Demystifying EVA and EVA Implementation Copyright © November 16, 1999 Icelandic Management...

51

-

date post

22-Dec-2015 -

Category

Documents

-

view

220 -

download

4

Transcript of Demystifying EVA and EVA Implementation Copyright © November 16, 1999 Icelandic Management...

Demystifying EVA

and

EVA Implementation

Copyright © November 16, 1999

Icelandic Management Association Conference on EVA®

Discussion Topics

Why has EVA become so popular?

Why is there a mystique associated with EVA adoption?

How do companies become “EVA companies”?

What are the pitfalls encountered in implementing EVA?

What’s next in EVA development?

®

EVA® is a registered trademark of Stern Stewart & Co.

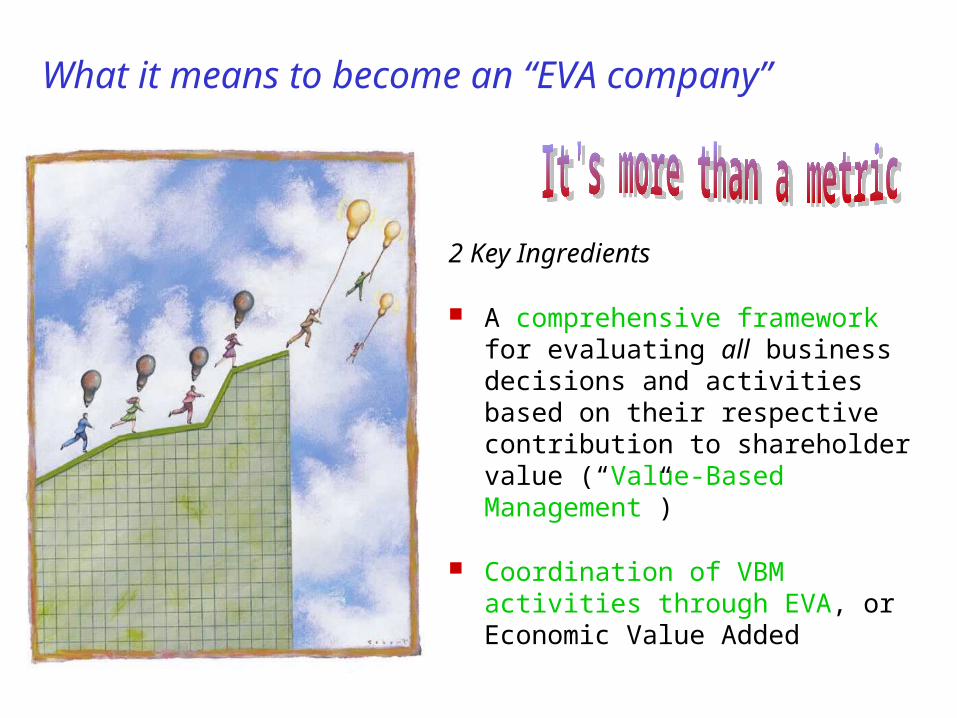

What it means to become an “EVA company”

2 Key Ingredients

A comprehensive framework for evaluating all business decisions and activities based on their respective contribution to shareholder value (“Value-Based Management”)

Coordination of VBM activities through EVA, or Economic Value Added

What it means to become an “EVA company”

A cohesive definition of success

A shared language for each area of financial management

A fundamental reformulation of the way the company structures incentives

The tools and understanding to make EVA line-of-sight, and thus part of day-to-day decision-making

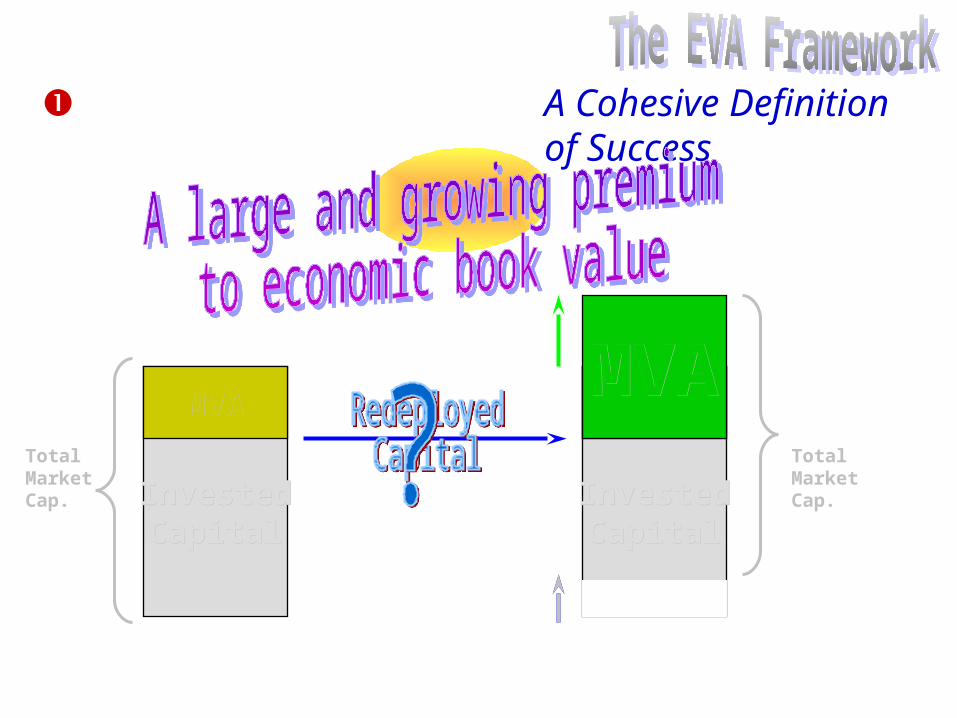

A Cohesive Definition of Success

MarketMarketValue ofValue ofInvestedInvestedCapitalCapital

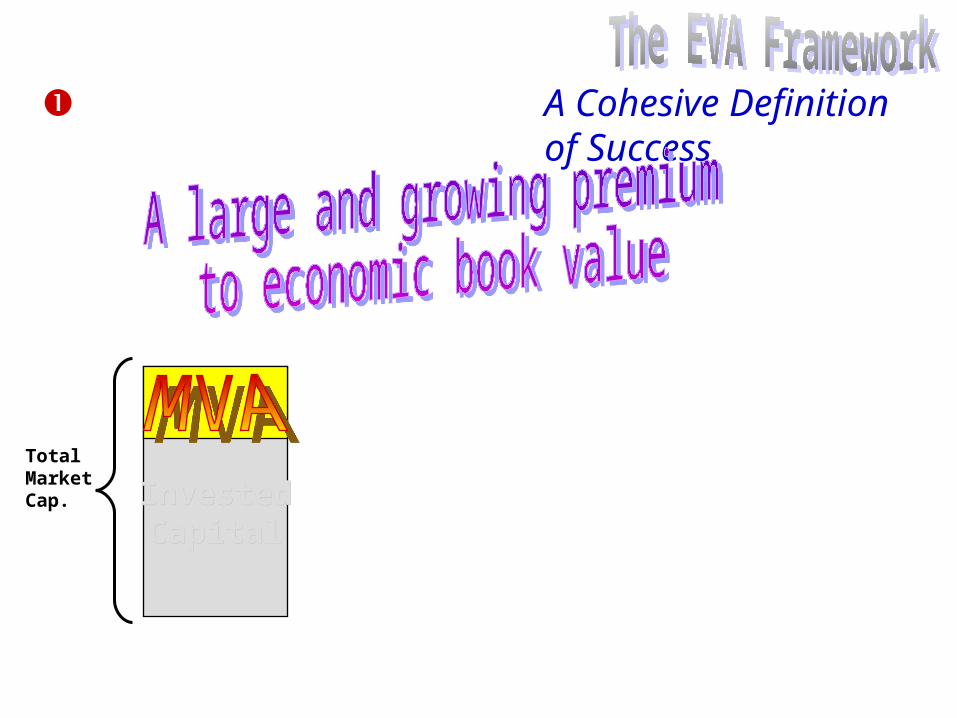

A Cohesive Definition of Success

InvestedInvestedCapitalCapital

TotalMarketCap.

A Cohesive Definition of Success

InvestedInvestedCapitalCapital

MVAMVA

TotalMarketCap.

InvestedInvestedCapitalCapital

MVAMVA

InvestedInvestedCapitalCapital

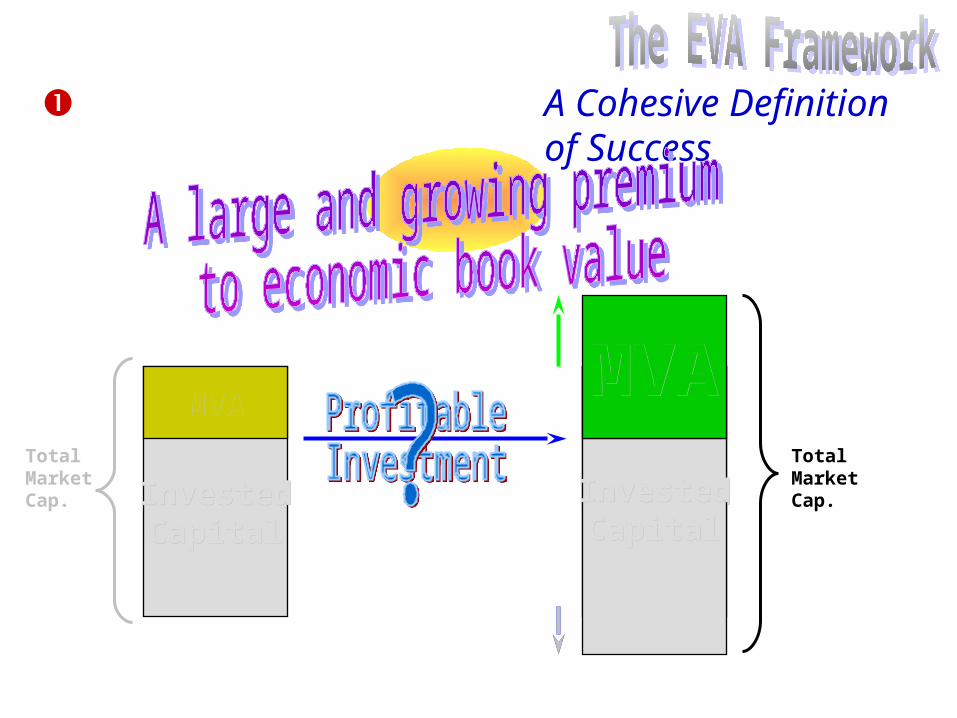

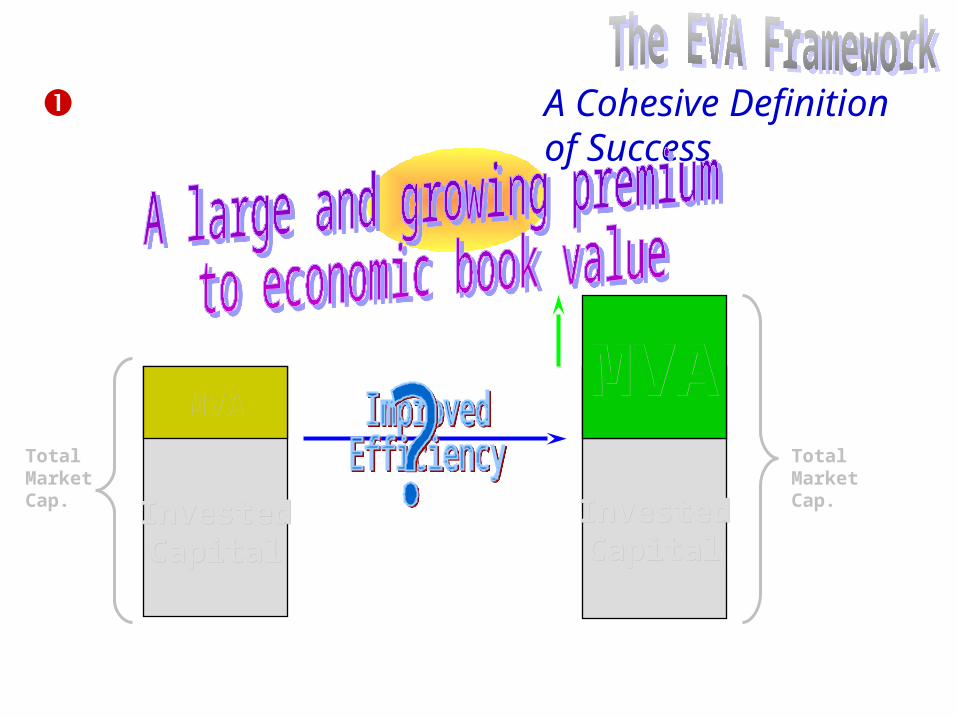

A Cohesive Definition of Success

MVAMVA

TotalMarketCap.

MVAMVA

InvestedInvestedCapitalCapital

InvestedInvestedCapitalCapital

A Cohesive Definition of Success

MVAMVA

TotalMarketCap.

TotalMarketCap.

MVAMVA

InvestedInvestedCapitalCapital

MVAMVA

InvestedInvestedCapitalCapital

A Cohesive Definition of Success

MVAMVA

TotalMarketCap.

TotalMarketCap.

MVAMVA

MVA comes from operations, not finance.

MVA depends on the future, not the past.

A Cohesive Definition of Success

How do EVA companies drive MVA?

MVA can only be measured externally.

No divisional surrogates.

No internal guidance about how to measure, promote and reward success.

A Cohesive Definition of Success

The Limitations of MVA

The single best internal determinant of MVA is EVA—or the “economic profit” remaining after imputing a charge for the carrying cost of equity. EVA is also known as “residual income.”

EVA-based planning systems identify and exploit the causal relationship between internal performance markers and external markers like MVA.

A Cohesive Definition of Success

Thesis

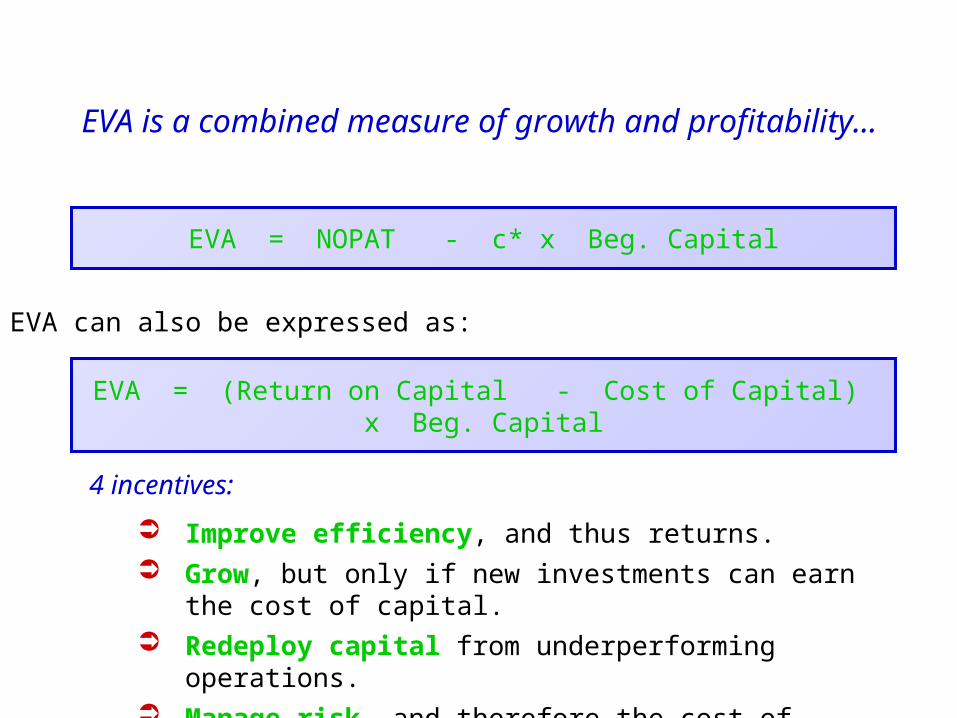

EVA = Operating Profit - Opportunity Cost of Running the Business

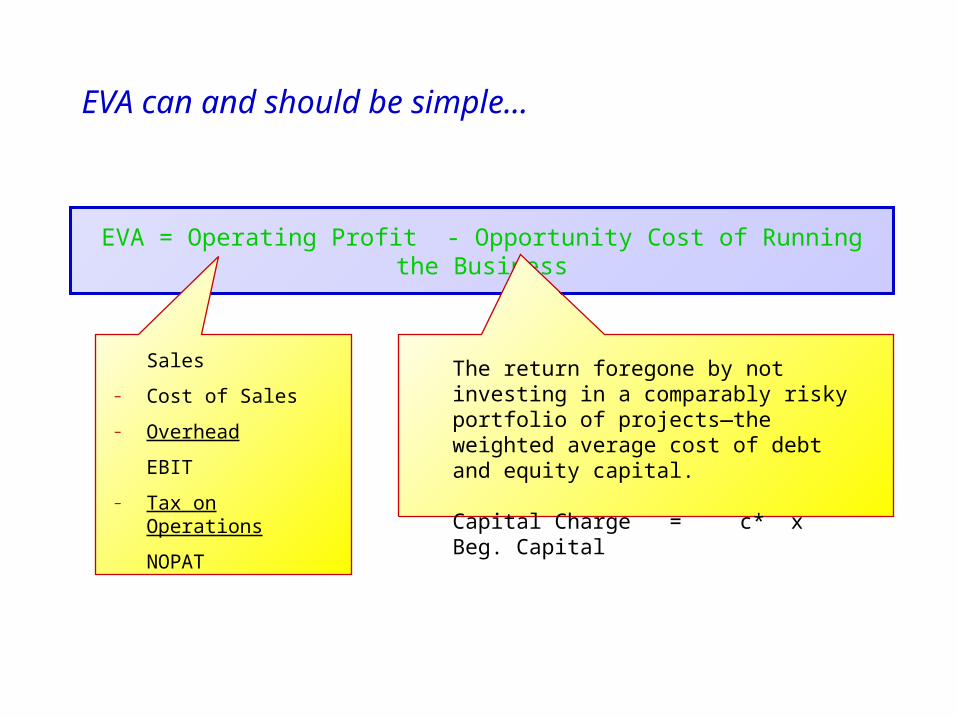

EVA can and should be simple...

Sales

– Cost of Sales

– Overhead

EBIT

– Tax on Operations

NOPAT

The return foregone by not investing in a comparably risky portfolio of projects—the weighted average cost of debt and equity capital.

Capital Charge = c* x Beg. Capital

EVA = NOPAT - c* x Beg. Capital

EVA can also be expressed as:

EVA = (Return on Capital - Cost of Capital) x Beg. Capital

4 incentives:

Improve efficiency, and thus returns. Grow, but only if new investments can earn the cost of capital. Redeploy capital from underperforming operations. Manage risk, and therefore the cost of capital.

EVA is a combined measure of growth and profitability...

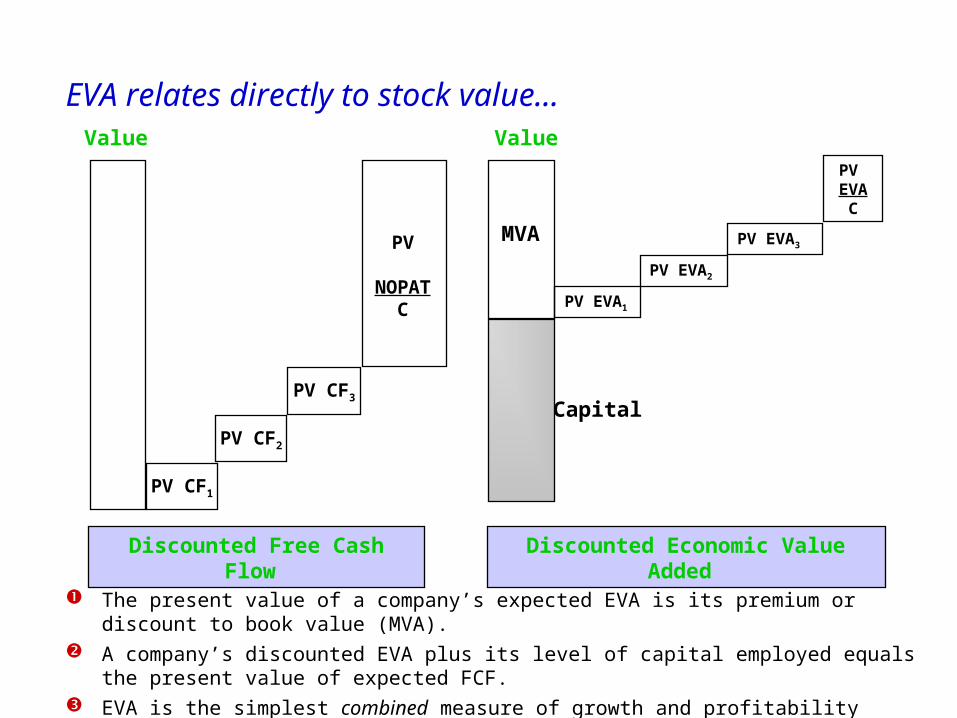

EVA relates directly to stock value...

PV CF1

Value

PV CF3

PV CF2

PV

NOPATC

Discounted Free Cash Flow

Discounted Economic Value Added

PV EVA1

PV EVA2

PV EVA3

PV EVA

C

Capital

Value

MVA

The present value of a company’s expected EVA is its premium or discount to book value (MVA). A company’s discounted EVA plus its level of capital employed equals the present value of expected FCF. EVA is the simplest combined measure of growth and profitability relating directly to stock value.

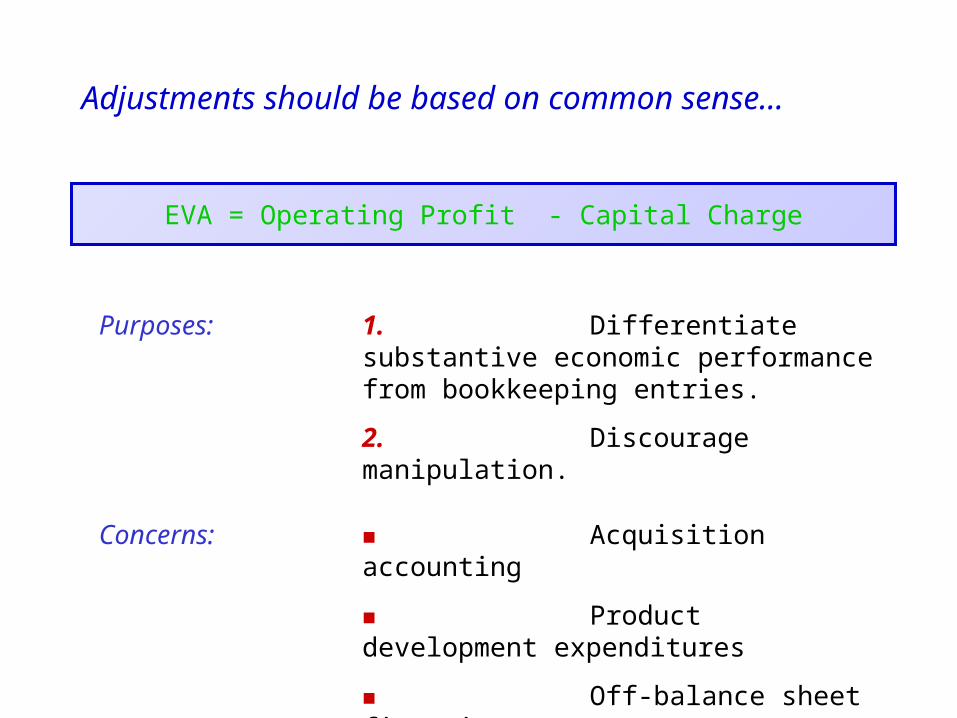

EVA = Operating Profit - Capital Charge

Adjustments should be based on common sense...

Purposes: 1. Differentiate substantive economic performance from bookkeeping entries.

2. Discourage manipulation.

Concerns: Acquisition accounting

Product development expenditures

Off-balance sheet financing

Reserves

Start-ups and high technology

The bottom line on metrics: Be practical!

EVA is one of the few performance measures that integrates growth and profitability objectives into a single scorecard.

Defining EVA can and should be simple: net economic profit after a charge for invested capital.

There is no universal definition of EVA for all companies. Most asserted proprietary adjustments are window dressing, doing more to obfuscate EVA’s directive than promote it.

Whether a company elects to measure performance in real or nominal terms, measure investment on a net or gross basis, benchmark against competitors, make bookkeeping adjustments, use cash-basis accounting, or capitalize periodic performance measures should depend on the specific business circumstances of the client—not upon what’s in fashion.

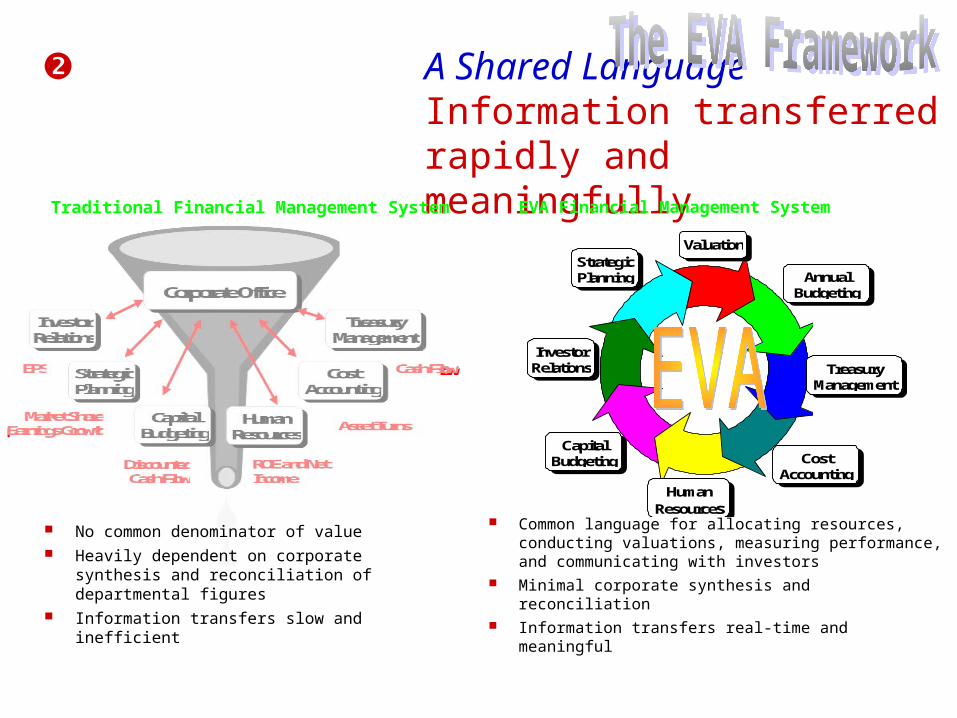

A Shared LanguageInformation transferred rapidly and meaningfully

Corporate Office

InvestorRelations

CapitalBudgeting

HumanResources

StrategicPlanning

CostAccounting

TreasuryManagement

DiscountedCash Flow

ROE and NetIncome

Market Share,Earnings Growth

EPS

Asset Turns

Cash Flow

EVA Financial Management System

Common language for allocating resources, conducting valuations, measuring performance, and communicating with investors

Minimal corporate synthesis and reconciliation Information transfers real-time and meaningful

StrategicPlanning

InvestorRelations

CapitalBudgeting

HumanResources

CostAccounting

TreasuryManagement

AnnualBudgeting

Valuation

Traditional Financial Management System

No common denominator of value Heavily dependent on corporate synthesis and

reconciliation of departmental figures Information transfers slow and inefficient

More than a formula

A greater portion of pay at risk

Wide and consistent participation

Real at-risk invested capital

Substantially increased leverage

Vast upside potential

Non-negotiated targets

Bonus separated from the budget

Identical long- and short-term performance measures

A Fundamental Change in Incentives

More than lip service

Management consensus and buy-in

Strong understanding of how value drivers interact

Tools to reinforce that understanding, perform sensitivity analysis, and conduct “what ifs”on key value drivers

Tools to track, forecast and simulate performance and bonus accruals

Ongoing training and communication

Development of EVA coaches

The Tools and Understanding to Guide Better Performance

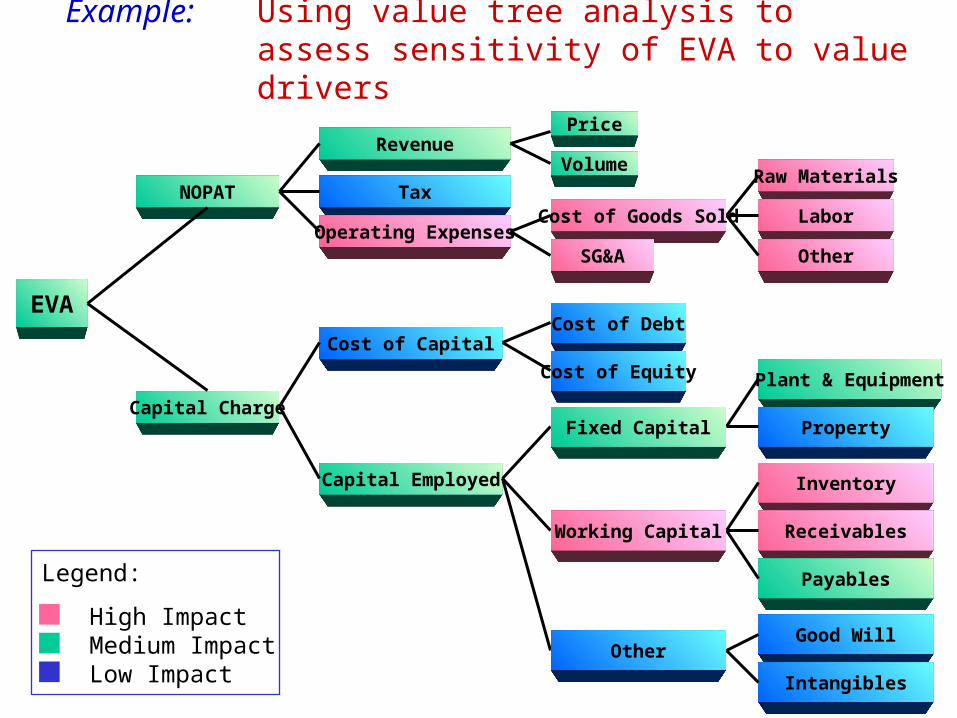

Raw Materials

Labor

Other

Plant & Equipment

Property

Inventory

Receivables

Payables

Good Will

Intangibles

Revenue

Tax

Operating Expenses

Cost of Capital

Capital Employed

Capital Charge

NOPAT

EVA

Legend:

High Impact Medium Impact Low Impact

Volume

Cost of Goods Sold

SG&A

Cost of Debt

Cost of Equity

Fixed Capital

Working Capital

Other

Price

Example: Using value tree analysis to assess sensitivity of EVA to value drivers

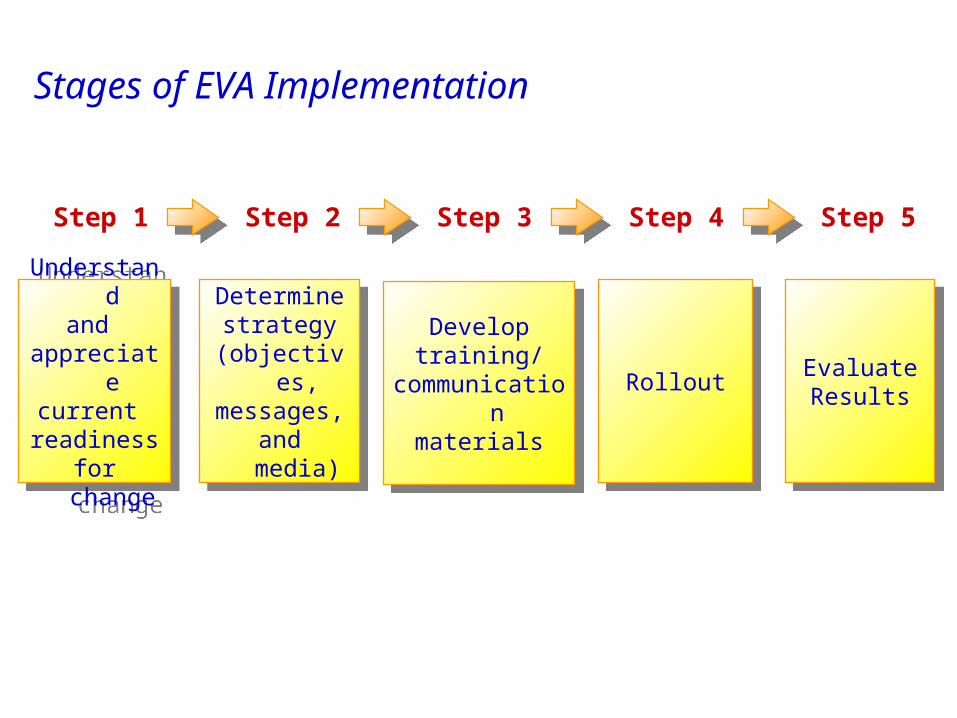

Stages of EVA Implementation

Understand

and appreciate

current readiness for change

Understand

and appreciate

current readiness for change

Determinestrategy

(objectives,messages,and media)

Determinestrategy

(objectives,messages,and media)

Developtraining/

communication

materials

Developtraining/

communication

materials

RolloutRollout EvaluateResults

EvaluateResults

Step 1 Step 2 Step 3 Step 4 Step 5

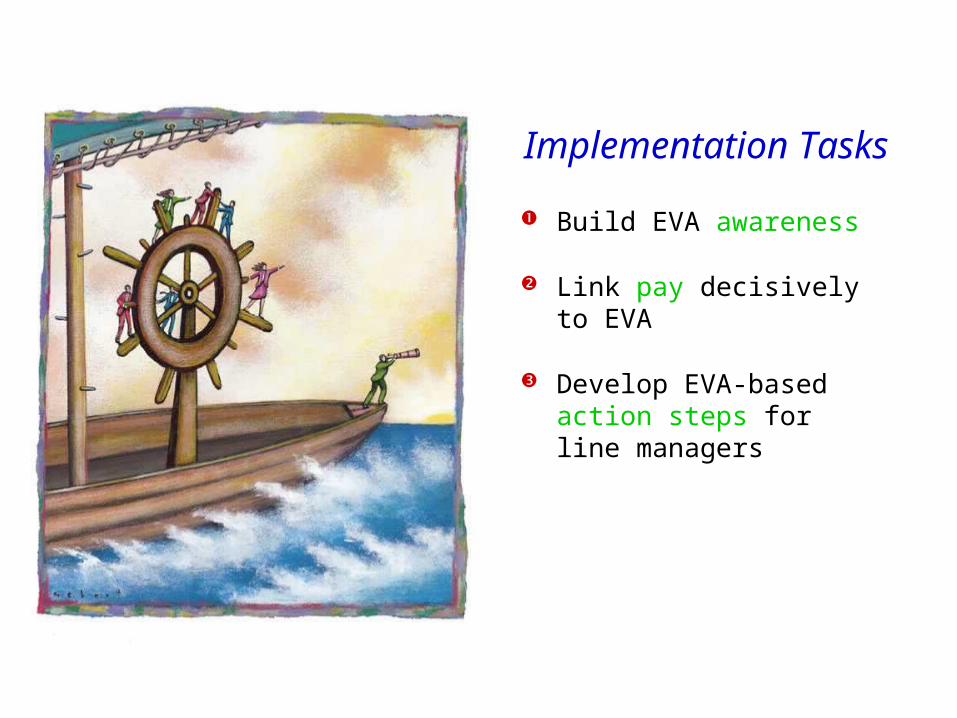

Implementation Tasks

Build EVA awareness

Link pay decisively to EVA

Develop EVA-based action steps for line managers

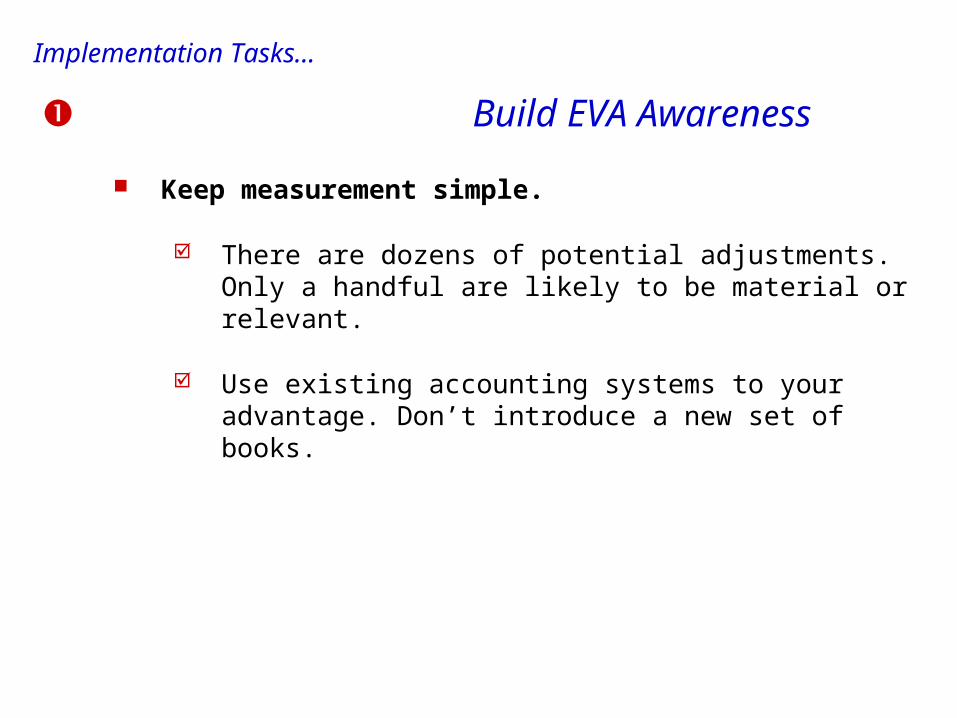

Build EVA Awareness

Keep measurement simple.

There are dozens of potential adjustments. Only a handful are likely to be material or relevant.

Use existing accounting systems to your advantage. Don’t introduce a new set of books.

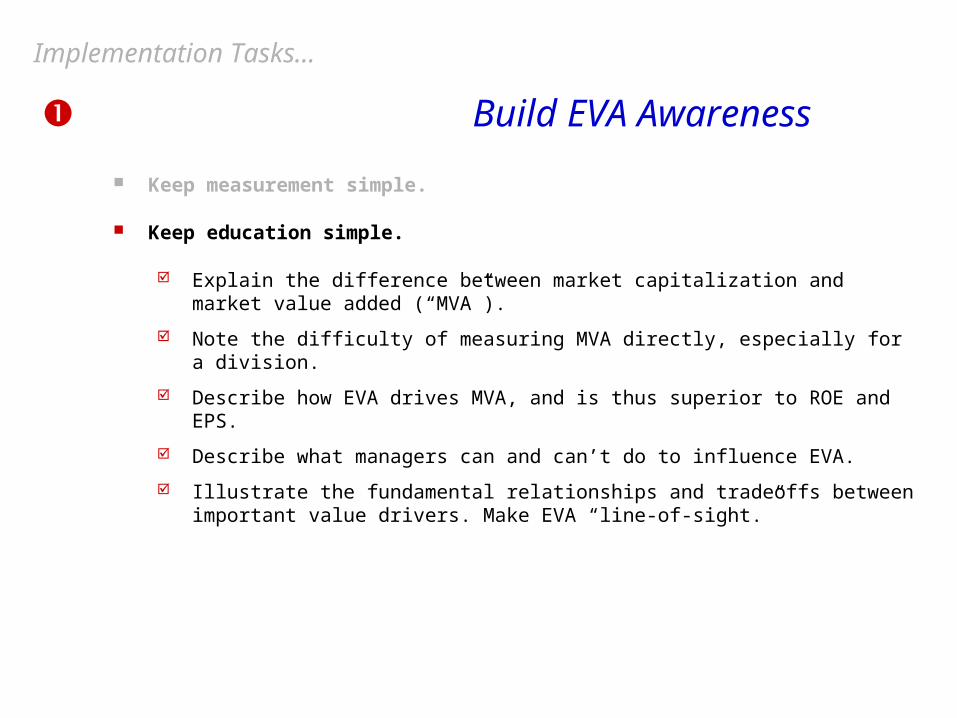

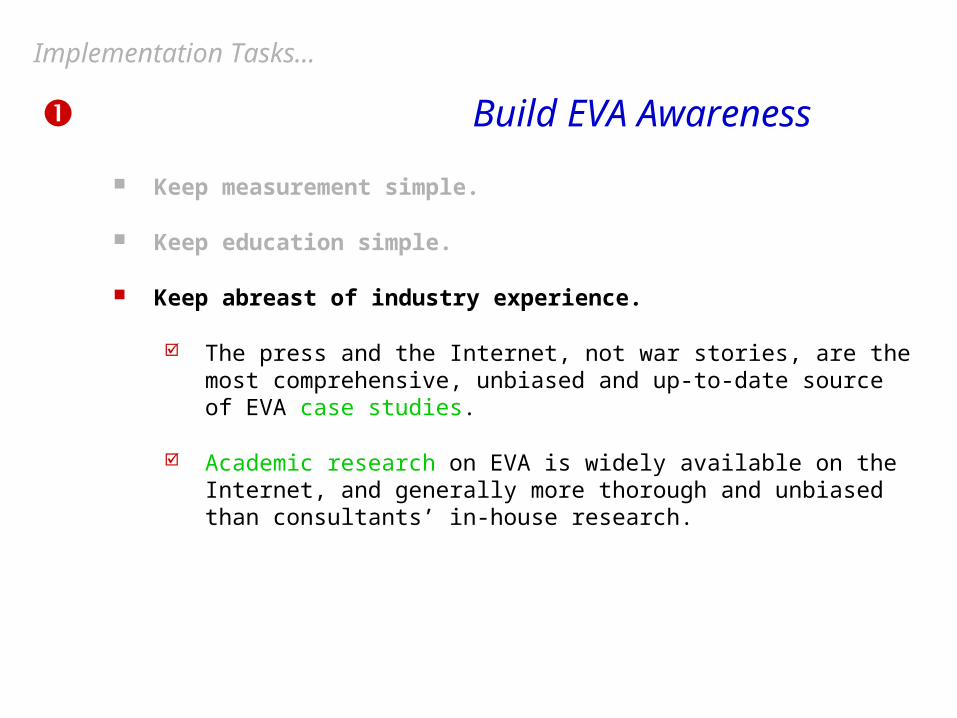

Implementation Tasks...

Build EVA Awareness

Keep measurement simple.

Keep education simple.

Explain the difference between market capitalization and market value added (“MVA”).

Note the difficulty of measuring MVA directly, especially for a division.

Describe how EVA drives MVA, and is thus superior to ROE and EPS.

Describe what managers can and can’t do to influence EVA.

Illustrate the fundamental relationships and tradeoffs between important value drivers. Make EVA “line-of-sight.”

Implementation Tasks...

Build EVA Awareness

Keep measurement simple.

Keep education simple.

Keep abreast of industry experience.

The press and the Internet, not war stories, are the most comprehensive, unbiased and up-to-date source of EVA case studies.

Academic research on EVA is widely available on the Internet, and generally more thorough and unbiased than consultants’ in-house research.

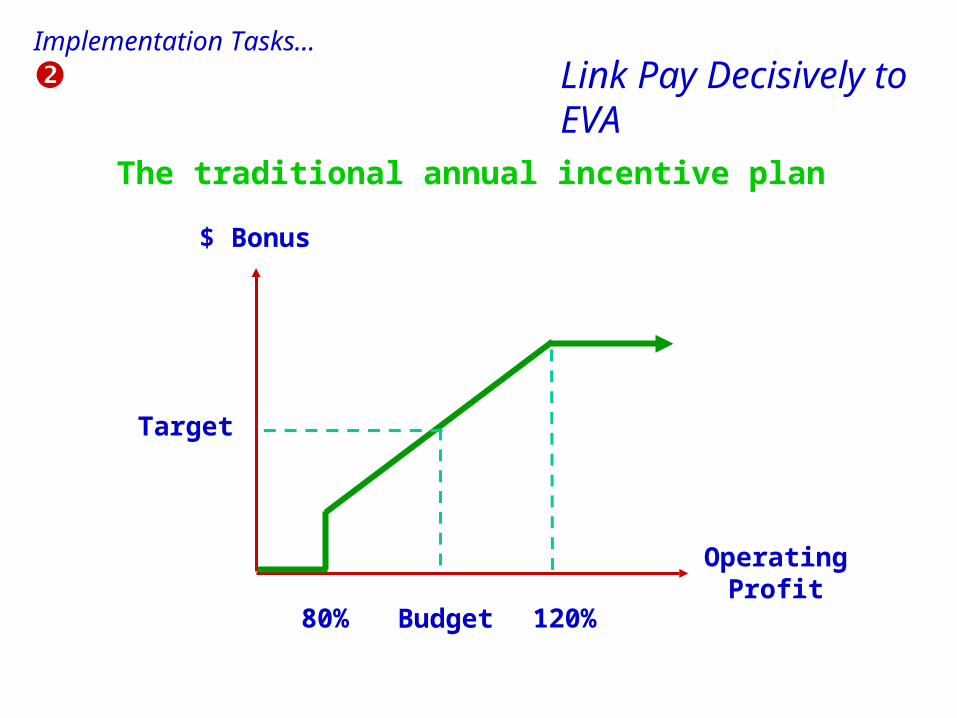

Implementation Tasks...

The traditional annual incentive plan

Target

$ Bonus

OperatingProfit

Budget80% 120%

Link Pay Decisively to EVA

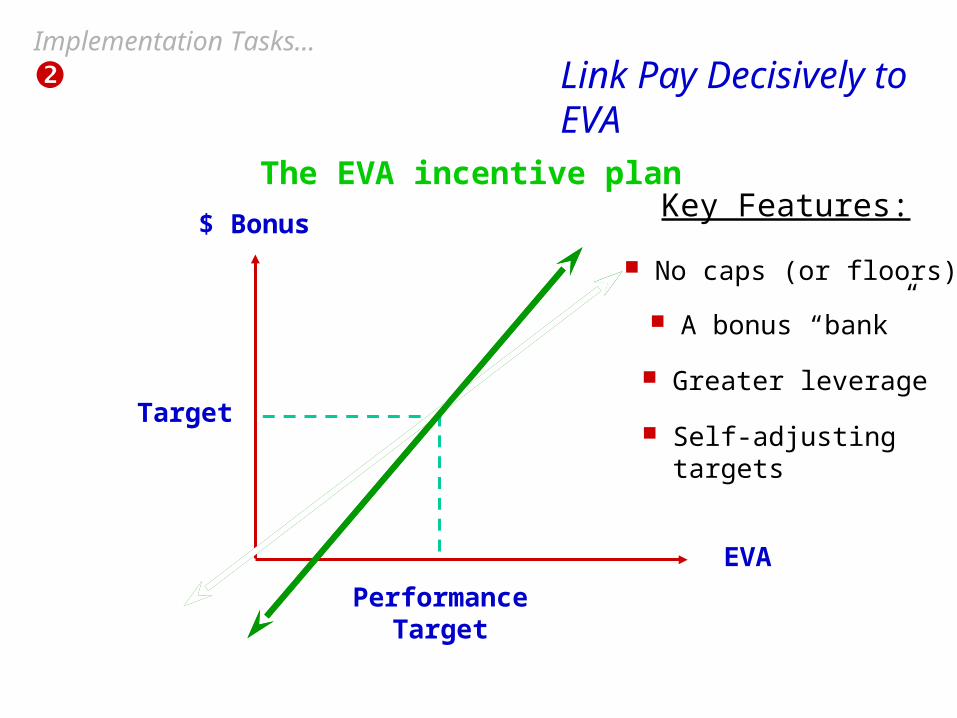

Implementation Tasks...

Target

$ Bonus

EVA

PerformanceTarget

Key Features:

No caps (or floors)

A bonus “bank”

Self-adjustingtargets

Greater leverage

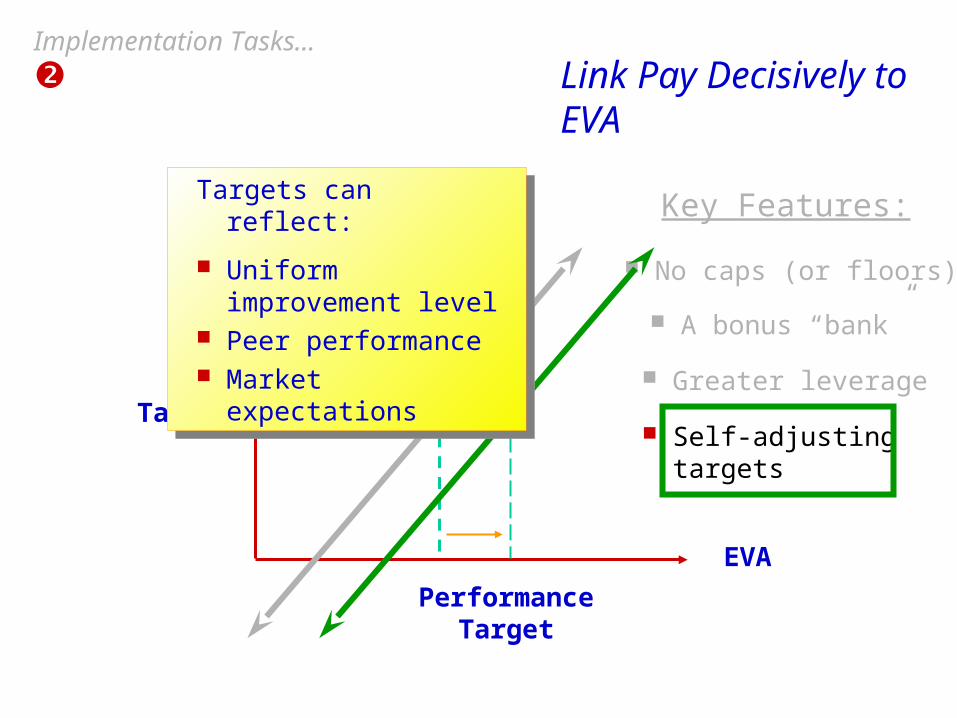

Link Pay Decisively to EVA

Implementation Tasks...

The EVA incentive plan

Target

$ Bonus

EVA

PerformanceTarget

Key Features:

No caps (or floors)

A bonus “bank”

Self-adjustingtargets

Greater leverage

Targets can reflect:

Uniform improvement level

Peer performance Market expectations

Targets can reflect:

Uniform improvement level

Peer performance Market expectations

Link Pay Decisively to EVA

Implementation Tasks...

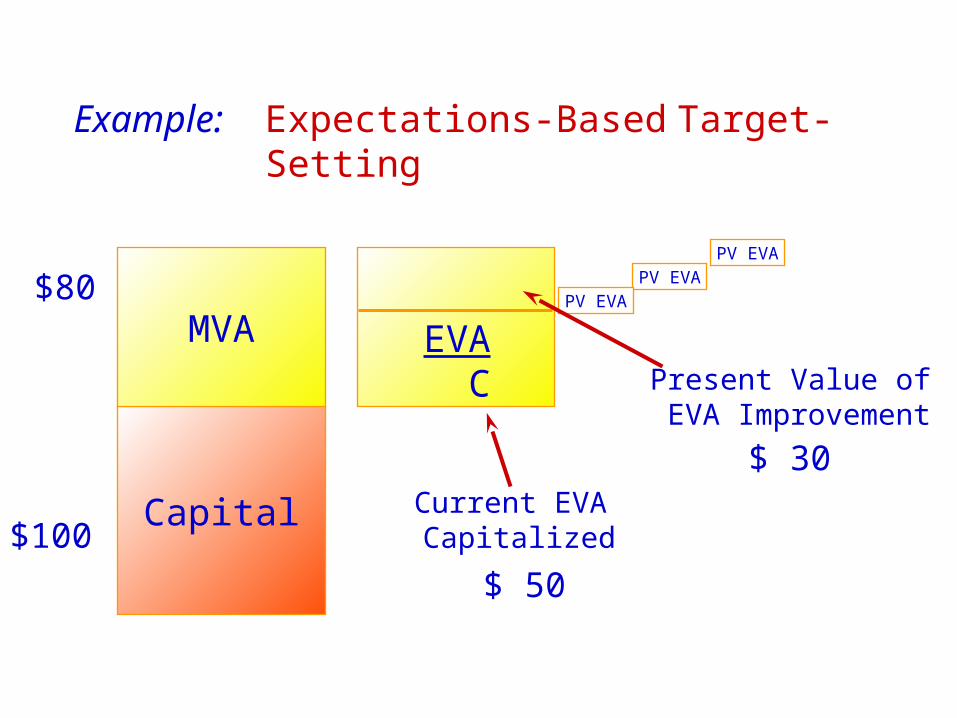

Example: Expectations-Based Target-Setting

Present Value of EVA Improvement

Current EVA Capitalized

$ 50

$80

$100Capital

MVA EVA C

$ 30

PV EVAPV EVA

PV EVA

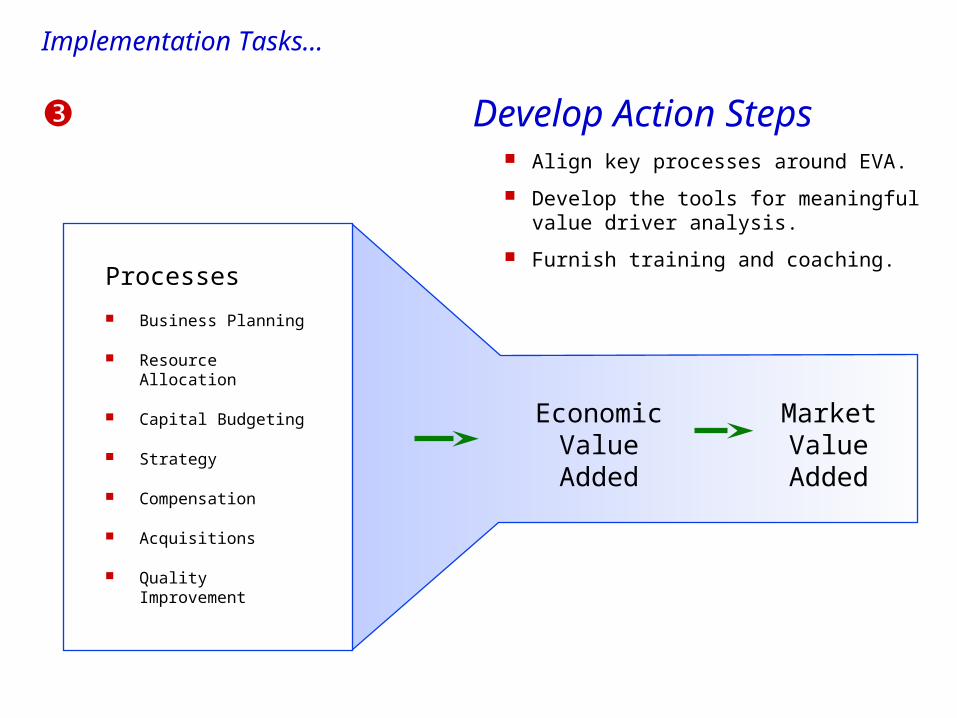

Develop Action Steps Align key processes around EVA.

Develop the tools for meaningful value driver analysis.

Furnish training and coaching.Processes

Business Planning

Resource Allocation

Capital Budgeting

Strategy

Compensation

Acquisitions

Quality Improvement

Economic Value Added

Market Value Added

Implementation Tasks...

Implementation Pitfalls Concentrating overly on the metric

Concentrating insufficiently on calibration

Not integrating EVA with other initiatives such as cycle time, customer satisfaction, and balanced scorecard

Not gaining early “buy-in” from operations

Analogizing too closely to LBO’s

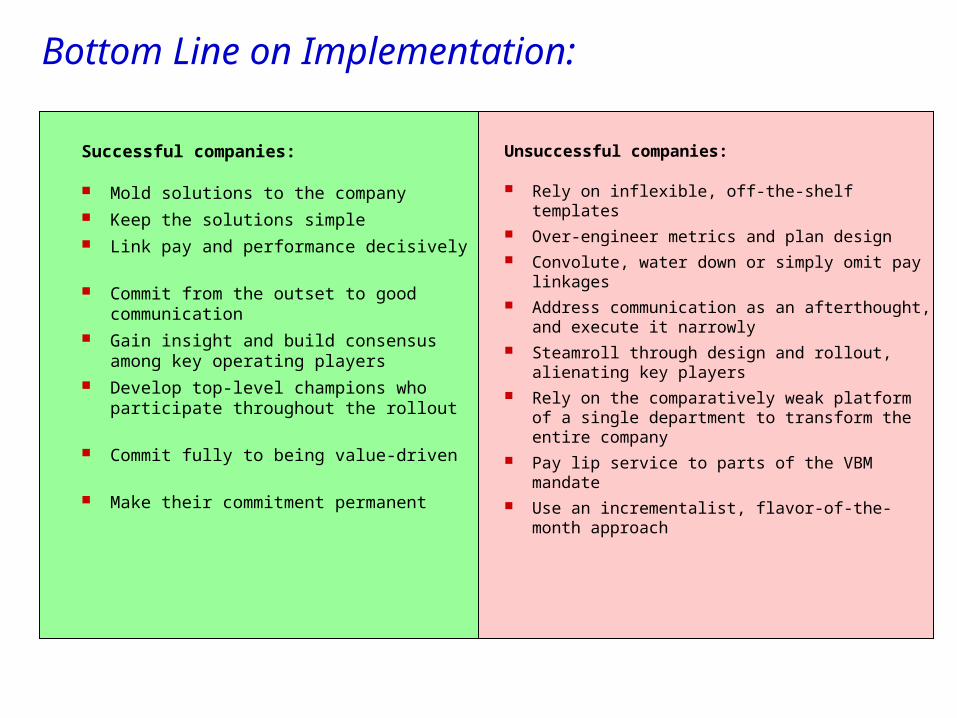

Successful companies:

Mold solutions to the company Keep the solutions simple Link pay and performance decisively

Commit from the outset to good communication

Gain insight and build consensus among key operating players

Develop top-level champions who participate throughout the rollout

Commit fully to being value-driven

Make their commitment permanent

Unsuccessful companies:

Rely on inflexible, off-the-shelf templates Over-engineer metrics and plan design Convolute, water down or simply omit pay

linkages Address communication as an afterthought,

and execute it narrowly Steamroll through design and rollout, alienating

key players Rely on the comparatively weak platform of a

single department to transform the entire company

Pay lip service to parts of the VBM mandate Use an incrementalist, flavor-of-the-month

approach

Bottom Line on Implementation:

The Next Step in EVA Development

Differentiate management performance from industry-wide performance.

Reformulate companies as management plays, rather than generalized bets on an industry or the economy.

Implications for:

Defining EVA Structuring equity incentives Communicating with investors Devising capital structure Planning models

Differentiating management performance...

Contention: Commodity price movements and stock market activity explain the vast majority of most companies’ stock price performance.

Example: The Specialty Chemical Industry

20% 10% 0% (10%) (20%)% Change in S&P 500

(10%)

(5%)

0%

5%

10%

% Change inMethanol Prices

(15%) (10%) (5%) 0% 5% 10% 15%

% Change in Market Value

(20%) 0% 20%% Change in Ethylene Prices

Sample:

Georgia Gulf CorpLyondell Petrochemical Co

Dow Chem Co

Union Carbide CorpOlin Corp

R 2

0 637

80 0%

.

.

Contention: Commodity price movements and stock market activity explain the vast majority of most companies’ stock price performance.

Contention: Commodity price movements and stock market activity explain the vast majority of most companies’ stock price performance.

Impact: Less than one-fifth of most industries’ stock market performance can be traced to contributions by management.

Conclusion:

During downturns, conventional stock and cash-based incentives are viewed as lottery tickets. During good times, conventional bonus plans perpetuate the impression that stockholder returns relate mainly to good management. Over time, even sub-par performance will be rewarded. Stockholders find all companies in an industry interchangeable.

Differentiating management performance...

Proposed solution? Short the competition

1. Index management’s stock options against industry performance.

Specifically: Exclude value gains (or losses) attributable to the S&P or industry.

Impact: Creates options where the difference between option value and exercise value (and thus the perception gap) is small. Justifies issuing more options as a consequence.

Examples: Dresser, Warner-Lambert, Itel

($40)

($20)

$0

$20

$40

$60

$80

$100

$120

$40 $60 $80 $100 $120 $140

1 Standard Option 1 Indexed Option 5.6 Indexed Options

1.0 Slope:

Slope: 5.4

Slope: 0.97

Portfolio of 5.6 at-the-money indexed options is worth just one out-of-the-money option, but ...

The difference in upside (and downside) potential is enormous, thus greatly amplifying incentives.

Opt

ion

Valu

e

Stock Value

Proposed solution? Short the competition

1. Index management’s stock options against industry performance.

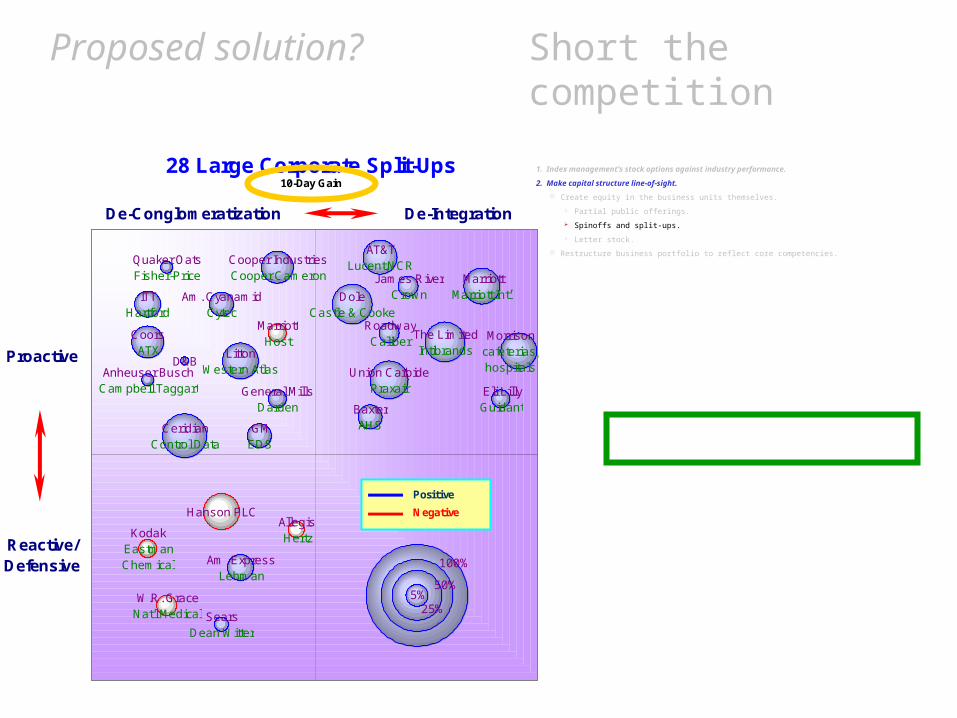

2. Make capital structure line-of-sight.

Create equity in the business units themselves.

Partial public offerings.

Spinoffs and split-ups.

Letter stock.

Restructure business portfolio to reflect core competencies.

28 Large Corporate Split-Ups10-Day Gain

5%25%

50%

100%

Hanson PLC

W.R. GraceNat'l Medical

MarriottHost

KodakEastman Chemical

AllegisHertz

D&BAnheuser Busch

Campbell Taggart

Quaker OatsFisher-Price

SearsDean Witter

General MillsDarden

Eli LillyGuidant

James RiverCrown

RoadwayCaliber

GMEDS

Am. CyanamidCytec

BaxterAHS

ITTHartford

Am. ExpressLehman

Cooper IndustriesCooper Cameron

CoorsATX

AT&TLucent,NCR

Morrisoncafeterias, hospitals

MarriottMarriott Int'l

LittonWestern Atlas Union Carbide

Praxair

DoleCastle & Cooke

The LimitedIntibrands

CeridianControl Data

De-Conglomeratization De-Integration

Proactive

Reactive/Defensive

Positive

Negative

Proposed solution? Short the competition

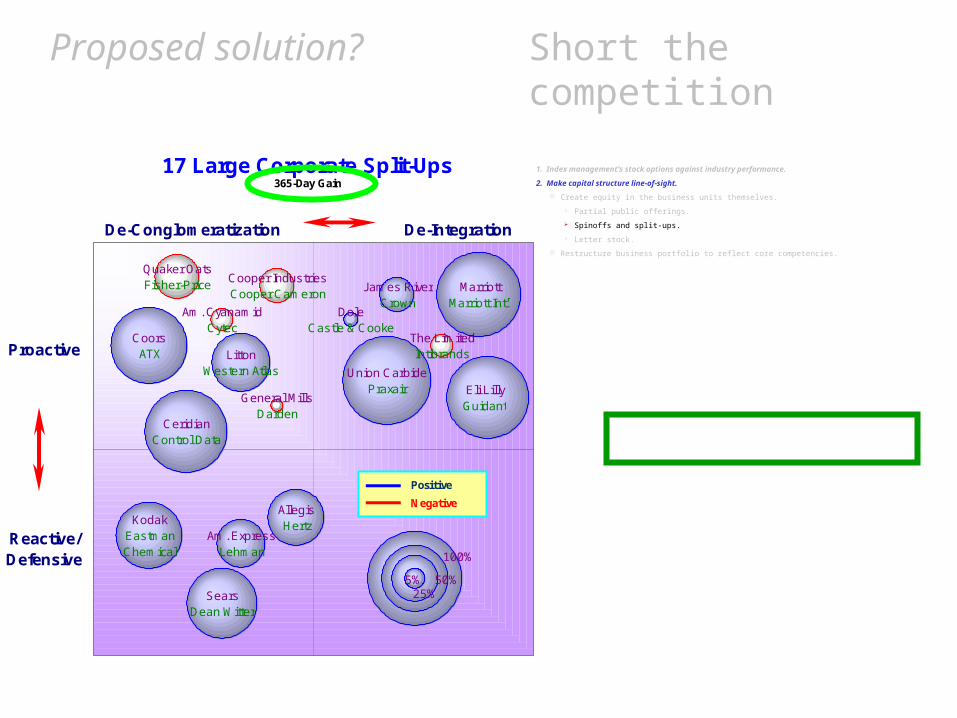

1. Index management’s stock options against industry performance.

2. Make capital structure line-of-sight.

Create equity in the business units themselves.

Partial public offerings.

Spinoffs and split-ups.

Letter stock.

Restructure business portfolio to reflect core competencies.

17 Large Corporate Split-Ups365-Day Gain

100%

5%25%

50%

Union CarbidePraxair

MarriottMarriott Int'l

CeridianControl Data

Eli LillyGuidant

CoorsATX

SearsDean Witter

KodakEastman Chemical

LittonWestern Atlas

AllegisHertz

Am. ExpressLehman

James RiverCrown

DoleCastle & Cooke

General MillsDarden

Am. CyanamidCytec

The LimitedIntibrands

Cooper IndustriesCooper Cameron

Quaker OatsFisher-Price

De-Conglomeratization De-Integration

Proactive

Reactive/Defensive

Positive

Negative

Proposed solution? Short the competition

1. Index management’s stock options against industry performance.

2. Make capital structure line-of-sight.

Create equity in the business units themselves.

Partial public offerings.

Spinoffs and split-ups.

Letter stock.

Restructure business portfolio to reflect core competencies.

Proposed solution? Short the competition

1. Index management’s stock options against industry performance.

2. Make capital structure line-of-sight.

3. Make the stock a management play rather than an industry play.

Issue equity-linked debt—pegged to the stock price of competitors.

Proposed solution? Short the competition

1. Index management’s stock options against industry performance.

2. Make capital structure line-of-sight.

3. Make the stock a management play rather than an industry play.

Specifics: DECS or Prides issued against competitors.

Hybrid debt instruments whose interest payments are linked to the performance of a particular stock—in this case, a market-weighted or equally-weighted portfolio of competitors.

Examples: Lyondell, Enron, NationsBank, Netscape, Nextel, Telecom Argentina

Proposed solution? Short the competition

1. Index management’s stock options against industry performance.

2. Make capital structure line-of-sight.

3. Make the stock a management play rather than an industry play.

Indexed capital structures...

Are an inexpensive way for company, and thus its shareholders, to place an extended bet against the competition while investing long in management.

Lessen industry risk (and thus beta).

Lower the cost of capital.

Improve cash flow.

Transform investing in company from an industry play into a management play without shuffling investors.

Proposed solution? Short the competition

1. Index management’s stock options against industry performance.

2. Make capital structure line-of-sight.

3. Make the stock a management play rather than an industry play.

Issue equity-linked debt—pegged to the stock price of competitors.

Issue commodity-linked debt—pegged to the price of raw materials.

Proposed solution? Short the competition

1. Index management’s stock options against industry performance.

2. Make capital structure line-of-sight.

3. Make the stock a management play rather than an industry play.

4. Index MVA and EVA.

XVA Dollar amount of MVA created during a prescribed number of years, over and above the MVA created by competitors—after indexing competitors’ beginning capital to the company’s

XEP Dollar increase in EVA during a prescribed number of years that cannot be explained by changes in the economic profit of competitors—again adjusted to reflect differences in beginning capital

Proposed solution? Short the competition

1. Index management’s stock options against industry performance.

2. Make capital structure line-of-sight.

3. Make the stock a management play rather than an industry play.

4. Index MVA and EVA.

5. Make planning models real-time and contingency aware.

Build probabilistic models, not charts of account.

Plan contingencies in advance.

Adapt targets based on real-time changes in externalities.

EVA in a nutshell EVA is more than a metric.

EVA can and should be simple.

Incentives must be powerful, consistent, and involve real at-risk capital.

Relative performance measures would address a significant defect of many EVA initiatives: inability to respond to changing industry or market conditions.

Management’s commitment to change must be fundamental.