CRISIL-Research CRISIL-Research_ier-report-nrb bearings ltdIer-report-nrb Bearings Ltd 2015

27

RESEARCH CRISIL IER Independent Equity Research Detailed Report NRB Bearings Ltd Enhancing investment decisions

description

CRISIL-Research_ier-report-nrb bearings ltd

Transcript of CRISIL-Research CRISIL-Research_ier-report-nrb bearings ltdIer-report-nrb Bearings Ltd 2015

RESEARCH

CRISIL IER Independent Equity Research

Detailed Report

NRB Bearings Ltd

Enhancing investment decisions

CRISIL IER Independent Equity Research

Explanation of CRISIL Fundamental and Valuation (CFV) matrix

The CFV Matrix (CRISIL Fundamental and Valuation Matrix) addresses the two important analysis of an investment making process – Analysis of Fundamentals (addressed through Fundamental Grade) and Analysis of Returns (Valuation Grade) The fundamental grade is assigned on a five-point scale from grade 5 (indicating Excellent fundamentals) to grade 1 (Poor fundamentals) The valuation grade is assigned on a five-point scale from grade 5 (indicating strong upside from the current market price (CMP)) to grade 1 (strong downside from the CMP).

CRISIL Fundamental Grade Assessment

CRISIL Valuation Grade Assessment

5/5 Excellent fundamentals 5/5 Strong upside (>25% from CMP) 4/5 Superior fundamentals 4/5 Upside (10-25% from CMP) 3/5 Good fundamentals 3/5 Align (+-10% from CMP) 2/5 Moderate fundamentals 2/5 Downside (negative 10-25% from CMP) 1/5 Poor fundamentals 1/5 Strong downside (<-25% from CMP)

About CRISIL Limited CRISIL is a global analytical company providing ratings, research, and risk and policy advisory services. We are India’s leading ratings agency. We are also the foremost provider of high-end research to the world’s largest banks and leading corporations. About CRISIL Research CRISIL Research is India's largest independent integrated research house. We provide insights, opinion and analysis on the Indian economy, industry, capital markets and companies. We also conduct training programs to financial sector professionals on a wide array of technical issues. We are India's most credible provider of economy and industry research. Our industry research covers 86 sectors and is known for its rich insights and perspectives. Our analysis is supported by inputs from our network of more than 5,000 primary sources, including industry experts, industry associations and trade channels. We play a key role in India's fixed income markets. We are the largest provider of valuation of fixed income securities to the mutual fund, insurance and banking industries in the country. We are also the sole provider of debt and hybrid indices to India's mutual fund and life insurance industries. We pioneered independent equity research in India, and are today the country's largest independent equity research house. Our defining trait is the ability to convert information and data into expert judgements and forecasts with complete objectivity. We leverage our deep understanding of the macro-economy and our extensive sector coverage to provide unique insights on micro-macro and cross-sectoral linkages. Our talent pool comprises economists, sector experts, company analysts and information management specialists. CRISIL Privacy CRISIL respects your privacy. We use your contact information, such as your name, address, and email id, to fulfil your request and service your account and to provide you with additional information from CRISIL and other parts of McGraw Hill Financial you may find of interest.

For further information, or to let us know your preferences with respect to receiving marketing materials, please visit www.crisil.com/privacy. You can view McGraw Hill Financial’s Customer Privacy Policy at http://www.mhfi.com/privacy.

Last updated: August, 2014 Analyst Disclosure Each member of the team involved in the preparation of the grading report, hereby affirms that there exists no conflict of interest that can bias the grading recommendation of the company. Disclaimer: This Company commissioned CRISIL IER report is based on data publicly available or from sources considered reliable. CRISIL Ltd. (CRISIL) does not represent that it is accurate or complete and hence, it should not be relied upon as such. The data / report is subject to change without any prior notice. Opinions expressed herein are our current opinions as on the date of this report. Nothing in this report constitutes investment, legal, accounting or tax advice or any solicitation, whatsoever. The subscriber / user assume the entire risk of any use made of this data / report. CRISIL especially states that, it has no financial liability whatsoever, to the subscribers / users of this report. This report is for the personal information only of the authorised recipient in India only. This report should not be reproduced or redistributed or communicated directly or indirectly in any form to any other person – especially outside India or published or copied in whole or in part, for any purpose. As per CRISIL’s records, none of the analysts involved has any ownership / directorship in the company. However CRISIL or its associates may have commercial transactions with the company.

RESEARCH

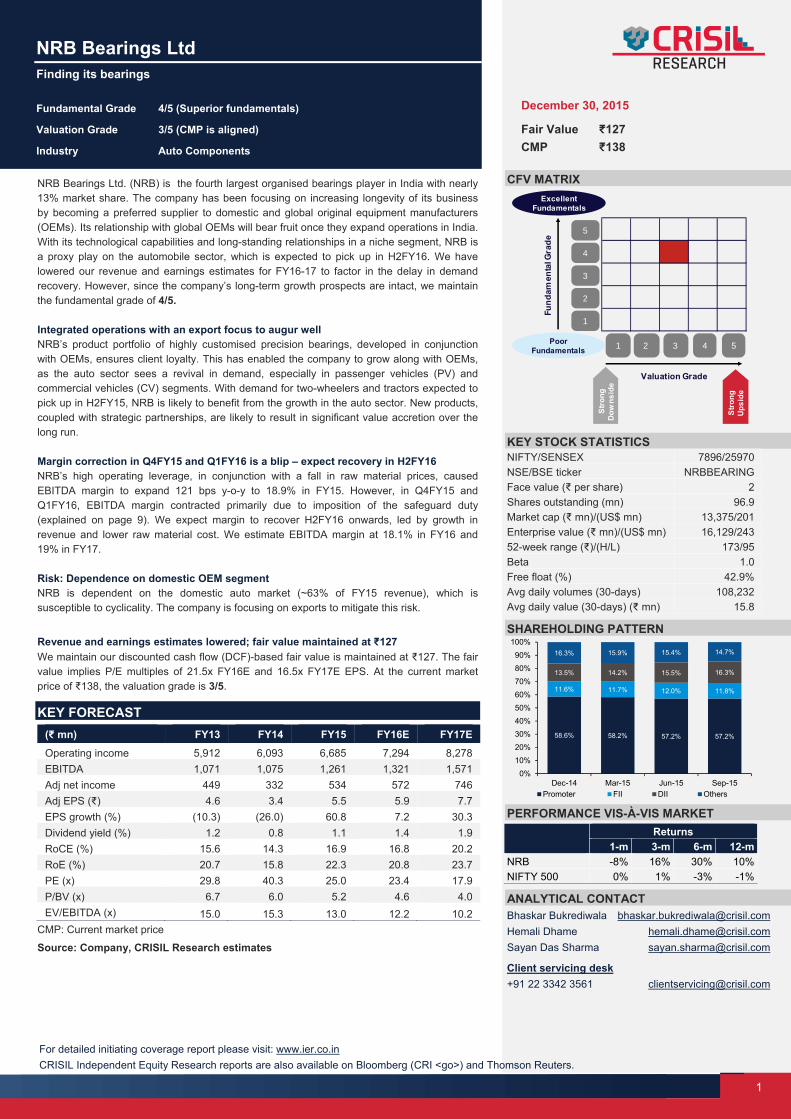

NRB Bearings Ltd

Finding its bearings

Fundamental Grade 4/5 (Superior fundamentals)

Valuation Grade 3/5 (CMP is aligned)

Industry Auto Components

1

December 30, 2015

Fair Value ₹127 CMP ₹138

For detailed initiating coverage report please visit: www.ier.co.in

NRB Bearings Ltd. (NRB) is the fourth largest organised bearings player in India with nearly 13% market share. The company has been focusing on increasing longevity of its business by becoming a preferred supplier to domestic and global original equipment manufacturers (OEMs). Its relationship with global OEMs will bear fruit once they expand operations in India. With its technological capabilities and long-standing relationships in a niche segment, NRB is a proxy play on the automobile sector, which is expected to pick up in H2FY16. We have lowered our revenue and earnings estimates for FY16-17 to factor in the delay in demand recovery. However, since the company’s long-term growth prospects are intact, we maintain the fundamental grade of 4/5.

CRISIL Independent Equity Research reports are also available on Bloomberg (CRI <go>) and Thomson Reuters.

Integrated operations with an export focus to augur well NRB’s product portfolio of highly customised precision bearings, developed in conjunction with OEMs, ensures client loyalty. This has enabled the company to grow along with OEMs, as the auto sector sees a revival in demand, especially in passenger vehicles (PV) and commercial vehicles (CV) segments. With demand for two-wheelers and tractors expected to pick up in H2FY15, NRB is likely to benefit from the growth in the auto sector. New products, coupled with strategic partnerships, are likely to result in significant value accretion over the long run.

Margin correction in Q4FY15 and Q1FY16 is a blip – expect recovery in H2FY16 NRB’s high operating leverage, in conjunction with a fall in raw material prices, caused EBITDA margin to expand 121 bps y-o-y to 18.9% in FY15. However, in Q4FY15 and Q1FY16, EBITDA margin contracted primarily due to imposition of the safeguard duty (explained on page 9). We expect margin to recover H2FY16 onwards, led by growth in revenue and lower raw material cost. We estimate EBITDA margin at 18.1% in FY16 and 19% in FY17.

Risk: Dependence on domestic OEM segment NRB is dependent on the domestic auto market (~63% of FY15 revenue), which is susceptible to cyclicality. The company is focusing on exports to mitigate this risk.

Revenue and earnings estimates lowered; fair value maintained at ₹127 We maintain our discounted cash flow (DCF)-based fair value is maintained at ₹127. The fair value implies P/E multiples of 21.5x FY16E and 16.5x FY17E EPS. At the current market price of ₹138, the valuation grade is 3/5.

KEY FORECAST

(₹ mn) FY13 FY14 FY15 FY16E FY17E

Operating income 5,912 6,093 6,685 7,294 8,278 EBITDA 1,071 1,075 1,261 1,321 1,571 Adj net income 449 332 534 572 746 Adj EPS (₹) 4.6 3.4 5.5 5.9 7.7 EPS growth (%) (10.3) (26.0) 60.8 7.2 30.3 Dividend yield (%) 1.2 0.8 1.1 1.4 1.9 RoCE (%) 15.6 14.3 16.9 16.8 20.2 RoE (%) 20.7 15.8 22.3 20.8 23.7 PE (x) 29.8 40.3 25.0 23.4 17.9 P/BV (x) 6.7 6.0 5.2 4.6 4.0 EV/EBITDA (x) 15.0 15.3 13.0 12.2 10.2

CMP: Current market price

Source: Company, CRISIL Research estimates

CFV MATRIX Excellent

Fundamentals

KEY STOCK STATISTICS NIFTY/SENSEX 7896/25970 NSE/BSE ticker NRBBEARING Face value (₹ per share) 2 Shares outstanding (mn) 96.9 Market cap (₹ mn)/(US$ mn) 13,375/201 Enterprise value (₹ mn)/(US$ mn) 16,129/243 52-week range (₹)/(H/L) 173/95 Beta 1.0 Free float (%) 42.9% Avg daily volumes (30-days) 108,232 Avg daily value (30-days) (₹ mn) 15.8

SHAREHOLDING PATTERN

PERFORMANCE VIS-À-VIS MARKET

Returns

1-m 3-m 6-m 12-mNRB -8% 16% 30% 10%NIFTY 500 0% 1% -3% -1%

ANALYTICAL CONTACT Bhaskar Bukrediwala [email protected] Hemali Dhame [email protected] Sayan Das Sharma [email protected]

Client servicing desk +91 22 3342 3561 [email protected]

4

3

2

1

1 2 3 4

5

Valuation Grade

Fund

amen

tal G

rade

5Poor Fundamentals

Stro

ngDo

wns

ide

Stro

ngUp

side

58.6% 58.2% 57.2% 57.2%

11.6% 11.7% 12.0% 11.8%

13.5% 14.2% 15.5% 16.3%

16.3% 15.9% 15.4% 14.7%

0%10%20%30%40%50%60%70%80%90%

100%

Dec-14 Mar-15 Jun-15 Sep-15Promoter FII DII Others

CRISIL IER Independent Equity Research

2

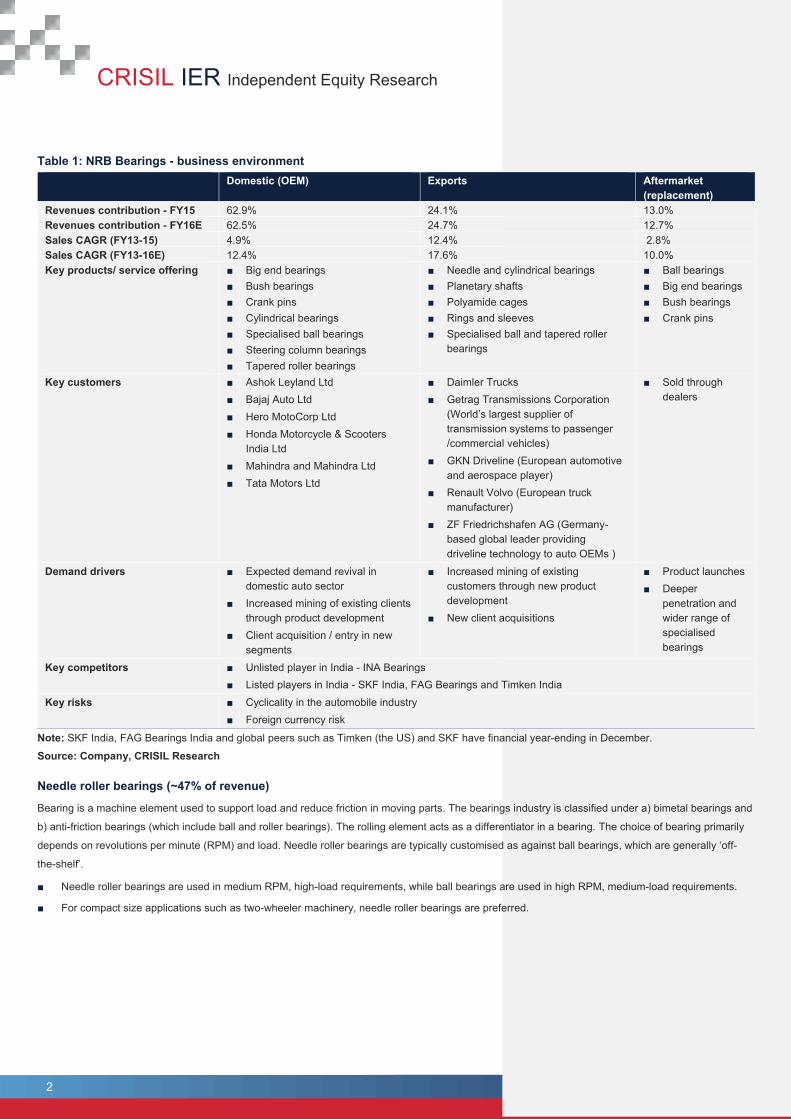

Table 1: NRB Bearings - business environment Domestic (OEM) Exports Aftermarket

(replacement) Revenues contribution - FY15 62.9% 24.1% 13.0% Revenues contribution - FY16E 62.5% 24.7% 12.7% Sales CAGR (FY13-15) 4.9% 12.4% 2.8% Sales CAGR (FY13-16E) 12.4% 17.6% 10.0% Key products/ service offering ■ Big end bearings

■ Bush bearings ■ Crank pins ■ Cylindrical bearings ■ Specialised ball bearings ■ Steering column bearings ■ Tapered roller bearings

■ Needle and cylindrical bearings ■ Planetary shafts ■ Polyamide cages ■ Rings and sleeves ■ Specialised ball and tapered roller

bearings

■ Ball bearings ■ Big end bearings ■ Bush bearings ■ Crank pins

Key customers ■ Ashok Leyland Ltd ■ Bajaj Auto Ltd ■ Hero MotoCorp Ltd ■ Honda Motorcycle & Scooters

India Ltd ■ Mahindra and Mahindra Ltd ■ Tata Motors Ltd

■ Daimler Trucks ■ Getrag Transmissions Corporation

(World’s largest supplier of transmission systems to passenger /commercial vehicles)

■ GKN Driveline (European automotive and aerospace player)

■ Renault Volvo (European truck manufacturer)

■ ZF Friedrichshafen AG (Germany-based global leader providing driveline technology to auto OEMs )

■ Sold through dealers

Demand drivers ■ Expected demand revival in domestic auto sector

■ Increased mining of existing clients through product development

■ Client acquisition / entry in new segments

■ Increased mining of existing customers through new product development

■ New client acquisitions

■ Product launches ■ Deeper

penetration and wider range of specialised bearings

Key competitors ■ Unlisted player in India - INA Bearings ■ Listed players in India - SKF India, FAG Bearings and Timken India

Key risks

■ Cyclicality in the automobile industry ■ Foreign currency risk

Note: SKF India, FAG Bearings India and global peers such as Timken (the US) and SKF have financial year-ending in December.

Source: Company, CRISIL Research Needle roller bearings (~47% of revenue)

Bearing is a machine element used to support load and reduce friction in moving parts. The bearings industry is classified under a) bimetal bearings and

b) anti-friction bearings (which include ball and roller bearings). The rolling element acts as a differentiator in a bearing. The choice of bearing primarily

depends on revolutions per minute (RPM) and load. Needle roller bearings are typically customised as against ball bearings, which are generally ‘off-

the-shelf’.

■ Needle roller bearings are used in medium RPM, high-load requirements, while ball bearings are used in high RPM, medium-load requirements.

■ For compact size applications such as two-wheeler machinery, needle roller bearings are preferred.

RESEARCH

NRB Bearings Ltd

Grading Rationale Figure 1: Revenue mix – FY15

Export, 24%

Aftermarket,

13%

Domestic(OEM 63%)

Growth moderated towards tail-end of FY15, to recover in FY16 As a well-established manufacturer of customised bearings for the mobility segment, NRB’s

performance is inextricably linked to growth in demand for automobiles, tractors and off-the-

highway vehicles. In that context, FY15 was a mixed bag— robust H1FY15 and a relatively

weaker H2FY15, reflecting ups and downs of the domestic auto sector.

The company derives ~48% of its domestic OEM revenue from two-wheelers, a segment that

has slowed down considerably largely due to weak rural demand. Further, export revenue

was adversely impacted by a sharp depreciation in the euro in Q4FY15. Total revenue in

FY15 grew 9.7% y-o-y to ₹6.7 bn, driven by revenue growth of 10% in the domestic OEM

segment, 14% in exports and 6% in growth in the aftermarket segment (all in y-o-y terms).

Two-wheelers account for ~48% of

domestic OEM revenues

In line with trends seen at the tail-end of FY15, revenue in Q1FY16 grew merely 2.1% y-o-y to

₹1.6 bn in Q1FY16. However, we expect demand to revive in H2FY16, due to a pick-up in

domestic sales (led by the festive season) and NRB’s continuous focus on exports (foray into

newer platforms). We estimate NRB’s revenue to post a CAGR of 11.3% y-o-y over FY15-

17E to ₹8.3 bn.

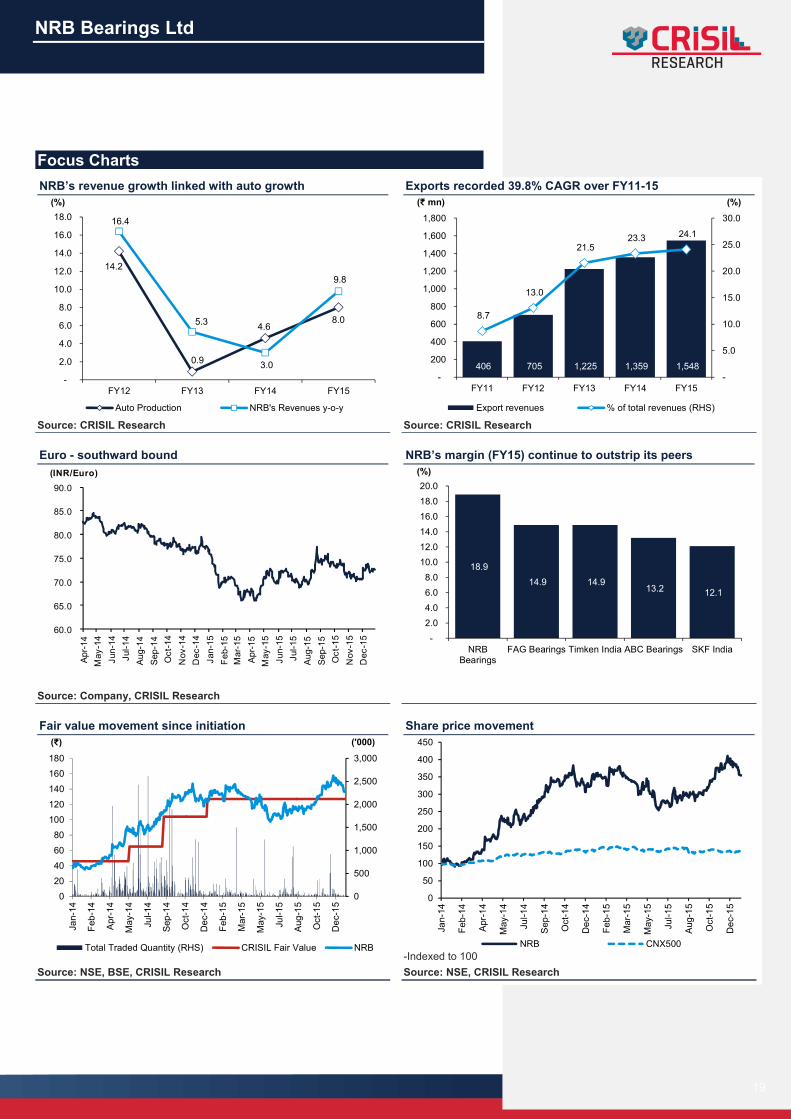

Figure 2: NRB’s revenue growth linked with auto sector growth

Source: CRISIL Research

Table 2: Moderate production growth of auto segment y-o-y growth (%) in production FY13 FY14 FY15 Q1FY16 Two wheelers 2.1 7.2 9.6 0.2 Thre wheelers -4.5 -1.1 14.3 9.0 Passenger cars -4.5 -4.2 4.0 7.6 Utility vehicles 32.6 -5.5 5.1 5.1 M&HCV (sales) -23.7 -22.2 17.4 23.1 LCV (sales) 11.6 -17.0 -9.9 -3.2 Tractors -10.5 22.3 -13.4 -13.8 Total 0.9 4.6 8.0 1.1

14.2

0.9

4.6 8.0

16.4

5.3

3.0

9.8

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

FY12 FY13 FY14 FY15

(%)

Auto Production NRB's Revenues y-o-y

Source: CRISIL Research

3

CRISIL IER Independent Equity Research

4

Demand from domestic OEMs to revive in H2FY16

Rural demand for two-wheelers is expected to remain muted in H1FY16 due to poor

monsoons. Though the festive season is likely to revive demand temporarily, we expect

tangible recovery only in FY17. Similarly, tractor demand is also likely to be impacted by a

weak rural economy and infrastructure activity. In contrast, PVs and CVs are likely to remain

on their growth trajectory, backed by new launches and recovery in economic activity,

respectively. We estimate NRB’s domestic OEM revenue to record a CAGR of 11.3% over

FY15-FY17E to ₹5 bn.

Figure 3: Trend in domestic OEM revenue growth

Source: CRISIL Research

Strategic focus on exports to further benefit the company As the domestic auto industry has been through a correction over last few years, NRB’s

decision to focus on exports has been fruitful. The company caters to global OEMs, namely,

Renault Volvo and Daimler Trucks in Europe, the US and Latin American countries.

Association with global OEMs helps the company enhance its engineering capabilities and

benchmark its quality to global standards. Some of these global OEMs are first-time entrants

into India and this relationship should encourage domestic sales. Further, NRB is working with

a luxury car manufacturer and this platform is likely to boost revenue and improve margin.

NRB’s total exports posted a healthy CAGR of 39.8% during FY11-15. The contribution of

exports to total sales increased to 24% in FY15 from 9% in FY11.

3,421 3,915 3,670 3,677 4,042

35.1

14.4

(6.3)

0.2

9.9

(15.0)

(8.0)

(1.0)

6.0

13.0

20.0

27.0

34.0

3,100

3,200

3,300

3,400

3,500

3,600

3,700

3,800

3,900

4,000

4,100

FY11 FY12 FY13 FY14 FY15

(%)(₹ mn)

Domestic OEM revenues y-o-y growth

Export revenues grew 14% y-o-y in

FY15, despite euro correction in

Q4FY15

RESEARCH

NRB Bearings Ltd

Figure 4: Exports have picked up smartly – 39.8% CAGR over FY11-15

Source: CRISIL Research

406 705 1,225 1,359 1,548

8.7

13.0

21.5 23.3 24.1

-

5.0

10.0

15.0

20.0

25.0

30.0

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

FY11 FY12 FY13 FY14 FY15

(%)(₹ mn)

Export revenues % of total revenues (RHS)

While export revenue grew 14% y-o-y in FY15, appreciation of rupee against the Euro (from

₹76.6/€ in December 2014 to ₹67.7/€ in March 2015) played spoilsport in Q4FY15. The fall

continued in Q2FY16, with rates stabilising lower than last year. Going forward, we expect

further growth in volume, thanks to initiatives taken by the company. We estimate NRB’s

export revenue to post a CAGR of 16.4% over FY15-FY17E to ₹2.1 bn.

Figure 5: Euro - southward bound

Source: CRISIL Research

60.0

65.0

70.0

75.0

80.0

85.0

90.0

Apr-1

4M

ay-1

4Ju

n-14

Jul-1

4A

ug-1

4S

ep-1

4O

ct-1

4N

ov-1

4D

ec-1

4Ja

n-15

Feb-

15M

ar-1

5Ap

r-15

May

-15

Jun-

15Ju

l-15

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

(INR/Euro)

Aftermarket segment to grow steadily

NRB’s aftermarket segment witnessed weakness in FY12 and FY13, but recouped with

product launches in H2FY14. While FY14 revenue was flat, FY15 revenue grew 6% y-o-y to

₹835 mn. With the company expanding presence in the domestic OEM and export markets,

overall contribution to revenue has stagnated at 13%.

Bearings in a vehicle should ideally

get replaced on completing 10,000

km

The aftermarket is crowded by several unorganised players, in addition to the threat of

cheaper imports, mainly from China. Further, NRB caters largely to the two and three-wheeler

5

CRISIL IER Independent Equity Research

6

industries, which are price-sensitive. However, the company’s current focus on the off-the-

highway segment should boost growth. We expect the aftermarket segment to grow

moderately by 10% over FY15-17E to ₹1 bn.

Foray into new segments to yield long-term benefits The company has made inroads in the defence segment, with a small order from the Defence

Research and Development Organisation (DRDO) for an under-development project. With the

government’s ‘Make in India’ focus, especially in the defense space, this should augur well in

the long run. In addition, the company has developed a working relationship with Indian

Railways, but this is yet to take off. It is also working on identifying opportunities in urban

transportation and aerospace. Some of these initiatives are likely to create a new segment for

the company and help de-risk business.

Engineering prowess will continue to yield results NRB’s focus on products that are well-engineered and involve client engagement right from

the conceptualisation phase has ensured steady relationships with leading OEMs, across the

automobile industry. To fortify its prowess, it has invested and developed technology that is

used to manufacture critical components such as transmission and engine systems, where

quality standards are important. Given its expertise and involvement, there is a high level of

customer loyalty, which acts as a natural entry barrier to new players. The company is a tier I

(direct supplier) supplier to leading domestic OEMs such as Hero MotoCorp, Bajaj Auto, Tata

Motors, Maruti Suzuki and Ashok Leyland. It is a tier I/II (direct and indirect supplier) supplier

to reputed global players such as Renault Volvo, Daimler Trucks, ZF Group and Getrag

Group. As a testament to its engineering prowess and products, NRB has managed to

improve its market share in the organised bearings sector from 11% in FY13 to 13% in FY15.

Table 3: Product usage in critical applications

Products Critical automobile application Polyamide cages Gearbox Needle brushes Gearbox / steering Nib end bearings Engine Crank pins Engine

Source: CRISIL Research

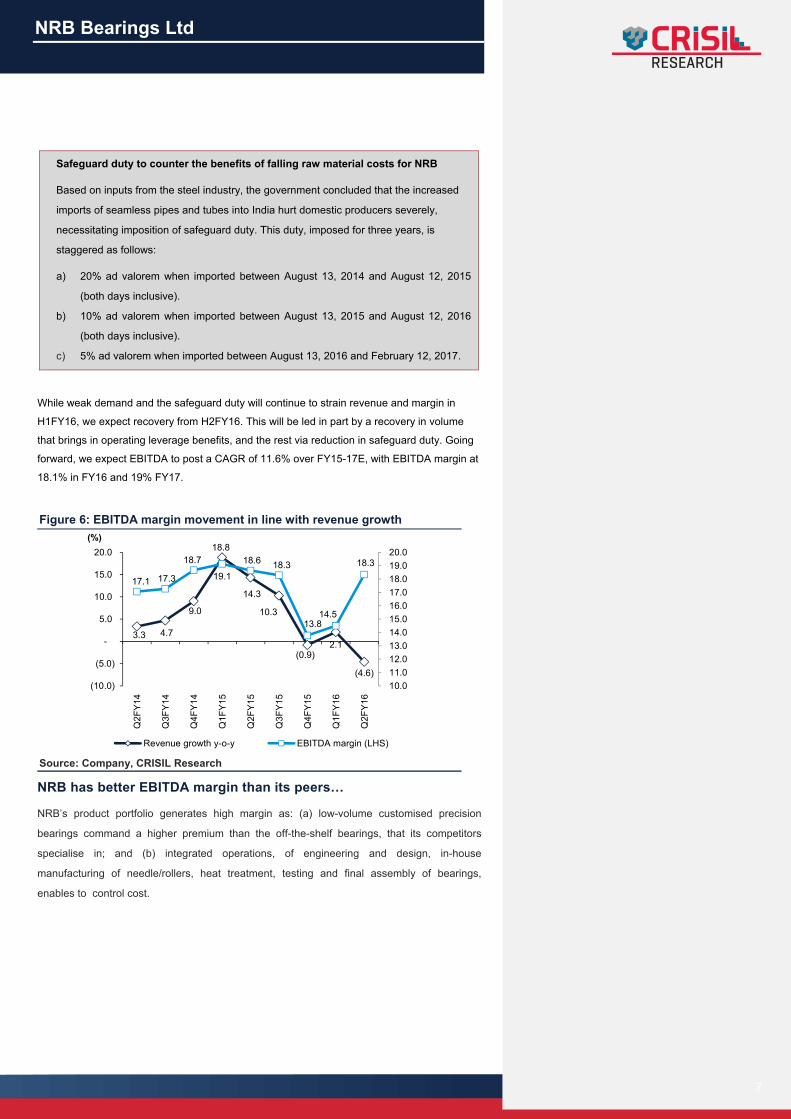

Recent margin correction is a blip, expect recovery in H2FY16 NRB’s cost structure incorporates a high degree of operating leverage that allows changes in

revenue to magnify margin. In line with this, the company’s EBITDA margin expanded 121 bps

y-o-y to 18.9% in FY15, mainly on account of higher operating leverage combined with a fall in

raw material prices. However, EBITDA margin was impacted in Q4FY15, due to several

reasons, including (a) negative operating leverage due to reduced volume, (b) provisioning for

slow moving finished goods inventory, in line with the company’s policy, (c) higher provisioning

for gratuity and pension liabilities, and (d) impact of safeguard duty on imported steel tubes.

RESEARCH

NRB Bearings Ltd

Safeguard duty to counter the benefits of falling raw material costs for NRB

Based on inputs from the steel industry, the government concluded that the increased

imports of seamless pipes and tubes into India hurt domestic producers severely,

necessitating imposition of safeguard duty. This duty, imposed for three years, is

staggered as follows:

a) 20% ad valorem when imported between August 13, 2014 and August 12, 2015

(both days inclusive).

b) 10% ad valorem when imported between August 13, 2015 and August 12, 2016

(both days inclusive).

c) 5% ad valorem when imported between August 13, 2016 and February 12, 2017.

While weak demand and the safeguard duty will continue to strain revenue and margin in

H1FY16, we expect recovery from H2FY16. This will be led in part by a recovery in volume

that brings in operating leverage benefits, and the rest via reduction in safeguard duty. Going

forward, we expect EBITDA to post a CAGR of 11.6% over FY15-17E, with EBITDA margin at

18.1% in FY16 and 19% FY17. Figure 6: EBITDA margin movement in line with revenue growth

Source: Company, CRISIL Research

3.3 4.7

9.0

18.8

14.3

10.3

(0.9)2.1

(4.6)

17.1 17.3

18.7

19.1

18.6 18.3

13.8 14.5

18.3

10.0 11.0 12.0 13.0 14.0 15.0 16.0 17.0 18.0 19.0 20.0

(10.0)

(5.0)

-

5.0

10.0

15.0

20.0

Q2F

Y14

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

(%)

Revenue growth y-o-y EBITDA margin (LHS)

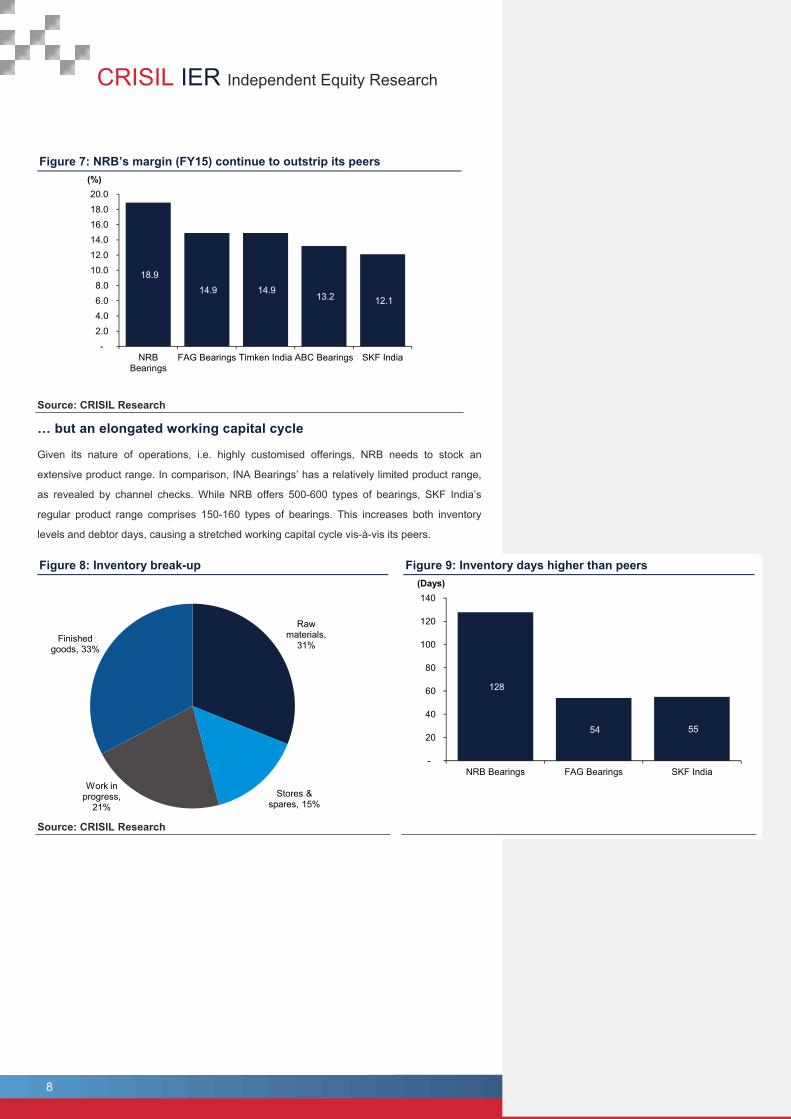

NRB has better EBITDA margin than its peers…

NRB’s product portfolio generates high margin as: (a) low-volume customised precision

bearings command a higher premium than the off-the-shelf bearings, that its competitors

specialise in; and (b) integrated operations, of engineering and design, in-house

manufacturing of needle/rollers, heat treatment, testing and final assembly of bearings,

enables to control cost.

7

CRISIL IER Independent Equity Research

8

Figure 7: NRB’s margin (FY15) continue to outstrip its peers

Source: CRISIL Research

… but an elongated working capital cycle

Given its nature of operations, i.e. highly customised offerings, NRB needs to stock an

extensive product range. In comparison, INA Bearings’ has a relatively limited product range,

as revealed by channel checks. While NRB offers 500-600 types of bearings, SKF India’s

regular product range comprises 150-160 types of bearings. This increases both inventory

levels and debtor days, causing a stretched working capital cycle vis-à-vis its peers. Figure 8: Inventory break-up Figure 9: Inventory days higher than peers

Source: CRISIL Research

18.9 14.9 14.9

13.2 12.1

- 2.0 4.0 6.0 8.0

10.0 12.0 14.0 16.0 18.0 20.0

NRBBearings

FAG Bearings Timken India ABC Bearings SKF India

(%)

Raw materials,

31%

Stores & spares, 15%

Work in progress,

21%

Finished goods, 33%

128

54 55

-

20

40

60

80

100

120

140

NRB Bearings FAG Bearings SKF India

(Days)

RESEARCH

NRB Bearings Ltd

9

Key Risks Dependence on domestic OEMs; cyclicality of industry NRB derives 63% of revenue from the domestic auto industry, which is cyclical in nature.

However, its presence across various sub-sectors (such as two-wheelers, three-wheelers, four

wheelers and commercial vehicles, etc.) mitigates this risk. Though we expect growth in the

auto industry to pick-up in H2FY16, a delay could have a negative impact.

Foreign currency volatility The company is exposed to foreign currency volatility through foreign currency loans and

exports (upto 24% of revenue). Although exports provide a natural hedge to its foreign

currency borrowings, the risk associated with volatile currency movements persists.

Volatility in raw material prices Passing on the rise in raw material costs - an industry-wide phenomenon - to customers is a

challenge. For instance, the company’s inability to pass on the sharp increase in raw material

costs (steel and oil) entirely to its customers led to low profitability in FY09.

CRISIL IER Independent Equity Research

10

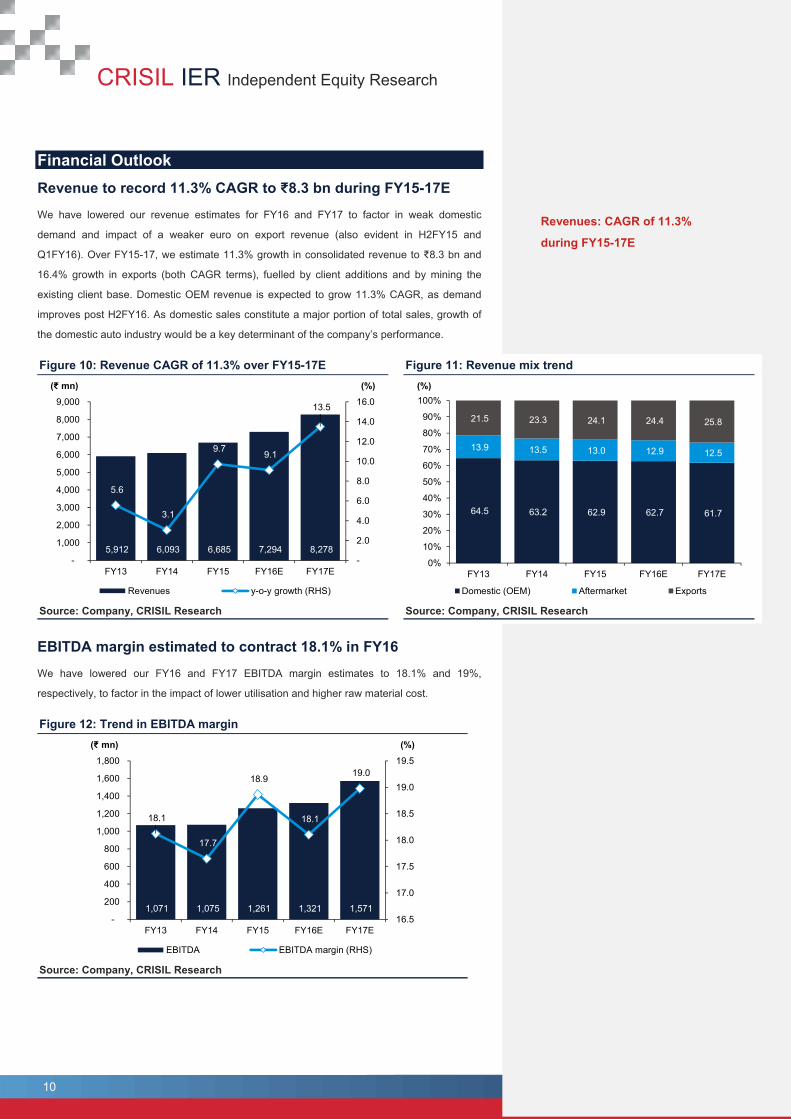

Financial Outlook Revenue to record 11.3% CAGR to ₹8.3 bn during FY15-17E We have lowered our revenue estimates for FY16 and FY17 to factor in weak domestic

demand and impact of a weaker euro on export revenue (also evident in H2FY15 and

Q1FY16). Over FY15-17, we estimate 11.3% growth in consolidated revenue to ₹8.3 bn and

16.4% growth in exports (both CAGR terms), fuelled by client additions and by mining the

existing client base. Domestic OEM revenue is expected to grow 11.3% CAGR, as demand

improves post H2FY16. As domestic sales constitute a major portion of total sales, growth of

the domestic auto industry would be a key determinant of the company’s performance. Figure 10: Revenue CAGR of 11.3% over FY15-17E Figure 11: Revenue mix trend

Source: Company, CRISIL Research Source: Company, CRISIL Research

EBITDA margin estimated to contract 18.1% in FY16 We have lowered our FY16 and FY17 EBITDA margin estimates to 18.1% and 19%,

respectively, to factor in the impact of lower utilisation and higher raw material cost. Figure 12: Trend in EBITDA margin

Source: Company, CRISIL Research

5,912 6,093 6,685 7,294 8,278

5.6

3.1

9.7 9.1

13.5

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

FY13 FY14 FY15 FY16E FY17E

(%)(₹ mn)

Revenues y-o-y growth (RHS)

64.5 63.2 62.9 62.7 61.7

13.9 13.5 13.0 12.9 12.5

21.5 23.3 24.1 24.4 25.8

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY13 FY14 FY15 FY16E FY17E

(%)

Domestic (OEM) Aftermarket Exports

1,071 1,075 1,261 1,321 1,571

18.1

17.7

18.9

18.1

19.0

16.5

17.0

17.5

18.0

18.5

19.0

19.5

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

FY13 FY14 FY15 FY16E FY17E

(%)(₹ mn)

EBITDA EBITDA margin (RHS)

Revenues: CAGR of 11.3%

during FY15-17E

RESEARCH

NRB Bearings Ltd

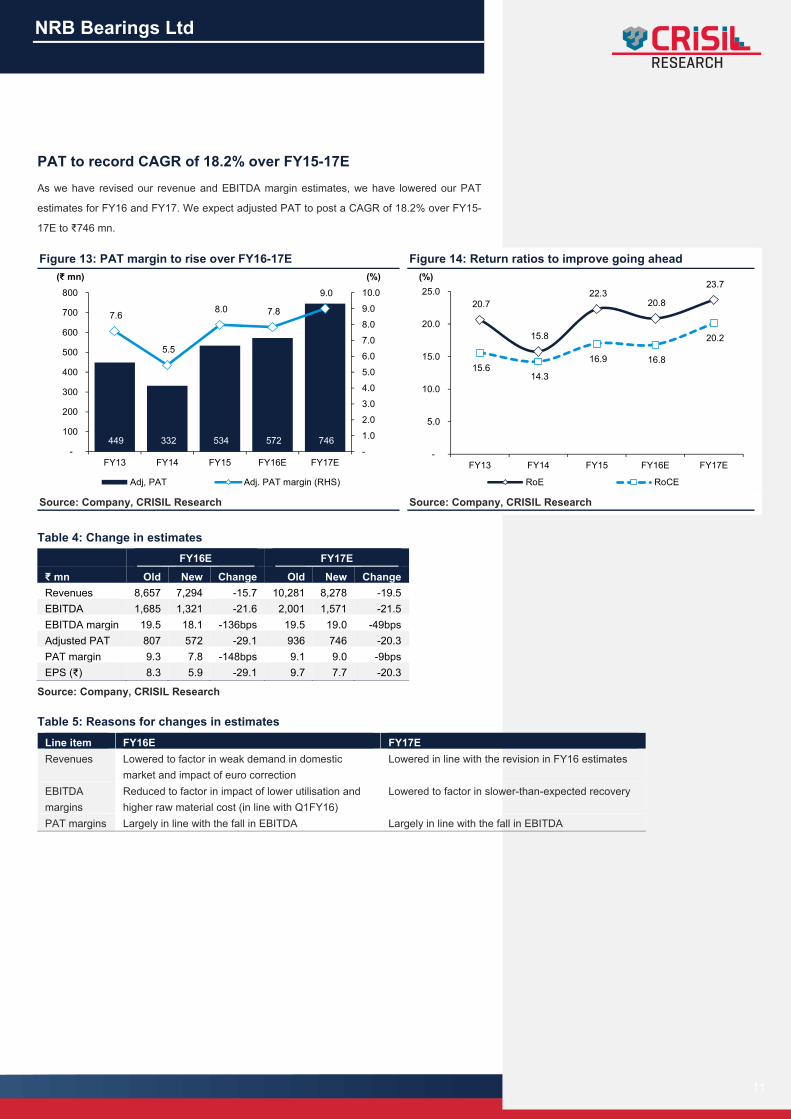

PAT to record CAGR of 18.2% over FY15-17E As we have revised our revenue and EBITDA margin estimates, we have lowered our PAT

estimates for FY16 and FY17. We expect adjusted PAT to post a CAGR of 18.2% over FY15-

17E to ₹746 mn. Figure 13: PAT margin to rise over FY16-17E Figure 14: Return ratios to improve going ahead

Source: Company, CRISIL Research Source: Company, CRISIL Research

449 332 534 572 746

7.6

5.5

8.0 7.8

9.0

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

-

100

200

300

400

500

600

700

800

FY13 FY14 FY15 FY16E FY17E

(%)(₹ mn)

Adj, PAT Adj. PAT margin (RHS)

20.7

15.8

22.3 20.8

23.7

15.6 14.3

16.9 16.8

20.2

-

5.0

10.0

15.0

20.0

25.0

FY13 FY14 FY15 FY16E FY17E

(%)

RoE RoCE

Table 4: Change in estimates

FY16E FY17E

₹ mn Old New Change Old New Change Revenues 8,657 7,294 -15.7 10,281 8,278 -19.5 EBITDA 1,685 1,321 -21.6 2,001 1,571 -21.5 EBITDA margin 19.5 18.1 -136bps 19.5 19.0 -49bps Adjusted PAT 807 572 -29.1 936 746 -20.3 PAT margin 9.3 7.8 -148bps 9.1 9.0 -9bps EPS (₹) 8.3 5.9 -29.1 9.7 7.7 -20.3

Source: Company, CRISIL Research Table 5: Reasons for changes in estimates

Line item FY16E FY17E Revenues Lowered to factor in weak demand in domestic

market and impact of euro correction Lowered in line with the revision in FY16 estimates

EBITDA margins

Reduced to factor in impact of lower utilisation and higher raw material cost (in line with Q1FY16)

Lowered to factor in slower-than-expected recovery

PAT margins Largely in line with the fall in EBITDA Largely in line with the fall in EBITDA

11

CRISIL IER Independent Equity Research

12

Management Overview CRISIL's fundamental grading methodology includes a broad assessment of management

quality, apart from other key factors such as industry and business prospects, and financial

performance. The board is broad-based; its members have multi-disciplinary experience,

which aids decision-making.

Experienced management Trilochan Singh Sahney, Executive Chairman, is the founder promoter of NRB. He has

handed over the operational management to his daughter Harshbeena Zaveri - currently the

Managing Director and President. She has almost 26 years of experience in the bearings

industry and spearheaded the company’s foray into design engineering. Under her leadership,

the company set up an R&D centre and increased export sales by tapping leading global

automobile OEMs. She is also the chairman of the board of SNL Bearings (subsidiary).

Strong focus on in-house R&D NRB set up an in-house R&D centre in 2000. This has enabled the company position itself as

a supplier of high-end /critical applications to domestic and global OEMs, offering a wide and

diversified product range. Being a preferred supplier also means that NRB is the first port of

call as global OEMs expand their footprint in India.

Strong second line of management The company has inducted various professionals at senior and mid-management levels, who

have significant experience in the bearings industry.

■ Tanushree Bagrodia, CFO, is an INSEAD MBA graduate and has substantial experience

in investment banking.

■ Sumit Mitra, MBA from IIM Calcutta, heads the international business and supply chain.

He has 16 years of experience in bearings, precision auto components and other

industries. He has previously worked at Honeywell Automation, SRF Group and Dalmia

Cement.

■ Mr Hemant Jog, Vice President, Manufacturing, heads the Waluj plant in Aurangabad.

He holds a Bachelor’s degree in Mechanical Engineering and Post Graduate Diploma in

Materials Management. He has 28 years of experience in the bearings industry.

■ Mr Hideki Kokubu, Vice President, International Business Development is responsible for

business from the ASEAN.

Fortune Magazine has ranked Ms.

Harshbeena Zaveri amongst the 15

most powerful businesswomen in

India from 2011 through 2014

RESEARCH

NRB Bearings Ltd

Corporate Governance CRISIL’s fundamental grading methodology includes a broad assessment of corporate

governance and management quality, apart from other key factors such as industry and

business prospects, and financial performance. In this context, CRISIL Research analyses

shareholding structure, board composition, typical board processes, disclosure standards and

related-party transactions. Any qualifications by regulators or auditors also serve as useful

inputs while assessing a company’s corporate governance.

NRB’s corporate governance is good. It is supported by a strong board and efficient practices.

It adheres to all regulatory requirements.

Board composition complies with the listing norms ■ The board comprises eight members, of whom one is an executive chairman and four

are independent directors, thereby meeting the requirements under Clause 49 of SEBI’s

listing guidelines.

Corporate governance is good. The

board has a judicious mix of

relevant and diversified experience ■ The independent directors are highly qualified, have strong industry experience and have

been on the board for more than three years.

Board processes ■ Necessary committees - audit, stakeholders’ relationship and nominations &

remuneration - are in place, headed by independent directors. These committees have a

wider scope and, hence, the decision-making process is collaborative and appropriate.

■ The company also has a Corporate Social Responsibility (CSR) committee that has

spent the mandatory 2% of average profit over last three years, reiterating the

management’s commitment to promote education and gender equality, empower women

and ensure environmental sustainability.

Quality of earnings and disclosure standards ■ Quality of earnings is good as reflected in the following:

- Accounting policies are appropriate and conservative.

- The company has been generating operating cash flow over last few years, in line

with revenue growth.

- High debtor and inventory days, due to the customised nature of its business, which

requires it to maintain high inventory.

Healthy dividend payment:

- The company has maintained a healthy dividend payout ratio of ~40% (average)

over last few years. Compared with PAT growth, the dividend payout is appropriate

and, hence, benefits minority shareholders.

Good disclosure standards:

- Based on publicly available information, including annual reports and website

uploads, the disclosure standards are satisfactory. Although the company does not

hold an investor conference call (post quarterly results), it shares information

regularly.

13

CRISIL IER Independent Equity Research

14

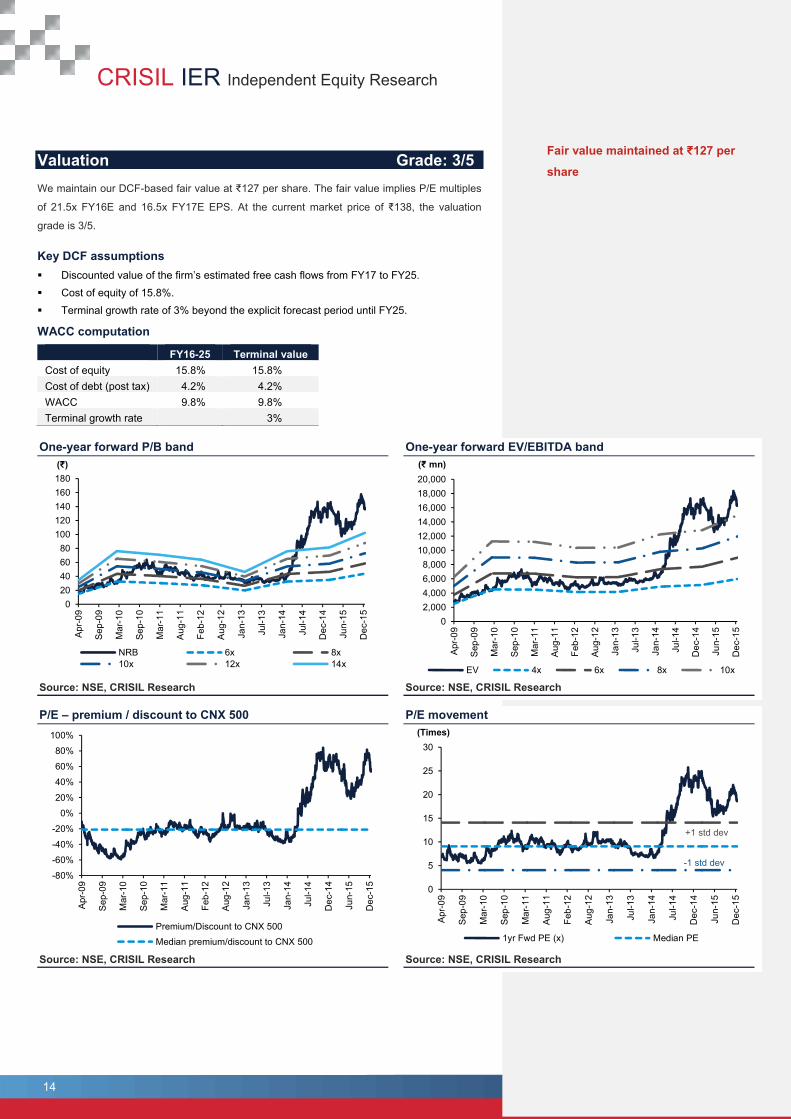

Valuation Grade: 3/5 We maintain our DCF-based fair value at ₹127 per share. The fair value implies P/E multiples

of 21.5x FY16E and 16.5x FY17E EPS. At the current market price of ₹138, the valuation

grade is 3/5. Key DCF assumptions Discounted value of the firm’s estimated free cash flows from FY17 to FY25. Cost of equity of 15.8%. Terminal growth rate of 3% beyond the explicit forecast period until FY25.

WACC computation

FY16-25 Terminal value Cost of equity 15.8% 15.8% Cost of debt (post tax) 4.2% 4.2% WACC 9.8% 9.8% Terminal growth rate 3%

One-year forward P/B band One-year forward EV/EBITDA band

Source: NSE, CRISIL Research Source: NSE, CRISIL Research

P/E – premium / discount to CNX 500 P/E movement

Source: NSE, CRISIL Research Source: NSE, CRISIL Research

020406080

100120140160180

Apr

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Aug

-11

Feb-

12

Aug

-12

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Dec

-14

Jun-

15

Dec

-15

(₹)

NRB 6x 8x10x 12x 14x

02,0004,0006,0008,000

10,00012,00014,00016,00018,00020,000

Apr

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Aug

-11

Feb-

12

Aug

-12

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Dec

-14

Jun-

15

Dec

-15

(₹ mn)

EV 4x 6x 8x 10x

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Apr

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Aug

-11

Feb-

12

Aug

-12

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Dec

-14

Jun-

15

Dec

-15

Premium/Discount to CNX 500Median premium/discount to CNX 500

0

5

10

15

20

25

30

Apr

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Aug

-11

Feb-

12

Aug

-12

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Dec

-14

Jun-

15

Dec

-15

(Times)

1yr Fwd PE (x) Median PE

+1 std dev

-1 std dev

Fair value maintained at ₹127 per

share

RESEARCH

NRB Bearings Ltd

15

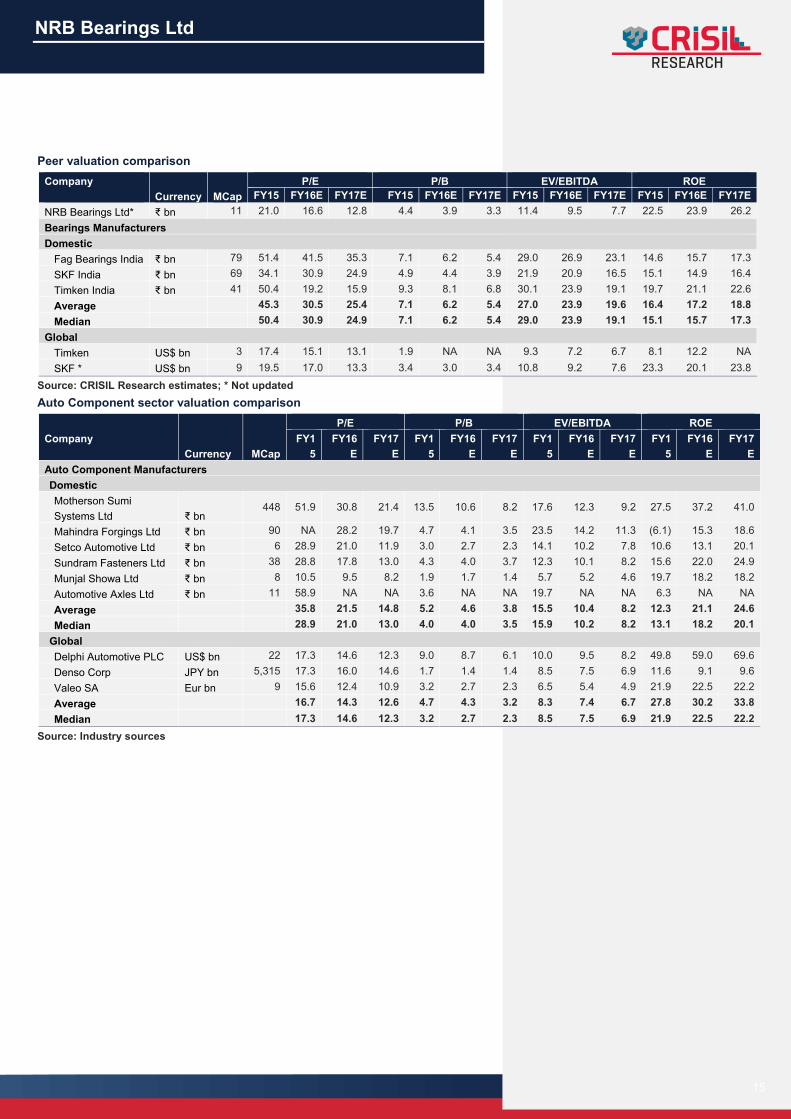

Peer valuation comparison Company Currency MCap

P/E P/B EV/EBITDA ROE FY15 FY16E FY17E FY15 FY16E FY17E FY15 FY16E FY17E FY15 FY16E FY17E

NRB Bearings Ltd* ₹ bn 11 21.0 16.6 12.8 4.4 3.9 3.3 11.4 9.5 7.7 22.5 23.9 26.2Bearings Manufacturers Domestic

Fag Bearings India ₹ bn 79 51.4 41.5 35.3 7.1 6.2 5.4 29.0 26.9 23.1 14.6 15.7 17.3SKF India ₹ bn 69 34.1 30.9 24.9 4.9 4.4 3.9 21.9 20.9 16.5 15.1 14.9 16.4Timken India ₹ bn 41 50.4 19.2 15.9 9.3 8.1 6.8 30.1 23.9 19.1 19.7 21.1 22.6Average 45.3 30.5 25.4 7.1 6.2 5.4 27.0 23.9 19.6 16.4 17.2 18.8Median 50.4 30.9 24.9 7.1 6.2 5.4 29.0 23.9 19.1 15.1 15.7 17.3

Global Timken US$ bn 3 17.4 15.1 13.1 1.9 NA NA 9.3 7.2 6.7 8.1 12.2 NASKF * US$ bn 9 19.5 17.0 13.3 3.4 3.0 3.4 10.8 9.2 7.6 23.3 20.1 23.8

Source: CRISIL Research estimates; * Not updated Auto Component sector valuation comparison

Company Currency MCap

P/E P/B EV/EBITDA ROE FY1

5 FY16

EFY17

EFY1

5FY16

EFY17

EFY1

5FY16

E FY17

E FY1

5FY16

EFY17

EAuto Component Manufacturers Domestic Motherson Sumi Systems Ltd ₹ bn

448 51.9 30.8 21.4 13.5 10.6 8.2 17.6 12.3 9.2 27.5 37.2 41.0

Mahindra Forgings Ltd ₹ bn 90 NA 28.2 19.7 4.7 4.1 3.5 23.5 14.2 11.3 (6.1) 15.3 18.6Setco Automotive Ltd ₹ bn 6 28.9 21.0 11.9 3.0 2.7 2.3 14.1 10.2 7.8 10.6 13.1 20.1Sundram Fasteners Ltd ₹ bn 38 28.8 17.8 13.0 4.3 4.0 3.7 12.3 10.1 8.2 15.6 22.0 24.9Munjal Showa Ltd ₹ bn 8 10.5 9.5 8.2 1.9 1.7 1.4 5.7 5.2 4.6 19.7 18.2 18.2Automotive Axles Ltd ₹ bn 11 58.9 NA NA 3.6 NA NA 19.7 NA NA 6.3 NA NAAverage 35.8 21.5 14.8 5.2 4.6 3.8 15.5 10.4 8.2 12.3 21.1 24.6Median 28.9 21.0 13.0 4.0 4.0 3.5 15.9 10.2 8.2 13.1 18.2 20.1

Global Delphi Automotive PLC US$ bn 22 17.3 14.6 12.3 9.0 8.7 6.1 10.0 9.5 8.2 49.8 59.0 69.6Denso Corp JPY bn 5,315 17.3 16.0 14.6 1.7 1.4 1.4 8.5 7.5 6.9 11.6 9.1 9.6Valeo SA Eur bn 9 15.6 12.4 10.9 3.2 2.7 2.3 6.5 5.4 4.9 21.9 22.5 22.2Average 16.7 14.3 12.6 4.7 4.3 3.2 8.3 7.4 6.7 27.8 30.2 33.8Median 17.3 14.6 12.3 3.2 2.7 2.3 8.5 7.5 6.9 21.9 22.5 22.2

Source: Industry sources

CRISIL IER Independent Equity Research

16

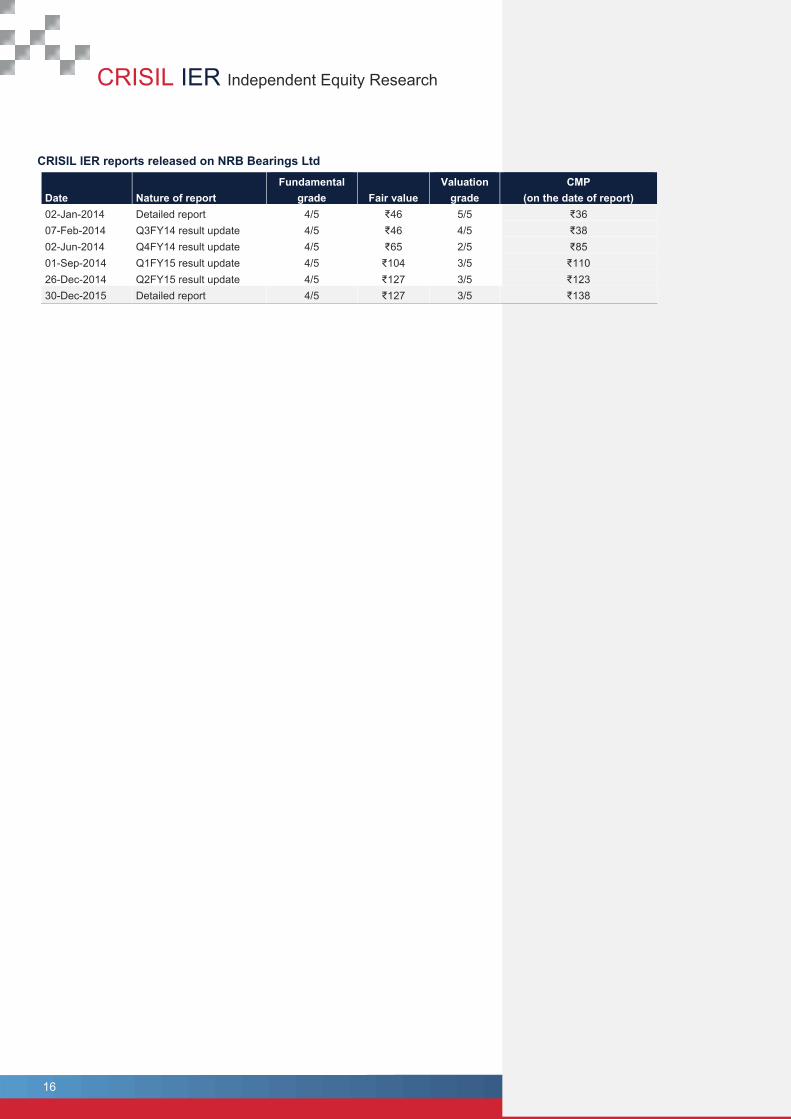

CRISIL IER reports released on NRB Bearings Ltd

Date Nature of report Fundamental

grade Fair value Valuation

grade CMP

(on the date of report) 02-Jan-2014 Detailed report 4/5 ₹46 5/5 ₹36 07-Feb-2014 Q3FY14 result update 4/5 ₹46 4/5 ₹38 02-Jun-2014 Q4FY14 result update 4/5 ₹65 2/5 ₹85 01-Sep-2014 Q1FY15 result update 4/5 ₹104 3/5 ₹110 26-Dec-2014 Q2FY15 result update 4/5 ₹127 3/5 ₹123 30-Dec-2015 Detailed report 4/5 ₹127 3/5 ₹138

RESEARCH

NRB Bearings Ltd

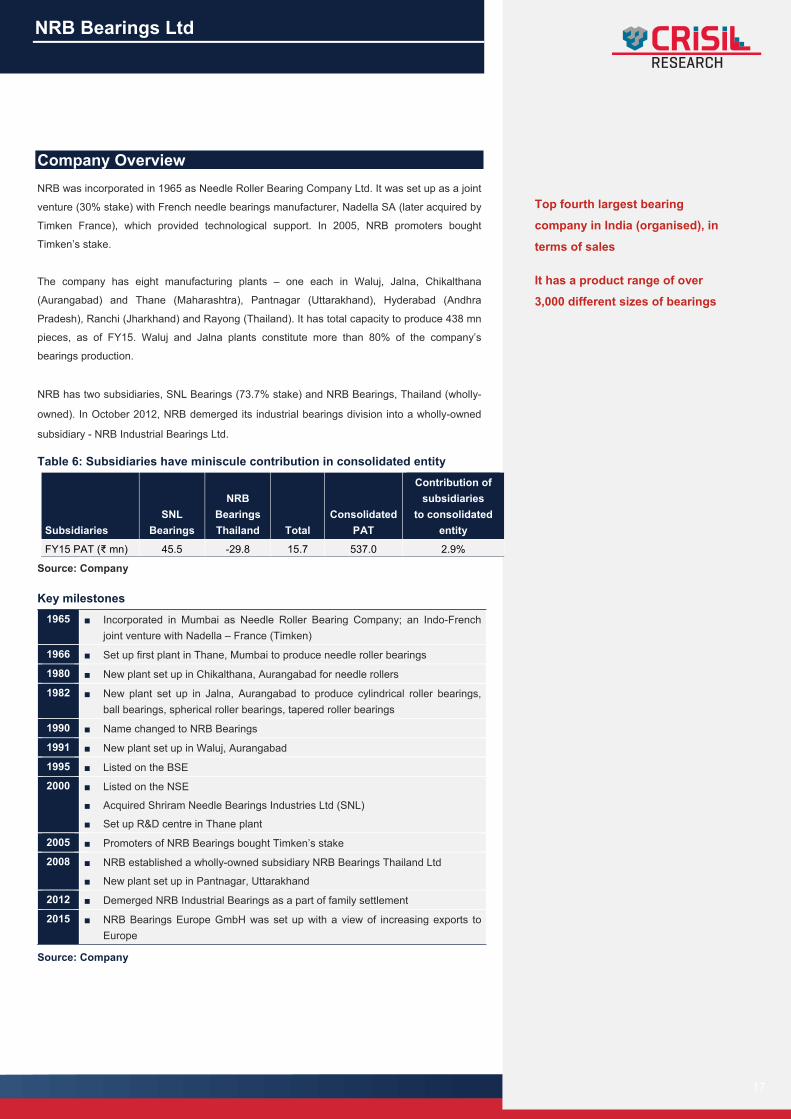

Company Overview NRB was incorporated in 1965 as Needle Roller Bearing Company Ltd. It was set up as a joint

venture (30% stake) with French needle bearings manufacturer, Nadella SA (later acquired by

Timken France), which provided technological support. In 2005, NRB promoters bought

Timken’s stake.

Top fourth largest bearing

company in India (organised), in

terms of sales

It has a product range of over

3,000 different sizes of bearings The company has eight manufacturing plants – one each in Waluj, Jalna, Chikalthana

(Aurangabad) and Thane (Maharashtra), Pantnagar (Uttarakhand), Hyderabad (Andhra

Pradesh), Ranchi (Jharkhand) and Rayong (Thailand). It has total capacity to produce 438 mn

pieces, as of FY15. Waluj and Jalna plants constitute more than 80% of the company’s

bearings production.

NRB has two subsidiaries, SNL Bearings (73.7% stake) and NRB Bearings, Thailand (wholly-

owned). In October 2012, NRB demerged its industrial bearings division into a wholly-owned

subsidiary - NRB Industrial Bearings Ltd.

Table 6: Subsidiaries have miniscule contribution in consolidated entity

Subsidiaries SNL

Bearings

NRB Bearings Thailand Total

Consolidated PAT

Contribution of subsidiaries

to consolidated entity

FY15 PAT (₹ mn) 45.5 -29.8 15.7 537.0 2.9%

Source: Company Key milestones

1965 ■ Incorporated in Mumbai as Needle Roller Bearing Company; an Indo-French joint venture with Nadella – France (Timken)

1966 ■ Set up first plant in Thane, Mumbai to produce needle roller bearings

1980 ■ New plant set up in Chikalthana, Aurangabad for needle rollers

1982 ■ New plant set up in Jalna, Aurangabad to produce cylindrical roller bearings, ball bearings, spherical roller bearings, tapered roller bearings

1990 ■ Name changed to NRB Bearings

1991 ■ New plant set up in Waluj, Aurangabad

1995 ■ Listed on the BSE

2000 ■ Listed on the NSE

■ Acquired Shriram Needle Bearings Industries Ltd (SNL)

■ Set up R&D centre in Thane plant

2005 ■ Promoters of NRB Bearings bought Timken’s stake

2008 ■ NRB established a wholly-owned subsidiary NRB Bearings Thailand Ltd

■ New plant set up in Pantnagar, Uttarakhand

2012 ■ Demerged NRB Industrial Bearings as a part of family settlement

2015 ■ NRB Bearings Europe GmbH was set up with a view of increasing exports to Europe

Source: Company

17

CRISIL IER Independent Equity Research

18

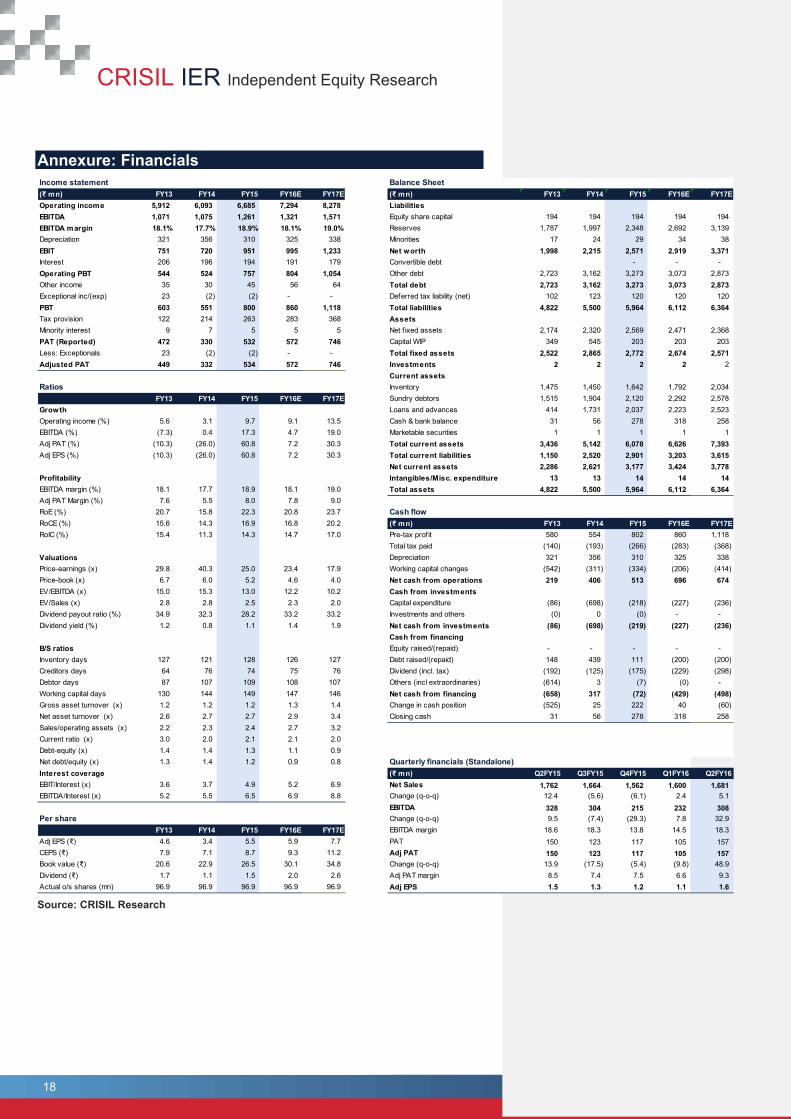

Annexure: Financials

Source: CRISIL Research

Income statement Balance Sheet(₹ mn) FY13 FY14 FY15 FY16E FY17E (₹ mn) FY13 FY14 FY15 FY16E FY1Operating income 5,912 6,093 6,685 7,294 8,278 LiabilitiesEBITDA 1,071 1,075 1,261 1,321 1,571 Equity share capital 194 194 194 194 194 EBITDA margin 18.1% 17.7% 18.9% 18.1% 19.0% Reserves 1,787 1,997 2,348 2,692 3,139 Depreciation 321 356 310 325 338 Minorities 17 24 29 34 38 EBIT 751 720 951 995 1,233 Net worth 1,998 2,215 2,571 2,919 3,371 Interest 206 196 194 191 179 Convertible debt - - - Operating PBT 544 524 757 804 1,054 Other debt 2,723 3,162 3,273 3,073 2,873 Other income 35 30 45 56 64 Total debt 2,723 3,162 3,273 3,073 2,873 Exceptional inc/(exp) 23 (2) (2) - - Deferred tax liability (net) 102 123 120 120 120 PBT 603 551 800 860 1,118 Total liabilities 4,822 5,500 5,964 6,112 6,364 Tax provision 122 214 263 283 368 AssetsMinority interest 9 7 5 5 5 Net f ixed assets 2,174 2,320 2,569 2,471 2,368 PAT (Reported) 472 330 532 572 746 Capital WIP 349 545 203 203 203 Less: Exceptionals 23 (2) (2) - - Total fixed assets 2,522 2,865 2,772 2,674 2,571 Adjusted PAT 449 332 534 572 746 Investments 2 2 2 2 2

Current assetsRatios Inventory 1,475 1,450 1,642 1,792 2,034

FY13 FY14 FY15 FY16E FY17E Sundry debtors 1,515 1,904 2,120 2,292 2,578 Growth Loans and advances 414 1,731 2,037 2,223 2,523 Operating income (%) 5.6 3.1 9.7 9.1 13.5 Cash & bank balance 31 56 278 318 258 EBITDA (%) (7.3) 0.4 17.3 4.7 19.0 Marketable securities 1 1 1 1 1 Adj PAT (%) (10.3) (26.0) 60.8 7.2 30.3 Total current assets 3,436 5,142 6,078 6,626 7,393 Adj EPS (%) (10.3) (26.0) 60.8 7.2 30.3 Total current liabilities 1,150 2,520 2,901 3,203 3,615

Net current assets 2,286 2,621 3,177 3,424 3,778 Profitability Intangibles/Misc. expenditure 13 13 14 14 14 EBITDA margin (%) 18.1 17.7 18.9 18.1 19.0 Total assets 4,822 5,500 5,964 6,112 6,364 Adj PAT Margin (%) 7.6 5.5 8.0 7.8 9.0 RoE (%) 20.7 15.8 22.3 20.8 23.7 Cash flowRoCE (%) 15.6 14.3 16.9 16.8 20.2 (₹ mn) FY13 FY14 FY15 FY16E FY1RoIC (%) 15.4 11.3 14.3 14.7 17.0 Pre-tax prof it 580 554 802 860 1,118

Total tax paid (140) (193) (266) (283) (368) Valuations Depreciation 321 356 310 325 338 Price-earnings (x) 29.8 40.3 25.0 23.4 17.9 Working capital changes (542) (311) (334) (206) (414) Price-book (x) 6.7 6.0 5.2 4.6 4.0 Net cash from operations 219 406 513 696 674 EV/EBITDA (x) 15.0 15.3 13.0 12.2 10.2 Cash from investmentsEV/Sales (x) 2.8 2.8 2.5 2.3 2.0 Capital expenditure (86) (698) (218) (227) (236) Dividend payout ratio (%) 34.9 32.3 28.2 33.2 33.2 Investments and others (0) 0 (0) - - Dividend yield (%) 1.2 0.8 1.1 1.4 1.9 Net cash from investments (86) (698) (219) (227) (236)

Cash from financingB/S ratios Equity raised/(repaid) - - - - - Inventory days 127 121 128 126 127 Debt raised/(repaid) 148 439 111 (200) (200) Creditors days 64 76 74 75 76 Dividend (incl. tax) (192) (125) (175) (229) (298) Debtor days 87 107 109 108 107 Others (incl extraordinaries) (614) 3 (7) (0) - Working capital days 130 144 149 147 146 Net cash from financing (658) 317 (72) (429) (498) Gross asset turnover (x) 1.2 1.2 1.2 1.3 1.4 Change in cash position (525) 25 222 40 (60) Net asset turnover (x) 2.6 2.7 2.7 2.9 3.4 Closing cash 31 56 278 318 258 Sales/operating assets (x) 2.2 2.3 2.4 2.7 3.2 Current ratio (x) 3.0 2.0 2.1 2.1 2.0 Debt-equity (x) 1.4 1.4 1.3 1.1 0.9 Net debt/equity (x) 1.3 1.4 1.2 0.9 0.8 Quarterly financials (Standalone)Interest coverage (₹ mn) Q2FY15 Q3FY15 Q4FY15 Q1FY16 Q2FY16EBIT/Interest (x) 3.6 3.7 4.9 5.2 6.9 Net Sales 1,762 1,664 1,562 1,600 1,681 EBITDA/Interest (x) 5.2 5.5 6.5 6.9 8.8 Change (q-o-q) 12.4 (5.6) (6.1) 2.4 5.1

FY17E EBITDA 328 304 215 232 308 Per share Change (q-o-q) 9.5 (7.4) (29.3) 7.8 32.9

FY13 FY14 FY15 FY16E FY17E EBITDA margin 18.6 18.3 13.8 14.5 18.3 Adj EPS (₹) 4.6 3.4 5.5 5.9 7.7 PAT 150 123 117 105 157 CEPS (₹) 7.9 7.1 8.7 9.3 11.2 Adj PAT 150 123 117 105 157 Book value (₹) 20.6 22.9 26.5 30.1 34.8 Change (q-o-q) 13.9 (17.5) (5.4) (9.8) 48.9 Dividend (₹) 1.7 1.1 1.5 2.0 2.6 Adj PAT margin 8.5 7.4 7.5 6.6 9.3 Actual o/s shares (mn) 96.9 96.9 96.9 96.9 96.9 Adj EPS 1.5 1.3 1.2 1.1 1.6

7E

7E

RESEARCH

NRB Bearings Ltd

Focus Charts NRB’s revenue growth linked with auto growth Exports recorded 39.8% CAGR over FY11-15

Source: CRISIL Research Source: CRISIL Research

Euro - southward bound NRB’s margin (FY15) continue to outstrip its peers

Source: Company, CRISIL Research

Fair value movement since initiation Share price movement

-Indexed to 100

Source: NSE, BSE, CRISIL Research Source: NSE, CRISIL Research

14.2

0.9

4.6 8.0

16.4

5.3

3.0

9.8

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

FY12 FY13 FY14 FY15

(%)

Auto Production NRB's Revenues y-o-y

406 705 1,225 1,359 1,548

8.7

13.0

21.5 23.3 24.1

-

5.0

10.0

15.0

20.0

25.0

30.0

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

FY11 FY12 FY13 FY14 FY15

(%)(₹ mn)

Export revenues % of total revenues (RHS)

60.0

65.0

70.0

75.0

80.0

85.0

90.0

Apr-1

4M

ay-1

4Ju

n-14

Jul-1

4A

ug-1

4S

ep-1

4O

ct-1

4N

ov-1

4D

ec-1

4Ja

n-15

Feb-

15M

ar-1

5Ap

r-15

May

-15

Jun-

15Ju

l-15

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

(INR/Euro)

18.9 14.9 14.9

13.2 12.1

- 2.0 4.0 6.0 8.0

10.0 12.0 14.0 16.0 18.0 20.0

NRBBearings

FAG Bearings Timken India ABC Bearings SKF India

(%)

0

500

1,000

1,500

2,000

2,500

3,000

0204060

80100120

140160180

Jan-

14

Feb-

14

Apr

-14

May

-14

Jul-1

4

Sep

-14

Oct

-14

Dec

-14

Feb-

15

Mar

-15

May

-15

Jul-1

5

Aug

-15

Oct

-15

Dec

-15

('000)(₹)

Total Traded Quantity (RHS) CRISIL Fair Value NRB

0

50

100

150

200

250

300

350

400

450

Jan-

14

Feb-

14

Apr

-14

May

-14

Jul-1

4

Sep

-14

Oct

-14

Dec

-14

Feb-

15

Mar

-15

May

-15

Jul-1

5

Aug

-15

Oct

-15

Dec

-15

NRB CNX500

19

CRISIL IER Independent Equity Research

This page is intentionally left blank

RESEARCH

This page is intentionally left blank

CRISIL IER Independent Equity Research

This page is intentionally left blank

RESEARCH

CRISIL Research Team

Senior Director

Manish Jaiswal CRISIL Research +91 22 3342 8290 [email protected]

Analytical Contacts

Prasad Koparkar Senior Director, Industry & Customised Research +91 22 3342 3137 [email protected]

Binaifer Jehani Director, Customised Research +91 22 3342 4091 [email protected]

Manoj Damle Director, Customised Research +91 22 3342 3342 [email protected]

Manoj Mohta Director, Customised Research +91 22 3342 3554 [email protected]

Jiju Vidyadharan Director, Funds & Fixed Income Research +91 22 3342 8091 [email protected]

Ajay Srinivasan Director, Industry Research +91 22 3342 3530 [email protected]

Rahul Prithiani Director, Industry Research +91 22 3342 3574 [email protected]

Ajay D'Souza Director, New Product Development +91 22 3342 3567 [email protected]

Business Development

Prosenjit Ghosh Director, Industry & Customised Research +91 99206 56299 [email protected]

Megha Agrawal Associate Director +91 98673 90805 [email protected]

Neeta Muliyil Associate Director +91 99201 99973 [email protected]

Ankesh Baghel Regional Manager (West) +91 98191 21510 [email protected]

Ravi Lath Regional Manager (West) +91 98200 62424 [email protected]

Sarrthak Sayal Regional Manager (North) +91 95828 06789 [email protected]

Priyanka Murarka Regional Manager (East) +91 99030 60685 [email protected]

Naveena R Regional Manager (Karnataka & Kerala) +91 95383 33088 [email protected]

Sanjay Krishnaa Regional Manager (Tamil Nadu & AP) +91 98848 06606 [email protected]

CRISIL IER Independent Equity Research

Our Capabilities

Making Markets Function Better

Economy and Industry Research ■ Largest team of economy and industry research analysts in India

■ Acknowledged premium, high quality research provider with track record spanning two decades

■ 95% of India’s commercial banking industry by asset base uses our industry research for credit decisions

■ Coverage on 86 industries: We provide analysis and forecast on key industry parameters including demand, supply,prices, investments and profitability, along with insightful opinions on emerging trends and impact of key events

■ Research on sectors and clusters dominated by small and medium enterprises covering analysis of relative attractiveness,growth prospects and financial performance

■ High-end customised research for many leading Indian and global corporates in areas such as market sizing, demandforecasting, project feasibility and entry strategy

Funds and Fixed Income Research ■ Largest and most comprehensive database on India’s debt market, covering more than 18,000 securities

■ Largest provider of fixed income valuations in India

■ Provide valuation for more than ₹81 trillion (US$ 1,275 billion) of Indian debt securities

■ Sole provider of fixed income and hybrid indices to mutual funds and insurance companies; we maintain 37 standardindices and over 100 customised indices

■ Ranking of Indian mutual fund schemes covering 75% of assets under management and ₹9 trillion (US$ 144 billion)by value

■ Business review consultants to The Employees’ Provident Fund Organisation (EPFO) and The National Pension System(NPS) Trust in monitoring performance of their fund managers

Equity and Company Research ■ Assigned the first IPO grade in India; graded more than 100 IPOs till date

■ Due Diligence and Valuation services across sectors; executed close to 100 valuation assignments

■ Due Diligence, IPO Grading and Independent Equity Research for SME companies planning to list or already listed in NSEEmerge platform

■ First research house to release exchange-commissioned equity research reports in India; covered 1,488 firms listed andtraded on the National Stock Exchange

Executive Training ■ Conducted 1200+ training programs on a wide spectrum of topics including credit, risk, retail finance, treasury, and

corporate advisory; trained more than 24,000 professionals till date

■ Training programs being conducted in India, Sri Lanka and Bangladesh through an extensive network of well-qualifiedfinancial professionals

Our Office

Ahmedabad 706, Venus Atlantis Nr. Reliance Petrol Pump Prahladnagar, Ahmedabad, India Phone: +91 79 4024 4500 Fax: +91 79 2755 9863

Hyderabad 3rd Floor, Uma Chambers Plot No. 9&10, Nagarjuna Hills, (Near Punjagutta Cross Road) Hyderabad - 500 482, India Phone: +91 40 2335 8103/05 Fax: +91 40 2335 7507

Bengaluru W-101, Sunrise Chambers, 22, Ulsoor Road, Bengaluru - 560 042, India Phone: +91 80 2558 0899

+91 80 2559 4802 Fax: +91 80 2559 4801

Kolkata Horizon, Block 'B', 4th Floor 57 Chowringhee Road Kolkata - 700 071, India Phone: +91 33 2289 1949/50 Fax: +91 33 2283 0597

Chennai Thapar House, 43/44, Montieth Road, Egmore, Chennai - 600 008, India Phone: +91 44 2854 6205/06

+91 44 2854 6093 Fax: +91 44 2854 7531

Pune 1187/17, Ghole Road, Shivaji Nagar, Pune - 411 005, India Phone: +91 20 2553 9064/67 Fax: +91 20 4018 1930

Gurgaon Plot No. 46 Sector 44 Opp. PF Office Gurgaon - 122 003, India Phone: +91 124 6722 000

Stay Connected | CRISIL Website | Twitter | LinkedIn |

YouTube | Facebook

CRISIL Limited CRISIL House, Central Avenue, Hiranandani Business Park, Powai, Mumbai – 400076. India Phone: +91 22 3342 3000 | Fax: +91 22 3342 8088 www.crisil.com

CRISIL Ltd is a Standard & Poor's company