CHAPTER 5 – Continued THE BALANCE SHEET AND STATEMENT OF CASH FLOWS Sommers – ACCT 3311.

25

CHAPTER 5 – Continued THE BALANCE SHEET AND STATEMENT OF CASH FLOWS Sommers – ACCT 3311

-

Upload

gerald-hicks -

Category

Documents

-

view

229 -

download

2

Transcript of CHAPTER 5 – Continued THE BALANCE SHEET AND STATEMENT OF CASH FLOWS Sommers – ACCT 3311.

CHAPTER 5 – Continued

THE BALANCE SHEET AND STATEMENT OF CASH FLOWS

Sommers – ACCT 3311

Word(s) of the Day

To provide relevant information about the cash receipts

and cash payments of an enterprise during a period.

The statement provides answers to the following

questions:

1. Where did the cash come from?

2. What was the cash used for?

3. What was the change in the cash balance?

Purpose of the Statement of Cash Flows

Statement of Cash Flows

Focus on

Perhaps the most noteworthy item reported on an income statement is net income—the amount by which revenues exceed expenses. The most noteworthy item reported on a statement of cash flows is not the amount of net cash flows.

The amount of net cash flows may in fact be the least important number on the statement. The increase or decrease in cash can be seen easily on comparative balance sheets. The purpose of the Statement of Cash Flows is not to report that cash increased or decreased by a certain amount, but why cash increased or decreased by that amount. The individual cash inflows and outflows provide that information.

Discussion Question

Q5-24 Differentiate between operating activities, investing activities, and financing activities.

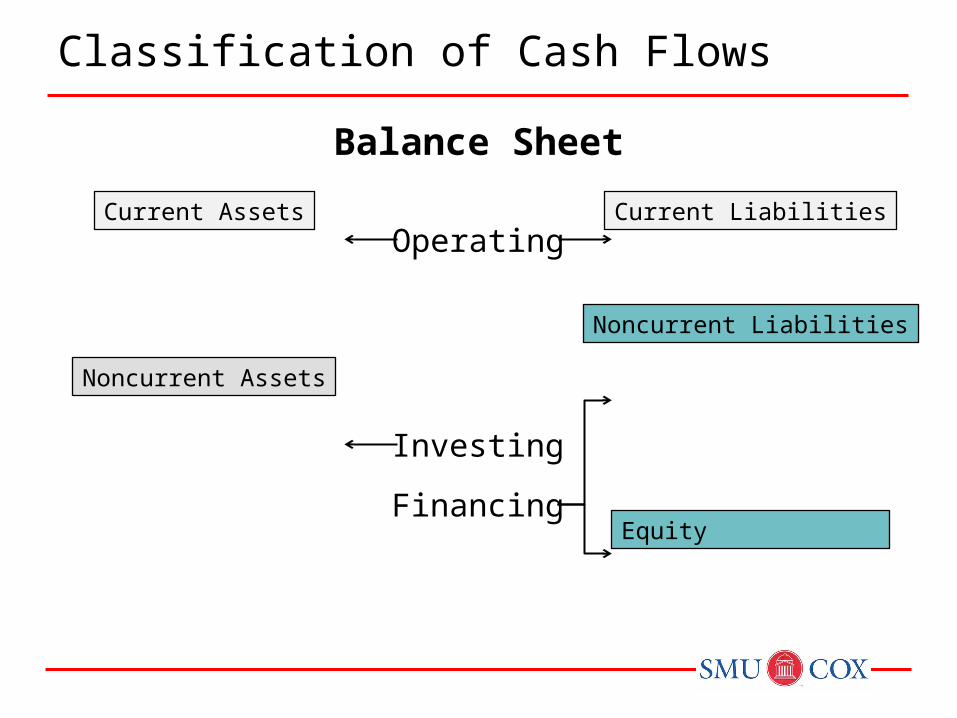

Classification of Cash Flows

Balance Sheet

Current Assets Current Liabilities

Noncurrent Assets

Noncurrent Liabilities

Equity

Operating

Investing

Financing

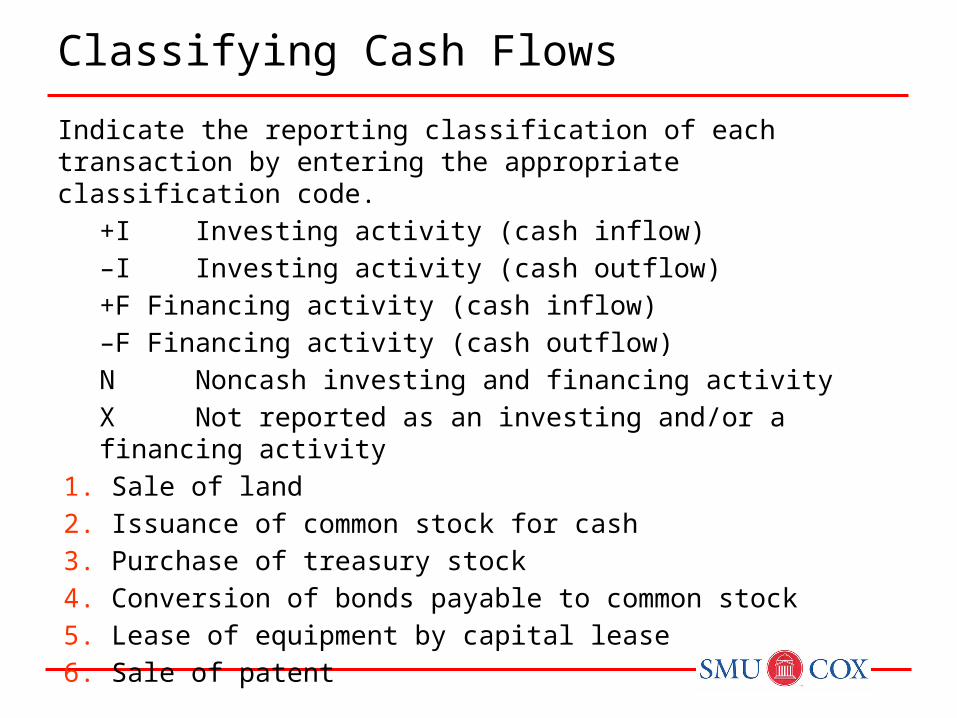

Classifying Cash Flows

Indicate the reporting classification of each transaction by entering the appropriate classification code.

+I Investing activity (cash inflow)

–I Investing activity (cash outflow)

+F Financing activity (cash inflow)

–F Financing activity (cash outflow)

N Noncash investing and financing activity

X Not reported as an investing and/or a financing activity

1. Sale of land

2. Issuance of common stock for cash

3. Purchase of treasury stock

4. Conversion of bonds payable to common stock

5. Lease of equipment by capital lease

6. Sale of patent

Classifying Cash Flows

+I Investing activity (cash inflow)

–I Investing activity (cash outflow)

+F Financing activity (cash inflow)

–F Financing activity (cash outflow)

N Noncash investing and financing activity

X Not reported as an investing and/or a financing activity

7. Acquisition of building for cash

8. Issuance of common stock for land

9. Collection of note receivable (principal amount)

10. Issuance of bonds

11. Payment of cash dividends

12. Issuance of short-term note payable for cash

13. Issuance of long-term note payable for cash

14. Purchase of marketable securities (“available for sale”)

Classifying Cash Flows

+I Investing activity (cash inflow)

–I Investing activity (cash outflow)

+F Financing activity (cash inflow)

–F Financing activity (cash outflow)

N Noncash investing and financing activity

X Not reported as an investing and/or a financing activity

15. Payment of note payable

16. Sale of equipment

17. Issuance of note payable for equipment

18. Repayment of long-term debt by issuing common stock

19. Loan to another firm

20. Sale of inventory to customers

21. Purchase of marketable securities (cash equivalents)

Reporting Cash Flows from Operating Activities

Two Formats for Reporting Operating Activities

Reports the cash effects of each

operating activity

Direct Method

Starts with accrualnet income and

converts to cash basis

Indirect Method

Note that no matter which format is used, the same amount of net cash flows operating activities is generated.

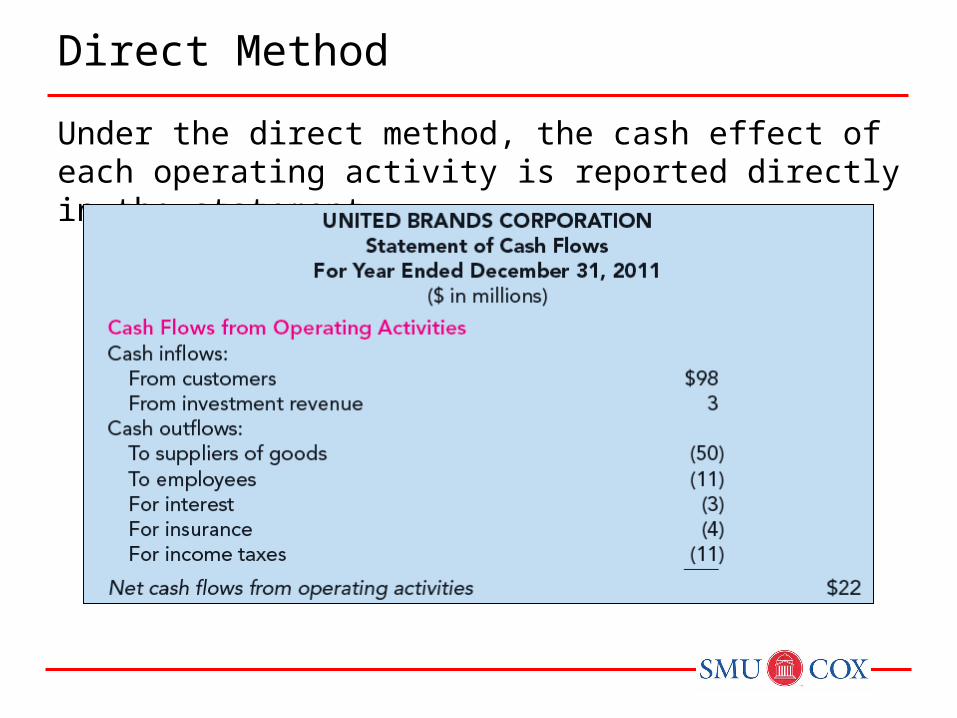

Direct Method

Under the direct method, the cash effect of each operating activity is reported directly in the statement.

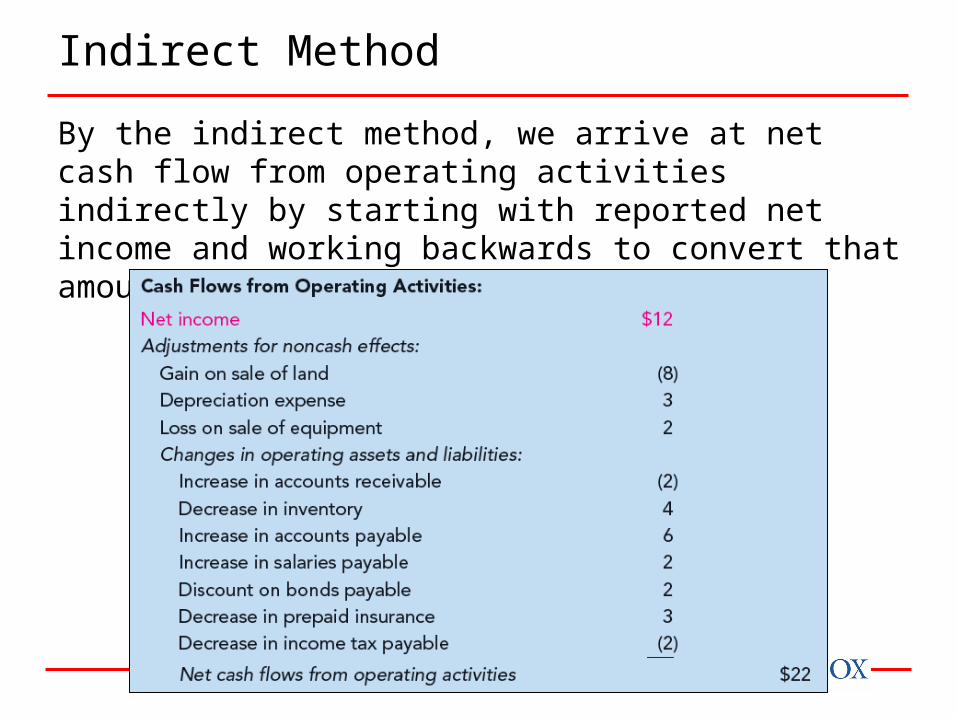

Indirect Method

By the indirect method, we arrive at net cash flow from operating activities indirectly by starting with reported net income and working backwards to convert that amount to a cash basis.

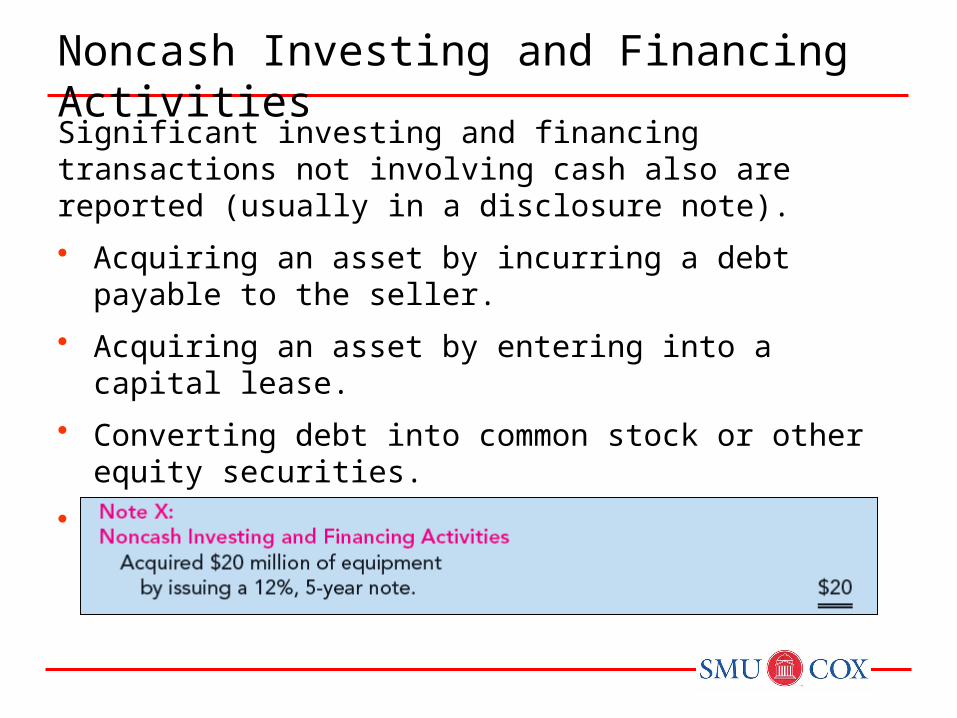

Noncash Investing and Financing Activities

Significant investing and financing transactions not involving cash also are reported (usually in a disclosure note).

• Acquiring an asset by incurring a debt payable to the seller.

• Acquiring an asset by entering into a capital lease.

• Converting debt into common stock or other equity securities.

• Exchanging noncash assets or liabilities for other noncash assets or liabilities.

Determining Cash Received or Paid

• When preparing a SCF using direct method, the numbers needed generally are not kept by the accounting system

– There is not an account that is the amount (balance) of cash paid to suppliers for merchandise

• Most people get these numbers by backing into them using accounting relations via T-accounts or by using journal entries

Determining Cash Received or Paid

Given: Beginning End

of year of year

Inventory $ 90 $ 93

Accounts payable 14 16

Cost of goods sold 300

Determine cash paid to merchandise suppliers.

• Cash paid to suppliers for merchandise

Cash from Customers

Given: Beginning End

of year of year

Accounts receivable $ 100 $110

Allowance for bad debts 5 3

Sales revenue 600

Bad debt expense 10

Determine cash received from customers.

• Cash received from customers

Proceeds from Sale

On July 15, 2011, M.W. Morgan Distribution sold land for $35 million that it had purchased in 2006 for $22 million. What would be the amount(s) related to the sale that Morgan would report in its statement of cash flows for the year ended December 31, 2011, using the direct method? The indirect method?

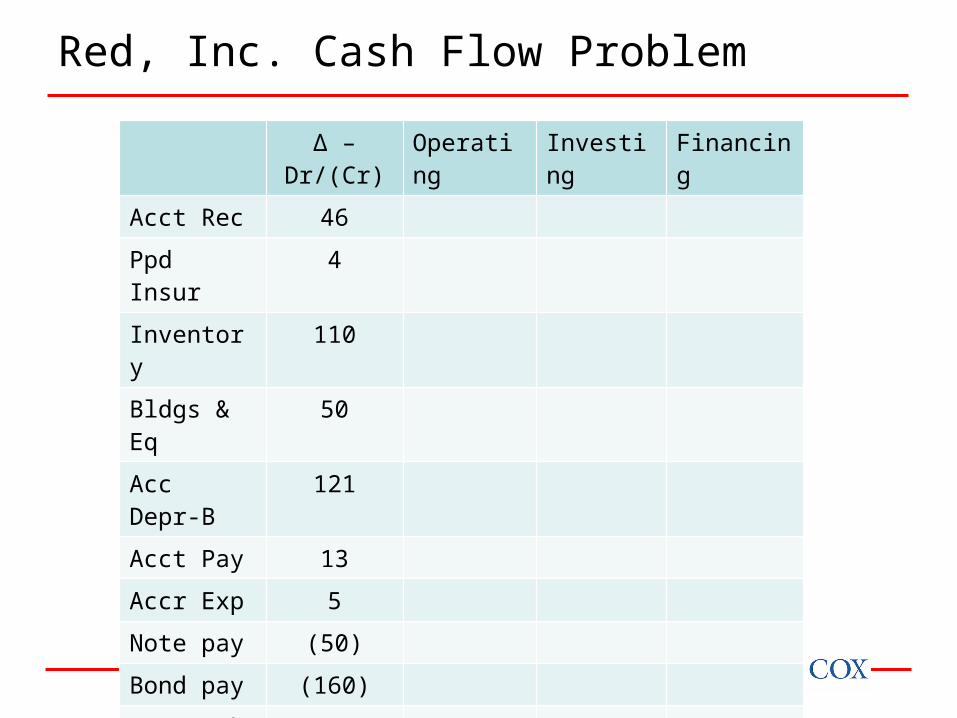

∆ – Dr/(Cr) Operating Investing Financing

Acct Rec 46

Ppd Insur 4

Inventory 110

Bldgs & Eq 50

Acc Depr-B 121

Acct Pay 13

Accr Exp 5

Note pay (50)

Bond pay (160)

Comm Stk 0

Ret Earn (53)

Red, Inc. Cash Flow Problem

Red, Inc. Cash Flow Problem

Red, Inc.Statement of Cash Flows

For year ended December 31, 2011

Red, Inc.Statement of Cash Flows

For year ended December 31, 2011

RELEVANT FACTS

Both IFRS and GAAP allow the use of title “balance sheet” or “statement of financial position.” IFRS recommends but does not require the use of the title “statement of financial position” rather than balance sheet.

Both IFRS and GAAP require disclosures about (1) accounting policies followed, (2) judgments that management has made in the process of applying the entity’s accounting policies, and (3) the key assumptions and estimation uncertainty that could result in a material adjustment to the carrying amounts of assets and liabilities within the next financial year. Comparative prior period information must be presented and financial statements must be prepared annually.

IFRS and GAAP require presentation of noncontrolling interests in the equity section of the balance sheet.

U.S. GAAP vs. IFRS

RELEVANT FACTS

IFRS requires a classified statement of financial position except in very limited situations. IFRS follows the same guidelines as this textbook for distinguishing between current and noncurrent assets and liabilities. However under GAAP, public companies must follow SEC regulations, which require specific line items.

Under IFRS, current assets are usually listed in the reverse order of liquidity. For example, under GAAP cash is listed first, but under IFRS it is listed last.

IFRS has many differences in terminology. For example in the equity section common stock is called share capital—ordinary.

Use of the term “reserve” is discouraged in GAAP, but there is no such prohibition in IFRS.

U.S. GAAP vs. IFRS

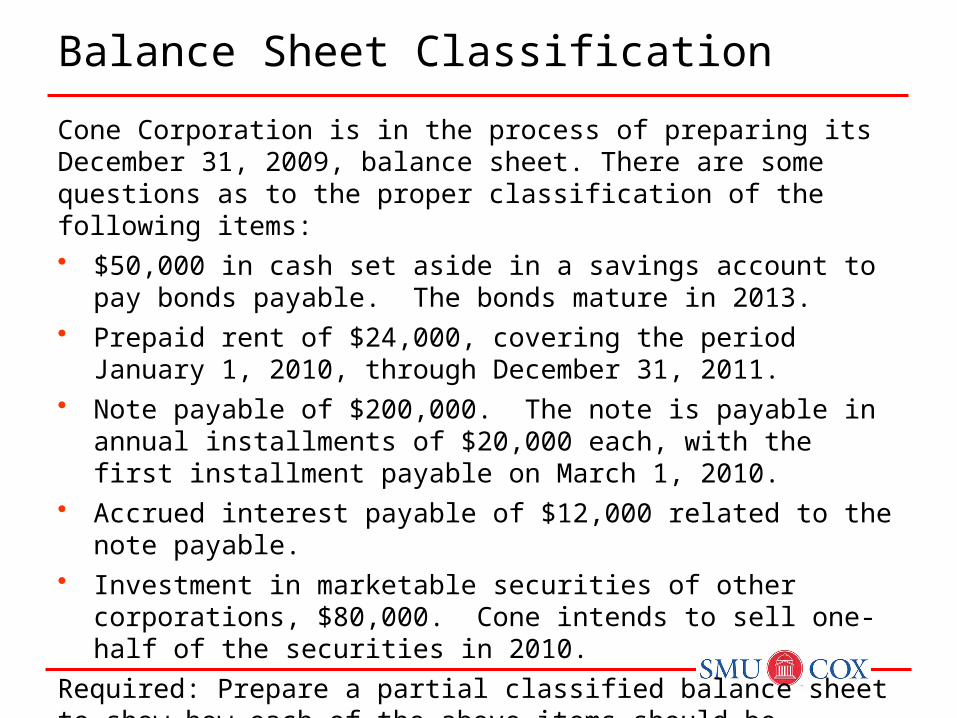

Balance Sheet Classification

Cone Corporation is in the process of preparing its December 31, 2009, balance sheet. There are some questions as to the proper classification of the following items:• $50,000 in cash set aside in a savings account to pay bonds

payable. The bonds mature in 2013.• Prepaid rent of $24,000, covering the period January 1, 2010,

through December 31, 2011.• Note payable of $200,000. The note is payable in annual

installments of $20,000 each, with the first installment payable on March 1, 2010.

• Accrued interest payable of $12,000 related to the note payable.• Investment in marketable securities of other corporations, $80,000.

Cone intends to sell one-half of the securities in 2010.

Required: Prepare a partial classified balance sheet to show how each of the above items should be reported.