Dealing with Multiple Sources of CARES Act Funding ...

69

Dealing with Multiple Sources of CARES Act Funding (Provider Relief Funding, PPP Loans, Accelerated Payments) and Preparation for Reporting Meg Pekarske, JD Husch Blackwell Bryan Nowicki, JD Husch Blackwell Mark Sharp, CPA, BKD M. Aaron Little, CPA, BKD Ted Cuppett, CPA, The Health Group 1

Transcript of Dealing with Multiple Sources of CARES Act Funding ...

Dealing with Multiple Sources of

CARES Act Funding (Provider Relief

Funding, PPP Loans, Accelerated

Payments) and Preparation for

Reporting

Meg Pekarske, JD Husch Blackwell

Bryan Nowicki, JD Husch Blackwell

Mark Sharp, CPA, BKD

M. Aaron Little, CPA, BKD

Ted Cuppett, CPA, The Health Group

1

Housekeeping• Instructions for Zoom questions

• No CEUs are awarded for this webinar

• Information presented is accurate as of May 18, 2020 but subject to change, based on changes in guidance from the federal government

2

Thank You• Faculty for today:

• Husch Blackwell: Meg Pekarske, JD and Bryan Nowicki, JD

• BKD: Mark Sharp, CPA and Aaron Little, CPA

• The Health Group: Ted Cuppett, CPA

3

CARES Act Provider Relief Fund

Payments: Terms and Conditions

Overview

Meg Pekarske, JD Husch Blackwell

Bryan Nowicki, JD Husch Blackwell

4

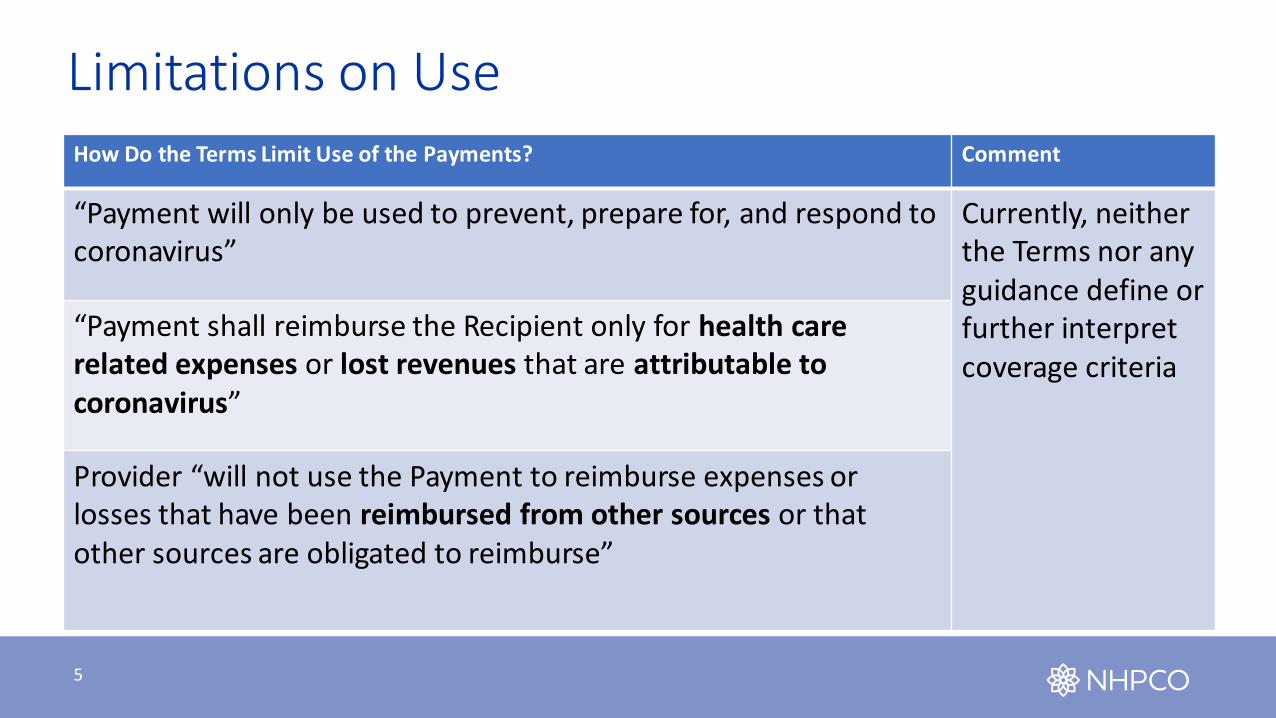

Limitations on UseHow Do the Terms Limit Use of the Payments? Comment

“Payment will only be used to prevent, prepare for, and respond to coronavirus”

Currently, neither the Terms nor any guidance define or further interpret coverage criteria

“Payment shall reimburse the Recipient only for health care related expenses or lost revenues that are attributable to coronavirus”

Provider “will not use the Payment to reimburse expenses or losses that have been reimbursed from other sources or that other sources are obligated to reimburse”

5

Evaluation Strategies• In the absence of additional guidance or rulemaking, how can providers

evaluate what expenses and losses may be covered?• Apply a “defense mindset”

• Use a “reasonableness” standard

• Understand the “risk continuum”

• Be guided by the purpose of the Payments

• Keep “optics/big picture” at the forefront

6

Documentation: Key Provisions in 45 C.F.R. Pt. 75Requirement Citation

The provider’s financial management systems must:

Be sufficient to permit “the tracing of funds to a level of expenditures adequate to establish that such funds have been used according to . . . the terms and conditions of the Federal award” and federal law

§ 75.302(a)

Provide for “[r]ecords that identify adequately the source and application of funds for federally-funded activities”

§ 75.302(b)(3)

Provide for “[e]ffective control over, and accountability for, all funds, property, and other assets”

§ 75.302(b)(4)

Provide for “[c]omparison of expenditures with budget amounts for each Federal award” § 75.302(b)(5)

Provide for “[w]ritten procedures to implement the requirements of § 75.305” § 75.302(b)(6)

All records pertinent to the federal award must be retained for 3 years from submission of final expenditure report

§ 75.361

HHS must have right of access to any records pertinent to the federal award “in order to make audits, examinations, excerpts, and transcripts”

§ 75.364

7

“Reasonableness” Considerations• Consistency—Are you treating similar expenses and losses the same?

• Benchmark—What benchmark will you use to quantify the expense or loss?

• HHS: Providers may use “a reasonable method” of estimating lost revenue attributable to coronavirus through benchmarks (e.g., budgeted revenue or revenue from same period in 2019)1

• Necessity—Is the expense necessary or merely discretionary?

• Coverage from Another Source?

• Per diem? Business interruption insurance? Other government funding (e.g., PPP loans)?

• What Is Your Risk Tolerance?

• What Is Your Big Picture?

• Adding it up—Would your individual decisions when combined give the appearance that your organization is financially “better off”?

8

Potential Enforcement forMisuse of Relief Fund Payments• HHS: “There will be significant anti-fraud and auditing work done by HHS,

including the work of the Office of the Inspector General.”1

• Potential enforcement actions or risks that could arise from misuse of Payments include:• Cost disallowance, termination of the award, and debarment from future awards• OIG audits, civil money penalties, and exclusion from federal and state health care

programs• False Claims Act criminal and civil liability

• See Husch Blackwell article further describing these potential enforcement actions and risks : https://www.huschblackwell.com/newsandinsights/risks-of-spending-public-health-and-social-services-emergency-fund-payments

9

Meg S.L. PekarskePartner608.234.6014meg.pekarske@huschblackwellcom

Bryan K. NowickiPartner608.234.6012bryan.nowicki@huschblackwellcom

10

Update on Provider Relief FundingMark Sharp, CPA

BKD

11

Partial Summary of “Relief Funds” for Hospice Providers

•Public Health & Social Services Emergency Fund (PHSSEF) administered by the U.S. Department of Health and Human Services (HHS)

•Also known as CARES Act Provider Relief Fund PaymentsHHS Emergency Funds

•Paycheck Protection Program (PPP) loans administered through the U.S. Small Business Administration (SBA) PPP Loans from SBA

•Expansion of the Accelerated & Advanced Payments (AAP) Program administered by the Centers for Medicare & Medicaid Services (CMS) CMS AAP Program

•Potential Business Interruption (BI) insurance coverage•Public Assistance Program administered by the Federal Emergency Management

Agency (FEMA)Other Options

12

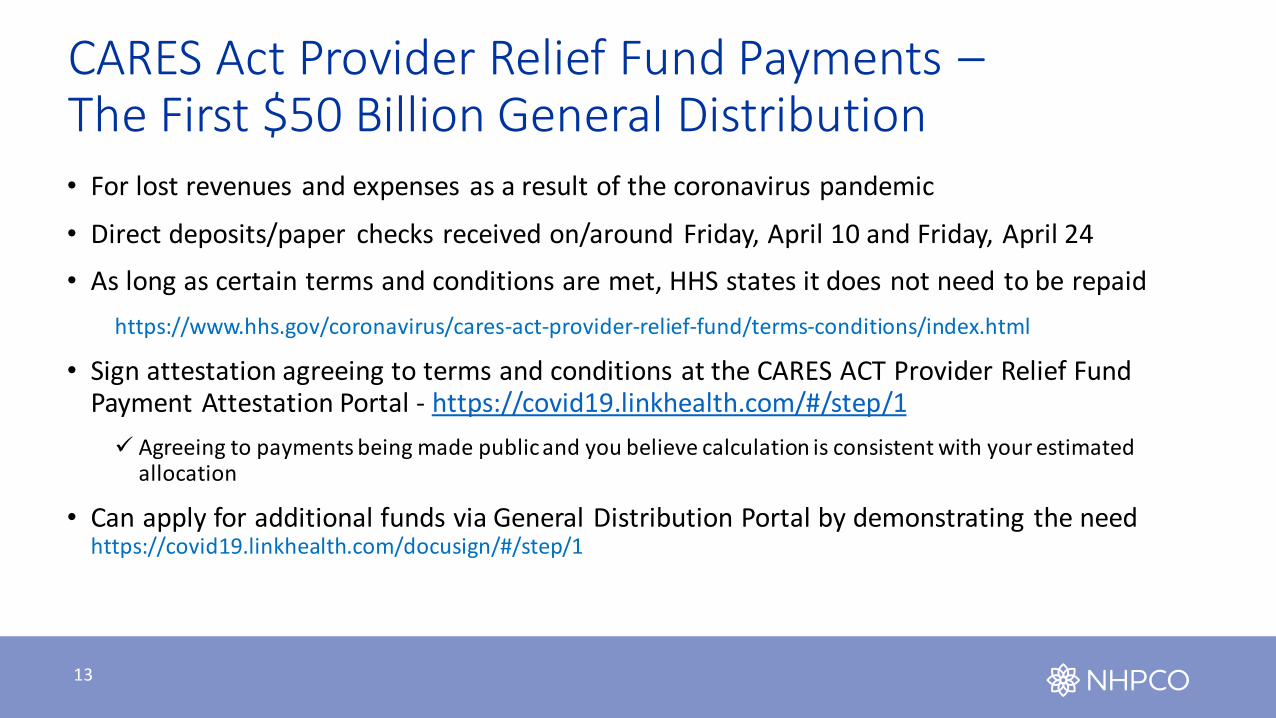

CARES Act Provider Relief Fund Payments –The First $50 Billion General Distribution• For lost revenues and expenses as a result of the coronavirus pandemic

• Direct deposits/paper checks received on/around Friday, April 10 and Friday, April 24

• As long as certain terms and conditions are met, HHS states it does not need to be repaid

https://www.hhs.gov/coronavirus/cares-act-provider-relief-fund/terms-conditions/index.html

• Sign attestation agreeing to terms and conditions at the CARES ACT Provider Relief Fund Payment Attestation Portal - https://covid19.linkhealth.com/#/step/1

✓ Agreeing to payments being made public and you believe calculation is consistent with your estimated allocation

• Can apply for additional funds via General Distribution Portal by demonstrating the need https://covid19.linkhealth.com/docusign/#/step/1

13

Sample Calculation – Initial HHS Distribution

6.2%

6.2%

14

Sample Calculation – Second HHS Distribution

2.0%

2.0%

15

Terms and Conditions• Funds received will only be used to:

✓Prevent, prepare for and respond to coronavirus

✓Reimburse only for health care related expenses or lost revenues attributable to coronavirus

• Funds will not be used to reimburse expenses or losses reimbursed from other sources or that other sources are obligated to reimburse

16

Terms and Conditions• Reporting required for providers receiving greater than $150,000 total in funds related to any

COVID Act

• Within 10 days after the end of each calendar quarter

• Providers receiving less than $150,000 can be subject to additional reporting

• Recipients are expected to maintain appropriate records and cost documentation to substantiate monies received and kept – regardless of amount of funds received

• Submit general revenue data (NPSR data) for calendar year 2018 to the Secretary when applying to receive a Payment, or within 30 days of having received a Payment

• Much uncertainty on revenue submission requirement if only received funds from the initial distribution only

17

Emergency Funds – NPSR Issues

No Revenue Reported On Cost Report

Accrual Versus Cash Basis Reporting

New Provider After 2018

Consolidated Reporting for

Chains

Double Dipping by Contractors

18

Paycheck Protection ProgramSBA-GUARANTEED LOAN PROGRAM

William T. (Ted) Cuppett, CPA

20

KEEPING AMERICAN WORKERS PAID AND EMPLOYED ACT

• Eligibility: During the covered period, in addition to small business concerns, any business concern, nonprofit organization, veterans organization, or Tribal business concern described in section 31(b)(2)(C) shall be eligible to receive a covered loan if the business concern, nonprofit organization, veterans organization, or Tribal business concern employs not more than the greater of 500 employees; or if applicable, the size standard in number of employees established by the Administration for the industry in which the business concern, nonprofit organization, veterans organization, or Tribal business concern operates.

21

Employee

“For purposes of determining whether a business concern, nonprofit organization, veterans organization, or Tribal business concern described in section 31(b)(2)(C) employs not more than 500 employees under clause (i)(I), the term ‘employee’ includes individuals employed on a full-time, part-time, or other basis.”

These are not FTE employees; this is a total count. This is used for loan qualification, not forgiveness.

22

Maximum Loan Amount

• “The sum of the product obtained by multiplying the average total monthly payments by the applicant for payroll costs incurred during the 1-year period before the date on which the loan is made, except that, in the case of an applicant that is a seasonal employer, as determined by the Administrator, the average total monthly payments for payroll shall be for the 12-week period beginning February 15, 2019, or at the election of the eligible recipient, March 1, 2019, and ending June 30, 2019; by 2.5.”

23

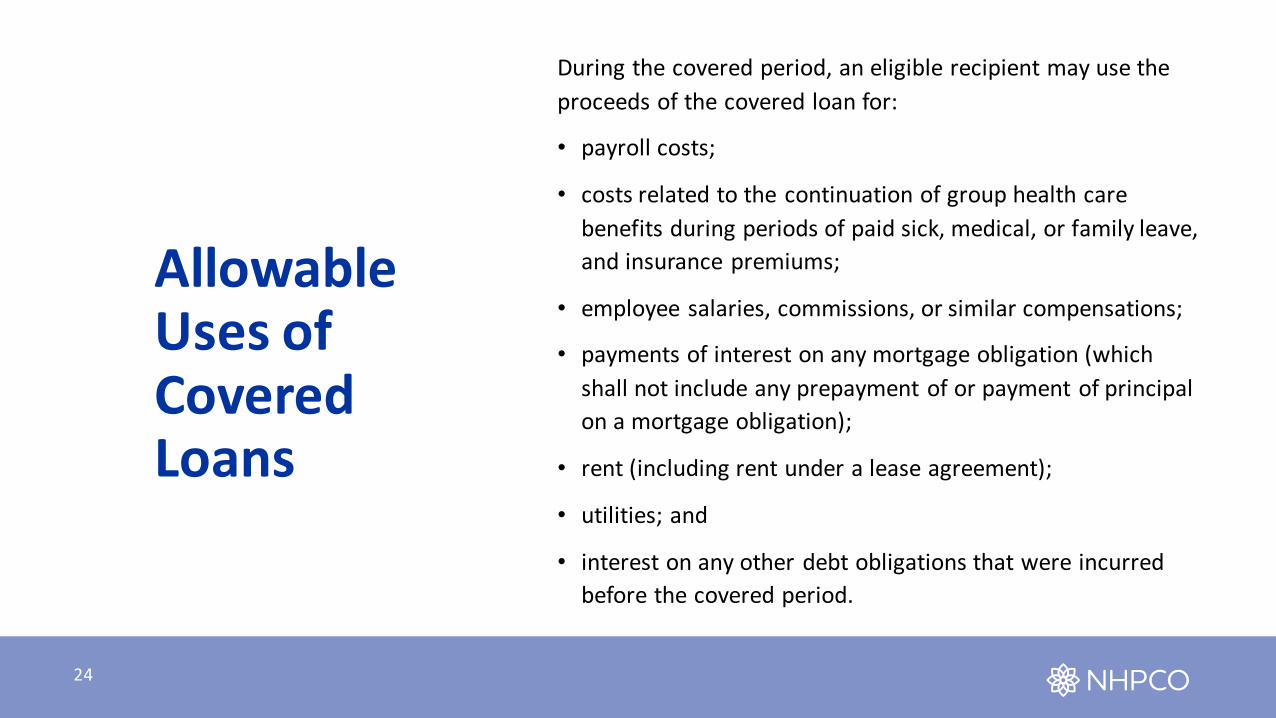

Allowable Uses of Covered Loans

During the covered period, an eligible recipient may use the

proceeds of the covered loan for:

• payroll costs;

• costs related to the continuation of group health care

benefits during periods of paid sick, medical, or family leave,

and insurance premiums;

• employee salaries, commissions, or similar compensations;

• payments of interest on any mortgage obligation (which

shall not include any prepayment of or payment of principal

on a mortgage obligation);

• rent (including rent under a lease agreement);

• utilities; and

• interest on any other debt obligations that were incurred

before the covered period.

24

Nonrecourse

• “Notwithstanding the waiver of the personal guarantee requirement or collateral under subparagraph (J), the Administrator shall have no recourse against any individual shareholder, member, or partner of an eligible recipient of a covered loan for nonpayment of any covered loan, except to the extent that such shareholder, member, or partner uses the covered loan proceeds for a purpose not authorized under clause (i).”

• TO BANK – “During the covered period, with respect to a covered loan—no personal guarantee shall be required for the covered loan; and no collateral shall be required for the covered loan.”

25

Certification• “An eligible recipient applying for a covered loan shall make a good faith certification—

• (I) that the uncertainty of current economic conditions makes necessary the loan request to support the ongoing operations of the eligible recipient;

• II) acknowledging that funds will be used to retain workers and maintain payroll or make mortgage payments, lease payments, and utility payments;

• (III) that the eligible recipient does not have an application pending for a loan under this subsection for the same purpose and duplicative of amounts applied for or received under a covered loan; and

• (IV) during the period beginning on February 15, 2020 and ending on December 31, 2020, that the eligible recipient has not received amounts under this subsection for the same purpose and duplicative of amounts applied for or received under a covered loan.”

26

Documenting Uncertainty• The current and estimated impact of COVID-19 to the business including uncertainties which

may be supported by communication from referral sources, contracting partners, patients, the MAC, CMS, and others regarding operations both today and in the future,

• History of the business and its financial performance,

• Cash reserves, borrowing ability, and servicing existing debt,

• Current and future plans regarding employee retention, workforce reductions, payroll costs, and estimated ability to reinstate lost workforce,

• Activities currently underway or anticipated to address economic uncertainty related to items other than payroll-related issues, and

• Anticipated revenue impacts both short-term and long-term because of the COVID-19 PHE.

27

Uncertainty – Further Clarification• Question: How will SBA review the borrower’s required good-faith certification concerning the necessity of their loan request?

• Answer: When submitting a PPP application, all borrowers must certify in good faith that “current economic uncertainty makes this loa n request necessary to support the ongoing operations of the Applicant.” SBA, in consultation with the Department of the Treasu ry, has determined that the following safe harbor will apply to SBA’s review of PPP loans with respect to this issue: Any borrower th at, together with its affiliates, received PPP loans with an original principal amount of less than $2 million will be deemed to have made the required certification concerning the necessity of the loan request in good faith.

• SBA has determined that this safe harbor is appropriate because borrowers with loans below this threshold are generally less likely to have had access to adequate sources of liquidity in the current economic environment than borrowers that obtained larger loan s. This safe harbor will also promote economic certainty as PPP borrowers with more limited resources endeavor to retain and rehire employees. In addition, given the large volume of PPP loans, this approach will enable SBA to conserve its finite audit resources and focus its reviews on larger loans, where the compliance effort may yield higher returns.

• If SBA determines in the course of its review that a borrower lacked an adequate basis for the required certification concern ing the necessity of the loan request, SBA will seek repayment of the outstanding PPP loan balance and will inform the lender that th e borrower is not eligible for loan forgiveness. If the borrower repays the loan after receiving notification from SBA, SBA will not pursue administrative enforcement or referrals to other agencies based on its determination with respect to the certification concerning necessity of the loan request.

28

Debt ForgivenessAn eligible recipient shall be eligible for forgiveness of indebtedness on a covered loan in an amount equal to the sum of the following costs incurred and payments made during the covered period:

• Payroll costs

• Any payment of interest on any covered mortgage obligation (which shall not include any prepayment of or payment of principal on a covered mortgage obligation)

• Any payment on any covered rent obligation.

• Any covered utility payment.

29

Covered Period• The term ‘‘covered period’’ means the 8-week period beginning on the

date of the origination of a covered loan ); DATE THAT FUNDS WERE DEPOSITED INTO THE RECIPIENT’S BANK ACCOUNT.

• There is now an Alternative Payroll Covered Period relating to payroll costs. Discussed later.

30

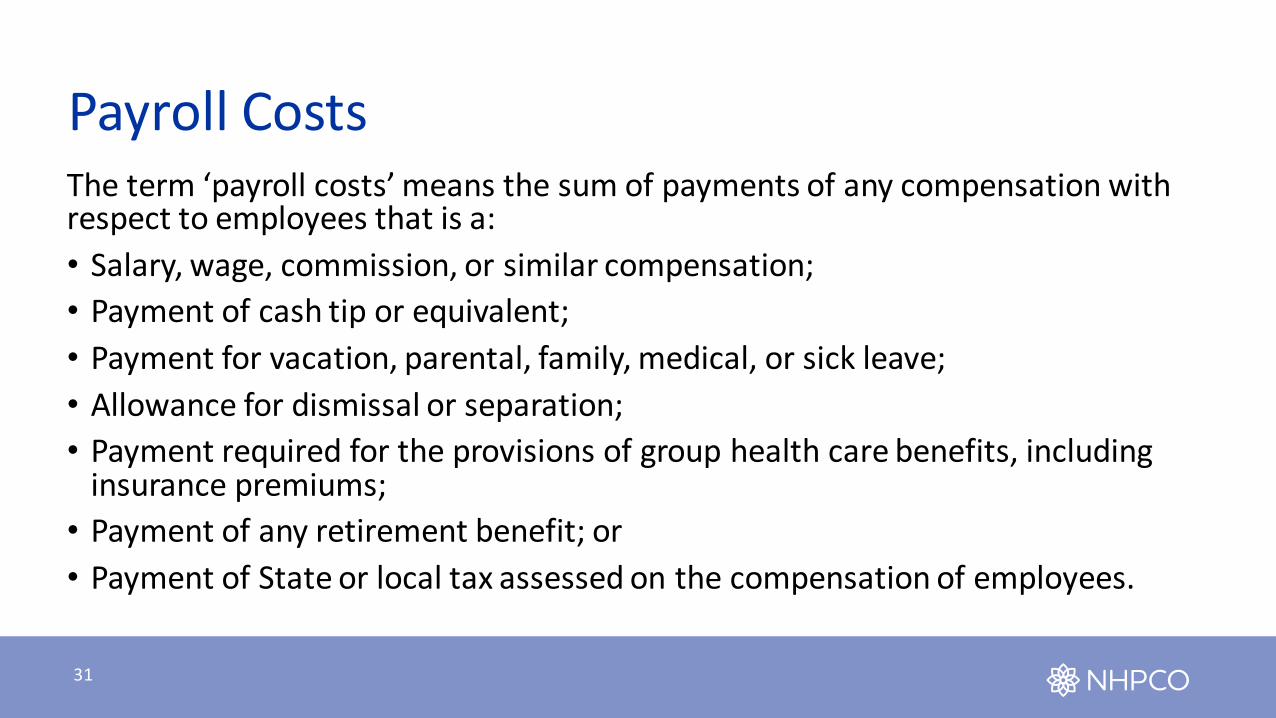

Payroll CostsThe term ‘payroll costs’ means the sum of payments of any compensation with respect to employees that is a:

• Salary, wage, commission, or similar compensation;

• Payment of cash tip or equivalent;

• Payment for vacation, parental, family, medical, or sick leave;

• Allowance for dismissal or separation;

• Payment required for the provisions of group health care benefits, including insurance premiums;

• Payment of any retirement benefit; or

• Payment of State or local tax assessed on the compensation of employees.

31

Payroll Costs Do Not Include• The compensation of an individual employee in excess of an annual salary of

$100,000, as prorated for the covered period;

• Taxes imposed or withheld under chapters 21, 22, or 24 of the Internal Revenue Code of 1986 during the covered period;

• Any compensation of an employee whose principal place of residence is outside of the United States;

• Qualified sick leave wages for which a credit is allowed under section 7001 of the Families First Coronavirus Response Act (Public Law 116–127); or

• Qualified family leave wages for which a credit is allowed under section 7003 of the Families First Coronavirus Response Act (Public Law 116–127).

32

Mortgage ObligationThe term ‘‘covered mortgage obligation’’ means any indebtedness or debt instrument incurred in the ordinary course of business that:

• Is a liability of the borrower;

• Is a mortgage on real or personal property; and

• Was incurred before February 15, 2020.

33

Rent Obligation• The term ‘‘covered rent obligation’’ means a rent obligated under a

leasing agreement in force before February 15, 2020.

34

Utility PaymentsThe term ‘‘covered utility payment’’ means payment for a service for the distribution of:• electricity, • gas,• water,• transportation,• telephone, or• internet access

Service had to have started before February 15, 2020;

35

Limitations On Forgiveness• FIRST LIMITATION-The amount of loan forgiveness under this section shall be reduced, but

not increased, by multiplying the amount described in subsection by the quotient obtained by

dividing the average number of full-time equivalent employees per month employed by the

eligible recipient during the covered period; by at the election of the borrower:

• the average number of full-time equivalent employees per month employed by the eligible recipient

during the period beginning on February 15, 2019 and ending on June 30, 2019; or

• the average number of full-time equivalent employees per month employed by the eligible recipient

during the period beginning on January 1, 2020 and ending on February 29, 2020.

The average number of full-time equivalent employees shall be determined by calculating the

average number of full-time equivalent employees for each pay period falling within a month.

36

Limitations On Forgiveness

• SECOND LIMITATION - The amount of loan forgiveness under this section shall be reduced by the amount of any reduction in total salary or wages of any employee described in subparagraph (B) during the covered period that is in excess of 25 percent of the total salary or wages of the employee during the most recent full quarter during which the employee was employed before the covered period.

• An employee described in this subparagraph is any employee who did not receive, during any single pay period during 2019, wages or salary at an annualized rate of pay in an amount more than $100,000.

37

Exemption For Re-hires• The amount of loan forgiveness under this section shall be determined without regard to a

reduction in the number of full-time equivalent employees of an eligible recipient or a reduction in the salary of or more employees of the eligible recipient, as applicable, during the period beginning on February 15, 2020 and ending on the date that is 30 days after the date of enactment of this Act, if• During the period beginning on February 15, 2020 and ending on the date that is 30 days after the date of

enactment of this Act, there is a reduction, as compared to February 15, 2020, in the number of full-time equivalent employees of an eligible recipient; and not later than June 30, 2020, the eligible employer has eliminated the reduction in the number of full-time equivalent employees;

• During the period beginning on February 15, 2020 and ending on the date that is 30 days after the date of enactment of this Act, there is a reduction, as compared to February 15, 2020, in the salary or wages of 1 or more employees of the eligible recipient; and not later than June 30, 2020, the eligible employer has eliminated the reduction in the salary or wages of such employees; or in which the events described in clause (i) and (ii) occur.

• Offer to rehire and employee declines employment?

38

Required DocumentationDocumentation verifying the number of full-time equivalent employees on payroll and pay rates for the periods described in subsection (d), including—

• Payroll tax filings reported to the Internal Revenue Service; and State income, payroll, and unemployment insurance filing

• Documentation, including cancelled checks, payment receipts, transcripts of accounts, or other documents verifying payments on covered mortgage obligations, payments on covered lease obligations, and covered utility payments;

• A certification from a representative of the eligible recipient authorized to make such certifications that the documentation presented is true and correct; and the amount for which forgiveness is requested was used to retain employees, make interest payments on a covered mortgage obligation, make payments on a covered rent obligation, or make covered utility payments; and

• Any other documentation the Administrator determines necessary.

39

Taxability• For purposes of the Internal Revenue Code of 1986, any amount which

(but for this subsection) would be includible in gross income of the eligible recipient by reason of forgiveness shall be excluded from gross income.

• IRS Notice 2020-32 and subsequent action.

40

Actions• STEP 1: Securing the loan

• By now, eligible healthcare providers have already applied for, secured the loan, or an application is pending. Due to the significant demand for these loans, it is doubtful, unless the program is expanded again, that any healthcare provider that has not applied will receive loan proceeds. Accordingly, we have briefly discussed the criteria for the loan and the application itself.

41

Actions• STEP 2: Preparing for forgiveness (FTE employees)

• The amount of the loan forgiveness will be reduced based on a reduction in FTE employees. This reduction is based on the lower number of FTE employees computed during two separate periods computed against FTE employees during the Covered Period. Accordingly, the average FTE employees per-month must be computed for the following periods and each payroll within these periods.

• February 15, 2019 through June 30, 2019

• January 1, 2020 through February 29, 2020

• Each loan recipient should secure information for each pay period that falls within the periods above to determine the number of FTE employees which will be compared against the payroll during the period that the loan proceeds are to be used. This loan forgiveness reduction can be reduced or remedied through June 30, 2020.

42

Actions• STEP 3: Preparing forgiveness (25% individual employee compensation)

• The amount of the loan forgiveness shall also be reduced by the amount of any reduction to total salaries or wages of any specific employee during the “Covered Period” that is in excess of 25% of the total salary and wages of that specific employee during the most recently completed full quarter during which the employee was employed before the covered period. Accordingly, the amount paid to each employee during the Covered Period will be compared to the quarter ended March 31, 2020. Loan recipients will need to secure a payroll summary, by employee, for the quarter ended March 31, 2020 to compare against the payrolls applicable to the Covered Period. This loan forgiveness reduction can be remedied through June 30, 2020.

43

Actions• 4: Projecting Expenses in Comparison to Loan:

• The healthcare provider should project the following expenses during the Covered Period for purposes of estimating the initial loan forgiveness prior to any FTE employee or 25% individual employee compensation reduction, briefly described above. Remember compensation to any employee who is paid in excess of $100,000 per-year is subject to reduction.

• Salaries and wages (gross pay, excluding employer-paid payroll taxes. Gross pay does not include mileage allowances and similar payments included in the employee’s paycheck which represents expense reimbursement; however, it does include bonus payments, overtime compensation, on-call compensation, vacation pay, parental leave, family leave, medical or sick leave, dismissal or separation pay, and similar items representing compensation taxable to the employee),

• Group health care benefits including insurance premiums (employer responsibility),

44

Actions• 4: Projecting Expenses in Comparison to Loan (continued):

• Retirement benefits paid by employer,

• Unemployment insurance paid by employer,

• Interest incurred during the Covered Period on mortgage obligations for obligations entered prior to February 15, 2020,

• Rent payments during the Covered Period on leases entered prior to February 15, 2020, and

• Utility payments related to the Covered Period (defined as electricity, gas, water, transportation, telephone, or internet access for services which began before February 15, 2020).

45

Actions• STEP 5: Comparison of Projection Against Loan Proceeds

• The healthcare provider should compare the projection against the loan proceeds to initially determine any shortfall which could reduce the loan forgiveness, prior to application of the limitations on forgiveness related to FTE reduction or specific employee compensation reductions that occurred. Additionally, non-payroll cost items should be reviewed to determine if such expenses would exceed 25% of the total qualifying expenses incurred. Non-payroll related items are qualifying interest, rent, and utility payments.

• STEP 6: Identification of Additional Expenses Qualifying

• Many providers have established or are considering providing additional employee compensation during the COVID-19 PHE in the form of a bonus or an increase in compensation. Such an increase in compensation or bonus during the Covered Period would qualify for consideration in the determination of loan forgiveness.

46

Actions• STEP 7: Accumulating Information to Support Forgiveness

• All loan recipients should be accumulating the following information in preparation for the forgiveness request:

• Payroll summaries, by employee for all the aforementioned payroll periods, including FTE computations,

• Payroll tax filings covering all the aforementioned payroll periods and the Covered Period,

• Cancelled checks for all items to be claimed, and

• Other documents supporting the items to be claimed.

47

Forgiveness Application Released• May 15, 2020, the SBA released the PPP loan forgiveness application (the “Application”). The

Application should be completed by borrowers and submitted to their lenders. The Application sets forth all of the documentation required to verify expenses for purposes of the forgiveness calculation. The Application also clarifies a few points regarding forgiveness, including:

• For administrative convenience, borrowers with biweekly payroll may elect to calculate eligible payroll costs using the 8 week period that begins on the first day of their first pay period following disbursement of the loan;

• Mortgage obligations include payments of interest on real or personal property, but the obligation must have been in place prior to February 15, 2020;

• Owner-employee or self-employed individual/general partners must not exceed eight weeks’ worth of 2019 compensation during the 8 week period;

48

Forgiveness Application Released (cont.)• Non-cash compensation payroll costs are limited to employer contributions for

employee health insurance and employee retirement plans, and employer state and local taxes assessed on employee compensation;

• Full time equivalents (“FTEs”) are considered on a 40 hour per week basis;

• For the salary reduction calculation, borrowers must compare the average annual salary or hourly wage from January 1, 2020 to March 31, 2020 to the average annual salary or hourly wage during the 8 week period, and a specific calculation is provided for hourly workers; and

• For the headcount reduction calculation rehire safe harbor, FTEs are counted as of June 30, 2020.

49

Interaction With Provider Relief Funds• Track all COVID-19 PHE expenses in the accounting records of the hospice.

Categorization of COVID-19 PHE expenses should be sufficient for cost reporting, tax, as well as HHS reporting.

• Segregate PPP loan forgiveness (two separate income accounts) between:• COVID-19 PHE expenses (principally salaries and benefits)

• Other loan forgiveness

• This allows providers to track all COVID-19 PHE expenses while not charging those expenses in HHS reporting that were paid via PPP loan forgiveness.

50

Next• Legislative changes, SBA issued guidance, bank issued guidance.

• AICPA has released recommendations. https://www.journalofaccountancy.com/news/2020/apr/ppp-loan-forgiveness-aicpa-recommendations-coronavirus-relief.html.

• Additional interpretations.

• Review bank submission for forgiveness closely

• Costs included for forgiveness can not be charged as a use of Provider Relief Funding

• Any loan funds not forgiven represent a low-interest loan, which may be liquidated immediately if desired.

• https://www.sba.gov/funding-programs/loans/coronavirus-relief-options/paycheck-protection-program

• Forgiveness Application at https://home.treasury.gov/system/files/136/3245-0407-SBA-Form-3508-PPP-Forgiveness-Application.pdf.

51

William T. Cuppett, CPA

Director

304.241.1261

www.healthgroup.comwww.ggmcpa.net

Accelerated PaymentsM. Aaron Little, CPA

BKD

53

Accelerated & AdvancePayment Program

Program intended to provide expedited payment when there is a disruption in claims submission &/or processing

Program was expanded during PHE due to passage of the CARES Act

One of the first & most immediately accessible funding option made available during the PHE

Payment was made available upon submission of request to MAC

Hospices were allowed an advanced payment of up to three months of Medicare payments

Over 17,000 payment requests were approved by CMS in first week resulting in $34 billion released to providers

54

Accelerated & AdvancePayment Program

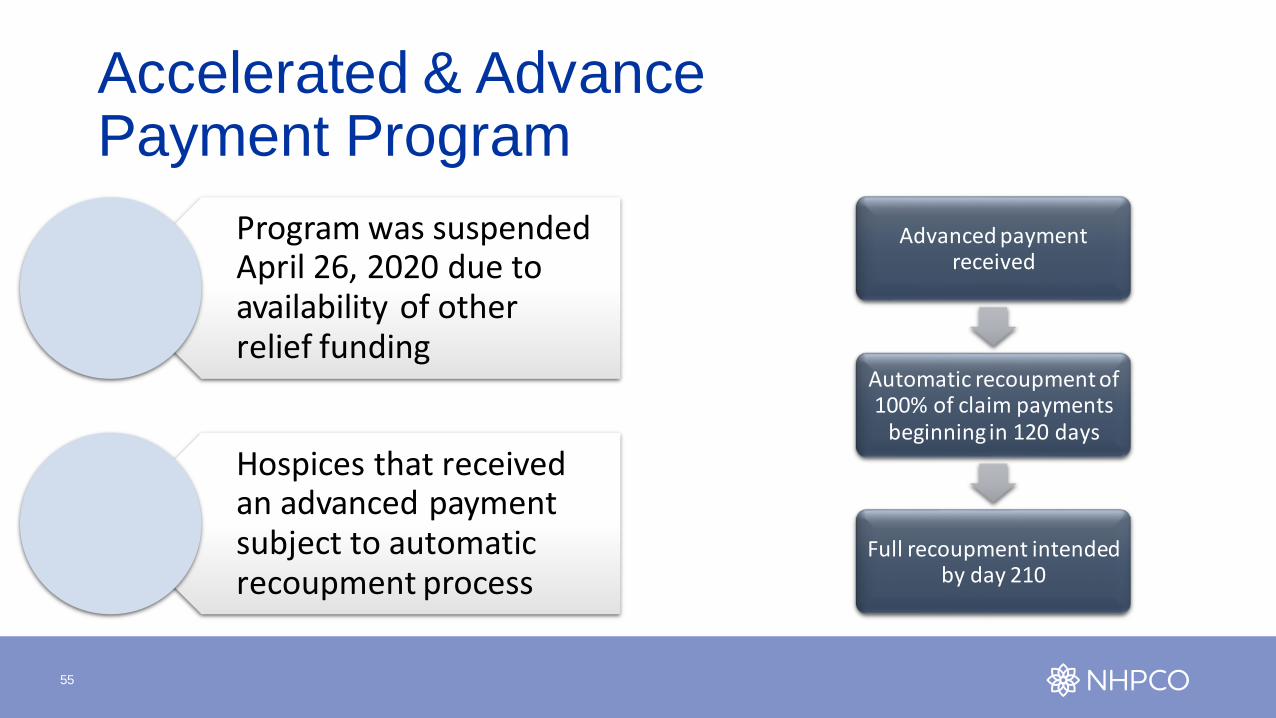

Program was suspended April 26, 2020 due to availability of other relief funding

Hospices that received an advanced payment subject to automatic recoupment process

Advanced payment received

Automatic recoupment of 100% of claim payments

beginning in 120 days

Full recoupment intended by day 210

55

Accelerated & AdvancePayment Program

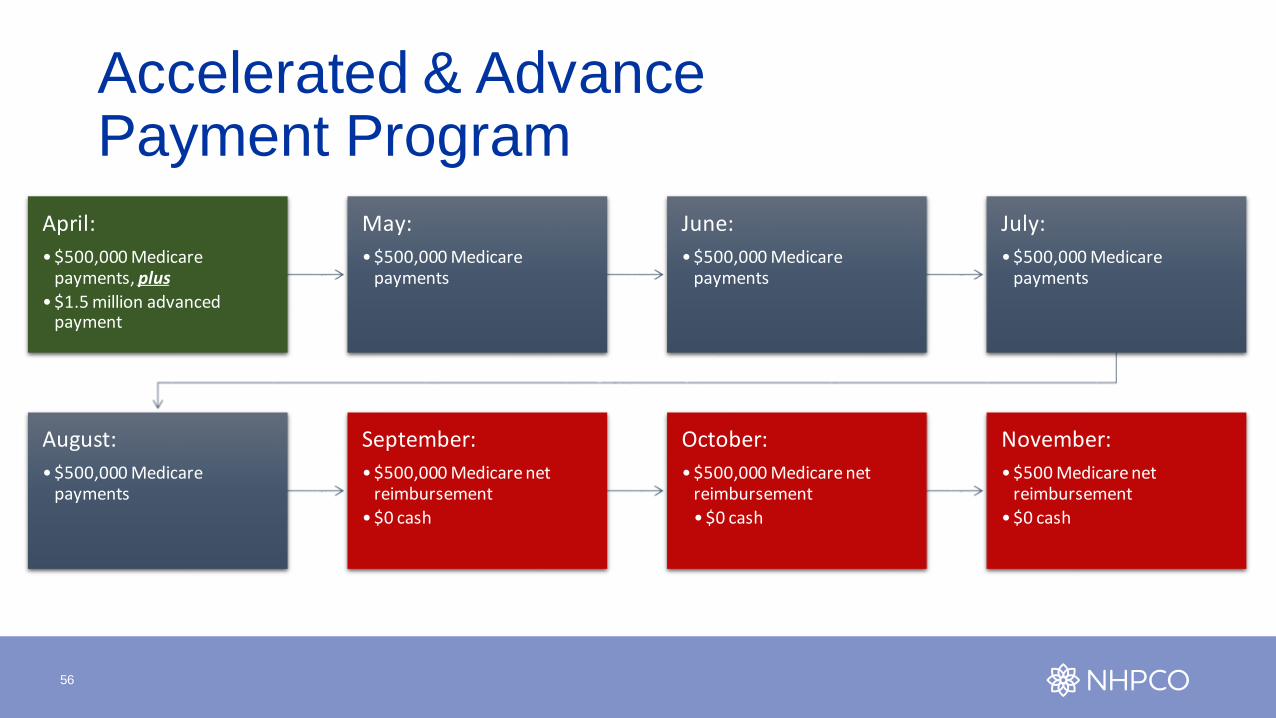

April:

• $500,000 Medicare payments, plus

• $1.5 million advanced payment

May:

• $500,000 Medicare payments

June:

• $500,000 Medicare payments

July:

• $500,000 Medicare payments

August:

• $500,000 Medicare payments

September:

• $500,000 Medicare net reimbursement

• $0 cash

October:

• $500,000 Medicare net reimbursement

• $0 cash

November:

• $500 Medicare net reimbursement

• $0 cash

56

Acronyms• CARES Act Coronavirus Aide, Relief,

& Economic Security Act

• CMS Centers for Medicare & Medicaid Services

• MAC Medicare Administrative Contractor

• PHE Public health emergency

57

Preparation for Reporting

59

Overview

Hospices need to be diligent and thorough in evaluating and tracking additional expenses and lost revenues related to COVID-19

Hospices are incurring additional costs each day responding to the changing regulatory and care environment

Clearly document and identify all “activities” that substantiate the need for COVID-19 funding to sustain operations

60

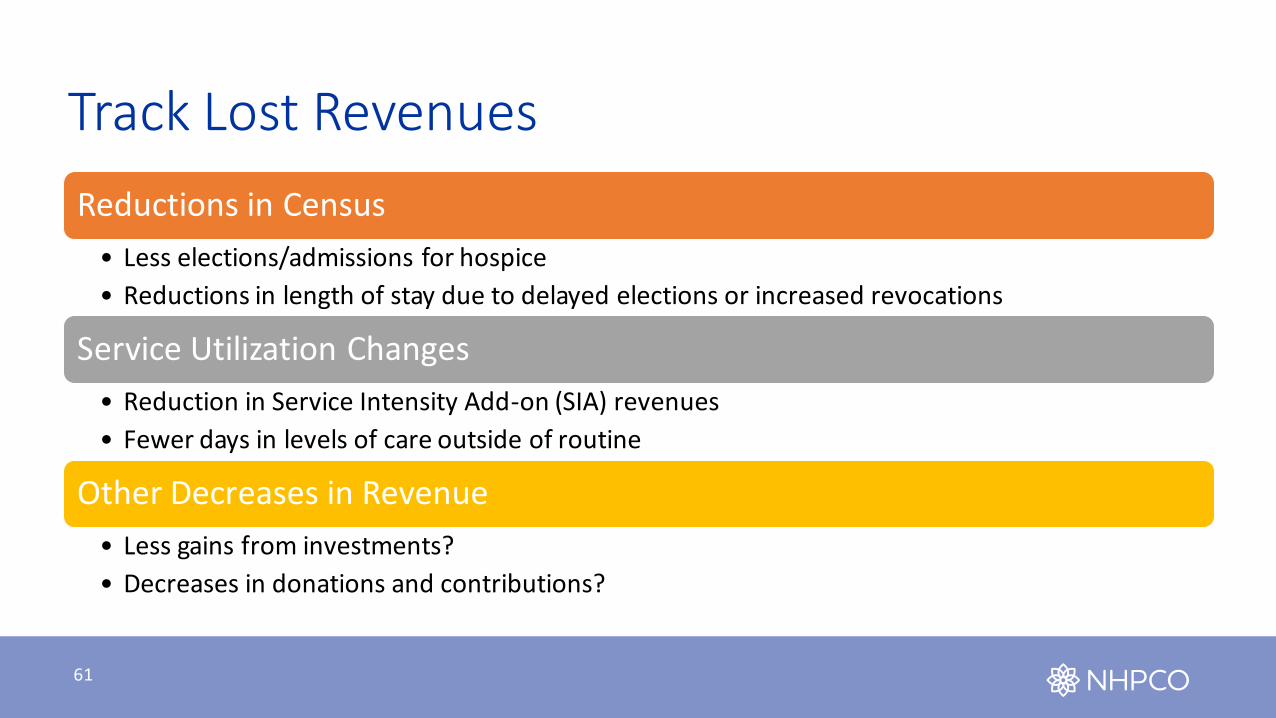

Track Lost Revenues

Reductions in Census

• Less elections/admissions for hospice

• Reductions in length of stay due to delayed elections or increased revocations

Service Utilization Changes

• Reduction in Service Intensity Add-on (SIA) revenues

• Fewer days in levels of care outside of routine

Other Decreases in Revenue

• Less gains from investments?

• Decreases in donations and contributions?

61

Track Labor and Non-Labor CostCurrently there is no guidance on the details of tracking expenditures. Therefore, we currently are relying on the OMB Uniform Guidance for these funds:

• Create separate bank accounts for COVID related funds

• Record the various funding sources in separate general ledger accounts

• Set up COVID related costs in a different general ledger account within its department

• Create a separate report that tracks all the funds

62

Administration Considerations

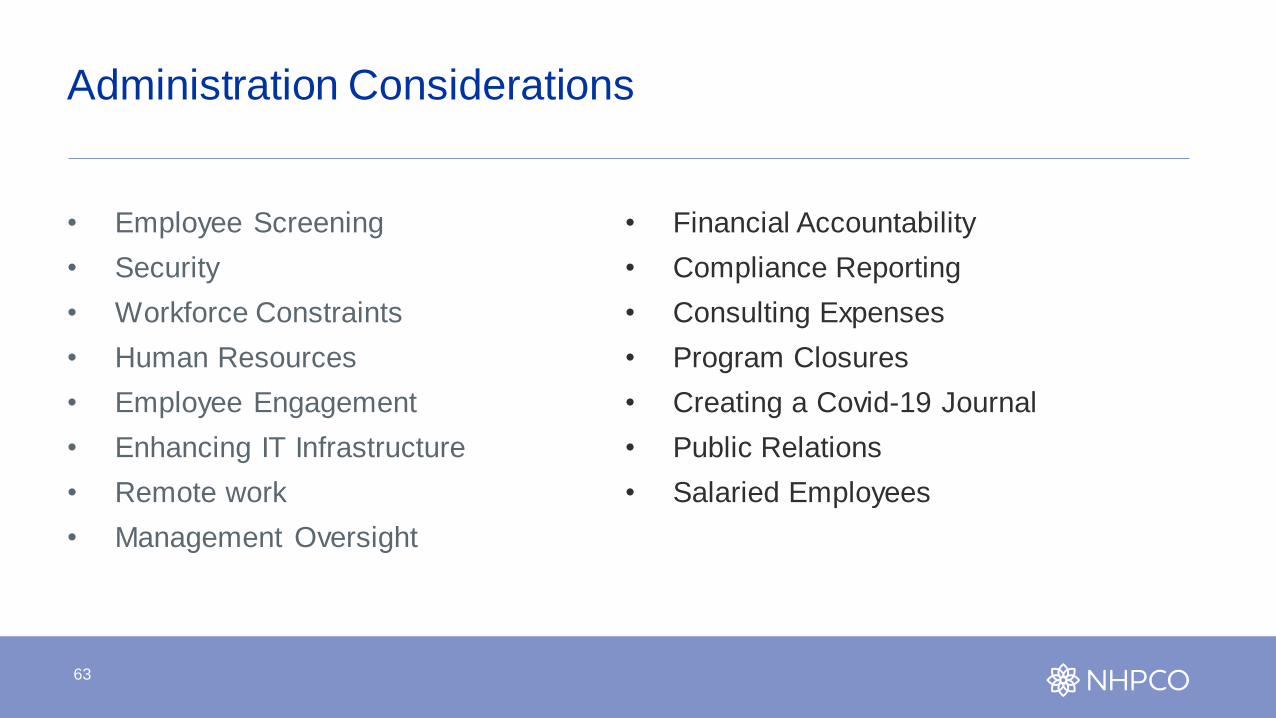

• Employee Screening

• Security

• Workforce Constraints

• Human Resources

• Employee Engagement

• Enhancing IT Infrastructure

• Remote work

• Management Oversight

• Financial Accountability

• Compliance Reporting

• Consulting Expenses

• Program Closures

• Creating a Covid-19 Journal

• Public Relations

• Salaried Employees

63

Nursing Considerations

• Infection Control Procedures• PPE Utilization• Nursing Documentation• HIS Redeployment• Nursing Equipment

• Patient Monitoring• Patient and Family Screening• Patient and Family Isolation• Telehealth

64

Inpatient Considerations

Dietary Department• Non-communal dining• Employee meals• Isolation meals

Activities Department• Family activities• Family and resident communication

General Services• Housekeeping Costs• Waste Services• Room Changes• Central Supply

65

Which Funds Get Obligated First• PPP Loan – Forgiven amount of salaries cannot be included

• HHS grant funds – Allowable expenses and lost revenues• Follow Terms and Conditions description

• Future funding could be more restricted• May only allow funds to be used for COVID expenses, not lost revenues

66

Overall Considerations• All organizations must provide an accurate accounting of all additional

resources received from various programs

• Organizations must accurately demonstrate that no additional expense or lost revenue was reimbursed more than once

• With many organizations expending additional resources at an extraordinary rate, proper accounting now is the key to avoid paying back funds later

• Understand accounting treatment in financial statements – IRS, GAAP and cost reporting

• Pay attention to all the updates!

67

NHPCO Government Funding Series• Webinar #3 – Update on Reporting Requirements

• June – Date TBD

68

69