DATA EXCELLENCE - Madura Microfinance

107

DATA EXCELLENCE FOR INTELLIGENT, VALUE DRIVEN GROWTH Annual Report 2014-15

Transcript of DATA EXCELLENCE - Madura Microfinance

DATA EXCELLENCEFOR INTELLIGENT,

VALUE DRIVEN GROWTH

Annual Report 2014-15

Targeted delivery of productive capital to enable greater

impact at lower cost and lower risk.

Value Lending

SCITYL

AN

A

UCT D INO NR OP VATION

ROG WTH

DATA

EXCELLENCE

SCITYL

AN

A

UCT D INO NR OP VATION

ROG WTH

DATA

EXCELLENCE

Powering our mission through

Mission

10101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010101010

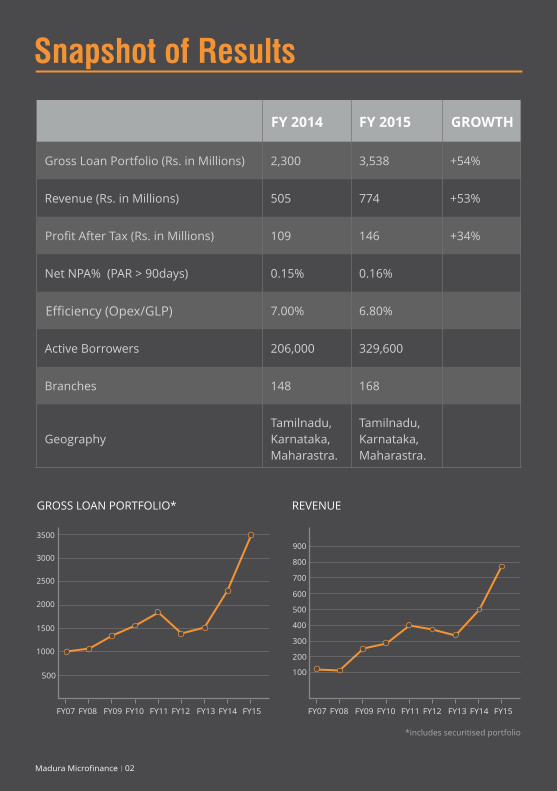

Snapshot of Results

Company

Letter from Chairman

Process Excellence

Product Innovation

Geographic Expansion

02

03

04

06

08

12

Data Excellence 10

Madura Microeducation 14

Auditor’s Report

Annexure (I,II,III,IV)

Balance Sheet

Cash Flow

25

41

42

43

Notes 44

Balance Sheet 65

Notes

66

67

MADURA MICRO FINANCE (STANDALONE)

MADURA MICRO EDUCATION

Director’s Report

22

16

MADURA MICRO FINANCE (CONSOLIDATED)

Auditor’s Report 74

Balance Sheet

Cash Flow

79

80

81

Notes 82

Contents

06

15

Process Excellence

Madura Microeducation

Data Excellence

10

09

Product Innovation

01Madura Microfinance

Gross Loan Portfolio (Rs. in Millions) 2,300 3,538 +54%

Revenue (Rs. in Millions) 505 774 +53%

109 146 +34%

Net NPA% (PAR > 90days) 0.15% 0.16%

7.00% 6.80%

Active Borrowers 206,000 329,600

Branches 148 168

Geography

Tamilnadu,

Karnataka,

Maharastra.

Tamilnadu,

Karnataka,

Maharastra.

GROWTH

500

1000

1500

2000

GROSS LOAN PORTFOLIO* REVENUE

*includes securitised portfolio

FY 2014 FY 2015

100

400

500

800

3500

900

02

3000

2500

200

300

600

700

Madura Microfinance

Profit After Tax (Rs. in Millions)

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Efficiency (Opex/GLP)

Snapshot of Results

Dr. Tara Thiagarajan

Mr. Ashok Mirza

Mr. R. Ramaraj

Mr. N.C. Sarabeswaran

Mr. Rahul Varma

Mr. Sandeep Farias

Mr. Mohan Eddy

(Chairman and Managing Director)

(Wholetime Director)

Mr. M. Narayanan

Company Secretary

Mr. Sanin Panicker

Madura Microfinance Ltd.,nd36, 2 Main Road,

Kasturba Nagar, Adyar,

Chennai - 600 020.

S.N.S. AssociatesthNo.2, 11 Cross street,

Indira Nagar, Chennai - 600020.

Auditors

Bankers/Financial Institutions

DIRECTORS

Chief Executive Officer

Company

03Madura Microfinance

Axis Bank | City Union Bank | Development Credit Bank | Dhanalakshmi Bank |

Industrial Development Bank of India | South Indian Bank | Canara Bank |

Small Industrial Development Bank of India | Lakshmi Vilas Bank | ING Vysys Bank |

Mas Financial services limited | Reliance Capital Limited | Dena Bank | Indian Bank |

Indusind Bank | ADFT | Maanaveeya Development and Finance (P) Ltd |

Andhra Bank | Bank of Baroda | Bank of Maharashtra | IFMR Capital Finance Private

Limited | Ratnakar Bank Limited | Reliance Home Finance | Tata Capital Financial

Services Limited | Vijaya Bank | Habitat Micro Build India Housing Finance Co. Pvt. Ltd.

ChairmanLetter from

Dear Members,

Madura Microfinance

80

04

Tara ThiagarajanChairman and Managing Director

05Madura Microfinance

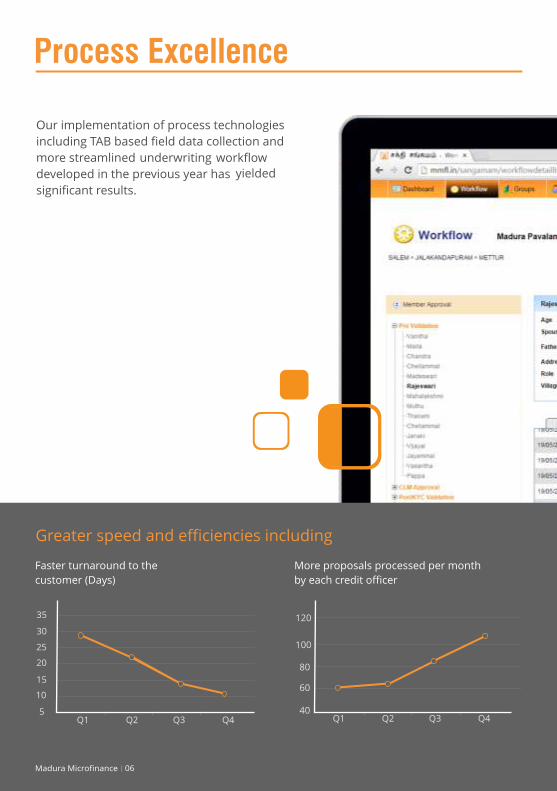

Process Excellence

Madura Microfinance 06

Faster turnaround to the

customer (Days)

More proposals processed per month

by each credit officer

40

60

80

100

120

450

500

550

600

650

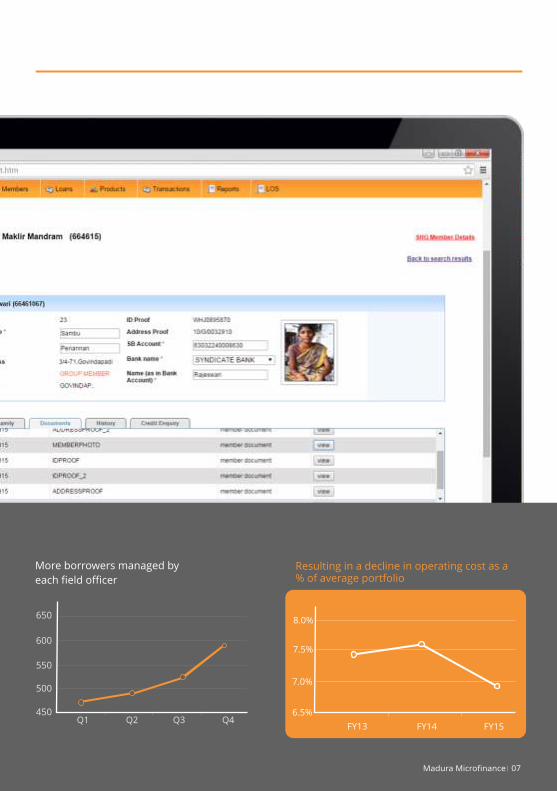

07Madura Microfinance

More borrowers managed by

each field officer

Target Market ~13 Mn

retailers with an

estimated credit need

of INR 300 Bn

Sourcing of new

customers through

distributor’s

retail network

Credit delivery and

collection through

distributors

Unique model that utilizes existing supply chains

Madura Microfinance 08

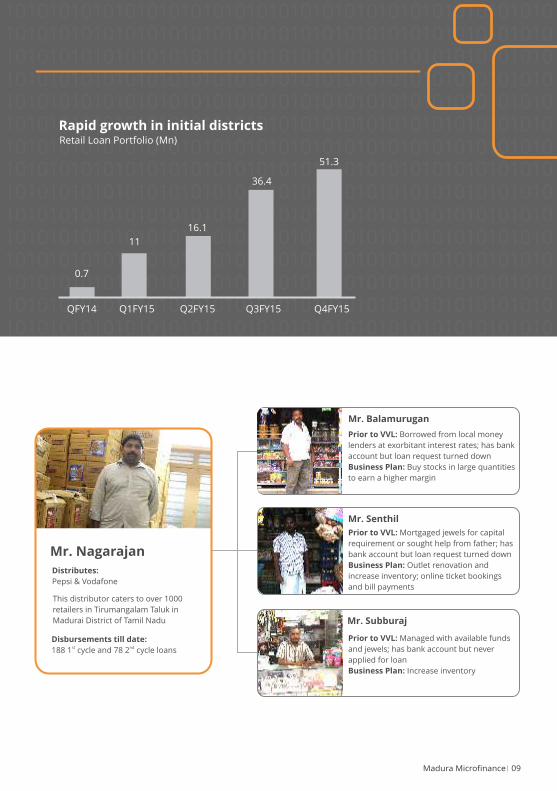

This year our Retail Microcapital product has gone from pilot to roll out

as an independent business unit

With strong results in the pilot regions and teams in place in 15 regions

in Tamil Nadu and Karnataka, it is now poised for rapid growth

Retail Micro Capital

Product Innovation

QFY14 Q1FY15 Q2FY15 Q3FY15 Q4FY15

Rapid growth in initial districtsRetail Loan Portfolio (Mn)

0.7

11

16.1

36.4

51.3

Disbursements till date: st nd

188 1 cycle and 78 2 cycle loans

Distributes:

Pepsi & Vodafone

Mr. Senthil

Mr. Subburaj

Mr. Nagarajan

Prior to VVL: Borrowed from local money

lenders at exorbitant interest rates; has bank

account but loan request turned down

Business Plan: Buy stocks in large quantities

to earn a higher margin

Mr. Balamurugan

Prior to VVL: Mortgaged jewels for capital

requirement or sought help from father; has

bank account but loan request turned down

Business Plan: Outlet renovation and

increase inventory; online ticket bookings

and bill payments

Prior to VVL: Managed with available funds

and jewels; has bank account but never

applied for loan

Business Plan: Increase inventory

This distributor caters to over 1000

retailers in Tirumangalam Taluk in

Madurai District of Tamil Nadu

09Madura Microfinance

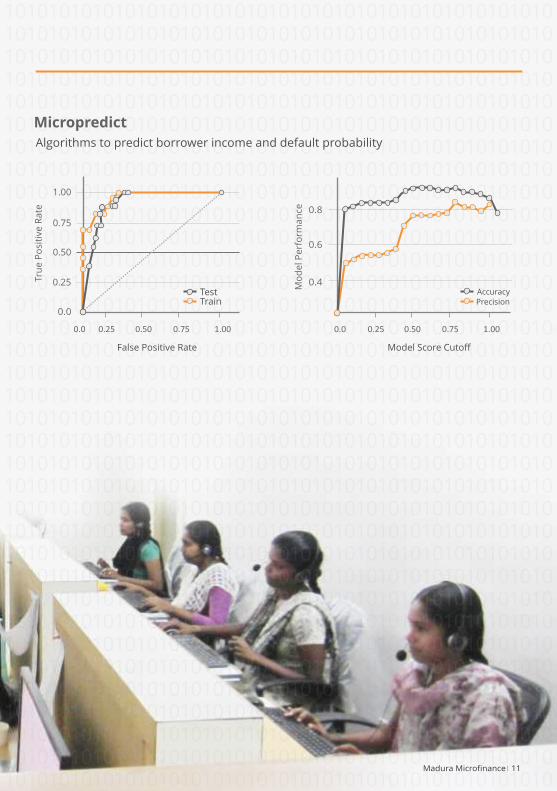

Data Excellence

Madura Microfinance 10

11Madura Microfinance

TestTrain

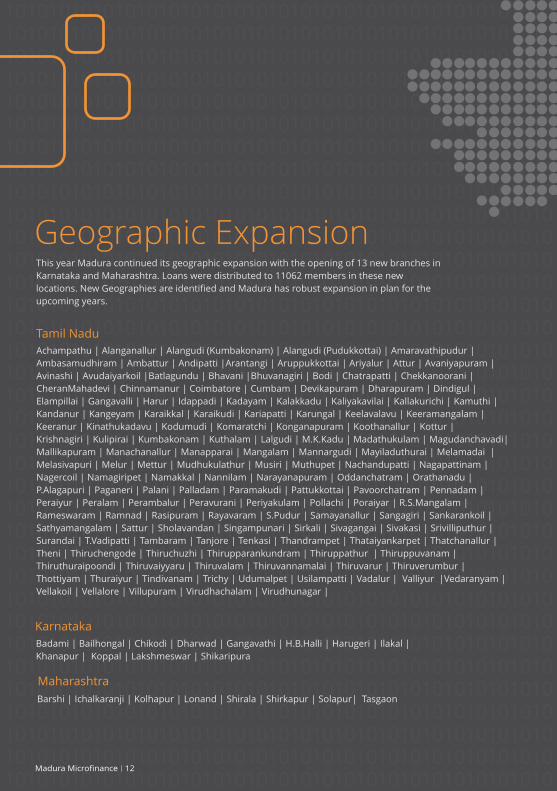

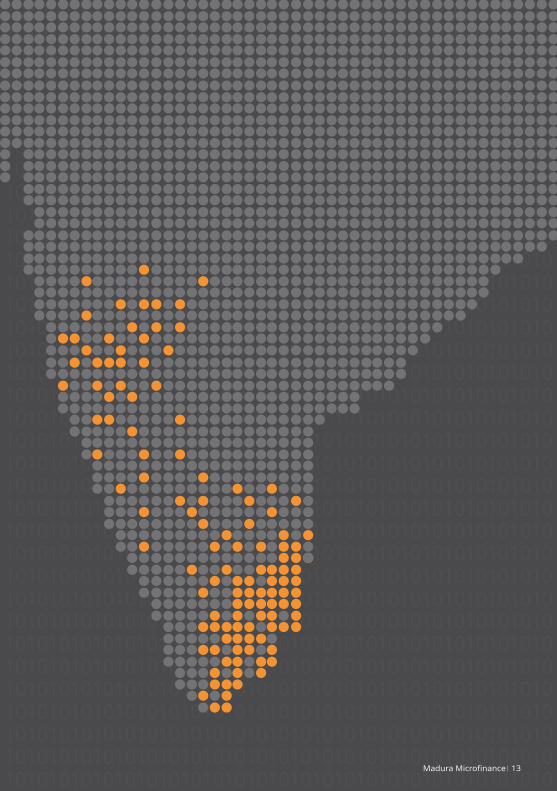

Geographic Expansion

Tamil Nadu

Karnataka

Badami | Bailhongal | Chikodi | Dharwad | Gangavathi | H.B.Halli | Harugeri | Ilakal |

Khanapur | Koppal | Lakshmeswar | Shikaripura

Maharashtra

Barshi | Ichalkaranji | Kolhapur | Lonand | Shirala | Shirkapur | Solapur| Tasgaon

Achampathu | Alanganallur | Alangudi (Kumbakonam) | Alangudi (Pudukkottai) | Amaravathipudur |

Ambasamudhiram | Ambattur | Andipatti |Arantangi | Aruppukkottai | Ariyalur | Attur | Avaniyapuram |

Avinashi | Avudaiyarkoil |Batlagundu | Bhavani |Bhuvanagiri | Bodi | Chatrapatti | Chekkanoorani |

CheranMahadevi | Chinnamanur | Coimbatore | Cumbam | Devikapuram | Dharapuram | Dindigul |

Elampillai | Gangavalli | Harur | Idappadi | Kadayam | Kalakkadu | Kaliyakavilai | Kallakurichi | Kamuthi |

Kandanur | Kangeyam | Karaikkal | Karaikudi | Kariapatti | Karungal | Keelavalavu | Keeramangalam |

Keeranur | Kinathukadavu | Kodumudi | Komaratchi | Konganapuram | Koothanallur | Kottur |

Krishnagiri | Kulipirai | Kumbakonam | Kuthalam | Lalgudi | M.K.Kadu | Madathukulam | Magudanchavadi|

Mallikapuram | Manachanallur | Manapparai | Mangalam | Mannargudi | Mayiladuthurai | Melamadai |

Melasivapuri | Melur | Mettur | Mudhukulathur | Musiri | Muthupet | Nachandupatti | Nagapattinam |

Nagercoil | Namagiripet | Namakkal | Nannilam | Narayanapuram | Oddanchatram | Orathanadu |

P.Alagapuri | Paganeri | Palani | Palladam | Paramakudi | Pattukkottai | Pavoorchatram | Pennadam |

Peraiyur | Peralam | Perambalur | Peravurani | Periyakulam | Pollachi | Poraiyar | R.S.Mangalam |

Rameswaram | Ramnad | Rasipuram | Rayavaram | S.Pudur | Samayanallur | Sangagiri | Sankarankoil |

Sathyamangalam | Sattur | Sholavandan | Singampunari | Sirkali | Sivagangai | Sivakasi | Srivilliputhur |

Surandai | T.Vadipatti | Tambaram | Tanjore | Tenkasi | Thandrampet | Thataiyankarpet | Thatchanallur |

Theni | Thiruchengode | Thiruchuzhi | Thirupparankundram | Thiruppathur | Thiruppuvanam |

Thiruthuraipoondi | Thiruvaiyyaru | Thiruvalam | Thiruvannamalai | Thiruvarur | Thiruverumbur |

Thottiyam | Thuraiyur | Tindivanam | Trichy | Udumalpet | Usilampatti | Vadalur | Valliyur |Vedaranyam |

Vellakoil | Vellalore | Villupuram | Virudhachalam | Virudhunagar |

Madura Microfinance 12

This year Madura continued its geographic expansion with the opening of 13 new branches in

Karnataka and Maharashtra. Loans were distributed to 11062 members in these new

locations. New Geographies are identified and Madura has robust expansion in plan for the

upcoming years.

13Madura Microfinance

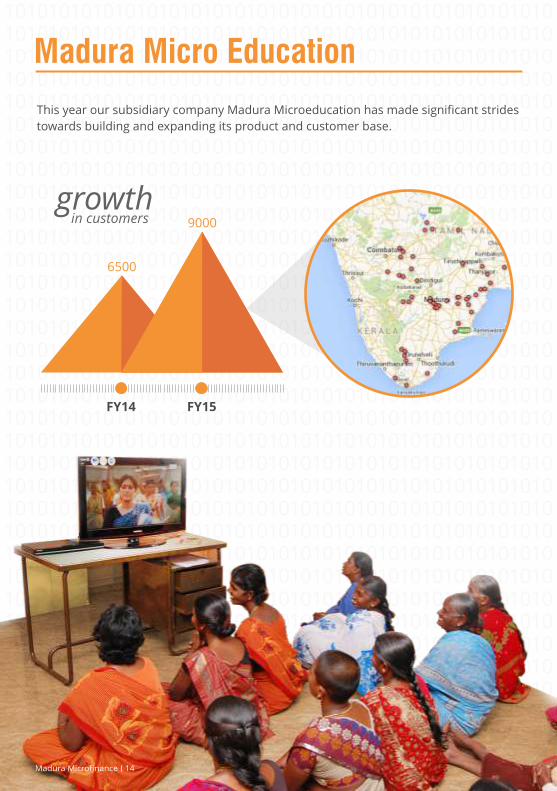

FY15FY14

in customersgrowth

6500

9000

Madura Micro Education

Madura Microfinance 14

20%

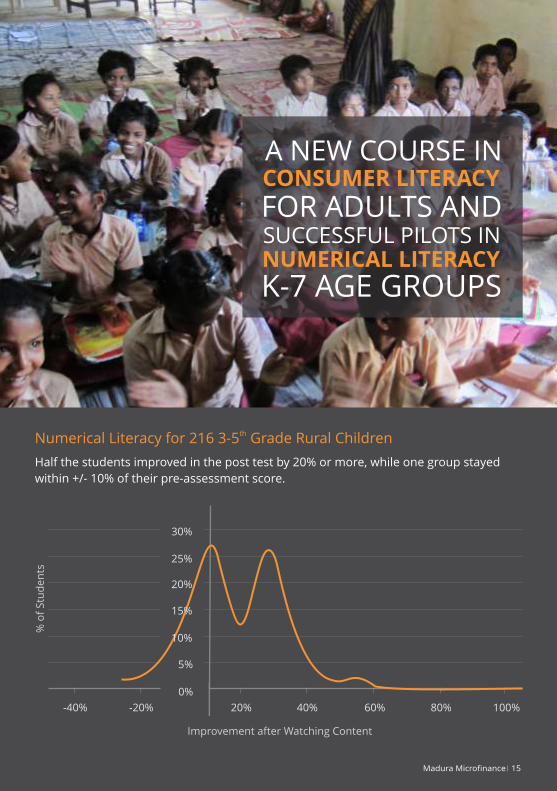

thNumerical Literacy for 216 3-5 Grade Rural Children

5%

30%

0%

40% 60% 80% 100%-40% -20%

Improvement after Watching Content

Half the students improved in the post test by 20% or more, while one group stayed

within +/- 10% of their pre-assessment score.

10%

15%

25%

% o

f S

tud

en

ts

20%

A NEW COURSE INCONSUMER LITERACY

FOR ADULTS AND SUCCESSFUL PILOTS INNUMERICAL LITERACY

K-7 AGE GROUPS

15Madura Microfinance

Director’s Report

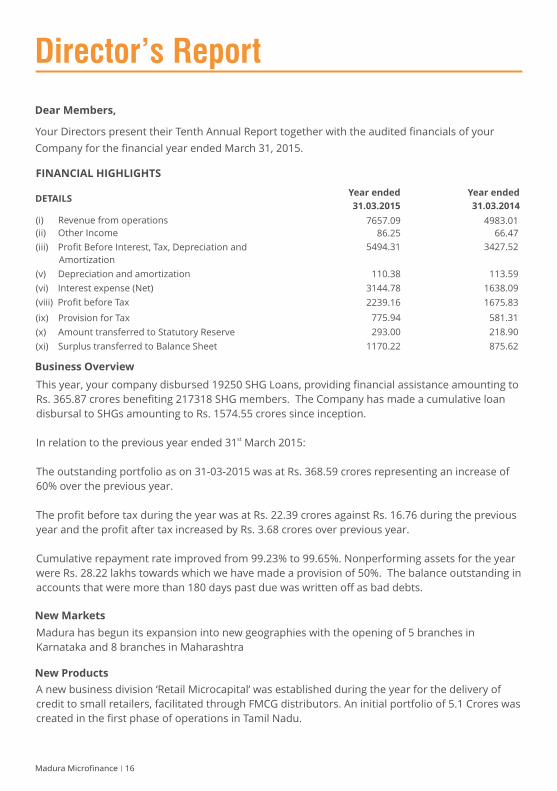

Dear Members,

Your Directors present their Tenth Annual Report together with the audited financials of your

C o mpany for the financial year ended March 31, 2015.

FINANCIAL HIGHLIGHTS

(i) Revenue from operations

(ii) Other Income

(iii) Profit Before Interest, Tax, Depreciation and

Amortization

(v) Depreciation and amortization

(vi) Interest expense (Net)

(viii) Profit before Tax

(ix) Provision for Tax

(x) Amount transferred to Statutory Reserve

(xi) Surplus transferred to Balance Sheet

DETAILSYear ended Year ended

31.03.2015 31.03.2014

Business Overview

This year, your company disbursed 19250 SHG Loans, providing financial assistance amounting to

Rs. 365.87 crores benefiting 217318 SHG members. The Company has made a cumulative loan

disbursal to SHGs amounting to Rs. 1574.55 crores since inception.

stIn relation to the previous year ended 31 March 2015:

The outstanding portfolio as on 31-03-2015 was at Rs. 368.59 crores representing an increase of

60% over the previous year.

The profit before tax during the year was at Rs. 22.39 crores against Rs. 16.76 during the previous

year and the profit after tax increased by Rs. 3.68 crores over previous year.

Cumulative repayment rate improved from 99.23% to 99.65%. Nonperforming assets for the year

were Rs. 28.22 lakhs towards which we have made a provision of 50%. The balance outstanding in

accounts that were more than 180 days past due was written off as bad debts.

New Markets

Madura has begun its expansion into new geographies with the opening of 5 branches in

Karnataka and 8 branches in Maharashtra

New Products

A new business division ‘Retail Microcapital’ was established during the year for the delivery of

credit to small retailers, facilitated through FMCG distributors. An initial portfolio of 5.1 Crores was

created in the first phase of operations in Tamil Nadu.

Madura Microfinance 16

7657.09

86.25

5494.31

110.38

3144.78

2239.16

775.94

293.00

1170.22

4983.01

66.47

3427.52

113.59

1638.09

1675.83

581.31

218.90

875.62

Subsidiary:

The company’s subsidiary Madura Micro Education Private Ltd provided skill development training

course to 9073 students during the year. The revenue from operations increased to 45.36 lakhs in

the current year as compared to 23.24 lakhs in the previous year.

During the year under review, the Company reported loss of Rs. 68.21 lakhs as compared to the

loss of Rs. 43.29 lakhs in the previous year.

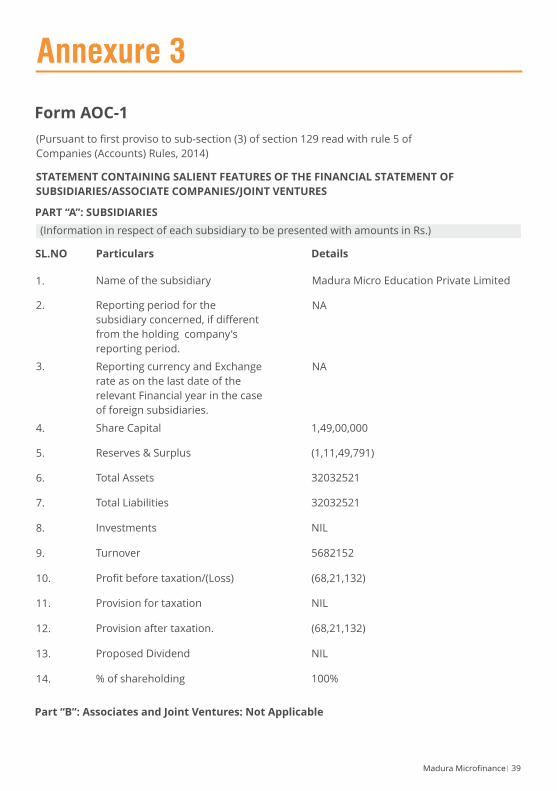

The detail of the subsidiary in Form AOC 1 is attached as Annexure 3.

Events Subsequent to the date of Financial Statements:

No material changes and commitments have occurred affecting the financial position of the

Company after March 31, 2015 till the date of this report.

Dividend:

In order to conserve resources for operations and future growth, your Directors do not

recommend any dividend for the year under review.

Transfer to Reserves:

As required under Section 45-IC of the Reserve Bank of India Act, 1934, an amount equivalent to

20 % of the profit after tax of Rs. 2.93 Crores has been transferred to the Statutory Reserve

Account.

Directors:

Presently, the Board of Directors comprise of seven Directors. There has been no change in the

constitution of the Board during the year.

Declaration by Independent Directors:

All the Independent Directors have submitted their declaration of independence as required

under Section 149(7) of the Companies Act, 2013.

Deposits:

Your Company has not accepted any deposits within the meaning of Section 73 of the Companies

Act, 2013 read with the Companies (Acceptance of Deposits) Rules, 2014.

Order of Court:

There are no significant material orders passed by the Regulators or Courts or Tribunals impacting

the going concern status and company's operations in future.

Directors’ responsibility statement:

Your Directors state:

I) That in the preparation of the annual accounts, the applicable accounting standards had been

followed along with proper explanation relating to material departures;

Director’s Report

17Madura Microfinance

(ii) That they had selected such accounting policies and applied them consistently and made

judgments and estimates that are reasonable and prudent so as to give a true and fair view of

the state of affairs of the Company at the end of the financial year and of the profit or loss of

the Company for that period;

(iii) That they had taken proper and sufficient care was taken for the maintenance of adequate

accounting records in accordance with the provisions of the Companies Act, 2013, for

safeguarding the assets of the Company and for preventing and detecting fraud and other

irregularities;

(iv) That they had prepared the annual accounts on a going concern basis.

(v) That they had devised proper systems to ensure compliance with the provisions of all

applicable laws and that such systems were adequate and operating effectively.

Corporate Governance

Development and Implementation of Risk Management Policy

Adequacy of Internal Financial Controls with reference to the Financial Statements

Board Meetings

Your Company has been complying with the principles of good Corporate Governance over the

years and is committed to the highest standards of compliance.

Company has developed and implemented a risk management policy, upon which the company

is ensuring that the activities are undertaken in a risk free environment.

The Company has implemented and evaluated the Internal Financial Controls which provide a

reasonable assurance in respect of providing financial and operational information, complying

with applicable statutes and policies, safeguarding of assets, prevention and detection of frauds,

accuracy and completeness of accounting records. The Directors and Management confirm that

the Internal Financial Controls (IFC) are adequate with respect to the operations of the Company.

Further, the Board annually reviews the effectiveness of the Company's internal control system.

Directors

Retirement by rotation

During the year, the Board of Directors of your Company met 6 times. The meetings were held on

08.04.2014, 23.06.2014, 30.09.2014, 12.12.2014, 19.02.2015 and 03.03.2015.

Mr. Ashok Mirza, Director, retires by rotation at the ensuing Annual General Meeting and being

eligible, offers himself for reappointment. Your Directors recommend his re-appointment.

Director’s Report

Madura Microfinance 18

Committee

NAME OF THE COMMITTEE MEMBERS

(I) Audit Committee

Mr. N C Sarabeswaran

Mr. Ashok Mirza

Mr. R Ramaraj

(II) Nomination & Remuneration Committee

Ms. Tara Thiagarajan

Mr. Ashok Mirza

Mr. Sandeep Farias

Mr. R Ramaraj

(III) Risk Management Committee

Mr. Sandeep Farias

Mr. N C Sarabeswaran

Mr. R Ramaraj

(IV) Asset Liability Management Committee

Mr. M Narayanan

Mr. Prakash J Paul

Mr. Ashok Kumar

(VI) IT Committee

Mr. Ashok Mirza

Mr. Mohan Eddy

Mr. R Ramaraj

(VII) Sexual Harassment CommitteeMr. N C Sarabeswaran

Mr. Ashok Mirza

Auditors

M/s S N S Associates, Chartered Accountants, Chennai, retire at the ensuing Annual General

Meeting and are eligible for reappointment. In terms of Section 139 and 141 of the Companies

Act, 2013 read with Companies (Audit and Auditors) Rules, 2014, the Board has recommended to

reappoint them to hold office from the conclusion of this Annual General Meeting until the

conclusion of the Twelfth AGM at remuneration to be fixed by the Board of Directors on the

recommendation of the Audit Committee.

Conservation of Energy, Technology Absorption and Foreign Exchange Outgo

The particulars prescribed under clause (m) of sub section (3) of Section 134 of the Companies Act,

2013 read with Rule 8 (3) of the Companies (Accounts) Rules, 2014 of the following:

Director’s Report

19Madura Microfinance

(V) Corporate Social Responsibility Committee

Ms. Tara Thiagarajan

Mr. Ashok Mirza

Mr. R Ramaraj

Mr.Rahul Varma

Particulars of Loans, Guarantees and Investments

The Company has not given any loans/guarantees and has not made any investments in securities

as covered under section 186 of the Companies Act, 2013 during the year.

Corporate Social Responsibility (CSR) Policy

Pursuant to the provisions of section 135 and Schedule VII of the Companies Act, 2013, CSR

Committee has been constituted and the said committee has recommended and the Board has

approved a policy on Corporate Social Responsibility (CSR).

For the financial year 2014-15, your Company is required to spend an amount of Rs. 19.50 lakhs.

Your Company is in the process of identifying the appropriate projects for spending the said

amount in the areas of enhancing the nutritional and education status of underprivileged rural

people.

Annual Report on CSR is attached as Annexure 1.

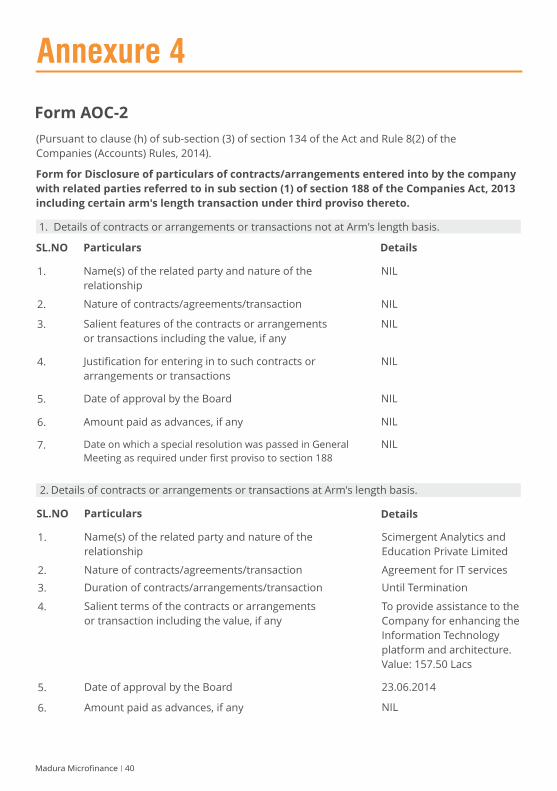

Related Party TransactionsstAll related party transactions that were entered into during the financial year ended 31 March,

2015 were on an arm's length basis and were in the ordinary course of business.

The particulars of contracts or arrangements with related parties referred to in sub section (1) of

section 188 entered by the Company during the financial year ended 31st March, 2015 is annexed

hereto as Annexure 4 in prescribed Form AOC-2 and forms part of this report.

Extract of Annual Return

As required pursuant to section 92(3) of the Companies Act, 2013 and Rule 12(1) of the Companies

(Management and Administration) Rules, 2014, an extract of Annual Return in Form MGT 9 as a

part of this Annual Report is attached as Annexure 2.

Director’s Report

Madura Microfinance 20

Conservation of Energy & Technology Absorption

In view of the nature of activities that are being carried out by the Company, the particulars

prescribed under clause (m) of sub section (3) of Section 134 of the Companies Act, 2013, read

with the Companies (Accounts) Rules 2014 on conservation of energy and technology absorption

are not applicable to the Company.

Foreign Exchange Earnings and Outgo

During the year, the Company did not have any foreign exchange earnings and had an outgo of

Rs. 9,47,577 lakhs.

Acknowledgement

Your Directors take this opportunity to thank the Reserve Bank of India, Government Departments,

Financial Institutions and Banks for their support and guidance to the Organization.

Your Directors wish to thank the Directors, Investors, Customers and Advisors for their continued

support. Your Directors also wish to place on record their appreciation of the valuable contribution

made by the employees at all levels.

Chennai For and on behalf of the Board th07 August 2015

Tara Thiagarajan

Chairman and Managing Director

Director’s Report

21Madura Microfinance

Employees' Particulars in terms of Section 134 read with Rules of the Companies Act, 2013

There were no Employees in the Company whose particulars are required to be given under

Section 197 of the Companies Act, 2013 read with Rule 5 (2) of the Companies (Appointment and

Remuneration of Managerial Personnel) Rules, 2014.

Disclosure under the Sexual Harassment of Women at Workplace (Prevention, Prohibition

and Redressal) Act, 2013

The Company has in place a Policy in line with requirements of the Sexual Harassment of Women

at Workplace (Prevention, Prohibition & Redressal) Act, 2013 that covers all employees. A Sexual

Harassment Committee has been set up to redress complaints received regarding sexual

harassment. No complaints regarding sexual harassment have been received during the financial

year.

sd/-

INDEPENDENT AUDITOR’S REPORT

TO THE MEMBERS OF MADURA MICRO FINANCE LIMITED

on the Standalone Financial Statements

Management’s Responsibility for the Standalone Financial Statements

Auditor’s Responsibility

Auditor’s Report

Madura Microfinance 22

st

Opinion

Report on Other Legal and Regulatory Requirements

)

Auditor’s Report

23Madura Microfinance

st

st

Auditor’s Report

Madura Microfinance 24

For S.N.S AssociatesCHARTERED ACCOUNTANTS

(FIRM REGISTRATION No:006297 S)S.NAGARAJAN (Partner)MEMBERSHIP No:20899

st

th

st

ANNEXURE TO THE INDEPENDENT AUDITORS’ REPORT

As required by the Companies (Auditors’ Report) Order, 2015

(“the Order”), we report that:

Annexure

25Madura Microfinance

Annexure

For S.N.S AssociatesCHARTERED ACCOUNTANTS

(FIRM REGISTRATION No:006297 S)S.NAGARAJAN (Partner)MEMBERSHIP No:20899

Madura Microfinance 26

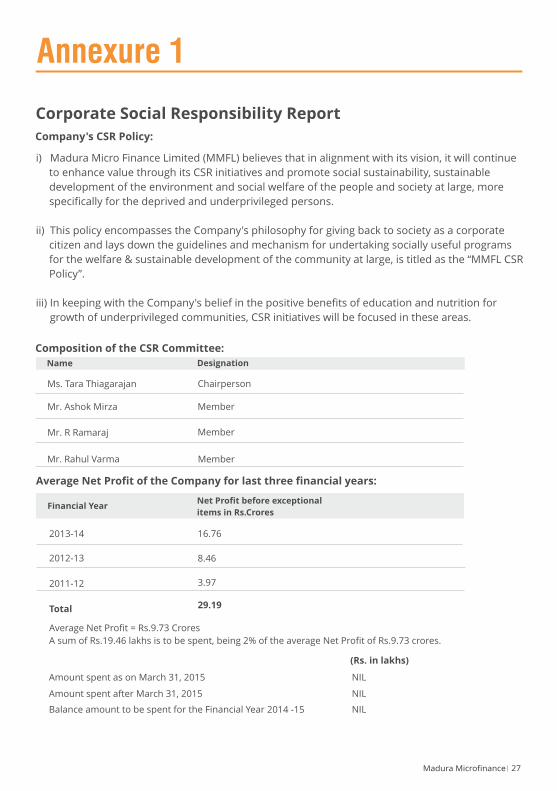

Corporate Social Responsibility Report

Company's CSR Policy:

i) Madura Micro Finance Limited (MMFL) believes that in alignment with its vision, it will continue

to enhance value through its CSR initiatives and promote social sustainability, sustainable

development of the environment and social welfare of the people and society at large, more

specifically for the deprived and underprivileged persons.

ii) This policy encompasses the Company's philosophy for giving back to society as a corporate

citizen and lays down the guidelines and mechanism for undertaking socially useful programs

for the welfare & sustainable development of the community at large, is titled as the “MMFL CSR

Policy”.

iii) In keeping with the Company's belief in the positive benefits of education and nutrition for

growth of underprivileged communities, CSR initiatives will be focused in these areas.

Composition of the CSR Committee:

Ms. Tara Thiagarajan

Mr. Ashok Mirza

Mr. R Ramaraj

Mr. Rahul Varma

Chairperson

Member

Member

Member

Average Net Profit of the Company for last three financial years:

2013-14

2012-13

2011-12

Total

16.76

8.46

3.97

29.19

Financial Year Net Profit before exceptional

items in Rs.Crores

Name Designation

Average Net Profit = Rs.9.73 Crores

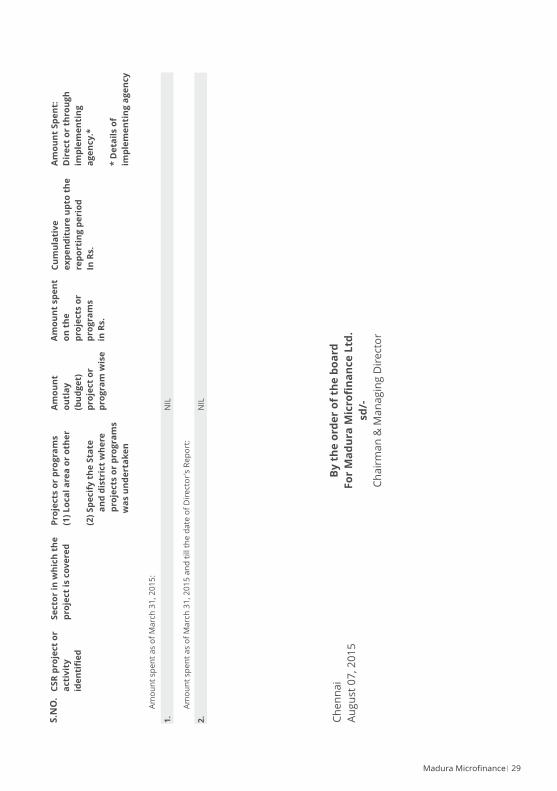

A sum of Rs.19.46 lakhs is to be spent, being 2% of the average Net Profit of Rs.9.73 crores.

Amount spent as on March 31, 2015

Amount spent after March 31, 2015

Balance amount to be spent for the Financial Year 2014 -15

(Rs. in lakhs)

Annexure 1

NIL

NIL

NIL

27Madura Microfinance

1. Reason for not spending the amount in its Board report.

The Company is in the process of identifying the appropriate projects and upon identification of

the right projects, the allocated amount will be spent.

2. Responsibility statement of the CSR Committee:

The implementation and monitoring of CSR Policy, is in compliance with CSR Objectives and

Policy of the Company.

Chairman & Managing Director

Annexure 1

Madura Microfinance 28

Whole-Time Director

sd/- sd/-

S.N

O.

CS

R p

roje

ct

or

acti

vit

y

ide

nti

fie

d

Se

cto

r in

wh

ich

th

e

pro

ject

is c

ov

ere

d

Pro

jects

or

pro

gra

ms

(1)

Lo

ca

l a

rea

or

oth

er

(2)

Sp

ecif

y t

he

Sta

te

a

nd

dis

tric

t w

he

re

p

roje

cts

or

pro

gra

ms

wa

s u

nd

ert

ak

en

Am

ou

nt

ou

tla

y

(bu

dg

et)

pro

ject

or

pro

gra

m w

ise

Am

ou

nt

spe

nt

on

th

e

pro

jects

or

pro

gra

ms

in R

s.

Cu

mu

lati

ve

ex

pe

nd

itu

re u

pto

th

e

rep

ort

ing

pe

rio

d

In R

s.

Am

ou

nt

Sp

en

t:

Dir

ect

or

thro

ug

h

imp

lem

en

tin

g

ag

en

cy

.*

* D

eta

ils

of

imp

lem

en

tin

g a

ge

ncy

Am

ou

nt

spe

nt

as

of

Ma

rch

31

, 2

01

5:

1.

NIL

Am

ou

nt

spe

nt

as

of

Ma

rch

31

, 2

01

5 a

nd

till th

e d

ate

of

Dir

ect

or'

s R

ep

ort

:

2.

NIL

Ch

en

na

i

Au

gu

st 0

7, 2

01

5

29Madura Microfinance

By

th

e o

rde

r o

f th

e b

oa

rd

Fo

r M

ad

ura

Mic

rofi

na

nce

Ltd

.

sd/-

Ch

air

ma

n &

Ma

na

gin

g D

ire

cto

r

FORM NO. MGT 9

EXTRACT OF ANNUAL RETURN

As on financial year ended on 31.03.2015

Pursuant to Section 92 (3) of the Companies Act, 2013 and

rule 12(1) of the Company (Management & Administration) Rules, 2014.

I. REGISTRATION & OTHER DETAILS

(I) CIN

(II) Registration Date

(III) Name of the Company

(IV) Category/Sub-category of the Company

(V) Address of the Registered office & contact details

(VII) Name, Address & contact details of the

Registrar & Transfer Agent, if any.

U65929TN2005PLC057390

September 2, 2005

Madura Micro Finance Limited

INDIA NON-GOVERNMENT COMPANY

36, II Main Road, Kasturiba Nagar, Adyar, Chennai 600020

(VI) Whether listed company No

NA

II. PRINCIPAL BUSINESS ACTIVITIES OF THE COMPANY

(All the business activities contributing 10 % or more of the total turnover of the company shall be stated)

S. No Name and Description of

main products / services

NIC Code of the Product/service % to total turnover of the company

1. Micro Finance 649

III. PARTICULARS OF HOLDING, SUBSIDIARY AND ASSOCIATE COMPANIES

(I) Name and address of the Company

(II) CIN / GLN

(III) Holding / Subsidiary/ Associate

(IV) % of shares held

(V) Applicable Section

Madura Micro Education Private Limited

U80301TN2013PTC091745

Subsidiary

100

2(87)

100

Annexure 2

Madura Microfinance 30

Nil

64

0,9

00

6

40

,90

0

11

.53

%N

il

64

0,9

00

6

40

,90

0

11

.53

%

CA

TE

GO

RY

OF

SH

AR

EH

OL

DE

RS

NO

. O

F

SH

AR

ES

H

EL

D A

T

TH

E

BE

GIN

NIN

G

OF

TH

E Y

EA

R [

AS

ON

31

-MA

RC

H-2

01

4]

NO

. O

F S

HA

RE

S H

EL

D A

T T

HE

EN

D O

F T

HE

YE

AR

[A

S O

N 3

1-M

AR

CH

-20

15

]

De

ma

tP

hy

sica

lTo

tal

% o

f To

tal

Sh

are

sD

em

at

Ph

ysi

ca

l

A.

PR

OM

OT

ER

S

(1)

Ind

ian

a)

Ind

ivid

ua

l/ H

UF

b)

Ce

ntr

al G

ovt

c) S

tate

Go

vt(

s)

d)

Bo

die

s C

orp

.

e)

Ba

nk

s /

FI

f) A

ny o

the

r

SU

B T

OT

AL

(A

) (1

)

(2)

Fo

reig

n

a)

NR

I In

div

idu

als

b)

Oth

er

Ind

ivid

ua

ls

c) B

od

ies

Co

rp.

d)

An

y o

the

r

SU

B T

OT

AL

(A

) (2

)

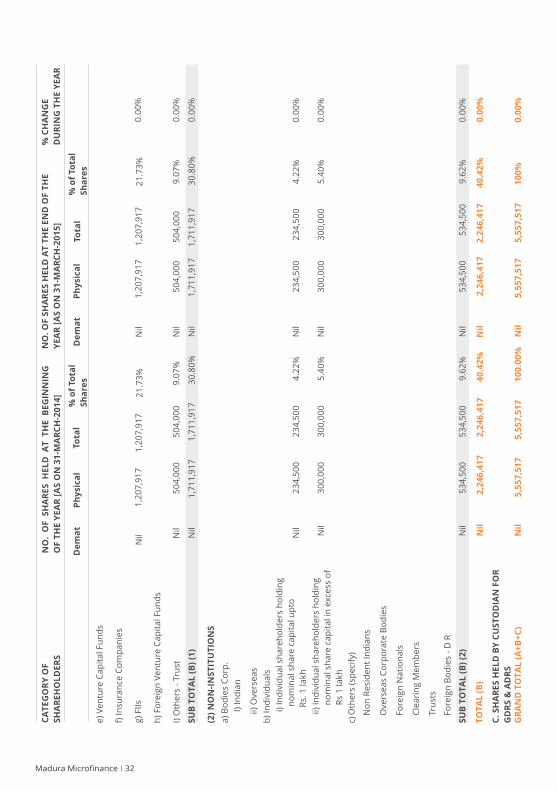

N i

l

2,6

70

,20

0

2

,67

0,2

00

4 8

.05

%

Nil

6

40

,90

0

6

40

,90

0

1

1.5

3%

Nil

2

,67

0,2

00

2,6

70

,20

0

48

.05

%

TO

TA

L (

A)

Nil

3

,31

1,1

00

3,3

11

,10

0

5

9.5

8%

Nil

3,3

11

,10

0

3

,31

1,1

00

59

.58

%

B.

PU

BL

IC S

HA

RE

HO

LD

ING

(1)

Inst

itu

tio

ns

a)

Mu

tua

l Fu

nd

s

b)

Ba

nk

s /

FI

c) C

en

tra

l G

ovt

d)

Sta

te G

ovt(

s)

(I)

CA

TE

GO

RY

-WIS

E S

HA

RE

HO

LD

ING

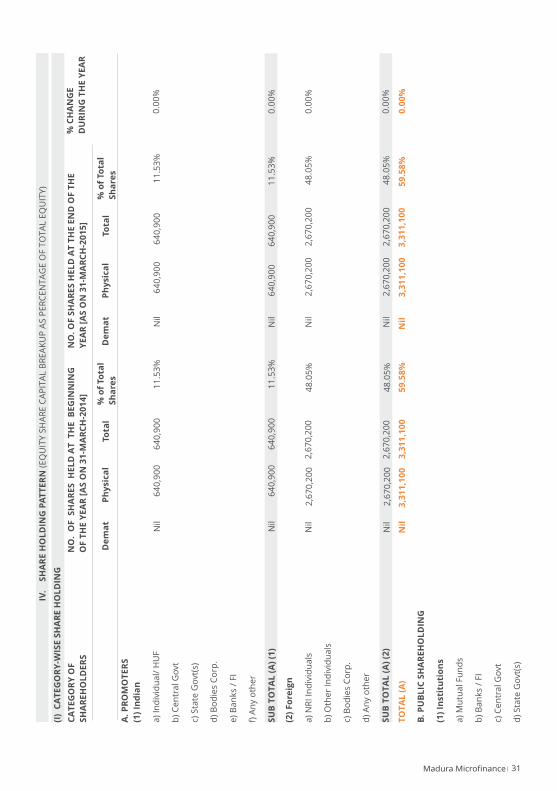

IV.

S

HA

RE

HO

LD

ING

PA

TT

ER

N (

EQ

UIT

Y S

HA

RE

CA

PIT

AL B

RE

AK

UP

AS

PE

RC

EN

TA

GE

OF T

OT

AL E

QU

ITY

)

31Madura Microfinance

Nil

64

0,9

00

6

40

,90

0

11

.53

%

N i

l

2,6

70

,20

0

2

,67

0,2

00

4 8

.05

%

N

il

2

,67

0,2

00

2,6

70

,20

0

48

.05

%

To

tal

% o

f To

tal

Sh

are

s

% C

HA

NG

E

DU

RIN

G T

HE

YE

AR

0.0

0%

0.0

0%

0.0

0%

0.0

0%

0.0

0%

CA

TE

GO

RY

OF

SH

AR

EH

OL

DE

RS

NO

. O

F

SH

AR

ES

H

EL

D

AT

T

HE

B

EG

INN

ING

OF

TH

E Y

EA

R [

AS

ON

31

-MA

RC

H-2

01

4]

NO

. O

F S

HA

RE

S H

EL

D A

T T

HE

EN

D O

F T

HE

YE

AR

[A

S O

N 3

1-M

AR

CH

-20

15

]

% C

HA

NG

E

DU

RIN

G T

HE

YE

AR

De

ma

tP

hy

sica

lTo

tal

% o

f To

tal

Sh

are

sD

em

at

Ph

ysi

ca

lTo

tal

% o

f To

tal

Sh

are

s

g)

FII

s

h)

Fo

reig

n V

en

ture

Ca

pit

al Fu

nd

s

I) O

the

rs -

Tru

st

SU

B T

OT

AL

(B

) (1

)

(2)

NO

N-I

NS

TIT

UT

ION

S

a)

Bo

die

s C

orp

.

I

) In

dia

n

ii)

Ove

rse

as

b)

Ind

ivid

ua

ls

Nil

1

,71

1,9

17

1

,71

1,9

17

30

.80

%

Nil

23

4,5

00

2

34

,50

0

4.2

2%

0.0

0%

0.0

0%

0.0

0%

Nil

23

4,5

00

23

4,5

00

4

.22

%

Fo

reig

n B

od

ies

- D

R

SU

B T

OT

AL

(B

) (2

)

C.

SH

AR

ES

HE

LD

BY

CU

ST

OD

IAN

FO

R

GD

RS

& A

DR

S

e)

Ve

ntu

re C

ap

ita

l Fu

nd

s

f) I

nsu

ran

ce C

om

pa

nie

s

i)

Ind

ivid

ua

l sh

are

ho

lde

rs h

old

ing

no

min

al sh

are

ca

pit

al u

pto

R

s. 1

la

kh

ii)

Ind

ivid

ua

l sh

are

ho

lde

rs h

old

ing

n

om

ina

l sh

are

ca

pit

al in

exce

ss o

f

R

s 1

la

kh

c) O

the

rs (

spe

cify

)

No

n R

esi

de

nt

Ind

ian

s

Ove

rse

as

Co

rpo

rate

Bo

die

s

Fo

reig

n N

ati

on

als

Cle

ari

ng

Me

mb

ers

Tru

sts

TO

TA

L (

B)

GR

AN

D T

OT

AL

(A

+B

+C

)

Nil

50

4,0

00

5

04

,00

0

9

.07

%0

.00

%

N

il

50

4,0

00

50

4,0

00

9.0

7%

Nil

1

,71

1,9

17

1,7

11

,91

7

30

.80

%

N

il

30

0,0

00

3

00

,00

0

5.4

0%

0.0

0%

Nil

30

0,0

00

30

0,0

00

5

.40

%

N

il

5

34

,50

0

5

34

,50

0

9

.62

%0

.00

%

N

il

5

34

,50

0

5

34

,50

0

9.6

2%

N

il

5

,55

7,5

17

5,5

57

,51

7

1

00

.00

%0

.00

%

N

il

5,5

57

,51

7

5

,55

7,5

17

10

0%

N

il

2

,24

6,4

17

2,2

46

,41

7

40

.42

%0

.00

%

N

il

2

,24

6,4

17

2

,24

6,4

17

4

0.4

2%

Nil

1,2

07

,91

71

,20

7,9

17

2

1.7

3%

Nil

1,2

07

,91

71

,20

7,9

17

2

1.7

3%

Madura Microfinance 32

Sh

are

ho

lde

rs N

am

e

SH

AR

EH

OL

DIN

G A

T T

HE

BE

GIN

NIN

G O

F T

HE

YE

AR

[A

S O

N 3

1-M

AR

CH

-20

14

]

SH

AR

E

HO

LD

ING

A

T

TH

E

EN

D

OF

T

HE

YE

AR

[A

S O

N 3

1-M

AR

CH

-20

15

]

No

. o

f

Sh

are

s

% o

f to

tal

Sh

are

s o

f

the

co

mp

an

y

% o

f S

ha

res

Ple

dg

ed

/en

cu

mb

ere

d

to t

ota

l sh

are

s

Mr.

Ash

ok

Mir

za

Mr.

R R

am

ara

j

At

the

be

gin

nin

g o

f th

e y

ea

r

Ch

an

ge

s d

uri

ng

th

e y

ea

r

NO

CH

AN

GE

No

. o

f

Sh

are

s

% o

f to

tal

Sh

are

s o

f

the

co

mp

an

y

% o

f S

ha

res

Ple

dg

ed

/

en

cu

mb

ere

d t

o t

ota

l

sha

res

Ms.

Ta

ra T

hia

ga

raja

n

Mr.

M N

ara

ya

na

n

TO

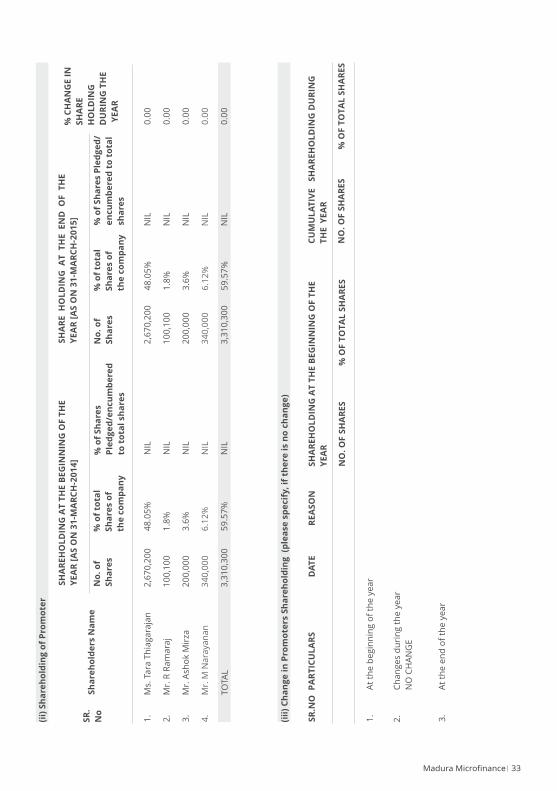

TAL

2,6

70

,20

0

10

0,1

00

20

0,0

00

34

0,0

00

48

.05

%

1.8

%

3.6

%

6.1

2%

NIL

NIL

NIL

NIL

3,3

10

,30

05

9.5

7%

NIL

2,6

70

,20

0

10

0,1

00

20

0,0

00

34

0,0

00

48

.05

%

1.8

%

3.6

%

6.1

2%

NIL

NIL

NIL

NIL

3,3

10

,30

05

9.5

7%

NIL

(ii)

Sh

are

ho

ldin

g o

f P

rom

ote

r

(iii

) C

ha

ng

e i

n P

rom

ote

rs S

ha

reh

old

ing

(p

lea

se s

pe

cif

y,

if t

he

re i

s n

o c

ha

ng

e)

PA

RT

ICU

LA

RS

DA

TE

RE

AS

ON

SH

AR

EH

OL

DIN

G A

T T

HE

BE

GIN

NIN

G O

F T

HE

YE

AR

CU

MU

LA

TIV

E

SH

AR

EH

OL

DIN

G D

UR

ING

TH

EY

EA

R

NO

. O

F S

HA

RE

S%

OF

TO

TA

L S

HA

RE

SN

O.

OF

SH

AR

ES

% O

F T

OT

AL

SH

AR

ES

At

the

en

d o

f th

e y

ea

r

SR

.NO

% C

HA

NG

E I

N

SH

AR

E

HO

LD

ING

DU

RIN

G T

HE

YE

AR

SR

.

No

1.

2.

3.

4.

0.0

0

0.0

0

0.0

0

0.0

0

0.0

0

1.

2.

3.

33Madura Microfinance

(iv

) S

ha

reh

old

ing

Pa

tte

rn o

f to

p t

en

Sh

are

ho

lde

rs (O

the

r th

an

Dir

ect

ors

, P

rom

ote

rs a

nd

Ho

lde

rs o

f G

DR

s a

nd

AD

Rs)

FO

R E

AC

H O

F T

HE

TO

P 1

0

SH

AR

EH

OL

DE

RS

SR

.

NO

DA

TE

WIS

E

INC

RE

AS

E/

DE

CR

EA

SE

IN

SH

AR

EH

OL

DIN

G

RE

AS

ON

SH

AR

EH

OL

DIN

G A

T T

HE

BE

GIN

NIN

G O

F T

HE

YE

AR

CU

MU

LA

TIV

E

SH

AR

EH

OL

DIN

G D

UR

ING

TH

E Y

EA

R

NO

. O

F S

HA

RE

S%

OF

TO

TA

L S

HA

RE

SN

O.

OF

SH

AR

ES

% O

F T

OT

AL

SH

AR

ES

(I)

Ele

va

r U

nit

us

Co

rpo

rati

on

a)

At

the

be

gin

nin

g o

f th

e y

ea

r

b)

Ch

an

ge

s d

uri

ng

th

e y

ea

r

c)

At

the

en

d o

f th

e y

ea

r

1,2

07

,91

7

Nil

1,2

07

,91

7

21

.73

%

0.0

0%

21

.73

%

1,2

07

,91

7

Nil

1,2

07

,91

7

21

.73

%

0.0

0%

21

.73

%

(II)

M

art

i G

Su

bra

hm

an

ya

m

a)

At

the

be

gin

nin

g o

f th

e y

ea

r

b)

C

ha

ng

es

du

rin

g t

he

ye

ar

c) A

t th

e e

nd

of

the

ye

ar

30

0,0

00

Nil

30

0,0

00

5.4

0%

0.0

0%

5.4

0%

30

0,0

00

Nil

30

0,0

00

5.4

0%

0.0

0%

5.4

0%

(III

) M

ad

ura

Mic

rocre

dit

Em

plo

ye

es

We

lfa

re T

rust

a)

At

the

be

gin

nin

g o

f th

e y

ea

r

b)

C

ha

ng

es

du

rin

g t

he

ye

ar

c)

At

the

en

d o

f th

e y

ea

r

50

4,0

00

Nil

50

4,0

00

9.0

7%

0.0

0%

9.0

7%

50

4,0

00

Nil

50

4,0

00

9.0

7%

0.0

0%

9.0

7%

(IV

) M

V S

ub

bia

h

a)

At

the

be

gin

nin

g o

f th

e y

ea

r

b)

C

ha

ng

es

du

rin

g t

he

ye

ar

c)

At

the

en

d o

f th

e y

ea

r

10

0,0

00

Nil

10

0,0

00

1.8

0%

0.0

0%

1.8

0%

10

0,0

00

Nil

10

0,0

00

1.8

0%

0.0

0%

1.8

0%

Madura Microfinance 34

35Madura Microfinance

(v)

Sh

are

ho

ldin

g o

f D

ire

cto

rs a

nd

Ke

y M

an

ag

eri

al

Pe

rso

nn

el:

(I)

M

s. T

ara

Th

iag

ara

jan

a)

A

t th

e b

eg

inn

ing

of

the

ye

ar

b)

C

ha

ng

es

du

rin

g t

he

ye

ar

c)

At

the

en

d o

f th

e y

ea

r

2,6

70

,20

0

Nil

2,6

70

,20

0

48

.05

%

0.0

0%

48

.05

%

2,6

70

,20

0

Nil

2,6

70

,20

0

48

.05

%

0.0

0%

48

.05

%

(II)

Mr.

R R

am

ara

j

a)

A

t th

e b

eg

inn

ing

of

the

ye

ar

b)

C

ha

ng

es

du

rin

g t

he

ye

ar

c)

At

the

en

d o

f th

e y

ea

r

10

0,1

00

Nil

10

0,1

00

1.8

0%

0.0

0%

1.8

0%

10

0,1

00

Nil

10

0,1

00

1.8

0%

0.0

0%

1.8

0%

(III

) M

r. A

sho

k M

irza

a)

A

t th

e b

eg

inn

ing

of

the

ye

ar

b)

C

ha

ng

es

du

rin

g t

he

ye

ar

c)

At

the

en

d o

f th

e y

ea

r

20

0,0

00

Nil

20

0,0

00

3.6

0%

0.0

0%

3.6

0%

20

0,0

00

Nil

20

0,0

00

3.6

0%

0.0

0%

3.6

0%

(IV

) M

r. M

oh

an

Ed

dy

a)

A

t th

e b

eg

inn

ing

of

the

ye

ar

b)

C

ha

ng

es

du

rin

g t

he

ye

ar

c)

At

the

en

d o

f th

e y

ea

r

20

,00

0

Nil

20

,00

0

0.3

6%

0.0

0%

0.3

6%

20

,00

0

Nil

20

,00

0

0.3

6%

0.0

0%

0.3

6%

(V)

Mr.

M N

ara

ya

na

n

a)

A

t th

e b

eg

inn

ing

of

the

ye

ar

b)

Ch

an

ge

s d

uri

ng

th

e y

ea

r

c)

At

the

en

d o

f th

e y

ea

r

34

0,0

00

Nil

34

0,0

00

6.1

2%

0.0

0%

6.1

2%

34

0,0

00

Nil

34

0,0

00

6.1

2%

0.0

0%

6.1

2%

SH

AR

EH

OL

DIN

G O

F

DIR

EC

TO

RS

AN

D E

AC

H

KE

Y M

AN

AG

ER

IAL

PE

RS

ON

NE

L

SR

.

NO

DA

TE

WIS

E

INC

RE

AS

E/

DE

CR

EA

SE

IN

SH

AR

EH

OL

DIN

G

RE

AS

ON

SH

AR

EH

OL

DIN

G A

T T

HE

BE

GIN

NIN

G O

F T

HE

YE

AR

CU

MU

LA

TIV

E

SH

AR

EH

OL

DIN

G D

UR

ING

TH

E Y

EA

R

NO

. O

F S

HA

RE

S%

OF

TO

TA

L S

HA

RE

SN

O.

OF

SH

AR

ES

% O

F T

OT

AL

SH

AR

ES

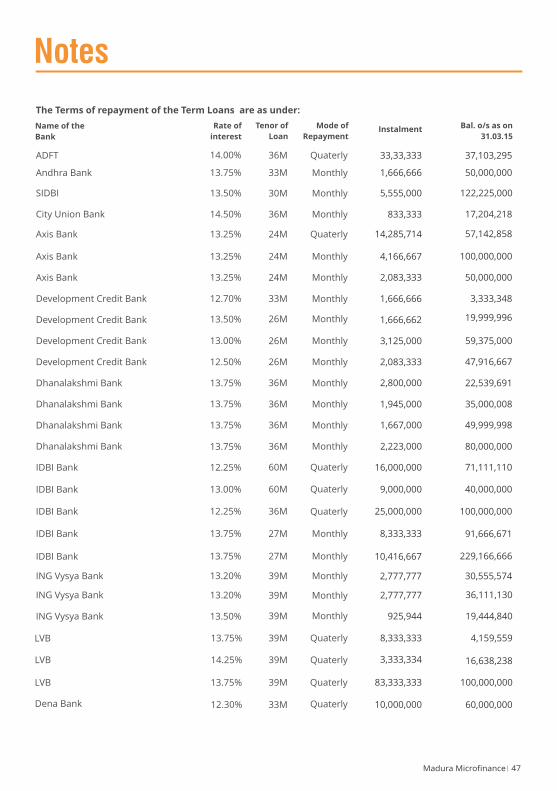

V.

IND

EB

TE

DN

ES

S

SE

CU

RE

D L

OA

NS

EX

CL

UD

ING

DE

PO

SIT

S

UN

SE

CU

RE

D L

OA

NS

DE

PO

SIT

S

(I)

In

de

bte

dn

ess

of

the

Co

mp

an

y in

clu

din

g in

tere

st o

uts

tan

din

g/a

ccru

ed

bu

t n

ot

du

e f

or

pa

ym

en

t.

TO

TA

L I

ND

EB

TE

DN

ES

S

(I)

P

rin

cip

al A

mo

un

t

(ii)

I

nte

rest

du

e b

ut

no

t p

aid

(a

) In

de

bte

dn

ess

at

the

be

gin

nin

g o

f th

e f

ina

ncia

l y

ea

r

1,7

52

,93

7,8

66

.00

NIL

NIL

1,7

52

,93

7,8

66

.00

(iii)

In

tere

st a

ccru

ed

bu

t n

ot

du

e

1,7

52

,93

7,8

66

.00

NIL

NIL

1,7

52

,93

7,8

66

.00

*A

dd

itio

n

*R

ed

uct

ion

(b)

Ch

an

ge

in

In

de

bte

dn

ess

du

rin

g t

he

fin

an

cia

l y

ea

r

2,4

95

,00

0,0

00

.00

NIL

14

3,3

63

,91

9.0

0N

IL

2,4

95

,00

0,0

00

.00

14

3,3

63

,91

9.0

0

3,0

98

,65

9,5

97

.00

NIL

NIL

3,1

04

,57

3,9

47

.00

NIL

NIL

(I)

P

rin

cip

al A

mo

un

t

(ii)

I

nte

rest

du

e b

ut

no

t p

aid

(iii)

In

tere

st a

ccru

ed

bu

t n

ot

du

e5

,91

4,3

50

.00

NIL

3,0

98

,65

9,5

97

.00

5,9

14

,35

0.0

0

2,6

38

,36

3,9

19

.00

NIL

NIL

2,6

38

,36

3,9

19

.00

3,1

04

,57

3,9

47

.00

Madura Microfinance 36

(c)

Ind

eb

ted

ne

ss a

t th

e e

nd

of

the

fin

an

cia

l y

ea

r

(Am

ou

nt

Rs/

La

kh

s)

PA

RT

ICU

LA

RS

TO

TA

L(i

)+(i

i)+

(iii

)

TO

TA

L(i

)+(i

i)+

(iii

)

NE

T C

HA

NG

E

VI.

RE

MU

NE

RA

TIO

N O

F D

IRE

CT

OR

S A

ND

KE

Y M

AN

AG

ER

IAL

PE

RS

ON

NE

L

TO

TA

L(B

)=(1

+2

)-

13

0,0

00

.00

Pa

rtic

ula

rs o

f R

em

un

era

tio

nS

R.

NO

A.

Re

mu

ne

rati

on

to

Ma

na

gin

g D

ire

cto

r, W

ho

le-t

ime

Dir

ect

ors

an

d/o

r M

an

ag

er:

Na

me

of

MD

/WT

D/

Ma

na

ge

rTo

tal

Am

ou

nt

Na

me

Ms.

Ta

ra T

hia

ga

raja

nM

r. M

oh

an

Ed

dy

(Rs/

La

kh

s)D

esi

gn

ati

on

Ma

na

gin

g D

ire

cto

rW

ho

le-t

ime

Dir

ect

or

1.

Gro

ss s

ala

ry

(a)

Sa

lary

as

pe

r p

rovis

ion

s co

nta

ine

d in

sect

ion

17

(1)

of

the

In

com

e-t

ax

Act

, 1

96

1.

(b)

Va

lue

of

pe

rqu

isit

es

u/s

17

(2)

Inco

me

-

tax

Act

, 1

96

1.

Pro

fits

in

lie

u o

f sa

lary

un

de

r se

ctio

n

17

(3)

Inco

me

- ta

x A

ct, 1

96

1.

2.

Sto

ck O

pti

on

3.

Sw

ea

t E

qu

ity

Co

mm

issi

on

- a

s %

of

pro

fit

- o

the

rs, sp

eci

fy

4.

Oth

ers

, p

lea

se s

pe

cify

5.

B

. R

em

un

era

tio

n t

o o

the

r D

ire

cto

rs

Pa

rtic

ula

rs o

f R

em

un

era

tio

nS

R.

NO

Na

me

of

Dir

ecto

rsTo

tal

Am

ou

nt

(R

s/La

kh

s)

1.

Ind

ep

en

de

nt

Dir

ect

ors

Fe

e f

or

att

en

din

g b

oa

rd c

om

mit

tee

me

eti

ng

s

Co

mm

issi

on

Oth

ers

, p

lea

se s

pe

cify

To

tal

(1)

2.

Oth

er

No

n-E

xe

cuti

ve

Dir

ect

ors

Fe

e f

or

att

en

din

g b

oa

rd c

om

mit

tee

me

eti

ng

s

Co

mm

issi

on

Oth

ers

, p

lea

se s

pe

cify

To

tal

(2)

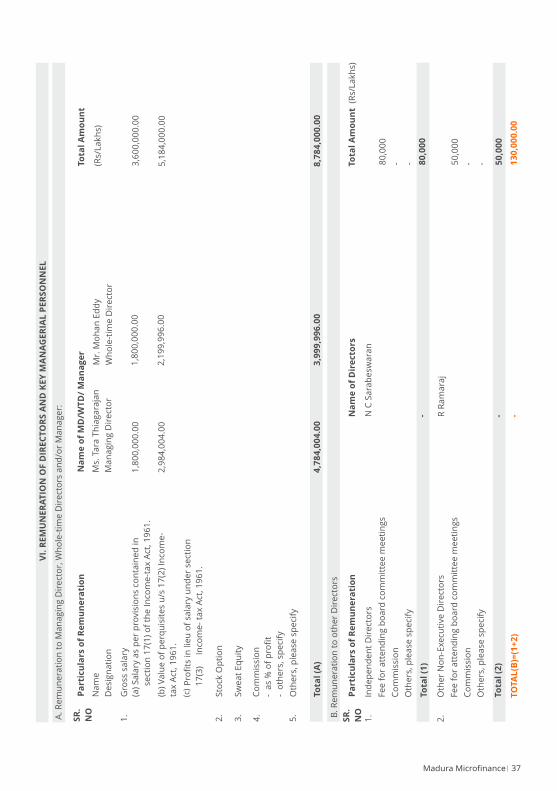

1,8

00

,00

0.0

01

,80

0,0

00

.00

3,6

00

,00

0.0

0

2,9

84

,00

4.0

02

,19

9,9

96

.00

5,1

84

,00

0.0

0

To

tal

(A)

4,7

84

,00

4.0

03

,99

9,9

96

.00

8,7

84

,00

0.0

0

80

,00

0

- - 80

,00

0

50

,00

0

- - 50

,00

0

- -N C

Sa

rab

esw

ara

n

R R

am

ara

j

37Madura Microfinance

Pa

rtic

ula

rs o

f R

em

un

era

tio

nS

R.

NO

Na

me

of

MD

/WT

D/

Ma

na

ge

rTo

tal

Am

ou

nt

Na

me

Mr.

M N

ara

ya

na

n(R

s/La

kh

s)

De

sig

na

tio

nC

EO

1.

Gro

ss s

ala

ry

(a)

Sa

lary

as

pe

r p

rovis

ion

s co

nta

ine

d in

sect

ion

17

(1)

of

the

In

com

e-t

ax

Act

, 1

96

1.

(b)

Va

lue

of

pe

rqu

isit

es

u/s

17

(2)

Inco

me

-

tax

Act

, 1

96

1.

Pro

fits

in

lie

u o

f sa

lary

un

de

r se

ctio

n

17

(3)

Inco

me

- ta

x A

ct, 1

96

1.

2.

Sto

ck O

pti

on

3.

Sw

ea

t E

qu

ity

Co

mm

issi

on

- a

s %

of

pro

fit

- o

the

rs, sp

eci

fy

4.

Oth

ers

, p

lea

se s

pe

cify

5.

1,8

00

,00

0.0

02

,15

5,1

40

.00

1,9

34

,00

4.0

0

3,7

34

,00

4.0

06

60

,57

6.0

0

C.

Re

mu

ne

rati

on

to

Ke

y M

an

ag

eri

al P

ers

on

ne

l o

the

r th

an

MD

/Ma

na

ge

r/W

TD

CFO

CS

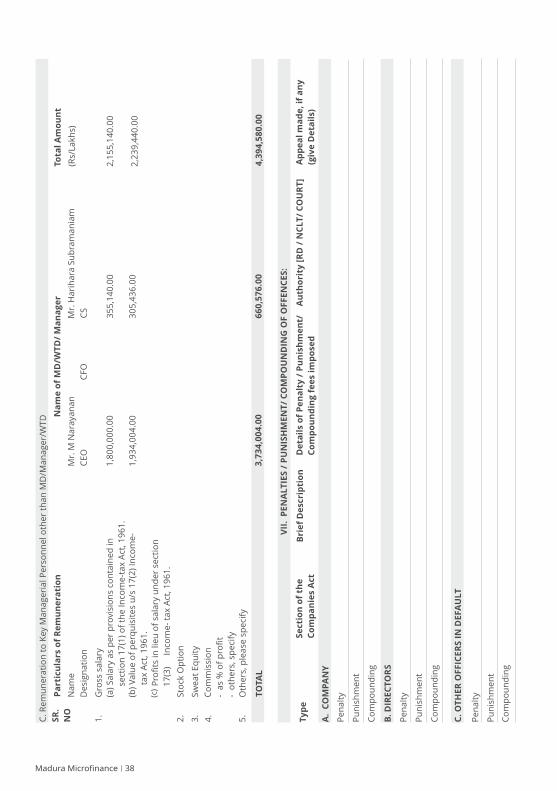

35

5,1

40

.00

30

5,4

36

.00

TO

TA

L

2,2

39

,44

0.0

0

4,3

94

,58

0.0

0

VII

. P

EN

AL

TIE

S /

PU

NIS

HM

EN

T/

CO

MP

OU

ND

ING

OF

OF

FE

NC

ES

:

Ty

pe

Se

cti

on

of

the

Co

mp

an

ies

Act

Bri

ef

De

scri

pti

on

De

tail

s o

f P

en

alt

y /

Pu

nis

hm

en

t/

Co

mp

ou

nd

ing

fe

es

imp

ose

d

Au

tho

rity

[R

D /

NC

LT

/ C

OU

RT

]A

pp

ea

l m

ad

e,

if a

ny

(giv

e D

eta

ils)

A.

CO

MP

AN

Y

Pe

na

lty

Pu

nis

hm

en

t

Co

mp

ou

nd

ing

B.

DIR

EC

TO

RS

Pe

na

lty

Pu

nis

hm

en

t

Co

mp

ou

nd

ing

C.

OT

HE

R O

FF

ICE

RS

IN

DE

FA

UL

T

Pe

na

lty

Pu

nis

hm

en

t

Co

mp

ou

nd

ing

Madura Microfinance 38

Mr.

Ha

rih

ara

Su

bra

ma

nia

m

Form AOC-1

(Pursuant to first proviso to sub-section (3) of section 129 read with rule 5 of

Companies (Accounts) Rules, 2014)

STATEMENT CONTAINING SALIENT FEATURES OF THE FINANCIAL STATEMENT OF

SUBSIDIARIES/ASSOCIATE COMPANIES/JOINT VENTURES

PART “A”: SUBSIDIARIES

(Information in respect of each subsidiary to be presented with amounts in Rs.)

SL.NO Particulars Details

Name of the subsidiary Madura Micro Education Private Limited

Reporting period for the

subsidiary concerned, if different

from the holding company's

reporting period.

NA

Reporting currency and Exchange

rate as on the last date of the

relevant Financial year in the case

of foreign subsidiaries.

Share Capital

NA

1.

2.

3.

4.

Reserves & Surplus5.

Total Assets6.

Total Liabilities7.

Investments8.

Turnover9.

Profit before taxation/(Loss)10.

Provision for taxation11.

Provision after taxation.12.

Proposed Dividend13.

% of shareholding14.

1,49,00,000

(1,11,49,791)

32032521

32032521

NIL

5682152

(68,21,132)

NIL

(68,21,132)

NIL

100%

Part “B”: Associates and Joint Ventures: Not Applicable

Annexure 3

39Madura Microfinance

Form AOC-2

(Pursuant to clause (h) of sub-section (3) of section 134 of the Act and Rule 8(2) of the

Companies (Accounts) Rules, 2014).

Form for Disclosure of particulars of contracts/arrangements entered into by the company

with related parties referred to in sub section (1) of section 188 of the Companies Act, 2013

including certain arm's length transaction under third proviso thereto.

SL.NO Particulars Details

Name(s) of the related party and nature of the

relationship

NIL1.

Nature of contracts/agreements/transaction NIL2.

Salient features of the contracts or arrangements

or transactions including the value, if any

NIL3.

Justification for entering in to such contracts or

arrangements or transactions

4. NIL

Date of approval by the Board5. NIL

Amount paid as advances, if any6. NIL

Date on which a special resolution was passed in General

Meeting as required under first proviso to section 188

7. NIL

2. D etails of contracts or arrangements or transactions at Arm's length basis.

SL.NO Particulars Details

Name(s) of the related party and nature of the

relationship

Scimergent Analytics and

Education Private Limited

1.

Nature of contracts/agreements/transaction Agreement for IT services2.

Duration of contracts/arrangements/transaction Until Termination3.

Salient terms of the contracts or arrangements

or transaction including the value, if any

4. To provide assistance to the

Company for enhancing the

Information Technology

platform and architecture.

Value: 157.50 Lacs

Date of approval by the Board5. 23.06.2014

Amount paid as advances, if any6. NIL

Annexure 4

Madura Microfinance 40

1. Details of contracts or arrangements or transactions not at Arm's length basis.

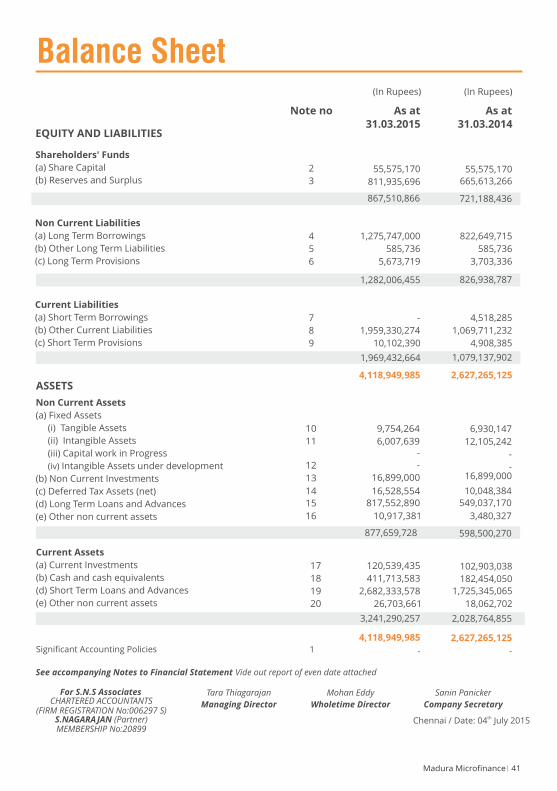

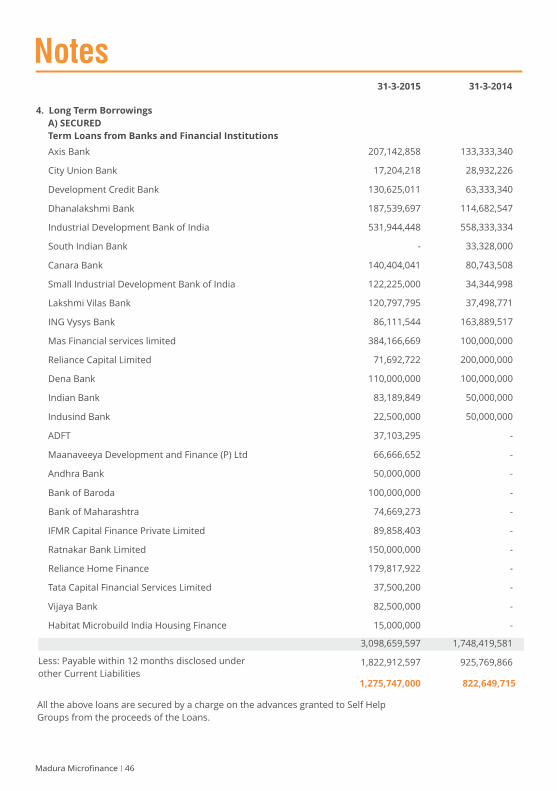

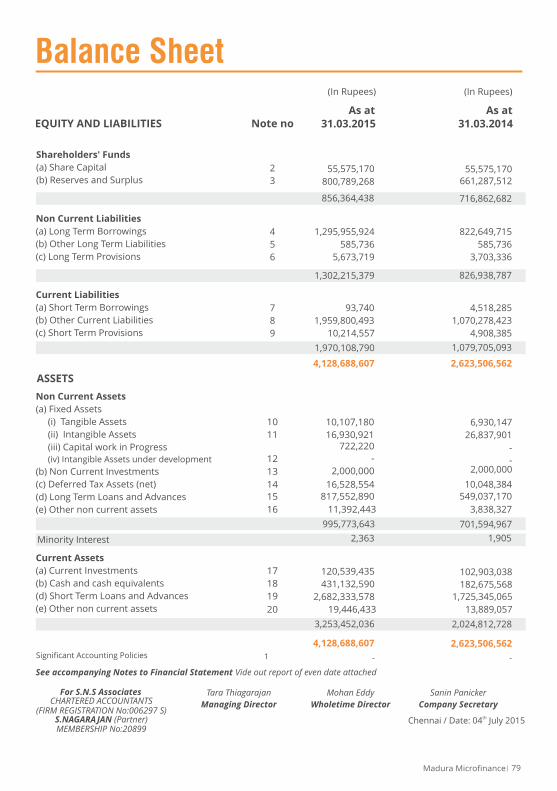

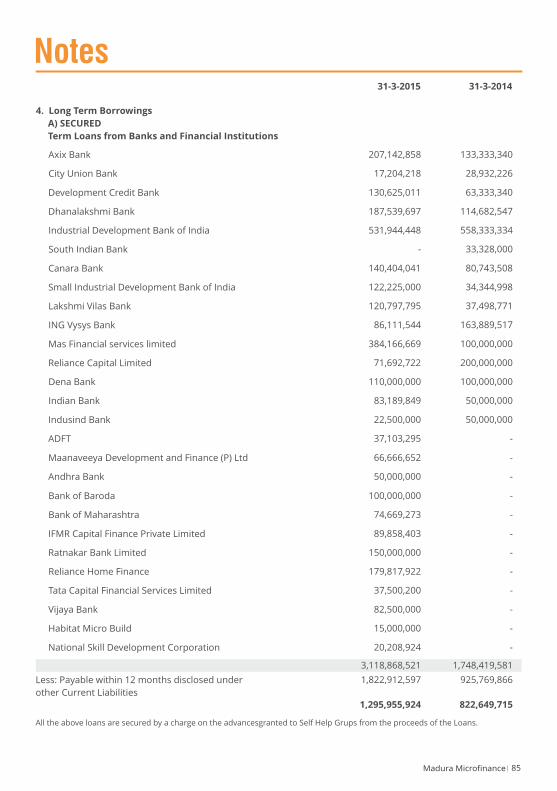

EQUITY AND LIABILITIES

Note no

Non Current Liabilities

(a) Long Term Borrowings

(b) Other Long Term Liabilities

(c) Long Term Provisions

Current Liabilities

(a) Short Term Borrowings

(b) Other Current Liabilities

(c) Short Term Provisions

Shareholders' Funds

(a) Share Capital

(b) Reserves and Surplus

2

3

1,275,747,000

585,736

5,673,719

4

5

6

867,510,866

1,282,006,455

55,575,170

665,613,266

822,649,715

585,736

3,703,336

721,188,436

826,938,787

-

1,959,330,274

10,102,390

7

8

9

1,969,432,664

4,518,285

1,069,711,232

4,908,385

1,079,137,902

4,118,949,985 2,627,265,125

9,754,264

6,007,639-

-

16,899,000

16,528,554

817,552,890

10,917,381

Non Current Assets

(a) Fixed Assets

(i) Tangible Assets

(ii) Intangible Assets

(iii) Capital work in Progress

(iv) Intangible Assets under development

(b) Non Current Investments

(c) Deferred Tax Assets (net)

(d) Long Term Loans and Advances

(e) Other non current assets

ASSETS

Current Assets

(a) Current Investments

(b) Cash and cash equivalents

(d) Short Term Loans and Advances

(e) Other non current assets

10

11

877,659,728 598,500,270

6,930,147

12,105,242

-

- 16,899,000

10,048,384

549,037,170

3,480,327

120,539,435

411,713,583

2,682,333,578

26,703,661

102,903,038

182,454,050

1,725,345,065

18,062,702

3,241,290,257 2,028,764,855

4,118,949,985 2,627,265,125

12

15

16

17

18

19

14

13

55,575,170

811,935,696

Balance Sheet

Significant Accounting Policies 1 - -

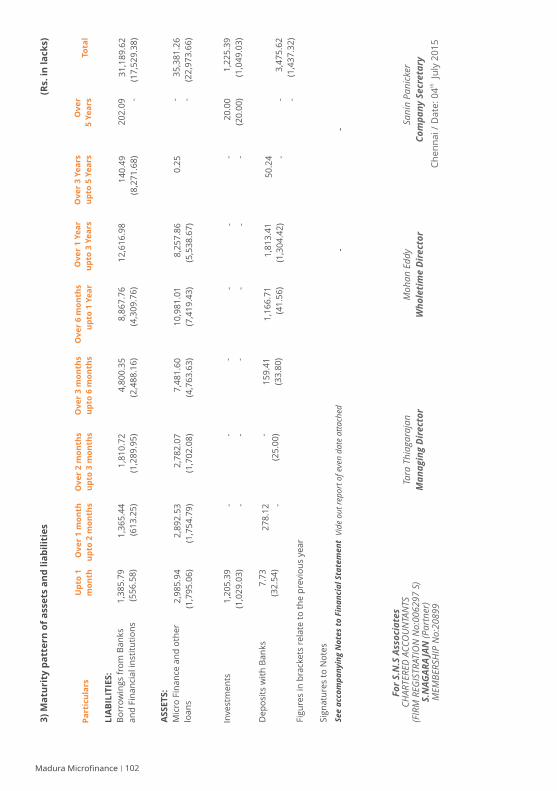

See accompanying Notes to Financial Statement Vide out report of even date attached

For S.N.S AssociatesCHARTERED ACCOUNTANTS

(FIRM REGISTRATION No:006297 S)S.NAGARAJAN (Partner)MEMBERSHIP No:20899

Tara Thiagarajan

Managing Director

Mohan Eddy

Wholetime Director

Sanin Panicker

Company Secretary

thChennai / Date: 04 July 2015

41Madura Microfinance

As at

31.03.2015

As at

31.03.2014

(In Rupees) (In Rupees)

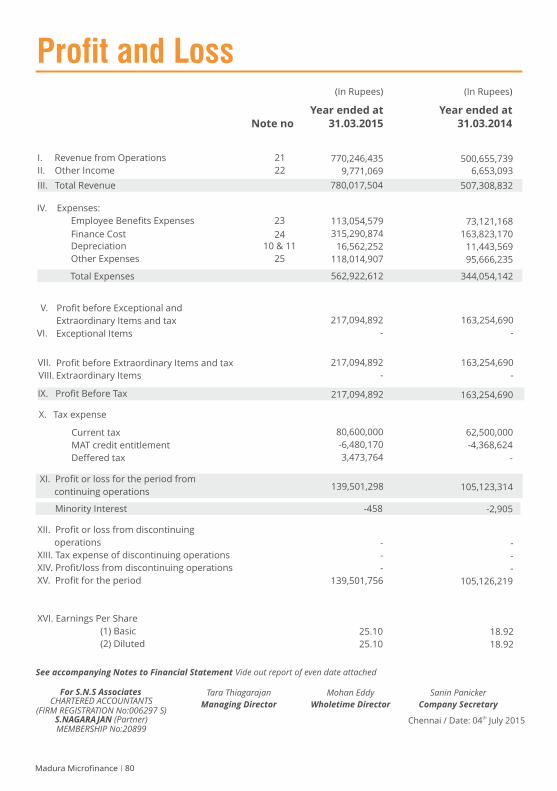

20

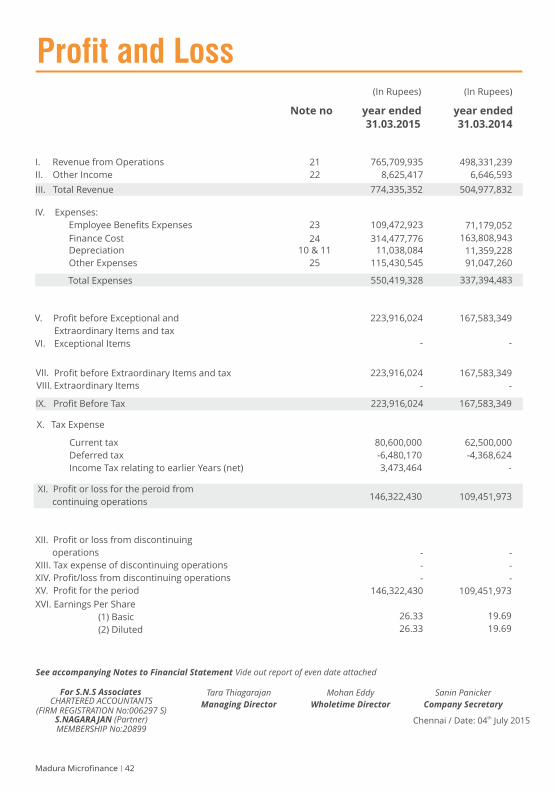

IV. Expenses:

Employee Benefits Expenses

Finance Cost

Depreciation

Other Expenses

Total Expenses

V. Profit before Exceptional and

Extraordinary Items and tax

VI. Exceptional Items

I. Revenue from Operations

II. Other Income

III. Total Revenue

21

22

109,472,923

314,477,776 11,038,084

115,430,545

23

2410 & 11

25

774,335,352

550,419,328

498,331,239

6,646,593

71,179,052

163,808,943

11,359,228

91,047,260

504,977,832

337,394,483

223,916,024

-

223,916,024

167,583,349

-

167,583,349

Current tax

Deferred tax

Income Tax relating to earlier Years (net)

765,709,935

8,625,417

VII. Profit before Extraordinary Items and tax

VIII. Extraordinary Items

IX. Profit Before Tax

X. Tax Expense

XI. Profit or loss for the peroid from

continuing operations

XII. Profit or loss from discontinuing

operations

XIII. Tax expense of discontinuing operations

XIV. Profit/loss from discontinuing operations

XV. Profit for the period

XVI. Earnings Per Share

(1) Basic

(2) Diluted

223,916,024

-

167,583,349

-

80,600,000

-6,480,170

3,473,464

62,500,000

-4,368,624

-

146,322,430

109,451,973

-

-

-

146,322,430

-

-

-

109,451,973

19.69

19.69

26.33

26.33

Profit and Loss

year ended

31.03.2015

year ended

31.03.2014

See accompanying Notes to Financial Statement Vide out report of even date attached

For S.N.S AssociatesCHARTERED ACCOUNTANTS

(FIRM REGISTRATION No:006297 S)S.NAGARAJAN (Partner)MEMBERSHIP No:20899

Tara Thiagarajan

Managing Director

Mohan Eddy

Wholetime Director

Sanin Panicker

Company Secretary

thChennai / Date: 04 July 2015

Madura Microfinance 42

Note no

(In Rupees) (In Rupees)

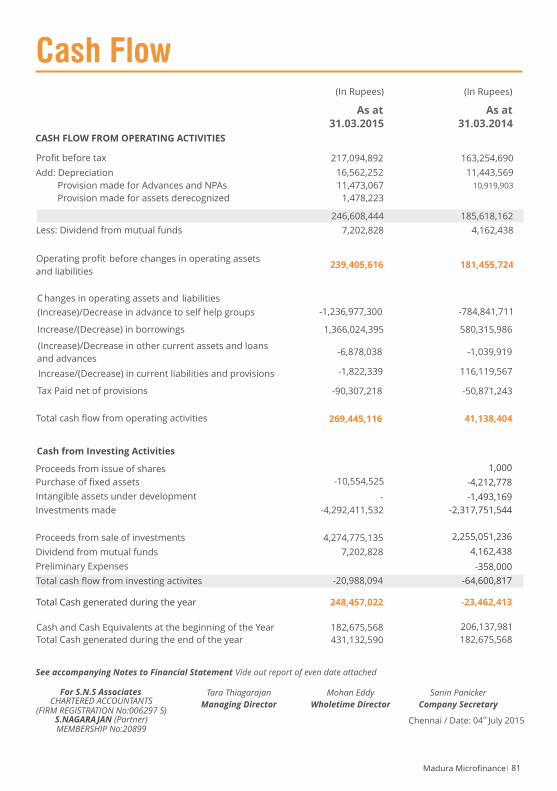

Cash Flow

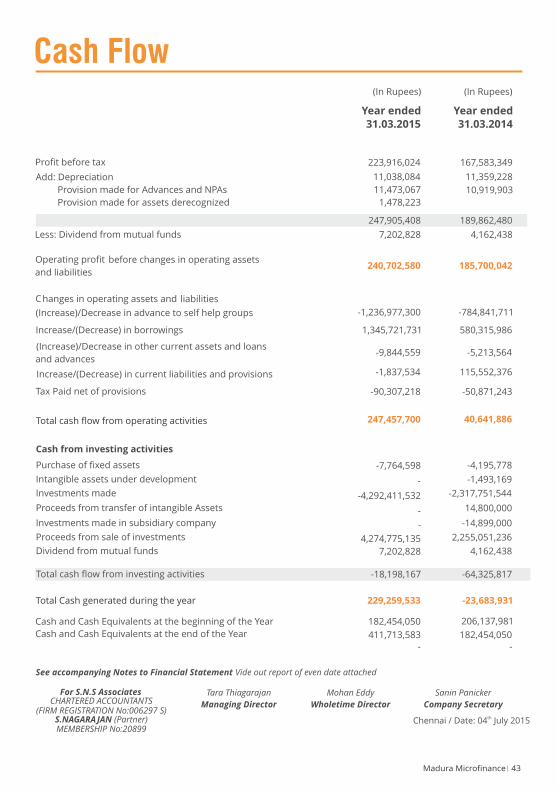

Profit before tax

Add: Depreciation

Provision made for Advances and NPAs

Provision made for assets derecognized

11,473,067

1,478,223

167,583,349

11,359,228

10,919,903

223,916,024

11,038,084

247,905,408 189,862,480

Less: Dividend from mutual funds 7,202,828

4,162,438

Operating profit before changes in operating assets

and liabilities 240,702,580 185,700,042

Changes in operating assets and liabilities

(Increase)/Decrease in advance to self help groups

Increase/(Decrease) in borrowings

(Increase)/Decrease in other current assets and loans

and advances

Increase/(Decrease) in current liabilities and provisions

Tax Paid net of provisions

-1,236,977,300

1,345,721,731

-9,844,559

-1,837,534

-90,307,218

-784,841,711

580,315,986

-5,213,564

115,552,376

-50,871,243

Total cash flow from operating activities 247,457,700 40,641,886

Cash from investing activities

Purchase of fixed assets

Intangible assets under development

Investments made

Proceeds from transfer of intangible Assets

Investments made in subsidiary company

Proceeds from sale of investments

Dividend from mutual funds

Total cash flow from investing activities

-7,764,598

-

-4,292,411,532

-

-

4,274,775,135

7,202,828

-18,198,167 -64,325,817

-4,195,778

-1,493,169

-2,317,751,544

14,800,000

-14,899,000

2,255,051,236

4,162,438

Total Cash generated during the year 229,259,533 -23,683,931

Cash and Cash Equivalents at the beginning of the Year 182,454,050 206,137,981

411,713,583 182,454,050

Year ended Year ended

31.03.2015 31.03.2014

See accompanying Notes to Financial Statement Vide out report of even date attached

For S.N.S AssociatesCHARTERED ACCOUNTANTS

(FIRM REGISTRATION No:006297 S)S.NAGARAJAN (Partner)MEMBERSHIP No:20899

Tara Thiagarajan

Managing Director

Mohan Eddy

Wholetime Director

Sanin Panicker

Company Secretary

thChennai / Date: 04 July 2015

43Madura Microfinance

- -

Cash and Cash Equivalents at the end of the Year

(In Rupees) (In Rupees)

Provision on Microfinance and other loans treated as non- performing assets is being made in

accordance with the Prudential Norms issued by Reserve Bank of India. The Company is also

creating a provision of 1% on all the Standard Advances.

In respect of assets derecognized, provision is made at the rate of 1% of the outstanding amounts of

assets derecognized from the books of the Company as at the balance sheet date.

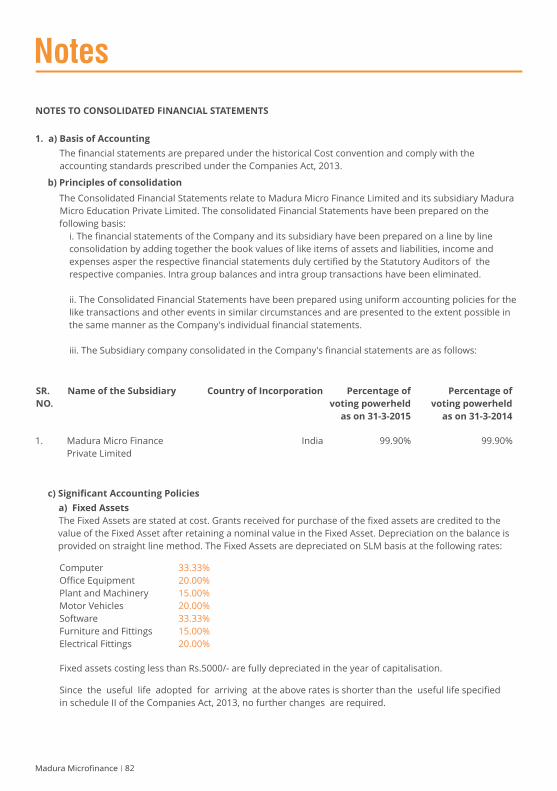

1. Significant Accounting Policies

a) Fixed Assets

The Fixed Assets are stated at cost. Grants received for purchase of the fixed assets are credited to the

value of the Fixed Asset after retaining a nominal value in the Fixed Asset. Depreciation on the balance

is provided on straight line method. The Fixed Assets are depreciated on SLM basis at the following

rates:

Computer

Office Equipment

Plant and Machinery

Motor Vehicles

Software

Furniture and Fittings

Electrical Fittings

33.33%

20.00%

15.00%

20.00%

33.33%

15.00%

20.00%

Fixed assets costing less than Rs.5000/- are fully depreciated in the year of capitalization.

Since the useful life adopted for arriving at the above rates is shorter than the useful life specified

in schedule II of the Companies Act, 2013, no further changes are required.

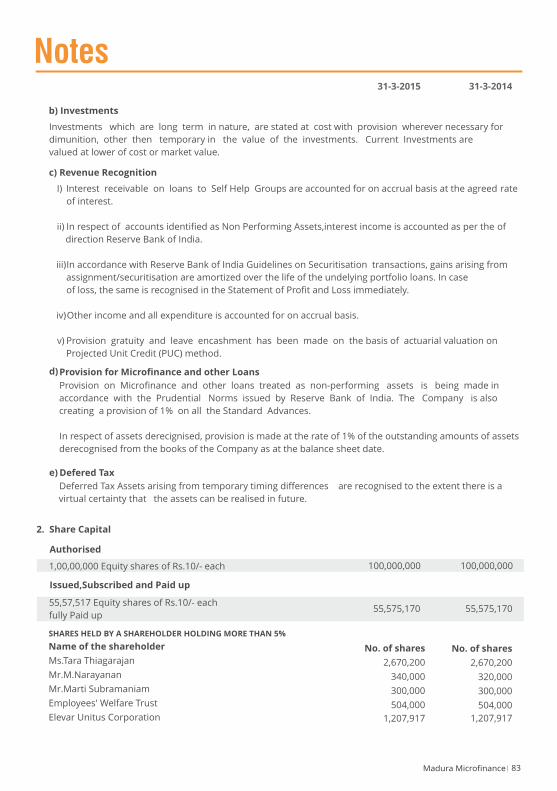

Investments which are long term in nature, are stated at cost with provision wherever necessary

for dimunition, other then temporary in the value of the investments. Current Investments are

valued at lower of cost or market value.

b) Investments

I) Interest receivable on loans to Self Help Groups are accounted for on accrual basis at the agreed

rate of interest.

ii) In respect of accounts identified as Non Performing Assets,i nterest income is accounted as per the

direction of Reserve Bank of India.

iii)I n accordance with Reserve Bank of India Guidelines on Securitization transactions, gains arising

f rom assignment/securitisation are amortized over t he life of the underlying portfolio loans. In case

o f loss, the same is recognized i n the Statement of Profit and Loss immediately.

iv) Other income and all expenditure is accounted for on accrual basis.

v ) Provision for gratuity and leave encasement has been made on t he basis of actuarial valuation on

Projected Unit Credit (PUC) m ethod.

c) Revenue Recognition

d) Provision for Microfinance and other Loans:

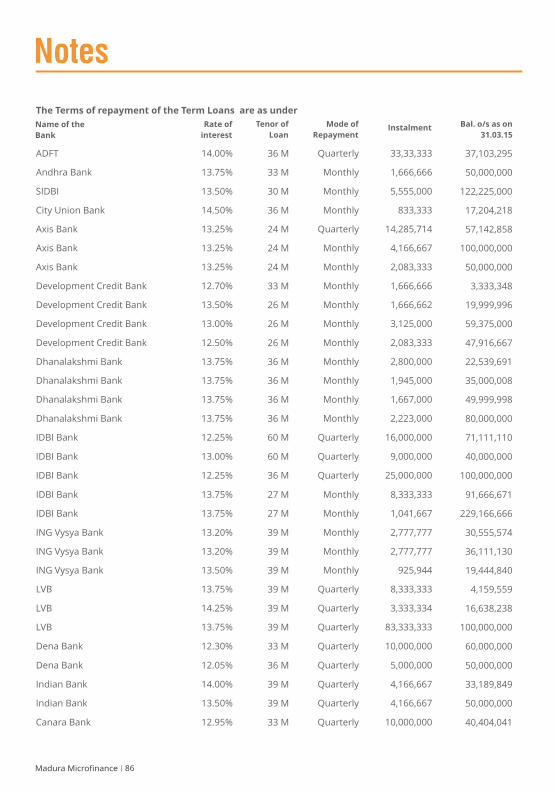

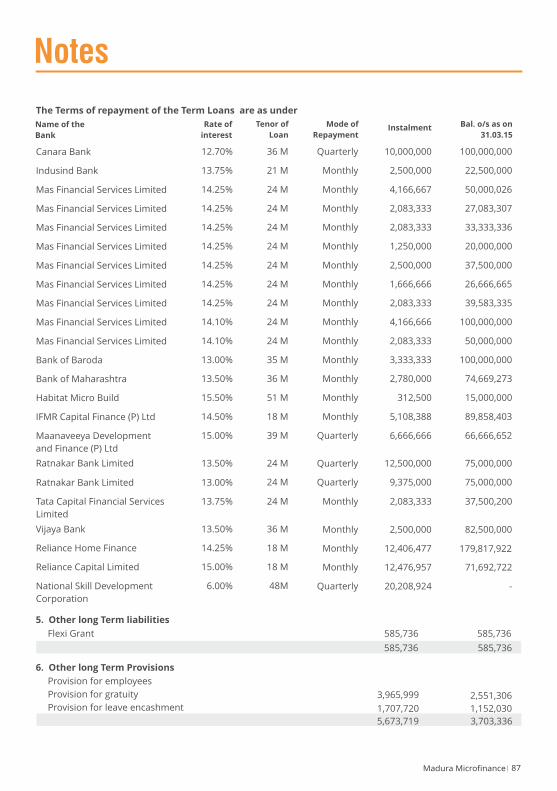

Notes

Madura Microfinance 44

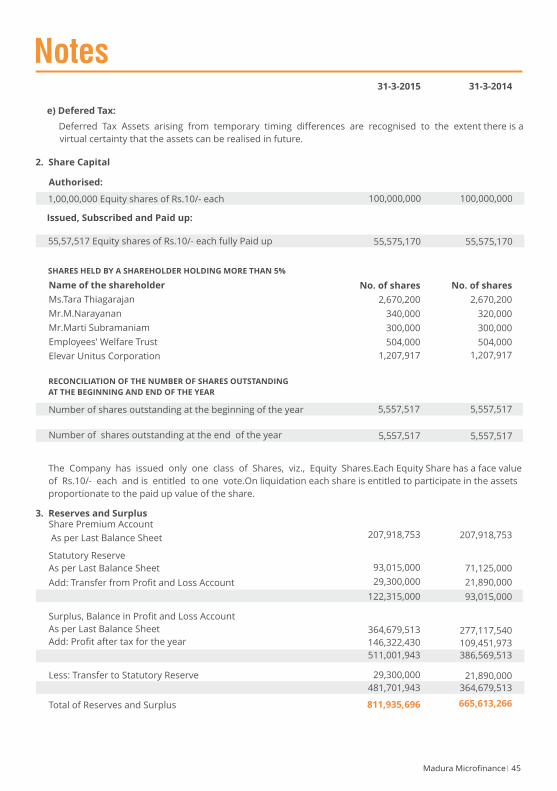

e) Defered Tax:

Deferred Tax Assets arising from temporary timing differences are recognised to the extent there is a

virtual certainty that the assets can be realised in future.

Authorised:

2. Share Capital

1,00,00,000 Equity shares of Rs.10/- each 100,000,000 100,000,000

Issued, Subscribed and Paid up:

Name of the shareholder

Ms.Tara Thiagarajan Mr.M.Narayanan Mr.Marti Subramaniam Employees' Welfare Trust Elevar Unitus Corporation

No. of shares

2,670,200

340,000 300,000

504,000

1,207,917

No. of shares

2,670,200

320,000

300,000

504,000

1,207,917

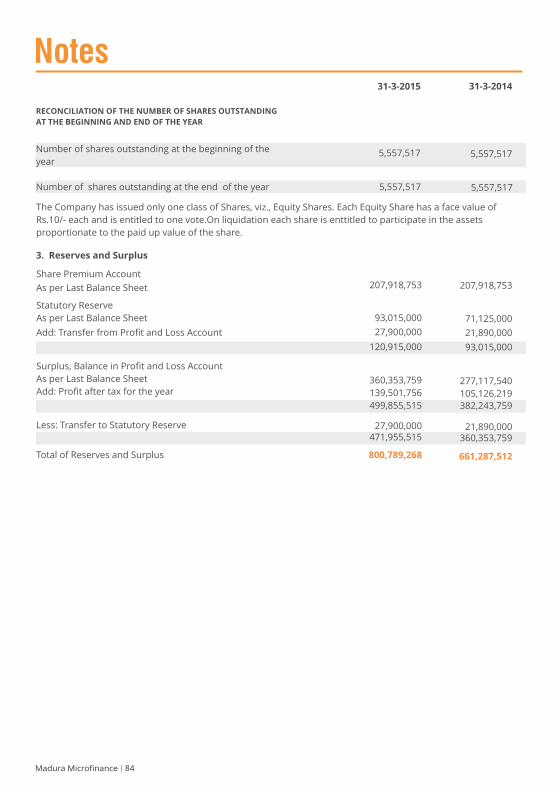

Number of shares outstanding at the beginning of the year

Number of shares outstanding at the end of the year

5,557,517

5,557,517

The Company has issued only one class of Shares, viz., Equity Shares. Each Equity Share has a face value

of Rs.10/- each and is entitled to one vote. On liquidation each share is entitled to participate in the assets

proportionate to the paid up value of the share.

3. Reserves and SurplusShare Premium Account As per Last Balance Sheet

Statutory Reserve As per Last Balance Sheet

Add: Transfer from Profit and Loss Account

Surplus, Balance in Profit and Loss Account

As per Last Balance Sheet