Collateral Underwriting (“CU”) Training Taking Appraisal Review To The Next Level.

22

Collateral Underwriting (“CU”) Training Taking Appraisal Review To The Next Level

-

Upload

erin-jennings -

Category

Documents

-

view

218 -

download

1

Transcript of Collateral Underwriting (“CU”) Training Taking Appraisal Review To The Next Level.

Collateral Underwriting (“CU”)

TrainingTaking Appraisal Review To The Next Level

What is FNMA Collateral Underwriter (“CU”)?

Collateral Underwriter (“CU”) is the latest addition to Fannie Mae’s comprehensive suite of risk management tools which will be made available for industry use on January 26, 2015. CU will provide additional transparency and certainty by giving lenders access to the same appraisal analytics used in Fannie Mae’s quality control process.

CU performs automated risk assessments of appraisals submitted to the Uniform Collateral Data Portal (“UCDP”) and returns risk scores from 1-5, flags, and messages to the submitting lender. CU risk scores and messages will be available to all UCDP users in real-time through the UCDP portal.

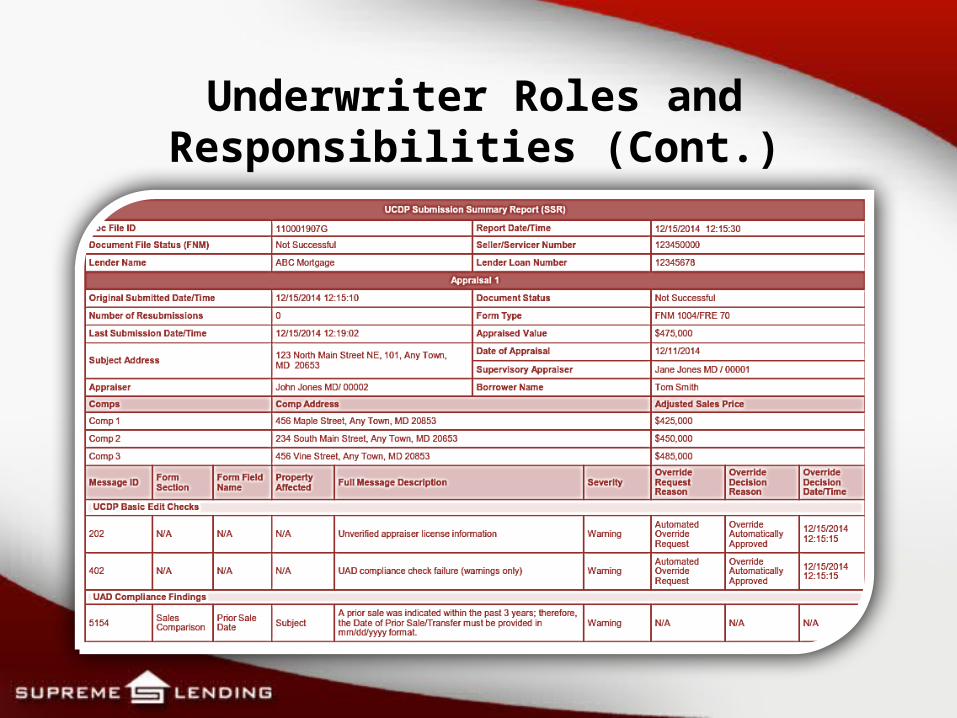

Submission Summary Report (“SSR”)

Understanding the New SSR Report

The introduction of CU also brings a revised Fannie Mae SSR report; however, Freddie Mac’s SSR remains the same. You will still retrieve the SSR the way you always have; however, you will now receive a risk assessment score from 1-5 on page two of the SSR.

Risk Scores, Flags and Messages

Lenders may use the CU risk score to segment appraisals by risk profile, resulting in more efficient resource allocation, workflow management and collateral risk management processes. The score will be provided in message ID FNM 1000 and will be based on CU’s automated assessment on a scale of 1.0 (lowest risk) to 5.0 (highest risk).

If a CU risk score cannot be generated on a 1004 or 1073 appraisal form, a “999” will be returned and a message in the FNM09XX series will provide more specific information about why the appraisal could not be scored. Some “999” messages can be resolved (for example, if there is a simple data entry error). CU risk scores and messages will not be returned for other form types.

Submission Summary Report (“SSR”)(Cont.)

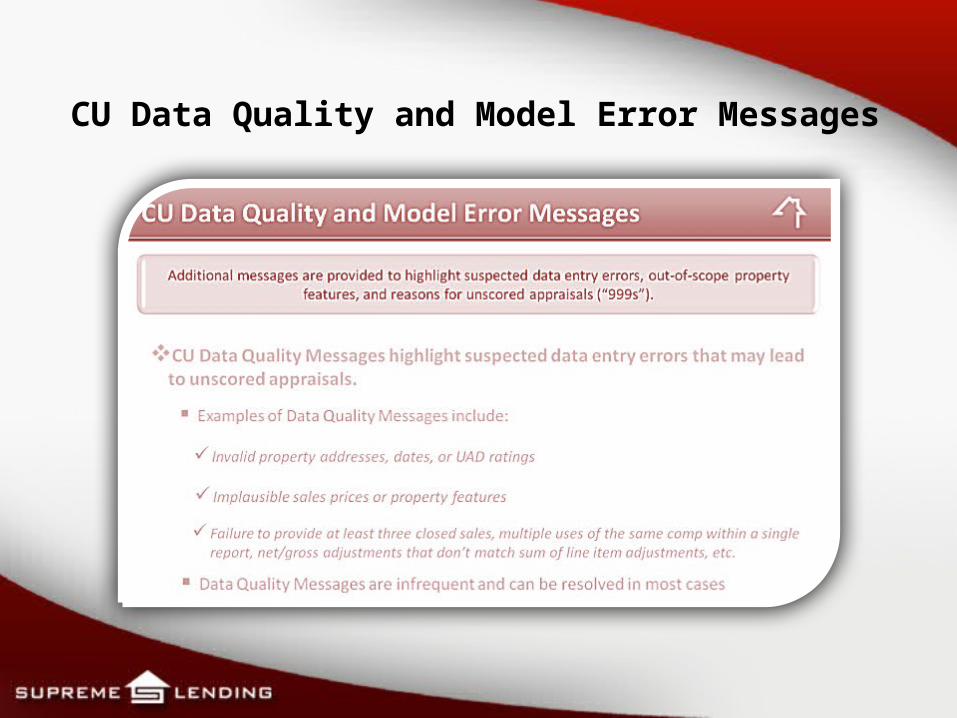

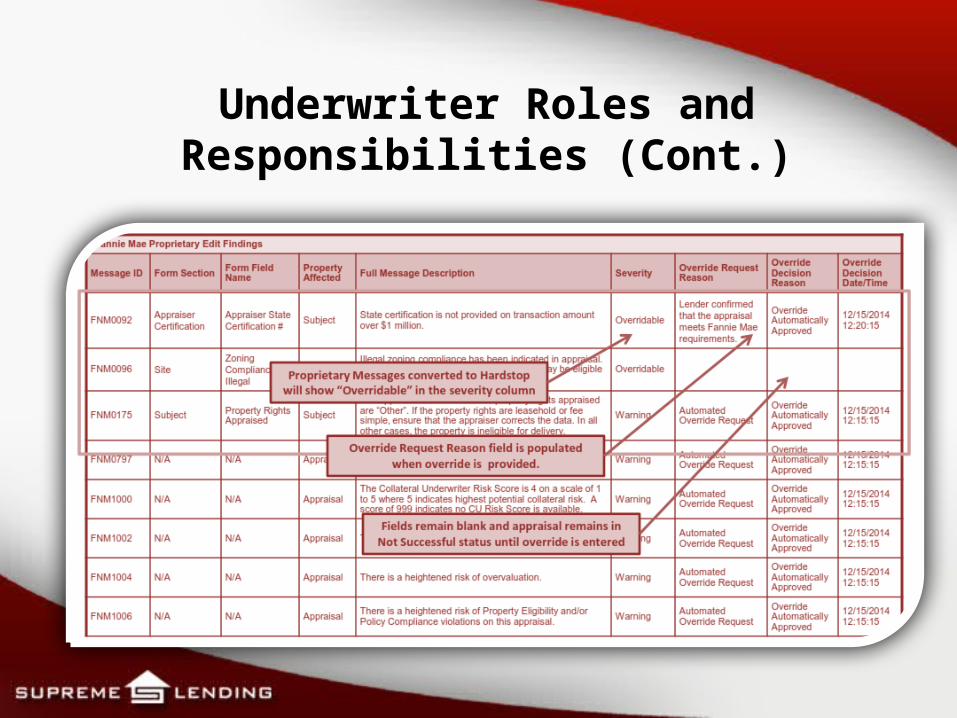

CU Data Quality and Model Error Messages

CU Data Quality and Model Error Messages (Cont.)

Underwriter Roles and Responsibilities

Critical Responsibilities

The Underwriter remains responsible for reviewing and decisioning the collateral.

Collateral Underwriter does not approve or decline a property.

Follow all existing procedures related to collateral review, in addition to the new action steps outlined below.

Underwriter Roles and Responsibilities (Cont.)

New Steps Related to the Collateral Review

The Underwriter must ensure the Submission Summary Report (SSR) has been successfully received.

o The SSRs will now be ordered by the processing team. The button to request the SSRs will now be available once the Sent To Processing milestone has been achieved. If not ordered by the processing team prior to underwriter receiving the file, the Underwriter is responsible to order.

o The SSR Submittal Button can be found on the Borrower Summary (Custom) screen.

The Underwriter reviews the SSR during their collateral review (see page 18). .

Underwriter Roles and Responsibilities (Cont.)

New Steps Related to the Collateral Review o For all business as usual data points:

Verify the Document File Status is Successful. If not, review the reasons, and contact your (RUM) Regional Underwriting Manager for additional assistance with addressing the hard stop(s).

An Unsuccessful status may be the result of a hard stop – see below for additional steps around hard stops.

Underwriter Roles and Responsibilities (Cont.)

New Steps Related to the Collateral Review (Cont.)

New – Review all messages and use the messages as a tool in your collateral review.

o Review specifically for any hard stop messages under the Fannie Mae Proprietary Edit Findings section.

o Hardstops are identified by the Severity = Overridable (see slide 19).

Access the Collateral Underwriter (CU) through the FNMA Collateral Underwriter landing page: https://www.fanniemae.com/singlefamily/collateral-underwriter

Review details to the messages during your collateral review.

Underwriter Roles and Responsibilities (Cont.)

Underwriter Roles and Responsibilities (Cont.)

Underwriter Roles and Responsibilities (Cont.)

Message

ID

Message Text Applicable Forms

Underwriter

Action Project Review Office Action Override Reason

Code Description Comments

FNM0101 The subject property may be a hotel / motel or condo hotel.

1004/2005, 1073/1075

Refer to Project Review Office

If determined not a CONDOTEL, override hard stop and enter comments

If determined a CONDOTEL, no action required

Notify UW of Record

Lender confirmed that the property meets FNMA requirements

Subject property verified not to be a CONDOTEL through the review of the appraisal and supporting HOA documents.

FNM0102 The subject property is in a condominium project that may be ineligible for delivery to Fannie Mae

1004/2005, 1073/1075

Refer to Project Review Office

If determined not a CONDOTEL, override hard stop and enter comments

If determined a CONDOTEL, no action required

Notify UW of Record

Lender confirmed that the property meets FNMA requirements

Subject property verified not to be a CONDOTEL through the review of the appraisal and supporting HOA documents.

FNM0174 The project name suggests that the property may be a condo hotel. Verify the subject is located in a project that meets Fannie Mae's Selling Guide Requirements

1073/1075 Refer to Project Review Office

If determined not a CONDOTEL, override hard stop and enter comment

If determined a CONDOTEL, no action required

Notify UW of Record

Lender confirmed that the property meets FNMA requirements

Subject property verified not to be a CONDOTEL through the review of the appraisal and supporting HOA documents.

Underwriter Roles and Responsibilities (Cont.)

Message

ID

Message Text Applicable Forms

Underwriter Action

Project Review

Office Action

Override Reason Code Description Comments

FNM0096 and FNM0097

Illegal zoning compliance has been indicated in appraisal. Review description to verify if the property may be eligible per the Selling Guide

1004/2055, 1073/1075

Review zoning and appraisal comments on the appraisal.

Determine if additional information is required by appraiser, if so send addendum.

Determine if the illegal zoning is permitted per Supreme Guidelines (section 406: Collateral Appraisals).o If determined

acceptable, override hard stop and enter comments.

o If determined not acceptable, no action required.

Lender confirmed that the property meets FNMA requirements

The subject's illegal zoning is in compliance with the FNMA Selling Guide.

Underwriter Roles and Responsibilities (Cont.)

Message

ID

Message Text Applicable Forms

Underwriter Action

Project Review Office Action

Override Reason Code Description Comments

FNM0098 and FNM0099

Present use is indicated as not highest and best use.

1004/2055 Review appraisal for comments surrounding the highest and best use.

Determine if additional information is required by appraiser, if so send addendum.

If no new information available to support the appraiser changing "use":o Unacceptable, no

action required.

Underwriter Roles and Responsibilities (Cont.)

Message

ID

Message Text Applicable Forms

Underwriter Action

Project Review Office Action

Override Reason Code Description

Comments

FNM0176 The appraisal indicates that the subject property has legal nonconforming zoning and cannot be rebuilt to the current density. This data indicates that the property is ineligible for delivery to Fannie Mae.

1073/1075 Validate the appraisal comments supports the message that the property cannot be rebuilt to current density.

Determine if additional information is required by the appraiser, if so send addendum.

If no new information available to support the appraiser changing "zoning data":o Unacceptable, no action required.

FNM0195 Fannie Mae will not accept appraisals from this appraiser.

1004/2055, 1073/1075

New Appraisal Required

FNM0196 Fannie Mae will not accept appraisals from this supervisory appraiser.

1004/2055, 1073/1075

New Appraisal Required

Underwriter Roles and Responsibilities (Cont.)

Message

ID

Message Text Applicable Forms

Underwriter Action

Project Review Office Action

Override Reason Code Description

Comments

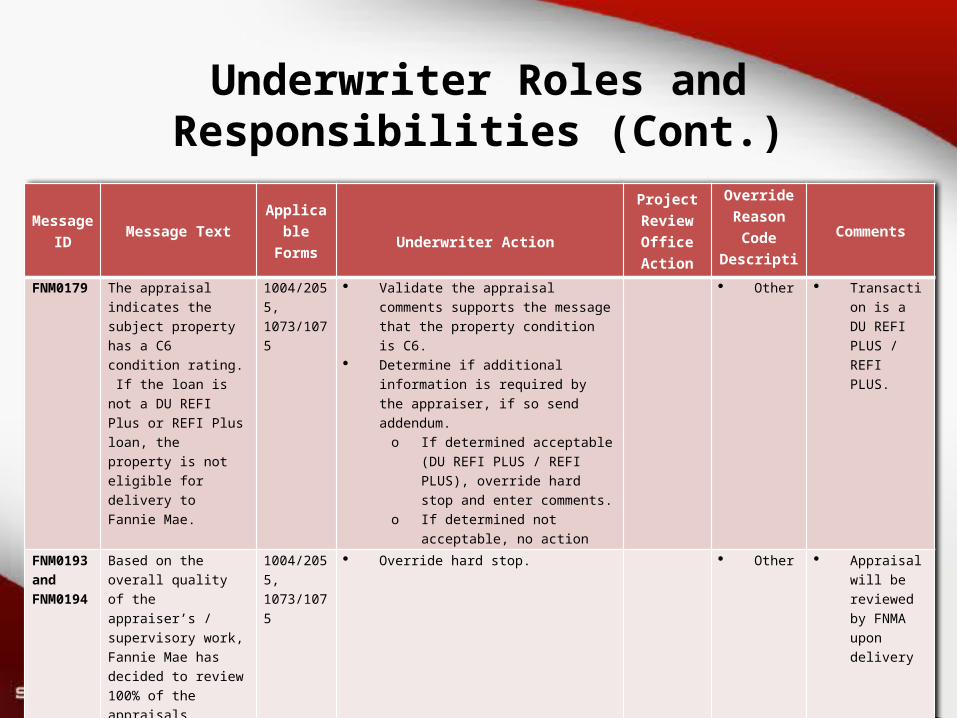

FNM0179 The appraisal indicates the subject property has a C6 condition rating. If the loan is not a DU REFI Plus or REFI Plus loan, the property is not eligible for delivery to Fannie Mae.

1004/2055, 1073/1075

Validate the appraisal comments supports the message that the property condition is C6.

Determine if additional information is required by the appraiser, if so send addendum.o If determined acceptable (DU REFI

PLUS / REFI PLUS), override hard stop and enter comments.

o If determined not acceptable, no action required

Other

Transaction is a DU REFI PLUS / REFI PLUS.

FNM0193 and FNM0194

Based on the overall quality of the appraiser’s / supervisory work, Fannie Mae has decided to review 100% of the appraisals prepared by this appraiser for any loans delivered to Fannie Mae.

1004/2055, 1073/1075

Override hard stop. Other Appraisal will be reviewed by FNMA upon delivery

Collateral Underwriting Access

URL for accessing and logging into Collateral Underwriter (CU).

https://www.fanniemae.com/singlefamily/collateral-underwriterOnce on the CU landing page you will then select Launch App

Once the Launch App has been selected, you will then arrive at the CU login screen. Once you enter your Fannie Mae credentials, the

log in screen will retain the information for future entry. Please see next slide for login page.

Collateral Underwriting Access

After logging in you will see the page below. Click on the box in the middle, reading Appraisal Review.

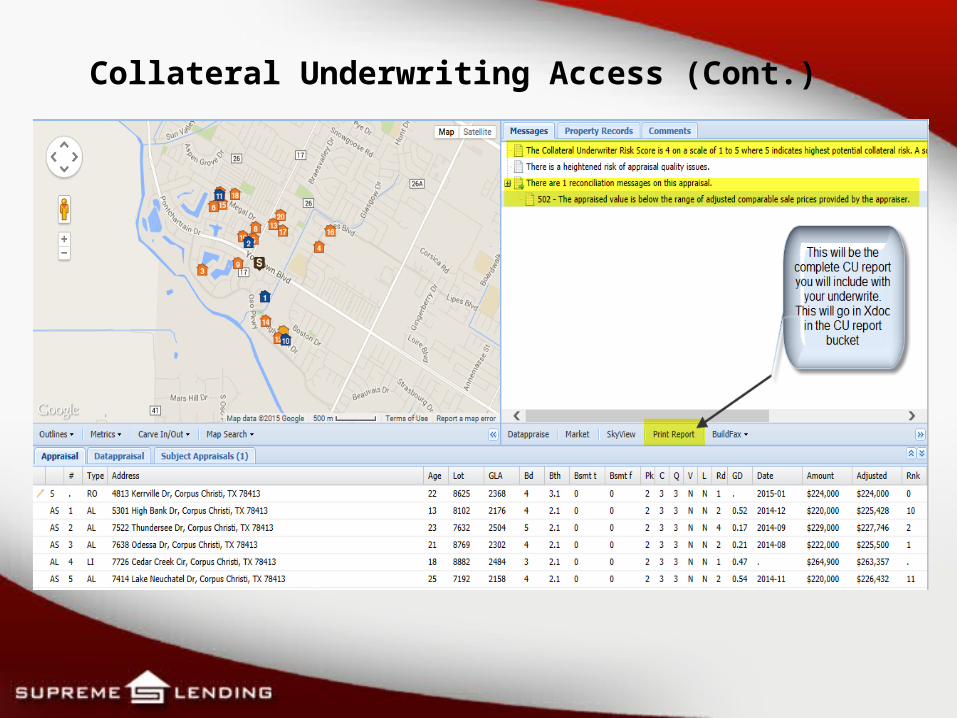

Collateral Underwriting Access (Cont.)

The next screen will take you to the CU report. (See next slide below). From the report you are able to view additional information about the score and any other messages CU suggests are relevant to this appraisal. Should you believe an addendum to the appraisal

is warranted based on your review, the addendum is sent to [email protected] . This addendum must include the CU findings,

and a detailed and specific request.

You will arrive at the page below, where you will need to enter the loan number in order to retrieve the report.

Collateral Underwriting Access (Cont.)

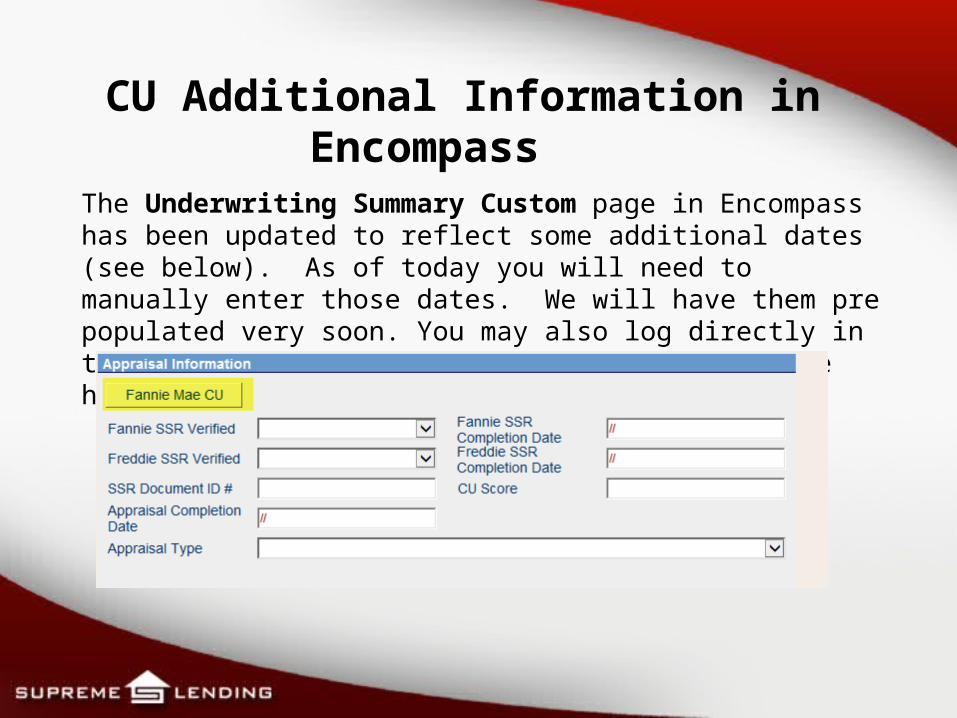

CU Additional Information in Encompass

The Underwriting Summary Custom page in Encompass has been updated to reflect some additional dates (see below). As of today you will need to manually enter those dates. We will have them pre populated very soon. You may also log directly in to CU from inside Encompass, by clicking on the highlighted button below.