Conference on Thailand-Mexico and Southeast Asia-Latin ...

58

INTEGRATION PROCESSES OF THAILAND WITH ASEAN ECONOMIC COMMUNITY AND LATIN AMERICA Bhanupong Nidhiprabha Faculty of Economics Thammasat University [email protected] Conference on Thailand-Mexico and Southeast Asia-Latin American Relations University of Colima September 23, 2011

Transcript of Conference on Thailand-Mexico and Southeast Asia-Latin ...

INTEGRATION PROCESSES OF THAILAND WITH ASEAN ECONOMIC COMMUNITY AND LATIN AMERICA Bhanupong Nidhiprabha

Faculty of Economics Thammasat University [email protected]

Conference on Thailand-Mexico and Southeast Asia-Latin American Relations University of Colima September 23, 2011

Main themes

Globalization

Free trade agreements

Trade and geography

Thailand’s direction of trade

Shocks and transmission mechanism

Asian Economic Community

Fiscal and monetary spaces

2

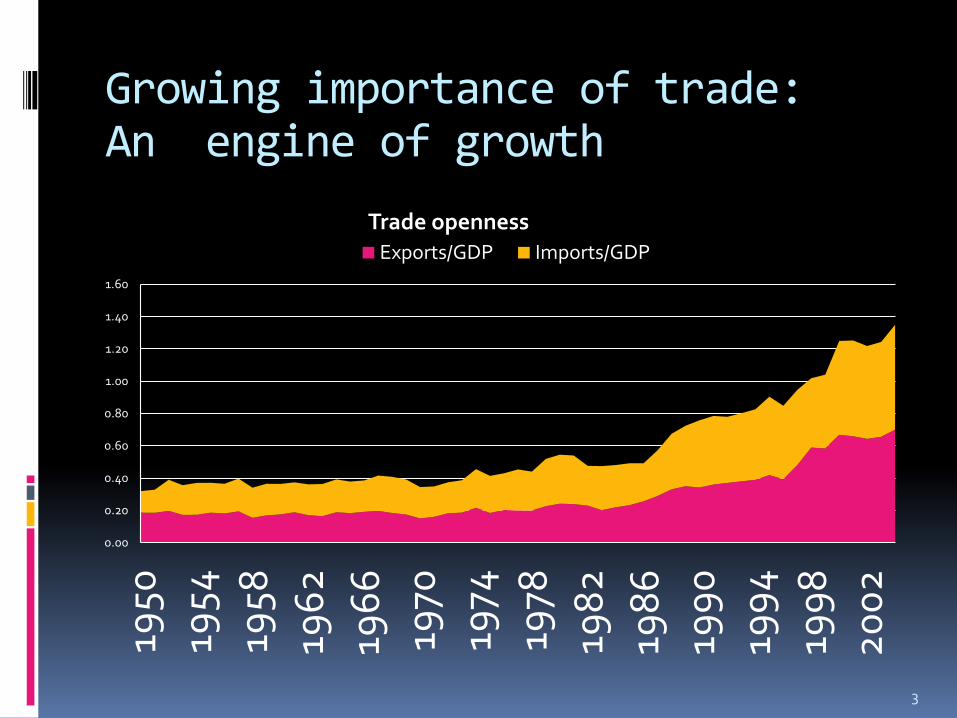

Growing importance of trade: An engine of growth

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1950

1954

1958

196

2

196

6

1970

1974

1978

198

2

198

6

199

0

199

4

199

8

20

02

Trade openness Exports/GDP Imports/GDP

3

4

0

0.2

0.4

0.6

0.8

1

1.2

1.4

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

p

Degree of Openness to trade Exports/GDP Imports/GDP

5

Jan

-06

Feb

-06

Mar

-06

Ap

r-0

6

May

-06

Jun

-06

Jul-

06

Au

g-0

6

Sep

-06

Oct

-06

No

v-0

6

Dec

-06

Jan

-07

Feb

-07

Mar

-07

Ap

r-0

7

May

-07

Jun

-07

Jul-

07

Au

g-0

7

Sep

-07

Oct

-07

No

v-0

7

Dec

-07

Jan

-08

Feb

-08

Mar

-08

Ap

r-0

8

May

-08

Jun

-08

Jul-

08

Au

g-0

8

Sep

-08

Oct

-08

1.4

1.6

1.8

2

2.2

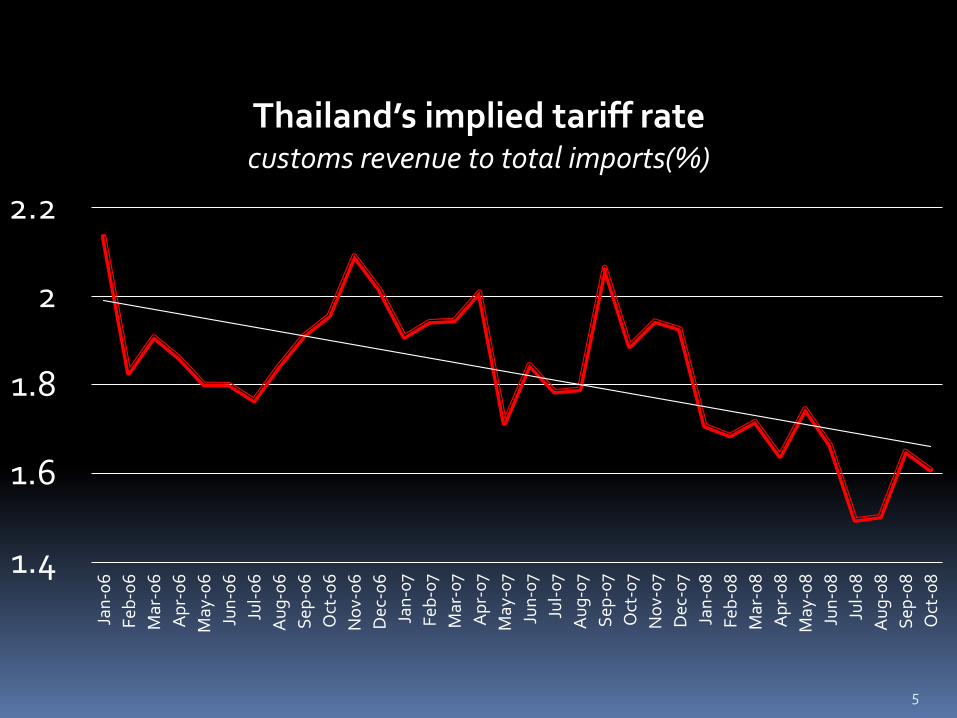

Thailand’s implied tariff rate customs revenue to total imports(%)

6

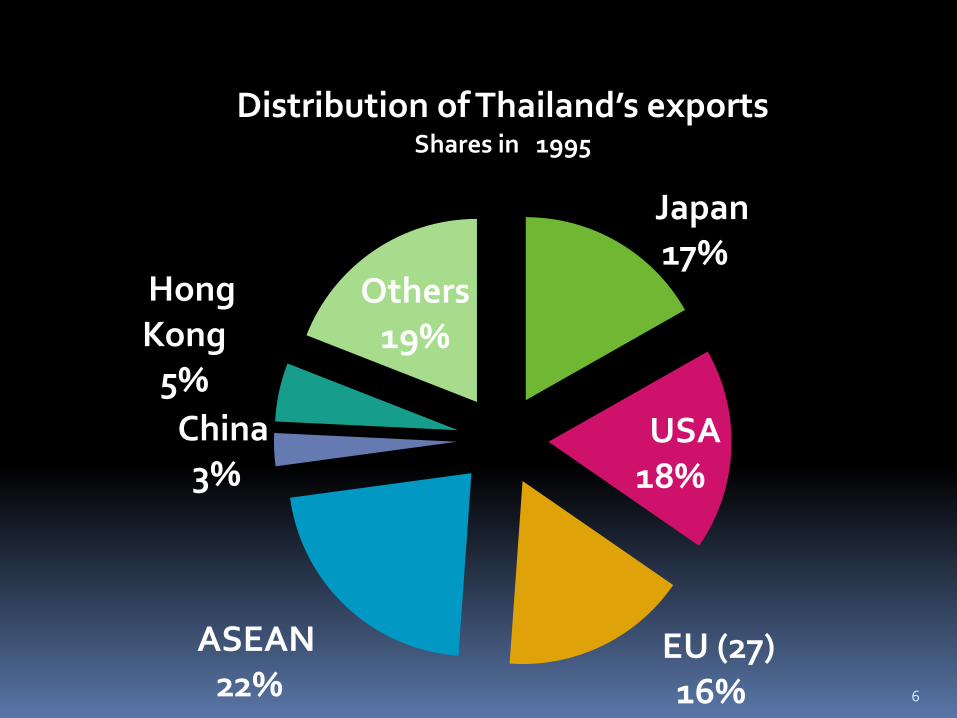

Japan 17%

USA 18%

EU (27) 16%

ASEAN 22%

China 3%

Hong Kong

5%

Others 19%

Distribution of Thailand’s exports Shares in 1995

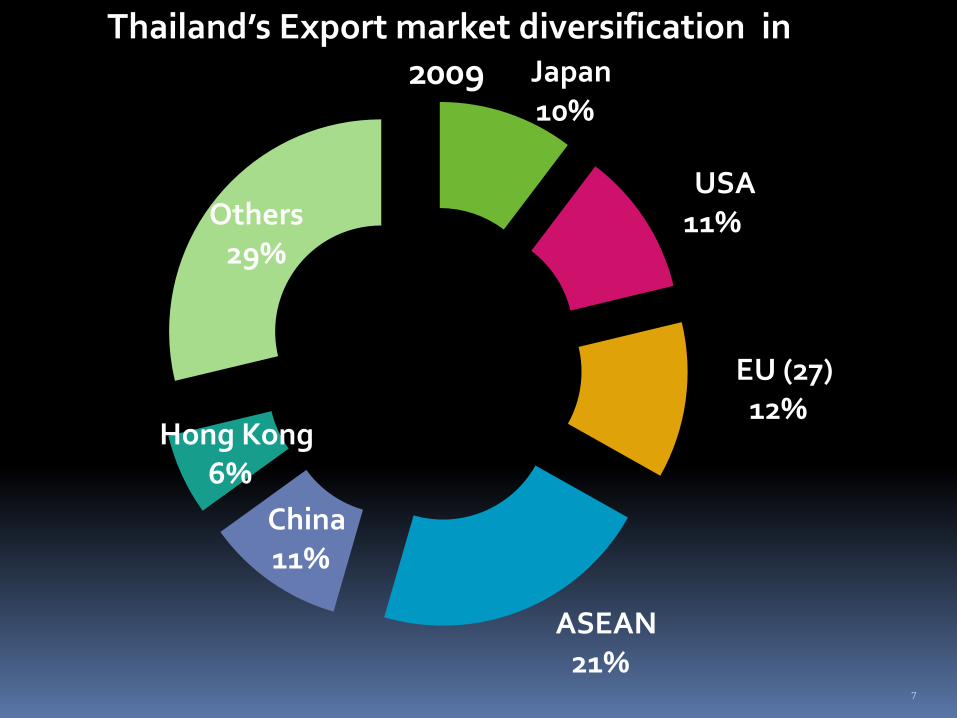

7

Japan 10%

USA 11%

EU (27) 12%

ASEAN 21%

China 11%

Hong Kong 6%

Others 29%

Thailand’s Export market diversification in 2009

ASEAN Countries

Small countries in South East Asia can avoid the limitation of their domestic market by exploiting the economies of scale from the ASEAN’s 550 million population with a GDP of 1.4 trillion USD

8

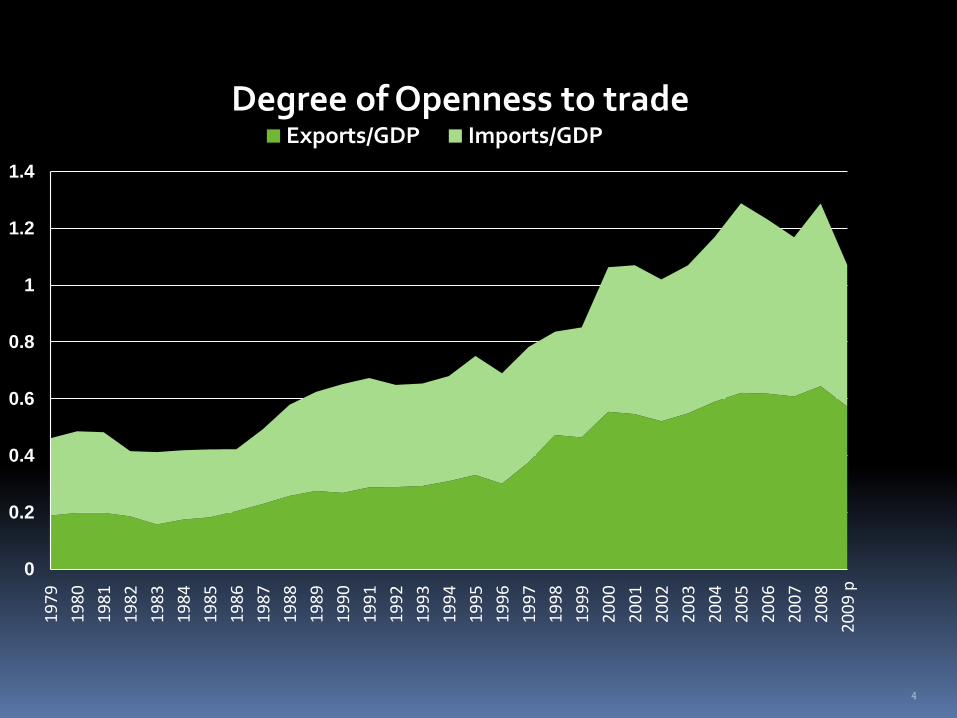

An integral part of the world economy

Thailand has increasingly become an integral part of the world economy.

By 1996, the value of international trade was as large as the size of GDP.

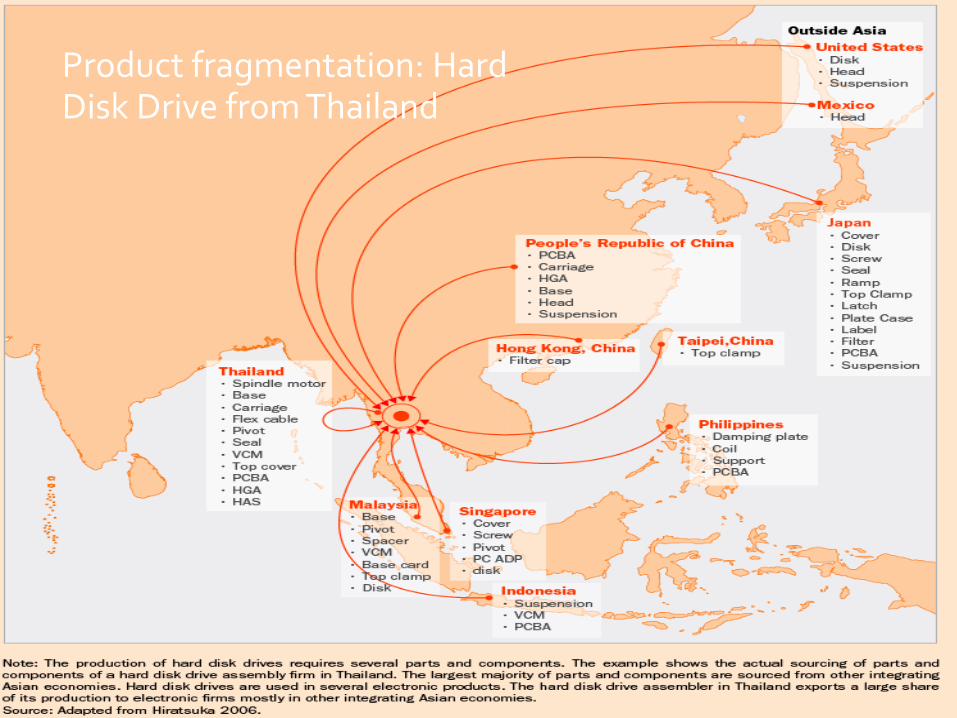

The degree of Asian regional integration of Thailand has been more pronounced through foreign investment in production fragmentation.

Trade fragmentation in parts and components of HDD

9

10

Product fragmentation: Hard Disk Drive from Thailand

11

Multiple Free Trade Agreements January 2010

COUNTRY

UNDER NEGOTIATION CONCLUDED

TOTAL Proposed

Framework

Agreement Signed/Under Ne

gotiation Under

Negotiation Signed In Effect

Australia 6 1 5 0 8 20

China 8 2 4 1 9 24

India 12 4 6 1 10 33

Philippines 4 0 1 0 7 12

Singapore 5 0 9 2 18 34

Viet Nam 2 0 2 0 7 11

Thailand 6 4 3 0 11 24

Existing bilateral trade agreements

Australia

New Zealand

Japan

China

India

Preferential exports contributed only 14.8 % of total exports in 2009.

12

ROO and NTBs

Rules of origin must be simplified to facilitate administration procedure without causing trade diversion or act as a hidden instrument to protect domestic industry.

If Thailand continues to reduce MFN tariff rates, the cost associated with the rules of origin can also be reduced.

The spaghetti bowl effect has been exaggerated.

Non-tariff barriers such as Sanitary and Phytosanitary (SPS) conditions must be agreed upon to make sure that they are not substitutes for the tariff reductions.

13

Political economy and leaders’ willpower

The comparative disadvantage sectors would strongly oppose FTAs, fearing that they would not be able to compete and would soon be wiped out.

Political economy plays an important part in deciding the direction of the FTAs.

Political will is a crucial factor in determining the speed and the coverage of the regional integration.

14

To forge ahead with integration There are trade-offs between benefits and

adverse consequences of new regionalism.

As long as the net benefits of expansion along the line of globalization exist, we should cautiously go ahead with multiple FTAs.

We should not let short-term micro adverse impacts obscure the long-term macro dynamic gains from rapid integrating into the world economy.

15

New Regionalism: Multiple FTAs

Thailand’s rush to negotiate FTAs with many countries, including USA, Japan, Australia, New Zealand, Bahrain, India, China, Chile, and Peru, can be described as new regionalism.

Although Japan had already established FTAs with Singapore, Thailand was a more difficult case for Japan, since negotiations involved agriculture and labor issues.

Singapore had already removed most of her tariff barriers, while the two countries’ levels of per capita income do not differ much.

16

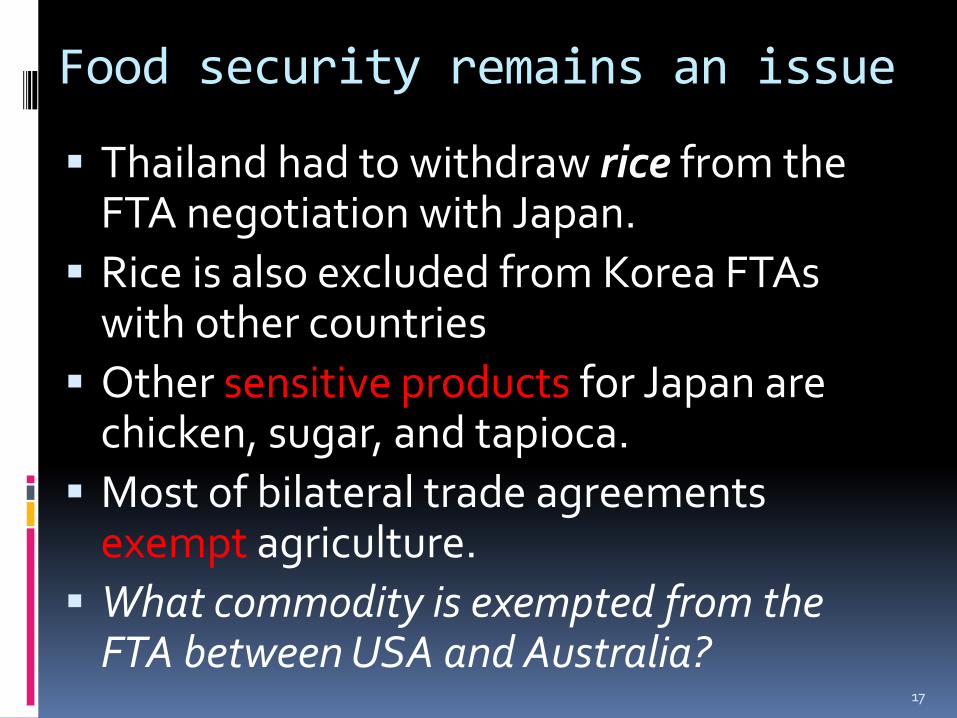

Food security remains an issue

Thailand had to withdraw rice from the FTA negotiation with Japan.

Rice is also excluded from Korea FTAs with other countries

Other sensitive products for Japan are chicken, sugar, and tapioca.

Most of bilateral trade agreements exempt agriculture.

What commodity is exempted from the FTA between USA and Australia?

17

Four sensitive items

ASEAN Free Trade Agreement (AFTA) is the most comprehensive free trade agreement, but Thailand cannot afford the removal of protection in four commodities:

Fresh-cut flowers

Dried coconut

Potatoes

coffee

18

Aspects of economic integration

Free flows of trade

Free flows of services

Mobility in skilled labor

Free flows of capital

Free flows of investment

19

ASEAN Economic Community

Trade liberalization under the AEC builds upon achievements over the past decades which began with trade integration under the ASEAN Free Trade Area (AFTA), signed in 1992.

Under AFTA, a substantial reduction of tariffs has already been achieved.

As of January 2010, ASEAN-6 applied zero tariffs to 99 percent of goods, while the CLMV countries plan to achieve the same goal by 2015.

20

The AEC blueprint

What the AEC aims to “transform ASEAN into a

single market and production base, a highly

competitive economic region, a region of

equitable economic development, and a region

fully integrated into the global economy”.

“Open regionalism” in a single market and

production base is expected to minimize

transaction costs and maximize trade gains.

But we need to standardize VAT and corporate income tax rates

21

Foreign ownership in service sector

Healthcare

Tourism

Air transport

Banking sector

ASEAN investors should have already been allowed to hold up to 70% of equity share in these sensitive sectors.

22

23

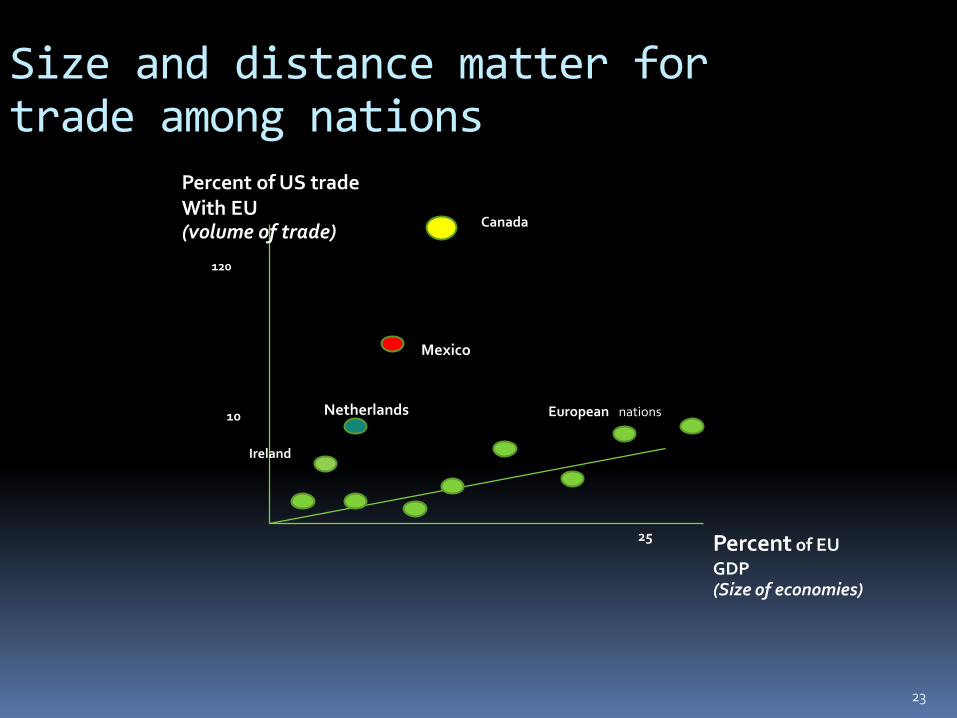

Size and distance matter for trade among nations

Percent of EU

GDP (Size of economies)

Percent of US trade With EU (volume of trade)

European nations

Canada

Mexico

Netherlands

Ireland

10

120

25

24

CLMVT countries

25

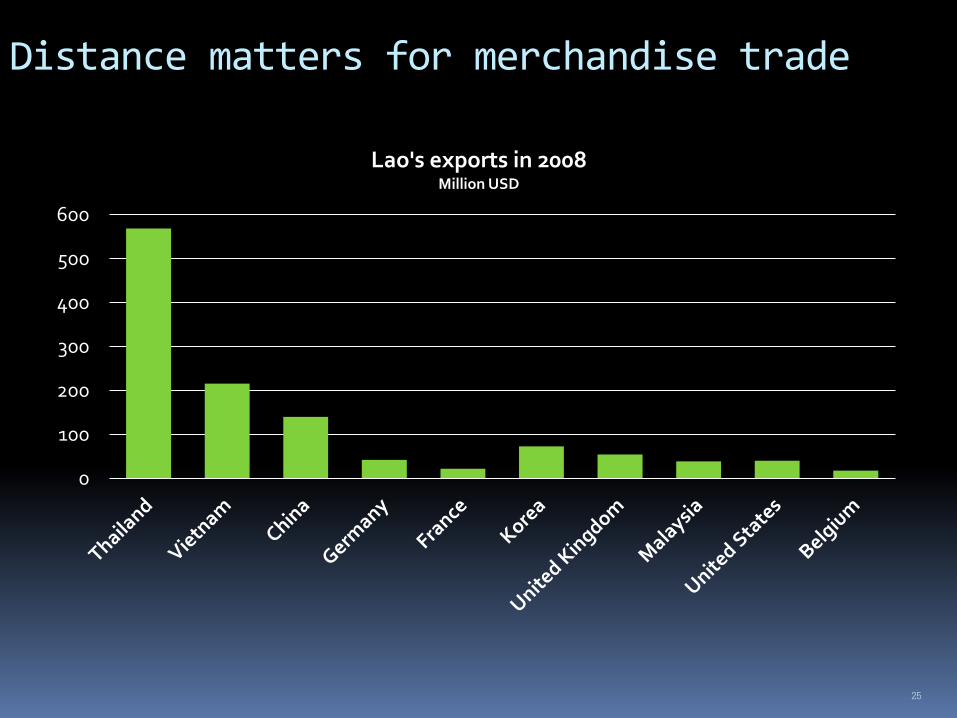

Distance matters for merchandise trade

0

100

200

300

400

500

600

Lao's exports in 2008 Million USD

Public investment in cross boarder transportation promote intra-regional trade

Transportation costs play a crucial role in shaping international and interregional trade. (Distance matters)

The interaction of market size with increasing returns plays an important role in determining the location of production.

Home market effect is a major explanation of trade through differences in population density and localized specialization.

A cumulative process in which large markets (ASEAN single market) attract production leads to agglomeration.

26

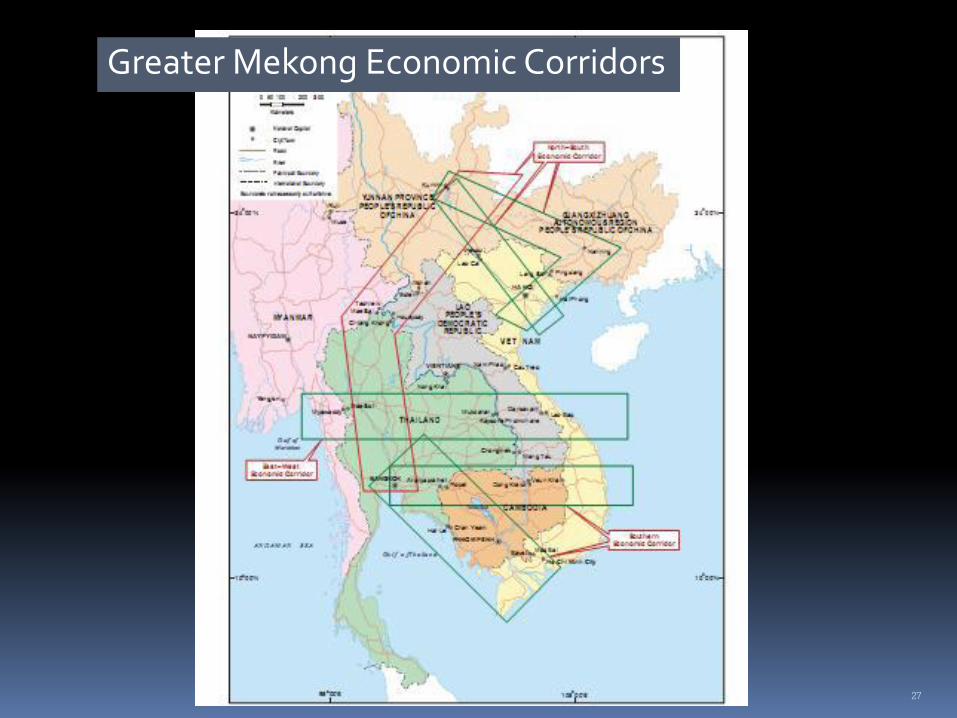

27

Greater Mekong Economic Corridors

But there is adverse impact of globalization

Exposure to external shocks

Export dependency

Increase business synchronization

Destroy traditional (uncompetitive) sectors

28

29

-20

-15

-10

-5

0

5

10

15

20

25

30

35

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

2010

pe

rce

nt

Export (%change) World Income (%change)

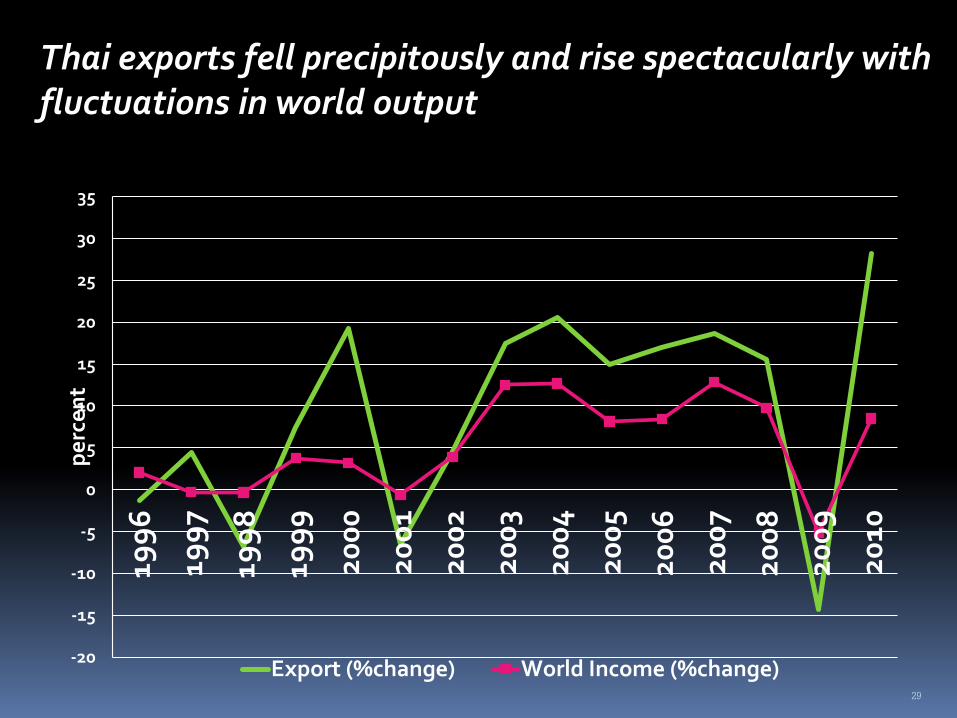

Thai exports fell precipitously and rise spectacularly with fluctuations in world output

Global recession is imminent

The IMF: Global growth will shrink to 4% in 2012, from 5% last year due to "major financial turbulence in the eurozone".

ASEAN needs a new growth pole

30

31

32

-15

-10

-5

0

5

10

15

20

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

2010

Ou

tpu

t g

row

th:

pe

rce

nt

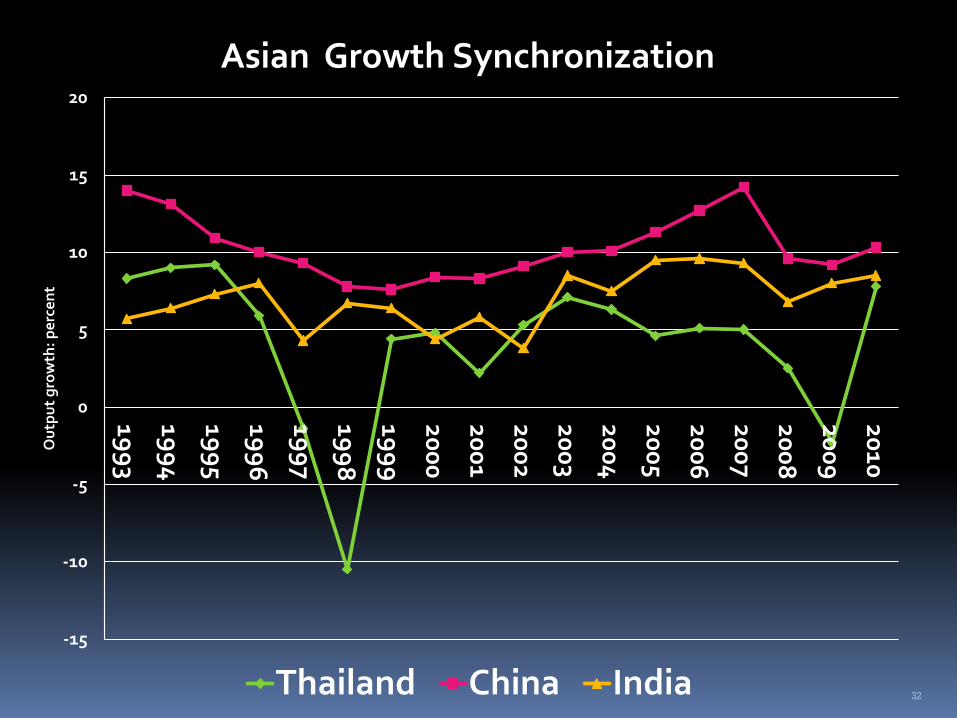

Asian Growth Synchronization

Thailand China India

33

Source: Eclipse, Arvind Subramanian Peterson Institute for International Economics

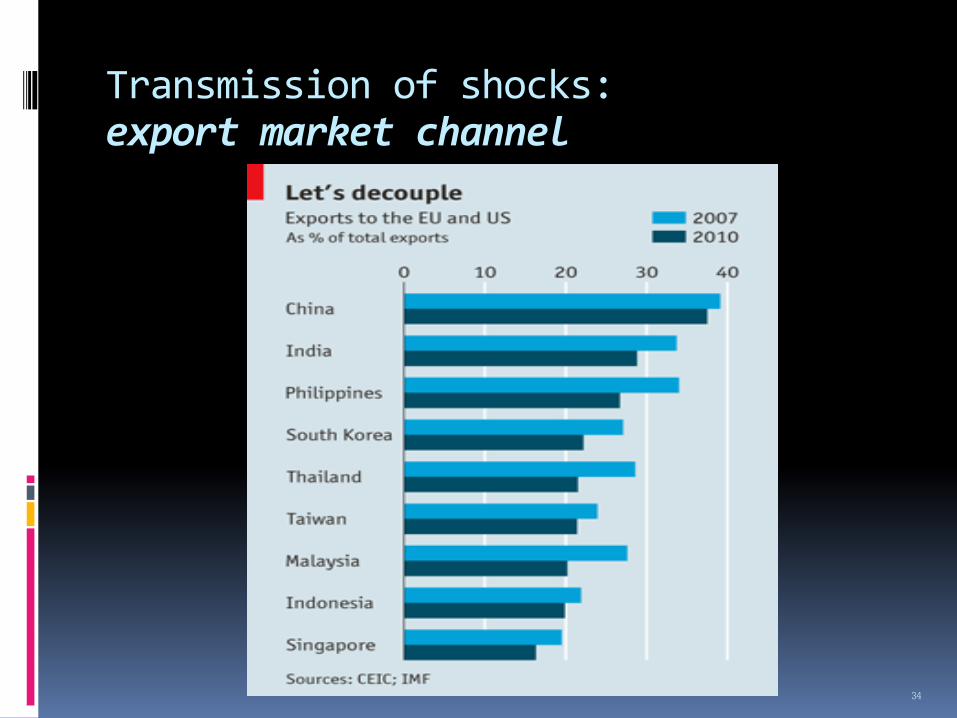

Transmission of shocks: export market channel

34

35

0

5000

10000

15000

20000

25000

199

3

199

5

199

7

199

9

20

01

20

03

20

05

20

07

20

09

mil

lion

US

D

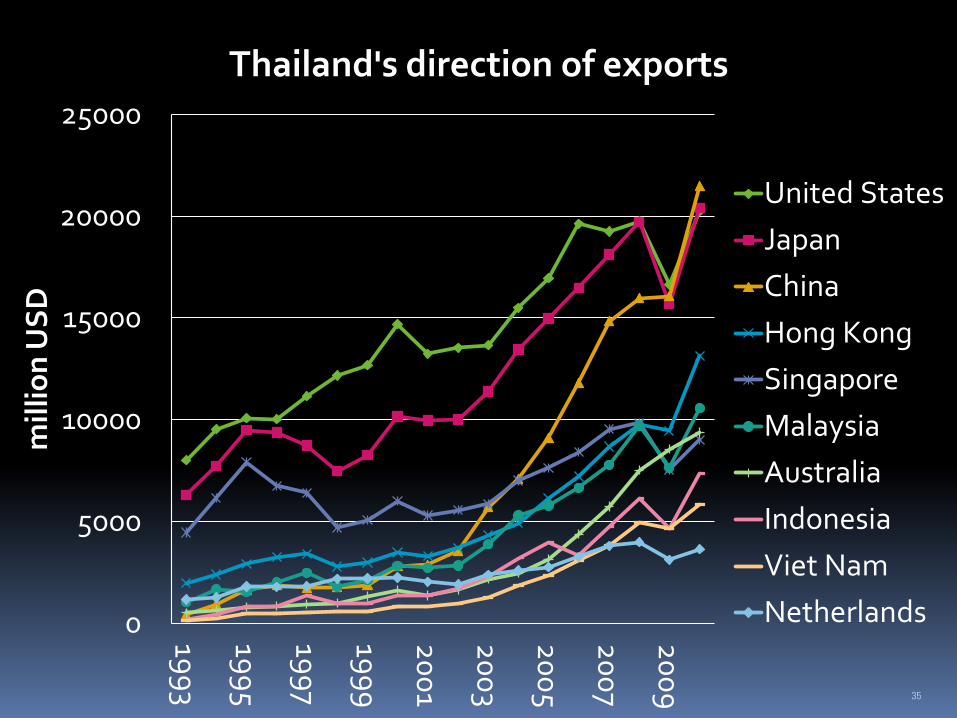

Thailand's direction of exports

United States

Japan

China

Hong Kong

Singapore

Malaysia

Australia

Indonesia

Viet Nam

Netherlands

36

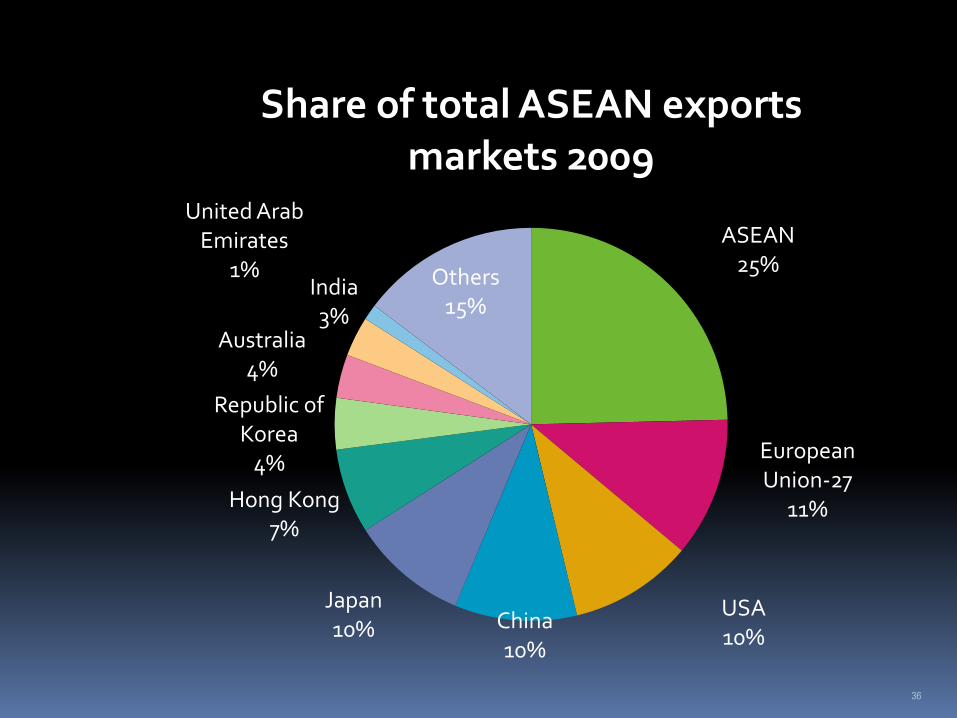

ASEAN 25%

European Union-27

11%

USA 10%

China 10%

Japan 10%

Hong Kong 7%

Republic of Korea

4%

Australia 4%

India 3%

United Arab Emirates

1% Others 15%

Share of total ASEAN exports markets 2009

37

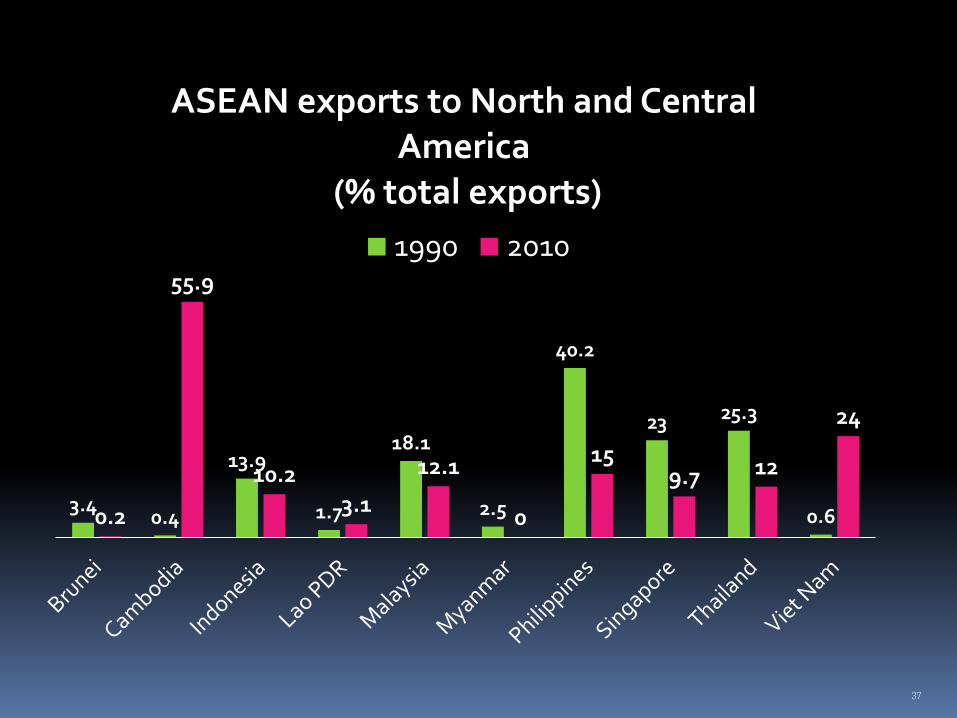

3.4 0.4

13.9

1.7

18.1

2.5

40.2

23 25.3

0.6 0.2

55.9

10.2 3.1

12.1

0

15 9.7 12

24

ASEAN exports to North and Central America

(% total exports)

1990 2010

38

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

199

3

199

5

199

7

199

9

20

01

20

03

20

05

20

07

20

09

mill

ion

US

D

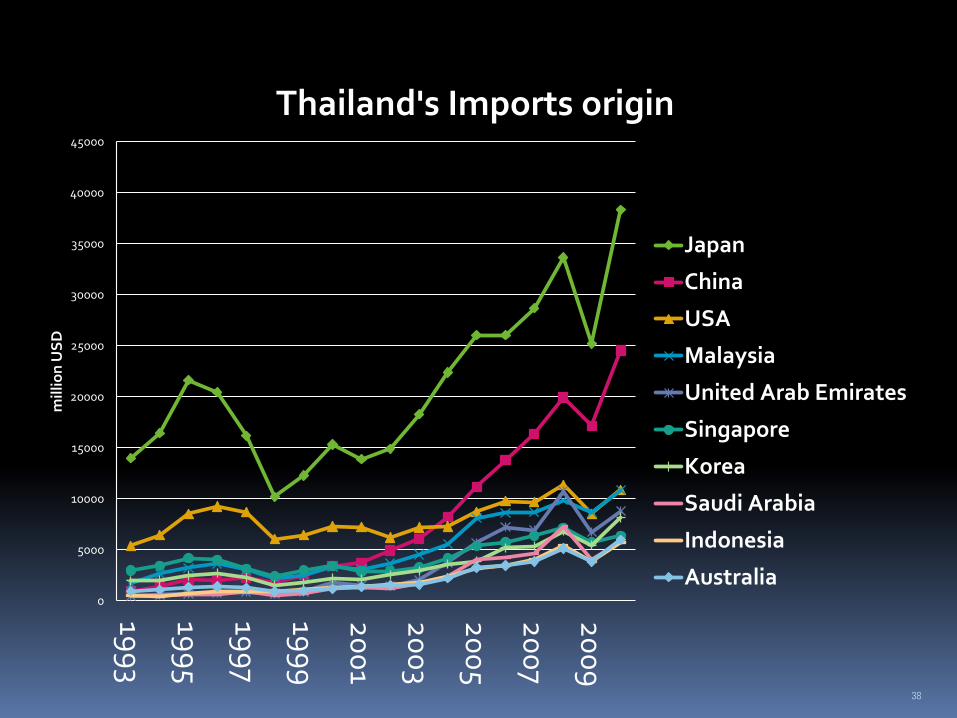

Thailand's Imports origin

Japan

China

USA

Malaysia

United Arab Emirates

Singapore

Korea

Saudi Arabia

Indonesia

Australia

39

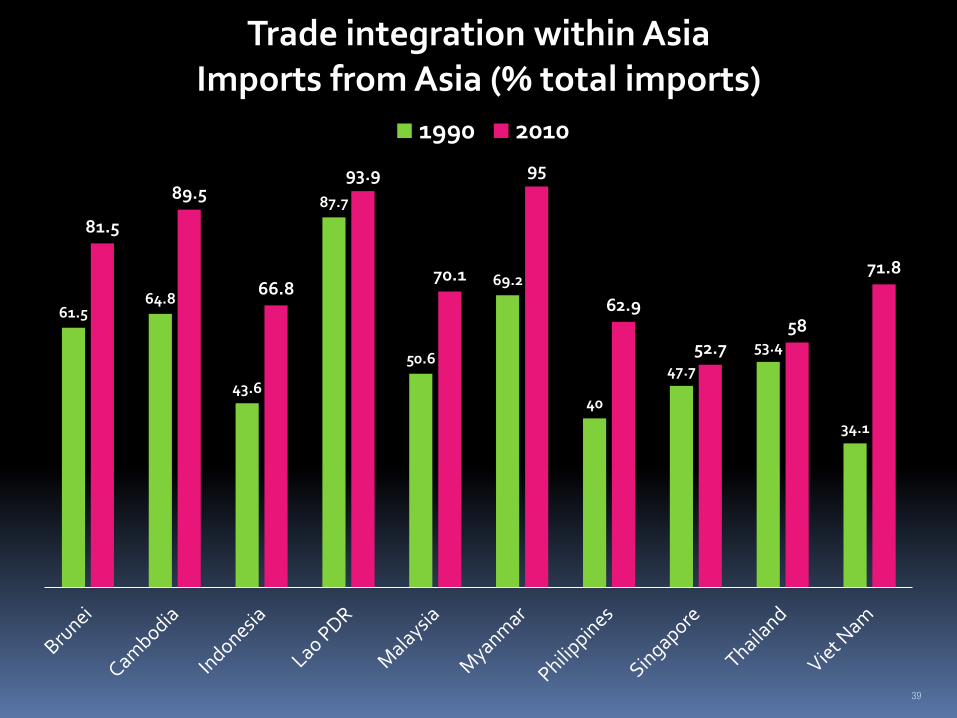

61.5 64.8

43.6

87.7

50.6

69.2

40

47.7

53.4

34.1

81.5

89.5

66.8

93.9

70.1

95

62.9

52.7 58

71.8

Trade integration within Asia Imports from Asia (% total imports)

1990 2010

40

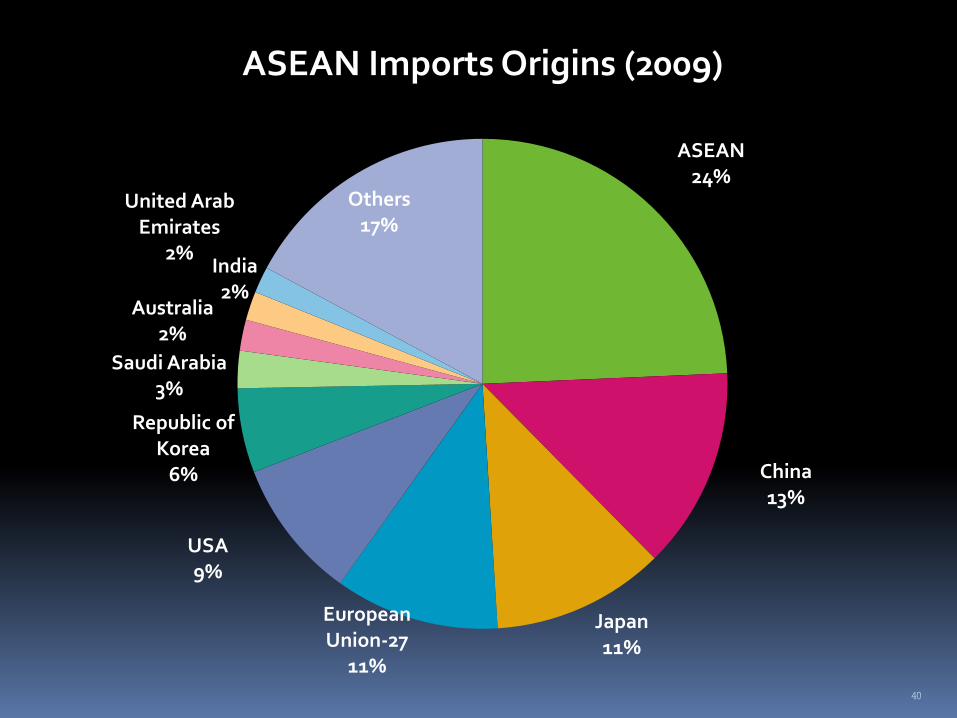

ASEAN 24%

China 13%

Japan 11%

European Union-27

11%

USA 9%

Republic of Korea

6%

Saudi Arabia 3%

Australia 2%

United Arab Emirates

2% India

2%

Others 17%

ASEAN Imports Origins (2009)

41

61.5 64.8

43.6

87.7

50.6

69.2

40

47.7

53.4

34.1

81.5 89.5

66.8

93.9

70.1

95

62.9

52.7 58

71.8

Direction of Merchandise Trade: Asia Imports (% total imports)

1990 2010

42

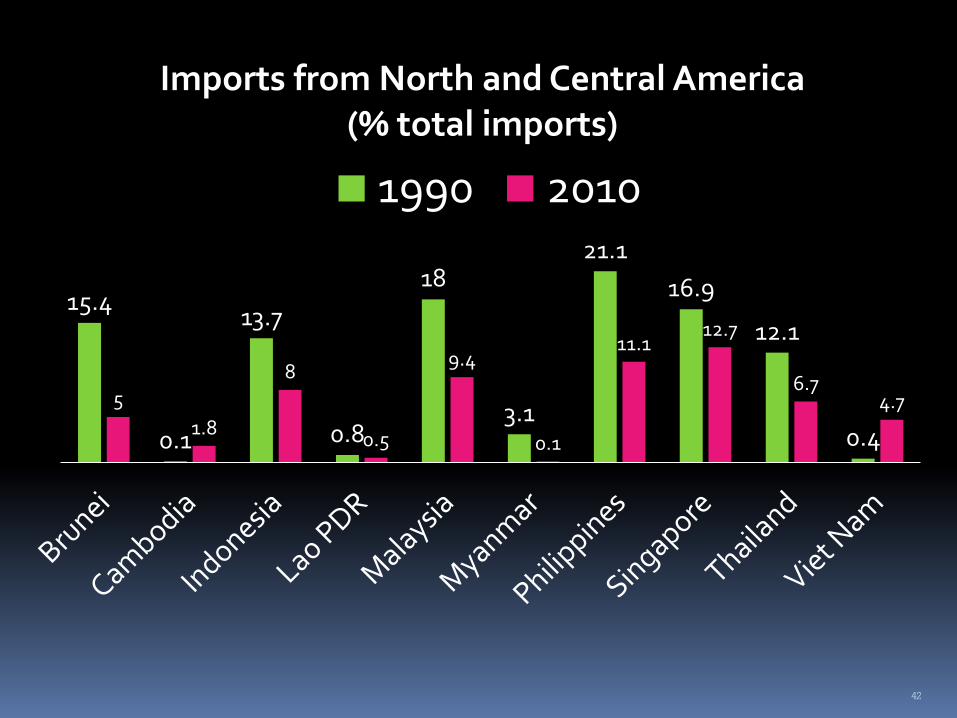

15.4

0.1

13.7

0.8

18

3.1

21.1

16.9

12.1

0.4

5

1.8

8

0.5

9.4

0.1

11.1 12.7

6.7 4.7

Imports from North and Central America (% total imports)

1990 2010

43

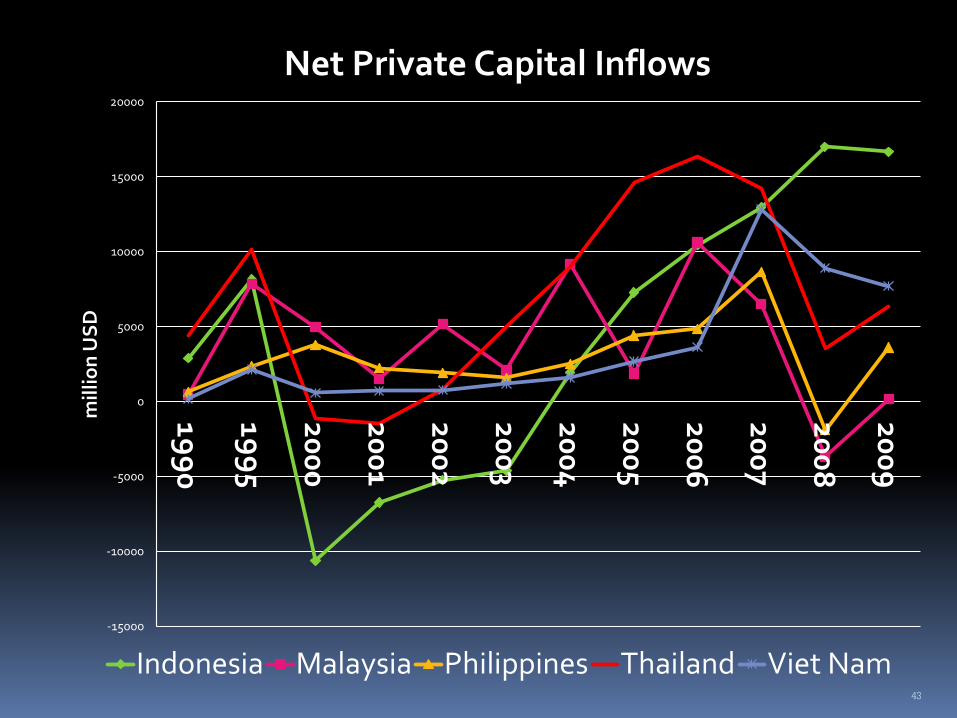

-15000

-10000

-5000

0

5000

10000

15000

20000

199

0

199

5

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9m

illi

on

US

D

Net Private Capital Inflows

Indonesia Malaysia Philippines Thailand Viet Nam

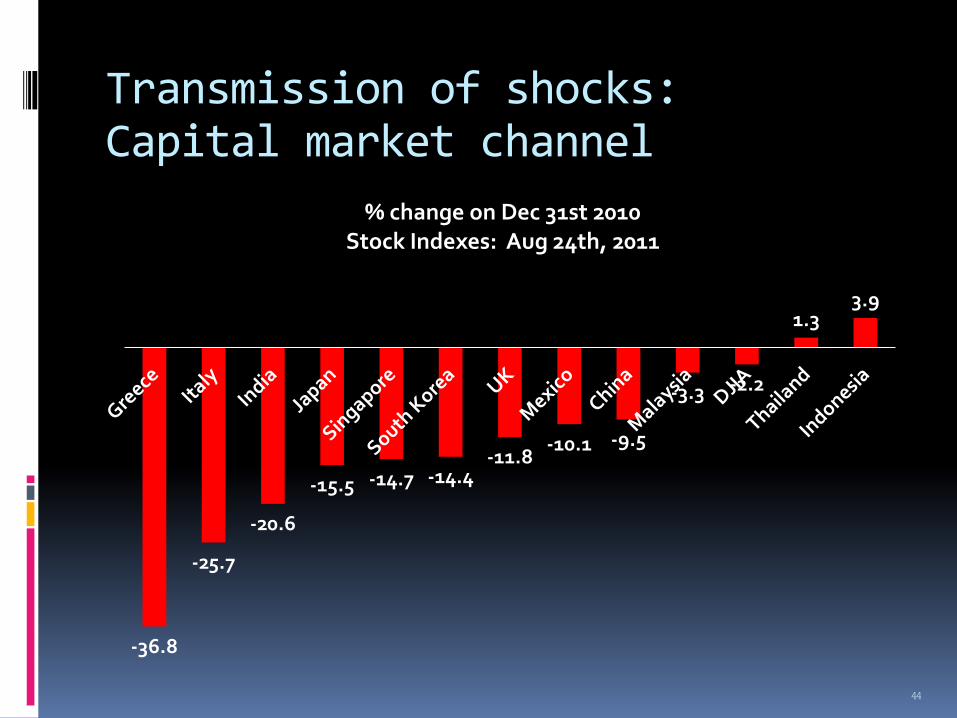

Transmission of shocks: Capital market channel

-36.8

-25.7

-20.6

-15.5 -14.7 -14.4 -11.8

-10.1 -9.5

-3.3 -2.2

1.3 3.9

% change on Dec 31st 2010 Stock Indexes: Aug 24th, 2011

44

45

46

Long-term unemployment can lead to marginalization from the labor market through depreciation of skills and a loss of motivation

Tax reform

Reduction in corporate income tax rate affects the effectiveness of fiscal automatic stabilizers.

Tax revenue structure reflects output and employment structure.

Difficult to imitate tax structure in countries with higher level of development

47

Don’t say no to domestic reform

Integrating the Thai economy with the regional trade bloc can serve as an instrument to speed up domestic reform.

Temporary subsidies to adversely affected industries are required to ease adjustment costs.

Firm datelines imposed by AEC imply more enthusiastic efforts to carry out difficult reform.

48

The big push

Utilization of free trade provisions remain relatively low due to high marginal transaction costs imposed by Rules of Origin.

Watch out: Non-tariff barriers are substitutes for tariff reduction.

Sensitive commodities are dictated by political interest.

A surge in the number of Thailand’s FTA negotiations should not be interpreted as diminished commitment to the multilateralism.

49

Lack of fiscal space: limit to fiscal stimulus

50

Fiscal expenditure

Productivity and human capital

Health capital

Focus spending on high-social rate of return

Avoid fiscal splurge

Spender of the last resort

51

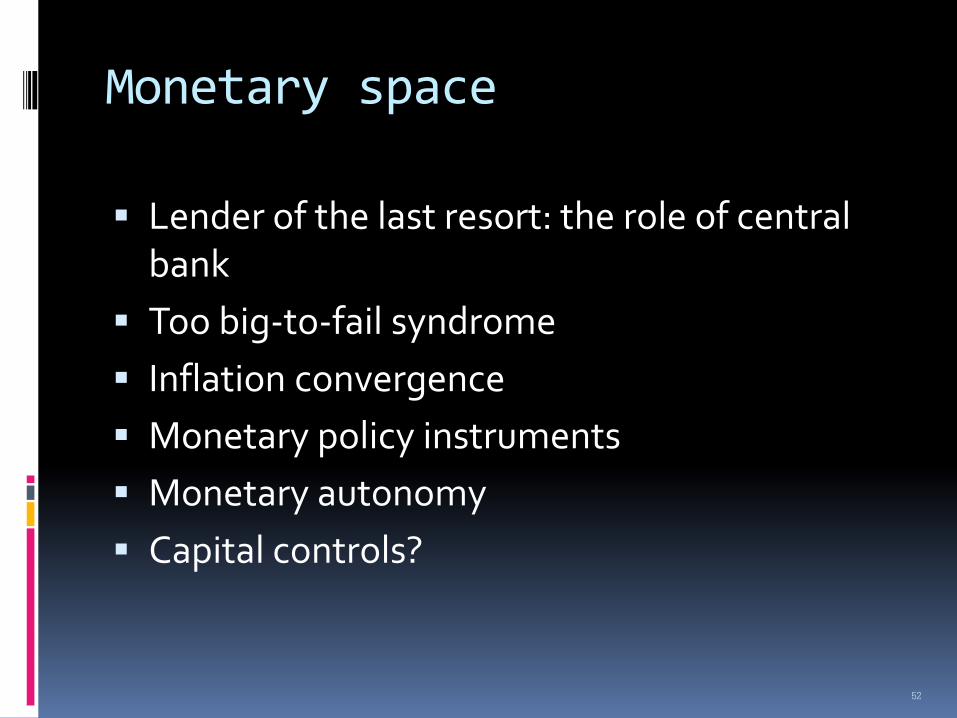

Monetary space

Lender of the last resort: the role of central bank

Too big-to-fail syndrome

Inflation convergence

Monetary policy instruments

Monetary autonomy

Capital controls?

52

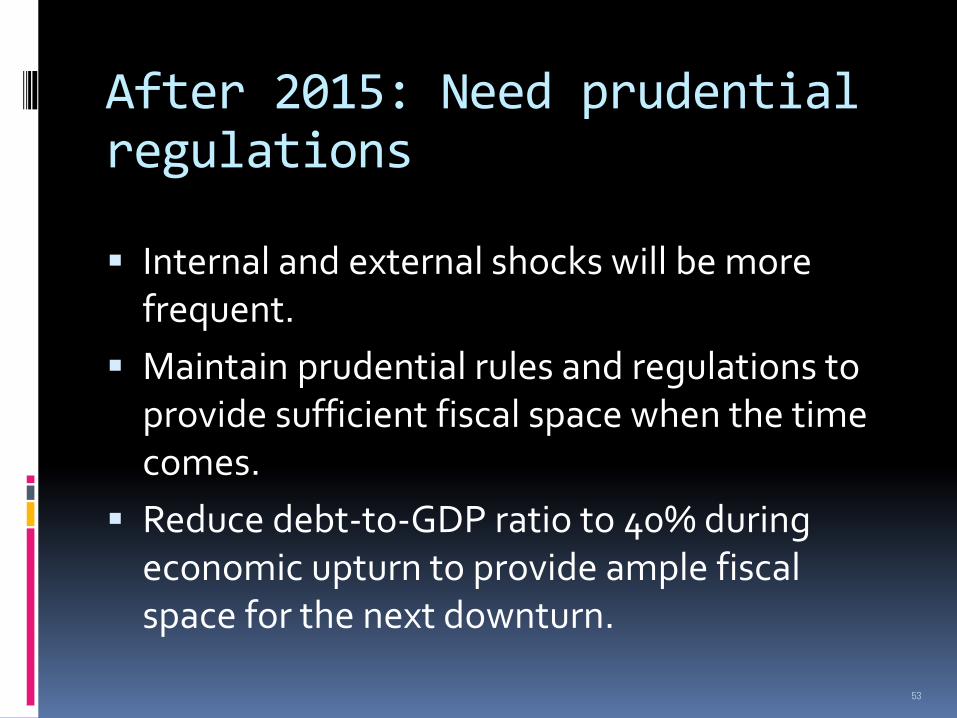

After 2015: Need prudential regulations

Internal and external shocks will be more frequent.

Maintain prudential rules and regulations to provide sufficient fiscal space when the time comes.

Reduce debt-to-GDP ratio to 40% during economic upturn to provide ample fiscal space for the next downturn.

53

Beyond the integration

Labor migration and wage differentials

Income convergence

Low unemployment

Price stability

Crisis contagion

Poverty

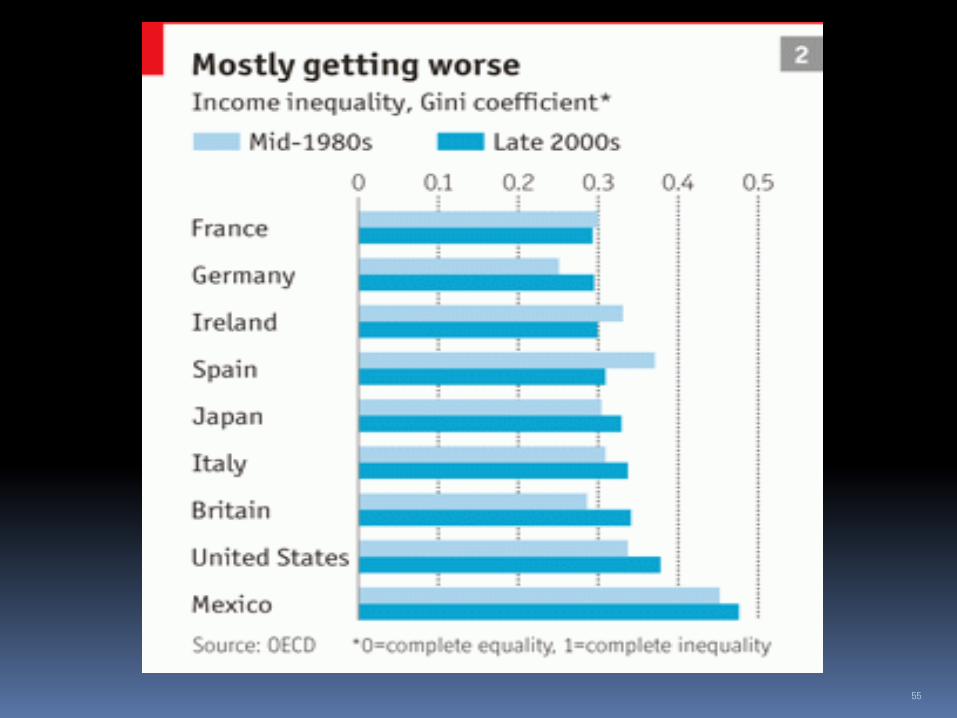

Income inequality

54

55

56

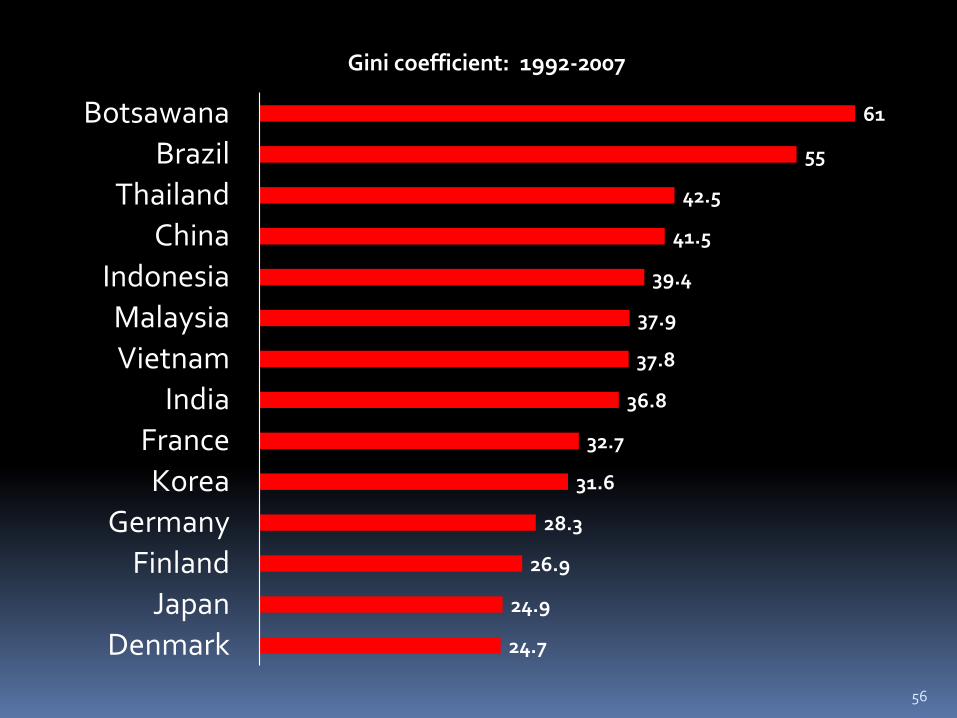

24.7

24.9

26.9

28.3

31.6

32.7

36.8

37.8

37.9

39.4

41.5

42.5

55

61

Denmark

Japan

Finland

Germany

Korea

France

India

Vietnam

Malaysia

Indonesia

China

Thailand

Brazil

Botsawana

Gini coefficient: 1992-2007

The way forward: After 2015

The baht exchange rate must be allowed to move more freely to cushion export fluctuations—less intervention.

Don’t have too much high hope on the Asian Economic Community

Its main benefit would be the breakup domestic monopoly power

Be cautiously optimistic

57

Conclusion

Integration of Thailand with ASEAN Economic Community is going ahead as scheduled.

Integration with Latin America is constrained by high transportation cost and imperfect information.

Direct investment can be promoted with revival of investment opportunity

Thailand and Mexico are facing similar economic problems: income distribution and monopoly.

Lessons can be learned from each other by examining policy mistakes in the past.

58