Crowds of Wisdom- Random Forest & Morningstar Quant...

58

©2015 Morningstar, Inc. All rights reserved. Andy Tang, CFA @QWAFAFEW Pittsburgh June 9 th , 2015 The Wisdom of Crowds - Random Forest™ and Morningstar Quant Equity Rating

Transcript of Crowds of Wisdom- Random Forest & Morningstar Quant...

©2015 Morningstar, Inc. All rights reserved.

Andy Tang, CFA

@QWAFAFEW Pittsburgh

June 9th, 2015

The Wisdom of Crowds - Random Forest™ and Morningstar Quant Equity Rating

Agenda

2

gRandom Forest™ methodology

gMorningstar Quant Equity Rating

gQ&A

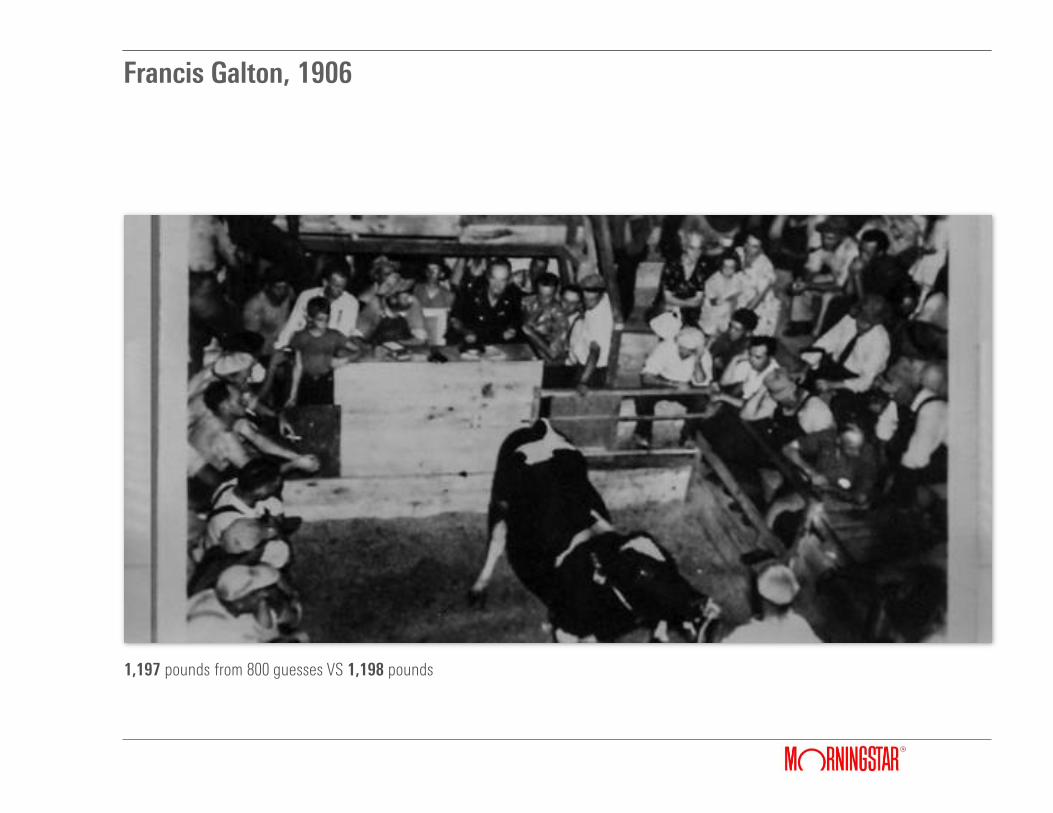

Francis Galton, 1906

1,197 pounds from 800 guesses VS 1,198 pounds

Ensemble Models

4

gCrowds aren’t wise unless:

/Independent– every guess must be independent from each other

/Talent – every guess must be slightly better than random guess

/Crowd – need a lot of guesses

gRandom Forests™ are structurally designed to take advantage of this phenomenon

Ensemble models mathematically formalize and capitalize on the concept of wisdom of crowds.

Random Forest™

5

gCollection of independent decision trees (“forest”)

gRandom subspaces to fit the trees (“random”)

g Idea: Wisdom of crowds

/Several weak predictions can be averaged to make ONE strong prediction

Random Forest™ Methodology

6

gHow to construct a decision tree?

/What to split?

/Where to split?

/When to stop splitting?

gHow to use Random Forest™?

/How to predict?

/Variable Importance

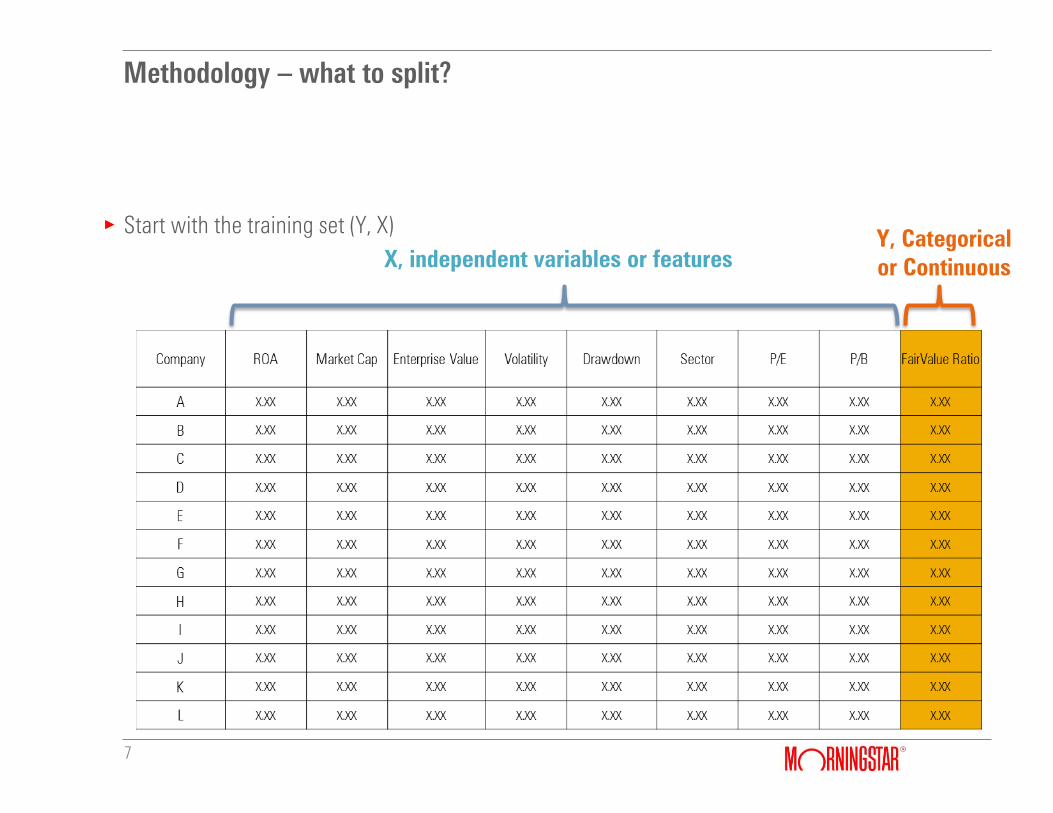

Methodology – what to split?

7

gStart with the training set (Y, X)

X, independent variables or features

Y, Categorical

or Continuous

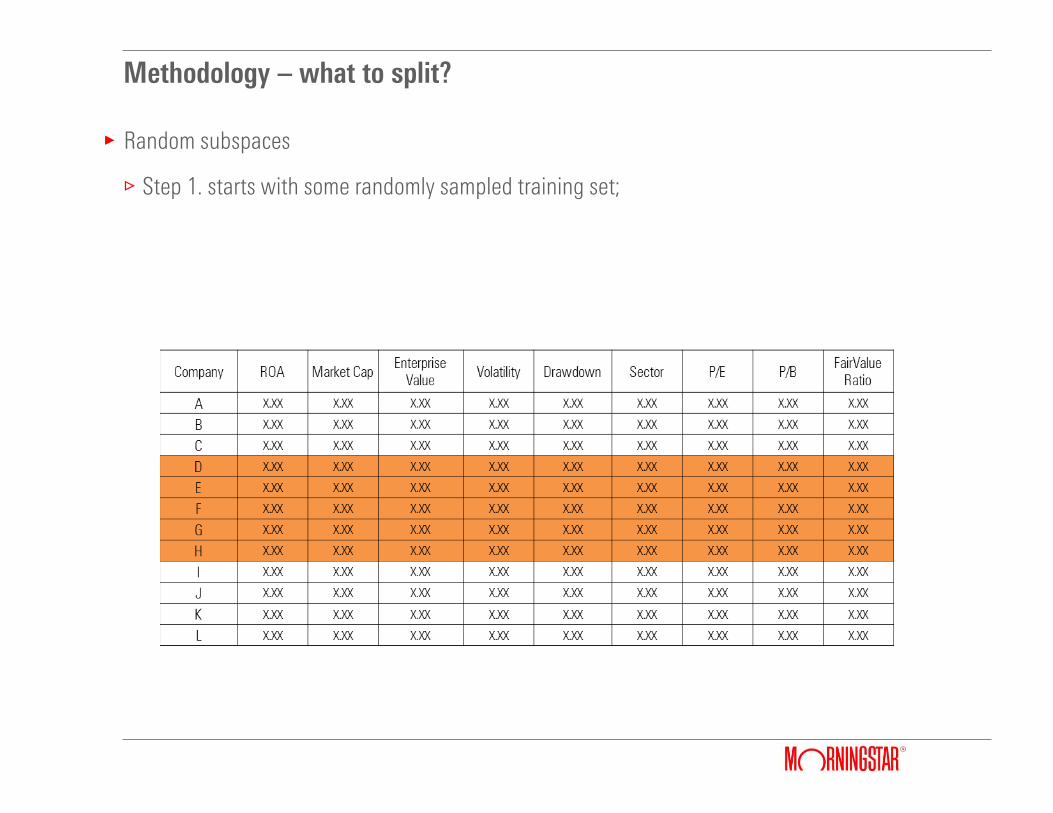

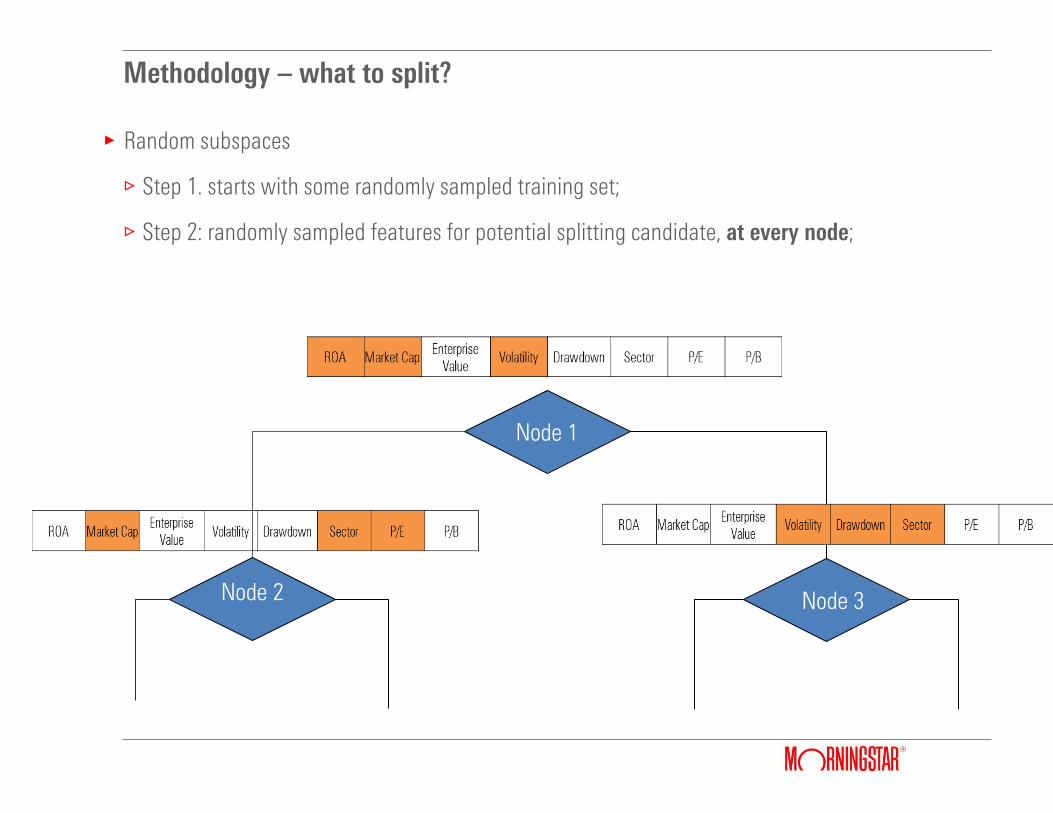

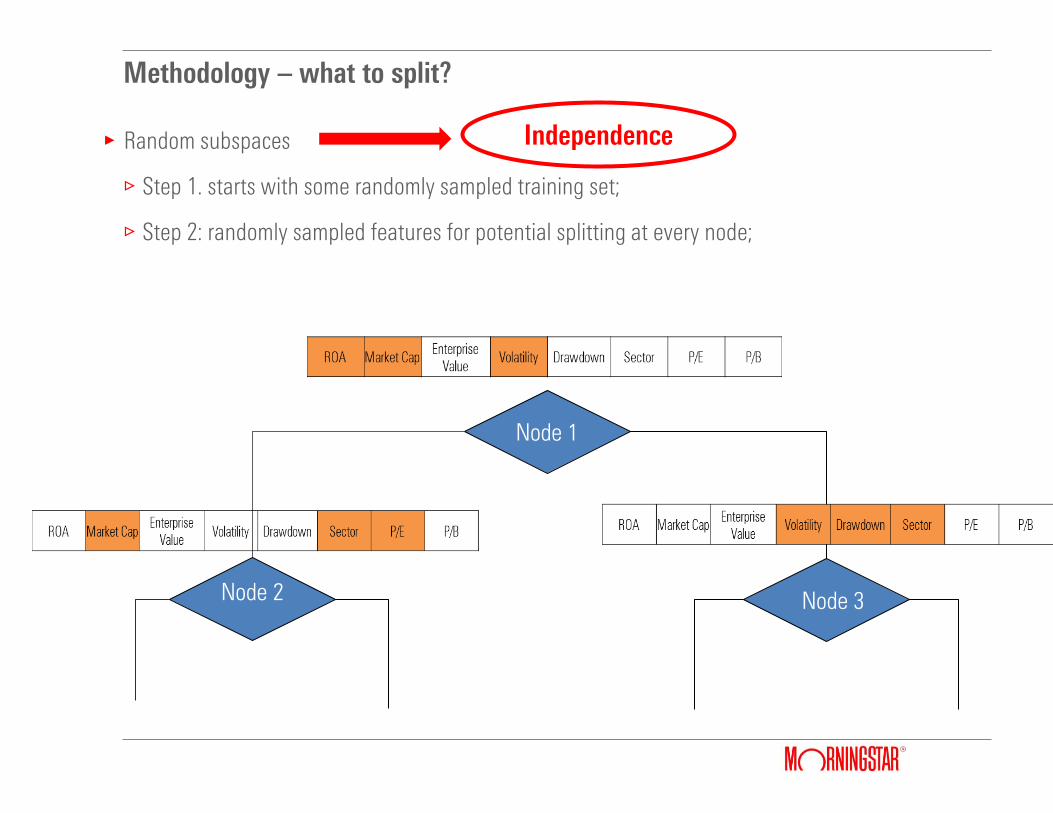

Methodology – what to split?

gRandom subspaces

/Step 1. starts with some randomly sampled training set;

Methodology – what to split?

gRandom subspaces

/Step 1. starts with some randomly sampled training set;

/Step 2: randomly sampled features for potential splitting candidate, at every node;

Node 1

Node 2 Node 3

Methodology – what to split?

gRandom subspaces

/Step 1. starts with some randomly sampled training set;

/Step 2: randomly sampled features for potential splitting at every node;

Node 1

Node 2 Node 3

Independence

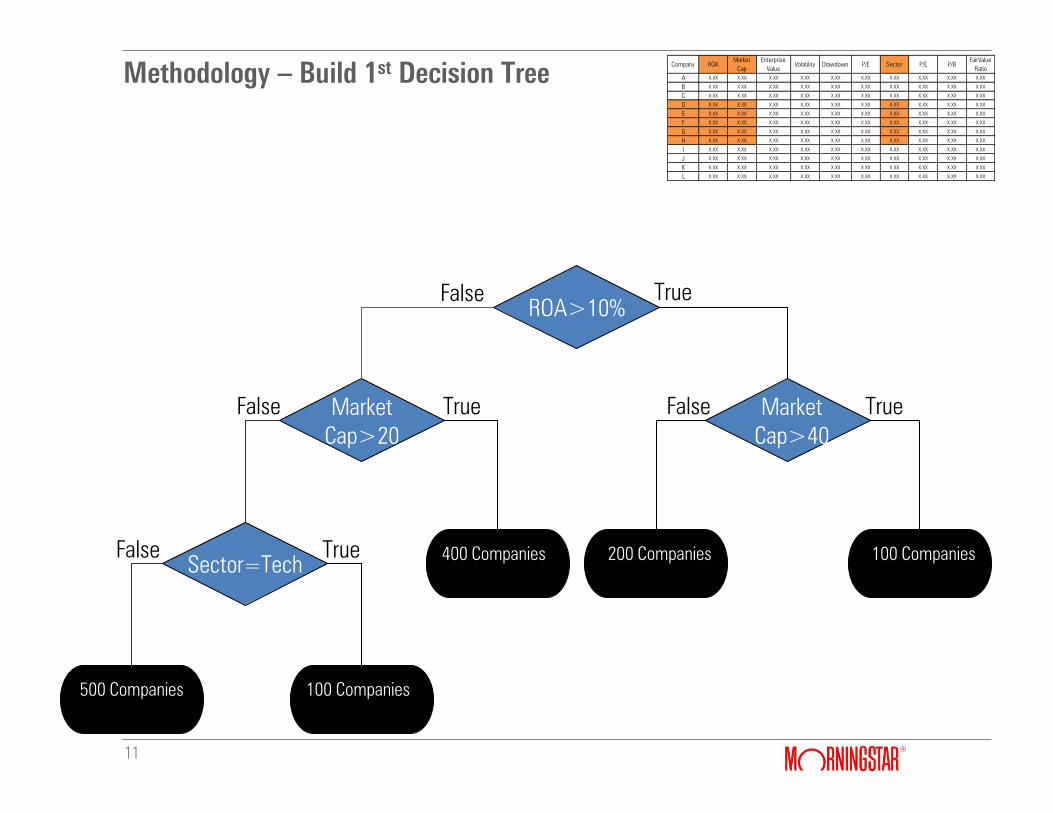

Methodology – Build 1st Decision Tree

11

ROA>10%

Market

Cap>20

Market

Cap>40

Sector=Tech

True False

False False True True

500 Companies 500 Companies

Avg P/FV = 0.8

False True

100 Companies

400 Companies

200 Companies

100 Companies

Company ROA

Market

Cap

Enterprise

Value

Volatility Drawdown P/E Sector P/E P/B

FairValue

Ratio

A X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

B X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

C X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

D X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

E X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

F X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

G X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

H X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

I X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

J X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

K X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

L X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

Methodology – Build 1st Decision Tree

12

ROA>10%

Market

Cap>20

Market

Cap>40

Sector=Tech

True False

False False True True

500 Companies

Avg P/FV = 0.8

500 Companies

Avg P/FV = 0.8

False True

100 Companies

Avg P/FV = 1.0

400 Companies

Avg P/FV = 1.2

200 Companies

Avg P/FV = 0.8

100 Companies

Avg P/FV = 1.8

Company ROA

Market

Cap

Enterprise

Value

Volatility Drawdown P/E Sector P/E P/B

FairValue

Ratio

A X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

B X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

C X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

D X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

E X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

F X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

G X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

H X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

I X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

J X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

K X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

L X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

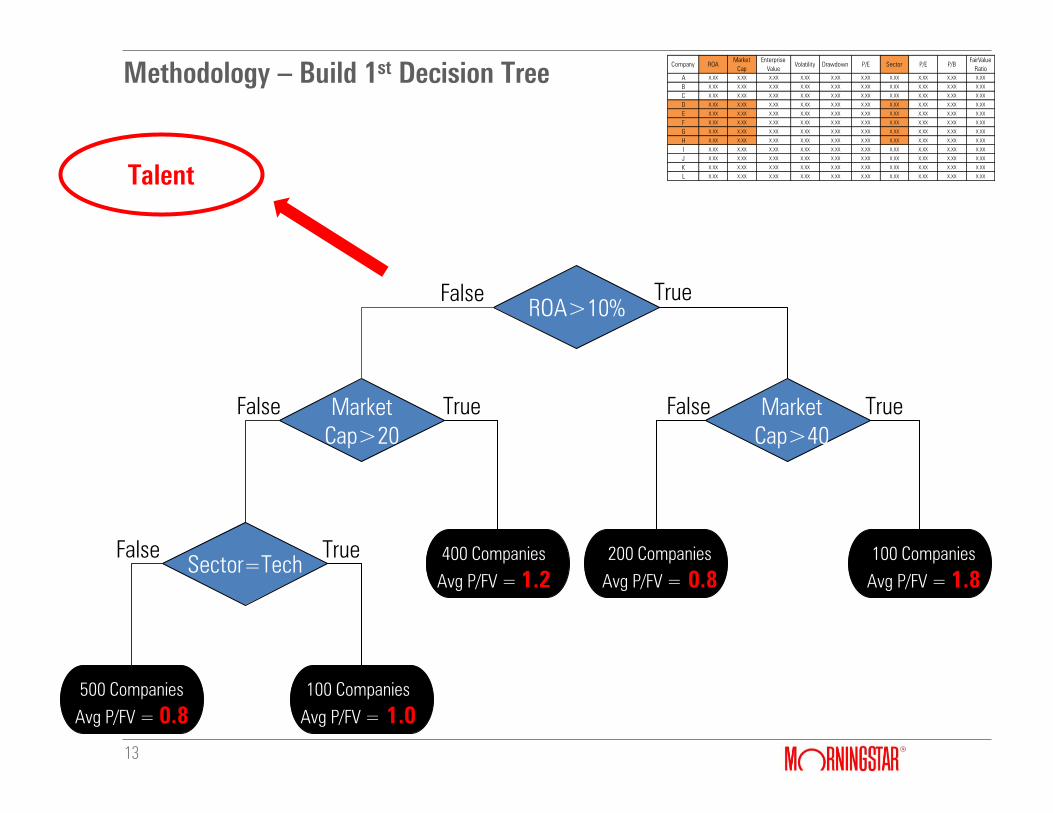

Methodology – Build 1st Decision Tree

13

ROA>10%

Market

Cap>20

Market

Cap>40

Sector=Tech

True False

False False True True

500 Companies

Avg P/FV = 0.8

500 Companies

Avg P/FV = 0.8

False True

100 Companies

Avg P/FV = 1.0

400 Companies

Avg P/FV = 1.2

200 Companies

Avg P/FV = 0.8

100 Companies

Avg P/FV = 1.8

Company ROA

Market

Cap

Enterprise

Value

Volatility Drawdown P/E Sector P/E P/B

FairValue

Ratio

A X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

B X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

C X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

D X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

E X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

F X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

G X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

H X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

I X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

J X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

K X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

L X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XXTalent

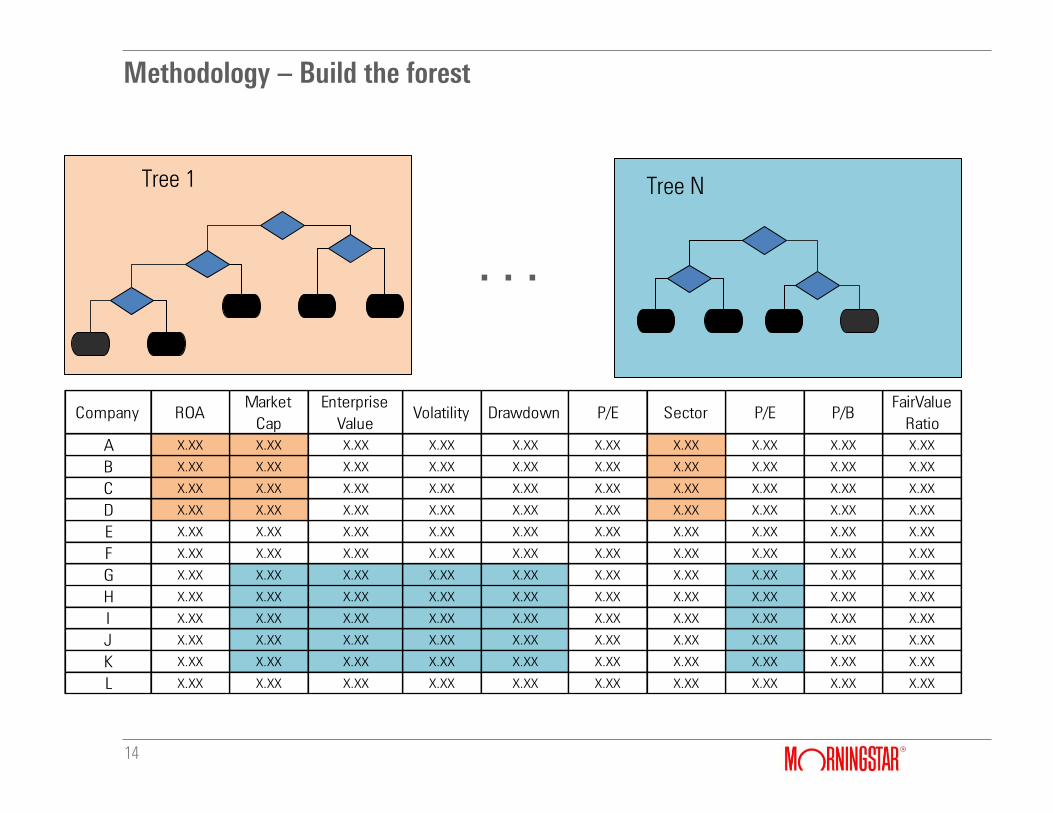

Methodology – Build the forest

14

Tree 1 Tree N

Company ROA

Market

Cap

Enterprise

Value

Volatility Drawdown P/E Sector P/E P/B

FairValue

Ratio

A X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

B X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

C X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

D X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

E X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

F X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

G X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

H X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

I X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

J X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

K X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

L X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

…

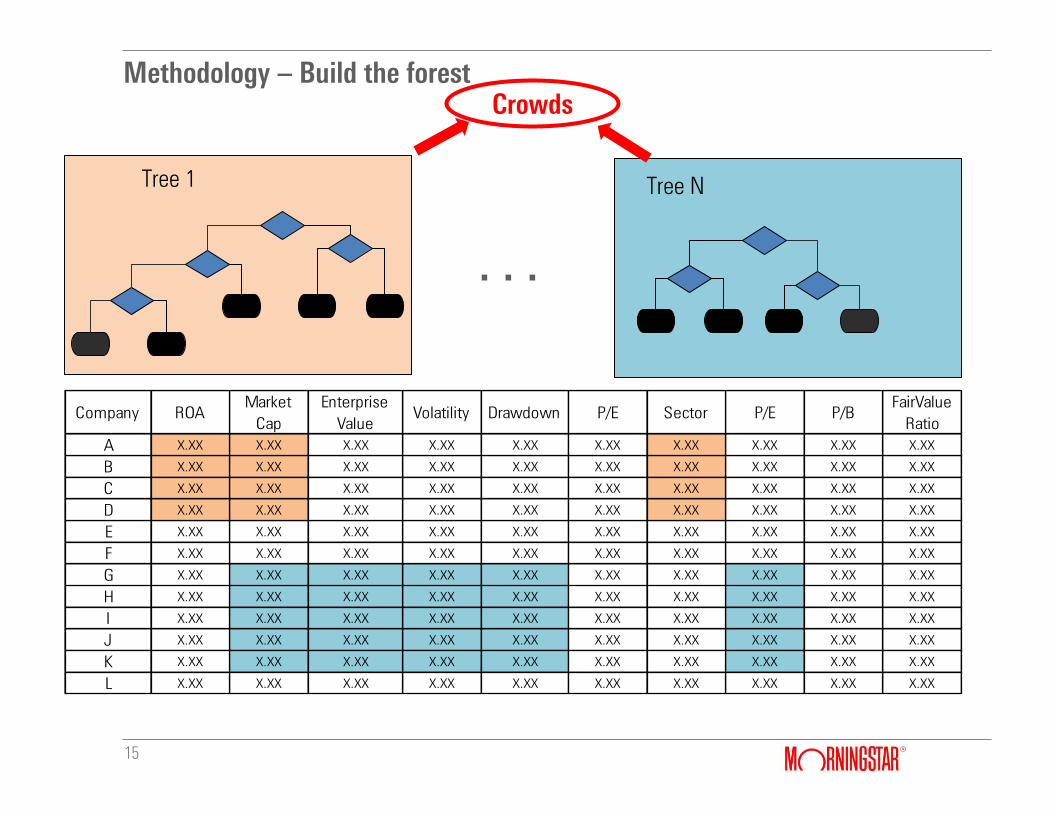

Methodology – Build the forest

15

Tree 1 Tree N

Company ROA

Market

Cap

Enterprise

Value

Volatility Drawdown P/E Sector P/E P/B

FairValue

Ratio

A X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

B X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

C X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

D X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

E X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

F X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

G X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

H X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

I X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

J X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

K X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

L X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX X.XX

…

Crowds

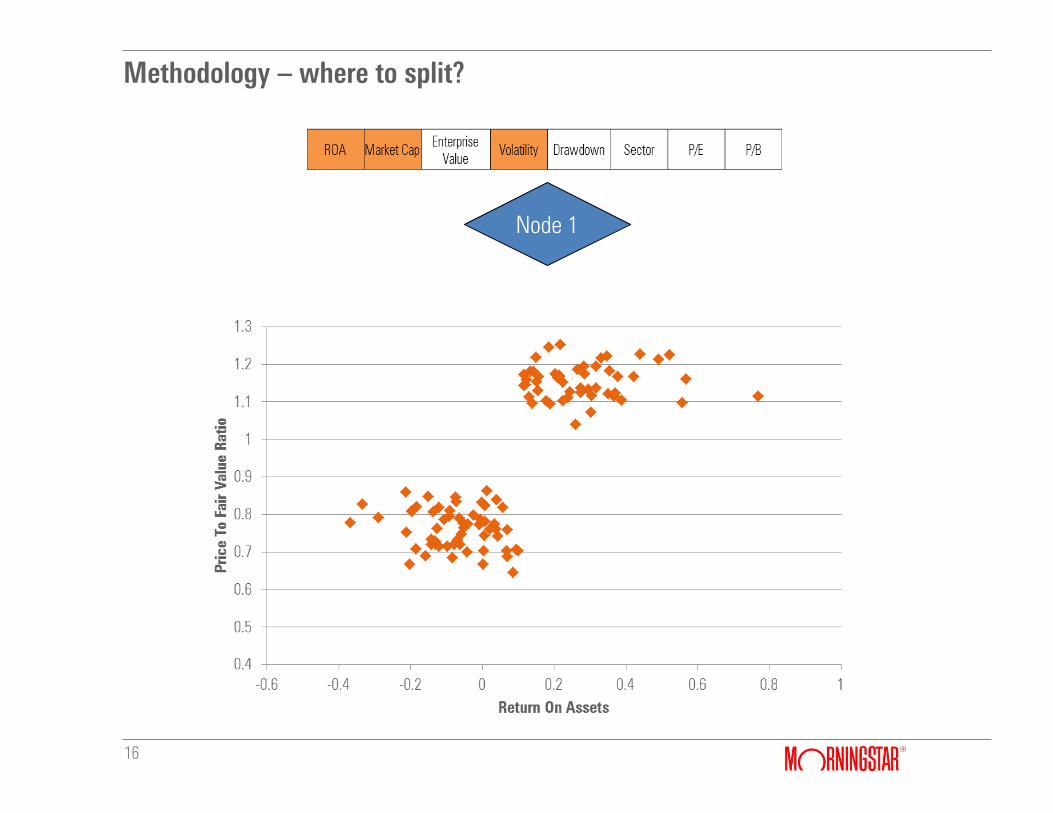

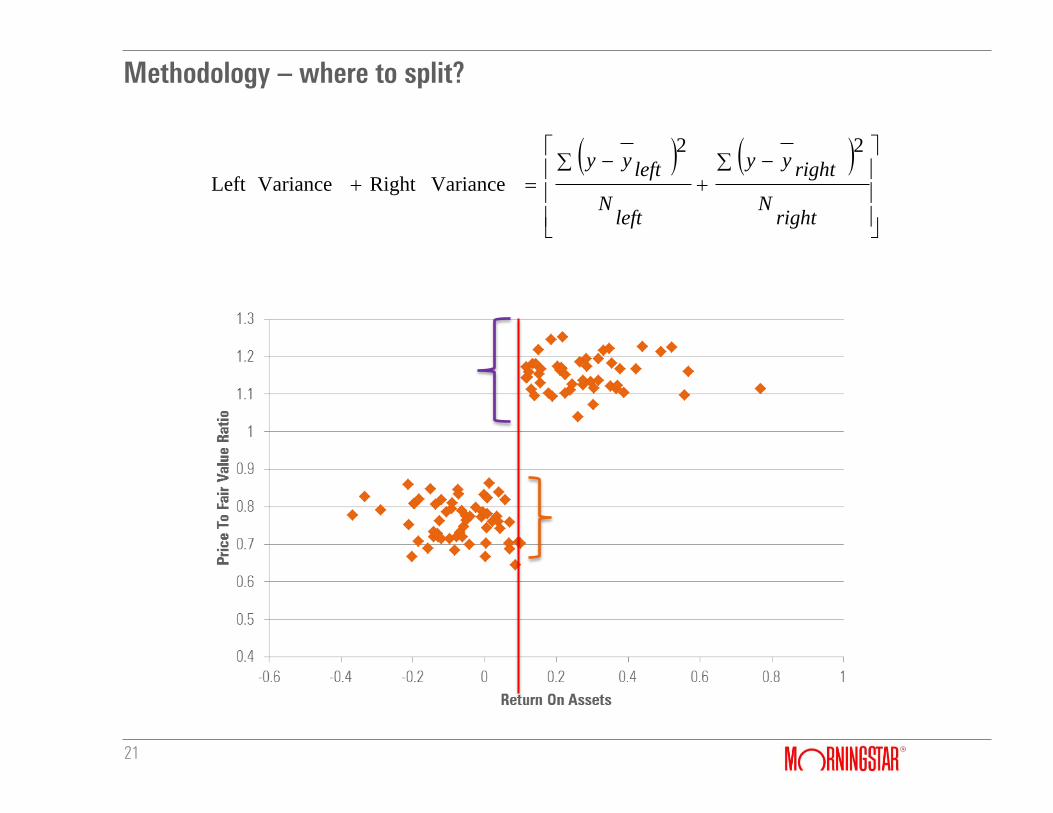

Methodology – where to split?

16

Node 1

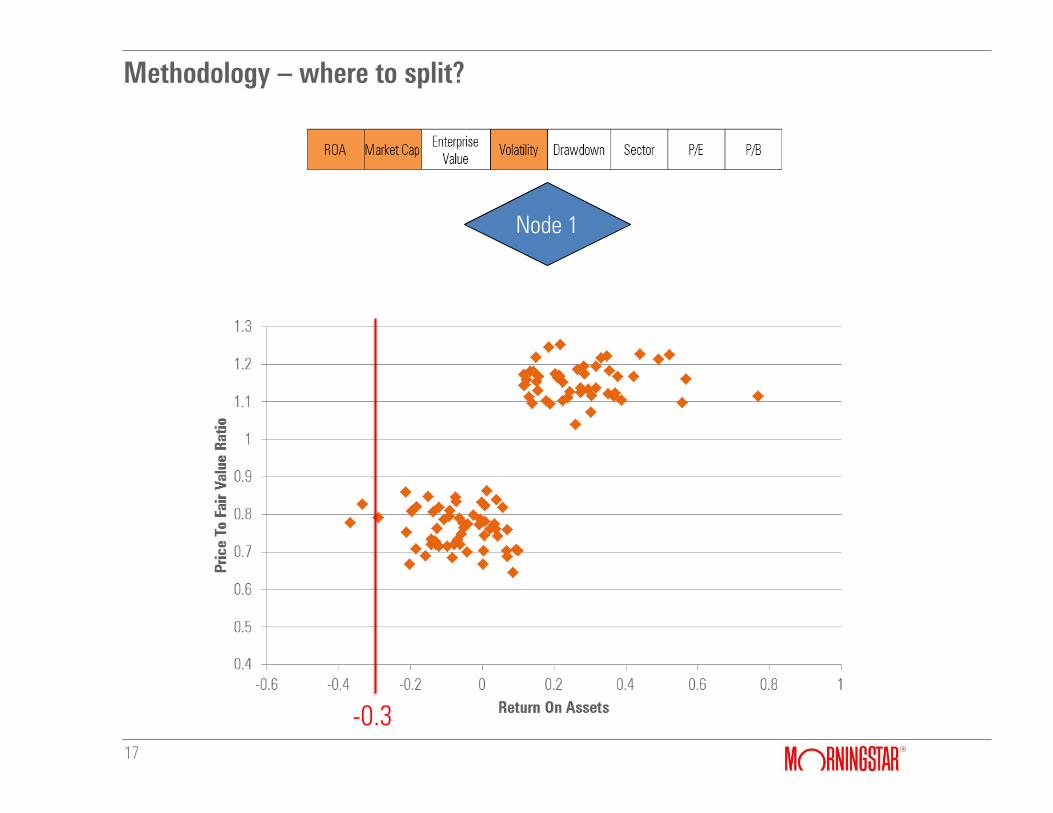

Methodology – where to split?

17

Node 1

-0.3

Methodology – where to split?

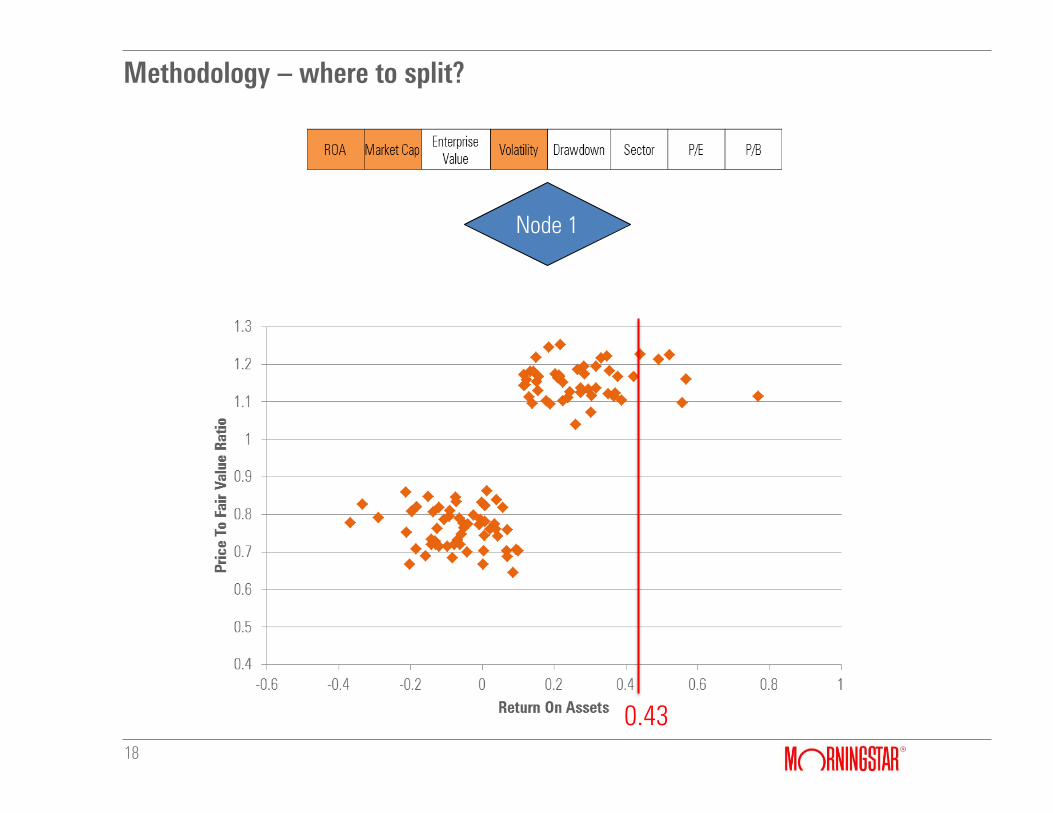

18

Node 1

0.43

Methodology – where to split?

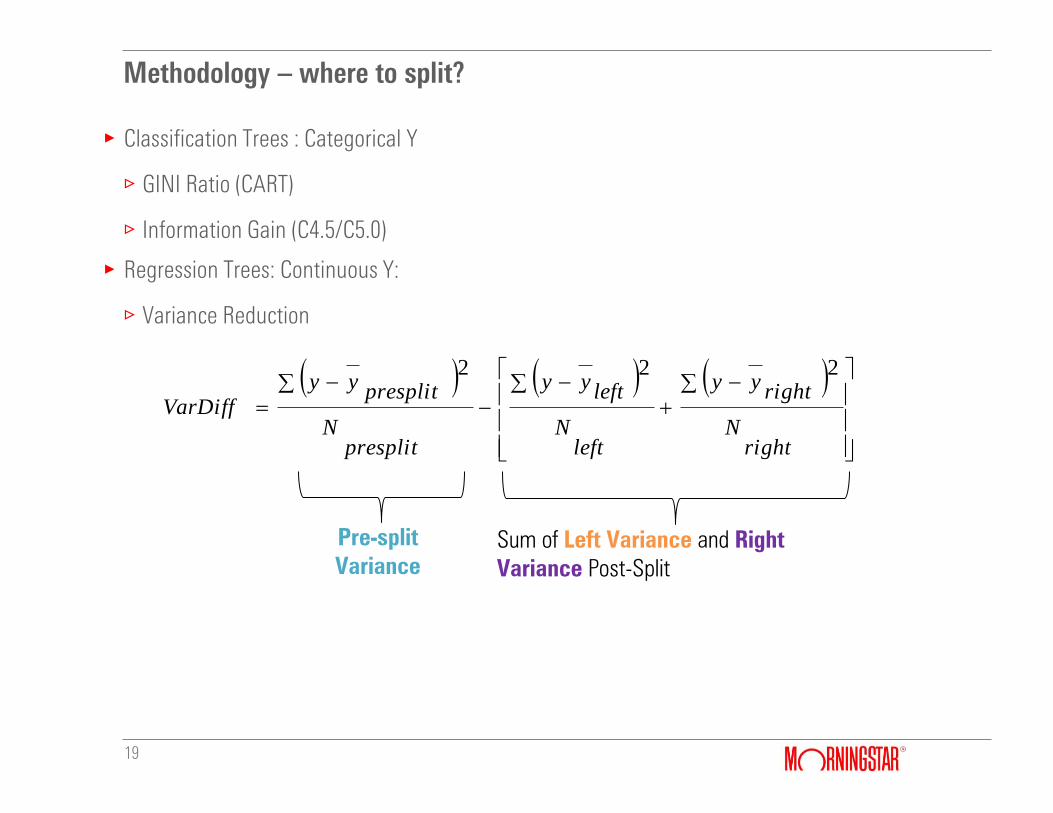

19

gClassification Trees : Categorical Y

/GINI Ratio (CART)

/ Information Gain (C4.5/C5.0)

gRegression Trees: Continuous Y:

/Variance Reduction

Pre-split

Variance

Sum of Left Variance and Right

Variance Post-Split

rightN

rightyy

leftN

leftyy

presplitN

presplityy

VarDiff

222

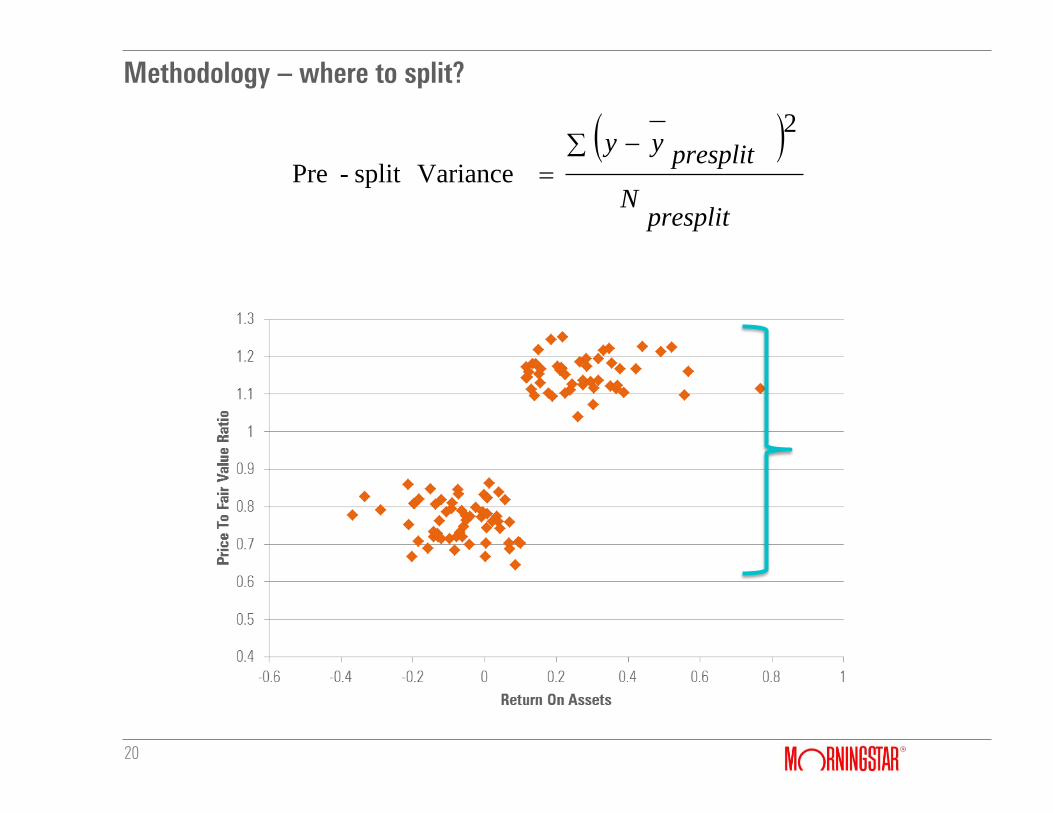

Methodology – where to split?

20

presplitN

presplityy

2

Variancesplit -Pre

Methodology – where to split?

21

rightN

rightyy

leftN

leftyy22

VarianceRight VarianceLeft

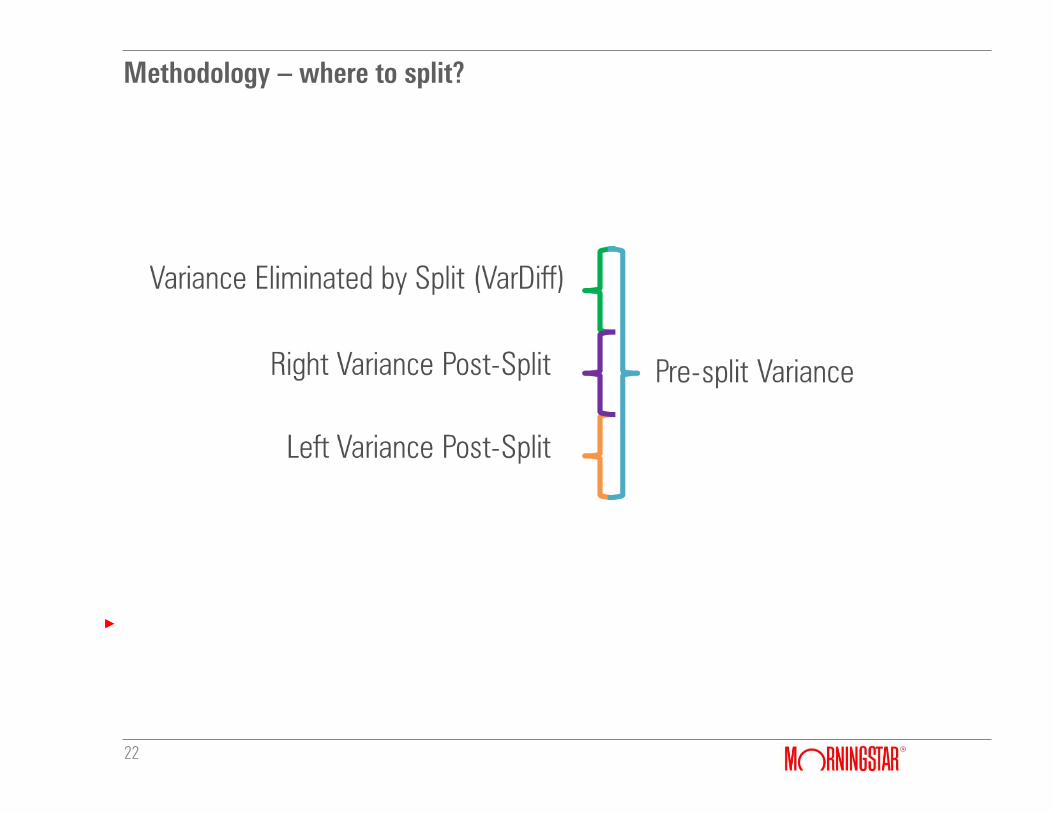

Methodology – where to split?

22

g

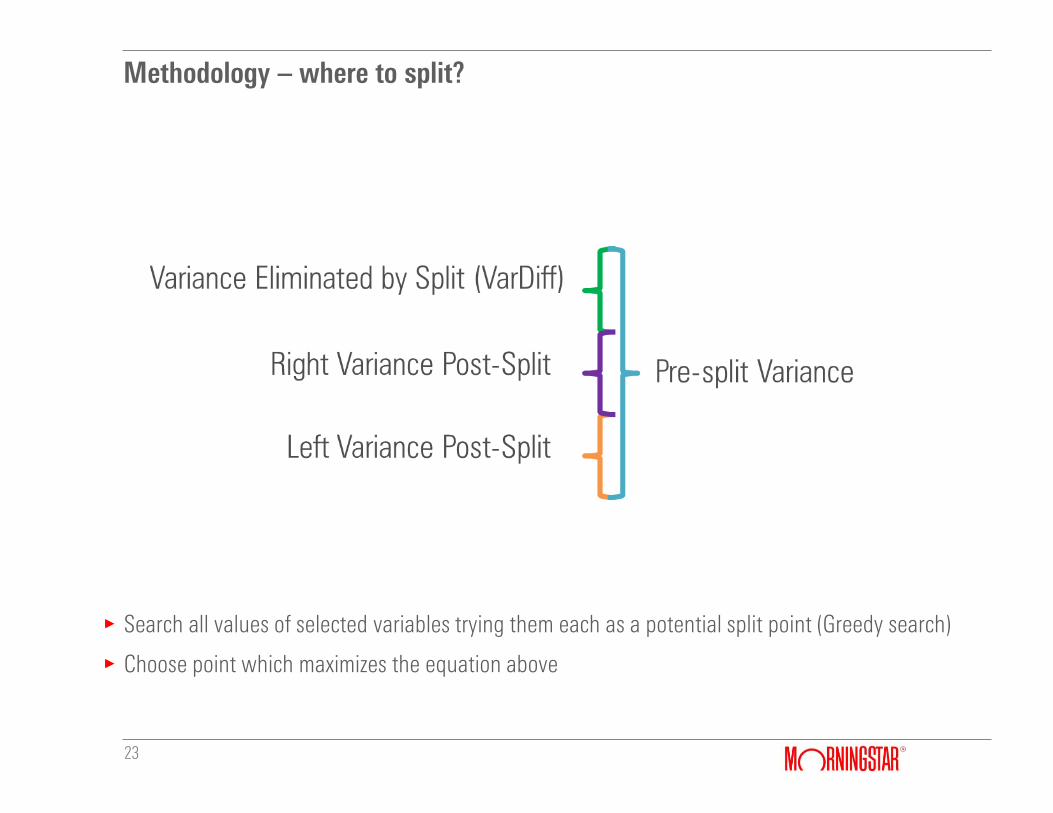

Methodology – where to split?

23

gSearch all values of selected variables trying them each as a potential split point (Greedy search)

gChoose point which maximizes the equation above

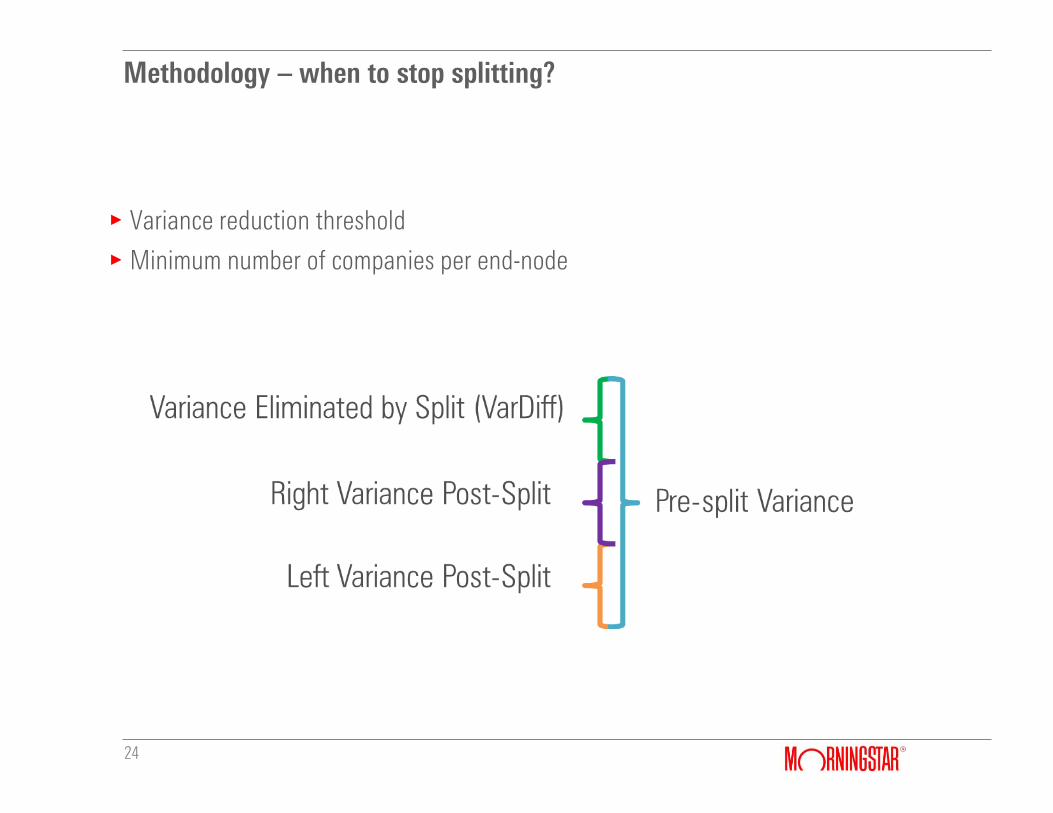

Methodology – when to stop splitting?

24

gVariance reduction threshold

gMinimum number of companies per end-node

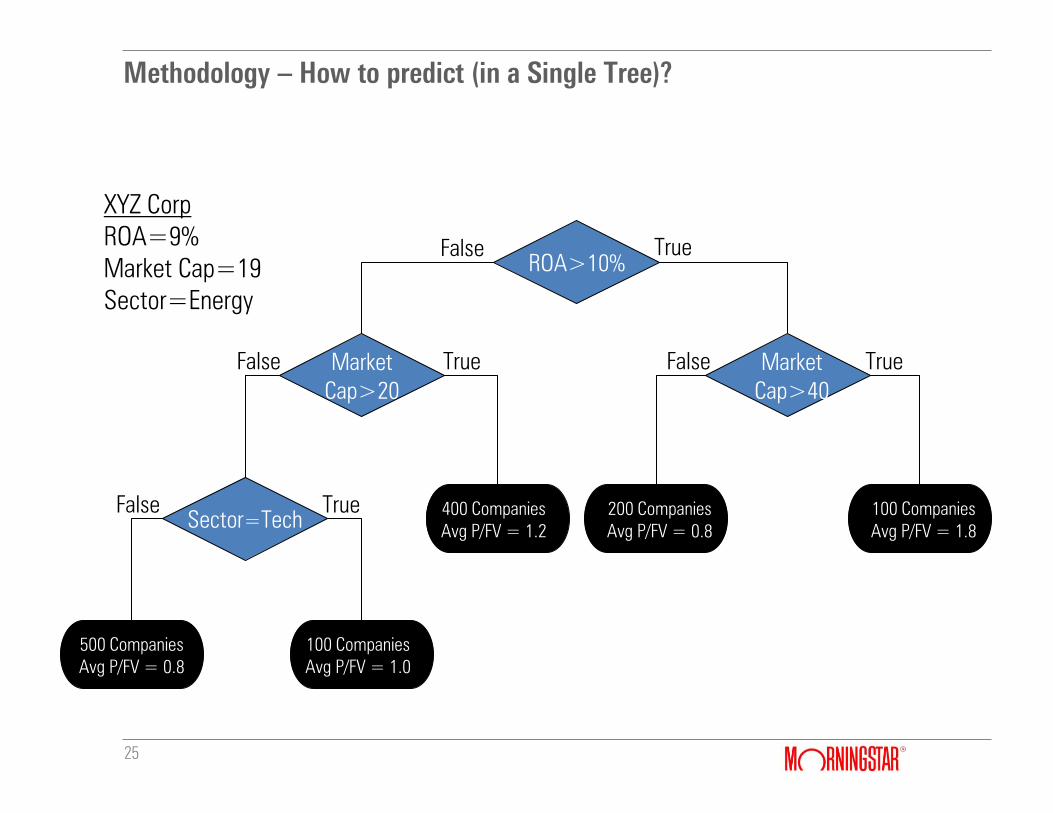

Methodology – How to predict (in a Single Tree)?

25

ROA>10%

Market

Cap>20

Market

Cap>40

Sector=Tech

True False

False False True True

500 Companies

Avg P/FV = 0.8

500 Companies

Avg P/FV = 0.8

XYZ Corp

ROA=9%

Market Cap=19

Sector=Energy

False True

100 Companies

Avg P/FV = 1.0

400 Companies

Avg P/FV = 1.2

200 Companies

Avg P/FV = 0.8

100 Companies

Avg P/FV = 1.8

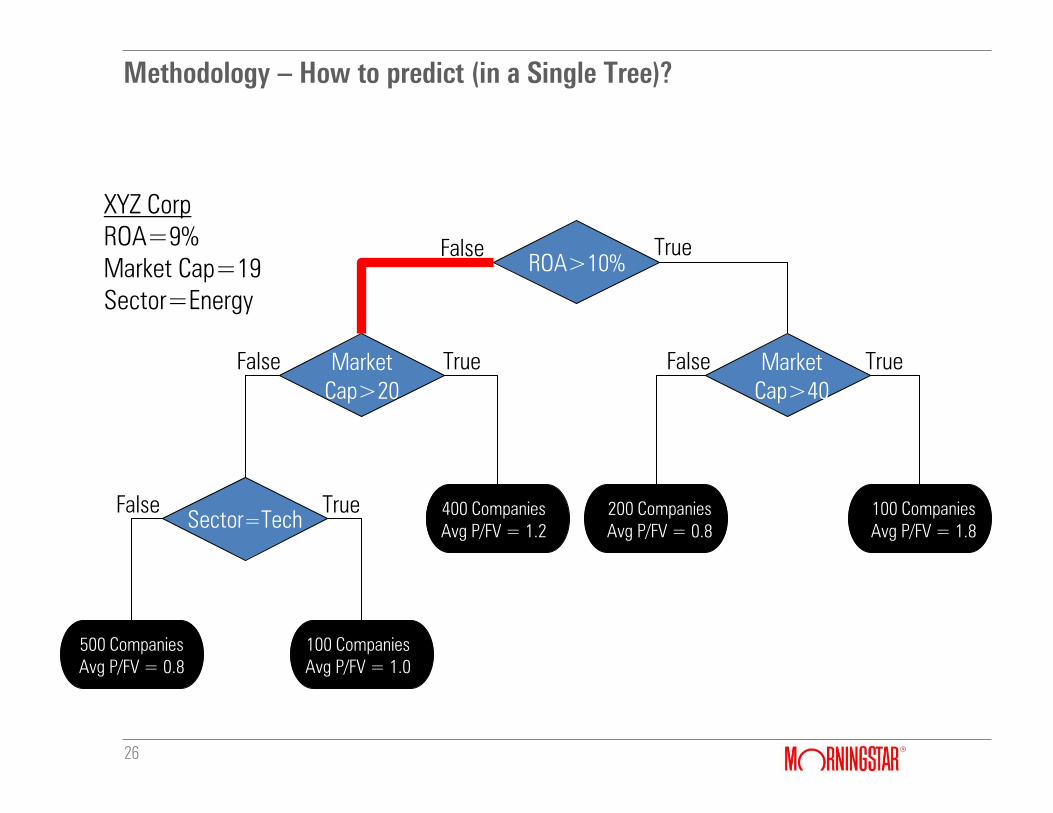

Methodology – How to predict (in a Single Tree)?

26

ROA>10%

Market

Cap>20

Market

Cap>40

Sector=Tech

True False

False False True True

500 Companies

Avg P/FV = 0.8

500 Companies

Avg P/FV = 0.8

XYZ Corp

ROA=9%

Market Cap=19

Sector=Energy

False True

100 Companies

Avg P/FV = 1.0

400 Companies

Avg P/FV = 1.2

200 Companies

Avg P/FV = 0.8

100 Companies

Avg P/FV = 1.8

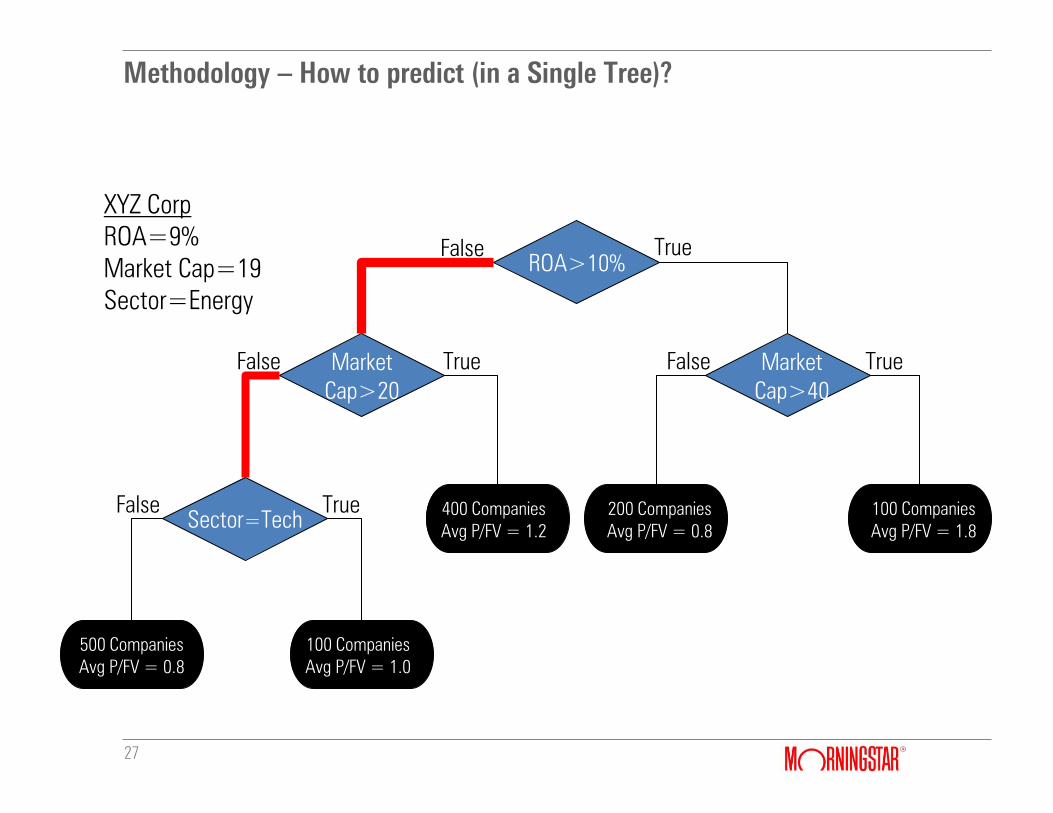

Methodology – How to predict (in a Single Tree)?

27

ROA>10%

Market

Cap>20

Market

Cap>40

Sector=Tech

True False

False False True True

500 Companies

Avg P/FV = 0.8

500 Companies

Avg P/FV = 0.8

XYZ Corp

ROA=9%

Market Cap=19

Sector=Energy

False True

100 Companies

Avg P/FV = 1.0

400 Companies

Avg P/FV = 1.2

200 Companies

Avg P/FV = 0.8

100 Companies

Avg P/FV = 1.8

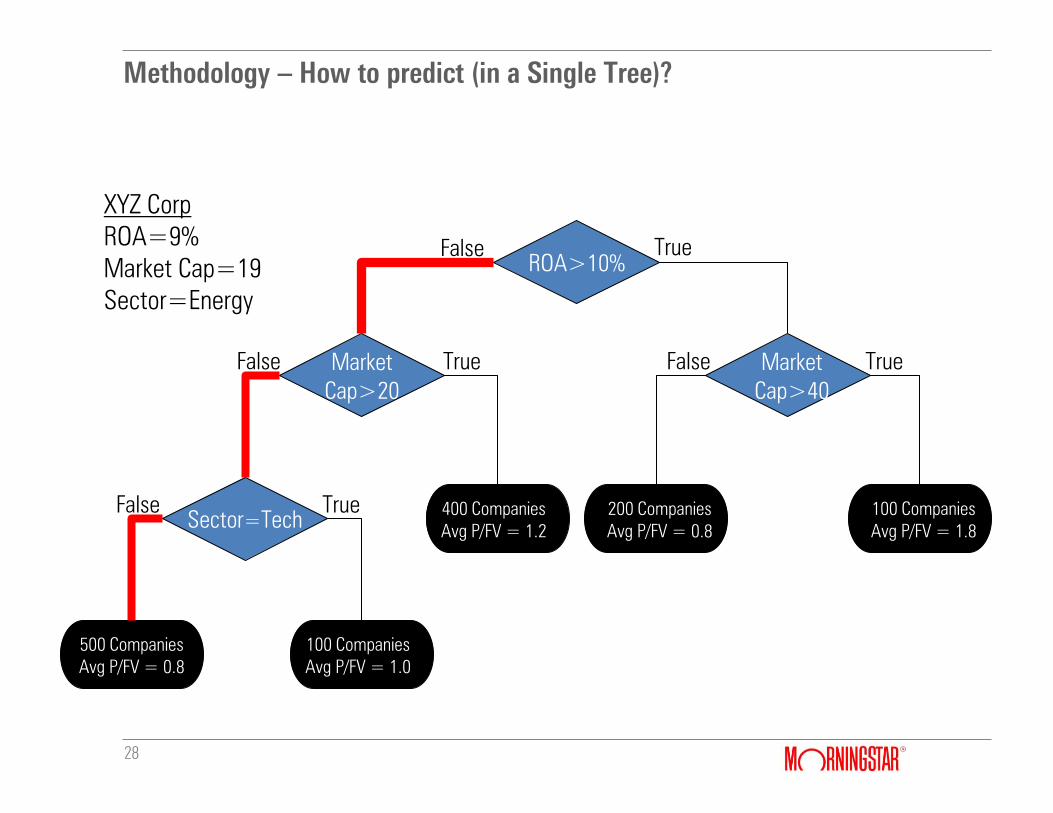

Methodology – How to predict (in a Single Tree)?

28

ROA>10%

Market

Cap>20

Market

Cap>40

Sector=Tech

True False

False False True True

500 Companies

Avg P/FV = 0.8

500 Companies

Avg P/FV = 0.8

XYZ Corp

ROA=9%

Market Cap=19

Sector=Energy

False True

100 Companies

Avg P/FV = 1.0

400 Companies

Avg P/FV = 1.2

200 Companies

Avg P/FV = 0.8

100 Companies

Avg P/FV = 1.8

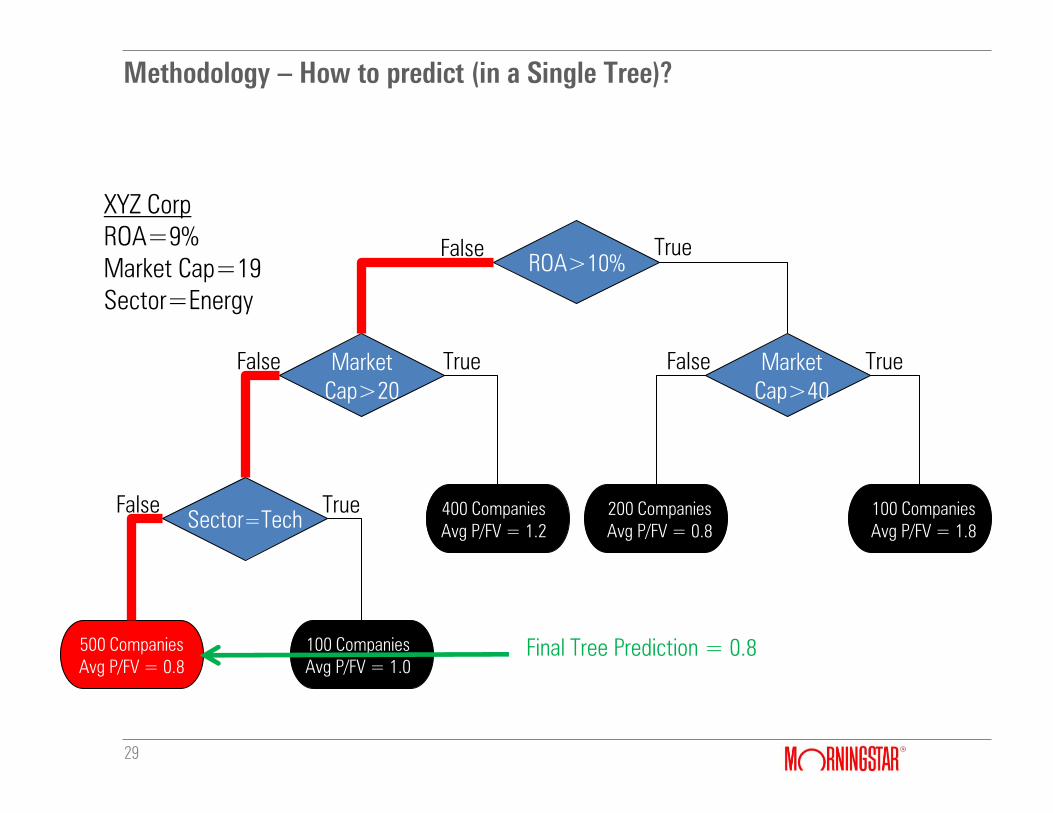

Methodology – How to predict (in a Single Tree)?

29

ROA>10%

Market

Cap>20

Market

Cap>40

Sector=Tech

True False

False False True True

500 Companies

Avg P/FV = 0.8

500 Companies

Avg P/FV = 0.8

XYZ Corp

ROA=9%

Market Cap=19

Sector=Energy

False

Final Tree Prediction = 0.8

True

100 Companies

Avg P/FV = 1.0

400 Companies

Avg P/FV = 1.2

200 Companies

Avg P/FV = 0.8

100 Companies

Avg P/FV = 1.8

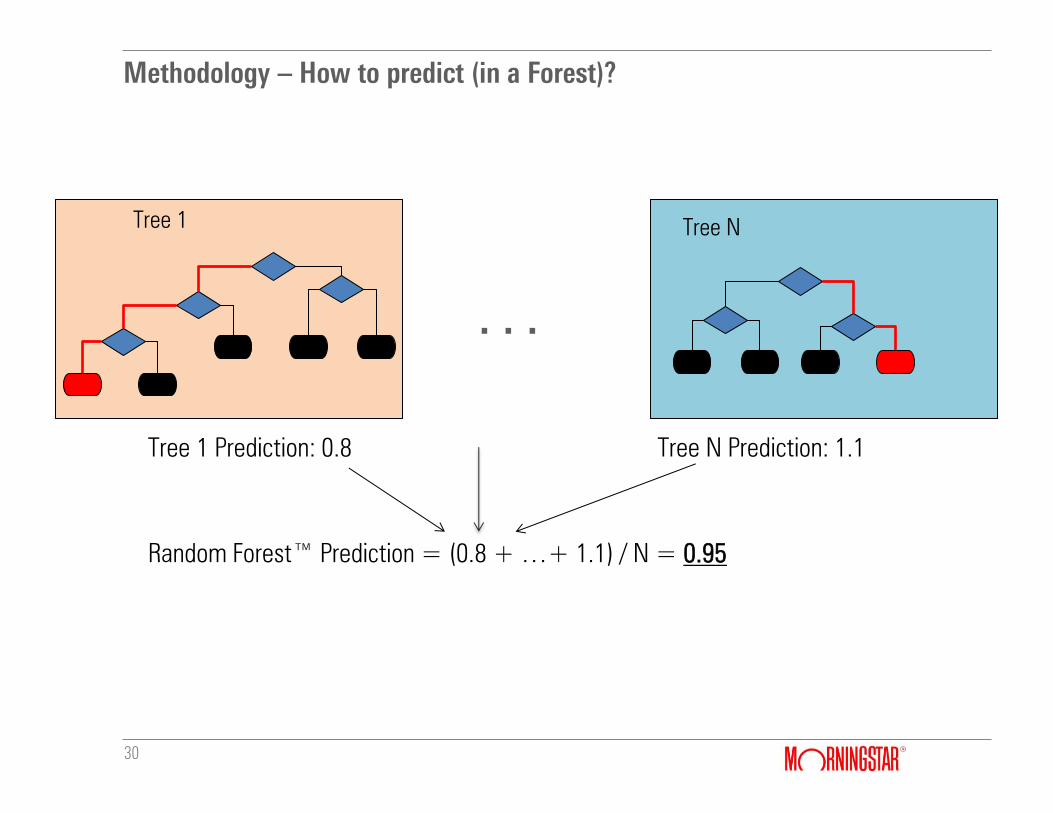

Methodology – How to predict (in a Forest)?

30

Tree 1 Prediction: 0.8 Tree N Prediction: 1.1

Random Forest™ Prediction = (0.8 + …+ 1.1) / N = 0.95

Tree 1 Tree N

…

31

Methodology – How to predict (in a Forest)?

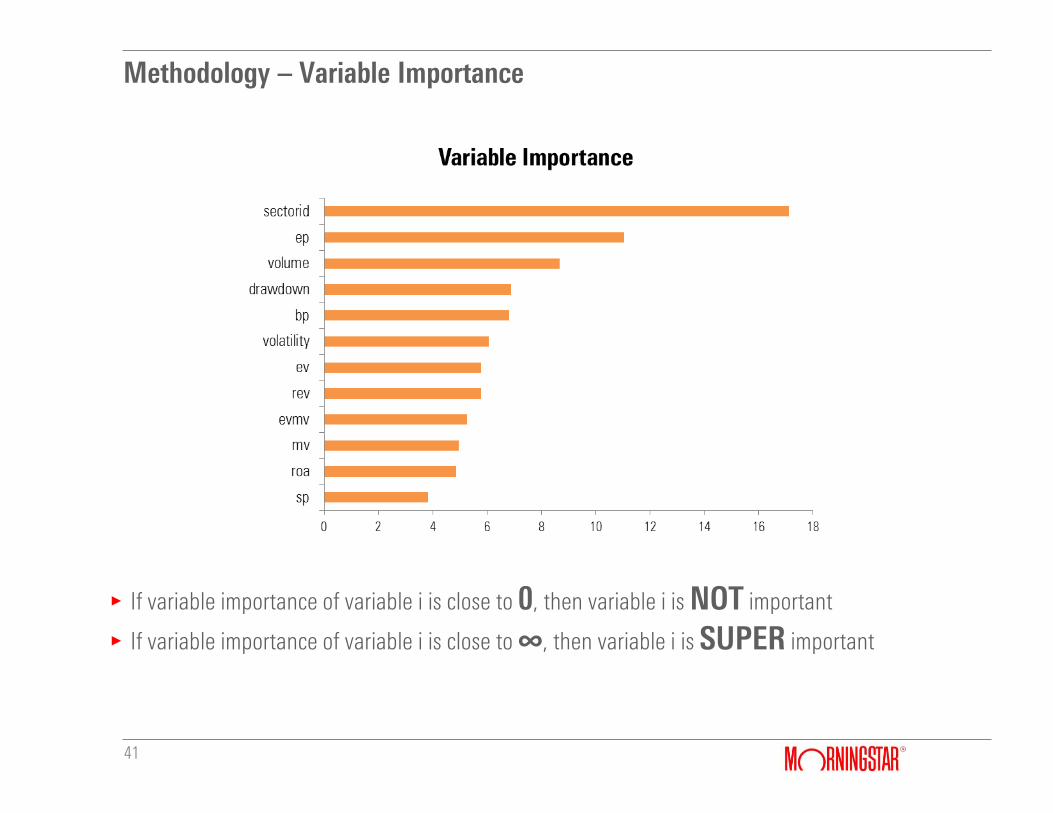

Methodology – Variable Importance

32

gWhat variables or features are important for our prediction, ROA or Market Cap?

Methodology – Variable Importance

33

gWhat variables or features are important for our prediction, ROA or Market Cap?

gOOB (Out-Of-Bag) Error Rate

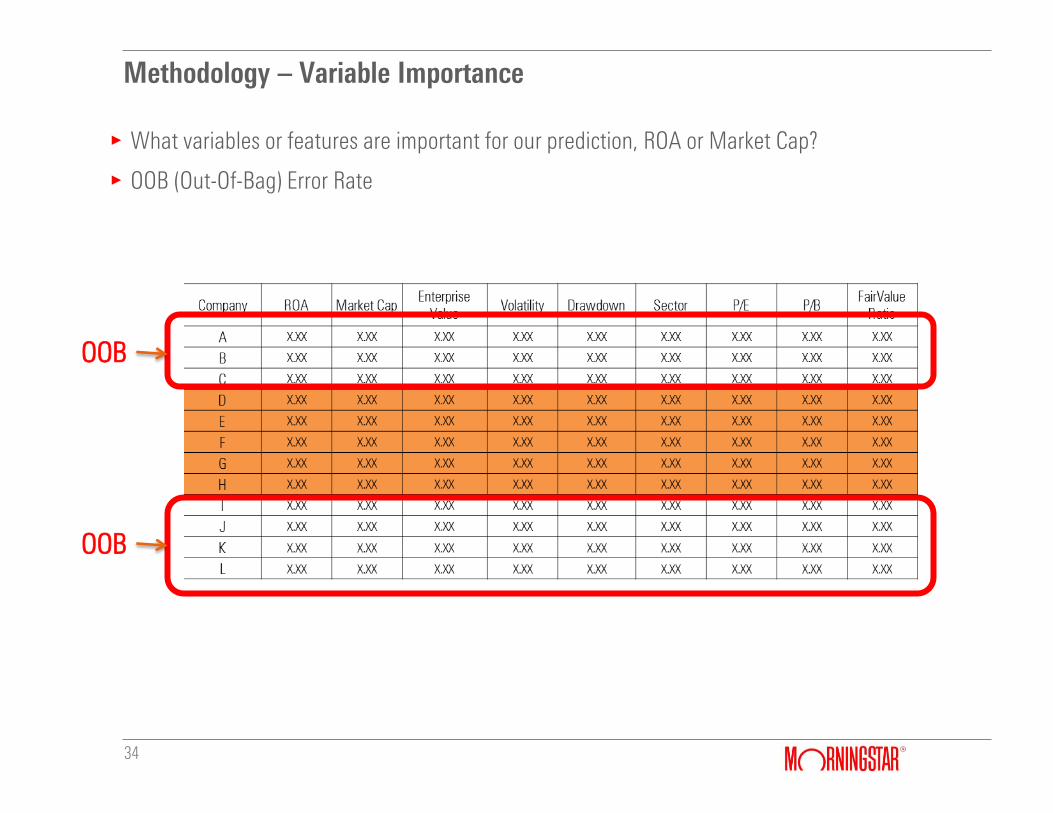

Methodology – Variable Importance

34

gWhat variables or features are important for our prediction, ROA or Market Cap?

gOOB (Out-Of-Bag) Error Rate

OOB

OOB

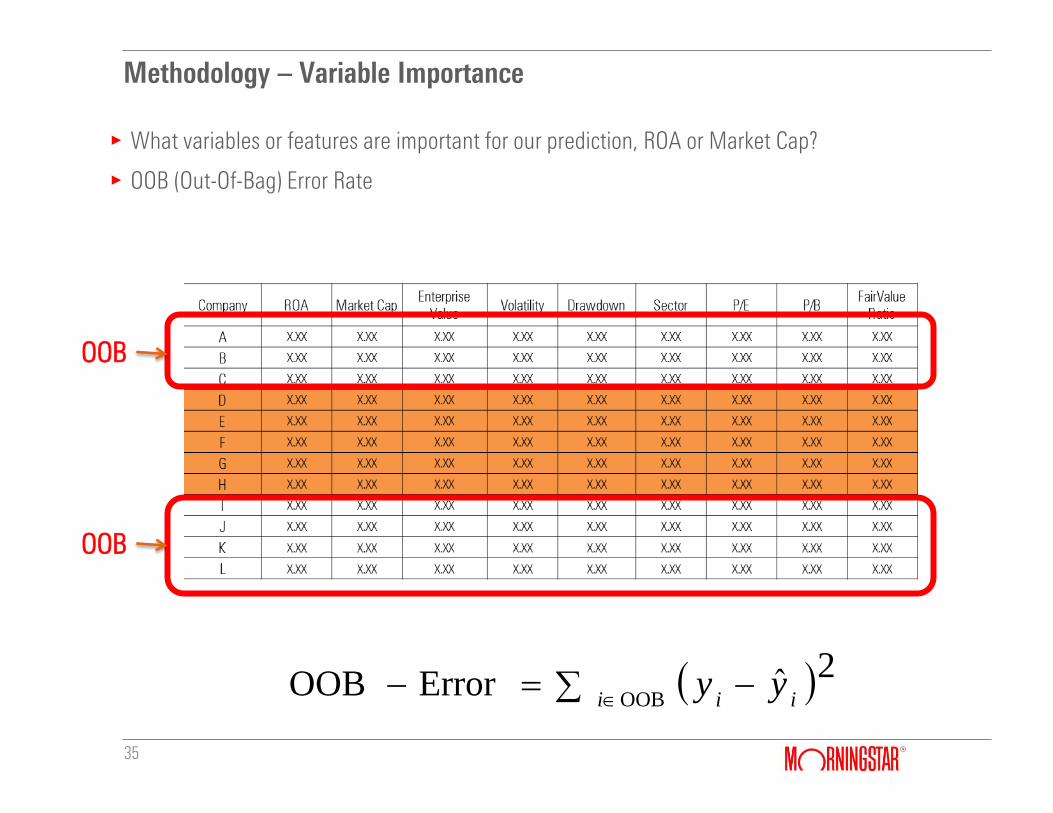

Methodology – Variable Importance

35

gWhat variables or features are important for our prediction, ROA or Market Cap?

gOOB (Out-Of-Bag) Error Rate

OOB

OOB

2ˆErrorOOBOOB iii

yy

Methodology – Variable Importance

36

gWhat variables or features are important for our prediction, ROA or Market Cap?

gOOB (Out-Of-Bag) Error Rate

gVariable Importance

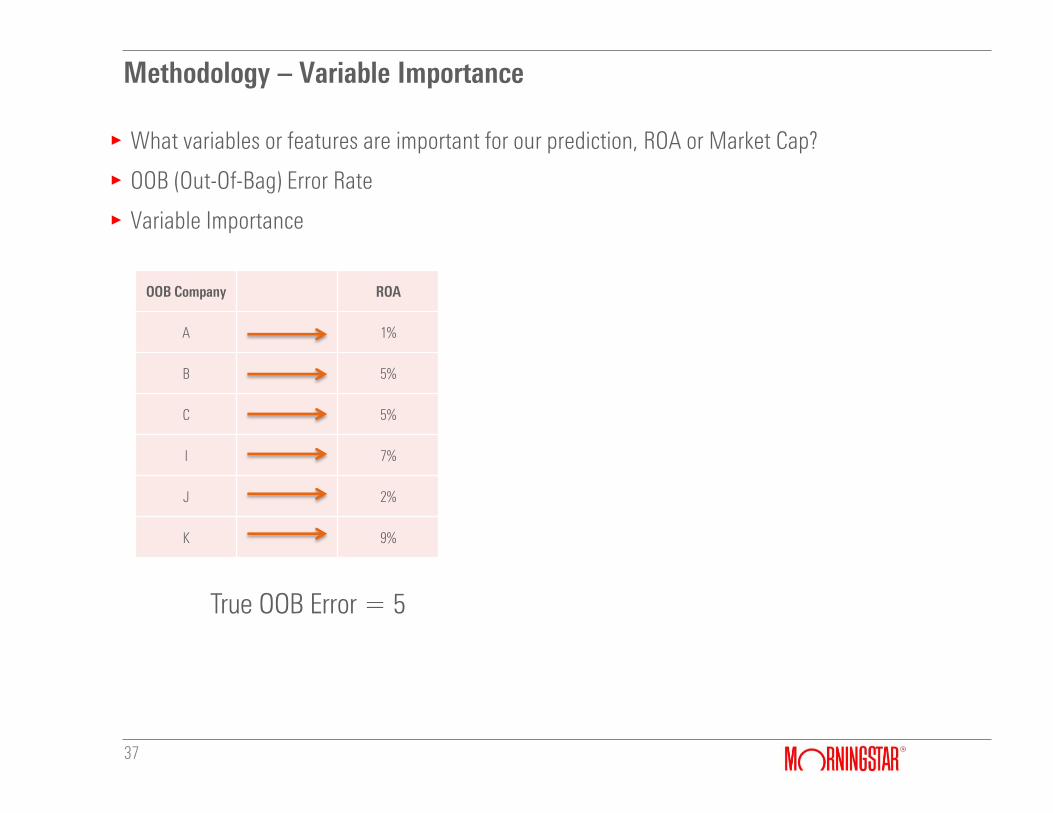

Methodology – Variable Importance

37

gWhat variables or features are important for our prediction, ROA or Market Cap?

gOOB (Out-Of-Bag) Error Rate

gVariable Importance

OOB Company ROA

A 1%

B 5%

C 5%

I 7%

J 2%

K 9%

True OOB Error = 5

Methodology – Variable Importance

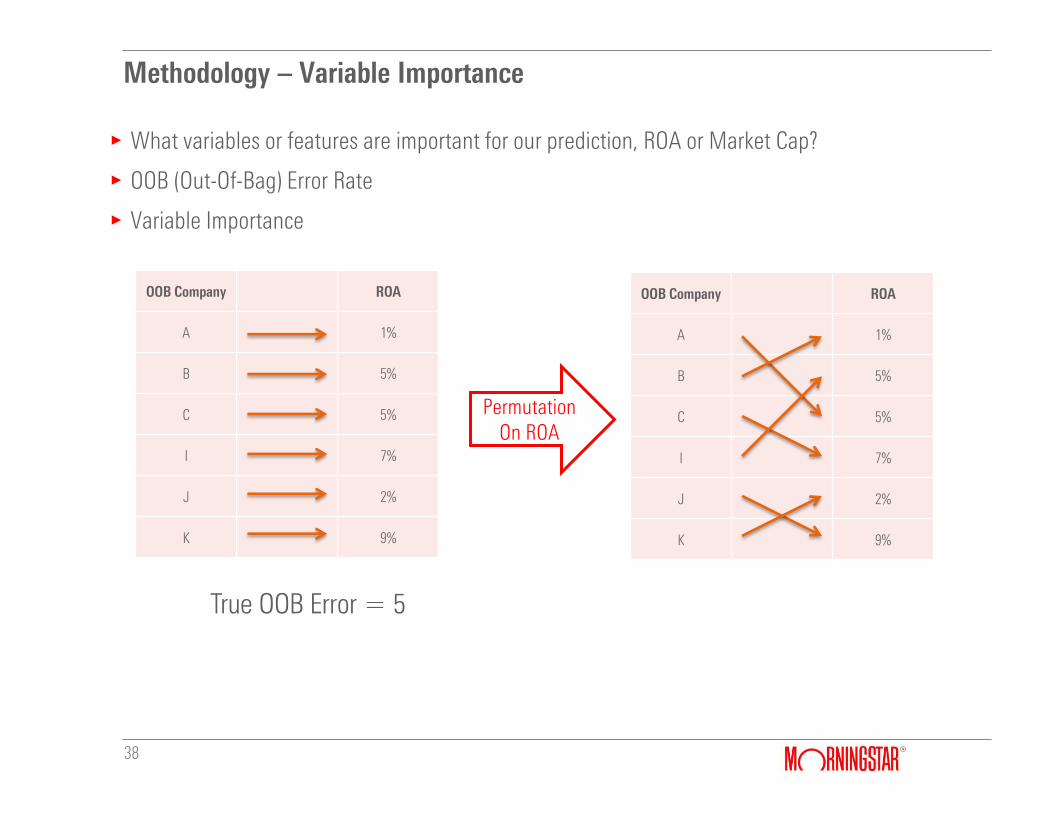

38

gWhat variables or features are important for our prediction, ROA or Market Cap?

gOOB (Out-Of-Bag) Error Rate

gVariable Importance

OOB Company ROA

A 1%

B 5%

C 5%

I 7%

J 2%

K 9%

OOB Company ROA

A 1%

B 5%

C 5%

I 7%

J 2%

K 9%

Permutation On ROA

True OOB Error = 5

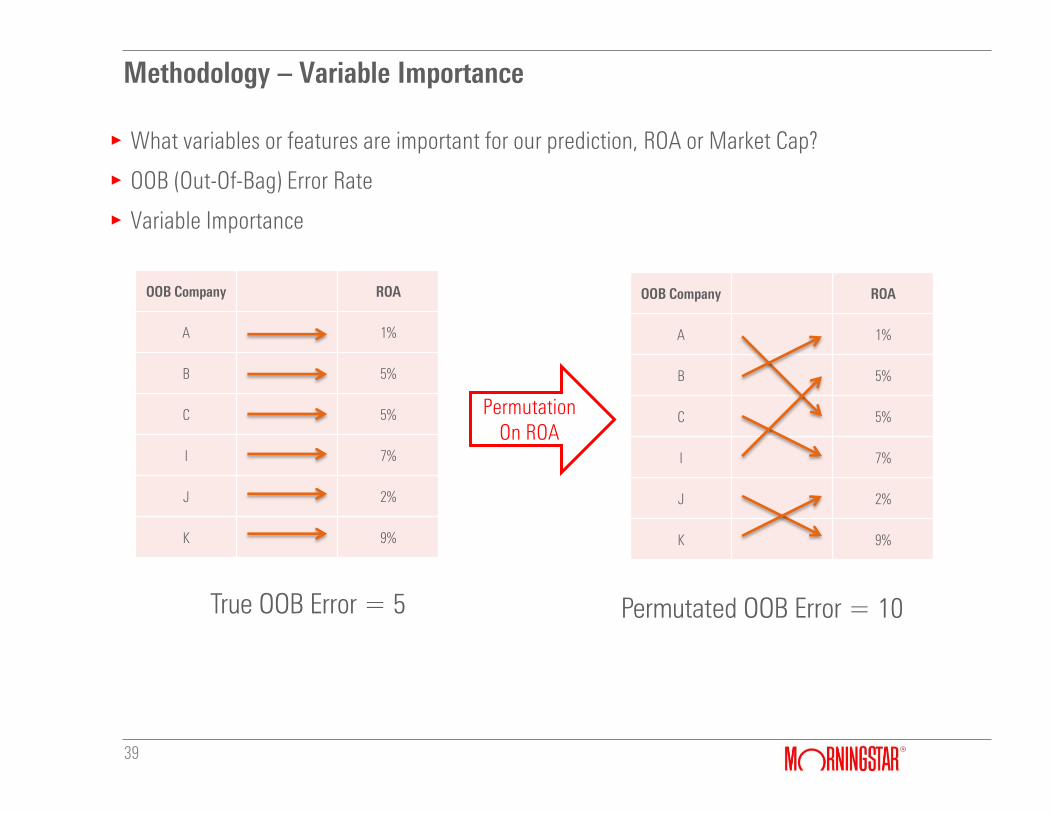

Methodology – Variable Importance

39

gWhat variables or features are important for our prediction, ROA or Market Cap?

gOOB (Out-Of-Bag) Error Rate

gVariable Importance

OOB Company ROA

A 1%

B 5%

C 5%

I 7%

J 2%

K 9%

OOB Company ROA

A 1%

B 5%

C 5%

I 7%

J 2%

K 9%

Permutation On ROA

True OOB Error = 5 Permutated OOB Error = 10

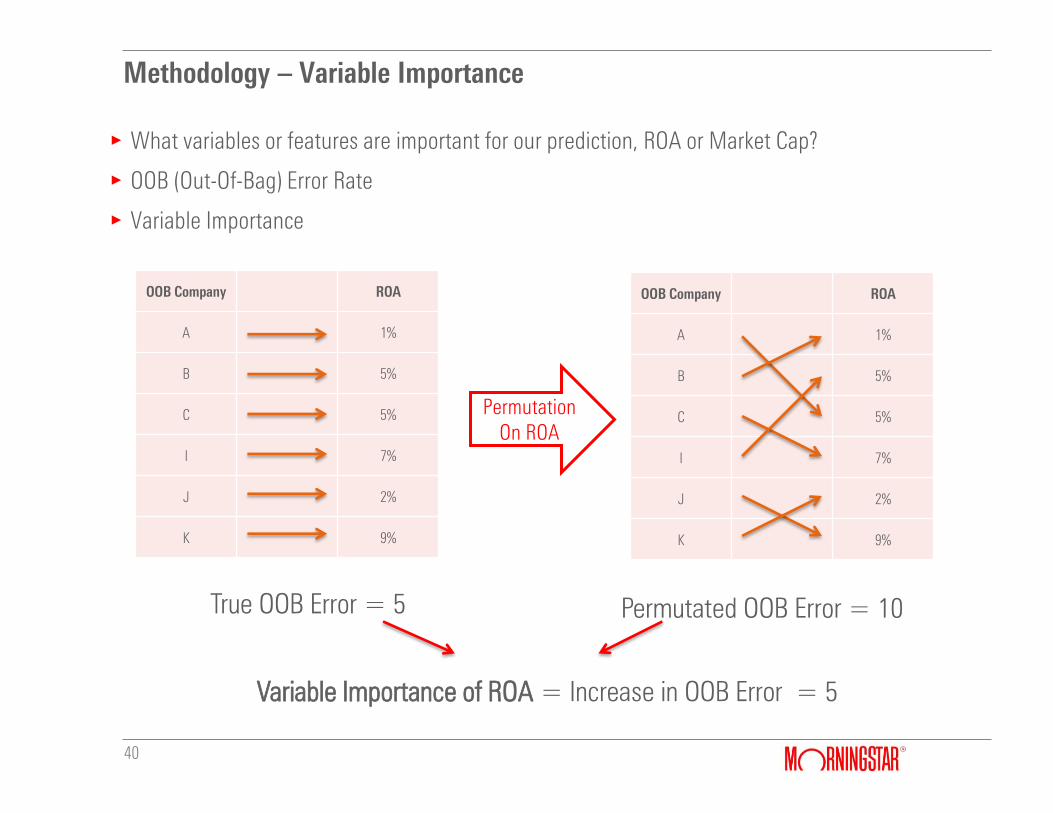

Methodology – Variable Importance

40

gWhat variables or features are important for our prediction, ROA or Market Cap?

gOOB (Out-Of-Bag) Error Rate

gVariable Importance

OOB Company ROA

A 1%

B 5%

C 5%

I 7%

J 2%

K 9%

OOB Company ROA

A 1%

B 5%

C 5%

I 7%

J 2%

K 9%

Permutation On ROA

Variable Importance of ROA = Increase in OOB Error = 5

True OOB Error = 5 Permutated OOB Error = 10

Methodology – Variable Importance

41

g If variable importance of variable i is close to 0, then variable i is NOT important

g If variable importance of variable i is close to ∞, then variable i is SUPER important

Methodology – Variable Importance

42

©2015 Morningstar, Inc. All rights reserved.

Morningstar Quantitative Research

44

Morningstar Quantitative Research Overview

Morningstar quantitative equity ratings vastly expand our coverage of the equity universe. They are designed to replicate the proven, proprietary, forward-looking analysis of our research team.

Morningstar Global Analyst Team

45

Morningstar Quantitative Research

Our accomplished team of award-winning analysts applies one consistent valuation methodology. Their work forms the basis for our quantitative model.

Equity and Credit Analysts

gOur analysts are

specialized and

organized by sector

gAverage coverage per

analyst is 16 companies

gMore than 2/3 of

our analysts have an

MBA or are CFA

charterholders, 1/3

have both

g13 Analyst Awards from

the Wall Street Journal

Valuation Methodology

gDiscounted cash flow

foundation applied

to all companies, across

all sectors

gEconomic Moat Committee

ensures consistent

assignment of Economic

Moat™ Rating

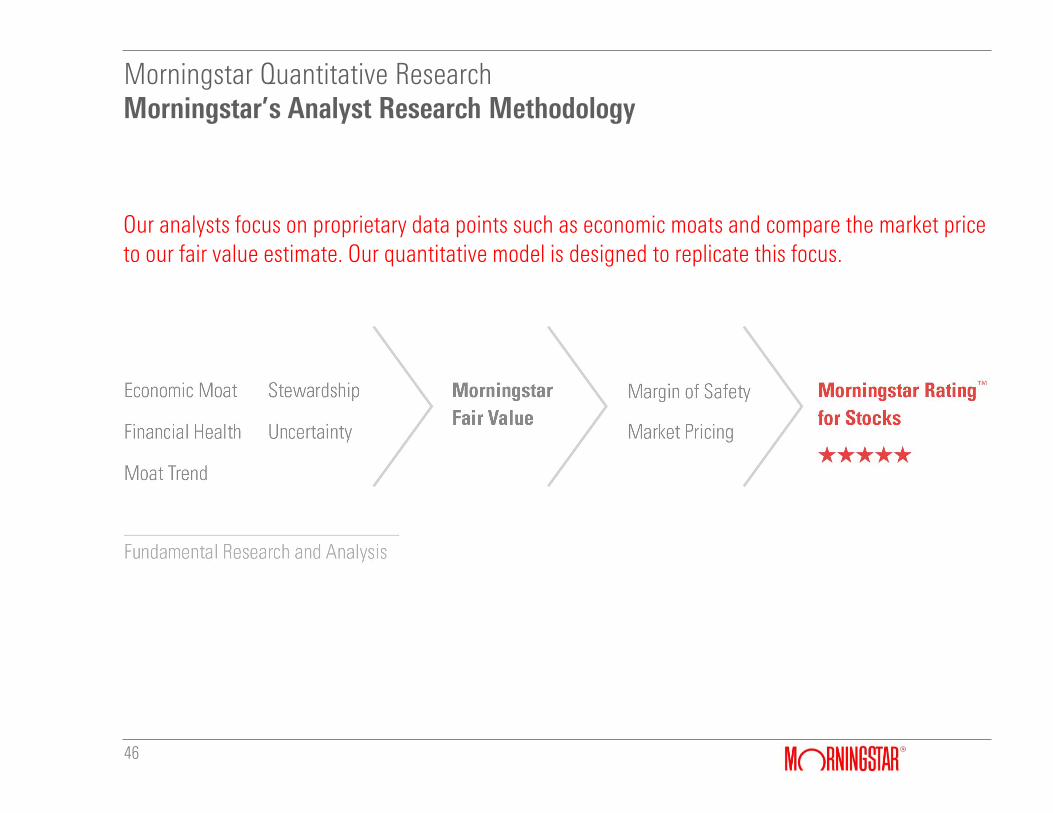

Morningstar’s Analyst Research Methodology

46

Morningstar Quantitative Research

Our analysts focus on proprietary data points such as economic moats and compare the market price to our fair value estimate. Our quantitative model is designed to replicate this focus.

The Effectiveness of Our Ratings Over Time

47

Morningstar Quantitative Research

Our methodology has proved effective, with five-star rated stocks outperforming all others.

Trailing Annualized Returns (%)

Morningstar Rating™ for stocks 1-Year 3-Year 5-Year 10-Year

Since Inception

(08/06/2001)

QQQQQ 17.7 17.6 19.1 17.7 13.0

QQQQ 5.9 13.5 12.9 11.2 12.1

QQQ 14.4 16.7 13.9 11.0 9.8

QQ 11.5 12.2 10.9 6.6 5.7

Q 4.5 14.4 10.0 14.9 10.2

Morningstar Coverage Universe 11.8 15.0 13.4 12.0 —

S&P 500 Index (cap-weighted) 12.7 16.1 14.5 8.0 —

Source: Morningstar Time-weighted returns through: March 31, 2015

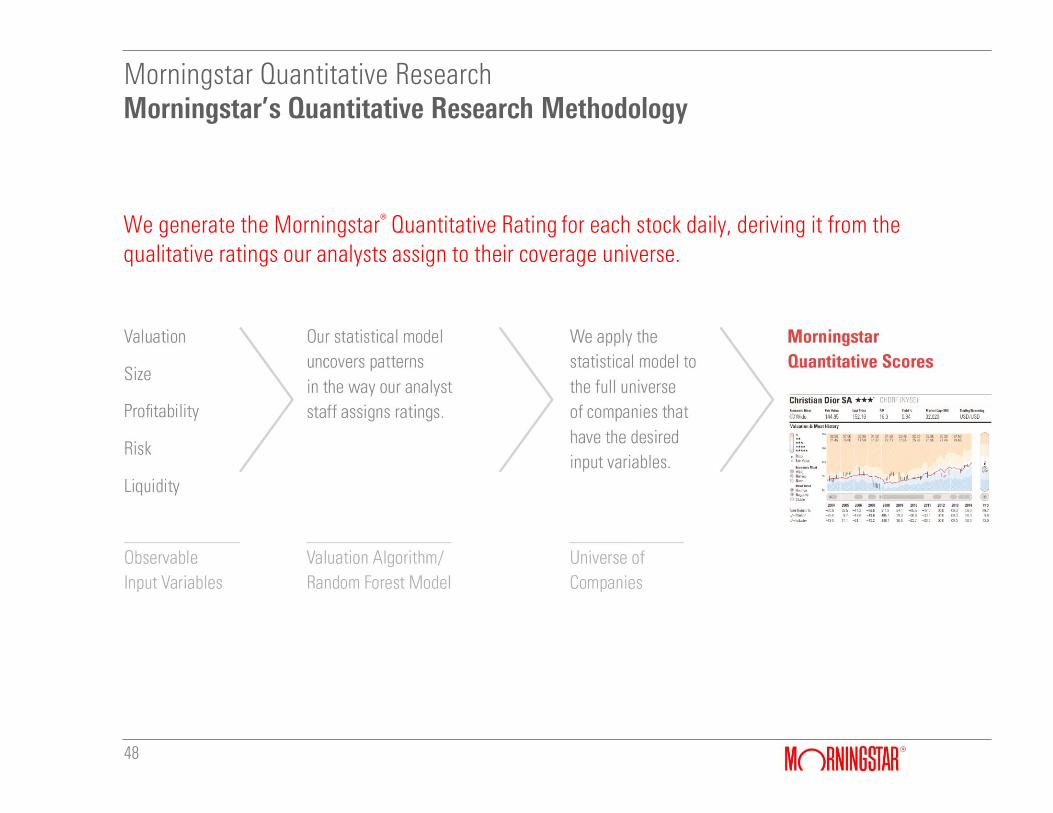

Morningstar’s Quantitative Research Methodology

48

Morningstar Quantitative Research

We generate the Morningstar® Quantitative Rating for each stock daily, deriving it from the qualitative ratings our analysts assign to their coverage universe.

Our Quantitative Model Matches Our Analyst Ratings

49

Morningstar Quantitative Research

The model shows meaningful disagreement with the direction of the analyst recommendation less than 12% of the time.

0.00

0.50

1.00

1.50

2.00

2.50

3.00

0 1 2 3 4 5

Qua

nt P

rice/

Fair

Valu

e R

atio

Analyst Price/Fair Value Ratio

Data as of March 31, 2015

R² = 0.7528

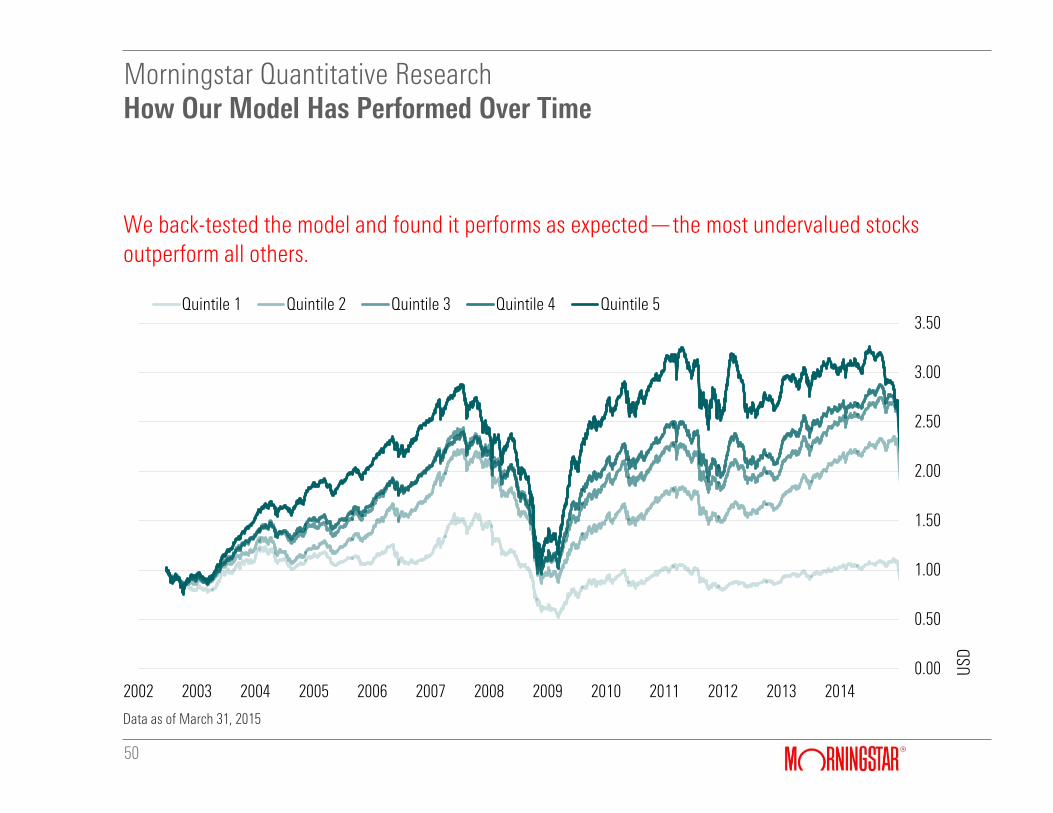

How Our Model Has Performed Over Time

50

Morningstar Quantitative Research

We back-tested the model and found it performs as expected—the most undervalued stocks outperform all others.

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

USD

Quintile 1 Quintile 2 Quintile 3 Quintile 4 Quintile 5

Data as of March 31, 2015

51

Role of the Economic Moat

We’ve harnessed our data and analyst insight to significantly expand our equity research coverage.

Morningstar Quantitative Research

736 Analyst Coverage

14,510 Quantitative Coverage

North America

253 Analyst Coverage

8,524 Quantitative Coverage

Europe

128 Analyst Coverage

13,898 Quantitative Coverage

Asia

32 Analyst Coverage

1,041 Quantitative Coverage

Latin America 42 Analyst Coverage

7,638 Quantitative Coverage

Eurasia/India/

Middle East/Africa

225 Analyst Coverage

2,067 Quantitative Coverage

Australia

1,416 Analyst Coverage

50,506 Quantitative Coverage

19x 33x 108x 181x

32x

9x

Data as of March 31, 2015. Coverage numbers are calculated by the number of companies in their respective countries of domicile.

52

Comprehensive Global Quantitative Equity Coverage

Our quantitative coverage is both broad across regions and deep within countries.

Morningstar Quantitative Research

North America

Country Companies

U.S. 10,746

Canada 3,277

Latin America

Brazil 485

Chile 222

Mexico 130

Argentina 100

Colombia 59

Asia Pacific

Country Companies

Japan 3,574

China 2,632

South Korea 1,810

Taiwan 1,780

Malaysia 903

Singapore 622

Thailand 641

Indonesia 501

Vietnam 302

Philippines 255

Hong Kong 223

Australia & New Zealand

Australia 1,837

New Zealand 141

Africa, India, Pakistan, & Middle East

Country Companies

India 4,718

Israel 481

Pakistan 487

South Africa 308

Bangladesh 276

Egypt 231

Kuwait 199

Nigeria 191

Saudi Arabia 163

Oman 116

U.A.E. 107

Iraq 92

Europe

Country Companies

U.K. 1,506

Germany 851

France 845

Poland 859

Russia 805

Sweden 408

Turkey 430

Italy 289

Switzerland 219

Greece 237

Spain 151

Norway 166

Netherlands 96

Belgium 152

Country Companies

Denmark 150

Finland 127

Austria 82

Ireland 28

Luxembourg 15

Portugal 60

Data as of March 31, 2015. Displaying countries with over 50 companies covered.

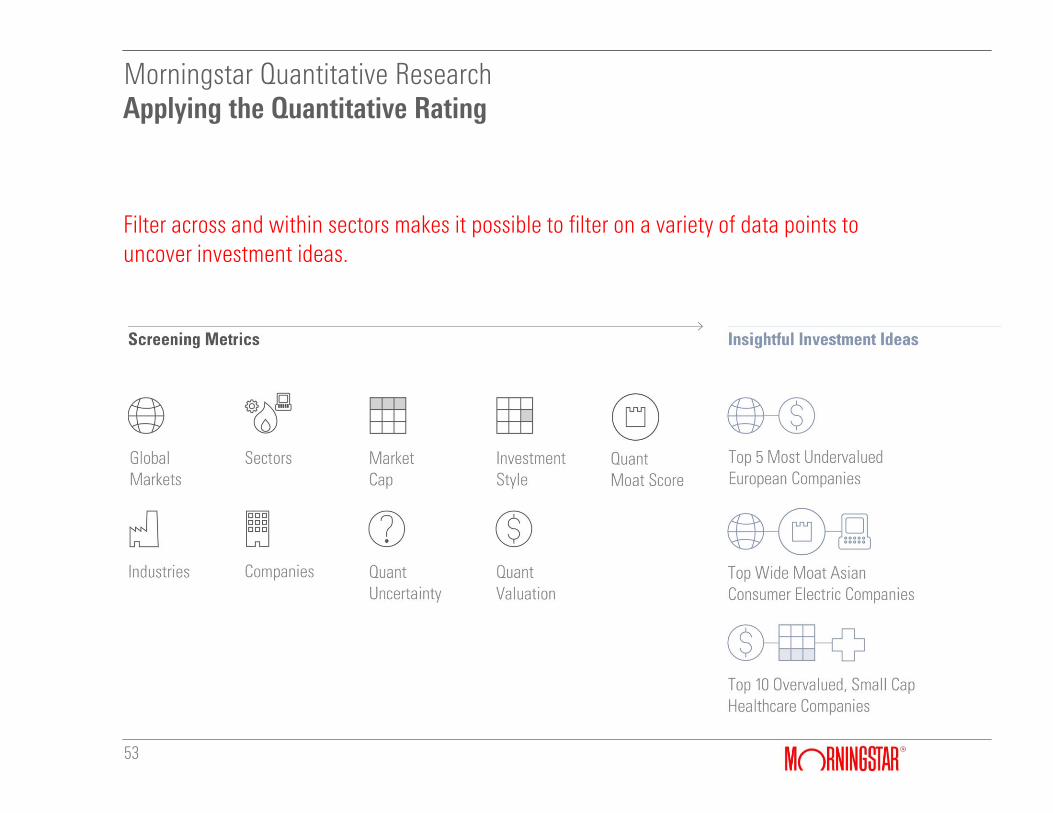

53

Applying the Quantitative Rating

Filter across and within sectors makes it possible to filter on a variety of data points to uncover investment ideas.

Morningstar Quantitative Research

Next Steps

54

Morningstar Quantitative Research

gMorningstar’s quantitative research:

/ Is forward-looking and distinct from other quantitative tools

/Applies the principles of 10 years of successful Morningstar analyst experience

/Aims to predict future alpha

/Offers broad and deep global coverage

gMeet with one of our quantitative analysts to learn more about our methodology and explore sample data

Andy Tang, CFA

Quantitative Analyst

(312) 384-4839

55

Appendix

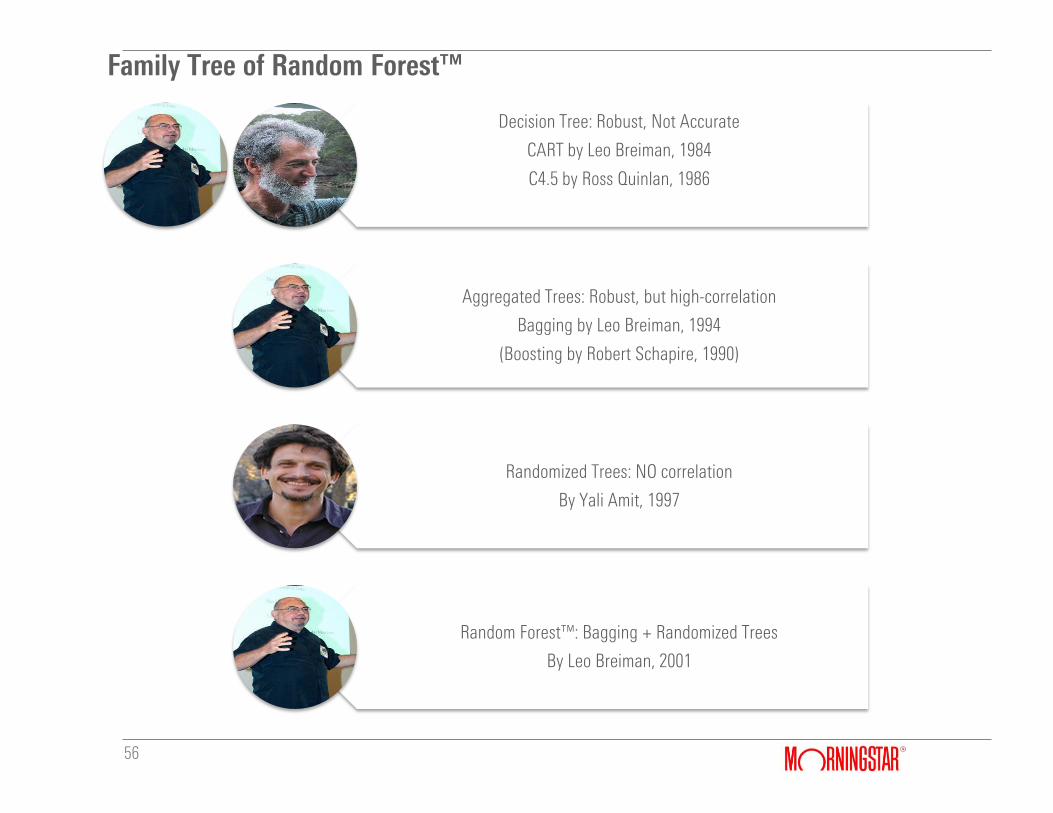

56

Decision Tree: Robust, Not Accurate

CART by Leo Breiman, 1984

C4.5 by Ross Quinlan, 1986

Aggregated Trees: Robust, but high-correlation

Bagging by Leo Breiman, 1994

(Boosting by Robert Schapire, 1990)

Randomized Trees: NO correlation

By Yali Amit, 1997

Random Forest™: Bagging + Randomized Trees

By Leo Breiman, 2001

Family Tree of Random Forest™

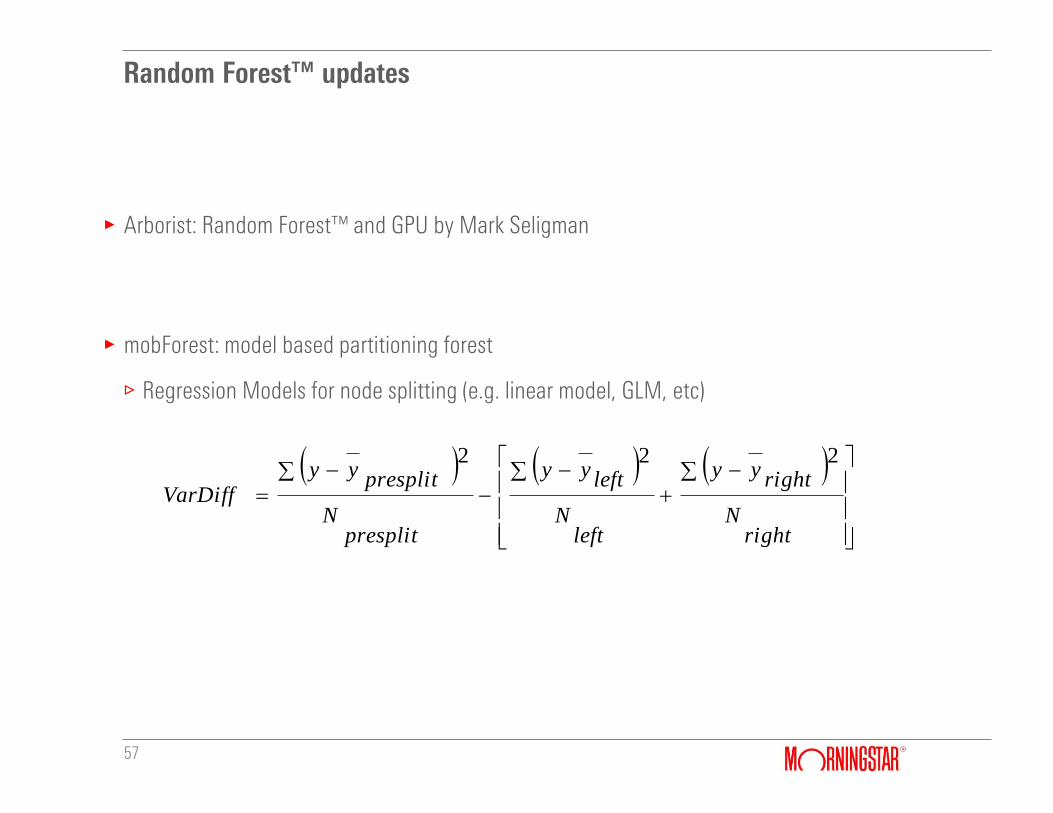

Random Forest™ updates

57

gArborist: Random Forest™ and GPU by Mark Seligman

gmobForest: model based partitioning forest

/Regression Models for node splitting (e.g. linear model, GLM, etc)

rightN

rightyy

leftN

leftyy

presplitN

presplityy

VarDiff

222