CNBC Aawaz and Liases Foras · 2019-07-23 · Figure 6: Price Trend in Tier 1 Cities Source: Liases...

17

Liases Foras Real Estate Rating & Research Pvt. Ltd. Independent Non-brokerage Real Estate Research Company Housing Charter 2018 The CNBC Aawaz and Liases Foras

Transcript of CNBC Aawaz and Liases Foras · 2019-07-23 · Figure 6: Price Trend in Tier 1 Cities Source: Liases...

Liases Foras Real Estate Rating & Research Pvt. Ltd.

Independent Non-brokerageReal Estate Research Company

Housing Charter 2018

The

CNBC Aawaz and Liases Foras

CONTENTS

01 MARKET TRENDS

02 WHY IS THE RECOVERY SO SLOW?

03 URGENT NEED TO FIX INEFFICIENCIES

04 EFFORTS TAKEN SO FAR

05 WHAT ELSE COULD BE DONE?

01

05

07

08

09

Independent Non-brokerageReal Estate Research Company

2017 has been the year of reforms for the real estate industry. Since the

introduction of Real Estate Regulatory Authority (RERA) Act and Goods and

Services Tax (GST) the real estate business has never been as usual. The

policies have forced developers to readjust their business models from a

finance and marketing perspective. Through these teething troubles the

market slowed down - but it has not tumbled. It is, in fact, beginning to show

signs of recovery. However the recovery is slow and needs match up to

urgent need for affordable housing in the country.

Productive land and rational taxation systems are crucial to increase the

supply of housing. But market inefficiencies, speculative accumulation, and

lack of transparency in land deals have inflated the cost of urban land in the

recent years. On the taxation front GST has tried to resolve the inefficiencies

of double taxation, but there remain inconsistencies and confusions about

its application.

The 2018 CNBC Charter notes the trends in the market and deliberates on

further measures that can help stimulate the supply of affordable housing.

PREFACE

Independent Non-brokerageReal Estate Research Company

MARKET TRENDS Data from Liases Foras’s quarterly surveys indicate that the market is slowly recovering. In Tier 1 cities, sales

have increased and prices have stagnated or marginally decreased. It is the cautious end users rather than

the exuberant investors that are driving the recovery process. Increase in income levels and availability of

funds from PMAY has helped some consumers bridge the affordability gap, this might be responsible for the

increase in sales. Developers who have targeted the priority sector have managed to sell more homes.

Improvement in Tier 1 Sales

Financial year comparisons between the last two years show a marginal improvement in sales. Overall,

sales in the country have grown at 8%. Tier 1 cities are fueling this growth. Metropolitan regions of Mumbai

and Delhi have emerged as top performers. Sales in these cities have increased by 25% and 19%

respectively. Tier 2 and 3 cities however, have shown a decline in sales

Table 1: All India Sales FY 17-18

Annual Sales Unsold

FY 17 FY 18 % Growth FY 17 FY 18 % Growth

All India 295,345 320,078 8% 1,123,128 1,129,499 1%

Tier 1 234,129 265,564 13% 953,856 929,415 -3%

Tier 2&3 61,216 54,514 -11% 1,69,272 2,00,084 18%

01

Figure 1: Quarterly Sales (units)

Source: Liases Foras

Tier 2 13,695 14,152 13,529 12,476 14,039 14,470

Tier 1 50,398 60,807 64,841 64,756 66,866 69,101

All India Months_x000d_Inventory 53 45 43 43 41 41

Q3 16-17 Q4 16-17 Q1 17-18 Q2 17-18 Q3 17-18 Q4 17-1810

15

20

25

30

35

40

45

50

55

60

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Mo

nth

s In

ve

nto

ry

Un

it S

ale

s

Un

it S

ale

s

Figure 2: FY 17-18 Sales for Tier 1 Cities

Source: Liases Foras

FY 17 24031 32019 14302 12766 10294 52800 52505 35412 61216

Fy 18 26489 30331 12105 14922 12035 66001 62322 41359 54514

Ahmedabad Bangalore Chennai Hyderabad Kolkata MMR NCR Pune TIER 20

10000

20000

30000

40000

50000

60000

70000

www.liasesforas.com

Independent Non-brokerageReal Estate Research Company

Priority Sector Leads Sales:

Financial Year comparisons for Tier 1 cities show that sales have grown at 25% in the priority segment. The

luxury segment has also shown a growth of 16%. This growth is largely driven by discounts and new

launches.

Figure 3: Sales by Segment for Tier 1 cities

Source: Liases Foras

FY 17 55,417 71,049 68,554 25,552 13,557

Fy 18 69,342 74,585 76,736 29,603 15,298

Priority

Segment

Affordable

Segmen

Mid

Segment

Luxury

Segment

Ultra Luxury

Segment

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Tier 2 cities have witnessed an overall drop in sales of 11%. But here too, sales in the priority segment have

merely dropped by 3%.

Un

it S

ale

s

Figure 4: Sales by Segment for Tier 2 cities

Source: Liases Foras

FY 17 19,971 20,637 15,900 3,684 1,024

Fy 18 19,356 17,705 13,569 2,984 900

This is not a surprising trend. As per the report of the technical group on urban housing shortage (2012)

there is a need for 18.78 million homes in urban India and 95% of the demand is from the EWS and LIG

segment. Given the volume of demand among the low-income groups, developers who have targeted the

priority sector are selling homes faster and in larger volumes.

Un

it S

ale

s

0

5,000

10,000

15,000

20,000

25,000

Priority

Segment

Affordable

Segmen

Mid

Segment

Luxury

Segment

Ultra Luxury

Segment

02

Rationalization in Size and Price

In order to sell at affordable rates, the developers have begun rationalizing sizes. The composite weighted

average size of newly launched units in the 8 Tier 1 cities, show a decline from 1254 sqft to 1084 sqft. This

trend is accompanied by a decline in price as well. This has led to a cumulative decline in the ticket size of

the unit of up to 20%.

www.liasesforas.com

Independent Non-brokerageReal Estate Research Company

Figure 5: Decrease in Unit Size and Price of New Launches in India

Source: Liases Foras

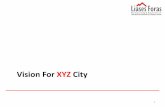

Depending upon geography, prices in the country have marginally decreased or remained steady over the

past 5 years. The graph below shows an exuberant spike in housing prices between 2009-14 for all Tier 1

cities; especially MMR where prices escalated two fold. After this initial spike, the prices have marginally

decreased or stabilized. In the meanwhile incomes have grown, thus bridging the affordability gap for some

buyers.

FY 14

-15

FY 15

-16

Fy16-

17

FY 17

-18

950

1000

1050

1100

1150

1200

1250

1300

Are

a (

sqft

)

Apt Sizes (Sqft) 1254 1198 1143 1084

Source: Liases Foras

FY 14

-15

FY 15

-16

Fy16-

17

FY 17

-18

Pri

ce P

SF

Price PSF 6105 5949 5771 5638

5400

5600

5800

6000

6200

Figure 6: Price Trend in Tier 1 Cities

Source: Liases Foras

0

2000

4000

6000

8000

10000

12000

14000

Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18

Ahmedabad Bangalore Chennai Hyderabad

Kolkata MMR NCR Pune

03www.liasesforas.com

Independent Non-brokerageReal Estate Research Company

Closing Affordability Gap

The graph below measures the housing price index against Liases Foras’s affordability index for service

sector employees in MMR. As is evident, stagnancy in the prices, increase in incomes and reduction in

interest rates has led to a decrease in the affordability gap. The affordability gap was at its maximum in

March 2014 (340 bases points). Since then it has gradually decreased. The gap between the two indices has

reduced to a level of 95 bases points as of March 2018. Availability of additional funds under PMAYs Credit

Linked Subsidy Scheme has further helped consumers bridge this gap. Developers are also enabling

consumers by offering them subvention schemes and freebies on maintenance and parking for the first few

years. For all these reasons, housing is potentially within the reach of the service class in the Mumbai

Metropolitan Region.

Figure 7: Affordability Gap for Service Sector in MMR

Source: Liases Foras

0

100

Jan

-05

Oct

-05

Oct

-06

No

v-0

7

Jun

-08

De

c-0

8

Ma

r-0

9

Jun

-09

Se

p-0

9

De

c-0

9

Ma

r-1

0

Jun

-10

Se

p-1

0

De

c-1

0

Ma

r-1

1

Jun

-11

Se

p-1

1

De

c-1

1

Ma

r-1

2

Jun

-12

Se

p-1

2

De

c-1

2

Ma

r-1

3

Jun

-13

Se

p-1

3

De

c-1

3

Ma

r-1

4

Jun

-14

Se

p-1

4

De

c-1

4

Ma

r-1

5

Jun

-15

Se

p-1

5

De

c-1

5

Ma

r-1

6

Jun

-16

Se

p-1

6

De

c-1

6

Ma

r-1

7

Jun

-17

Se

p-1

7

De

c-1

7

Ma

r-1

8

200

300

400

500

600

Interest adjusted Affordability Index Inflation adjusted Price Index

Ind

ex

10

0

11

8

14

4

13

6

12

0

10

9

13

3

13

0

12

5

12

7

13

2

13

7

13

5

12

6

11

5

11

2

11

6

12

1

12

6

15

0

15

3

15

7

16

1

16

5

16

9

17

3

18

9

20

5

21

5

22

0

23

8

25

1

25

8

26

4

28

4

30

0

31

9

35

6

38

3

39

8

40

8

41

9

41

6

10

0

11

2

2

01

3

02

2

91

2

47

2

23

2

05

2

08

2

35

2

75

2

97

3

44

3

26

3

54

3

69

3

87

4

12

4

18

42

8

42

8

4

45

4

54

4

57

4

50

4

90

5

29

50

5

51

3

53

9

51

2

50

0

51

5

50

4

51

1

4

88

51

1

51

1

50

6

51

6

50

8

51

1

51

1

04www.liasesforas.com

Independent Non-brokerageReal Estate Research Company

WHY IS THE RECOVERY SO SLOW?In the past 7 years, unsold stock in the country has grown more than three times. Having a high supply of

units in the market need not be bad from a consumer point of view as it keeps prices in check. But in order to

prevent stagnation increase in sales needs to accompany the increase in housing stock.

Figure 8: Increase in Unsold Stock In Tier 1 Cities

Source: Liases Foras

311155 324805405712

454736511530

607201

711539

897924 953867 921828

0

200000

400000

600000

800000

1000000

Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Dec-17

MMR Pune Hyderabad NCR Bangalore Chennai Kolkata Ahmedabad Series9 Total

Inefficiencies in economic geography could explain why developers are left with large inventory of unsold

homes in spite of the high demand for housing in the country.

Market exuberance between 2005-2014 led to increase in urban land prices. During this period of 12 years

land prices have grown 9 times for tier 1 cities. Developers who wished to build homes at affordable prices,

moved further away from city centers in search of cheaper land. The diagram given below shows the

distance at which the maximum supply of homes less than 30 lakhs is available.

In Mumbai, there is a negligible supply of homes less than 30 lakh for the first 40 km of the city radius. For

Delhi NCR and Chennai this distance shrinks to 20 km. Bengaluru performs better as the distance further

shrinks to 10 km. (see graph below)

05

Ahmedabad

Tie

r 1

Cit

ies

Distance in km

Bangalore

Chennai

Hyderabad

Kolkata

MMR

Pune

0 - 10

NCR

10 - 20 20 - 30 30 - 40 40 - 50 50 - 60 60 & Above

Percentage of homes below 30 lacs

0-10% 11-30% 31-50% 50% & Above

6%

0%

1%

2%

2%

0%

0%

2%

11%

58%

34%

54%

39%

0%

21%

36%

0%

13%

26%

3%

7%

7%

25%

19%

0%

0%

2%

3%

0%

44%

22%

0%

1%

3%

9%

3%

1%

32%

28%

5%

0%

0%

0%

0%

0%

17%

4%

0%

82%

26%

27%

36%

52%

0%

0%

39%

Source: Liases Foras

Figure 9: Total Supply of homes under 30 lakh till March 2018 by distance

www.liasesforas.com

Independent Non-brokerageReal Estate Research Company

While the city has expanded due to price, infrastructure hasn't kept

up. Neighbourhoods emerging in the peri urban areas often lack the

necessary physical and social infrastructure for daily needs and fast

and efficient transit connectivity to workspaces in the city. This

mismatch between job and housing locations pushes people who

buy peri urban homes to spend more time commuting. The value

proposition of ill equipped affordable housing in the peri urban areas

may simply not be worth the work travel time they impose on their residents. This makes peri urban housing

less desirable for the urban working population and could be the cause of slow sales despite the high demand

in the priority and affordable housing segment.

06

While the city has expanded

due to price, infrastructure

hasn't kept up.

www.liasesforas.com

Independent Non-brokerageReal Estate Research Company

URGENT NEED TO FIX INEFFICIENCIESThere is an urgent need to fix the affordable housing deficit. The Census tells us that, India is a young country,

riding on its demographic dividend. Approximately 35% of the urban population fell within the working age

group of 25 to 45 in 2016. But the window for this working age population to buy formal homes is limited.

Middle class working couples between the age of 25-45 have traditionally been the preferred target customers

for developers as this demographic begins to have the surplus income for downpayment and is eligible for

loans. Over the years the mortgage market has expanded to include the lower income groups as well. However,

in the past decade, the expansion in housing finance has been accompanied by an escalation in housing costs.

Consumers are holding off on buying homes as they are unaffordable or far away from their place of work. This

has led to an increase in the average age of the housing mortgage seeker. As per analysis done by Liases Foras,

the age of a mortgage seeker has risen from 31 in 2005 to 41 by 2016. Only 54% of target customers can seek

loans and the mortgage market is shrinking. As banks begin to factor

in mortality risks, interest rates on loans increase for older age

customers adding to the cost of housing.

If affordable housing market misses the demographic window there

is a risk, that in the future, India will have to provide for a large

population of retired senior citizens that are living in rental homes or

worse in slums or homeless conditions. Thus, there is an urgent need

for the economy to provide for jobs as well as affordable housing for

its working age population. The construction industry can play a key

role in providing for both these needs.

In order to provide homes at favorable locations and at affordable

rates, the government needs to take efforts to make land and finance

cheaper and more productive.

Figure 10: Age and Population Graph (2016)

Source: Census 2011 – extrapolated for 2016

0 10 20 30 40

5-910-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-79

80+Not stated

Persons in Millions

Ag

e I

nte

rva

ls

07

If affordable housing market

misses the demographic

window there is a risk, that

in the future, India will have

to provide for a large

population of retired senior

citizens that are living in

rental homes or worse in

slums or homeless conditions

www.liasesforas.com

Independent Non-brokerageReal Estate Research Company

EFFORTS TAKEN SO FARGovernment policies like PMAY, RERA and GST have tried to address some of the hurdles mentioned in the

section above.

Pradhan Mantri Awas Yojana (PMAY): The government is working towards a daunting task of providing

affordable housing for all by 2022. As per estimates, there is a need for 18 million homes in urban India and

another 43.6 million homes in the rural areas. Although work has begun on approximately 20% of

requirement of homes in both the urban and rural category; only 2% homes in urban areas and 8.3 %

homes in rural areas have been completed.

Figure 11: PMAY Progress Report April 2018

Pradhan Mantri Awas Yojana- Housing for All (HFA)

PMAY Urban Progress

(Including RAY & CLSS)

No of

Household units

% of Urban

housing shortage

PMAY Gramin

Progress

No of Household

units

% of Rural housing

shortage

Urban Housing

Shortage 1,80,00,000

Rural Housing

Shortage 4,36,00,000

Houses involved 44,35,663 25% Total Target 94,69,918 22%

Houses grounded

forconstruction 19,30,844 11%

Total

Beneficiaries

Registered

97,26,560 22%

Houses Completed 4,00,074 2%Total House

Sanctioned 78,61,513 18%

Houses Occupied 3,55,741 2%Total House

Completed 36,34,865 8%

Source: http://ruraldiksha.nic.in/RuralDashboard/PMAYG_NEW.aspx & http://mohua.gov.in/upload/uploadfiles/files/All_India_PMAY(U)(1).pdf

Real Estate Regulatory Act: RERA’s consumer protection policies have played an important role in reshaping

the industry from being investor driven to being end user driven. The policy protects consumers from

undisciplined builders by ensuring that projects are sold only after building permissions are attained and all

necessary disclosures pertaining to project launch, possession, amenities and facilities are provided.

Builders are expected to put 70% of the money collected from buyers into an escrow account to ensure that

consumer money for one project is not diverted into other projects. RERA has not been uniformly

implemented in all States. But there is a push from the center to see the implementation through without

dilutions.

Goods and Services Tax: The GST bill has tried to simplify the taxation process and prevent double taxation

that took place under the VAT system. GST on property is now 18%, the effective rate is 12%, thanks to

abatement provided on land value. Before GST, the rate was 10-15%. However reports[ See: Impact of GST

on residential markets, JLL, 2018] suggest that contractors and developers are still adjusting to the system

and compliance in the entire production chain is shoddy. It also points out that there remain some design

problems with respect to land. Only 1/3 of the contract value is deductible as land value for GST purposes.

However there are cities where land values are as much as 50-60% of the entire project cost. Once these

problems are resolved we might begin to see some benefits to the consumers.

Further government efforts to bring in the Benami property law can help check land corruptions. A multi

pronged approach that includes incentives through taxation, finance and planning along with punitive

measures for those who are speculating can help curb price escalations

1See: Impact of GST on residential markets, JLL, 2018

08www.liasesforas.com

Independent Non-brokerageReal Estate Research Company

WHAT ELSE COULD BE DONE? While taxation, consumer protection, and transparency are important issues being addressed by the

government; little has been done to address the issue of land and finance costs.

Given below is a the cost structure for housing development in Mumbai. It shows that the cost of land has

increased 9 times since 2005. Finance cost has increased close to 7 times. The percentage of developer

profit has shrunk. This is the primary reason why despite rising inventory prices are stagnant in the city.

Similar patterns can be seen in cities across the country.

In our previous charter on land, we have elaborated on the problem of land speculation and suggested

punitive taxation measures like the vacant land tax to curb the speculative bubbles that lock land expensive

and decrease its mobility for housing. In this charter we would like to explore the various incentive

measures that can decrease the cost of land and finance and make housing more affordable.

Period 2005 2007 2009 2012 2015 20172005 -2017

(Change Multiple)

Price in PSF 2,700 6,700 5,100 10,300 11,600 11,820 4.38

Developers Profit (in INR) 464 1,644 428 1,416 552 727 1.57

Finance Cost (in INR) 720 1,786 1,860 3,842 5,024 4,839 6.72

Land Cost @ Salaeable Area (in INR) 300 1,500 1,000 2,300 2,800 2,800 9.33

Approval Cost (in INR) 216 670 612 1,442 1,624 1,655 7.66

Construction Cost (in INR) 1,000 1,100 1,200 1,300 1,600 1,800 1.80

Construction and Sales Time (Years) 3 4 4 5 6 6 2.00

09www.liasesforas.com

Figure 12: Structure of Cost

Independent Non-brokerageReal Estate Research Company

Reduction in Land Price

As explained in the section above, price of land is pushing affordable housing to the outskirts of cities, but

due to inefficient transit to places of work and lack of social infrastructure, peri urban areas are not attractive

to all consumers as housing locations.

Provision of infrastructure and amenities in the peri urban areas can help increase the supply of suitable

land for affordable housing. The Central government has taken cognizance of the need for better

infrastructure and planning for our expanding cities. Starting with JNNURM & RAY to AMRUT & PMAY, there

has been a consistent effort by the Central government to allocate money for development of cities and

urban regions. However, there remain bottlenecks in comprehensive planning and governance that produce

disconnected undesirable development patterns.

Cities would benefit from planning at the regional level. Further, to ensure that decisions regarding land are

supported with efficient transportation, State governments could consider setting up of land and

transportation authorities that work in tandem. This can help ensure that when land is opened up through

highways, additional social, physical and transit infrastructure for affordable housing is planned along with it.

Providing higher FARs where infrastructure is available can help increase supply of housing in favorable

locations within a city. However, it’s important that the FAR should be provided at rational costs and

subjected to time bound delivery of project for which the additional FAR is given. Master Plans that monetize

additional FAR through an expensive premium, in turn risk making the housing supply from it expensive.

Making FAR time bound is important to prevent speculation on the increase.

Both measures, if planned strategically, can help increase the supply of housing in favorable locations and

bring down the cost of its development.

Improve Planning and Infrastructure:

10

Reduce Other Costs

l Improve Planning and Infrastructure

l Increase FAR in strategic locations

l Allow private sector banks to finance

land for affordable housing

l Bring Taxation measures to curb

speculation

l Decrease GST on real estate

l Lower taxation for housing delivered on

time

l Increase Loan To Value for the purchase

of housing

l Expedite approvals

Re

du

ce

La

nd

Co

sts

www.liasesforas.com

Independent Non-brokerageReal Estate Research Company

Reduction in Other Costs

The RERA act ensures that developers adhere to a strict committed timelines. But in order to remain on the

right side of law most developers are committing to inflated timelines in their contracts. Affordable housing

production is time sensitive and must be produced and sold quickly to avoid speculation or cost over run. In

order to further incentivize the process, governments could lower taxation for projects produced within a

lower time frame.

Lower taxation for housing delivered on time:

As explained in the section above, housing prices have stagnated in the country. Sales are seeing an

improvement. The risk of price correction is minimal. Given that the market has endured shocks like

demonetization without a drop in price, our outlook is that the prices for the next two years will remain

stagnant. At this point the government can revise the loan to value for housing from 75% to 90% of the

contract value. This can help younger buyers buy homes quicker.

Increase Loan To Value for purchase of housing

Auto DCR systems have been implemented in many parts of the country, however, the approval process

has not undergone a dramatic change in time frame. Approval process is still long and tardy. In order to

expedite production and lower the cost of production, the cost of approvals and related timelines must be

reduced.

Expedite Approvals

Currently banks are not allowed to finance land purchase for real estate. Developers looking for loans for

land are approaching non banking finance corporations (NBFC). These loans are expensive and the cost is

passed to the end users. Governments could consider the option to allow Private banks to give loans to

developers looking to buy land for time bound production of affordable housing. This would help bring

down the cost of finance.

Allow private sector banks to finance land for affordable housing:

We would like to reiterate the need for taxation measures that prevent speculation on of land and in turn

make land more productive. Vacant land that is not being used for primary activities (like agriculture or fish

drying) or any other job creating functions should be subjected to a vacant land tax. Similarly inventory and

vacant house tax can help prevent speculation on built housing in turn reducing cost of rental and capital

values.

Bring Taxation measures to curb land speculation and accumulation of inventory and

vacant stock

11www.liasesforas.com

Independent Non-brokerageReal Estate Research Company

12

Disclaimer

Information contained here, has been obtained from sources believed to be reliable. While we do not doubt

its accuracy, we have not verified it and make no guarantee, warranty or representation about it. The

readers are encouraged to independently assess the relevance, accuracy and completeness of the

information of this publication. This report is for general guidance and informational purposes only, and

does not constitute professional advice.

Whilst every effort has been taken to provide authentic data and analysis, Liases Foras Real Estate Rating &

Research Pvt. Ltd. Or any of its employees are not responsible for any loss, major or minor incurred on the

basis of the information and analyses provided or are liable to any damages in any form or shape All rights

to this material are reserved and cannot be reproduced without prior written permission from Liases Foras

Real Estate Rating & Research Pvt. Ltd.

www.liasesforas.com

Ms. Namrata Kapoor

Research Lead

Email id: [email protected]

Authors:

Mr. Pankaj Kapoor

Founder and MD - Liases Foras Real Estate Ratings and Research Pvt. Ltd

Email id: [email protected]

Independent Non-brokerageReal Estate Research Company

Liases Foras is an independent real estate research institute having offices in Mumbai, Bangalore and New

Delhi. Liases Foras was founded in 1998 as a boutique non-broking real estate consultancy, and has since

evolved into a data-focused real estate research lab employing over 120 people. Liases Foras tracks and closely

examines the health of the real estate sector in over 60 cities across India, including all metro and capital cities.

Liases Foras is the official consulting partner of the National Housing Bank and is currently engaged in re-

building the RESIDEX property price index for NHB.

About UsLiases Foras: The Pioneer in Scientific Research in Real estate

Strategic Partner : information

Data & Coverage

Our database includes 125,000 projects amounting to over 50 billion square feet of real estate space, spread

across 60 cities in India. Currently, we are monitoring close to 18,000 on-going projects on a quarterly basis.

PRODUCTS

Ressex

Ressex, our online data

interface provides

structured solutions to

day-to-day questions

pertaining to real estate

markets and projects.

Desktop valuation &

Comparables

Comparables is a first of its

kind, web based property

value validation tool.

Developer’s Rating

Extensive analysis of on-

ground performance of

more than 9000 developers

across 62 cities in India.

Business Intelligence

and Risk Analytics

A hybrid product that helps

banks, HFCs and corporates

to identify potential

opportunities and

underlying risks.

Crystal

Crystal is a valuation

workflow system which

streamlines the interaction

between lenders, valuators,

and surveyors in carrying

out valuations using

automation and mobile

devices.

Highest and best-use

analysis

Every structure belongs to

its location and time. The

analysis scans various

options to find out the one

which gives the highest/

maximum development

realisation.

Valuation advisory

Liases Foras offers

transparent, scientific,

data-driven and unbiased

valuation solutions.

Urban planning services

We prepare City

Development Plans

outlining the vision and

development strategy for

unlocking land in a city.

Preparing design briefs

Extending beyond the best-

use prognosis, we write

uncluttered, contextual

design briefs for Master

Planners/Architects.

Consumer survey &

profiling

We specialise in the field of

real estate-specific

consumer surveys.

Product viability study

This study is to ascertain

whether the envisaged

development and product

plan of the developers are

correct or risky.

Risk reports

Risk Reports are carried out

primarily to assess the state

of the market and measure

the price correction during

oversupply scenario or

default risks in the market.

Portfolio optimization

strategy

Every structure has an

opportunity cost. We

analyse organisational

functions, manpower and

real estate assets to arrive

at an optimal cost and an

effective portfolio.

Location & Entry strategy

This study understands the

growth patterns of a city

and real estate

developments, to arrive at

an ideal location for

projects and

establishments.

Marketing strategy

Partnering with the

developer to formulate a

marketing plan keeping in

mind the target audience,

positioning, product and

pricing.

ADVISORY SERVICES

Wholly Owned by Reserve Bank of India

NATIONALHOUSING BANK

OUR CLIENTS:

13www.liasesforas.com

Independent Non-brokerageReal Estate Research Company

Liases Foras Real Estate Rating & Research Pvt. Ltd.

Office No. 208, 2nd Floor Square1,

Saket District Center, New Delhi -

110017. Tel: +91 11 40105461

103, Raheja Chambers (Next to Post

office), Museum Road, Bengaluru

560001. O: +91 8041139314

Reg Office: S-6, Pinnacle Business Park,

Mahakali Caves Rd, Nr Ahura Centre,

MIDC, Andheri E, Mumbai 400093. O:

+912228391486/63

www.liasesforas.com | www.ressex.com • Offices: Mumbai | New Delhi | Bengaluru | UK | Singapore

Mumbai Bengaluru New Delhi