Connected World: New Material Challenges and Webinar · PDF file2001 2002 2003 2004 2005 2006...

57

Webinar Connected World: New Material Challenges and Solutions – Market Update and Outlook Wed, Sep 27, 2017 5:00-6:00 PM CEST

Transcript of Connected World: New Material Challenges and Webinar · PDF file2001 2002 2003 2004 2005 2006...

WebinarConnected World: New Material Challenges and Solutions – Market Update and Outlook

Wed, Sep 27, 2017 5:00-6:00 PM CEST

Agenda & Speakers

Introduction: By Marcel Wieland, Deputy Director Technology Development Globalfoundries

A general Materials market update and outlook

Dan Tracy, Sr. Director, Industry Research and Statistics

Trends in the Materials Market in 2017

Mark Thirsk, Managing Partner, Linx Consulting

Application requirements driving the Technology Development

Marcel Wieland, Deputy Director Technology Development Globalfoundries

Wed, Sep 27, 2017 5:00 PM - 6:00 PM CEST

Free Webinar linked to:SEMICON Europa 2017 — Materials Conference

Connected World: New Material Challenges and SolutionsDate: 15–16 November 2017

Empowering Innovation and Shaping the Value Chain

More Information and Registration

KEYNOTES:

• Juan Cordovez, Region Head, EMEA, GLOBALFOUNDRIES

• Christophe Maleville, EVP, Digital Electronics Business Unit General Manager, SOITEC

• Andreas Aal, Semiconductor Strategy, Volkswagen AG

• Makoto Momota, Research Manager, FUJIFILM Corporation

• Rozalia Beica, Global Director New Business Development, The Dow Chemical Company

A general Materials market update and outlook

Dan Tracy, Sr. Director, Industry Research and Statistics

SEMI's Outlook - Fab Investments, Equipment and

Materials ForecastsSeptember 2017Dan Tracy, Sr. Director

SEMI Industry Research & Statistics

Agenda

• Status Year-to-Date

• Overall Fab Investments

• China Investments

• Equipment & Materials Forecast

• Summary

Year-to-Date Status

Silicon Wafer Shipments-

On a very strong double-digit pace for 2017

• Globally, shipments are

up 11% year-to-date

• 200mm up double-digits

0

500

1000

1500

2000

2500

3000

3500

Europe Japan North America Taiwan Other Asia

Millio

n S

qu

are

In

ch

es

Silicon Wafer Area Shipment(Through August)

2016

Source: SEMI SMG

Semiconductor Equipment Billings-

+42.7% so far for the year

• Year-to-year basis, billings

are higher in all regions

except SEA/ROW

• Spending in Korea on a

record pace

– Billings through July are

already >$2B above

entire 2016

$0

$2

$4

$6

$8

$10

$12

US

$ B

illio

ns

Semiconductor Equipment Billings(Through July)

2016

Source: SEMI/SEAJ WWSEMS

0.0%

-2.6%

4.8%

9.9%

-0.2%

1.1%

17.0%

4.3%

-5%

0%

5%

10%

15%

20%

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2011 2012 2013 2014 2015 2016 2017F 2018F

Annu

al G

row

th(%

)

Sem

iconducto

r R

even

ue

($U

S B

illio

n)

Semiconductor Revenue Annual Growth

Semiconductor Cycles-

Revenues to reach $400 billion

Source: SIA/WSTS historical and August 2017 Forecast

2018 Semiconductor Forecasts

Gartner (Jul 17), 2.0%

WSTS (Jun 17), 2.7%

Cowan LRA (Aug 17), 3.1%

IHS Markit (Aug 17), 3.7%

IC Insights (Jul 17), 7.0%

Semico Research (Jul 17), 7.8%

Future Horizons (Sep 17), 16.0%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Overall Fab Investments

14

Fab Investments 2017 and 2018-Back to Back Record Years for Fab Investments

Billion Dollar

Spenders in 2017• Samsung

• Intel

• TSMC

• SK Hynix

• Micron

• Toshiba

• GLOBALFOUNDRIES

• SMIC

• Western Digital (SanDisk)

• UMC

• Nanya

• Sony

• Infineon

• ST Microelectronics

• Renesas

Key Fab Projects

NAND

• Samsung NAND fab in Xian and Line 18

• SK Hynix M14 3D NAND line

• Micron Fab 10X in Singapore

• Toshiba/Flash Alliance Fab 2, Fab 6 and new

R&D Center

• Intel Fab 68 in China

• YMTC (XMC) 3D NAND fab in China

Foundry

• TSMC Fab 12, Fab 14 and Fab 15

• Samsung S2 and S3

• GLOBALFOUNDRIES Fab 1, Fab 8 and Fab

11

• SMIC Beijing B2 and B3, new Shanghai

300mm fab and Shenzhen 300mm fab.

• UMC Fab 12A P5 and Xiamen fab.

$0

$5

$10

$15

$20

$25

NAND Foundry

US

$ B

illi

on

s

Fab Investments

2015 2016F 2017F 2018F

Source: SEMI World Fab Forecast, September 2017

Change 2016 to 2021

MEMS 60%

Discrete 22%

Power 19%

Analog 15%

Foundry 11%

Logic 6%

MPU 0%

Other 0%Source: 200mm Fab Outlook, July 2017, SEMI

4Q15 to 4Q21

MEMS make big leap

200mm Fab Capacity Changes by Product TypeDriven mainly by mobile and wireless, IOT, and automotive

200mm Capacity Changes by Region-China to add the most capacity, though…

Change 2016 to 2021China 48%

SE Asia 35%

Americas 15%

Japan 5%

Taiwan 5%

Europe & Mideast 4%

Korea 0%Source: 200mm Fab Report, July 2017, SEMI

Capacity for following products:

China: Foundry, Analog, Logic, and MEMS

SE Asia: Power

Americas: MEMS and Logic

4Q15 to 4Q21

China Investments

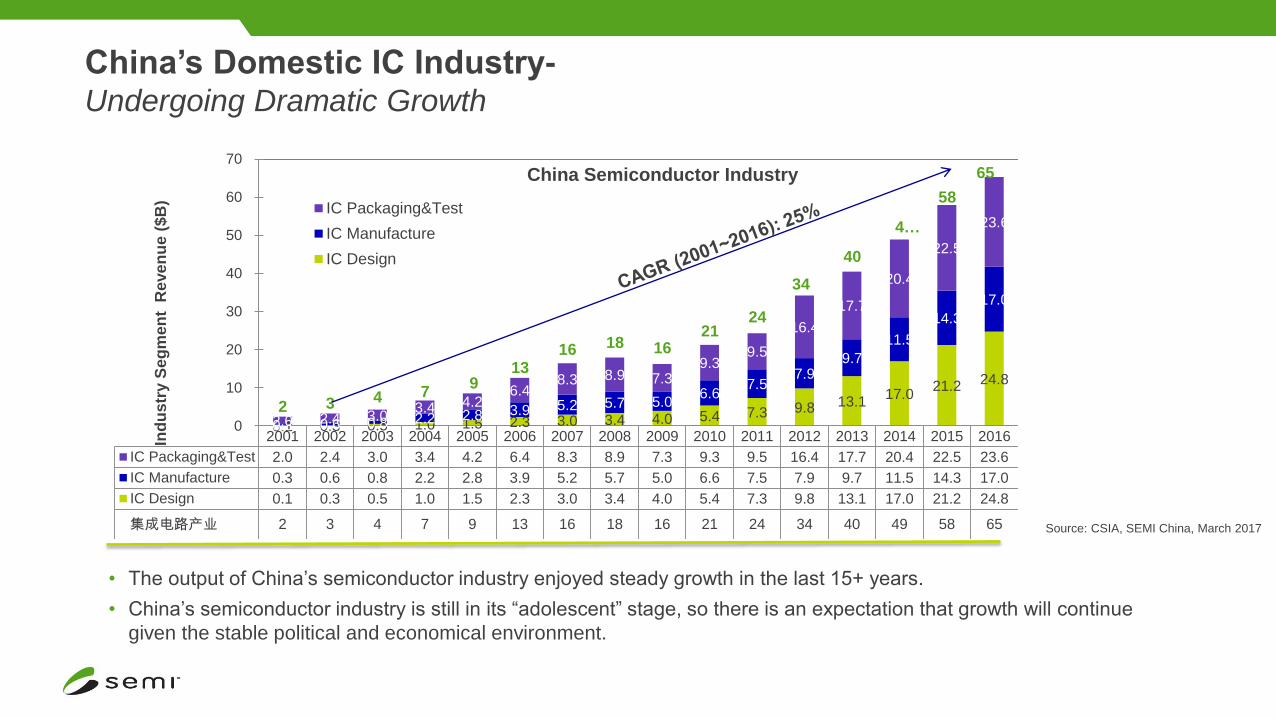

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

IC Packaging&Test 2.0 2.4 3.0 3.4 4.2 6.4 8.3 8.9 7.3 9.3 9.5 16.4 17.7 20.4 22.5 23.6

IC Manufacture 0.3 0.6 0.8 2.2 2.8 3.9 5.2 5.7 5.0 6.6 7.5 7.9 9.7 11.5 14.3 17.0

IC Design 0.1 0.3 0.5 1.0 1.5 2.3 3.0 3.4 4.0 5.4 7.3 9.8 13.1 17.0 21.2 24.8

集成电路产业 2 3 4 7 9 13 16 18 16 21 24 34 40 49 58 65

0.1 0.3 0.5 1.0 1.5 2.3 3.0 3.4 4.0 5.4 7.3 9.8 13.117.0

21.2 24.8

0.3 0.6 0.8 2.2 2.8 3.9 5.2 5.7 5.06.6

7.57.9

9.7

11.5

14.3

17.0

2.0 2.4 3.03.4 4.2

6.48.3 8.9 7.3

9.39.5

16.4

17.7

20.4

22.5

23.6

2 3 4 79

1316 18 16

2124

34

40

4…

58

65

0

10

20

30

40

50

60

70In

du

str

y S

eg

me

nt

Re

ve

nu

e (

$B

)China Semiconductor Industry

IC Packaging&Test

IC Manufacture

IC Design

China’s Domestic IC Industry-Undergoing Dramatic Growth

• The output of China’s semiconductor industry enjoyed steady growth in the last 15+ years.

• China’s semiconductor industry is still in its “adolescent” stage, so there is an expectation that growth will continue

given the stable political and economical environment.

Source: CSIA, SEMI China, March 2017

New Fab Projects on the Rise-

China leads the way

• 15 new fab projects in

China from 2017 on

• Majority of projects (10)

from China-owned entities

Surging China Fab InvestmentsWith Foundry & Memory leading

$U

SD

(M

illio

n)

Source: SEMI World Fab Forecast, June 2017

?

Key Spending Projects

2017• Intel Fab 68 - upgrade to 3D NAND

• SK Hynix C2

• UMC Fab 12X

• SMIC B2

2018• Intel Fab 68 Phase 2

• TSMC Nanjing Phase 1

• Hua Li Fab 2

• Fujian Jin Hua - DRAM

2019/2020• Tsinghua Unigroup (Nanjing) and Yangtze

Memory Technology (Wuhan)

• Samsung Xian phase 2

• SK Hynix C3

• GlobalFoundries Chengdu

• SMIC Beijing B3 and new Shanghai fab

• Hefei Chang Xin Memory

Leadframes

37%

SH Material(JPN)

Mitsui High-tec(JPN)

ASM Pacific (HK)

Shinko(JPN)

Kangqiang

Hualong

Trinity

Bonding Wire

32%

Heraeus(JPN)

Tanaka Denshi(JPN)

Nippon Micro (JPN)

Doublink

Kangqiang

Substrates

13%

Ibiden (JPN)

NanYa (TWN)

Shinko (JPN)

Samsung Electro-Mech. (KOR)

Shennan Circuits

Zhuhai Yueya

Encapsulation Resins

33%

Sumitomo Bakelite(JPN)

Henkel(GER)

Hitachi-Chemical (JPN))

Sinopaco

HHCK

Die attach Materials

23%

Henkel(GER)

Hitachi Chemical (JPN)

Sumitomo Bakelite (JPN)

Darbond

China Market

Share in 2016

Global

Companies

China

Mainland

Overview of Global Packaging Materials Suppliers in China

Source: SEMI China

Equipment & Materials

Market Forecast

2014 2015 2016 2017F 2018F

China 4.37 4.90 6.46 7.33 11.09

Europe 2.38 1.94 2.18 3.24 3.73

Japan 4.18 5.49 4.63 5.91 6.09

Korea 6.84 7.47 7.69 17.05 15.46

North America 8.16 5.12 4.49 5.10 5.71

SEA/ROW 2.15 1.97 3.55 2.87 3.17

Taiwan 9.41 9.64 12.23 12.83 10.93

$0

$10

$20

$30

$40

$50

$60

US

$ B

illio

ns

Taiwan SEA/ROW North America Korea Japan Europe China

$36.53$41.23

$54.33

$37.50

$56.18

SEMI® 2017 Equipment Forecast-

By Market Region

Source: SEMI September 2017New equipment. Totals may not add due to rounding

• Korea- record spending

year for any region

• Previous spending highs:• $12.9B N. America

(2000)

• $12.2B Taiwan (2016)

Semiconductor Fab Materials Markets

8+% Revenue Growth in 2017; 5+% Growth Forecasted for 2018

China8% Europe

10%

Japan18%

South Korea19%

North Americ

a17%

SEA/ROW5%

Taiwan23%

2016 = $24.7 billion

Region2017F

$US B

2018F

$US B

China $2.38 $2.68

Europe 2.70 2.78

Japan 4.50 4.60

South Korea 5.09 5.36

North America 4.60 4.80

SEA/ROW 1.40 1.49

Taiwan 6.23 6.59

Total $26.9 $28.3

Source: SEMI Materials Market Data Subscription, August 2017

Totals may not add due to rounding

Worldwide Wafer Fab Materials Forecast

Totals may not add due to roundingSource: SEMI August 2017

Actual Forecast

2015

US$ M

2016E

US$ M

2017

US$ M

2018

US$ M

Silicon Wafers1 $7,580 $7,650 $8,678 $9,086

Photomasks2 $3,267 $3,321 $3,462 $3,573

Photoresist $1,326 $1,450 $1,577 $1,662

Photoresist Ancillaries3 $1,796 $1,906 $2,051 $2,152

Wet Chemicals4 $1,416 $1,473 $1,531 $1,593

Gases $3,497 $3,631 $3,956 $4,152

Sputter Targets $628 $677 $707 $755

CMP Slurry & Pads5 $1,588 $1,667 $1,768 $1,835

Other/New Materials $2,853 $2,955 $3,122 $3,496

Total $23,952 $24,730 $26,853 $28,303

% Growth 3.2% 8.6% 5.4%

Semiconductor Packaging Materials Markets

China23%

Europe3%

Japan12%

South Korea13%

North Americ

a3%

SEA/ROW25%

Taiwan21%

2016 = $19.6 billion

Region2017F

$US B

2018F

$US B

China $4.65 $4.78

Europe 0.64 0.64

Japan 2.38 2.39

South Korea 2.48 2.49

North America 0.59 0.58

SEA/ROW 4.81 4.84

Taiwan 4.25 4.25

Total $19.8 $20.0

Source: SEMI Materials Market Data Subscription, August 2017

Totals may not add due to rounding

Worldwide Packaging Materials Forecast

Totals may not add due to rounding

Source: SEMI August 2017

Actual Forecast

2015

US$ M

2016E

US$ M

2017

US$ M

2018

US$ M

Leadframes $2,991 $3,038 $3,149 $3,190

Organic Substrates1 $7,779 $7,841 $7,658 $7,621

Ceramic Packages $2,082 $2,138 $2,206 $2,261

Encapsulation Resins $2,583 $2,758 $2,910 $2,987

Bonding Wire2 $2,966 $2,846 $2,809 $2,767

Die Attach Materials3 $679 $700 $749 $787

Others $258 $292 $323 $371

Total $19,338 $19,613 $19,804 $19,984

% Growth 1.4% 1.0% 1.0%

© 2017 TechSearch International, Inc.© 2017 TechSearch International, Inc.

Challenges for Large Area Panel Processing

• Economics to justify ROI– Large volume of a single part number with sufficiently large size– Not necessarily same applications as reconstituted wafer FO-WLP!!

• High accuracy placement is required, but high throughput is also needed

• Warpage (after mold and RDL) can cause tolerance issues, especially as feature size shrinks (≤10µm L/S)– Planarity issues (if die and mold are not planar, there will be line width distortion)– Warped panel makes die placement challenging and inspection difficult

• Dielectric dispense methods: dry film lamination? slot coating?

• Yield is critical– >98% are required for first RDL because compounding effect of yield can easily

diminish or eliminate savings in panel process– Mold compound is the largest source of defects (particles are generated during

thinning)– Final yield depends on quality of RDL

Summary

Summary

• 2017 will be a record setting year for the industry

– Record fab investments; All-time high for total equipment spending

– Spending in Korea will smash previous regional spending record

• Record spending forecasted for 2018

• China spending to surge in 2018 and could lead the market in 2019 & 2020

• Stronger revenue growth in fab materials compared to packaging materials

– Pricing recovery in silicon wafer market

Trends in the Materials Market in 2017

Mark Thirsk, Managing Partner, Linx Consulting

www.linx-consulting.com

Trends in the Materials Supply Ecosystem

• Mark Thirsk – Linx Consulting Inc.

SMC 2017

www.linx-consulting.com

Linx ESF

ESF 2017 Q3 Forecast

(August 2017)

2017Q1 2017Q2 2017Q3F 2017Q4F 2018Q1F 2018Q2F

MSI 2858 2978 3001 2875 2912 3183

%Change 3.4% 4.2% 0.8% -4.2% 1.3% 9.3%

%Change vs prior year 12.6% 10.1% 9.9% 4.0% 1.9% 6.9%

2,200

2,400

2,600

2,800

3,000

3,200

3,400

3,600

14 15 16 17 18 19

SEMIMSI

ESF 2017 Q3 (August)

ESF 2017 Q2 (May)

Annual Percent Change In MSI

2014 2015 2016 2017 2018 2019

11.4% 3.3% 2.9% 9.1% 7.1% 4.6%

Mill

ion

Sq

uar

e In

ches

History: Semi.org

Forecast: Hilltop Economics, LLC

SMC 2017

www.linx-consulting.com

Silicon Production Forecast

0

1000

2000

3000

4000

5000

6000

7000

2015 2016 2017 2018 2019 2020 2021

MSI by Device Type

Analog ASIC MPU DRAM NAND-2D NAND-3D

SMC 2017

Discretes not included

CAGR ‘16-’21

Analog 2.8%

ASIC 4.2%

MPU 0.4%

DRAM 6.7%

NAND-2D -22.8%

NAND-3D 58.9%

www.linx-consulting.com

300mm Annual Wafer Starts

-

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

ASIC MPU DRAM NAND-2D NAND-3D

SMC 2017

www.linx-consulting.com

≤200mm Annual Wafer Starts

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

2016 2017 2018 2019 2020 2021

Analog ASIC

SMC 2017Discretes not included

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

>= 350nm <350nm

www.linx-consulting.com

Technology trends

SMC 2017

www.linx-consulting.com

Technology Drivers

• Computing Demand

• Intelligent ubiquitous computing

• Multiple machine to machine networks for

• AI, Machine Learning, VR/AR and IOT

• Memory Bit growth

• Industry and Consumer demand increased demand to support computing growth

• Automotive

• Increase in automotive electronics

• ADAS

• Autonomous vehicles

• IOT

• Distributed sensors

• Edge cloud

• Cloud computing

• AR/VR

• Novel environments for improved performance

• Architecture change

• Scaling, equivalent scaling etc. are dead

• Silicon moving into the Third Dimension

• Process Needs

• Horizontal and vertical GAA Nanowires

• FET stacking

• Sub 10nm DRAM scaling

• Stackable storage class memory

• Dense MRAM

• Complex packaging

• 3D packaging for bit density improvement

• Hybrid FOWLP packaging

• CoWoS

• 3D x 3D Scaling

SMC 2017

www.linx-consulting.com

Device Trends

0

10

20

30

40

50

60

70

80

90

100

04 06 09 12 14 17 20 23 25

nm

Device Analysis

Logic

DRAM

2D NAND

3D NAND

Expon. (Logic)

Expon. (DRAM)

Expon. (2D NAND)

SMC 2017

Logic & DRAM - Min Metal 1/2 pitch (nm)2D NAND - Uncontacted poly 1/2 pitch (nm) 3D NAND Channel Hole (nm)

193i Single Patterning

193i LELE Patterning

193i SADP

193i SAQPEUV 2D SE

EUV 1D SE

EUV Multi-patterning

Source: IC Knowledge and Linx

www.linx-consulting.com

Automotive Growth

Impact Implication

Market $3 billion Processing market is anticipated to grow at 10+% CAGR, 2015 – 2020.

Growth still exist for 8 bit MCU as well as 32 and 64 bit devices for more complex applications.

Technology Trends

The level of processing power required for ECU consolidation will drive advanced designs.

Advanced devices will move to Foundry.

The level of processing power for “mainstream” body electronics will stay the same.

Growing demand for 8 bit MCU.

Quality Quality certification locks in processes and materials.

Significant barriers to entry and exit.

Complexity Safety and reliability drive redundancy.

Increased gate counts and complexity.

GreaterChina

Strong growth in auto production in China

Quality material supply will be required.

SMC 2017

www.linx-consulting.com

Storage Class Memory

3D SRAM

STT-MRAM

3D DRAM

STT-MRAM

FeRAM

eMRAM

3D NAND

3D XPoint

Co

st p

er

Bit

Pe

rfo

rma

nce

• Bit growth (AGR 2017):

• NAND ~45%

• DRAM ~15%

• DRAM lateral scaling is slowing and facing cost problems.

• There are no “universal” memory replacements, but new

segments are emerging.

Sources: AMAT, Micron

SMC 2017

-

1

2

3

4

$0

$100

$200

$300

$400

$500

2D NAND16nm

3D NAND 64L 3DXP 2L

Gb

/mm

2

NV Mem Material Cost

Wet strip chemicals

Wet etch chemicals

Wet clean chemicals

Spin-on

Reticles

Quartzware

PVD targets

Plating chemicals

Monitor wafers

Lithography materials

Implant sources

Dry etch gases

CVD precursors

CMP consumables

Bulk gases

Anneal gases

ALD

Bit Density Gb/mm2

www.linx-consulting.com

Materials Market Landscape

Analog 200mm

6%

Discrete 200mm

41%

ASIC 200mm

8%

ASIC6%

MPU3%

DRAM17%

NAND-2D13%

NAND-3D6%

2017 Si Demand - MSI

$-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$/sq in

SMC 2017

www.linx-consulting.com

Materials Markets

Analog 200mm

4%Discrete 200mm

12%

ASIC 200mm

7%

ASIC11%

MPU14%

DRAM25%

NAND-2D18%

NAND-3D9%

Materials Share by Device Type

ALD8% Anneal gases

1%

Bulk gases14%

CMP consumables

14%

CVD precursors

10%

Dry etch gases

6%

Implant sources

0%

Lithography materials

25%

Plating chemicals

1%

PVD targets4%

Spin-on10%

Wet clean chemicals

3%

Wet etch chemicals

3%

Wet strip chemicals

1%

Materials Segment

SMC 2017

www.linx-consulting.com

Film Deposition

• Demand Drivers

• CuBS demand increasing in Logic Interconnect

• Limitations of current architectures

• FinFET gate deposition

• GAA Nanowire development

• High mobility materials

• Memory technology extension

• 3D-NAND growth

• DRAM capacitor dielectric

• Novel architectures

• Pitch doubling and quadrupling

• Low temperature spacers

• Lithography aids

• Opportunities

• Possible changes in conductor metal

• Cu Co Barrier Ru?

• 3D-NAND aspect ratio

• Novel process development

• CVD Continuous etch

• ALD ALE

• Self Assembling Materials for selective processes

• Few new PVD applications

• 3DXpoint / MRAM?

• Complex supply chain requiring unique capabilities

• Supply of Co intermediates

SMC 2017

www.linx-consulting.com

CMP

Demand Drivers

• Continued addition of CMP processes

• CMP is becoming an enabling process

• Cleaning and particle removal through buff processes

• Implementation into SADP pattern transfer processes

• CMP of sacrificial layers for CDU

• Novel metals in MOL and BEOL processes

Opportunity

• High purity colloidal type abrasives are taking place in both silica and ceria segments for defect control.

• Close collaboration among CMP materials supply chain players is required to meet advanced CMP process requirements.

• Highly consolidated supply side.

• Integration of Polish and Cleaning processes to optimize defectivity.

• Local sources in China.

SMC 2017

www.linx-consulting.com

Patterning

Demand Drivers

• Increasing cost driver for advanced devices.

• Extension of resolution for 193i processes .

• Self aligned process patterning

• Mandrel thermal stability and cost

• SAQP MO spacers

• Multicolor cut mask processes

• High aspect ratio etch resistant hard masks.

• EUV implementation.

Opportunities

• Process aids

• Image reversal

• EPE improvement

• Photoresist smoothing strategies

• Etch

• Vapor

• DSA

• Deposition

EUV

• Source Power

• Acceptability of metal oxide nanoparticles

• Metal Oxide underlayers for EUV sensitivity

• Pellicle design

SMC 2017

www.linx-consulting.com

Worldwide Wafer Fab Materials Forecast

US$ Millions 2016 2017 2018 2020 CAGR

2016 to ‘20

ALD $311 $340 $456 $671 21%

CVD $1,292 $1,390 $1,565 $1,744 8%

PVD $728 $782 $817 $856 4%

Plating $185 $206 $225 $258 9%

Spin On Dielectrics $475 $512 $553 $525 3%

Pads and Slurries $1,908 $2,001 $2,090 $2,119 3%

Wet Chemicals $2,448 $2,597 $2,769 $2,960 5%

Lithography Materials $2,925 $3,081 $3,361 $3,553 5%

Etchant Gases $283 $301 $321 $368 7%

Dopant Gases $191 $165 $162 $172 -3%

Litho Gases $145 $159 $173 $208 9%

Total (Direct Mats) $10,891 $11,534 $12,492 $13,434 5%

SMC 2017

Application requirements driving the Technology Development

Marcel Wieland, Deputy Director Technology Development Globalfoundries

Holistic Approach 15–16 November 2017

Substrates

Materials

Components

Subassemblies

Equipment IP

Design

Fabless

Device

Manufacturing

Packaging

Test

System

Integration

Applications

R&D

Consortia

Potential topics along the value chain to be addressed in Call for Paper

• Automotive:

high reliability,

Grade 0-2

• E-vehicles

• Communication

RF: high

frequencies

about 300GHz

• Ultra low- k

material for

automotive

• Metrology

Focus FDSOI and Non Volatile Memory

• Over

molding

• Interposer

• Photonics

• WLP

• Antenna

integration

• Memory

integration

• Optic on

board (less

power

consumption)

Want to get more?

The Material Conference will focus on:

• Requirements for automotive (high reliability) and mobile communication (high frequency) applications

• FD-SOI and ferroelectric memories

Program

Session 1 - FDSOI - Continuation of Innovation

Session 2 - Microcontrollers and Nonvolatile Memories

Session 3 - Materials and Processes for Frontend/Backend of Line Applications

15–16 November 2017

Session 1 - FDSOI - Continuation of Innovation 15–16 November 2017

Session 1 - FDSOI - Continuation of Innovation 15–16 November 2017

Session 2 - Microcontrollers and Nonvolatile Memories

15–16 November 2017

Session 3 - Materials and Processes for Frontend/Backend of Line Applications

15–16 November 2017

Thank you!See you in Munich 14-17 NOV 2017