Digital SMBs: Powering India into the future -...

40

Digital SMBs Powering India into the Future… – January 2015

Transcript of Digital SMBs: Powering India into the future -...

Digital SMBs Powering India into the Future…

– January 2015

Conceptualizing a ‘Digital SMB’…

2

‘Digital’ SMB: An SMB leveraging digital technologies across business processes thus driving top line growth, maximizing output

and deriving cost efficiencies

A modern ‘Digital SMB’ is powered by solutions touching multiple business levers

Operational

Excellence

Risk

Management

Workforce

Enablement

Customer

Acquisition

SMB

2.

4. 3.

1.

Hg

Compared to enterprises, SMBs adopt digital technologies differently

Digital solutions for SMBs need to reflect 5 key characteristics

Op-ex model with immediate payback

Cap-ex heavy solutions 1

Mobile First solutions Requirement of large IT infrastructure

2

Micro-vertical specific solutions Generic enterprise solutions lacking vertical centricity

3

Enable end-to-end workflow Multiple functional solutions addressing specific workloads

4

Prioritization of ease over features Complex, feature rich solutions with high learning curve

5

SMBs face multiple challenges while adopting solutions typically meant for

enterprises

Successful Digital SMB Solutions impact multiple business levers and enable end-to-end workflow

Discovery platform; Appointment Booking; Practice Management

Access to passengers; Automated Payment;

Vehicle Tracking

Connecting with potential tourists; Booking and

schedule management

Source – Zinnov Primary Research and Analysis

Zinnov leveraged insights gathered from 5000+ SMBs over the last year to assess the digital

opportunity

3

Which SMBs to

target?

12 Mn SMBs with high

degree of tech influence

Why talk about

them now?

Nexus of enablers driving SMBs to go

digital

What solutions do

they need?

Solutions addressing strategic business

challenges

How big is the

opportunity?

USD 26 Bn of opportunity across

solutions in 2020

How to tap the

opportunity?

Interventions across product, business

model and outreach

What is the

impact?

By 2020, impact of USD 1 Tr on GDP; 126 mn on employment

A B C D E F

Understanding the Digital SMB Opportunity

Source – Zinnov Analysis

India houses a massive base of tech influenced SMBs across

verticals

4

Which SMBs to

target?

116 Mn

GDP

Contribution Total

Exports

Total

Employment

Collective contribution of India’s SMBs

51 Mn strong SMB base in India

Micro Enterprises (<10 employees)

96.3%

Small Enterprises (10-100 employees)

3.4%

Medium Enterprises (100-1000 employees)

0.3%

Segmentation of Indian SMBs – by Size

Distribution of Tech-

influenced SMBs across

top 8 verticals

18%

Retail

19%

Professional Services

4%

Auto & Auto Ancillaries

8%

Real Estate

9%

Education

10%

Restaurants & Hospitality

14%

Travel & Logistics

14%

Manufacturing

38% 40%

A

Distribution of SMBs by level of tech influence

‘Tech Influenced’ SMBs: 40% 2015

~90% 2020

L4: 5 Mn

L3: 12 Mn

L2: 14 Mn

L1: 20 Mn

L1: Access to digital

infrastructure Devices/connectivity

L2: Use of consumer

centric services Such as messaging, email

etc.

L4: Business workflow

productivity tools Business centric solutions and services

L3: Digital discoverability

of businesses Company Websites, business

listings, etc.

Source –MSME, Press Articles, Zinnov Analysis

Nexus of 3 enablers are increasingly driving SMBs towards

digital enablement

5

Why talk about

them now?

Access to Enabling Infrastructure Availability of Solutions & Services

Push from Customers &

Ecosystem Stakeholders

Exploding smartphone usage

Availability of low

price devices

Smartphones & tablets

available for as low as

$40-80

Easy access to internet

Internet adoption

in SMBs to grow

exponentially

<10 Mn Users

2014

>30 Mn Users

2020

2X increase in average internet

speed in 3 years

>70% price reduction in average 3G mobile

access prices over last 3 years; internet

access expected to become free

Enterprise grade solutions becoming

affordable

Basic versions available for

free access Google Apps

SMBs realizing benefits of Cloud enablement

of solutions

50% reduction in ownership cost and deployment time

70-75% cost saving with advantages like scalability, set-

up time, etc.

Mobile app ecosystem thriving

Mobile app downloads

in India to increase

100 Mn Monthly app downloads

2014

400 Mn Monthly app downloads

2020

Easy Mobile App

development <3 hours Required to build a

functional app

9,000+ Indian Mobile app development

companies

Consumers spending more time on

the internet

140 Mn Hours

2014

1500 Mn Hours

2020

Internet aiding customer

purchases Growing use of digital

medium by SMBs

1,125 Million searches by

consumer in FY 2014

Ecosystem stakeholders and government

initiatives aiding SMBs

50,000+ SMB sellers on-

boarded by top 3 e-commerce

players

Flipkart, Snapdeal offering

easy access to loans for SMBs

through partners

Easy access to loans Enabling SMBs to sell online

Digital India Initiative

<10 Mn Users

2014

Near universal

adoption 2020

High adoption levels

Better &

affordable

services

‘Digital India’ campaign will likely propel

Indian govt. spending on IT to $7.2 Bn by

2015

5,000 business tenders

added everyday

B

Source –Akamai, BCG Report, Ericsson Market Insights, Avendus Mobile Internet Report, Flipkart Market Insights, Digital India Insights, Zinnov Analysis

Pockets of innovations disrupting four key business SMB

business levers

6

What solutions

do they need?

IOT

Mobility

Analytics

Cloud

Digital SMBs Social

Customer Targeting and Engagement

Operational Excellence and SCM

Workforce Enablement

Risk Management

Discoverability and Reach

Managing Customer Relationships

Customer Intelligence

Optimizing Sales Motions

New Sales Channels

Ensuring Efficiency in Operations

Optimal Resource Utilization

Customer Experience Enhancement

Optimization of Inventory and Logistics

Partner Identification and Visibility

1

2

3

4

5

Talent Sourcing

Productivity Enhancement

Skilling

1

2

3

Data security

Counterfeit protection

Physical security of assets and resources

Safeguarding against financial risks

1

2

3

4

1

2

3

4

5

CRM on Mobile

SMS-based Website Creation and Management

Missed Call Marketing

Online Kirana shops

Mobile-based Accounting / Book-

keeping Solution

Cloud-based Production

Planning & Control

Cloud-based Project Management

Solutions

Mobile based POS

Cloud-based Collaboration

Solution

Mobile Job Marketplace

Online Training & Learning Solutions

Online Job Portals

Counterfeit Prevention

Solutions

Cloud-based Backup and

Recovery Solutions

Cloud-based Invoicing for SMBs

Low-cost Security Solutions

C

Source – News Articles, Company Websites, Zinnov Analysis

Digital enablement of Indian SMBs presents a multi-billion dollar

opportunity for tech vendors

7

How big is the

opportunity?

Customer Targeting and Engagement

Operational Excellence and SCM

Workforce Enablement

Risk Management 306

484

370

467

310

383

431

551

417

462

518

788

421

683

367

658

219

279

199

384

564

783

621

964

Note: Opportunity assessment done on the basis of relevance of sub categories of solutions to 5 largest SMB verticals, average solution prices, and number of tech addressable SMBs. Source – Company Websites of solutions providers, MSME, Press Articles, Zinnov Analysis

D

Opportunity across key

verticals (USD Mn) Manufacturing Travel and Logistics Retail Professional Services

Restaurants and Hospitality

Others

Total Opportunity: USD 11.6 Bn (2015)

USD 25.8 Bn (2020)

Addressable opportunity by verticals and business

areas (USD Mn) XX

8

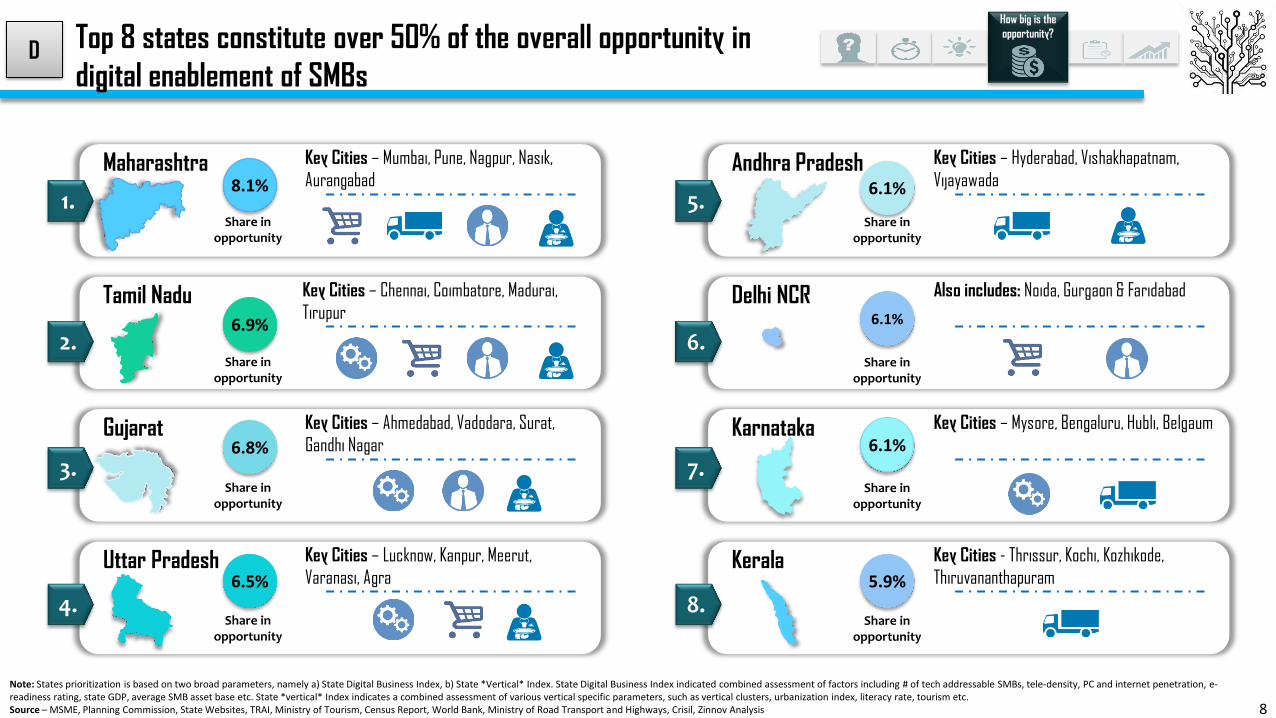

Note: States prioritization is based on two broad parameters, namely a) State Digital Business Index, b) State *Vertical* Index. State Digital Business Index indicated combined assessment of factors including # of tech addressable SMBs, tele-density, PC and internet penetration, e-readiness rating, state GDP, average SMB asset base etc. State *vertical* Index indicates a combined assessment of various vertical specific parameters, such as vertical clusters, urbanization index, literacy rate, tourism etc. Source – MSME, Planning Commission, State Websites, TRAI, Ministry of Tourism, Census Report, World Bank, Ministry of Road Transport and Highways, Crisil, Zinnov Analysis

Key Cities – Mumbai, Pune, Nagpur, Nasik,

Aurangabad 8.1% Maharashtra

Key Cities – Chennai, Coimbatore, Madurai,

Tirupur Tamil Nadu

Key Cities – Ahmedabad, Vadodara, Surat,

Gandhi Nagar Gujarat

Key Cities – Lucknow, Kanpur, Meerut,

Varanasi, Agra Uttar Pradesh

6.8%

6.5%

6.9%

Share in opportunity

Share in opportunity

Share in opportunity

Share in opportunity

1.

2.

3.

4.

Key Cities – Hyderabad, Vishakhapatnam,

Vijayawada Andhra Pradesh

Also includes: Noida, Gurgaon & Faridabad Delhi NCR

Key Cities – Mysore, Bengaluru, Hubli, Belgaum Karnataka

Key Cities - Thrissur, Kochi, Kozhikode,

Thiruvananthapuram Kerala

6.1%

6.1%

6.1%

5.9%

5.

6.

7.

8.

How big is the

opportunity?

Top 8 states constitute over 50% of the overall opportunity in

digital enablement of SMBs D

Share in opportunity

Share in opportunity

Share in opportunity

Share in opportunity

Strategic initiatives required to be set in motion to tap into the

digital SMB opportunity

How to tap the

opportunity?

Engineering Product for SMB use Optimum pricing to ease SMB adoption High Impact outreach enabling large scale

Successfully targeting SMBs necessitates 3-pronged approach

Vertical specific solutions addressing end to end

needs SMBs are receptive to solutions that digitize entire workflow of their vertical

Mobile first solutions

Given high adoption of smartphones among Indian SMBs, it is imperative for solutions to be fully operable over mobile interface

Low set-up time/ready to use

SMBs have limited resources to invest in implementation of solutions and hence prefer ones that work out of the box

Digitization of entire workflow for a doctor, including,

discoverability CRM & operations

Op-ex model: Reduction in up-front cost Greatest deterrent to adoption of solutions is requirement of high upfront investment. Need to reduce the burden by offering pay-per use pricing

Tiered pricing

- Encourage free trial to ensure high initial uptake - Freemium models of engagement to ensure maximum value realization

Creation of channel with non-traditional reach

Need to almost create FMCG reach of solutions across geographic barriers. Experiment with on-boarding entities such as cyber cafés operators, and ticketing agents, as partners to ensure last mile reach

Mass scale evangelization • Need to enhance visibility of

products through mass evangelization

• Use of viral marketing techniques

Enabling easy payments

Tie-up with telecom service providers to enable SMB payments through telecom bills

1. 2. 3.

E

Source – Company Websites, Press Articles, Zinnov Analysis

Targeting new-age digital SMBs requires strategic realignment of

channel

10

How to tap the

opportunity?

E

I. Chaotic: Partner strategy in complete chaos, sells any IT

products to make ends meet; hasn’t invested in growth and capability

II. Reactive: Only fulfils demand generated by principal

vendor, no investments into customer relationships, minimal ability to value sell, poor sales team

III. Proactive: Has set key accounts and made investments

into solutions, limited capabilities to value sell, has growth aspirations yet struggles with scaling sales, may not have competent leadership

IV. Invested: High investment into driving product sales;

capabilities to build solutions; high growth aspirations supported by strong leadership and ability to scale; have own brand presence

Build 2-3 year growth

plan per partner

Build Individual partner

GTM

Define individual

capability development

plan for each partner

Segment partners by

maturity level

Key Impacts of digital SMB solution characteristics on vendor channel operations

Off the shelf nature of products Op-ex model of pricing Low Switching costs

Focus on product sales instead

of professional services Widen funnel, push free trials Accelerate sales cycle

Handhold customers into

solution usage, high focus on

customer engagement

Ensure customer loyalty, Derive

higher lifetime value (LTV)

1 2 3 4 5

Fulfilment, onboarding and configuration done by customer itself

Software vs. services revenue nearly 1:1

Low upfront income per customer Recurring revenue from customers

Need to ensure high customer engagement and satisfaction to maximize LTV

Sales vs. services revenue

# of SMB Customers

Length of sales cycle

Customer lifetime value

Management Commitment

Partner Capability

Credit and Profit Potential

Revenue contribution

Strategic realignment of channel to target SMBs

Source – Zinnov Analysis

Assessment of partner maturity for SMB sales Framework to classify partners by maturity level Strategic Interventions into partner operations

Digital enablement of SMBs would have a multifold impact on

India’s GDP, exports and employment

11

What is the

impact?

Collectively, digital

enablement of Indian

SMBs will lead to

following additional*

contribution by 2020

Additional jobs are expected to be created to power

incremental output aided by digitization

~168 Mn

Additional GDP

Additional annual contribution to the GDP

due to adoption of digital technologies by SMBs

~$ 1.1 Tr

Increase in Exports

Increment in SMB contribution to Indian

exports ~$ 264 Bn

Notes: 1) Based on revenue enhancement and cost optimization effects of digitization of tech addressable SMBS on projected GDP of India in 2020

*Contribution attributable to digital enablement; over and above the expected contribution due to overall Indian GDP growth

Incremental Employment

Generation

Overall Economic Impact of Digital

Enablement on an SMB –

75% of current

revenue

Impact through Revenue Enhancement

50%

Impact through Cost Optimization

25%

F

Source – DNB, MSME, Press Articles, Zinnov Analysis

12

Deep Dive

Agenda

13

Nexus of Forces Driving Digital Enablement of

SMBs

Digital Enablement Impacts Key Business Levers

Digital Enablement of SMBs Key for India’s Holistic Development

Digital Native Solutions Driving SMB Disruptions

Opportunity Deep Dive – Vertical and Geo View

Increasing device penetration

Enhancement in internet connectivity

Customer IT adoption

Availability of enterprise grade

solutions/services at SMB price points

Initiatives from ecosystem

stakeholders

Thriving app ecosystem

Access to Enabling Infrastructure

Availability of Solutions & Services

Push from Customers &

Ecosystem Stakeholders

1

2

3

Nexus of 3 key drivers pushing SMBs to go Digital

A

B

C

D

E

F

14

Increasing propulsion of Indian SMBs toward digital adoption can be attributed to three key

drivers…

Source – Zinnov Analysis

Adoption of smart devices in conjunction with enhancement in internet availability, enabling easy

digital access

15

Increasing

device

penetration

Considerable use of smartphone by

SMBs

2015

2020

1

Meanwhile, low cost

smartphones & tablets are

readily available

$40

$60-80 “

Enhancement in

internet

connectivity

High device penetration

complemented with Rapid

consumerization of IT

Almost the same price as feature phones

Low cost tablets are available from more

than 10 different brands

Growing use of Online collaboration

services like dropbox, google docs,

skype etc. for both personal and

professional work

Increasing broadband & mobile

internet adoption in SMBs

~7 Mn

>30Mn

2015

2020

Reducing internet access

prices

A

B

~7-8 Mn

Near universal

“

“ “

“ “

2X increase in average

internet speed in 3 years 0.9 Mbps

2.0 Mbps

7.0 Mbps

2011 2014 2017

“ “

>70% reduction in 3G mobile prices over the last 2

years

Expectation of data services access for free

Source – Zinnov Analysis, Akamai, BCG Report, Ericsson Market insights, Avendus Mobile Internet Report

16

2 Various SMB relevant solutions and services are available across desktop and mobile platforms

Enterprise grade

solutions/services

at SMB Price points

Thriving app

eco-system

100 Mn

400 Mn

2014

2020

4X Increase of monthly mobile app

downloads in India by 2020

Top Business

Apps

Over 75+ Million average downloads

per app worldwide

Mobile app development is becoming

increasingly viable for SMBs “ <3 hours Required to build a functional app

9,000+ Indian Mobile app development companies

45% reduction in prices in 2013;

base version available for free

31% reduction in prices in 2014;

base version available for free

Google Apps

Easy affordability of cloud enabled

enterprise grade solutions “

“

Cost effectiveness of

cloud-based solutions

50%

50%

Reduction in cost of ownership

Lower deployment time

Public cloud

infrastructure fit for

SMBs

70-75% Advantages like scalability, low management requirement

and low set up time

C

D

“

“

“ cost savings with adoption of public

cloud

Source – Zinnov Analysis, AMI Partners

17

3 Adoption of IT across customers and push from ecosystem stakeholders, fueling SMBs’ digital

journey

Increasing

customer IT

adoption

Initiatives from

Ecosystem

stakeholders

Consumers spending more

time on the internet Internet aiding

purchases across

consumer segments “

1,125 Million searches by consumer in FY 2014

37 Mn ratings and reviews, signifying high

engagement

Increasing use of

digital medium by

enterprises “ 5,000 business tenders added everyday

5-6 average leads for SMB/day

E-commerce companies helping SMBs

to sell on digital platforms

50,000+ SMB sellers on-boarded by top 3

e-commerce players

Rapid growth of e-commerce market

$13 Bn

$70 Bn

2014 2020

“

“

Easy access to loans

for SMBs through

partners Flipkart, Snapdeal offering easy access to

loans for SMBs through partners

Government initiatives

aligned to help SMBs

digital uptake

‘Digital India’ campaign will likely propel Indian govt. spending on

IT to $7.2 Bn by 2015

Government launched scheme to promote ICT in MSME sector

extending support of basic ICT infrastructure

E

F

140 Mn Hours

2013

2020

1500 Mn Hours

“ “

“

“

Source – Zinnov Analysis, Global WebIndex Wave, Company websites

Agenda

18

Nexus of Forces Driving Digital Enablement of SMBs

Digital Enablement Impacts Key Business

Levers

Digital Enablement of SMBs Key for India’s Holistic Development

Digital Native Solutions Driving SMB Disruptions

Opportunity Deep Dive – Vertical and Geo View

Led by digital enablers, SMBs are witnessing disruptions across four key business levers

19

Social

Mobility

Analytics Cloud

IOT

Digital SMBs

Discoverability and reach Managing customer relationships Customer intelligence Optimizing sales motions New sales channels

Customer Targeting and

Engagement

A

Efficiency in operations Customer experience enhancement Optimal resource utilization Partner identification and visibility Optimization of inventory and logistics

Operational Excellence B

Sourcing of relevant talent Tackling attrition Productivity enhancement Skilling

Workforce Enablement C

Counterfeit protection Data security Physical security of assets and resources Safeguarding against financial risk

Risk Management F

Four key business Levers impacted by tech

adoption

Source – Zinnov Analysis

20

Discoverability and Reach

Access to clients in distant geographies and create greater visibility and mindshare among

target segments

Managing Customer Relationships

Ensure efficient management of new and existing customer

relationships; personalization in engagement

Customer Intelligence

Understand customers buying patterns and their requirements to push relevant offerings along with

upselling of complementary products

Optimizing Sales Motions

Gather real time visibility into the existing partner network, measure

their performance and effectiveness of campaigns

executed

New Sales Channels

Engage in various online channels like aggregator websites, online

marketplaces ,etc. to undergo non-linear growth

Illustrative SMB focused Solutions

SMB focused CRM available through cloud across web and mobile interfaces

Used by ~400k SMBs globally

CRM on Mobile

Solution categories to enhance customer targeting and engagement

1 2 3 4 5

A Various solutions are available to address SMB needs related to customer targeting and

engagement

Customer Targeting & Engagement Operational Excellence and SCM Workforce Enablement Risk Management

Quick website creation – in 13 minutes

Website update over SMSs; Auto – SEO

SMS-based Website Creation and Management

Use of missed calls to generate leads, deliver coupons, run contests etc.

High quality leads, positive customer

engagement

Missed Call Marketing

Tie up with local retail SMBs to deliver grocery orders received online

Online Kirana shops

Source – Zinnov Analysis, Company websites, Press Articles

Zinnov estimates an opportunity of USD 3.8 Bn in provision of Customer Targeting and Engagement

solutions to Indian SMBs

21

Total Discoverability andReach

Managing CustomerRelationships

CustomerIntelligence

Optimizing SalesProcesses

New Sales Motions

$ 3,800 Mn

$ 1,250 Mn

$ 550 Mn

$ 550 Mn $ 100 Mn

$ 1,350 Mn

Avenues to enhance discoverability, such as website creation and portal listings, constitute a large market within SMBs

In addition, enabling SMBs to sell over internet can potentially drive annual revenues in access of a billion dollars for the enabling platforms

A

Customer Targeting & Engagement Operational Excellence and SCM Workforce Enablement Risk Management

FY2015

FY2020 $8.4Bn

$3.8Bn

Addressable Opportunity in Customer Targeting and Engagement across

Tech-influenced SMBs

Opportunity Split – by Sub components (2015)

Note: Opportunity assessment done on the basis of relevance of sub categories of solutions to 5 largest SMB verticals, average solution prices, and number of tech addressable SMBs. Source – Company Websites of key solutions providers, MSME, Press Articles, Zinnov Analysis

Customer Targeting & Engagement Operational Excellence and SCM Workforce Enablement Risk Management

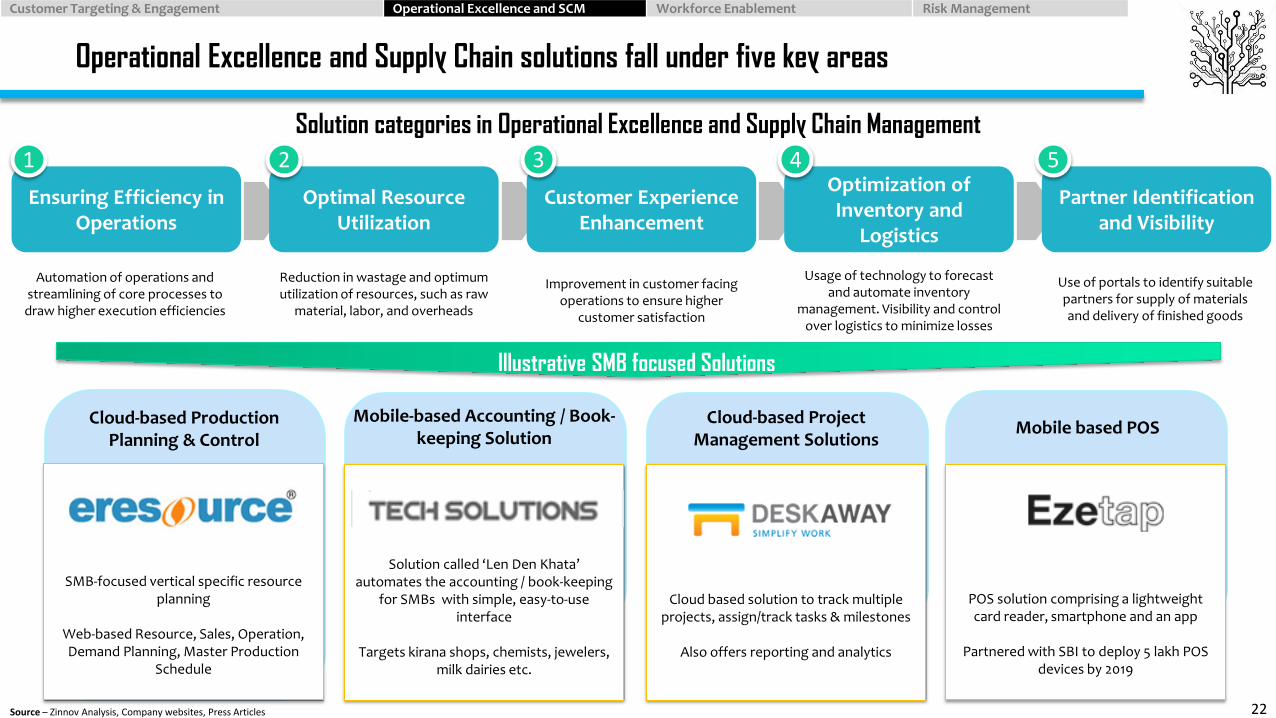

Ensuring Efficiency in Operations

Automation of operations and streamlining of core processes to draw higher execution efficiencies

Optimal Resource Utilization

Reduction in wastage and optimum utilization of resources, such as raw

material, labor, and overheads

Customer Experience Enhancement

Improvement in customer facing operations to ensure higher

customer satisfaction

Optimization of Inventory and

Logistics

Usage of technology to forecast and automate inventory

management. Visibility and control over logistics to minimize losses

Partner Identification and Visibility

Use of portals to identify suitable partners for supply of materials and delivery of finished goods

Illustrative SMB focused Solutions

Solution categories in Operational Excellence and Supply Chain Management

1 2 3 4 5

Operational Excellence and Supply Chain solutions fall under five key areas

22

Solution called ‘Len Den Khata’ automates the accounting / book-keeping

for SMBs with simple, easy-to-use interface

Targets kirana shops, chemists, jewelers,

milk dairies etc.

Mobile-based Accounting / Book-keeping Solution

SMB-focused vertical specific resource planning

Web-based Resource, Sales, Operation, Demand Planning, Master Production

Schedule

Cloud-based Production Planning & Control

Cloud based solution to track multiple projects, assign/track tasks & milestones

Also offers reporting and analytics

Cloud-based Project Management Solutions

POS solution comprising a lightweight card reader, smartphone and an app

Partnered with SBI to deploy 5 lakh POS

devices by 2019

Mobile based POS

Source – Zinnov Analysis, Company websites, Press Articles

Zinnov estimates an opportunity of USD 2.5 Bn in provision of Operational Excellence solutions to

Indian SMBs

23

Total Ensuring efficiencyin processes

Optimal ResourceUtilization

CustomerExperience

Enhancement

Optimization ofinventory and

logistics

Partneridentification and

visibility

$ 2,500 Mn

$ 950 Mn

$ 400 Mn $ 200 Mn

$ 800 Mn

$ 150 Mn

SMBs require solutions that help address issues around inventory management, efficient logistics and overall efficiency of operations

Overall market for operational excellence solutions is expected to grow at a CAGR of 17% to reach $5.5 Bn by 2020

A

Customer Targeting & Engagement Operational Excellence and SCM Workforce Enablement Risk Management

Opportunity Split – by Sub components (2015) Addressable Opportunity in Operational Excellence across Tech-

influenced SMBs

FY2015

FY2020 $5.5Bn

$2.5Bn

Note: Opportunity assessment done on the basis of relevance of sub categories of solutions to 5 largest SMB verticals, average solution prices, and number of tech addressable SMBs. Source – Company Websites of key solutions providers, MSME, Press Articles, Zinnov Analysis

Customer Targeting & Engagement Operational Excellence and SCM Workforce Enablement Risk Management

Talent Sourcing

Usage of technology solutions to address workforce shortfall by

identifying talent and hire as per requirement

Productivity Enhancement

Ensuring collaboration amongst employees and enable monitoring to increase employee productivity

Skilling

Use of web based solutions to provide training to employees

across skill categories

Illustrative SMB focused Solutions

Solution categories in Workforce Enablement

1 2 3

Includes solutions, such as email, calendar, storage, productivity apps

delivered over cloud

Cost effective – INR 1,500 per person per annum

Cloud-based Collaboration Solution

Saral Rozgar Card allows users to connect to job market place from mobiles;

location based mapping, aiding both “job seekers” and “job providers”

2 Million registered users across 800 cities

in just 2 years

Saral Rozgar - Mobile Job Marketplace

200+ Courses of professional certification

Accredited by 20+ global bodies

Over 100,000 professionals trained across 150+ countries

Online Training & Learning Solutions

Users can apply for jobs across 50+ job boards in one submission

Built-in Social Recruiting to take

advantage of integrated social network postings

Online Job Portals

Workforce Enablement solutions solve problems related to talent sourcing, productivity and skill

Source – Zinnov Analysis, Company websites, Press Articles

Zinnov estimates an opportunity of USD 3.1 Bn in provision of workforce enablement solutions to

Indian SMBs

25

Total Talent Sourcing, tacklingattrition, hiring

Productivity Enhancement Skilling

$ 3,100 Mn

$ 2,300 Mn

$ 400 Mn

$ 400 Mn

Workforce hiring and retention are one of the biggest pain points in SMB. Solutions addressing the same across hierarchy levels have a massive opportunity among SMBs

A

Customer Targeting & Engagement Operational Excellence and SCM Workforce Enablement Risk Management

Opportunity Split – by Sub components (2015) Addressable Opportunity in

Workforce Enablement across Tech-influenced SMBs

FY2015

FY2020 $6.8Bn

$3.1Bn

Note: Opportunity assessment done on the basis of relevance of sub categories of solutions to 5 largest SMB verticals, average solution prices, and number of tech addressable SMBs. Source – Company Websites of key solutions providers, MSME, Press Articles, Zinnov Analysis

Data security Counterfeit protection

Physical security of assets and resources

Safeguarding against financial risks

1 2 3 4

Customer Targeting & Engagement Operational Excellence and SCM Workforce Enablement Risk Management

Prevention of leakage of critical business data on finances, customers, operations etc.

Adopting mechanisms to help consumers identify a counterfeit

product from a real one

Use of surveillance, asset control and tracking solutions to ensure

physical safety of assets

Illustrative SMB focused Solutions

Advanced physical layer authentication to prevent counterfeiting

Counterfeit Prevention Solutions

Integrated backup for offsite data storage and disaster recovery

Available as a service delivered over cloud

Cloud-based Backup and Recovery Solutions

Provides monitoring and reports / analytics on invoicing and payments on a

freemium model

5 mn users across 120 countries

Cloud-based Invoicing for SMBs

Provides CCTV surveillance, Metal detectors, etc. along with electronic

security-as-a-service

Low-cost Security Solutions

Ensure healthy working capital by safeguarding against financial

defaults on receivables

26

SMBs can mitigate risks by adopting technology across 4 major areas

Risk Management solutions can be categorized in four broad buckets

Source – Zinnov Analysis, Company websites, Press Articles

Zinnov estimates an opportunity of USD 2.2 Bn in provision of Risk Management solutions to Indian

SMBs

27

Total Data Security Counterfeit protection Physical security ofresources

Safeguarding againstfinancial risk

$ 2,250 Mn

$ 610 Mn $ 110 Mn

$ 1,030 Mn

$ 500 Mn

Safeguarding enterprise data and security of physical assets are critical to SMBs and represent the largest opportunity for providers of relevant solutions

A

Customer Targeting & Engagement Operational Excellence and SCM Workforce Enablement Risk Management

Opportunity Split – by Sub components (2015) Addressable Opportunity in Risk

Management across Tech-influenced SMBs

FY2015

FY2020 $5.0Bn

$2.2Bn

Note: Opportunity assessment done on the basis of relevance of sub categories of solutions to 5 largest SMB verticals, average solution prices, and number of tech addressable SMBs. Source – Company Websites of key solutions providers, MSME, Press Articles, Zinnov Analysis

Agenda

28

Nexus of Forces Driving Digital Enablement of SMBs

Digital Enablement Impacts Key Business Levers

Digital Enablement of SMBs Key for India’s Holistic Development

Digital Native Solutions Driving SMB Disruptions

Opportunity Deep Dive – Vertical and Geo View

Opportunity Assessment – Manufacturing Vertical

29

Customer Targeting and Engagement

Operational Excellence and SCM

Workforce Enablement

Risk Management

Total Opportunity USD 1,627 Mn

Manufacturing Vertical

306

484

370

467

(USD Mn)

Manufacturing Retail Travel and Logistics Professional Services Restaurants and Hospitality

Uttar Pradesh Key Cities – Lucknow, Kanpur, Meerut

Maharashtra Key Cities - Mumbai, Pune, Aurangabad

Andhra Pradesh Key Cities - Hyderabad, Visakhapatnam, Vijayawada

Karnataka Key Cities - Bangalore, Mysore, Hubli

Tamil Nadu Key Cities - Chennai, Coimbatore, Tirupur

Rajasthan Key Cities - Kota, Jaipur, Udaipur

4.9%

9.2%

7.1%

6.1%

7.5%

6.4%

6.6%

5.7%

Gujarat Key Cities – Ahmedabad, Vadodara, Surat

Note: States prioritization is based on two broad parameters, namely a) State Digital Business Index, b) State *Vertical* Index. State Digital Business Index indicated combined assessment of factors including # of tech addressable SMBs, tele-density, PC and internet penetration, e-readiness rating, state GDP, average SMB asset base etc. State *vertical* Index indicates a combined assessment of various vertical specific parameters, such as vertical clusters, urbanization index, literacy rate, tourism etc. Source – Zinnov Analysis, MSME, Planning Commission

Kerala Key Cities - Thrissur, Kochi, Thiruvananthapuram

States with highest contribution to manufacturing opportunity

Opportunity Assessment – Retail Vertical

30

Customer Targeting and Engagement

Operational Excellence and SCM

Workforce Enablement

Risk Management

Total Opportunity USD 2,184 Mn

Retail Vertical

(USD Mn)

Manufacturing Retail Travel and Logistics Professional Services Restaurants and Hospitality

417

462

518

788 6.9%

6.5%

7.0%

6.2%

6.2%

7.2%

9.0%

5.8%

Uttar Pradesh Key Cities – Lucknow, Kanpur, Varanasi

West Bengal Key Cities – Kolkata, Siliguri, Asansol

Maharashtra Key Cities - Mumbai, Pune, Nagpur

Andhra Pradesh Key Cities - Hyderabad, Visakhapatnam, Vijayawada

Karnataka Key Cities - Mysore, Bangalore, Belgaum

Tamil Nadu Key Cities - Chennai, Coimbatore, Madurai

Delhi NCR Includes Noida, Gurgaon, Faridabad

Gujarat Key Cities – Ahmedabad, Vadodara, Surat

Note: States prioritization is based on two broad parameters, namely a) State Digital Business Index, b) State *Vertical* Index. State Digital Business Index indicated combined assessment of factors including # of tech addressable SMBs, tele-density, PC and internet penetration, e-readiness rating, state GDP, average SMB asset base etc. State *vertical* Index indicates a combined assessment of various vertical specific parameters, such as vertical clusters, urbanization index, literacy rate, tourism etc. Source – Zinnov Analysis, MSME, Census, World Bank, Crisil

States with highest contribution to retail opportunity

Opportunity Assessment – Travel and Logistics Vertical

31

Customer Targeting and Engagement

Operational Excellence and SCM

Workforce Enablement

Risk Management

Total Opportunity USD 1,675 Mn

Travel and Logistics Vertical

(USD Mn)

Manufacturing Retail Travel and Logistics Professional Services Restaurants and Hospitality

310

383

431

551

Tamil Nadu Key Cities - Chennai, Coimbatore, Madurai

Kerala Key Cities - Thrissur, Kochi, Thiruvananthapuram

3.9%

4.7%

5.6%

4.5%

6.5%

5.5%

6.6%

5.7%

7.0%

Uttar Pradesh Key Cities – Lucknow, Kanpur, Varanasi

West Bengal Key Cities – Kolkata, Durgapur, Asansol

Maharashtra Key Cities - Mumbai, Nasik, Pune

Andhra Pradesh Key Cities - Hyderabad, Visakhapatnam, Vijayawada

Karnataka Key Cities - Hubli, Bangalore, Mangalore

Rajasthan Key Cities – Kota, Jaipur, Udaipur

Gujarat Key Cities – Ahmedabad, Gandhinagar, Surat

Note: States prioritization is based on two broad parameters, namely a) State Digital Business Index, b) State *Vertical* Index. State Digital Business Index indicated combined assessment of factors including # of tech addressable SMBs, tele-density, PC and internet penetration, e-readiness rating, state GDP, average SMB asset base etc. State *vertical* Index indicates a combined assessment of various vertical specific parameters, such as vertical clusters, urbanization index, literacy rate, tourism etc. Source – Zinnov Analysis, MSME, Crisil, Ministry of Road Transport and Highways

States with highest contribution to travel and logistics opportunity

Opportunity Assessment – Professional Services Vertical

32

Customer Targeting and Engagement

Operational Excellence and SCM

Workforce Enablement

Risk Management

Total Opportunity USD 2,129 Mn

Professional Services Vertical

(USD Mn)

Manufacturing Retail Travel and Logistics Professional Services Restaurants and Hospitality

421

683

367

658 8.3%

6.9%

5.9%

7.0%

8.8%

5.8%

6.6%

Uttar Pradesh Key Cities – Lucknow, Kanpur, Varanasi

Maharashtra Key Cities - Mumbai, Nagpur, Pune

Karnataka Key Cities - Mysore, Bangalore, Belgaum Tamil Nadu

Key Cities - Chennai, Coimbatore, Madurai

Kerala Key Cities - Kozhikode, Kochi, Thiruvananthapuram

Delhi NCR Includes Noida, Gurgaon, Faridabad

Gujarat Key Cities – Ahmedabad, Vadodara, Surat

Note: States prioritization is based on two broad parameters, namely a) State Digital Business Index, b) State *Vertical* Index. State Digital Business Index indicated combined assessment of factors including # of tech addressable SMBs, tele-density, PC and internet penetration, e-readiness rating, state GDP, average SMB asset base etc. State *vertical* Index indicates a combined assessment of various vertical specific parameters, such as vertical clusters, urbanization index, literacy rate, tourism etc. Source – Zinnov Analysis, MSME, Census Report, World Bank

5.4%

West Bengal Key Cities – Kolkata, Durgapur, Siliguri

States with highest contribution to professional services opportunity

Opportunity Assessment – Restaurants and Hospitality Vertical

33

Customer Targeting and Engagement

Operational Excellence and SCM

Workforce Enablement

Risk Management

Total Opportunity USD 1081 Mn

Restaurants and Hospitality Vertical

(USD Mn)

Manufacturing Retail Travel and Logistics Professional Services Restaurants and Hospitality

219

279

199

384 5.7%

6.9%

7.2%

6.8%

7.4%

9.6%

6.6%

Uttar Pradesh Key Cities – Agra, Mathura, Varanasi

Maharashtra Key Cities - Mumbai, Aurangabad, Pune

Andhra Pradesh Key Cities - Hyderabad, Visakhapatnam, Vijayawada

Karnataka Key Cities - Mysore, Bangalore, Mangalore

Tamil Nadu Key Cities - Chennai, Coimbatore, Madurai

Delhi NCR Includes Noida, Gurgaon, Faridabad

Gujarat Key Cities – Ahmedabad, Junagarh, Surat

Note: States prioritization is based on two broad parameters, namely a) State Digital Business Index, b) State *Vertical* Index. State Digital Business Index indicated combined assessment of factors including # of tech addressable SMBs, tele-density, PC and internet penetration, e-readiness rating, state GDP, average SMB asset base etc. State *vertical* Index indicates a combined assessment of various vertical specific parameters, such as vertical clusters, urbanization index, literacy rate, tourism etc. Source – Zinnov Analysis, MSME, World Bank, Ministry of Tourism, Census

States with highest contribution to restaurants and hospitality opportunity

Agenda

34

Nexus of Forces Driving Digital Enablement of SMBs

Digital Enablement Impacts Key Business Levers

Digital Enablement of SMBs Key for India’s Holistic Development

Digital Native Solutions Driving SMB

Disruptions

Opportunity Deep Dive – Vertical and Geo View

Disrupted traditional procurement methods of individual buying at low scale

Driving cost efficiencies through aggregated demand

Cloud based solution enabling demand aggregation

Collective payment through online channel

Enterprise scale

procurement for SMBs

Digital native solutions driving SMB disruptions (1/2)

35

Operations structured around merely three employees per city which handle thousands of accounts (SMBs)

Made possible due to extensive digitization of operations

Disrupting customer engagement through permission based marketing using missed call (toll free for customers)

Provides actionable leads with serious intent

Easy to use solutions encompassing entire SMB (Doctor) workflow : Enhancing discoverability by customers Managing customer relationships Enabling operational workflow

1

2

3

4

Completely mobile workflow

Ease of operation for both drivers and consumers

Engaging customers through lowest denominator of technological adoption – telephone calls

Digitization of entire workflow on an integrated cloud based platform

SMB reach without feet on street

Enabling end-to-end

vertical specific workflows

Non-intrusive

customer engagement at scale

Source – Zinnov Analysis, Company websites, press articles

Help Individuals derive value out of their “underutilized assets”

Companies have created trusted market places for respective offerings: Air BnB – Accommodation Lyft – Car Ride

Digitally enabled crowd sourcing of user ratings

Ease of execution –fully operational through a mobile app

Powering new breed of SMBs

Digital native solutions driving SMB disruptions (2/2)

36

Organization of blue collar workforce through saral rozgar card

Registered job seeker base of close to 2 million and reached 1 Lac job openings in March 2014

Used as a medium for both internal (employees) and external (clients) communication

Rapidly emerging as an effective mass marketing tool

End-to end solution to create and manage websites

13 minutes for creation of websites; auto SEO

Ability to manage/update websites over SMS

5

6

7

8

Enablement through mobile phones which have a significant penetration in the target workforce

Mobile only solution with high penetration

Low learning curve; near Zero Cost

Extreme ease in web-presence creation and management

Organizing the

unorganized

Consumer apps for business

Web presence

made simple

Source – Zinnov Analysis, Company websites, press articles

Agenda

37

Nexus of Forces Driving Digital Enablement of SMBs

Digital Enablement Impacts Key Business Levers

Digital Enablement of SMBs Key for India’s

Holistic Development

Digital Native Solutions Driving SMB Disruptions

Opportunity Deep Dive – Vertical and Geo View

38

Overall Economic Impact of Tech Adoption on

an SMB – 75% of current revenue

Revenue Enhancement –

50% Cost Optimization–

25%

Notes: 1) Economic impact has been calculated based on 100% adoption of all relevant digital technologies and estimating %age revenue enhancement and cost reduction resulting from tech adoption across each of the 4 business levers

Customer Targeting and Engagement, 38%

Risk Management, 22%

Workforce Enablement, 20%

Operational Excellence, 20%

90%, Operational Excellence

10%, Customer targeting and Engagement

Zinnov estimates 75% overall enhancement in SMB performance due to technology adoption across

6 key business levers

Source – Zinnov Analysis, Company Websites, Press Articles

Digital SMBs would have a multifold impact on India’s GDP, exports and employment

39

Additional* Contribution

of Digitally enabled Indian

SMBs in 2020

Additional jobs are expected to be created to

power incremental output aided by digitization

~168 Mn

Additional GDP Additional annual

contribution to the GDP due to adoption of digital

technologies by SMBs ~$ 1.1 Tr

Increase in Exports Increment in SMB

contribution to Indian exports ~$ 264 Bn

Notes: 1) Based on revenue enhancement and cost optimization effects of digitization of tech addressable SMBS on projected GDP of India in 2020

*Contribution attributable to digital enablement; over and above the expected contribution due to overall Indian GDP growth.

Incremental

Employment Generation

Source – DNB, MSME, Press Articles, Zinnov Analysis

Thank you

40

21, Waterway Ave,

Suite 300

The Woodlands

TX – 77380

PH: +1-281-362-2773

Meilifang Tower 4, Entrance 4,

10/F #1003,

11 Beiyuan Shuangying Road,

Chaoyang District,

Beijing China 100012

Level 42,

Suntec Tower Three

8 Temasek Boulevard

Singapore 038988

PH:+65 6829 2123

69 "Prathiba Complex", 4th 'A' Cross,

Koramangala Ind. Layout

5th Block, Koramangala

Bangalore – 560095

PH: +91-80-41127925/6

First Floor,

Plot # 131,

Sector - 44,

Gurgaon – 122002

PH: +91-124- 4420100

3701 Patrick Henry Dr.

Building 7

Santa Clara

CA – 95054

PH: +1-408-716-8432

Zinnov Worldwide

www.zinnov.com @Zinnov