DIALOGUE - Allianz Global Corporate & Specialty - … us what you think. We look forward to your...

16

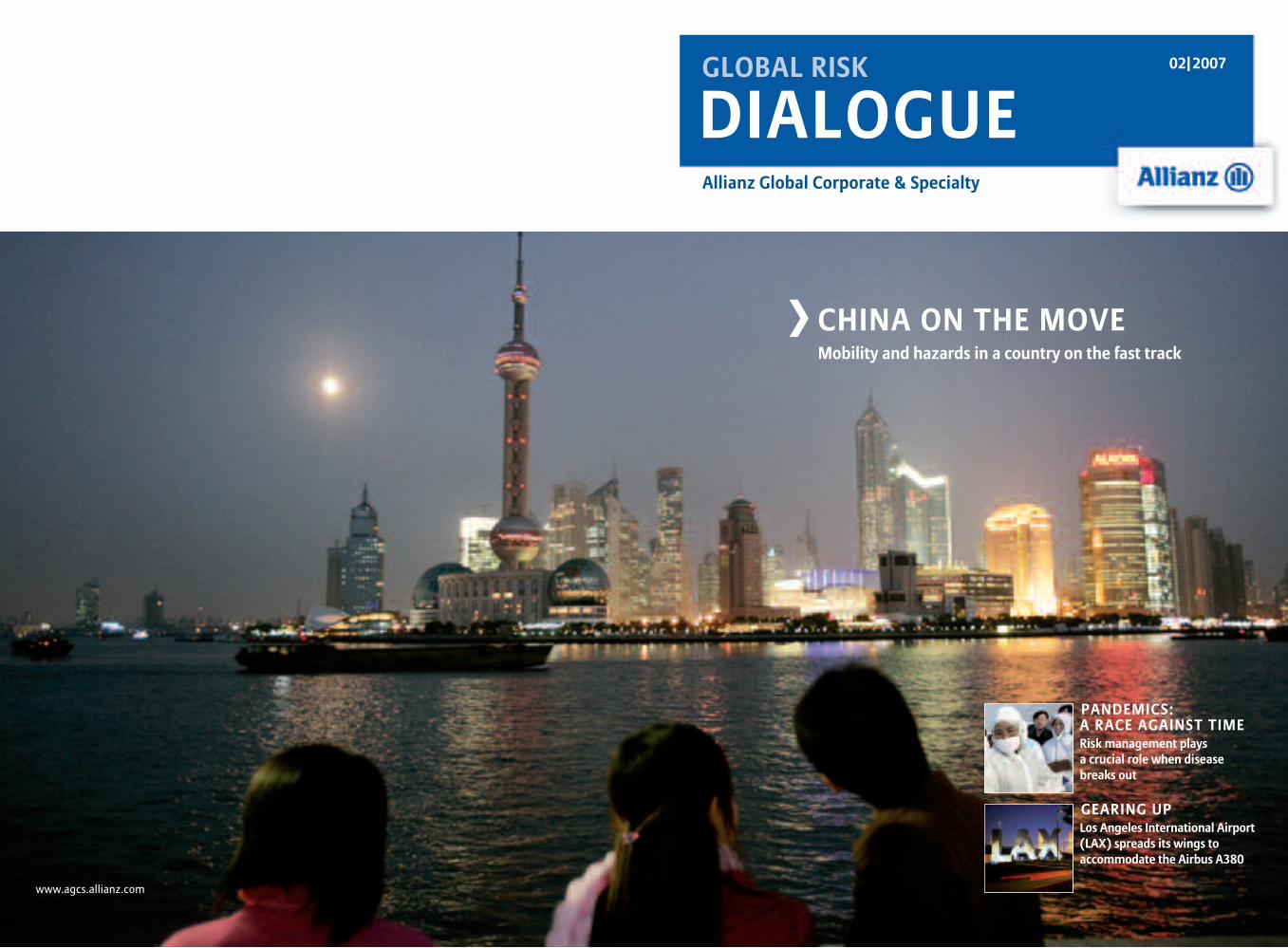

Allianz Global Corporate & Specialty 02| 2007 GLOBAL RISK DIALOGUE CHINA ON THE MOVE Mobility and hazards in a country on the fast track ❯ PANDEMICS: A RACE AGAINST TIME Risk management plays a crucial role when disease breaks out GEARING UP Los Angeles International Airport (LAX) spreads its wings to accommodate the Airbus A380 www.agcs.allianz.com

Transcript of DIALOGUE - Allianz Global Corporate & Specialty - … us what you think. We look forward to your...

Allianz Global Corporate & Specialty

02|2007GLOBAL RISK

DIALOGUE

CHINA ON THE MOVEMobility and hazards in a country on the fast track

❯

PANDEMICS: A RACE AGAINST TIMERisk management plays a crucial role when disease breaks out

GEARING UPLos Angeles International Airport(LAX) spreads its wings toaccommodate the Airbus A380

www.agcs.allianz.com

What are your thoughts? Here is how to reach us. [email protected] www.agcs.allianz.comLAX TAKES OFF 22

EXPERT DAYS WITH AZT 4

WHEN A PANDEMIC HITS 16

CHINA: GOING PLACES 8

TABLE OF CONTENTS

Welcome to Global Risk DIALOGUE. You may know the high-quality client magazine REPORT

that Allianz Global Risks published. With the founding of Allianz Global Corporate & Specialty comes a new platform to express the carrier’s fresh approach, global innovation and focus on clients. So have a look around, andtell us what you think. We look forward to yourcomments and your future interest in DIALOGUE.

N E W SPAGE 04 AZT Expert Days

Specialists gather to discuss reducing CO2 emissions, and Allianz is on the scene.

PAGE 05 In Other NewsAllianz SE gets S&P upgrade · New “cat bond” · Four questions for…

G L O B A L L I N K SPAGE 08 China on the Move

By land, sea and air, the Far Eastern nation is reinventing how its citizens get around.

PAGE 14 Step Up to the RunwaySix seats, flexible scheduling, no lavatories: Will very light jets reinvent aviation?

R I S K F U T U R E SPAGE 16 A Race Against Time

When life-threatening disease breaks out, risk management has a crucial role to play.

PAGE 20 Old Source of New EnergyBiomass: a fuel from humanity’s ancient past, now a fuel for our near future

R E G I O N A L E Y EPAGE 22 Gearing Up

Los Angeles International Airport (LAX) is undergoing a complex restructuring.

PAGE 26 Actuality DivergenceA day in the life of a risk manager overseeing a turbine shipment in India

PAGE 28 Winds of ChangeLiability exposures from new European laws promoting employment diversity

I N C O N C L U S I O NPAGE 30 The Last Word

A commentary by Andreas Richter on cat bonds and gap insurance

PAGE 31 Calendar and imprint

❯❯

Axel Theis | CEO, Allianz Global Corporate & Specialty AG

| 5

Klaus Töpfer, former Executive Direc-tor of the United Nations Environ-ment Program and also former Ger-man environment minister, openedthe conference with a call for non-fossil fuels and decentralized energynets. Allianz Global Corporate & Spe-cialty (AGCS) CEO Axel Theis thendescribed Allianz activities in thearea. The Allianz Group offers poli-cies to promote “green” behaviorand works together with bodies such

as the World Wildlife Fund to raiseawareness about global warming. Inaddition to insuring and providingrisk consulting for the energy sector,AGCS issued its cat bond (see p. 7)partially in response to climate-based peak risks.

STRATEGIC SYNERGIES

After hearing about the latest devel-opments in hydroelectric power, aloss case study of a dam in Brazil and

carbon sequestering to generate CO2-free electricity, participants learnedabout a unique offshore wind farmunder construction off the North Seacoast of Germany. Talks the next dayfocused on risk management in pow-er plants, risk evaluation and loss les-sons learned, as well as insights inbiomass energy risks. ❚

AZT EXPERT DAYS

4 | NEWS

ON JUNE 18–19, ALLIANZ CENTER FOR TECHNOLOGY (AZT) BROUGHTTOGETHER EXPERTS IN THE FIELD OF POWER GENERATION TO DISCUSSTECHNOLOGICAL INNOVATIONS FOR REDUCING CO2 EMISSIONS.

ENERGY AND CLIMATE

Celebrating AZT’s 75th anniversaryduring the Expert Days

At the Expert Days, AZT also looked back on 75 years of tradition, growingfrom its origin as a materials testing office in 1932 to become an integratedpart of Allianz Global Corporate & Specialty today. As part of the conference,it hosted a reception in the new Aviation History Museum in Oberschleiss-heim, Germany, a suburb of Munich.

“Shaping technology in a safe and economic way has been the task of theAllianz Center for Technology for 75 years,” said Lutz Cleeman, director ofAZT. “With a team of experienced engineers and scientists working in thecore skill of damage assessment, AZT is in a unique position for this changefrom a purely technical point of view to an overall consideration of risk, andso will create substantial added value for Allianz and AGCS.” ❚

75 YEARS OF AZTA N N I V E R S A R Y

JÜRGEN LIESKEAZT Marketing and [email protected]

❯ F O U R Q U E S T I O N S F O R …

DIALOGUE: Chris, what exactlydoes Allianz Risk Transfer (ART) do? FISCHER: In a nutshell, we offer tai-lored, non-commoditized solutionsfor our clients. Those solutions typi-cally bundle insurance and financialmarkets components. In addition, ourcompany is known to break freshground in alternative investmentsand risk solutions. Rather than com-peting with the traditional insuranceand banking products offered by theAllianz Group, we either complementtheir offerings, combine them orcomplete existing programs by fillingin the gaps.

So what areas is ART involved in?We have four distinct business lines.The first is corporate solutions, wherewe provide structured (re)insurancedirectly to the client or the captive.Secondly, we provide unique reinsur-ance solutions (whether for propertycat or specialty lines) that demand

very specific approaches. We’ve alsomade a name for ourselves as solu-tion providers for and investor in thealternative assets markets, our thirdarea, where—for example—we struc-ture film finance solutions togetherwith Fireman’s Fund and Dresdner.Other areas include financial en-hancements, future flow financings,private equity and many others. Ourfourth line is managing risk funds forinvestors, who are looking to co-invest with us into the various riskswe like to write for ourselves such asnatural catastrophe, film finance andcollateralized debt obligations.

What do you enjoy most about ART?That’s easy: We’re right on the pulseof market changes. The beauty ofART, as we say, is that we can writeinsurance, reinsurance and deriva-tives, make investments, and managethird-party assets. Every option is onthe table, and through an iterative

process with our clients we jointlydevelop solutions that fit their specific needs.

What are the big challenges today?One is the soft market. Buyers havelots of leverage for standard insur-ance products, but when you come torisks that have unique or odd charac-teristics, that is where ART comes intoplay. We don’t offer price-based, off-the-shelf solutions but rather look tooffer ones that allow clients to man-age their risk capital with greater certainty. This is best done in a collab-orative process among partners, i.e.,the client and ART. In other areas, theoversupply of liquidity reduces thenumber of opportunities that meetprudent risk-reward standards. Lastly,changes in regulation have an impacton the way we conduct our business.This also creates opportunities for us.At the end of the day, proper under-writing and disclosure will succeed.

… CHRIS FISCHER HIRS, CEO OF ALLIANZ RISK TRANSFER(ART), A WHOLLY-OWNED SUBSIDIARY OF ALLIANZ GLOBALCORPORATE & SPECIALTY

NEWS | 5

Lutz Cleeman, AZT director, speaks to theassembled guests

6 | NEWS

On July 1, Allianz Global Corporate &Specialty began operating in dedi-cated legal offices in Austria andSwitzerland. The carrier assumedthe renewals rights of the corporatebusiness of the leading AustrianProperty/Casualty insurer Allianz Elementar-Versicherungs AG. Thischange created Allianz Global Cor-porate & Specialty Branch Austria.

The same insurance areas fromSwiss entity Allianz Suisse went toAllianz Risk Transfer (ART), a wholly-owned subsidiary (see page 5).

“We are extending the reach andimproving the service levels of thecompany’s operations with the ad-dition of official branch officesacross Europe,” says Euro 8 headUwe Kutschera. “This will allow us to

better focus on and react morequickly to the needs of our clients.”The new dedicated offices in Austriaand Switzerland are the first steps inthis direction. Additional branchesare planned in France, the Nether-lands, Italy, Spain and Belgium. ❚

NEW ORGANIZATIONS FOR AUSTRIA AND SWITZERLAND G R E A T E R I N T E G R A T I O N

UWE KUTSCHERAHead of Euro 8 [email protected]

On July 11, Standard & Poor’s an-nounced that it was raising its long-term counterparty credit and insurerfinancial strength rating for AllianzSE to “AA (stable).”

The rating confirms Allianz’s po-sition among the strongest world-wide players in the insurance indus-try. It applies not only to Allianz SE as a whole but also to its core operat-ing entities, which includes Allianz

Global Corporate & Specialty, theGroup’s newly founded corporate in-surance arm.

This evaluation represents an in-crease of one notch from its previous“AA- (positive outlook).” It is a reflec-tion of both the Group’s improvedprofitability and a favorable view ofits management, “combined withthe expectation that it will continueto execute its strategy,” a statement

from the credit rating agency said.The agency added, “The ratings arefurther supported by Allianz’s verystrong competitive position and fi-nancial flexibility.”

“Instead of growing complacent,it means that we have to continue inthis direction, redoubling our effortsto perform as a global leader,” saysAxel Theis, CEO of Allianz Global Corporate & Specialty. ❚

S&P “AA (STABLE)” UPGRADEC R E D I T R A T I N G

The client emphasis of Allianz Glob-al Corporate & Specialty has led tothe introduction of market manage-ment to optimize client and brokerrelations and boost the carrier’sleading position in corporate insur-ance. In this context, the companyhas created the new function of keyaccount manager as the primaryperson in charge of intensifying un-derwriter contact.

In this way, the carrier will be ableto gain a better understanding of theneeds of clients and brokers throughcloser risk dialogue. As part of a glob-al approach to meeting localized

needs, key account managers willensure consistent offerings and ac-cess best know-how across the widerAllianz Group. They will act as adoor-opener and collaborate withEuler Hermes and Dresdner Klein-wort as well the pension, life, health,affinity and many other Allianz divi-sions. “The decisive factor is not thenumber of account managers but

their qualifications,” explains An-dreas Berger, global head of marketmanagement and communicationat Allianz Global Corporate & Spe-cialty. “We have established a dis-tinct career path and training mod-ules tailored to specific skill andindustry profiles. We’re not sellingcommodities. We’re providing cus-tomized solutions.” ❚

KEY ACCOUNT MANAGER MODEL SPREADSC L I E N T & B R O K E R R E L A T I O N S

Allianz Global Corporate & Specialtyintroduced a catastrophe bond (“catbond”) on April 10 for $150 million. Ittransfers the risk of severe riverfloods in Great Britain and earth-quakes in Canada and the US, exclud-ing California.

The first part of a $1 billion pro-gram, this insurance-linked securityrepresents a flexible tool for optimiz-

ing and managing the carrier’s expo-sure to catastrophic events. It is thefirst cat bond to cover flood risk inGreat Britain. To do this, its archi-tects had to develop a parametric in-dex and post-event process robustand transparent enough to satisfyinvestors and the rating agency,and limit the basis risk for Allianz. The transaction was fronted and

arranged by Swiss Re. The securitieswere issued by Blue Wings Ltd., aCayman Island vehicle, and offer areturn of 3.15 percent over LIBORwith an annualized insurance risk of0.54 percent. S&P gave the bond aBB+ rating. ❚

CAT BOND COVERS FLOODS & EARTHQUAKEI N S U R A N C E - L I N K E D S E C U R I T Y

MARC HANNEBERTHead of Reinsurance [email protected]

Andreas Berger | Allianz Global Corporate & Specialty

The decisive factor is not the number ofaccount managers but their qualifications.

AA (stable) is one of thebest ratings in corporateinsurance

Floods in England caused significant damage, as seen here in Cheltenham, but did not trigger a payment from the cat bond.

CHINA ON THE MOVE

NEW RAIL NETWORKS,INCREASED AIR TRAVEL,MORE CARS: CHINA’S RAPID-LY EXPANDING ECONOMY IS PUTTING HUGE DEMANDSON INFRASTRUCTURE.by Douglas Merrill

GLOBAL LINKS | 9

❯ Since the first opening of the early 1980s, China’s ba-sic allure for businesses has been straightforward:

the world’s most populous nation, potentially its largestmarket and market-friendly policies. After more than adecade of boom, the world’s fastest-growing large econo-my is transforming its transportation infrastructure withsimilar fervor. However, this remarkable expansion inmobility and its many new superlatives like the world’sbusiest port and highest railway also demonstrate thechallenges this rising power present for businesses at-tracted by that allure.

China is climbing steadily upward. Its National Bu-reau of Statistics (NBS) estimates annual GDP growth of11.5 percent in the first half of 2007, a trend that meansChina will probably overtake Germany as the world’sthird-largest economy this year. As recently as 2003, theInternational Monetary Fund was debating whether Chi-na was ranked sixth or seventh.

That said, China still is far from the prosperity of oth-er large economies. Depending on the definitions in-volved, China’s per capita GDP ranks between 80 and 90worldwide. China is on the move, but it still has a longway to go. Its transportation sector mirrors both thisspectacular growth and how much still needs to happen.It also shows the complex interplay of regulatory, envi-ronmental and safety concerns that present obstacles onthe road to greater prosperity.

THE RAILROAD: BACKBONE OF A NATION

One good vantage point to see the country’s changes isthe new railway station atop the Tanggula Pass. At an al-titude of 5,068 meters, it’s the world’s highest station. Itrests on a line that connects the Chinese rail networkwith Lhasa, the Tibetan capital, with tracks laid acrosspermafrost, and in seismically active regions. Travelersenjoy pressurized cars and extra oxygen upon request, aunique onboard amenity. However, this remarkableachievement was also a strong political statement aboutthe integration of Tibet with China that did not go unno-ticed in the foreign press.

A few years ago, the world’s first commercial high-speed magnetic levitation train in Shanghai was alsograbbing headlines, while a damage case associated withits construction demonstrates the importance of global

Five of the world’s 10 busiestports are in China

COVER STORY:

10 | GLOBAL LINKS GLOBAL LINKS | 11

insurance partners in the face of complex local regula-tions. The Shanghai maglev, or Transrapid, connects thecity center with Shanghai’s airport. The train is levitatedby powerful magnets. With effectively no resistance fromthe ground, it reaches a maximum normal operatingspeed of 431 km/h. In test runs, it has exceeded 500 km/hand is hailed as the world’s fastest commercial train.

For this showcase project, its builders employedmaglev technology developed by the Transrapid Consor-tium in Germany but never put to commercial use. Theconsortium contributed key parts and know-how and as-sisted in construction. Required by Chinese law to insurewith a local Chinese company, an arrangement somecountries prefer for foreign partners, the Transrapid Con-sortium used a common strategy for this kind of legisla-tion and purchased additional coverage in its homecountry, in this case from Allianz. As a result, when a de-fective grounding cable led to a major loss, it was able toturn to Allianz for the claim which would have been toohigh for the local insurer to pay.

Beyond these high-profile projects, China’s rail sys-tem is crucial to the country and urgently needs to be up-dated. Leisure travel alone, which was nearly unheard oftwo decades ago, is exploding and putting a huge strainon the country’s railroads. Each year, during the two weeks preceding and following the lunar new year, Chinese traditionally travel to visit family. ExpertsThe country’s shipbuilding industry is booming as well

Source: American Association of Port Authorities

1 SHANGHAI CHINA 443.0 2 SINGAPORE SINGAPORE 423.33 ROTTERDAM NETHERLANDS 376.64 NINGBO CHINA 272.45 TIANJIN CHINA 245.1

WORLD’S BUSIEST PORTS (MILLIONS OF TONS)cargo volume, are in China: Shanghai, Ningbo, Tianjin,Guangzhou and Hong Kong. (Unfamiliar as these namesmay be to Western readers, each city has a population ofat least 6 million.) Four more Chinese ports appear in theinternational top 20. With more than 1555 ships on orderfrom China on Jan. 1, 2007, the country also leads theworld in shipbuilding, and with 25,667 cargo tons underconstruction it is currently third behind Korea and Japanin total tonnage, according to the Institute of ShippingEconomics and Logistics in Bremen, Germany.

CAR SALES BOOMING

China’s streets filled with bicycle riders is an indeliblepart of the nation’s image. Now automobiles are the lordsof the road and fabled cyclists make way. When in July2007 the China Association of Automobile Manufactur-ers announced figures for the first half of the year, it said

The city of Shanghai is returning to its key role in the economy of China

estimate that more than 150 million of these journeys aremade by rail, imposing an extra 1 million to 1.5 millionpassengers per day on the system. This blend of traditionand modernity that typifies contemporary China finds itsparallel in its rail technology. The maglev train may becutting-edge, but China also had steam engines in regu-lar main-line service through late 2005. In fact, the Jining-Tongliao line in northern China that opened in 1995 wasserved exclusively by steam engines until 2004 becauseof the steepness of the grade. Furthermore, most of itstrains today are diesel-powered, a large part of China’sgrowing demand for oil.

RESURGENT SHIPPING

The futuristic connection between Shanghai’s centerand its airport is appropriate for a city that is returning toits key role in the economy of China. Distrusted in earlieryears of communist rule, the city has come roaring backas an international point of entry. After jockeying withRotterdam and Singapore through much of the 1990s forthe title of the world’s busiest port, Shanghai is now ontop, handling 443 million tons of freight in 2005, the lat-est year for which comparative figures are available. Incontainerized traffic, Singapore still holds the top slot,followed by Hong Kong, Shanghai and Shenzhen.

Nor does Shanghai have shipping all to itself. Five of the world’s 10 busiest ports, as measured by total

COUNTRY 2007 2015 EST.

1 CHINA 1,322 1,3932 INDIA 1,130 1,2603 UNITED STATES 301 3264 INDONESIA 235 2475 BRAZIL 190 209

POPULATION (MILLIONS)

Source: US Census, CIA World Factbook, UN Secretariat

GLOBAL LINKS | 13

that sales were up 25.9 percent over 2006, exceeding expectations. From January to June, 3.08 million passen-ger vehicles were sold nationwide. This compares withapproximately 800,000 as recently as 2001.

But the continuous rise in automobile ownershiphas brought significant environmental issues, particu-larly air quality. In July 2007, the mayor of Shenzhen, acity of approximately 10 million residents just north of

Source: Allcountries.org, Chinese National Bureau of Statistics

Length of railways in operation 74,408Length of navigable inland waterways 123,337Total length of highways 1,870,661

Of which expressway 34,288first class 33,522second class 231,715

CHINA’S TRANSPORTATION INFRASTRUCTURE (KM)

COUNTRY PERCENTAGE RANK

CHINA 37 149INDIA 28 177UNITED STATES 77 45INDONESIA 42 139BRAZIL 82 38

Source: UN Secretariat, Population Division; national censuses

URBANIZATION IN COMPARISON

pollution. The city plans to ban significant numbers ofcars from traveling during the Olympics—up to one-third of the 3 million vehicles normally running in thecity—and previewed the effort with a four-day test.

TAKING TO THE SKIES

China is also on the move in the air. With a burgeoningmiddle class, personal travel is becoming increasinglycommon. Chinese civil aviation is integrating with glob-al structures, and growing at the rapid pace that is com-mon throughout the economy. “The Chinese aviation in-dustry is developing at an incredible pace, withdouble-digit growth anticipated for the foreseeable fu-ture,” said Giovanni Bisignani, Director General and CEOof the International Air Transport Association, when hisorganization signed a comprehensive memorandum ofunderstanding with China’s General Administration ofCivil Aviation in August 2006. They are working togetherto bring China up to global standards in many areas ofaviation. Change is rapid. For example, usage of e-ticketsrose from 0.2 percent to 60 percent in the 19 months aftera national e-ticket effort began in 2005.

Significant growth is the rule throughout the avia-tion sector. In 2005, for example, passenger turnover roseby 14.6 percent, cargo turnover by 7.9 percent, and inter-national turnover by 9.2 percent. Nor can those figures beaccounted for by growth from a low base. China’s overallturnover for regular flights in 2005 reached 25.77ton/kilometers, a standard measurement in the indus-try, ranking second in the world after the United States.

Air travel is also becoming integrated into Chinesetraditions. Some 20 million people made the trip homefor lunar new year by plane in 2007, according to the Administration of Civil Aviation, 13 percent more than in 2006. Overfilled airports may soon become as much a holiday tradition in China as they are in other industri-alized nations. ❚

KLAUS VOESTECEO, Allianz Insurance Company Guangzhou [email protected]

LUTZ FULLGRAFHead of Allianz Global Corporate & Specialty DivisionAllianz SE - Reinsurance Branch Asia [email protected]

A new image: cars, not bicycles, now rule the roads

Hong Kong, appealed to residents to stop buying auto-mobiles. “Although I have no legal power to do this, I amasking everyone to not buy cars,” he told a public forumat City Hall. He said that cars cause nearly 70 percent ofthe city’s air pollution, and that people were buying carsfaster than the city could build roads and facilities to ac-commodate them. This led to increasing congestion andthe accompanying emissions. The mayor expects thenumber of cars in Shenzhen to increase by roughly200,000 in 2007, more than the city can handle.

For insurers, this boom also carries a lot of risks. Mostvehicles and drivers are not insured, because incomeshave not yet achieved sufficient levels to finance what isseen as an additional cost for a car, and they are driving onroads not designed for them. However, building bettertransportation infrastructure is similarly difficult from arisk management perspective. “There is a positive move-ment with lots of new standards and regulations,” saysChan Whye Loon, regional manager from the non-lifetreaty division of Allianz SE Reinsurance Branch Asia Pacific, “but their enforcement needs to become moretransparent. It’s moving in the right direction but slowly.”

How many cars are too many? One year before thethe Summer Olympics in Beijing, local and national lead-ers are worried about the quality of air. Visiting the cityfor the one-year countdown celebration, InternationalOlympic Committee president Jacques Rogge said thatsome events might have to be postponed because of air

Air travel in China jumped 13 percent between early 2006 and early 2007

12 | GLOBAL LINKS

14 | GLOBAL LINKS

STEP UP TO THE RUNWAYJET SPEED, FLEXIBILITY ANDCOSTS LESS THAN A HOUSE INLONDON. WILL THE VERY LIGHT JET REMAKE AVIATION?

�Depending on who is talking, the very light jet, or VLJ,is either going to change the way travelers fly, or it’s

going to fall short of its backers’ lofty projections andmerely become the new entry-level personal jet.

The concept of a very small business/personal jetdates back to the late 1970s, when Tony Fox, an Americanentrepreneur, began promoting his idea for the twin-engine Foxjet. In the late 1990s, other entrepreneurs andaviation companies began to come around to his way ofthinking, evolving a new category of small jet that offersabout half a dozen seats for less than $1 million.

A NEW KIND OF PLANE

It has been a long road, but earlier in 2007, Eclipse Avia-tion began delivering the first FAA-certified VLJs. Theyrepresent the first real step toward confounding themany critics of this new form of personal travel. Veteranobservers in the sector now give reasonable odds for success to about half a dozen contenders in the field. In-dustry giant Cessna was actually first to fully certify a VLJ(its Citation Mustang), but did not rush into deliveries after certification. Other companies developing VLJs forcertification and production include Spectrum, Adam,Cirrus, Diamond and Embraer. Honda also sees a marketfor small jets and is in the ring.

Spectrum also did not rush to be first, but is commit-ted with its Independence S-33 and is enthusiastic aboutthe future of the VLJ. “I think it will do for personal air trav-el what cellular technology did for telephones or the Internet has done for information,” explains StefanoSturlese, European CEO of Spectrum Aeronautics. “Youdon’t need to rely on huge infrastructure, but rather cango virtually from point to point at a much larger range ofdestinations at increasingly lower costs.”

It remains to be seen whether hordes of VLJs willdarken the skies carrying regional passengers in an air-taxi role, but would-be operators of VLJ fleets in the Unit-ed States and Europe are convinced they can make theeconomics of such services work, and that the travelingpublic will embrace this alternative to driving and theever more inconvenient airline experience, even thoughit will mean flying with strangers in close quarters, oftenwithout a lavatory.

DayJet, an American firm, will be first to take to theskies with its “per-seat, on-demand” air taxi service. Thename neatly conveys its mission: turn trips that wouldnormally require a hotel night into one-day out-and-re-turn itineraries. The price of a ticket will vary with the de-gree of scheduling flexibility the traveler is willing to ac-cept—the more flexible the departure and return times,the cheaper the fare. Complex software will handle the crewing and scheduling and keep enough seats filled

for DayJet to function and make a profit, insists founderand CEO Ed Iacobucci.

A NEW SET OF CHALLENGES

Other related issues that have generated lively discus-sion during the gestation of the VLJs include pilot skills,training and insurance coverage. Professional crews offull-size business jets and jetliners have expressed con-cern about sharing the stratosphere with owner-pilotswho might have previously only flown piston airplanes.All VLJ developers emphasize that they recognize the im-portance of the quality and suitability of the trainingtheir customers will receive. Cessna signed up withFlightSafety, and has distanced itself from the term VLJ,preferring to call the Mustang its “entry-level jet.”

One school of thought in the United States holds thatthe VLJ developers’ rosy predictions have fueled the airline-led movement toward funding aviation’s

infrastructure with user fees, since the forecast hordes ofthese small machines will need airspace and runwayslots that are already alleged to be in short supply. Gener-al aviation operators counter that the argument is bogus,because VLJs—like business jets—will operate mostlyfrom fringe airports and not from the clogged major-cityhubs that are the root cause of much of America’s currentairline congestion woes.

Even if the per-seat, on-demand model falls short ofsome expectations, the VLJ has a bright future as a moreaffordable ticket to jet operations for existing aircraftowners for whom buying a new personal or business jethas been out of reach thus far. z

&www.ainonline.comwww.aviation.com/business

WILLIAM WELBOURNCOO, Allianz Aviation [email protected]

Spectrum Independence put throughits paces in the Utah mountains

(above). The interior of a SpectrumIndependence (inset) provides

fliers with the comforts of a private jet, at a much lower price.

by Nigel Moll

16 | RISK FUTURES

� Ghostly images made their way around the world inthe spring of 2006—government officials and scien-

tists in rubber boots and full-body protective suits bend-ing over the remains of dead swans. Dead birds and lifeless fowl, the emergency slaughter of entire flocks atchicken farms, quarantine zones and police barriers.Bird flu had moved into public consciousness and, withit, the concern that the H5N1 “avian plague” virus mightmutate into a form that would threaten human life. Thencame the all-clear signal. The crisis disappeared asquickly as it had come. The virus passed out of sight andthe pandemic did not occur. Yet.

One year later the much-feared bird flu virus reap-peared, this time with much less resonance in the media.“The question is not whether there will be a pandemic,but rather when,” says Reinhard Kurth, president of theRobert Koch Institute, Berlin. In view of the genetic insta-bility of influenza viruses, it is only a matter of time beforea mutation occurs that is transmissible from human tohuman. Recent dramatic scenarios include the Spanishflu (1918–20), the Asian flu (1957) and the Hong Kong flu(1968), when influenza claimed millions of lives all overthe world (see box next page). In addition to the humantragedy, such events bring huge financial costs to bear.Based on its experience with the epidemic respiratory ill-ness SARS in 2003, the World Bank estimates global costsof approximately $800 billion in the event of a pandemic.

SETTING LIMITS

From a risk perspective, pandemics are classic catastro-phe scenarios. They are similar to earthquakes and tor-nadoes—events “with potentially large impacts but, atthe same time, low probability of occurrence,” accordingto Andreas Schaer of the Allianz Global Corporate &

Specialty PharmChem team in Zurich. The conse-quences of a pandemic could be very serious because ofthe associated restrictions on public and economic life.“The insurance industry needs to focus its attention notonly on the impacts in the areas of life, property andhealth insurance, but also on financial markets,” he says.“In serious events, investors would prefer to transfer theircapital to assets that are believed to be more secure.”

Under such circumstances, when there is pressingneed for rapid development of vaccines at the same timethat clinical testing has only limited feasibility, liabilityissues for vaccine manufacturers take on particular significance. “Pandemics require thinking outside thebox,” says Johannes Klose of the Zurich PharmChemteam. “At some point, the welfare of the community atlarge becomes the issue. Indemnity, meanwhile, is acomplicated aspect, because it is regulated differently inevery country.”

PLANNING AHEAD

What do these concerns add up to for dealing with a pan-demic? What is needed, above all, is continuous profes-sional work on the part of government agencies, the sci-entific and research communities, and all stakeholdersin the risk industry. The basis for such work is provided bythe six-step model for risk assessment propagated by theWorld Health Organization (WHO). Currently the assess-

PANDEMICS: A RACE AGAINST TIME WHEN VIRUSES CAUSE NATIONAL OR GLOBAL OUTBREAKS OF LIFE-THREATENING DISEASES, RISK MANAGEMENT HAS A CRUCIALROLE TO PLAY IN THE RACE AGAINST TIME.

by Marcus Schick

At the height of the SARS outbreak in 2003, Hong Kong residents wore protective masks against

contagion (above). Ducks in China awaitingimmunization against avian flu in 2005 (below).

18 | RISK FUTURES RISK FUTURES | 19

ment stands at Phase III, the beginning of the alarmphase. At this level, there is a regular exchange of infor-mation among WHO, government agencies and the scientific community. “The excitement in the media in2006 and this bird flu, which was not transmitted to hu-mans after all, did do some good,” says Klose. “It generat-ed helpful political pressure.” For example, he notes, thedrug industry pledged to build up its production capaci-ty for vaccines and to keep reserve production capacityavailable for use in the event of large-scale diseases.

Time saved by planning and preparation is always asignificant factor in the defense against a pandemic. Forexample, production of an adequate amount of avian fluvaccines requires that genetically modified H5N1 seedviruses be provided to WHO reference labs. Schaer notesthat “approximately 20 pharmaceutical companies are

facto license through their clinical data, providing thebasis for quick licensing of an actual pandemic vaccinein a serious situation. “The license will go through in afew days, because no more clinical studies will have to beconducted before the granting of the license,” says vac-cine expert Norbert Hehme.

PRODUCING VACCINES

Solutions have been found to many puzzling aspects ofthe H5N1 virus, which initially had been regarded as unsolvable. “As long as human-to-human transmissionis not taking place on a large scale, time is on our side,”Schaer says. “On the technical front, many innovations

In addition to the vaccines that are intended to pro-vide specific protection against the pathogen causingthe pandemic, broad-spectrum vaccines are also in theprocess of being developed and licensed. The latter vac-cines can be used before the outbreak of the pandemicillness, but the down-side of the broad-spectrum ap-proach is that it does not offer specific protection againstthe particular virus strain. z

The question is not whetherthere will be apandemic, butrather when.

Reinhard Kurth | President of the Robert Koch Institute

Facilities for mass production of influenza vaccines at GlaxoSmithKline

in Dresden, Germany (left)

are showing progress.” Research into transmission andvaccination, he notes, is currently taking place at the level of cell cultures.

Until recently, the production of influenza vaccinesrelied on fertile eggs, and production volume had beenlimited by capacity for inoculating these eggs. “The com-position of the vaccine against avian flu is already de-scribed in the seed vaccine dossiers; a broad-spectrumvaccine in the process of development and licensing,” explains Schaer. “The final work on the puzzle will entailfinding and placing the last decisive piece in the generalpicture.” This will require no small amount of luck inchallenging circumstances.

DISEASE TIME CASUALTIES

Spanish flu 1918–20 40–50 millionAsian flu 1957 1–2 millionHong Kong flu 1968 ca. 1 million

Two of the three catastrophic pandemic pathogens of the last century came from the mingling of bird flu and human flu viruses. The pathogen associated with the Spanish flu developed into a human-transmissibleform on its own.

PANDEMICS IN THE 20TH CENTURY

Sources: WHO, BBC, globalsecurity.org

&

JOHANNES KLOSE ANDREAS SCHAERPharmChem Team PharmChem [email protected] [email protected]

www.who.org

doing research in this area according to the data of theInternational Federation of Pharmaceutical Manufactur-ers and Associations (IFPMA), headquartered in Geneva,Switzerland. Nevertheless, the bottom line is that thepandemic pathogen’s genetic code is still the greatestunknown in this calculation.”

Especially in the race against time that a pandemicinherently creates, innovative research is needed. In thepast year, for example, GlaxoSmithKline (GSK) submitteda “mock-up” vaccine dossier to the European MedicinesAgency (EMEA). Model vaccines, which replicate the basic genetic structure of the pathogen in the broadestpossible way, lay the foundation for an interim de

OLD SOURCE OF NEW ENERGY

20 | RISK FUTURES

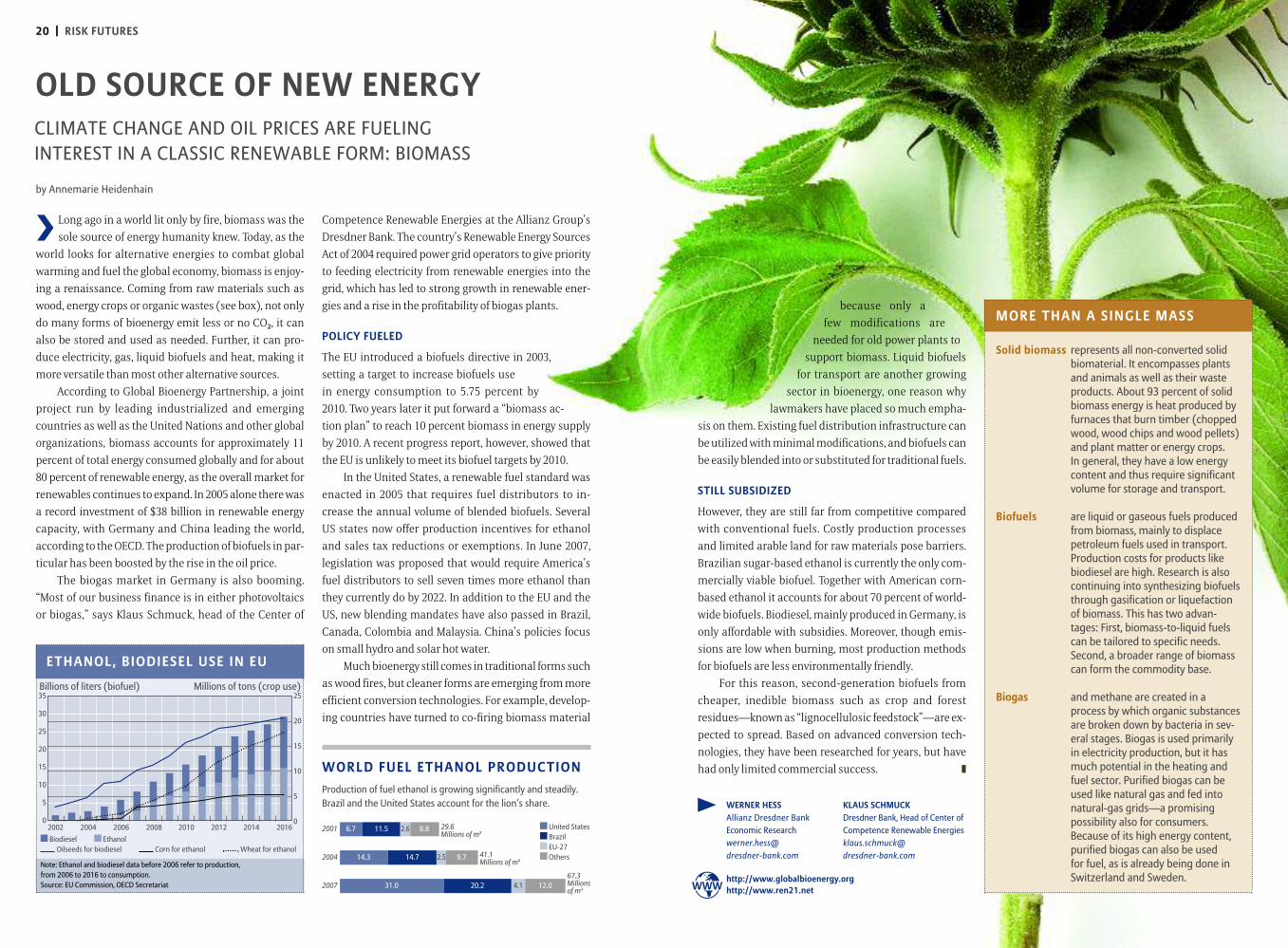

� Long ago in a world lit only by fire, biomass was thesole source of energy humanity knew. Today, as the

world looks for alternative energies to combat globalwarming and fuel the global economy, biomass is enjoy-ing a renaissance. Coming from raw materials such aswood, energy crops or organic wastes (see box), not onlydo many forms of bioenergy emit less or no CO2, it canalso be stored and used as needed. Further, it can pro-duce electricity, gas, liquid biofuels and heat, making itmore versatile than most other alternative sources.

According to Global Bioenergy Partnership, a jointproject run by leading industrialized and emergingcountries as well as the United Nations and other globalorganizations, biomass accounts for approximately 11percent of total energy consumed globally and for about80 percent of renewable energy, as the overall market forrenewables continues to expand. In 2005 alone there wasa record investment of $38 billion in renewable energy capacity, with Germany and China leading the world, according to the OECD. The production of biofuels in par-ticular has been boosted by the rise in the oil price.

The biogas market in Germany is also booming.“Most of our business finance is in either photovoltaics or biogas,” says Klaus Schmuck, head of the Center of

Competence Renewable Energies at the Allianz Group’sDresdner Bank. The country’s Renewable Energy SourcesAct of 2004 required power grid operators to give priorityto feeding electricity from renewable energies into thegrid, which has led to strong growth in renewable ener-gies and a rise in the profitability of biogas plants.

POLICY FUELED

The EU introduced a biofuels directive in 2003,setting a target to increase biofuels usein energy consumption to 5.75 percent by2010. Two years later it put forward a “biomass ac-tion plan” to reach 10 percent biomass in energy supplyby 2010. A recent progress report, however, showed thatthe EU is unlikely to meet its biofuel targets by 2010.

In the United States, a renewable fuel standard wasenacted in 2005 that requires fuel distributors to in-crease the annual volume of blended biofuels. Several US states now offer production incentives for ethanoland sales tax reductions or exemptions. In June 2007, legislation was proposed that would require America’sfuel distributors to sell seven times more ethanol thanthey currently do by 2022. In addition to the EU and theUS, new blending mandates have also passed in Brazil,Canada, Colombia and Malaysia. China’s policies focuson small hydro and solar hot water.

Much bioenergy still comes in traditional forms suchas wood fires, but cleaner forms are emerging from moreefficient conversion technologies. For example, develop-ing countries have turned to co-firing biomass material

because only afew modifications are

needed for old power plants tosupport biomass. Liquid biofuels

for transport are another growingsector in bioenergy, one reason why

lawmakers have placed so much empha-sis on them. Existing fuel distribution infrastructure canbe utilized with minimal modifications, and biofuels canbe easily blended into or substituted for traditional fuels.

STILL SUBSIDIZED

However, they are still far from competitive comparedwith conventional fuels. Costly production processesand limited arable land for raw materials pose barriers.Brazilian sugar-based ethanol is currently the only com-mercially viable biofuel. Together with American corn-based ethanol it accounts for about 70 percent of world-wide biofuels. Biodiesel, mainly produced in Germany, isonly affordable with subsidies. Moreover, though emis-sions are low when burning, most production methodsfor biofuels are less environmentally friendly.

For this reason, second-generation biofuels fromcheaper, inedible biomass such as crop and forestresidues—known as “lignocellulosic feedstock”—are ex-pected to spread. Based on advanced conversion tech-nologies, they have been researched for years, but havehad only limited commercial success. z

M O R E T H A N A S I N G L E M A S S

Solid biomass represents all non-converted solidbiomaterial. It encompasses plantsand animals as well as their wasteproducts. About 93 percent of solidbiomass energy is heat produced byfurnaces that burn timber (choppedwood, wood chips and wood pellets)and plant matter or energy crops. In general, they have a low energycontent and thus require significantvolume for storage and transport.

Biofuels are liquid or gaseous fuels producedfrom biomass, mainly to displacepetroleum fuels used in transport.Production costs for products likebiodiesel are high. Research is alsocontinuing into synthesizing biofuelsthrough gasification or liquefactionof biomass. This has two advan-tages: First, biomass-to-liquid fuelscan be tailored to specific needs.Second, a broader range of biomasscan form the commodity base.

Biogas and methane are created in aprocess by which organic substancesare broken down by bacteria in sev-eral stages. Biogas is used primarilyin electricity production, but it hasmuch potential in the heating andfuel sector. Purified biogas can beused like natural gas and fed intonatural-gas grids—a promising possibility also for consumers.Because of its high energy content,purified biogas can also be used for fuel, as is already being done inSwitzerland and Sweden.

by Annemarie Heidenhain

WERNER HESS KLAUS SCHMUCKAllianz Dresdner Bank Dresdner Bank, Head of Center ofEconomic Research Competence Renewable Energies werner.hess@ [email protected] dresdner-bank.com

CLIMATE CHANGE AND OIL PRICES ARE FUELING INTEREST IN A CLASSIC RENEWABLE FORM: BIOMASS

E T H A N O L , B I O D I E S E L U S E I N E U

25

20

15

10

5

0

35

30

25

20

15

10

5

0

Billions of liters (biofuel) Millions of tons (crop use)

Biodiesel EthanolOilseeds for biodiesel Corn for ethanol Wheat for ethanol

Note: Ethanol and biodiesel data before 2006 refer to production, from 2006 to 2016 to consumption.Source: EU Commission, OECD Secretariat

2002 2004 2006 2008 2010 2012 2014 2016

W O R L D F U E L E T H A N O L P R O D U C T I O NProduction of fuel ethanol is growing significantly and steadily.Brazil and the United States account for the lion’s share.

2001

2004

United StatesBrazilEU-27Others

6.7 11.5 8.8

14.3 14.7 9.7

2007 31.0 20.2 12.04.1

29.6 Millions of m3

41.1 Millions of m3

67.3Millions of m3 & http://www.globalbioenergy.org

http://www.ren21.net

2.6

2.5

22 | REGIONAL EYE

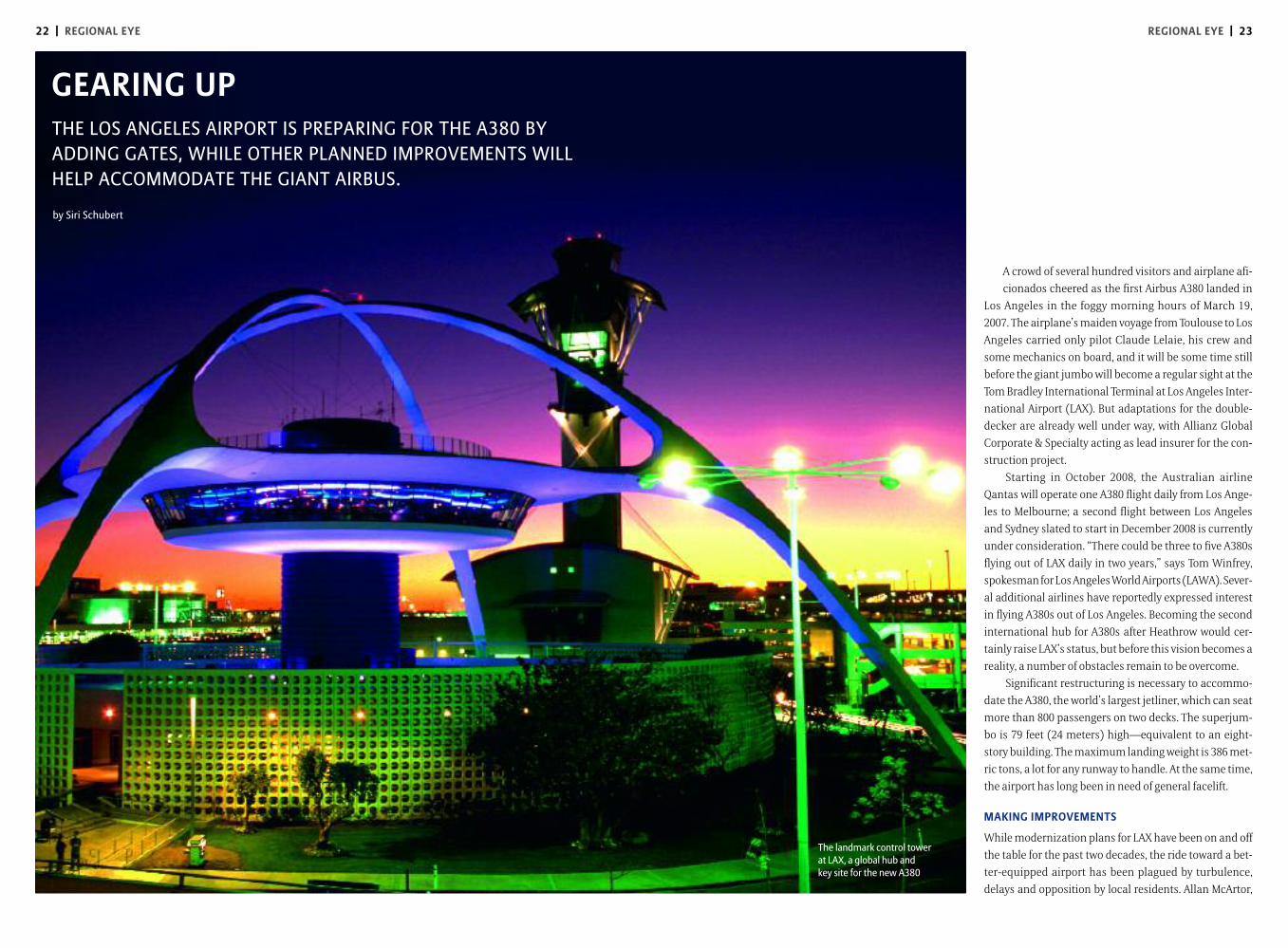

GEARING UP

by Siri Schubert

THE LOS ANGELES AIRPORT IS PREPARING FOR THE A380 BYADDING GATES, WHILE OTHER PLANNED IMPROVEMENTS WILLHELP ACCOMMODATE THE GIANT AIRBUS.

�A crowd of several hundred visitors and airplane afi-cionados cheered as the first Airbus A380 landed in

Los Angeles in the foggy morning hours of March 19,2007. The airplane’s maiden voyage from Toulouse to LosAngeles carried only pilot Claude Lelaie, his crew andsome mechanics on board, and it will be some time stillbefore the giant jumbo will become a regular sight at theTom Bradley International Terminal at Los Angeles Inter-national Airport (LAX). But adaptations for the double-decker are already well under way, with Allianz GlobalCorporate & Specialty acting as lead insurer for the con-struction project.

Starting in October 2008, the Australian airline Qantas will operate one A380 flight daily from Los Ange-les to Melbourne; a second flight between Los Angelesand Sydney slated to start in December 2008 is currentlyunder consideration. “There could be three to five A380sflying out of LAX daily in two years,” says Tom Winfrey,spokesman for Los Angeles World Airports (LAWA). Sever-al additional airlines have reportedly expressed interestin flying A380s out of Los Angeles. Becoming the secondinternational hub for A380s after Heathrow would cer-tainly raise LAX’s status, but before this vision becomes areality, a number of obstacles remain to be overcome.

Significant restructuring is necessary to accommo-date the A380, the world’s largest jetliner, which can seatmore than 800 passengers on two decks. The superjum-bo is 79 feet (24 meters) high—equivalent to an eight-story building. The maximum landing weight is 386 met-ric tons, a lot for any runway to handle. At the same time,the airport has long been in need of general facelift.

MAKING IMPROVEMENTS

While modernization plans for LAX have been on and offthe table for the past two decades, the ride toward a bet-ter-equipped airport has been plagued by turbulence,delays and opposition by local residents. Allan McArtor,

The landmark control tower at LAX, a global hub and key site for the new A380

REGIONAL EYE | 23

24 | REGIONAL EYE REGIONAL EYE | 25

chairman of Airbus North American Holdings Inc., criticized the lack of momentum in an interview with theLos Angeles Business Journal earlier in 2007. “If L.A. can’tmodernize itself to attract these new airplanes, thenthey’re likely to go elsewhere,” he said.

Completion of the complex restructuring projectnow ranks high on LAX’s agenda. To accommodate thenew planes and the 79 million passengers that LAX ex-pects after the renovation is finished, the airportlaunched a 4-phase construction project approved by theFederal Aviation Agency (FAA) in 2005: moving the southrunway, building a new taxiway, upgrading the interna-tional terminal and improving baggage handling andscreening for the whole facelift.

TAKING OFF

While the costs of modernization at LAX total around$1.6 billion, $121 million are being spent on upgrades re-lated directly to the A380. Among other things, the mas-ter plan calls for two additional gates for the A380 at theTom Bradley International Terminal. One of the gates atthe southern tip of the terminal, costing $9 million, hasbeen completed; the other one, at the north end, budget-ed at around $30 million, will be ready soon. The runwayproject will also provide more room and thus directlybenefit the A380 with its 261-foot wingspan. This phaseshould finish by spring 2008, in time for the L.A.-Melbourne connection.

The interior terminal work should be completed byabout 2010. This work is slower, more complex and moreopen to loss damage because the terminal will be in gener-al use. “Construction will be in close proximity to runningoperations and already existing structures,” explains CarlDoby, director of technical underwriting at the Burbank,California, unit of Allianz Global Corporate & Specialty.

A Master Builder’s Policy insures the whole project.This includes the work on the international terminal for

over $500 million as well as the $235 million runway andtaxiway work and the $275 million in-line baggage han-dling upgrades. The Master Builder’s Policy is a single pol-icy with clearly defined sub-policies covering the individ-ual phases. “These phases represented the greatestchallenge because they begin and end at different times,”Doby recalls. “With this flexible policy, the part that coverseach phase is only triggered when it begins.”

The airport competition is not standing still. SanFrancisco International has already received FAA A380certification and has five gates ready. A380s have alreadytouched down at New York’s JFK airport, Chicago’s O’Hare,and Washington’s Dulles International airport as part oftheir U.S. test flight route. For LAX, only fast moderniza-tion can ensure the other airports do not steal the spot-light associated with landing the giant jumbo-jets. z

& www.laxmasterplan.orgwww.airports.org

Source: Airports Council International

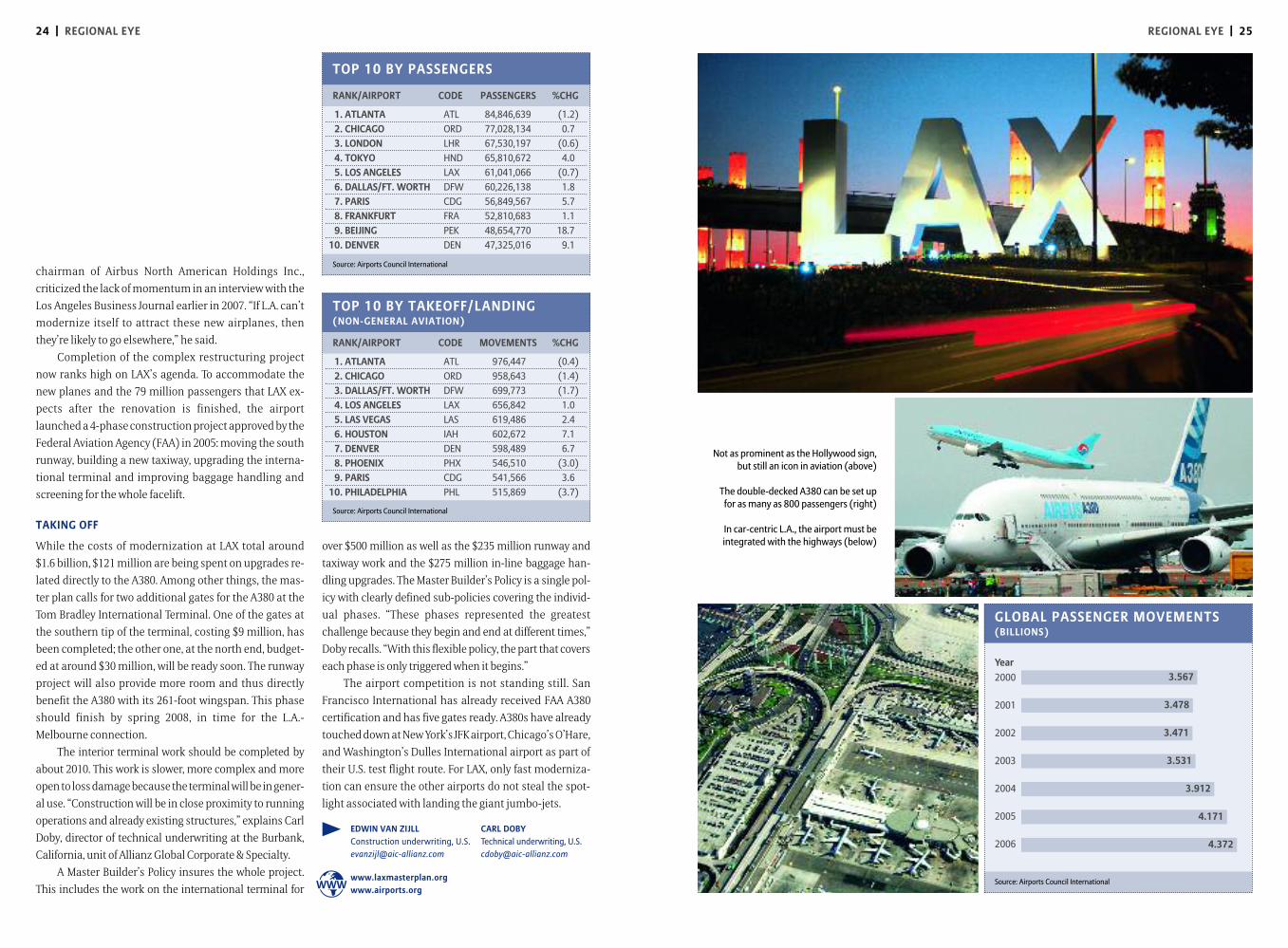

Not as prominent as the Hollywood sign,but still an icon in aviation (above)

The double-decked A380 can be set up for as many as 800 passengers (right)

In car-centric L.A., the airport must beintegrated with the highways (below)

RANK/AIRPORT CODE PASSENGERS %CHG

1. ATLANTA ATL 84,846,639 (1.2)2. CHICAGO ORD 77,028,134 0.73. LONDON LHR 67,530,197 (0.6)4. TOKYO HND 65,810,672 4.05. LOS ANGELES LAX 61,041,066 (0.7)6. DALLAS/FT. WORTH DFW 60,226,138 1.87. PARIS CDG 56,849,567 5.78. FRANKFURT FRA 52,810,683 1.19. BEIJING PEK 48,654,770 18.7

10. DENVER DEN 47,325,016 9.1

Source: Airports Council International

EDWIN VAN ZIJLL CARL DOBYConstruction underwriting, U.S. Technical underwriting, [email protected] [email protected]

TOP 10 BY PASSENGERS

TOP 10 BY TAKEOFF/LANDING(NON-GENERAL AVIATION)

3.567

3.478

3.471

3.531

3.912

4.171

4.372

Source: Airports Council International

Year2000

2001

2002

2003

2004

2005

2006

GLOBAL PASSENGER MOVEMENTS(BILLIONS)

RANK/AIRPORT CODE MOVEMENTS %CHG

1. ATLANTA ATL 976,447 (0.4)2. CHICAGO ORD 958,643 (1.4)3. DALLAS/FT. WORTH DFW 699,773 (1.7)4. LOS ANGELES LAX 656,842 1.05. LAS VEGAS LAS 619,486 2.46. HOUSTON IAH 602,672 7.17. DENVER DEN 598,489 6.78. PHOENIX PHX 546,510 (3.0)9. PARIS CDG 541,566 3.6

10. PHILADELPHIA PHL 515,869 (3.7)

REGIONAL EYE | 27

IN 2005 RALF ZIBELL FLEW TO MUMBAI TO SUPERVISE THE FIRST PART SHIPMENT FOR A DAM. THE LAST ONE IS CURRENTLYUNDERWAY, AND THERE HAVE BEEN NO MAJOR INCIDENTS.

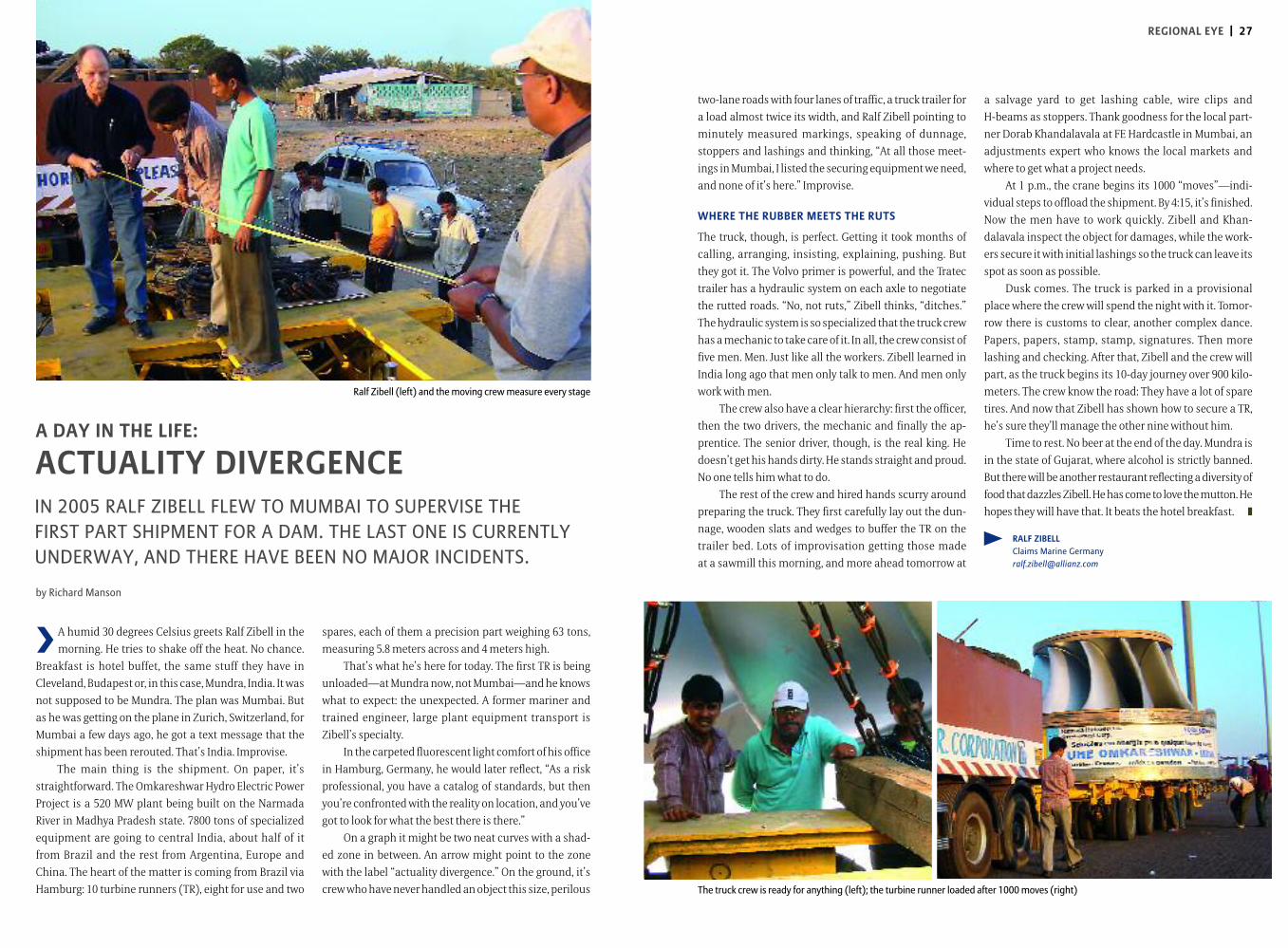

� A humid 30 degrees Celsius greets Ralf Zibell in themorning. He tries to shake off the heat. No chance.

Breakfast is hotel buffet, the same stuff they have inCleveland, Budapest or, in this case, Mundra, India. It wasnot supposed to be Mundra. The plan was Mumbai. Butas he was getting on the plane in Zurich, Switzerland, forMumbai a few days ago, he got a text message that theshipment has been rerouted. That’s India. Improvise.

The main thing is the shipment. On paper, it’sstraightforward. The Omkareshwar Hydro Electric PowerProject is a 520 MW plant being built on the Narmada River in Madhya Pradesh state. 7800 tons of specializedequipment are going to central India, about half of itfrom Brazil and the rest from Argentina, Europe and China. The heart of the matter is coming from Brazil viaHamburg: 10 turbine runners (TR), eight for use and two

spares, each of them a precision part weighing 63 tons,measuring 5.8 meters across and 4 meters high.

That’s what he’s here for today. The first TR is beingunloaded—at Mundra now, not Mumbai—and he knowswhat to expect: the unexpected. A former mariner andtrained engineer, large plant equipment transport is Zibell’s specialty.

In the carpeted fluorescent light comfort of his officein Hamburg, Germany, he would later reflect, “As a riskprofessional, you have a catalog of standards, but thenyou’re confronted with the reality on location, and you’vegot to look for what the best there is there.”

On a graph it might be two neat curves with a shad-ed zone in between. An arrow might point to the zonewith the label “actuality divergence.” On the ground, it’screw who have never handled an object this size, perilous

two-lane roads with four lanes of traffic, a truck trailer fora load almost twice its width, and Ralf Zibell pointing tominutely measured markings, speaking of dunnage,stoppers and lashings and thinking, “At all those meet-ings in Mumbai, I listed the securing equipment we need,and none of it’s here.” Improvise.

WHERE THE RUBBER MEETS THE RUTS

The truck, though, is perfect. Getting it took months ofcalling, arranging, insisting, explaining, pushing. Butthey got it. The Volvo primer is powerful, and the Tratectrailer has a hydraulic system on each axle to negotiatethe rutted roads. “No, not ruts,” Zibell thinks, “ditches.”The hydraulic system is so specialized that the truck crew has a mechanic to take care of it. In all, the crew consist offive men. Men. Just like all the workers. Zibell learned inIndia long ago that men only talk to men. And men onlywork with men.

The crew also have a clear hierarchy: first the officer,then the two drivers, the mechanic and finally the ap-prentice. The senior driver, though, is the real king. Hedoesn’t get his hands dirty. He stands straight and proud.No one tells him what to do.

The rest of the crew and hired hands scurry aroundpreparing the truck. They first carefully lay out the dun-nage, wooden slats and wedges to buffer the TR on thetrailer bed. Lots of improvisation getting those made at a sawmill this morning, and more ahead tomorrow at

a salvage yard to get lashing cable, wire clips and H-beams as stoppers. Thank goodness for the local part-ner Dorab Khandalavala at FE Hardcastle in Mumbai, anadjustments expert who knows the local markets andwhere to get what a project needs.

At 1 p.m., the crane begins its 1000 “moves”—indi-vidual steps to offload the shipment. By 4:15, it’s finished.Now the men have to work quickly. Zibell and Khan-dalavala inspect the object for damages, while the work-ers secure it with initial lashings so the truck can leave itsspot as soon as possible.

Dusk comes. The truck is parked in a provisionalplace where the crew will spend the night with it. Tomor-row there is customs to clear, another complex dance. Papers, papers, stamp, stamp, signatures. Then morelashing and checking. After that, Zibell and the crew willpart, as the truck begins its 10-day journey over 900 kilo-meters. The crew know the road: They have a lot of sparetires. And now that Zibell has shown how to secure a TR,he’s sure they’ll manage the other nine without him.

Time to rest. No beer at the end of the day. Mundra isin the state of Gujarat, where alcohol is strictly banned.But there will be another restaurant reflecting a diversity offood that dazzles Zibell. He has come to love the mutton. Hehopes they will have that. It beats the hotel breakfast. z

The truck crew is ready for anything (left); the turbine runner loaded after 1000 moves (right)

by Richard Manson

RALF ZIBELLClaims Marine [email protected]

A DAY IN THE LIFE:

ACTUALITY DIVERGENCE

Ralf Zibell (left) and the moving crew measure every stage

28 | REGIONAL EYE REGIONAL EYE | 29

� “Wal-Mart employees claim $1.6 billion in damagesfor gender discrimination,” Europeans read about

one of today’s most high-profile employment practicesliability (EPL) cases. The phrase refers to all claims byemployees against their employer, on whatever grounds.It also includes claims based on bullying, unfair dis-missal, working conditions and equal payment. Newlaws prohibiting direct and indirect discrimination andharassment are changing the EPL landscape in Europe.

SHIFTING STANDARDS

With regard to gender, the European Court of Justice hasmade clear that these prohibitions have to be interpretedin the broadest possible terms. Furthermore, all of the directives demand “effective, proportionate and deter-rent” measures. Court rulings have confirmed this meansthat national laws limiting damage awards in general donot comply with the directives. Additionally, the burden of proof has now been shifted to the employer, a require-ment widely criticized, for example in Germany, when thedirectives were implemented. Finally, the directives pro-hibit victimization, call for the creation of national agen-cies specifically to address discrimination and allow pos-itive measures such as quotas to achieve equality.

The history of discrimination-based claims in Euro-pean law goes back to the first directive in 1976 stipulat-ing equality of women and men in the workplace. After

numerous amendments to the European Union direc-tive, a revised version was issued in 2006. In the mean-time, the year 2000 saw two directives requiring equaltreatment irrespective of race, ethnicity, religion or

WINDS OF CHANGEEU DIRECTIVES REQUIRE MEMBER STATES TO IMPLEMENTA WIDE RANGE OF LAWS PROHIBITING EMPLOYMENTDISCRIMINATION AND MANDATING EQUAL TREATMENT.

by Kristina Leffler

belief, disability, age, or sexual orientation. During im-plementation, some European countries have addedother specific discrimination prohibitions to their na-tional laws. A few prohibit “discrimination” in general—for any further reason (see table previous page). Othermember states have broadened the scope of their anti-discrimination legislation to prohibit actions suchas “third party discrimination,” the denial of goods orservices to specific groups of people.

In the UK, employers already have some experiencewith EPL, with nearly 200,000 cases over the last two years.Banks are especially popular targets for such claims.Since 2000, in at least five cases more than £1 million (€1.5 million) have been awarded to the claimants or paidin settlements. The percentage of discrimination cases isstill relatively small (see chart right), but recent evalua-tions show that number is steadily rising.

The climate is also changing in continental Europe.In Germany, the maximum damage awarded to employ-ees harassed by colleagues has increased to nearly€100,000 from €1000 within the last 10 years. In Spain, acourt awarded nearly €300,000 to a female employee forbeing discriminated against on grounds of gender. In oth-er countries, such as Austria, the first rulings based on the

new anti-discrimination legislation have been published.In most known cases, not only the company, but alsomanagers and colleagues have been sued.

REMAINING DIFFERENT

Still, there are no signs of claims or judgments compara-ble to the United States. Headline-grabbing cases like theWal-Mart claim will remain a matter for Americancourts. But EPL has become a serious issue for all employ-ers in Europe. While a single claim may be easily taken bya company, it may be a serious threat if a group of em-ployees pursue a claim against discriminatory practices,particularly because laws permitting a kind of class-action suit have also spread. Just recently, a Germancourt found a social plan discriminatory and thereforeentirely void. Companies are well advised to review theirHR practices and compliance with legislation on anti-discrimination and equality.

U K I N D I V I D U A L E P L D I S P U T E S *

*all jurisdictions

& http://ec.europa.eu/employment_social/gender_equalityhttp://ec.europa.eu/employment_social/fundamental_rights

JOACHIM ALBERS KRISTINA LEFFLERFinancial Lines Underwriting Financial Lines [email protected] [email protected]

Diverse work forces demandequal treatment

Source: ACAS Annual Report and Accounts 2005/2006, United Kingdom

23.1% Unfair dismissal

17.9% Working time

17.3% Wages act

13.4% Breach of contract

11.3% Discrimination

7.4% Equal pay

3.6% Redundancy pay

6.0% Other

B E Y O N D T H E D I R E C T I V E S : D I S C R I M I N A T I O N P R O H I B I T I O N S B Y C O U N T R Y

Belgium Skin color, parentage, family status, birth,property, health, physical characteristics, any further reasons

Finland Any further reasons

Hungary Part-time employment, any further reasons

Netherlands Part-time employment

Poland Part-time employment, any further reasons

Portugal Genotype, family status

Slovenia Education, financial status, any further reasons

Source: European Net of independent experts in the non-discrimination field: Developing Anti-Discrimination Law in Europe, September 2005, updated November 2006

As a way of responding to this new challenge facingcompanies and their management, Allianz Global Corporate & Specialty has developed a tailor-made,stand-alone insurance policy that considers and coversexposures specifically caused by these directives, in order to protect the company, its managers and its employees across the European Union. The product waslaunched in Germany at the end of 2006 and is currentlybeing rolled out in further European markets to meet the demands of clients. z

30 | THE LAST WORD

❯ The market for insurance-linked securities (ILS) hasbeen rather slow to develop, although the insurance

industry has paid it considerable attention since its startin the early 1990s. Recently, however, the market has in-creased significantly, in part due to an expansion of thetypes of risks ILS cover. Total risk capital issued via catas-trophe (cat) bonds, perhaps the most popular of the in-surance-linked securities, peaked in 2006 at about $ 4.69billion. A cat bond is a bond whose interest or principal isforgiven when a certain pre-defined catastrophe occurs.Risk is thus passed from the issuer, typically a specialpurpose vehicle set up by an insurer, to the bondholders.While they originally covered natural catastrophe riskonly, the same kind of structure has spread to hedge other types of risk such as liability or mortality surprises.

The economic rationale for ILS includes a variety ofreasons. In particular, securitization unbundles insur-ance risk, offering investors an opportunity to take a pureposition on an insured event. Also, cat bonds can be usedto reduce or even exclude the credit risk immanent in ca-tastrophe reinsurance. These bonds also allow for long-term pricing, which protects the hedging party from theprice cycles of the reinsurance markets.

A key characteristic of a cat bond is its trigger. As intraditional (re)insurance, the trigger can be the spon-sor’s actual losses (indemnity trigger), but it may also be

DEFINING THE TRIGGERCATASTROPHE BONDS COVER A WIDENING RANGEOF RISKS AND HELP IMPROVE EFFICIENCY.

“Depending on their design,index triggers can add trans-parency for investors and helpaddress moral hazard.”Andreas Richter, Professor, Chair of theInstitute for Risk and Insurance Management atLudwig-Maximilians-Universität Munich

A guest commentary by Andreas Richter

CALENDAR /IMPRINT | 31

DATE/LOCATION EVENT INFORMATION

C A L E N D A R

D I S C L A I M E R Contributors’ comments do not necessarily reflect the views of the editor or the publisher. The editor reserves the right to publish articles in an edited and abridged form. Information in this publication provides only a general outline of subjects and does not substitute for individual advice. Although care has been taken in compiling this information, neither the publisher nor the editor accepts responsibilityfor errors or omissions or for any damage, loss or expenses incurred from the use of any information contained herein. The publisher assumes no obligation to update any forward-looking information contained herein.

Phot

o:xx

xxxx

xxxx

xxxx

xxxx

x

I M P R I N T Volume 1, Number 2/ 2007

P U B L I S H E RAllianz Global Corporate &Specialty AG, Fritz-Schäffer- Str. 9, D-81737 Munich,Germany © Allianz GlobalCorporate & Specialty. All rights reserved. The con-tents of this publication maynot be reproduced whole or in part without written consentof the copyright owner. The cut-off date for this issue’s

editorial content was July 31, 2007.O V E R A L LR E S P O N S I B I L I T YAndreas Berger, Global Head of Market Management &Communication, Allianz GlobalCorporate & Specialty.Postal address same as thepublisher’s above. E D I T O R - I N - C H I E FRichard Manson, Phone:

+49-89-3800-5509, Fax: +49-89-3800-13289, [email protected] P U B L I S H I N G H O U S EBurdaYukom Publishing GmbH, Konrad-Zuse-Platz 11, D-81829 Munich, Germany E D I T O R I A L S T A F F Elmar zur Bonsen, Douglas Merrill, Wolfgang Miller, Asa Tomash

A R T D I R E C T O RBlasius Thätter M A N A G I N G E D I T O RSusan Sablowski G R A P H I C D E S I G NAndrea Hüls, Anja Frieda SchneiderP R O D U C T I O NFranz Kantner,Cornelia Sauer P H O T O E D I T O RElisabeth Wighton

P R I N T E R Pinsker Druck und MedienGmbH D I S T R I B U T I O N T E R M S Allianz Global Risk Dialogue is published twice a year.Excluding VAT and shippingcosts, the price per copy is€20.00. CO N T A C T F O RS U B S C R I P T I O [email protected]

O C T O B E R 2 9 – N O V E M B E R 1 IRMI – 27th Construction Risk Conference www.irmi.comOrlando, FL, USA International Risk Management Institute (IRMI)

O C T O B E R 3 0 – 3 1 Corporate Security, Business Continuity www.conference-board.orgNew York, NY, USA and Crisis Management Conference

The Conference Board

N O V E M B E R 2 5 – 2 7 RMIA – Annual Conference www.rmiaconference.comGold Coast, Australia Risk Management Institution of Australia (RMIA)

N O V E M B E R 5 – 7 17th World Captive Forum www.worldcaptiveforum.comScottsdale, AZ, USA World Captive Forum

D E C E M B E R 9 – 1 2 SRA Annual Meeting “Risk 007: Agents of Analysis” www.sra.orgSan Antonio, TX, USA The Society for Risk Analysis

J A N U A R Y 2 3 – 2 5 AMRAE Annual Conference Association pour le Management www.amrae.frDeauville, France des Risques et des Assurances de l’Entreprise (AMRAE)

F E B R U A R Y 1 0 – 1 3 PARMA Conference www.parma.comAnaheim, CA, USA Public Agency Risk Managers Association (PARMA)

F E B R U A R Y 2 5 – 2 8 GARP’s 9th Annual Risk Management Convention www.garp.comNew York, NY, USA Global Association of Risk Professionals

A P R I L 2 4 DVS Annual Meeting www.dvs-schutzverband.deBonn, Germany Deutscher Versicherungs-Schutzverband e.V. (DVS)

A P R I L 2 7 – M A Y 1 RIMS 2008 Annual Conference & Exhibition www.rims.org San Diego, CA, USA Risk & Insurance Management Society (RIMS)

J U N E 1 – 4 PRIMA 2008 Annual Conference www.primacentral.orgAnaheim, CA, USA Public Risk Management Association (PRIMA)

J U N E 1 7 – 1 8 AIRMIC Conference 2008 “Communicating Risk Management” www.airmic.comEdinburgh, Scotland Association of Insurance and Risk Managers (AIRMIC)

J U N E 2 9 – J U L Y 1 ALARM 16th Annual Conference www.alarm-uk.orgBirmingham, UK Association of Local Authority Risk Managers (ALARM)

J U L Y 6 – 9 Asia-Pacific Risk & Insurance Association 12th Annual Conference www.apria.orgSydney, Australia Asia Pacific Risk & Insurance Association

J U L Y 1 3 – 1 6 IIS 44th Annual Seminar www.iisonline.orgTaipei, Taiwan International Insurance Society (IIS)

S E P T E M B E R 6 – 1 2 Le Rendez-Vous de Septembre International Convention of www.rvs-monte-carlo.comMonte Carlo, Monaco Insurers, Reinsurers, Brokers, and Reinsurance Consultants

S E P T E M B E R 1 4 – 1 7 IUMI 2008 Conference www.iumi2008.comVancouver, Canada Danish Insurance Association

S E P T E M B E R 2 1 – 2 4 2008 RIMS Canada Conference www.rimscanada.org Toronto, Canada Risk & Insurance Management Society (RIMS)

some other variable correlated but not identical withthese losses, such as an industry loss index or a paramet-ric index describing the strength of the event.

Index triggers involve a trade-off. The mismatch be-tween the index and actual losses results in basis risk,which is offset by certain efficiency gains: depending ontheir design, index triggers can add transparency for in-vestors. Also, they provide a new contractual device to ad-dress the moral hazard (re)insurance transactions con-tain: the primary insurer selects its portfolio of insuredrisks, negotiates terms with its own policyholders and set-tles claims with them. Each activity is costly to the pri-mary but can affect the frequency and severity of claims.If the primary is heavily reinsured, the reinsurer benefitsfrom loss reduction, but the primary bears the cost. Thus,

the level of reinsurance affects the effort dedicated tothese activities. In order to reduce moral hazard, reinsur-ance contracts may be experience-rated or retrospective-ly priced, and long-term and brokered relationships arecommon. Tying payoffs to an index, instead of the actuallosses, provides a new way of addressing moral hazard.

The recent spread of index triggers suggests themoral hazard argument matters. However, as the degreeof basis risk seems very important to the markets, this development also indicates progress in reducing andevaluating basis risk. ❚