Chapter One Partnerships

12

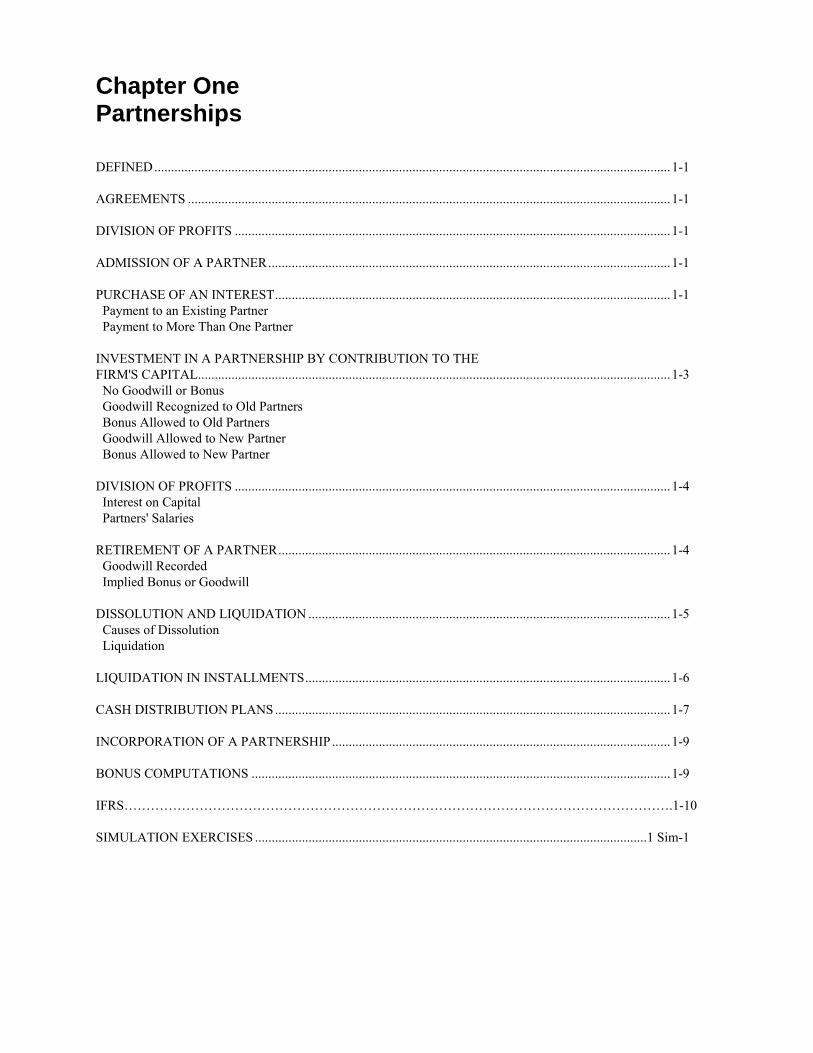

Chapter One Partnerships DEFINED .......................................................................................................................................................... 1-1 AGREEMENTS ................................................................................................................................................ 1-1 DIVISION OF PROFITS .................................................................................................................................. 1-1 ADMISSION OF A PARTNER ........................................................................................................................ 1-1 PURCHASE OF AN INTEREST...................................................................................................................... 1-1 Payment to an Existing Partner Payment to More Than One Partner INVESTMENT IN A PARTNERSHIP BY CONTRIBUTION TO THE FIRM'S CAPITAL............................................................................................................................................. 1-3 No Goodwill or Bonus Goodwill Recognized to Old Partners Bonus Allowed to Old Partners Goodwill Allowed to New Partner Bonus Allowed to New Partner DIVISION OF PROFITS .................................................................................................................................. 1-4 Interest on Capital Partners' Salaries RETIREMENT OF A PARTNER ..................................................................................................................... 1-4 Goodwill Recorded Implied Bonus or Goodwill DISSOLUTION AND LIQUIDATION ............................................................................................................ 1-5 Causes of Dissolution Liquidation LIQUIDATION IN INSTALLMENTS ............................................................................................................. 1-6 CASH DISTRIBUTION PLANS ...................................................................................................................... 1-7 INCORPORATION OF A PARTNERSHIP ..................................................................................................... 1-9 BONUS COMPUTATIONS ............................................................................................................................. 1-9 IFRS…………………………………………………………………………………………………………….1-10 SIMULATION EXERCISES .....................................................................................................................1 Sim-1

Transcript of Chapter One Partnerships

Chapter One Partnerships

DEFINED..........................................................................................................................................................1-1 AGREEMENTS ................................................................................................................................................1-1 DIVISION OF PROFITS ..................................................................................................................................1-1 ADMISSION OF A PARTNER........................................................................................................................1-1 PURCHASE OF AN INTEREST......................................................................................................................1-1 Payment to an Existing Partner Payment to More Than One Partner INVESTMENT IN A PARTNERSHIP BY CONTRIBUTION TO THE FIRM'S CAPITAL.............................................................................................................................................1-3 No Goodwill or Bonus Goodwill Recognized to Old Partners Bonus Allowed to Old Partners Goodwill Allowed to New Partner Bonus Allowed to New Partner DIVISION OF PROFITS ..................................................................................................................................1-4 Interest on Capital Partners' Salaries RETIREMENT OF A PARTNER.....................................................................................................................1-4 Goodwill Recorded Implied Bonus or Goodwill DISSOLUTION AND LIQUIDATION ............................................................................................................1-5 Causes of Dissolution Liquidation LIQUIDATION IN INSTALLMENTS.............................................................................................................1-6 CASH DISTRIBUTION PLANS ......................................................................................................................1-7 INCORPORATION OF A PARTNERSHIP.....................................................................................................1-9 BONUS COMPUTATIONS .............................................................................................................................1-9 IFRS…………………………………………………………………………………………………………….1-10 SIMULATION EXERCISES .....................................................................................................................1 Sim-1

Chapter One Partnerships

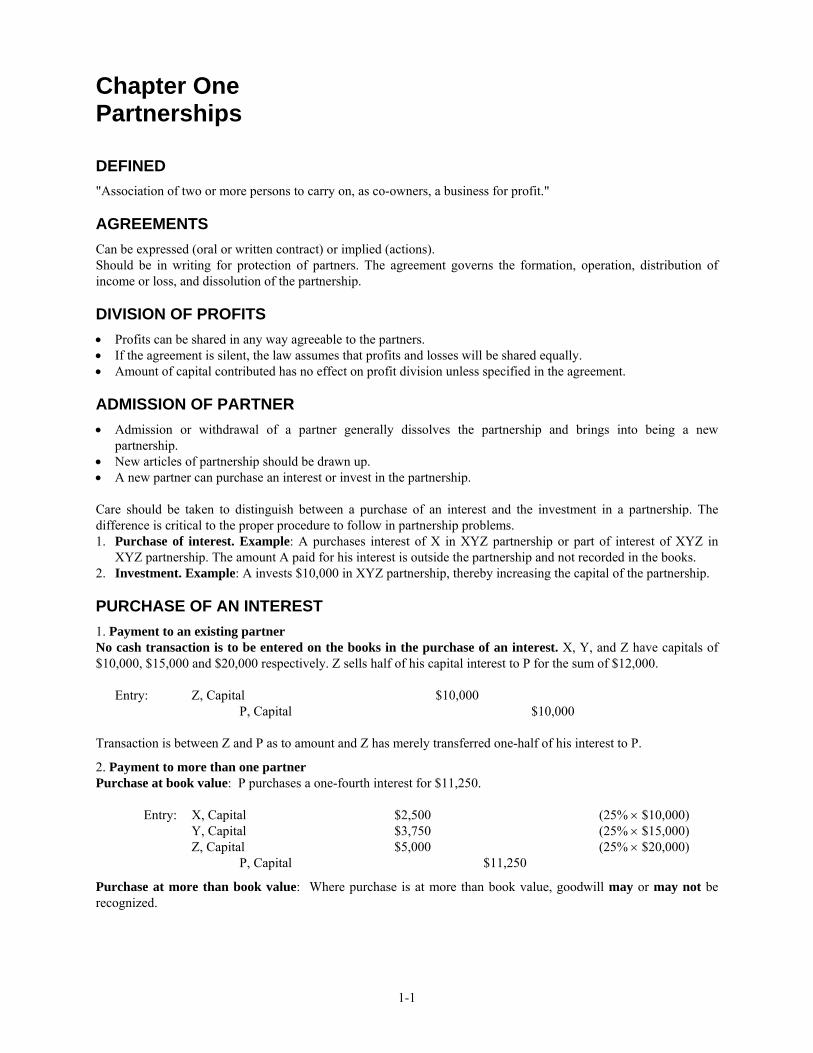

DEFINED

"Association of two or more persons to carry on, as co-owners, a business for profit." AGREEMENTS Can be expressed (oral or written contract) or implied (actions). Should be in writing for protection of partners. The agreement governs the formation, operation, distribution of ncome or loss, and dissolution of the partnership. i

DIVISION OF PROFITS • Profits can be shared in any way agreeable to the partners. • If the agreement is silent, the law assumes that profits and losses will be shared equally. • Amount of capital contributed has no effect on profit division unless specified in the agreement. ADMISSION OF PARTNER • Admission or withdrawal of a partner generally dissolves the partnership and brings into being a new

partnership. • New articles of partnership should be drawn up. • A new partner can purchase an interest or invest in the partnership. Care should be taken to distinguish between a purchase of an interest and the investment in a partnership. The difference is critical to the proper procedure to follow in partnership problems. 1. Purchase of interest. Example: A purchases interest of X in XYZ partnership or part of interest of XYZ in

XYZ partnership. The amount A paid for his interest is outside the partnership and not recorded in the books. 2. Investment. Example: A invests $10,000 in XYZ partnership, thereby increasing the capital of the partnership. PURCHASE OF AN INTEREST 1. Payment to an existing partner No cash transaction is to be entered on the books in the purchase of an interest. X, Y, and Z have capitals of $10,000, $15,000 and $20,000 respectively. Z sells half of his capital interest to P for the sum of $12,000. Entry: Z, Capital $10,000 P, Capital $10,000 Transaction is between Z and P as to amount and Z has merely transferred one-half of his interest to P. 2. Payment to more than one partner Purchase at book value: P purchases a one-fourth interest for $11,250. Entry: X, Capital $2,500 (25% × $10,000) Y, Capital $3,750 (25% × $15,000) Z, Capital $5,000 (25% × $20,000) P, Capital $11,250 Purchase at more than book value: Where purchase is at more than book value, goodwill may or may not be recognized.

1-1

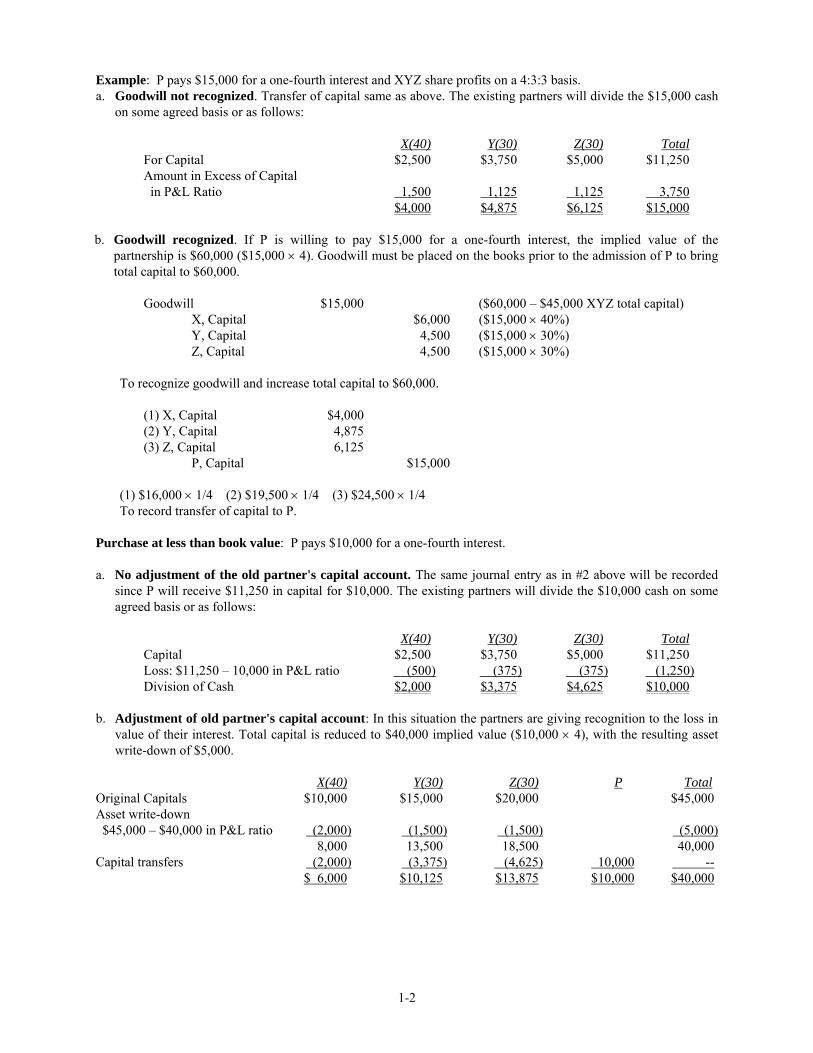

Example: P pays $15,000 for a one-fourth interest and XYZ share profits on a 4:3:3 basis. a. Goodwill not recognized. Transfer of capital same as above. The existing partners will divide the $15,000 cash

on some agreed basis or as follows: X(40) Y(30) Z(30) Total For Capital $2,500 $3,750 $5,000 $11,250 Amount in Excess of Capital in P&L Ratio 1,500 1,125 1,125 3,750 $4,000 $4,875 $6,125 $15,000 b. Goodwill recognized. If P is willing to pay $15,000 for a one-fourth interest, the implied value of the

partnership is $60,000 ($15,000 × 4). Goodwill must be placed on the books prior to the admission of P to bring total capital to $60,000.

Goodwill $15,000 ($60,000 – $45,000 XYZ total capital) X, Capital $6,000 ($15,000 × 40%) Y, Capital 4,500 ($15,000 × 30%) Z, Capital 4,500 ($15,000 × 30%) To recognize goodwill and increase total capital to $60,000. (1) X, Capital $4,000 (2) Y, Capital 4,875 (3) Z, Capital 6,125 P, Capital $15,000

(1) $16,000 × 1/4 (2) $19,500 × 1/4 (3) $24,500 × 1/4 To record transfer of capital to P. Purchase at less than book value: P pays $10,000 for a one-fourth interest. a. No adjustment of the old partner's capital account. The same journal entry as in #2 above will be recorded

since P will receive $11,250 in capital for $10,000. The existing partners will divide the $10,000 cash on some agreed basis or as follows:

X(40) Y(30) Z(30) Total Capital $2,500 $3,750 $5,000 $11,250 Loss: $11,250 – 10,000 in P&L ratio (500) (375) (375) (1,250) Division of Cash $2,000 $3,375 $4,625 $10,000 b. Adjustment of old partner's capital account: In this situation the partners are giving recognition to the loss in

value of their interest. Total capital is reduced to $40,000 implied value ($10,000 × 4), with the resulting asset write-down of $5,000.

X(40) Y(30) Z(30) P TotalOriginal Capitals $10,000 $15,000 $20,000 $45,000 Asset write-down $45,000 – $40,000 in P&L ratio (2,000) (1,500) (1,500) (5,000) 8,000 13,500 18,500 40,000 Capital transfers (2,000) (3,375) (4,625) 10,000 -- $ 6,000 $10,125 $13,875 $10,000 $40,000

1-2

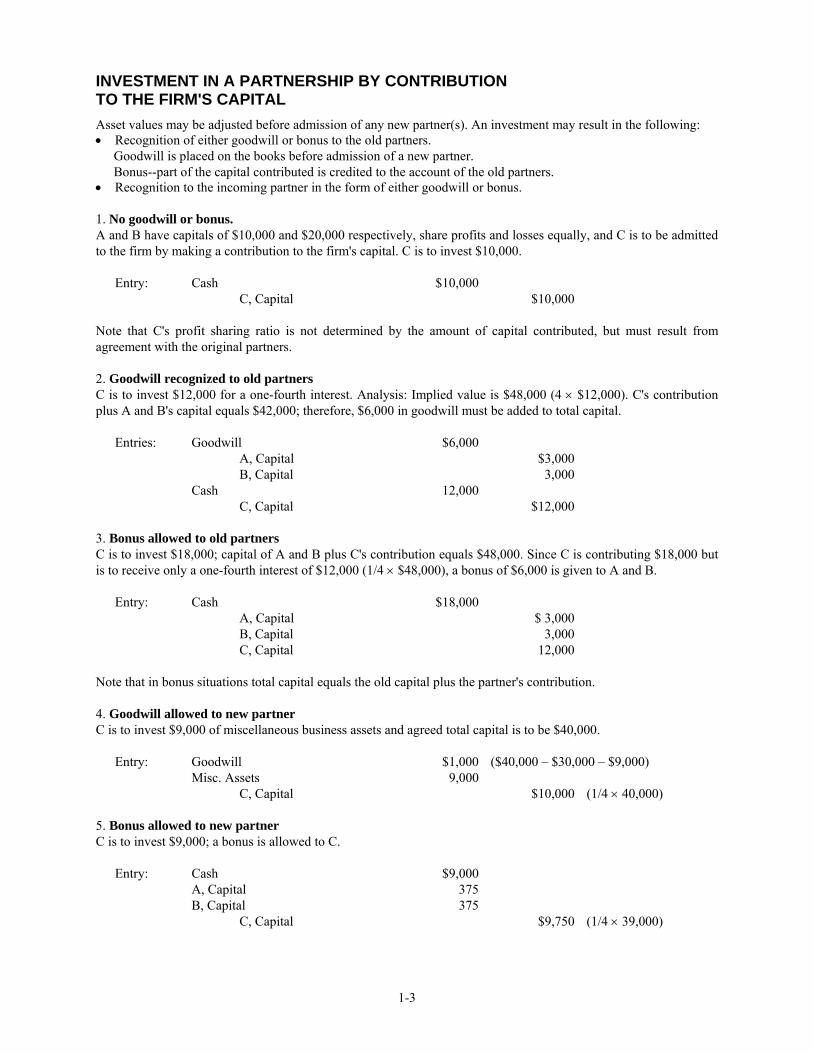

INVESTMENT IN A PARTNERSHIP BY CONTRIBUTION TO THE FIRM'S CAPITAL Asset values may be adjusted before admission of any new partner(s). An investment may result in the following: • Recognition of either goodwill or bonus to the old partners.

Goodwill is placed on the books before admission of a new partner. Bonus--part of the capital contributed is credited to the account of the old partners.

• Recognition to the incoming partner in the form of either goodwill or bonus. 1. No goodwill or bonus. A and B have capitals of $10,000 and $20,000 respectively, share profits and losses equally, and C is to be admitted to the firm by making a contribution to the firm's capital. C is to invest $10,000.

Entry: Cash $10,000 C, Capital $10,000 Note that C's profit sharing ratio is not determined by the amount of capital contributed, but must result from agreement with the original partners. 2. Goodwill recognized to old partners C is to invest $12,000 for a one-fourth interest. Analysis: Implied value is $48,000 (4 × $12,000). C's contribution plus A and B's capital equals $42,000; therefore, $6,000 in goodwill must be added to total capital.

Entries: Goodwill $6,000 A, Capital $3,000 B, Capital 3,000 Cash 12,000 C, Capital $12,000 3. Bonus allowed to old partners C is to invest $18,000; capital of A and B plus C's contribution equals $48,000. Since C is contributing $18,000 but is to receive only a one-fourth interest of $12,000 (1/4 × $48,000), a bonus of $6,000 is given to A and B. Entry: Cash $18,000 A, Capital $ 3,000 B, Capital 3,000 C, Capital 12,000 Note that in bonus situations total capital equals the old capital plus the partner's contribution. 4. Goodwill allowed to new partner C is to invest $9,000 of miscellaneous business assets and agreed total capital is to be $40,000.

Entry: Goodwill $1,000 ($40,000 – $30,000 – $9,000) Misc. Assets 9,000 C, Capital $10,000 (1/4 × 40,000) 5. Bonus allowed to new partner C is to invest $9,000; a bonus is allowed to C.

Entry: Cash $9,000 A, Capital 375 B, Capital 375 C, Capital $9,750 (1/4 × 39,000)

1-3

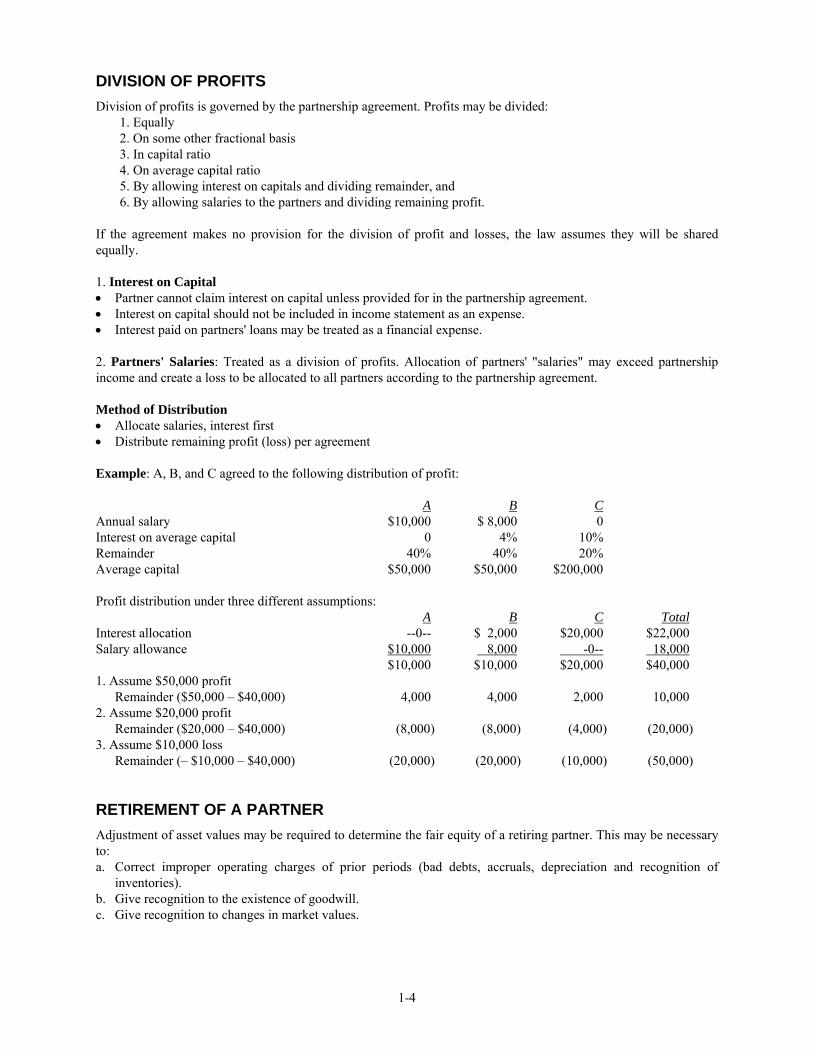

DIVISION OF PROFITS Division of profits is governed by the partnership agreement. Profits may be divided:

1. Equally 2. On some other fractional basis 3. In capital ratio 4. On average capital ratio 5. By allowing interest on capitals and dividing remainder, and 6. By allowing salaries to the partners and dividing remaining profit.

If the agreement makes no provision for the division of profit and losses, the law assumes they will be shared equally. 1. Interest on Capital • Partner cannot claim interest on capital unless provided for in the partnership agreement. • Interest on capital should not be included in income statement as an expense. • Interest paid on partners' loans may be treated as a financial expense. 2. Partners' Salaries: Treated as a division of profits. Allocation of partners' "salaries" may exceed partnership income and create a loss to be allocated to all partners according to the partnership agreement. Method of Distribution • Allocate salaries, interest first • Distribute remaining profit (loss) per agreement Example: A, B, and C agreed to the following distribution of profit: A B C Annual salary $10,000 $ 8,000 0 Interest on average capital 0 4% 10% Remainder 40% 40% 20% Average capital $50,000 $50,000 $200,000 Profit distribution under three different assumptions: A B C Total Interest allocation --0-- $ 2,000 $20,000 $22,000 Salary allowance $10,000 8,000 -0-- 18,000 $10,000 $10,000 $20,000 $40,000 1. Assume $50,000 profit Remainder ($50,000 – $40,000) 4,000 4,000 2,000 10,000 2. Assume $20,000 profit Remainder ($20,000 – $40,000) (8,000) (8,000) (4,000) (20,000) 3. Assume $10,000 loss Remainder (– $10,000 – $40,000) (20,000) (20,000) (10,000) (50,000) RETIREMENT OF A PARTNER Adjustment of asset values may be required to determine the fair equity of a retiring partner. This may be necessary to: a. Correct improper operating charges of prior periods (bad debts, accruals, depreciation and recognition of

inventories). b. Give recognition to the existence of goodwill. c. Give recognition to changes in market values.

1-4

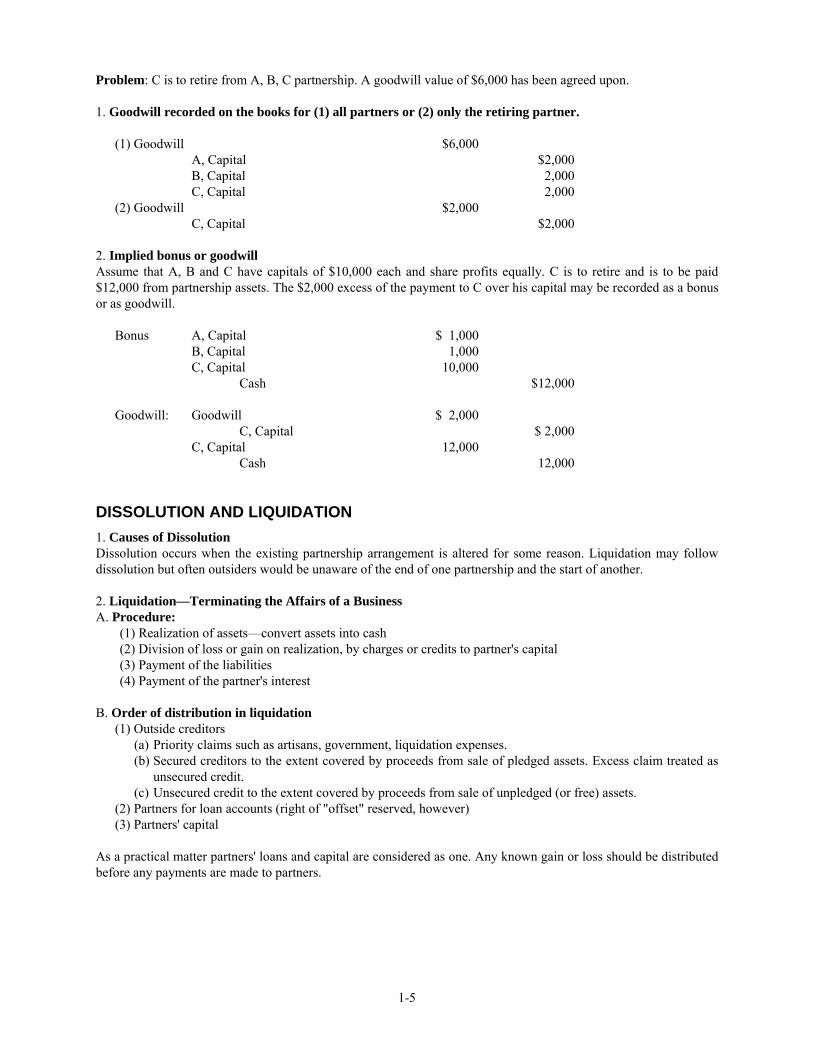

Problem: C is to retire from A, B, C partnership. A goodwill value of $6,000 has been agreed upon. 1. Goodwill recorded on the books for (1) all partners or (2) only the retiring partner.

(1) Goodwill $6,000 A, Capital $2,000 B, Capital 2,000 C, Capital 2,000 (2) Goodwill $2,000 C, Capital $2,000 2. Implied bonus or goodwill Assume that A, B and C have capitals of $10,000 each and share profits equally. C is to retire and is to be paid $12,000 from partnership assets. The $2,000 excess of the payment to C over his capital may be recorded as a bonus or as goodwill. Bonus A, Capital $ 1,000 B, Capital 1,000 C, Capital 10,000 Cash $12,000 Goodwill: Goodwill $ 2,000 C, Capital $ 2,000 C, Capital 12,000 Cash 12,000 DISSOLUTION AND LIQUIDATION 1. Causes of Dissolution Dissolution occurs when the existing partnership arrangement is altered for some reason. Liquidation may follow dissolution but often outsiders would be unaware of the end of one partnership and the start of another. 2. Liquidation—Terminating the Affairs of a Business A. Procedure:

(1) Realization of assets—convert assets into cash (2) Division of loss or gain on realization, by charges or credits to partner's capital (3) Payment of the liabilities (4) Payment of the partner's interest

B. Order of distribution in liquidation

(1) Outside creditors (a) Priority claims such as artisans, government, liquidation expenses. (b) Secured creditors to the extent covered by proceeds from sale of pledged assets. Excess claim treated as

unsecured credit. (c) Unsecured credit to the extent covered by proceeds from sale of unpledged (or free) assets.

(2) Partners for loan accounts (right of "offset" reserved, however) (3) Partners' capital

As a practical matter partners' loans and capital are considered as one. Any known gain or loss should be distributed before any payments are made to partners.

1-5

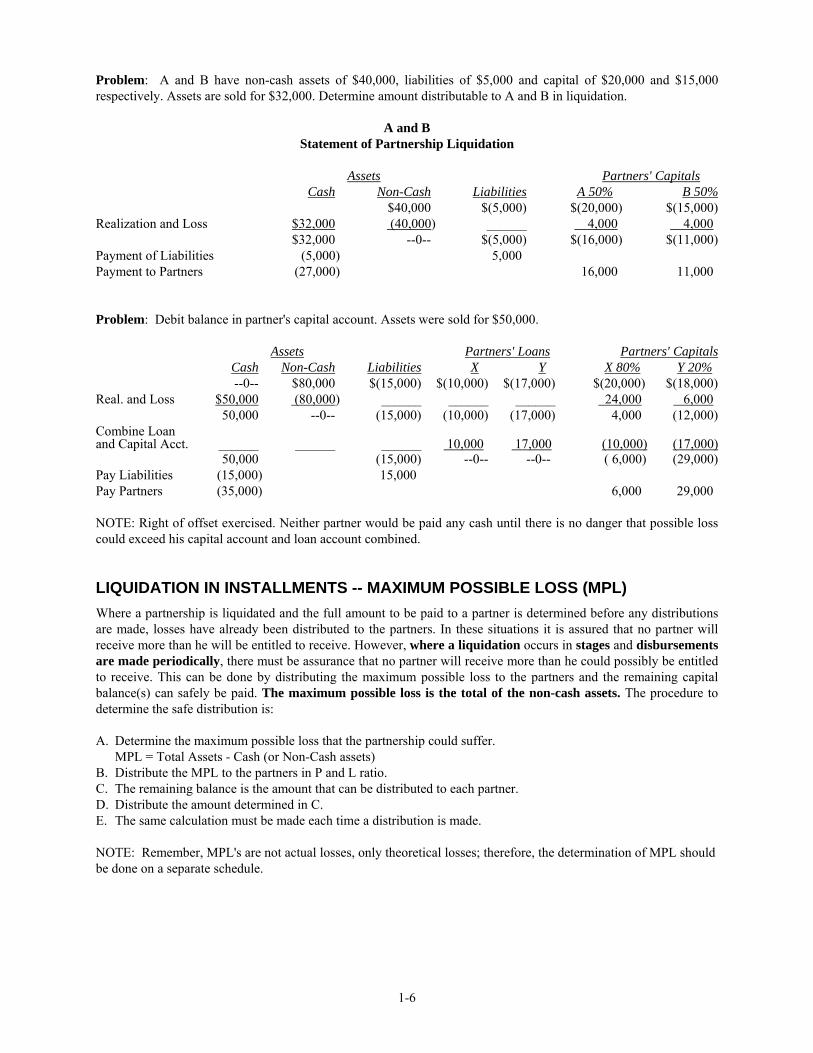

Problem: A and B have non-cash assets of $40,000, liabilities of $5,000 and capital of $20,000 and $15,000 respectively. Assets are sold for $32,000. Determine amount distributable to A and B in liquidation.

A and B

Statement of Partnership Liquidation

Assets Partners' Capitals Cash Non-Cash Liabilities A 50% B 50% $40,000 $(5,000) $(20,000) $(15,000) Realization and Loss $32,000 (40,000) ______ 4,000 4,000 $32,000 --0-- $(5,000) $(16,000) $(11,000) Payment of Liabilities (5,000) 5,000 Payment to Partners (27,000) 16,000 11,000 Problem: Debit balance in partner's capital account. Assets were sold for $50,000. Assets Partners' Loans Partners' Capitals Cash Non-Cash Liabilities X Y X 80% Y 20% --0-- $80,000 $(15,000) $(10,000) $(17,000) $(20,000) $(18,000) Real. and Loss $50,000 (80,000) ______ ______ ______ 24,000 6,000 50,000 --0-- (15,000) (10,000) (17,000) 4,000 (12,000) Combine Loan and Capital Acct. ______ ______ ______ 10,000 17,000 (10,000) (17,000) 50,000 (15,000) --0-- --0-- ( 6,000) (29,000) Pay Liabilities (15,000) 15,000 Pay Partners (35,000) 6,000 29,000 NOTE: Right of offset exercised. Neither partner would be paid any cash until there is no danger that possible loss could exceed his capital account and loan account combined. LIQUIDATION IN INSTALLMENTS -- MAXIMUM POSSIBLE LOSS (MPL) Where a partnership is liquidated and the full amount to be paid to a partner is determined before any distributions are made, losses have already been distributed to the partners. In these situations it is assured that no partner will receive more than he will be entitled to receive. However, where a liquidation occurs in stages and disbursements are made periodically, there must be assurance that no partner will receive more than he could possibly be entitled to receive. This can be done by distributing the maximum possible loss to the partners and the remaining capital balance(s) can safely be paid. The maximum possible loss is the total of the non-cash assets. The procedure to determine the safe distribution is: A. Determine the maximum possible loss that the partnership could suffer.

MPL = Total Assets - Cash (or Non-Cash assets) B. Distribute the MPL to the partners in P and L ratio. C. The remaining balance is the amount that can be distributed to each partner. D. Distribute the amount determined in C. E. The same calculation must be made each time a distribution is made. NOTE: Remember, MPL's are not actual losses, only theoretical losses; therefore, the determination of MPL should be done on a separate schedule.

1-6

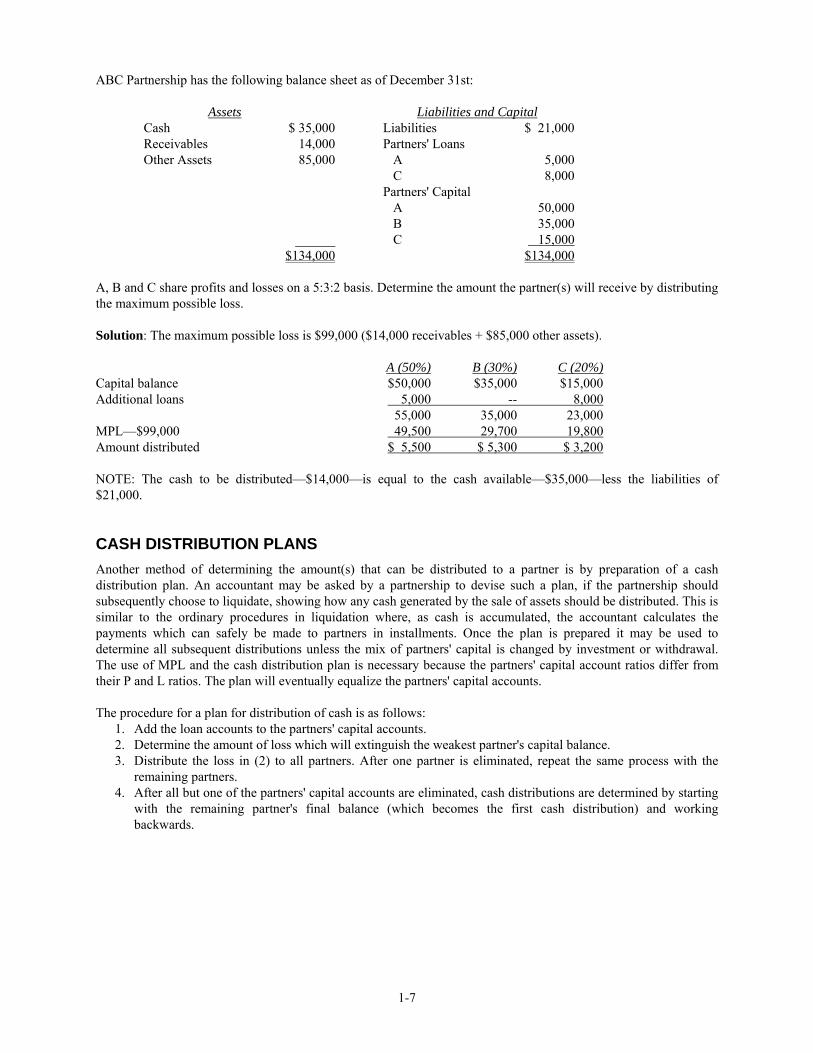

ABC Partnership has the following balance sheet as of December 31st: Assets Liabilities and Capital Cash $ 35,000 Liabilities $ 21,000 Receivables 14,000 Partners' Loans Other Assets 85,000 A 5,000 C 8,000 Partners' Capital A 50,000 B 35,000 ______ C 15,000 $134,000 $134,000 A, B and C share profits and losses on a 5:3:2 basis. Determine the amount the partner(s) will receive by distributing the maximum possible loss. Solution: The maximum possible loss is $99,000 ($14,000 receivables + $85,000 other assets). A (50%) B (30%) C (20%) Capital balance $50,000 $35,000 $15,000 Additional loans 5,000 -- 8,000 55,000 35,000 23,000 MPL—$99,000 49,500 29,700 19,800 Amount distributed $ 5,500 $ 5,300 $ 3,200 NOTE: The cash to be distributed—$14,000—is equal to the cash available—$35,000—less the liabilities of $21,000. CASH DISTRIBUTION PLANS Another method of determining the amount(s) that can be distributed to a partner is by preparation of a cash distribution plan. An accountant may be asked by a partnership to devise such a plan, if the partnership should subsequently choose to liquidate, showing how any cash generated by the sale of assets should be distributed. This is similar to the ordinary procedures in liquidation where, as cash is accumulated, the accountant calculates the payments which can safely be made to partners in installments. Once the plan is prepared it may be used to determine all subsequent distributions unless the mix of partners' capital is changed by investment or withdrawal. The use of MPL and the cash distribution plan is necessary because the partners' capital account ratios differ from their P and L ratios. The plan will eventually equalize the partners' capital accounts. The procedure for a plan for distribution of cash is as follows:

1. Add the loan accounts to the partners' capital accounts. 2. Determine the amount of loss which will extinguish the weakest partner's capital balance. 3. Distribute the loss in (2) to all partners. After one partner is eliminated, repeat the same process with the

remaining partners. 4. After all but one of the partners' capital accounts are eliminated, cash distributions are determined by starting

with the remaining partner's final balance (which becomes the first cash distribution) and working backwards.

1-7

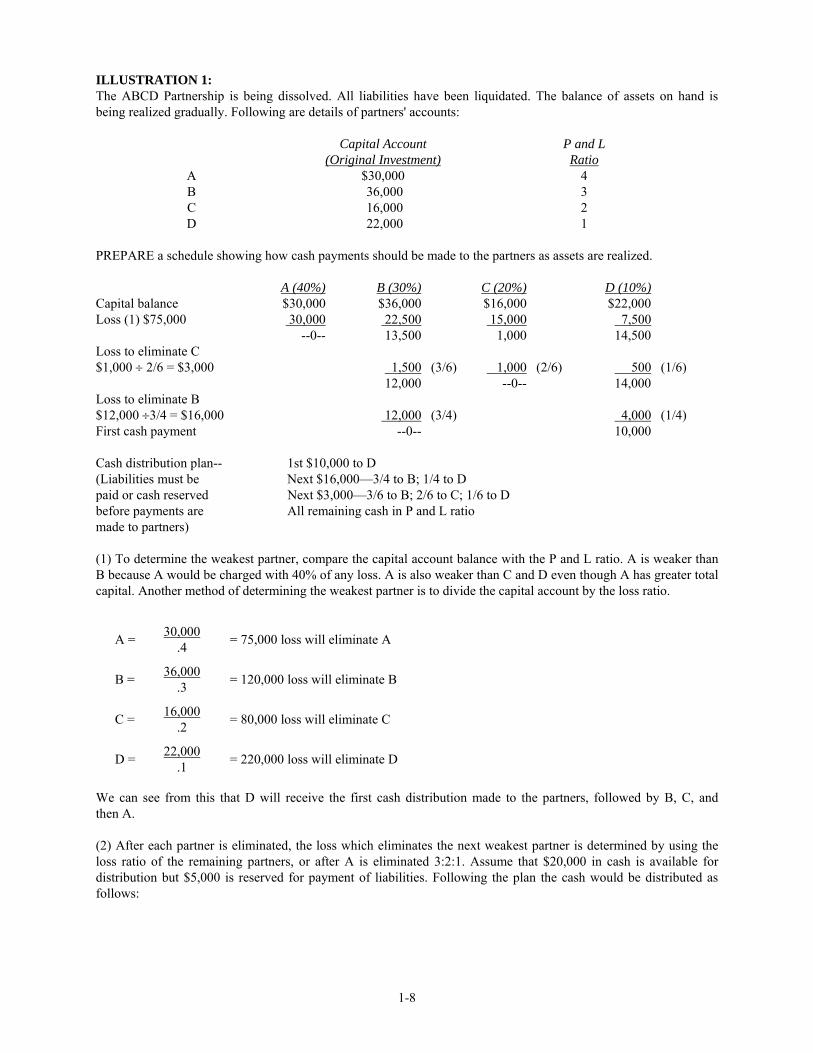

ILLUSTRATION 1: The ABCD Partnership is being dissolved. All liabilities have been liquidated. The balance of assets on hand is being realized gradually. Following are details of partners' accounts: Capital Account P and L (Original Investment) Ratio A $30,000 4 B 36,000 3 C 16,000 2 D 22,000 1 PREPARE a schedule showing how cash payments should be made to the partners as assets are realized. A (40%) B (30%) C (20%) D (10%)Capital balance $30,000 $36,000 $16,000 $22,000 Loss (1) $75,000 30,000 22,500 15,000 7,500 --0-- 13,500 1,000 14,500 Loss to eliminate C $1,000 ÷ 2/6 = $3,000 1,500 (3/6) 1,000 (2/6) 500 (1/6) 12,000 --0-- 14,000 Loss to eliminate B $12,000 ÷3/4 = $16,000 12,000 (3/4) 4,000 (1/4) First cash payment --0-- 10,000 Cash distribution plan-- 1st $10,000 to D (Liabilities must be Next $16,000—3/4 to B; 1/4 to D paid or cash reserved Next $3,000—3/6 to B; 2/6 to C; 1/6 to D before payments are All remaining cash in P and L ratio made to partners) (1) To determine the weakest partner, compare the capital account balance with the P and L ratio. A is weaker than B because A would be charged with 40% of any loss. A is also weaker than C and D even though A has greater total apital. Another method of determining the weakest partner is to divide the capital account by the loss ratio. c

30,000 A = .4 = 75,000 loss will eliminate A 36,000 B = .3 = 120,000 loss will eliminate B 16,000 C = .2 = 80,000 loss will eliminate C 22,000 D = .1 = 220,000 loss will eliminate D

We can see from this that D will receive the first cash distribution made to the partners, followed by B, C, and then A. (2) After each partner is eliminated, the loss which eliminates the next weakest partner is determined by using the loss ratio of the remaining partners, or after A is eliminated 3:2:1. Assume that $20,000 in cash is available for distribution but $5,000 is reserved for payment of liabilities. Following the plan the cash would be distributed as follows:

1-8

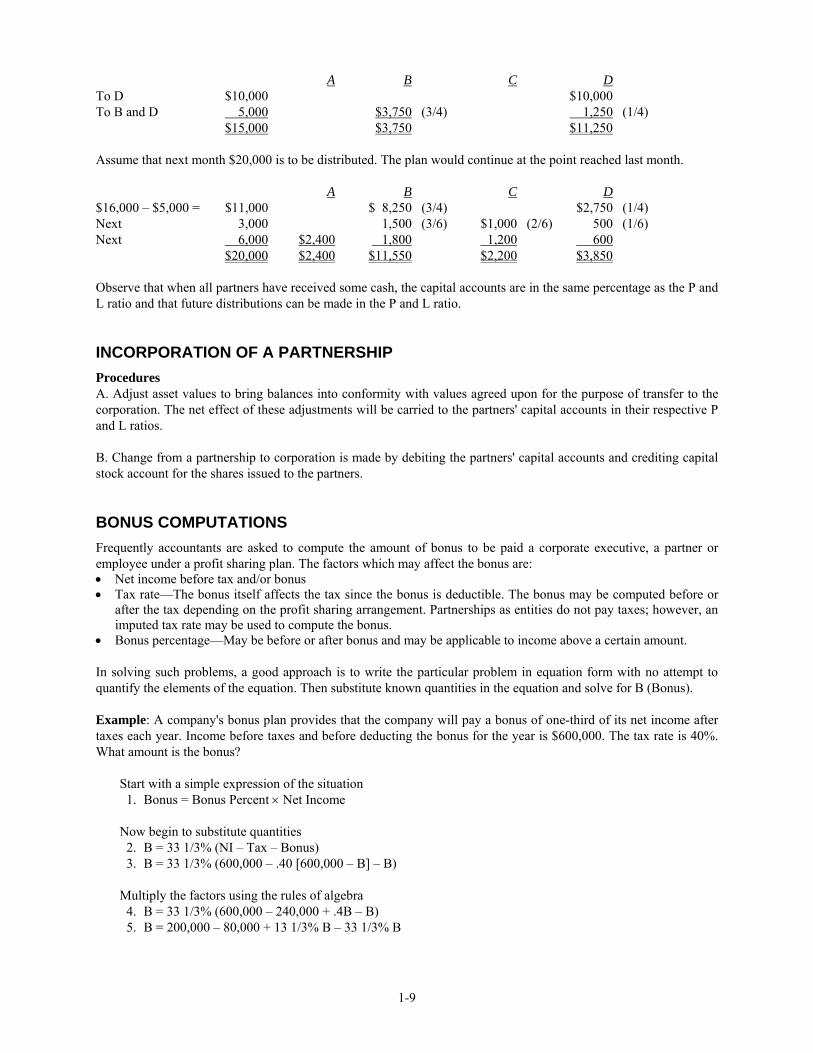

A B C DTo D $10,000 $10,000 To B and D 5,000 $3,750 (3/4) 1,250 (1/4) $15,000 $3,750 $11,250 Assume that next month $20,000 is to be distributed. The plan would continue at the point reached last month. A B C D$16,000 – $5,000 = $11,000 $ 8,250 (3/4) $2,750 (1/4) Next 3,000 1,500 (3/6) $1,000 (2/6) 500 (1/6) Next 6,000 $2,400 1,800 1,200 600 $20,000 $2,400 $11,550 $2,200 $3,850 Observe that when all partners have received some cash, the capital accounts are in the same percentage as the P and L ratio and that future distributions can be made in the P and L ratio. INCORPORATION OF A PARTNERSHIP Procedures A. Adjust asset values to bring balances into conformity with values agreed upon for the purpose of transfer to the corporation. The net effect of these adjustments will be carried to the partners' capital accounts in their respective P and L ratios. B. Change from a partnership to corporation is made by debiting the partners' capital accounts and crediting capital stock account for the shares issued to the partners. BONUS COMPUTATIONS Frequently accountants are asked to compute the amount of bonus to be paid a corporate executive, a partner or employee under a profit sharing plan. The factors which may affect the bonus are: • Net income before tax and/or bonus • Tax rate—The bonus itself affects the tax since the bonus is deductible. The bonus may be computed before or

after the tax depending on the profit sharing arrangement. Partnerships as entities do not pay taxes; however, an imputed tax rate may be used to compute the bonus.

• Bonus percentage—May be before or after bonus and may be applicable to income above a certain amount. In solving such problems, a good approach is to write the particular problem in equation form with no attempt to quantify the elements of the equation. Then substitute known quantities in the equation and solve for B (Bonus). Example: A company's bonus plan provides that the company will pay a bonus of one-third of its net income after taxes each year. Income before taxes and before deducting the bonus for the year is $600,000. The tax rate is 40%. What amount is the bonus?

Start with a simple expression of the situation 1. Bonus = Bonus Percent × Net Income Now begin to substitute quantities 2. B = 33 1/3% (NI – Tax – Bonus) 3. B = 33 1/3% (600,000 – .40 [600,000 – B] – B) Multiply the factors using the rules of algebra 4. B = 33 1/3% (600,000 – 240,000 + .4B – B) 5. B = 200,000 – 80,000 + 13 1/3% B – 33 1/3% B

1-9

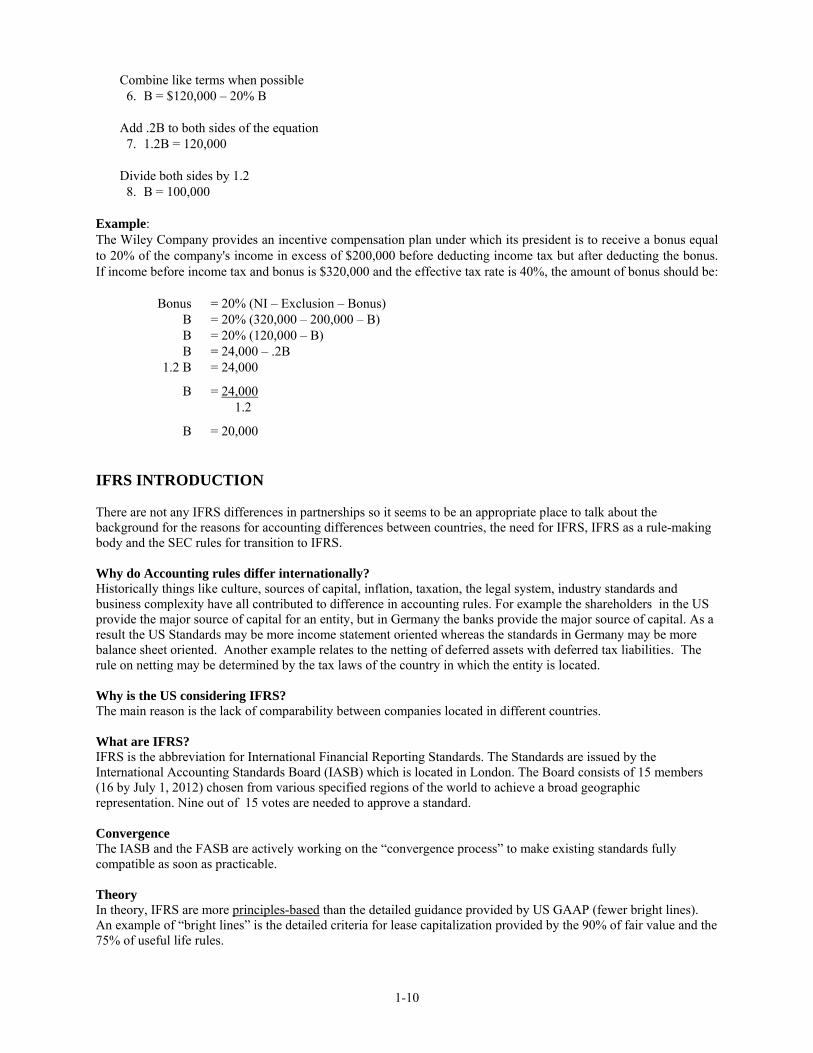

Combine like terms when possible 6. B = $120,000 – 20% B Add .2B to both sides of the equation 7. 1.2B = 120,000 Divide both sides by 1.2 8. B = 100,000

Example: The Wiley Company provides an incentive compensation plan under which its president is to receive a bonus equal to 20% of the company's income in excess of $200,000 before deducting income tax but after deducting the bonus. If income before income tax and bonus is $320,000 and the effective tax rate is 40%, the amount of bonus should be: Bonus = 20% (NI – Exclusion – Bonus) B = 20% (320,000 – 200,000 – B) B = 20% (120,000 – B) B = 24,000 – .2B

1.2 B = 24,000

B = 24,000

1.2

B = 20,000 IFRS INTRODUCTION There are not any IFRS differences in partnerships so it seems to be an appropriate place to talk about the background for the reasons for accounting differences between countries, the need for IFRS, IFRS as a rule-making body and the SEC rules for transition to IFRS. Why do Accounting rules differ internationally? Historically things like culture, sources of capital, inflation, taxation, the legal system, industry standards and business complexity have all contributed to difference in accounting rules. For example the shareholders in the US provide the major source of capital for an entity, but in Germany the banks provide the major source of capital. As a result the US Standards may be more income statement oriented whereas the standards in Germany may be more balance sheet oriented. Another example relates to the netting of deferred assets with deferred tax liabilities. The rule on netting may be determined by the tax laws of the country in which the entity is located. Why is the US considering IFRS? The main reason is the lack of comparability between companies located in different countries. What are IFRS? IFRS is the abbreviation for International Financial Reporting Standards. The Standards are issued by the International Accounting Standards Board (IASB) which is located in London. The Board consists of 15 members (16 by July 1, 2012) chosen from various specified regions of the world to achieve a broad geographic representation. Nine out of 15 votes are needed to approve a standard. Convergence The IASB and the FASB are actively working on the “convergence process” to make existing standards fully compatible as soon as practicable. Theory In theory, IFRS are more principles-based than the detailed guidance provided by US GAAP (fewer bright lines). An example of “bright lines” is the detailed criteria for lease capitalization provided by the 90% of fair value and the 75% of useful life rules.

1-10

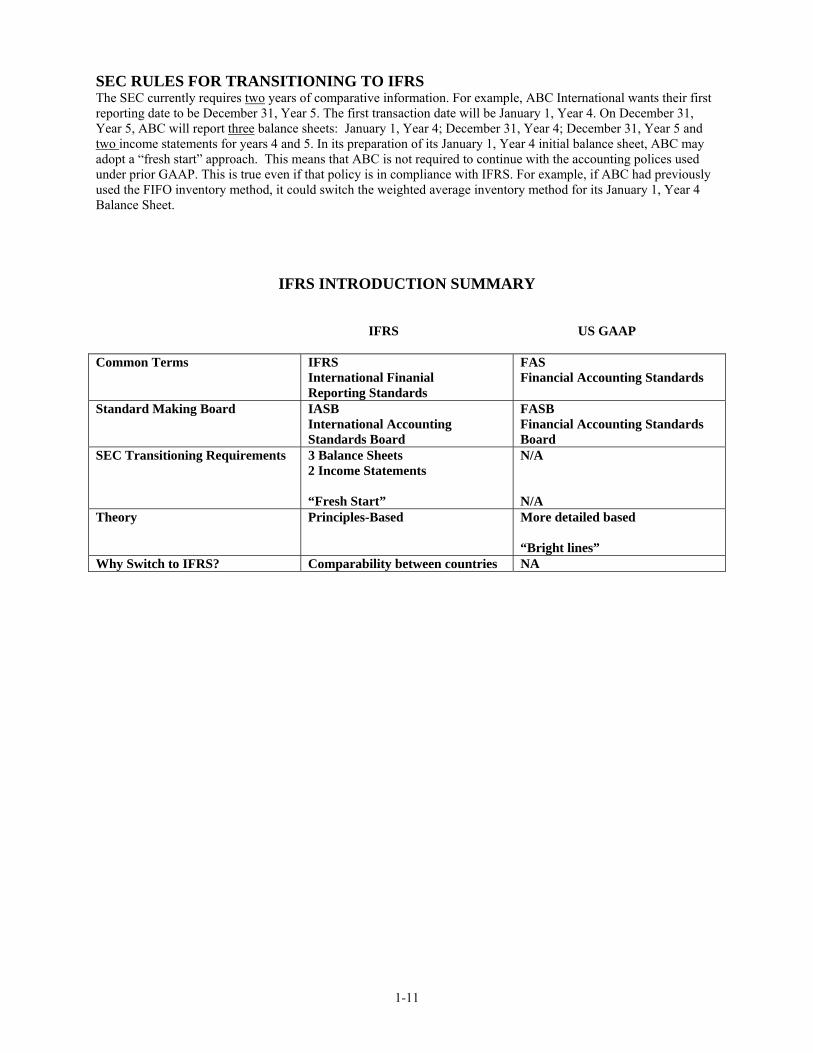

SEC RULES FOR TRANSITIONING TO IFRS The SEC currently requires two years of comparative information. For example, ABC International wants their first reporting date to be December 31, Year 5. The first transaction date will be January 1, Year 4. On December 31, Year 5, ABC will report three balance sheets: January 1, Year 4; December 31, Year 4; December 31, Year 5 and two income statements for years 4 and 5. In its preparation of its January 1, Year 4 initial balance sheet, ABC may adopt a “fresh start” approach. This means that ABC is not required to continue with the accounting polices used under prior GAAP. This is true even if that policy is in compliance with IFRS. For example, if ABC had previously used the FIFO inventory method, it could switch the weighted average inventory method for its January 1, Year 4 Balance Sheet.

IFRS INTRODUCTION SUMMARY

IFRS US GAAP

Common Terms IFRS International Finanial Reporting Standards

FAS Financial Accounting Standards

Standard Making Board IASB International Accounting Standards Board

FASB Financial Accounting Standards Board

SEC Transitioning Requirements 3 Balance Sheets 2 Income Statements “Fresh Start”

N/A N/A

Theory Principles-Based More detailed based “Bright lines”

Why Switch to IFRS? Comparability between countries NA

1-11