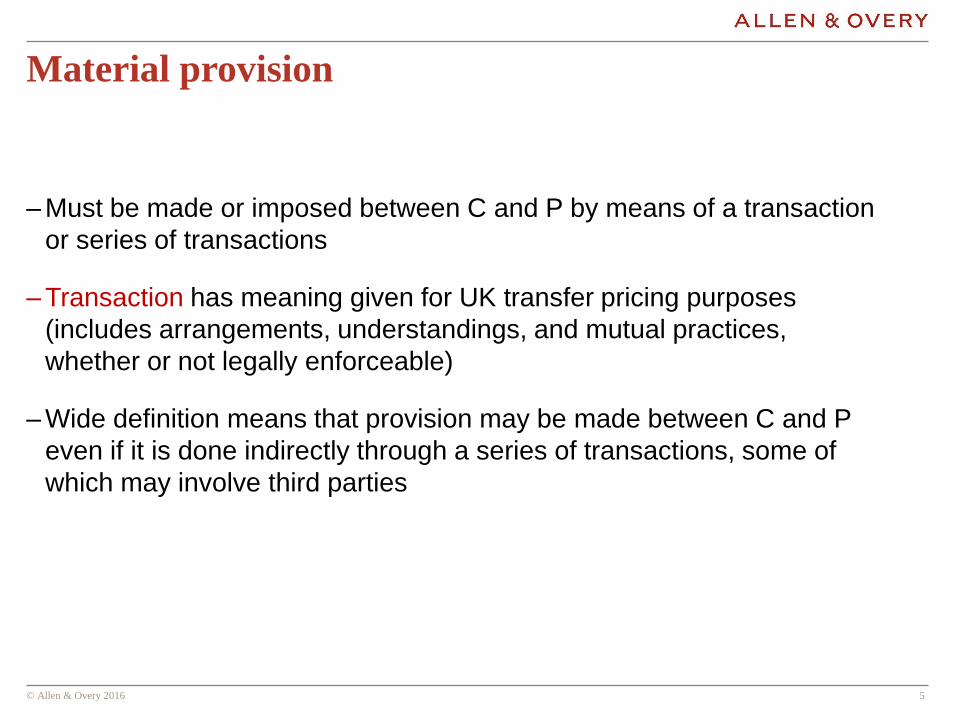

Material provision

– Must be made or imposed between C and P by means of a transaction

or series of transactions

– Transaction has meaning given for UK transfer pricing purposes

(includes arrangements, understandings, and mutual practices,

whether or not legally enforceable)

– Wide definition means that provision may be made between C and P

even if it is done indirectly through a series of transactions, some of

which may involve third parties

© Allen & Overy 2016 6

Participation condition

– Very broad based on UK transfer pricing rules

– Applied when material provision is made (except where it relates to

financing arrangements, when can look forward 6 months).

– Direct and indirect participation (control test)

– Control is the ability to secure that the company’s affairs are

conducted in accordance with your wishes through the possession

of shares or voting power, or by reason of powers conferred by the

articles of association or another document regulating the company

– Extensive attribution rules

– Also catches “major participants” – one of two 40% holders

© Allen & Overy 2016 7

Effective tax mismatch outcome

– relevant tax = UK income and corporation tax and non-UK tax on

income

– material provision results in deductible expenses of C, or reduction

in C’s taxable income

– reduction in C’s relevant tax liability exceeds resulting increase in

relevant taxes payable by P

– this result is not specifically exempted (charities, pension schemes,

sovereign immunity, certain widely held funds)

– P does not meet 80% test:

𝑖𝑛𝑐𝑟𝑒𝑎𝑠𝑒 𝑖𝑛 𝑃′𝑠 𝑡𝑎𝑥 𝑙𝑖𝑎𝑏𝑖𝑙𝑖𝑡𝑦 < 80% 𝑟𝑒𝑑𝑢𝑐𝑡𝑖𝑜𝑛 𝑖𝑛 𝐶′𝑠 𝑡𝑎𝑥 𝑙𝑖𝑎𝑏𝑖𝑙𝑖𝑡𝑦

– Doesn’t matter what causes the mismatch

© Allen & Overy 2016 8

Example

Shareholders

TopCo

CP

Royalty 100m

income

Country X

Country Y UK

Arrangements:

• C in UK, P in country Y

• C pays 100m royalty payment to P

Tax treatment:

• Royalty deductible for C at 20% (20m)

• Withholding tax of 5% (5m) under

relevant tax treaty

• No corporate taxes in country Y

Tax mismatch:

‒ Reduction in C’s liability of 20m

‒ Increase in P’s liability of 5m

‒ 5m < 80% * 20m

Effective tax mismatch outcome

© Allen & Overy 2016 9 9

Excepted loan relationship outcome

‒ An effective tax mismatch outcome is an excepted loan relationship

outcome if it arises wholly from

– anything that would produce debits or credits under the UK loan

relationship regime (for corporate debt) or

– a loan relationship and a derivative contract entered into entirely as a

hedge of risk in connection with the loan relationship

© Allen & Overy 2016 10

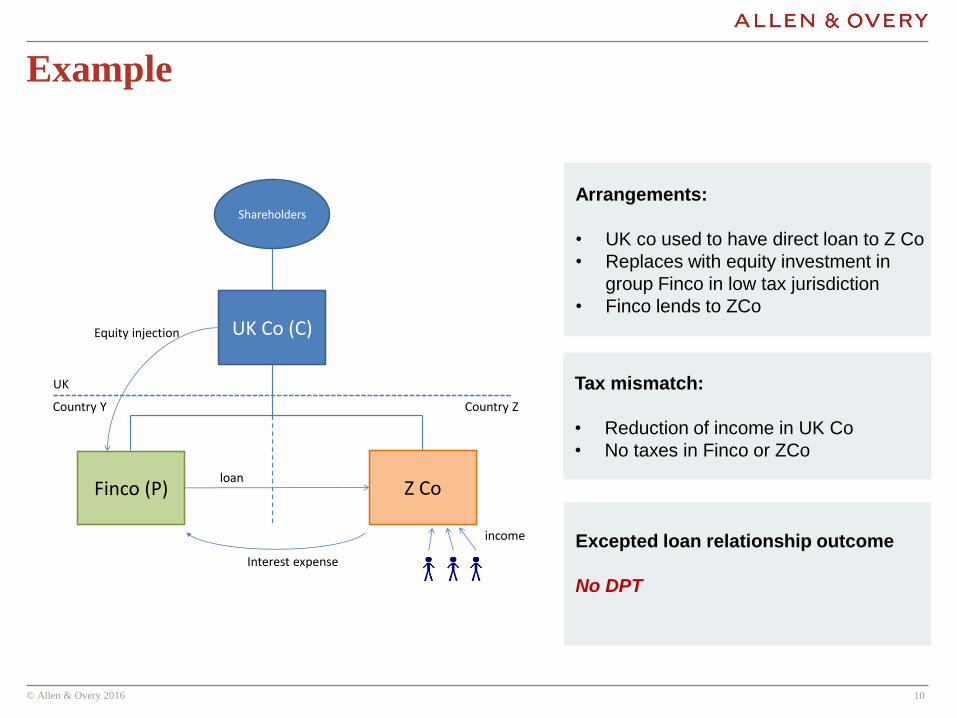

Example

Shareholders

UK Co (C)

Z CoFinco (P)

Interest expense

income

UK

Country Y Country Z

Equity injection

loan

Arrangements:

• UK co used to have direct loan to Z Co

• Replaces with equity investment in

group Finco in low tax jurisdiction

• Finco lends to ZCo

Tax mismatch:

• Reduction of income in UK Co

• No taxes in Finco or ZCo

Excepted loan relationship outcome

No DPT

© Allen & Overy 2016 11

Insufficient economic substance condition

– DPT applies to arrangements that lack economic substance and are

designed to reduce tax

– To be designed

– there must be some degree of contrivance

– arrangements must differ in some material way to those that would

have been made but for the opportunity to achieve the tax reduction

– Lacking economic substance

– Compare non-tax benefits of transaction(s)/activities of P’s staff with

the financial benefit of the tax reduction

– Compare income generated by activities of P’s staff with other

income from the transaction(s)

– Condition is met if any of three tests are satisfied: transaction based

tests and entity based test

© Allen & Overy 2016 12

Transaction(s) based tests

– Test one: If the tax mismatch is referable to a single transaction

– is it reasonable to assume that the transaction was designed to

secure the tax reduction ?

– have regard to all of the circumstances (including any additional

tax)

– If so you are caught unless non-tax financial (commercial) benefit

greater than financial benefit of tax reduction

– test applied when material provision is made

– look at all periods when the transaction is in place, and position

of first and second party together

– Test two: Same test for tax mismatch that is referable to multiple

transactions

© Allen & Overy 2016 13

Entity based test

– Test three: If a person is a party to the transaction(s)

– is it reasonable to assume that the person’s involvement in the

transaction(s) was designed to secure the tax reduction ?

– have regard to all of the circumstances (including any additional

tax)

– If so you are caught unless

– reasonable to assume non-tax benefits of people functions exceed

financial benefit of tax reduction taking into account

– All accounting periods for which transaction has effect

– Position of first and second party taken together

OR

– in respect of the period, greater part of the person’s income in

relation to the transaction is attributable to on-going people functions

(but ignore holding, maintaining or legal protection of assets)

© Allen & Overy 2016 14 14

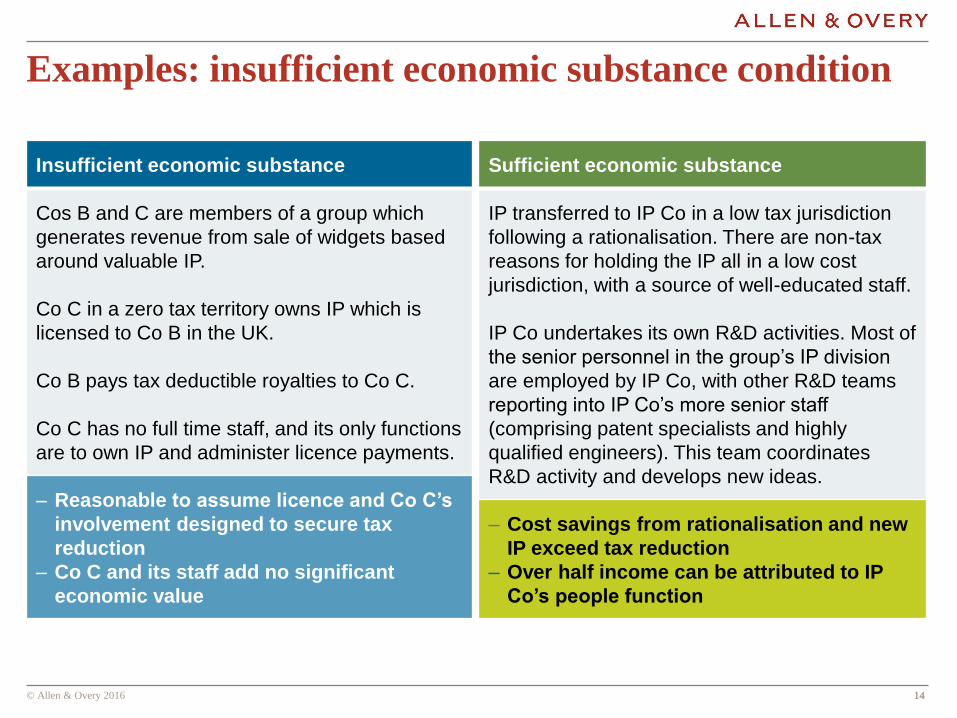

Examples: insufficient economic substance condition

Insufficient economic substance

Cos B and C are members of a group which

generates revenue from sale of widgets based

around valuable IP.

Co C in a zero tax territory owns IP which is

licensed to Co B in the UK.

Co B pays tax deductible royalties to Co C.

Co C has no full time staff, and its only functions

are to own IP and administer licence payments.

– Reasonable to assume licence and Co C’s

involvement designed to secure tax

reduction

– Co C and its staff add no significant

economic value

Sufficient economic substance

IP transferred to IP Co in a low tax jurisdiction

following a rationalisation. There are non-tax

reasons for holding the IP all in a low cost

jurisdiction, with a source of well-educated staff.

IP Co undertakes its own R&D activities. Most of

the senior personnel in the group’s IP division

are employed by IP Co, with other R&D teams

reporting into IP Co’s more senior staff

(comprising patent specialists and highly

qualified engineers). This team coordinates

R&D activity and develops new ideas.

– Cost savings from rationalisation and new

IP exceed tax reduction

– Over half income can be attributed to IP

Co’s people function

© Allen & Overy 2016 15

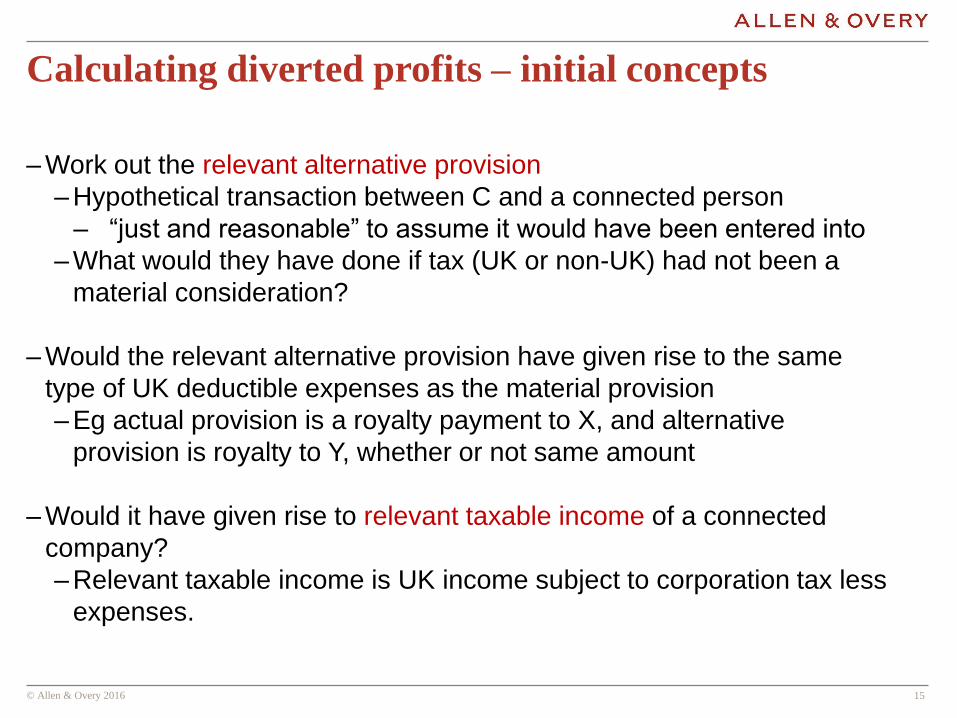

Calculating diverted profits – initial concepts

– Work out the relevant alternative provision

– Hypothetical transaction between C and a connected person

– “just and reasonable” to assume it would have been entered into

– What would they have done if tax (UK or non-UK) had not been a

material consideration?

– Would the relevant alternative provision have given rise to the same

type of UK deductible expenses as the material provision

– Eg actual provision is a royalty payment to X, and alternative

provision is royalty to Y, whether or not same amount

– Would it have given rise to relevant taxable income of a connected

company?

– Relevant taxable income is UK income subject to corporation tax less

expenses.

© Allen & Overy 2016 16

Calculating diverted profits - repricing

Where the hypothetical provision gives rise to the same type of

expenses as the actual provision:

– Any relevant taxable income PLUS

– Amount of any transfer pricing adjustment that would be made in

respect of the material provision

– UNLESS the amount of the adjustment is reflected in C’s

corporation tax return prior to the end of the review period (1 year

plus 30 days after a charging notice is served)

Incentive for taxpayer to agree HMRC’s transfer pricing analysis within

the review period to avoid charge

© Allen & Overy 2016 17 17

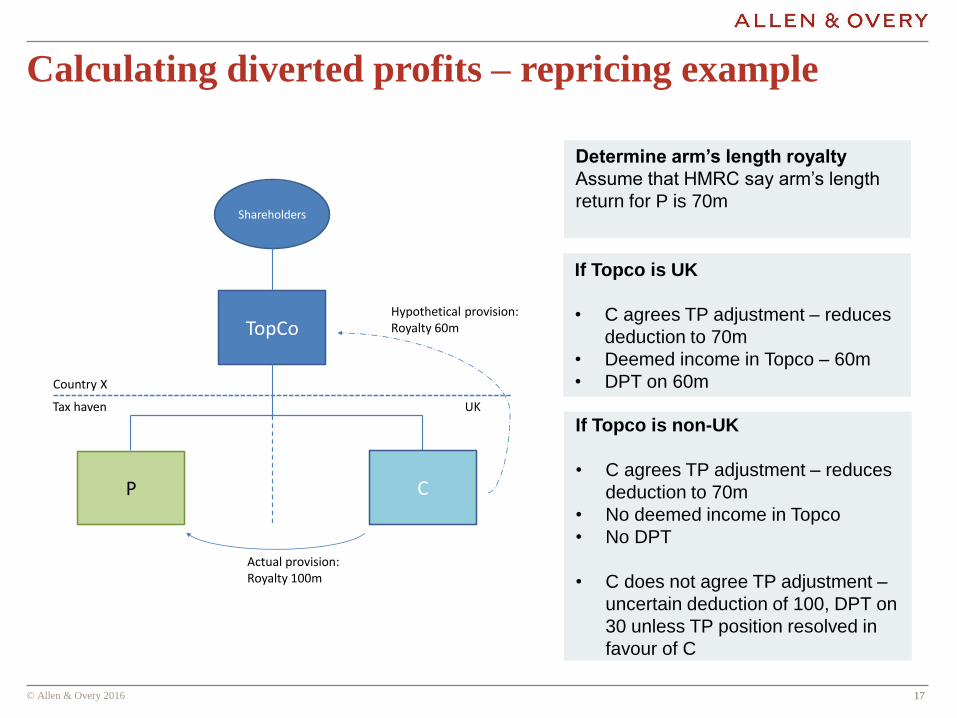

Calculating diverted profits – repricing example

Shareholders

TopCo

CP

Royalty 100m

income

Country X

Country Y UK

Shareholders

TopCo

P

Actual provision: Royalty 100m

Country X

Tax haven UK

C

Hypothetical provision: Royalty 60m

Determine arm’s length royalty

Assume that HMRC say arm’s length

return for P is 70m

If Topco is UK

• C agrees TP adjustment – reduces

deduction to 70m

• Deemed income in Topco – 60m

• DPT on 60m

If Topco is non-UK

• C agrees TP adjustment – reduces

deduction to 70m

• No deemed income in Topco

• No DPT

• C does not agree TP adjustment –

uncertain deduction of 100, DPT on

30 unless TP position resolved in

favour of C

© Allen & Overy 2016 18

Calculating diverted profits (3) - recharacterisation

Where the hypothetical provision does not give rise to the same type of

expenses as the actual provision:

– Any relevant taxable income that would have arisen from the

hypothetical provision PLUS

– Amount to which C would have been chargeable to corporation tax

had the hypothetical provision been imposed MINUS

– The amount of any transfer pricing adjustment that would be made in

respect of the material provision AND is reflected in C’s corporation tax

return before the end of the review period.

© Allen & Overy 2016 19 19

Calculating diverted profits – recharacterisation

example

Shareholders

TopCo

CP

Royalty 100m

income

Country X

Country Y UK

Shareholders

TopCo

P

Actual provision: Royalty 100m

Country X

Tax haven UK

C

Hypothetical provision: C holds the IP itself – no royalty

Determine arm’s length royalty

Assume that HMRC say arm’s length

return for P is 70m

C agrees TP adjustment

• Reduces deduction to 70m

• No deemed income

• Hypothetical provision involves no

deduction at all

• DPT on 70 (ie 100 minus TP

adjustment of 30)

C does not agree TP adjustment

• Deduction of 70/100 depending on

ultimate TP position

• No deemed income

• DPT on 100 unless/until TP position

resolved in favour of C

© Allen & Overy 2016 20 20

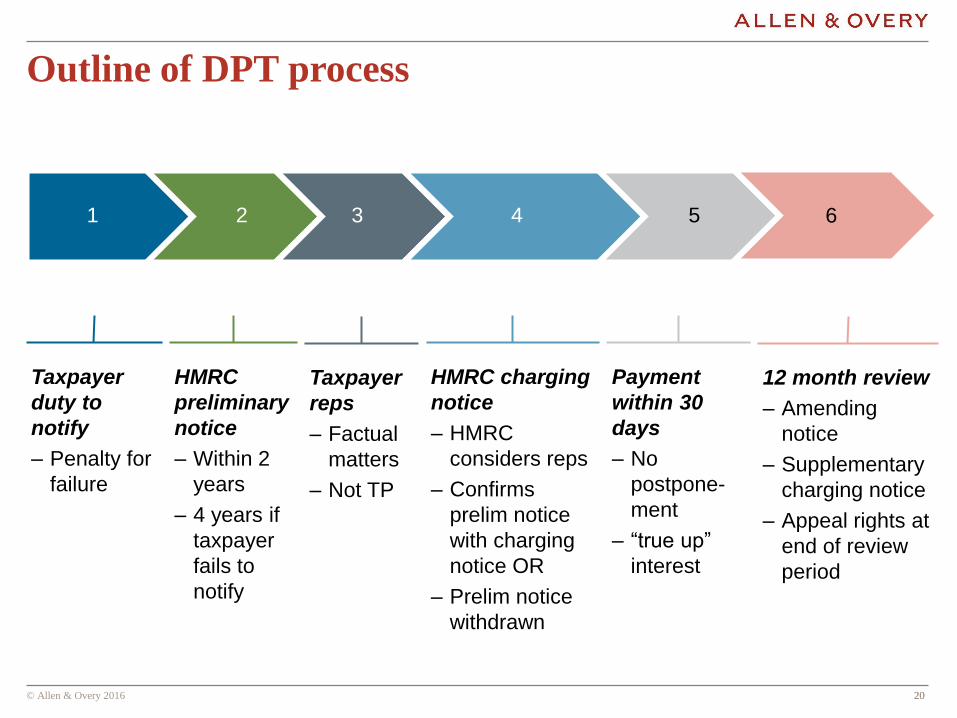

Outline of DPT process

1 2 3 4 5

Taxpayer

duty to

notify

– Penalty for

failure

Payment

within 30

days

– No

postpone-

ment

– “true up”

interest

HMRC charging

notice

– HMRC

considers reps

– Confirms

prelim notice

with charging

notice OR

– Prelim notice

withdrawn

Taxpayer

reps

– Factual

matters

– Not TP

HMRC

preliminary

notice

– Within 2

years

– 4 years if

taxpayer

fails to

notify

6

12 month review

– Amending

notice

– Supplementary

charging notice

– Appeal rights at

end of review

period

© Allen & Overy 2016 21 21

Estimating profits for notices

‒ Preliminary and charging notices contain an estimate of diverted profits

‒ Best judgment estimate

‒ inflated expenses condition (upfront 30% disallowance of deductions)

– material provision results in deductible expenses for CT purposes

– expenses responsible for effective tax mismatch outcome

– HMRC considers that expenses are not arm’s length

© Allen & Overy 2016 22 22

Differences between UK DPT and Australian

proposals

1 UK has no de minimis threshold (cf £10m threshold for avoided PE)

2 UK rules are not confined to cross-border transactions

3 UK has transaction(s) and entity (people function) tests for insufficient

economic substance

4 UK allows credit for foreign tax paid on diverted profits

5 Australian proposal has no exception for corporate debt

6 Australian proposal has no duty on taxpayer to notify

7 Different time periods for notices, payment, and representations

8 Rates: 25/20 vs 40/30

9 Diverted profits computations ?

© Allen & Overy 2016 23 23

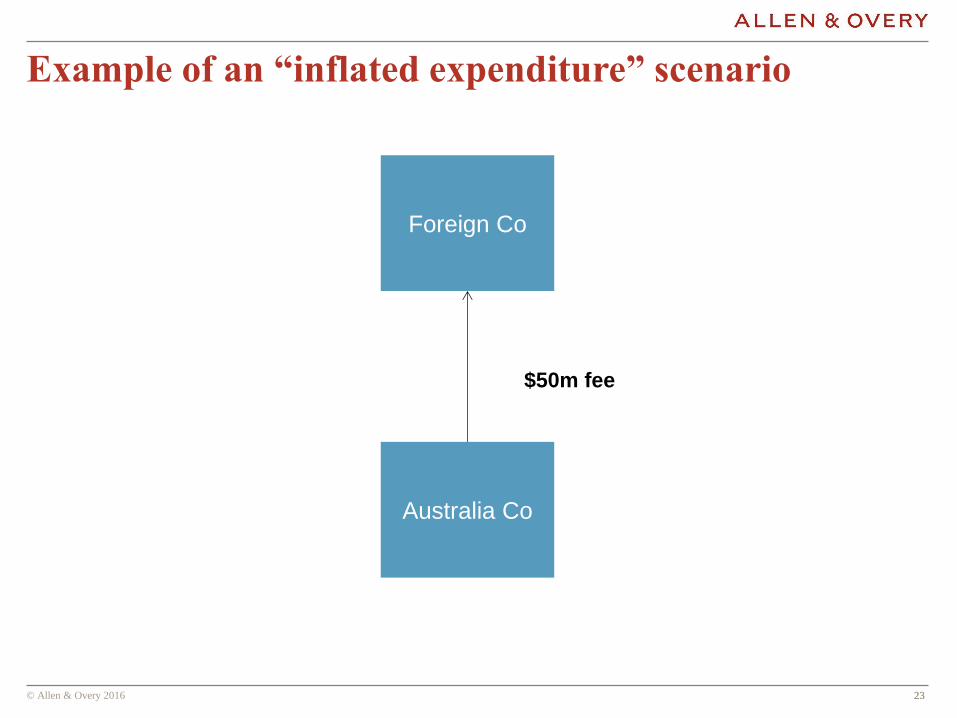

Example of an “inflated expenditure” scenario

Foreign Co

Australia Co

$50m fee

© Allen & Overy 2016 24 24

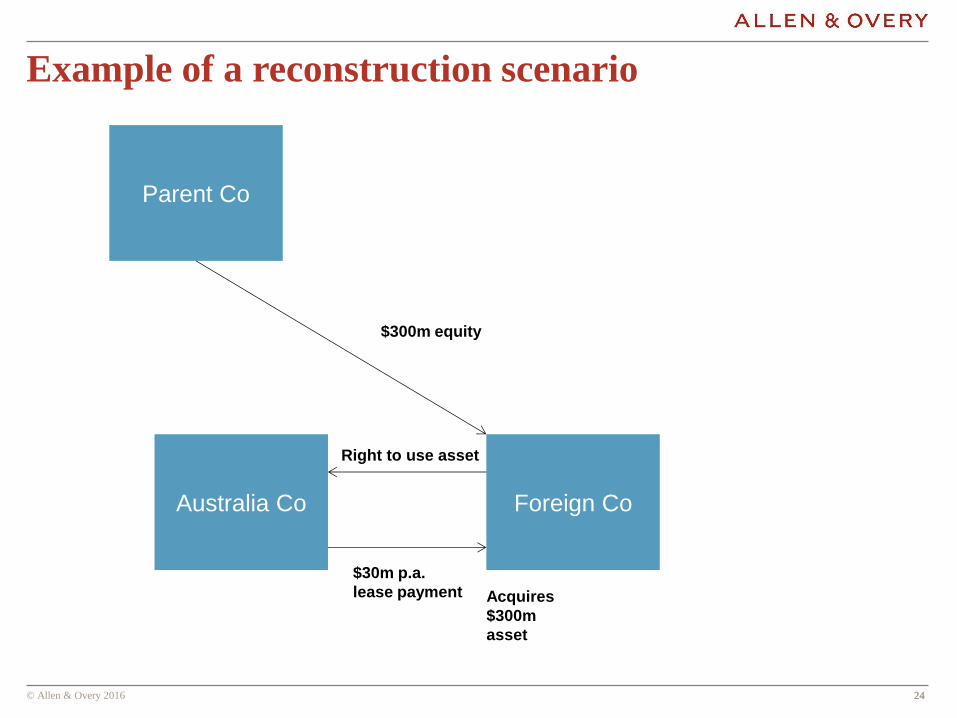

Example of a reconstruction scenario

Parent Co

Australia Co Foreign Co

$300m equity

Right to use asset

$30m p.a.

lease payment Acquires

$300m

asset

© Allen & Overy 2016 25 25

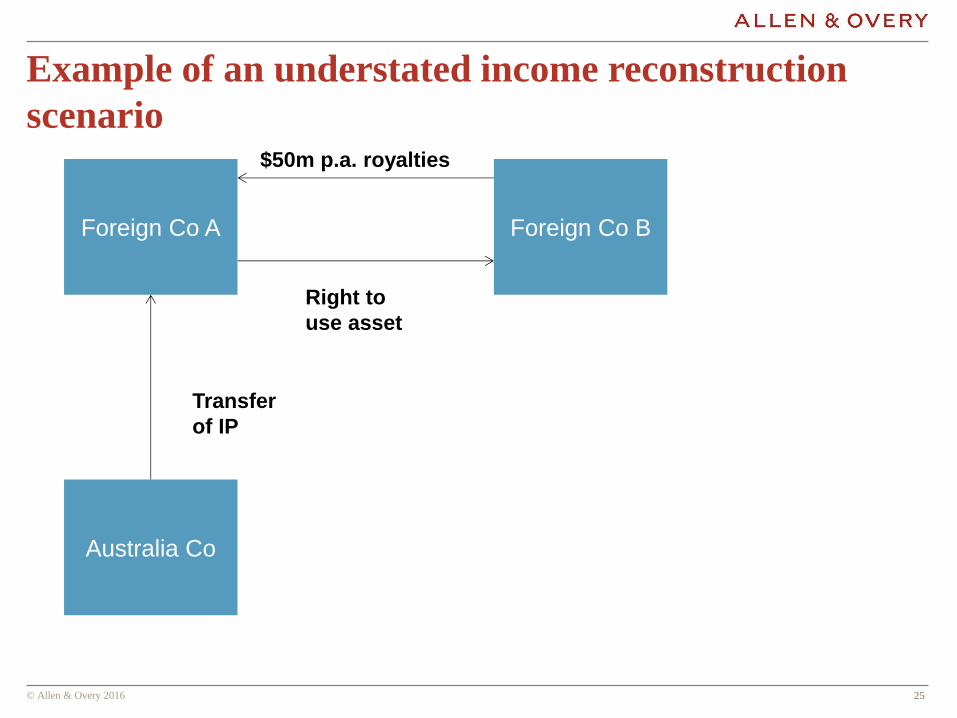

Example of an understated income reconstruction

scenario

Foreign Co A

Australia Co

Foreign Co B

Transfer

of IP

$50m p.a. royalties

Right to

use asset

© Allen & Overy 2016 26 26

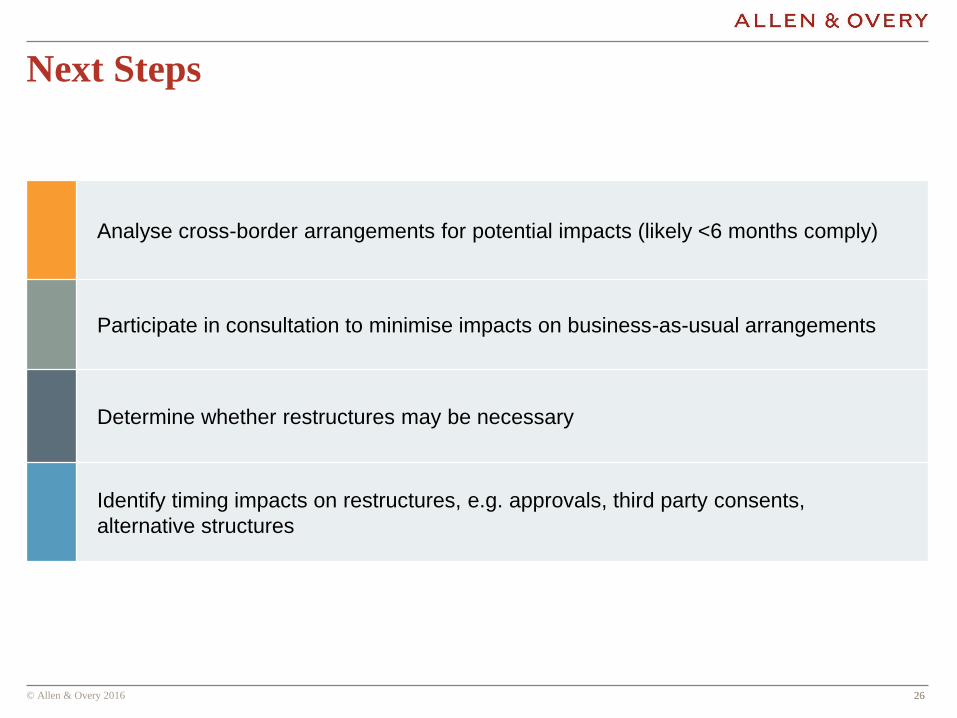

Next Steps

Analyse cross-border arrangements for potential impacts (likely <6 months comply)

Participate in consultation to minimise impacts on business-as-usual arrangements

Determine whether restructures may be necessary

Identify timing impacts on restructures, e.g. approvals, third party consents,

alternative structures

© Allen & Overy 2016 27 27

Questions?

These are presentation slides only. The information within these slides does not

constitute definitive advice and should not be used as the basis for giving definitive

advice without checking the primary sources.

Allen & Overy means Allen & Overy LLP and/or its affiliated undertakings. The term

partner is used to refer to a member of Allen & Overy LLP or an employee or consultant

with equivalent standing and qualifications or an individual with equivalent status in one

of Allen & Overy LLP’s affiliated undertakings.