CONTENT · PDF fileCONTENT FOREWORD EXECUTIVE SUMMARY INTRODUCTION TO MOBILE VIRTUAL NETWORK...

44

Transcript of CONTENT · PDF fileCONTENT FOREWORD EXECUTIVE SUMMARY INTRODUCTION TO MOBILE VIRTUAL NETWORK...

CONTENTFOREWORDEXECUTIVE SUMMARY

INTRODUCTION TO MOBILE VIRTUAL NETWORK OPERATORS (MVNOs) DefiningMVNOs DifferentCategoriesofMVNO

MVNO EVOLUTION

CLASSIFICATION OF MVNO DiscountMVNO LifestyleMVNO Advertisement-basedofMVNO EthnicMVNO

PROSPECTIVE MVNOs

WHY MVNOs? MVNOsValueProposition

IMPACT OF MVNOs MinimisingCannibalisationRisk

MVNO LAUNCH RISK AND ENTRY BARRIERS

MVNO REVENUES, COSTS AND PRICING Revenues Cost Pricing

UNDERSTANDING THE SUCCESS AND FAILURE OF MVNO SuccessFactors CaseStudy:VirginMobile,US VirginMobileMVNO FactorstoAvoid

GLOBAL AND REGIONAL PERSPECTIVES OF MVNO INDUSTRY GlobalCurrentandExpectedGrowth Number of MVNOs Number of MVNOs Subscriptions MVNO Revenues GlobalMarketReadinessforMVNOs RegionalMVNOsTrends United Kingdom United States Asia

REGULATORY CONSIDERATIONS IN MVNOs Supporter of Regulatory Intervention Opponents of Regulatory Intervention LevelsofRegulatoryIntervention MVNORegulatoryRegimeWorldwide

ENABLEMENT PARTNER– THE MOBILE VIRTUAL NETWORK ENABLER (MVNE)

MVNOs IN MALAYSIA TrendsinMalaysia Malaysia’sMarketReadinessforMVNOs MVNOsandtheMalaysiaRegulatoryEnvironment

CONCLUSIONACRONYMSAPPENDIXCONTACT US

CONTENT23

556

8

9999

10

10

1112

1414

15

16161618

1818192020

21212123232424252629

3232323233

34

34343537

383940

2 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

Thankyou.

DatukDr.HalimShafieChairmanMalaysianCommunicationsandMultimediaCommission(SKMM)

FOREWORD

TheMalaysianCommunicationsandMultimediaCommission(SKMM)isworkingonanumberofspecialindustryresearchreportsplannedfortheyearof2008anditiswithbothhonourandgreatpleasure,IpresenttoourreaderstheindustryresearchreportonMobile Virtual Network Operators (MVNOs) – The Redefining Game.

ThereportfeaturesabriefoverviewonMVNOsindustryincludingthedevelopment,growthand focus of MVNO in Malaysia and worldwide. There is a brief discussion on overallapproaches ofMVNO, namely discountMVNO; lifestyleMVNO; advertising-basedMVNOandethnicMVNO.

Furthermore,thereisalsoabriefdiscussionontheimpactofMVNOupontheMobileNetworkOperators(MNOs)andthemobilemarket;itssocio-economicbenefits,includingeconomiccosts. The discussion also covers revenue resources, cost, roaming issues and pricingmodelintheMVNOmarket.

Plus,thereareanalysisanddiscussiononsuccessandfailurefactorsintheMVNOindustry,includinghowfaraMVNOmodelissustainabledependingonthevalueitofferstocustomersaswellasitshostMobileNetworkOperator(MNO).TheanalysiscoversacomparisonoftheMVNOcompaniesworldwide. TheanalysisinthepublicationarebasedonvariousinformationsourcessuchasinternalinformationfromtheSKMMaswellasexternaldataandinformationpurchasedorobtainedfromothercompanies,includingpublicsourcesofnews,industryviews,researchreportsandotherdatabasesources.

AsoftcopyofthisreportcanbeobtainedfromtheSKMMwebsiteat:

http://www.skmm.gov.my/what_we_do/Research/industry_studies.asp

ItrustthisreportwillprovideusefulinformationtothereadersandcanservetobringtolightsomeperspectivestopropelthecommunicationsandmultimediaindustrydevelopmentinMalaysia. We look forwardtohearingyour feedback,whichwillhelpus improveourindustryreportsinthefuture.Pleasesendyourcommentstowebmaster@skmm.gov.my.

3MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

EXECUTIVE SUMMARY

MobileVirtualNetworkOperators(MVNOs)havegainedalotoffootholdintheglobalmobiletelecommunicationindustryandhaveevenattractedmuchinterestinAsialately.MVNOsarebasicallyresellerswhodonotownanynetworkfacilities,purchaseairtimeatwholesaleratesfromMobileNetworkOperators(MNOs)andthenresellwirelesssubscriptionstoconsumersthroughitsownbrandingandothervalueaddedservices.Aswidelyobserved,thereappearstobethreegenericcategoriesofMVNOs–resellers,enhancedserviceprovidersandfullMVNOs,witheachhavingadifferentmixofinfrastructureandoperationaltasksdependingonthebreadthanddepthof itsrelationshipwithitshostnetwork,theMNOs.However,MVNOstodaygobeyondbeingasimplereseller(firstgenerationmodel).MVNOsnowhavetakentheapproachofbeingafullMVNO(secondgenerationmodel)capableofprovidingamorecompellingservicemixtotheendusersthansimplydiscountvoiceonly.

Comparativestudieshaveshownthat,MVNOsalsohavefourgenericclassificationmodelsbasedontheirmarketingstrategies–discountMVNO,lifestyleMVNO,advertisement-basedMVNOandethnicMVNO.Eachmarketingstrategyleveragesonthenichemarketittargetsand the service and product differentiation opportunities. While the MVNOs greateststrengthisbeingabletoidentifyandtargetmarketsinneedoftheirservices,theirgreatestweaknessisthelackofeconomiesofscaleascomparedtoMNOs.

Nevertheless,withmobiletechnologicaladvances,higherbandwidthandmoreapplicationsthatspurthedemandforwirelessusage,theMVNOmodelremainsattractivefornewplayerswithpotentialentrantscuttingacross industrieswithmajoritynon-telcobasedoperatorssuchasretailers,financialinstitutionsandmediacompanies.Asseveralnon-telcobasedMVNOshavedemonstrated,UnitedKingdom(UK)leadssuccessinMVNObusiness.TherearemanyotherindustrydriverscontributingtothedevelopmentandproliferationofMVNOswhich include market opportunity, technology evolution and competitive dynamics. Inaddition,tobeasuccessfulMVNO,serviceprovidersnotonlyneedagoodbusinessmodel,theyhavetohaveanappealingvaluepropositionthatisnotonlygoingtoattract,butholdontocustomersthatareunique.

AlthoughmostMNOshavecometoaccepttheexistenceofMVNOsinthemarket,therestillstandsthefactthatMVNOshaveincreasedthecompetitivemarketpressureintheindustry,sometimes,indirectcompetitionwiththeMNOmarket.Subsequently,thereisincreasedriskofcannibalisationoftheMVNObytheMNO,whichusuallyhascomparativelyhighcontroloftheMVNO.Itisinterestingtonotethatontheupside,MVNOsdoprovideeconomicbenefitstotheMNOsastheyappeartoprovidegoodopportunitiessuchas increasedsubscriberbase,moderatesubscriberchurn,andincreasedtrafficdependingontheiragreementorbusiness relationshipwith theMVNOs. In otherwords, the incumbent is positioned tobenefit in terms ofmarket penetration and expansion, better network utilisation, loweroperationalcostsduetohighereconomiesofscaleandgenerationofadditionalrevenuesthroughwholesalevolumes.

On theotherhand,as thenumberofMVNOplayers increase, sodo the risks involved.Asestimatedbyanalysts, it takesonaverage,USD25milliontoUSD50millionandtwoyearstolaunchaMVNO1.SettingupanMVNOisalmostamonumentaltaskaseachstepup in itsservicedeliverychainposessomeentrybarrierand launchrisks. TheMVNO’scostandpricingmodelsarealsoimportantelementsastheywilldetermineifitwouldbeasustainablyprofitableentity.Consequently,noteveryMVNOthatislaunchedisableto

1 “Entering the Wireless Market – What You Need to Know to Launch and Operate Your Own Wireless Business” by Ovum, 2006

4 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

survivelongenoughtobreakevenintermsofprofit.MVNOshavemixedsuccessacrosstheworldandthereappearsnooneuniquesuccessformula.Keyfindingshaveshownthatstrongpartnerships,leveragingonbrand,widedistributionchannel,asolidcustomerbase,relevantvalueaddedservices,goodplanning,ampleaccesstocapitalandstrongexecutionteamareimportantelementsforawinningMVNOmodel.

EventhoughtherearebarriersandrisksinvolvedinlaunchinganMVNO,itisnoteworthythatthenumberofMVNOshasgrownsteadilyworldwideovertheyears,withUnitedStates(US),UKandcountriesinEuropeleadingtheway.Industryanalyst,BlycroftPublishing,estimatesthattherewere230activeMVNOsin2006.Byearly2007,accordingtoconsultancyfirm,TakashiMobile,thereare360plannedoroperationalMVNOsworldwide.Additionally,researchbyInformaTelecomsandMediaestimatedthatsubscriptionstoMVNOwillreach150millionworldwideby2013.IntheUS,Tracfone,VirginMobile,USandBoostMobileareamongthemajorplayerswhohavesuccessfullyadoptedtheMVNObusinessmodels.Evidently,UKhasoneof thebiggestMVNOmarkets intheworldwithVirginMobile,UKbeing thefirstMVNO in the countryandEuropeandnotably themost successful. ThepresenceinAsiaisalsobeingfelt latelywithrenewedinterestbeginningfrom2006.Todate,HongKongisthehighestMVNOpenetratedmarketinAsiawith720,000customersrepresenting7.5%ofHongKong’smarketpenetration.Overall,MVNOsareexpectedtohaveincreasinglysignificantimpactinthetelecommunicationsindustry.

Meanwhile, in termsof regulation,different countrieshavedifferingapproaches in theirregulatory regime towards MVNO business. Industry trends indicate that a supportiveregulatoryenvironmentisimportantforthedevelopmentsoftheMVNOindustry.Infact,MVNOsinUSandUKareobservedthrivingduetounregulatedenvironment,whereregulatorstake a non-interventionist, but “watchdog” ormonitoring stance towards the voluntaryMNO-MVNOrelationships.However,marketslikeHongKonghaveMVNO-relatedregulationthatrequires3Glicencestoopenupto30%oftheirnetworkcapacitytounaffiliatedMVNOswhileinItaly,thereisstrictprohibitiontowardsMVNOentry.

Likemanyothercountries,theMalaysialandscapeshowsreadinessforMVNOs.Factorssuchasincreasingmobilesubscribers,highnumberofprepaidsubscribers,diversifieddemographicstructuresuchasdifferentethniccommunitiesandsofarnon-intrusiveregulatoryregimeareencouragingdevelopmentsintheMVNOmarketinMalaysia.Recently,therearefourpioneeringMVNOsinMalaysia,namelyMerchantradeAsiaSdnBhd,REDtoneInternationalBhd,TuneTalkSdnBhdandXOX.comSdnBhd.Theseopenwindowsofopportunitiesfornon-telcooperatorstoaddmoremobileapplicationsandservices.ItwillbeinterestingtoseehowMVNOdevelopmentsunfold andenhance the telecommunications landscape inMalaysia.

5MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

INTRODUCTION TO MOBILE VIRTUAL NETWORK OPERATORS (MVNOs)

TherehasbeenanexponentialgrowthandfocusonMobileVirtualNetworksOperators(MVNOs)inthetelecommunicationsindustryworldwideinaperiodjustshortofadecade.ManymobilemarketshaveseensomeactivityintheMVNOspace,withmuchrenewedinterestinthismarketinthelasttwoyears.However,wheretherearemanyMVNOsinacountry,thenewentrantsinvariablyfaceahighlycompetitivemarketplace.

DEFINING MVNOs

Atpresent,thereisnocommonandagreeddefinitiononwhatconstitutesanMVNO.RegulatorybodiesaroundtheworldhavecometoadoptvariousdefinitionsanddifferentformsofregulatoryinterventiondependingontheextenttowhichanMVNOreliesonthefacilitiesoftheMobileNetworkOperator(MNO).Generally,MVNOsarecompanies thatdonotowna licensedcommunicationband,but resellwirelessservicesundertheirownbrandname,usingthenetworkofanotherMobileNetworkOperator(MNO).AfewexamplesofMVNOdefinitionsareasfollows:

Have specific network capabilities of their own, such as their own numberranges,SIMcardsorcorenetworkelements.AlightMVNOhasalittlemobilenetworkcapabilityotherthanthemanagementofSubscriberIdentityModule(SIM) cards,while a heavyMVNO invests in various infrastructures. MVNOoffersdistinctmobileservices,whichappeartocustomerstobeindependentfromtheunderlyinghostnetwork.

Providesmobilevoiceanddataservices toendusers throughasubscriptionagreement,withouthavingaccesstospectrum.MVNOnegotiatestobuyexcesscapacityforre-saletocustomersthroughcommercialagreementswithlicensedmobilenetworkoperators.

Enhancedserviceproviderthatindependentlybrandsandmarketsitswirelessservice,usuallytargetedatspecificmarketnichesandsupportedbyanexistingcustomerbaseholdingsomeaffinitywiththebrand.OwnsthecustomerbutusesthetelecomnetworkandradiospectrumofaMNO.

AGlobalSystemforMobile(GSM)phenomenonwhereanoperatororcompanydoes not own a licensed spectrum and generally without own networkinginfrastructure. MVNOs resell wireless services under their brand name anduseregulartelecomoperator’snetwork.MVNOsbuyminutesofusefromthelicensedtelecomoperatorandthenresellminutesofusagetotheircustomers.

Resellair timeandservicesbought fromthe licensedMNOs,adding insomefeaturessuchasbranding,alternativechannelstomarket,billingandcustomisedservices.

InvestinsomehardwareallowingittodifferentiateitsoffertothecustomersandmakeitlessdependentontheMNO’scapacity.HasfullcontroloverthecustomerwhowillhavetosignacontractwiththeproviderandissuetheirownSIMcards.

Resellersofferingservicetoconsumersbypurchasingairtimeatwholesaleratesfromfacilities-basedprovidersandresellingitatretailprices.

Provides mobile telecommunications services to customers throughinterconnectionwithandaccesstotheradiocommunications infrastructureofaMNO.

Organisationthatdoesnothaveassignmentof3Gspectrumbutiscapableofprovidingpubliccellularservicestoenduserbyaccessingradionetworksofoneormore3Gspectrumholders.

Analysys Research

Pyramid Research

KPMG

Telecomspace.com

Ovum Consulting

UK Office of Communications (Ofcom)

US Federal Communications Commission (FCC)

Office of the Telecommunications Authority (OFTA), Hong Kong

Malaysian Communications and Multimedia Commission (SKMM)

Source MNVO Definition

Source: Various websites

Industry Definition of MVNO

6 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

DIFFERENT CATEGORIES OF MVNO

ThereisawiderangeofMVNOmodels,fromsimpleResellertoEnhancedServiceProviders(ESP)andeventofullMVNOs.Eventhen,thereisyettobeasustainablewinningformula,althoughtherehasbeenmixedsuccessofMVNOsacrosscountries.

AccessNetworkMNO

MNO Position in the Mobile Value Chain

Mobile Network Operator (MNO)

CoreNetwork

ApplicationPlatform

SubscriberMangement

OperatorBillingCRM

DistributionSalesBranding

Degree of control and ownership

Reseller

Enhanced Service Provider (ESP)

Full Mobile Virtual Network Operator (MVNO)

Mobile Virtual Network Enabler(MVNO)

Source: Adapted from “Mobile Virtual Network Operator White Paper” by Nokia Siemens Networks, 2006

The appropriate businessmodels in positioning, branding,marketing and partnership appeals as keyfactors for success. How far anMVNO has control and ownership over its business depends on theworkingrelationshipitestablishesandbuildswithitsMNO.Insomecases,thereisalsoanotherentityarisingbetweentheMVNOandMNO,which isusuallyabusinessmodelspecialising insupporting thenetwork-operator-sidefortheMVNOthatistheservicesoftheMobileVirtualNetworkEnabler(MVNE)2.(Note:Thediscussions in the rest of this report focuson theMVNOmodel, although there is abriefintroductiontotheMVNEinalatersectionofthereport).

Ingeneral, thereare threecategoriesofMVNOs,namelyreseller,enhancedserviceprovidersand fullMVNO.Eachcategoryhasadifferentmixofnetworkinfrastructureandoperationaltasksinrespectiveareassuchasbranding,ownershipofSIM,networkinfrastructureincludingbillingandcustomercare.

2 MVNE provides the technical architecture and may enter into a wholesale agreement with a host MNO to enable mobile service provision. MVNE does not directly provide services to mobile users. Instead, it acts as an enabler for any number of MVNOs Sourced from “Mobile Virtual Network Operator White Paper” by Nokia Siemens Network, 2006

7MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

3 http://www.mobilein.com/what_is_a_mvno.htm

Abletosecuretheirownnumberingrange,offerownSIMcardandhavefullflexibilityonthedesignoftheservicesandtariffstructures.

Ownorprovidenetworkfacilitiesandnetworkservicessuchastowers,mobileswitchingcentres,HLRandcellularmobileservices.

Carryouttheircustomercareandbillinginhouse.

Fullyindependentbrandingandcustomerownership.

Ownpricing

*NFP(I)licencefor networkfacilities*NSP(I)licencefor networkservices*ASPlicencetoprovide publiccellularservice toendusers.

SIM, National Destination Code (NDC)

Network Infrastructure

Billing and customer care

Branding

Pricing

Licence*

Havetheabilitytosecuretheirownnumberingrange,operateownHomeLocationRegister(HLR)andofferSIMcardwithitsownmobilenetworkcode.

Donotownorprovidenetworkfacilities.DependentonMNOsfornetworkfacilitiesandradionetwork;abletomaintainsomeindependencefromMNOsasenhancedserviceprovidersareabletodifferentiatetheirproducts.

Carryouttheircustomercareandbillinginhouse.

Independentbranding,billingandhighlevelofcustomerownership.

Ownpricing,negotiationbased

*NSP(I)toprovide bandwidthservices, cellularmobileservices ormobileapplication services*ASPlicencetoprovide publiccellularservices toendusers.

DonothaveownSIMcardbutstillabletooffertheirownbrandedpackages.

RelyonMNOsforaccesstotheradionetworkandnetworkfacilities.

Carryouttheircustomercareandbillinginhouse.

Bundledbrandingandpossibleownbilling.

Ownpricing,negotiationbased

*ASPlicencefor providingpubliccellular services.

Infrastructure and Operational Task Full MVNO Enhanced Service

Providers Reseller

* MVNO in Malaysian environment as per Guideline on Regulatory Framework for 3G Mobile Virtual Network Operators dated 16 February 2005Note: NFP (I) = Network Facilities Provider (Individual); NSP (I) = Network Service Provider (Individual); ASP (I) = Application Service Provider Source: Various websites, Industry, SKMM

WhileMVNOstypicallydonothavetheirowninfrastructure,someleadingprovidersdodeploytheirownMobileSwitchingCenters(MSC),andinsomecases,evenServiceControlPoints(SCP).LeadingMVNOsdeploytheirownmobileIntelligentNetwork(IN)infrastructureinordertofacilitatethemeanstooffervalue-addedservices.Inthisway,MNVOscantreatincumbentinfrastructuresuchasradioequipmentasacommodity,whiletheMVNOoffersitsownadvancedanddifferentiatedservicesbasedonexploitationoftheirownintelligentnetworkinfrastructure3.

Thegoalofofferingvalue-addedservicesistodifferentiateversustheincumbentmobileoperator,allowingMVNOcustomeracquisitionnotorientedtocompeteonthebasisofpricealone.WhilesometimesofferingOperationalSupportSystems (OSS)andbusiness support systems forMVNOs, the incumbentmobileoperatorsusuallykeeptheirownOSS/BusinessSupportSystem(BSS)processesandproceduresseparateanddistinctfromthoseoftheMVNO.

AllthreeMVNO,MNO(andMobileVirtualNetwork(MVNE)wheretheseoccur)elementscreateadynamicecosystemstructurethatenablesoperationalefficiencyacrossdifferentcomponentsprovidingsupporttotheMVNObusiness.

Categories of MVNO

8 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

INFRASTRUCTURE OFFER

FINANCE

CUSTOMER

CORECAPABILITIES

COSTSTRUCTURE

REVENUESTREAMS

MVNO

Increasethenumberofmobilephoneusersandpenetratingmarketsegments

thatMNOfindworthytotarget

Mobileoperatorthat“rent

out”capacitytoMVNOscompanies

Providingback-office

processesandsystemsforMVNO

PARTNERNETWORK

VALUEPROPOSITION

CUSTOMERRELATIONSHIP

DISTRIBUTIONCHANNEL

TARGETCUSTOMER

Involvemarketsegmentation

AdvertisingSalesforce

Include“NofrillsMVNOs”,“SomefrillsMVNOs”

and“LotsoffrillsMVNOs”

•Pricingandservices•Content•Brand•Handsetpackage•Distribution•Customercare

•Interconnect•Operational•Investment•Marketing•Innovation•Others

•Subscriptionusers•Advertising•M-commerce•Contentapplication•Others

ReduceCapitalExpenditure(CAPEX)andrisk

Buildsbrand

Leadtopricecompetitionandnichespecificity

Limitedservicecreationcapabilitiesanddifferentiation

MostlyrelyonMNO’scorenetworkinfrastructureandserviceplatforms

•CallCentre•Instoreservice•Selfservice (e.g,.:Web)•Others

•Direct•Indirect

MNO

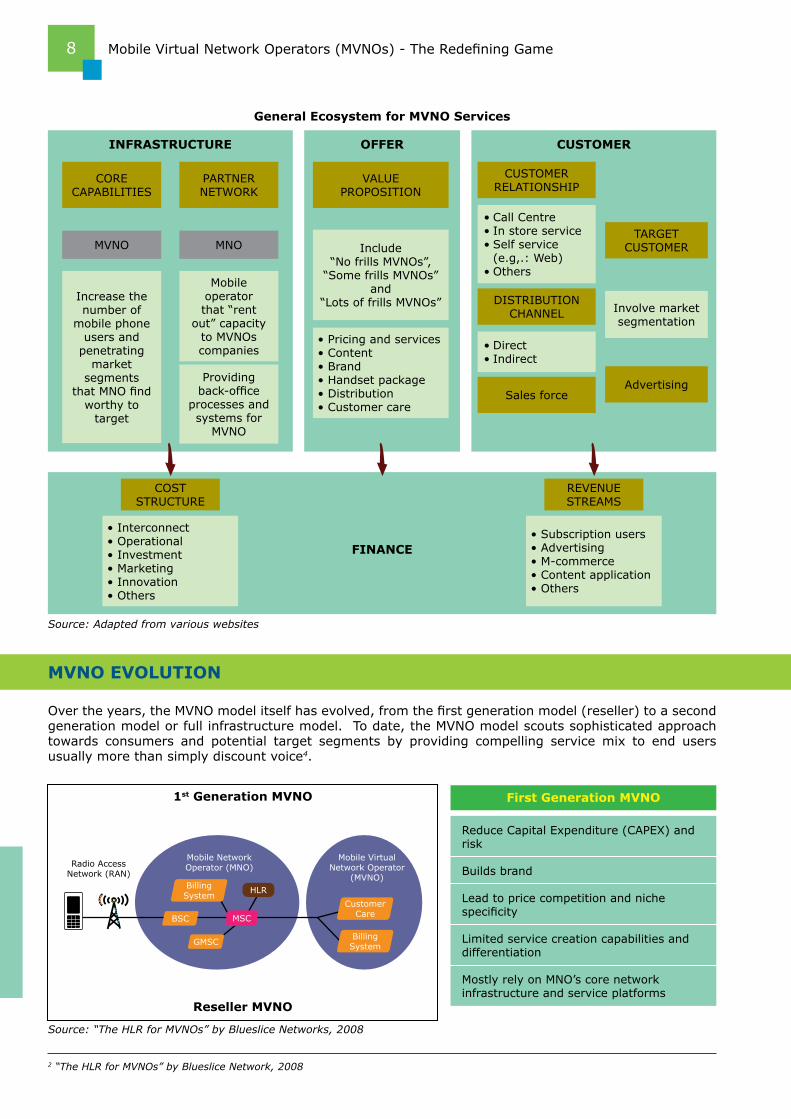

General Ecosystem for MVNO Services

Source: Adapted from various websites

Source: “The HLR for MVNOs” by Blueslice Networks, 2008

MVNO EVOLUTION

Overtheyears,theMVNOmodelitselfhasevolved,fromthefirstgenerationmodel(reseller)toasecondgenerationmodelorfullinfrastructuremodel.Todate,theMVNOmodelscoutssophisticatedapproachtowards consumers and potential target segments by providing compelling servicemix to end usersusuallymorethansimplydiscountvoice4.

2 “The HLR for MVNOs” by Blueslice Network, 2008

First Generation MVNO1st Generation MVNO

Reseller MVNO

MobileNetworkOperator(MNO)RadioAccess

Network(RAN)

MobileVirtualNetworkOperator

(MVNO)BillingSystem

HLR

GMSC

BSC MSC

BillingSystem

CustomerCare

9MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

CLASSIFICATION OF MVNO

DecreasedependenceonMNOnetwork

Totalsubscriberownership

Servicecreationanddeploymentagility

Harderforotherresellerstoentermarket

MVNOservicedifferentiationdrivesMNOsuccess

Second Generation MVNO

Source: “The HLR for MVNOs” by Bluslice Networks, 2008

Likeitsdefinition,thereisnooneclassificationforMVNOs. Froman operator’s viewpoint, there aregenerallyfourgenericMVNOapproachesbasedonits marketing strategies, namely discount MVNO,lifestyle MVNO, advertising-based MVNO andethnicMVNO.AsusuallyabasicgoalofanMVNOistoappealoutsideoftheexistingprevalentvoicemarket, such MVNO strategies essentially targetspecific niche markets by taking advantage ofserviceandproductdifferentiationopportunities.

Discount MVNO

DiscountMVNOsarerelativelystraightforward.ItisbasedonlowerprepaidorpostpaidtariffswithbasicvoiceandShortMessageService(SMS)servicesandis coupled with cheap cell phones and affordablepricingplans.Insomemarkets,itcanprovidecut-pricecallratestocertainmarketsegments.Mostofthehandsetsofferedareprettybasic,usuallymeantforthosewhojustwantaphonetomakecalls.

In a very competitivemobilemarket today, suchopportunities to grow MVNO using this approachappears tough for sustainability. An example isVirginMobile inanearlierpredominantlypostpaidUSmobilemarketwhichstartedoffthiswaybuthassinceevolvedovertimetoincludelifestylefeaturesincombinationwithoperationalefficiencies.

Lifestyle MVNO

LifestyleMVNOsoperatebyfocusingonspecificnichemarkets marked by demographics from youngerusersallthewaytoseniorcitizens.Handsetlineups

can therefore vary widely, as do services offeredandpricingplanscateringtowhatappealsintheserespectivemarketsegments.

Forexample,intheUS,MVNOsfocusingonyoungadultsareHelioandBoostMobileofferinggames,music, videos and evenmobile social networkingsuchasMySpaceapplication,whileDisneyMobileand Kajeet are family oriented MVNOs. GreatCalltargetstheelderlycommunityofferingsimplehandsets with larger than average buttons,24-hour operators assistance and simple serviceplans. Basically, lifestyle MVNO market is notextremelypricesensitivesincethephonescatertothefeature-hungry,notthevalueconscious.

Advertisement-based MVNO

A new trend in mobile phone content is theemergenceof advertising on this communicationsplatform. The advertisement-based MVNO offersfreeorsubsidisedmobilephoneserviceinexchangefor subscribers viewing a number of subscribertargeted advertisements. These MVNO’s utilisea “one person per presentation” model whererelevancyofanygivenadvertisement isbasedonuserdemographics,questionnaires,andtheliketobuild itsrevenuesfromadvertisingbyprovidingapre-setamountof freevoice, textandcontent tothesubscribers.

Inotherwords,mobileadvertising,whenexecutedappropriately, is no longer advertising in itstraditional sense; instead it effectively providesusefulandrelevantinformationtothesubscriberinapersonalisedmode.AnexampleofsuchaMVNOconsideredsuccessfulis,Blyk.

2nd Generation MVNO

Full Infrastructure MVNO

MobileNetworkOperator(MNO)RadioAccess

Network(RAN)

MobileVirtualNetworkOperator

(MVNO)

BillingSystem

BillingSystem

ServicePlatformsHLR

HLR

GMSC

GMSCBSCSoftswitch Auc

SMSCVoicemailEtc.

MSC

10 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

Ethnic MVNO

TheethnicMVNOapproachcancertainlybeagoodideainamarketwhereahugeforeigncommunitybaseispresent.Forexample,inUSthereisasubstantialpresenceofChinesecommunitybasedthereandthisincludesimmigrants,studentsandbusinesstraderswithtiesinChina.TobridgethetelecommunicationsgapforChinesespeakingpeopleresidingintheUS,in2006,RedPocketMobilewaslaunchedasthefirstUStelecomoperatorwithChinese languagecharactersandcustomerserviceagentswhospeakAsianlanguagesprovidingfreeinternationallongdistancecallsknownas“Asiaisalocalcall”.

AccordingtoresearchbyPiranPartners,thesubscribersofethnicMVNOscanbethenewimmigrantstoacountryandalsopeoplewithfamilyrootsinothercountrieswithhigherthanaveragedisposableincomeandaneedtokeepintouchwithfamilybackhome.Theyrepresentagenuinesourceofnew,highqualitymobilephonecustomers,muchneededinacompetitivecommunicationsmarketsohighlycharacterisedbychurn.

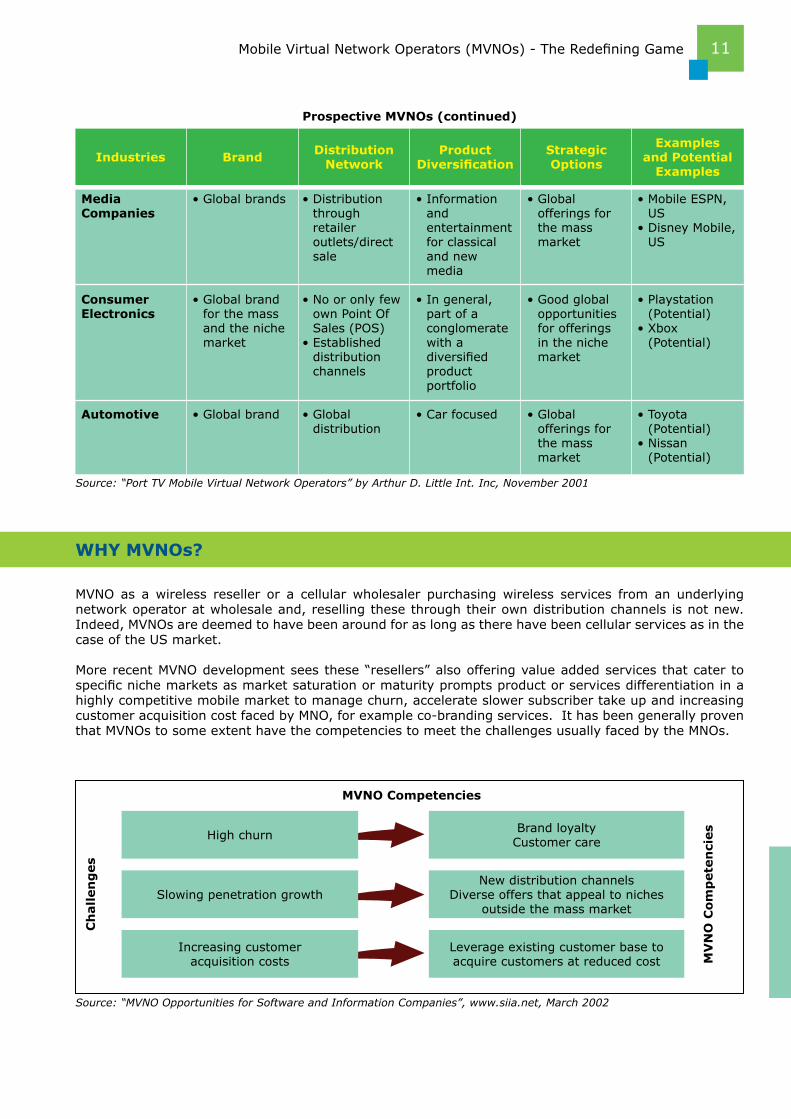

PROSPECTIVE MVNOS

Asthemobilemarketmaturesovertimeresultingfrom increasing customer base and intensecompetitionresultinginmoderatingmargins,thereis an increasing need for products and servicedifferentiationtomaintainmarketshareoracquirenew customers. This together with new mobiletechnologicaladvances,suchashigherbandwidthandmoreapplications,thedemandfortheusageofwirelessservicewillspellopportunitiesfornotonlyexistingserviceprovidersbutalsonewentrants.

Fixed NetworkOperator

Retailer

FinancialInstitutions

•Partlyglobal brands

•National brandswhich arestrongin retailingbut notimplicitly suitedfor brand differentiation

•National/ globalbrands

•Established distribution channels•Existing customerbase

•National distribution network

•National distribution network

•Fixed/mobile convergent•Fixedand mobile bundles

•Retailing diversifies intofinancial service industry (discount cards,leasing purchases)

•Product portfolio focusedon financial services

•Modest opportunityto expandinto new businesses

•National offerings inthemass market•Noexperience inmarketing forexisting targetgroups

•Goodvertical opportunities forspecial applications (e.g.mobile payment)

•BT,UK•AAPT, Australia

•TescoMobile, UK•Sainsbury’s One,UK•7-Eleven SpeakOut,US

•RaboMobiel (RaboBank), Netherlands•KFTCI,Korea•Standard Chartered (Potential)•Bankof America (Potential)

Prospective MVNOs

Industries Brand DistributionNetwork

ProductDiversification

StrategicOptions

Examples and Potential

Examples

Hence, the MVNO business model remains anattractiveoneinthesetimes,especiallythosewithstrongbrandsandextensivedistributionchannels.Evenfixednetworkoperators,andindeednon-telcobasedoperatorslikeretailers,financialinstitutions,mediacompaniesandautomotivecompaniesstandarelativelygoodchanceinpositioningitselfasanMVNO, or working in partnership or alliance withanMVNO,byleveragingontheirexistingbrandsaswellasoptimisingtheirdistributionnetwork.

11MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

WHY MVNOs?

MVNOas awireless reseller or a cellularwholesaler purchasingwireless services froman underlyingnetworkoperatoratwholesaleand,resellingthesethroughtheirowndistributionchannelsisnotnew.Indeed,MVNOsaredeemedtohavebeenaroundforaslongastherehavebeencellularservicesasinthecaseoftheUSmarket.

MorerecentMVNOdevelopmentseesthese“resellers”alsoofferingvalueaddedservicesthatcatertospecificnichemarketsasmarketsaturationormaturitypromptsproductorservicesdifferentiationinahighlycompetitivemobilemarkettomanagechurn,accelerateslowersubscribertakeupandincreasingcustomeracquisitioncostfacedbyMNO,forexampleco-brandingservices.IthasbeengenerallyproventhatMVNOstosomeextenthavethecompetenciestomeetthechallengesusuallyfacedbytheMNOs.

Media Companies

ConsumerElectronics

Automotive

•Globalbrands

•Globalbrand forthemass andtheniche market

•Globalbrand

Highchurn

Slowingpenetrationgrowth

Increasingcustomeracquisitioncosts

BrandloyaltyCustomercare

NewdistributionchannelsDiverseoffersthatappealtoniches

outsidethemassmarket

Leverageexistingcustomerbasetoacquirecustomersatreducedcost

•Distribution through retailer outlets/direct sale

•Nooronlyfew ownPointOf Sales(POS)•Established distribution channels

•Global distribution

•Information and entertainment forclassical andnew media

•Ingeneral, partofa conglomerate witha diversified product portfolio

•Carfocused

•Global offeringsfor themass market

•Goodglobal opportunities forofferings intheniche market

•Global offeringsfor themass market

•MobileESPN, US•DisneyMobile, US

•Playstation (Potential)•Xbox (Potential)

•Toyota (Potential)•Nissan (Potential)

Industries Brand DistributionNetwork

ProductDiversification

StrategicOptions

Examples and Potential

Examples

Prospective MVNOs (continued)

Source: “Port TV Mobile Virtual Network Operators” by Arthur D. Little Int. Inc, November 2001

MVNO Competencies

Ch

all

en

ges

MV

NO

Co

mp

ete

nci

es

Source: “MVNO Opportunities for Software and Information Companies”, www.siia.net, March 2002

12 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

USD10billiontoUSD12billionrevenueprojectedby2008dueto:

Opportunitiesforcustomeracquisitionbynon-wirelesscompaniesbasedontheirexistingcorecompetenciessuchascontent,brandextensionsorefficientdistributionchannels.

Opportunitiestocapturenon-consumingwirelesscustomersthroughniche,targetedofferings.

Consumermarketismatureandhighlysegmented,opportunitiesinniche/segmentedmarketsrequireuniqueandintegratedofferings.

Mobilemarketisreachingsaturationandtheintroductionofprepaidsubscriptionshashadalargeimpact.

Thefocusinrevenuesisexpectedtoshiftfrombasicservicestomorecontent-basedvalue-addedservices.

Maturingof3G(highspeedwirelessnetworks)enablingmedia/entertainmentoffers

EmergingintegrationtechnologiessuchasIMS(IPMultimediaSystems)whichsupportintegrationofvoiceanddataproductssuchasvideo,music,andgamingmakingmobileaviablemediacontentchannel.

Slowinggrowthoftheoverallwirelessmarket–thusmakingwholesaleanattractiverevenuesourcetothewirelesscarriers.

Consolidationofmegawirelesscarrierscreatinganeedfordifferentiation.

Competitivepressuretocontinuetoinvestinimprovingthenetwork.

MVNO Drivers

Market Opportunity Technology Evolution Competitive Dynamics

Source: “Mobile Virtual Network Operators: Converge in Action: Is an MVNO right for you?” by Deloitte, Technology, Media and Telecommunications, 2006; “Mobile Virtual Network Operators: Introducing the Business Concept of “One Does Not Need to Own a Cow to Milk a Cow”, during seminar on Mobile Operator, Strategies and Games, November 2003

MVNOs Value Proposition

Forend-users,valuecouldbeequatedtothemobileexperiencederivedfromusageofthemobileservicespaidfor.Ontheotherhand,valuetotheserviceprovidersandnetworkoperatorsisrelatedtorevenue.Similarly,MVNOsbasetheirstrategiesoncreatingvaluesfortheirtargetmarket.Theyarealsomoreinclined to consider consumerpreferenceand identify consumerneeds, tooffer specific serviceswithvalue-addedperspectives.

AccordingtoAccenture,MVNOsbasetheirstrategieseitherontargetingapartofthemarketplacethatiscurrentlyunservedorunderservedor,alternatively,by“hyper-serving”asegmentofthepopulationwithanoverwhelmingvaluepropositionthatconvincesconsumersinthatsegmenttoswitchfromtheircurrentproviders6.

6 “Virtually Mobile” by Accenture, 2006

13MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

Customer care

Product and Services

Handset Packages

Distribution

Brand

Pricing

-Dealingwithcustomersincontext.Forexample,agentsofMVNO companiesaretrainedtospeakinthelanguageoftheirbase, respondingtocustomers’complaintnotwithformalisedplatitudes butratherwithcolloquialexpressions.

-MVNOsneedtodetermineproductisprepaid,postpaidorsome combinationofthetwo.-Identifyvoiceservices,dataservicesandcontentthatenrich customer’sexperience.

-Understandtherequireddevicefunctionalityandthenconstructa handsetportfolio,identifyingtheproposedvendors

-Representsamajorcost.However,someMVNOscanderive significantcostadvantagesfromtheirdistributionstrategy.

-Involvesprospectingforpotentialsubscribers,brandingwhich positionsanddifferentiatestheMVNO,anduseofthemediato promotethebrand.

-Mustdifferentiatethepricing;voiceanddatarates,contentpricing andhandsetpricing.

MVNO Value Proposition

7 “Your Brand, Unplugged: A Strategic and Structured Approach to Launching an MVNO” by DiamondCluster International Inc., 2005

TobeasuccessfulMVNO,serviceprovidersnotonlyneed a good businessmodel, they have tohaveanappealingvaluepropositionthatisgoingto attract and havecustomers holding onto that unique servicesor products offered.Given these inputs, theMVNOvaluepropositionfromend-userspointofviewcanbedividedintosix segmentswhich arecustomer care, productand services, handsetpackages, pricing,brand, and distribution.Each of these valuepropositions serves todifferentiate the MVNOfrom the operators andat the same time stillbe coherent with eachother, their segmentneeds, and spendingdisposition, whencombined, producingthe desired valueproposition.

Source: “The MVNO Opportunity” by Ericsson, September 2006

Source: “Your Brand, Unplugged: A Strategic and Structured Approach to Launching an MVNO” by DiamondCluster International Inc., 2005

MVNOValue

Proposition

HandsetPackages

Product&Services

CustomerCare

•Callcentre•Instoreservice•Selfservice (IVR,Web)

•Functionality•2G/3G•Portfolio•Customisation

•Voice•Data•Content•Broadband•Handset subsidy

•Ownstores•Indirectchannels•Directsalesforce•Corporate•Logistic

•Marketsegments•Marketcommunications•Media•Advertising

•Pre-paid•Voice/Data•Content

Distribution Pricing

Brand

14 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

IMPACT OF MVNOs

There isnodoubtthat thearrivalofMVNOswill increasecompetitionthuscreating increasingmarketpressures. As MVNOs can provide both socio-economic benefits and economic costs to incumbents,MVNOsneedtofindtheappropriatebalancetomoderatethepossibleincumbentlossofbusinessortakeadvantageandturnthemintoopportunities.FindingshaveshownthefollowingimpacttowardsMNOsandthemobilemarket:

InadditiontolosingtraditionallypostpaidcustomerstoMVNOs,MNOscanalsofindthemselvescompetingdirectlywithMVNOsintheprepaidsegment

MVNOcantriggerpricewarsandundermineprofitabilityofallplayersanddrivingthemobilemarkettowardslowerARPU.

IfMNOislinkedtoanMVNOthatprovidessubstandardqualityservice,theMNOwillriskitsownbrandreputationbygettingtheblamefromcustomers,ratherthantheMVNOforpoorcustomerservice.

ThoughMVNOcanincreaseMNOsnetworkutilisation,itcanalsocauseseriousnetworkcongestionproblemwhichleadstoreductionsinservicequality.

Theincreasednumberofavailablecompetitivealternativesmaymotivatecustomerstochangetheirrespectivemobileserviceprovidersmorefrequently.

MVNOspromoteprepaidplansthatgeneratemuchlowerARPUwhereMNOsareforcedtooffertheirownlow-ARPU

ExtendingservicestomarketsegmentsthatarenotviablefortheMNOe.g.,nichemarket

ExpandsmarketreachorbringsmorebusinessinmarketsegmentswheretheMNOisalreadystrong

Betternetworkutilisation

MostMVNOsdotheirownbilling,customerserviceoperations,collectionandmarketingandsales.ThisreducescostburdenonMNOs.

Generatesadditionalrevenuesthroughhighwholesalevolumesand/orthroughparticipationfrompremiumprice

Market Segments(Strategic)

Market Expansion(Market)

Network Utilisation(Operational)

Lower Operational Costs(Operational)

Increased Profits(Financial)

Market Share Cannibalisation(Strategic)

Price Erosion(Financial)

Branding Impact(Strategic)

Network Congestion(Operational)

Increased Churn(Market)

Lower ARPU(Financial)

Economic Benefits Economic Costs

Source: “Mobile Virtual Network Operators: Blessing or Curse? An Economic Evaluation of the MVNO Relationship with Mobile Network Operators” by NERA, 2006; “Mobile Virtual Network Operators” by Arthur D. Little Int. Inc, 2001

Impact of MVNOs to MNOs and the Mobile Market

Minimising Cannibalisation Risk

AsMNOsmay,atsomepointintimeduringthedevelopmentofaMVNO,seetheMVNOasathreattotheirbusiness,thereisinherentriskofMVNOcannibalising.Toavoidsuchdevelopment,andtosustainitselfinthebusiness,ithasbeenreportedthatsomeMVNOshaveundertakendifferentstrategiestoprotectthemselvesasfollows:

1.ExpandthebusinesstoasubstantialsizethattheMVNOisabletocompetewiththeothersignificant mobileproviders.AnexamplecouldbeVirginMobilewhosebusinesshasgrownsignificantinsizeina relativelyshortperiodoftimethatenablesittosurviveinacompetitiveindustry.

15MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

MVNO LAUNCH RISKS AND ENTRY BARRIERS

• Lackofwirelessdistributionskills/ expertise•Brandbuildinginvestments•Highdistributioncostsorlackof capillarity

• Lackofwirelessofferskills/expertise•Highofferdevelopmentcosts• Lackofscaletonegotiatewith CertificationandAccreditation(C&A) providers/partners

• Lackofhandset/skillsexpertise•Highhandsetsubsidies• Lowvolumeofhandsetstonegotiate withOEMs

• Lackofmobiledataskills/expertise•Highintegrationcosts• Lackofscaletonegotiatewithmobile dataplatformproviders

• Lackofback-officeskills/expertise•Highintegrationcosts• Lackofscaletonegotiatewithback- officeproviders/MVNEs

• Lackofwirelessnetworkskills/ expertise• LackofscaletonegotiatewithMNO

•Branddesignandcosteffectivelaunch•Selectionandnegotiationwithdistribution channels

•Targetedandattractiveofferdesign•Targetedandprofitablepricingplan design•Selectionandnegotiationwithkey ContentandApplication(C&A) providers/partners

•Selectionandnegotiationwithhandset OriginalEquipmentManufacturers(OEMs)•Customisationhandsets•CertificationofhandsetswithMNO

•Selectionandnegotiationwithmobile dataplatformproviders•Systemintegrationbetweenmobiledata platformsandback-officesystems

•Selectionandnegotiationwithback-office providers/MVNEs•Managementandsystemintegrationof multipleproviders

•SelectionandnegotiationwithMNOs•SystemintegrationwithMNO

Brandanddistribution

Offerdevelopment

Handsets

Mobiledataplatform

Back-officeprocessesandsystems

Network

End-user Launch Risks Entry Barriers

MVNO Launch Risks and Entry Barriers in the Service Delivery Value Chain

ThelaunchandoperationofanMVNOrequire: a. awholesaleagreementwithanMNO; b. start-upcapital;and c. capitaltocoveroperationalexpendituresandconsumeracquisitioncosts.

Industryestimatesarethat,ittakesonaverageUSD25milliontoUSD50millionandtwoyearstolaunchanMVNO8.Despiterealisingthepotentialforsuccess,settingupanMVNOisrelativelylabourintensiveandamassivetaskduetoentrybarriersthatneedtobefacilitatedandratherhigh“launch”risksasitislegendarythatnotallMVNOssucceedintheirbusinesses.Furthermore,anMVNOmustmanageawidearrayofresponsibilitiesandrelationshipsasitmovesthroughtheservicedeliverychain.Forexample,criticaltothelaunchisthenegotiationofwholesaleagreement.Furthertothat,ifanMVNOmanagesitsownbusiness,ithastopurchaseacustomerrelationshipsoftwareapplication,adataplatformandbillingsoftware9whichareallelementsintheservicedeliverychain.EachofthestepsintheservicedeliverychainislinkedwithpotentialobstaclesandpartnershipdependenciesthatcouldderailtheMVNO’slaunchplan.Asummaryofthelaunchrisksandentrybarriersassociatedwitheachstepintheservicedeliveryvaluechainisshowninthetablebelow:

8 “Entering the Wireless Market – What You Need to Know to Launch and Operate Your Own Wireless Business” by Ovum, 2006.9 “Mobile Virtual Network Operators (MVNOs) in Israel: Economic Assessment and Policy Recommendation” by NERA Economic Consulting, August 2007

2.Theotherstrategyistoextendoperationsintoamarketthatissmallanddifficultenoughtodissuade theotheroperatorsfromhavinginteresttopursuetheMVNO.

3.Alternatively,thereisthe“surrender”strategywherebyMVNOsareabletomakeasignificantprofit for themselves by expanding the business substantially enough to make it so lucrative for other carrierstobeinterestedinbuyingitover.

Source: “MVNO 3.0: How a New Breed of Wireless Providers will Bring Strong Brands in the MVNO Space” by Diamond Management and Technology Consultants, 2006

Serv

ice D

eli

very

Ch

ain

16 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

MVNO REVENUES, COST AND PRICING MODEL

Revenues

ForanMVNO,themainsourceofrevenueisusuallyfrom its customers where the customers pay forcallconnectionandservices.However,abusinessdependentonvoiceonlyisnotviableenoughtodaytoobtainrevenuemargins.Asanexample,MVNOswhich are resellers that resell voice plans usuallyobtains low-revenuemarginproposition,generallyin single-digits. Makingmoney off voiceminuteswill be a persistent issue due to price erosion.EncouraginglyMVNOsareabletoimprovemarginsintherangeof15%to17%bysellingvalueaddeddataorcontentapplicationservices.Hence,inordertosucceedbydevelopingsignificantvolume,anMVNOneedtobeable toalsosourceotherkeyrevenue

The situation is different for MVNO as it doesnot own its ownnetwork, thusno customers canroamdirectlytootherMNOsorMVNOs.However,all customers of the MVNO have to roam to thenetworkofthesupportingMNObeforeroamingtootheroperators.

elementssuchasadvertisingorm-commerceontopofprovidinginnovativevalueaddeddataservices.SuchcombinationsorpackagesareuniquesourcesofincomethattheMVNOcanandisabletocontroltotally10.

Costs

Cost is associated with roaming issues. Roamingallows customers from one mobile operator(MNO or MVNO) to access the network of otheroperators(MNOs).RoamingbetweenMNOsisusualinthesensethatcustomersofMNO1roamstothenetwork ofMNO2, and some customers ofMNO2roamstothenetworkofMNO1.

Source: Adapted from “Option Pricing of Mobile Virtual Network Operators” by Telektronikk Vol. 4, 2001

Consequently,MVNOpaysforinterconnectioncosttoMNO forbothoutgoingand incomingcallsandinterconnection payments to other operators forcompleting outgoing calls11. Additionally, MVNOshaveotherkeycostelementssuchasoperational,investment marketing and innovation costs tomanage.

10 & 11 “The Mobile Virtual Network Operator Concept: Truth and Myths” by Telektronikk Vol. 4, 2001

RoamingMVNOto1(MVNO’snetworkprovider)beforeroamingto2(anotherMNO)

MNO2network(otheroperators)

MNO1networkRoaming2to1

Roaming1to2

MVNO

MVNO

MVNO

17MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

Source: Adapted from “How do the Price Agreements Affect the Business Case of an MVNO?” by Telektronikk Vol. 4, 2001

Source: Adapted from “Mobile Virtual Network Operators: Introducing the Business Concept of “One Doesn’t Need to Own a Cow to Milk a Cow” during Seminar on Mobile Operators, Strategies and Games, November 2003

SummaryoftherevenueandcostelementsforaMVNOisasfollows:

Revenue and Cost Elements for an MVNO

SIM–SubscriberIdentificationModuleIN–IntelligentNetworkHLR–HomeLocationRegisterVLR–VisitorLocationRegisterMSC–MobileSwitchingCentre

Outgoingcall/roamingout

Incomingcall/roamingin

Outgoingcall/interconnectother

Incomingcall/interconnecttoMVNO

Signaling/database

MSC MSC

SIM

SIMMNO

MVNO

IN IN

VLR

HLR

HLR

Other operator

TargetCustomer

VoiceServices

CostLeader

Subcription/Usage

Interconnect

Advertising

M-commerce

Contentapplication

InnovativeValue

AddedServices

Operational

Investment

Marketing

Innovation(R&D)

ServiceLeader

InnovationLeader

ValueAddedServices

-Limitedservicemix-Fewtarget customersgroup

-Largeservicemix-Manytarget customersgroup

-Higherinnovation investment-Fasterintroductionof newservics

Service Mix

Key Cost Elements

Key Revenue Elements

MVNO

MVNO’s Customers Making and Receiving Calls Architecture

18 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

Pricing

Pricing is an important element in thecommunicationsservicesbusiness.FortheMVNO,the right pricing can tip thebalance enabling theMVNOtobecomeaprofitableentity.Ontheotherhand,theadverseeffectofpoorpricingcan incurfatality. A win-win situation in price negotiationsbetween theMNO and theMVNO is desirable forsustained opportunities offering enhanced returnsall around, both in the short and the long term.Strikingthebalancewithaviewofawin-winformulawouldofferMNOsthebenefitsthatMVNOcanoffertoitsreturnonbusinessinvestments,andfortheMVNOstoinvestforanticipatedreturns,whichoneortheotherwouldnotobtainwithoutthismutuallybeneficial relationship inthefirstplace. Inshort,

MVNOsareobservedtofaceaseriesofoperatingchallengesinthediversemarketsinwhichtheyareimplemented. The success and failure ofMVNOsappear dependent on amix of factors. AlthoughthereappearshighlaunchriskforMVNOsworldwide,successful ones do exhibit sustained businesssuccess,andnewMVNOshaveinvariablycontinuedtoenterthemarket.

Nevertheless, how far an MVNO model is trulysustainable depends on the value it offers tocustomers as well as its host MNO. SeveralMVNOs like VirginMobile andBoostMobile in UShave demonstrated ability to outlive others in acompetitivelandscapeduetoappropriatebusinessmodelcapitalisingontheirstrengths.

havingashareof thebiggerpiegoesa longwayforderivationofnecessarilysustainablereturnsoninvestments.

OurfindingshaveshownthatthereareanumberofdifferenttariffmodelsthatcanbeappliedbyMVNOsonpricingstrategy. Theprovisionof tariffshouldalsoreflectthenatureoftheMVNOs,whetheritisapureresellerorafullMVNO.

TherearetwopossiblegeneraltariffmodeloptionsbetweenMVNOsandMNOseitherwithorwithoutregulatoryinterference,whichisthegenericmodelsofretailminusandcostplus.Asthedynamicsofthedetailsinsuchpricingmodelscannotbeadequatelytouchedinthisreport,sufficetonoteherethatthebasicsofsuchcostingmodelsareasfollows:

•LowMVNOmargins•Discouragepricecompetition•DefendMNOspositionand interest

•HighermarginsforMVNOs•Freedomtocompeteonprice

•Tariffmodel“Retailminus”•Retailprice–Negotiatedprice

•Tariffmodel“Costplus”•Costprice+agreedpremium/ margin

DeterminedbyMNO

DeterminedbytheRegulator

Tariff Models

Source: Adapted from “MVNOs in the Middle East: Threat or Opportunity?” by Delta Partners, July 2007

UNDERSTANDING THE SUCCESS AND FAILURE OF MVNO

Success Factors

MVNO’ssuccess isbuilt, inpart,by leveragingonthe brand, distribution channel, a solid customerbaseandanofferwhichincludescontent,platformsandinfrastructure.Tosucceed,accordingtoVirginMobile,MVNOsneedtoexecutethefollowing:

1.Targetcustomersthatmostcarriersignorelike low-credit,prepaidcustomersthatVirginMobile andTracfoneinUSfocuson;2.Launchadifferentiatedproduct;3.Buildcheapplatformslikesimplephones;4.Focus on crazy retail like selling big national retailchainsfromdayone;5.Acquirecustomercheaply;and6.Focus on the right metrics: Revenue per megabyteorperminute.

19MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

Case Study: Virgin Mobile, US

VirginMobile,USjointlyownedbySprintNextelandVirginMobileHoldings,PLCwaslaunchedin2002.By2007,thecompanyowned5.1millioncustomerswhichisabout10%ofSprint’scustomers.Virgin’sstrongbranding,VirginMobileutilisedtheparentcompany’sexistingproductsandservicessuchastravel,musicandbankingtorepresentitscontent.

Virgin’s Strategic Assets Include a Strong Brand, Channel and Relevant Content.

VirginMobileUSlaunched

OnemillioncustomersmakingitthefastestUSwirelessoperatortohitthismark

Atop10USwirelessprovider

2006AdjustedEBITDAofUSD47.9million

J.D.PowerandAssociateshighestprepaidcustomersatisfaction

ExceedsUSD1billioninannualrevenues

Secondyearrunning,J.D.PowerandAssociateshighestprepaidcustomersatisfaction

VirginMobilelistedinNYSEas“VM”

5.1millioncustomers

FinancialYear2007AdjustedEBITDAofUSD95–USD100million

July2002

November2003

March2004

January2006toDecember2006

August2006

December2006

August2007

October2007

December2007

January2007–December2007

Brand-Oneofthemostrecognisedbrandsinyouth segment-Youthappeal-People’schampion

Distribution-Sellsproductsthroughdirectdistributionchannels consistingofitswebsiteandcustomercarecenter, aswellasthird-partyretaildistributionchannels

Content-Music,travelandentertainment-VirginMobileSugarMama-serviceenhancement andmobilebyviewingadvertisementsfromvarious businesspartners

Virginbrandmorepowerfultoconsumersthanincumbentcarriers

Moreretaildistributionpointsthananycarrier

Contentwhichrepresentsfun(entertainment)andutility(travel)

Month/Year Market Events

Note: EBITDA is Earning Before Interest, Taxes, Depreciation and AmortisationSource: Adapted from “Technology, Telcom and Internet Conference 2008” by Virgin Mobile, February 2008

Source: “MVNO Opportunities for Software and Information Companies”, www.siia.net, March 2002

Developments of Virgin Mobile

20 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

-Sprintcontrastto2027-Near-ownereconomicswithlimitedcapex-Accesstocurrent/futuretechnologies-Nationwide

-MVNO-heavyapproach-Ownthecustomerexperience-Real-timebilling/pricing/promotions

-Worldclassyouthorientedbrand-LeverageoverUSD350millioninglobalannualspend-Lowercustomeracquisitioncosts-Brandlicenceto2027

-49%ofnewcustomersareovertheageof34-63%areemployed-88%payforsomeoralloftheirservices-Customerrace/ethnicitymirrorsUSpopulation,exceptHispanics

-Leadingproviderinhigh-growth,no-contractmarket • BroadNationalAppeal-ResilientMVNObusinessmodel • Lowfixedcoststructure • Abilitytocompeteinvaryingprice/economicsenvironment • Strongcashflowmanagement-Trackrecordofconsumer-driveninnovation-StrongVirginbrandequity-Primiernationalretaildistribution-Highestcustomersatisfactionintheprepaidindustry

Network

Infrastructure

Brand

ValueProposition

SustainableCompetitiveAdvantage

MVNO Business Model

Source: Adapted from “Technology, Telcom and Internet Conference 2008” by Virgin Mobile, February 2008

Virgin Mobile MVNO

Factors to Avoid

BythelooksofthenumbersofMVNOscomingintotheworldwidemarket,therehasnotbeenaslowdowninthedevelopmentsandprogressofMVNOindustryoverall.Nevertheless,therearefactorstoavoidforMVNOs.OurfindingsidentifiedthatabasiclackofcustomerbasereducesthesuccessofMVNOtostaycompetitiveinamarket.

FindingtherightMNOpartnershipcanalsomakeorbreakanMVNOcompany.VirginMobileconsidersthefollowingtobebadlyconceivedfactors12:

1.MVNOstargetcustomersthatcarriersthemselvesarefindingithardtoget;2.Launchofanot-very-distinctiveproductpropositionthatfocusesonallthesamethingsthatcarriers themselvesareoffering;3.Buildsexpensivenewproductplatformswithloadsofcapexandopex;4.Ignoresbasicretailingsuchasbigmedialaunchingwithnoorlittlestoreavailability;5.Acquirescustomerexpensively;and6.Getsdistractedbythe“high”ARPUthatpeoplewillspendavastamountofmoneywithyourservice.

12 “Amol Sarva: How to Make an MVNO Work” by Sillicon Alley Insider, October 2007

21MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

Global Current and Expected Growth

Oflate,thenumbersofMVNOsaregrowingsteadilyworldwideespeciallywithmoreassignmentsofthirdgenerationmobilelicences.Manyoperatorshavearticulatedkeeninteresttoenterthismarket,ledbycountrieslikeNetherlands,Belgium,Germany,UK,SwedenandUS.

Number of MVNOs

In2005,therewereapproximately200plannedoroperationalMVNOsworldwide14.ByJune2006,BlycroftPublishingestimated230activeMVNOs15.AccordingtoconsultancyfirmTakashiMobile,byearly2007therewereapproximately360plannedoroperationalMVNOsworldwide.

Interestingly,amplyfundedorwell-brandedstartupslikeMobileESPN,DisneyMobileandAmp’dhavenotsustainedbusinessformorethan3years.Eachhasincurredsomeoftheabovefactors.AsummaryofmorefactorstoavoidisinAppendix1.

Overall, the changing landscape of thetelecommunication industry poses challenges tooperators, especially later start-ups in the MVNOindustry. Somerealities in today’smarketareasfollows13:

1.As competition in the wireless industry intensifies and market gets more saturated, innovation for product differentiation may becomescarce;

2.Subscriber acquisition can be already high, fuelledbycheaperavailablehandsetsinmarket otherthatthoseMVNOcanprovide;

3.Strongbrandcompetitionno longerguarantees success. However, affinity by a group of customerbasetoaparticularbranddoesexist. Monetising brands may not be as simple as it

looks,forexampletheMVNOs,MobileESPNand DisneyMobile;and

4.The youth market is generally lacking purchasing power and premium content approach is elusive. To them paying for content isunnecessarywhen thesamecontent is obtainable at no additional cost from other channelslikebroadbandortelevision.

While successful MVNOs like Virgin Mobile orTescoMobile are able to sustain their businessesfor a longperiod in the industry, replicating theirbusinessmodelmay be elusive for others due tomanydifferencessuchastimingoflaunch,appetiteofconsumersorcontextualchallenges.

Overall, therearenoshortcutstosuccess.Rather,there is much required excellent ground work,solid planning, and ample access to capital,good communication skills as well as a strongmanagementteamthatissensitivetomarketandconsumerbehaviourchangesandisnimblemindedenoughtobeproactiveorreactiveaccordingly.

GLOBAL AND REGIONAL PERSPECTIVE OF MVNO INDUSTRY

13 “The Retske Report: New Strategy for Winning, Surrender”, www.prepaid-press.com, May 200614 “Mobile Virtual Network Operators (MVNOs) (Special Reference to Regulatory Environments)” insert-research paper submitted to the University of Manchester, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=108726215 http://www.mvno.eu

22 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

Asof2006,thespreadofnumbersinMVNOrelationshipstotal345inwholesalerelationships,189MVNOand156ESPs.NotethattheseareonlyourtotalsbasedontheselectedcountriescitedinthetablebelowtoobtainaflavouroftheMVNOmarketscenarioworldwide:

Australia

Austria

Belgium

Canada

Denmark

Estonia

Finland

France

Germany

Hong Kong

Ireland

Latvia

Liechtenstein

Lithuania

Luxemborg

Malaysia

The Netherlands

New Zealand

Norway

Philippines

Poland

Portugal

Russia

Singapore

Slovenia

South Africa

Spain

Sweden

Switzerland

Taiwan

Ukraine

United Kingdom

United States

TOTAL

29

3

29

6

14

3

10

13

32

6

4

1

1

2

1

2

36

1

13

1

5

3

2

1

2

1

4-5

23

5

2

2

27

60

345

1

1

3

6

4

2

5

9

13

0

3

0

1

2

1

2

6

1

12

1

3

3

2

1

1

1

3-4

20

3

2

2

24

50

189

28

2

26

0

10

1

5

4

19

6

1

1

0

0

0

0

30

0

1

0

2

0

0

0

1

0

1

3

2

0

0

3

10

156

* All figures as of January 2006** Wholesale Relationships - Service providers that purchase wholesale mobile minutes from a network operators and resell to end-users*** MVNOs - Mobile Service Providers having their own switching infrastructure**** ESP – “Enchanced” Mobile Service providers having more branded customer interfacesSource: “Incentives to License Virtual Mobile Network Operators (MVNOs)”, http://web.si.umich.ed; www.takashimobile.com/mvno.html

Number of MVNOs in Selected Countries*

Country Wholesale Relationships** MVNOs*** ESPs****

23MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

Number of MVNO Subscriptions

WhileMVNObusinessmodelsfaceclaimsofdifficultyinsustainability,studiesbyInformaTelecoms&MediarevealtheoverallglobalperformanceofMVNOstohaveimprovedwithanincreaseof23%foratotalMVNO subscription at the end of 2007 comparedwiththeendof2006.TheseimprovementscomeastheWesternEuropeMVNOmarketstabilisedwithmany of thoseMVNOs launched during the latterpartof2005and2006maturingandexperiencingsustainabilityover200716.

Additionally, subscriptions to MVNO services willreach 150 million worldwide by 2013 with 58%coming from outside Western Europe. This willrepresent3%ofthetotalglobalmobilesubscriptionsaccordingtonewresearchfromInformaTelecoms&Media. Juniper Research forecasted subscriberstoMVNOsataround93millionin2006globallyto352millionby2012.Newconsumersareexpectedto continue to be hungry for low-cost voiceservices(USD42billionby2012)buttheyarealsoincreasinglylookingformobileentertainment,suchasmusicandgames.

MVNO Revenues

Worldwide MVNO revenue on the other hand, isexpectedtopoststeadygrowth.IN-StatforecastedrevenueforMVNOworldwideatnearlyUSD40billionin2009andmorethanUSD60billionbytheyear2010.Onasimilarnote,JuniperResearchpredictedrevenues for MVNOs to increase from USD15.4billionin2006toUSD67.4billionby2012.Ofthis,USD42billion(62.3%)willbefromvoiceservices,withtheremainderbeingaccountedforbymobiledataservices,mainlymusicandgames.

70

60

50

40

30

20

10

0

90,000

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

90,000

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

MVNO Revenues Worldwide 2004-2010

Worldwide MVNO Revenues Forecast by Region(USD million) 2006-2012

MVNO Revenues Forecast Voice/Data Split(USD million) 2006-2012

2004 2005 2006 2007 2008 2009 2010

Revenues(USbillions)

Source: IN-Stat

Source: Juniper Research Limited

Source: Juniper Research Limited

2006

2006

2007

2007

2008

2008

2009

2009

2010

2010

2012

2012

Africa&MiddleEast

RestofAsiaPac

IndianSubContinent

FarEast&China

EastEurope

WestEurope

SouthAmerica

NorthAmerica

MVNODataRevenues

MVNOVoiceRevenues

2006

93millionglobalsubscribers

2013

150millionglobalsubscribers

2012

352millionglobalsubscribers

2012

150millionsubscribers

Source

InformaTelecoms&Media

JuniperResearch

PyramidResearch

MVNO Service Subcription Forecast

Summary of Forecasts

16 “Global and Regional MVNO Market Development” by Informa Telecoms & Media, July 2008

24 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

2009

USD40billion

2006

USD15.4billion

2010

USD60billion

2012

USD67.4billion

2012

USD30billion

Source

IN-Stat

JuniperResearch

PyramidResearch

MVNO Revenue Forecast

Summary of Forecasts (continued)

Inconclusion,mostanalystsexpectMVNOssubscriptionsandrevenuestobeonuptrendinthecomingyears,albeitinvaryingdegreesofgrowthinvariousmarkets.

Global Market Readiness for MVNOs

Themobiletelecommunicationindustryisbuoyedbytherelativelyfastchangingdevelopmentsandevenparadigmshifts.TrendsthatindicatethelikelihoodofmarketreadinessforMVNOs,therebypropellingorpromptingMVNOsbusinessesareasfollows:

Regional MVNOs Trends

Themarketplace saw the appearance of many leading MVNOs with various MVNOs businessmodelsespeciallyinbrand-led,niche-focusedMVNOs.MostsuccessfulMVNOshaveshownthemobileindustryhowtocapitaliseonnichemarketsandexploitthe“longtail”.WhilemostleadingMVNOsarelocatedintheUK,EuropeandtheUS,thereisanincreasingnumberofMVNOsemerginginAsia.

a.Mobilemarketsaregettingsaturated. Overthepast20years,themobilemarketsare reachingorhavereachedsaturationormaturity, especiallyinvoiceservices,mostlyindeveloped countries. Thus, these are poised for data services take-up such as MVNOs which can sustaincustomerloyaltyandreducechurnorto increasedifferentiation;b.The mobile telecommunication industry is moving towards 3G. 3G provides opportunities for existing MVNOs to increase their data revenues;c.Convergence emerging in cross industry productsandservicesinthewirelessspace;d.DecliningARPU;e.Increasingsubscriberacquisitioncost;andf. The need for segmentation increases opportunities.

MVNO Revenues Worldwide 2004-2010

Penetration(%)

Time

Europe

Americas

VNOASPSP

Branding&Segmentation

Fewmajorplayers

100%

50%

Saturation Consolidation

Asia

Source: Adapted from “Mobile Virtual Network Operators and Enablers in Challenging Market Environment – Market Assessment and Study” by Logan Orviss International Deutchland GmbH

25MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

UK MVNOs

MVNO Fast Facts*

United Kingdom

Intermsofsubscribers,UKhasoneofthelargestmarkets formobile services in Europe. In 2007,there are 73.4million totalmobile subscribers inUK and it is expected to grow to 76.7million in201017. Whereas the wireless penetration in theUKmarket has surpassed 100% since 2003, andreachedapenetrationrateof117%bymid-200718,itisexpectedtoreach121.6%in201019.

Duetothehighmobilepenetrationrate,thenumberofMVNOsintheUKhasincreasedrapidly.Ithas

•Countries with the most MVNOs: Netherlands (43),Belgium(38),Germany(31)andFrance(22)•Most active Host Network Operators (HNOs): KPN in Netherlands (35),BaseinBelgium(31) andE-PlusinGermany(11)•Most active MNO Groups acting as HNO: T-Mobile (19 MVNOs in 3 countries)andOrange(15 MVNOsin5Countries)•Country with the highest MVNO market share: Netherlands with 3.05 million customers servedbyMVNOsin1Q2007•Largest MVNOs by number of subscribers: Debitel (roughly 13 million in Germany alone)and VirginMobile(roughly6millionintheUKalone)•Fastest growing new MVNOs: Tesco Mobile in the UK(500,000customersduringfirst12months, +1.5milliontoday),M6inFrance(400,000customersinfirst12months,+1.0milliontoday),Virgin MobileinFrance(300,000customersinfirst10months),NRJMobileinFrance(300,000customersin 12months,+400,000today)

* from FRiENDi mobile MVNO market research of 18 countries in Western Europe, with a total of 399 million peopleSource: FRiENDi Mobile, 27 August 2007

oneofthebiggestMVNOmarkets intheworldbyvolume of customers, with more than 6 millionMVNOcustomersbytheendof200420. UK’sandEurope’sfirstMVNOwasVirginMobile,whichwaslaunchedin1999.

Bymid-2005, there were sevenmajor MVNOs inthemarket,outofanestimated53MVNOsacrossEurope as a whole. Of the UK operators, Virginhas been the most notably successful21, followedbyTescoMobile, the second largestMVNO inUK.Among themorenotableUKMVNOsarenoted inthetable:

•Nocontracts.•Nohiddenfees.•Historyofbrand extension.

•Offerscustomers value,simplicityand choice,alongwith supermarketstyle offersandthe chancetoearn Clubcardpoints whenbuying handsetsandcall time.

•Createsvalue andprofitabilityin cellphoneservice industry.•Targetsmarketages 15–29years.•Toservetheyouth marketinaway theyhavenever beenservedbefore.

•Leverageits competitive advantageof distributionand strongbrand associationby havingbranded pre-paidphones onsaleinstores andthroughtesco.com.

DiscountMVNO

DiscountMVNO

Youthandyoungadults

Loyalandpriceconsciouscustomers

T-Mobile

O2

1999

2003

VirginMobile(Prepaid)

TescoMobile(Prepaid)

MVNO (Service Plan)

Launch Year

Hosting MNO Objective Differentiating

FactorsTarget

SegmentsMVNO

Classification

17 http://www.reuters.com/article/pressRelease/idUS110953+25-Jan-2008+BW2008012518 “Mobile Virtual Network Operators (MVNOs) in Israel – Economic Assessment and Policy Recommendation”, www.moc.gov.il, August 200719 http://www.reuters.com/article/pressRelease/idUS110953+25-Jan-2008+BW2008012520 “The Future of MVNOs in the 3G Era” by Analysys, 200521 “The Communications Market” by Ofcom, February 2006

26 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

UK MVNOs (continued)

•Servicesincludea mobileVirtual PrivateNetwork service,Business Circleand Conferenceon Demand,aswell asnewtariffsto givelargeandsmall businessesgreater freedomtostructure pricesaccordingto theirneeds.

•Ads,promotionsand marketingmessages inexchangeforfree calls/voiceminutes andtextmessages.

•Supportcustomers byownlanguage customerservice beforeandafterthe purchase.

•OnelowpriceforUK calls.•Onelowpricefor texts.FreeSIMcard.•Nocontract.•Nomonthlycontract.•Nominimumspend.

•Providingfixedmobile convergenceutilising itsMVNOcapabilities.

•Builtaservicearound whatyoungpeople wantandneed–free communication,ease ofuseandrelevant messagesfrombrands andallowsadvertisers toreachyoungpeople usingtheonlychannel thattheycarrywith themeverywhere.

•Acompetitiveway forpermanentlybased immigrantsintheUK, andmigrantvisitors andworkerstotheUK, tousetheirmobilesto calloverseas.

•Pre-paidservices thatwillbeavailable toIkeaFamilyLoyalty programmemembers andallIkeastaff.

LifestyleMVNO

Ad-fundedMVNO

EthnicMVNO

DiscountMVNO

Corporatemarketandhighusageresidentialcustomers

16yearsoldto24yearsold

UKimmigrantsandmigrantworkers

MembersofIkeaFamilyLoyaltyprogramme

Vodafone

Orange

Vodafone

T-Mobile

2004

2007

2007

2008

BTMobile(Prepaid)

Blyk(Prepaid)

LebaraMobile(Prepaid)

IkeaMobile(Prepaid)

MVNO (Service Plan)

Launch Year

Hosting MNO Objective Differentiating

FactorsTarget

SegmentsMVNO

Classification

Source: Adapted from various websites

However,eventhoughtherehasbeensoundsuccessinEurope,therewasanabundanceofMVNOlowcostdiscounterswhichareputtingdownwardpressureonprices.Onasimilarnote,UKisexperiencingthistrendwheremanyoftheMVNOsalsoarelowdiscounters.

United States

In2004and2005,traditionalmarketsegmentsareapproachingmaturity,asmobilepenetrationgrowstohighlevels.Already,theUSwirelessmarketsawanumberofMNOconsolidations,forexample,CingularWirelessmergerwithAT&TWireless,andSprint’smergerwithNextel.ThishasresultedinfournationalMNOs,VerizonWireless,CingularWireless,SprintNextelandT-Mobile22.

Intermsofsubscribergrowth,analysiscompany,SNLKaganprojectedmobilepenetrationintheUStosurpass100%by2013.ForecastisforthetotalUSwirelessservicerevenuetoincreaseata5%CAGRfrom2007to2017,fromUSD155billionthisyeartoUSD253.6billionin2017.

22 “Mobile Virtual Network Operators: Blessing or Curse? An Economic Evaluation of the MVNO Relationship with Mobile Network Operators” by NERA, 2006

27MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

Notknowntomany,theMVNOsorcellularresellersastheyareknown,havebeenaroundintheUSforaslongastherehasbeencellularservice.ManyofthecarriersthatexistwereresellersbuttherigidwholesalepricingstructureofferedbycarriershaspreventedtheMVNOsfromofferinginnovativepricingandproductdifferentiation.

Inthemid90s,thethenemergingcarrierssuchasSprintPCSandCingularWirelesscitingmoreopenattitudetowardsresellerchannelsstartedtoworkcollaborativelywithresellers. Initially,mostmobileoperatorsintheUSlackedenthusiasmforprepaidwireless,whencomparedtotheircoreandverylucrativepostpaid, contractbusiness. In contrast, prepaidgenerated lessARPUand facedhigher churn rates.However,withincreasedcompetitionandmoresaturatedmarketplace,MNOshadtorelookthewirelessprepaidopportunitytoreapthishistoricallyunderservedmarketsegment.

Overtheyears,withreasonablesuccessofTracfone,VirginMobileandBoostMobile,thenumberofMVNOsintheUShasgrownrapidly.In1999,therewerelessthan500,000intheUS,representinglessthan1%ofthemobilemarket.By2010,thenumberofMVNOsubscribersisexpectedtogrowto25million.

In2005,thetotalMVNOrevenuewasUSD4.6billionandby2010,NERAprojectsMVNOrevenuestobeUSD29.6billion.By2006,thereareapproximately40MVNOsoperatinginthecountry,afterthefirstUSMVNO,Tracfonewaslaunchedin1996.Tracfoneitselfhassincegrowntoapproximately10millioncustomersandnearlyUSD200millionEBITDAin2007.AselectionofUSMVNOsisshowninthetablebelowon“USMVNOs”:

Source: SNL Kagan, a division of SNL Financial LC estimates

Source: Nera Research Source: Nera Research

350

300

250

200

USCellphonePenetration

(million)

2006

77.4%%Penetration 84.3% 88.3% 91.7% 94.6% 96.9% 98.5% 100.0% 101.2% 102.3% 103.5% 104.2%

233.0

256.0

300.9 303.8 306.8

WirelessSubsEOY

USPopulation

309.8 312.8 315.8 318.9 322.0329.0

328.3 331.6 334.8

271.0

284.0296.0

306.0314.0

100%Penetrationin2013

322.0 325.2

336.0343.0

349.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

50

40

30

20

10

0

225

200

175

150

125

100

75

50

25

0

MVNOSubcribers TotalMobileSubcribers Percentage

14

12

10

8

6

4

2

0USMVNOLaunches(Cumulative)

Subscribers(million)

Percentage

1996

1

1997

1

1998

2

1999

3

2000

3

2001

3

2002

8

2003

10

2004

17

2005

30

2006201020092008200720062005200420032002200120001999

43

US MVNO Launches, 1996 - 2006 US MVNO Subscriber as Percentage of Mobile Subscribers, 1999-2010

28 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

US MVNOs

•Offersservicesunder twobrands: TracFoneandNet10.•Offersprepaid servicesonboth CDMAandGSM networks.•Doesnotuse contractsnordoesit conductcredit checks.

•OffersPay-as-you- goandmonthly planswithno contractrequired.•Strongfocuson music,ringtone dealsandspecialist youthhandsets.

•OffersbothCDMA andiDENphones.•OffersPush-to-Talk (PTT)serviceor walkie-talkiestyle communications throughMotorola phonesonly.•Monthlyuserscan choosefromthree plans,eachwith unlimitedcalling. Planswithunlimited messagingand Internetare availableaswell.

•Offeringpostpaid wirelessservices toresidentialand businesscustomers aspartofa quadrupleplay.

•Servicesare deliveredprimarilyin Spanish.

•Tomakecellphone serviceavailableto everyonewithout theneedfora contractorahigh creditrating.

•Tomakeprepaid servicesomething coolandsocially acceptable.

•Developingand distributingwireless communications productsforthe youthmarket.

n.a.

•Providingpay-as- you-govoiceand dataaccesswith anemphasison internationaland Spanish-language contentandservice.

DiscountMVNO

DiscountMVNO

LifestyleMVNO

DiscountMVNO

EthnicMVNO

Lowerincome,lower-volumecustomers,seniorcitizens,casualcellphoneusers,parents,safetyusers.

Youthmarket

Youthmarket(14yearsoldto34yearsold),urbandemographic,Hispanicmarket

Residentialandbusinesscustomer

Hispanicmarket

VerizoneWireless,Cingular,AT&TWirelessandAlltel

SprintNextel

SprintNextel

VerizonWirelesssince2008(previouslySprintNextel)

SprintPCS

1996

2002

2002

2003

2005-ceasedoperation

Tracfone(Prepaid)

VirginMobileUSA(Prepaid)

BoostMobile(Prepaid)

QwestWireless-Postpaid

Movida(Prepaid)

MVNO (Service Plan)

Launch Year

Hosting MNO Objective Differentiating

FactorsTarget

SegmentsMVNO

Classification

29MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

US MVNOs (continued)

•Offersentertainment- focusedDisney- themedcontent. Child-andparent- focusedservicessuch asFamilyMonitor,to helpparentscontrol thefamily’swireless spending.FamilyAlert, forsendingpriority messagestotheentire familyatthesame time.CallControl, toenableparentsto controlthedaysand timesthatchildren’s phonescanbeused andFamilyLocator,a Location-BasedService (LBS)thatusesGPS toenableaparent topinpointonamap thelocationofachild’s phone.

n.a.LifestyleMVNO

Familieswithkids

Sprint2006 -ceasedoperation

DisneyMobile-Prepaid

MVNO (Service Plan)

Launch Year

Hosting MNO Objective Differentiating

FactorsTarget

SegmentsMVNO

Classification

Asia

Although the majority of countries in Asiapride themselves as having one of the fastestdevelopmentsinthemobileandtelecommunicationnetworks,themarketforMVNOsisstillatnascentstage.MVNOsdevelopmentisnotasvisibleastheirEuropean counterpartswhereMVNOs therehavebeengainingalotoftractionoverthepastyears.

According to a report by Yankee Group, MVNOpenetrationislessthan1%ofthetotalsubscribersin Asia Pacific by the end of 2006. The slowpenetration is attributable to amongst others,regulatorypolicieswhichpreviouslyhavenotbeenveryopenandsupportivefornetworkaccess.Otherchallengesincludehighpenetrationlevels,lowpricesanddifficultyincompetingonValueAddedServices(VAS)asprepaidusersusuallydonotconsumeVASasmuchaspostpaidusers.

The failedattemptsbyVirginMobile inSingaporeafterninemonthsofoperationduetohighwholesalepricing and Shell in Hong Kong due to lack ofcustomerbasearegoodexamples.However,theseexampleshavenotdamperinvestors’anticipationinventuringintotheMVNOmarket.InvestorsinAsia

arestillhopeful indrawing inspirationfromhighlysuccessfulMVNOsinEurope.

With a growing large share ofmobile terrain, anoverallaverageof33%ofmobilepenetration23andexpectedpenetrationratejustover50%by201024,theproliferationofMVNOisexpectedtomatureinAsianmarketinthenearfuture.ErnstandYoungreported there being renewed interest in MVNO,particularly in the two most highly penetratedmarketsofSingaporeandTaiwansince2006. Todate,HongKonghasthehighestMVNO-penetratedmarketinAsiawith720,000customers,representing7.5%HongKongmarketpenetration25. By2007,the trend has spread across other AsianmarketslikeSouth,Korea,Japan,ThailandandMalaysiaaswell.

Experiences drawn from other countries indicatethatMVNOsthrive inmorematureand liberalisedmarketsasopposedtoemergingmarkets,especiallythose with restrictive regulatory regime. Hence,there are different opportunities to stimulatecompetitionviaMVNOentryincountriesacrossAsiaduetomarketmaturityandregulatorystancetaken.When markets are more mature (higher marketpenetration),MVNOsareseenmorepertinent.

23 “Asia Calling – Taking on the Rising MVNO Wave in Asia, Global Telecommunication Centre” by Ernst and Young, 200724 “Asia Phone Penetration to Reach 50% by 2010” by Cellular News, http://www.cellular-news.com/story/17162.php25 “Asia Calling – Taking on the Rising MVNO Wave in Asia, Global Telecommunication Centre” by Ernst and Young, 2007

n.a.: not availableSource: Adapted from various website

30 MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

Source: “Asia Calling, Taking on the Rising MVNO Wave in Asia” by Ernst & Young, 2008

Asia MVNOs

MVNO Activities No MVNO

•Comprehensiveand largestrangeof mobilephonesand plansinAustralia.

•OfferingIslamic contentdeliverysuch asprayertimetables.

n.a.

n.a.

n.a.

n.a.

•Theworld’sfirst text-basedmoney remittanceservice, Bibleverses,24-hour customerservicefrom fellowFilipinos,make long-distancecallsto thePhilippinesand textmessagesfor around50%lessthan theywouldotherwise payonalocalHong Kongnetwork.

•Providingquality customerservice andofferingthe bestpossibleprices.

•Connectingglobal ethniccommunities, withouttheexcessive costs.•Providingethnic- orientedMVNO offeringlow internationalcalls.

n.a.

n.a.

n.a.

n.a.

•ProvidingFilipinosin HongKongwith accesstothesame Smartmobile servicesandcontent theycanuseinthe Philippines.

Blue-collarworker

Ethnicmarket

n.a.

n.a.

n.a.

n.a.

Ethnic/affinitygroup–overseasFilipinoworkers

VodafoneAustralia

VodafoneAustralia

FarEasTone

FarEasTone

FarEasTone

TelekomMalaysia

ThePhilippinesLongDistanceTelephoneCompany

2007

2005

2006

2007

2007

2007

2004

CrazyJohn

SlimTel

Arcoa

PresidentChain

StoreCorp(7-Eleven)

FamilyMart

Samarti-Mobile

PLDT‘1528Smart’

Australia

Taiwan

Thailand

HongKong

MVNO (Service Plan)

Launch Year

Hosting MNO Objective Differentiating

FactorsTarget

SegmentsMVNO

Classification

ExamplesofsomeofAsiaMVNOsareasperthetablebelow:

160

140

120

100

80

60

40

20

0

MobilePenetration

(%)

Singapore

HongKong

NewZealand

Australia

Taiwan

SouthKorea

Mal

aysia

Japan

Thailand

Philippines

China

Indonesia

Vietnam

Dynamic MVNO Activities in Mature Mobile Markets, June 2007

31MobileVirtualNetworkOperators(MVNOs)-TheRedefiningGame

Asia MVNOs (continued)

n.a.

•Nomonthly subscriptionfee. Instead,customers willpayaperhalf- minutepriceforall calls,oraone-off paymentpermonth forunlimitedcalls.•Toofferservices andhandsetsfully usableinthemobile environment,similar tothecurrentPC environmentathome oroffice.

•High-speed nationwidemobile environment.•International roaming.•UniqueMVNOfee plan.•Fixed-rateplan, Packetshareplan, andConnectionshare plan.•Secure,stablemobile communications environment.

•Subcriberscan receivea“phoneand fly”rebateofupto 15centsinthedollar ontheirtelcobills, whichtheycanspend ontravelproducts offeredthrougha sistercompany.

n.a.

n.a.

•Aimsatstablemobile bankingserviceto protectcustomers’ dataasdirectly administeredbythe operatingbanks.

•Providing“high-speed datacommunications bybuildingmobile broadbandservices supportedbythe latest“HSDPA”(High- SpeedDownlink PacketAccess)andIP networktechnologies.

•Providing comprehensive solutions(including one-stopcorporate networkconstruction andoperationthat includesmobiledata communications)for businessesemploying mobilebroadband.

n.a.

n.a.

n.a.

n.a.

n.a.

Corporatebusinesscustomers

Smallandmediumsized

corporateusers

Smallandmediumenterprisebusinesscustomers

Customerswhodonotwanttobetiedupwithlongtermcontracts

SKTelecom

NTTDoCoMo

NTTDOCOMO(3GFOMAnetwork)

VodafoneNZ

TelecomNZ(CDMA)

VodafoneNZ

2007

2008

2008

2007

2007

2008(notlaunched)

KoreaFinancialTelecom&ClearingsInstitute

EMobile

IIJMobile

M2Telecoms

TelstraClear

Black+White

Korea

Japan

NewZealand

MVNO (Service Plan)

Launch Year