CREDIT BUREAU REPORTING: What you should be asking your Collection Agency and Why? Tuesday, June 2,...

47

CREDIT BUREAU REPORTING: What you should be asking your Collection Agency and Why? Tuesday, June 2, 2015

-

Upload

amy-helena-griffith -

Category

Documents

-

view

221 -

download

2

Transcript of CREDIT BUREAU REPORTING: What you should be asking your Collection Agency and Why? Tuesday, June 2,...

CREDIT BUREAU REPORTING:

What you should be asking your Collection Agency and Why?

Tuesday, June 2, 2015

Kenlyn T. GretzPresident and CEO

Email: [email protected]

This is not legal advice. You should contact your company attorney for legal

advice.

In 2014, Roughly 1 in 5 American Adults Were Contacted by a Debt Collection Agency about Medical

Bills” – Nerd Wallet

http://www.nerdwallet.com/blog/health/2014/10/08/medical-bills-debt-crisis/#_ftn2

Medical Debt Responsibility Act

According to the U.S. Census, there are 245 million American adults 18 or over.

According to the Urban Institute, more than one-third of adults have debt in collections.

According to the ACA’s Top Market Collections, the majority of new business in the third-party

collections market is for health.

Who do they report to?Big Three Credit Bureaus

Some counties still have smaller credit bureaus

Usually ineffective

What do they know about the FCRA?

Not just the agency saying:

“we have to report

what is true and accurate.”

Fair Credit Reporting Act

Fair Credit Reporting Act

The plaintiff has two years from the date of discovering the violation that is the basis for liability or five years from the date on which the cause of action arose, whichever is earlier.

Example:

If the violation occurs on Jan 01, 2005, the plaintiff has until Jan 01, 2010 to file suit.

Fair Credit Reporting ActThe plaintiff has two years from the date of discovering

the violation that is the basis for liability or five years from the date on which the cause of action arose, whichever is earlier.

Example:

If the plaintiff discovers the violation on Jan 01, 2006, the plaintiff only has until Jan 01, 2008 to file suit as the Statute of Limitations would run from the date of discovery.

Fair Credit Reporting Act

The plaintiff has two years from the date of discovering the violation that is the basis for liability or five years from the date on which the cause of action arose, whichever is earlier.

Example:

If the plaintiff discovers the violation on Jan 01, 2009, the plaintiff only has until Jan 01, 2010 to file suit because the five year statute of limitation cannot be extended by the discovery of the violation.

Fair Credit Reporting Act

Willful violations: $100 to $1000 per violation, attorney fees and punitive damages.

Negligent violations: only awarded actual damages and attorney fees.

Do they have enough FCRA compliance education?

Do they have a CCCO on staff?

Credit & Collection Compliance Officer (CCCO) Designation (Advanced Level)Designed for the advanced professional, typically a Chief Compliance Officer, this designation provides an in-depth range of knowledge on compliance strategy in the debt collection industry.

Fair Credit Reporting Act Certificate from

Consumer Data Industry Association

http://www.cdiaonline.org/About/content.cfm?ItemNumber=10922

Who We Report To and When All Three $10.00 for Experian and Equifax and $50.00

TransUnion 10th & 25th of the month after 60 days of listings –

METRO2 Format of Data Allows notice and many phone attempts Lenders do not always pull all three bureaus

What We Report

Creditor Name unless Medical, then it says Medical Account

Amount owed Original Default date from the original

creditor Any payments made at our office Compliance Condition Code Redacted Account number

Update Frequency

Within next 2-3 months, we are moving toward reporting daily to decrease the amount of calls about credit files.

Why We Report

Leverage to pay before Smaller Balances have no legal leverage Leverage to pay when denied Canceled must remove from credit file-FCRA Skips Refuse to communicate

Credit Bureau Listings

Lowers Score for 7 years Even after paid, but not as much Consumer who is paying monthly will have a

better score than those that do not pay until the end.

Lenders will often require consumers to pay the debts before a loan can be issued, especially now.

I don’t Care “I don’t care if you put it on my credit file, it is messed up!” “I don’t care if you list the account with Americollect, my credit

is ruined anyway.”

“John, you sound like a hard working person who is really struggling now. I realize that right now, you may think – what is one more account. In a year or so from now when you are working hard at re-building your credit, you may think that “I wish I would have worked with XYZ’s office when they called to work out a payment plan.” John – I have several options for you.”

Demand for Removal

Not allowed.

I need to get this account paid in full.It is on my credit file.

Your Staff Gets the Inbound

“Thanks for calling and I am sure I can help you, but I first need to update my system. What is your current address? Phone number, including cell number.”

Get Info.

“Now are you trying to get a loan or have you been denied?”

Get Info.

“I personally cannot help you, but I am going to transfer you to our collection agency. One second.”

Call us with your info or use weblink www.americollect.com

Your Staff Gets the Inbound

Why should you not give a pay out? Legal Interest Unrecorded Court costs or attorney fees

Sometimes you still take the payment. We understand. WRONG:“Your account is cleared in full and your credit will be cleared up

(removed ).”

CORRECT: “The balance that we show is paid in full but you may owe more to the agency. You can call them and check. I will be contacting them with your payment of $.XX. They will report to the credit bureau what is true and accurate within 30 days.”

Helping Out

Hurry to Pay You – When they want something.

15 days to update with credit bureau normal way-inline Metro2 reporting.

If they ask, we offer to send a letter to their financial institution.

The can be your customer again.

What are the agency’s reasons for removal of a credit file?

Removal Circumstances

Account was listed in error Mistake made on your part Misapplied payments Certain instances where consumer didn’t get

notification of the debt Payment in Full at times.

How long? Consumer 15 days but soon, daily.

We can do it instantly, but a manual process.

How do they handle repeat frivolous credit bureau disputes?

Sample Letters

Credit Repair Companies

Rip Off All of the instructions are at

www.annualcreditreport.com

=

Credit Repair

Reporting Accurate Negative InformationWhen negative information in your report is accurate, only the

passage of time can assure its removal. A consumer reporting company can report most accurate negative information for seven years and bankruptcy information for 10 years. Information about an unpaid judgment against you can be reported for seven years or until the statute of limitations runs out, whichever is longer. To calculate the seven-year reporting period, start from the date the event took place.

Is the agency prepared to deal with the NY Attorney General

Schneiderman?

Knowledge Center

http://www.americollect.com/three-national-credit-reporting-agencies-settle-with-new-york-a-g-schneiderman/

Schneiderman Agreement

Phase 1 initiatives: Completed within 180 days.DOBs will be required. Americollect will be prohibited from reporting debts without a date of birth and Experian, Equifax, and TransUnion will reject data that does not comply with this requirement.

Guarantor DOB’s are important. Please add them to your placement files or create a piggy back file.

Schneiderman Agreement

Phase 2 initiatives: Completed within 18 monthsMust have a CCC of “BP: Paid by Insurance” and “AB: Being paid by insurance” While delinquencies ordinarily remain on credit reports even after a debt has been paid, Experian, Equifax, and TransUnion will remove all medical debts from a consumer’s credit report after the debt is paid by insurance.

(CRAs will remove these from the credit file – III.A.3.c)

Clients need to tell us if insurance paid or personal paid.

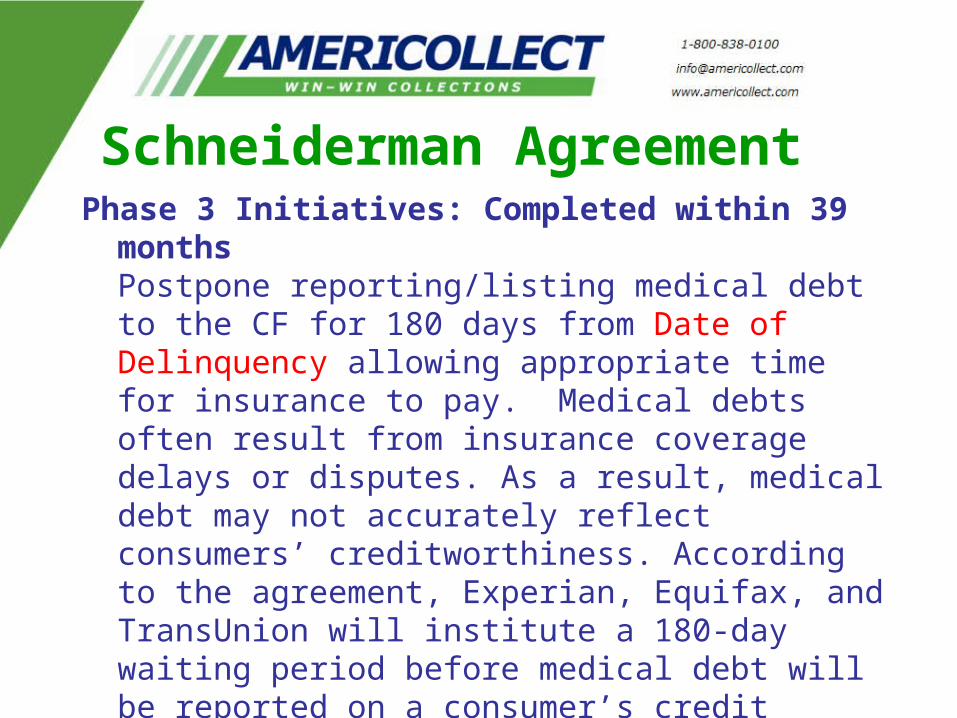

Schneiderman AgreementPhase 3 Initiatives: Completed within 39 months

Postpone reporting/listing medical debt to the CF for 180 days from Date of Delinquency allowing appropriate time for insurance to pay. Medical debts often result from insurance coverage delays or disputes. As a result, medical debt may not accurately reflect consumers’ creditworthiness. According to the agreement, Experian, Equifax, and TransUnion will institute a 180-day waiting period before medical debt will be reported on a consumer’s credit report.

Does your agency have the tools?

What are they doing about IRS Rule 501(r)

http://www.americollect.com/501r/

Shawn Gretz, VP of Marketing

501(r) for Non-Profits

Extraordinary Collection Activity

Credit Bureau Reporting must

be done AFTER 120 days from

first discharge bill date.

Are you providing the first post discharge bill date?

Can your statement vendor provide this?

How do they handle E-Oscar Management?

E-oscar!!

http://www.e-oscar.org/

What is their back log? Do they simply remove from the credit

file or do they do an investigation? Skill set of those working it.

Join Us NEXT WEEK For ASpecial Webinar

501(r)(6) ECA & CREATING COLLECTION POLICYLearn the Requirements to Stay Compliant

Host: Shawn Gretz

Tuesday, June 9th, 20151:00 PM - 1:45 PM CST

If you would like to register today, visit our website at https://attendee.gotowebinar.com/register/5530171118996348162

OR send an email to [email protected]

JOIN US AGAIN IN AUGUST NEXT WEBINAR

CHAPTER 13 BANKRUPTCYDoes it pay for you to file a claim based on the labor and

repayment length? Host: Kenlyn T. Gretz

Tuesday, August 11, 20151:00 PM - 1:45 PM CST

If you would like to register today, visit our website at https://attendee.gotowebinar.com/register/6758039732159836930

OR send an email to [email protected]

You’ll receive a registration email about two weeks prior to the webinar.

Thank You. [email protected]

SIX time winner of Inc Magazine’s Fastest Growing Private Company!

2009 – 2014

SIX time winner of Inside ARM Best Places to work in Collections.