The MPS opportunity for SMBs

17

© Quocirca 2014 - 1 - Louella Fernandes Quocirca Ltd Tel : +44 7786 331924 Email: [email protected] Clive Longbottom Quocirca Ltd Tel: +44 118 948 3360 Email: [email protected] The MPS opportunity for SMBs How MPS maturity is driving greater print management efficiency April 2014 - Excerpt SMBs (small and medium businesses) across all industry sectors continue to rely on printing to some extent. This reliance can be at a huge cost and be a productivity drain, as many SMBs lack the resources or budget to deal with time consuming print management tasks. As more SMBs embrace cloud services and their workforce becomes more mobile-enabled, they are becoming more receptive to subscription-based managed print services (MPS). An MPS contract enables better control of costs (see later) through predictable expenses and reduced burden on IT staff through proactive service and supplies management. This paper, based on original Quocirca research, examines the need for MPS and how SMBs are faring as they embark on their MPS journey. It reveals that SMBs that have moved beyond basic services to embrace broader full MPS are gaining the most from their contracts.

Transcript of The MPS opportunity for SMBs

© Quocirca 2014 - 1 -

Louella Fernandes Quocirca Ltd Tel : +44 7786 331924 Email: [email protected]

Clive Longbottom Quocirca Ltd Tel: +44 118 948 3360 Email: [email protected]

The MPS opportunity for SMBs

How MPS maturity is driving greater print management efficiency

April 2014 - Excerpt

SMBs (small and medium businesses) across all industry sectors continue to rely on printing to some extent. This reliance can be at a huge cost and be a productivity drain, as many SMBs lack the resources or budget to deal with time consuming print management tasks. As more SMBs embrace cloud services and their workforce becomes more mobile-enabled, they are becoming more receptive to subscription-based managed print services (MPS). An MPS contract enables better control of costs (see later) through predictable expenses and reduced burden on IT staff through proactive service and supplies management. This paper, based on original Quocirca research, examines the need for MPS and how SMBs are faring as they embark on their MPS journey. It reveals that SMBs that have moved beyond basic services to embrace broader full MPS are gaining the most from their contracts.

© Quocirca 2014 - 2 -

SMBs are struggling to control costs

Cost control is the top print management challenge faced by SMBs across Europe. Despite a heavy reliance on printing and rising colour print costs, 70% of SMBs indicate that they do not have the tools to track printing across all devices. This lack of insight leads to spiralling costs.

The burden on IT staff from print management is increasing

SMBs do not necessarily have the resources to devote to print management. Almost three quarters have one or more dedicated IT staff members supporting their print environment. Small SMBs are more likely (44%) than larger SMBs (33%) to be using one dedicated in-house resource. On average, SMBs say that they are devoting approximately 12% of their IT resources to print management. Almost a third expects the burden to rise, particularly smaller SMBs.

SMB confidence in MPS is growing

SMB confidence in MPS is growing, with 50% of existing MPS users expanding their engagements and 43% of non-users expecting to invest in their first basic print service during 2014. These “MPS expanders” are most commonly in the UK and Germany, which lead in MPS maturity. While France and Spain have lower adoption rates, many are showing more interest in basic MPS. These countries represent an opportunity for MPS providers to target, with entry-level packaged offerings to get them started on the MPS path.

Cost is the top MPS driver

The overriding reason to move to MPS is to reduce costs (both for consumables and hardware); this is rated highest amongst SMBs using a full MPS. German SMBs bucked this trend with improving document security cited as the top driver, reflecting their relative MPS maturity.

MPS adoption drives satisfaction

MPS usage directly correlates with satisfaction levels around print management. Those that have moved to a full MPS show a higher satisfaction rate with print management (3.73) compared to non-MPS users (3.47). This satisfaction rate is boosted by a higher usage of other services (mobility, document security and workflow), as SMBs look to drive further business value from their MPS contracts.

MPS is not meeting cost expectations

However, MPS is failing to meet cost expectations. This is primarily due to the majority of SMBs being at the early stages of their MPS journey. Although full MPS users rate their success in achieving cost savings higher than basic MPS users, there is room for improvement. Consequently, SMBs cite better insight into cost and usage the top area for MPS improvement.

Lack of knowledge is inhibitor to growth

The top barrier to adoption, cited by 56% of non-MPS users, is the belief that an MPS contract would be more costly than managing printing in-house. This is followed by 31% of respondents citing a lack of clarity around the cost benefits of MPS. Both vendors and channel partners have a vital role in helping overcome this perception and reality (see last bullet) and both need to get the message across and deliver on expectations.

Executive Summary

The MPS opportunity for SMBs Although the MPS market for SMBs is gaining maturity, there are still wide variations in how well it is achieving its expectations. With many SMBs still at the early stages of their journey, MPS has yet to make a significant impact. However, those that have moved to broader full MPS agreements are most likely to be enjoying improved productivity and reduced IT burden through more effective print management.

The SMB MPS opportunity

© Quocirca 2014 - 3 -

PLEASE NOTE THIS IS AN EXCERPT OF THE FULL STUDY WHICH INCLUDES A COMPREHENSIVE REPORT AND RESEARCH FINDINGS PRESENTATION. PLEASE CONTACT [email protected] FOR MORE INFORMATION

TABLE OF CONTENTS

INTRODUCTION ......................................................................................................................................................................... 4

METHODOLOGY AND DEFINITIONS ............................................................................................................................................ 5

THE NEED FOR MPS ................................................................................................................................................................... 6

MPS ADOPTION ......................................................................................................................................................................... 8

MPS DRIVERS............................................................................................................................................................................ 10

MPS PERFORMANCE ................................................................................................................................................................. 11

MPS INHIBITORS ....................................................................................................................................................................... 13

THE SOLUTIONS OPPORTUNITY ................................................................................................................................................ 14

FUTURE OUTLOOK .................................................................................................................................................................... 15

ABOUT QUOCIRCA .................................................................................................................................................................... 17

The SMB MPS opportunity

© Quocirca 2014 - 4 -

Introduction

As the backbone to the European economy, representing more than 99% of European businesses (according to the European Commission

1), most SMBs rely on IT as an enabler to drive business productivity. Like their enterprise

counterparts, SMBs need to make the most of their resources to drive business efficiency and compete successfully. However, most SMBs are constrained by limited budgets and a lack of IT resources. Consequently, they need to do more with less, ensure their technology is up to date and safeguard their capital expenditure budgets. This has led many SMBs towards the cloud as a utility model of IT consumption, with an estimated 60% of European SMBs using at least one cloud service

2.

With cloud services, SMBs gain access to enterprise-class technology on a pay-per-use basis. SMBs benefit from predictable expenses, lower costs and a reduced burden through not having to deploy a physical infrastructure such as file and email servers, storage systems and software. The growing awareness of the benefits that the cloud can deliver is driving the MPS opportunity amongst SMBs. MPS marks a shift from an ad hoc, hardware-centric, transactional approach to a contractual approach. MPS contracts are typically monthly or quarterly, encompassing hardware (purchased or leased) along with service and supplies (ink, toner), based on a cost-per-page model. Automation is key to the success of any effective managed service. Through proactive service and supplies management, the typical ad hoc manual purchasing of consumables is eliminated, leaving SMB staff free to focus on core business activities. Meanwhile, uptime and availability of devices can be maximised through remote monitoring, which can also help track usage and help SMBs tackle escalating costs. The outlook for MPS amongst the diverse SMB market is positive. Overall, SMB confidence in MPS is growing with 50% of existing customers expanding their current MPS footprint (MPS expanders) and 43% of non-users (MPS converters) expecting to invest in their first basic print service during 2014. In terms of adoption today, Quocirca estimates that, in Europe, approximately 20% of SMBs already use some form of basic print service, rising to over 40% adoption in more mature MPS regions such as the UK and Germany. The diverse nature of the SMB market demands a range of MPS approaches to suit individual business needs and is dependent on the number and type of printers and MFPs. For smaller SMBs, with a small device fleet based on one brand, a basic print service is a good first step, but where SMBs are seeing the most benefits is when they transition to a full MPS. Quocirca’s study examines the print management challenges that are creating the need for MPS. It also discusses where MPS is failing to meet expectations. While most SMBs are at the early stage of their MPS journey, it is worth persevering. Those progressive SMBs that have moved beyond basic print services to a full MPS are the most confident about MPS and most likely to be reaping the benefits of lower costs and reduced burden on IT staff.

The SMB MPS opportunity

© Quocirca 2014 - 5 -

Methodology and Definitions

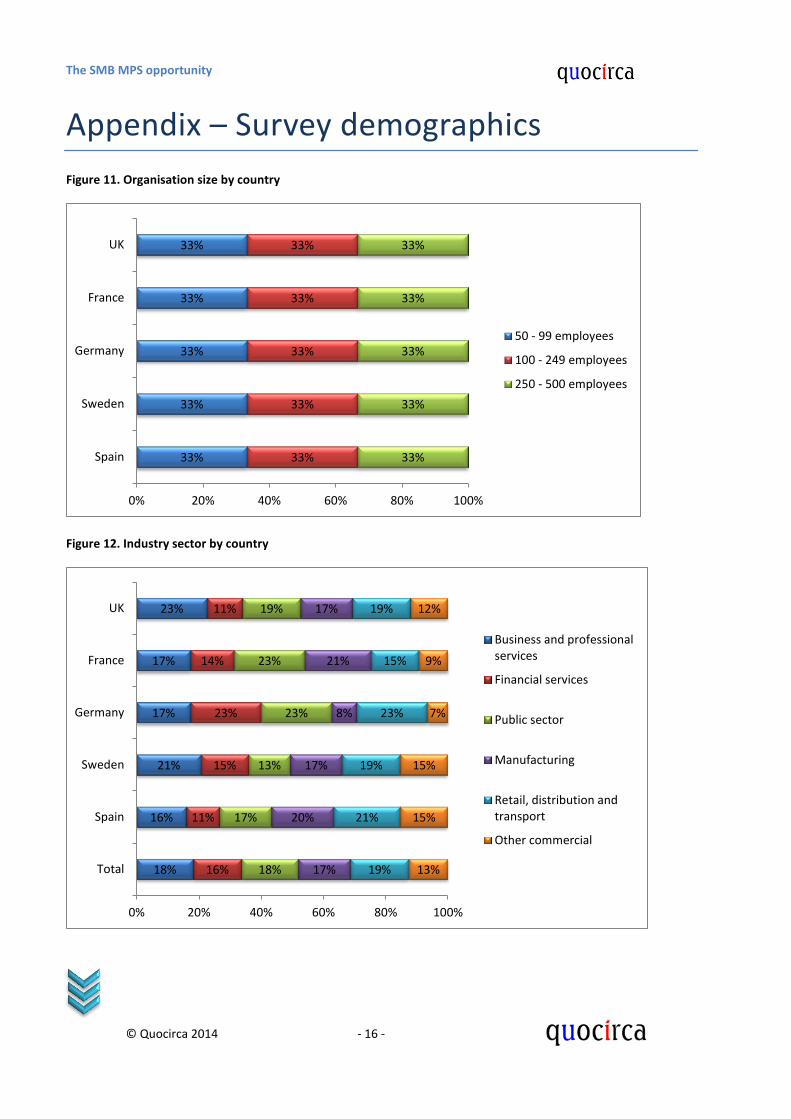

Methodology Quocirca surveyed 750 SMBs across 5 countries – the UK, France, Germany, Sweden and Spain in November 2013. 150 interviews were conducted in each region and split evenly between three organisation size categories: 50–99, 100–249 and 250–500 employees. Surveys were spread evenly across a range of industries.

Definitions Quocirca defines a ‘managed print service’ as a service from an external provider to assess, optimise and continuously manage an organisation’s document output environment. MPS allows organisations to reduce costs and lower risk while improving efficiency by rationalising their print environment. It also makes use of existing investments in multifunction peripherals (MFPs) while continually monitoring usage to ensure the optimised infrastructure meets a business’s ongoing needs. This report covers MPS for the SMB market, which is split into the following broad categories:

Basic MPS – A fixed monthly or quarterly fee contractual approach to purchasing or leasing printer hardware, service, supplies and support on a cost-per-page basis.

Full MPS – A broader MPS contract that may include assessment, on-going proactive management and software service.

The SMB MPS opportunity

© Quocirca 2014 - 6 -

The need for MPS

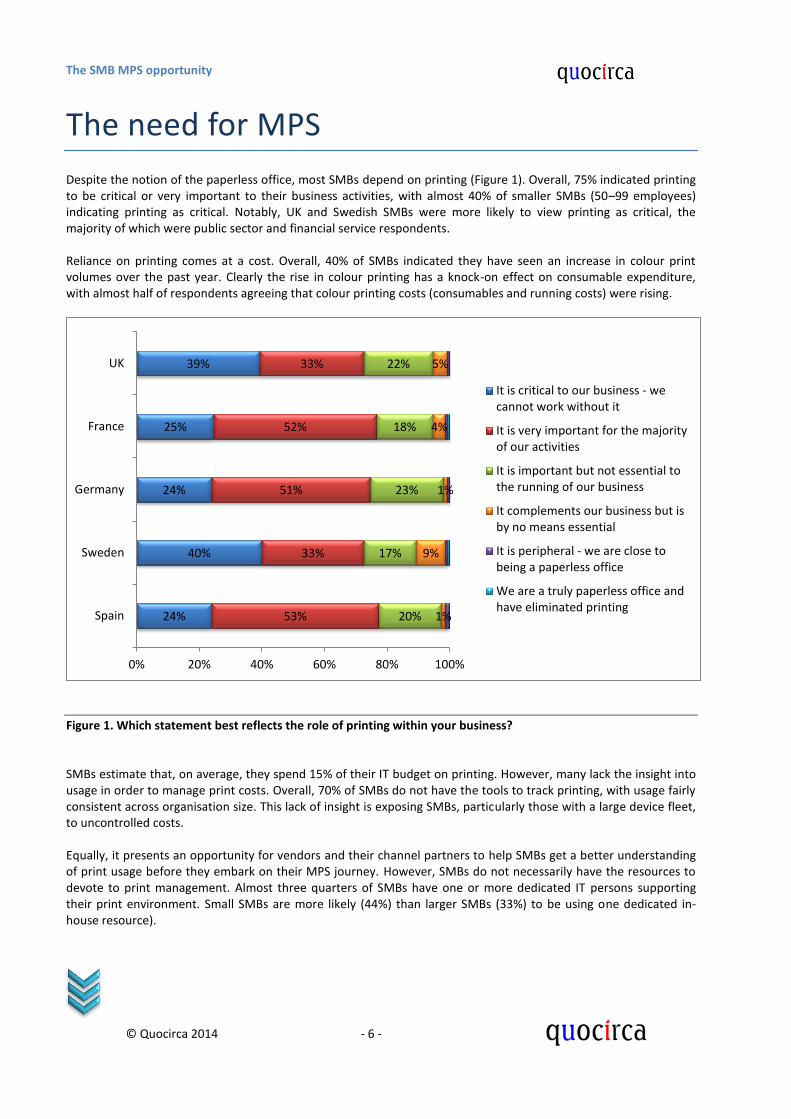

Despite the notion of the paperless office, most SMBs depend on printing (Figure 1). Overall, 75% indicated printing to be critical or very important to their business activities, with almost 40% of smaller SMBs (50–99 employees) indicating printing as critical. Notably, UK and Swedish SMBs were more likely to view printing as critical, the majority of which were public sector and financial service respondents. Reliance on printing comes at a cost. Overall, 40% of SMBs indicated they have seen an increase in colour print volumes over the past year. Clearly the rise in colour printing has a knock-on effect on consumable expenditure, with almost half of respondents agreeing that colour printing costs (consumables and running costs) were rising.

Figure 1. Which statement best reflects the role of printing within your business? SMBs estimate that, on average, they spend 15% of their IT budget on printing. However, many lack the insight into usage in order to manage print costs. Overall, 70% of SMBs do not have the tools to track printing, with usage fairly consistent across organisation size. This lack of insight is exposing SMBs, particularly those with a large device fleet, to uncontrolled costs. Equally, it presents an opportunity for vendors and their channel partners to help SMBs get a better understanding of print usage before they embark on their MPS journey. However, SMBs do not necessarily have the resources to devote to print management. Almost three quarters of SMBs have one or more dedicated IT persons supporting their print environment. Small SMBs are more likely (44%) than larger SMBs (33%) to be using one dedicated in-house resource).

24%

40%

24%

25%

39%

53%

33%

51%

52%

33%

20%

17%

23%

18%

22%

1%

9%

1%

4%

5%

0% 20% 40% 60% 80% 100%

Spain

Sweden

Germany

France

UK

It is critical to our business - wecannot work without it

It is very important for the majorityof our activities

It is important but not essential tothe running of our business

It complements our business but isby no means essential

It is peripheral - we are close tobeing a paperless office

We are a truly paperless office andhave eliminated printing

The SMB MPS opportunity

© Quocirca 2014 - 7 -

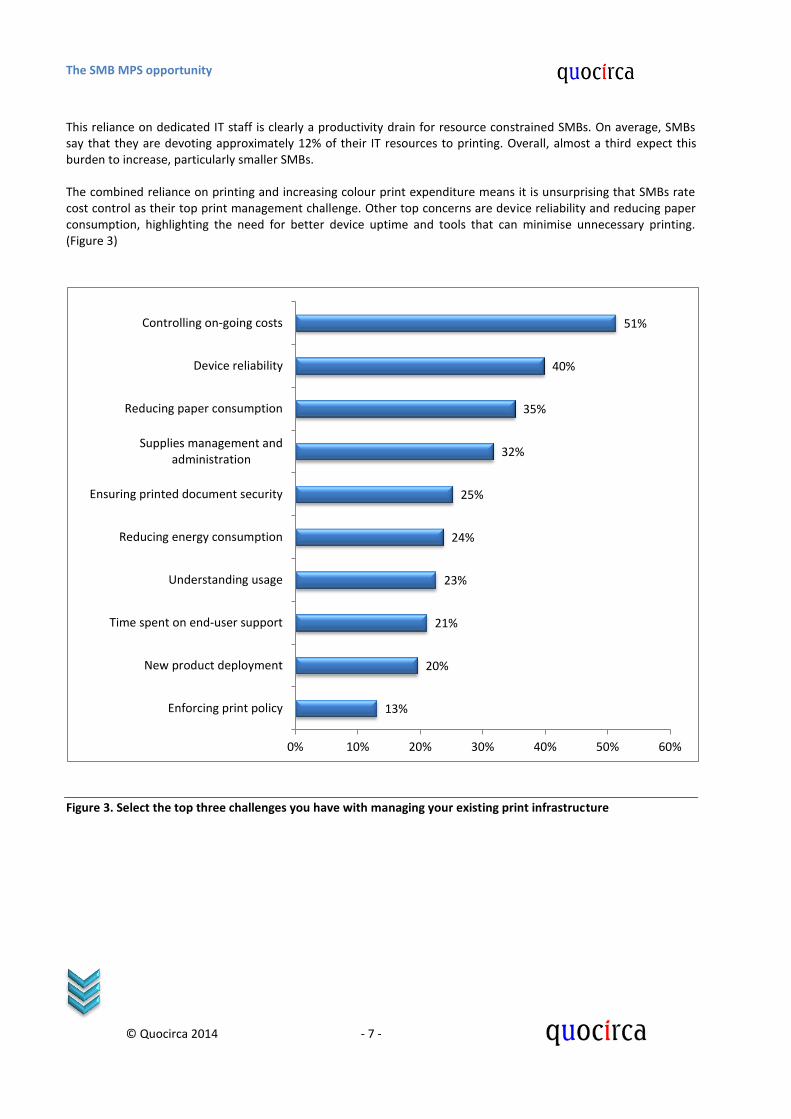

This reliance on dedicated IT staff is clearly a productivity drain for resource constrained SMBs. On average, SMBs say that they are devoting approximately 12% of their IT resources to printing. Overall, almost a third expect this burden to increase, particularly smaller SMBs. The combined reliance on printing and increasing colour print expenditure means it is unsurprising that SMBs rate cost control as their top print management challenge. Other top concerns are device reliability and reducing paper consumption, highlighting the need for better device uptime and tools that can minimise unnecessary printing. (Figure 3)

Figure 3. Select the top three challenges you have with managing your existing print infrastructure

13%

20%

21%

23%

24%

25%

32%

35%

40%

51%

0% 10% 20% 30% 40% 50% 60%

Enforcing print policy

New product deployment

Time spent on end-user support

Understanding usage

Reducing energy consumption

Ensuring printed document security

Supplies management andadministration

Reducing paper consumption

Device reliability

Controlling on-going costs

The SMB MPS opportunity

© Quocirca 2014 - 8 -

MPS adoption

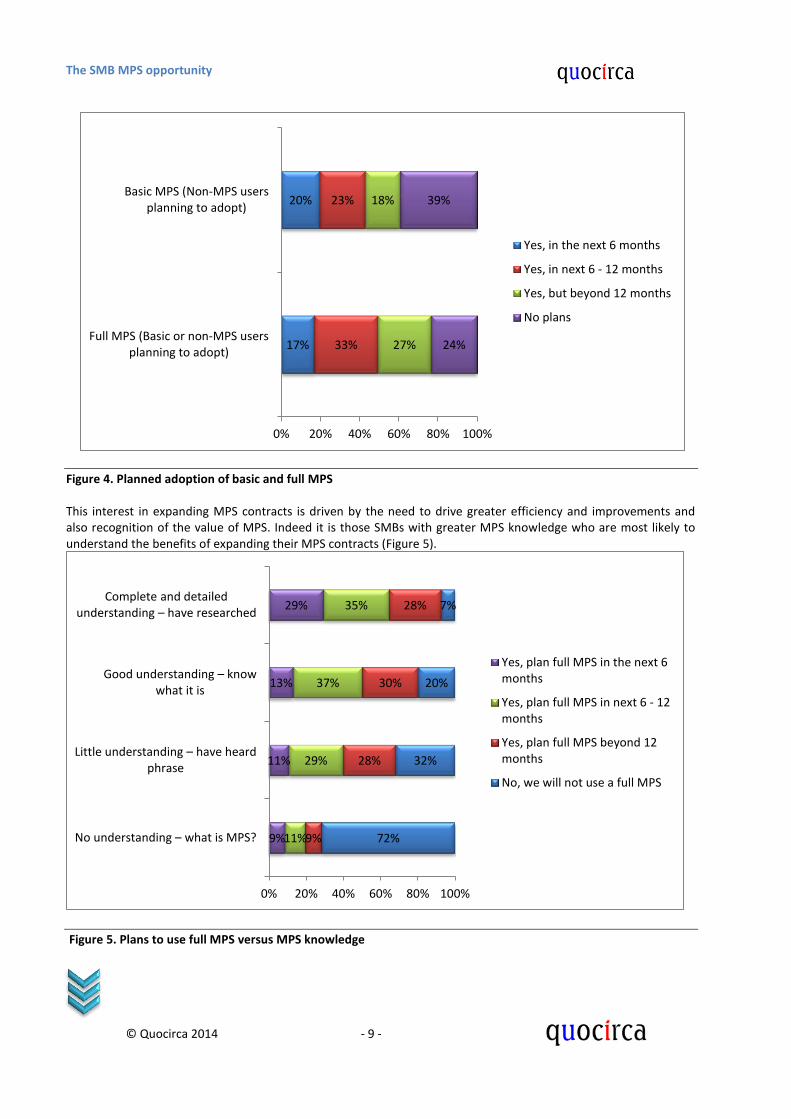

All these challenges can be mitigated through a more effective approach to print management. At a hardware level this means replacing outdated single function devices with modern energy efficient MFPs, a form of device consolidation that reduces the need for costly desktop printers, for instance. However, the most effective approach is an integrated and proactive MPS to provide the insight into print usage and costs, while providing a more predictable cost model. Quocirca estimates that basic print services are becoming more widespread across Europe with distinct regional variations. The UK and Germany are the most mature markets for MPS although, given the diverse spread of SMB sizes, adoption rates tend to be higher amongst larger SMBs. Overall, almost 40% of non-MPS users in this study were planning to adopt some form of MPS. According to Quocirca’s study, by 2014 SMBs are expecting a conservative increase in the devices they purchase under an MPS contract. From an average of 25% they expect this to rise to 28% by the end of 2014, with a slightly higher increase expected among larger SMBs. Quocirca defines MPS adoption across Europe in two main groups:

MPS Converters: These SMBs are moving from a transactional, ad hoc approach of purchasing print to a basic MPS contract. MPS is still patchy in terms of availability, but the majority of these SMBs are aware of MPS and actively investigating. This segment will benefit from basic services initially.

MPS Expanders: MPS is more mature among the SMBs that have moved from basic MPS some years ago. These SMBs are now looking to move to broader full MPS and take advantage of proactive management to improve productivity.

Overall, 43% of SMBs that do not currently use an MPS are planning to adopt a basic MPS within the next 12 months. Meanwhile there is strong interest amongst basic MPS users to expand their MPS contracts – 50% are planning to do this within the next 12 months (Figure 4).

The SMB MPS opportunity

© Quocirca 2014 - 9 -

Figure 4. Planned adoption of basic and full MPS This interest in expanding MPS contracts is driven by the need to drive greater efficiency and improvements and also recognition of the value of MPS. Indeed it is those SMBs with greater MPS knowledge who are most likely to understand the benefits of expanding their MPS contracts (Figure 5).

Figure 5. Plans to use full MPS versus MPS knowledge

9%

11%

13%

29%

11%

29%

37%

35%

9%

28%

30%

28%

72%

32%

20%

7%

0% 20% 40% 60% 80% 100%

No understanding – what is MPS?

Little understanding – have heard phrase

Good understanding – know what it is

Complete and detailed understanding – have researched

Yes, plan full MPS in the next 6months

Yes, plan full MPS in next 6 - 12months

Yes, plan full MPS beyond 12months

No, we will not use a full MPS

17%

20%

33%

23%

27%

18%

24%

39%

0% 20% 40% 60% 80% 100%

Full MPS (Basic or non-MPS usersplanning to adopt)

Basic MPS (Non-MPS usersplanning to adopt)

Yes, in the next 6 months

Yes, in next 6 - 12 months

Yes, but beyond 12 months

No plans

The SMB MPS opportunity

© Quocirca 2014 - 10 -

MPS drivers

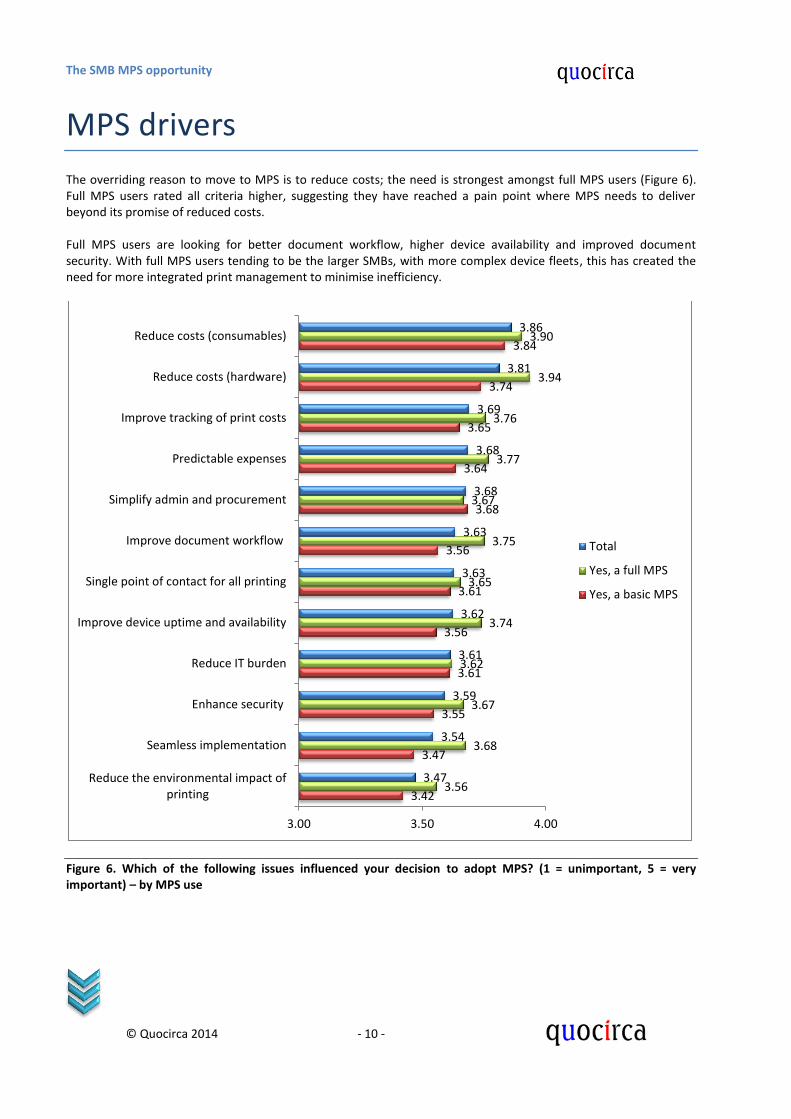

The overriding reason to move to MPS is to reduce costs; the need is strongest amongst full MPS users (Figure 6). Full MPS users rated all criteria higher, suggesting they have reached a pain point where MPS needs to deliver beyond its promise of reduced costs. Full MPS users are looking for better document workflow, higher device availability and improved document security. With full MPS users tending to be the larger SMBs, with more complex device fleets, this has created the need for more integrated print management to minimise inefficiency.

Figure 6. Which of the following issues influenced your decision to adopt MPS? (1 = unimportant, 5 = very important) – by MPS use

3.42

3.47

3.55

3.61

3.56

3.61

3.56

3.68

3.64

3.65

3.74

3.84

3.56

3.68

3.67

3.62

3.74

3.65

3.75

3.67

3.77

3.76

3.94

3.90

3.47

3.54

3.59

3.61

3.62

3.63

3.63

3.68

3.68

3.69

3.81

3.86

3.00 3.50 4.00

Reduce the environmental impact ofprinting

Seamless implementation

Enhance security

Reduce IT burden

Improve device uptime and availability

Single point of contact for all printing

Improve document workflow

Simplify admin and procurement

Predictable expenses

Improve tracking of print costs

Reduce costs (hardware)

Reduce costs (consumables)

Total

Yes, a full MPS

Yes, a basic MPS

The SMB MPS opportunity

© Quocirca 2014 - 11 -

MPS performance

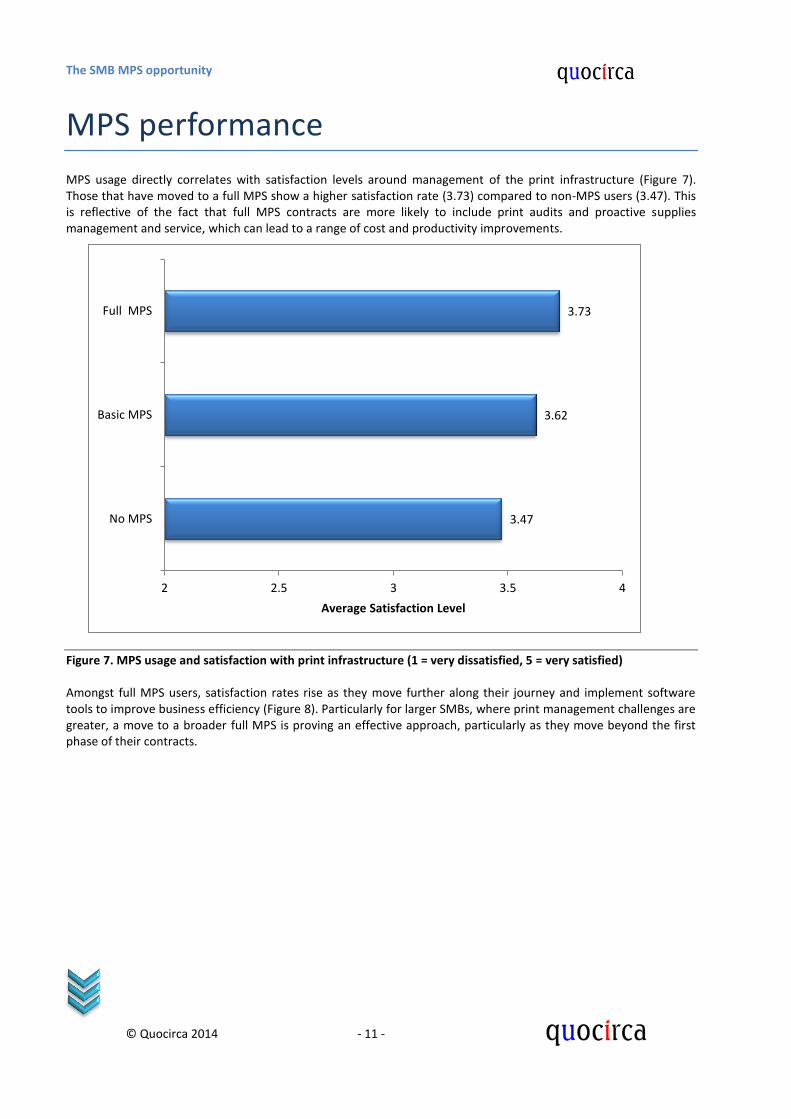

MPS usage directly correlates with satisfaction levels around management of the print infrastructure (Figure 7). Those that have moved to a full MPS show a higher satisfaction rate (3.73) compared to non-MPS users (3.47). This is reflective of the fact that full MPS contracts are more likely to include print audits and proactive supplies management and service, which can lead to a range of cost and productivity improvements.

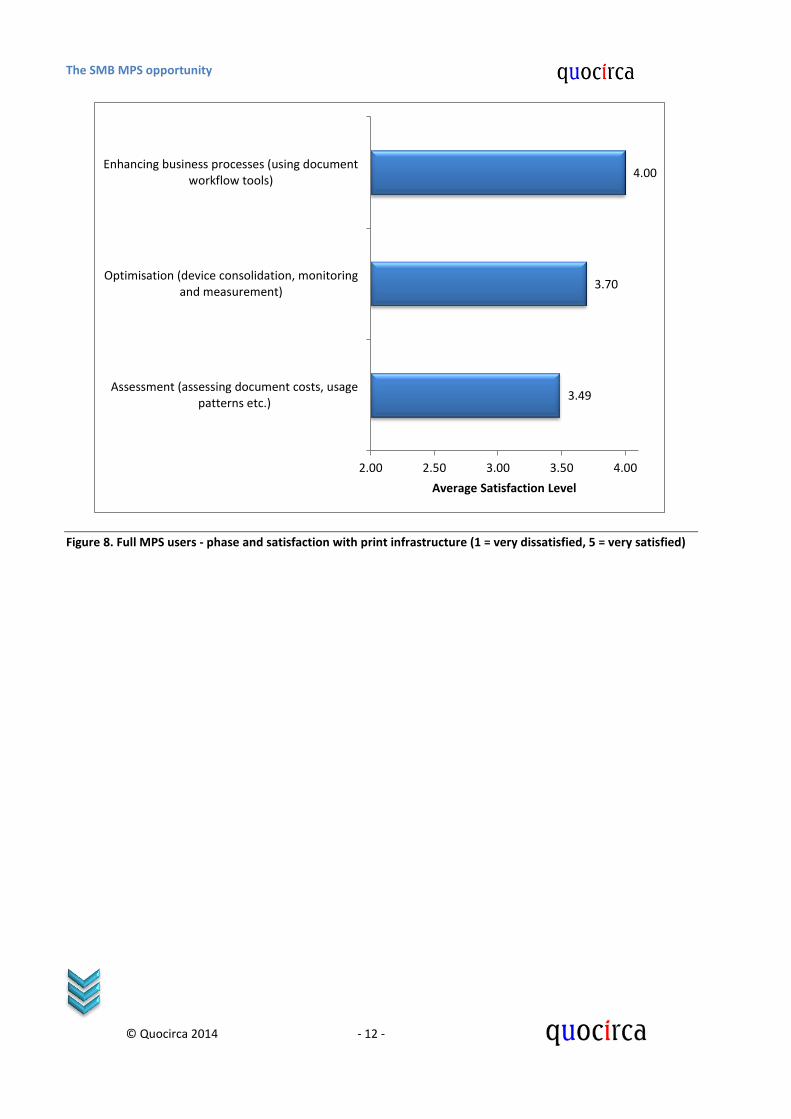

Figure 7. MPS usage and satisfaction with print infrastructure (1 = very dissatisfied, 5 = very satisfied) Amongst full MPS users, satisfaction rates rise as they move further along their journey and implement software tools to improve business efficiency (Figure 8). Particularly for larger SMBs, where print management challenges are greater, a move to a broader full MPS is proving an effective approach, particularly as they move beyond the first phase of their contracts.

3.47

3.62

3.73

2 2.5 3 3.5 4

No MPS

Basic MPS

Full MPS

Average Satisfaction Level

The SMB MPS opportunity

© Quocirca 2014 - 12 -

Figure 8. Full MPS users - phase and satisfaction with print infrastructure (1 = very dissatisfied, 5 = very satisfied)

3.49

3.70

4.00

2.00 2.50 3.00 3.50 4.00

Assessment (assessing document costs, usagepatterns etc.)

Optimisation (device consolidation, monitoringand measurement)

Enhancing business processes (using documentworkflow tools)

Average Satisfaction Level

The SMB MPS opportunity

© Quocirca 2014 - 13 -

MPS inhibitors

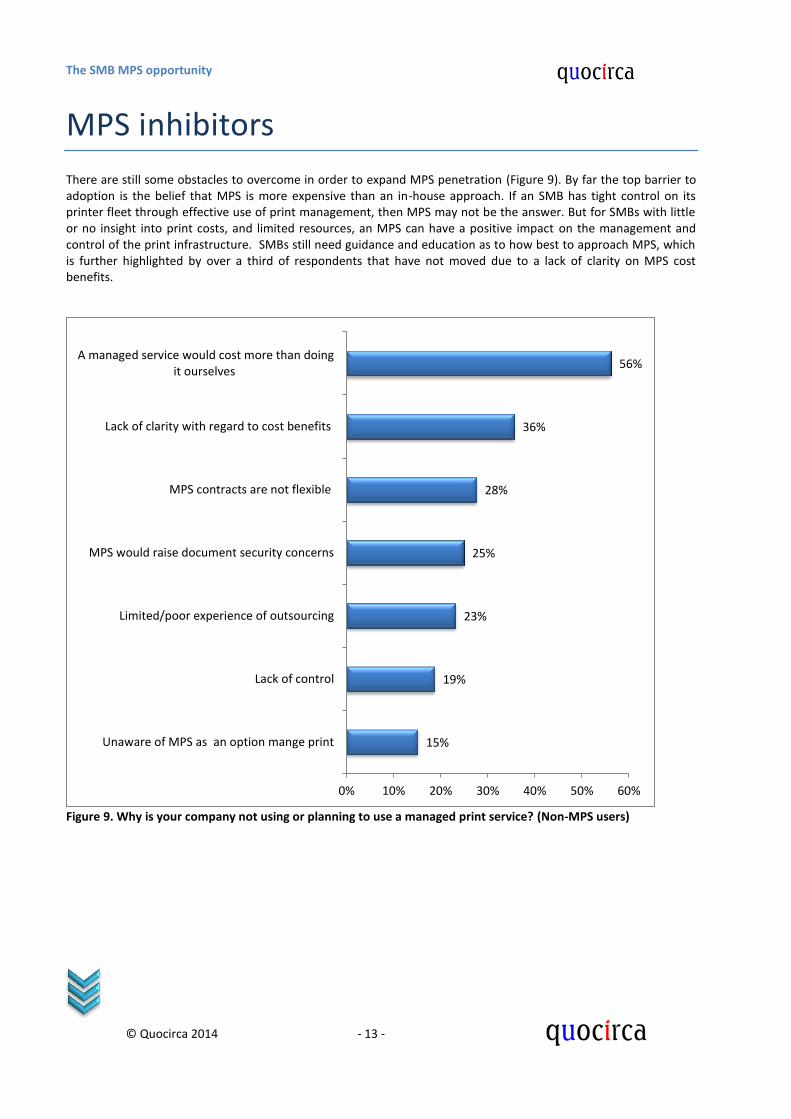

There are still some obstacles to overcome in order to expand MPS penetration (Figure 9). By far the top barrier to adoption is the belief that MPS is more expensive than an in-house approach. If an SMB has tight control on its printer fleet through effective use of print management, then MPS may not be the answer. But for SMBs with little or no insight into print costs, and limited resources, an MPS can have a positive impact on the management and control of the print infrastructure. SMBs still need guidance and education as to how best to approach MPS, which is further highlighted by over a third of respondents that have not moved due to a lack of clarity on MPS cost benefits.

Figure 9. Why is your company not using or planning to use a managed print service? (Non-MPS users)

15%

19%

23%

25%

28%

36%

56%

0% 10% 20% 30% 40% 50% 60%

Unaware of MPS as an option mange print

Lack of control

Limited/poor experience of outsourcing

MPS would raise document security concerns

MPS contracts are not flexible

Lack of clarity with regard to cost benefits

A managed service would cost more than doingit ourselves

The SMB MPS opportunity

© Quocirca 2014 - 14 -

The solutions opportunity

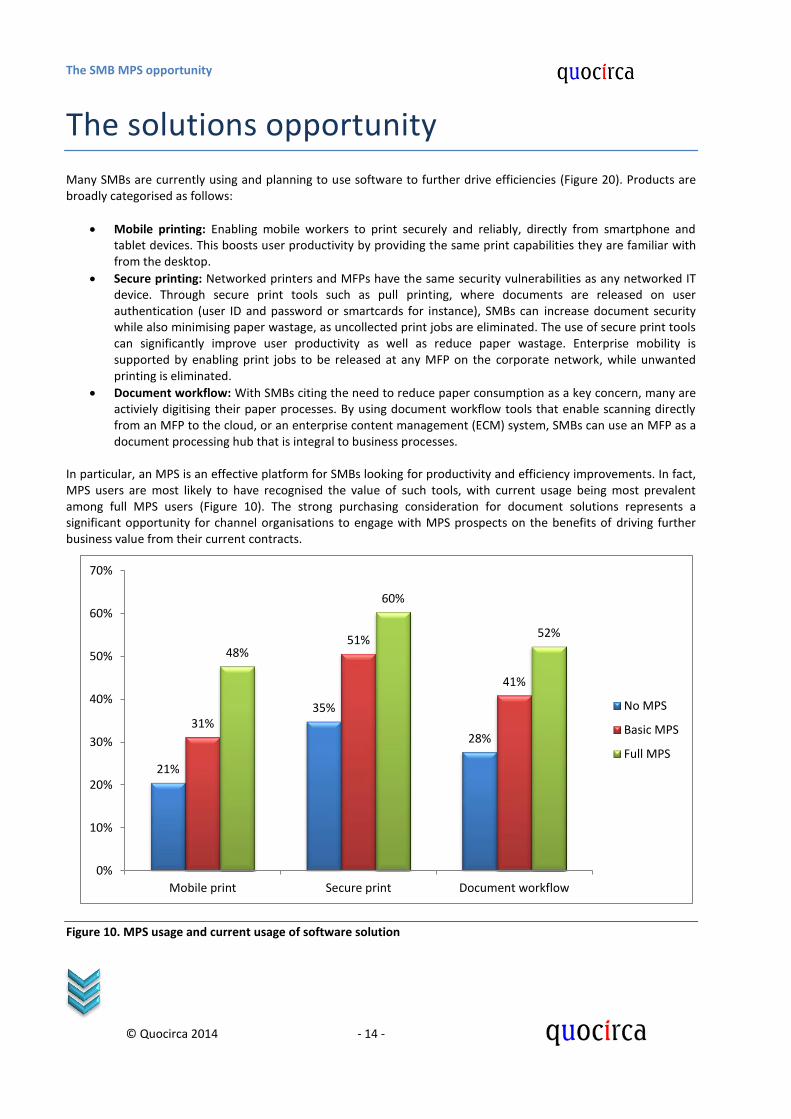

Many SMBs are currently using and planning to use software to further drive efficiencies (Figure 20). Products are broadly categorised as follows:

Mobile printing: Enabling mobile workers to print securely and reliably, directly from smartphone and tablet devices. This boosts user productivity by providing the same print capabilities they are familiar with from the desktop.

Secure printing: Networked printers and MFPs have the same security vulnerabilities as any networked IT device. Through secure print tools such as pull printing, where documents are released on user authentication (user ID and password or smartcards for instance), SMBs can increase document security while also minimising paper wastage, as uncollected print jobs are eliminated. The use of secure print tools can significantly improve user productivity as well as reduce paper wastage. Enterprise mobility is supported by enabling print jobs to be released at any MFP on the corporate network, while unwanted printing is eliminated.

Document workflow: With SMBs citing the need to reduce paper consumption as a key concern, many are activiely digitising their paper processes. By using document workflow tools that enable scanning directly from an MFP to the cloud, or an enterprise content management (ECM) system, SMBs can use an MFP as a document processing hub that is integral to business processes.

In particular, an MPS is an effective platform for SMBs looking for productivity and efficiency improvements. In fact, MPS users are most likely to have recognised the value of such tools, with current usage being most prevalent among full MPS users (Figure 10). The strong purchasing consideration for document solutions represents a significant opportunity for channel organisations to engage with MPS prospects on the benefits of driving further business value from their current contracts.

Figure 10. MPS usage and current usage of software solution

21%

35%

28% 31%

51%

41%

48%

60%

52%

0%

10%

20%

30%

40%

50%

60%

70%

Mobile print Secure print Document workflow

No MPS

Basic MPS

Full MPS

The SMB MPS opportunity

© Quocirca 2014 - 15 -

Future outlook

MPS is no longer an emerging model, having achieved mainstream adoption within an increasingly competitive market. The SMB market is large and diverse so a homogenous approach to MPS will not address the varying needs in this segment. For many SMBs, a basic MPS is an essential first step but, with many failing to achieve cost savings expectations, they will need to transition to a full MPS to gain wider benefits. Based on the current and emerging attitudes to MPS found in this study, Quocirca expects the following trends to shape the SMB MPS market in the coming year.

Increased MPS adoption. First time adoption of MPS will increase over the next year, with Quocirca estimating that more than half of SMBs across Europe will be using some form of MPS by 2015. Both France and Spain show signs of momentum while the UK and German markets will lead the transition to broader MPS contracts.

Channel maturity will evolve at a slower pace. With SMBs increasingly confident about moving to MPS, they will be looking for guidance in navigating a diverse and crowded market. Quocirca’s channel MPS study revealed that many resellers are still finding their feet with MPS. Vendors will need to accelerate this transition to fill the gap rapidly between SMB demand and channel capability.

MPS choice will expand. Most printer vendors are driving broader channel engagement through a range of new and expanded MPS offerings. However, the printer channel also faces emerging competition from managed IT service providers, which are also looking to expand their services portfolio to encompass print. SMBs will benefit from the wider choice, but will need to carefully evaluate the credentials and track record of potential MPS providers.

The cloud will have a positive impact. Almost 70% of resellers indicated that the cloud was making it easier to sell MPS. As SMBs become comfortable with the utility approach to IT consumption, the cloud will be a core enabler for MPS. This will also be driven by broader convergence around mobility, which will expand the need for mobile and cloud connected MFPs.

A hybrid approach to MPS. SMBs estimate that 28% of new print devices will be purchased under an MPS contract by 2015. This reflects that the vast majority of SMBs will follow a ‘hybrid’ strategy of both transactional hardware purchasing and contractual approaches. As MPS proves successful, there will be the opportunity for channel partners to manage a wider device fleet – but the channel must be able to support, service and monitor a range of devices in order to address this need.

Smart MFPs will be key to success. Printer and MFP technology innovation around BYOD, Big Data and Apps will enable channel partners to promote the document integration (capture and routing) capabilities of MFPs as a means to accelerate the shift to document workflows. Energy efficient and cloud connected MFPs will become a more common feature in MPS contracts, and will help boost productivity and drive efficiencies.

New billing models will emerge. MPS vendors are experimenting with different billing models. Although pay as you go will continue to stimulate interest, and may work for SMBs with irregular print requirements, it is likely that many SMBs will prefer the predictability of monthly or quarterly costs.

Service level quality. SMB’s reliance on printing means they cannot afford the disruption that is caused by printer downtime. As such, MPS contracts will become more standardised around service levels, and MPS vendors will seek to differentiate on service response times.

References 1 http://ec.europa.eu/enterprise/policies/sme/index_en.htm

2 Spiceworks, State of SMB IT report, 2013

The SMB MPS opportunity

© Quocirca 2014 - 16 -

Appendix – Survey demographics

Figure 11. Organisation size by country

Figure 12. Industry sector by country

33%

33%

33%

33%

33%

33%

33%

33%

33%

33%

33%

33%

33%

33%

33%

0% 20% 40% 60% 80% 100%

Spain

Sweden

Germany

France

UK

50 - 99 employees

100 - 249 employees

250 - 500 employees

18%

16%

21%

17%

17%

23%

16%

11%

15%

23%

14%

11%

18%

17%

13%

23%

23%

19%

17%

20%

17%

8%

21%

17%

19%

21%

19%

23%

15%

19%

13%

15%

15%

7%

9%

12%

0% 20% 40% 60% 80% 100%

Total

Spain

Sweden

Germany

France

UK

Business and professionalservices

Financial services

Public sector

Manufacturing

Retail, distribution andtransport

Other commercial

The SMB MPS opportunity

© Quocirca 2014 - 17 -

About Quocirca

Quocirca is a primary research and analysis company specialising in the business impact of information technology and communications (ITC). With world-wide, native language reach, Quocirca provides in-depth insights into the views of buyers and influencers in large, mid-sized and small organisations. Its analyst team is made up of real-world practitioners with first-hand experience of ITC delivery who continuously research and track the industry and its real usage in the markets. Through researching perceptions, Quocirca uncovers the real hurdles to technology adoption – the personal and political aspects of an organisation’s environment and the pressures of the need for demonstrable business value in any implementation. This capability to uncover and report back on the end-user perceptions in the market enables Quocirca to provide advice on the realities of technology adoption, not the promises. Quocirca research is always pragmatic, business orientated and conducted in the context of the bigger picture. ITC has the ability to transform businesses and the processes that drive them, but often fails to do so. Quocirca’s mission is to help organisations improve their success rate in process enablement through better levels of understanding and the adoption of the correct technologies at the correct time. Quocirca has a pro-active primary research programme, regularly surveying users, purchasers and resellers of ITC products and services on emerging, evolving and maturing technologies. Over time, Quocirca has built a picture of long term investment trends, providing invaluable information for the whole of the ITC community. Quocirca works with global and local providers of ITC products and services to help them deliver on the promise that ITC holds for business. Quocirca’s clients include Oracle, IBM, CA, O2, T-Mobile, HP, Xerox, Ricoh and Symantec, along with other large and medium sized vendors, service providers and more specialist firms. Details of Quocirca’s work and the services it offers can be found at http://www.quocirca.com Disclaimer: This report has been written independently by Quocirca Ltd. During the preparation of this report, Quocirca may have used a number of sources for the information and views provided. Although Quocirca has attempted wherever possible to validate the information received from each vendor, Quocirca cannot be held responsible for any errors in information received in this manner. Although Quocirca has taken what steps it can to ensure that the information provided in this report is true and reflects real market conditions, Quocirca cannot take any responsibility for the ultimate reliability of the details presented. Therefore, Quocirca expressly disclaims all warranties and claims as to the validity of the data presented here, including any and all consequential losses incurred by any organisation or individual taking any action based on such data and advice. All brand and product names are recognised and acknowledged as trademarks or service marks of their respective holders.