Deploying effective strategies in tackling VAT fraud - OECD · Deploying effective strategies in...

10

Deploying effective strategies in tackling VAT fraud Portugal’s experience Second Global Forum on VAT Tokyo 18 th of April, 2014

-

Upload

hoangquynh -

Category

Documents

-

view

221 -

download

0

Transcript of Deploying effective strategies in tackling VAT fraud - OECD · Deploying effective strategies in...

Deploying effective strategies in

tackling VAT fraud

Portugal’s experience

Second Global Forum on VAT

Tokyo

18th of April, 2014

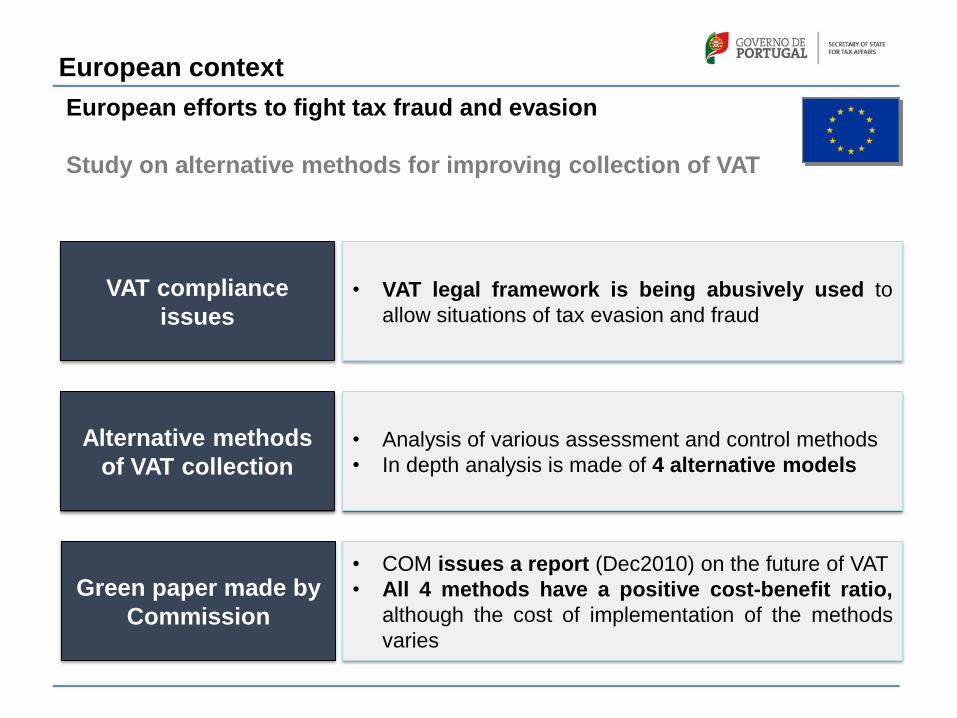

European context

European efforts to fight tax fraud and evasion

Study on alternative methods for improving collection of VAT

VAT compliance

issues

Alternative methods

of VAT collection

Green paper made by

Commission

• VAT legal framework is being abusively used to

allow situations of tax evasion and fraud

• Analysis of various assessment and control methods

• In depth analysis is made of 4 alternative models

• COM issues a report (Dec2010) on the future of VAT

• All 4 methods have a positive cost-benefit ratio,

although the cost of implementation of the methods

varies

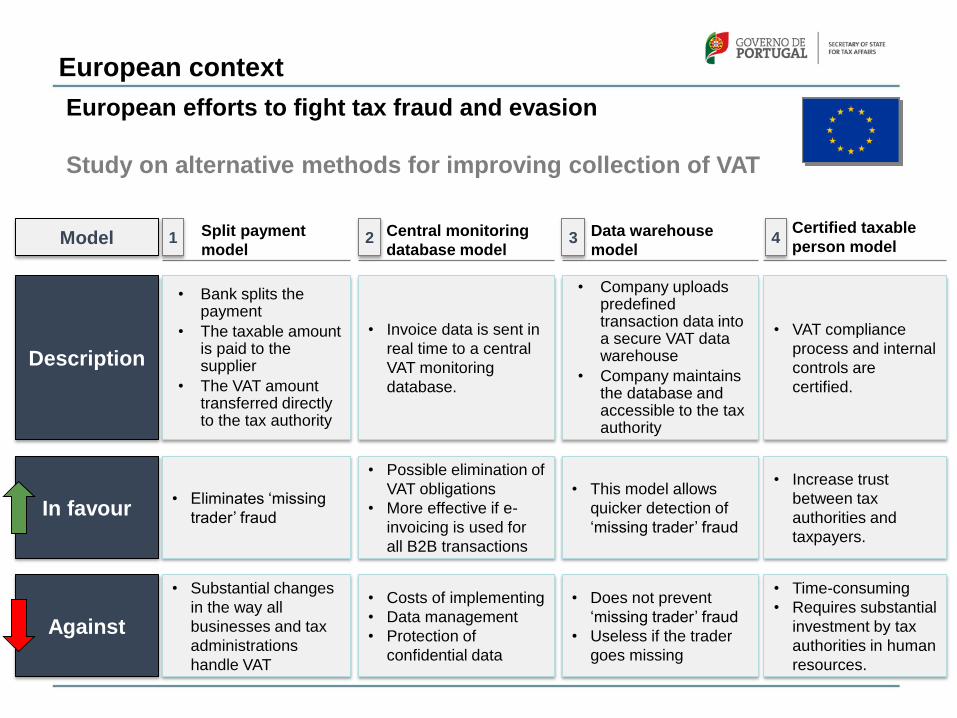

European context

European efforts to fight tax fraud and evasion

Study on alternative methods for improving collection of VAT

Description

Against

In favour

• Bank splits the payment

• The taxable amount is paid to the supplier

• The VAT amount transferred directly to the tax authority

• Eliminates ‘missing

trader’ fraud

• Substantial changes

in the way all

businesses and tax

administrations

handle VAT

Split payment

model 1

Model

• Invoice data is sent in

real time to a central

VAT monitoring

database.

• Possible elimination of

VAT obligations

• More effective if e-

invoicing is used for

all B2B transactions

• Costs of implementing

• Data management

• Protection of

confidential data

Central monitoring

database model 2

• Company uploads predefined transaction data into a secure VAT data warehouse

• Company maintains the database and accessible to the tax authority

• This model allows

quicker detection of

‘missing trader’ fraud

• Does not prevent

‘missing trader’ fraud

• Useless if the trader

goes missing

Data warehouse

model 3

• VAT compliance

process and internal

controls are

certified.

• Increase trust

between tax

authorities and

taxpayers.

• Time-consuming

• Requires substantial

investment by tax

authorities in human

resources.

Certified taxable

person model 4

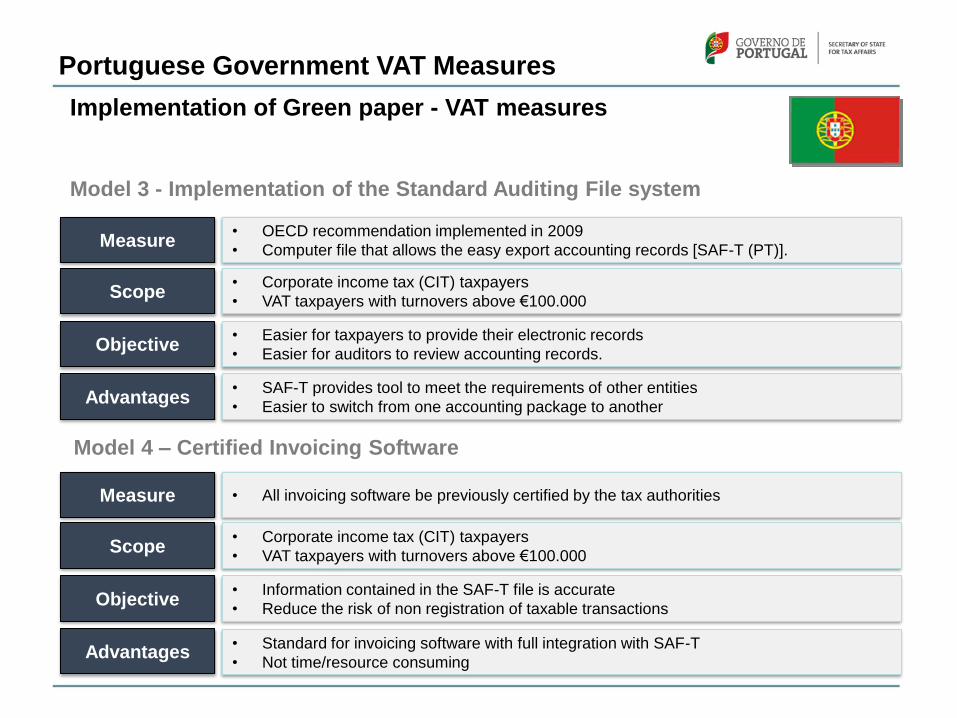

Implementation of Green paper - VAT measures

Model 3 - Implementation of the Standard Auditing File system

Portuguese Government VAT Measures

Measure

Objective

Scope

• OECD recommendation implemented in 2009

• Computer file that allows the easy export accounting records [SAF-T (PT)].

• Easier for taxpayers to provide their electronic records

• Easier for auditors to review accounting records.

• SAF-T provides tool to meet the requirements of other entities

• Easier to switch from one accounting package to another

Advantages

• Corporate income tax (CIT) taxpayers

• VAT taxpayers with turnovers above €100.000

• All invoicing software be previously certified by the tax authorities

Measure

Objective

• Information contained in the SAF-T file is accurate

• Reduce the risk of non registration of taxable transactions

• Standard for invoicing software with full integration with SAF-T

• Not time/resource consuming

Scope

• Corporate income tax (CIT) taxpayers

• VAT taxpayers with turnovers above €100.000

Advantages

Model 4 – Certified Invoicing Software

Portuguese Government VAT Measures

Measure

Objective

Advantages

Scope

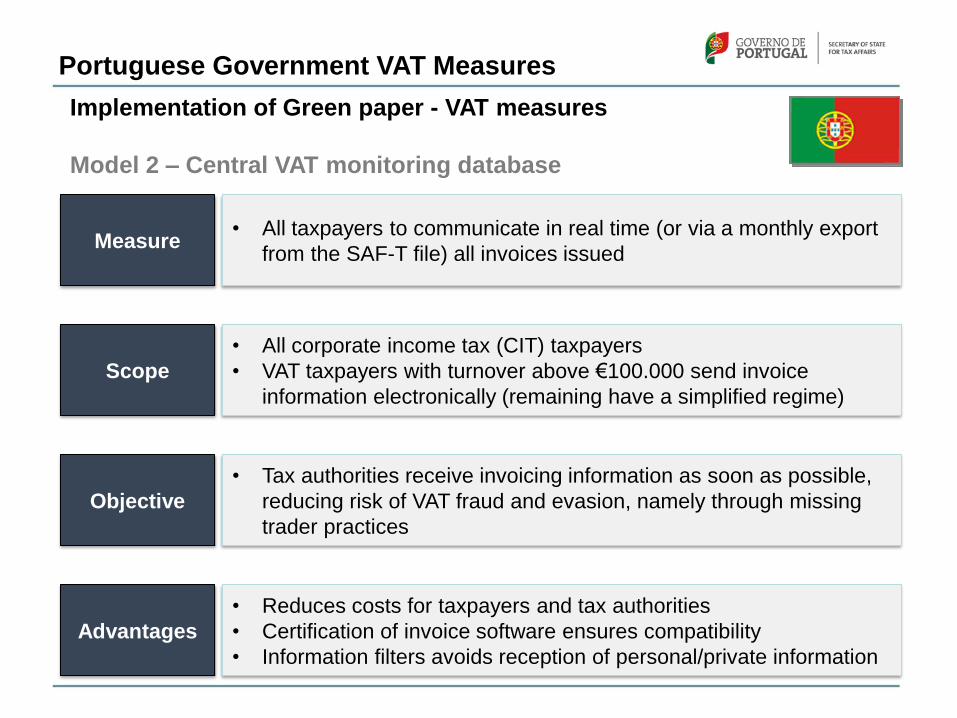

• All taxpayers to communicate in real time (or via a monthly export

from the SAF-T file) all invoices issued

• Tax authorities receive invoicing information as soon as possible,

reducing risk of VAT fraud and evasion, namely through missing

trader practices

• Reduces costs for taxpayers and tax authorities

• Certification of invoice software ensures compatibility

• Information filters avoids reception of personal/private information

• All corporate income tax (CIT) taxpayers

• VAT taxpayers with turnover above €100.000 send invoice

information electronically (remaining have a simplified regime)

Implementation of Green paper - VAT measures

Model 2 – Central VAT monitoring database

Portuguese Government VAT Measures

Implementation of Green paper - VAT measures

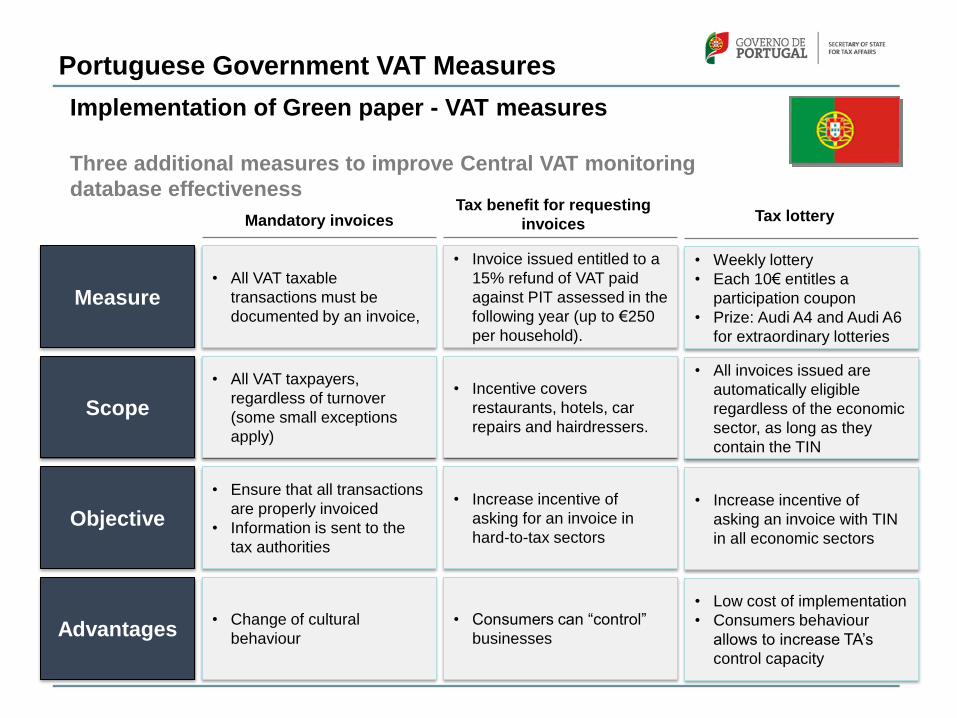

Three additional measures to improve Central VAT monitoring

database effectiveness

Measure

Objective

Advantages

Scope

• All VAT taxable

transactions must be

documented by an invoice,

• Ensure that all transactions

are properly invoiced

• Information is sent to the

tax authorities

• Change of cultural

behaviour

• All VAT taxpayers,

regardless of turnover

(some small exceptions

apply)

• Invoice issued entitled to a

15% refund of VAT paid

against PIT assessed in the

following year (up to €250

per household).

• Increase incentive of

asking for an invoice in

hard-to-tax sectors

• Consumers can “control”

businesses

Mandatory invoices

• Incentive covers

restaurants, hotels, car

repairs and hairdressers.

Tax benefit for requesting

invoices

• Weekly lottery

• Each 10€ entitles a

participation coupon

• Prize: Audi A4 and Audi A6

for extraordinary lotteries

• Increase incentive of

asking an invoice with TIN

in all economic sectors

• Low cost of implementation

• Consumers behaviour

allows to increase TA’s

control capacity

• All invoices issued are

automatically eligible

regardless of the economic

sector, as long as they

contain the TIN

Tax lottery

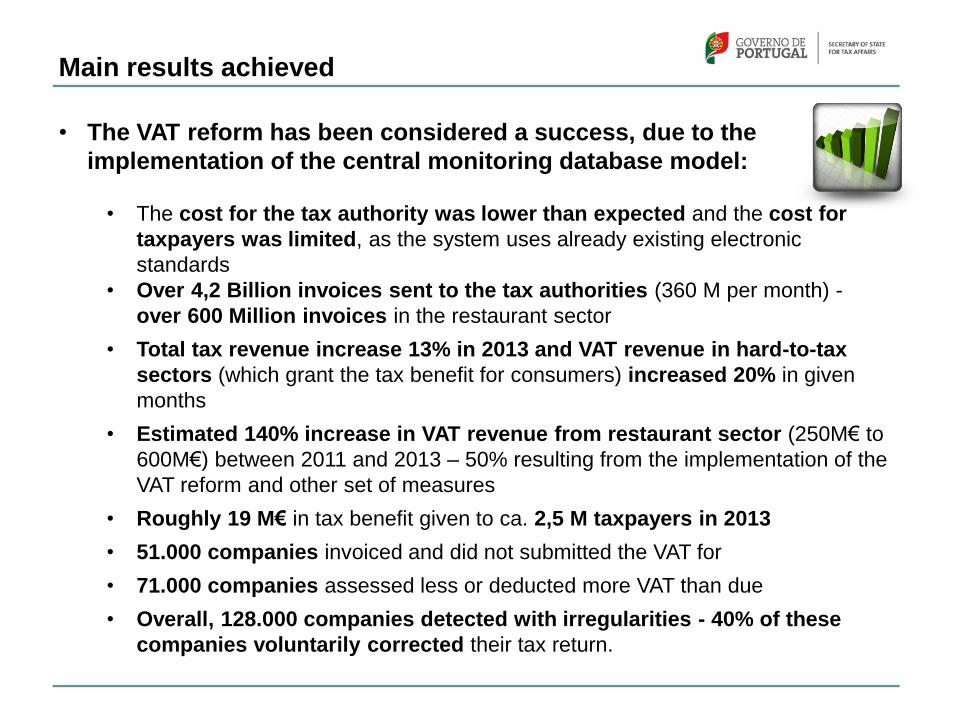

• The VAT reform has been considered a success, due to the

implementation of the central monitoring database model:

• The cost for the tax authority was lower than expected and the cost for

taxpayers was limited, as the system uses already existing electronic

standards

• Over 4,2 Billion invoices sent to the tax authorities (360 M per month) -

over 600 Million invoices in the restaurant sector

• Total tax revenue increase 13% in 2013 and VAT revenue in hard-to-tax

sectors (which grant the tax benefit for consumers) increased 20% in given

months

• Estimated 140% increase in VAT revenue from restaurant sector (250M€ to

600M€) between 2011 and 2013 – 50% resulting from the implementation of the

VAT reform and other set of measures

• Roughly 19 M€ in tax benefit given to ca. 2,5 M taxpayers in 2013

• 51.000 companies invoiced and did not submitted the VAT for

• 71.000 companies assessed less or deducted more VAT than due

• Overall, 128.000 companies detected with irregularities - 40% of these

companies voluntarily corrected their tax return.

Main results achieved

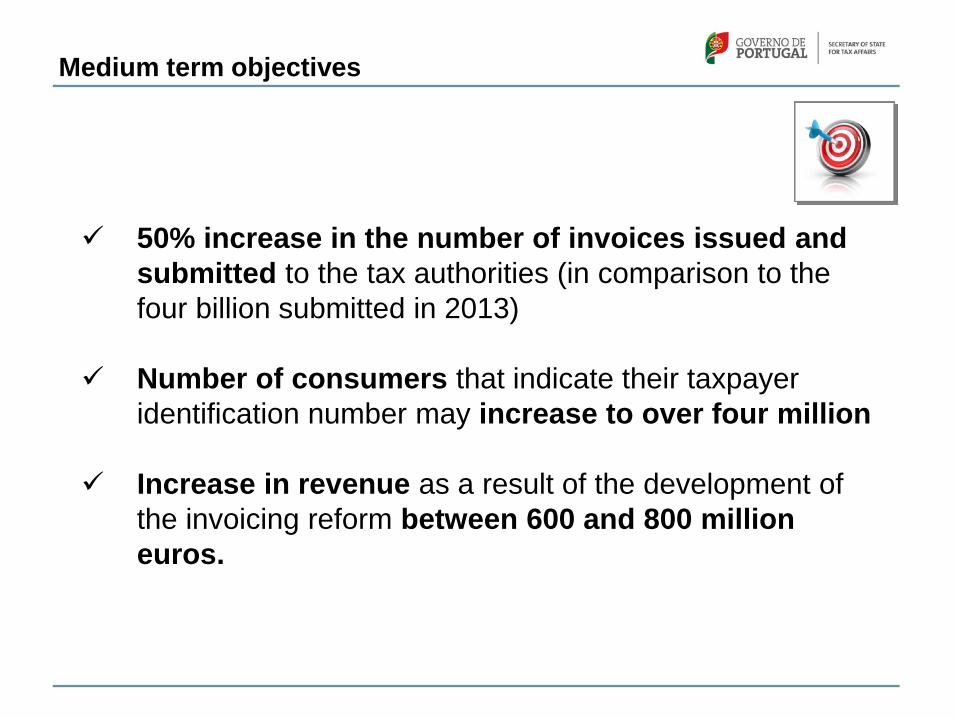

50% increase in the number of invoices issued and

submitted to the tax authorities (in comparison to the

four billion submitted in 2013)

Number of consumers that indicate their taxpayer

identification number may increase to over four million

Increase in revenue as a result of the development of

the invoicing reform between 600 and 800 million

euros.

Medium term objectives

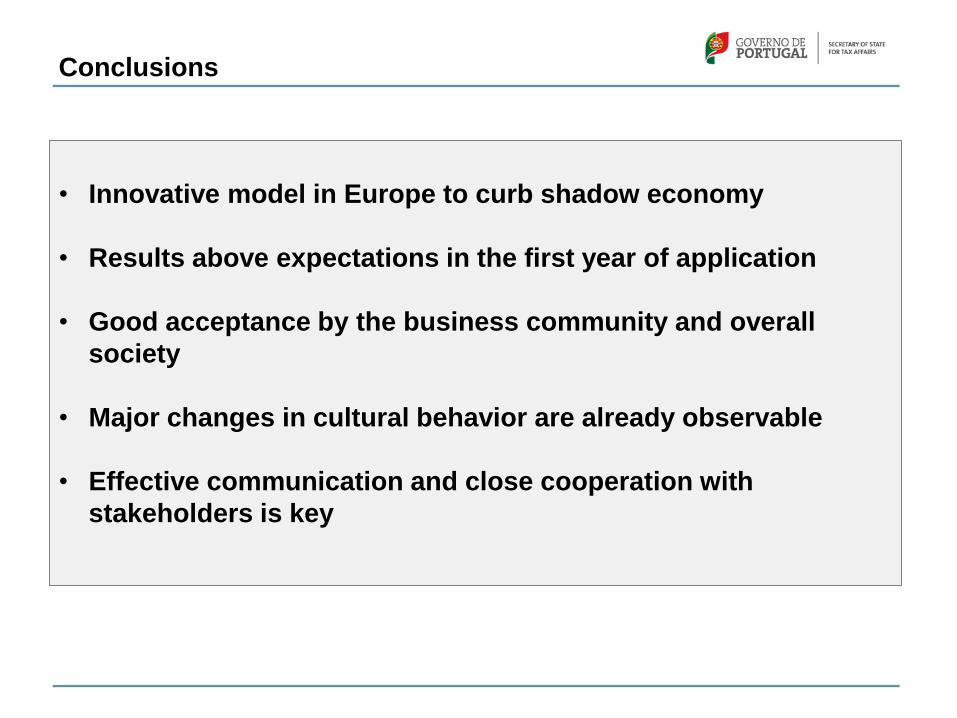

• Innovative model in Europe to curb shadow economy

• Results above expectations in the first year of application

• Good acceptance by the business community and overall

society

• Major changes in cultural behavior are already observable

• Effective communication and close cooperation with

stakeholders is key

Conclusions

Deploying effective strategies in

tackling VAT fraud

Portugal’s experience

Second Global Forum on VAT

Tokyo

18th of April, 2014