Damian Sylvia: How to Prepare for a Successful Retirement

36

This Presentation is brought to you by Damian Sylvia 220 Monmouth Road 2 nd Floor Oakhurst, NJ 07755 www.RetirementSolutionsNJ.com

-

Upload

damian-sylvia -

Category

Presentations & Public Speaking

-

view

63 -

download

1

Transcript of Damian Sylvia: How to Prepare for a Successful Retirement

This Presentation is brought to you by

Damian Sylvia220 Monmouth Road

2nd FloorOakhurst, NJ 07755

www.RetirementSolutionsNJ.com

simple solutions for retirement

Housekeeping Matters

Please silence any cell phones

Restrooms are located through the door in the front where you walked in

The seminar will last about 45 minutes

Please hold your questions until we come around to your table – we have a lot of information to cover

You will be offered a free consultation at the conclusion of this seminar

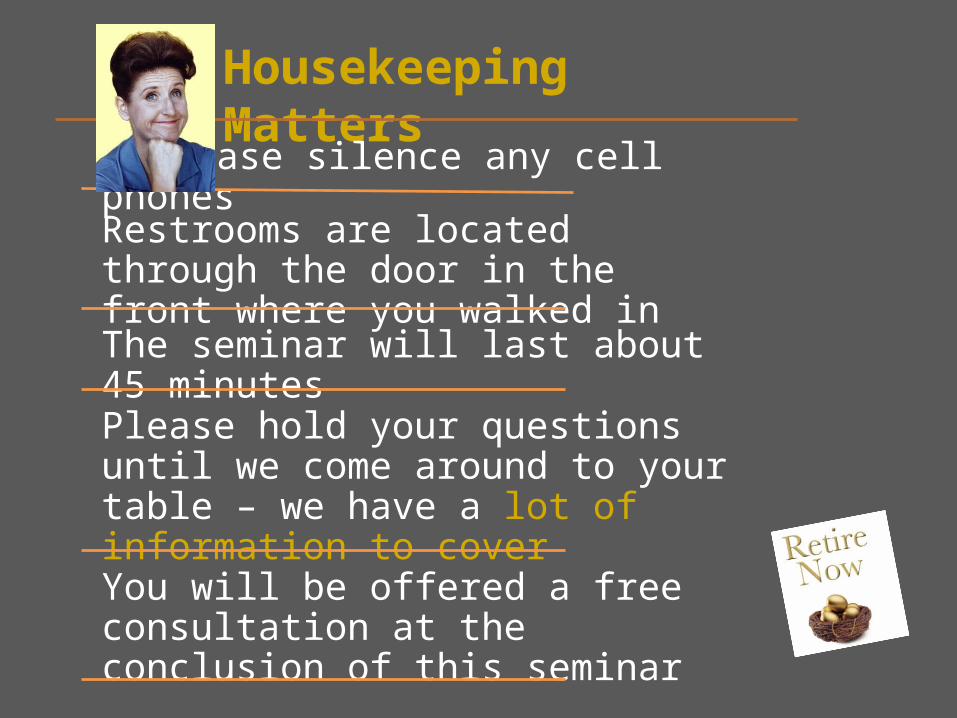

Retire NowYesterday

Worked for employer 30 + years

Earned a pension thru Employer’s Contribution

Earned Social Security

Saved addt’l money to supplement pension and

social security

Today

Worked for Multiple Employers

Entitled to little or no Pension

Earned Social Security

Saved YOUR OWN money through 401K

to supplement retirement

Saved more of your own after-tax money

Yesterday vs. Today

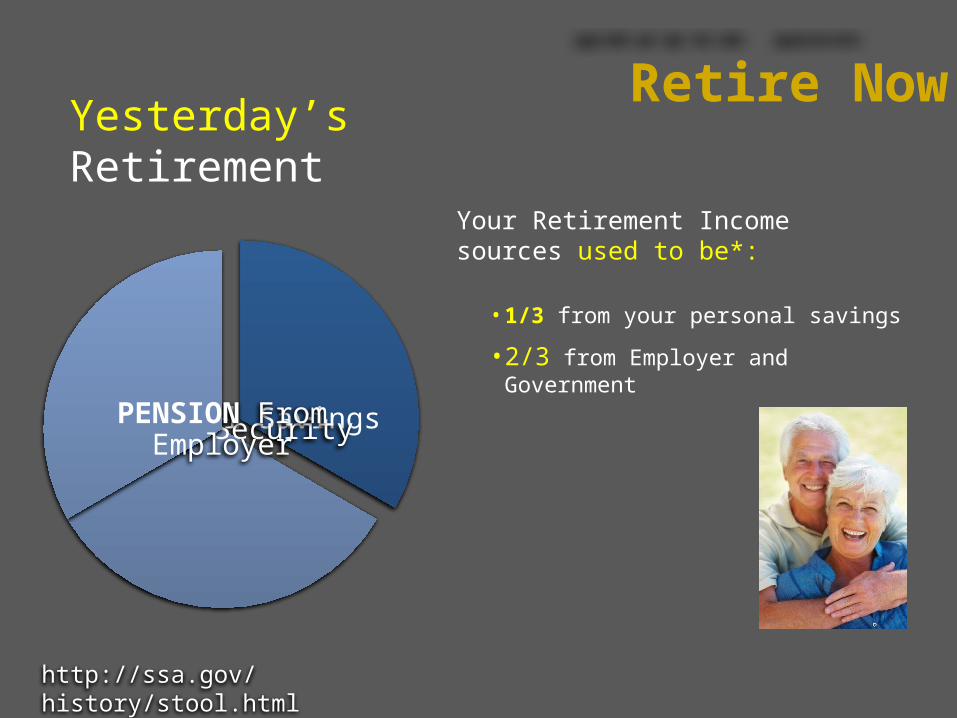

Retire NowYesterday’s Retirement

Your Retirement Income sources used to be*:

• 1/3 from your personal savings

• 2/3 from Employer and Government

Personal Savings

Social Security

PENSION From

Employer

http://ssa.gov/history/stool.html

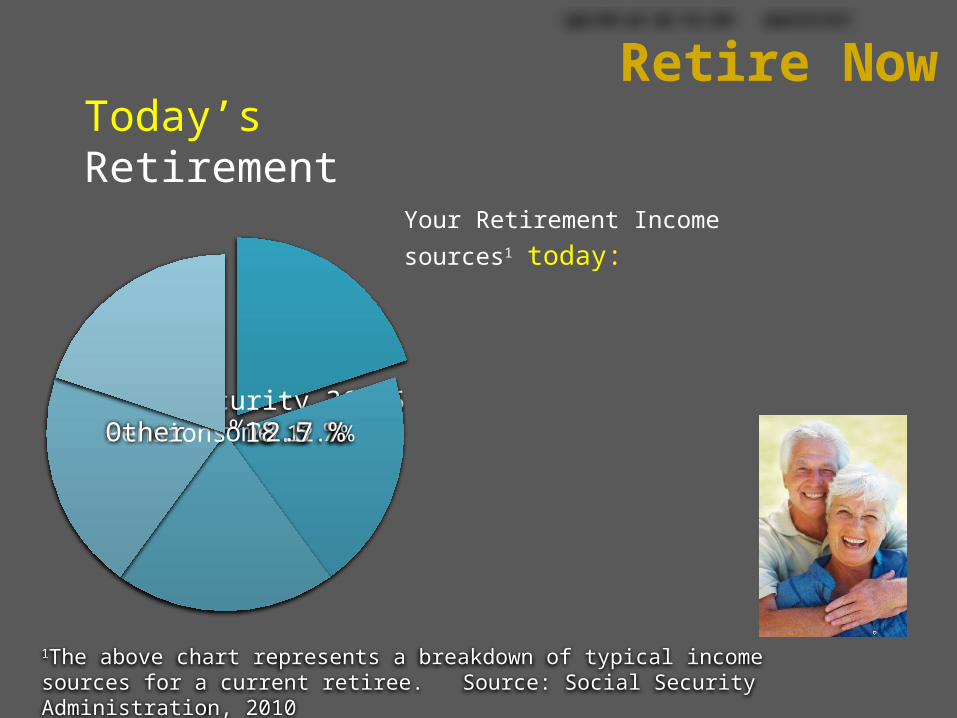

Retire NowToday’s Retirement

Your Retirement Income sources1

today:

Social Security 36. 5 %

Earnings 29.6 %

Asset Income

12.7%

Pensions 18.5 %

Other 2.7 %

1The above chart represents a breakdown of typical income sources for a current retiree. Source: Social Security Administration, 2010

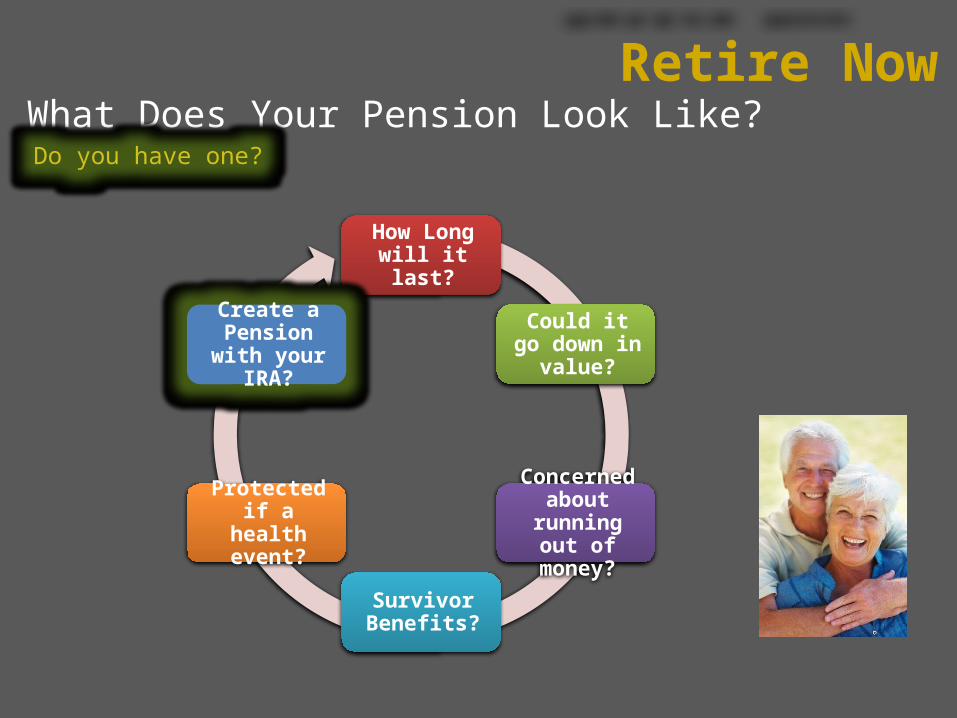

Retire Now

How Long will it last?

Could it go down in value?

Concerned about running out of money?

Survivor Benefits?

Protected if a health event?

Create a Pension with

your IRA?

What Does Your Pension Look Like?Do you have one?

Retire Now

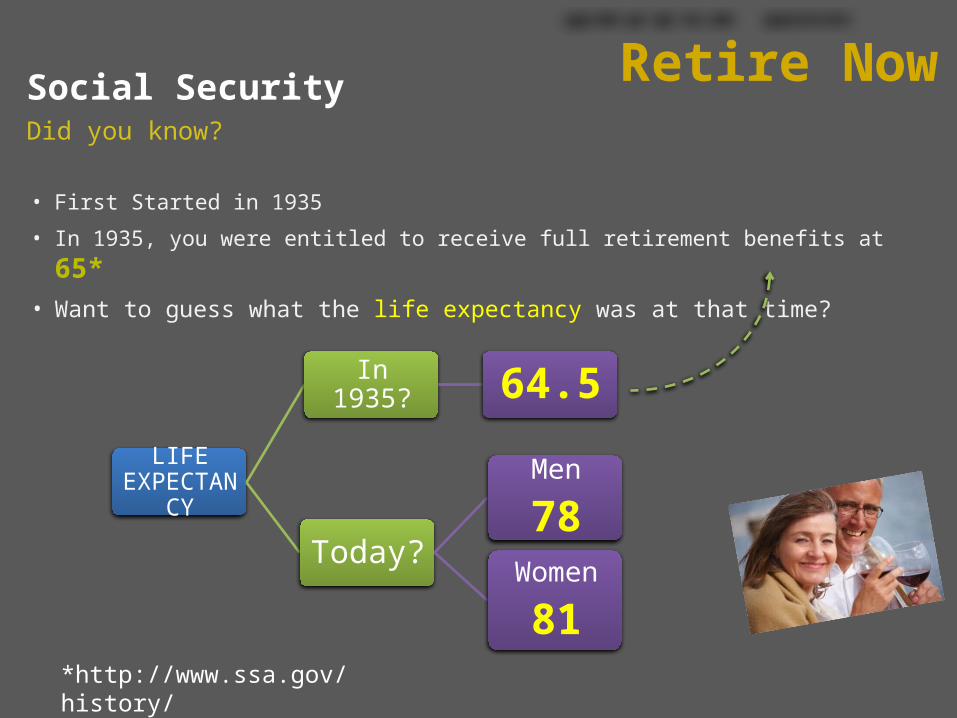

• First Started in 1935

• In 1935, you were entitled to receive full retirement benefits at 65*• Want to guess what the life expectancy was at that time?

Social SecurityDid you know?

LIFE EXPECTANCY

In 1935? 64.5

Today?

Men

78Women

81*http://www.ssa.gov/history/

Retire NowWhy are so many concerned aboutRunning Out of Money?

Procrastination

Don’t want to

Face the problem

Hoping someone will

do it for them

Lack of knowledge as to what’s available

Accumulationvs.

Distribution

No Plan for their money

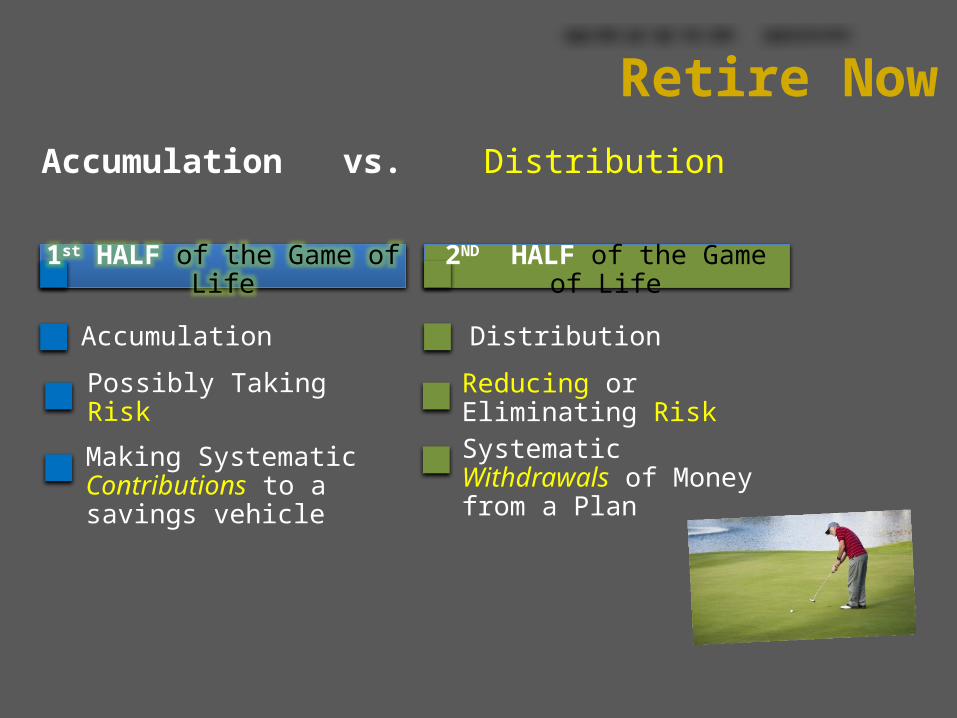

Retire NowAccumulation vs. Distribution

1st HALF of the Game of Life

Accumulation

Possibly Taking Risk

Making Systematic Contributions to a savings vehicle

2ND HALF of the Game of Life

Distribution

Reducing or Eliminating Risk

Systematic Withdrawals of Money from a Plan

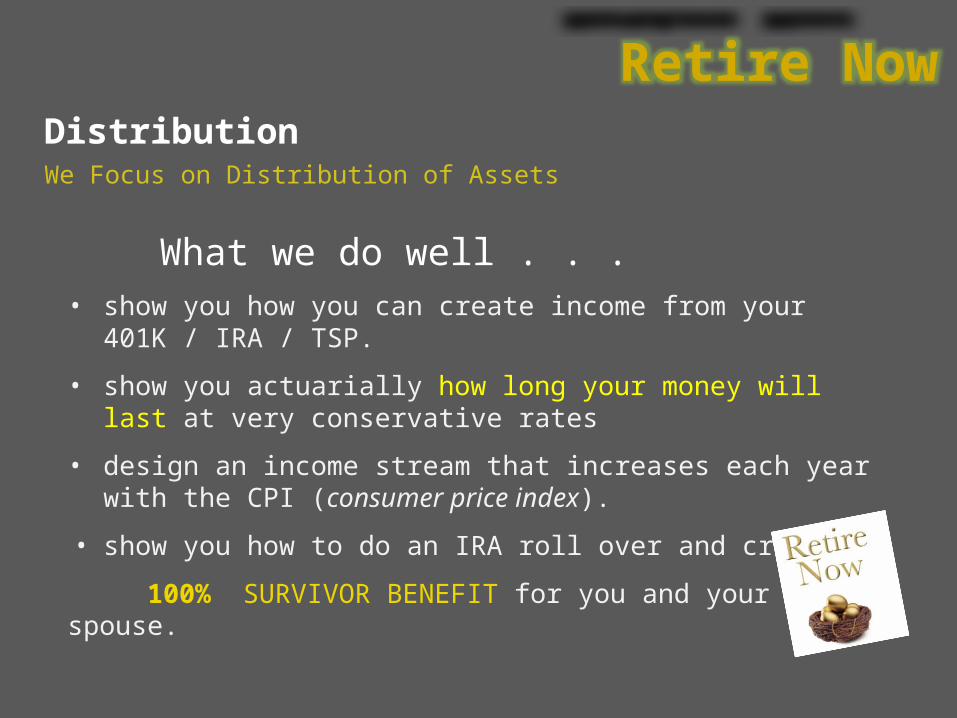

Retire NowDistributionWe Focus on Distribution of Assets

What we do well . . . • show you how you can create income from your 401K /

IRA / TSP.

• show you actuarially how long your money will last at very conservative rates

• design an income stream that increases each year with the CPI (consumer price index).

• show you how to do an IRA roll over and create a

100% SURVIVOR BENEFIT for you and your spouse.

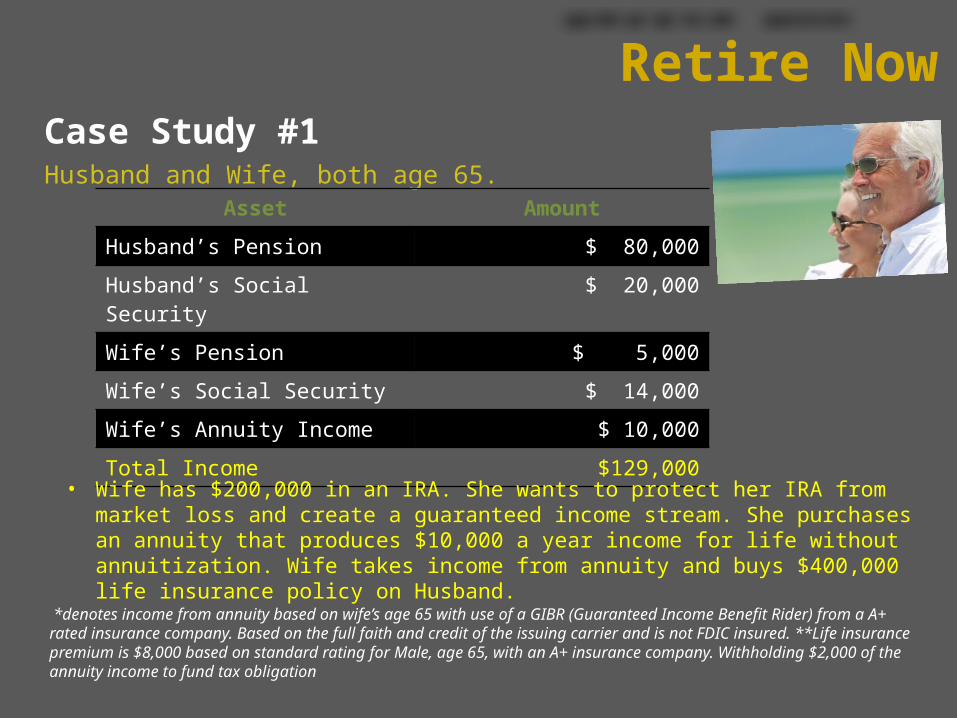

Retire NowCase Study #1Husband and Wife, both age 65.

Asset Amount

Husband’s Pension $ 80,000

Husband’s Social Security $ 20,000Wife’s Pension $ 5,000Wife’s Social Security $ 14,000

Wife’s Annuity Income $ 10,000

Total Income $129,000

• Wife has $200,000 in an IRA. She wants to protect her IRA from market loss and create a guaranteed income stream. She purchases an annuity that produces $10,000 a year income for life without annuitization. Wife takes income from annuity and buys $400,000 life insurance policy on Husband.

*denotes income from annuity based on wife’s age 65 with use of a GIBR (Guaranteed Income Benefit Rider) from a A+ rated insurance company. Based on the full faith and credit of the issuing carrier and is not FDIC insured. **Life insurance premium is $8,000 based on standard rating for Male, age 65, with an A+ insurance company. Withholding $2,000 of the annuity income to fund tax obligation

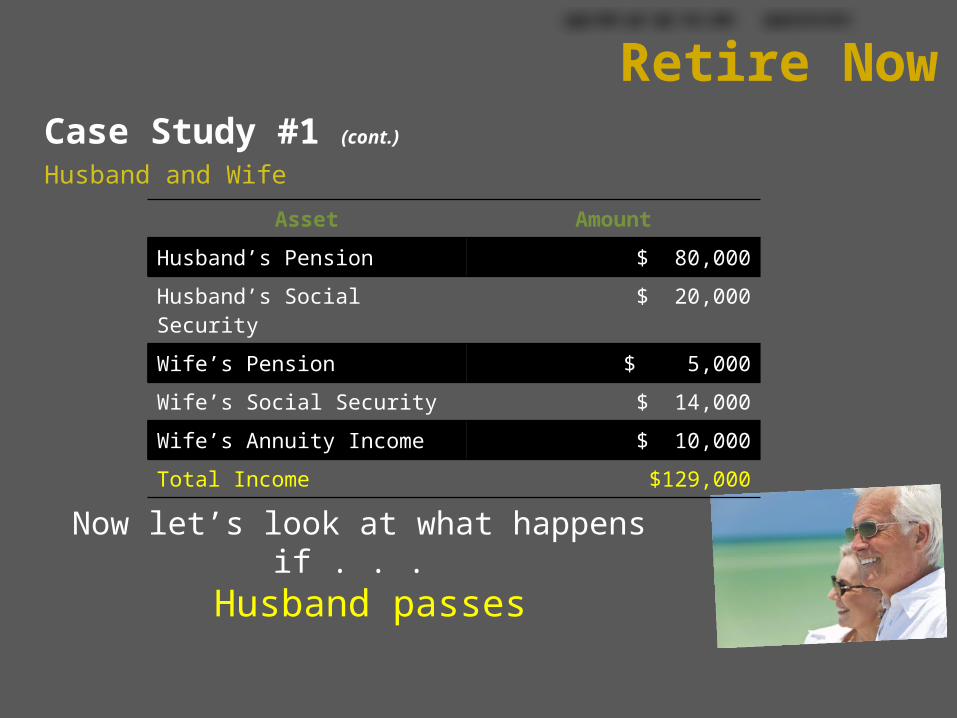

Retire NowCase Study #1 (cont.)Husband and Wife

Asset Amount

Husband’s Pension $ 80,000

Husband’s Social Security $ 20,000

Wife’s Pension $ 5,000Wife’s Social Security $ 14,000

Wife’s Annuity Income $ 10,000

Total Income $129,000

Now let’s look at what happens if . . . Husband passes

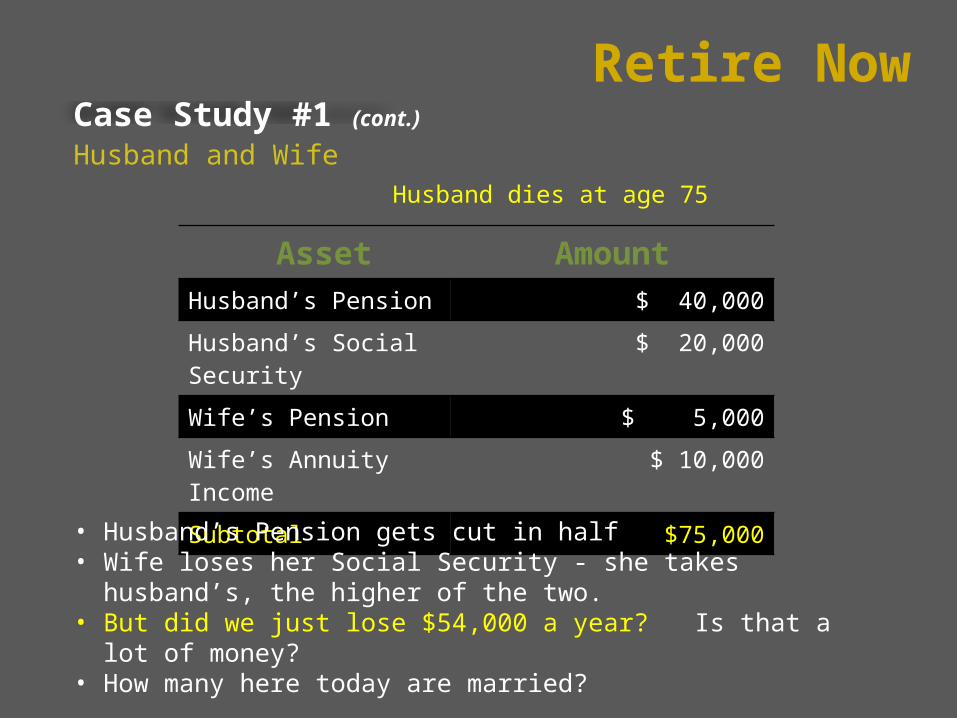

Case Study #1 (cont.)Husband and Wife

Asset AmountHusband’s Pension $ 40,000Husband’s Social Security $ 20,000

Wife’s Pension $ 5,000

Wife’s Annuity Income $ 10,000Subtotal $75,000

Husband dies at age 75

• Husband’s Pension gets cut in half• Wife loses her Social Security - she takes husband’s, the higher of the two.• But did we just lose $54,000 a year? Is that a lot of money?• How many here today are married?

Retire Now

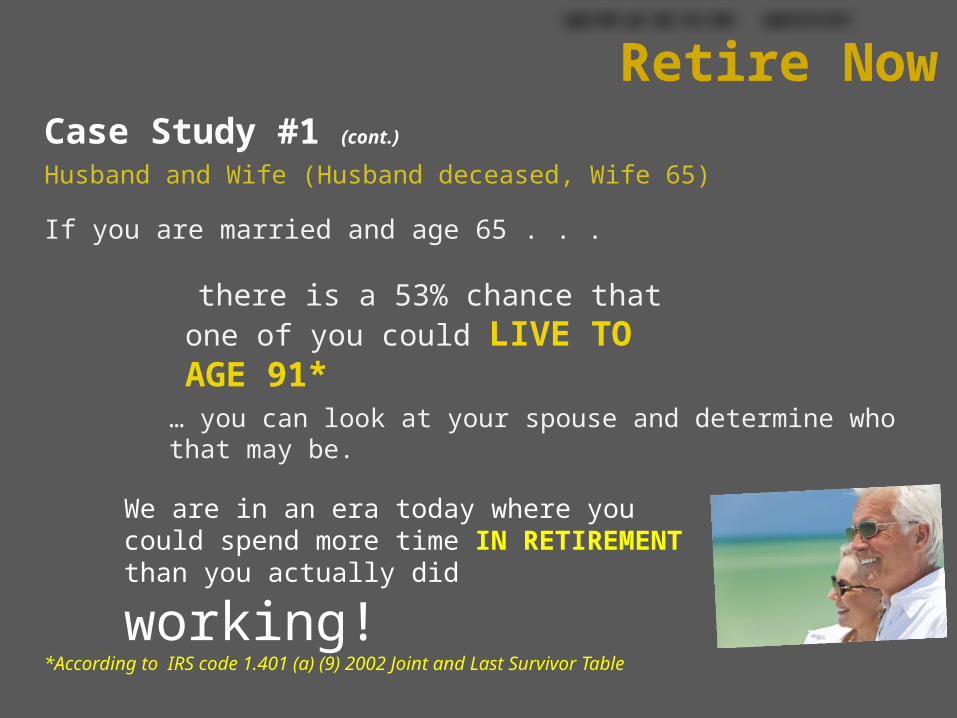

Retire NowCase Study #1 (cont.)Husband and Wife (Husband deceased, Wife 65)

If you are married and age 65 . . .

there is a 53% chance that one of you could LIVE TO AGE 91*

… you can look at your spouse and determine who that may be.

We are in an era today where you could spend more time IN RETIREMENT than you actually did

working!*According to IRS code 1.401 (a) (9) 2002 Joint and Last Survivor Table

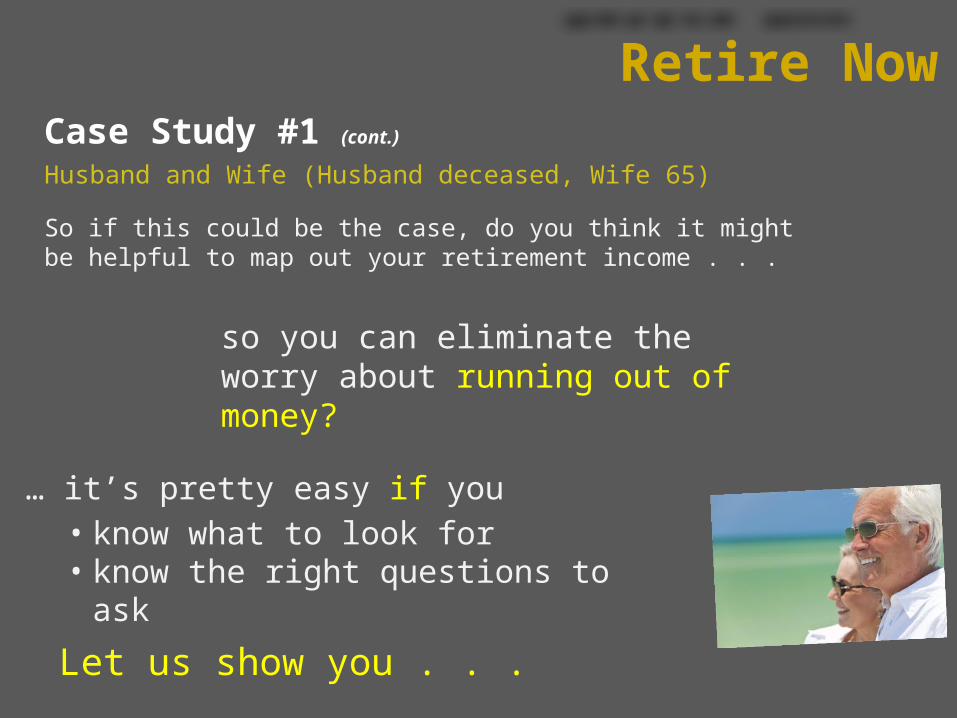

Retire NowCase Study #1 (cont.)Husband and Wife (Husband deceased, Wife 65)

So if this could be the case, do you think it might be helpful to map out your retirement income . . .

so you can eliminate the worry about running out of money?

… it’s pretty easy if you • know what to look for • know the right questions to

askLet us show you . . .

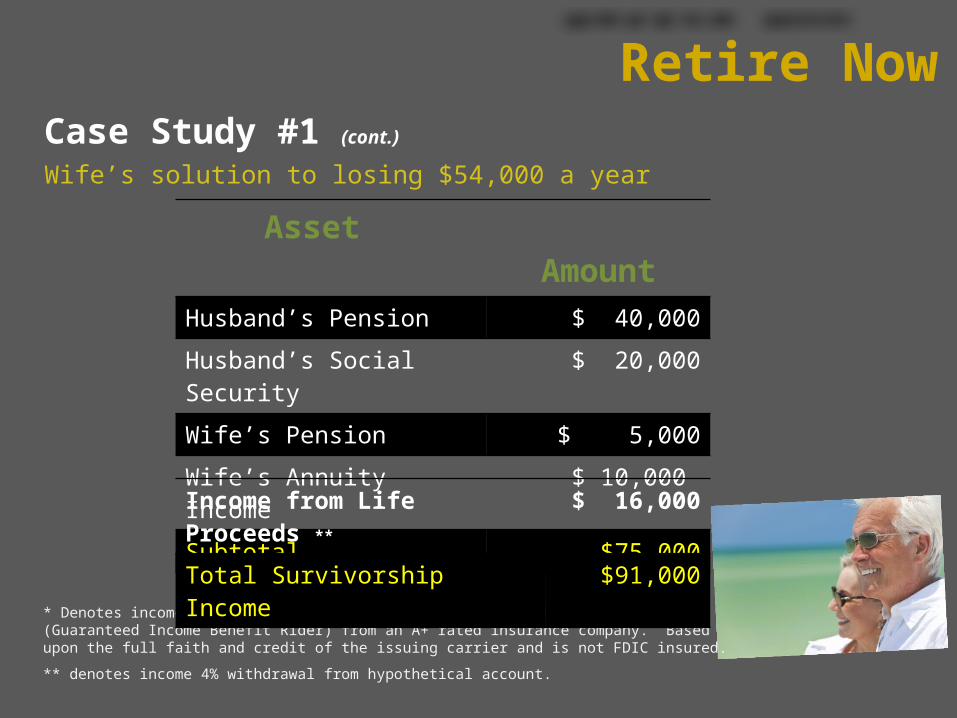

Retire NowCase Study #1 (cont.)Wife’s solution to losing $54,000 a year

* Denotes income from annuity based on Sally's age 65 with use of a GIBR (Guaranteed Income Benefit Rider) from an A+ rated insurance company. Based upon the full faith and credit of the issuing carrier and is not FDIC insured.

** denotes income 4% withdrawal from hypothetical account.

Asset AmountHusband’s Pension $ 40,000

Husband’s Social Security $ 20,000

Wife’s Pension $ 5,000

Wife’s Annuity Income $ 10,000

Subtotal $75,000

Income from Life Proceeds ** $ 16,000

Total Survivorship Income $91,000

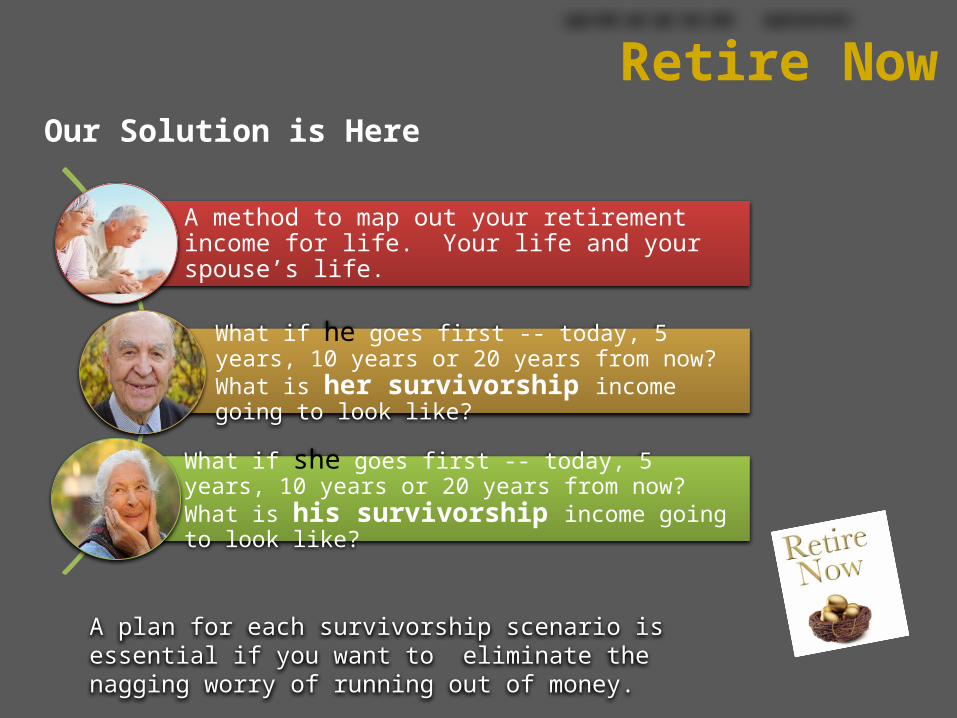

Retire NowOur Solution is Here

A method to map out your retirement income for life. Your life and your spouse’s life.

What if he goes first -- today, 5 years, 10 years or 20 years from now? What is her survivorship income going to look like?

What if she goes first -- today, 5 years, 10 years or 20 years from now? What is his survivorship income going to look like?

A plan for each survivorship scenario is essential if you want to eliminate the nagging worry of running out of money.

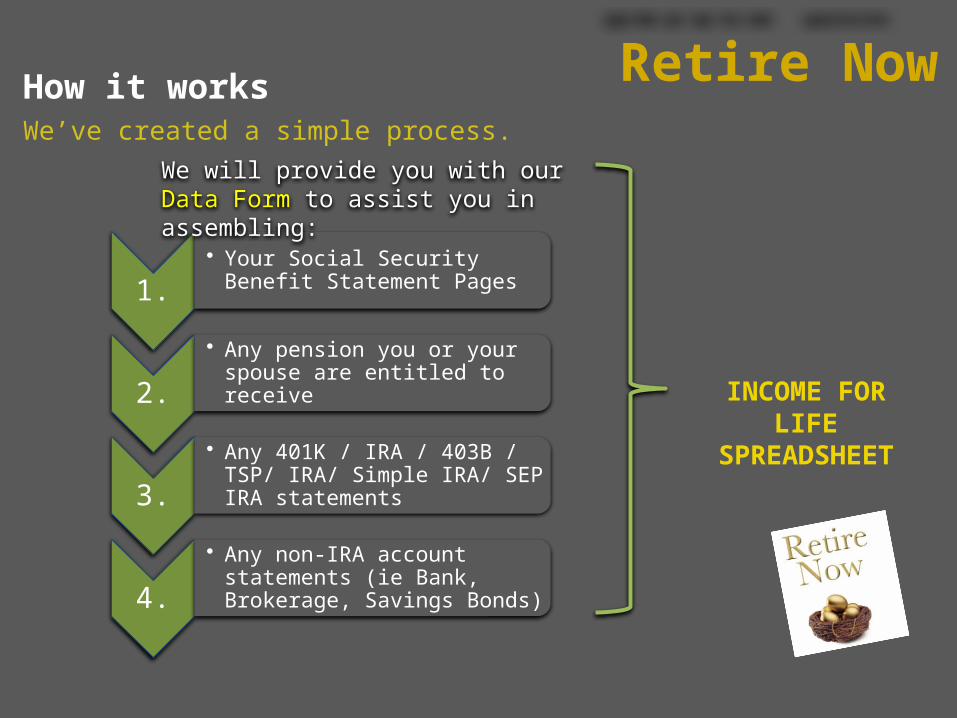

Retire NowHow it worksWe’ve created a simple process.

1.• Your Social Security Benefit

Statement Pages

2.• Any pension you or your spouse are

entitled to receive

3.• Any 401K / IRA / 403B / TSP/ IRA/

Simple IRA/ SEP IRA statements

4.• Any non-IRA account statements (ie

Bank, Brokerage, Savings Bonds)

We will provide you with our Data Form to assist you in assembling:

INCOME FOR LIFE

SPREADSHEET

Retire NowHow it worksYou assemble, we create.

Creating the Income for Life spreadsheet

Many people say they have never seen this easy-to-read-and-follow format

This will start to answer the questions you have had about where your income will likely come in YOUR retirement.

Retire NowCase Study #2Husband and Wife, both age 65.

• Husband and Wife are classic do-it-yourselfers, they manage their own portfolios

• They have recently gone through his father and her mother in a Long Term Care situation

• They have no desire to have that repeated in their lives, watching each of their parents spend down huge sums of their estates

Let’s look at their financial situation. . .

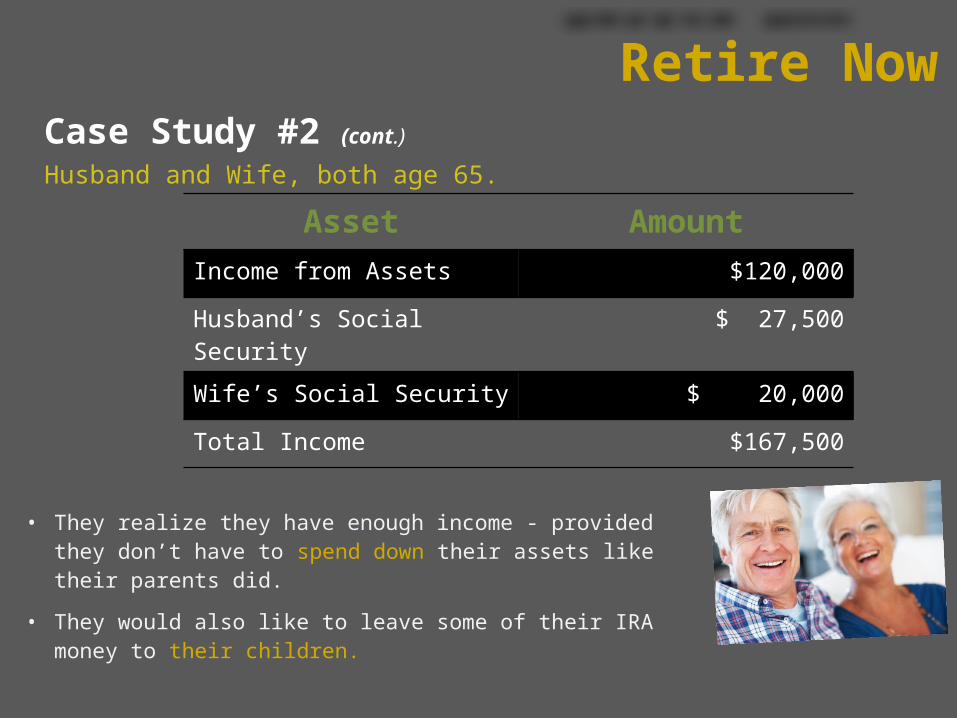

Retire NowCase Study #2 (cont.)Husband and Wife, both age 65.

Asset Amount

Income from Assets $120,000

Husband’s Social Security $ 27,500

Wife’s Social Security $ 20,000

Total Income $167,500

• They realize they have enough income - provided they don’t have to spend down their assets like their parents did.

• They would also like to leave some of their IRA money to their children.

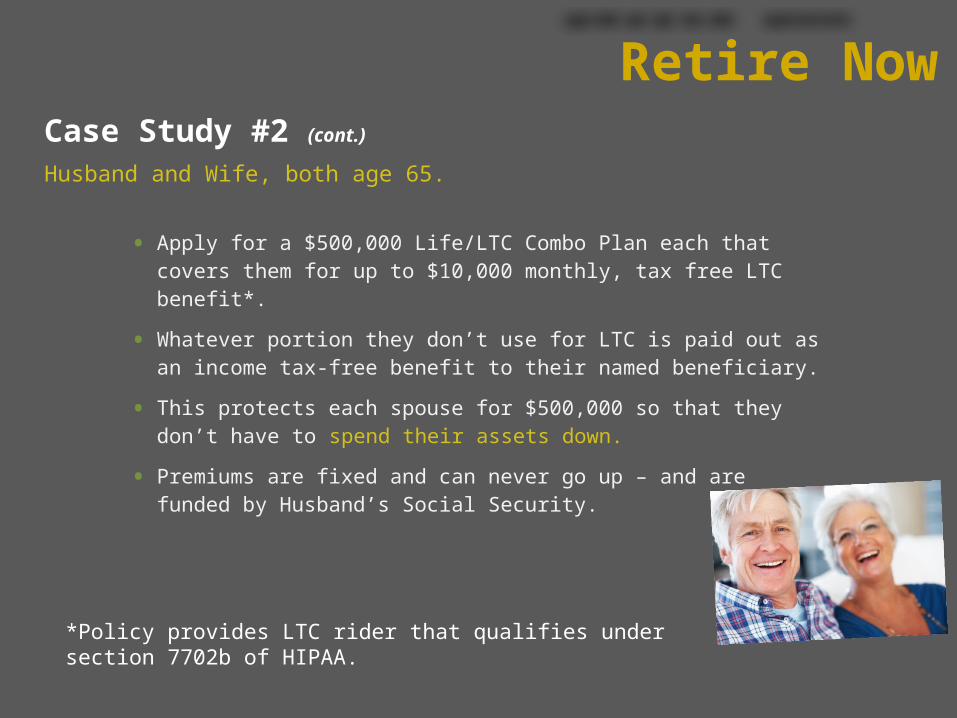

Retire NowCase Study #2 (cont.)Husband and Wife, both age 65.

• Apply for a $500,000 Life/LTC Combo Plan each that covers them for up to $10,000 monthly, tax free LTC benefit*.

• Whatever portion they don’t use for LTC is paid out as an income tax-free benefit to their named beneficiary.

• This protects each spouse for $500,000 so that they don’t have to spend their assets down.

• Premiums are fixed and can never go up – and are funded by Husband’s Social Security.

*Policy provides LTC rider that qualifies under section 7702b of HIPAA.

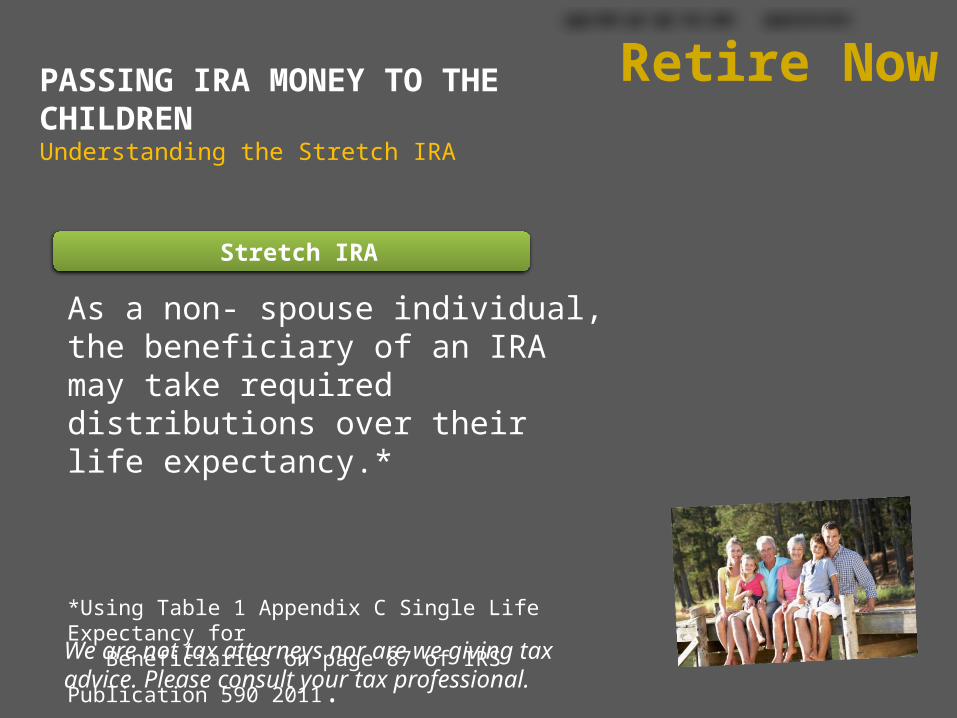

Retire NowPASSING IRA MONEY TO THE CHILDRENUnderstanding the Stretch IRA

Stretch IRA

We are not tax attorneys nor are we giving tax advice. Please consult your tax professional.

As a non- spouse individual, the beneficiary of an IRA may take required distributions over their life expectancy.*

*Using Table 1 Appendix C Single Life Expectancy for

Beneficiaries on page 87 of IRS Publication 590 2011.

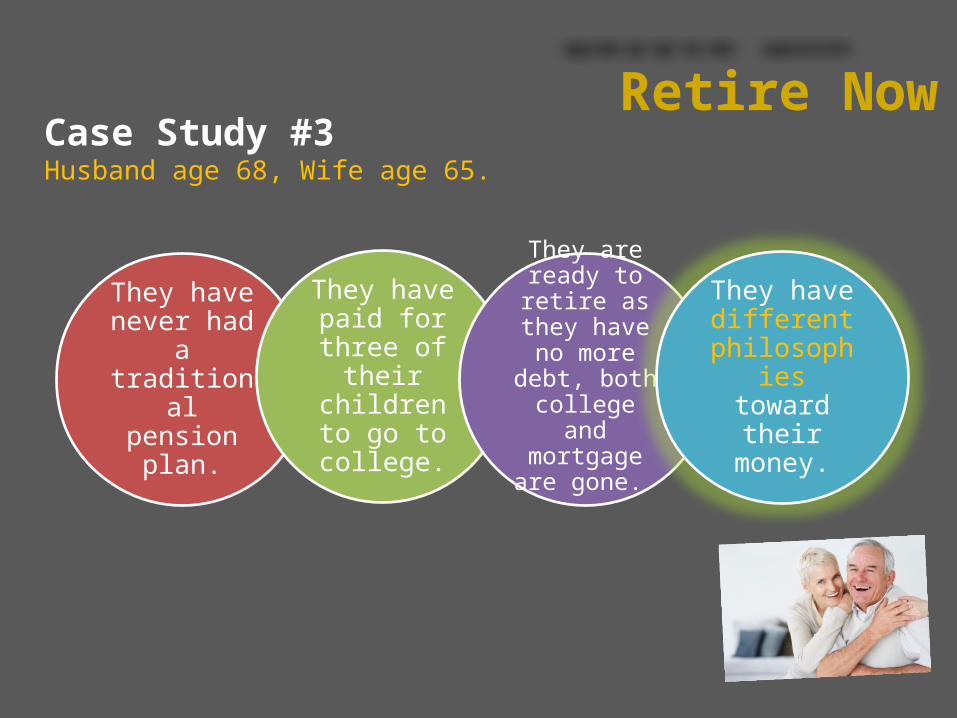

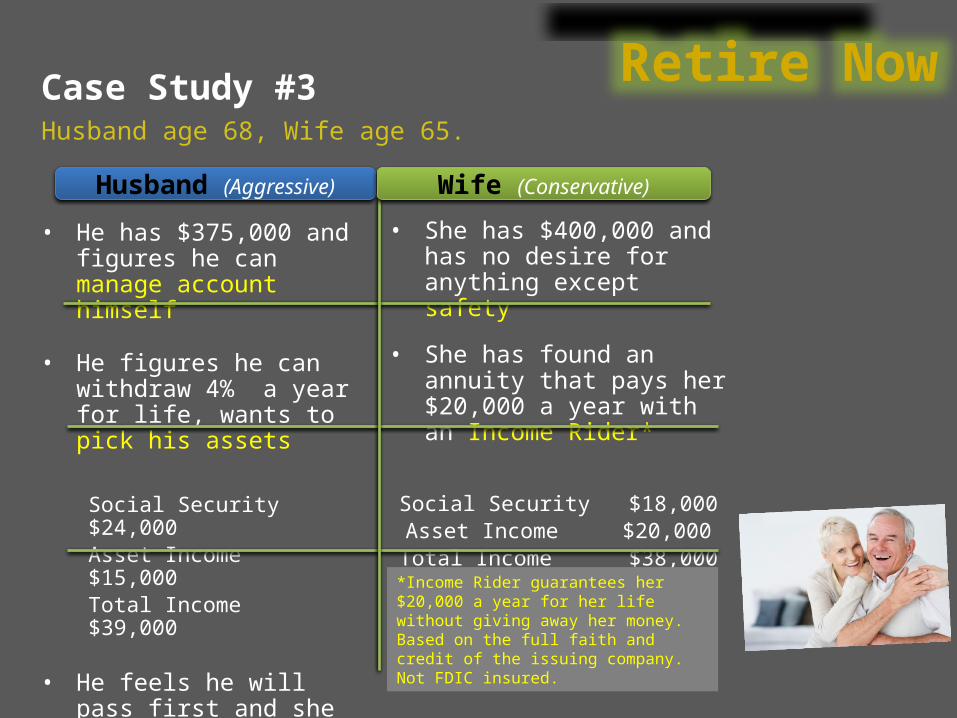

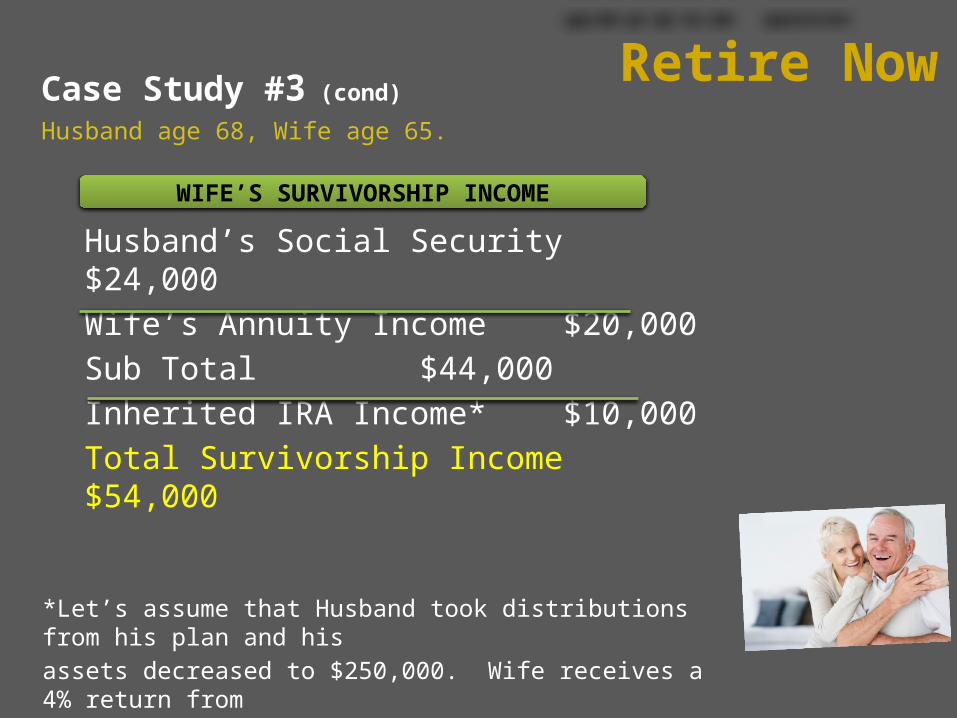

Retire NowCase Study #3Husband age 68, Wife age 65.

They have never had

a traditional pension

plan.

They have paid for three of

their children to

go to college.

They are ready to retire as

they have no more

debt, both college and mortgage

are gone.

They have different

philosophies toward

their money.

Retire Now

• He has $375,000 and figures he can manage account himself

• He figures he can withdraw 4% a year for life, wants to pick his assets

Social Security $24,000Asset Income $15,000Total Income $39,000

• He feels he will pass first and she will get his Social Security since hers is the smaller account.

Case Study #3Husband age 68, Wife age 65.

• She has $400,000 and has no desire for anything except safety

• She has found an annuity that pays her $20,000 a year with an Income Rider*

Social Security $18,000Asset Income $20,000Total Income $38,000

*Income Rider guarantees her $20,000 a year for her life without giving away her money. Based on the full faith and credit of the issuing company. Not FDIC insured.

Husband (Aggressive) Wife (Conservative)

Retire Now

Husband’s Social Security $24,000Wife’s Annuity Income $20,000Sub Total $44,000Inherited IRA Income* $10,000Total Survivorship Income $54,000

*Let’s assume that Husband took distributions from his plan and his assets decreased to $250,000. Wife receives a 4% return from a hypothetical account.

WIFE’S SURVIVORSHIP INCOME

Case Study #3 (cond)

Husband age 68, Wife age 65.

Retire NowCaring for a Parent or ChildWith Special Needs

• Nearly 1/3 of retirees still have at least one parent living and that may have a huge bearing as to when and where we retire.

• Many people may also have a child that has a special needs situation.

• Often times it is recommended to have a Special Needs Trust* initiated with specific language that will insure the person in question is properly cared for.

* Please contact your personal attorney to create a Special Needs Trust.

Retire Now

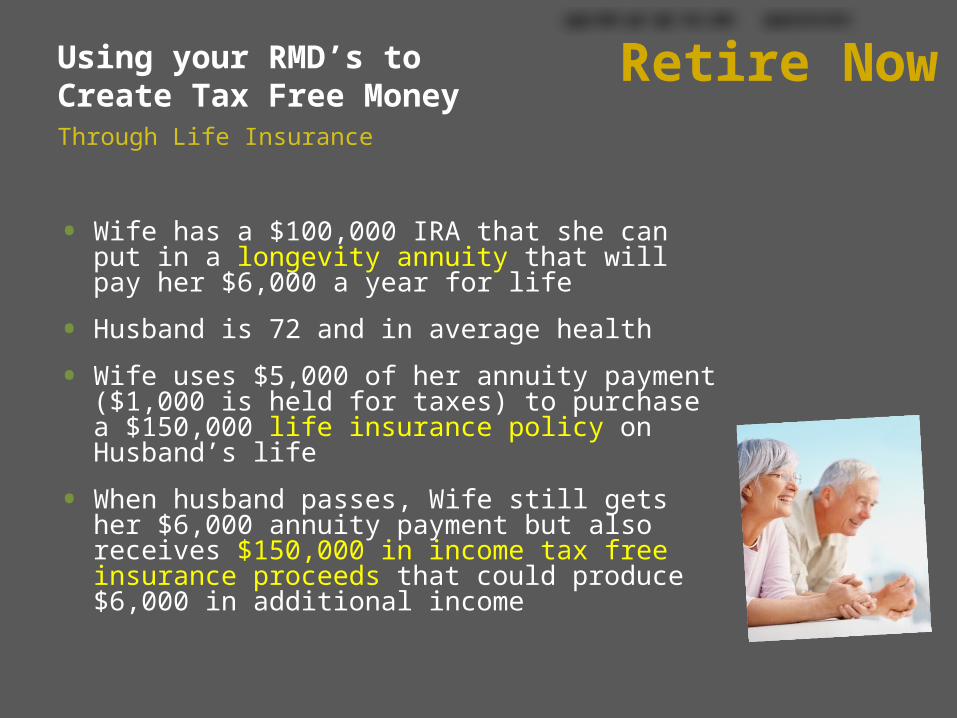

• Wife has a $100,000 IRA that she can put in a longevity annuity that will pay her $6,000 a year for life

• Husband is 72 and in average health

• Wife uses $5,000 of her annuity payment ($1,000 is held for taxes) to purchase a $150,000 life insurance policy on Husband’s life

• When husband passes, Wife still gets her $6,000 annuity payment but also receives $150,000 in income tax free insurance proceeds that could produce $6,000 in additional income

Using your RMD’s to Create Tax Free MoneyThrough Life Insurance

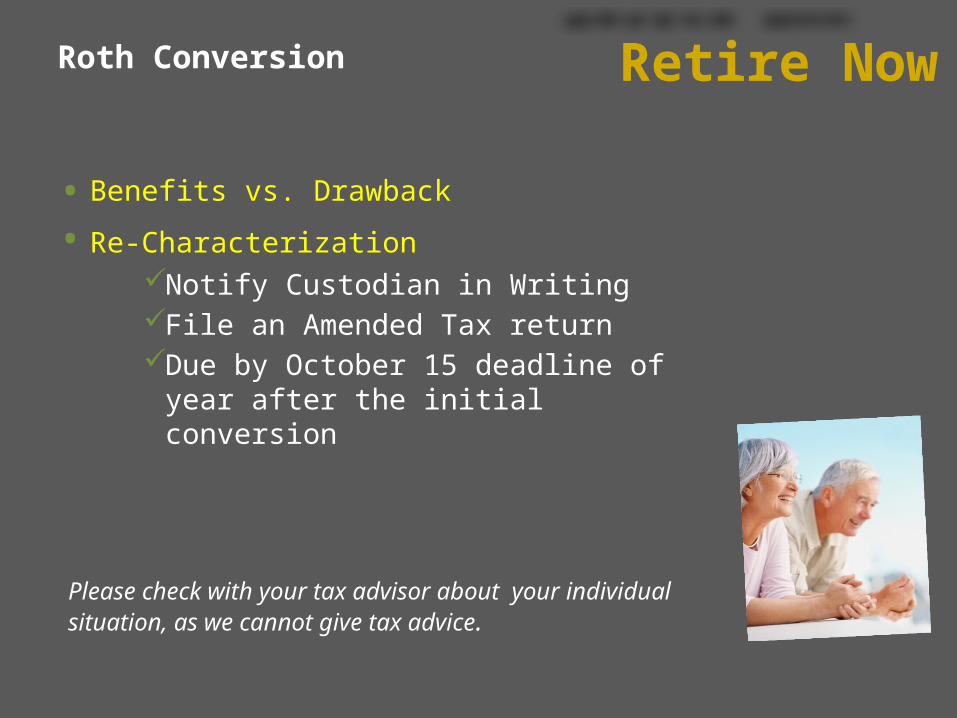

Retire NowRoth Conversion

• Benefits vs. Drawback

• Re-CharacterizationNotify Custodian in WritingFile an Amended Tax returnDue by October 15 deadline of year after

the initial conversion

Please check with your tax advisor about your individual situation, as we cannot give tax advice.

Retire Now

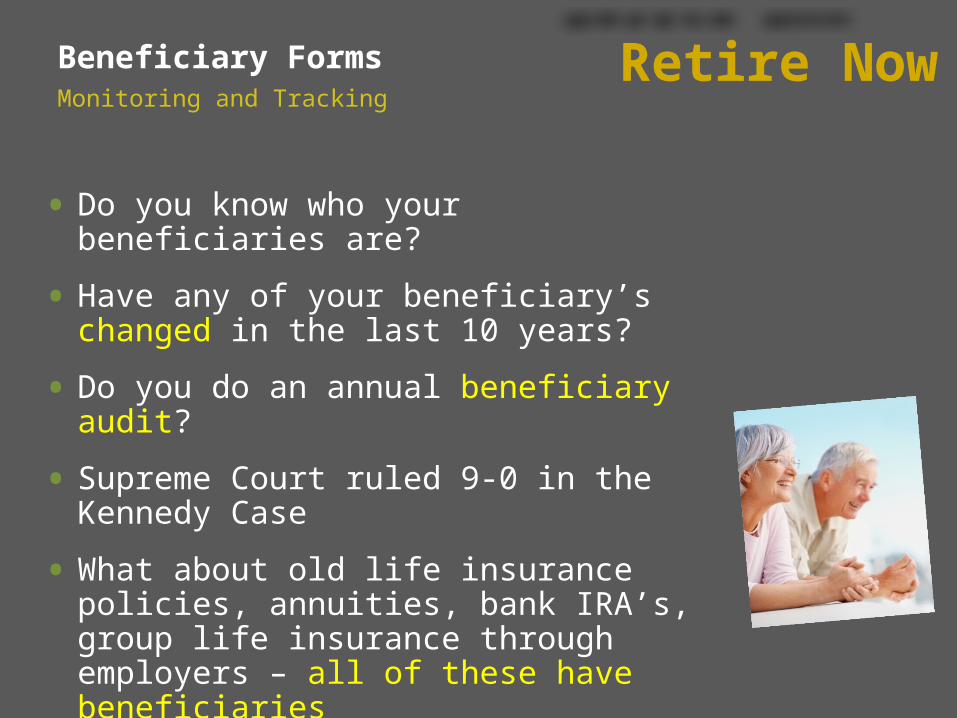

• Do you know who your beneficiaries are?

• Have any of your beneficiary’s changed in the last 10 years?

• Do you do an annual beneficiary audit?

• Supreme Court ruled 9-0 in the Kennedy Case

• What about old life insurance policies, annuities, bank IRA’s, group life insurance through employers – all of these have beneficiaries

Beneficiary FormsMonitoring and Tracking

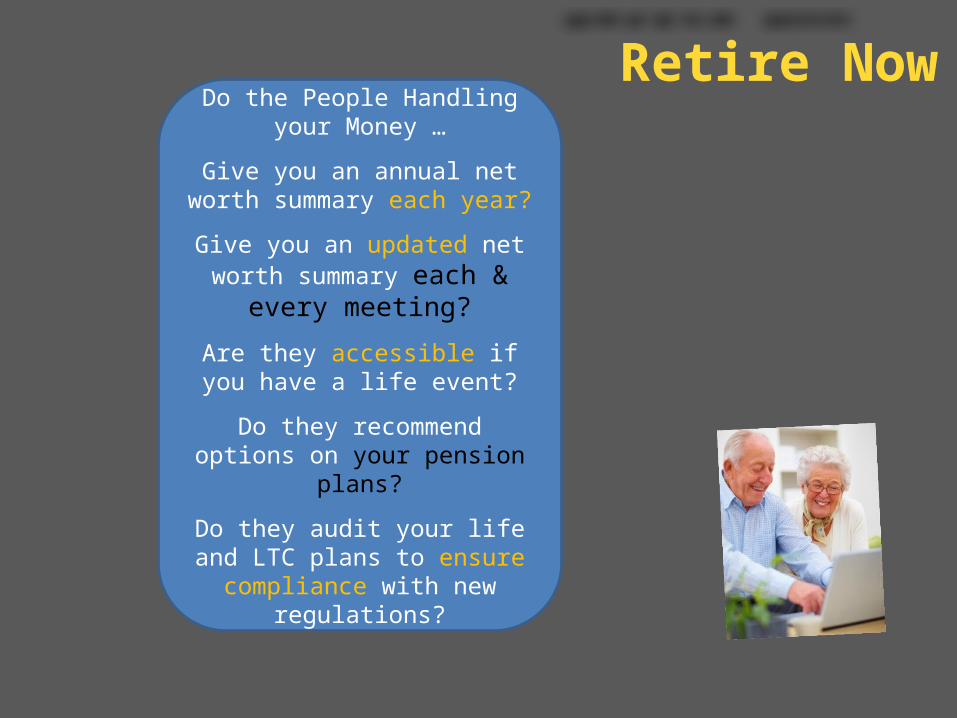

Do the People Handling your Money …

Give you an annual net worth summary each year?

Give you an updated net worth summary each & every

meeting?

Are they accessible if you have a life event?

Do they recommend options on your pension plans?

Do they audit your life and LTC plans to ensure compliance with

new regulations?

Retire Now

Retire Now

Your Needs, Goals, Desires

PLAN A

Protect Her Money He Self-Manages

PLAN B

Protect Her Money Protect Some of His He Self-Manages Some

PLAN C

Protect Some Money Client Self-Manages Some Look at Health Care Event Life/LTC Combo

How We Assist YouDetermining Your Needs, Goals, Desires

Retire NowYour Next Step Letting Us Know If We Can Be Of Help

Please fill out our evaluation form

Decide for yourselves if there is an indication of interest

If yes, you will receive this special package that explains the items you would need to bring in for your complimentary initial consultation

There is no charge for an initial consultation if you have attended this seminar

A staff member will be in the back or will visit your table to set up an initial consultation.

Retire NowYour Next Step (cont.)Letting Us Know If We Can Be Of Help

If you are setting up a consultation today, we would like to leave you with your RETIRE NOW KIT.

It contains our folder with informative reading materials

We look forward to meeting you soon at our office.

With a packet to help you organize

Retire NowWhat To ExpectWhen you visit us

We will meet for less than 60 minutes

We never do business on an initial meeting

We will discuss your situation

We will show you on our Flat Screen what you could expect if we design a plan for you

We look forward to showing you how to structure your retirement income.

Thank you!