Never mind 4Q, look at the RUP benefits P/E (x) 11.1 …...EBIT Margin 1.9% 1.6% 4.7% 4.2% -0.3 pp...

27

Please see the last page of this report for important disclosures. RESEARCH 1 23 February, 2015 Tupras Market Perform (Maintained) Last Price TL 53.30TL 12-month Target Price TL 62.50TL Potential Return TL 17% Current Mcap (TLmn) 13,347 Current EV (TLmn) 17,385 5,441 Bloomberg/Reuters: 1 mth 3 mth 12mth 1% 1% 6% 32.3 YTD TL Return: -4% 250 Free Float (%): 49 86% Financials and Ratios 2013 2014E 2015E 2016E Research Analyst: Onur Marşan Net Sales (TLmn) 41,078 40,389 34,764 45,577 +90 (212) 384 1125 EBITDA (TLmn) 1,014 1,013 2,015 2,346 [email protected] Net Profit (TLmn) 1,197 1,392 1,174 1,312 EBITDA Margin 2.5% 2.5% 5.8% 5.1% Sales Contact: P/E (x) 11.1 9.6 11.4 10.2 +90 (212) 384 1155-58 EV/EBITDA (x) 17.1 17.2 8.6 7.4 [email protected] EV/Sales (x) 0.42 0.43 0.50 0.38 EPS (TL) 4.78 5.56 4.69 5.24 DPS (TL) 1.58 0.20 1.20 0.80 Current Mcap (US$mn) Price Performance (TL) Stock Market Data TUPRS.TI / TUPRS.IS Relative Performance: 52 Week Range (TL): 37.2 / 56.9 Foreign Ow nership in Free Float (%): Average Daily Vol (US$mn) 3 mth: Shares Outstanding (mn): 30.00 36.00 42.00 48.00 54.00 60.00 01.14 02.14 03.14 04.14 05.14 06.14 07.14 08.14 09.14 10.14 11.14 12.14 01.15 02.15 TUPRS BIST-100 Never mind 4Q, look at the RUP benefits Tupras’ 4Q results due on March 2, will be hit by FX and inventory losses as reflected in tax financials. The hydrocracker project is now on-stream, yet the fall in oil prices, and lower spreads remain major threats to the Company’s profitability. We maintain our Market Perform recommendation with a 12-month price target of TL62.50, implying 17% upside potential. The stock trades at a 2015E EV/EBITDA multiple of 7.5x - at a premium over the 6.0x average multiple of its global regional peers. Expect a weak 4Q amid inventory and FX losses Oil prices continued their downward trajectory with the Brent price falling by 39% from $94/bbl at the beginning of the quarter to $57.50/ bbl by the end. Although Med margins have remained strong, the reported US$204mn inventory loss (higher than our US$150mn expectation) will have eaten up most of the operating profitability. Tax results point to a no dividend yet we forecast a tiny TL50mn to be distributed from reserves. The deferred tax income will be the saviour for the bottom line in the IFRS results. Note that tax financials included the Competition Board fine of TL309mn recorded at 2013- end. We revised down our 4Q net income from TL192 to TL146mn. RUP now operational, but full impact to be seen later his year Although the opening ceremony took place in December, the RUP is still in the testing phase and will become fully operational by 2Q15. Low crude prices, along with slimmer diesel/fuel-oil spreads, could erode profitability in the short term; yet once we observe some stabilization in demand and pricing, Tupras will reap the rewards of higher profitability. Tupras expects the RUP to generate an additional US$550mn in annual EBITDA and expects the hydrocracker to provide the Company with more flexibility in a changing demand environment. Tax fine puts some pressure on the share price After the tax investigation for the 2009-2013 period, the Tax Office fined Tupras a total of TL160mn (TL65.6mn original tax + TL94.4mn tax related fines) plus overdue interest for the related period. Although Tupras stated that it would exercise all of its legal rights regarding the tax fine, we believe a settlement option is more likely for the resolution. The Company has not yet set aside any provision for the fine. Turkey - Equity - Oil & Gas Company Update

Transcript of Never mind 4Q, look at the RUP benefits P/E (x) 11.1 …...EBIT Margin 1.9% 1.6% 4.7% 4.2% -0.3 pp...

Please see the last page of this report for important disclosures.

RESEARCH

1

23 February, 2015

Tupras Market Perform (Maintained)

Last Price TL 53.30TL

12-month Target Price TL 62.50TL

Potential Return TL 17%

Current Mcap (TLmn) 13,347

Current EV (TLmn) 17,385

5,441

Bloomberg/Reuters:

1 mth 3 mth 12mth

1% 1% 6%

32.3

YTD TL Return: -4%

250

Free Float (%): 49

86%

Financials and Ratios 2013 2014E 2015E 2016E Research Analyst: Onur Marşan

Net Sales (TLmn) 41,078 40,389 34,764 45,577 +90 (212) 384 1125

EBITDA (TLmn) 1,014 1,013 2,015 2,346 [email protected]

Net Profit (TLmn) 1,197 1,392 1,174 1,312

EBITDA Margin 2.5% 2.5% 5.8% 5.1% Sales Contact:

P/E (x) 11.1 9.6 11.4 10.2 +90 (212) 384 1155-58

EV/EBITDA (x) 17.1 17.2 8.6 7.4 [email protected]

EV/Sales (x) 0.42 0.43 0.50 0.38

EPS (TL) 4.78 5.56 4.69 5.24

DPS (TL) 1.58 0.20 1.20 0.80

Current Mcap (US$mn)

Price Performance (TL)

Stock Market Data

TUPRS.TI / TUPRS.IS

Relative Performance:

52 Week Range (TL): 37.2 / 56.9

Foreign Ow nership in Free Float (%):

Average Daily Vol (US$mn) 3 mth:

Shares Outstanding (mn):

30.00

36.00

42.00

48.00

54.00

60.00

01.1

4

02.1

4

03.1

4

04.1

4

05.1

4

06.1

4

07.1

4

08.1

4

09.1

4

10.1

4

11.1

4

12.1

4

01.1

5

02.1

5

TUPRS BIST-100

Never mind 4Q, look at the RUP benefits

Tupras’ 4Q results due on March 2, will be hit by FX and

inventory losses as reflected in tax financials.

The hydrocracker project is now on-stream, yet the fall

in oil prices, and lower spreads remain major threats to

the Company’s profitability.

We maintain our Market Perform recommendation with a

12-month price target of TL62.50, implying 17% upside

potential. The stock trades at a 2015E EV/EBITDA

multiple of 7.5x - at a premium over the 6.0x average

multiple of its global regional peers.

Expect a weak 4Q amid inventory and FX losses

Oil prices continued their downward trajectory with the Brent price

falling by 39% from $94/bbl at the beginning of the quarter to $57.50/

bbl by the end. Although Med margins have remained strong, the

reported US$204mn inventory loss (higher than our US$150mn

expectation) will have eaten up most of the operating profitability. Tax

results point to a no dividend yet we forecast a tiny TL50mn to be

distributed from reserves. The deferred tax income will be the saviour

for the bottom line in the IFRS results. Note that tax financials

included the Competition Board fine of TL309mn recorded at 2013-

end. We revised down our 4Q net income from TL192 to TL146mn.

RUP now operational, but full impact to be seen later his year

Although the opening ceremony took place in December, the RUP is

still in the testing phase and will become fully operational by 2Q15.

Low crude prices, along with slimmer diesel/fuel-oil spreads, could

erode profitability in the short term; yet once we observe some

stabilization in demand and pricing, Tupras will reap the rewards of

higher profitability. Tupras expects the RUP to generate an additional

US$550mn in annual EBITDA and expects the hydrocracker to provide

the Company with more flexibility in a changing demand environment.

Tax fine puts some pressure on the share price

After the tax investigation for the 2009-2013 period, the Tax Office

fined Tupras a total of TL160mn (TL65.6mn original tax + TL94.4mn

tax related fines) plus overdue interest for the related period. Although

Tupras stated that it would exercise all of its legal rights regarding the

tax fine, we believe a settlement option is more likely for the resolution.

The Company has not yet set aside any provision for the fine.

Turkey - Equity - Oil & Gas

Company Update

Please see the last page of this report for important disclosures.

2

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

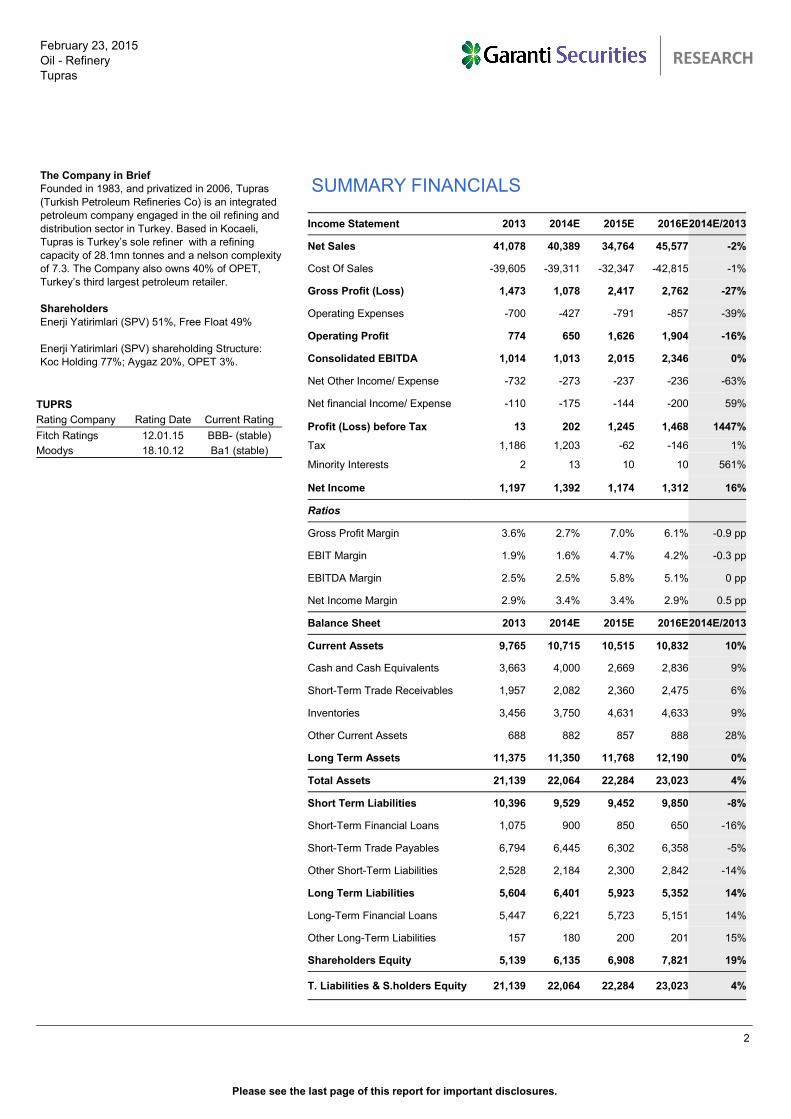

The Company in Brief

Founded in 1983, and privatized in 2006, Tupras

(Turkish Petroleum Refineries Co) is an integrated

petroleum company engaged in the oil refining and

distribution sector in Turkey. Based in Kocaeli,

Tupras is Turkey’s sole refiner with a refining

capacity of 28.1mn tonnes and a nelson complexity

of 7.3. The Company also owns 40% of OPET,

Turkey’s third largest petroleum retailer.

Shareholders

Enerji Yatirimlari (SPV) 51%, Free Float 49%

Enerji Yatirimlari (SPV) shareholding Structure:

Koc Holding 77%; Aygaz 20%, OPET 3%.

Income Statement 2013 2014E 2015E 2016E 2014E/2013

Net Sales 41,078 40,389 34,764 45,577 -2%

Cost Of Sales -39,605 -39,311 -32,347 -42,815 -1%

Gross Profit (Loss) 1,473 1,078 2,417 2,762 -27%

Operating Expenses -700 -427 -791 -857 -39%

Operating Profit 774 650 1,626 1,904 -16%

Consolidated EBITDA 1,014 1,013 2,015 2,346 0%

Net Other Income/ Expense -732 -273 -237 -236 -63%

Net financial Income/ Expense -110 -175 -144 -200 59%

Profit (Loss) before Tax 13 202 1,245 1,468 1447%

Tax 1,186 1,203 -62 -146 1%

Minority Interests 2 13 10 10 561%

Net Income 1,197 1,392 1,174 1,312 16%

Ratios

Gross Profit Margin 3.6% 2.7% 7.0% 6.1% -0.9 pp

EBIT Margin 1.9% 1.6% 4.7% 4.2% -0.3 pp

EBITDA Margin 2.5% 2.5% 5.8% 5.1% 0 pp

Net Income Margin 2.9% 3.4% 3.4% 2.9% 0.5 pp

Balance Sheet 2013 2014E 2015E 2016E 2014E/2013

Current Assets 9,765 10,715 10,515 10,832 10%

Cash and Cash Equivalents 3,663 4,000 2,669 2,836 9%

Short-Term Trade Receivables 1,957 2,082 2,360 2,475 6%

Inventories 3,456 3,750 4,631 4,633 9%

Other Current Assets 688 882 857 888 28%

Long Term Assets 11,375 11,350 11,768 12,190 0%

Total Assets 21,139 22,064 22,284 23,023 4%

Short Term Liabilities 10,396 9,529 9,452 9,850 -8%

Short-Term Financial Loans 1,075 900 850 650 -16%

Short-Term Trade Payables 6,794 6,445 6,302 6,358 -5%

Other Short-Term Liabilities 2,528 2,184 2,300 2,842 -14%

Long Term Liabilities 5,604 6,401 5,923 5,352 14%

Long-Term Financial Loans 5,447 6,221 5,723 5,151 14%

Other Long-Term Liabilities 157 180 200 201 15%

Shareholders Equity 5,139 6,135 6,908 7,821 19%

T. Liabilities & S.holders Equity 21,139 22,064 22,284 23,023 4%

SUMMARY FINANCIALS

TUPRS

Rating Company Rating Date Current Rating

Fitch Ratings 12.01.15 BBB- (stable)

Moodys 18.10.12 Ba1 (stable)

Please see the last page of this report for important disclosures.

3

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

INVESTMENT THESIS

We change our 12 month target price for Tupras from TL55.30 to TL62.50

per share, implying 17% upside potential. The steep fall in crude oil prices

led to some hefty one-off inventory losses, as reported US$204mn in the

4Q14 financial statements due on March 2, yet the strong refining margins

could compensate some of these massive losses in 4Q14. We welcome

the recent upward trend in crude oil prices in 1Q15 that could pave the

way for inventory gains, while the appreciation in the US$ will have a

positive impact on operation profitability. All in all, we maintain our Market

Perform recommendation for Tupras. We deem the Company’s business

prospects are solid following the completion of the RUP Project, yet we

will await better entry points for the stock.

Higher refining margins thanks to lower oil prices

Brent prices declined for a sixth consecutive month in December, with the

average price falling by a further $17/barrel (bbl) on the month to $62/bbl,

the lowest since May 2009. Overall, crude oil prices have tumbled by 56%

since June, with no indication that the decline will stop there. There have

even been market rumours of a $40/bbl price, with authorities in Saudi

Arabia declaring that they would be comfortable even if prices fell as low

as $20/bbl.

The price of oil continued to collapse into January as rising supplies

coincided with weak demand growth, with OPEC maintaining its

commitment not to cut production. Despite lower prices, lowest level seen

as US$45.5 per barrel seen on January 13, within the growth in global

demand is only forecasted to accelerate to 0.9mb/d in 2015.

The weakness in oil prices so far manifested itself in the form of higher

gross refining margins thanks to the increase in product price spreads.

Although winter is known as a low margin season, we have seen very

strong Med region refining margins reaching 6$/bbl on a daily basis.

However, it should also be borne in mind that this strong margin

environment should be a temporary phenomenon, and once there is some

stabilization in crude prices we would expect refining margins to come

down sharply as demand dynamics suggest. The combination of abundant

supply from U.S. oil production and strong global supply, combined with a

weakening outlook for the global economy and oil demand growth, could

be listed as the main reasons behind the fall.

Source: IEA

-

2.00

4.00

6.00

8.00

Jan

.13

Fe

b.1

3

Ma

r.13

Ap

r.1

3

May.1

3

Jun

.13

Jul.13

Au

g.1

3

Se

p.1

3

Oct.1

3

Nov.1

3

Dec.1

3

Jan

.14

Fe

b.1

4

Ma

r.14

Ap

r.1

4

May.1

4

Jun

.14

Jul.14

Au

g.1

4

Se

p.1

4

Oct.1

4

Nov.1

4

Dec.1

4

Refining Margins ($/bbl)

Brent Cracking Urals (Cracking)

Please see the last page of this report for important disclosures.

4

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

Refining margins unlikely to improve in the coming years

Once crude prices bottom out and stabilise, we would expect product

spreads to plunge from their current high levels, leading to lower refining

margins. Under such conditions, we would also expect Tupras’ margins to

decline, although the Company will have the capacity to switch to more

profitable products now that the fuel-oil conversion (RUP) unit is up and

running - although this may not be sufficient to maintain strong profitability,

unless we see a strong recovery in the demand composition.

We believe the most bountiful years for refining margins are now behind

us, while we do not expect the global refining market to return to its pre-

crisis levels for the foreseeable future, with refining margins likely to come

under pressure in the coming years. Crude differentials are likely to

remain below their historical averages, while expanding refining capacity

will lead to an even more competitive market amid a lack of sufficient

growth drivers in the coming period.

In this context, the completion of the RUP project will prove vital in

sustaining Tupras’ profitability. We would also note that although Tupras

has welcomed Socar’s entry into the market as a second player from 2018

and beyond with its STAR refinery that is planned to be operational by

2017-end, we believe the intensified competition will undoubtedly squeeze

Tupras’ margins, despite the strong local growth.

The STAR refinery will have a refining capacity of 10mn tonnes, mainly

focused on the production of naphtha, a feedstock for Petkim. Even then,

the new diesel capacities will still not be sufficient to meet local demand.

Source: Tupras, Reuters

We expect Tupras to close 2014 with a net refining margin of US$2.75/

bbl. For 2015 and beyond, we expect refining margins to hover at around

US$4-5/bbl, thanks to the addition of the RUP.

0

20

40

60

80

100

120

140

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

Med -TUPRS Margins versus Brent Prices

Med Margins TUPRS margins Brent Prices (rhs)

Please see the last page of this report for important disclosures.

5

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

Despite being a one-off, we expect inventory losses to take their toll on

the share price

At tax financilas, the inventory loss came at US$204mn in the 4th quarter

on the back of a steep 39% fall in oil prices. After the beginning of the

year, prices continued their downtrend and had plunged by another 16%

as of January 16, hitting $48 per barrel levels. We assume that the FX

losses will have a one-off impact. Recently, we observed the crude prices

climbing back to US$55-60 per barrel levels paving for inventory gains in

1Q15.

Tupras Inventory effect versus change in Brent prices

Source: Tupras, Reuters

Residual Fuel Oil Conversion (RUP) project to bring strong flexibility

Work on the project got underway in 2008, and was completed with a

capex investment of around US$2.9bn. The project will enable the refinery

to process 4.2mn tonnes of high sulphur fuel oil - where there is a surplus

in Turkey - and produce approximately 3.5mn tonnes of high quality

diesel/jet fuel, gasoline and LPG to Euro-V standards. It also enables the

production of 690,000 tonnes of petroleum coke and 86,000 tonnes of

sulphur. Following the completion of the RUP, the Nelson Complexity

Index of the Izmit refinery increased from the current 7.78 to 14.5 (based

on design capacity).

Source: Tupras

(0.60)

(0.50)

(0.40)

(0.30)

(0.20)

(0.10)

-

0.10

0.20

0.30

0.40

(400)

(300)

(200)

(100)

-

100

200

300

1Q

08

4Q

08

3Q

09

2Q

10

1Q

11

4Q

11

3Q

12

2Q

13

1Q

14

4Q

14

(US

$m

n)

Inventory Impact

Product inv. (US$mn)

Crude inv. (US$mn)

Change in Brent price (rhs)

Please see the last page of this report for important disclosures.

6

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

We calculate that the RUP will contribute around US$500mn in annual

EBITDA, a figure lower than the Company’s expectations at the current

product price ratios. We incorporated the RUP product yields announced

by Tupras into our valuation. We would expect product price ratios to

remain depressed in the second half of 2015 on the back of low oil prices,

decreasing the profitability of the project. Nevertheless, we still calculate

that the project will be able to create a minimum of US$350-400mn in

additional EBITDA going forward.

Tupras to still be a dominant player by the end of 2017

Tupras’ existing four refineries account for 100% of Turkey’s domestic

production. Even after the RUP project, there will still be room for

additional refining capacity. In this context, we welcome the addition of the

Socar-Turcas Refinery (STAR), which will come on stream by the end of

2017 with the completion of the US$5.5bn investment. Tupras, as

Turkey’s sole refiner, will continue to enjoy its dominant position (60%

market share, with the rest imported) in the next 3 years. The STAR

refinery will have a refining capacity of 10mn tonnes, mainly focused on

the production of naphtha, a feedstock for Petkim. Even then, the new

diesel capacities will still not be sufficient to meet local demand.

Demand still buoyant in Turkey

Oil has long been one of the key sources of energy in Turkey, accounting

for some 28% of the country’s Total Primary Energy Supply (TPES).

Turkey’s demand for oil increased slightly from 29mn tonnes in 2003 to

35mn tonnes in 2013, chalking up a 10 year CAGR of 2%. The transport

sector accounted for almost half of total oil consumption in 2013. We

expect the current demand composition to be maintained going forward

with an increasing contribution from the transport sector. The airline sector

is projected to grow at a rate double that of GDP, with automotive sales on

course to grow at a rate at least 1-2 percentage points in excess of GDP

growth over the next decade.

Oil products consumption in Turkey (000 tonnes)

Source: Tupras

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Other

Asphalt

Lube Oil

Fuel Oil

Diesel

Jet Fuel

Gasoline

Naphtha

LPG

Please see the last page of this report for important disclosures.

7

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

EIA continuously revising its assumptions downwards

Contrary to what we had been accustomed to, the EIA has revised its

crude oil price assumptions for 2015 downward three times since October

2014, in line with the falling trend in oil prices and OPEC’s decision not to

cut production. The EIA now forecasts that Brent crude oil prices will

average $58/bbl in 2015 and $75/bbl in 2016. The current values for

futures and options contracts suggest a very high level of uncertainty for

the pricing outlook. We do not expect a major change in crude

assumptions in the next reports, now that Brent prices have started to

level out at around US$55 per barrel.

Source: EIA

Will there be a production cut in 2015?

OPEC is resolute that it will not cut production and maintains its

production at 28.8mn barrels a day. OPEC notes that if the recent price

trend continues, the long-term sustainability of capacity expansion plans

and investment projects may be put at risk. OPEC is of the view that a

lack of investment may lead to a supply shortage in the long run, leading

to excessive pricing as seen in 2008. The 12-member Organization of the

Petroleum Exporting Countries pumps about a third of the world's oil.

OPEC states that any oil supply cut would lead to spare production

capacity, a lack of investment and an eventual shortage and price spike

that could exceed that seen in 2008, when oil hit a record high of over

$147 a barrel. Meanwhile, non-OPEC oil producers are expected to

increase output in 2015 at a slower rate than previously forecasted, aiding

a recovery in crude prices. The slowdown in non-OPEC output is intended

to lead to a “rebalancing” of the currently over-supplied global markets in

the second half of 2015, reviving prices, according to International Energy

Agency (IEA). OPEC appears to be closely following how the markets will

respond at the end of 1H15 before considering some concrete moves

towards production cut.

Who says falling oil prices do not affect American production?

About 4,000 workers at nine plants, including seven refineries accounting

for 10% of U.S. refining capacity, went on strike on February 2nd,

immediately sending oil prices up by $3 per barrel. The strike ended on

February 5, with the strikers’ demands met. Since bargaining first started

on January 21, the union has rejected five offers and demanded for an

annual pay rise of 6%. Meanwhile, executives stated that raising pay

could prove highly challenging that now crude prices have tumbled by

60% since June 2014, eroding profits. We now are seeing more reports

that U.S. oil production may stop growing in the second half of 2015 and

could fall in 2016, as low oil prices render the majority of oil wells

uneconomical to run. The oversupply of oil has forced a slowdown in

drilling and put the brakes on a five-year boom that pushed U.S.

production to record highs. The slowdown has largely been driven by the

economics of drilling.

EIA Assumptions 2013 2014 2015E 2016E

WTI Crude Oil ($/bbl) 97.91 93.26 54.58 71.00

Brent Crude Oil ($/bbl) 108.64 99.02 57.58 75.00

Please see the last page of this report for important disclosures.

8

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

More than half U.S. oil wells drilled in 2014 were uneconomical below $60/

bbl and 30% per cent of new wells had break even levels of $81 or higher,

according to a HIS article. A slowdown in over production could have

economic impacts as well.

Breakevens for US shale plays

Source: Wood & MacKenzie, EIA

Will Iraqi oil support Tupras’ margins?

The bitter dispute between Baghdad and Erbil, which became an

international issue, has now finally reached a breakthrough agreement.

The central government and the KRG signed a temporary agreement to

settle the oil dispute in November 2014. With the announcement of this

agreement, Tupras has finally declared that it will be able to pump Iraqi oil

from storage at the Mediterranean port of Ceyhan to the central Turkish

city of Kirikkale for processing. Tupras has not purchased crude from

SOMO (Iraq’s State Oil Marketing Organization) since March 2014. Kirkuk

oil is highly suitable for the Kirikkale refinery in terms of complexity.

Source: Tupras

Please see the last page of this report for important disclosures.

9

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

Lower foreign exchange risks and bond issue

The loans for Tupras' RUP project are US$ denominated. Any

depreciation of the TL against the US$ worsens Tupras’ credit ratios,

especially in the event of a sudden depreciation in the TL towards the end

of its financial year. We forecast a $/TL exchange rate of 2.45 at the end

of 2015 and 2.54 in 2016-end. We believe Tupras' currency risk will be

lower once the output from RUP is realized. Tupras also plans to increase

its TL denominated debt exposure by issuing up to TL1bn of bonds and

hedging its foreign exchange exposure with forward and swap contracts.

The first TL200mn tranche of this TL1bn bond was released on January

19. The bond has a 2 year maturity carrying 6 monthly coupons and a

fixed interest rate of 8.99%, with principal payment and interest to be paid

on maturity. The bond issue will help Tupras diversify its loan portfolio as

well as its investor base.

Tax fine represents another threat to Tupras’ profitability

The tax office levied a TL160mn (U$69mn) tax fine on Tupras after an 18-

month investigation. The tax demand for TL65.6mn and related fines of

TL94.4mn is for 2009-2013 period; Tupras announced that it would

exercise all of its legal rights, including negotiations. We believe Tupras

will use its negotiation option, as it has in the past. Recall that, the

Competition Board had issued a TL412mn fine to Tupras back in 2012 for

abusing its dominant position in pricing and contracts. In 2010, the

Company had also faced a total of TL605mn in tax fines for the 2005-2009

period (tax and related fines), which Tupras negotiated down to TL153mn.

Although, we see no significant risk surrounding the tax fine, the provision

to be set aside for the fine will have a direct impact on the tax financials,

pressurising the dividend payment.

Dividend issue will be difficult from 2014 distributable net income

With the low EBITDA generation due to high inventory losses and the

Competition Board’s fine that may impact 2014 dividend, we revised down

our dividend estimate to TL50mn to be distributed from reserves. We also

note that the increase in cash-flow from RUP will lead to higher dividend in

2016 and onwards.

Tax Financials were disappointing

Tupras announced TL856mn net loss in its 2014 tax financials versus

TL337mn before tax net profit recorded a year ago. Operational results

point to a US$204mn inventory loss in 4Q14, totalling US$236mn

inventory loss for 2014. Tupras paid the TL309mn Competition Board fine

in its tax results. The sharp and continuous fall in crude prices led to

higher refining margins and recorded as US$4.56/bbl in 4Q14 (4Q13:

US$2.03/bbl). The capacity utilization rate was recorded as 74.9% in 2014

down 5.3% YoY.

Please see the last page of this report for important disclosures.

10

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

Market Perform maintained

We maintain our Market Perform recommendation despite the upward

revision to our target price: We appoint equal weight to DCF method

(5.5% risk-free rate in $ terms, 5.5% equity risk premium, 1x beta, 6.5%

cost of debt($) and 3.0% terminal value) and to peer comparison to value

Tupras. The Company trades at a premium compared to specifically its

Mediterranean peers yet we believe this premium is justified given the

expected positive free cash flow expectations, thanks to the contribution

from the RUP project.

In this report, we raise our 12-M target share price by %13 from TL55.30

to TL62.5. The key drivers behind the revision to our target price are:

i) lower crude oil price and higher refining margin forecasts

ii) a higher expected contribution from the RUP compared to our

previous assumptions starting from 2015E.

As our revised target price implies 17% upside potential, we maintain our

Market Perform recommendation for the Company. We believe global

risks on product prices and increasing global refining capacity, fluctuations

on $/TL rates and tax issues represent the most significant risks for

Tupras.

Trading above its historical average multiples

Tupras’ trailing trading multiples in the last 2 years have been confusing

as the P/E multiple looked cheap as a result of the deferred tax income.

As Bloomberg combines 2014 and 2015 forecasts for EBITDA and net

income proportionately, the EV/EBITDA multiple declines with the higher

contribution of 2015 EBITDA forecast. We deem 10x P/E multiple and 7x

EV/EBITDA is the fair multiple for Tupras, trading slightly above its global

peers.

Source: Bloomberg

6x

7x

8x

9x

10x

11x

12x

13x

12-0

9

03-1

0

06-1

0

09-1

0

12-1

0

03-1

1

06-1

1

09-1

1

12-1

1

03-1

2

06-1

2

09-1

2

12-1

2

03-1

3

06-1

3

09-1

3

12-1

3

03-1

4

06-1

4

09-1

4

12-1

4

1 year Forward Looking P/E

P/E Average +1s -1s +2s -2s

2x

3x

4x

5x

6x

7x

8x

9x

10x

11x

12x

12-0

9

02-1

0

04-1

0

06-1

0

08-1

0

10-1

0

12-1

0

02-1

1

04-1

1

06-1

1

08-1

1

10-1

1

12-1

1

02-1

2

04-1

2

06-1

2

08-1

2

10-1

2

12-1

2

02-1

3

04-1

3

06-1

3

08-1

3

10-1

3

12-1

3

02-1

4

04-1

4

06-1

4

08-1

4

10-1

4

12-1

4

1 year Forward Looking EV/EBITDA

EV/EBITDA Average +1s -1s +2s -2s

Please see the last page of this report for important disclosures.

11

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

REVISIONS TO FORECASTS

With this report, we have revised our assumptions, mainly based on the

fall in oil prices and revised $/TL exchange rate assumptions. We believe

the slowdown in global economies will be partially reflected to the refining

outlook, and is more likely to pull refining margins lower after a

stabilization in oil prices. We expect the deferred tax income to continue to

have a positive impact on the bottom line in 4Q.

Bloomberg vs. Garanti Forecasts

Our target price of TL62.50 is slightly above the Bloomberg consensus of

TL58.0.

Source: Bloomberg, Garanti Securities

Tupras OLD NEW Difference

(TLmn) 2014E 2015E 2014E 2015E 2014E 2015E

Net Sales 43,031 37,022 40,389 34,764 -6% -6%

EBITDA 950 1,864 1,013 2,015 7% 8%

Net Profit 1,439 1,024 1,392 1,174 -3% 15%

EBITDA Margin 2.2% 5.0% 2.5% 5.8% 0.3 pp 0.8 pp

Net Profit Margin 3.3% 2.8% 3.4% 3.4% 0.1 pp 0.6 pp

Target Share Price 55.30 62.50 13%

Tupras Bloomberg Garanti Securities Difference

(TLmn) 2014E 2015E 2014E 2015E 2014E 2015E

Net Sales 40,407 37,433 40,389 34,764 0% -7%

EBITDA 964 2,253 1,013 2,015 5% -11%

Net Profit 1,150 1,246 1,392 1,174 21% -6%

EBITDA Margin 2.4% 6.0% 2.5% 5.8% 0.1 pp -0.2 pp

Net Income Margin 2.8% 3.3% 3.4% 3.4% 0.6 pp 0 pp

Target Share Price 58.02 62.50 8%

Please see the last page of this report for important disclosures.

12

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

VALUATION Our 12-month target Mcap of US$6.4bn (TL15.6bn) for Tupras is derived

from an equally weighted average of DCF analysis and international peer

group comparison.

DCF Valuation We calculated a target value of US$7.4bn for Tupras based on DCF

analysis, assuming a 1.5% terminal growth rate in our DCF model. We

applied the yield on the 10-year Eurobond as the risk free rate while

assuming a market risk premium of 5.5% in calculating the cost of equity.

Accordingly, we assume a 9% WACC for Tupras’ cash flows.

Valuation (US$mn) Value Weight in Valuation

Value

DCF 7,633 50% 3,816

Multiples 5,144 50% 2,572

Est M. Cap of Tupras 6,388

Current M. Cap 5,441

12M - Target Share Price (TL) 62.50

Current Share Price (TL) 53.30

Upside potential (TL) 17%

Assumptions and Results (US$mn) - 12M

Weight of equity 65% PV of FCF 3,782

Cost of Equity 11.0% PV of Terminal Value 5,504

Beta 1.0 Implied Firm Value 9,286

Risk free rate ($) 5.5% Net Cash (9M14, tax fine inc.) -1,654

Market Risk Premium 5.5% Target Mcap 7,633

Cost of Debt 6.0%

Tax rate 20.0%

WACC 9.0%

Terminal Value Growth 3%

Please see the last page of this report for important disclosures.

13

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

Peer Group Comparison We also carried out a peer comparison to arrive at a fair value for Tupras.

We compared the Company with global peers in the region. We took both

2015E and 2016E P/E and EV/EBITDA multiples into consideration with

equal weighting in our comparative analysis, driving a fair value of

US$5.14bn from the peer group comparison.

* 2014 figures are for information purposes only Source: Bloomberg, Garanti Securities

Company Name Country P/E* 2014

P/E 2015

P/E 2016

EV/EBITDA*

2014

EV/EBITDA

2015

EV/EBITDA

2016

EV/ SALES*

2014

EV/SALES 2015

EV/ SALES 2016

European Refiners

Hellenic Petroleum SA GREECE - 15.2 7.8 10.6 6.9 5.7 0.3 0.3 0.3

Polski Koncern Naftowy Orlen SA POLAND 15.0 12.4 11.5 6.5 6.3 6.0 0.3 0.4 0.3

Neste Oil OYJ FINLAND 15.6 14.5 - 9.7 8.1 7.7 0.5 0.6 0.5

MOL Hungarian Oil & Gas PLC HUNGARY 12.6 12.3 9.0 5.0 5.1 4.2 0.5 0.6 0.5

OMV AG AUSTRIA 8.8 14.3 9.3 3.8 4.3 3.4 0.4 0.5 0.5

Total SA FRANCE 10.1 15.5 11.9 4.6 6.1 5.0 0.7 0.9 0.8

Average (1) 12.4 14.0 9.9 6.7 6.1 5.3 0.5 0.5 0.5

Asian Refiners

Indian Oil Corp Ltd INDIA 13.7 12.9 9.0 9.7 9.7 7.6 0.3 0.3 0.3

SK Innovation Co Ltd S. KOREA - 13.0 10.2 22.6 9.7 8.5 0.3 0.4 0.3

Bharat Petroleum Corp Ltd INDIA 24.2 15.8 12.5 11.5 10.3 8.8 0.3 0.3 0.3

S-Oil Corp S. KOREA - 16.1 - - 9.9 8.9 0.4 0.5 0.4

GS Holdings Corp S. KOREA - 12.3 9.9 32.5 14.7 12.6 1.0 0.9 0.9

Thai Oil PCL THAILAND - 12.3 10.7 23.1 7.6 6.9 0.4 0.4 0.4

Hindustan Petroleum Corp Ltd INDIA 21.7 13.0 9.9 12.1 9.9 9.0 0.3 0.3 0.3

Average (2) 19.9 13.6 10.4 18.6 10.2 8.9 0.4 0.4 0.4

American Refiners

Marathon Petroleum Corp USA 13.9 12.6 10.9 7.2 6.6 6.2 0.4 0.4 0.4

Phillips 66 USA 12.1 12.3 10.5 6.7 7.2 6.3 0.3 0.4 0.3

Tesoro Corp USA 11.8 13.2 11.7 5.7 5.8 5.3 0.3 0.4 0.4

Valero Energy Corp USA 9.6 10.7 9.7 4.8 5.3 5.0 0.3 0.4 0.3

Delek US Holdings Inc USA 10.4 - 12.1 4.9 6.0 5.5 0.3 0.3 0.3

Western Refining Inc USA 9.2 12.4 11.7 5.1 6.3 7.8 0.4 0.5 0.4

Average (3) 11.2 12.2 11.1 5.7 6.2 6.0 0.3 0.4 0.4

Arithmetic Average (1-2-3) 14.5 13.3 10.5 10.3 7.5 6.7 0.4 0.5 0.4

Average 5,144

Please see the last page of this report for important disclosures.

14

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

Tupras at a glance Tupras controls Turkey’s entire refining capacity of 28.1mn tonnes and

qualifies as the seventh largest refiner in Europe overall, with a 5% share

in total capacity. The refiner meets 60-65% of Turkey’s entire demand for

petroleum products. Tupras also owns all of Turkey’s crude oil storage

and around 45% of the country’s product storage capacity.

European refiners by capacity

Source: Oil and Gas Journal

Tupras has four main refineries in Turkey with a total refining capacity of

28.1mn tonnes.

N.C: Nelson Complexity

Source: Tupras

1984

1681

1197

876 854709

613521

427 403 399 396 350 313 311 304 304 300 295 210

To

tal S

a

Exx

on M

ob

il

Roya

l Dutc

h S

hell

Ag

ip P

etr

oli

SP

A

BP

Repso

l YP

F

Tu

pra

s

Pe

troplu

s

CE

PS

A

Ineos

Om

v

ER

G G

roup

Conoco

Phili

ps

Helle

nic

Petr

ole

um

Nest

e O

il

Sta

toil

Ga

lp E

ne

rgia

Sa

ras

Pe

trole

os

Va

lero

Crude Capacity (b/cd)

Tonnes (mn)

Capacity N.C. Before

RUP N.C. After

RUP Sales (2013) (mn tonnes)

Personnel (2013)

Izmit 11 7.78 14.5* 10.7 1,763

Izmir 11 7.66 7.66 8.8 1,267

Kirikkale 5 6.32 6.32 3.8 872

Batman 1.1 1.83 1.83 0.2 463

Total 28.1 7.25 9.9 23.5 4,365

Please see the last page of this report for important disclosures.

15

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

OPET - Fuel Distribution

Tupras holds a 40% stake in Opet, which has 1,388 filling stations (961 of

the OPET brand and 427 of the Sunpet brand) and 1.1mn cubic metres of

storage capacity.

Source. Tupras

Opet is engaged in retail, commercial and industrial sales, storage

operations and the international trade of petroleum products. The

Company also operates in the lubricating oil and jet fuel categories

through its subsidiaries.

Opet commands a number two position in the distribution business with a

19.1% market share in white products. The Company also ranks second

after Petrol Ofisi in the black products segment. Opet recorded total

EBITDA of US$290mn in 2013, with an operating profit margin of 2.3%.

DITAS - Marine Transportation

DİTAS is Turkey’s leading tanker and maritime trade company. Tupras

owns almost 80% of the shares in the company. Providing services for

tanker management, brokerage/chartering, piloting, tugging, audit and

agency services, Ditaş undertakes crude oil transport operations in line

with Tupras’s needs, and the transport of petroleum products in

accordance with the needs of both Tupras and other suppliers. The

Company uses its own tankers as well as tankers it charters based on the

time or line.

Total revenues reached US$103.1mn in 2013 with an operating profit of

US$25.2mn. A total of 4.4mn tonnes of crude oil and 3.1mn tonnes of

product was transported by the company.

Source: Tupras

OPET Terminals Storage Capacity (000 m3)

Marmara 721,000

Mersin 240,000

Aliaga 54,506

Giresun 43,130

Körfez 37,165

Antalya 19,392

Total 1,115,193

Ditaş Tankers M/T

Cumhuriyet M/T

T.Sevgi M/T

T. Gonul M/T

T. Suna M/T

T. Leyla M/T

T. Esra

Tanker Type Crude Oil Oil/Chem. Oil/Chem. Oil/Chem. Oil/Chem. Oil/Asphalt

Year built 2001 2008 2009 2012 2011 2014

Slop Tank Cap. (m3) 4,443 406.4 413.4 1,019.36 141.4 -

Cargo Tank Cap. (m3) 173,759 12,247 12,224 52,925 7,209 16,940

DWT (tonnes) 164,859 10,983 10,983 51,532 6,297 19,968

GRT (tonnes) 84,476 7,318 7,318 29,754 4,225 15,674

Net Tonnage (tonnes) 53,710 3,651 3,651 14,116 2,047 4,702

Length mt 274.18 131.85 131.85 183.31 121.62 156.5

Please see the last page of this report for important disclosures.

16

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

Crude Oil Purchases

Turkey is conveniently located at the heart of the World’s key oil producing

regions, enabling Tupras to diversify its crude sources. In fact, Turkey's

importance in global energy markets has been growing, both as a regional

energy transit hub and as a growing consumer. Turkey's demand for

energy has increased rapidly over the past few years, and is likely to

sustain its growth in the future.

One of Tupras strongest capabilities is the use of its geographical

advantage in diversifying its sources of crude oil. The Company

purchases 18 different types of crude oil from ten countries, with specific

gravities ranging between 19-48 API.

Source: Tupras

Tupras - Crude Suppliers breakdown (2013)

Source: Tupras

Tupras imports c. 90% of its crude oil need from international suppliers.

Crude Oil Suppliers (mn tonnes)

2009 2010 2011 2012 2013

Domestic 2.3 2.5 2.4 2.3 2.4

Iran 3.2 7.4 9.7 7.2 5.1

Russia 5.5 2.9 2.1 2.0 1.5

Saudi Arabia 2.1 1.8 2.0 2.8 2.9

Iraq 1.8 2.1 3.1 3.8 6.1

Kazakhstan 0.6 2.2 1.1 2.5 1.5

Italy 0.2 0.1 0.1 0.3 0.3

Libya 0.0 0.0 0.0 1.0 0.7

Others 0.7 0.4 0.3 0.6 0.6

TOTAL 16.4 19.4 20.8 22.5 21.1

Domestic11%

Iran 24% Russia

7%

S. Arabia14%

Iraq29%Kazakhstan

7%

Italy1%

Libya3%

Others3%

Please see the last page of this report for important disclosures.

17

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

Until the imposition of the sanctions on Iran, Iran had supplied as much as

50% of Tupras’ total crude needs. After that, Tupras started to reduce its

purchases from Iran to comply with the US sanctions, replacing its

supplies from Iran with Iraqi and Saudi oil.

There is a significant prospect that the sanctions imposed against Iran

may be eased in 2016 or 2017, yet the situation remains unclear. On

November 24th, 2014, Iran and six powers extended the nuclear talks with

Iran by a further 7 months. If Iran complies with the Geneva Interim

agreement, there is a possibility that the sanctions could be eased. Still,

our assumptions do not incorporate any easing in sanctions in 2015 or

beyond. Any positive surprise on this front would serve as a positive

trigger for Tupras. Turkey will be one of the direct beneficiaries of any

possible relaxation in the oil-embargo on Iran imposed by the West.

Tupras enjoys a cost advantage on Iranian heavy crude, which generally

sells at a discount to Brent crude. However, this margin has narrowed as

oil prices have fallen.

Brent versus Iran and Ural crude oil discount (average)

Source: Tupras

Tupras versus Med Refining Margins $/bbl

Source: Tupras

-6.00

-5.00

-4.00

-3.00

-2.00

-1.00

0.00

2009 2010 2011 2012 2013 2014

Dis

co

un

t (U

S$/b

bl)

Tit

le

IRAN HEAVY IRAN LIGHT URAL

(4.00)

(2.00)

0.00

2.00

4.00

6.00

8.00

10.00

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2010 2011 2012 2013 2014

Tupras versus Med Refining Margins $/bbl

Difference Tupras Med. Ural

Please see the last page of this report for important disclosures.

18

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

RUP project now up and running

Work on the project got underway in 2008 and was completed with a

capex investment of around US$2.9bn. The project enables the refinery to

process 4.2mn tonnes of high sulphur fuel oil - of which there is a surplus

in Turkey - and produce approximately 3.5mn tonnes of high quality

diesel/jet fuel, gasoline and LPG to Euro-V standards. The unit will also

enable the production of 690,000 tonnes of petroleum coke and 86,000

tonnes of sulphur. Following the completion of the RUP, the Nelson

Complexity Index of the Izmit refinery increased from the current 7.78

currently to 14.5 (based on design capacity).

RUP started with test operations and will be fully operational by 2Q15.

Tupras calculates the project to bring in US$550mn of additional EBITDA,

through higher white product yields.

Source: Tupras

We anticipate that Tupras’s total production volume will increase from

21.6mn tonnes in 2012 to 25mn tonnes by 2016. Our calculation for the

RUP is more conservative, expecting US$500mn in additional EBITDA.

While we concur that the RUP project will provide the Company with more

flexibility in periods of volatility, the spread between diesel and fuel oil will

be the main determinant of the RUP’s profitability. However, we still

believe the prospective improvement in EBITDA that the project will bring,

has been almost fully priced-in.

RUP flowchart

Source:Tupras

White Products (000 tonnes) Total Charge (000 tonnes)

Atm. Dip 3,036 LPG 69

Vacuum Dip 1,214 Gasoline 522

Natural Gas 246 Diesel 2,883

Sulphur 86

Total 4,496 Petcoke 696

Natural Gas (fuel) 112 Total 4,256

Please see the last page of this report for important disclosures.

19

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

The financing of the project has generally been a success with attractive

terms and conditions.

Source: Tupras

* The 10 banks are Banco Bilbao Vizcaya Argentaria, S.A., The Bank Of Tokyo-Mitsubishi

Ufj, Ltd., BNP Paribas, Crédit Agricole Corporate And Investment Bank, Deutsche Bank AG-

London Branch, HSBC Bank Plc, Banco Santander, S.A., Sumitomo Mitsui Banking

Corporation Europe Limited, Societe Generale, WestLB AG- London Branch

Investments

Tupras has now completed much of its master plan capex with the

completion of the RUP. The Company’s master plan for the years 2006-

2015 totalled US$5.4bn; much of which has been completed. We expect

the Company to spend a further US$250mn on various energy efficiency

and operational excellence investments in 2015.

Source: Tupras

RUP Financing Loan (US$ mn) Tenor Terms

CESCE 1,110 4+8 Libor +3.05%

SACE 624 4+8 Libor +3.10%

Commerical* (10 banks) 359 4+3 Libor +2.85%

Total 2,093

US$1,950mn

US$1,389mn

US$5,400mn

1989-2005 2006-2010 2006-2015

Investments

Master Plan

274

355395

188 177

628

974

1,201

959

250

2006 2007 2008 2009 2010 2011 2012 2013 2014E 2015E

Capex (US$ mn)

Please see the last page of this report for important disclosures.

20

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

Dividend

Tupras has been a continuous dividend payer with attractive yields. This

situation is unlikely to change. Tupras generally pays out 90% of its net

profit or 100% of distributable income, or the maximum allowed. The

remaining US$248mn debt of the parent Company, Enerji Yatirimları

(SPV) is expected to be paid in a two year horizon. We still believe there

will be a tiny TL50mn dividend to be paid from the reserves 0.2TL DPS

from 2014 figures.

Source: Matriks

4Q14 expectations

Falling oil prices will saddle Tupras with more inventory losses in 4Q,

although Tupras is working on minimum inventory to avoid bulky losses

and these have been mitigated by plump Med margins so far. Therefore,

negative sentiment caused by falling oil prices may be partly balanced by

strong margins. Meanwhile, clement weather will be supportive

of demand. We expect Tupras to record TL214mn of EBITDA implying a

2.8% EBITDA margin in 4Q. The benefits of improvement in the refinery

margins are negatively impacted by large inventory losses owing to crude

price decline. We believe there is downside to our EBITDA expectation

depending on the inventory losses recorded in the quarter. Looking at

Tupras’ refining EBITDA in the past decade, we believe that 2014E will

most likely be one of the worst years.

Source:Tupras 2014 Tax Results

1.42

2.121.94

2.63

4.19

2.312.50

2.98

3.93 3.85

1.58

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

0.00

1.00

2.00

3.00

4.00

5.00

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Tupras: DPS & Dividend Yield (2003-2013

DPS Dividend Yield - rhs

Inventory Effect (U$mn)

2014

Crude Product Total

1.Q 11.8 38.1 49.9

2.Q -9.9 -0.9 -10.8

3.Q -22.6 -49.0 -71.6

4.Q -60.8 -143.5 -204.3

2014 Total -81.5 -155.4 -236.8

Date TUPRAS

Ref. Margins Med.Ural

Ref. Margin Diff.

2Q 2.63 2.52 0.11

3Q 4.13 1.05 3.08

4Q 2.03 0.30 1.73

1Q 2.41 0.44 1.97

2Q (0.28) 0.06 (0.34)

3Q 5.53 3.45 2.09

4Q 4.56 3.84 0.73

2013 2.45 1.67 0.78

2014 3.21 1.95 1.26

Source: Tupras 2014 Tax Results

Please see the last page of this report for important disclosures.

21

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

Turkey Demand Assumptions

TURKEY oil products demand

(000 tons) 2009 2010 2011 2012 2013 2014 E 2015 E 2016 E 2017 E 2018 E 2019 E 2020 E

LPG 3,620 3,659 3,746 3,706 3,777 3,844 3,911 3,978 4,045 4,045 4,045 4,045

Naphta 1,688 1,650 1,700 1,750 1,760 1,778 1,800 1,800 1,800 1,800 1,800 1,800

Gasoline 2,187 2,075 1,979 1,848 1,854 1,880 1,899 1,908 1,918 1,927 1,937 1,947

Jet Fuel 2,665 2,920 3,288 3,757 3,981 4,316 4,445 4,570 4,700 4,834 4,971 5,113

Diesel 13,942 14,090 14,934 15,786 16,922 17,262 17,626 18,148 18,687 19,241 19,812 20,400

Black Products 4,734 4,503 4,495 4,565 4,846 3,767 3,943 4,171 4,220 4,255 4,280 4,240

Fuel Oil 2,736 1,726 1,499 1,630 1,564 1,474 1,330 1,221 1,190 1,165 1,150 1,070

Asphalt 1,998 2,777 2,996 2,935 3,282 2,292 2,613 2,950 3,030 3,090 3,130 3,170

Other 1,528 2,218 2,467 1,915 1,819 1,829 1,846 1,816 1,821 1,831 1,834 1,836

Lube Oil 314 451 531 409 312 322 339 309 314 324 327 329

Other 1,214 1,766 1,936 1,506 1,506 1,506 1,506 1,506 1,506 1,506 1,506 1,506

Total 30,364 31,116 32,608 33,327 34,959 34,675 35,469 36,392 37,190 37,933 38,679 39,380

TURKEY DEMAND (growth)

LPG 1% 2% -1% 2% 2% 2% 2% 2% 0% 0% 0%

Naphta -2% 3% 3% 1% 1% 1% 0% 0% 0% 0% 0%

Gasoline -5% -5% -7% 0% 1% 1% 0% 0% 0% 0% 0%

Jet Fuel 10% 13% 14% 6% 8% 3% 3% 3% 3% 3% 3%

Diesel 1% 6% 6% 7% 2% 2% 3% 3% 3% 3% 3%

Black Products -5% 0% 2% 6% -22% 5% 6% 1% 1% 1% -1%

Fuel Oil -37% -13% 9% -4% -6% -10% -8% -3% -2% -1% -7%

Asphalt 39% 8% -2% 12% -30% 14% 13% 3% 2% 1% 1%

Other 45% 11% -22% -5% 1% 1% -2% 0% 1% 0% 0%

Lube Oil 44% 18% -23% -24% 3% 5% -9% 2% 3% 1% 1%

Other 46% 10% -22% 0% 0% 0% 0% 0% 0% 0% 0%

Total 2.5% 4.8% 2.2% 4.9% -0.8% 2.3% 2.6% 2.2% 2.0% 2.0% 1.8%

Demand composition

LPG 11.9% 11.8% 11.5% 11.1% 10.8% 11.1% 11.0% 10.9% 10.9% 10.7% 10.5% 10.3%

Naphta 5.6% 5.3% 5.2% 5.3% 5.0% 5.1% 5.1% 4.9% 4.8% 4.7% 4.7% 4.6%

Gasoline 7.2% 6.7% 6.1% 5.5% 5.3% 5.4% 5.4% 5.2% 5.2% 5.1% 5.0% 4.9%

Jet Fuel 8.8% 9.4% 10.1% 11.3% 11.4% 12.4% 12.5% 12.6% 12.6% 12.7% 12.9% 13.0%

Diesel 45.9% 45.3% 45.8% 47.4% 48.4% 49.8% 49.7% 49.9% 50.2% 50.7% 51.2% 51.8%

Black Products 15.6% 14.5% 13.8% 13.7% 13.9% 10.9% 11.1% 11.5% 11.3% 11.2% 11.1% 10.8%

Fuel Oil 9.0% 5.5% 4.6% 4.9% 4.5% 4.3% 3.7% 3.4% 3.2% 3.1% 3.0% 2.7%

Asphalt 6.6% 8.9% 9.2% 8.8% 9.4% 6.6% 7.4% 8.1% 8.1% 8.1% 8.1% 8.0%

Other 5.0% 7.1% 7.6% 5.7% 5.2% 5.3% 5.2% 5.0% 4.9% 4.8% 4.7% 4.7%

Lube Oil 1.0% 1.5% 1.6% 1.2% 0.9% 0.9% 1.0% 0.8% 0.8% 0.9% 0.8% 0.8%

Other 4.0% 5.7% 5.9% 4.5% 4.3% 4.3% 4.2% 4.1% 4.1% 4.0% 3.9% 3.8%

Source: Tupras

Please see the last page of this report for important disclosures.

22

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

Tupras Sales Volume Assumptions

Dom. Sales from prod. (0000 tons) 2010 2011 2012 2013 2014 E 2015 E 2016 E 2017 E 2018 E 2019 E 2020 E

LPG 701 817 827 803 803 900 915 930 930 930 930

Naphta 523 168 239 107 92 564 564 564 564 564 564

Gasoline 1,784 1,810 1,782 1,817 1,833 1,861 1,870 1,879 1,831 1,840 1,849

Jet Fuel 2,484 2,720 3,215 3,414 3,686 3,750 3,853 3,959 4,067 4,184 4,152

Gas Oils 4,637 4,961 6,959 5,303 4,350 7,344 8,539 8,712 9,045 9,189 9,536

Black Products 3,843 3,779 3,792 3,718 2,565 2,870 3,038 2,983 2,974 2,933 2,894

Fuel Oil 1,097 828 983 792 1,192 1,124 1,024 995 972 958 884

Asphalt 2,746 2,951 2,809 2,926 1,945 2,352 2,655 2,666 2,719 2,692 2,726

Others 316 380 266 162 234 282 266 269 274 276 277

Total (000 tons) 14,289 14,635 17,081 15,325 13,562 17,571 19,045 19,296 19,685 19,917 20,202

Import Volume

LPG 125 66 25 0 0 0 0 0 0 0 0

Naphta 30 34 30 30 30 30 30 30 30 30

Gasoline

Jet Fuel 156 94 118 133 146 1613 169 177 186 190 194

Gas Oils 2,076 2,910 1,609 2,809 2,350 2,350 2,350 2,500 2,500 2,500 2,500

Black Products 522 533 438 640 672 706 741 778 817 817 817

Fuel Oil 522 533 438 640 672 706 741 778 817 817 817

Asphalt

Others 1,023 420 60 80 100 100 100 100 100 100 100

Total (000 tons) 3,902 4,053 2,283 3,693 3,298 3,347 3,390 3,585 3,633 3,637 3,641

T. Dom. Sales imp+prod (tons)

LPG 826 883 852 803 803 900 915 930 930 930 930

Naphta 523 198 273 138 122 594 594 594 594 594 594

Gasoline 1,784 1,810 1,782 1,817 1,833 1,861 1,870 1,879 1,831 1,840 1,849

Jet Fuel 2,640 2,815 3,332 3,547 3,832 3,911 4,022 4,136 4,254 4,375 4,346

Gas Oils 6,713 7,871 8,568 8,113 6,700 9,694 10,889 11,212 11,545 11,689 12,036

Black Products 4,365 4,312 4,230 4,358 3,237 3,575 3,779 3,761 3,791 3,750 3,711

Fuel Oil 1,619 1,361 1,421 1,432 1,292 1,224 1,124 1,095 1,072 1,058 984

Asphalt 2,746 2,951 2,809 2,926 1,945 2,352 2,655 2,666 2,719 2,692 2,726

Others 755 857 543 463 334 382 366 369 374 376 377

Total 17,606 18,745 19,581 19,239 16,861 20,917 22,435 22,882 23,319 23,554 23,843

Export Sales (000 tons)

LPG 20 23 25 22 23 0 0 0 0 0 0

Naphta 168 14 17 15 0 0 0 0 0 0

Gasoline 2,010 2,420 2,859 2,772 2,493 3,095 3,184 3,327 3,479 3,576 3,675

Jet Fuel 110 230 119 127 29 752 874 863 851 783 865

Gas Oils 318 163 195 131 100 160 0 0 0 0 0

Black Products 2,330 2,148 2,511 1,725 2,670 3,153 3,045 2,917 2,749 2,619 2,492

Others 7 137 50 4 219 261 284 306 334 363

Total 4,795 5,152 5,860 4,844 5,333 7,379 7,364 7,391 7,386 7,311 7,395

Source: Tupras

Please see the last page of this report for important disclosures.

23

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

Tupras Production Assumptions

Capacity 2010 2011 2012 2013 2014 E 2015 E 2016 E 2017 E 2018 E 2019 E 2020 E

Total Capacity (000 tons) 28,100 28,100 28,100 28,100 28,100 28,100 28,100 28,100 28,100 28,100 28,101

Crude Oil Processed (000 tons) 19,552 20,896 22,118 21,568 20,044 24,370 25,133 25,474 25,784 25,897 26,020

CUR % 70% 74% 79% 77% 71% 87% 89.4% 90.7% 91.8% 92.2% 92.6%

Total Sales (000 tons) 23,265 24,401 26,319 25,051 23,152 29,137 30,557 30,999 31,402 31,548 31,846

Output (000 tonnes)

LPG 685 760 783 794 702 785 800 816 833 849 866

Naphta 795 532 303 146 100 100 100 100 100 100 100

Gasoline 3,809 4,292 4,571 4,573 4,346 4,955 5,055 5,206 5,310 5,416 5,525

Jet Fuel 2,621 2,875 3,293 3,545 3,550 4,502 4,727 4,822 4,918 4,967 5,017

Gas Oils 4,947 5,310 5,560 5,643 5,307 7,504 7,842 8,077 8,320 8,403 8,487

Black Products 5,197 6,172 6,287 5,645 5,403 6,023 6,083 5,900 5,723 5,552 5,385

Others 2,713 826 863 653 482 501 526 553 580 609 640

Total 20,768 20,767 21,661 21,001 19,890 24,370 25,133 25,474 25,784 25,897 26,020

Growth in output

LPG 10.7% 10.8% 3.1% 1.5% -11.7% 11.8% 2.0% 2.0% 2.0% 2.0% 2.0%

Naphta 555.2% -33.0% -43.1% -51.6% -31.9% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Gasoline -4.9% 12.7% 6.5% 0.0% -4.9% 14.0% 2.0% 3.0% 2.0% 2.0% 2.0%

Jet Fuel 30.8% 9.7% 14.6% 7.6% 0.1% 26.8% 5.0% 2.0% 2.0% 1.0% 1.0%

Gas Oils 4.9% 7.4% 4.7% 1.5% -6.0% 41.4% 4.5% 3.0% 3.0% 1.0% 1.0%

Black Products 27.2% 18.8% 1.9% -10.2% -4.3% 11.5% 1.0% -3.0% -3.0% -3.0% -3.0%

Others -8.7% -69.5% 4.4% -24.3% -26.2% 4.0% 5.0% 5.0% 5.0% 5.0% 5.0%

Yield

LPG 3.3% 3.7% 3.6% 3.8% 3.5% 3.2% 3.2% 3.2% 3.2% 3.3% 3.3%

Naphta 3.8% 2.6% 1.4% 0.7% 0.5% 0.4% 0.4% 0.4% 0.4% 0.4% 0.4%

Gasoline 18.3% 20.7% 21.1% 21.8% 21.9% 20.3% 20.1% 20.4% 20.6% 20.9% 21.2%

Jet Fuel 12.6% 13.8% 15.2% 16.9% 17.8% 18.5% 18.8% 18.9% 19.1% 19.2% 19.3%

Gas Oils 23.8% 25.6% 25.7% 26.9% 26.7% 30.8% 31.2% 31.7% 32.3% 32.4% 32.6%

Black Products 25.0% 29.7% 29.0% 26.9% 27.2% 24.7% 24.2% 23.2% 22.2% 21.4% 20.7%

Others 13.1% 4.0% 4.0% 3.1% 2.4% 2.1% 2.1% 2.2% 2.3% 2.4% 2.5%

Source: Tupras

Please see the last page of this report for important disclosures.

24

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

Tupras Key Operating Assumptions

2010 2011 2012 2013 2014 E 2015 E 2016 2017 2018 2019 2020

Crude Oil Price (Brent) $/bbl 79.47 111.27 111.58 108.66 98.99 58.00 75.00 70.00 70.00 70.00 75.00

Urals $/bbl 78.01 109.59 110.65 108.28 98.09 57.36 74.18 69.23 69.23 69.23 74.18

Crude Oil Price Discount 1.46 1.68 0.93 0.38 0.90 0.64 0.83 0.77 0.77 0.77 0.83

Tupras Refining Margin 5.87 5.48 5.11 5.27 3.21 5.04 5.22 5.28 5.28 5.37 5.31

Tons (000 tonnes)

Production 20,768 20,767 21,661 21,001 19,890 24,370 25,133 25,474 25,784 25,897 26,020

Total Domestic Sales 17,606 18,745 19,581 19,239 16,861 20,917 22,435 22,882 23,319 23,554 23,843

Sales From Production 13,704 14,692 17,298 15,546 13,562 17,571 19,045 19,296 19,685 19,917 20,202

Imports 3,902 4,053 2,283 3,693 3,298 3,347 3,390 3,585 3,633 3,637 3,641

Exports 2,886 4,147 5,083 4,149 3,920 3,075 3,992 4,045 4,089 4,338 4,434

Revenue (US$ mn)

Sales from production (US$mn) 13,696 18,450 19,731 19,045 15,967 12,870 16,200 15,580 15,796 15,890 16,905

Salesfrom imports (US$mn) 2,513 3,442 1,963 3,166 2,493 1,660 2,049 2,052 2,078 2,080 2,201

Total Sales (US$mn) 16,209 21,891 21,694 22,212 18,460 14,530 18,249 17,632 17,874 17,970 19,107

Core Production Cost (US$ mn) 12,653 17,389 18,626 17,981 15,212 11,670 14,962 14,323 14,521 14,608 15,615

Raw Material Cost 12,424 17,156 18,374 17,738 14,981 11,387 14,670 14,026 14,221 14,305 15,310

Raw Material 78.71 106.90 109.09 109.37 97.48 60.36 75.35 70.94 70.94 70.94 75.45

Crude Cost 76.2 104.4 106.6 106.9 94.8 57.7 72.7 68.2 68.2 68.2 72.8

Others 2.5 2.5 2.5 2.5 2.7 2.7 2.7 2.7 2.7 2.7 2.7

Other Production Cost (US$mn) 228.9 232.7 252.7 243.3 230.5 283.0 292.0 296.6 300.7 302.5 304.4

Other production cost (US$/bbl) 1.45 1.45 1.5 1.5 1.5 1.5 1.5 1.5 1.5 1.5 1.5

Sales from imports

Import volume (000 bbl) 28,963 29,938 16,757 26,965 23,996 24,329 24,621 26,044 26,366 26,395 26,425

Sales (US$mn) 2,513 3,442 1,963 3,166 2,493 1,660 2,049 2,052 2,078 2,080 2,201

Mark-up for imported goods 5% 3% 3% 3% 3% 3% 3% 3% 3% 3% 3%

COGS 15,283 21,012 20,834 21,357 17,967 13,579 17,233 16,588 16,815 16,887 18,029

Core production cost (US$ mn) 12,653 17,389 18,626 17,981 15,212 11,670 14,962 14,323 14,521 14,608 15,615

Cost of import (US$ mn) 2,387 3,338 1,904 3,087 2,423 1,618 1,998 2,001 2,026 2,028 2,146

Depreciation 113 153 152 133 166 160 164 159 161 144 153

Other Costs 130 131 152 155 166 131 109 106 107 108 115

Gross profit 926 879 860 854 493 951 1,016 1,044 1,059 1,083 1,078

Refining Margin 5.87 5.48 5.11 5.27 3.21 5.04 5.22 5.28 5.28 5.37 5.31

Please see the last page of this report for important disclosures.

25

February 23, 2015

Oil - Refinery

Tupras

RESEARCH

APPENDIX

3Q14 Results - Solid 3Q, positive margins

2014 Tax Financials

Tupras announced TL85mn net loss in its 2014 tax financials versus

TL337mn net profit recorded a year ago. Operational results point to a

US$204mn FX loss in 4Q14 totaling US$236mn FX loss for the whole

year. Refining margin came in as US$4.56 versus US$2.03/bbl refining

margin in 4Q13.

2014 2013 Change

Sales (TL mn) 39,817.0 41,199.7 -3.4% EBIT (TL mn) 859.3 842.348 2.0%

Net Income (before tax) (TL mn) -81.66 336.8 n.m.

Net Income (TL mn) 85.24 - -

Tupras Refining Margin ($/bbl) 4.56 2.03 2.53

Med Refining Margin ($/bbl) 3.84 0.30 3.54

CUR (%) 74.9% 79.1% -4.2 pp

Inventory Gain/(Loss) (US$ mn) (236.80) 93.84 n.m.

Tupras Summary Financials

(mn TL) 3Q13 4Q13 1Q14 2Q14 3Q14 9M13 9M14 3Q14/3Q13 3Q14/2Q14 9M14/9M13

Net Sales 12,167 10,596 9,276 9,598 11,812 30,482 30,686 -3% 23% 1%

Gross Profit 661 335 409 28 600 1,139 1,037 -9% 2018% -9%

Operating Profit 493 125 251 -127 423 649 547 -14% n.m. -16%

EBITDA 553 185 313 -64 488 829 737 -12% n.m. -11%

Net Other Income/Expense -121 -446 21 107 -273 -287 -144 n.m. n.m. n.m.

Financial Inc./ Exp. (net) -1 -15 -63 -69 -36 -95 -169 n.m. n.m. n.m.

Tax 404 437 281 444 249 749 975 -38% -44% 30%

Tax on Income (Expenses) -5 0 -4 2 -1 -6 -3 n.m. n.m. n.m.

Inc. (Exp.) of Deferred Tax 409 438 285 442 250 755 977 -39% -43% 29%

Minority Interests 1 -2 2 3 2 4 7 60% -39% 98%

Net Income 818 114 511 358 377 1,084 1,246 -54% 6% 15%

Net Cash -2,563 -2,859 -4,367 -3,969 -3,642 -2,563 -3,642

Working Capital -813 -1,381 -552 -1,808 -2,646 -813 -2,646

Shareholders Equity 5,016 5,139 5,258 5,616 5,998 5,016 5,998

Ratios

Gross Margin 5.4% 3.2% 4.4% 0.3% 5.1% 3.7% 3.4% -0.4 pp 4.8 pp -0.4 pp

Operating Margin 4.1% 1.2% 2.7% n.m. 3.6% 2.1% 1.8% -0.5 pp n.m. -0.3 pp

EBITDA Margin 4.5% 1.7% 3.4% n.m. 4.1% 2.7% 2.4% -0.4 pp n.m. -0.3 pp

Net Profit Margin 6.7% 1.1% 5.5% 3.7% 3.2% 3.6% 4.1% -3.5 pp -0.5 pp 0.5 pp

Change

Please see the last page of this report for important disclosures.

RESEARCH

26

Disclaimer

Recommendation History

Source: Garanti Securities

Definition of Stock Ratings

OUTPERFORM (OP) The stock's return is expected to exceed the return of the BIST100 in 12 months.

MARKET PERFORM (MP) The stock's return is expected to be in line with the BIST100 in 12 months.

UNDERPERFORM (UP) The stock's return is expected to fall below the return of the BIST100 in 12 months.

Disclaimer

This document and the information, opinions, estimates and recommendations expressed herein,

have been prepared by Garanti Securities Research Department, to provide its customers with

general information regarding the date of issue of the report and are subject to changes without prior

notice. All opinions and estimates included in this report constitute our judgment as of this date and

are subject to change without notice.

This document and its contents do not constitute an offer, invitation or solicitation to purchase or

subscribe to any securities or other instruments, or to undertake or divest investments. Neither shall

this document nor its contents form the basis of any contract, commitment or decision of any kind.

Investors who have access to this document should be aware that the securities, instruments or

investments to which it refers may not be appropriate for them due to their specific investment goals,

financial positions or risk profiles, as these have not been taken into account to prepare this report.

Therefore, investors should make their own investment decisions considering the said circumstances

and obtaining such specialized advice as may be necessary. The information in this report has been

obtained by Garanti Securities Research Department from sources believed to be reliable. However,

Garanti Securities cannot guarantee the accuracy, adequacy, or completeness of such information,

and cannot be responsible for the results of investment decisions made on account of this report.

The market prices of securities or instruments or the results of investments could fluctuate against

the interests of investors. Investors should be aware that they could even face a loss of their

investment. Transactions in futures, options and securities or high-yield securities can involve high

risks and are not appropriate for every investor. Indeed, in the case of some investments, the

potential losses may exceed the amount of initial investment and, in such circumstances, investors

may be required to pay more money to support those losses. Thus, before undertaking any

transaction with these instruments, investors should be aware of their operation, as well as the rights,

liabilities and risks implied by the same and the underlying stocks. Investors should also be aware

that secondary markets for the said instruments may be limited or even not exist.

This report is to be distributed to professional emerging markets investors only. This report is for

private use only and intended solely for the individual(s). No information in this report may be copied,

modified, republished or exploited in anyway without the prior consent of Garanti Securities.

Additionally, with respect to our statements above, all our claims and plea rights are covered in the

regulations which apply in the countries that this report has been sent to.

Garanti Securities

Etiler Mah. Tepecik Yolu

Demirkent Sokak No:1

34337 Besiktas, Istanbul / Turkey

Phone: +90 (212) 384-1155

Fax: +90 (212) 352-4240

RESEARCH