CONSTRUCTING AN ECONOMIC COMPOSITE INDICATOR · PDF fileConstructing an Economic Composite...

14

CONSTRUCTING AN ECONOMIC COMPOSITE INDICATOR FOR THE UAE 1 ASSIL EL MAHMAH Research and Statistics Department June 2017 1 The views expressed in this paper are those of the author and should not be interpreted as those of the Central Bank of the United Arab Emirates.

Transcript of CONSTRUCTING AN ECONOMIC COMPOSITE INDICATOR · PDF fileConstructing an Economic Composite...

CONSTRUCTING AN ECONOMIC COMPOSITE

INDICATOR FOR THE UAE1

ASSIL EL MAHMAH

Research and Statistics Department

June 2017

1 The views expressed in this paper are those of the author and should not be interpreted as those of the Central Bank

of the United Arab Emirates.

2

Constructing an Economic Composite Indicator for the UAE

__________________________________________

Abstract

In order to assess the economic activity for the UAE, policymakers examine different economic

variables that could provide them high frequency information about the economic developments.

However, since the UAE GDP, the main measure of the economic activity, is available only on

an annual basis with a considerable publication delay, policymakers have to make decisions with

a large amount of information obtained from different sources.

To overcome this problem, this paper proposes to construct an Economic Composite Indicator

(ECI) that can closely track the economic activity of the UAE on a quarterly basis. Given the

absence of a reference variable, the Principal Component Analysis (PCA) is the most appropriate

method to calculate this indicator. This approach aims to extract a common factor from a group

of relevant economic series and to capture the highest level of common trend.

The results show that, the ECI reflects the economy’s historical performance since 2006 and

confirms the economic development recorded by the UAE Purchasing Managers' Index (PMI).

On an annual basis, there is a high correlation between the constructed ECI and the historical

GDP growth of the UAE. Thus, the ECI can be considered as a valuable tool for the

policymakers to provide them timely information about the development of the UAE economic

activity and an early indication of turning points.

Keywords: UAE economic activity, Composite indicator, Principal Components Analysis

JEL classification codes: C32, C51, C87, E32

3

I. INTRODUCTION

Given the increasing need to obtain an early and a clear signal about the current and future

developments of economic activity, policymakers examine different economic variables from

different sources. Nevertheless, not all economic variables are published simultaneously, with

various lags and frequencies, delaying the appropriate policy responses.

The most used tool to resolve this problem is the composite indicator, which is an aggregate

index of a large number of relevant variables reflecting the development of the economic

activity. While such indicators are widely used and well developed in all advanced economies, it

has received relatively little attention in many emerging and developing economies, because of

the lack of long historical as well as high frequency reliable data.

In the United Arab Emirates (UAE), to overcome the lack of the quarterly GDP, the Central

Bank of UAE (CBUAE) constructed an Economic Composite Indicator (ECI) to assess the

economic activity of the UAE. This is the first experience at the national level that aims to

improve the understanding of the direction of economic activity and to estimate economic

growth on a quarterly basis.

This constructed indicator could be a useful analytical and empirical tool for the policymakers

since it offers a timely clear picture about the current economic situation. The ECI has three

important advantages: first, it takes into account all important policy issues by synthesizing a

large number of economic variables, both at the national and international levels. Secondly, it

captures economic fluctuations for the UAE at relatively high frequency, compared to the

available information. Finally, it will be used to give an early indication of turning points.

This paper presents an estimation of an Economic Composite Indicator for the UAE, which aims

to provide an interesting reference for the construction of these indicators for other similar

economies and also to facilitate future research on the UAE. The remainder of this paper is

organized as follows: Section II describes the available data as well as criteria and

transformations applied in this paper. Section III gives an overview of the adopted

methodological approach, while section IV focuses on the main steps in the construction of the

ECI. The section V presents the empirical results and the interpretation of the estimated indicator

from a historical perspective. Finally, section VI concludes.

4

II. DATA DESCRIPTION

The building of the dataset represents the crucial step for the computation of the composite

indicator, since the quality of the constructed index depends highly on the quality of data. The

dataset should contain relevant variables on a quarterly basis reflecting the overall economic

activity and taking into account all important policy issues. However, the choice of the data

sample is dictated by data availability and the structure of the economy. While there are some

reliable and well-established databases for most of the advanced countries, there is no large

dataset containing a large number of macroeconomic variables for the UAE, at the requested

frequency. Therefore, the selected macroeconomic variables are collected from different sources,

in order to obtain a data set that covers a wide range of economic indicators, such as the global

economy, sectorial activity, financial markets, price trends and the money market.

To ensure objectivity throughout the selection process of most appropriate series, we have

chosen two main criteria: economic significance and statistical significance. The first

requirement is that the selected series should ensure good representation of the relevant sectors

of the economy and reflect the anticipation of future economic fluctuations. The second

requirement is the availability of long historical series on a quarterly basis, timely and easily

accessible. These variables should be highly correlated with GDP growth, with clear trends and

low volatility.

Thus, according to the two criteria and the availability of data, the final dataset consists of 14

series on a quarterly basis from 2006Q1 to 2017 Q1. It covers, as much as possible, the major

sectors of the UAE economy. It also includes some international variables that can influence the

national economic activity. The table below presents the detailed list of all variables used to

construct the ECI.

Table 1: Information on variables used to construct the ECI

Sector Variables Sources

Global Economy

• US GDP (Quarterly y-o-y, % change) International Monetary Fund

• EU GDP (Quarterly y-o-y, % change) International Monetary Fund

• Emerging market GDP (Quarterly y-o-y, % change) International Monetary Fund

• Brent oil price (Quarterly y-o-y, % change) Energy Information Administration

Financial Markets • MSCI UAE (Quarterly y-o-y, % change) Bloomberg/ MSCI

Prices • CPI (Quarterly y-o-y, % change) Federal Competitiveness and Statistics Authority

Sectorial activity

• UAE's oil production (Barrel/day) OPEC

• Industrial Production Index (IPI) (Quarterly y-o-y, % change) Statistics Centre −Abu Dhabi

• UAE airport passenger traffic (Quarterly y-o-y, % change) UAE airports

• Dubai Economic Tracker (DET) Emirate NBD / Markit

Money

• M3 (Quarterly y-o-y, % change) Central Bank of UAE

• Domestic credit (Quarterly y-o-y, % change) Central Bank of UAE

• Gross international reserves (Quarterly y-o-y, % change) Central Bank of UAE

• Real effective exchange rates Bank for International Settlements

5

III. METHODOLOGICAL APPROACH

A wide range of methodologies for estimating the composite indices have been developed over

time and used in many advanced economies, such as the weighted average method, the

regression model and the principal component approach. However, the choice of the appropriate

methodology depends highly on the quality of the data available and on the reference indicator

measuring the economic activity.

In order to construct a composite index, the first step is to determine a reference series for the

state of the economy. The main variable that more closely approximates the economic activity

and is mainly used is real GDP. According to the literature, the non-oil GDP, the non-agricultural

GDP and the Industrial Production Index (IPI) are the main reference series used in many

developed countries and international organizations for building quarterly composite indices.

Nevertheless, in the UAE, real GDP and its components are available only on an annual basis

and with a considerable publication delay, while the available (Industrial Proudction Index) IPI

provides only a partial coverage of the economy, especially with the rising share of services and

financial sector which are not taken into consideration.

Given the absence of a relevant reference variable and the lack of long historical, as well as high

frequency reliable data, the Principal Component Analysis (PCA) is the most appropriate method

to calculate this indicator for the UAE. This approach, introduced for the first time by Karl

Pearson (1901) and developed afterwards by Harold Hotelling (1933), aims to extract a common

factor from a group of relevant economic series and to capture the highest level of common

trend.

Formally, the PCA approach stipulates that for any set of variables X1, X2, X3, …, Xn, n>=1, it is

possible to create a set of variables Z1, Z2, Z3, …, Zn, n>=1 as a linear combination of the first

set. Analytically, the model can be presented as follows:

∑

Where is the coefficient of the corresponding eigenvector, to be the biggest eigenvalues of the

symmetric variance-covariance matrix of the original variables. The principal components are

ranked such that: Var( ) ≥ Var( ) ≥ … ≥ Var( ). Thus, the variation of the data set can be

described by k principal components, with k ≤ n. Therefore, with a few common factors, the

contribution of the variables to the total variance is important, especially if the original variables

are highly correlated.

In this sense, the first principal component is considered as an indicator of economic activity

since it contains the most relevant information contained in the data.

6

IV. ESTIMATION OF THE ECI

The construction procedures of this Economic Composite Indicator (ECI) consist of four main

steps (see figure 1). The first step is to determine a reference series reflecting the economic

activity fluctuation. As mentioned in section II, there is no available relevant reference variable

that can closely approximate the economic activity on a quarterly basis. To overcome this

limitation, many studies and working papers propose to interpolate quarterly real GDP from

annual real GDP. However, even if this method has often good results, there might be some

errors in the interpolation which can influence the quality and the precision of the constructed

indicator. For all these reasons, a reference series is not used in this paper.

Figure 1: Main steps in constructing this indicator

The second step is the important one, since the quality of the constructed indicator depends

highly on the quality of data. As mentioned above, according to the economic and the statistical

criteria, the final data set contains 14 time series on a quarterly basis, both at the national and

international levels, from 2006Q1 to 2017Q1.

In the third step, given the absence of a reference variable, the Principal Component Analysis

(PCA) is the most appropriate method to calculate this indicator. This approach aims to extract a

common factor from the data set and to capture the highest level of common trend.

However, the PCA is very sensitive to the unit of measurement in which the data are expressed.

For this reason, before computing the common components, each time series was normalized so

that it has a zero sample mean and a unit variance. This procedure allows the series to be

independent of any unit of measurement. This normalization is a necessary step in order to avoid

overweighting any given time series with a large variance during the estimation of the ECI.

7

The fourth step consists of applying PCA method, by using Eviews, to transform the 14 selected

variables to an equal number of orthogonal variables called principal components. Each

component contributes to the explanation of the total variance. According to the eigenvalue

criterion (Appendix Figure 2), the results obtained by Eviews shows that, there is only one

principal component to extract. The contribution of the first component exceeds 60% (see

table 2). Therefore, we can consider the first principal component as an indicator of the

economic activity of the UAE.

Table 2: Eviews output of PCA to construct the ECI

Principal Components Analysis

Sample (adjusted): 2006Q1 2017Q1

Included observations: 44 after adjustments

Computed using: Ordinary correlations

Extracting 14 of 14 possible components

Eigenvalues: (Sum = 14, Average = 1)

Cumulative Cumulative

Number Value Difference Proportion Value Proportion 1 8.740900 6.571981 0.624164 8.7409 0.6242

2 2.168919 0.873748 0.154877 10.9098 0.7790

3 1.295171 0.642080 0.092485 12.2050 0.8715

4 0.653091 0.193383 0.046635 12.8581 0.9182

5 0.459708 0.178471 0.032827 13.3178 0.9510

6 0.281237 0.131389 0.020082 13.5990 0.9711

7 0.149848 0.059669 0.010700 13.7489 0.9818

8 0.090180 0.003882 0.006439 13.8391 0.9882

9 0.086298 0.055496 0.006162 13.9212 0.9944

10 0.030802 0.009383 0.002199 13.9520 0.9966

11 0.021419 0.003501 0.001529 13.9734 0.9981

12 0.017918 0.012909 0.001279 13.9913 0.9994

13 0.005009 0.001342 0.000358 13.9963 0.9997

14 0.003667 --- 0.000262 14.0000 1.0000

Given the importance of the oil sector and its implication on the UAE economy, we construct a

second index, reflecting the development of the economic activity in the non-oil sector. To this

end, the same steps are applied, excluding the Brent oil price and the UAE oil production from

the data set (see table 3).

8

Table 3: Eviews output of PCA to construct the Non-oil ECI

Principal Components Analysis

Sample (adjusted): 2006Q1 2017Q1

Included observations: 44 after adjustments

Extracting 12 of 12 possible components

Eigenvalues: (Sum = 12, Average = 1)

Cumulative Cumulative

Number Value Difference Proportion Value Proportion 1 8.216381 6.597105 0.684698 8.216381 0.684698

2 1.619276 0.595204 0.134940 9.835657 0.819638

3 1.024072 0.616531 0.085339 10.859729 0.904977

4 0.407541 0.108029 0.033962 11.267270 0.938939

5 0.299511 0.111434 0.024959 11.566781 0.963898

6 0.188078 0.091410 0.015673 11.754859 0.979572

7 0.096667 0.039799 0.008056 11.851526 0.987627

8 0.056868 0.002330 0.004739 11.908394 0.992366

9 0.054538 0.036087 0.004545 11.962932 0.996911

10 0.018451 0.006366 0.001538 11.981383 0.998449

11 0.012085 0.005552 0.001007 11.993467 0.999456

12 0.006533 --- 0.000544 12.000000 1.000000

Thus, the results obtained by Eviews show that, there is only one principal component to extract,

according to the eigenvalue criterion (Appendix Figure 3). The contribution of the first

component is around 68% (see table 3). Therefore, we can consider the first principal component

as an indicator of the non-oil economic activity of the UAE.

V. MAIN RESULTS: ANALYSIS AND APPLICATIONS

In this section, the quarterly Economic Composite Indicator (ECI) is constructed using the

principal component analysis. The main results confirmed the historical developments observed

in the UAE economy, especially during the financial crisis 2008 (Figures 2 & 3). These results

are also consistent with the conjecture stipulating that the UAE is experiencing a slowdown amid

the continued fiscal consolidation. During the first quarter of 2017, the overall economy

expanded by 3.3%, following 3.7% in the previous quarter (Figure 2). This slowdown was due

mainly to slower rate of growth in oil production in the first quarter of 2017. In fact, oil

production increased by 3.6% in the first quarter of 2017 on a year-on- year basis against an

increase of 4.6% in the previous quarter. Moreover, the Non-Oil Economic Composite Indicator

(Non-Oil ECI), showed an improvement of the non-oil economic activity in the UAE (Figure 3),

reaching 3.1% compared to 2.8% recorded during the last quarter of 2016 on a year-on- year

basis.

9

Figure 2 : Overall ECI development (y-o-y, %) Figure 3 : Non-oil ECI development (y-o-y, %)

Source: CBUAE analysis

Therefore, this ECI can track down ongoing economic developments on a quarterly basis and

provide to the policy-makers the current situation of the UAE economy, in the absence of any

reliable information about the quarterly GDP, the main measure of the economic activity.

Moreover, given the importance of the emirates of Abu Dhabi and Dubai in the UAE economy,

Figures 4 & 5 showed the high correlation between the ECI and the GDP growth of the two

emirates, confirming the observed trends.

Figure 4: Non-oil ECI and Dubai GDP growth Figure 5 : Overall ECI and Abu Dhabi GDP growth

Source: DSC, SCAD and CBUAE analysis

In addition, the non-oil ECI is highly correlated with the Purchasing Managers’ Index2 (PMI),

the only high frequency available indicator that is commonly used to track the non-oil economy

in the UAE.

2 The Purchasing Managers’ Index (PMI) measures the performance of UAE’s companies in non-oil private sector and is derived from a survey of

400 companies, including manufacturing, services, construction and retail.

10

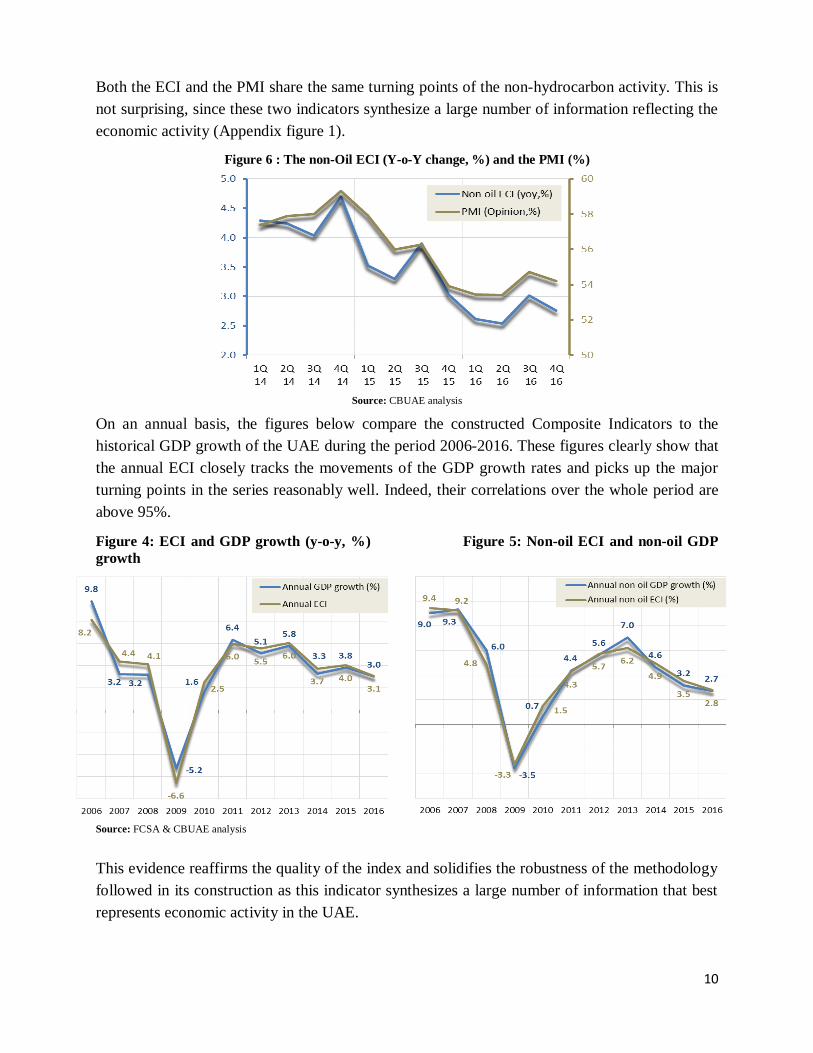

Both the ECI and the PMI share the same turning points of the non-hydrocarbon activity. This is

not surprising, since these two indicators synthesize a large number of information reflecting the

economic activity (Appendix figure 1).

Figure 6 : The non-Oil ECI (Y-o-Y change, %) and the PMI (%)

Source: CBUAE analysis

On an annual basis, the figures below compare the constructed Composite Indicators to the

historical GDP growth of the UAE during the period 2006-2016. These figures clearly show that

the annual ECI closely tracks the movements of the GDP growth rates and picks up the major

turning points in the series reasonably well. Indeed, their correlations over the whole period are

above 95%.

Figure 4: ECI and GDP growth (y-o-y, %) Figure 5: Non-oil ECI and non-oil GDP

growth

Source: FCSA & CBUAE analysis

This evidence reaffirms the quality of the index and solidifies the robustness of the methodology

followed in its construction as this indicator synthesizes a large number of information that best

represents economic activity in the UAE.

11

VI. CONCLUSION

This paper tries to construct an ECI for the UAE, in order to provide policymakers high

frequency information about the development of the UAE economic activity and an early

indication of turning points.

Based on this research, the first experiment with the ECI construction has yielded fruitful results.

We believe that the methodology adopted to construct the ECI is the most appropriate method to

calculate this indicator, taking into consideration all available data. This approach allows to

extract a common factor from a group of relevant economic series and to capture the highest

level of common trend. Thus, the constructed ECI is a useful tool, which can closely track the

economic activity of the UAE on a quarterly basis.

However, this study is still in preliminary stage due to the non-availability of the quarterly GDP

and the lack of alternative sources for evaluating economic activity. The utility and the quality of

the ECI seems promising, but could be improved if more data are available in a long-enough

time series for our purposes and if there is more information reflecting the development of

economic activity at relatively high frequency.

Going forward, quarterly estimates of the ECI will be presented in the context of the Quarterly

Review of the Central Bank on a regular basis. Revisions will be illustrated to reflect changes in

the estimate based on the most recent available data. Using the updated estimates, projections for

the year and subsequent years will be updated in the context of regular publications of the

Central Bank.

12

REFERENCES

Camba-Mendez, G., M. Kapetanios, R. J. Smith, and M. R. Weale (2001): “An automatic leading

indicator of economic activity: forecasting GDP growth for European countries,” Econometrics

Journal, 4, 56–90.

Schneider, M., and M. Spitzer, 2004, “Forecasting Austrian GDP using the generalized dynamic

factor model,”

Artis, J. M., A. Banerjee, and M. Marcellino (2002): “Factor forecasts for the UK,” CEPR

discussion paper 3119, Center for Economic and Policy Research.

Hotelling, Harold (September 1933). "Analysis of a complex of statistical variables into

principal components". Journal of Educational Psychology (American Psychological

Association) 24 (6): 417–441.

Geweke, J., 1977, The Dynamic Factor Analysis of Economic Time Series Models. Paper

presented at the Latent Variables in Socio-Economic, Amsterdam.

Bai, J., and S. Ng, 2002, “Determining the Number of Factors in Approximate Factor Models,”

Econometrica, 70(1), pp. 191–221.

Boivin, J., & S. Ng, 2006, “Are More Data Always Better for Factor Analysis?,” Journal of Econometrics, 132(1), pp. 169–194.

Cristadoro, R., M. Forni, L. Reichlin, and G. Veronese, 2005, “A Core Inflation Indicator for the

Euro Area,” Journal of Money, Credit, and Banking, 37(3), pp. 539–560.

Forni, M., M. Hallin, M. Lippi, and L. Reichlin, 2005 “The Generalized Dynamic Factor Model:

One-Sided Estimation and Forecasting,” Journal of the American Statistical Association,

100(471), pp. 830-840.

13

APPENDIX

Appendix Figure 1: The Economic Composite Indicator and the relevant variable

reflecting the UAE economy

Quarterly non-oil ECI vs MSCI Quarterly non-oil ECI vs DET

Quarterly ECI vs Credit Quarterly non-oil ECI vs US GDP

Quarterly ECI vs Brent price Quarterly non-oil ECI vs M3 growth

Source: FCSA, IMF, SCAD & CBUAE analysis

14

Appendix Figure 2: Variance Explained of the Principal Components for the ECI

Appendix Figure 3: Variance Explained of the Principal Components for the non-oil ECI