Cyfrowy Polsat S.A. - Strona głó · PDF filePolish Equity Conference 2-3 April 2009,...

36

Cyfrowy Polsat S.A. Poland’s No 1 DTH platform Polish Equity Conference 2-3 April 2009, London

Transcript of Cyfrowy Polsat S.A. - Strona głó · PDF filePolish Equity Conference 2-3 April 2009,...

Cyfrowy Polsat S.A.Poland’s No 1 DTH platform

Polish Equity Conference

2-3 April 2009, Londonp

Disclaimer

This presentation includes 'forward-looking statements'. These statements contain the wordsti i t " "b li " "i t d" " ti t " " t" d d f i il i All t t t th th t t t f hi t i l f tanticipate", "believe", "intend", "estimate", "expect" and words of similar meaning. All statements other than statements of historical facts

included in this presentation, including, without limitation, those regarding the Company’s financial position, business strategy, plans and objectives of management for future operations (including development plans and objectives relating to the Company's products and services) are forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of the Company to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements Such forward-looking statements are based on numerous assumptionsachievements expressed or implied by such forward looking statements. Such forward looking statements are based on numerous assumptions regarding the Company's present and future business strategies and the environment in which the Company will operate in the future. These forward-looking statements speak only as at the date of this presentation. Company expressly disclaims any obligation or undertaking to disseminate any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company's expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based. The Company cautions you that forward-looking statements are not guarantees of future performance and that its actual financial position, business strategy, plans and objectives of management for future operations may differ materially from those made in or suggested by the forward-looking statements contained in this presentation. In addition, even if the Company's financial position, business strategy, plans and objectives of management for future operations are consistent with the forward-looking statements contained in this presentation, those results or developments may not be indicative of results or developments in future periods. The Company does not undertake any obligation to review or confirm or to release publicly any revisions to any forward-looking statements to reflect events that occur or circumstances that arise after the date of this

t tipresentation.

The information and opinions contained in this document are provided as at the date of this presentation and are subject to change without notice.

2

Cyfrowy Polsat on the WSE

3

Cyfrowy Polsat shares on WSE

We debut on the WSE on 6 May 2008. Since that day the WIG index decreased by over 40% and our share price increased by 4%decreased by over 40% and our share price increased by 4%

Our shares entered MSCI EME Index on 25 November 2008

Our shares entered WIG 20 Index as of 20 March 2009

CPS vs. WIG

11

4

Introduction to Cyfrowy Polsat

5

Cyfrowy Polsat highlights

AttractiveAttractive, unconsolidated

market with significant growth

potential

Largest DTH operator in Poland,

5th largest in Europe

Experienced senior

Extensive, high-quality

i ffExperienced senior management team programming offer

at competitive prices

Strong brand name and highStrong financial name and high

customer satisfaction

Strong financialprofile Upfront payment

subscription and STB sale business model with low

churn rates

6

churn rates

Cyfrowy Polsat today

L t id f DTH i i P l d ith 2 7 illi b ib 1Largest provider of DTH services in Poland with 2.7 million subscribers1

Comprehensive programming offering with 74 Polish language channels andComprehensive programming offering, with 74 Polish language channels and over 500 FTA foreign language channels

First DTH operator to launch DVR, in November 2006

HDTV available since November 2007

Launched MVNO services on 8 September 2008 (pre-paid and post-paid)

7

Note:1 As at 31 December 2008

Dynamic growth

Significant subscriber and revenue growth

1 136

50

1 200

Subscribers Revenues and EBITDA

2,068

2,727

2 000

2 500

0s) 797

1,136

30

40

800

1 000

1 200

)

1,274

,

1 000

1 500

(000

282

483

34817%

21%

31%

20

30

400

600 (%)

(PLN

m)

657

0

500

282

46 74

166

17% 15%

0

10

0

200

2005 2006 2007 2008 2005 2006 2007 2008

Revenues EBITDA EBITDA margin (rhs)

8

Source: Calculated based on Grupa Cyfrowy Polsat S.A. audited IFRS financial statements for 2004–2008,Notes:1 Year end subscriber numbers for 2004–20082 2006 financials are reclassified to conform with FY 2007 results; results from the subsidiary EMARKET, sold on 31 August 2007 are presented

under "net profit/(loss) from discontinued operations“

Polish Pay TV market

9

TV viewing time

Average daily TV viewing minutes per adult (2007)Average daily TV viewing minutes per adult (2007)

Poland has one of the highest average daily TV viewing minutes

289

253 253 252234250

300

350

Watching Pay TV is a common and generally cheap form of entertainment

234217 210

186 184

100

150

200

250

(min

utes

)

0

50

Serb

ia

olan

d

ngar

y

reec

e

man

ia

este

rn

es 1

Russ

ia

ovak

ia

publ

ic

ActivityIllustrativecost (PLN)S Po

Hun G

r

Rom

Aver

age

top

5 W

eEu

rope

an c

outr

ie R

Slo

Czec

h Rep Activity cost (PLN)

Mini Package monthly 10

Menu McDonald 12

Mini Max Package monthly 20

Source: WARC (World Advertising Research Center) 2007

Note

A Mini Max Package monthly 20

Movie ticket 22-27

Family Package monthly 38

10

Note: 1 Includes Italy, Germany, France, UK and Spain ½h of bowling 45

The Polish DTH market

Poland is one of the largest DTH markets in Europe, with significant room for growthg g

Polish pay TV market penetration forecast69 71 74 78 81Total (%)

Increase in CATV/DTH subscribers in Poland

2% 2% 3%4% 5%

75%

100%

4,380 4,500 4,600 4,700 4,6075 000

6 000

34% 36% 38% 41% 43%

2% 2%

50%

(000

s)

2,215

3,388

2 000

3 000

4 000

(000

s)

33% 33% 33% 33% 33%

0%

25%1,439

0

1 000

2 000

2005 2006 2007 2008 2005 2006 2007 2008

Source: Informa , Eastern European TV 12th Edition (cable

2009 2010 2011 2012 2013

CATV DTH IPTV

2005 2006 2007 2008 2005 2006 2007 2008

CATV Pay DTH

Source: GUS, KRRiTV, PIKE, Informa, own estimates

11

Source: Informa , Eastern European TV 12th Edition (cable penetration adjusted for the homes passed)

Source: GUS, KRRiTV, PIKE, Informa, own estimates

Poland’s fastest growing DTH player

DTH t i P l d D b 2008 C f P l t' h f DTH thDTH operators in Poland - December 2008 Cyfrowy Polsat's share of DTH growth

75% 80%

Our market share of net adds 72% 52%

300*

2 500

3 000

)

3.027

1.098

1.276

1 000

1 200

1 400

2.727

1.3801 500

2 000

subs

crib

ers

(‘0

00

776

617

795

659

600

800

1 000

000s

)

92**500

1 000

Num

ber

of s

592327

264

200

400

600(

500

0

1 2 30

2005 2006 2007 2008

T t l DTH t dditi C f P l t t dditi

12

Source: Press publicataions,TVN Grup Annual Report

Source: Press, Company information

*Users having the set-top box with the coding system and being able to get the pay television immediately after paying a subscription fee** Users of Telewizja na kartę

Total pay DTH net additions Cyfrowy Polsat net additions

Our product

13

Our packagesOver 500 TV channels and 9 Polish radio channels

Subscribers (000s)

Price(PLN)

No. ofChannels

Family (Basic)

2,286 47 37.90

CivilisationScience

Relax MixFamily

63 +19.90

2

Upgrade from Family PackagePolska

F ilRelax Mix as aboveRelax Mix +

HBO

Super Film

Upgrade from Family Package

Upgrade from

Family66 +

39.90

Family68

Relax Mix as above+

Relax Mix as above+

2Super Film package

Upgrade from Family Package

68 +49.90

+

HD

Family /HBO 5 +

6.00 per A la carte

Mini 441 19 9.90

pchannel

14Mini Max 23 19.90

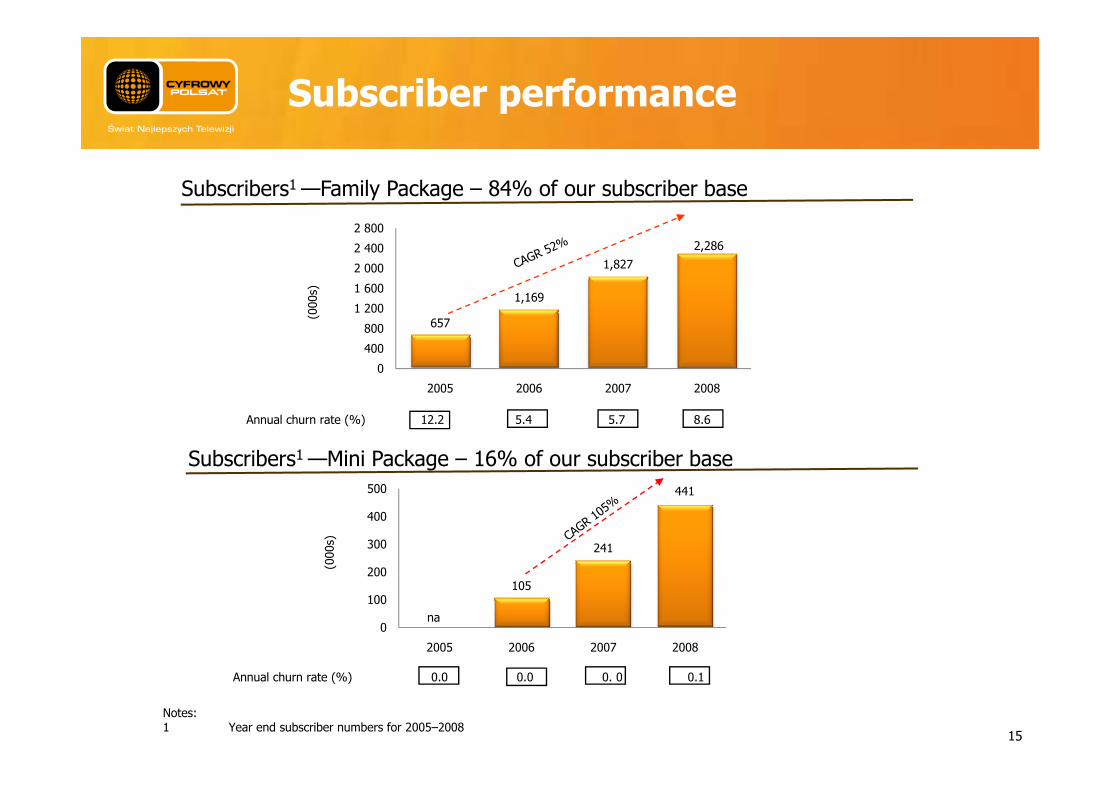

Subscriber performance

Subscribers1 —Family Package – 84% of our subscriber base

1,169

1,8272,286

1 200

1 600

2 000

2 400

2 800

00s)

657

0

400

800

1 200

2005 2006 2007 2008

(00

Subscribers1 —Mini Package – 16% of our subscriber base500

Annual churn rate (%) 12.2 5.4 5.7 8.6

241

441

200

300

400

500

(000

s)

105

0

100

200

2005 2006 2007 2008

na

15

Notes:1 Year end subscriber numbers for 2005–2008

Annual churn rate (%) 0.0 0.0 0. 0 0.1

ARPU performance

ARPU1 —Family Package

30.235.9 37.8 39.4

30

40

50

onth

)

0

10

20

30

(PLN

/mo

ARPU1 —Mini Package2005 2006 2007 2008

8.4 8.610

5

(PLN

/mon

th)

0

2005 2006 2007 2008

S C l l t d b d G C f P l t S A dit d IFRS fi i l t t t f 2004 2008 d C

na na

16

Source: Calculated based on Grupa Cyfrowy Polsat S.A. audited IFRS financial statements for 2004–2008 and CompanyNotes:1 ARPU is calculated as subscription revenues divided by average numer of subscribers (based on the monthly average)

Poland’s DTH players comparison

Cyfrowy Polsat maintains competitive prices while offering high quality services

Launch date December 1999 November 1998 October 2006

Subscribers 1 2,726,993 c. 1,380,000 c. 500,000

Channels 74 Polish TV Access to over 500 FTA

channels via HotBird

72 Polish TV Access to FTA channels

via HotBird

77 Polish TV Access to FTA channels

via HotBird

Content Key content: 2 exclusive sports channels; 15 movie channels incl. HBO

Polsat and all key TVN, TVP channels

Key content: 2 exclusive sports channels; 20 movie channels incl. CANAL + and HBO

Key TVN, TVP but no Polsat channels

Key content: 1 exclusive sports channel; 20 movie channels incl. HBO

Key TVN, TVP channels but no Polsat channels

Packages (monthly fees)

Entry: PLN 10/€2.4 Full: PLN 112/€26.8

Entry: PLN 19/€4.6 Full: PLN 147/€35.2

Entry: PLN 32/€7.7 Full: PLN 190/€45.5

New services (launch date)

HDTV (November 2007) DVR (November 2006)

HDTV (Q4 2006) IPTV in co-operation with

HDTV (Q4 2006) VoD (September 2007)

MVNO (September 2008) TPSA (2006) DVR (2008)

DVR (December 2006)

17

Source: Company information, PressNotes:1 As at 31 December 2008

Our strategy

18

Strategy: highlights

Increase penetration of pay DTH satellite broadcastingIncrease penetration of pay DTH satellite broadcasting services

Increase ARPU through creation of new packages, launch of new products and possible increases of subscription prices

Continue to build value of our DTH business with key new products and possible increases of subscription prices

Continue to manage existing operations cost-effectively and efficiently (e.g. improve profitability through in-house production of STBs)

business with key targets to:

production of STBs)

Leverage brandMVNO services launched on 8 September 2008

Consider offering broadband and fixed-line telephony in thefuture

Leverage brand name and existing subscriber base to

launch bundled services

19

The MVNO opportunity

Combination of DTH and MVNO can serve as the basis for a potential future multiple-play offering Large addressable market beyond DTH customer base

Strategically valuable option

Limited incremental investment Numerous operational synergies (sales, customer care, marketing, etc.)

Controllable costs , g, )

Access to mobile content from current business partners

Leverages brand equity and sales network of 1,296 PoSPh d i t tLi it d i k Phased investmentEarly entrant in a fast-growing market

Limited risk

New business generating incremental profitsMaintain DTH customer loyalty and reduce churnCross-promotion and cross-selling

High potential return

20

The MVNO provides attractive upside potential

Financial highlights

21

Impressing revenue growth Much slower growth in the operating costs uc s o e g o t t e ope at g costs

Revenues

1 000

1 200

797

1,136

400

600

800

(PLN

m)

0

200

2007 2008

Operating costsOperating costs

800

1 000

652812

200

400

600

( PLN

m)

0

200

2007 200822

Revenues up by 42% due to an increase in subscription feesp

Revenues 2008 revenues breakdown (%)

1500

10016

42

1000

9%

2% 4%

107

100

1215

1000

(PLN

m)

663

97850086%

0

2007 2008

Subscription fees

Sales of satellite television receiving equipment

(‘000 PLN) 2008 2007 ChangeRevenues, of which: 1,136,281 796,669 42%

Sales of signal transmission services

Other operating revenues

Subscription fees 977,678 662,521 48%

Sales of satellite television receiving equipment 100,180 107,205 (7%)

Sales of signal transmission services 16,440 11,602 42%

Other operating revenues 41,987 15,341 174%

23

Operating costs grew slower than revenues

Operating costs (m PLN)

109800

20242

65209

13254

400

(PLN

m)

152221

48

59126

42

(‘000 PLN) 2008 2007 ChangeOperating costs, of which:

Amortisation

811,987

23,547

651,522

20,777

25%

13%

21 240

2007 2008Amortisation

Programming costs

Signal transmission services costs

Amortisation 23,547 20,777 13%

Programming costs 221,443 152,031 46%

Signal transmission services costs 59,006 48,402 22%

Di t ib ti k ti d t tSignal transmission services costs

Distribution and marketing costs

Salaries and employee-related expenses

Costs of satellite television receiving equipment sold

Distribution, marketing and customer care costs202,465 125,919 61%

Salaries and employee-related expenses 64,589 41,701 55%

Costs of satellite television receiving equipment sold132,122 209,028 (37%)

Other operating costs

Other operating costs 108,815 53,664 103%

24

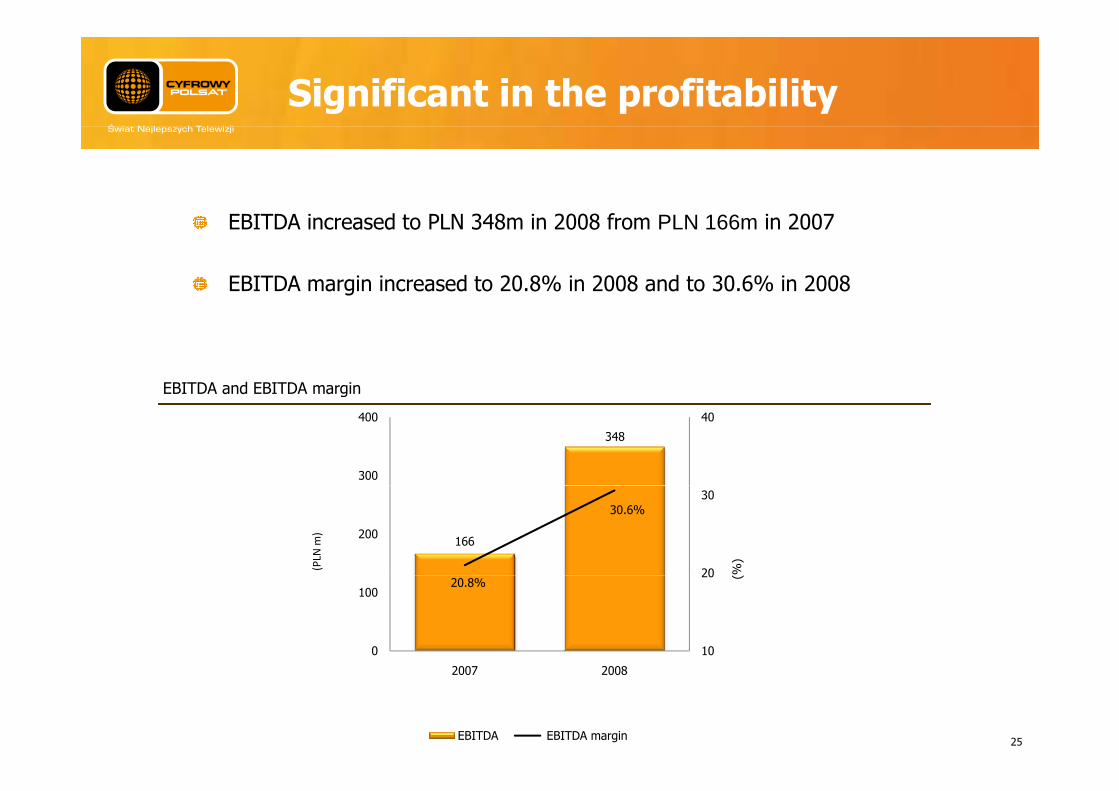

Significant in the profitability

EBITDA i d t PLN 348 i 2008 f PLN 166 i 2007EBITDA increased to PLN 348m in 2008 from PLN 166m in 2007

EBITDA margin increased to 20.8% in 2008 and to 30.6% in 2008

EBITDA and EBITDA marging

348

40

300

400

166

30.6%

20

30

200

%)

(PLN

m)

20.8%

10

20

0

100

(25

2007 2008

EBITDA EBITDA margin

Net income more than doubled

Net income

30300

270

23.7%

20200

113

14.2%

20200

(%)

( PLN

m)

10100

00

2007 2008

Net income Net income marging

26

Safe debt level

As of 31 December 2008 our cash balance was higher than our debt balance by PLN 136m

In 2008 we repaid PLN 108m under our loan agreements

Entire debt denominated in the foreign currencies was repaid; debt under

Debt balance vs. cash balance

Entire debt denominated in the foreign currencies was repaid; debt under current loan agreement is only in PLN

246

300

221

200

(PLN

m)

111

151

100

31 December 2007 31 December 2008

Debt balance Cash balance27

Our cash balance increased by PLN 96 m (64%)

N h fl 2008Net cash flow – 2008

600

3167 77

108

400

500

14 3814

246300

400

( PLN

m)

150

100

200

0

Cash at the begining of the period

Cash flow from

operations

Settlement of IPO

expenses

Capex Debt repayment

Interest Dividend payout

Other Cash at the end of the

period

28

Currency risk and hedging arrangements

Following categories of costs are dependent on fluctuations of exchange rates:Approx. 44% of our programming costs is denominated in Euro and approx. 55% in USD100% of our signal transmission services costs is denominated in Euro

Fluctuations of exchange rates also influence our costs of satellite television receiving equipment :Approx. 20% of our costs of satellite television receiving equipment and telephones sold is denominated in Euro and approx. 60% in USD

Our costs of satellite television receiving equipment are based on historical exchange rates – PLN weakening will not be visible in the results of Q4 2008

Hedging arrangements

Forward transactions for the purchase of the USD 2 m monthly at the rate of PLN 2.3180/USD until S t b 2009September 2009Forward transactions for the purchase of Euro 1.5 m monthly at the rate of PLN 3.4590/Euro until March 2009

We hedge approximate 66% of our foreign currency denominated costs in USD until September 2009We hedge approximate 66% of our foreign currency denominated costs in USD until September 2009 and approx. 55 % of our foreign currency denominated costs in Euro until March 2009

Our Q4 2008 operating costs increased by PLN 12 m as a result of PLN weakening in Q4 2008 (includingforward transactions)

29

forward transactions)

In 2008 we recognized the gain on realized forwards and gain on the revaluation of unrealized forwards of PLN 18 m.

Outlook for 2009

30

Outlook for 2009

Sale in January 2009 higher than in the corresponding period 2008

An increased in proportion of the leased receiving equipment will have positive impact on EBITDA

New promotional offers – starting from February 2009 – offering 1, 3 and 6 months without subscription payments

We consider introduction of new packages (DTH)

We limit our costs on the MVNO project – sale of MVNO services only to our newWe limit our costs on the MVNO project – sale of MVNO services only to our new and existing DTH subscribers

As a result of the change in the MVNO strategy the number of MVNO subscribersAs a result of the change in the MVNO strategy the number of MVNO subscribers will grow slower than initially anticipated

Change of the mobile termination rates – 21.6 gr/min until 30 June 2009,

31

Change of the mobile termination rates 21.6 gr/min until 30 June 2009, 16.8 gr/min starting from 1 July 2009

Additional informationAppendix

32

Milestones in our history

1996 1999 2003 2004 2005 2006 20082000 20071996

Joint stock company established under the business name of Market S.A.

1999 2003 2004 2005 20062000

1996

2007

Started to broadcast satellite signal in December 19991999

Full commercial launch; entered into co-operation agreement with Telewizja Polsat S.A. acting as commission-based distributor for its digital platform2000

Granted licence for wireless satellite network broadcasting services to become a fully independent operator of the digital platform; acquired DTH operations from Telewizja Polsat S.A. and other related businesses

2003

Changed name to Cyfrowy Polsat S A2004 Changed name to Cyfrowy Polsat S.A.2004

Merged with Polsat Sp. z o.o., lessor of distributed STBs2005

Acquired HQ building; became largest DTH satellite broadcasting operator in Poland by subscribers2006

Launched production of own STBs in November 20072007

33

Successfully completed IPO in May 20082008

Corporate governance

Supervisory Board

Zygmunt Solorz-ŻakChairman

Robert GwiazdowskiMember

Andrzej PapisMember

Leszek ReksaMember

Heronim RutaMember

Management Board

Dominik LibickiChief Executive Officer and the President of the Management Board

Maciej GruberChief Financial Officer

Andrzej MatuszyńskiChief Marketing Officer

Dariusz DziałkowskiChief Technology Officer

34

Shareholder structure

Sharehoder Number of shares

% of shares

Number of votes

% of votes

1 Polaris Finance B.V. 162.943.750 60,73% 317.968.750 69,76%

2 Zygmunt Solorz-Zak 30.603.750 11,41% 61.207.500 13,43%

3 Others 74.777.500 27,86% 76.648.750 16,81%

T t l 268 325 000 100 00% 455 825 000 100 00%Total 268.325.000 100,00% 455.825.000 100,00%

% of shares

17%

% of votes

61%11%

28%

70%

13%

Polaris Finance BV Zygmunt Solorz-Zak Others Polaris Finance BV Zygmunt Solorz-Zak Others

Notes:1 85% of shares belongs to Mr Zygmunt Solorz-Żak and 15% of shares belongs to Mr Heronim Ruta2 13.43% of shares belongs to Mr Zygmunt Solorz-Żak , 0.70 % of shares belongs to Mr Heronim Ruta and 0.24% shares belongs to the

members of the Management Board35

Our DTH satellite distribution network

6

5

1 3

4

7

KEY:

= Cyfrowy Polsat’s 1,296 PoS

= Cyfrowy Polsat’s 27 wholesale distributors

Warsaw

2

1 5 Gdańsk

8

Kraków

Poznan

Łódź

2

3

4

Gdańsk

Szczecin

Wroclaw

Katowice

6

7

8

36

Specialised DTH network

![CHAPTER 13 WET DIGESTION METHODS - Strona Głó · PDF fileCHAPTER 13 WET DIGESTION METHODS ... material pertinent to either organic [15-18] or ... Glassy carbon graphite](https://static.fdocuments.us/doc/165x107/5a9e111e7f8b9a29228d2334/chapter-13-wet-digestion-methods-strona-gl-chapter-13-wet-digestion-methods.jpg)