CYPRUS TOURISM STRATEGY Elasticity of Demand 1,30 1,00 0,70 0,50 Price Elasticity of Demand 1,30...

53

CYPRUS TOURISM STRATEGY CYPRUS TOURISM STRATEGY Stakeholder presentation Nicosia, October 3, 2017 Jörn Gieschen 1

-

Upload

nguyenminh -

Category

Documents

-

view

224 -

download

0

Transcript of CYPRUS TOURISM STRATEGY Elasticity of Demand 1,30 1,00 0,70 0,50 Price Elasticity of Demand 1,30...

CYPRUS TOURISM STRATEGY

CYPRUS TOURISMSTRATEGYStakeholder presentation

Nicosia, October 3, 2017

Jörn Gieschen

1

CYPRUS TOURISM STRATEGY

2

Not another one for the bookshelves, please!

CYPRUS TOURISM STRATEGY

3

Two central pillars for strategy success

Participation

System

Implementation

System

CYPRUS TOURISM STRATEGY

4

Ministry of Energy, Commerce, Tourism

and Industry

Cyprus Tourism Organization

Hermes Airports

Ambitious, knowledgeable, and caring partners

CYPRUS TOURISM STRATEGY

5

An intensive ongoing participatory process

33

One-to-one Interviews

• 33 interviews to selected

stakeholders, covering private

and public sectors, such as:

⌐ Government

⌐ Regional & local authorities

⌐ Chambers of Commerce

⌐ Museums & leisure entities

⌐ Professional associations

⌐ Universities

⌐ Accommodation

⌐ Developers & Investors

⌐ Tour Operators

⌐ Etc.

17

Workshops

(114 participants)

2 Types:

• Territorial workshops, one per

region

• Sectorial workshops

⌐ Accommodation

⌐ F&B

⌐ Airlines

⌐ Historic & cultural heritage

⌐ Natural preservation areas

⌐ Travel agencies & operators

⌐ Handicraft & local products

⌐ MICE

⌐ Wineries

⌐ Tourism planners and

managers

Working sessions &

questionnaires to

Offices abroad

• Project Management Team

sessions

• Sounding Board sessions

• The CTO (1 week-long session)

Additionally…

• Online questionnaires to CTO

offices abroad.

Site inspection trip

• The field visit was a key

element of the research

phase, as it provided the team

with an overall picture of

Cyprus and an understanding

of how Cyprus performs as a

tourism destination

CYPRUS TOURISM STRATEGY

6

External Analysis – More interviews

Secondary Market Research

•European Travel Monitor /Behavior

•WEF Competitiveness Index

•17 Countries & 7 segments reports

Interviews with collaborators:

airlines and tour operators

•31 tour operators in 5 selected source markets.

•10 airlines in main source and key markets.

Consumer Survey

in selected source markets

•1.700 interviews in 5 countries

•Brand Adoption Process Research

CYPRUS TOURISM STRATEGY

7

Two central pillars for strategy success

Participation

System

Implementation

System

CYPRUS TOURISM STRATEGY

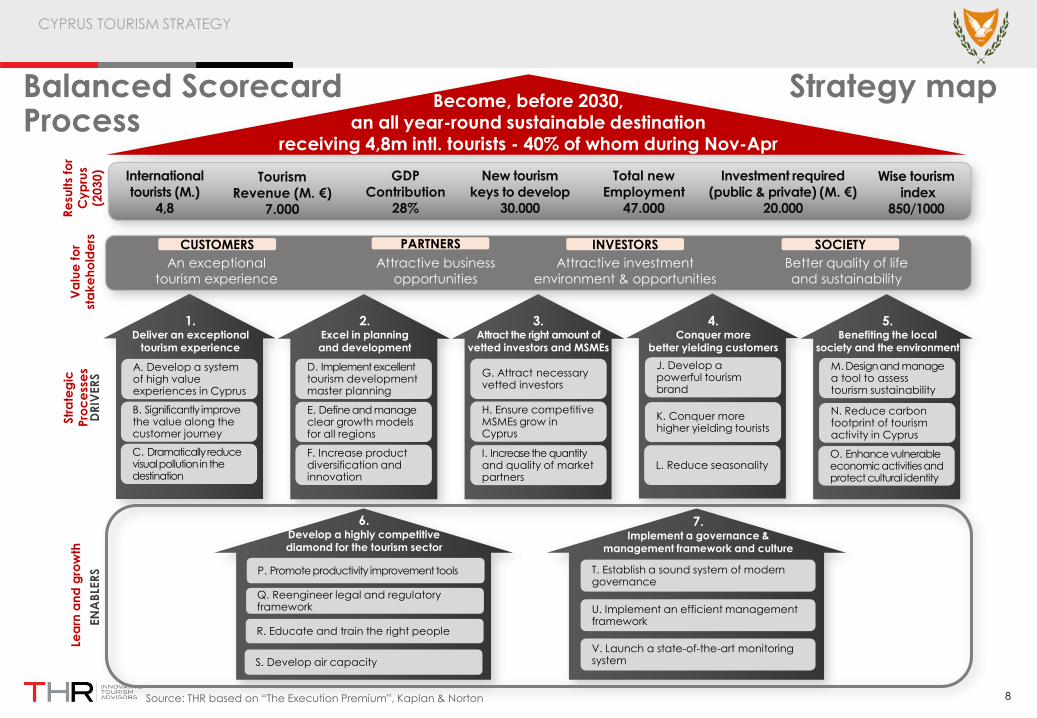

Source: THR based on “The Execution Premium”, Kaplan & Norton 8

Balanced Scorecard Strategy mapProcess

1.Deliver an exceptional

tourism experience

B. Significantly improve the value along the customer journey

C. Dramatically reduce visual pollution in the destination

A. Develop a system of high value experiences in Cyprus

Lea

rn a

nd

gro

wth

Str

ate

gic

P

roc

ess

es

DR

IVER

SEN

AB

LER

S

2.Excel in planningand development

D. Implement excellent tourism development master planning

E. Define and manage clear growth models for all regions

F. Increase product diversification and innovation

6.Develop a highly competitive diamond for the tourism sector

Q. Reengineer legal and regulatory framework

R. Educate and train the right people

P. Promote productivity improvement tools

7.Implement a governance &

management framework and culture

T. Establish a sound system of modern governance

U. Implement an efficient management framework

V. Launch a state-of-the-art monitoring system

3. Attract the right amount of

vetted investors and MSMEs

H. Ensure competitive MSMEs grow in Cyprus

I. Increase the quantity and quality of market partners

G. Attract necessary vetted investors

4.Conquer more

better yielding customers

K. Conquer more higher yielding tourists

J. Develop a powerful tourism brand

L. Reduce seasonality

Become, before 2030,an all year-round sustainable destination

receiving 4,8m intl. tourists - 40% of whom during Nov-Apr

Va

lue

fo

rst

ak

eh

old

ers

An exceptional

tourism experience

Attractive investment

environment & opportunities

Better quality of life

and sustainability

Attractive business

opportunities

CUSTOMERS PARTNERS SOCIETYINVESTORS

Re

sults

for

Cy

pru

s (2

03

0)

Tourism

Revenue (M. €)7.000

Wise tourism

index850/1000

GDP

Contribution28%

Total new

Employment47.000

New tourism

keys to develop30.000

Investment required

(public & private) (M. €)20.000

International

tourists (M.)4,8

5.Benefiting the local

society and the environment

N. Reduce carbon footprint of tourism activity in Cyprus

M. Design and manage a tool to assess tourism sustainability

O. Enhance vulnerable economic activities and protect cultural identity

S. Develop air capacity

CYPRUS TOURISM STRATEGY

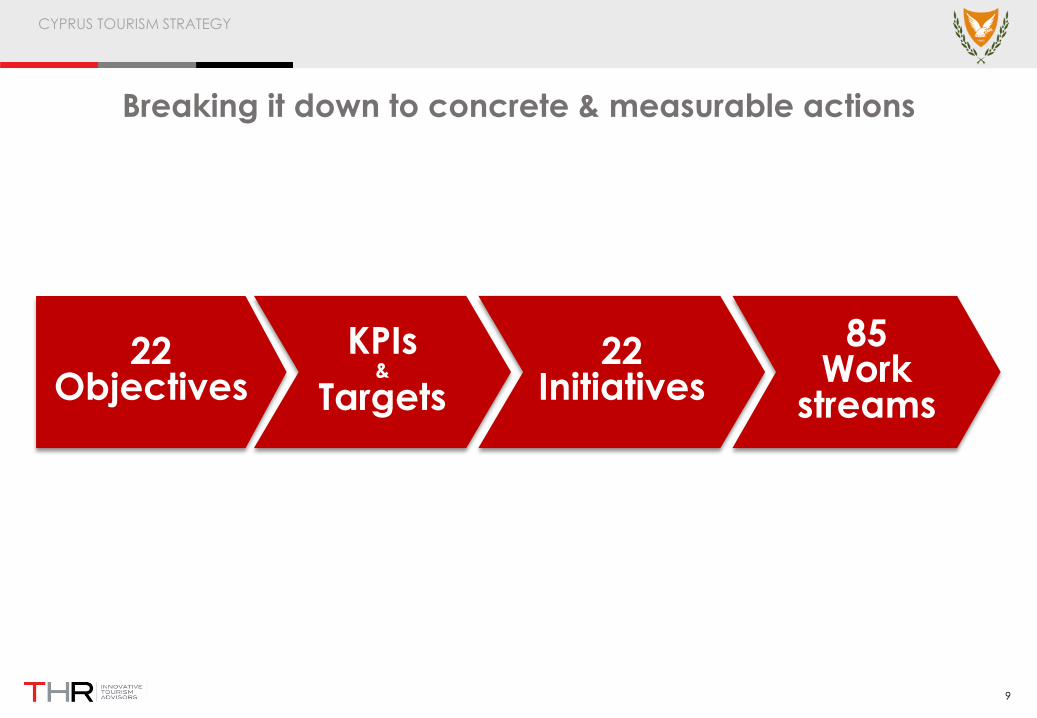

9

Breaking it down to concrete & measurable actions

22Objectives

KPIs&

Targets

22 Initiatives

85Work

streams

CYPRUS TOURISM STRATEGY

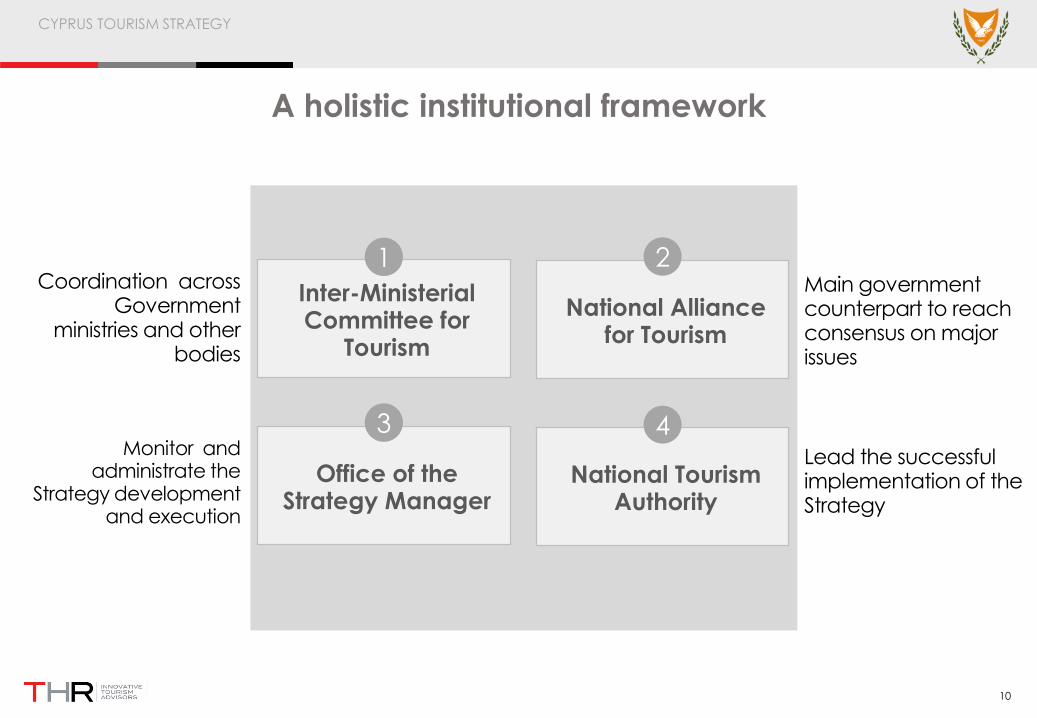

10

A holistic institutional framework

Coordination across Government

ministries and other bodies

Inter-Ministerial Committee for

Tourism

Office of theStrategy Manager

1

3Monitor and

administrate the Strategy development

and execution

National Alliance for Tourism

2Main government counterpart to reach consensus on major issues

National Tourism Authority

4Lead the successful implementation of the Strategy

CYPRUS TOURISM STRATEGY

11

Tourism vision 2030

Becoming, before 2030,

an all year-round

sustainable “premium”

destination

receiving 4,8m intl.

tourists - 40% of whom

between Nov-Apr

CYPRUS TOURISM STRATEGY

12

A sophisticated Simulation Platform has been developed

The simulation

model is a

comprehensive

platform in which

the principal tourism

figures and

macroeconomic

impacts are

projected for 2030

1. CYPRUS TOURIST BEHAVIOUR ASSUMPTIONS BY PURPOSE OF VISIT (2030)

A. INTERNATIONAL TOURISTS

A1. PLEASURE A3. VISIT FRIENDS AND RELATIVES

Behaviour Variables Low Cost Mass Affluent Luxury Behaviour Variables Low Cost Mass Affluent Luxury

Average Length of Stay 9,5 9,5 9,5 10,0 Average Length of Stay 12,0 15,0 18,0 21,0

Average Expenditure / Day 78,75 105,00 157,50 420,00 Average Expenditure / Day 37,88 50,50 75,75 126,25

Price Elast icity of Demand 1,30 1,00 0,70 0,50 Price Elast icity of Demand 1,30 1,00 0,70 0,50

% Usage of Tourism Accomod. 70% 70% 75% 75% % Usage of Tourism Accomod. 0% 0% 3% 5%

Double Occupancy Rate 1,85 1,85 1,85 1,85 Double Occupancy Rate 1,85 1,85 1,85 1,85

A2. BUSINESS A4. DAY VISITORS

Behaviour Variables Low Cost Mass Affluent Luxury Behaviour Variables Low Cost Mass Affluent Luxury

Average Length of Stay 4,0 4,5 4,5 5,0 Average Length of Stay 1,0 1,0 1,0 1,0

Average Expenditure / Day 130,50 145,00 290,00 580,00 Average Expenditure / Day 37,88 50,50 75,75 126,25

Price Elast icity of Demand 1,30 1,00 0,70 0,50 Price Elast icity of Demand 1,30 1,00 0,70 0,50

% Usage of Tourism Accomod. 95% 95% 100% 100% % Usage of Tourism Accomod. 0% 0% 0% 0%

Double Occupancy Rate 1,10 1,10 1,10 1,10 Double Occupancy Rate 1,00 1,00 1,00 1,00

B. DOMESTIC TOURISTS

B1. DOMESTIC

Behaviour Variables Low Cost Mass Affluent Luxury

Average Length of Stay 5,5 6,0 6,0 6,5

Average Expenditure per Day 35,20 44,00 66,00 132,00 Calculat ions:

Price Elast icity of Demand 1,20 1,00 0,80 0,60 Price elasticity in absolute value

% Usage of Tourism Accomod. 35% 40% 40% 40% E = dQ/dP

Double Occupancy Rate (DOR) 1,85 1,85 1,85 1,85

Segment by Degree of Sophistication

Segment by Degree of Sophistication Segment by Degree of Sophistication

Segment by Degree of Sophistication

Segment by Degree of Sophistication

2. CVP POSITIONING STRATEGY OF CYPRUS (2030)

A. INTERNATIONAL TOURISTS

A1. PLEASURE A3. VISIT FRIENDS AND RELATIVES

Market Segments Structure Market Segments Structure

Low Cost Market 20% 10% 5% Low Cost Market 20% 10% 5%

Mass Market 50% 20% 10% Mass Market 50% 20% 15%

Affluent Market 25% 55% 60% Affluent Market 25% 55% 60%

Luxury Market 5% 15% 25% Luxury Market 5% 15% 20%

100% 100% 100% 100% 100% 100%

A2. BUSINESS A4. DAY VISITORS

Market Segments Structure Market Segments Structure

Low Cost Market 20% 10% 5% Low Cost Market 20% 10% 5%

Mass Market 50% 20% 10% Mass Market 50% 20% 15%

Affluent Market 25% 55% 60% Affluent Market 25% 55% 60%

Luxury Market 5% 15% 25% Luxury Market 5% 15% 20%

100% 100% 100% 100% 100% 100%

B. DOMESTIC TOURISTS

B1. DOMESTIC

Market Segments Structure

Low Cost Market 30% 25% 20%

Mass Market 40% 40% 40%

Affluent Market 25% 30% 35%

Luxury Market 5% 5% 5%

100% 100% 100%

World

AveragePremium High-End

World

AveragePremium High-End

CVP Positioning Strategy CVP Positioning Strategy

Premium High-EndWorld

Average

World

AveragePremium High-End

CVP Positioning Strategy CVP Positioning Strategy

CVP Positioning Strategy

Premium High-EndWorld

Average

8. PROJECTED DEMAND & ROOM NIGHTS (2030)

Purpose of Visit World Av. Premium High-end

International 5.834.401 4.848.804 4.374.634

Pleasure 4.887.195 4.062.143 3.648.205

Business 323.520 259.401 232.130

VFR 367.017 310.274 290.877

Day Visitors 256.670 216.987 203.422

Domestic 1.406.745 1.365.611 1.324.477

Total 7.241.147 6.214.415 5.699.111

-1.026.731 -1.542.036

Purpose of Visit World Av. Premium High-end

International 19.126.680 16.388.633 14.987.393

Pleasure 17.858.666 15.287.087 13.958.038

Business 1.239.118 1.032.762 949.577

VFR 28.895 68.784 79.778

Day Visitors 0 0 0

Domestic 1.681.871 1.653.014 1.624.156

Total 20.808.551 18.041.647 16.611.549

-2.766.904 -4.197.002 Difference from World Average

A. PROJECTED TOURISM ARRIVALS

B. TOURISM ACCOMMODATION ROOM NIGHTS

CVP Positioning Strategy

CVP Positioning Strategy

Difference from World Average

0

1.000.000

2.000.000

3.000.000

4.000.000

5.000.000

6.000.000

7.000.000

8.000.000

World Av. Premium High-end

Projected Tourism Arrivals

Domestic

Day Visitors

VFR

Business

Pleasure

0

5.000.000

10.000.000

15.000.000

20.000.000

25.000.000

World Av. Premium High-end

Tourism Accommodation Room Nights

Domestic

Day Visitors

VFR

Business

Pleasure

9. REQUIRED ACCOMMODATION (2030)

Accom. Cat egory World Av. Premium High-end

Hotels / Hotel Apart. 74.203 66.690 64.293

5* Grand Luxury 742 1.667 3.215

5* 10.388 18.340 22.503

4* 29.681 23.342 22.503

3* 33.391 23.342 16.073

Inns 5.429 3.138 2.167

Comfort 2.715 2.040 1.517

Basic (Economy) 2.715 1.098 650

Special Lodging 8.144 6.277 4.334

Enhanced Comfort 2.036 1.883 1.734

Comfort 2.850 3.138 1.734

Basic (Economy) 3.258 1.255 867

Guest Houses 1.810 1.569 722

Enhanced Comfort 452 471 289

Comfort 633 628 289

Basic (Economy) 724 471 144

Campsites 905 785 722

Enhanced Comfort 226 235 289

Comfort 317 353 361

Basic (Economy) 362 196 72

Total keys 90.492 78.459 72.240

- Current licensed keys -48.144 -48.144 -48.144

Net Total to be developed 42.348 30.315 24.096

-12.033 -18.252

CVP Positioning Strategy

A. TOURISM ACCOMMODATION KEYS REQUIRED

Difference from World Average

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

World Av. Premium High-end

Hotel Keys Required

3*

4*

5*

5* Grand

Luxury

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

World Av. Premium High-end

Other Accommodation Keys Required

Inns

Campsites

Guest Houses

Special

Lodging

INPUTS

OUTPUTS

CYPRUS TOURISM STRATEGY

13

3 different growth models for Cyprus

“Standard” model

Aiming to maximise the full growth potential.This model attracts a

higher number of tourists, although not of

revenues (as lower expenditure tourists are

targeted).

A“Premium & wise growth” model

Focuses on growing intelligently and with greater economic,

social and environmental

profitability. This model attracts fewer tourists

than the “Standard” as a result of a demand strategy that targets

higher spending tourists

B“Premium & soft growth”

model

Based on the “Premium & wise growth” model but with an even lower volume of tourists, but maintaining their high

spending profile, therefore it requires less

new developments.

C

THR recommends

this model

CYPRUS TOURISM STRATEGY

* The CTS is adopting a Premium Demand Strategy, according to which by 2030 Cyprus will be visited annually by 4.63 million international tourists,

0.21 million same day visitors and 1.36 million domestic visitors. This will represent lower visitor numbers, with higher expenditure and economic

contribution, and with lower negative impacts.

14

A Premium Demand Strategy is recommended

Longer stay

Higher per day

expenditure

More discerning and

lower negative impacts

Luxury

Affluent

Low cost

Standardstrategy

Premiumstrategy

High-endstrategy

20%10%

5%

50%

20%

10%

25%

55%

60%

5%15%

25%

Mass market

CYPRUS TOURISM STRATEGY

15

Tourism demand results alternatives (2030)

(1) CYSTAT 2015,(2) CYSTAT 2014-Statistics on Movements of Travellers,(3) CYSTAT 2014-Annual data on domestic and outbound trips of Residents of Cyprus

Main variables Units 2015Standard

destination

2030

Premium

destination

2030

High-end

destination

2030

1International

Visitors Thousands 2.656(1) 5.578 4.631 4.368

2Same day

VisitorsThousands 120(2) 257 216 203

3Domestic

TourismThousands 1.297(3) 1.407 1.366 1.324

4Total Visitor

volumeThousands 4.070 7.241 6.214 5.699

CYPRUS TOURISM STRATEGY

16

Tourism demand results alternatives (2030)

(4) No distinction is made between accommodation types (hotels/apartments, licensed/unlicensed) (5) CYSTAT 2014(6) CYSTAT 2014

Main variables Units 2015Standard

destination

2030

Premium

destination

2030

High-end

destination

2030

5Overnight

Stays (4)Thousands 30.545 61.076 53.263 49.037

6

Average

expenditure /

day

Euro 94(5) 102,53 133,91 157,78

7

Average

expenditure /

stay

Euro 794(6) 874,84 1.147,74 1.357,59

8Tourism

ExpenditureMill. Euro 2.352 6.335 7.133 7.737

CYPRUS TOURISM STRATEGY

17

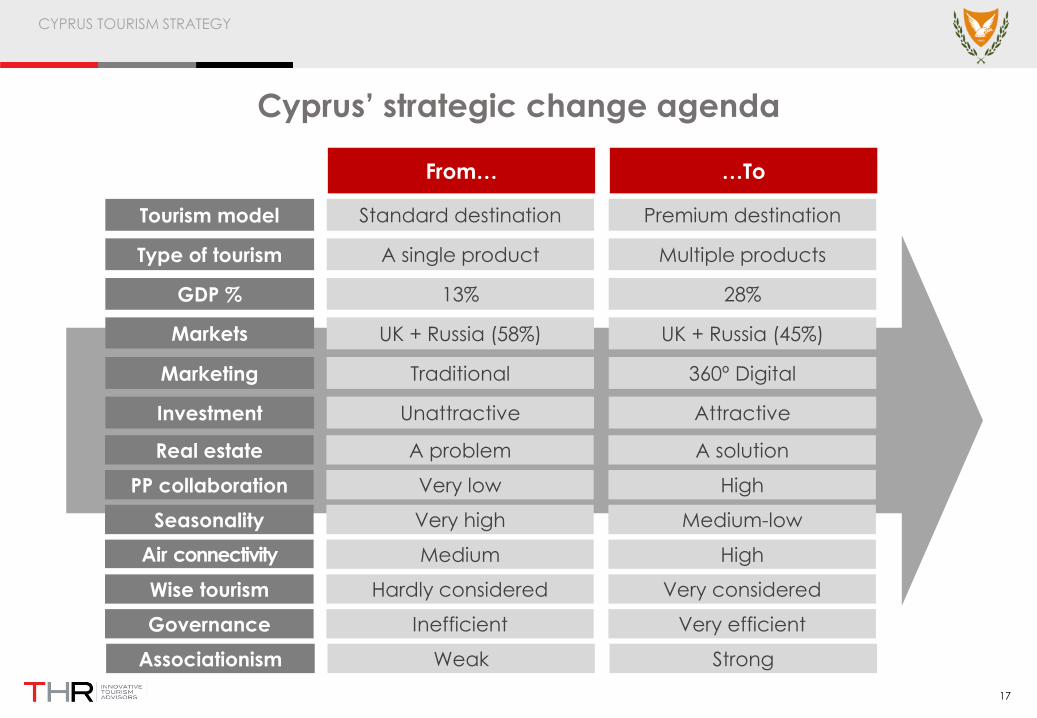

Cyprus’ strategic change agenda

From… …To

Tourism model Standard destination Premium destination

Type of tourism A single product Multiple products

GDP % 13% 28%

Markets UK + Russia (58%) UK + Russia (45%)

Marketing Traditional 360º Digital

Investment Unattractive Attractive

Real estate A problem A solution

PP collaboration Very low High

Seasonality Very high Medium-low

Air connectivity Medium High

Wise tourism Hardly considered Very considered

Governance Inefficient Very efficient

Associationism Weak Strong

CYPRUS TOURISM STRATEGY

18

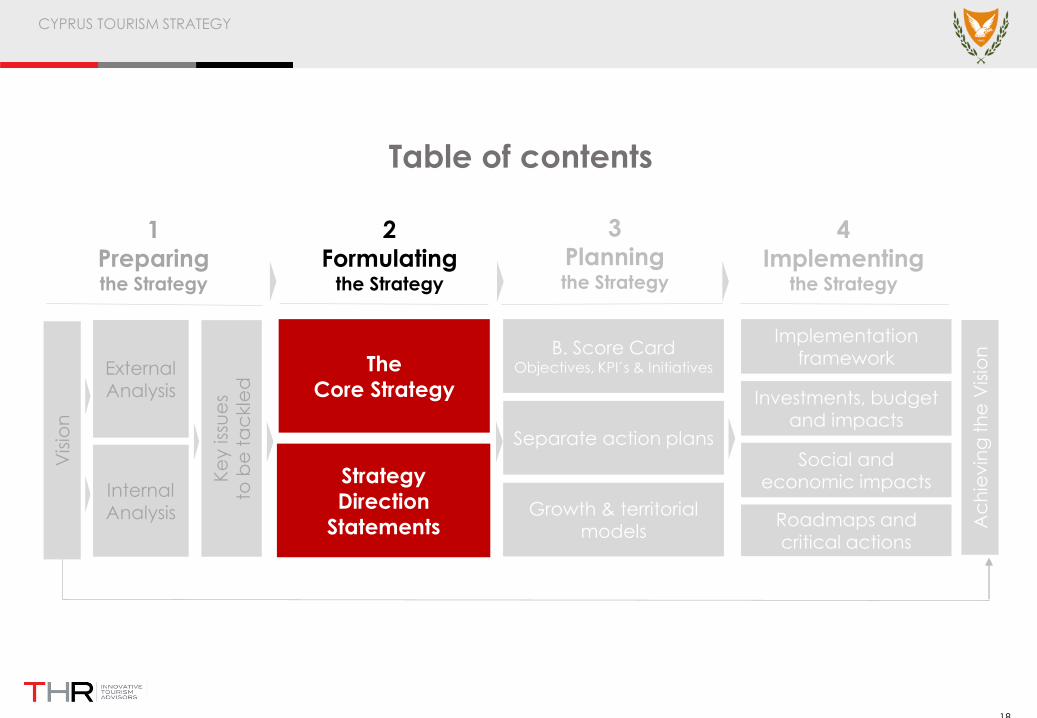

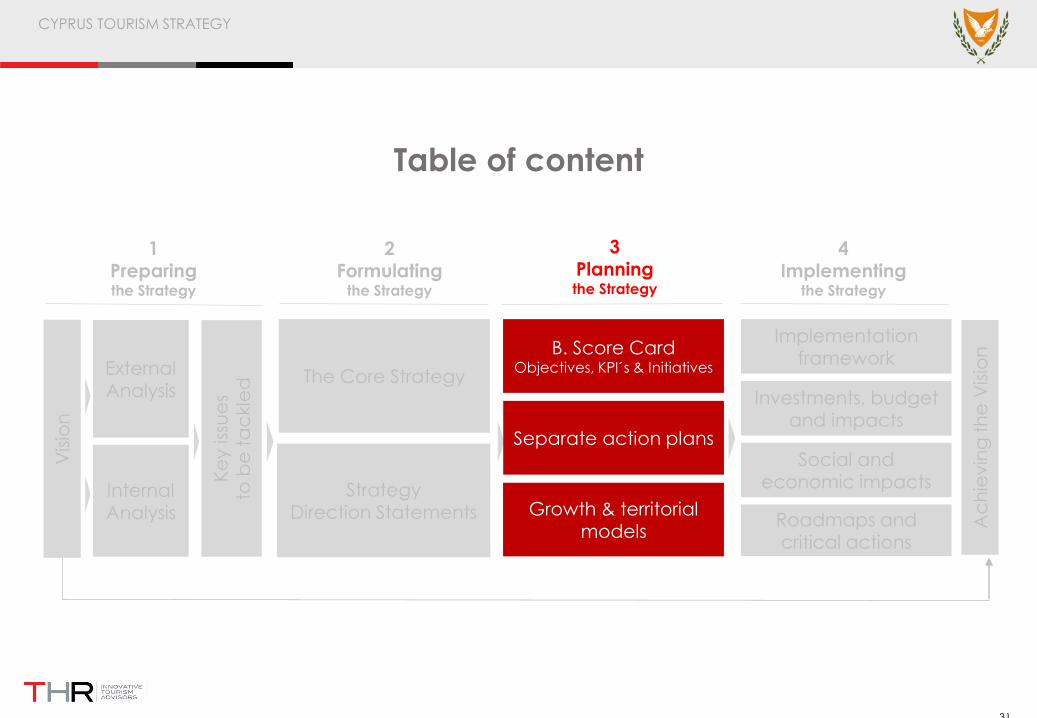

Table of contents

InternalAnalysis

Vis

ion

ExternalAnalysis

Ke

y iss

ue

s

to b

e t

ac

kle

d

The

Core Strategy

Strategy

Direction

Statements

B. Score CardObjectives, KPI´s & Initiatives

Separate action plans

Growth & territorial models

Implementation framework

Investments, budget and impacts

Roadmaps and critical actions

Social and economic impacts

Ac

hie

vin

g t

he

Vis

ion

1

Preparingthe Strategy

2

Formulatingthe Strategy

3

Planningthe Strategy

4

Implementingthe Strategy

CYPRUS TOURISM STRATEGY

19

Best climate in Europe, all year-round

2.1 The Main Competitive Advantage

CYPRUS TOURISM STRATEGY

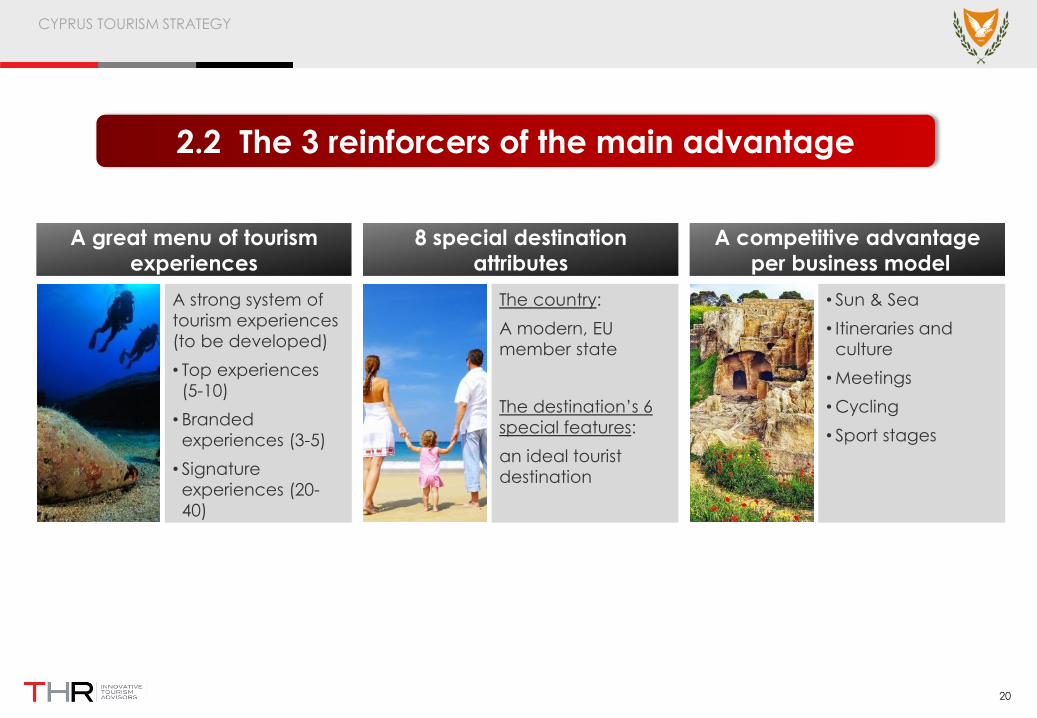

20

A great menu of tourism

experiences

A strong system of

tourism experiences

(to be developed)

• Top experiences

(5-10)

• Branded

experiences (3-5)

• Signature

experiences (20-

40)

8 special destination

attributes

The country:

A modern, EU

member state

The destination’s 6

special features:

an ideal tourist

destination

A competitive advantage

per business model

• Sun & Sea

• Itineraries and

culture

•Meetings

•Cycling

• Sport stages

2.2 The 3 reinforcers of the main advantage

CYPRUS TOURISM STRATEGY

21

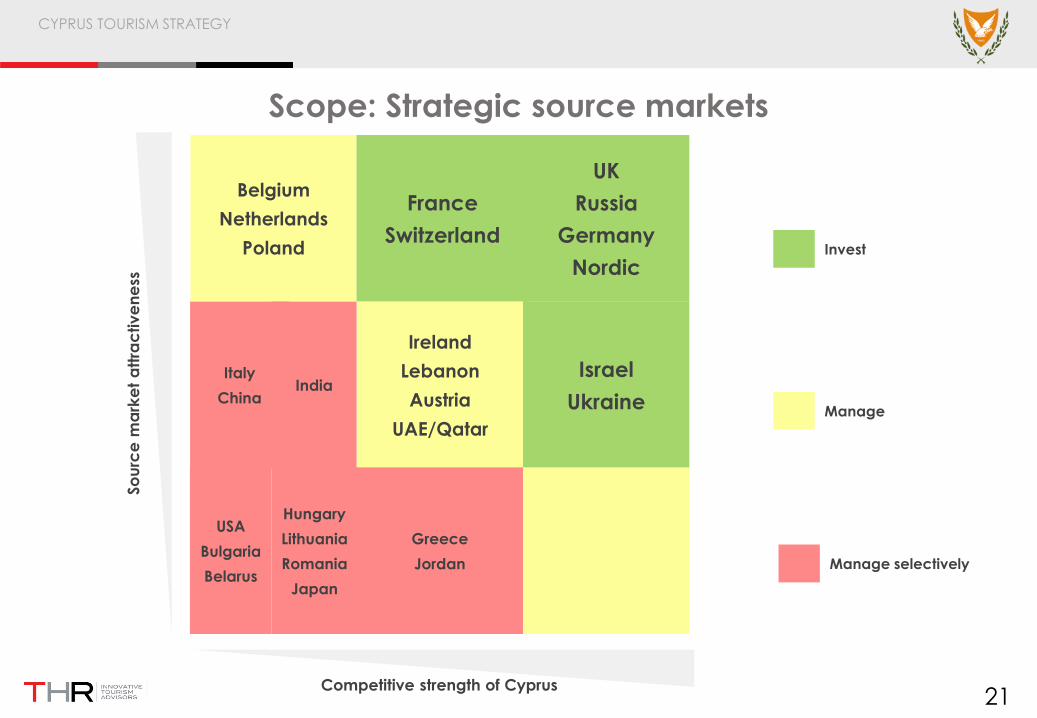

Scope: Strategic source markets

Belgium

Netherlands

Poland

France

Switzerland

Ireland

Lebanon

Austria

UAE/Qatar

Israel

Ukraine

Greece

Jordan

USA

Bulgaria

Belarus

UK

Russia

Germany

Nordic

So

urc

e m

ark

et

att

rac

tive

ne

ss

Competitive strength of Cyprus

Hungary

Lithuania

Romania

Japan

Italy

ChinaIndia

Invest

Manage

Manage selectively

CYPRUS TOURISM STRATEGY

22

Brand adoption funnel Cyprus - Lots of work to do…

Source: Brand adoption survey

Base: Past visit to Cyprus: 691 / No past visit to Cyprus: 1.025

85%

48%

95%

66%

97%

100%

-15%

-52%

-5%

-34%

-3%

Purchase intention

short/mid term

Affordability

Attractivness

Understanding

Awareness

Total universe

Having visited Cyprus

63%

40%

94%

22%

92%

100%

-37%

-60%

-6%

-78%

-8%

Not having visited Cyprus

CYPRUS TOURISM STRATEGY

23

Positive and negative perceptions

2%

3%

4%

4%

6%

10%

12%

14%

18%

39%

Lots to see and do

Quiet / relax / peaceful

Affordable / cheap

Flight connection / easy to

reach

Good food / Gastronomy

Friendly / warm people

Rich / interesting culture

Landscape / nature

Beaches

Climate / sun

2%

4%

5%

5%

6%

8%

10%

13%

13%

24%

Language barriers

Not enough sites to visit /

too small destination

Migrants, refugees

presence

Economic crisis / poverty

Too long flight, too far

Too hot, unpleasant

climate

Unsafe, crime, terrorism

risks

Expensive, unfavorable

exchange rate

Too busy / touristy /

overcrowded /noisy

Geopolitic problems /

tensions with Turkey

Source: THR based on Brand adoption survey

Base: Total sample: 1.700

CYPRUS TOURISM STRATEGY

24

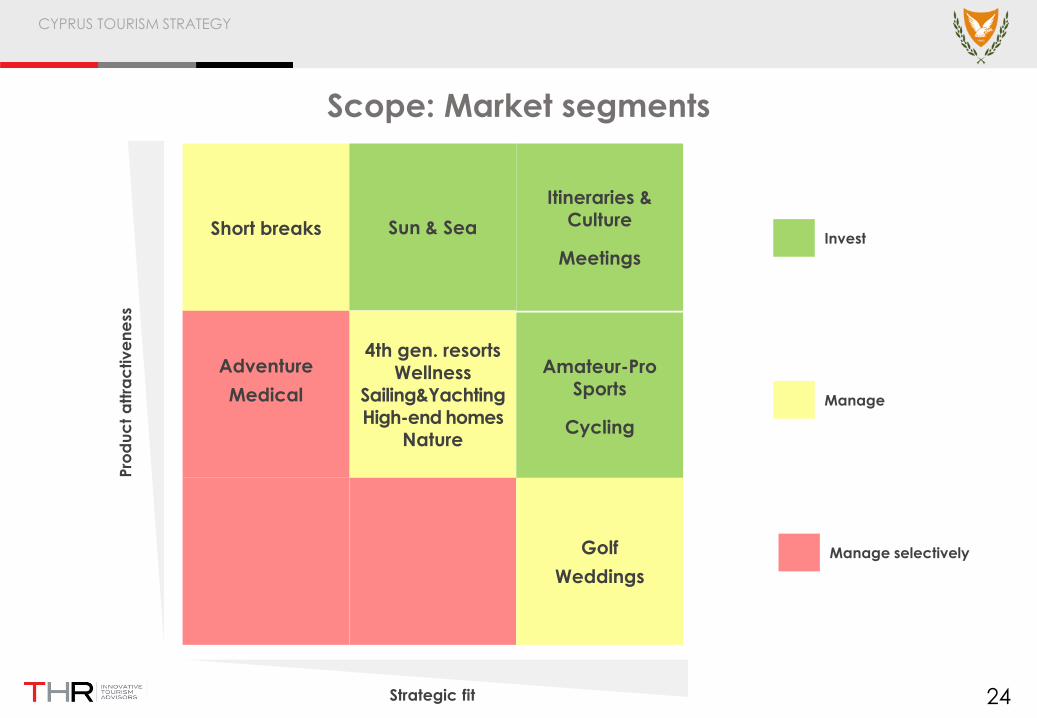

Scope: Market segments

Short breaks Sun & Sea

4th gen. resortsWellness

Sailing&YachtingHigh-end homes

Nature

Amateur-Pro Sports

Cycling

Golf

Weddings

Itineraries & Culture

Meetings

Pro

du

ct

att

rac

tive

ne

ss

Strategic fit

Adventure

Medical

Invest

Manage

Manage selectively

CYPRUS TOURISM STRATEGY

25

Example: Itineraries & Culture business model

CUSTOMER SEGMENTS

VALUE PROPOSITION

KEY ACTIVITIESKEY PARTNERS

KEY RESOURCES

CUSTOMER RELATIONSHIPS

CHANNELS

REVENUE STREAMS (2030)COST STRUCTURE

Communicate the

market strategy for the “Grand Tour of

Cyprus”

Develop a dedicated

“Grand Tour of Cyprus” website

Establish a network of

“Grand Tour of Cyprus” partners

Develop the brand

“Grand Tour of Cyprus”

Attract renowned

international hospitality brands

Implement a

communication strategy for the “Grand Tour of

Cyprus”

Conduct specialized

educational programs for different

stakeholder groups

EM R

M

Coordinate the

development of “Grand Tour of

Cyprus” with rental companies

A

In

Develop and manage

a network of diverse, thematic and

attractive routes

I

Design and manage

the experiential system of the “Grand Tour of

Cyprus”

MM

M

M

M

Action X Type of action

620.000 arrivals ≈1.280 EUR/arrival ≈ 790 mill. EURX =

CYPRUS TOURISM STRATEGY

26

Example: The Grand Tour of Cyprus

Comfortable “drive yourself” routes

Memorable experiencesAttractive mix of natural and cultural attractions

High quality service

Booking platformCypriot flavours and eating experiences

Boutique hotels 24-hrs road assistance service

CYPRUS TOURISM STRATEGY

27

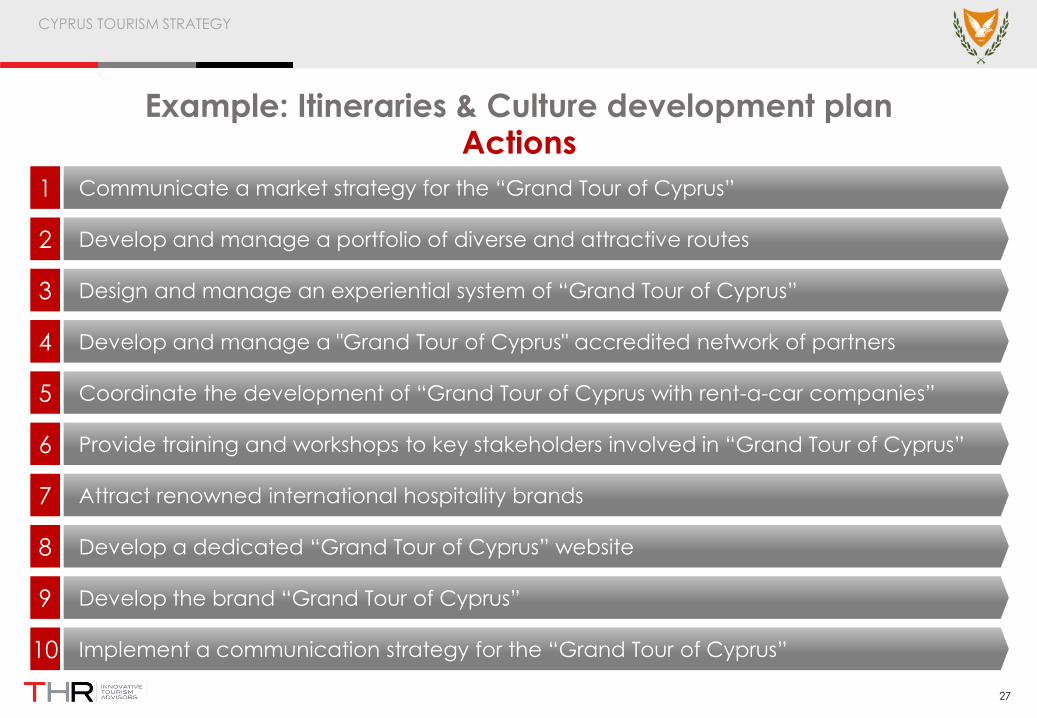

Example: Itineraries & Culture development plan

Communicate a market strategy for the “Grand Tour of Cyprus”1

Develop and manage a portfolio of diverse and attractive routes2

Design and manage an experiential system of “Grand Tour of Cyprus”3

Actions

Develop and manage a "Grand Tour of Cyprus" accredited network of partners4

Coordinate the development of “Grand Tour of Cyprus with rent-a-car companies”5

Provide training and workshops to key stakeholders involved in “Grand Tour of Cyprus”6

Attract renowned international hospitality brands7

Develop a dedicated “Grand Tour of Cyprus” website8

Develop the brand “Grand Tour of Cyprus”9

Implement a communication strategy for the “Grand Tour of Cyprus”10

CYPRUS TOURISM STRATEGY

28

Table of contents

Vis

ion

ExternalAnalysis

InternalAnalysis

Ke

y iss

ue

s

to b

e t

ac

kle

d The Core Strategy

StrategyDirection Statements

B. Score CardObjectives, KPI´s & Initiatives

Separate action plans

Growth & territorial models

Implementation framework

Investments, budget and impacts

Roadmaps and critical actions

Social and economic impacts

Ac

hie

vin

g t

he

Vis

ion

1Preparing the Strategy

2Formulating

the Strategy

3Planning the Strategy

4Implementing

the Strategy

CYPRUS TOURISM STRATEGY

Present

Vision

Key obstacles

Key enablers

25 key issues

25 key issues identified to be tackled by strategy

CYPRUS TOURISM STRATEGY

30

Example: Issues, Strategy Directions and Objectives (cont.)

Issue / Strategic Question

A. Develop a system of high value experiences in Cyprus.

All over Cyprus we will “wow” our guests with arange of unique and authentic natural andcultural experiences. The public sector will lead thisdevelopment of a new experience culture,applying highly creative methods and smartmanagement, generating happy visitors andprofitable businesses.

Tourism experiences

How can we develop a unique

system of tourism experiences in

Cyprus?

Strategy Directions Objective

B. Significantly improve the value along the customer journey

With the help of an attractive labelling system, wewill increase and guarantee selected qualitystandards and characteristics, guide tourists, andhelp to manage expectations. We will constantlymonitor and manage customer satisfaction acrossthe different labelled destinations, products, andservices.

Satisfaction on services

What can we do to improve service

satisfaction?

C. Dramatically reduce visual pollution in the destination

All stakeholders will make maximum efforts toenhance and protect the visual aesthetic ofCyprus. We will remove unnecessary and/ordegraded signage and advertising panels,protect urban spaces from unregulateddevelopment and pollution and reflect ourcultural heritage in our planning and buildingdesign.

Visual pollution

How can we dramatically reduce

visual pollution in Cyprus?

2. Customer journey’s value

CYPRUS TOURISM STRATEGY

31

Table of content

Vis

ion

ExternalAnalysis

InternalAnalysis

Ke

y iss

ue

s

to b

e t

ac

kle

d The Core Strategy

StrategyDirection Statements

B. Score CardObjectives, KPI´s & Initiatives

Separate action plans

Growth & territorial models

Implementation framework

Investments, budget and impacts

Roadmaps and critical actions

Social and economic impacts

Ac

hie

vin

g t

he

Vis

ion

1Preparing the Strategy

2Formulating

the Strategy

3Planning the Strategy

4Implementing

the Strategy

Cyprus Tourism Strategy 32

Strategic objective Measure KPI Initiative

Outcome 1

Deliver an exceptional tourism experience

Develop a system of

high value

experiences in

Cyprus

Number of experiences developed/ year

2018: 2 brand experiences

2019: 3 top and 10 signature experiences

Set up the

“Experience

Cyprus” program1A

% of tourism services and companies labelled/ year

2018: 15%

2019: 20%

2020: 30%

Introduce the

Cyprus Quality

Label system2

Significantly improve

the value along the

customer journeyB

“Black spots” removed /year

2018: 10

2019: 15

2020: 20

Run a visual

pollution initiative3

Dramatically reduce

visual pollution in the

destinationC

Cyprus Tourism Strategy

CYPRUS TOURISM STRATEGY

Source: THR based on “The Execution Premium”, Kaplan & Norton 33

The Strategy Map

1.Deliver an exceptional

tourism experience

B. Significantly improve the value along the customer journey

C. Dramatically reduce visual pollution in the destination

A. Develop a system of high value experiences in Cyprus

Lea

rn a

nd

gro

wth

Str

ate

gic

P

roc

ess

es

DR

IVER

SEN

AB

LER

S

2.Excel in planningand development

D. Implement excellent tourism development master planning

E. Define and manage clear growth models for all regions

F. Increase product diversification and innovation

6.Develop a highly competitive diamond for the tourism sector

Q. Reengineer legal and regulatory framework

R. Educate and train the right people

P. Promote productivity improvement tools

7.Implement a governance &

management framework and culture

T. Establish a sound system of modern governance

U. Implement an efficient management framework

V. Launch a state-of-the-art monitoring system

3. Attract the right amount of

vetted investors and MSMEs

H. Ensure competitive MSMEs grow in Cyprus

I. Increase the quantity and quality of market partners

G. Attract necessary vetted investors

4.Conquer more

better yielding customers

K. Conquer more higher yielding tourists

J. Develop a powerful tourism brand

L. Reduce seasonality

Become, before 2030,an all year-round sustainable destination

receiving 4,8m intl. tourists - 40% of whom during Nov-Apr

Va

lue

fo

rst

ak

eh

old

ers

An exceptional

tourism experience

Attractive investment

environment & opportunities

Better quality of life

and sustainability

Attractive business

opportunities

CUSTOMERS PARTNERS SOCIETYINVESTORS

Re

sults

for

Cy

pru

s (2

03

0)

Tourism

Revenue (M. €)7.000

Wise tourism

index850/1000

GDP

Contribution28%

Total new

Employment47.000

New tourism

keys to develop30.000

Investment required

(public & private) (M. €)20.000

International

tourists (M.)4,8

5.Benefiting the local

society and the environment

N. Reduce carbon footprint of tourism activity in Cyprus

M. Design and manage a tool to assess tourism sustainability

O. Enhance vulnerable economic activities and protect cultural identity

S. Develop air capacity

CYPRUS TOURISM STRATEGY

34

Example: Initiative and workstreams

1. Install the Cyprus Experience Agency

3. Launch the Signature Experiences programme

4. Promote Brand Experiences

5. Initiate experience marketing and communication system

2. Start the Top Experience programme

Initiative 1.

Set up the “Experience Cyprus

Programme”

CYPRUS TOURISM STRATEGY

35

Example: Initiative and workstreams

1. Establish a Centralised Tourism Planning Unit (CTPU)

3. Review and redraft the Legal and Regulatory Framework

4. Establish a Land Acquisition Strategy

2. Launch Regional Tourism Development Master Plans

Initiative 4.

Implement the National Tourism

Planning Initiative

CYPRUS TOURISM STRATEGY

36

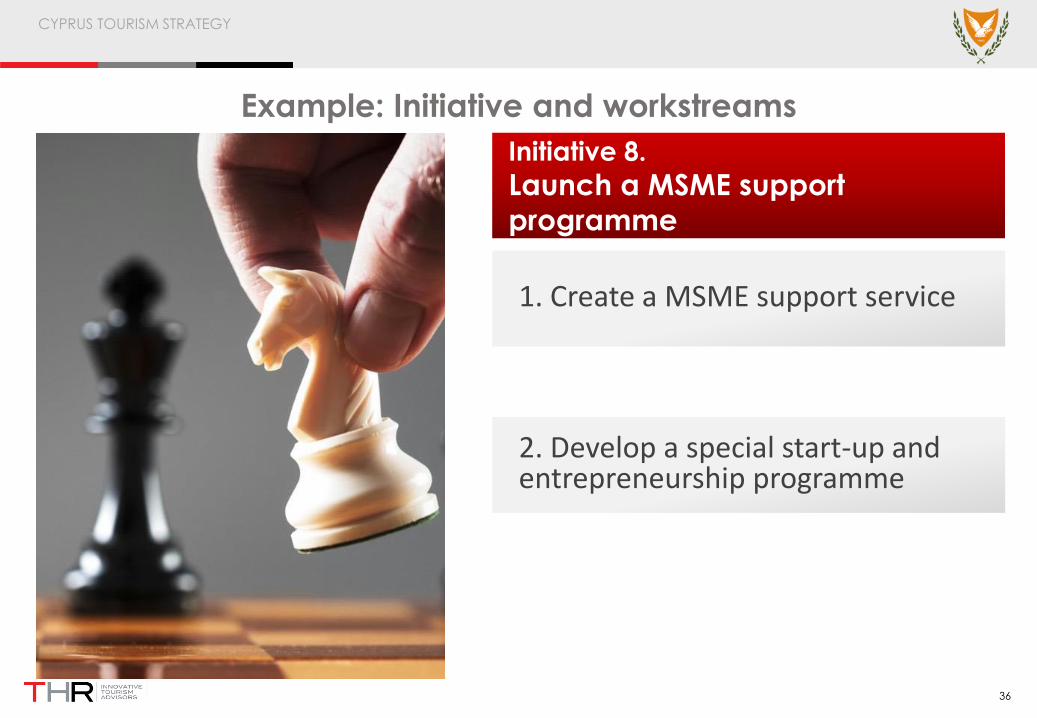

Example: Initiative and workstreams

1. Create a MSME support service

2. Develop a special start-up and entrepreneurship programme

Initiative 8.

Launch a MSME support

programme

CYPRUS TOURISM STRATEGY

37

Example: Initiative and workstreams

Initiative 13.

Elaborate the Wise Tourism Index

1. Define Cyprus’ Wise Tourism Index

2. Measure and publish the Wise Tourism Index results

3. Provide technical support for local authorities for continuous sustainability improvement

CYPRUS TOURISM STRATEGY

38

Example: Initiative and workstreams

Initiative 17.

Reengineer the legal and

regulatory framework

1. Elaboration of the Cyprus Tourism Law

3. Create Public Electronic Platform for legal matters

4. Create a One-Stop Shop/fast track for administrative processes

2. Simplification of the current regulatory framework

5. Facilitate regularisation of the unlicensed accommodation offer

CYPRUS TOURISM STRATEGY

39

Example: Initiative and workstreams

Initiative 22.

Launch performance monitor

1. Determine sector’s performance metrics

2. Launch a Tourism Intelligence Platform

CYPRUS TOURISM STRATEGY

40

Table of content

Vis

ion

ExternalAnalysis

InternalAnalysis

Ke

y iss

ue

s

to b

e t

ac

kle

d The Core Strategy

StrategyDirection Statements

B. Score CardObjectives, KPI´s &

Initiatives

Separate action plans

Growth & territorial models

Implementation framework

Investments, budget and impacts

Roadmaps and critical actions

Social and economic impacts

Ac

hie

vin

g t

he

Vis

ion

1Preparing the Strategy

2Formulating

the Strategy

3Planning the Strategy

4Implementing

the Strategy

CYPRUS TOURISM STRATEGY

41

The 14 main actions of the Quality Plan

Set up the Cyprus Quality Labels (CQL)

Management Unit

Develop the Cyprus Quality Label System

Deploy the CQL System

Wo

rk s

tre

am

sA

ctio

ns

Market and promote the CQL in Cyprus and the

markets

1. Reach an agreement on the organisational structure for the CQL Unit

2. Staffing the CQL Unit

3. Define the labels (concepts plus visuals)

4. Define the quality standards and the rules of the game for the CQL

5. Develop the E-Platform to support the CQL System

6. Provide training to the team of advisors

7. Organise public launching event of the CQL system

8. Conduct initial assessments of applicants

9. Prepare and implement a CQL Marketing Plan

10. Develop rich and engaging B2C online marketing content

11. Audit periodically the Cyprus brand performance

Implement a strong monitoring and enforcement

system

12. Control compliance with the quality standards on a regular basis

13. Continuously monitor customer satisfaction

14. Launch the Quality

Excellence Awards

CYPRUS TOURISM STRATEGY

42

The 13 main actions of the Branding Plan

Implement the branding

system

Align the new tourist

brand visual and

baseline with the

Strategy

Develop an integrated

360º brand

communication system

Wo

rk s

tre

am

sA

ctio

ns

Monitor the brand

implementation and

its performance

1. Achieve a general

agreement on the

proposed brand

identity and its

positioning

2. Approve a tourism

brand architecture

encompassing

product and regional

brands and labels

3. Commission the

design of the new

brand visual and

baseline

4. Test the proposals of

baseline / brand

visual and get the

official approval

5. Implement a strong

launching of the new

brand

6. Commission and

implement Cyprus’ ‘Big

idea’

7. Launch Media

Relations Special

Programme

8. Develop branded

content

9. Launch targeted

online advertising

campaigns

10.Perform co-op

branding actions

11.Appoint a Brand

Manager with clear

responsibilities and

functions

12.Create the ‘Brand

Committee’

13.Audit periodically the

Cyprus brand

performance

CYPRUS TOURISM STRATEGY

43

The 11 main actions of the Seasonality Plan

Create the PPS Product Club and

a PPS Label System

Develop attractive

products for the PPS

Develop a specific PPS

communication strategy

Wo

rk s

tre

am

sA

ctio

ns

Develop and implement a specific PPS sales system

1. Create the Pre

and Post Season

Product Club

2. Design and

implement a PPS

Label System

3. Identify and

prioritise product/

segments with PPS

potential

4. Develop

marketable PPS

experiences

5. Support the

organisation of

PPS events

6. Communicate PPS

advantages

through PR and

targeted

advertising

7. Develop an

attractive website

to market the PPS

offering

8. Provide training for

PPS Product Club

members

9. Develop a “push”

attitude towards

the travel trade

and airlines

10.Foster direct online

sale of PPS

products

Prepare and implement the Winter Season

strategy

10.Prepare and test

the Winter Season

strategy in one

cluster

11. Implement the

tested Winter

Season on all

clusters with

potential

CYPRUS TOURISM STRATEGY

44

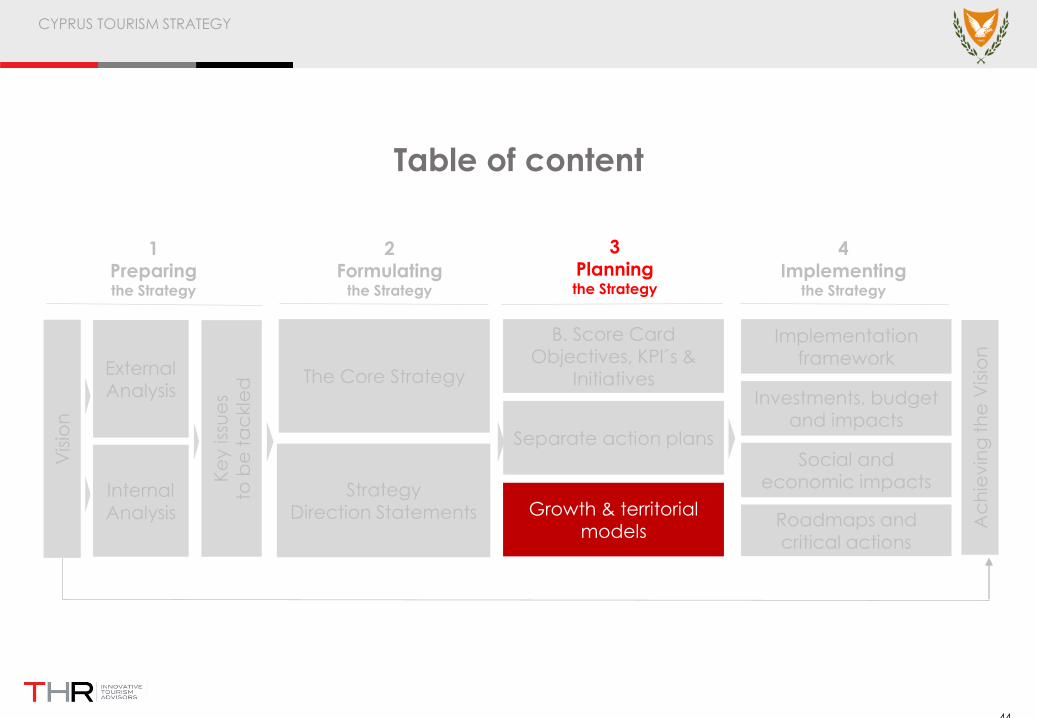

Table of content

Vis

ion

ExternalAnalysis

InternalAnalysis

Ke

y iss

ue

s

to b

e t

ac

kle

d The Core Strategy

StrategyDirection Statements

B. Score CardObjectives, KPI´s &

Initiatives

Separate action plans

Growth & territorial models

Implementation framework

Investments, budget and impacts

Roadmaps and critical actions

Social and economic impacts

Ac

hie

vin

g t

he

Vis

ion

1Preparing the Strategy

2Formulating

the Strategy

3Planning the Strategy

4Implementing

the Strategy

CYPRUS TOURISM STRATEGY

45

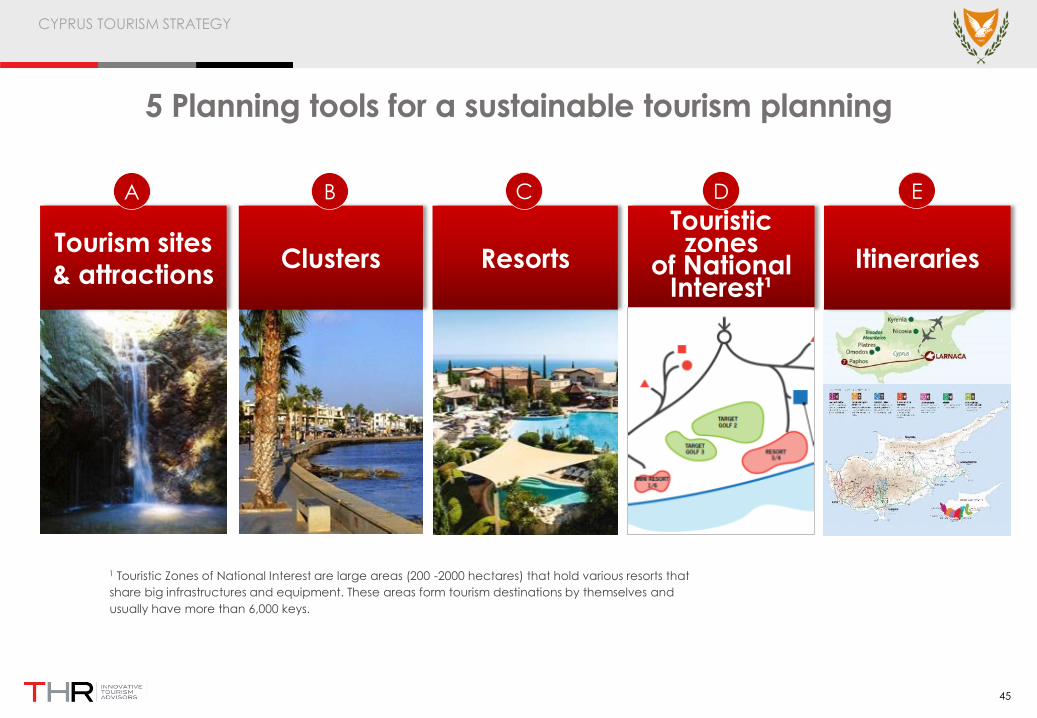

5 Planning tools for a sustainable tourism planning

1 Touristic Zones of National Interest are large areas (200 -2000 hectares) that hold various resorts that

share big infrastructures and equipment. These areas form tourism destinations by themselves and

usually have more than 6,000 keys.

Tourism sites

& attractions

A

Itineraries

E

Resorts

C

Touristic zones

of National Interest¹

D

Clusters

B

CYPRUS TOURISM STRATEGY

46

Integrated spatial plan guiding principles

3 Establish binding development objectives

3Retain tight control over protected lands - follow a pro-active policy

towards its management and use;

4Strengthen agriculture and forestry through tourism, and accept them as

partners in the tourism development process;

5 Maintain and preserve cultural traditions

6Integrate the knowledge of tourism industry stakeholders into the decision-

making and management system

2 Support the elements of tourism that require special care

1 Recognise the need for action

CYPRUS TOURISM STRATEGY

47

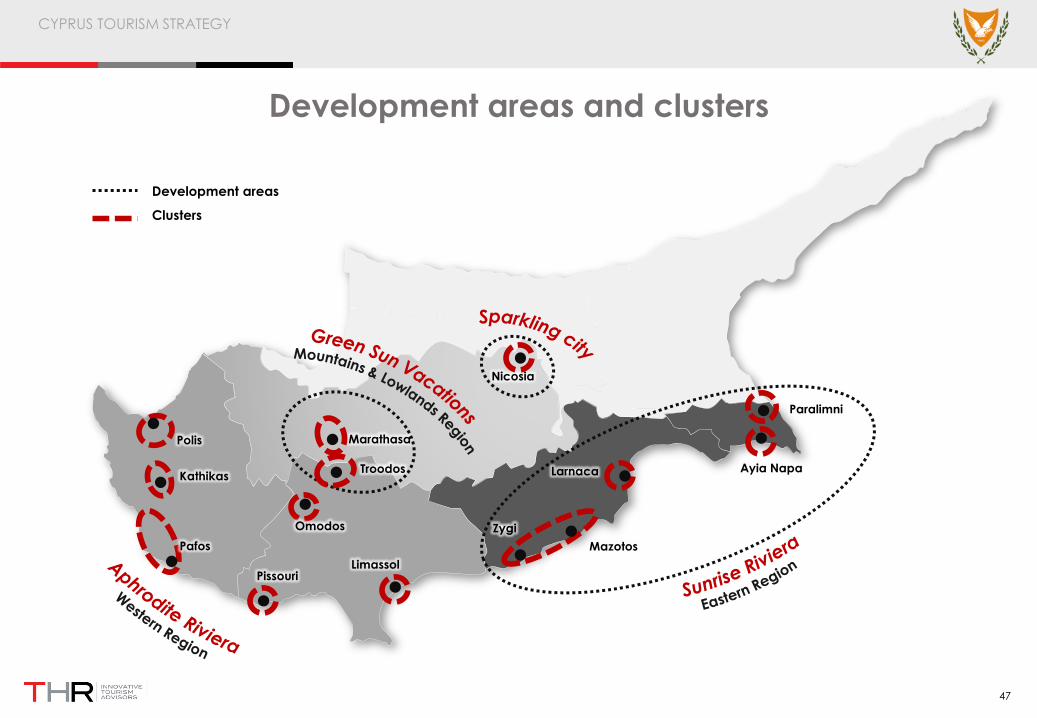

Development areas and clusters

Omodos

LimassolPissouri

Pafos

Kathikas

Polis

Larnaca Ayia Napa

Paralimni

Mazotos

Zygi

Troodos

Marathasa

Nicosia

Development areas

Clusters

CYPRUS TOURISM STRATEGY

48

Example: Eastern region > Protaras - Pernera (Paralimni)

Vision 2030

Paralimni will be the most sought after family

tourism cluster in Cyprus

Customer value proposition

A cluster of resorts offering the best quality

family sun, beach experience in Cyprus,

complemented by adjacency to nature and

exceptional marine experiences

Market positioning

A 4-star ‘sun, sea and family entertainment’

destination

Target

International

Domestic

Key tourist activities and experiences

Multi-generational

Water sports

DivingSun & Sea Sailing / boating

Potential development areas

CYPRUS TOURISM STRATEGY

Note: The numbers have been rounded up, so slight differences may be found.

49

Total investment by typology 2017-2030 (Million Euro)

CYPRUS TOURISM STRATEGY

50

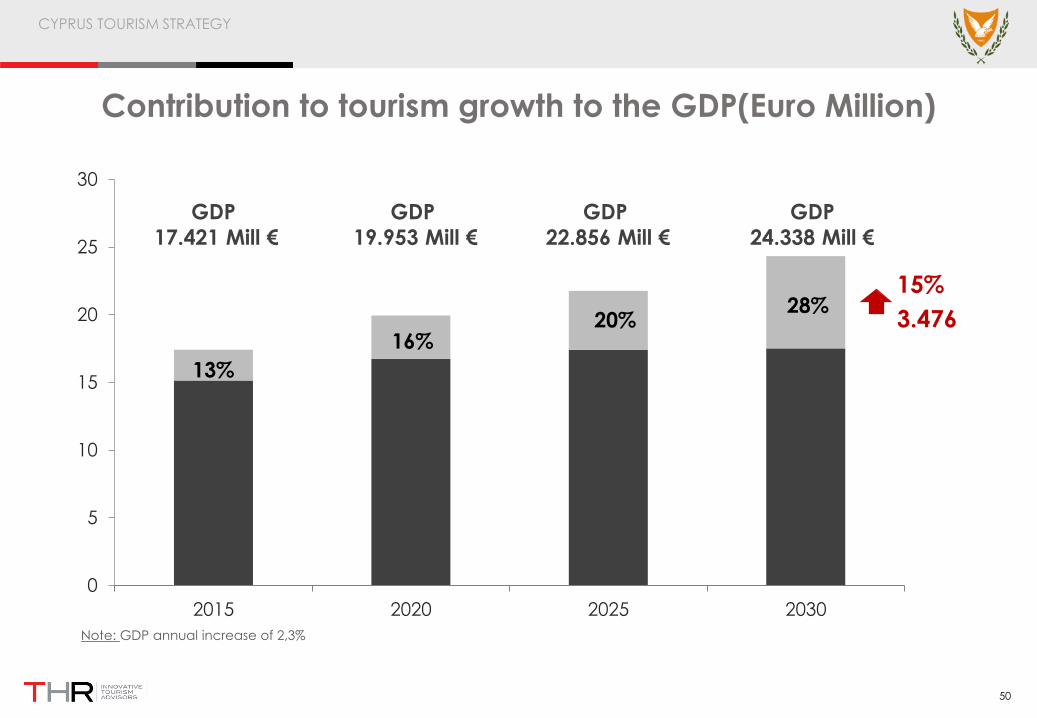

Contribution to tourism growth to the GDP(Euro Million)

0

5

10

15

20

25

30

2015 2020 2025 2030

13%

16%20%

28%15%

3.476

GDP

17.421 Mill €

GDP

24.338 Mill €

GDP

19.953 Mill €

GDP

22.856 Mill €

Note: GDP annual increase of 2,3%

CYPRUS TOURISM STRATEGY

Source: THR projections

* Does not include the direct and indirect required construction employment related with investment

24.00039.941 43.107 50.130

49.500

61.45663.831

69.098

2015 2020 2025 2030

Direct tourism employment Indirect tourism employment

51

Contribution of tourism growth to employment

Total tourism employment (direct and indirect) by 2030

CYPRUS TOURISM STRATEGY

52

Value Gap in Direct Tourism production 2030

- 0% vs. 100% “Wise growth” strategy implementation -

FactorsValue Gap

(Million Euro)%

Increase of tourists 4.911 18

Longer Average stay 5.962 22

Greater Daily Expenditure per

tourist16.416 60

Total 27.285 100

CYPRUS TOURISM STRATEGY

53

Cyprus’ tourism mission

Offer the world

memorable tourism

experiences and

improve the quality of

life of the Cypriots

![VEKAPLAN S · 2021. 1. 8. · Density [g/cm3] DIN EN ISO 1183 0,43 0,50 0,43 0,50 0,45 0,55 E-modulus [MPa] ISO 527 (50 mm/min) 1050 1050 1050 Impact strength (Charpy) [kJ/m2] ISO](https://static.fdocuments.us/doc/165x107/60db4a44a86f95166c3856a3/vekaplan-s-2021-1-8-density-gcm3-din-en-iso-1183-043-050-043-050-045.jpg)

![EDITORIAL - Schwanog · [PWP 17] 8,50 6 0,50 1,5 0,50° R0,15 15,50 R0,15 4 118° Y X X X-X = 15°/ 30° frei Y = 22°/35° frei PWP 17 26,50 11 R37,50 80 16 Z 3 10° 1,50 0,50 Fassette](https://static.fdocuments.us/doc/165x107/5fac738cfe9a4a4fc1472f32/editorial-schwanog-pwp-17-850-6-050-15-050-r015-1550-r015-4-118-y.jpg)