Corporate ValuationOperating Leases Advanced Valuation Issues: Operating Leases Professor David...

20

Corporate Valuation Operating Leases Advanced Valuation Issues: Operating Leases Professor David Wessels The Wharton School of the University of Pennsylvania © 2005.

-

Upload

douglas-barker -

Category

Documents

-

view

217 -

download

1

Transcript of Corporate ValuationOperating Leases Advanced Valuation Issues: Operating Leases Professor David...

Corporate Valuation Operating Leases

Advanced Valuation Issues: Operating Leases

Professor David Wessels

The Wharton School of the University of Pennsylvania © 2005.

Professor David WesselsThe Wharton School of the University of Pennsylvania 2

Corporate Valuation Operating Leases

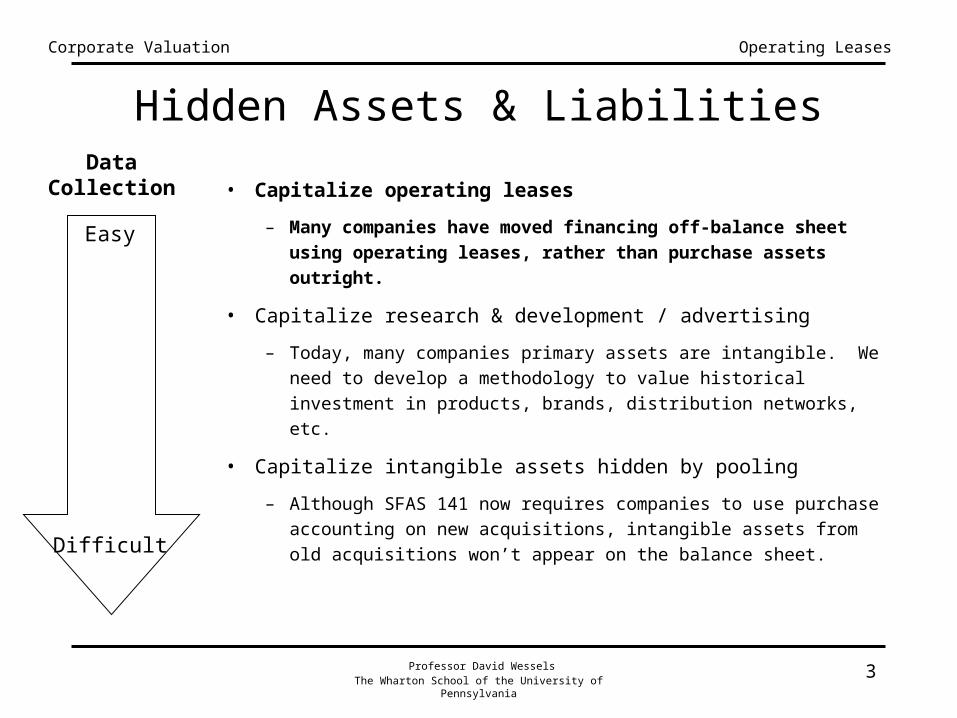

Hidden Assets & Liabilities

• Companies have three

major hidden assets:

– Hide assets by using off-

balance sheet financing

such as operating leases.

– Expense, rather than

capitalize, intangible

investment (R&D).

– Hide ownership dilution

through historical

pooling.

Operations Financing

Working Cash Notes Payable

+ Accounts Receivable + Dividends Payable

+ Inventories Current Liabilities

- Accounts Payable

- Accrued Expenses + Long Term Debt

Operating Working Capital + Off-Balance Sheet Debt (leases)

- Excess Cash

+ Net Property, Plant

+ Hidden Physical Assets (Leases) + Deferred Taxes

+ Organic Intangibles (R&D) + Owners Equity

+ Acquired Intangibles (pooling) + Understated Equity (R&D)

+ Long Term Assets + Missing Equity (pooling)

- Long Term Liabilities Total Invested Capital

Total Invested Capital

Economic Balance Sheet

Professor David WesselsThe Wharton School of the University of Pennsylvania 3

Corporate Valuation Operating Leases

Hidden Assets & Liabilities

• Capitalize operating leases

– Many companies have moved financing off-balance sheet using

operating leases, rather than purchase assets outright.

• Capitalize research & development / advertising

– Today, many companies primary assets are intangible. We need to

develop a methodology to value historical investment in products,

brands, distribution networks, etc.

• Capitalize intangible assets hidden by pooling

– Although SFAS 141 now requires companies to use purchase

accounting on new acquisitions, intangible assets from old

acquisitions won’t appear on the balance sheet.

DataCollection

Easy

Difficult

Professor David WesselsThe Wharton School of the University of Pennsylvania 4

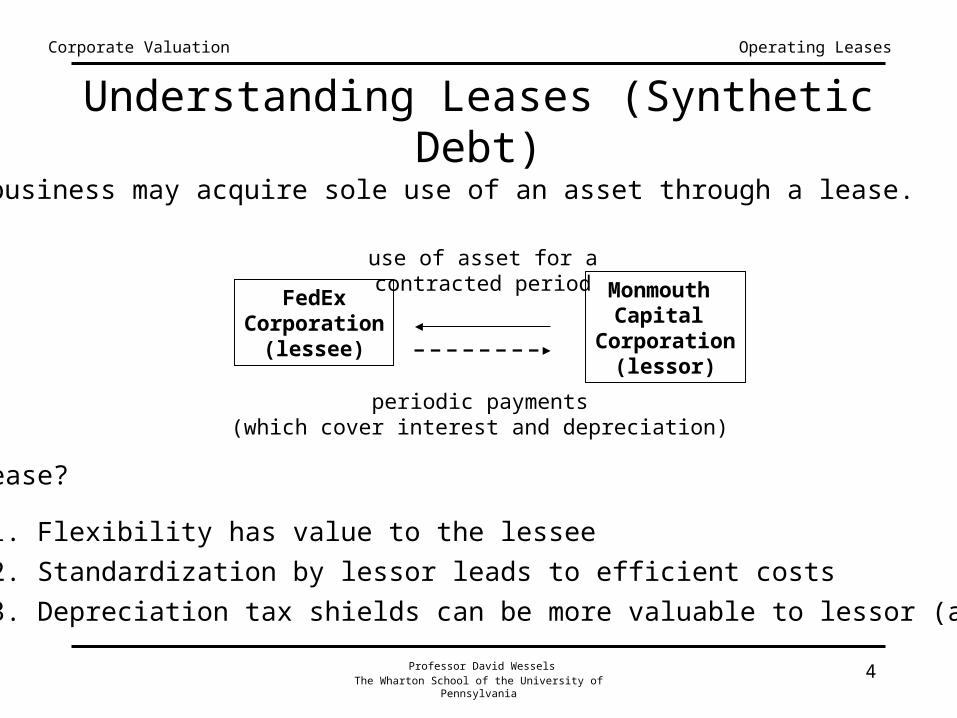

Corporate Valuation Operating Leases

Understanding Leases (Synthetic Debt)

Monmouth Capital

Corporation(lessor)

FedExCorporation

(lessee)

use of asset for acontracted period

periodic payments(which cover interest and depreciation)

• Why Lease?

1. Flexibility has value to the lessee

2. Standardization by lessor leads to efficient costs

3. Depreciation tax shields can be more valuable to lessor (avoid AMT).

• A business may acquire sole use of an asset through a lease.

Professor David WesselsThe Wharton School of the University of Pennsylvania 5

Corporate Valuation Operating Leases

The Growth of Operating Leases• Rental expenses for have grown steadily over the last fifteen years. As

a percentage of sales, the number has remained relatively constant

(1.5% of sales). Since interest rates have declined, the present value

of leases have outpaced revenue growth.

Total Rental ExpensesNon-Financial S&P 500 Companies 1985-2004

18.8 20.5 21.824.3

27.030.5 32.5 34.7 35.3 36.5

39.2 40.145.1

50.1

56.361.5

68.6 70.473.1 75.0

0

10

20

30

40

50

60

70

80

90

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003

$ B

illi

on

s

Estimated Value of Operating Leases Non-Financial S&P 500 Companies

1985-2004

0

100

200

300

400

500

600

700

800

900

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003

$ B

illio

ns

If operating leases had

grown with total debt

If operating leases had grown with revenues

Professor David WesselsThe Wharton School of the University of Pennsylvania 6

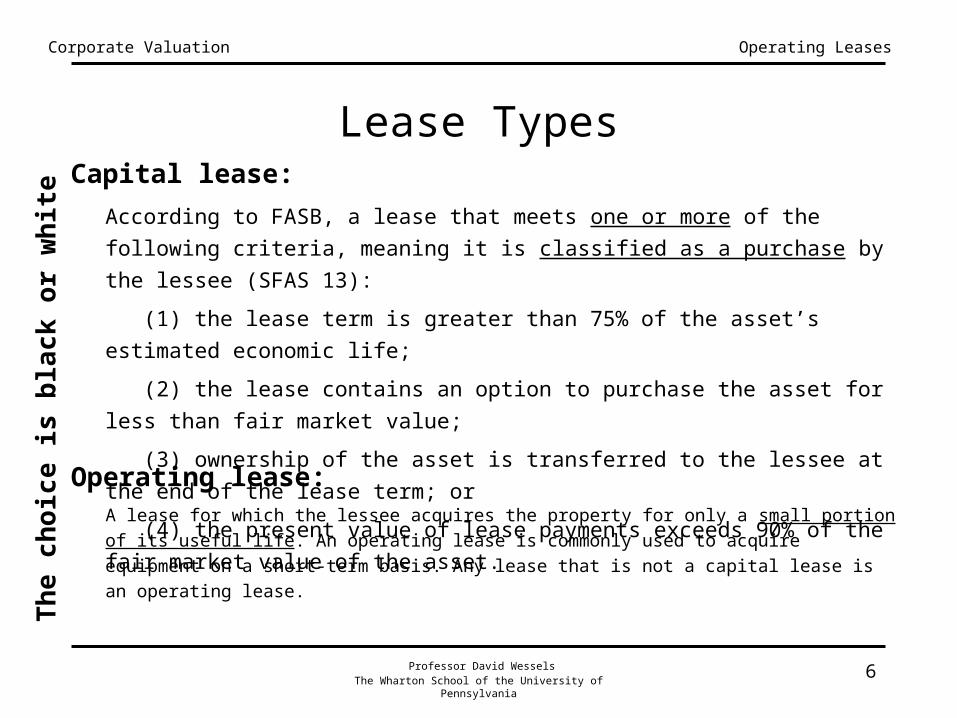

Corporate Valuation Operating Leases

Lease Types

According to FASB, a lease that meets one or more of the following criteria, meaning it is

classified as a purchase by the lessee (SFAS 13):

(1) the lease term is greater than 75% of the asset’s estimated economic life;

(2) the lease contains an option to purchase the asset for less than fair market value;

(3) ownership of the asset is transferred to the lessee at the end of the lease term; or

(4) the present value of lease payments exceeds 90% of the fair market value of the asset.

Capital lease:

A lease for which the lessee acquires the property for only a small portion of its useful life.

An operating lease is commonly used to acquire equipment on a short-term basis. Any lease

that is not a capital lease is an operating lease.

Operating lease:

Th

e ch

oice

is b

lack

or

wh

ite

Professor David WesselsThe Wharton School of the University of Pennsylvania 7

Corporate Valuation Operating Leases

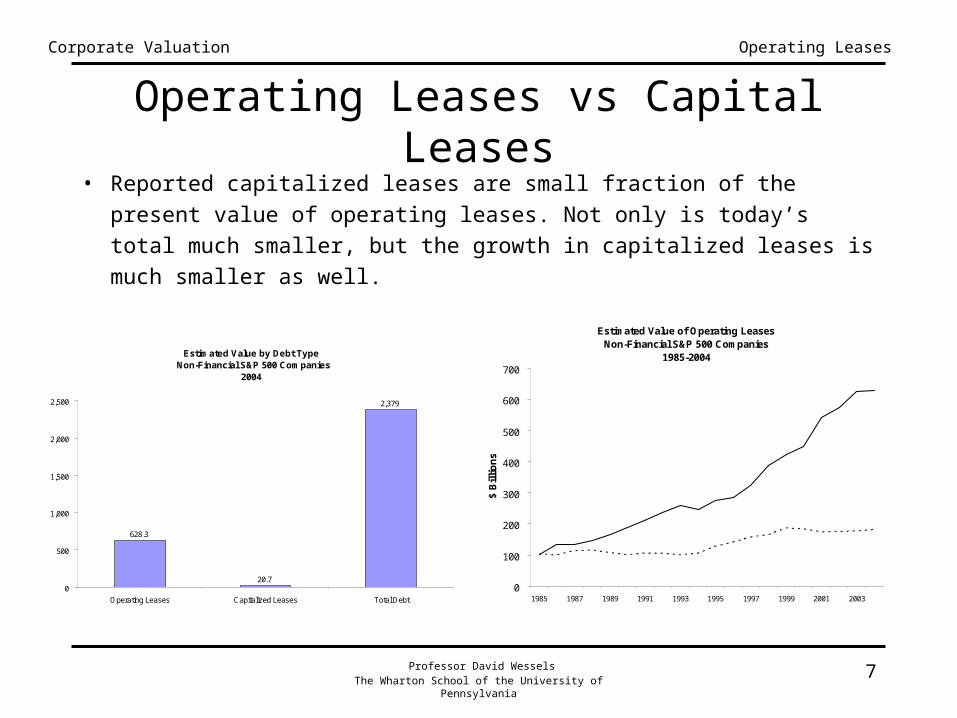

Operating Leases vs Capital Leases

• Reported capitalized leases are small fraction of the present value of

operating leases. Not only is today’s total much smaller, but the growth

in capitalized leases is much smaller as well.

Estimated Value by Debt Type Non-Financial S&P 500 Companies

2004

628.3

20.7

2,379

0

500

1,000

1,500

2,000

2,500

Operating Leases Capitalized Leases Total Debt

Estimated Value of Operating Leases Non-Financial S&P 500 Companies

1985-2004

0

100

200

300

400

500

600

700

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003

$ B

illi

on

sIf operating leases

had grown with capitalized leases

Professor David WesselsThe Wharton School of the University of Pennsylvania 8

Corporate Valuation Operating Leases

Explicit Capital: Capitalized Leases

• The good news: Capitalized leases are already included on the income

statement and balance sheet, even though not explicitly. Details are

often hidden within the footnotes (which is OK).

Assets Liabilities & Shareholder Equity

Aggregated within PP&E: Aggregated within Long-Term

Aircraft 221 Unsecured debt 1,529Package handling and ground support equipment and vehicles 207 Capital lease obligations 422

Other, principally facilities 137Other debt, interest rates of 6.80% to 9.98%, due through 2017 66

Gross Capitalized Leases 565 Total Debt 2,017 Less accumulated amortization -268 Less current portion 308Net Capitalized Leases 297 Long-Term Debt 1,709

Source: Fedex 10-K Note 7 Source: Fedex 10-K Note 6

FedEx Corporation

Revenues 22,487

Operating ExpensesSalaries and employee benefits 9,778Purchased transportation 2,155Rentals and landing fees 1,803Depreciation and amortization 1,351Fuel 1,349Maintenance and repairs 1,398Other 3,182Operating Income 1,471

Interest, net -118Other, net -15Income Before Income Taxes 1,338

Income StatementFedEx Corporation

Professor David WesselsThe Wharton School of the University of Pennsylvania 9

Corporate Valuation Operating Leases

Hidden Capital: Operating Leases

• The bad news: Operating leases

combine depreciation and interest

payments into a single item called

rental payments.

• More bad news: the present value

of operating leases do NOT

appear on the balance sheet.

• We must find a way of

recapitalizing the off-balance

sheet item back onto the balance

sheet.

Revenues 22,487

Operating ExpensesSalaries and employee benefits 9,778Purchased transportation 2,155Rentals and landing fees 1,803Depreciation and amortization 1,351Fuel 1,349Maintenance and repairs 1,398Other 3,182Operating Income 1,471

Interest, net -118Other, net -15Income Before Income Taxes 1,338

Income StatementFedEx Corporation

Professor David WesselsThe Wharton School of the University of Pennsylvania 10

Corporate Valuation Operating Leases

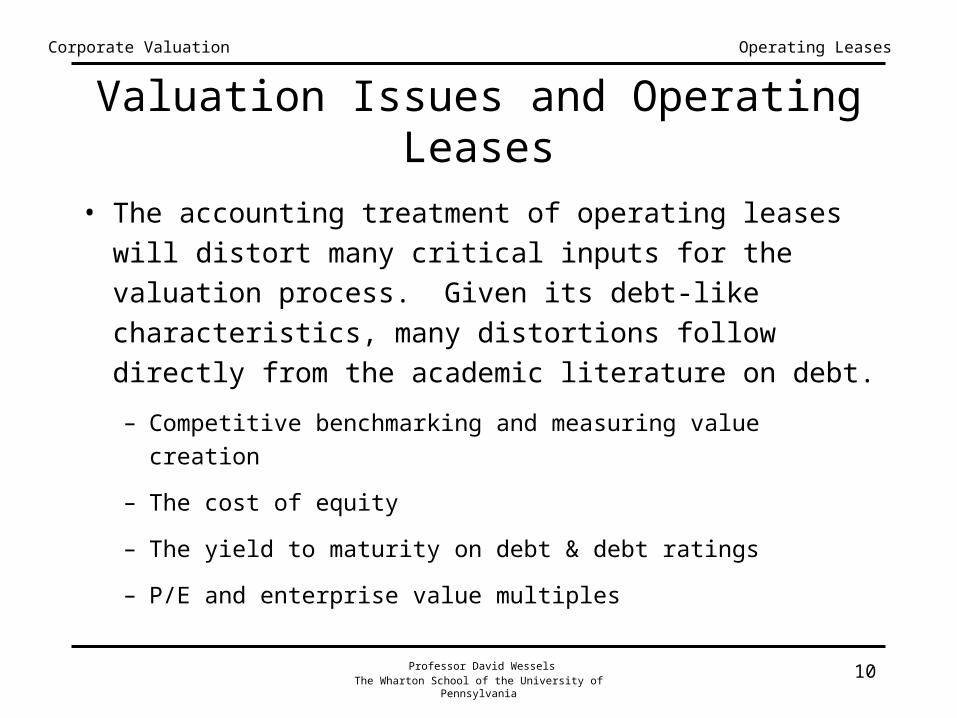

Valuation Issues and Operating Leases

• The accounting treatment of operating leases will distort

many critical inputs for the valuation process. Given its

debt-like characteristics, many distortions follow directly

from the academic literature on debt.

– Competitive benchmarking and measuring value creation

– The cost of equity

– The yield to maturity on debt & debt ratings

– P/E and enterprise value multiples

Professor David WesselsThe Wharton School of the University of Pennsylvania 11

Corporate Valuation Operating Leases

Note 8. Long-Term Debt and Commitments

Future Capital Operating Future Capital OperatingYear Leases Leases Year Leases Leases 2004 44 1,368 2004 68 3182005 125 1,285 2005 68 2512006 102 1,192 2006 93 1842007 11 1,155 2007 68 1362008 11 1,045 2008 113 104

Thereafter 238 8,342 Thereafter 241 555 531 14,387 651 1,548

United Parcel ServiceNote 7: Lease Commitments

FedEx Corporation

• From the notes, we can collect information on operating leases:

Operating Leases: FedEx versus UPS

• FedEx uses operating leases heavily. How will this affect competitive

benchmarking and value creation?

Professor David WesselsThe Wharton School of the University of Pennsylvania 12

Corporate Valuation Operating Leases

• Using the accepted methodology of discounting operating lease

payments at the cost of debt (6%) to ascertain the value of off-balance

sheet assets, FedEx doesn’t look as asset efficient any more!

Distortion of Capital Turnover

United Parcel Service

% of % of Line Item $ Millions Revenues $ Millions RevenuesTotal Revenues 22,487 100.0% 31,272 100.0%

Book PP&E 8,700 38.7% 13,612 43.5%Estimated Leases 9,969 44.3% 1,213 3.9%Adjusted PP&E 18,669 83.0% 14,825 47.4%

FedEx Corp

Professor David WesselsThe Wharton School of the University of Pennsylvania 13

Corporate Valuation Operating Leases

Distortion of ROIC

• ROIC measures financial performance without regard to a company’s

capital structure. If one fails to adjust ROIC for operating leases, ROIC

will be systematically distorted by lease choice.

PV(Lease)-Capital Invested

PV(Lease))k(ROIC ROICROIC dunadj

After-tax lease interest rate

ROIC with no operating

leases

Reported capital

Professor David WesselsThe Wharton School of the University of Pennsylvania 14

Corporate Valuation Operating Leases

The Cost of Equity

• Ely (1995) tests whether investors view operating leases as leverage. To

do this, Ely test the following theoretical relation:

ue σE

DT)(11σ

• using the following regression:

EBI/Assets3EBI/Assets2EBI/Assets1e σE

PVOLbσ

E

Dbσbασ

• and finds:

EBI/AssetsEBI/AssetsEBI/Assetse σ353.σ084.σ328.083.σE

PVOL

E

D

(40.26) (5.70) (5.72) (2.38)

Professor David WesselsThe Wharton School of the University of Pennsylvania 15

Corporate Valuation Operating Leases

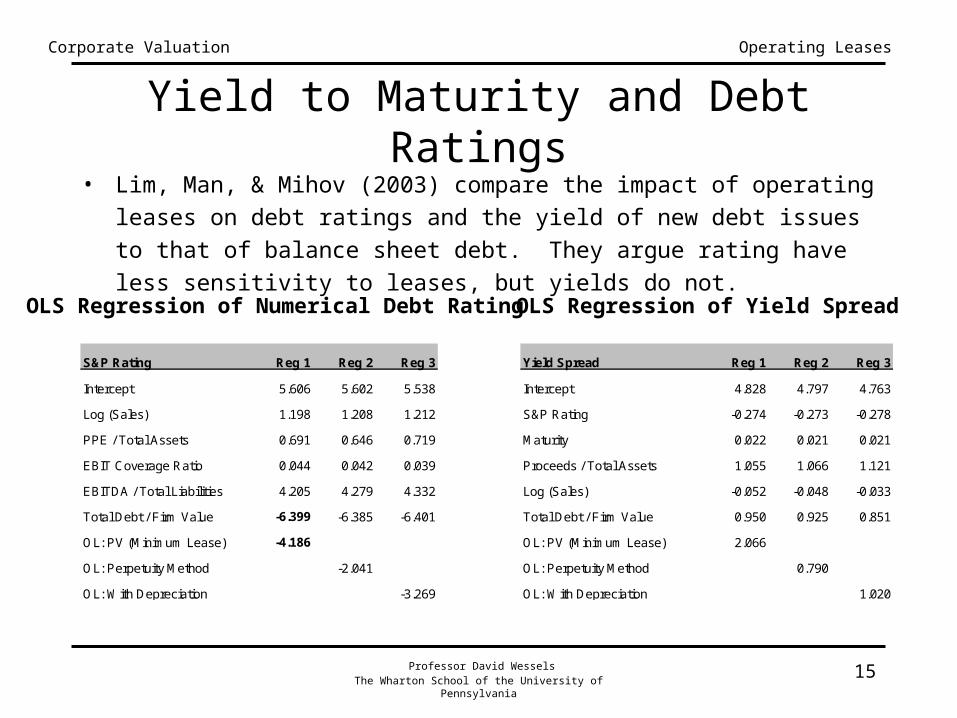

Yield to Maturity and Debt Ratings• Lim, Man, & Mihov (2003) compare the impact of operating leases on debt

ratings and the yield of new debt issues to that of balance sheet debt. They

argue rating have less sensitivity to leases, but yields do not.

OLS Regression of Numerical Debt Rating OLS Regression of Yield Spread

S&P Rating Reg 1 Reg 2 Reg 3 Yield Spread Reg 1 Reg 2 Reg 3

Intercept 5.606 5.602 5.538 Intercept 4.828 4.797 4.763

Log (Sales) 1.198 1.208 1.212 S&P Rating -0.274 -0.273 -0.278

PPE / Total Assets 0.691 0.646 0.719 Maturity 0.022 0.021 0.021

EBIT Coverage Ratio 0.044 0.042 0.039 Proceeds / Total Assets 1.055 1.066 1.121

EBITDA / Total Liabilities 4.205 4.279 4.332 Log (Sales) -0.052 -0.048 -0.033

Total Debt / Firm Value -6.399 -6.385 -6.401 Total Debt / Firm Value 0.950 0.925 0.851

OL: PV (Minimum Lease) -4.186 OL: PV (Minimum Lease) 2.066

OL: Perpetuity Method -2.041 OL: Perpetuity Method 0.790

OL: With Depreciation -3.269 OL: With Depreciation 1.020

Professor David WesselsThe Wharton School of the University of Pennsylvania 16

Corporate Valuation Operating Leases

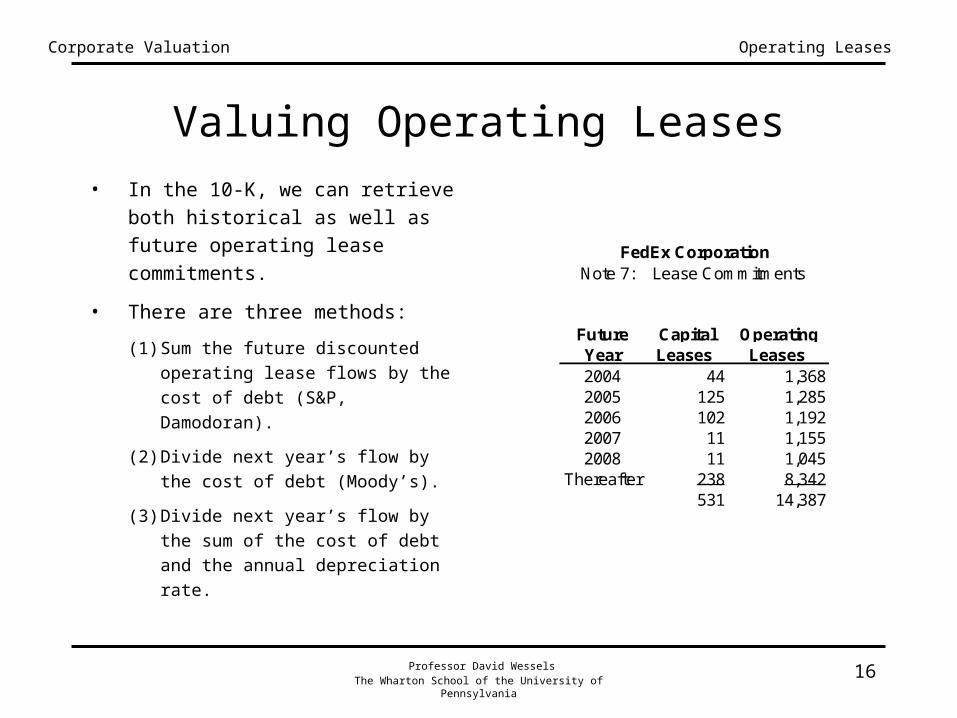

Valuing Operating Leases

• In the 10-K, we can retrieve both

historical as well as future

operating lease commitments.

• There are three methods:

(1) Sum the future discounted

operating lease flows by the cost

of debt (S&P, Damodoran).

(2) Divide next year’s flow by the

cost of debt (Moody’s).

(3) Divide next year’s flow by the

sum of the cost of debt and the

annual depreciation rate.

Future Capital OperatingYear Leases Leases 2004 44 1,3682005 125 1,2852006 102 1,1922007 11 1,1552008 11 1,045

Thereafter 238 8,342 531 14,387

Note 7: Lease Commitments FedEx Corporation

Professor David WesselsThe Wharton School of the University of Pennsylvania 17

Corporate Valuation Operating Leases

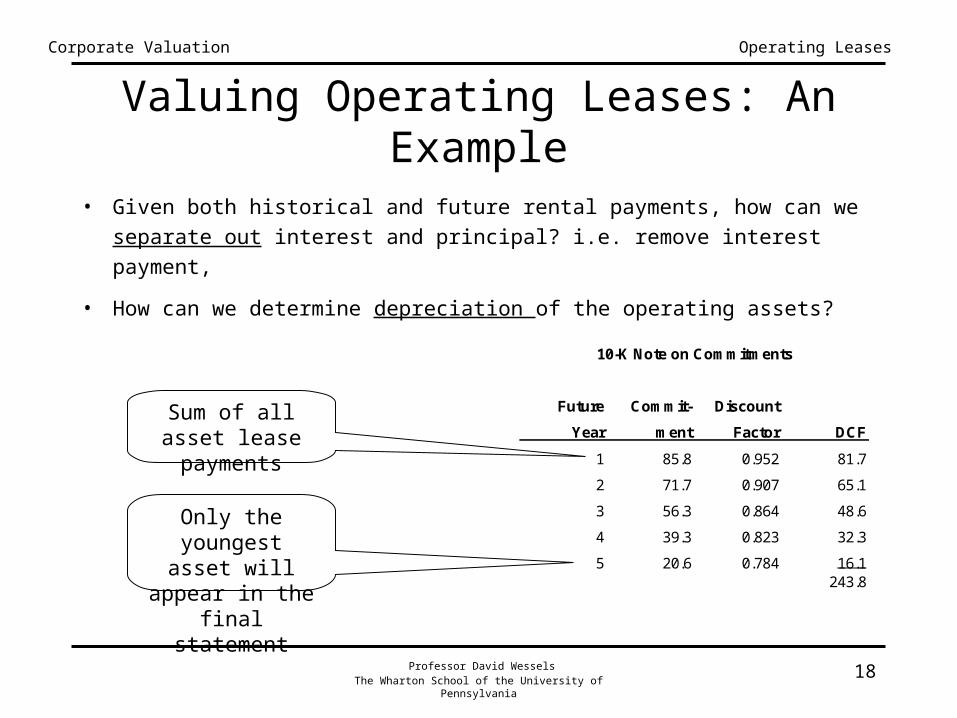

Valuing Operating Leases: An Example

• To understand how well each methodology works, let’s build a hypothetical

leasing example. In our example, we assume the company leases assets for

the first five of their ten-year lives, at an interest rate of 5%.

Assume asset life of 10

years, lease for first 5

years

Assets have been growing

at 10%

Cost of debt equals 5%

Original Current Net PV ofYears Asset Annual Asset Original Annuity AnnualAgo Value Depr Value Loan Factor Payment

4 100.0 10.0 60.0 60.8 4.33 14.03 110.0 11.0 77.0 66.9 4.33 15.52 121.0 12.1 96.8 73.6 4.33 17.01 133.1 13.3 119.8 81.0 4.33 18.70 146.4 14.6 146.4 89.1 4.33 20.6

610.51 500.0 85.8

Leasing Worksheet

Professor David WesselsThe Wharton School of the University of Pennsylvania 18

Corporate Valuation Operating Leases

Valuing Operating Leases: An Example

• Given both historical and future rental payments, how can we separate out

interest and principal? i.e. remove interest payment,

• How can we determine depreciation of the operating assets?

Sum of all asset lease payments

Only the youngest asset will appear in the final statement

Future Commit- Discount

Year ment Factor DCF

1 85.8 0.952 81.7

2 71.7 0.907 65.1

3 56.3 0.864 48.6

4 39.3 0.823 32.3

5 20.6 0.784 16.1243.8

10-K Note on Commitments

Professor David WesselsThe Wharton School of the University of Pennsylvania 19

Corporate Valuation Operating Leases

Valuation Methodology

• The most common method, discounted minimum rental commitments,

systematically underestimates the operating leases. A simple perpetuity

method (Rental expense / kd) systematically overestimates lease value.

Methodology PV Actual Error

Discounted cash flow (at kd) 243.8 500.0 -51%

Perpetuity valuation (at kd) 1715.4 500.0 243%

Wall Street rule of thumb (8x) 686.2 500.0 37%

McKinsey formula (asset life): 571.8 500.0 14%

Modified formula (avg lease & asset life): 467.8 500.0 -6%

Methodology Performance

Professor David WesselsThe Wharton School of the University of Pennsylvania 20

Corporate Valuation Operating Leases

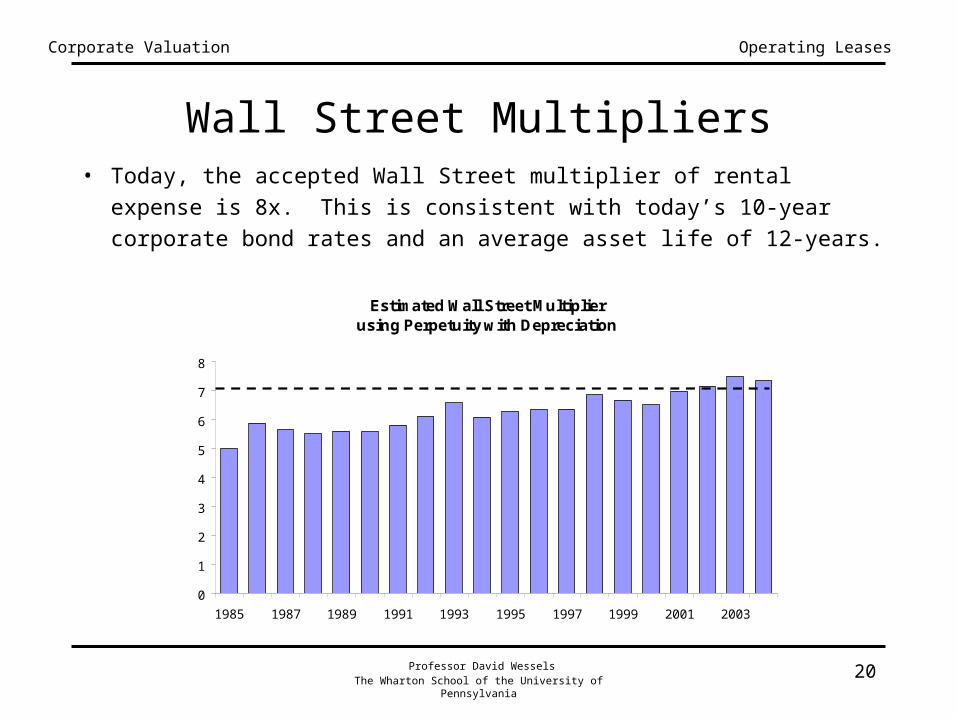

Wall Street Multipliers• Today, the accepted Wall Street multiplier of rental expense is 8x.

This is consistent with today’s 10-year corporate bond rates and an

average asset life of 12-years.

Estimated Wall Street Multiplierusing Perpetuity with Depreciation

0

1

2

3

4

5

6

7

8

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003