NHS Change Day 2015 Wednesday 11 March Making a change for better together.

Military CoMMerCialJoint StoCk Bank 2008

A n n u a l R e p o r t

Change to Be Better

01 MB to be stable and trustworthy for 15 years03 Vision, mission and core value06 Chairman’s message08 Remarkable events10 Financial highlights12 Board of Directors’s Report16 Board of Management’s Report26 Organization chart28 Board of Management30 Board of Directors32 Supervisory Board34 BOD and Supervisory Board activities35 Statistics of shareholders36 Financial Statements96 Highlights of 200898 Contribution to community99 Notable awards

Content

Vietnam economy has witnessed major changes in the past 15 years. The country has benefited from rapid economic growth as well as has been negatively affected by regional and global financial crises, among which 1997 Asian financial crisis and the recent global one to be named.

In such a volatile environment, MB has taken the right steps in making quick adaptations to the market. 15 years on, the bank has always been ranked in the top 5 commercial joint-stock banks in terms of pretax profitability.

With the motto “Professionalism and enthusiasm” given as top priority, over 2000 staff at MB have always been ready to serve every need of our customers.

Our experienced and specialized team in risk evaluation and financial services offers our customers with integrated and smart financial solutions.

Our nationwide network of 90 transaction offices along with MB247 Customer Service Center, ATMs and POS systems brings our best-in-class banking services to maximize customer’s satisfaction and convenience.

These are the fundamentals why MB, a relatively new player in the industry, at its chartered capital raised up to VND 3,400 billion with just 15 years of operation, has made a familiar name across the country.

Having been successful in business, MB takes up social responsibilities by lending a helping hand to community, government- policy families, etc. in a variety of meaningful charitable activities.

With achievements in business performance and social activities, MB is highly appreciated and ranked A by the State Bank of Vietnam. In particular, MB is honorably granted Prime Minister’s merit certificate for outstanding business performance and “Vietnam Humanitarian Award” for great social contributions and selected as “Vietnam Excellent Brand 2008”.

Toward its 15th anniversary, MB is committed to upholding the objectives of safe and sound business practices, sustainable developments, management competence improvements, high-skilled workforce and staff training and strives for a 15 to 30 percent growth of all set targets.

Backed by a fifteen-year history, MB will remain as a reliable address for our valued customers, partners, shareholders and staffs and actively co-operate with the government on the implementation of its monetary policies for the sustainable development of economy.

MBto Be StaBle

and truStworthy

for 15 yearS

The 4th of November 2009 marks the 15th anniversary of MB

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 1

nearly 2,500 people at MB full of enthusiasm and initiatives are

working towards common targets.

viSionTo be one of the leading joint-stock commercial bank groups in Vietnam in

our chosen markets in principle urban areas, focusing on:Leveraging on our core corporate business and developing important

economic customer group.Selectively growing the SME market.

Building a strong capability in consumer bankingExpanding our treasury operations.

Developing our investment banking business andGrasping opportunities to extend our activities through related companies

towards a strong banking financial group.

MiSionMB to invest all efforts into building a professional staff whose expertise and dedication to client services will bring cost-effective and satisfactory

banking and financial solutions.

Core valueMB’s value is not defined by its assets, but is inherent in six core values which

are respected and upheld by each and every member of MB, including:Teamwork across the bank

TrustworthyCustomer care

CreativeProfessional

Performance driven

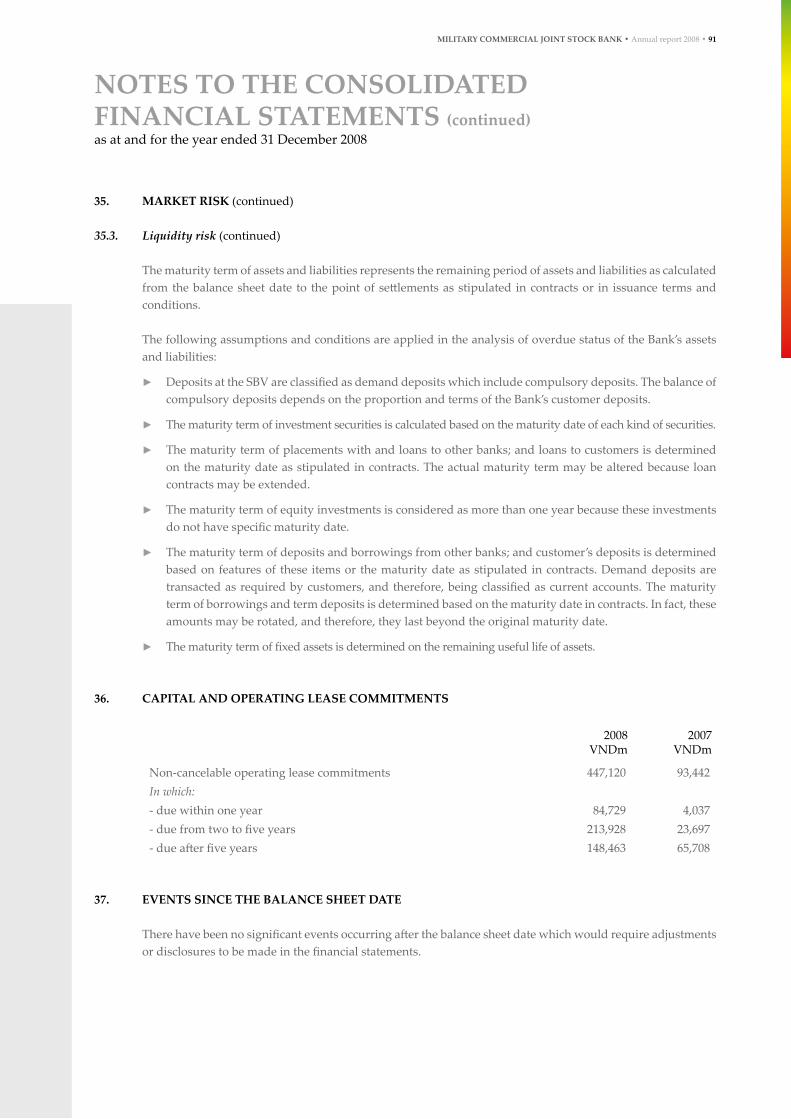

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 3

Oil price skyrocketed to USD 147/barrel in July, and plummeted to US$34/barrel thereafter.

Steel billet reached a record peak of USD1,200/ton, then fell to USD255/ton in November.

The U.S financial crisis which began with subprime mortgage credit crunch, especially after the collapse of Washington Mutual, Lehman Brothers and the acquisition of Merrill Lynch and Wachovia, etc.triggered a global economic turmoil.

2008 GloBal and vietnaM eConoMy

Annual GDP growth was only 6.23% compared to 8.48% in 2007.

Inflation made a 10-year record of 22.97%.

Trade balance deficit increased by 20.5%, up to USD 17 billion.

The prime interest rate was raised sharply to 14% per annum as of June 10th and then lowered to 8.5% as of December 22th to accompany with policies to prevent the country from

an economic recession.

The State Bank kept a tight rein on real estate and securities lending and raised the required reserve ratio to 11%.

The stock market experienced the worst development in its history, with the VN-Index losing two thirds of its value from the peak at over 1,100 in Mar 2007 to 315.62.

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 5

Ladies and gentlemen,

I am delighted to inform you that despite negative impact of global economic crisis, MB has managed to achieve impressive growth in all aspects, with a chartered capital at VND 3,400 billion, equity capital of VND 4,118.3 billion, total assets at VND 44,346 billion and pretax profits rising to VND 860.88 billion.

Last year, MB pioneered in complying with international risk management standards, with the first internal credit rating system approved by the State Bank of Vietnam Governor.

MB, as a leading commercial bank, played an active role in participating and implementing the Government’s

inflation-restraining measures to stabilize the macro economy and to meet the capital needs for socio-economic development. With such efforts and contributions, MB was honored with Certificate of Merit from the Prime Minister.

These are achievements accumulated from many years of organizational restructuring and the implementation of the five-year development plan initiated since 2004. The Board of Management and Board of Executives have agreed to target safe and sound business developments. Thanks to improvements in systematic management capability, business

forcasting and analysis, the Bank have implemented appropriate measures and reactions to market fluctuations and grasped opportunites.

During the past year, MB continued to foster comprehensive cooperation with large corporations such as Viettel Corporation, Vietnam National Coal-Mineral Industries Group, Vietnam National Petroleum Corporation, Mai Linh Corporation, Military Petroleum Corporation, Saigon New Port Company, Services Flight Corporation etc.

Besides, human resources continue to be one of the most decisive factors in determining MB’s success

Chairman’s

MeSSaGe

in 2008. They are the professional and innovative MB employees nurtured in a business culture filled with solidarity and sympathy.

In addition, compliance with legal stipulations, transparency in operation, and harmonization of the interests of customers, shareholders, workers and society has allowed MB to gain gradual advancements towards sustainable development.

2009, MB shall hold the 15th Anniversary with the message: “15 years stable and trustworthy”. The global economy and Vietnam’s alike is forecasted to continue to be in recession this year, while the financial and banking industry shall continue to pose more challenges. Heading towards the 15th anniversary, given the Bank’s current financial strengths and determination of our staffs, MB shall give priority to comprehensive growth not only for the Bank but also for all subsidiary companies.

Ladies and gentlement,

We would like to extend our special thanks and gratitude to the Ministry of Defence, the State Bank, related Authorities, our valued equity holders and customers whose diligent support drives our development. We are firmly convinced that with the core values in hand, we will always be your solid and trustworthy partner.

Sincerely yours,

TRUONG QUANG KHANHChairman

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 7

Remarkable events

MB was established in 1994 under the Decision No. 00374/GP-UB granted by Hanoi People’s Committee. On the 4th of November 2009, the Bank officially came into operation under License No. 0054/NH-GP granted by The State Bank of Vietnam with the term of 50 years.

2004Successfully organizing shares auction: MB was the first bank to organize a shares auction with value of VND 20 billion. Our message was that MB served not only military enterprises but also the public.

Launching Active Plus Card: It was the first time in the market that cardholders were insured up to VND 10 million.

Organization restructuring: Under new business model, MB transformed towards separating management unit and business operations unit with customer focus and completing all the procedures and regulations to improve its efficiency.

Receiving Certificate of Merit from the State Bank Governor for its outstanding performance in 2003.

2005Signing a multilateral agreement with Vietcombank and Viettel Corporation to pay Viettel bills via ATM card.

Signing comprehensive cooperation agreement with Citibank

2006Deploying the project of modernizing the IT system of Temenos Group – Switzerland in order to increase competitiveness and bring the best banking facilities and services to customers.

Launching Mobile Banking and Internet Banking services.

Successfully issuing 5-year convertible bonds worth VND 220 billion.

Sponsoring and promoting the APEC 14th Summit 2006, Vietnam’s biggest event of the year.

Receiving the Vietnam Excellent Brand Award for 2005.

Establishing Hanoi Fund Management Company.

Cooperating with CIDA in strengthening risk management capacity.

2007Implementing successfully IT system modernizing project with the installation of corebanking software provided by Temenos group. Online transactions are supported.

Deploying the internal credit rating project under the consultancy of Earnst & Young Vietnam.

Officially becoming a member of Asian Bankers Association – ABA.

Signing Comprehensive Cooperation Agreement with Vietnam Machinery Erection Corporation (LILAMA), Hanoi Housing Development and Investment Corporaton (Handico), Military Petroleum Company (MPC), PetroVietnam Joint stock Finance Corporation (PVFC)

Signing cooperation agreement with PetroVietnam Securities Company (PVS) and Sacombank, and strategic cooperation agreement with Vietcombank

Successfully holding the 2007 General Shareholder Meeting, whereby the plan for raising chartered capital to VND 7,300 billion by the end of 2010 was approved.

Became the first public bank to be granted the license to offer convertible bonds to the public by the State Securities Commission on 15 June 2007.

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 9

50%^

finanCial hiGhliGhtS

58%^total mobilised funds

4,93

3

7,04

6.6 11

,602

.4

23,1

36.4

36.5

29,1

2004 2005 2006 2007 2008

VND

bill

ion

total assets

2004 2005 2006 2007 2008

VND

bill

ion

6,99

5

8,43

2 13,6

11.3

29,6

23.6

44,3

46

36%^ 41%^ 24.48%total outstanding loans

2004 2005 2006 2007 2008

VND

bill

ion

3,92

1

4,47

0

6,16

6.6

11,6

16.6

15,7

40.4

Pre-tax profits

2004 2005 2006 2007 2008

VND

bill

ion

148,

7 269,

6

608,

9

860,

883

roe (Return on Equity)

2004 2005 2006 2007 2008

%

27.5

1

30.1

6

27.7

8

24.7

0

24.4

8

Key tarGetS in 2009

Pre-tax Profits : VND 950 billion

Total Assets : VND 58,500 billion

Outstanding Loans : VND 21,500 billion

Mobilized Funds : VND 45,000 billion

Number of Employees : 2,950 people

Network : 111 branches and transaction offices

105,

4

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 11

Board of Directors’s Report

The year of extremes 2008 was over, and MB’s performance remained solid and was marked by a series of distinguished events: raising chartered capital up to 3.400 billion dongs, sucessfully implementing internal credit rating system and receiving prestigious awards for excellent brand.

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 13

Highlights of business results

The eventful and challenging 2008 has tested the banking industry’s health, and MB’s sound management capability and widely known brand name have proven its strengths to overcome difficulties and adapt to market changes.

MB’s performance remained stable, highlighted by various events: increasing chartered capital to VND 3,400 billion, achieving good growth in all criteria, successfully deploying internal credit rating systems and being granted with a number of prestigious brand awards.

As of 31st December 2008, pre-tax profit of the Group was VND 860.883 billion (of which VND 770.708 billion came from the Bank), equal to 141% from the result of 2007 and 117% as planned. Mobilized funds reached VND 36,529.1 billion, up 58% compared to 2007. Total assets respectively grew to VND 44,346 billion, 1.5 times higher than earlier in the year. Total outstanding loans stood at VND 15,740 billion, 36% higher compared to late 2007.

Chartered capital increased to VND 3,400 billion following plans approved during General Shareholder’s Meeting on 19th of May 2008 by converting 2006 issued convertible bonds valued at VND220 billion into common shares, delivering stock bonuses to our shareholders and issuing more shares to domestic strategic partners.

Due to positive business results, sufficient liquidity and bright outlook, MB’s share is one of the most the preferred stock in the OTC exchange.

In 2008, Military Bank was honored to receive the Certificate of Merit from the Prime Minister in addition to other prestigious awards such as the Golden Cup for Prestige Securities Brand; The Leading Joint Stock Company of Vietnam; Enterprise with Best Customer Services; Top 100 Vietnam Leading Brand names,etc.

Major changes of the year

Firstly, it was the midterm transfer of the Chairman’s office from Mr. Pham Tuan to Mr. Truong Quang Khanh. Without creating any disorder in the organization and activities of the Board of Management, the transfer brought extremely good outcomes. The former Chairman continues to contribute to the Bank as a senior member of the Consulting Council. The new Chairman took the office and has since performed well, despite his tight schedule as a member of the Central Party Committee.

Second is the implementation of new organizational structure in accordance with 2004 – 2008 strategy, including the setting-up and assignment of functions and mandates to Divisions, establishment of new units under Divisions and Departments, branch upgrading, and preparation for setting up Senior Committees.

Besides, MB also standardized hierachy level for all designations and implemented HR consultancy project including completing personnel strategy, standardizing organizational structure among the Bank, and bringing in line performance management and other policies to achieve substainable human resource development.

With the guideline of continuous enhancement of customers’ benefits, MB pays much attention to improving existing products, researching and launching new products and services. For our corporate clients, MB offers services such as overdraft, trade finance, international factoring, Internet banking, negotiation of export documents, bancassurance.

For medium and small enterprises, MB has specialized products such as installment loans, and loans for equipment purchasing (medium and long term), etc.

For retail customers, MB has fully developed valuable paper mortgage loan, loan for small vendors, craft villages, housing loan, loan

Developing a geographically rich network • with focus on ASEAN countries and setting up representative offices at regional hubs.

Facilitated by advanced technological • infrastructure, maximizing customers’ benefits with the latest and cost-effective products and services. An advanced technology base shall also provide an efficient Management Information System to support banking and business management.

Managing investment portfolio for the group’s • best benefits.

Ensuring employees’ satisfactory income, • balancing and contributing to social development and maximizing shareholders’ interests and values.

for overseas study, household business loan, loan for home construction and renovation, and other products such as overdraft, wealth management, etc.

Outlook and future plan

With the above-average growth rate, MB is making rapid and vigorous strides towards becoming one of Vietnam’s leading banking and financial groups.

In addition, performance quality, efficiency and soundness are placed as top priority. MB is also on its way to make diligent improvements in customer-oriented model and risk management system.

Meanwhile, the Bank is constantly increasing its competitiveness, expanding network and enhancing executive management capacity and risk management.

In the year, MB has also reshuffled our shareholder structure, focusing on the establishment of strategic shareholder group and consolidating the Board of Directors, Board of Management and preparing for IPO in late 2009 or early 2010. MB plans to increase its chartered capital to VND 7,300 billion in 2010.

In the long run, MB’s targets have set forth for the period 2009-2013 as below:

Becoming a first class banker with strong • capital base and excellent brand name.

Having dynamic and qualified Executive • Board and staff with business ethics under the management of a strong Board of Directors.

Operating in diversed market segments: • Large corporates, SMEs and consumers. For each market, we will design a tailored-made strategy to penetrate and exploit effectively.

Providing a wide range of services packages • in form of integrated financial solutions, customized for each client. It includes commercial banking, retail banking, investment banking, private banking (wealth management), insurance companies (life and non-life insurance), consumer lending, real estate lending and leasing.

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 15

Board of Management’s Report

“MB is among few banks who have efficient liquidity management and acts as major lender in the interbank market, easing liquidity shortage faced by other credit institutions, which is highly recognized by the State Bank”

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 17

Profitability

The 2008 turbulence in the banking industry left its mark on MB’s results, a slight decline in profitability ratios. However, the overall figures remained stable and above-average. Although average equity increased rapidly, pushing returns on equity (ROE) down by 0.2% to 24.5%, it was still high and thus, shareholders’ benefits were protected. Returns on assets (ROA) stood at 2.41%, slightly decreasing from 2.82% of previous year, but it remained higher than the industry average (of about 1-2%).

Solvency

Tough economic conditions in the early months of the year led to liquidity problems for many banks; however, MB managed to maintain sufficient liquidity. With prudent capital utilization, MB’s solvency ratio was always higher than 1, exceeding the mandatory prudent ratio stipulated by the State Bank. MB was among few banks who have efficient liquidity management and acted as major lender in the interbank market, easing liquidity shortage faced by other credit institutions, which was highly recognized by the State Bank. The percentage of Medium and Long-term Loans funded by short term Resources was only 4.57%, much lower than the State Bank’s permitted level at 40%s.

ROE (%)

27.7

8

24.7

24.5

2006 2007 2008

ROA (%)2.

44

2.82

2.41

2006 2007 2008

report on finanCial perforManCe

Solvency ratio (%)

1.79

5.95

1.19

2006 2007 2008

The percentage of Medium and long term loans funded by short term resources (%)

0 0.59

4.57

2006 2007 2008

for impaired loans in line with international standards, realistically and holistically reflecting customers’ credit quality.

Changes in shareholders’ equity

Upon implementing plans for raising chartered capitals to meet the rising needs of the banking business, and in accordance with the Resolutions of MB’s General Shareholders’ Meeting, approved by the State Bank of Vietnam and the State Securities Commission, MB completed to convert convertible bonds issued in 2006 (totalled VND220 billion) into common shares, pay stock bonuses to shareholders and issue stocks to local strategic partners.

As of December 31st 2008, the outstanding stock issued by MB included:

Share

Total par value: VND3,400 billionQuantity: 340,000,000 sharesPar value: VND10,000 per share

Convertible bond

Total par value: VND1,000 billionPar value: VND1 million per convertible bond, including:

* VND420 billion convertible bonds issued in batch 1 of 2007 with the term of 2 years, yield of 8% per year;

* VND580 billion convertible bonds issued in batch 2 of 2007 with the term of 3 years and yield of 8% per year.

Dividend

With the motto “capital preservation and growth together with shareholders’ benefits protection” MB over the past years has exercised a stable dividend policy exceeding 15% per annum. In 2008, MB issued 12.4% bonus shares to its shareholders and delivered 3 times advanced dividends of 18%.

Capital adequacy ratio (%)

15.4

7

14.2

1

12.3

5

2006 2007 2008

Non -performing Loans ratio (%)

2.7

1.01

1.83

2006 2007 2008

report on finanCial perforManCe

Capital Adequacy Ratio (CAR) and Non-performing Loans (NPLs)

As MB strictly follows the principle for cautious use of capital together with allocative efficiency and optimal tradeoff between risks and return, we maintained our CAR at 12.35% throughout 2008, well beyond the minimum of 8% stipulated by the State Bank.

Credit activities exhibited considerable risks stemming from credit risks, legal risks, and exchange rate risks in 2008. Thanks to our appropriate credit policy, strict adherence to banking safety regulations, and administration of our loan portfolio through remote and on-site monitoring, in addition to cautious credit expansion on the basis of restructuring outstanding loans, MB was able to limit risks despite the deteriorating economic environment.

Meanwhile, MB frequently provides direct instructions, to supervise and inspects its branches ensuring system-wide strict compliance with the State Bank’s regulations and policies. This made it possible for MB to keep tight control on overdue debts. As of December 31st, 2008, NPL stood at 1.83% out of total outstanding loans, much lower than the industry average of 3.5%. Our internal credit rating system, approved by the State Bank was officially deployed, facilitating MB to categorize outstanding loans and make provisions

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 19

In 2008, MB’s business indicators met its planned targets and performed significantly better than 2007.

Total assets stood at VND 44,346 billion, a 50% increase compared to 2007, meeting the expansion requirements, suitable for the equity growth rate of the Bank.

Despite the liquidity fluctuation and severe competition over the year, capital mobilization of MB remained sound. As of December 31st

2008, total mobilized capital grew 58% y-o-y to VND 36,529.1 billion, achieving 118% of planned targets. This is mainly attributable to economic organizations and inviduals deposits being VND 27,162 billion, 53% higher compared to the previous year.

In 2008, MB followed the State Bank’s policies in tightening credits to restrain inflation. As a result,

its outstanding loans grew by 36% compared to 2007, while total outstanding loans reached VND 15,740 billion. Pertaining to loan structure, short-term debts accounted for 63% of total debts, with the remaining 37% that are composed of medium to long-term loans; out of which, 86% were made out to economic organizations, and 14% to individuals. Non-performing loan from category 3 to 5 accounted for 1.83% of the total outstanding loans, much lower than 3.5% of the industry’s average.

For 2008, MB is proud to have achieved good business results, amid economic downturn. Profit of the Group arrived at VND 861 billion, a 41% increase from 2007, surpassing 17% of its target. Of the total profits, VND 770.7 billion came from the Bank and VND 90.2 billion was contributed by subsidiaries and affiliated companies. With 2008 results, MB ranks amongst the top 5 commercial banks in terms of profitability and ROE.

Services saw positive improvements and developments. Income from this area was VND 262 billion, 28% higher than 2007.

In addition to business growth, MB always fulfills its tax duties with the government.

MB’S iMproveMentS in 2008

Organizational strucuture, policies and management

In 2008, MB undergone restructuring of its functional departments: head office, branch-offices, and transaction offices, in accordance with new modern bank model, and completed hierachy levels for all designations. We have also completely implemented new compensation schemes, bringing higher salary to all positions held, to encourage and motivate staffs.

report on BuSineSS reSultS

Total outstanding loans

Total assetsPre-tax profits

36,5

29

31,0

00

23,1

36

15,7

40

15,6

00

11,6

13

44,3

46

45,0

00

29,6

24

861

735

609

Total mobilised funds

Implementation 2007

Plan 2008

Implementation 2008

Unit: VND billion

Customer care

Striving to make the best possible customer services, MB continues to research into new solutions, providing detailed action plans to implement its findings. Sets of customer services manuals and MB’s trading floor standards were issued to standardize and improve services qualities.

In addition to services quality standards, MB carried out “Mystery Customer programs” to spontaneously investigate on the actual services quality at MB’s transaction offices, as well as ensuring the standards are put into practice. The program was held 4 times across the Bank, which provided an insight on MB’s services quality making it possible to work out new solutions to improve customer services.

Moreover, to further enhance staff’s awareness of services quality, a contest named “Golden Bees” was held for all MB’s tellers, helping them experience various situations with customers, improve their knowledge and communication skills. The contest successfully delivered profound lessons on the importance of customer services quality and the necessity to provide customers with state-of-the-art quality.

Network development

During the year, MB opened 25 new transaction points, expanding its operating network to 90 transaction points as of December 31st, 2008. The new offices were set up based on careful researches of customer demands, and were aligned with the Bank’s scales and development strategies. All transaction offices began operating efficiently and attracted a great number of customers soon after its opening. 99% of them became profitable after 6 months of operation.

Services development

With a clear focus on customer, MB never ceased its researches and deployment of new products to best satisfy our customers’ diverse needs.

MB has established relations with numerous large corporations and economic groups, such as Song Da Corporation, Viettel Corporation, Military Petroleum Corporation, Vinacafe, Mai Linh Group, Vietnam National Coal - Mineral Industries Group, Vietnam Southern Food Corporation, etc. MB will provide these partners with packages of banking and financial services, including lending, international settlements, salary payments via accounts, and unsecured lending for employees, etc.

For small and medium enterprises, MB will make continuous improvements on existing products, including valuable papers mortgage loans, and inventory and/or receivables mortgage loans. In addition, new products such as international factoring and overdraft facilities are being researched and launched.

During the year, MB has completed regulations on investor portfolio management, collection and disbursement services, overseas study loans, household business lending, and house renovation loans. We have researched and launched our asset management services to our VIP customers, overseas remittance services, credit card and debit card services, mobile payments, web payments, and savings deposit with lottery drawing on the MB’s 14th Anniversary.

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 21

Human resource development

MB’s human resource has grown significantly with better input.

MB has successfully implemented HR consultancy project including completing personnel strategy, standardizing organizational structure among the Bank, and bringing in line performance management and other policies to achieve substainable human resource development.

In 2008, MB recruited an addition of 585 employees. As of December 31st, 2008, MB’s workforce totaled 2,435 employees, of which 95% have bachelor degrees and above. Average monthly salary at MB in 2008 was VND 8.01 million/capita, significantly higher than the average VND 5.08 million in 2007.

MB pays much attention to staff training. Since its inception, MB’s Training Center has held 146 courses, both local and international with up to 4,489 participants. Self-improvement is highly promoted and encouraged across the bank. Last year, MB successfully organized a competition named “MB’s Got Hipo”, and attracted a large number of employees. It was to facilitate the Bank to seek for and develop new talents and train them to be the future’s leaders.

Technology

After successfully implementing the new software program T24, MB continued to develop additional modules within the T24 project, complete the back-up transmission line, build new system platforms, invest additional hardware equipment, deploy

Card software along with the Way 4 software of Open Way Corporation and bring Contact Center into operation. During the year, MB also started to connect accounts with securities companies such as Dai Viet, VNS, TSC and tested the payment connection with Paynet, VinaPay and Mobivi, etc. in order to launch the payment services through Mobile, POS and electronic payment tools.

Supervisory Activities

MB gave top priorities to risk management in every aspect of the operation. During the course of the year, the Bank diligently performed risk managements and internal supervisions and auditings. Regular and random spot checks were carried out to inspect credit qualities, data management and treasury safety at all units. This enabled timely fault detection and amendment to ensure stable operation and compliance with MB and State Bank regulations.

MB’s internal credit rating system has facilitated the planning and implementation of credits, risk management and customer policies for the safety and efficiency of its operation. This rating system helped to evaluate credit portfolio quality and determine the exact credit losses with regard to product range or economic sector as well as analyze the risks and returns for each product range.

Moreover, debt recovery was also thoroughly carried out, helping reduce NPL ratio to 1.83%, against the industry average of 3.5%.

Community Contribution

Having been successful in business, MB takes up social responsibilities by lending a helping hand to community, government- policy families, etc. in a variety of meaningful charitable activities. Deemed as MB’s responsibility as well as a root of corporate culture, social activities received strong awareness and participation from both the Bank and its staff.

In 2008, MB was honorably received the “Vietnam Humanity” award for its continuous contribution to the community.

Future development plan

The global economy is expected to continue its decline in 2009, and Vietnam economy will less likely escape this climate. The banking industry will face much more difficulties and fluctuations, adding much complexities and risks.

In 2009, MB determines to “Maintain sound and safe business practices, enhance management capabilities, develop high quality personnel, and make full use of cooperation programs amongst MB’s subsidiaries. Meanwhile, MB seizes every opportunity to invest in potential sectors and gaining greater market share, paving the way for further developments in 2010”.

Detailed targets were set forth for the heading 2009 as follows: Total Assets reach VND 58,500 billion, Outstanding Loans amount to VND 21,500 billion, Mobilized Funds rise to VND 45,000 billion, Pretax Profits achieve VND 950 billion whilst NPL will be kept under 2%.

The Bank is weighing two plans to increase chartered capital in 2009.

Option 1: to increase minimum to VND 4,400 billion

Option 2: to increase minimum to VND 5,300 billion

It is considered as a critical step on the path to reach a increase chartered capital of up to VND 7,300 billion by the year 2010 approved by the Shareholders’ Meeting.

To achieve 2009 targets, a number of measures will put emphasis on:

Strategy improvement: Based on the 2004-2008 strategies, the Bank shall complete its strategy and 2013-2015 vision with the aim to be the Vietnam’s leading commercial bank in chosen markets.

Organization reinforcement: MB continues to improve and reinforce organization model from the Head Office to branches, streamline internal relations with specific stipulations on job descriptions. MB also offers the most favorable conditions for consulting agencies of MB’s subsidiaries to use the Bank’s human resources and other resources

effectively. Consolidation will be carried out in all transaction offices together with re-evaluation of business activities. Online sales channels project will be completed.

Personnel and training: MB plans to enhance capabilities of management staffs at all levels, quickly fill up vacant positions for the Bank’s development and improve its professionalism; Personnel policies focus on encouraging staff’s initiatives and attracting high-quality talents (remunerations, bonus-schemes, promotion opportunities, training, career advancements, etc.). At MB we often emphasize the importance of career ethics and focus much attention to our training qualities, grooming talents for further integration.

Project completion: Make the best use of Core-banking systems; develop strong retail banking products, namely e-banking. Continue to invest in management modules, enhance system operation capacities. Implement ISO quality management project and Customer Relation Management (CRM) project.

Continue MB’s brand promotion program. Take the Bank’s 15th Anniversary as an opportunity to promote “MB - 15 years of stability and trustworthiness”. Build media plan based on a consistent, creative and effective brand promotion program. MB shall carry on developing corporate culture with its own identity, strengthen internal and external media activities.

Stringent risk management: To continuously improve risk management infrastructure, especially risk management and supervisory system; Constantly develop procedures to ensure compliance; Operate in conformity with applicable laws and regulations; Ensure safety at transaction sites, warehouses, cash-transportations, cash counting, prevent negative actions and operational risks.

The Board of Executives firmly believe that with a close watch on the economic climate under the direction of the Board of Management and with the contributing efforts of our staffs, MB shall strive to overcome challenges and difficulties to achieve its targets.

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 23

related CoMpanieS

Companies which hold over 50% stakes of MB

At present, no companies are holding more than 50% stakes of MB.

Companies which MB holds over 50% stakes

SubsidiaryBusiness

licenseBusiness

scopeTotal

investment

Thang Long Securities Company

License No. 05/GPHĐKD Investing and trading stock

83.33%

Hanoi Fund Management License No. 21/UBCK-GP Fund management 60%

AMC Asset Management Company Ltd

License No. 0104000066 Debt and asset management

100%

MB Land Joint Stock Company

License No. 0103022148 Real Estate trading 65.26%

Summary of operation and financial situation of the companies which MB holds more than 50% stakes

Thang Long Securities Company (TSC)

The stock market experienced much turmoil in 2008. Transaction volume decreased while share prices tumbled by 70 to 80 per cent for most stocks. Majority of investors incurred heavy losses, and securities companies had to scale down their businesses. Under such circumstances, TSC managed to remain in sound business. The Company completed procedures to increase its chartered capital to VND 420 billion as planned, strengthening its organization, recruitment of talents, application for ISO quality management requirements, and implementing its new IT software program. More importantly, 2008 witnessed dramatic improvements of TSC staffs. The Company undergone researches and structured various models for analysis, evaluation and forecast of stock price fluctuations, which were highly praised by our investors.

AMC Asset Management Company (AMC)

During the year, VND 34.342 billion bad loans have been recovered. The Company also designed, constructed and upgraded 40 transaction points and 30 ATM machines for the Bank.

For the real estate business, the Company focused on gaining control and utilizing buildings, continued the sale of loan collaterals, and executed the Bank’s projects as planned.

Hanoi Fund Management (HFM)

HFM’s activities have been geared towards strengthening its organizational structure, completing the drafting, enforcing of business processes and regulations in accordance with the regulations on asset management issued by the Ministry of Finance. In September 2008, HFM signed a strategic cooperation agreement with Saigon Asset Management Corporation (SAM) and Vietnam Equity Holding (VEH) - an USD 80- million- investment fund listed in Germany Stock exchange, according to which HFM shall provide porfolio management services for VEH. This partly reflected HFM’s reputation and capability in the business world. At the end of the fiscal year of 2008, HFM was one of five largest funds in terms of total managed assets.

MB Land Joint Stock Company

In 2008, MBLand has improved its organization structure, issued its Charter and Regulations, built up corporate culture as well as recruited more personnel. At the present, the number of staff reaches 142. Simulteneously, the Company has carried out various feasible and effective investment projects in principal areas.

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 25

Human & Organization

orGanizationChart

head offiCe ManaGeMent

riSK ManaGeMent

BuSineSS

Board of direCtorS

Board of ManaGeMent

internal audit r&d

Credit CoMMitteeSenior CoMMitteeS

SuperviSory Board

internal Control

Planning Business Support

Legal & Compliance Admin & Quality management

PR Network & Distribution channel management

Finance & Accouting

IT Centre

Human Resources

Public Unions

MB Representative in Southern area

Corporate & Financial institutional

SME

TREASURY

Personal banking

Investment

ShareholderS

BuSineSS Support

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 27

BOARD OF MANAGEMENT

1. Mr. le van BeChief Executive Officer

Mr. Le Van Be holds a Bachelor Degree in Economics; he has taken office as the CEO since 1996. The CEO is responsible for all businesses and operations of the Bank in accordance with the laws and acts as counselor of the Board of Directors in planning major targets. He is assisted by Deputy General Directors, Chief Finance Officer and expert teams.

1 2

4

3

5

7

6

8 9

2. Mr. le CongDeputy Director General

Mr. Le Cong holds a Bachelor of Eonomics Degree from Finance & Accounting University, and a Bachelor Degree from Hanoi University of Technology. He received his Master of Economics Degree from Army Ordnance Academy of Vietnam. He has been working for MB since its establishment in 1994. Currently he is the Head of SME Division and Chairman of Military Insurance Company (MIC) of which MB is a major shareholder.

3. Mr. do van hungDeputy Director General

Mr. Do Van Hung holds a Bachelor Degree in Banking from the Vietnam National Economic University, and a Bachelor Degree in English from Hanoi Foreign Language University. He has accumulated over 10 years of experience in Banking and Finance. At MB, Mr. Hung is in charge of Operations Division.

4. Mr. le van MinhDeputy Director General

Mr. Le Van Minh graduated from Banking Academy of Vietnam with a Bachelor Degree. After years as the Deputy Manager of Financial Department at Army Zone 3, and Chief Accountant of Song Hong Corporation, he was later appointed as the Deputy Director General of MB in November 2000. He is in charge of MB’s Hanoi Transaction Office.

5. Mr. dang Quoc tienDeputy Director General

Prior to joining MB in June 1996, Mr. Dang Quoc Tien was in charge of Foreign Economic Affairs at Army Zone 7 under control of the Ministry of Defense. Mr. Tien received his Bachelor Degree in Economics from Foreign Trade University in Vietnam, and later received his Master in Economics from the Pacific Western University. He has attended securities specialist training courses at the Banking Academy and business administration specialist courses at Hanoi National University. He is assigned to be in charge of the Southern region.

6. Ms. vu thi hai phuongDeputy Director General

As one of the pioneers of MB since 1994, with excellent achievements, Ms. Vu Thi Hai Phuong was been entrusted to hold several important positions throughout the years: Head of Transaction Office (1998-2004); Deputy Director then Director of Dien Bien Phu Branch (2004-2007). Ms. Phuong holds a Master Degree in Monetary Finance, from the Banking Academy of Vietnam. She is now undertaking Corporate and Financial Institutions Division.

7. Ms. Cao thi thuy ngaDeputy Director General

Ms. Cao Thi Thuy Nga has 11 years of experiences in the credit division at the Bank for Investment and Development of Vietnam, and has more than 12 years of experiences working as the Chief Accountant cum HR Director at VIDPUBLIC Joint Venture Bank. She graduated with a Master Degree from Finance University of Vietnam and participated in International auditing courses held Vietnam Auditing Company. With her significant contribution to building MB’s Brand, Ms. Nga is in charge of Administration, Quality Management, Network Development as well as Public Relations Division.

8. Mr. luu trung thaiDeputy General Director (appointed in April 2008)

Joining MB since 1997, Mr. Luu Trung Thai has been appointed to hold numerous important positions such as: Head of Credit Department of MB at Head Office, Director of Danang Branch also is in charge of Midland region, Personnel Manager, etc.Graduated with a Bachelor Degree from the Banking Academy of Vietnam, B.A of Law and MBA from University of Hawaii – USA; Mr. Thai is considered as the founder for MB’s development in Central Vietnam. Designated as the Deputy Director General in April 2008, he is currently in charge of Human Resource Division, Personal Banking and IT Division.

9. Ms. pham thi tyChief Financial Officer

Ms. Pham Thi Ty graduated from Finance and Accounting University in Vietnam. Previously, she served for almost 10 years as the Chief Accountant in Accounting Department of the State Bank of Vietnam, and Vietinbank Ba Dinh Branch. She first joined MB holding the position as Chief Accountant, and was later promoted to Chief Financial Officer.

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 29

BOARD OF DIRECTORS

As elected representatives for the Bank’s shareholders, the Board of Directors is duly authorized by the shareholders to make decisions within its authority.

The Board of Directors appoints a Standing Board that oversees the Bank’s operation and timely handle issues beyond the authority of the Chief

Executive Officer. In 2008, the Board of Director and the Standing Board closely directed the Board of Management to successfully complete

the 2008 plan. They also established procedures and operation regulations to ensure legal compliance and efficiency.

1 2

4

3

5 6

1. Mr. truong Quang KhanhChairman

Appointed as MB’s Chairman in May 2008, Mr. Truong Quang Khanh has oriented the Bank throughout the eventful 2008 towards remarkable results.

Graduating with a Ph.D, and having good command of both Russian and English, Mr. Truong Quang Khanh is currently a member of the 10th Communist Party Central Committee, National Assembly Delegate and Deputy Minister of Defense.

2. Mr. pham viet thichVice Chairman

Mr. Pham Viet Thich has made significant contributions to MB’s development as the Vice Chairman for many successive years. He holds a Bachelor Degree in Economics, and has accumulated many years of experience in finance and business administration. He is currently the Deputy Director of Department of Economics –Ministry of Defense.

3. Mr. le van BeVice Chairman

Mr. Le Van Be is the Vice Chairman cum CEO of MB. He held various positions in finance management at the Ministry of Defense and was directly involved in the establishment of MB. He has demonstrated excellent leadership over the past MB’s 15- year history, and has led the Bank to gain a firm foothold in Vietnam’s financial market. He pays special attention to the MB’s corporate culture and considers it as a key factor in internal solidarity, contributing to the Bank’s success. Currently, Mr. Le Van Be is also the Chairman of Thang Long Securities Company (TSC), Hanoi Fund Management (HFM) and Asset Management Company (AMC).

4. Mr. le van daoMember

Mr. Le Van Dao holds a Master of Economics from the Vietnam Maritime University. He was appointed to many important positions such as Director of Saigon Military Port, Vice Admiral of the Vietnamese Naval Force etc. Mr. Dao brings with him, more than 3 decades of management experience including 6 years in financial and banking industry.

5. Ms. nguyen thi BaoMember

Ms. Nguyen Thi Bao holds a Bachelor Degree in Economics from the Foreign Trade University of Vietnam and a Master Degree from Vietnam -Belgium Program (the cooperation between Université Libre de Bruxelles and Vietnam National University of Economics). Ms. Bao has extensive experiences in the financial and banking industry with more than three decades working at Vietcombank. Prior to her appointment as Deputy Director of Transaction Office, she was the Vice Manager of Investment & Guarantee Department, Head of Credit Department, and Head of Appraisal & Stock Investment Department of Vietcombank.

6. Mr. dau Quang lanhMember

Mr. Dau Quang Lanh holds a Master of Economics from Vietnam National University of Economics. Mr. Lanh held many management positions in finance and business administration. He is now the Director General of Garment 28 Corporation.

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 31

The Supervisory Board monitors the Bank’s financing activities, supervises the compliance with auditing and

accounting procedures, in addition to activities of the internal checking and supervising system.

SUPERVISORY BOARD

1 2 3 4

1. Mr. nguyen dinh KhamChief Supervisor

Mr. Nguyen Dinh Kham brings with him 53 years of experiences in the financial & banking industry. Prior to taking the office as Chief Supervisor for MB, Mr. Kham held various positions in the Bureau of Finance under the Ministry of Defense.

2. Mr. nguyen Xuan truongMember

Prior to becoming a member of the Supervisory Board in 2005, Mr. Nguyen Xuan Truong was the Vice Chairman of MB’s Board of Directors from 1994 to 2005, and held important financial management positions in the Ministry of Defense.

3. Mr. nguyen tien hungMember

Graduating from the Academy of Finance, Mr. Hung has years of experiences holding financial auditing positions for enterprises, including foreign joint-venture firms. Since October 2002, Mr. Hung held the position as Chief Accountant and Deputy Director of Tay Ho Company.

4. Ms. le thi duonMember

Graduating from the Academy of Finance, Ms. Le Thi Duon held positions as the Vice Director for the Information Equipment Factory No. 1, Vietnam Data-Communication Company and Management Committee for Hanoi Fiber Optic Cable. She was also a Member of the Supervisory Board for VNPT’s Board of Management, Member for the Board of Management and Director VNPT Insurance Company. In 2005, she officially became MB’s Supervisory Board Member.

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 33

Bod and SuperviSory Board aCtivitieS

Activities of the Board of Directors

As elected representatives for the Bank’s shareholders, the Board of Directors is duly authorized by the shareholders to make decisions within its authority. The Board of Directors appoints a Standing Board that oversees the Bank’s operation and timely handle issues beyond the authority of the Chief Executive Officer. In 2008, the Board of Director and the Standing Board closely directed the Board of Executives to successfully complete the 2008 plan. They also established procedures and operation regulations to ensure legal compliance and efficiency.

Activities of the Supervisory Board

The Supervisory Board monitors the Bank’s financing activities, supervises the compliance with auditing and accounting procedures, in addition to activities of the internal checking and supervising system.

Senior Committees under the Board of Directors

Credit and Investment Committee: Reviews, comments and reports on credit and investment issues that are beyond the CEO’s authority to the Standing Board.

Personnel and Compensation Policy Committee: Reviews, comments and submits personnel issues such as appointment, dismissal, transfer and lay-off positions; compensation packages, bonuses and discipline policies; related personnel regulations to the Standing Board

Risk Management Committee: Decides on risk management issues and risk mitigation policies. Reviews and reports directly to the Standing Board to carry out risk process using the Risk Provision Fund.

Financial Committee: Reviews and reports directly to the Standing Board on financial decisions, including fixed assets and equipment purchases that are beyond the CEO’s authority.

Rights of Members of Board of Directors: Members of the Board of Directors are not allowed to engage in any business transactions, whereas their rights or benefits are against direct or indirect those of MB’s.

Repeat voting of at least one third of the Board of Directors and the Supervisory Board

There was no repeat voting of at least one third of Board of Management and Supervisory Board in 2008.

Remuneration of the Members of Board of Directors and of Supervisory Board

Remuneration of the Members of Board of Directors and the Supervisory Board is approved and revised annually by the Shareholder’s Meeting.

Updates on stakes of Board of Directors’ members

Name

Ownership percentageas of

31/12/2007

Ownership percentage as of 31/12/2008

Truong Quang Khanh 0% 0,019%

Pham Viet Thich 0,06% 0,054%

Le Van Be 0,30% 0,229%

Le Van Dao 0,01% 0,012%

Dau Quang Lanh 0,02% 0,017%

Nguyen Thi Bao 0% 0%

StatiStiCS of ShareholderS

Local ShareholdersDetailed information

Detailed information of major shareholdersUp to 31 December 2008, MB has 3 major shareholders (owning 5% or above).

Changes in stake holding by Major Shareholders

Shareholder Number of Shareholders Number of shares Stake

Individual 7,875 167,423,401 49.24%

Institutional 98 172,576,599 50.76%

Total 7,973 340,000,000 100%

Name Address Business ScopeNumber of

sharesPercentage of

Ownership

Flight Service Corporation 172 Truong Chinh Street, Hanoi

Flight Services 40,771,646 11.99%

Viettel Corporation No. 1 Giang Van Minh, Hanoi Telecomunication Services

34,000,000 10%

Vietcombank 198 Tran Quang Khai, Hanoi Banking Services 27,160,058 7.99%

Name Address

Percentage of ownership up to

31/Dec/2007

Percentage of ownership up to

31/Dec/2008

Vietnam Flight Service Corporation 172 Truong Chinh Street, Hanoi 14.21% 11.99%

Viettel Corporation No. 1 Giang Van Minh, Hanoi 0% 10%

Vietcombank 198 Tran Quang Khai, Hanoi 6.31% 7.99%

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 35

Financial Statements

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 37

ContentS

Page

REPORT OF THE BOARD OF DIRECTORS ............................................................................................................38 - 40

INDEPENDENT AUDITORS’ REPORT .......................................................................................................................... 41

AUDITED CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED BALANCE SHEET ......................................……………………………………………………42 - 44

CONSOLIDATED INCOME STATEMENT .....................................................................................................................45

CONSOLIDATED STATEMENT OF RETAINED EARNINGS .........................................................................………46

CONSOLIDATED STATEMENT OF CASH FLOWS ...............................................................................................47 - 48

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS …………………………………….....……..49 - 92

The Board of Directors of Military Commercial Joint Stock Bank (“the Bank”) is pleased to present its report and the consolidated financial statements of the Bank for the year ended 31 December 2008.

the BanK

Military Commercial Joint Stock Bank (herein referred to as “the Bank”) is a commercial joint stock bank incorporated and registered in the Socialist Republic of Vietnam.

The Bank was established in accordance with the Business Licence No. 0054/NH-GP of the State Bank of Viet Nam granted on 14th September, 1994 and Decision No. 00374/GP-UB by the Hanoi People’s Committee. The operational duration under the license is fifty (50) years and the Bank operated officially on 4th November 1994.

The Bank has been established to provide banking services including receiving short, medium and long-term deposits from organizations and individuals; making short, medium and long-term loans and advances to organizations and individuals based on the nature and capability of the bank’s sources of capital; also including foreign exchange transactions, international trade financial services, discount of commercial papers, bonds and other valuable papers, and providing other banking services allowed by the State Bank of Vietnam.

The Head Office of Military Commercial Joint Stock Bank is located at No. 3 Lieu Giai Street, Ba Dinh District, Hanoi, Vietnam. As at 31 December 2008, the Bank has one (1) Head Office, one (1) Operation Center, three (3) subsidiaries, thirty four (34) branches and fifty four (54) transaction offices located in cities and provinces all over Vietnam.

ConSolidated reSultS and dividendS

Current yearVNDm

Previous yearVNDm

Net profit for the year 703,368 491,683Dividend paid during the year 763,774 55,136Retained earnings at the end of the year 288,766 537,732

Board of direCtorS

The members of the Board of Directors during the financial year 2008 are as follows:

full name title date of appointment/re-appointmentMr. Truong Quang Khanh Chairman appointed on 26 June 2008Mr. Pham Tuan Chairman resigned on 26 June 2008Mr. Pham Viet Thich Vice Chairman appointed on 16 June 2005Mr. Le Van Be Vice Chairman appointed on 16 June 2005Mr. Le Van Dao Member appointed on 16 June 2005Mr. Dau Quang Lanh Member appointed on 16 June 2005Ms. Nguyen Thi Bao Member appointed on 16 June 2005

report of the Board of direCtorS

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 39

audit CoMMittee

The members of the audit committee during the financial year 2008 are as follows:

full name title date of appointment/re-appointmentMr. Nguyen Dinh Kham Chief Appointed on 16 June 2005 Mr. Nguyen Tien Hung Member Appointed on 16 June 2005Mr. Nguyen Xuan Truong Member Appointed on 16 June 2005Ms. Le Thi Duon Member Appointed on 16 June 2005

eventS SinCe the BalanCe Sheet date

There have been no significant events occurring after the balance sheet date which would require adjustments or disclosures to be made in the consolidated financial statements.

auditorS

The auditors, Ernst & Young Vietnam Limited, have expressed their willingness to accept reappointment.

StateMent of the ManaGeMent’S reSponSiBility of the BanK’S in reSpeCt of the ConSolidated finanCial StateMentS

The Board of Management of the Bank is responsible for the consolidated financial statements of year 2008 which give a true and fair view of the state of affairs of the Bank and of its results and cash flows for the year. In preparing those consolidated financial statements, the Board of Management is required to:

select suitable accounting policies and then apply them consistently;►

make judgments and estimates that are reasonable and prudent; ►

state whether applicable accounting standards have been followed, subject to any material departures disclosed ►and explained in the consolidated financial statements; and

prepare the consolidated financial statements on the going concern basis unless it is inappropriate to presume that ►the Bank will continue in business.

The Board of Management of the Bank is responsible for ensuring that proper accounting records are kept which disclose, with reasonable accuracy at any time, the financial position of the Bank and to ensure that the accounting records comply with the registered accounting system. It is also responsible for safeguarding the assets of the Bank and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

The Board of Management of the Bank has confirmed to the Board of Directors that the Bank has complied with the above requirements in preparing the accompanying consolidated financial statements.

report of the Board of direCtorS (continued)

approval of the ConSolidated finanCial StateMentS

We hereby approve the accompanying consolidated financial statements which give a true and fair view of the financial position of the Bank as at 31 December 2008 and the results of its operations and cash flows for the year then ended in accordance with the Vietnamese Accounting Standards and Accounting System for Credit Institutions and comply with other relevant regulations by State Bank of Vietnam and Ministry of Finance.

On behalf of the Board of Directors

Mr. Le Van BeStanding Vice Chairman

Hanoi, Vietnam31 March 2009

report of the Board of direCtorS (continued)

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 41

to: Board of directors and Board of Management of Military Commercial Joint Stock Bank

We have audited the consolidated balance sheet of Military Commercial Joint Stock Bank (“the Bank”) and its subsidiaries as at 31 December 2008, and the consolidated income statement and consolidated statement of cash flows for the year then ended and the notes thereto as set out on pages 5 to 55 (collectively referred to as “the consolidated financial statements”). These consolidated financial statements are the responsibility of the Bank’s management. Our responsibility is to express an opinion on these consolidated financial statements based on our audit. The consolidated financial statements of the Bank for the year ended 31 December 2007 were audited by another auditors whose report dated 15 April 2008 expressed an un-qualified opinion on those consolidated financial statements.

Basis of Opinion

We conducted our audit in accordance with Vietnamese and International Standards on Auditing applicable in Vietnam. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the consolidated financial statements. An audit also includes assessing the accounting principles used and significant estimates made by the Board of Management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provides a reasonable basis for our opinion.

Opinion

In our opinion, the consolidated financial statements, in all material aspects, give a true and fair view of the financial position of the Bank as at 31 December 2008 and of its financial performance and its cash flows for the year then ended in accordance with the Vietnamese Accounting Standards and Accounting System for Credit Institutions and comply with other relevant regulations by State Bank of Vietnam and Ministry of Finance.

Ernst & Young Vietnam Limited

Vo Tan Hoang Van Nguyen Phuong Nga Deputy General Director Auditor in-charge Registered Auditor Registered Auditor Certificate No. 0264/KTV Certificate No. 0763/KTV

Hanoi, Vietnam31 March 2009

independent auditorS’ report Reference: 60755036/13547778

Notes2008

VNDm2007

VNDm

aSSetCash and cash equivalents 3 411,633 352,321Balances with the State Bank of vietnam (“the SBv”) 4 515,139 191,318due from banks 5 16,010,231 14,014,064trading securities 150,175 290,547

Trading securities 6 208,878 297,058 Provision for impairment of trading securities 11 (58,703) (6,511)

loans and advances to customers 15,493,509 11,468,799 Loans and advances to customers 7 15,740,426 11,612,575Provision for loans to customers 8 (246,917) (143,776)

investment securities 9 8,477,960 1,675,726Investment securities - available for sale 9.1 6,053,818 373,101 Investment securities - held to maturity 9.2 2,542,981 1,302,625 Provision for impairment of investment securities 11 (118,839) -

long-term investments 10 1,180,427 811,115Investments in associates 10.1 68,783 4,125 Other long-term investments 10.2 1,362,321 806,990 Provision for impairment of long-term investments 11 (250,677) -

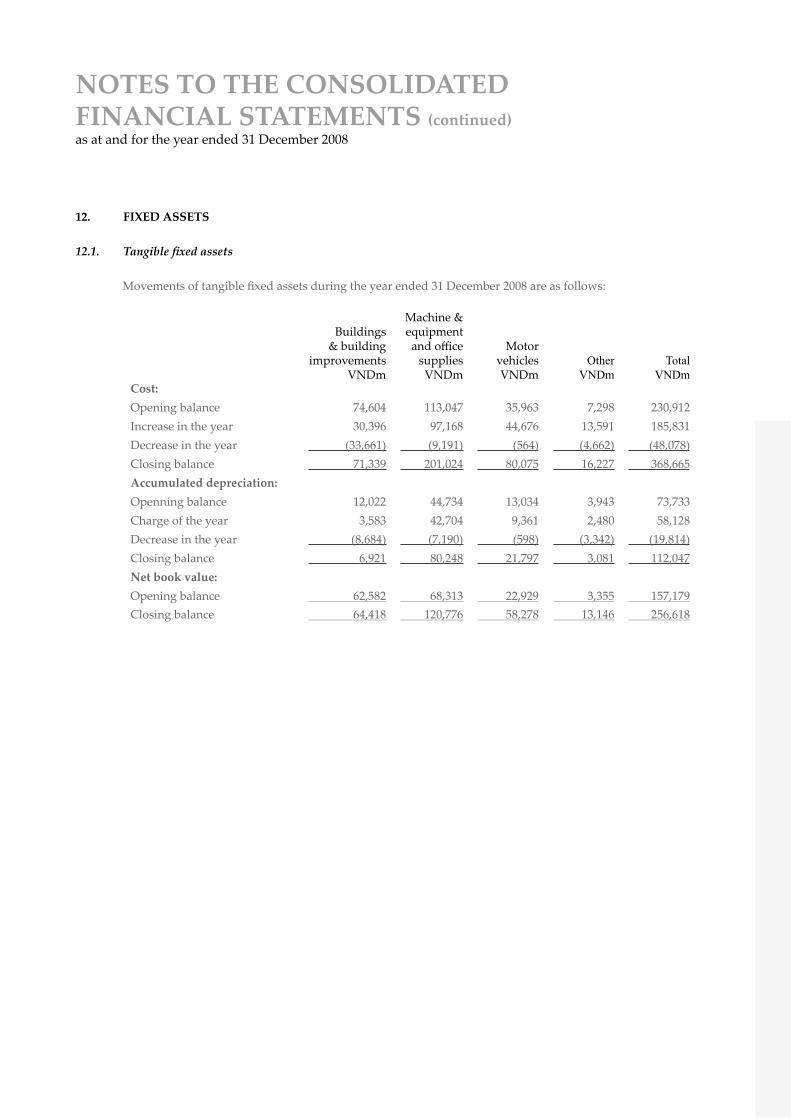

fixed assets 12 629,394 234,445Tangible fixed assets 12.1 256,618 157,179 Cost 368,665 230,912 Accumulated depreciation (112,047) (73,733)Intangible assets 12.2 372,776 77,266 Cost 389,652 86,200 Accumulated amortization (16,876) (8,934)

investment property 13 515,906 114,838Cost 516,071 115,267 Accumulated depreciation (165) (429)

other assets 961,732 470,409 Interest receivables 702,673 190,575 Construction in progress 17,955 10,065 Accounts receivable 14 149,675 131,107 Other assets 91,429 138,662

total aSSetS 44,346,106 29,623,582

ConSolidated BalanCe Sheet as at 31 December 2008

The accompanying notes from 1 to 38 form part of these consolidated financial statements

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 43

Notes2008

VNDm2007

VNDm

liaBilitieSBorrowings from the Government and the SBv - 68,547due to banks 15 8,531,866 4,992,934due to customers 16 27,162,881 17,784,837other borrowed funds 17 834,361 290,126valuable papers issued 18 2,137,326 2,020,000other liabilities 1,003,019 917,272

Interest payables 403,425 258,187Tax payables 21 80,989 89,086Other payables 19 401,765 516,434Provision for off-balance sheet commitments 20 116,840 53,565

total liaBilitieS 39,669,453 26,073,716

ownerS’ eQuityCapital and reservesCapital 22 3,939,725 2,815,946

Chartered capital 3,400,000 2,000,000Share premium 30,200 306,421Other capitals 509,525 509,525

Reserves 22 195,573 125,843Retained earnings 22 288,766 537,732Minority interest 22 252,589 70,345

total liaBilitieS, ownerS’ eQuity and Minority intereSt 44,346,106 29,623,582

ConSolidated BalanCe Sheet (continued)as at 31 December 2008

The accompanying notes from 1 to 38 form part of these consolidated financial statements

off-BalanCe Sheet iteMS

Notes2008

VNDm2007

VNDm

Financial guarantees 3,726,792 2,788,197 Letters of credit 10,124,777 10,196,649 Undrawn loan commitments 2,523,628 850,403 total off-BalanCe Sheet CoMMitMentS 33 16,375,197 13,835,249

Prepared by Approved by Approved by

Ms. Nguyen Thu HuongDeputy Head of Accounting

Department

Ms. Pham Thi TyChief Finance Officer

Mr. Le Van BeChief Executive Officer

Hanoi, Vietnam31 March 2009

ConSolidated BalanCe Sheet (continued)as at 31 December 2008

The accompanying notes from 1 to 38 form part of these consolidated financial statements

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 45

Notes2008

VNDm2007

VNDm

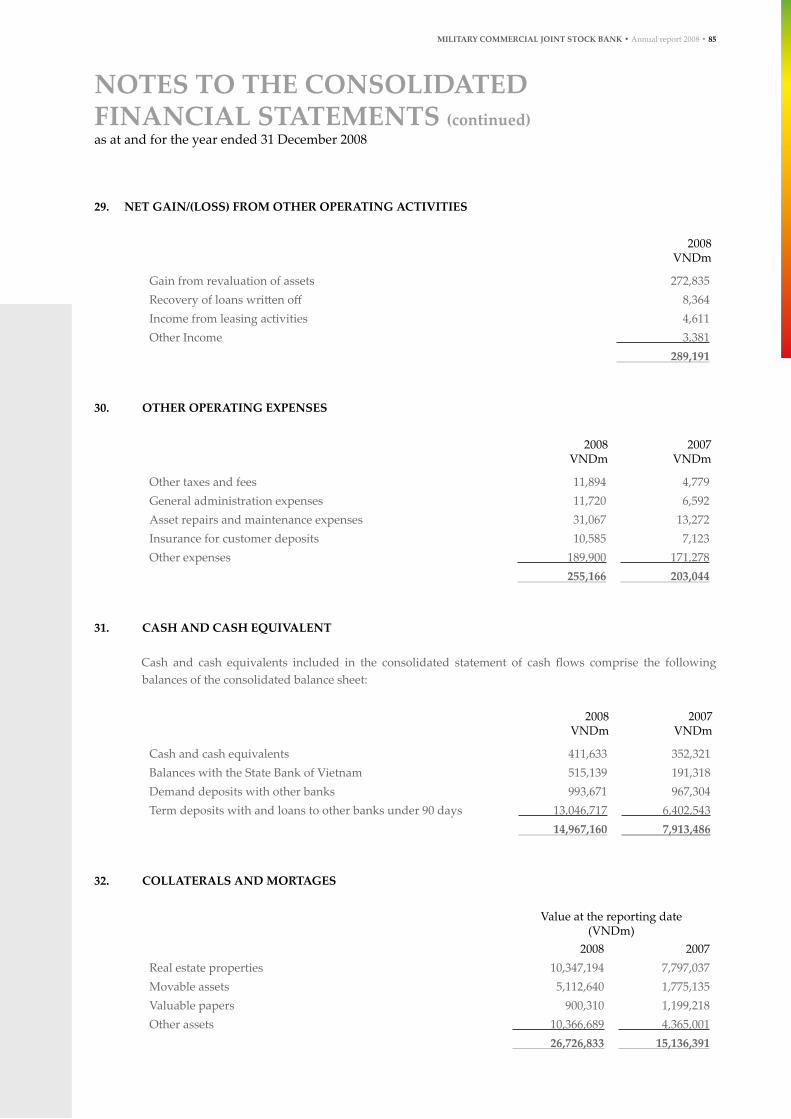

Interest and similar income 24 3,679,299 1,581,122 Interest and similar expenses 25 (2,258,587) (947,805)NET INTEREST INCOME 1,420,712 633,317 Fees and commission income 261,986 204,905 Fees and commission expenses (70,778) (13,190)net fees and commission income 26 191,208 191,715 net gain/(loss) from foreign currencies trading 27 101,403 21,124 net gain/(loss) from trading and investment securities 28 (167,710) 83,067 net gain/(loss) from other operating activities 29 289,191 90,842 net share of profit from investments in associates (1,029) - provision for impairment of long-term investments 11 (250,677) - dividend income 54,986 34,367 total operatinG inCoMe 1,638,084 1,054,432

operatinG eXpenSeSPersonnel expenses (234,025) (118,146)Depreciation and amortization of fixed assets 12 (66,247) (39,695)Other operating expenses 30 (255,166) (203,044)total operatinG eXpenSeS (555,438) (360,885)

Profit before provision for credit losses 1,082,646 693,547

Provision for credit losses 8 (158,488) (40,845)Provision for off-balance sheet commitments 20 (63,275) (43,716)profit Before taX 860,883 608,986 Current enterprise income tax 21 (164,678) (116,378)Deferred income tax expense 21 - - profit for the year 696,205 492,608 Minority interest (7,163) 925 net profit for the year 703,368 491,683 Basic earning per share (VND/share price of 10,000 VND each) 22.3 3,173 4,187 Diluted earning per share (VND/share price of 10,000 VND each) 22.3 2,366 3,073

Prepared by Approved by Approved by

Ms. Nguyen Thu HuongDeputy Head of Accounting

Department

Ms. Pham Thi TyChief Finance Officer

Mr. Le Van BeChief Executive Officer

Hanoi, Vietnam31 March 2009

ConSolidated inCoMe StateMentfor the year ended 31 December 2008

The accompanying notes from 1 to 38 form part of these consolidated financial statements

Notes2008

VNDm2007

VNDm

RETAINED EARNINGS AT THE BEGINNING OF THE YEAR 22.1 537,732 195,854Net profit for the year 703,368 491,683RETAINED EARNINGS BEFORE APPROPRIATIONS 1,241,100 687,537- Increased share capital (373,579) - - Additional creation of reserves for prior year (140,902) (94,884)- Temporary creation of reserves for current year (28,187) - - Dividend paid in advance for current year (400,014) - - Dividend paid for prior years (7,302) (55,136)- Additional taxes paid as a result of tax assessments (2,350) - - Others - 215 retained earninGS at the end of the year 22.1 288,766 537,732

Prepared by Approved by Approved by

Ms. Nguyen Thu HuongDeputy Head of Accounting

Department

Ms. Pham Thi TyChief Finance Officer

Mr. Le Van BeChief Executive Officer

Hanoi, Vietnam31 March 2009

ConSolidated StateMent of retained earninGSfor the year ended 31 December 2008

The accompanying notes from 1 to 38 form part of these consolidated financial statements

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 47

Notes2008

VNDm2007

VNDm

operatinG aCtivitieSInterest and similar income receipts 3,167,201 1,475,665 Interest and similar expense payments (2,113,348) (821,113)Fees and commission income receipts 261,987 204,905 Fees and commission expense payments (70,778) (13,190)Receipts from foreign currency trading 101,403 21,124 Receipts from investment securities trading 3,321 89,552 Net gain/(loss) from other operating income 7,992 90,842 Recovery from written-off bad debts 8,364 - Payments to employees (219,715) (118,146)Payments to other operating activities (252,634) (202,987)Enterprise income tax paid in the year 21 (176,687) (50,056)

net cash flows from operating activities before changes in operating assets and liabilities 717,106 676,596

Changes in operating assets(Increase)/decrease in due from banks 4,674,374 (4,595,406)(Increase)/decrease in loans and advances to customers (4,183,198) (5,673,595)((Increase)/decrease in other assets 18,243 (179,603)Changes in operating liabilitiesIncrease/(decrease) in borrowings from the Government and the SBV (68,547) 38,547 Increase/(decrease) in due to banks 3,538,932 3,821,704 Increase/(decrease) in due to customers 9,378,044 7,472,218 Increase/(decrease) in other borrowed funds 544,235 201,558 Increase/(decrease) in other liabilities (237,709) 278,947 Reserves utilized in the year (94,139) (48,249)net cash flows from operating activities 14,287,341 1,992,717 inveStinG aCtivitieS(Increase)/decrease in fixed assets (168,371) (112,676)(Increase)/decrease in long-term investments (618,296) (595,694)(Increase)/decrease in trading securities 88,180 34,332 (Increase)/decrease in investment securities (6,921,073) (1,807,272)Purchase of investment property (400,804) (97,808)Dividend receipts in the year 52,264 34,367 net cash flows from investing activities (7,968,100) (2,544,751)

ConSolidated StateMent of CaSh flowS for the year ended 31 December 2008

The accompanying notes from 1 to 38 form part of these consolidated financial statements

Notes2008

VNDm2007

VNDm

finanCinG aCtivityIncrease/(decrease) in chartered capital in cash 22.1 530,200 1,203,625 Increase/(decrease) from issuing bonds 337,326 2,309,525 Shares issued to minority interest 185,000 66,000 Dividends paid to shareholders (318,205) (55,136)Increase/(decrease) of reserves 112 581 net cash flows from financing activities 734,433 3,524,595 net increase/(decrease) in cash and cash equivalents 7,053,674 2,972,561 Cash and cash equivalents at beginning of the year 31 7,913,486 4,940,925 Cash and cash equivalents at the end of the year 31 14,967,160 7,913,486

Prepared by Approved by Approved by

Ms. Nguyen Thu HuongDeputy Head of Accounting

Department

Ms. Pham Thi TyChief Finance Officer

Mr. Le Van BeChief Executive Officer

Hanoi, Vietnam 31 March 2009

ConSolidated StateMent of CaSh flowS (continued)for the year ended 31 December 2008

The accompanying notes from 1 to 38 form part of these consolidated financial statements

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 49

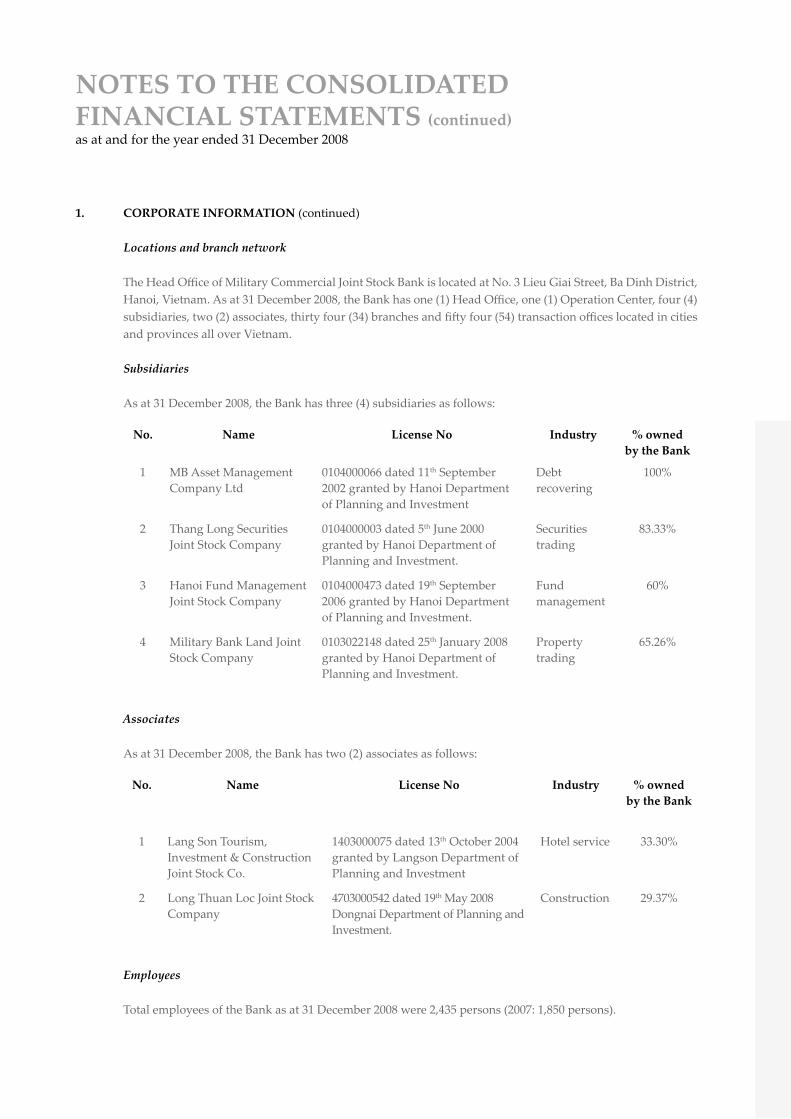

1. Corporate inforMation

Military Commercial Joint Stock Bank (herein referred to as “the Bank”) is a commercial joint stock bank incorporated and registered in the Socialist Republic of Vietnam.

Establishment and Operations

The Bank was established in accordance with the Business Licence No. 0054/NH-GP of the State Bank of Viet Nam granted on 14th September, 1994 and Decision No. 00374/GP-UB by the Hanoi People’s Committee. The operational duration under the license is fifty (50) years and the Bank operated officially on 4th November 1994.

The Bank has been established to provide banking services including receiving short, medium and long-term deposits from organizations and individuals; making short, medium and long-term loans and advances to organizations and individuals based on the nature and capability of the bank’s sources of capital; also including foreign exchange transactions, international trade financial services, discount of commercial papers, bonds and other valuable papers, and providing other banking services allowed by the State Bank of Vietnam.

Chartered Capital

The original chartered capital of the Bank was VNDm 20,000 in 1994 and subsequently supplemented for each period under the approval of the shareholders. The chartered capital as at 31 December 2008 was VNDm 3,400,000 (2007: VNDm 2,000,000).

Board of Management

The members of the Board of Management during the financial year 2008 are as follows:

name position date of appointment/re-appointmentMr. Le Van Be Chief Executive Officer Appointed on 16 October 1995 Mr. Le Cong Deputy General Director Appointed on 21 April 1997Mr. Dang Quoc Tien Deputy General Director Appointed on 07 May 2002Mr. Le Van Minh Deputy General Director Appointed on 01 October 2002Mr. Do Van Hung Deputy General Director Appointed on 18 October 2005Ms. Cao Thi Thuy Nga Deputy General Director Appointed on 01 January 2006Ms. Vu Thi Hai Phuong Deputy General Director Appointed on 11 June 2007Mr. Luu Trung Thai Deputy General Director Appointed on 15 April 2008Ms. Pham Thi Ty Chief Financial Director Appointed on 14 November 2005

noteS to the ConSolidated finanCial StateMentS as at and for the year ended 31 December 2008

1. Corporate inforMation (continued)

Locations and branch network

The Head Office of Military Commercial Joint Stock Bank is located at No. 3 Lieu Giai Street, Ba Dinh District, Hanoi, Vietnam. As at 31 December 2008, the Bank has one (1) Head Office, one (1) Operation Center, four (4) subsidiaries, two (2) associates, thirty four (34) branches and fifty four (54) transaction offices located in cities and provinces all over Vietnam.

Subsidiaries

As at 31 December 2008, the Bank has three (4) subsidiaries as follows:

no. name license no industry % owned by the Bank

1 MB Asset Management Company Ltd

0104000066 dated 11th September 2002 granted by Hanoi Department of Planning and Investment

Debt recovering

100%

2 Thang Long Securities Joint Stock Company

0104000003 dated 5th June 2000 granted by Hanoi Department of Planning and Investment.

Securities trading

83.33%

3 Hanoi Fund Management Joint Stock Company

0104000473 dated 19th September 2006 granted by Hanoi Department of Planning and Investment.

Fund management

60%

4 Military Bank Land Joint Stock Company

0103022148 dated 25th January 2008 granted by Hanoi Department of Planning and Investment.

Property trading

65.26%

Associates

As at 31 December 2008, the Bank has two (2) associates as follows:

no. name license no industry % owned by the Bank

1 Lang Son Tourism, Investment & Construction Joint Stock Co.

1403000075 dated 13th October 2004 granted by Langson Department of Planning and Investment

Hotel service 33.30%

2 Long Thuan Loc Joint Stock Company

4703000542 dated 19th May 2008 Dongnai Department of Planning and Investment.

Construction 29.37%

Employees Total employees of the Bank as at 31 December 2008 were 2,435 persons (2007: 1,850 persons).

noteS to the ConSolidated finanCial StateMentS (continued) as at and for the year ended 31 December 2008

Military CoMMerCial Joint StoCk Bank • Annual report 2008 • 51

2. SiGnifiCant aCCountinG poliCieS

2.1 Accounting standards and system

Statement of compliance with Vietnamese Accounting Standards and Accounting System for credit institutions

The Board of Management of the Bank states that accompanying consolidated financial statements have been prepared in compliance with Vietnamese Accounting Standards and Accounting System for Credit Institutions.

Basis of presentation

The consolidated financial statements of the Bank, which are expressed in millions of Vietnamese Dong (“VNDm”), are prepared in accordance with Accounting System for Credit Institutions required under Decision No. 479/2004/QD-NHNN issued on 29 April 2004 by the Governor of the State Bank of Vietnam which was enacted from 1 October 2004; Decision No. 16/2007/QD-NHNN issued on 18 April 2007 by the Governor of the State Bank of Vietnam; Vietnamese Accounting Standards and related regulations issued by the Ministry of Finance as:

Decision No. 149/2001/QD-BTC dated 31 December 2001 on the Issuance and Promulgation of Four ►Vietnamese Standards on Accounting (Series 1);

Decision No. 165/2002/QD-BTC dated 31 December 2002 on the Issuance and Promulgation of Six ►Vietnamese Standards on Accounting (Series 2);

Decision No. 234/2003/QD-BTC dated 30 December 2003 on the Issuance and Promulgation of Six ►Vietnamese Standards on Accounting (Series 3);