City Report Mumbai Office Market Q3 2009

16

CITY REPORT MUMBAI OFFICE MARKET Q3 2009

-

Upload

guesta5a31d -

Category

Real Estate

-

view

2.703 -

download

2

description

Transcript of City Report Mumbai Office Market Q3 2009

CITY REPORTMUMBAI OFFICE MARKET

Q3 2009

CITY REPORTMUMBAI OFFICE MARKET - Q3 2009

Summary p. 3

Macroeconomic Context p. 4

Mumbai Office Market p. 5

Central Business District (CBD) p. 6

Extended Central Business District (ECBD) p. 7

Alternate Central Business District (Alternate CBD) p. 8

Secondary Business District (SBD) p. 9

Periphery Business District (PBD) p. 10

Key Projects

p. 12Capital Values

p. 13Key Transactions

p. 14

Summary

Prime Rents p. 11

Glossary p. 15

3I I

SUMMARY

In Mumbai, the demand for commercial space in the third quarter (July - September), marginally increased over the second quarter. There is a general perception among corporate occupiers that rents have “bottomed out”. The take up improved significantly especially in the suburbs, though there is an increasing supply being added in the market. The vacancy rates in CBD area of Nariman point continue to increase further and now is forcing the owners to become more flexible in their commercial terms. The fund flow situation of large real estate developers improved dramatically as they were able to successfully raise capital via Qualified Institutional Placement’s (QIP) and other alternate investment vehicles promoted by international capital market advisors. However the small and medium scale developers are still facing liquidity issues and have therefore delayed the the construction of their projects by at least 6 months.

A lot of opportunistic buying is on the anvil as domestic and NRI investors are now finding the valuations a bit interesting. These investors are seeking net returns in excess of 12% per annum. There are also many fence sitters , still, who feel that there is a scope for 5-10% of further correction, by the end of December. Most of the development companies, are only offering properties for lease and are not releasing any commercial office space for sale. Since there is an availability of 10 million sq.ft. of new, modern supply of office space in Mumbai, our assessment is there will be downward pressure on rents and capital values at least for the next 6 months.

Cautious investing is on the anvil, albeit increasing supply

CITY REPORTMUMBAI OFFICE MARKET - Q3 2009

DLF Limited 16,498.6 17,509.4 -6% 3,960 4,397.4 -10%

India Bulls 2,965.9 3,245.3 -9% 711.3 719 -1%

Peninsula Land 1,687.2 1,154 46% 728.7 328.5 122%

Pheonix 263.9 247.9 6% 175.4 153.3 14%

MahindraLifespaces 635.2 472.6 34% 173.4 104.2 66%

Ackruti City 782.9 409 91% 297.9 100.2 197%

13-A

ug-0

713

-Sep

t-07

13-O

ct-0

713

-Nov

-07

13-D

ec-0

713

-Jan

-08

13-F

eb-0

813

-Mar

-08

13-A

pr-0

813

-May

-08

13-J

un-0

813

-Jul

-08

13-A

ug-0

813

-Sep

t-08

13-O

ct-0

813

-Nov

-08

13-D

ec-0

813

-Jan

-09

13-F

eb-0

913

-Mar

-09

13-A

pr-0

913

-May

-09

13-J

un-0

913

-Jul

-09

13-A

ug-0

913

-Sep

t-09

0

5,000

10,000

15,000

20,000

25,000

-4%-2%0%

4%

8%10%12%

2%

6%

14%

05-J

ul-0

8

05-A

ug-0

8

05-S

ept-

08

05-O

ct-0

8

05-N

ov-0

8

05-D

ec-0

8

05-J

an-0

9

05-F

eb-0

9

05-M

ar-0

9

05-A

pr-0

9

05-M

ay-0

9

05-J

un-0

9

05-J

ul-0

9

05-A

ug-0

9

05-S

ept-

09

4I I

MACROECONOMIC CONTEXT

GDP growth rate beat all estimates. Records 7.9%

India recorded a GDP growth of 7.9 % in the quarter – July –September of 2009, which is more than estimated rate of 6.1%. In fact, this is the highest growth in GDP rate ever since 1996. The key factors are increase in domestic consumption, global recovery and abundant liquidity in the system. The manufacturing and service sector grew by more than 9% . Despite the weak credit demand, the banking and financial sector also showed a healthy growth. The agriculture sector showed the highest growth, however the perception among the industry leaders is that the harvest shortfall will get captured in the next quarter and therefore the overall GDP will be lower for the next quarter. There is also a perception that the central bank is now poised to increase the Cash Reserve Rate (CRR) Ratio and Reverse Repo Rate as the inflation is expected to breach central bank's comfort level by January 2010. The finance ministry has also made a statement that it will review the situation in February 2010. Major business chambers feel there's a need for the government to continue with the existing monetary and fiscal policies to sustain the process of economic recovery.

The high GDP rate indicate that the government policy measures have been successful in reversing the impact of the global slowdown. It is expected that the recovery will be sustainable, as investment and consumption are showing an upswing, and with policy guidance a growth rate of 7% can be achieved in the current financial year.

Wholesale Price Index (WPI)

Sensex Nifty

Sensex & Nifty

CITY REPORTMUMBAI OFFICE MARKET - Q3 2009

Source: Confederation of Indian Industries

Source: Confederation of Indian Industries

Source: Confederation of Indian Industries

Gross Domestic Product (GDP)

Q12008

Q22008

Q32008

Q42008

Q12009

Q22009

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

10.10%

9.30%9.70%

9.20%9.30%

8.80% 8.80%

7.90%7.60%

5.30%5.80%

6.10%

Q32006

Q42006

Q12007

Q22007

Q32007

Q42007

Q32009

7.90%

Real Estate Most of the real estate development companies showed high growth rate both in sales and profits. This is fuelled by lowering of interest rates on home loans by banks & financial institutions and further lowering of property prices. Most of the growth is due to higher sales in residential developments and also due to sale of land which have resulted in windfall profits for certain companies in this quarter. In the stock markets, the stocks of major listed real estate development companies saw a surge both in terms of price and volumes. It is expected that the demand for commercial real estate development will pick up across the country, in the next two quarters both in terms of sales and leasing.

in certain cases,

Major Real EstateCompanies in

India

Sales (In INR / In Million) Profits (In INR / In Million)Q3 09 Q2 09 Q on Q

Change %Q3 09 Q2 09 Q on Q

Change %

Unitech 5,094.9 5,149 -1% 1,778.6 1,577.7 13%

Sobha Developers 2,236 1,771 26% 275 127 117%

ParsvnathDevelopers 1,684.7 1,137.2 48% 614.3 138.1 345%

Omaxe Limited 2,239.2 1,189.1 88% 225.1 149.7 50%

Ananthraj 871.3 824.8 6% 712.7 689.3 3%

Ansal Properties 1,768.4 1,367.4 29% 316 103.2 206%

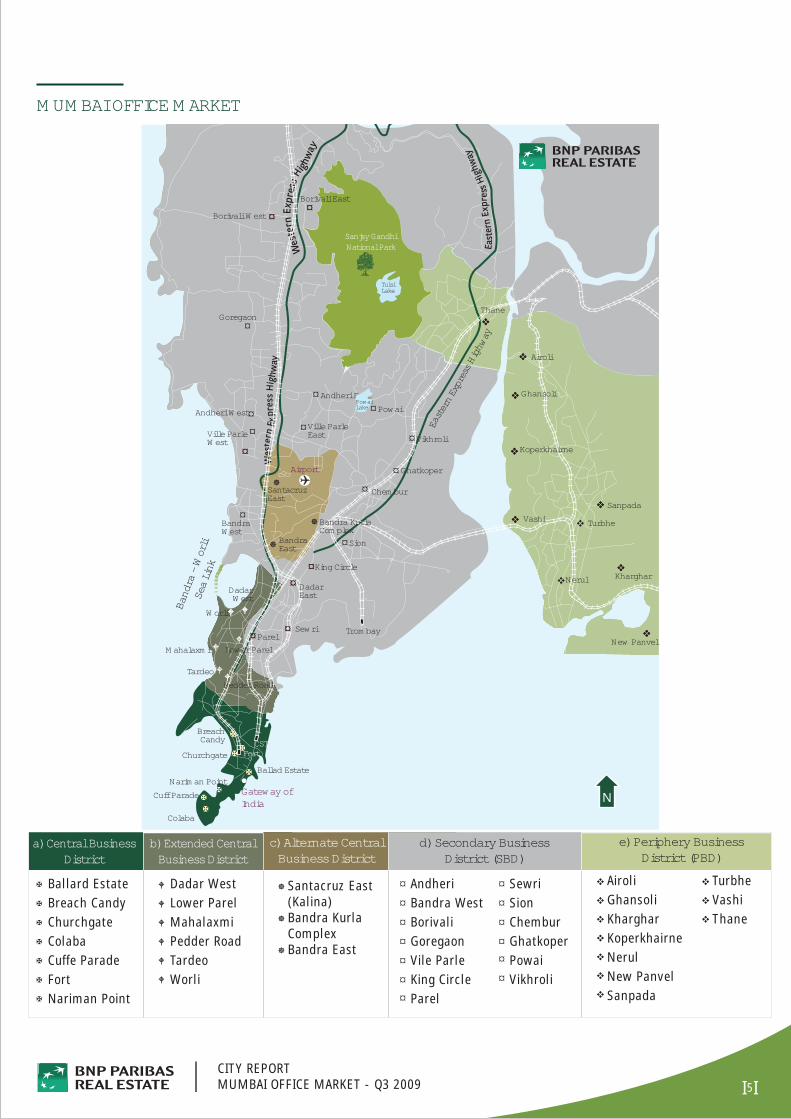

MUMBAI OFFICE MARKET

5I I

Ballard EstateBreach CandyChurchgateColabaCuffe ParadeFortNariman Point

X

X

X

X

X

X

X

Dadar WestLower ParelMahalaxmiPedder RoadTardeoWorli

W

W

W

W

W

W

]

]

]

Santacruz East (Kalina)Bandra KurlaComplexBandra East

a) Central BusinessDistrict

c) Alternate CentralBusiness District

d) Secondary District (SBD)

Businessb) Extended CentralBusiness District

Band

ra -

Wor

liSe

a Li

nk

X

¤

X

X

XX

X

¤

¤¤

¤

¤

v

v

v

v

v

Sanjay GandhiNational Park

¤

v

v

v

WW

yawhgiH sserpxE nretsaE

X

W

]

¤

v

X

X

XX

X

W

W

WW

W¤

¤¤

]

¤

¤¤¤

¤

¤

¤¤

¤

¤

¤

v

v

v

v v

v

v

v

Airport

Colaba

Cuff Parade Gateway ofIndia

Ballad Estate

Churchgate

BreachCandy

XNariman Point

Fort

DadarWest

Lower ParelMahalaxmi

Pedder RoadTardeo

Worli

SantacruzEast

BandraEast

]Bandra KurlaComplex

Andheri East

Andheri West

BandraWest

Borivali East

Borivali West

Goregaon

¤Ville ParleEastVille Parle

West

DadarEast

King Circle

ParelSewri

Sion

Chembur

Vikhroli

Airoli

Ghansoli

Kharghar

Koperkhairne

vNerul

New Panvel

Sanpada

TurbheVashi

Thane

e) Periphery BusinessDistrict (PBD)

AiroliGhansoliKhargharKoperkhairneNerulNew PanvelSanpada

v

v

v

v

v

v

v

TurbheVashiThane

v

v

v

N

¤Powai

¤Ghatkoper

SewriSionChemburGhatkoperPowaiVikhroli

¤¤¤¤¤¤

CITY REPORTMUMBAI OFFICE MARKET - Q3 2009

AndheriBandra WestBorivaliGoregaonVile ParleKing CircleParel

¤¤¤¤¤¤¤

PowaiLake

TulsiLake

Trombay

CST

6I I

CENTRAL BUSINESS DISTRICT (CBD)

In the CBD area, no fresh suppy was added. However a few old buildings are being refurbished and repositioned as the new Grade- A supply. One such example is Express Towers in Nariman point, located at walking distance from Trident – Oberoi Hotel. The letting rates have now stabilised, though the owners have become more flexible in offering long term leases (9 years). There is an opportunistic demand from small and medium investors to own offices between 3,000- 10,000 sq.ft. in the Nariman point/ Fort/ Cuffe Parade area. However, no fresh supply is recorded in this area. There is a demand for office space in excess of 50,000 sq.ft. from 4-5 corporates in the banking and financial services industry.

Q22008

Q32008

Q42008

Q12009

Q22009

—

10,000

20,000

30,000

40,000

50,000

60,000

Nariman Point Ballard Estate

Cuffe Parade Fort

Capi

tal V

alue

s (in

Rs

/ sq.

ft)

CITY REPORTMUMBAI OFFICE MARKET - Q3 2009

Repositioning of old stock has started to happen

70,000

Q22008

Q32008

Q42008

Q12009

Q22009

0

100

200

300

400

500

Nariman Point Ballard Estate

Cuffe Parade Fort

600

Rent

al V

alue

s (in

Rs

/ sq.

ft /

mon

th)

Q32009

Q32009

Ballard Estate 450 400 300 275 250

Nariman Point 500 450 375 350 325Fort 300 250 170 150 150

Cuffe Parade 350 280 250 225 200

Q22008

Q32008

Q42008

Q12009

Q22009

RENTALS OVER THE PAST 6 QUARTERS

Source: BNP Paribas Real Estate, India

Q32009

250

325150

200

Q22008

Q32008

Q42008

Q12009

Q22009

Ballard Estate 45,000 42,000 38,000 35,000 35,000

Nariman Point 60,000 50,000 45,000 40,000 40,000Fort 30,000 27,500 25,000 22,500 22,500

Cuffe Parade 35,000 32,000 32,000 30,000 30,000

CAPITAL VALUES OVER THE PAST 6 QUARTERS

Source: BNP Paribas Real Estate, India

Q32009

35,000

40,00022,500

30,000

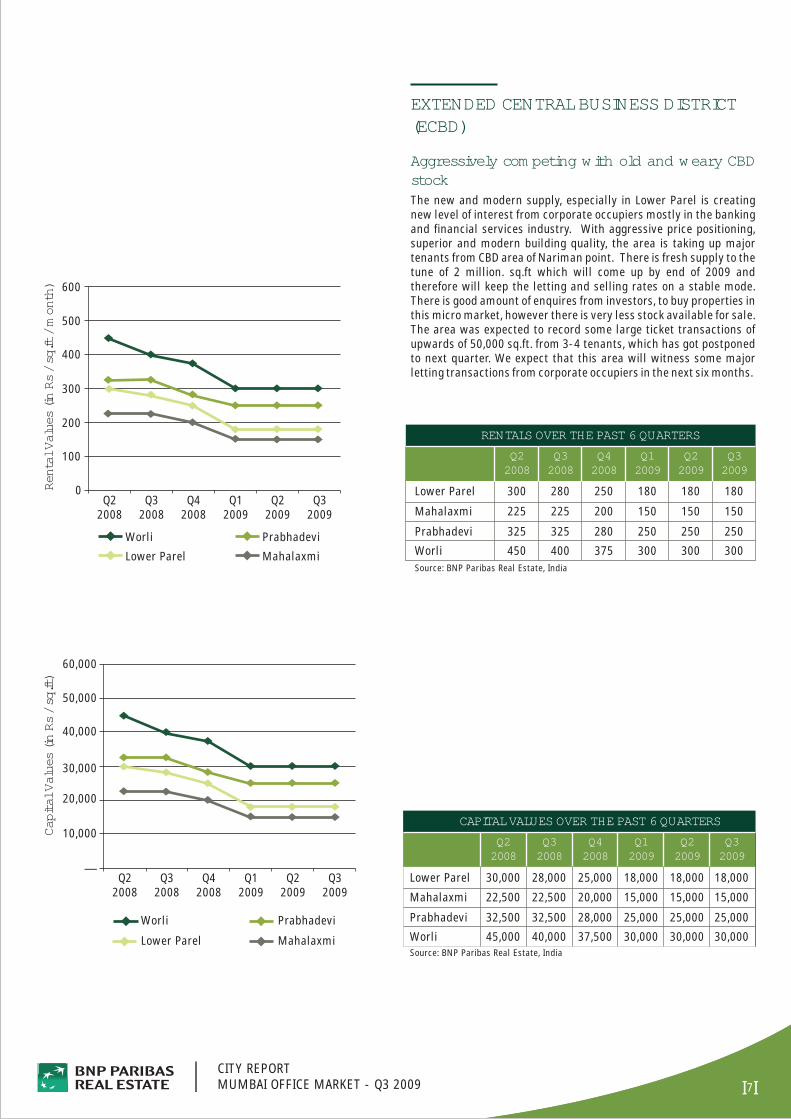

EXTENDED CENTRAL BUSINESS DISTRICT(ECBD)

The new and modern supply, especially in Lower Parel is creating new level of interest from corporate occupiers mostly in the banking and financial services industry. With aggressive price positioning, superior and modern building quality, the area is taking up major tenants from CBD area of Nariman point. There is fresh supply to the tune of 2 million. sq.ft which will come up by end of 2009 and therefore will keep the letting and selling rates on a stable mode. There is good amount of enquires from investors, to buy properties in this micro market, however there is very less stock available for sale. The area was expected to record some large ticket transactions of upwards of 50,000 sq.ft. from 3-4 tenants, which has got postponed to next quarter. We expect that this area will witness some major letting transactions from corporate occupiers in the next six months.

7I ICITY REPORTMUMBAI OFFICE MARKET - Q3 2009

Aggressively competing with old and weary CBD stock

Rent

al V

alue

s (in

Rs

/ sq.

ft /

mon

th)

Q22008

Q32008

Q42008

Q12009

Q22009

0

100

200

300

400

Worli Prabhadevi

Lower Parel Mahalaxmi

500

600

Q32009

Capi

tal V

alue

s (in

Rs

/ sq.

ft)

Q22008

Q32008

Q42008

Q12009

Q22009

—

10,000

30,000

40,000

Worli Prabhadevi

Lower Parel Mahalaxmi

50,000

60,000

20,000

Q32009

Mahalaxmi 225 225 200 150

Lower Parel 300 280 250 180

Worli 450 400 375 300 300

Prabhadevi 325 325 280 250 250

150

180

Q22008

Q32008

Q42008

Q12009

Q22009

RENTALS OVER THE PAST 6 QUARTERS

Source: BNP Paribas Real Estate, India

Q32009

300

250

150

180

Q22008

Q32008

Q42008

Q12009

Q22009

Mahalaxmi 22,500 22,500 20,000 15,000

Lower Parel 30,000 28,000 25,000 18,000

Worli 45,000 40,000 37,500 30,000 30,000

Prabhadevi 32,500 32,500 28,000 25,000 25,000

15,000

18,000

CAPITAL VALUES OVER THE PAST 6 QUARTERS

Source: BNP Paribas Real Estate, India

Q32009

30,000

25,000

15,000

18,000

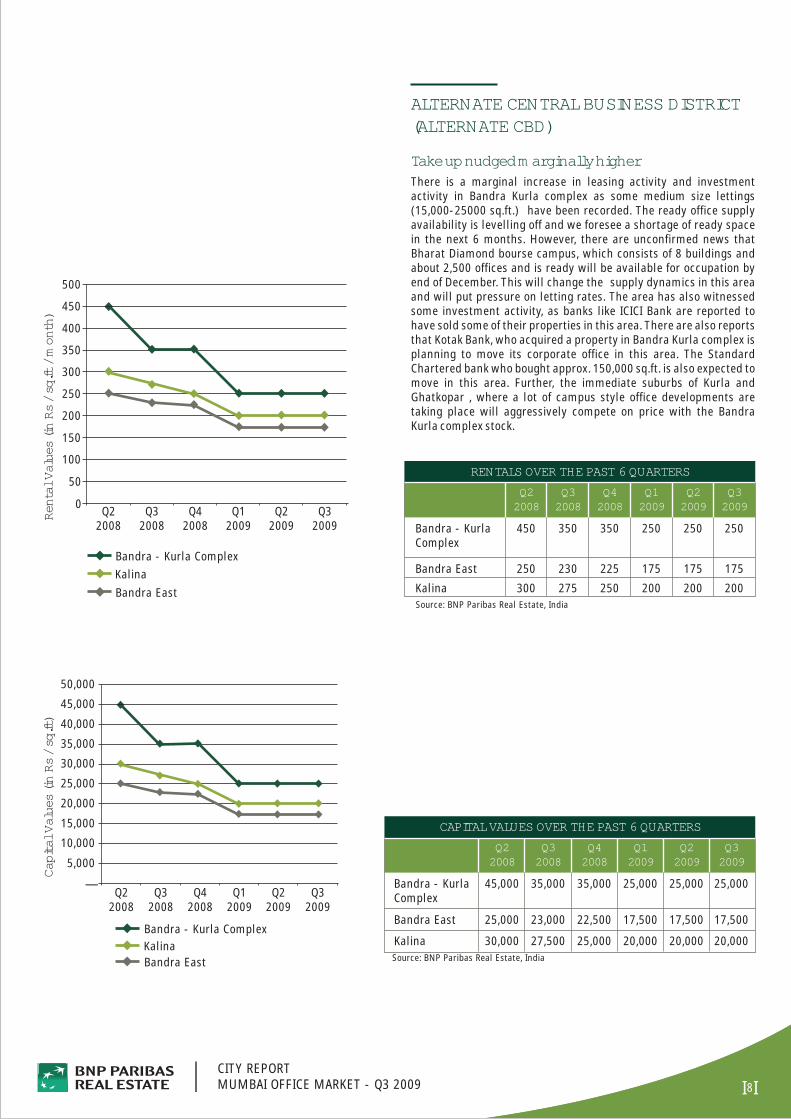

ALTERNATE CENTRAL BUSINESS DISTRICT(ALTERNATE CBD)

There is a marginal increase in leasing activity and investment activity in Bandra Kurla complex as some medium size lettings (15,000-25000 sq.ft.) have been recorded. The ready office supply availability is levelling off and we foresee a shortage of ready space in the next 6 months. However, there are unconfirmed news that Bharat Diamond bourse campus, which consists of 8 buildings and about 2,500 offices and is ready will be available for occupation by end of December. This will change the supply dynamics in this area and will put pressure on letting rates. The area has also witnessed some investment activity, as banks like ICICI Bank are reported to have sold some of their properties in this area. There are also reports that Kotak Bank, who acquired a property in Bandra Kurla complex is planning to move its corporate office in this area. The Standard Chartered bank who bought approx. 150,000 sq.ft. is also expected to move in this area. Further, the immediate suburbs of Kurla and Ghatkopar , where a lot of campus style office developments are taking place will aggressively compete on price with the Bandra Kurla complex stock.

8I I

Capi

tal V

alue

s (in

Rs

/ sq.

ft)

Q22008

Q32008

Q42008

Q12009

Q22009

—

5,000

20,000

25,000

40,000

10,000

15,000

30,000

35,000

Bandra - Kurla ComplexKalinaBandra East

CITY REPORTMUMBAI OFFICE MARKET - Q3 2009

Take up nudged marginally higher

50,000

45,000

Q32009

Bandra - Kurla ComplexKalinaBandra East

Rent

al V

alue

s (in

Rs

/ sq.

ft /

mon

th)

Q22008

Q32008

Q42008

Q12009

Q22009

0

50

100

150

200

250

300

350

400

450

500

Q32009

Q22008

Q32008

Q42008

Q12009

Q22009

Bandra - KurlaComplex

450 350 350 250 250

Bandra East 250 230 225 175 175

Kalina 300 275 250 200 200

RENTALS OVER THE PAST 6 QUARTERS

Source: BNP Paribas Real Estate, India

Q32009

250

175

200

Bandra - KurlaComplex

45,000 35,000 35,000 25,000 25,000

Bandra East 25,000 23,000 22,500 17,500 17,500

Kalina 30,000 27,500 25,000 20,000 20,000

Q22008

Q32008

Q42008

Q12009

Q22009

CAPITAL VALUES OVER THE PAST 6 QUARTERS

Source: BNP Paribas Real Estate, India

Q32009

25,000

17,500

20,000

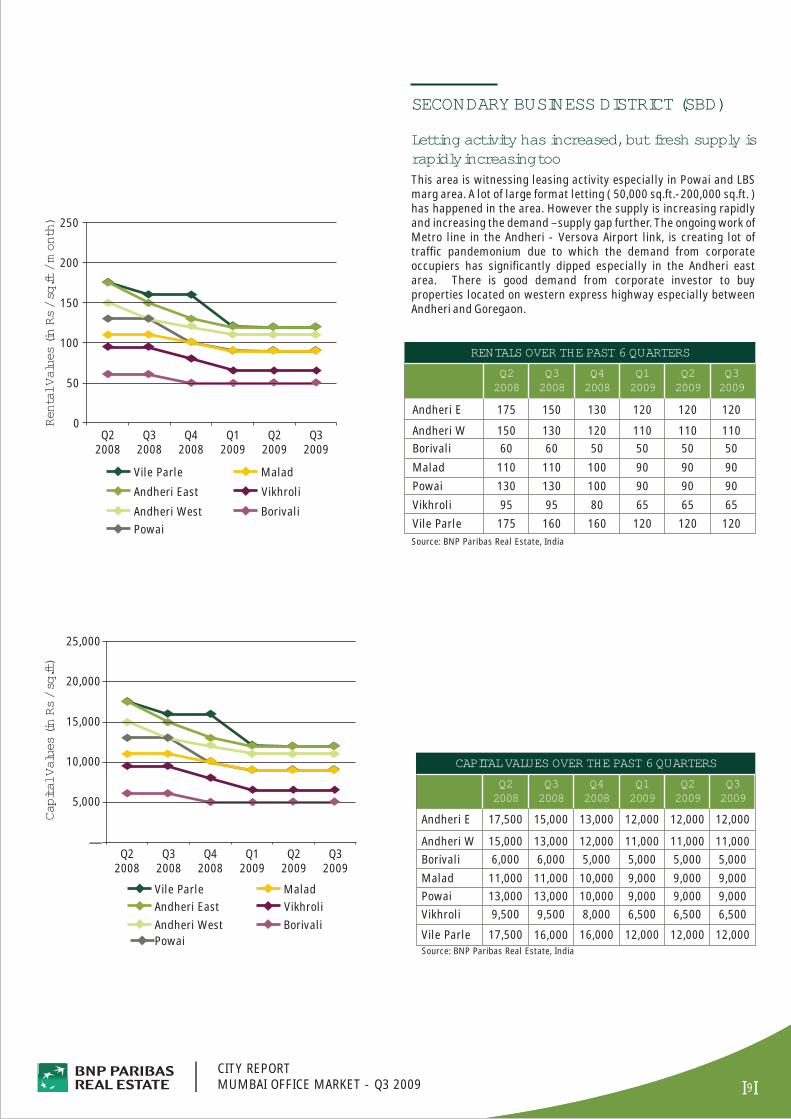

SECONDARY BUSINESS DISTRICT (SBD)

This area is witnessing leasing activity especially in Powai and LBS marg area. A lot of large format letting ( 50,000 sq.ft.-200,000 sq.ft. ) has happened in the area. However the supply is increasing rapidly and increasing the demand –supply gap further. The ongoing work of Metro line in the Andheri - Versova Airport link, is creating lot of traffic pandemonium due to which the demand from corporate occupiers has significantly dipped especially in the Andheri east area. There is good demand from corporate investor to buy properties located on western express highway especially between Andheri and Goregaon.

9I ICITY REPORTMUMBAI OFFICE MARKET - Q3 2009

Letting activity has increased, but fresh supply is rapidly increasing too

Capi

tal V

alue

s (in

Rs

/ sq.

ft)

—

5,000

25,000

20,000

Vile ParleAndheri EastAndheri WestPowai

MaladVikhroliBorivali

10,000

15,000

Q22008

Q32008

Q42008

Q12009

Q22009

Q32009

Rent

al V

alue

s (in

Rs

/ sq.

ft /

mon

th)

Q22008

Q32008

Q42008

Q12009

Q22009

0

100

150

200

Vile Parle

Andheri East

Andheri WestPowai

Malad

Vikhroli

Borivali

50

250

Q32009

Q22008

Q32008

Q42008

Q12009

Q22009

Vile Parle 175 160 160 120 120

Andheri W 150 130 120 110 110

Andheri E 175 150 130 120 120

Powai 130 130 100 90 90Vikhroli 95 95 80 65

Malad 110 110 100 90Borivali 60 60 50 50

65

9050

RENTALS OVER THE PAST 6 QUARTERS

Source: BNP Paribas Real Estate, India

Q32009

120

110

120

9065

9050

Vile Parle 17,500 16,000 16,000 12,000 12,000

Andheri W 15,000 13,000 12,000 11,000 11,000

Andheri E 17,500 15,000 13,000 12,000 12,000

Powai 13,000 13,000 10,000 9,000 9,000Vikhroli 9,500 9,500 8,000 6,500 6,500

Malad 11,000 11,000 10,000 9,000 9,000Borivali 6,000 6,000 5,000 5,000 5,000

Q22008

Q32008

Q42008

Q12009

Q22009

CAPITAL VALUES OVER THE PAST 6 QUARTERS

Source: BNP Paribas Real Estate, India

Q32009

12,000

11,000

12,000

9,0006,500

9,0005,000

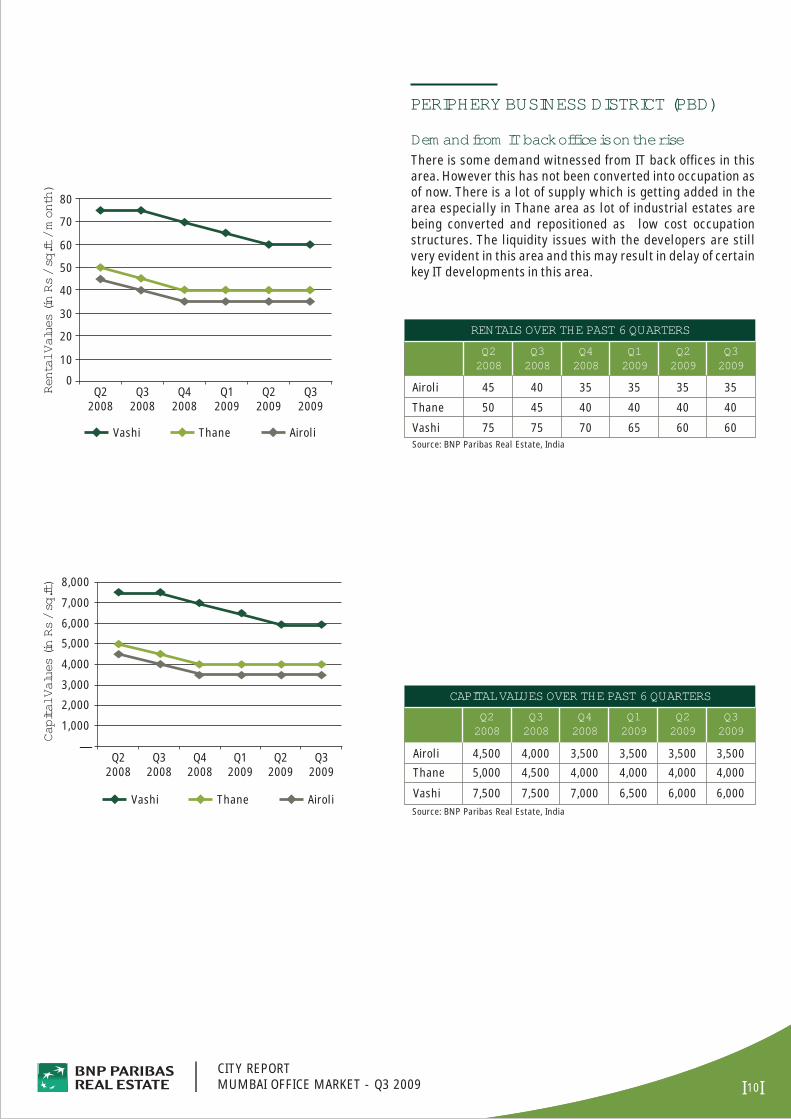

PERIPHERY BUSINESS DISTRICT (PBD)

There is some demand witnessed from IT back offices in this area. However this has not been converted into occupation as of now. There is a lot of supply which is getting added in the area especially in Thane area as lot of industrial estates are being converted and repositioned as low cost occupation structures. The liquidity issues with the developers are still very evident in this area and this may result in delay of certain key IT developments in this area.

10I ICITY REPORTMUMBAI OFFICE MARKET - Q3 2009

Demand from IT back office is on the rise

Q22008

Q32008

Q42008

Q12009

Q22009

0

10

20

30

40

50

60

70

80

Vashi Thane Airoli

Rent

al V

alue

s (in

Rs

/ sq.

ft /

mon

th)

Q32009

Q22008

Q32008

Q42008

Q12009

Q22009

—

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Capi

tal V

alue

s (in

Rs

/ sq.

ft)

Vashi Thane Airoli

Q32009

Thane 50 45 40 40 40

Airoli 45 40 35 35 35

Vashi 75 75 70 65 60

Q22008

Q32008

Q42008

Q12009

Q22009

RENTALS OVER THE PAST 6 QUARTERS

Source: BNP Paribas Real Estate, India

Q32009

40

35

60

Thane 5,000 4,500 4,000 4,000 4,000

Airoli 4,500 4,000 3,500 3,500 3,500

Vashi 7,500 7,500 7,000 6,500 6,000

Q22008

Q32008

Q42008

Q12009

Q22009

CAPITAL VALUES OVER THE PAST 6 QUARTERS

Source: BNP Paribas Real Estate, India

Q32009

4,000

3,500

6,000

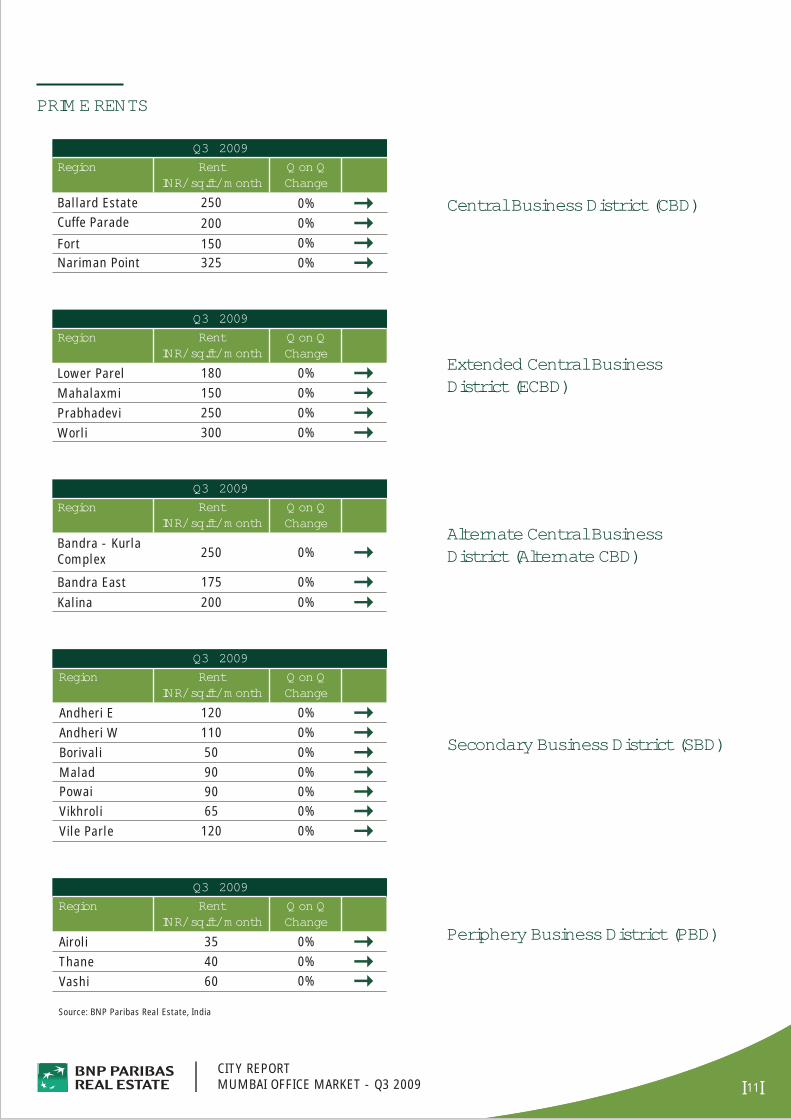

PRIME RENTS

Central Business District (CBD)

Extended Central BusinessDistrict (ECBD)

Alternate Central BusinessDistrict (Alternate CBD)

11I I

Secondary Business District (SBD)

Periphery Business District (PBD)

CITY REPORTMUMBAI OFFICE MARKET - Q3 2009

RentINR/ sq.ft/ month

Ballard Estate 250

Nariman Point 325Fort 150

Cuffe Parade 200

Region Q on QChange

Q3 2009

Mahalaxmi 150 0%Lower Parel 180

Worli 300Prabhadevi 250 0%

Region RentINR/ sq.ft/ month

0%

0%

Q on QChange

Q3 2009

Bandra - KurlaComplex 250 0%

Bandra East 175 0%Kalina 200 0%

Region RentINR/ sq.ft/ month

Q on QChange

Q3 2009

Vile Parle 120 0%

Andheri W 110Andheri E 120

Powai 90

Region

Vikhroli 65

Malad 90Borivali 50

RentINR/ sq.ft/ month

0%0%

0%

0%0%

0%

Q on QChange

Q3 2009

Thane 40 0%Airoli 35 0%

Vashi 60

Region RentINR/ sq.ft/ month

Q on QChange

Q3 2009

Source: BNP Paribas Real Estate, India

0%0%

0%

0%

0%

CAPITAL VALUES

Central Business District (CBD)

Extended Central BusinessDistrict (ECBD)

Alternate Central BusinessDistrict (Alternate CBD)

12I I

Secondary Business District (SBD)

Periphery Business District (PBD)

CITY REPORTMUMBAI OFFICE MARKET - Q3 2009

Thane 4,000 0%Airoli 3,500 0%

Vashi 6,000

Region Q on QChange

CAPITAL Q3 2009

Vile Parle 12,000 0%

Andheri W 11,000Andheri E 12,000

Powai 9,000Vikhroli 6,500

Malad 9,000Borivali 5,000

0%0%

0%

0%0%

0%

Region Q on QChange

CAPITAL Q3 2009

Bandra - KurlaComplex 25,000 0%

Bandra East 17,500 0%Kalina 20,000 0%

Region Q on QChange

CAPITAL Q3 2009

Mahalaxmi 15,000 0%Lower Parel 18,000

Worli 30,000Prabhadevi 25,000 0%

0%

0%

Region Q on QChange

CAPITAL Q3 2009

Ballard Estate 35,000 0%

Nariman Point 40,000 0%Fort 22,500 0%Cuffe Parade 30,000 0%

RegionCAPITAL Q3 2009

INR / sq.ft Q on QChange

INR / sq.ft

INR / sq.ft

INR / sq.ft

INR / sq.ft

Source: BNP Paribas Real Estate, India

0%

13I I

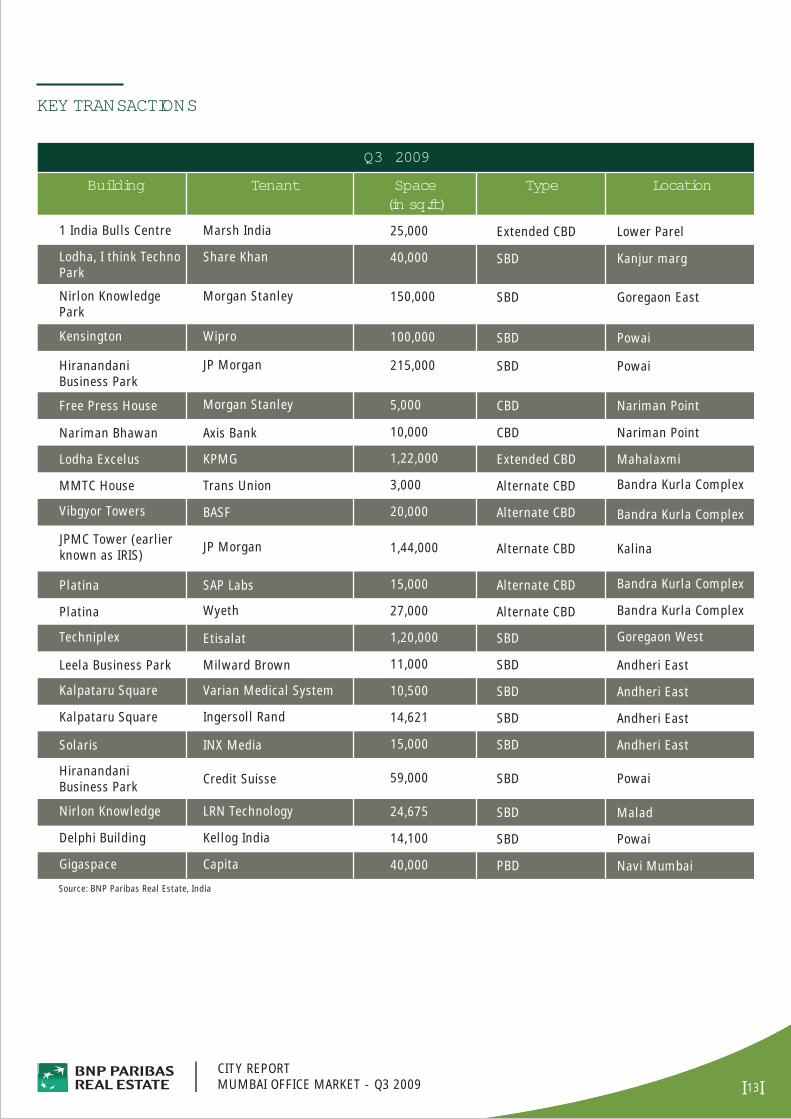

KEY TRANSACTIONS

Building Tenant Space(in sq.ft)

Type Location

CITY REPORTMUMBAI OFFICE MARKET - Q3 2009

Q3 2009

Nariman Bhawan Axis Bank 10,000 CBD Nariman Point

MMTC House Trans Union 3,000 Alternate CBD

JPMC Tower (earlierknown as IRIS) JP Morgan 1,44,000 Alternate CBD Kalina

Bandra Kurla Complex

Platina Wyeth 27,000 Alternate CBD Bandra Kurla Complex

Leela Business Park Milward Brown 11,000 SBD Andheri East

Kalpataru Square Ingersoll Rand 14,621 SBD Andheri East

HiranandaniBusiness Park Credit Suisse 59,000 SBD Powai

Delphi Building Kellog India 14,100 SBD Powai

Free Press House Morgan Stanley 5,000 CBD Nariman Point

Lodha Excelus KPMG 1,22,000 Extended CBD Mahalaxmi

Vibgyor Towers BASF 20,000 Alternate CBD Bandra Kurla Complex

Platina SAP Labs 15,000 Alternate CBD Bandra Kurla Complex

Techniplex Etisalat 1,20,000 SBD Goregaon West

Kalpataru Square Varian Medical System 10,500 SBD Andheri East

Solaris INX Media 15,000 SBD Andheri East

Nirlon Knowledge LRN Technology 24,675 SBD Malad

Gigaspace Capita 40,000 PBD Navi Mumbai

Source: BNP Paribas Real Estate, India

1 India Bulls Centre Marsh India 25,000 Lower Parel

Lodha, I think TechnoPark

Share Khan 40,000 Kanjur marg

Nirlon KnowledgePark

Morgan Stanley 150,000 Goregaon East

Kensington Wipro 100,000 Powai

JP Morgan 215,000 Powai

Extended CBD

SBD

SBD

SBD

SBD

HiranandaniBusiness Park

14I I

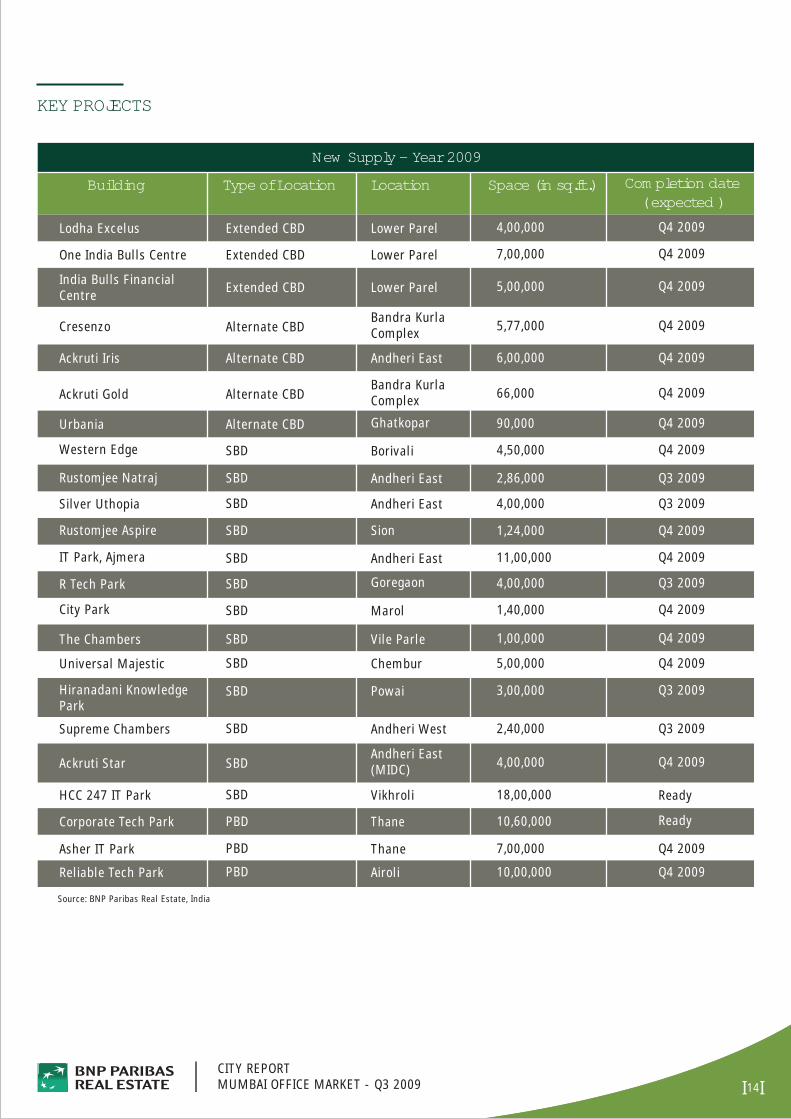

KEY PROJECTS

Building Type of Location Location Space (in sq.ft.) Completion date( expected )

CITY REPORTMUMBAI OFFICE MARKET - Q3 2009

New Supply – Year 2009

Lodha Excelus Extended CBD Lower Parel 4,00,000 Q4 2009

One India Bulls Centre Lower Parel Q4 2009Extended CBD 7,00,000

India Bulls FinancialCentre Extended CBD Lower Parel 5,00,000 Q4 2009

Cresenzo Alternate CBDBandra KurlaComplex 5,77,000 Q4 2009

Ackruti Star SBDAndheri East(MIDC) 4,00,000 Q4 2009

Ackruti Iris Alternate CBD Andheri East 6,00,000 Q4 2009

Rustomjee Aspire SBD Sion 1,24,000 Q4 2009

Supreme Chambers SBD Andheri West 2,40,000 Q3 2009

Bandra KurlaComplexAckruti Gold Alternate CBD 66,000 Q4 2009

Hiranadani KnowledgePark

SBD Powai 3,00,000 Q3 2009

Western Edge SBD Borivali 4,50,000 Q4 2009

Silver Uthopia SBD Andheri East 4,00,000 Q3 2009

IT Park, Ajmera SBD Andheri East 11,00,000 Q4 2009

City Park SBD Marol 1,40,000 Q4 2009

Universal Majestic SBD Chembur 5,00,000 Q4 2009

Asher IT Park PBD Thane 7,00,000 Q4 2009

Source: BNP Paribas Real Estate, India

Urbania Alternate CBD Ghatkopar 90,000 Q4 2009

Rustomjee Natraj SBD Andheri East 2,86,000 Q3 2009

R Tech Park SBD Goregaon 4,00,000 Q3 2009

The Chambers SBD Vile Parle 1,00,000 Q4 2009

Reliable Tech Park PBD Airoli 10,00,000 Q4 2009

Corporate Tech Park PBD Thane Ready

HCC 247 IT Park SBD Vikhroli Ready18,00,000

10,60,000

GLOSSARYQ3:

Absorption:

Bare Shell:

BPO:

BUA:

CBD:

ECBD:

ACBD:

SBD:

PBD:

Completed Stock:

DU:

EPIP:

FAR:

Grade A:

Ground Coverage:

Hard Option:

INR:

Rs:

PBD:

Pre-lease:

Speculative Stock:

Stock:

Supply:

Tier I Cities:

Tier II Cities:

Transaction Volumes:

Vacancy:

Warm Shell:

Q on Q:

y-o-y:

IT:

ITES:

NCR:

ORR:

Repo Rate:

Reverse Repo Rate:

SEC A, B, C & D Socio:

Sq.ft:

Stamp Duty:

Quarter 3 of the financial year

Occupied Stock (n) – Occupied Stock (n-1); Where “n” is the specified period (quarter, year etc.)

Premises consisting of basic structure with lifts, power supply to junction box, water supply line, toilets

Business Process Outsourcing

Built up area

Central Business District

Extended Central Business District

Alternate Central Business District

Secondary Business District

Periphery Business District

Either the building has received occupancy certificate or the client has moved in and occupied space and started working in a particular premises

Dwelling Unit

Export Promotion Industrial Park

Floor Area Ratio (BUA/ Plot Area)

Space Office Space with efficiency in excess of 75%, floor plate in excess of 15,000 sq. ft., Car Parking ratio of atleast 1 per 1000 sq. ft., Floor-to-ceiling height in excess of 3.75 m, Power provision of 1.25KVA per 100 sq. ft. with 100% power-backup wherever applicable and professionally managed facilities

It is the total covered area on ground by the built component and is expressed as a percentage of the plot area

Real estate space reserved by the lessee for future occupation within a particular time frame and at a pre-decided rental

Indian National Rupees

Rupees

Peripheral Business District

Space committed for lease before completion of construction

The stock which can be leased and excludes Built-to-Suit (BTS) and Campus facilities.

Cumulative Supply

New construction in a particular specified period

NCR, Mumbai and Bangalore

Chennai, Hyderabad, Pune, Kolkata

Total number of transaction in a particular specified period

Total vacant space in the completed stock

Premises consisting of power backup, high side A.C., common area fit outs and fitted out toilets

Quarter on Quarter

year-on-year (All growth figures in this report are y-o-y unless otherwise mentioned

Information Technology

Information Technology Enabled Services (includes various services ranging from call centres, claims processing, medical transcription, e-CRM, SCM to back-office operations such as accounting, data processing, and data mining)

National Capital Region (includes urban agglomeration of Delhi, Gurgaon, Faridabad, Noida, Gaziabad etc.)

Outer Ring Road

Rate that an eligible depository institution (such as a bank) is charged to borrow short term funds directly from the central bank through the discount window

Interest rate that a bank earns for lending money to the Reserve Bank of India in exchange for government securities

Economic Classification; SEC A represents the highest propensity to spend and SEC D represents the lowest propensity to spend.

Square Feet

Form of tax charged on instruments (written documents) requiring a physical stamp (for government legality) to be attached to or impressed.

NRI:

New:

Non Resident Indian.

Building built within the last 5 years.

Major Refurbishment:

Recent:

Renovated:

Modern:

Old:

CCI (Cost of construction index):

Demand:

For the occupier:

New Supply:

Completed new supply:

Planning permission granted:

Planning permission submitted:

Pre-letting:

Headline rent:

Average headline rent:

Underlying rent:

Prime rents:

Top rent:

Second hand premises:

Renovated:

Very good condition:

Existing state of repair:

To be renovated:

Supply available within 1 year:

Take-up:

Vacancy rate:

Building which has undergone structural alteration less than 5 years ago, subject to planning permission.

Building less than 10 years old.

Building which has undergone renovation work not requiring for planning permission less than 5 years ago.

High-performance building over 10 years old.

Low-performance building over 10 years old.

Index that makes quarterly measurements of construction prices for new house building. It is the price after VAT paid by the owner to construction companies. It excludes land-related prices and costs (site development, special foundations, etc.), fees and financial costs.

A search for premises expressed to BNP Paribas Real Estate. The analysis pertains only to the flow of new demand expressed.

Operation undertaken by an occupier for its own purposes.

Any new building and/or heavily refurbished building that adds to the existing stocks. These are analysed according to progress.

Buildings on which construction work is finished.

Under construction: Buildings on which construction has effectively begun. Prior demolition work is not taken into account.

Authorisation to build obtained, generally booked after settlement of third party claims.

Planning permission requested, being processed.

Transaction by an occupier more than 6 months before the delivery of the building.

Annual rent per square meter, featured on the lease, and expressed excluding taxes and charges. Does not include attached premises such as parking areas, archives, staff canteens, etc. If the rental is progressive, the value applied is the average for the first 3 years or the fixed term of the lease.

Weighted average of rented area. The average featured is a moving average over 3 quarters, to smooth out the changes.

Annual rent per square meter expressed free of tax and charges and excluding advantages agreed by the owners (rent incentive building works, etc).

Represents the top headline rent (excluding non significant transactions) for an office unit:- of standard size, of the highest quality and specification, in the best location in each market.

Represents the top headline rent for an office unit. It is not necessarily a prime rent.

Premises that have been previously occupied by an occupier for vacant for more than 5 years.

Premises that have been renovated for the new occupier.

High-performance premises of high quality.

Low-performance premises that can be rented as they are.

Low performance premises that need renovation.

All premises and buildings available within 1 year including the supply available immediately, new supply that has not been pre-let and second hand supply that will be vacated definitively (notable terminated leases).

Rental or sale of a property asset, finalised by the signature of a lease or a bill of sale including turnkey transactions and owner-occupier. The transaction is only taken into account once any existing conditional clauses have been lifted.

Ration measuring the relationship between the supply immediately available and the existing stock.

BNP Paribas Real Estate cannot be held responsible if, despites its best efforts, the information contained in the present report turns out to be inaccurate or incomplete. This report is released by BNP Paribas Real Estate and the information in it is dedicated to the exclusive use of its clients. The report and the information contained in it may not be copied or reproduced without prior permission from BNP Paribas Real Estate.

15I ICITY REPORTMUMBAI OFFICE MARKET - Q3 2009

ALBANIADanosBoulevard Deshmoret e KombitTwin Towers - Tower 211th FloorTiranaTel: +355-4-2280488Fax: +355-4-2280192

AUSTRIADr. Max Huber & PartnerDr. Karl-Lueger-Platz 51010 WienTel: +43-1-513 29 39 0Fax: +43-1-513 29 39 14

BULGARIADanos28, Hristo Botev BoulevardSofiaTel: +359-2-9532314Fax: +359-2-9532399

CANADACresa PartnersTel: +1-212-758 3131Fax: +1-212-980 1977

USA787 Seventh Avenue31st FloorNew York City, NY 10019Tel: +1-917-472 4970Fax: +1-212-471 8100

GREECEDanos1, Eratosthenous Str.11635 AthensTel: +30-210 7 567 567Fax: +30-210 7 567 267

JAPANRISA Partners5F Akasaka Intercity 1-11-44Akasaka, Minato-ku107-0052 TokyoTel: +81-3-5573 8011Fax: +81-3-5573 8012

PORTUGALFenaluAv. Eng. Duarte PachecoTorre 2Piso 10, Sala 6/71070-102 LisboaTel: +351-21-3833106Fax: +351-21-3833107

NETHERLANDSHolland Realty PartnersJ.J. Viottastraat 33, 1071 JPAmsterdam,Postbus 96691006 GD AmsterdamTel: +31-20-305 97 20Fax: +31-20-305 97 21

NORTHERN IRELANDWhelan Property Consultants44 Upper Arthur StreetBelfast Bt1 4GJTel: +44-28-9044 1000Fax: +44-28-9033 2266

POLANDKancelaria BrochockiKrakowskie Przedmiescie 1400325 WarsawTel: +48-22-826 14 14Fax: +48-22-828 15 45

Bangalore403, The Estate,121, Dickenson Road,Bangalore - 560 042Tel: +91 80 4050 8888Fax: +91 80 4050 8899

Contact: Anuj [email protected]

Mumbai704, Level 7, MMTC House, C-22,Bandra Kurla Complex, Bandra (E),Mumbai - 400 051Tel: +91 22 6138 8088Fax: +91 22 6138 8089

Contact: Raja [email protected]

DelhiLevel 4, Wing B, Statesman House,Barakhamba Road,New Delhi - 110 001Tel: +91 11 3044 6406Fax: +91 11 3044 6507

Contact: Arjun S. [email protected]

INDIA

LOCATIONS ALLIANCESRUSSIAAstera10, b.2 Nikolskaya Str.Moscow, 109012Tel/Fax: +7-495-925 00 05

SERBIADanos6, Vladimira Popovica StreetBelgrade 11000Tel: +381-11-2600 603Fax: +381-11-2601 571

UKRAINEAstera2a Konstantinovskaya Street04071, KievTel: +38-044-501 50 10Fax: +38-044-501 50 11

USACresa Partners100 Park Avenue, 24th FloorNew York, NY 10017Tel: +1-212-758 3131Fax: +1-212-980 1977

BAHRAINBahrain Financial HarbourWest Tower16th FloorP.O. Box 5253ManamaTel: +971-505 573 055Fax: +973-17 536 506

BELGIUMBlue TowerAvenue Louise 326B14 Louizalaan1050 BrusselsTel: +32-2-646 49 49Fax: +32-2-646 46 50

DUBAIEmmar SquareBuilding No. 1, 7th FloorP.O. Box 7233Dubai, UAETel: +971-505 573 055Fax: +971-44 257 817

FRANCE13 boulevard du Fort de Vaux75017 ParisTel: +33-1-55 65 20 04Fax: +33-1-55 65 20 00

GERMANYGoetheplatz 460311 Frankfurt am MainTel: +49-69-2 98 99 0Fax: +49-69-29 29 14

IRELAND40 Fitzwilliam PlaceDublin 2Tel: +353-1-66 11 233Fax: +353-1-67 89 981

ITALYCorsa Italia, 15/A20122 MilanTel: +39-02-58 33 141Fax: +39-02-58 33 14 39

JERSEY4th Floor, Conway HouseConway StreetSt HelierJersey Je2 3NTTel: +44-15 34-62 90 01Fax: +44-15 34-62 90 11

ABUDHABIAl Bateen AreaPlot No. 144, W-11New Al Bateen MunicipalityStreet 32P.O. Box 2742Abu Dhabi, UAETel: +971-505 573 055Fax: +971-44 257 817

LUXEMBOURGEBBC, Route de Trèves 6Bloc D2633 SenningerbergTel: +352-34 94 84Fax: +352-34 94 73

ROMANIAUnion International Center11 Ion Campineanu StreetSector 1Bucharest 010031Tel: +40-21-312 7000Fax: +40-21-312 7001

SPAINMaría de Molina, 5428006 MadridTel: +34-91-454 96 00Fax: +34-91-454 97 65

UNITED KINGDOM90 Chancery LaneLondon WC2A 1EUTel: +44-20-7338 4000Fax: +44-20-7430 2628

USA787 Seventh Avenue31st FloorNew York City, NY 10019Tel: +1-917-472 4970Fax: +1-212-471 8100

www.realestate.bnpparibas.com