Corporate restructuring - ctconline.org - Mr.Amrish... · Restructuring options in light of recent...

41

Corporate restructuring October 2013

Transcript of Corporate restructuring - ctconline.org - Mr.Amrish... · Restructuring options in light of recent...

Corporate restructuring

October 2013

Role of CFOPage 2

► Recent trends in M&A

► Reorganization prerequisites

► Fund raising/cash infusion in operations

► Unlocking business value

► Tax planning

► Restructuring options in light of recent tax & regulatory developments

Content

Role of CFOPage 3

Glossary

CG Central Government

DDT Dividend Distribution Tax

IPR Intellectual property right

ITA Income-tax Act, 1961

LLP Limited Liability Partnership

MAT Minimum Alternate Tax

M&A Mergers and Acquisitions

NCLT National Company Law Tribunal

OL Official Liquidator

ROC Registrar of Companies

SCRA Securities Contract (Regulation) Act, 1956

SEBI Securities and Exchange Board of India

WOS Wholly owned subsidiary

CBDT Central Board of Direct Taxes

Role of CFOPage 4

Recent trends in M&A

Role of CFOPage 5

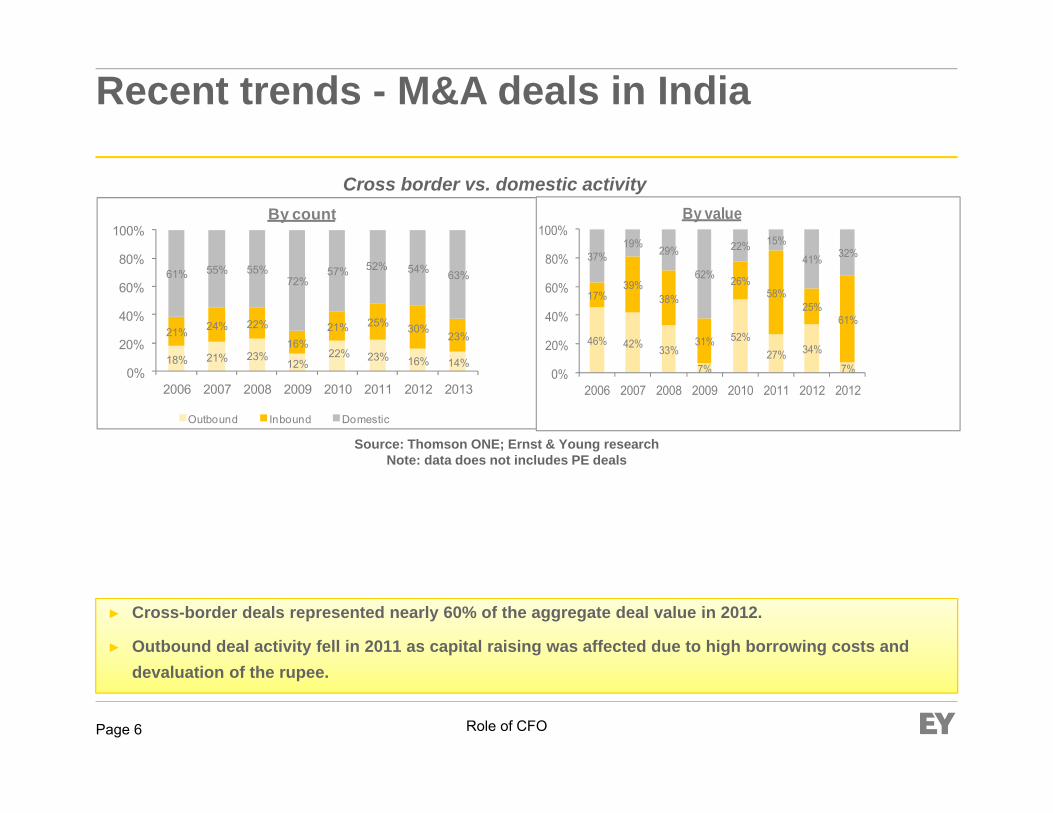

Recent trends - M&A deals in India

Source: Thomson ONE; Ernst & Young researchNote: data does not includes PE deals

30.7

43.9

53.8

40.7

17.9

62.2

34.6 34.8

1,107

1,298 1,296

1,209 1,134 1,196

840

977

0

200

400

600

800

1,000

1,200

1,400

0

10

20

30

40

50

60

70

80

90

100

2005 2006 2007 2008 2009 2010 2011 2012

Deal

coun

t

Deal

value

(US$

bn)

Deal value Deal count

Role of CFOPage 6

Recent trends - M&A deals in India

18% 21% 23%12%

22% 23% 16% 14%

21% 24% 22%

16%21% 25% 30%

23%

61% 55% 55%72%

57% 52% 54% 63%

0%

20%

40%

60%

80%

100%

2006 2007 2008 2009 2010 2011 2012 2013

By count

Outbound Inbound Domestic

46% 42% 33%

7%

52%27% 34%

7%

17%39%

38%

31%

26%58%

25%61%

37%19% 29%

62%

22% 15%

41% 32%

0%

20%

40%

60%

80%

100%

2006 2007 2008 2009 2010 2011 2012 2012

By value

Cross border vs. domestic activity

Source: Thomson ONE; Ernst & Young researchNote: data does not includes PE deals

► Cross-border deals represented nearly 60% of the aggregate deal value in 2012.

► Outbound deal activity fell in 2011 as capital raising was affected due to high borrowing costs and devaluation of the rupee.

Role of CFOPage 7

Restructuring Rationale

Commercial

Financial

► Business synergies► Inorganic growth► Gain more competitive position ► Focus on core competencies► Achieve economies of scale► Stake enhancement► Greater control over assets and operations► Exit► Strategic alliances/ partnerships► Unlocking value

► Tax savings► Reducing administrative and management costs► Upstreaming cash ► Encashing value► Cash infusion in operations► Projecting stronger financials► Organic growth► Larger dividends to promoters

Role of CFO integral in identifying opportunities/business requirements

Reorganization prerequisites: a snapshot

Role of CFOPage 8

Fund raising/cash infusion in operations

Role of CFOPage 9

Modes of restructuring for fund raising

Fund raising

Split

Consolidation

Vertical, horizontal and hybrid split – suitable for value split, when funds are required in specified business

Consolidation of similar business via merger, demerger and slump sale

Role of CFOPage 10

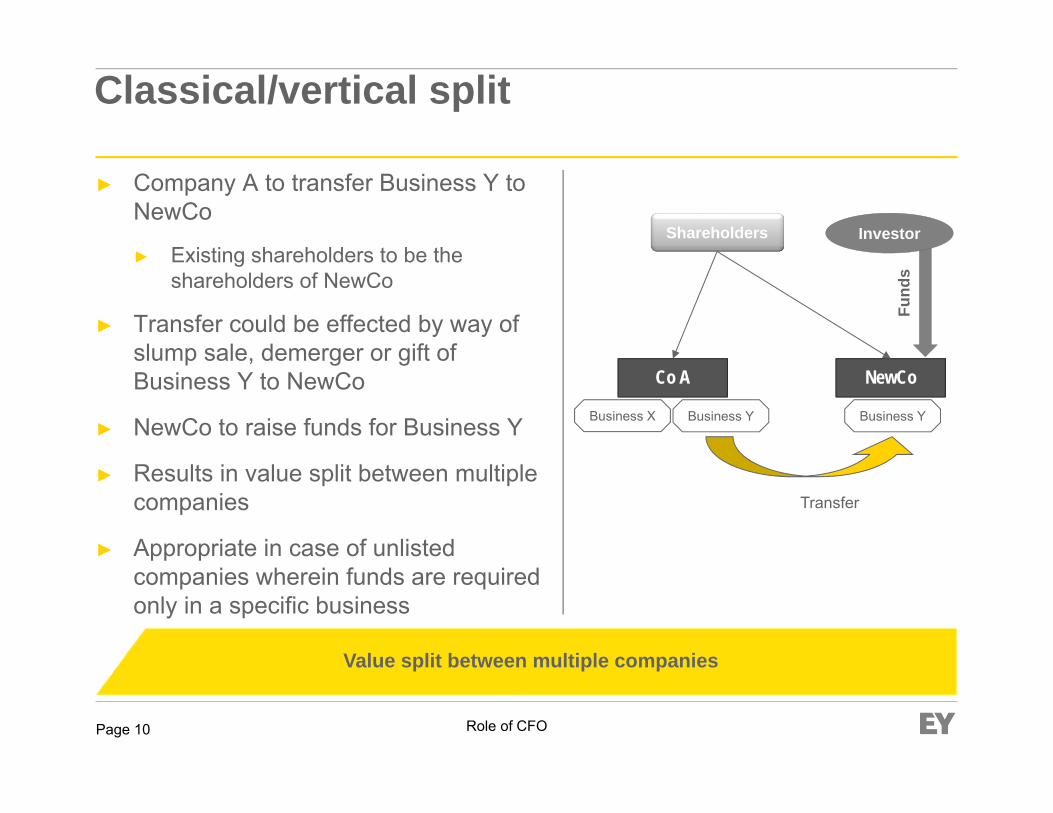

Classical/vertical split

► Company A to transfer Business Y to NewCo

► Existing shareholders to be the shareholders of NewCo

► Transfer could be effected by way of slump sale, demerger or gift of Business Y to NewCo

► NewCo to raise funds for Business Y

► Results in value split between multiple companies

► Appropriate in case of unlisted companies wherein funds are required only in a specific business

Co A

Shareholders

NewCo

Business YBusiness X

Transfer

Business Y

Investor

Fund

s

Value split between multiple companies

Role of CFOPage 11

Downward/horizontal split

► Company A to transfer Business Y to its WOS

► Transfer to be effected by way of slump sale, demerger or gift of Business Y to WOS

► WOS to raise funds for Business Y

► Value captured at Co A level

► Appropriate in case of listed companies wherein funds are required in only in a specific business

Co A

Shareholders

WOS

Business YBusiness X

Transfer

Business Y

Investor

Funds

Value consolidation along with fund raising efficiency

Role of CFOPage 12

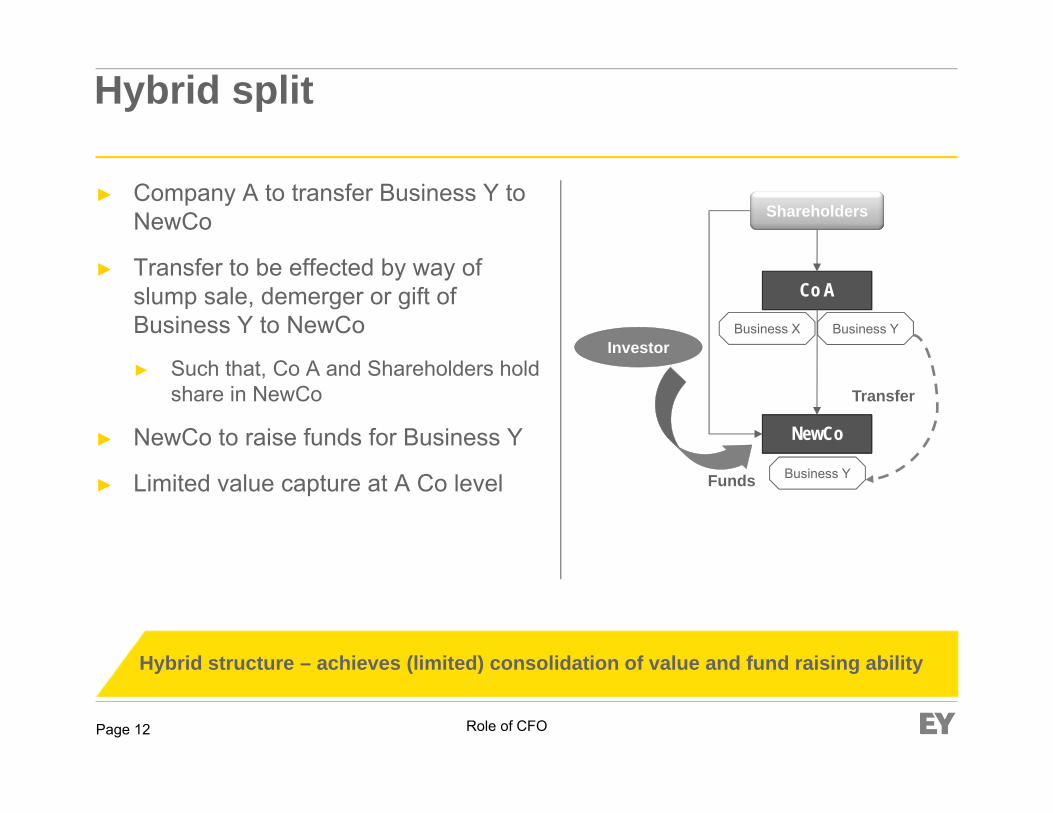

Hybrid split

► Company A to transfer Business Y to NewCo

► Transfer to be effected by way of slump sale, demerger or gift of Business Y to NewCo

► Such that, Co A and Shareholders hold share in NewCo

► NewCo to raise funds for Business Y

► Limited value capture at A Co level

Co A

Shareholders

NewCo

Business YBusiness X

Transfer

Business Y

Investor

Funds

Hybrid structure – achieves (limited) consolidation of value and fund raising ability

Role of CFOPage 13

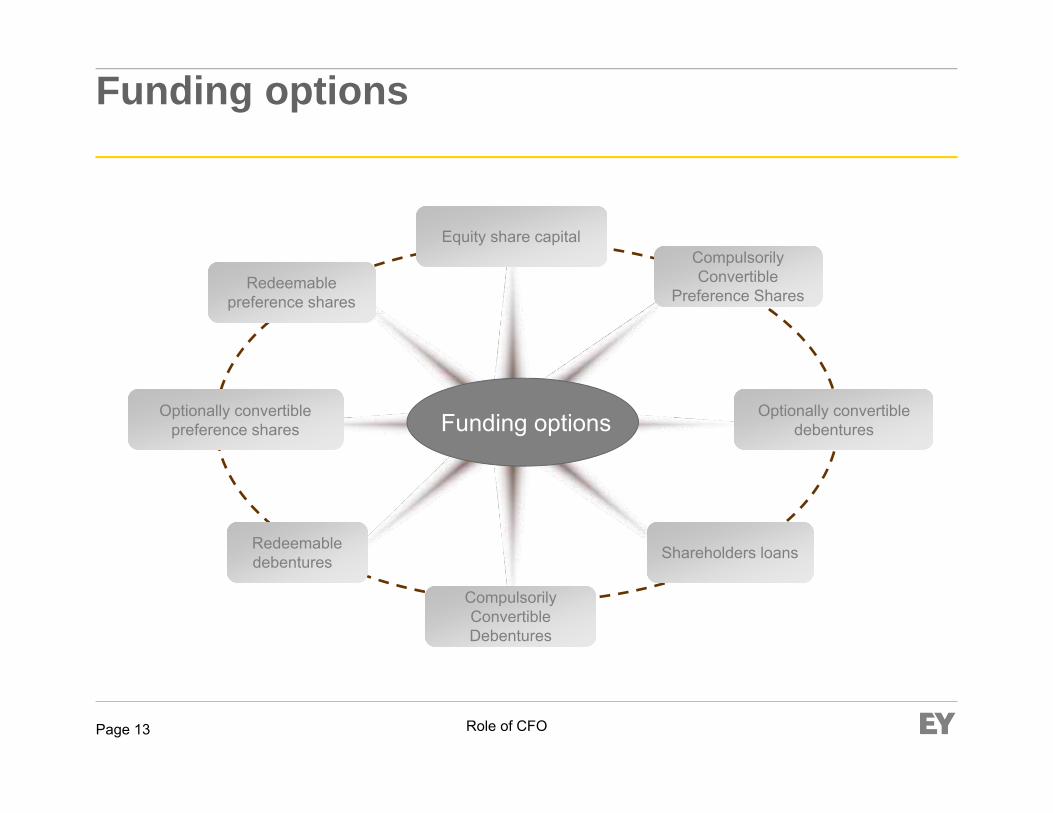

Funding options

Equity share capital

Compulsorily Convertible Debentures

Shareholders loans

Compulsorily Convertible

Preference Shares

Redeemable debentures

Optionally convertible preference shares

Redeemable preference shares

Optionally convertible debentures

Funding options

Role of CFOPage 14

Funding options – Key considerations

Ease of repatriation

Commercial considerations

Extent of control and voting rights

Tax efficiencyIndian exchange

control regulationsIndian company law regulations

Key

con

side

ratio

ns

Role of CFOPage 15

Unlocking business value

Role of CFOPage 16

Unlocking business value - Modes

Acquisitions Takeover of a sick entityConsolidation of operationsEnhancing promoter holdingsTax savingsEliminate multiple layers of

holdings

Focus in management, achieve higher market value, etcSegregation of core and non-core

businessesSale of business in a tax efficient

mannerMaking an entity exit ready

Unlocking business

value

Disinvestment of non-core businessConsideration may be structured

(Cash / shares)Time sensitivity

Transfer of single/ identified assetNo requirement for the Buyer Co

to continue to undertake the business

Role of CFOPage 17

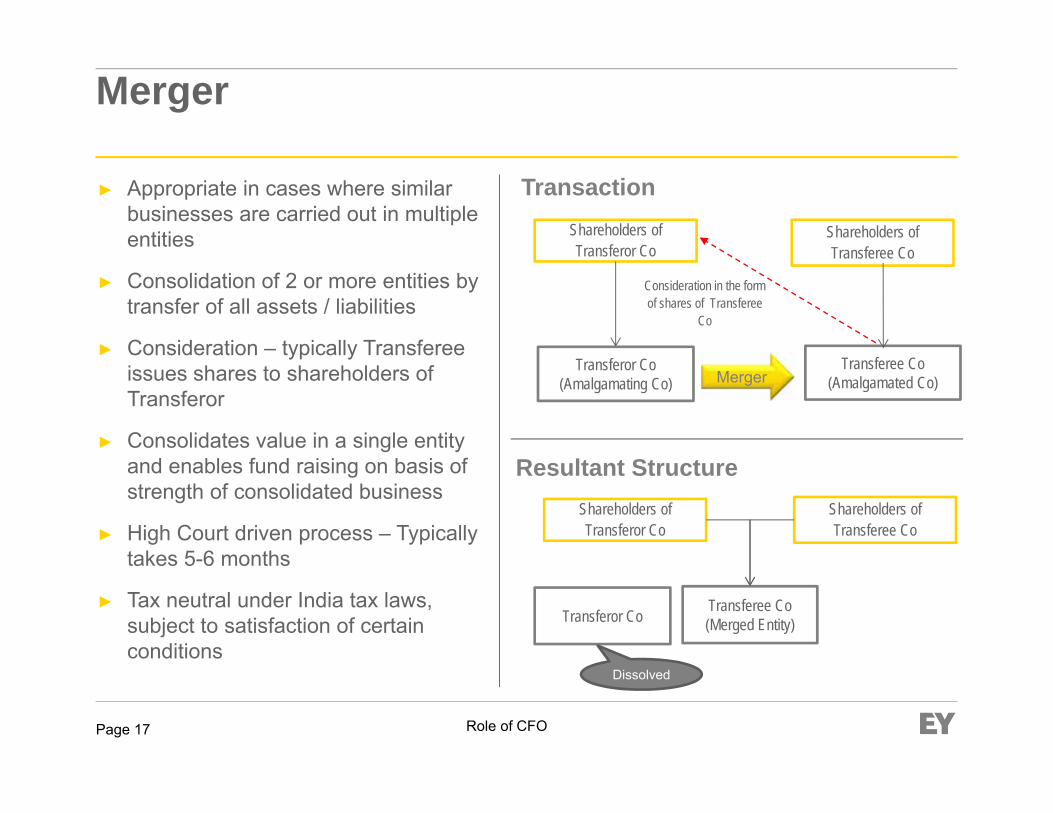

Merger

► Appropriate in cases where similar businesses are carried out in multiple entities

► Consolidation of 2 or more entities by transfer of all assets / liabilities

► Consideration – typically Transferee issues shares to shareholders of Transferor

► Consolidates value in a single entity and enables fund raising on basis of strength of consolidated business

► High Court driven process – Typically takes 5-6 months

► Tax neutral under India tax laws, subject to satisfaction of certain conditions

MergerTransferor Co

(Amalgamating Co)Transferee Co

(Amalgamated Co)

Shareholders of Transferor Co

Consideration in the form of shares of Transferee

Co

Shareholders of Transferee Co

Shareholders of Transferor Co

Shareholders of Transferee Co

Transferee Co(Merged Entity)Transferor Co

Transaction

Resultant Structure

Dissolved

Role of CFOPage 18

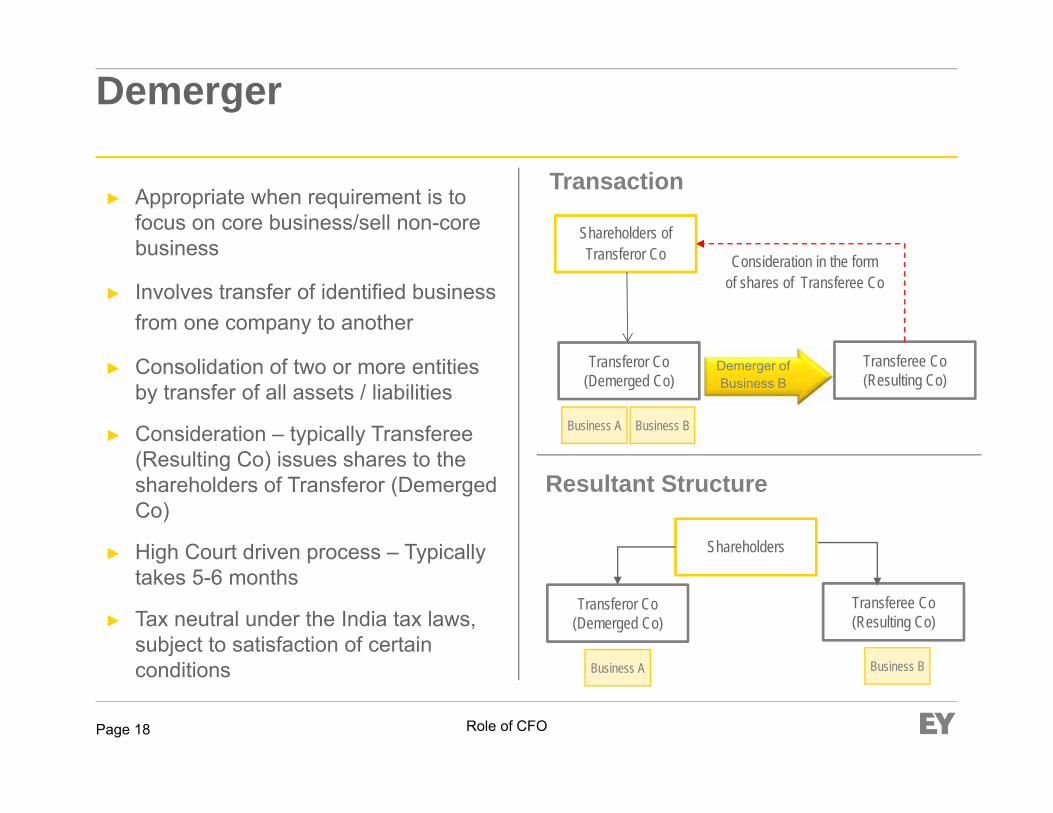

► Appropriate when requirement is to focus on core business/sell non-core business

► Involves transfer of identified business from one company to another

► Consolidation of two or more entities by transfer of all assets / liabilities

► Consideration – typically Transferee (Resulting Co) issues shares to the shareholders of Transferor (Demerged Co)

► High Court driven process – Typically takes 5-6 months

► Tax neutral under the India tax laws, subject to satisfaction of certain conditions

Shareholders

Resultant Structure

Transferor Co(Demerged Co)

Transferee Co(Resulting Co)

Shareholders of Transferor Co

Demerger ofBusiness B

Consideration in the form of shares of Transferee Co

Transaction

Business A Business B

Transferor Co(Demerged Co)

Transferee Co(Resulting Co)

Business A Business B

Demerger

Role of CFOPage 19

► Involves transfer of identified business for lump sum consideration from one company to another

► In consideration, the buyer company can issue shares / pay cash to the seller company

► No Court interference

► Freedom of structuring consideration as cash / shares unlike in a demerger

► Different between sale consideration and net worth of the business taxable as capital gains

Transaction

Post slump sale scenario

Selling company (Company A)

Shareholders

Consideration as shares/ cash

Shareholders

Selling company (Company A)

SellingCompany Buyer

companySlump sale of Business B

BusinessA

BusinessB

Slump sale

Role of CFOPage 20

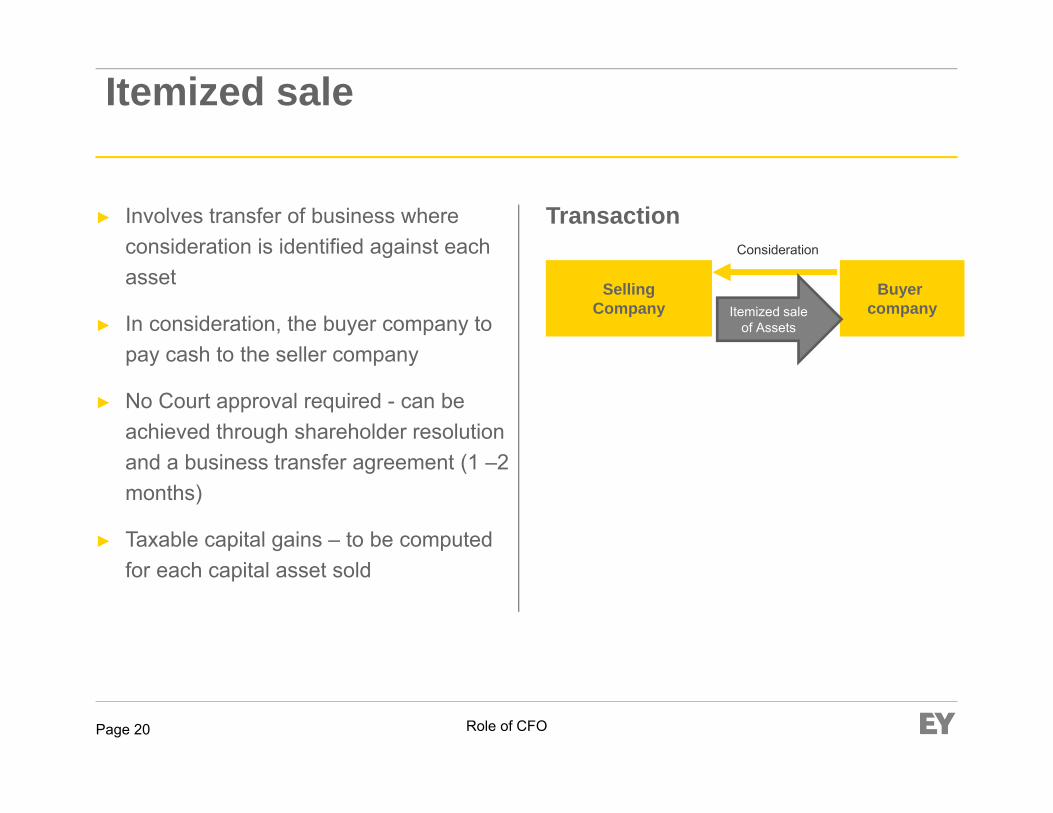

► Involves transfer of business where consideration is identified against each asset

► In consideration, the buyer company to pay cash to the seller company

► No Court approval required - can be achieved through shareholder resolution and a business transfer agreement (1 –2 months)

► Taxable capital gains – to be computed for each capital asset sold

TransactionConsideration

SellingCompany

Buyer companyItemized sale

of Assets

Itemized sale

Role of CFOPage 21

Tax planning

Role of CFOPage 22

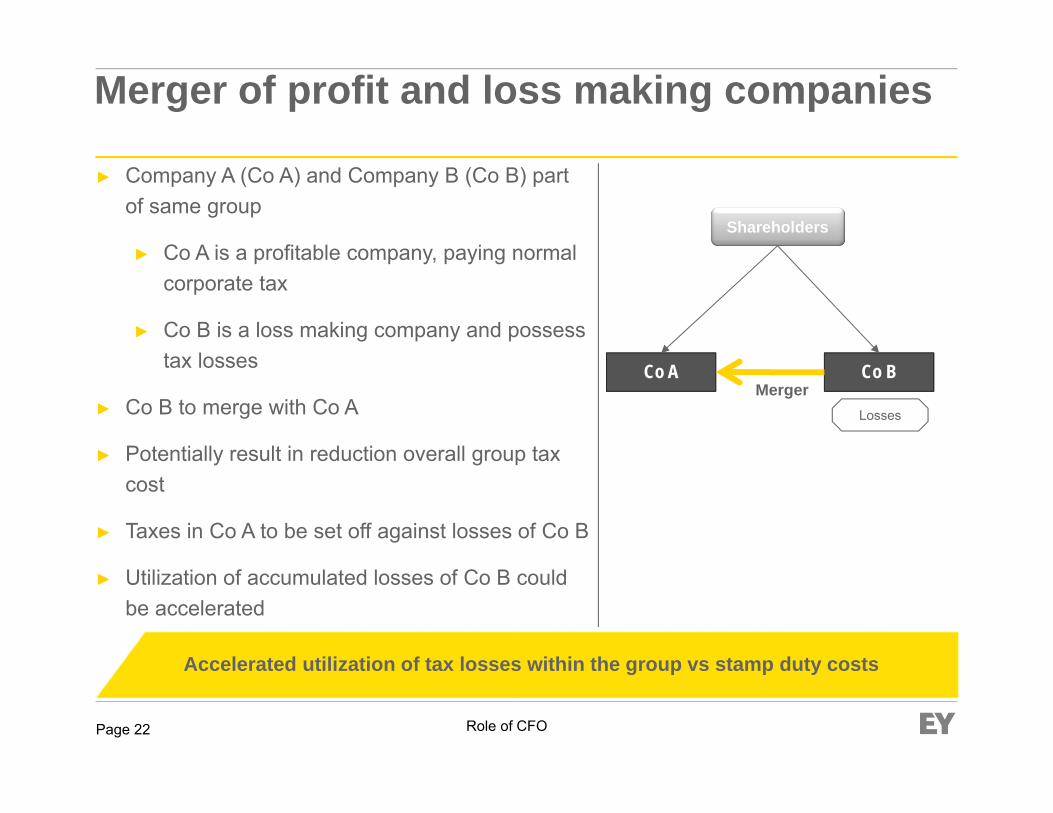

Merger of profit and loss making companies

► Company A (Co A) and Company B (Co B) part of same group

► Co A is a profitable company, paying normal corporate tax

► Co B is a loss making company and possess tax losses

► Co B to merge with Co A

► Potentially result in reduction overall group tax cost

► Taxes in Co A to be set off against losses of Co B

► Utilization of accumulated losses of Co B could be accelerated

Co A

Shareholders

Co BMerger

Losses

Accelerated utilization of tax losses within the group vs stamp duty costs

Role of CFOPage 23

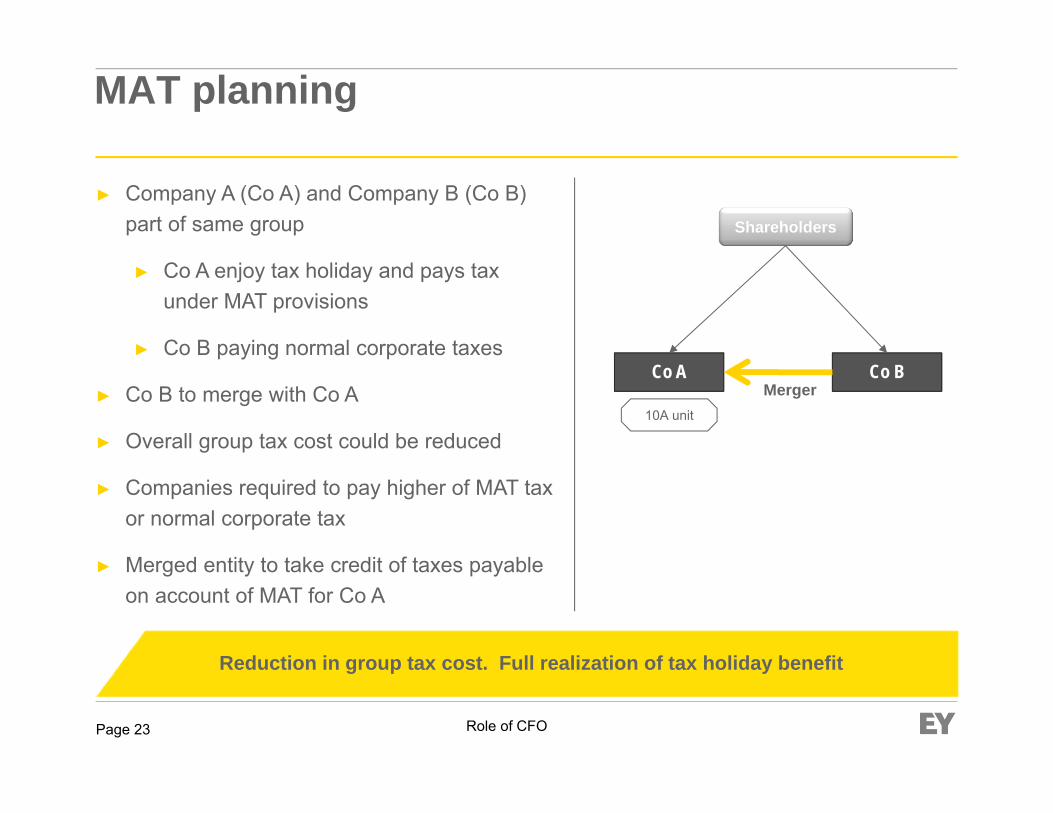

MAT planning

► Company A (Co A) and Company B (Co B) part of same group

► Co A enjoy tax holiday and pays tax under MAT provisions

► Co B paying normal corporate taxes

► Co B to merge with Co A

► Overall group tax cost could be reduced

► Companies required to pay higher of MAT tax or normal corporate tax

► Merged entity to take credit of taxes payable on account of MAT for Co A

Co A

Shareholders

Co BMerger

10A unit

Reduction in group tax cost. Full realization of tax holiday benefit

Role of CFOPage 24

Other features► LLP to have minimum 2 individuals (one of them to be Indian resident) as designated

partners► No cap on number of partners► Flexibility in adjusting profit share vis-à-vis capital contribution ► Rights of a partner to share profits or losses transferable► Foreign investment has been allowed in LLP via Government approval

LLP - A hybrid entity structure

Features of LimitedLiability

Partnership (LLP)

Features common with Company

Features common with Partnership firm

► Body Corporate► Distinct Legal Entity► Limited Liability ► Perpetual Succession► Common Seal

► Minimum 2 partners► Mutual Agreement► Partners personally

liable for their own wrongful act or omission

Role of CFOPage 25

DDT planning

Mechanism

► Ind Co. belongs to Foreign/Indian owned group

► Ind Co. converted to LLP

► Parent Company is partner in LLP

► LLP distributes profits to partners

Key benefits

► No DDT

► Profits exempt in hands of partners of LLP

Challenges

► Tax implications upon conversion of existing company into LLP

Profit distribution

Conversion to LLP

Shareholder

Partner

Transferor Co

Ind Co

India LLP

Role of CFOPage 26

Deemed dividend

Mechanism

► Parent with multiple Indian operating entities

► Indian operating entities set up as LLPs

► Excess cash in one operating entity and need for cash in another

► Inter-LLP loan

Key benefits

► Inter-LLP not considered as deemed dividend

► Tax efficient movement of cash within operating entities

Loan

India LLP 2India LLP 1 India LLP 3

India Co 3India Co 1 India Co 2

Parent

Role of CFOPage 27

Restructuring options in light of recent tax and regulatory developments

Role of CFOPage 28

Recent tax and regulatory developments

Developments

Companies Act 2013

Others

► Companies Bill introduced in 2008

► Passed by the Lok Sabha in Dec 2012

► Passed by the Rajya Sabha and Presidential assent in August 2013

► SEBI

Tax► Key recent developments in

the Indian tax landscape

Role of CFOPage 29

The Companies Act, 2013

Role of CFOPage 30

Investment layers

► Restriction shall not apply to:

► Acquiring a company incorporated outside India if such subsidiary has investment subsidiaries beyond two layers as per laws of that country; or

► Subsidiary having investment subsidiaries for meeting statutory requirements

H Co (Op Co)

Inv Co 1

Inv Co 2

Inv Co 3

Target Co

H CO (Op Co)

Inv Co 1

Inv Co 2

Inv Co 3

Target Co

Companies Act, 2013Companies Act, 1956

Impact

► The new restriction may need to be considered while evaluating any group restructuring

► To evaluate whether existing multi layered structures will be impacted

Role of CFOPage 31

Treasury shares

► Presently on merger of wholly or partially owned subsidiary with its parent, new shares in lieu of shares held by parent itself may be allotted to a trust which will hold such shares for parent’s benefit

► Companies Act, 2013 prohibit companies from holding shares in the name of trusts either on its behalf or on behalf of any subsidiaries or associate companies

► Provision likely to be effective prospectively

Impact

► Negates the dual advantage available earlier to the company to

► Indirectly hold such shares to provide access to liquidity; and

► Allowing promoters to retain a controlling stake

Role of CFOPage 32

Treasury Shares – Case Study…

Cos Act, 1956 Cos Act, 2013

A Co

Trust X

C Co

100%

Flexibilities relating to liquidity and increase in promoter control is available

A Co*

C Co

100%

100%

Flexibilities relating to liquidity and increase in promoter control may no

more be available

* No issue of shares on merger

Role of CFOPage 33

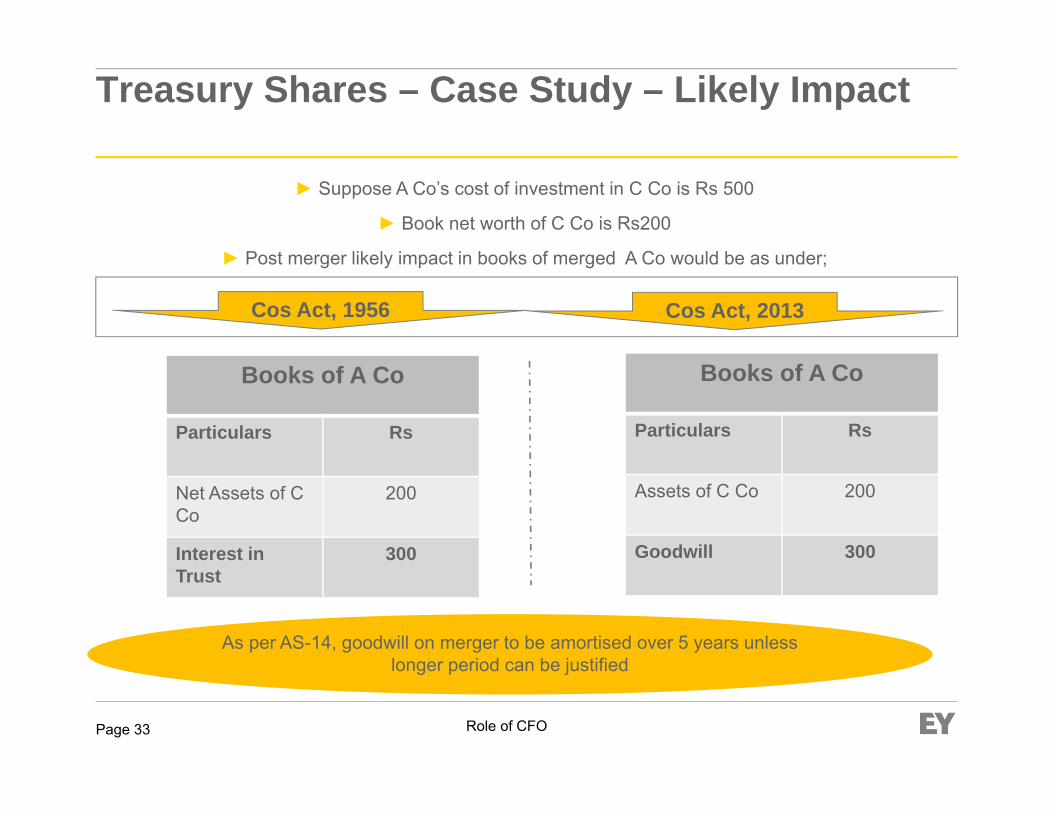

Treasury Shares – Case Study – Likely Impact

Cos Act, 1956 Cos Act, 2013

Books of A Co

Particulars Rs

Net Assets of C Co

200

Interest in Trust

300

Books of A Co

Particulars Rs

Assets of C Co 200

Goodwill 300

► Suppose A Co’s cost of investment in C Co is Rs 500

► Book net worth of C Co is Rs200

► Post merger likely impact in books of merged A Co would be as under;

As per AS-14, goodwill on merger to be amortised over 5 years unless longer period can be justified

Role of CFOPage 34

Cross border mergers

► Companies Act, 2013 permits outbound mergers i.e. amalgamation of Indian companies with Foreign companies

► Requirements relating to inter alia notified foreign jurisdiction and compliance with prescribed rules applicable to inbound as well as outbound merger

► Consideration to shareholders of merging entity could be in form of cash or depository receipts

Impact

► Scope of inbound mergers may get restricted to notified jurisdictions

► Tax and FEMA regulations to be aligned

Role of CFOPage 35

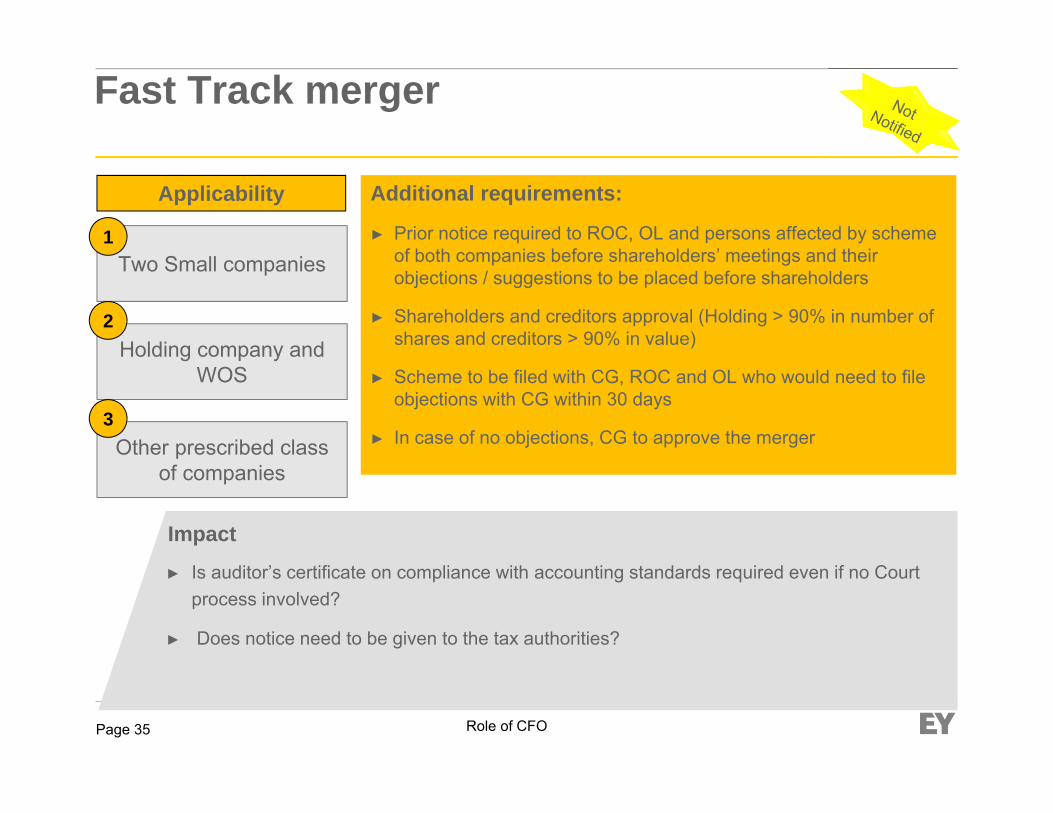

Fast Track merger

Two Small companies

Holding company and WOS

Other prescribed class of companies

1

2

3

Additional requirements:

► Prior notice required to ROC, OL and persons affected by scheme of both companies before shareholders’ meetings and their objections / suggestions to be placed before shareholders

► Shareholders and creditors approval (Holding > 90% in number of shares and creditors > 90% in value)

► Scheme to be filed with CG, ROC and OL who would need to file objections with CG within 30 days

► In case of no objections, CG to approve the merger

Applicability

Impact

► Is auditor’s certificate on compliance with accounting standards required even if no Court process involved?

► Does notice need to be given to the tax authorities?

Role of CFOPage 36

Merger of Listed Co. in to Unlisted Co.

Impact

► Provisions are applicable for both merger as well as demerger

► Indirect way of minority squeeze-out / delisting?

► Impact on tax neutrality of amalgamation if more than 25% shareholders opt for exit route?

► Companies Act, 2013 specifically provides that transferee company shall remain an unlisted company until it becomes a listed company

► Provision for an exit route for shareholders of the transferor company

► Payment of value of shares and other benefits in accordance with pre-determined price formula or as per prescribed valuation

► Payment/ valuation should not be less than what has been specified by SEBI

Role of CFOPage 37

Recent updates

Role of CFOPage 38

Recent updates - SEBI Circulars & notifications

Pre-emption and options in SHA

► Till recently, SEBI has restricted universally accepted contractual rights like pre-emptive rights, put-call options in Public companies

► SEBI has now issued a notification permitting contracts in shareholders agreements or articles of companies relating to pre-emption including right of first refusal, tag-along, drag-along rights and put-call arrangements

► The put-call arrangements are permitted subject to the following conditions:

► The title and ownership of the underlying securities are held continuously by the selling party to such a contract for a minimum period of one year from the date of entering into the contract

► The price or consideration payable is in compliance with all the laws for the time being in force

► The contract has to be settled by way of actual delivery of the underlying securities

► Contracts need to be in accordance with FEMA regulations

► The notification applies only prospectively, and does not affect or validate any contract which has been entered into prior to the date of the notification

Role of CFOPage 39

Recent updates - Others

Listing overseas► Unlisted companies that are incorporated in India were not

allowed to directly list in overseas markets without prior or simultaneous listing in Indian markets.

► It has now been decided with the approval of the Union Finance Minister that unlisted companies may be allowed to raise capital abroad without the requirement of prior or subsequent listing in India.

Role of CFOPage 40

Questions?

Thank you

Ernst & Young LLP

Assurance | Tax | Transactions | Advisory

www.ey.com/india

© 2013 Ernst & Young LLP All Rights Reserved.Ernst & Young is a registered trademark.

This presentation contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither Ernst & Young LLP nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.