China's approach to offset and counter-trade in the global ...€¦ · China's approach to offset...

13

China's approach to offset and counter-trade in the global defence markets: Developments, rationale, and implications Guy Anderson, Senior Principal Analyst – A&D (Industry) November 14 - 15 2012 Frankfurt, Germany – ECCO Symposium

Transcript of China's approach to offset and counter-trade in the global ...€¦ · China's approach to offset...

China's approach to offset and counter-trade in the global defence markets:Developments, rationale, and implicationsGuy Anderson, Senior Principal Analyst – A&D (Industry)November 14 - 15 2012Frankfurt, Germany – ECCO Symposium

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

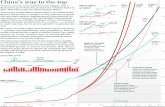

China: Growing world defence market share

2

Source: SIPRIFigures SIPRI TIV values. Based on platform / systems / major subsystem sales

1. Chinese export sales*1

increased 347% from 2000 to 2011a. US sales climbed 30% over periodb. Sales of European leaders*2 climbed 31%c. World export market grew by 58%

2. China’s world market share more than doubled from 1.5% to nearly 5% from 2000 to 2011a. US share fell from 40% to 33%b. Share of European leaders fell from 26% to 21%

*1 Source all figures: SIPRI*2 European leaders: UK, France, Germany, Italy and Sweden

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Chinese export markets: Countries to which China and Chinese-owned organisations supplied military systems and sub-systems between 2000 and 2011

China: Growing global customer-base

3

Sou

rce:

SIP

RI /

UN

/ IH

S J

ane’

s

China exported materiel to 33 countries from 1990 to 1999, and 44 between 2000 to 2011

Overlap between Chinese and Western export markets has grown:eg, Saudi Arabia, Malaysia, Indonesia, Jordan, Kuwait, Argentina, and Oman

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

China: Rationale and the approach to offsetApproach to offset and counter‐trade in context of military exports:

1.

Direct offset:a.

Growing emphasis on direct technology transfer and industrial participation through in‐country

production b.

Co‐development programmes evident (eg, Pakistan JF‐17 / Thailand (guided multiple launch rocket

system)c.

Clear emphasis on “appropriate”

participation and transfer geared to target market capabilities

/

sophistication d.

Current emphasis on aerospace / C4I technologies reflects growing Chinese defence industrial

sophistication2.

Indirect offset: a.

Willingness to invest in the development of commercial and military infrastructure – eg, Pakistan’s Karachi

and Gawadr shipyards and Nigeria’s DICON. Points to long‐term view of markets3.

Counter‐trade:a.

Flexible terms underscore Chinese defence trade –

willingness to accept goods from hydrocarbons (eg,

Myanmar) to dried fruit (eg, Thailand) in exchange for materiel4.

Intangible / unconventional benefits:a.

Trade underpinned by soft‐loans (eg,2009 Ecuador aircraft loan)b.

Alignment with UN Permanent Security Council member attractive – China has backed Nigeria’s claim on

permanent seat to cement tiedc.

Training and joint exercises typically offered to facilitate defence trade

4

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

China: Rationale and the approach to offset

Rationale – the three strands of China’s military export strategy:

1.

China’s goals of industrial and economic transformationa.

Eg, AVIC aims to draw 25% of revenues from exports by 2015 (2009: 7%)

2.

Export of strategic influence (notably in South / South‐East Asia)

3.

Access to raw materials (from oil and gas in Asia, the Middle East and North Africa to

uranium in sub‐Saharan Africa)

5

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

China: Rationale and the approach to offset Issues and observations

1.

Chinese reach is growing – more than 10 agreements reached between 2010 and 2012 to enhance or begin

defence industrial co‐operation.

2.

China does not face the same constraints as Western suppliers:

a.

Unified ownership of military, energy and banking assets allows for agility and profit is not always a

primary motiveb.

Loss of control of IP through ToT less of an issue for China than western competitors. Chinese technologies

are effective rather than world‐class, and therefore neither seepage of IP nor competitor creation are

significant risks

3.

China showing increasing flexibility and sophistication where necessary (eg, South‐East Asian markets), aided by

rapid military industrial advancement and understanding of international markets

1.

Capabilities of Chinese industry meant past industrial participation / ToT accords were of a relatively low level –

that is changing with emphasis on complex weapons, aerospace platforms and C4 solutions increasingly

apparent (eg, in South East Asia)

2.

For materiel buyers, industrial advancement through partnerships

with Western / Russian suppliers is no

longer the only available option

6

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

China: Recent programme examples

7

Offset / trade

facilitation packageMarket example

Local production with transfer

of technology

Nigeria: 2012 accord to procure two Chinese‐designed offshore patrol vessels (China Shipbuilding and

Offshore International 95m design). Local production of ship #2 (50%‐70% share)

Myanmar: 2009 K‐8 deal based on three phases. First called for delivery of 12 aircraft from China; second the

transfer of technologies and tooling; and the third the local production of remaining 48 aircraft

Joint development (with ToT)

Thailand: Joint project to develop guided multiple launch rocket system (announced 2012) based on Chinese

SCAIC WS‐1 302mm MLR

Pakistan: On‐going joint development of JF‐17 fighter aircraft and Chinese‐designed Sword‐class (F‐22P)

frigates

Counter‐tradeThailand: In 2006 China agreed to supply Thailand the WMZ‐551B 6*6 APC in return for 100,000 tonnes of

dried longans. USD30 million programme

Energy / commodities accessMyanmar: 2009 purchase of 60 K‐8 trainers (USD550 million) linked to Chinese access to Myanmar’s energy

fields plus pipeline access

State‐backed loansEcuador: USD52 million advanced in 2009 for unspecific military aircraft purchase

Pakistan: USD2 billion soft loan to facilitate JF‐17 / J‐10 fighter aircraft deliveries to PAK

Direct investment Nigeria: Investment in Nigeria’s state‐controlled DICON plant (linked to land and small arms acquisitions)

Infrastructure development /

investment

Pakistan: F‐22P procurement included Chinese investment in Karachi and Gawadar shipyards

Diplomatic alignmentNigeria: Chinese sale of OPV / aircraft to Nigeria linked to lobbying efforts to secure Nigerian permanent seat

on UN Security Council

Training / exercises Pakistan(industrial and military), Armenia

(military), Nigeria

(industrial and military)

Source: IHS Jane’s

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

China: Government-to-government military co- operation agreements – developments 2010 to 2012

8

Thailand:Apr 2012:

Agreement on

joint

development of

guided MLRS

signed. Based on

Chinese WS‐2

302mm MRL

Indonesia:Jul 2012. MoU on licensed

production of anti‐ship

missile systems

Armenia:Jan 2012. Bilateral defence

technology agreement

(unspecified projects)

Belarus:Oct 2010: Defence industrial

collaboration agreement

signed. Unspecified projects

Brazil:Sept 2010: Outline of military

technical co‐operation

agreement concluded

Nigeria:Mar 2012: Co‐

production of

OPVs

announced

South Africa: Aug 2010:

Defence science and

technology partnership

signed

Ghana:Nov 2012:

Defence

collaboration

agreement

signed Cambodia:

Jun 2011: Offer

to expand

defence

collaboration

appeared to

refer to

military land

systems co‐

operation

Ukraine:Apr 2011: Agreement to

increase flow of Ukrainian

sub‐systems to Chinese

platforms to underpin

materiel trade

Source: IHS Jane

’s

Algeria: 2011: Collaboration with

AVIC discussed

Vietnam:2011: Defence R&D collaboration

accord signed

Saudi Arabia: 2011: Pledge to

extent security

ties. Industrial co‐

operation relating

to energy

Strengthening of

security ties (and

offer of materiel)

aimed at securing

energy access.

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

China: Approach to offset and rationale by region

9

South Asia:Rationale: China has

sought the export of

influence through co‐

operation to contain and

restrain the growing

influence of India

Approach: Soft loans

have eased sales (eg,

Pakistan and Bangladesh)

with extensive defence

industrial and security /

military co‐operation

South East Asia: Rationale: China viewed

exports / ToT agreements as

means of cementing

relations to build influence /

counter US influence.

Energy access a secondary

concern

Approach: Extension of

joint programme

development and ToT

opportunities consistent

with industrialisation

capabilities and ambitions of

client. Training and joint

exercise offers used to build

trust.

South America: Rationale: China views

countries such as Brazil as a

potential ally in the formation

of a counter‐weight to US

influence (alongside Russia); a

valuable export market; and a

significant source of raw

materials and hydrocarbons

Approach: Efforts to enter

market through licensed

production agreements (eg,

Argentina) plus broader

security accords (Colombia,

Brazil)

North America: Rationale: China made tentative efforts to

enter US defence market through partnerships

and acquisitions with aim of improving export

profile

Approach: Partnership approach failed and

significant barriers to trade noted. China has

acquired US companies on fringe of market (eg,

batteries / commercial aerospace), reflecting a

low‐key interpretation of western approach to

US market access

AfricaRationale: Push for access to

raw materials notable.

Approach: Defence trade an

adjunct to a wider economic and

diplomatic strategy. Materiel

provided on advantageous terms

with unconventional payment

terms and appropriate local

involvement offered. Industrial

training offered in addition to

military co‐operation (training and

joint exercises)

Middle EastRationale: Efforts to sell Chinese

materiel to Middle‐East notable (eg,

PLZ‐45 to KSA in 2007). China

motivated by energy access and

aerospace export sales

Approach: Establishment of

security partnerships, offer of training

and joint excercises and civilian

infrastructure partnerships (eg, civil

nuclear energy)

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

China: Export market strengths and weaknesses

+ Strengths:

1.

Sales without political strings

2.

Alignment through trade with a UN Permanent Security Council Member

3.

Military technical co‐operation typically accompanies sales, along with joint military

exercises and

training

4.

Potential for unconventional trade (eg, access to raw materials in exchange for materiel) likely to

prove attractive to resource rich / financially poor emerging buyers

5.

Alignment of state industries, banks and industrial operations put China in a strong position to

provide compelling packages (eg, materiel sales to African countries underpinned by soft loans

from state banks/infrastructure projects in Sri Lanka)

6.

Chinese materiel has historically come with significant cost advantages (eg, ZFB05 APC – at

$300,000 roughly a third of the cost of Western equivalents)

10

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

China: Export market strengths and weaknesses

‐

Weaknesses:

1.

Quality / long‐term support may be open to question

2.

Export advancement hinges on domestic industrial advancement, and challenges remain: China

lacks an innovative SME sector while hierarchical approach to industry may stifle development

3.

Limited advanced capabilities may limit appeal

4.

Remaining concern that exports from China could jeopardise strategic relations with (and aid

from) the United States

11

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

China's approach to offset and counter-trade in the global defence markets: Implications for competitors

Final thoughts

1.Broadening customer base:

Relatively sophisticated customers with no historic alignment with China beginning to

look east (eg, Saudi Arabia). Competition between East and West will become the norm in many markets

2.Profit not China’s primary motive:

The sale of materiel is not always an end in itself, suggesting that the potential

for loss‐leading benefits packages should not be discounted

3.Alignment: State‐ownership of energy interests, banks and defence companies puts China in a strong position to put

together compelling benefits packages

4.Continued growth? The generosity of Chinese offset packages hinge in part on continued demand for raw materials to

fuel growth on‐going liquidity of Chinese banks to finance packages on easy terms. Much depends on the outlook for the

wider Chinese economy.

5.Growing sophistication has limits:a.

China’s defence industries continue to advance, but sophistication still limited in areas such as aerospace and

C4I technologies

b.

There is currently a ceiling on China’s capacity to meet more sophisticated ToT / industrialisation aspirations of

client countries

12

China's approach to offset and counter-trade in the global defence markets:Developments, rationale, and implications

Thank you for your attentionGuy AndersonSenior Principal Analyst – A&DEmail: [email protected]: 0044 (0) 20 32532190Cell: 0044 (0) 7725823632

Thanks to:

David ReethsDirector Aerospace and Defence

Consulting (EMEA)[email protected]

Jon GrevattChief Asia‐Pacific AnalystIHS Jane’sEmail:[email protected]

Mattthew