Country update: Indonesia, Philippines · PDF filenatural resources attracting demand ......

66

Country update: Indonesia, Philippines and Thailand www.pwc.com Brian Arnold Partner, PwC Indonesia Lawrence Biscocho Partner, PwC Philippines Somboon Weerawutiwong Partner, PwC Thailand

-

Upload

nguyenkiet -

Category

Documents

-

view

215 -

download

2

Transcript of Country update: Indonesia, Philippines · PDF filenatural resources attracting demand ......

Country update: Indonesia, Philippines and Thailand

www.pwc.com

Brian ArnoldPartner, PwC IndonesiaLawrence BiscochoPartner, PwC PhilippinesSomboon WeerawutiwongPartner, PwC Thailand

Indonesia

Brian ArnoldPartner, PwC Indonesia

PwC

Highlights of the past year

• 2014 was a landmark year for Indonesian politics

• Jokowi was elected President after a fair and transparent election process – tight race but clearly democracy at work

• Initial sentiment from the foreign business community was very positive

• But reality has quickly settled in

• Will things improve?

3Global Tax Symposium – Asia 2015

PwC

Considerations for investment in Indonesia

Strengths

Amongst the top 50 fastest improving

economies

Large consumption base with rising middle income

Proven abundance of natural resources attracting demand

from China and India

Low labour costs attracting outsourcing

opportunities

Challenges

Slowing economy –GDP expected to dip

below 5% in 2015

Underdeveloped infrastructure

Labour union issues

Difficult tax and regulatory landscape,

rule of law issues

Opportunities

Active reformation of business regulations

Attempts to simplify regulatory

requirements

Government support to lift up infrastructure

Huge untapped potential in the eastern

part of the country

Tone from the top has become more friendly to foreign investment, but still troubling developments in the regulatory environment

4Global Tax Symposium – Asia 2015

PwC

Tax landscape

5Global Tax Symposium – Asia 2015PwC

PwC

Very small companies(Turnover

<IDR4.8bn)

1% final of turnover

General tax tariff

Corporate tax25%

Public companies

20%(cut off 5%)

Small companies(Turnover

<IDR50bn)

Disc. 50% proportionally

6Global Tax Symposium – Asia 2015

PwC

Exit tax on share sale by non-resident

Unlisted: 5% of sales listed: 0.1%

General tax tariff

Individual tax

30% (top rate)

Value added tax

10%

Withholding taxes to non-

residents

20%

7Global Tax Symposium – Asia 2015

PwC

Tax environment

8Global Tax Symposium – Asia 2015PwC

PwC

Indonesian tax environmentGrowth of total tax revenue target and actual tax revenue received*(in IDR trillion )

*Source: Ministry of Finance’s website http://www.kemenkeu.go.id/kemenkeu/sites/default/files/infografis/Infografis%20Maret%202015/files/assets/common/downloads/page0001.pdf

980.51077.3

1143.31016.2

1148.41246.1

1489.3

0200400600800

1000120014001600

2012 2013 2014 2015Years

ActualTarget

±15% to 17% increases year-on-year30% increase

8Global Tax Symposium – Asia 2015

PwC

Base erosion of profit shifting (BEPS) implications for Indonesian taxpayers

• Why is BEPS important to Indonesia?

G20 member and OECD ‘key partner’

Increasing importance in global trade/services with OECD and G20 members

• The Director General of Taxation (DGT) is currently drafting new transfer pricing regulation considering BEPS recommendations

• Increased focus on substance

DGT seeking to strengthening anti-avoidance rules

Debt to equity rules

• Increased focus on transparency

Exchange of information

More than ever, both sides of the transactions need to be considered

10Global Tax Symposium – Asia 2015

PwC

Typical holding structures

11Global Tax Symposium – Asia 2015PwC

PwC

Establishing a presence in Indonesia

Representative office Subsidiary company

• For long term purposes

• Can perform commercial activities e.g. provide services, trading goods

• More investment requirement

• Lengthy licensing process i.e. can take more than 6 months

• More compliance requirements

• Negative Investment List

• Generally for short term to ‘test the water’

• Limited activities: Market research, promotion, marketing, liaison, coordination, searching for business opportunities

• Easy and less costly to set up

• Less compliance requirements

For certain business e.g. construction services, there may be more than one option available: Subsidiary Company or Construction Representative Office (Commercial Branch)

12Global Tax Symposium – Asia 2015

PwC

Typical holding structure

Investor

Sing Co

PT Indo

Investor

HK Co

PT Indo

Dividend

10%/15%

Interest

10%

Dividend

5%/10%

Interest

10%

No treaty relief on exit Potentially treaty relief on exit, BUT practical issues on application of treaty continue to exist

13Global Tax Symposium – Asia 2015

PwC

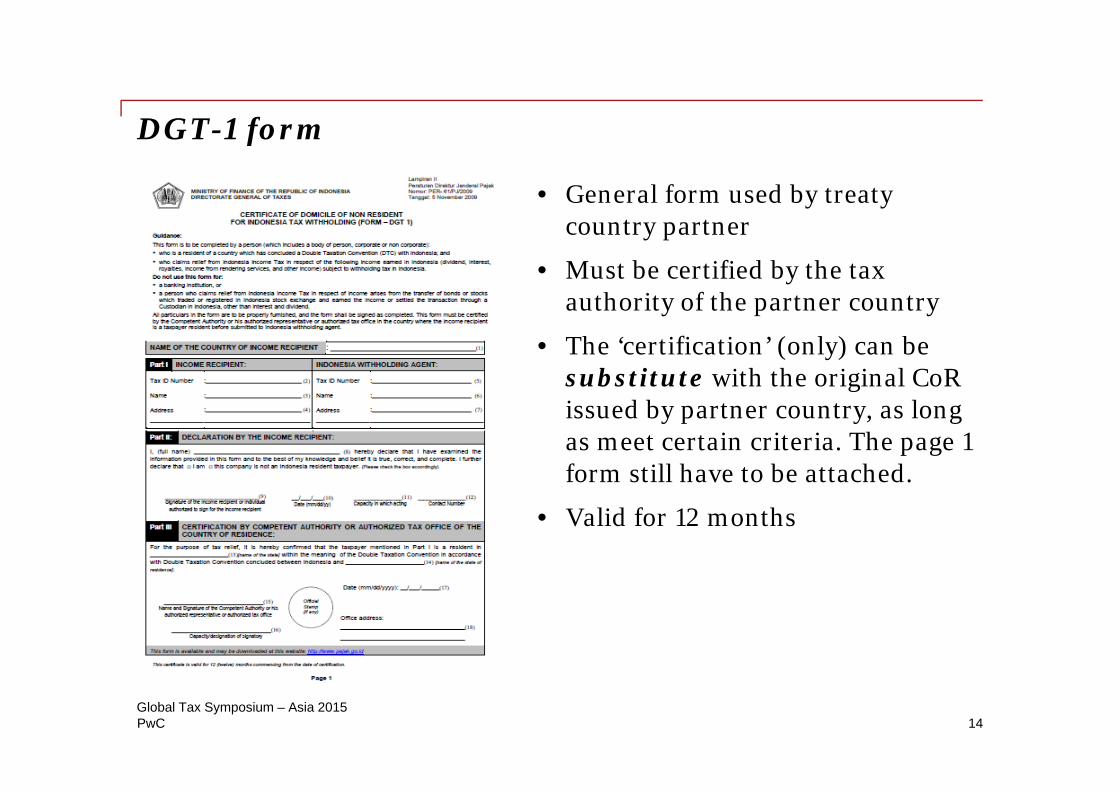

DGT-1 form

• General form used by treaty country partner

• Must be certified by the tax authority of the partner country

• The ‘certification’ (only) can be substitute with the original CoRissued by partner country, as long as meet certain criteria. The page 1 form still have to be attached.

• Valid for 12 months

14Global Tax Symposium – Asia 2015

PwC

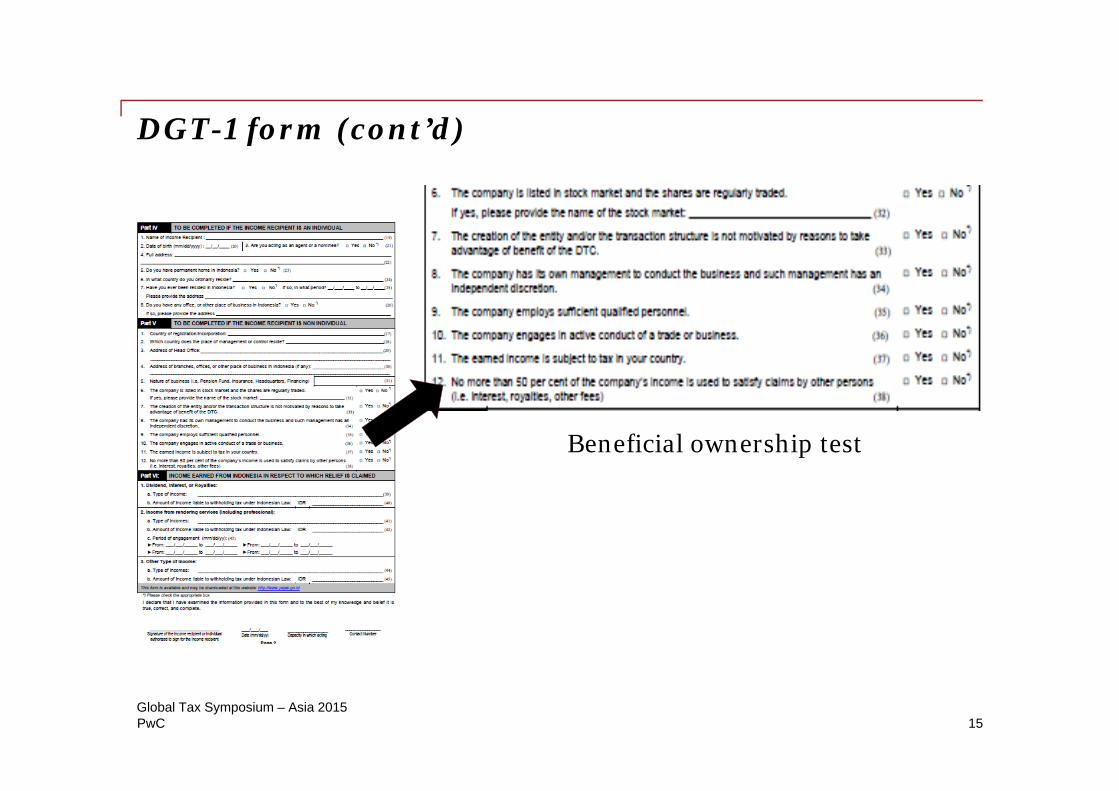

DGT-1 form (cont’d)

Beneficial ownership test

15Global Tax Symposium – Asia 2015

PwC

Debt financing issues

Slide 16Global Tax Symposium – Asia 2015PwC

PwC

Thin capitalisation rules

• Currently no specific regulation

• General transfer pricing provisions may be used in cases of related parties

• Given lack of regulation in the past, BKPM ratio (3:1) was often used in practice

Current status

The Ministry of Finance has finally announced but watch this space as nothing is certain until issued.

4:117

Global Tax Symposium – Asia 2015

PwC

Tax incentives

18Global Tax Symposium – Asia 2015PwC

PwC

Tax incentives – facilities granted

Tax allowance Tax holiday

• For new or additional investment, no investment minimum

• 30% of net tax deduction of the total investment charged for 6 years for 5% annually

• Accelerated depreciation and amortisation

• Dividend paid to offshore is subject to 10% income tax or lower based on DTA; and

• Extended loss carry forward period to 6-10 years

• For new investment – minimum IDR1 trillion

• Corporate Income Tax relief for 5 to 10 years starting from the tax year when commercial production commences; and

• Additional Corporate Income Tax reduction at 50% of the outstanding Income Tax for 2 years after the end of the Corporate Income Tax relief period.

19Global Tax Symposium – Asia 2015

PwC

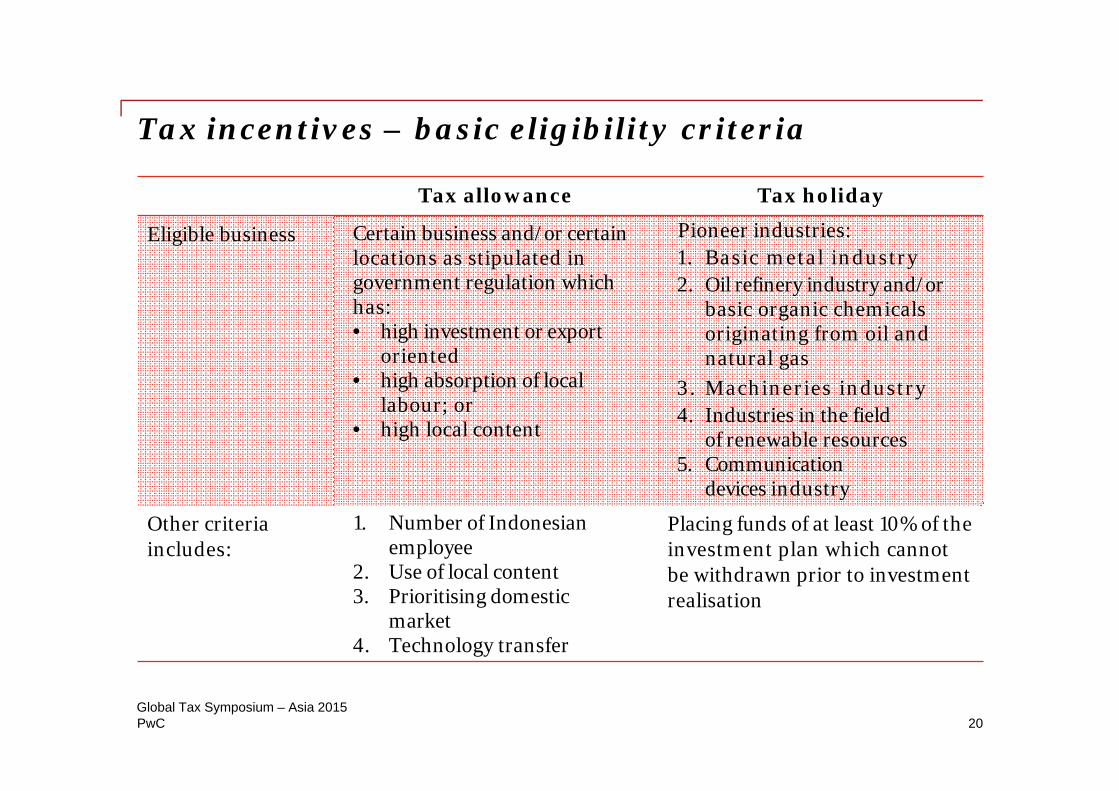

Tax incentives – basic eligibility criteria

Tax allowance Tax holiday

Eligible business Certain business and/or certain locations as stipulated in government regulation which has: • high investment or export

oriented • high absorption of local

labour; or • high local content

Pioneer industries: 1. Basic metal industry 2. Oil refinery industry and/or

basic organic chemicals originating from oil and natural gas

3. Machineries industry4. Industries in the field

of renewable resources5. Communication

devices industry

Other criteria includes:

1. Number of Indonesian employee

2. Use of local content3. Prioritising domestic

market4. Technology transfer

Placing funds of at least 10% of the investment plan which cannot be withdrawn prior to investment realisation

20Global Tax Symposium – Asia 2015

PwC

Sunset Policy – 2nd

round

is part of a series incentives to increase tax compliance as well as boosting national tax revenue

21Global Tax Symposium – Asia 2015PwC

PwC

Sunset Policy – grants an elimination or reduction in administrative sanctions

Sanction potentially waived

Late submission of Annual and Monthly Income Tax Returns for 2014 and prior years

• fine of IDR1m per corporate • fine of IDR500k per VAT return• fine of IDR100k per individual

Late payment of underpaid tax reported in the qualified returns

• interest penalty of 2%/month

Late payment and reporting irregularities for VAT returns

• interest penalty of 2%/month;and/or

• fine of 2% x tax base

But will it really work?

22Global Tax Symposium – Asia 2015

PwC

Regulatory update

23Global Tax Symposium – Asia 2015PwC

PwC

Payment and settlement of all domestic commercial transactions and obligations

Regulatory issues – currency Law

IDR must be used for all transactions conducted within Indonesia, with effect from 1 July 2015.

1. Transactions related to the state budget2. Grants given by or to a foreign state3. International commercial transactions4. Bank deposits denominated in foreign currencies; and5. International finance transactions6. Others?

Coverage

Exemption

24Global Tax Symposium – Asia 2015

PwC

Regulatory issues – one stop service at BKPM

• The policy from President Jokowi on full implementation of One Stop Service in BKPM to boost investment climate

• To minimise contact between applicant and processing officer including to reduce middlemen role in application processes

• To enhance the processing efficiency of BKPM

Background

25Global Tax Symposium – Asia 2015

Philippines

Lawrence BiscochoPartner, PwC Philippines

PwC

Agenda

1. Country overview

2. Tax and regulatory updates

3. Moving forward

27Global Tax Symposium – Asia 2015

PwC

Economic performance

Structure of GDP

• The economy expanded by 6.1% in 2014, fueled by sustained increases in private consumption, higher fixed investment, and recovery in exports.

• For the 4th quarter of 2014, the country’s GDP accelerated to 6.9 percent from 6.3 percent in the same period of last year.

• Strong GDP growth is projected for 2015 and 2016 based on buoyant private consumption, a solid outlook for investment and exports, and recovery in government expenditure. GDP is projected to increase by 6.4% in 2015 and 6.3% in 2016.

28Global Tax Symposium – Asia 2015

PwC

Economic overview2015

Foreign Direct Investment

• From 2011 to 2013, FDI inflows steadily moved up in the Philippines, from $2 billion (in 2011) to $3.86 billion (in 2013).

• US and Japan are the major source of FDI.

29Global Tax Symposium – Asia 2015

PwC

Tax and regulatory updates

Global Tax Symposium – Asia 201530

PwC

Tax developments/BEPS impact

31Global Tax Symposium – Asia 2015

• OECD announced that the Philippines is one of the 10 developing countries that would participate in the meetings of the Committee on Fiscal Affairs (CFA)—the key decision-making body of the BEPS project—as well as its technical working groups beginning January 2015.

• Philippine Commissioner of Internal Revenue Kim Henares was appointed by United Nations Secretary General Ban Ki-moon to the UN Committee of Experts on International Cooperation in Tax Matters.

PwC

Tax developments/BEPS impact

32Global Tax Symposium – Asia 2015

• US$38B - CY 2015 Target Revenue of PH Tax Authority (Bureau of Internal Revenue or BIR)

• Transfer Pricing Programme – Part of 27-pt priority programme of BIR

• BIR released TP guidelines in 2013

• Tax audit now includes TP issues

PwC

Exchange of Information

33Global Tax Symposium – Asia 2015

• Republic Act No. 10021 entitled An Act to Allow the Exchange of Information by the Bureau of Internal Revenue on Tax Matters Pursuant to Internationally-Agreed Tax Standards

• Implementing regulations - Revenue Regulations 10-10 and 03-14

PwC

Treaty relief

34Global Tax Symposium – Asia 2015

• In 2010, BIR required prior treaty relief application to avail of incentives under Philippine double tax treaty

• 24 January 2014 – Supreme Court ruled with finality that failure to apply for prior relief does not deprive taxpayer of treaty benefit

PwC

Renewable energy

35Global Tax Symposium – Asia 2015

Incentives

• Income tax holiday incentive for 7 years (maximum of 21 years)

• 10% tax

PwC

ROHQ

3627 May 2015Global Tax Symposium – Asia 2015

• Increasing number of foreign and local companies setting up regional operating headquarters due to incentives

• Requirements

• Minimum of 2 foreign affiliates

• ROHQ services consist of qualifying support services

• Services must rendered to affiliates

• Incentives

• 10% tax on net income

• 15% tax on qualified on foreigners and qualified local employees

PwC

Incentive-giving agencies

3727 May 2015Global Tax Symposium – Asia 2015

PEZA and other special economic zones

• Income tax holiday incentive (maximum of 8 years)

• 5% gross income tax

PwC

Challenges

3827 May 2015Global Tax Symposium – Asia 2015

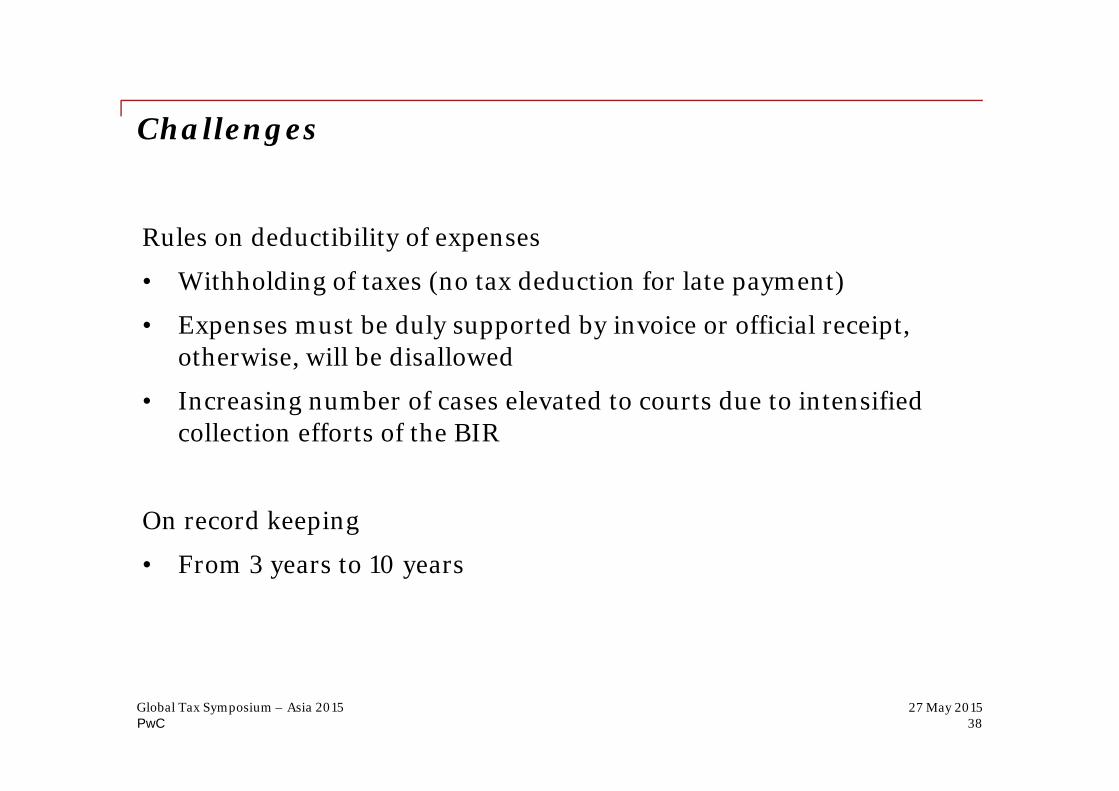

Rules on deductibility of expenses

• Withholding of taxes (no tax deduction for late payment)

• Expenses must be duly supported by invoice or official receipt, otherwise, will be disallowed

• Increasing number of cases elevated to courts due to intensified collection efforts of the BIR

On record keeping

• From 3 years to 10 years

PwC

Moving forward

Global Tax Symposium – Asia 201539

PwC

Base Erosion Profit Shifting (BEPS)

• Local tax jurisdictions may amend domestic legislation in response to the BEPS initiative.

• Aggressive tax audit

4027 May 2015Global Tax Symposium – Asia 2015

PwC

Amendment of incentive laws

• Proposal to impose sunset provision on incentives (income tax holiday and 5% tax)

• Limit industries qualified for incentives

• Centralised administrative body

4127 May 2015Global Tax Symposium – Asia 2015

PwC

Intensified tax collection

• Run after tax evaders programme

• Moving towards electronic filing for all tax returns

4227 May 2015Global Tax Symposium – Asia 2015

Thailand

Somboon WeerawutiwongPartner, PwC Thailand

PwC

Agenda

1. Country overview

2. Tax update

3. Looking forward

Global Tax Symposium – Asia 201544

PwC

Highlights of 2014

• Political instability and street protests resulted in military assuming power in May 2014

• Martial law since repealed but military retains absolute power

• New constitution and general election expected in 2016

Global Tax Symposium – Asia 201545

PwC

Economic overview2015

Structure of GDP

Global Tax Symposium – Asia 201546

• GDP growth of 0.7% for 2014

• Forecast growth of 3.2-3.6% for 2015

• Inflation of 0.6% for 2014 and 0.2% forecast for 2015

• Economy remains heavily reliant on manufacturing sectorManufacturing

PwC

Economic overview2015

Foreign direct investment

FDI fell 11.8% in 2014 mainly as a result of political uncertainties but Jan and Feb 2015 recorded an increase of 127% over the same period of the prior year.

Japan remains the major source of FDI but China and ASEAN investment is continuing to grow.

47Global Tax Symposium – Asia 2015

PwC

Tax update

Global Tax Symposium – Asia 201548

PwC

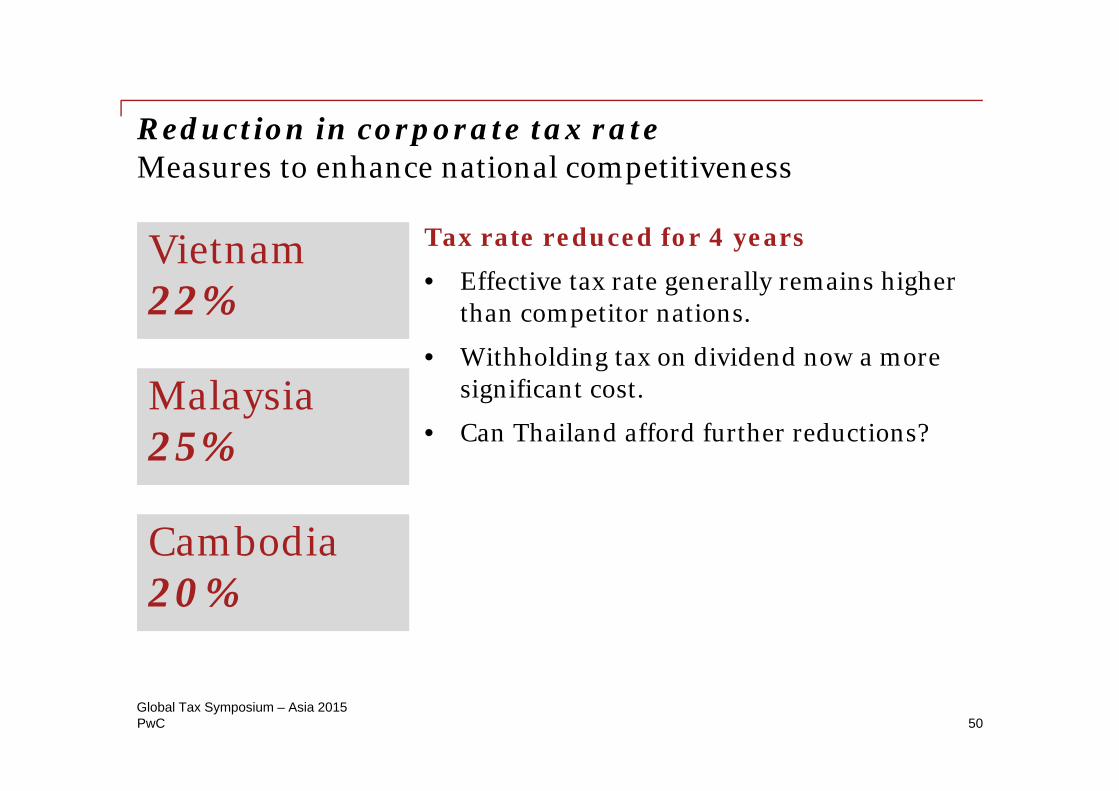

Reduction in corporate tax rateMeasures to enhance national competitiveness

Tax rate reduced for 4 years

• Reduction applies for accounting periods beginning on or after 1 January 2012.

• This temporary reduction is expected to be made permanent.

• Withholding tax of 10% applies to distribution of dividends.

• Effective tax rates are 30.7% for 2012 and 28% for 2013 onwards (down from 37%).

• Reduction also granted to SME.

Global Tax Symposium – Asia 201549

201223%201320%201420%201520%

PwC

Reduction in corporate tax rateMeasures to enhance national competitiveness

Tax rate reduced for 4 years

• Effective tax rate generally remains higher than competitor nations.

• Withholding tax on dividend now a more significant cost.

• Can Thailand afford further reductions?

Global Tax Symposium – Asia 201550

Vietnam22%

Malaysia25%

Cambodia20%

PwC

Trends in Thai tax policy – corporate income tax

30.0%

23.5%25.0%

35.0%

25.0%

30.0%

17.0%

25.0%

20.0% 20.0% 20.0%

25.0%24.0%

25.0% 25.0%

30.0%

17.0%

22.0%

15%

20%

25%

30%

35%

Thailand Brunei Cambodia Indonesia Laos Malaysia Myanmar Philippines Singapore Vietnam

2010

2011

2012

2013

2014

Global Tax Symposium – Asia 201551

2010-2014 ASEAN corporate income tax (CIT) ratesIn 2013-2014, Thailand has the second lowest corporate tax rate in ASEAN while Singapore is the first.

PwC

Service fee 100

Profit 10

Tax 20% 2

WHT 3

Refund 1

Trends in Thai tax policy – corporate income taxWithholding tax

Global Tax Symposium – Asia 201552

CIT 30% WHT 1% for transportation, insurance

2% for advertisement

3% for service fees

5% for rental

CIT 20% ?WHT

Example Service fee 100

Profit 10

Tax 30% 3

WHT 3

No refund 0

PwC

Trends in Thai tax policy – value added taxValue added tax rates in ASEAN (2015)

0

10 10 10

6

0

12

7 7

10

0

2

4

6

8

10

12

14

Percent

Country

Global Tax Symposium – Asia 201553

Until 30 Sep2015

PwC

Tax incentives for international headquarters (IHQ)

Objective

To grant tax incentives to attract foreign firms to establish IHQ in Thailand

IHQ

A company incorporated under the law of Thailand providing IHQ functions to its associated enterprises or branches situated in Thailand or abroad.

Effective

2 May 2015

Global Tax Symposium – Asia 201554

PwC

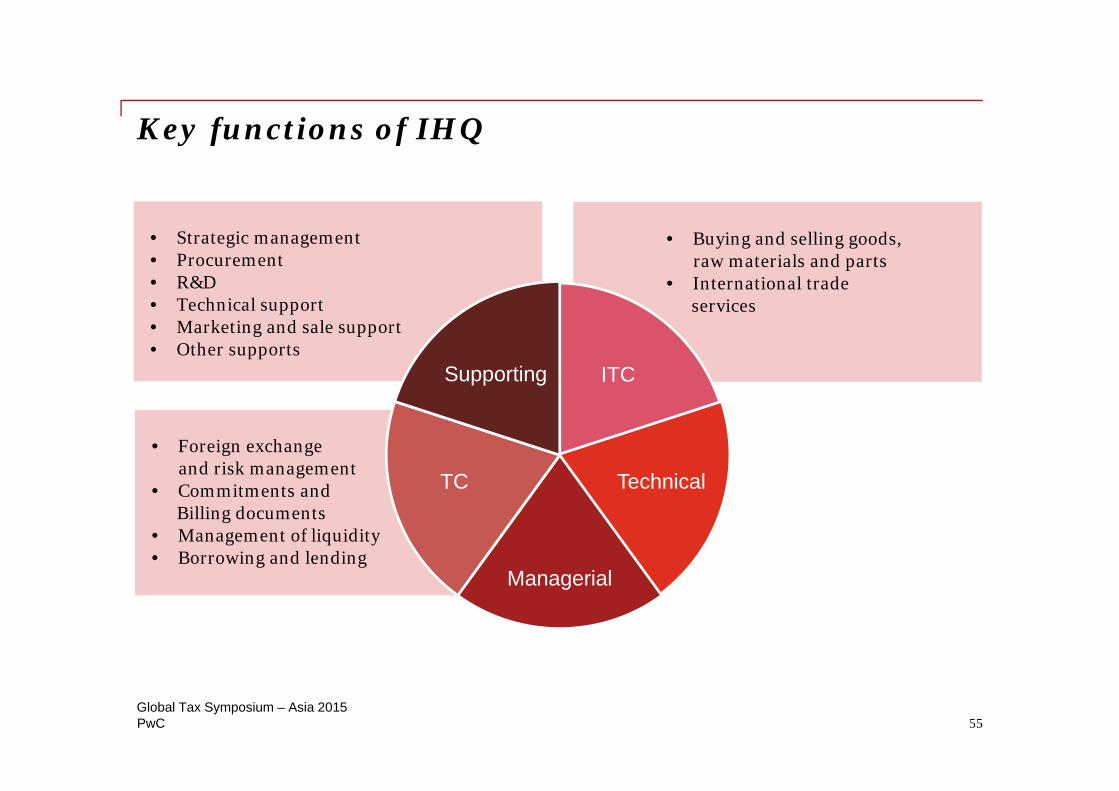

Key functions of IHQ

• Buying and selling goods, raw materials and parts

• International trade services

• Foreign exchangeand risk management

• Commitments andBilling documents

• Management of liquidity• Borrowing and lending

ITC

Technical

Managerial

TC

Supporting

• Strategic management • Procurement • R&D• Technical support• Marketing and sale support• Other supports

55Global Tax Symposium – Asia 2015

PwC

Criteria for IHQ

Global Tax Symposium – Asia 201556

> THB10m for paid-up capital

Onshore < Offshore incomeCap for 10% CIT reduction

Revocation of benefits – year-to-year

> THB15m on business spending

PwC

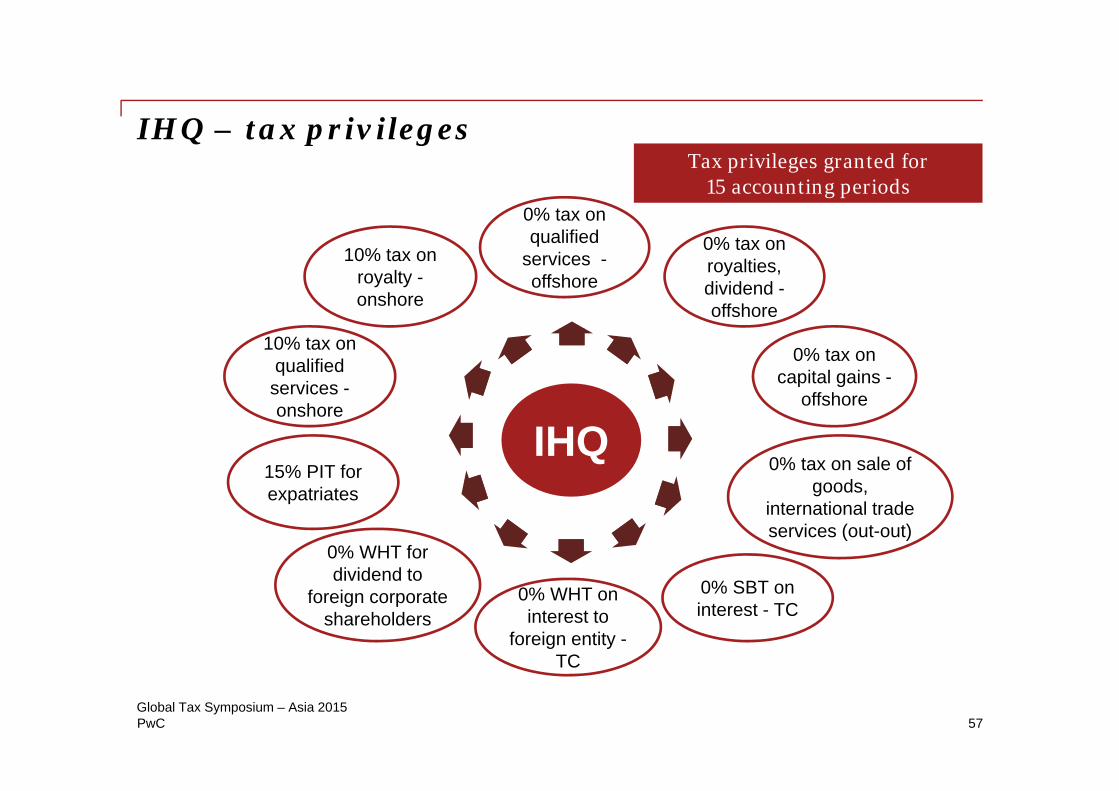

IHQ – tax privileges

Global Tax Symposium – Asia 201557

10% tax on qualified services -onshore

0% tax on qualified

services -offshore

0% tax on royalties, dividend -offshore

0% tax on capital gains -

offshore

10% tax on royalty -onshore

0% tax on sale of goods,

international trade services (out-out)

IHQ15% PIT for expatriates

0% WHT for dividend to

foreign corporate shareholders

0% SBT on interest - TC

0% WHT on interest to

foreign entity -TC

Tax privileges granted for 15 accounting periods

PwC

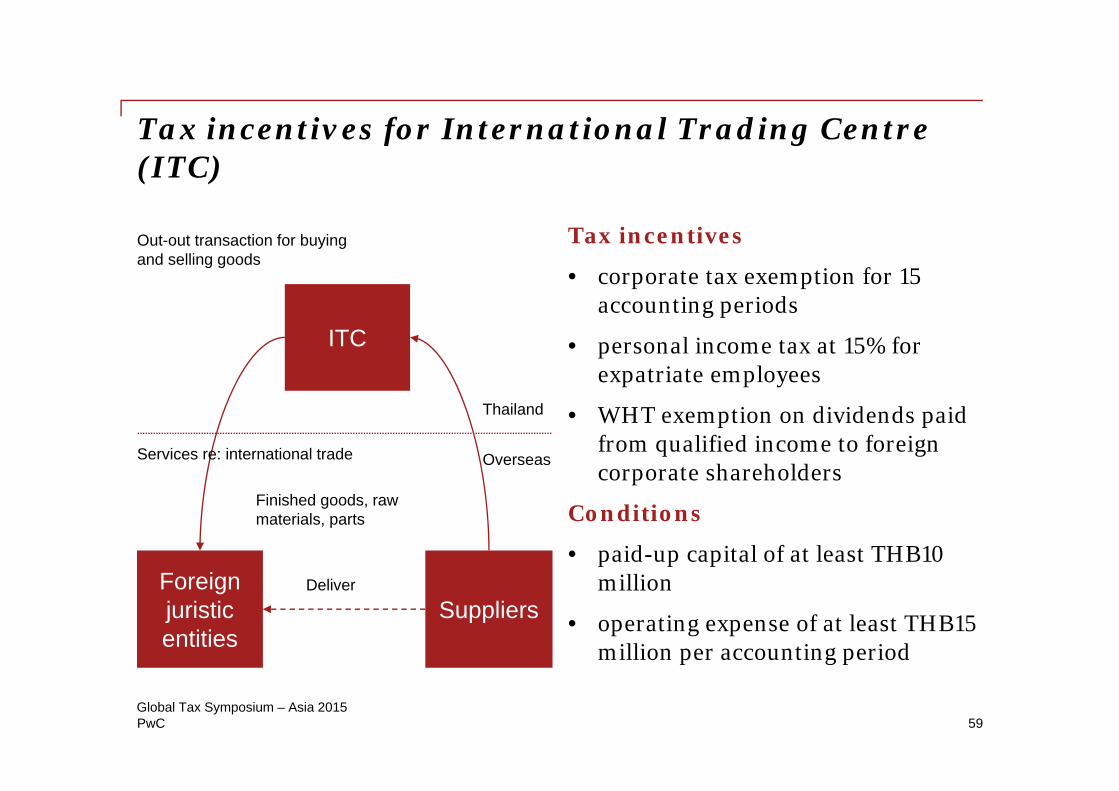

Tax incentives for International Trading Centre (ITC)

Activities of ITC

• procure and sell finished goods, raw materials and parts to foreign juristic entities (out-out transaction)

• provide services relating to international trade

Services re: international trade

• procuring, maintaining, packaging, transporting, providing insurance, advising and training relating to goods

Global Tax Symposium – Asia 201558

ITC

Foreign juristic entities

Suppliers

Finished goods, raw materials, parts

Services re: international trade

Deliver

Out-out transaction for buying and selling goods

Thailand

Overseas

PwC

Tax incentives for International Trading Centre (ITC)

Tax incentives

• corporate tax exemption for 15 accounting periods

• personal income tax at 15% for expatriate employees

• WHT exemption on dividends paid from qualified income to foreign corporate shareholders

Conditions

• paid-up capital of at least THB10 million

• operating expense of at least THB15 million per accounting period

Global Tax Symposium – Asia 201559

ITC

Foreign juristic entities

Suppliers

Finished goods, raw materials, parts

Services re: international trade

Deliver

Out-out transaction for buying and selling goods

Thailand

Overseas

PwC

Looking forward

Global Tax Symposium – Asia 201560

PwC

Base erosion profit shifting (BEPS)

Global Tax Symposium – Asia 201561

• Local tax jurisdictions may amend domestic legislation in response to the BEPS initiative.

• The Tax Authority may get tougher on tax-driven planning, even without formal General Anti Avoidance Rules (GAAR). Possible areas:

1. Denial of treaty benefits to foreign treaty shoppers (e.g. equipment lease payments via Singapore sub-lessor).

2. Changing stance on ‘net book value’ as proxy for ‘market value’3. Changing stance on ‘beneficial ownership’ versus ‘legal ownership’.4. Aggressively use transfer pricing as a tax-collection tool, where

Thai legislation does not support taxation of foreign companies.

PwC

BEPS – impacts to Thailand

• Transparency and tax

• Exchange of information

• Risk assessment for international transaction and tax audit

• Transfer pricing

• Thin capitalisation

• Controlled foreign corporation

• Reconsideration of treaty provision

Global Tax Symposium – Asia 201562

PwC

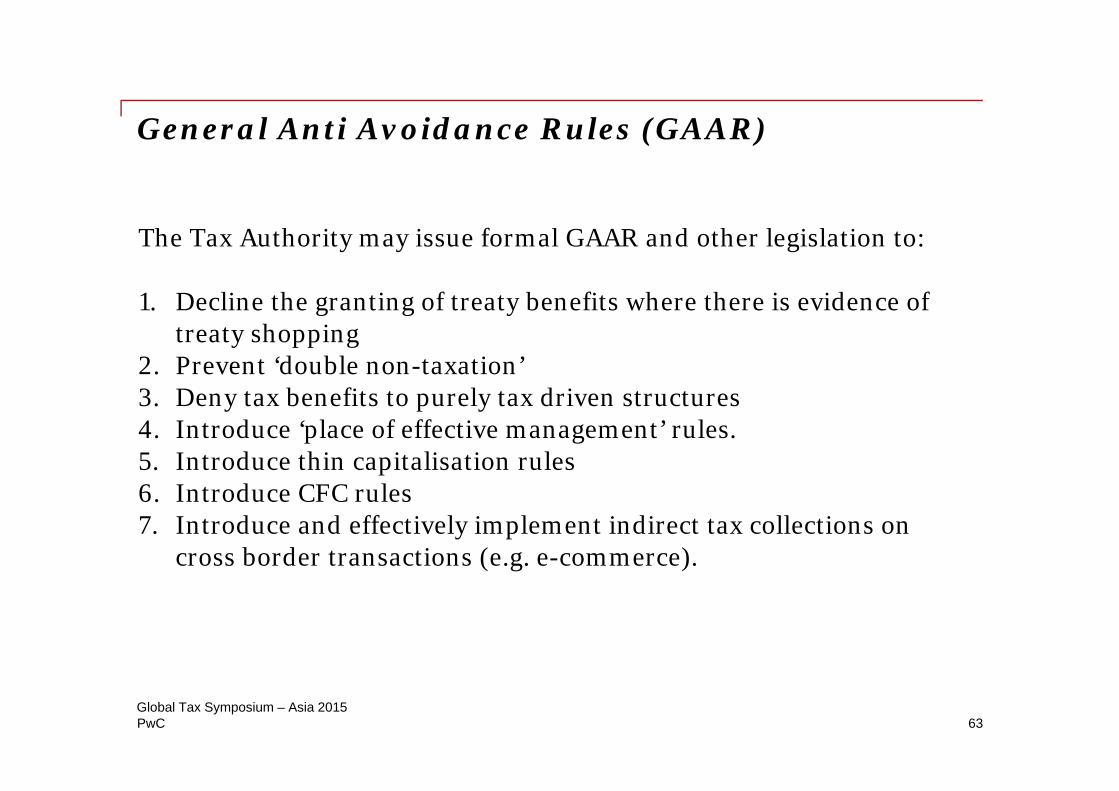

General Anti Avoidance Rules (GAAR)

Global Tax Symposium – Asia 201563

The Tax Authority may issue formal GAAR and other legislation to:

1. Decline the granting of treaty benefits where there is evidence of treaty shopping

2. Prevent ‘double non-taxation’3. Deny tax benefits to purely tax driven structures4. Introduce ‘place of effective management’ rules.5. Introduce thin capitalisation rules6. Introduce CFC rules7. Introduce and effectively implement indirect tax collections on

cross border transactions (e.g. e-commerce).

PwC

Looking forward Summary

• Policy directed at reducing taxes for businesses

• Introducing new anti-avoidance legislations (e.g. The Cabinet approved the draft Act governing transfer pricing on 7 May 2015)

Global Tax Symposium – Asia 201564

Global Tax Symposium – Asia 2015PwC

Contact us

Brian Arnold

Partner, PwC [email protected]

Lawrence Biscocho

Partner, PwC [email protected]

Somboon Weerawutiwong

Partner, PwC [email protected]

6565

Thank you.

The information contained in this presentation is of a general nature only. It is not meant to be comprehensive and does not constitute the rendering of legal, tax or other professional advice or service by PricewaterhouseCoopers Ltd. ("PwC"). PwC has no obligation to update the information as law and practices change. The application and impact of laws can vary widely based on the specific facts involved. Before taking any action, please ensure that you obtain advice specific to your circumstances from your usual PwC client service team or your other advisers.

The materials contained in this presentation were assembled in 15 May 2015 and were based on information available at that time.

© 2015 PricewaterhouseCoopers. All rights reserved. ‘PricewaterhouseCoopers’ and/or ‘PwC’ refers to the individual members of the PricewaterhouseCoopers organisation in Thailand, each of which is a separate and independent legal entity. Please see www.pwc.com/structure for further details.