CER March 2014

52

Regulatory surprises await Regulatory surprises await Chinese miners in Greenland Chinese miners in Greenland Q&A: A state-owned hospitality Q&A: A state-owned hospitality giant turns to the middle class giant turns to the middle class Overpriced and overcrowded Overpriced and overcrowded Small store owners struggle to Small store owners struggle to build brands on Tabao and Tmall build brands on Tabao and Tmall 中经评论:新消费时代 中经评论:新消费时代 www.chinaeconomicreview.com MARCH 2014 VOL. 25, NO. 3 BUSINESS EDUCATION

description

China Economic Review 中经评论

Transcript of CER March 2014

Regulatory surprises await Regulatory surprises await Chinese miners in GreenlandChinese miners in Greenland

Q&A: A state-owned hospitality Q&A: A state-owned hospitality giant turns to the middle classgiant turns to the middle class

Overpriced and overcrowdedOverpriced and overcrowdedSmall store owners struggle to Small store owners struggle to

build brands on Tabao and Tmallbuild brands on Tabao and Tmall

中经评论:新消费时代中经评论:新消费时代

www.chinaeconomicreview.comMARCH 2014 VOL. 25, NO. 3

BUSINESS

EDUCATION

MARCH 2014VOL. 25, NO. 3FEATURED CONTENT

MONTH IN REVIEW8 NEWS BRIEF | Th e biggest China news stories in February

COVER STORY14 OVERPRICED AND OVERCROWDED | Small online stores struggle to build brands on Taobao and Tmall

MARKETS & FINANCE30 UPWARD PRESSURE | Retail investors are leading grassroots fi nancial reform32 CLOSED BOOKS | US regulators are engaged in a fi ght with China they can never win

BUSINESS 26 THE CRACKS WIDEN | Declining property prices in smaller cities are a real risk for investors this year27 FROZEN FRONTIER | Chinese companies entering Greenland face an unfamiliar regulatory surprise29 STUDY ABROAD | Tourists can learn a few things overseas

ECONOMICS & POLICY

18 RECLAIMING THE GHOST TOWNS | Ordos is fi nally fi guring out how it can bring in people to fi ll its empty houses20 AVOIDING THE TAPERING TIDE | China will ride it out22 NOT AGAIN | January trade data is not necessarily fake24 HEALTHIER SERVING | A major change to agricultural policy underscores that the people’s demand for better food is being heard

Q&A10 TURNING TO THE MASSES | A state-owned hospitality group switches focus from public offi cials to the middle class12 BUSINESS AS NORMAL | As China becomes a more mature market, US fi rms will need to adjust

MARCH 2014 VOL. 25, NO. 3

HKABC membership approved and certifi ed

Published monthly since 1990

PublisherChina Economic Review Publishing

EditorOliver Pearce

Staff WriterDon Weinland

Chinese EditorLiu Chen

Associate EditorBrenda Yang

InternsMiljan Glenny, Greg Isaacson, Skye Sun,

Winkie Zhang, Sean Lee

Art DirectorJason Wong

Editor at LargeGraham Earnshaw

Associate PublisherGareth Powell

Director of Sales and MarketingPierre Zolghardi

Account ManagersRalph Wang, Jerry Cheng

CHINA ECONOMIC REVIEW

(ISSN: 1350-6390) is published by

China Economic Review Publishing

Enquiries [email protected]

AddressesThe Plaza Building, 102 Lee High Road

London, SE13 5PT, England

Room 1801, 18F

Public Bank Centre

120 Des Voeux Road

Central, Hong Kong

Hong Kong printer01 Printing Limited

Suite M, 3/F, Tower 3,

Kwun Tong Industrial Centre,

448 Kwun Tong Road, Kowloon

CHINA ECONOMIC REVIEW welcomes

letters. Please write to the editor at:

HKABC membership approved and certifi ed

Advertising enquiries

Hong Kong: +852 3174 6136

Shanghai: +8621 5187 9633 ext 811

THE HOUSE VIEW05 KEEP ON CLEANING | Environmental progress should spur Beijing to press on with its green plans06 HANDS ON THE PUMP | While markets shouldn't panic over January’s high credit rollout, there is some reason to worry

No creature represents the power and symbolism of China’s ties to nature and

the land quite like the horse. For centuries, strong steeds helped farm-ers feed the nation.

Even so, perhaps it is no more than sheer coincidence that just as the people of China settled down to usher in the Year of the Horse, some good news regarding the country’s torrid pollution was highlighted by a leading environmental report.

The 2014 edition of the annual Environmental Performance Index, compiled by US-based Yale and Co-lumbia universities, said China had made huge strides in slowing the growth of its greenhouse gas emis-sions in the past decade.

“Despite high economic expan-sion averaging greater than 10% an-nual growth in GDP, China reported a 20% decrease in carbon intensity between 2005 and 2010,” the report noted. This is the amount of carbon emitted for each unit of economic growth.

Reducing the speed at which the world’s largest industrial nation is

pumping harmful gases into the atmo-sphere may not be the same as actually reducing overall emissions, the crite-rion by which rich nations are judged, but it is a start. The report’s authors are optimistic that the policies that de-livered this deceleration will continue to bear fruit and may one day lead China to actually reduce emissions.

Under its 12th five-year economic plan, running 2011-2015, China vowed to reduce carbon intensity by 16-17% from 2005 baselines levels, with a longer-term goal of 40-45% reductions by 2020. That target may even be tightened in future plans.

“Although it is too soon to tell how effective these early steps will be, China’s performance … demon-strates the tangible results of policies implemented over the last few years that have helped to reduce energy and carbon intensity,” the report said.

This doesn’t mean that China has made similar progress in other environmental areas. It hasn’t. Heavy smog engulfed Shanghai, these days primarily a services hub, on the night before Chinese New Year. China Economic Review cycled past

Keep on cleaningcountless open incinerators burning household rubbish and highly pollut-ing tractors on country roads in Gui-lin province on a recent trip.

The index ranked China at the bottom globally in terms of air pollu-tion with most of its residents exposed to dangerously high levels of PM2.5, a fine particulate matter. Overall it came 118th out of 178 countries, far-ing poorly also on issues like water.

Even on carbon emissions China’s progress could be better. The target of a 16-17% reduction in carbon inten-sity by the end of 2015 from 2005 levels looks like it may not be met, judging by early results for the five-year period.

Failing on this front would under-mine all the small but important gains that China has made in improving its environmental record. Although the situation is dire, the country is tak-ing steps to curb emissions and has invested billions of dollars in clean energy products and services with the potential to be deployed anywhere in the world.

Pollution threatens the health of the people of China and undermines their quality of life – the very thing the Communist Party has staked its legitimacy on improving. Top officials have no excuses not to force the issue home at all levels of government.

One argument they frequently wheel out to defend their record is that economic development is still the priority in order to pull its people out of poverty, something the report agrees with. Yet as the chief economist of technology group Intel warned, if not tackled, bad air will undermine China’s future economic growth.

Green fields and clean skies are a sign of a better life; they also symbol-ize progress. China simply cannot af-ford to keep damaging its natural sur-roundings any longer. At the very least it must meet all of the environmental targets that it has set for itself.

Environmental progress should spur Beijing to press on with its green plans

THE HOUSE VIE W

SPOILT LANDSCAPE: China boasts many outstanding natural beauty spots but the countryside is rav-

aged by pollution and environmental damage. Slowly, however, there are signs of progress

Cre

dit

: A

nd

rew

Tu

rne

r

China Economic Review | March 2014 05

THE HOUSE VIE W

The good news is the gears that keep China’s economy turning were well-oiled in January as credit

expanded to an all-time high. The bad news is that such rapid growth in lend-ing has revived worries about the overall health of China’s banking sector.

New loans in January hit RMB1.32 trillion (US$217.6 billion), a four-year high. Total social financing, or TSF, Chi-na’s broadest measure of credit growth, reached a new record of RMB2.58 trillion, far ahead of the estimate of RMB1.9 tril-lion in a Bloomberg survey.

The figures are somewhat surpris-ing given the People’s Bank of China’s (PBOC) tightened stance on liquidity. Since last June, the central bank has sig-naled that it won’t allow runaway credit growth, especially in the face of heightened off-balance-sheet lending.

Markets shouldn’t react with alarm to the surge in credit growth. In the first month of the year new loans are usually high. Banks have just received new loan quotas and have backlogs of loan applica-tions from the year before. Many institu-tions will “front load” their loans, or loan as much as they can early on with the hope of generating more income on interest. The jump in lending a year ago was similar, al-though not quite as strong.

The data give some cause for worry, too. The percentage of new loans was high-er than off-balance-sheet lending, unlike in December. That means the ratio of lending that was being channeled into the shadow

banking sector was lower. Yet, off-balance-sheet lending hit RMB993 billion in Janu-ary, up from RMB555 billion in December. The figure was slightly lower than a year ago but shows that attempts to restrict the risky and opaque practice are failing.

Perhaps it takes an industry scare to fight shadow lending. New trust loans, one of the three main categories in off-balance-sheet lending, weakened compared to De-cember and the year before. China Credit Trust, a wealth management product (WMP) funded by trust loans, came to the brink of defaulting on payments, exposing their increasingly not-so-hidden risks.

At the same time, the remaining two categories of off-balance-sheet lending surged. Entrusted loans hit an all-time high at RMB396.5 billion. So did bank-

Hands on the pumpWhile there

is no need to

panic over

January’s high

credit rollout,

there is some

reason to

worry

The people of Fuzhou like their sea-

food. High-end restaurants in the

coastal city, the provincial capital of

Fujian, don’t skimp on the abalone

in their soups. During Chinese New

Year’s, no dinner is complete without

the free fl ow of Chinese spirits such as

baijiu.

But luxury eateries didn’t do well

in the early days of the Year of the

Horse. Neither did supermarkets and

vendors that sold fi ne seafood and li-

quors. In Fuzhou, sales for high-end

seafood gift sets dropped by 50%

year-on-year while fi ne spirit sales

sunk 70%, according to the Ministry of

Commerce.

After more than a year of party

boss Xi Jinping’s anti-corruption cam-

paign, which has gone after commu-

nist cadres with a taste for fi ne wine

and pricey watches, the steep slump

in sales of luxury products during the

holiday shouldn’t come as too great a

surprise.

Yet, while the best dining rooms

had empty banquet halls during the

seven-day break (revenues at Hei-

longjiang province’s best restaurants

fell by 20% compared to last year),

sales at mass-market venues surged

by 20% in several provinces.

That was the tone for Year-of-the-

Horse spending: Retail was strong but

for more modest goods.

National retail and catering rev-

enues during the weeklong holiday

increased by 13.3% year-on-year. That

was lower than last year’s 14.7% in-

crease but analysts have pointed out

that the offi cial national holiday this

year did not include New Year’s Eve,

China celebrates a less-corrupt Lunar New Year’s

GENTLY DOES IT: Bank lending needs to be kept in

check but too severe controls could disrupt credit fl ows

China Economic Review | March 201406

ers’ acceptances at RMB490 billion, indicating that investors still sought dangerous shadow products.

For those rooting for strong eco-nomic data this year, the jumpstart in credit might belie the true state of growth. Much of the lending in Janu-ary went to corporations looking to roll over loans. About 38% of new loans in January went to corporations. Compa-nies in China must repay US$427 bil-lion in principle and interest this year, almost a fifth higher than in 2013. The Chinese government might even let a couple of firms go bankrupt in 2014.

So, despite the record high TSF, not much was going into new projects, but rather propping up highly lever-aged companies. “Real investment

demand remains weak, as evidenced by slowing fixed-investment since Au-gust,” according to Mizuho Research.

The market is now looking to PBOC for some insight on the credit outlook for the rest of the year.

At the close of 2013, regulators at the central bank looked determined to rein in credit expansion at the cost of economic growth. While they still might be willing to make some sacri-fices, PBOC has lightened up a bit.

In the bank’s fourth quarter mon-etary report, it stressed “stability” and “overall planning.” That comes in sharp contrast to the cash crunches it engineered last year with the in-tent of sending a message home to banks that said “manage your balance

sheets better.” Barclays analysts said that PBOC’s self-described “prudent” policy stance can be tough to interpret and “at times this could mean tighten-ing, loosening, a neutral policy stance, or a neutral stance with a tightening or loosening bias.”

However, PBOC isn’t as hawk-ish as it wants banks to think. When central bankers tightened liquidity and sent interbank rates soaring in 2013, GDP was posting strong figures, in-flation was rising slowly and property prices were climbing rapidly. Things have changed. Growth is slowing at home, while tapering in the US has hit emerging markets and potentially their orders for Chinese goods.

The central bank will likely be more cautious going forward and lenders needn’t worry as much as last year over another major PBOC-de-signed squeeze in the money market. As Wang Tao, a Hong Kong-based economist at UBS, noted, the true risk now is the volatility of credit.

Last month the central bank put out new regulations on WMPs in the interbank market, one of several strat-egies to beat back off-balance-sheet funds. These kinds of regulations put sudden stoppages in the credit market. So would any full-on defaults in the shadow banking sector. If regulators come in with tougher measures, or credit defaults take the center stage, that will make for a highly unpredict-able credit supply during the rest of 2014 and likely hurt real growth.

commonly a night for big spending.

“People make big purchases and dine

out on the Lunar Year Eve,” Lu Ting,

China economist at Bank of America

Merrill Lynch, said in a report, noting

that the new holiday schedule could

have a material impact on holiday

spending fi gures.

The travel industry cashed in on

the break. National tourism revenues

soared by 16.4% year-on-year and air

passengers increased by nearly 20%,

according to China National Tourism

Administration. Chinese have typi-

cally returned home for the seven-day

break but increasing numbers are

now taking the opportunity to travel

abroad: 4.73 million overseas trips

were recorded this year, an 18.1% in-

crease over 2012.

Xi’s anti-corruption campaign

could even be pushing along holiday

spending, just not at the high end. As

offi cials and businesspeople cut back

on extravagant meals and gift-giving,

luxury restaurants and hotels are low-

ering prices.

“High-end restaurants and ho-

tels are seen offering discounts and

cheaper dishes” when their deep-

pocketed patrons stop spending, Bar-

clays Research said in a note. In this

sense, the corruption crackdown is

actually driving private consumption.

That probably wasn’t what Xi had in

mind when he launched the campaign

in late 2012. Nonetheless, it made for

nice holiday shopping for members of

China’s middle class, a group of peo-

ple always looking for more bang for

their buck and perpetually in the hunt

for a good deal.

THE HOUSE VIE W

China Economic Review | March 2014 07

NE WS ROUNDUP

MONTH IN REVIEWECONOMICSForeign direct investment (FDI) into China reached US$10.76 billion in January, an increase of 16.1% from a year earlier, according to a statement by the Ministry of Commerce. Min-istry spokesman Shen Danyang told a media briefing that the rising FDI shows that confidence in China’s economy remains firm even as growth cools. The majority of the new invest-ment, some US$6.33 billion, went into China’s services industry, while investment in manufacturing fell 21.7%. Investment from 10 Asian countries and regions rose 22.2% to US$9.55 billion, while investment from the US rose 34.9% to US$369 million.

China’s exports jumped 10.6% year-on-year in January, beating expec-tations across the board, The Wall Street Journal reported, citing data released by the General Administra-tion of Customs. This was up from December’s 4.3% rise and far above economists’ median forecast of a 0.1% expansion, according to a survey of 11 economists by The Wall Street

Journal. Imports rose 10% compared with a year ago, up from the 8.3% rise in December and beating the economists’ median forecast of a 3% increase. China’s trade surplus wid-ened in January to US$31.86 billion from US$25.6 billion in December, surpassing the median US$27.1 bil-lion forecast.

FINANCEChina’s new local-currency loans reached US$217.6 billion (RM217.6 billion) in January, the highest in about four years, Reuters reported, citing a statement by the People’s Bank of China. The January loans of Chinese banks beat a US$180 billion forecast and were nearly three times December’s level. It is usual for loans to spike in January when banks try to lend as much as they can to grab mar-ket share, but last month’s surge was unusually strong. The figures may assuage those who worry about Chi-na’s hazy economic outlook following recent data that showed conflicting trends.

The People’s Bank of China pub-lished rules governing investment by wealth management products (WMPs) in the country’s interbank bond market. The new rules, posted on the website of the central bank-backed National Interbank Funding Center, aim to curb the risks posed by banks’ off-balance-sheet business by forcing them to strictly segregate on- and off-balance-sheet assets. WMPs are short-term investment products that banks market to cus-tomers as higher-yielding alternatives

to traditional deposits. At the end of September, outstanding bank WMPs were RMB 9.9 trillion (US$1.63 tril-lion), according to official data.

China’s State Council has set grain output targets below domestic con-sumption rates, effectively aban-doning its long-standing grain self-sufficiency policy, Financial Times reported. The guidelines call for grain production to “stabilize” at rough-ly 550m tonnes by 2020, below the 2013 harvest of 602m tonnes. “While putting emphasis on food quantity, pay more attention to food safety and quality,” a document said, in a shift in tone and emphasis. A more liberal grains import policy was floated as a reform that might be adopted by President Xi Jinping, even before he became head of the Communist party in 2012.

POLITICS & SOCIETYChina saw an alarming rise of new cancer cases and deaths in 2012 amid a global rise of the disease, with the country registering the most new can-cer cases and deaths from four types of malignant tumors, South China

OPENING THE PUMPS: State-owned Sinopec is

welcoming private investment in its retail oil unit

Cre

dit

: L

ian

Ch

an

g

65

Number of years it took for the mainland and Taiwan to hold offi cial high-level talks

CHINA BY NUMBERS

Increase in Swiss luxury watch exports to China in December from a year earlier

18.8%

$217.6 billion

Size of local-currency loans in January, a four-year high

$19.5 billion

Value of polluting projects scrapped by the environment ministry

China Economic Review | March 201408

Morning Post reported. In the latest edition of the World Cancer Report, China accounted for 3.07 million newly diagnosed cases, 21.8% of the global total. China also saw around 2.2 million deaths, around 26.9% of the world’s total death rate. However, China is still not among the countries with the highest cancer rates or high-est mortality rates.

China is directing a recent crack-down on prostitution, gambling and drugs to go national, Reuters report-ed, citing statement by the Minis-try of Public Security. The campaign started in February after state broad-caster CCTV aired an expose of vice

in the city of Dongguan, where sub-sequent police raids led to the deten-tion of nearly 1,000 people. In a warning to the “protective umbrella” of official collusion, the ministry said officials would be “seriously investi-gated, and crimes will be resolutely investigated in accordance with the law.”

BUSINESSChina Petroleum & Chemical Cor-poration, known as Sinopec, said it will open up its domestic market-ing and distribution operations to outside investors, The Wall Street Journal reported. It didn’t give details about the investment program and stopped short of fully opening up its gasoline stations and other dis-tribution operations to third parties by capping the amount of outside investment at 30%. The move is a nod to Beijing’s latest efforts to reform state-owned companies and encourage a mixed-ownership econ-omy. Sinopec has the largest petro-leum sales-and-distribution network in China, with 30,532 fuel stations as of the end of last year.

Tencent Holdings bought about a 20% stake in Dianping Holdings, the operator of a customer reviews website often compared to US-based Yelp, Bloomberg reported, citing a statement by Tencent. The acquisi-tion will strengthen Tencent’s loca-tion-based services, allowing Asia’s largest internet company to tap into Dianping’s almost 100 million monthly active users who access the website’s reviews and discounts for food and entertainment. The Shen-zhen-based Tencent may invest as much as $500 million in Dianping, Sina.com reported on February 17th, without citing a source.

Alibaba Group Holding announced that two of its US subsidiaries are set to launch an e-commerce site in the US as it seeks to expand in the world’s largest e-commerce market, The Wall Street Journal reported. The two subsidiaries, Vendio and Auc-tiva, will soon launch a website called “11 Main,” which will offer high-quality products from select mer-chants in industries like fashion and jewelry. Though Alibaba’s revenue has surged in China on the popularity of its e-commerce platforms Taobao and T Mall, the company has had limited success abroad.

Chinese PC maker Lenovo Group reported a 30% increase in fiscal third-quarter earnings to US$265.3 million due to robust demand of PCs and smartphones in China, The Wall Street Journal reported. Lenovo, which last year overtook Hewlett-Packard as the world’s biggest PC maker by shipment volume, said on Wednesday net profit for the three months ended December 31 rose 30% from US$204.9 million a year earlier, while revenue rose 15% to US$10.79 billion from US$9.36 bil-lion. Lenovo’s solid quarterly results, which beat analysts’ expectations, come after the PC maker unveiled plans for two big US acquisitions.

NE WS ROUNDUP

1,000

People detained in a prostitution crackdown in Dongguan3.07 million

Estimated number of newly diagnosed cancer cases in China in 2012

Annual domestic grain production for 2020 set by the State Council

550 million tons

$132 million

Amount cosmetics maker Avon is putting aside as a bribery penalty estimate

Cre

dit

: M

ina

le T

att

ers

fi e

ld

Cre

dit

: J

uli

en

Go

ng

Min

China Economic Review | March 2014 09

Q&A: HOSPITALIT Y

China Economic Review | March 201410

Turning to the masses

Talk of Chinese s t a t e - o w n e d enterprises usu-

ally centers on banks and b ig indus t r i a l groups. But Beijing and local governments control much more than just factories and shipyards; they over-see a vast portfolio of companies that spread right into the heart of

the country’s middle class consumer revolution.

One of the largest is Shang-hai Jin Jiang International Hotels, a huge group that owns some of the most popular hospitality proper-ties in China. Zhou Zhi Qiang, vice president of Jin Jiang International Catering Investment and previously general manager of Jin Jiang Hotels, talked to China Economic Review about the evolution of the domestic catering industry and how the com-pany is adapting to the slowdown in spending by officials and state-owned enterprises.

Zhou speaks of the “populariza-tion” of the industry, highlighting how a company under the direction of the Communist Party is transi-tioning from an elite, deep-pocketed clientele to one more dominated by the masses.

The catering industry in China is changing rapidly. Can you please tell me what the major changes are in this particular industry?The catering industry will definitely start moving towards popularization. As the standard of living is improving for the Chinese people, they tend to choose a better dining environment. There are two main aspects of the catering industry that operators need to concentrate on: Dining environ-ment and supply chain safety. As long as these two aspects are under con-

A state-owned hospitality group switches focus from public offi cials to the middle class

trol, the catering industry will gradu-ally improve.

The catering industry is facing a time of making improvements [to cost performance] and transitions. Restaurants want to create a high-class dining environment for people to enjoy at a reasonable price. In gen-eral, we have to improve our cost per-formance [to enable this].

In the past, public [state] con-sumption accounted for a large part of Jin Jiang’s revenue and Jin Jiang was mostly involved in government affairs. However, Jin Jiang is now going to return back to [focus] on [wider] society in order to restructure this aspect of the hotel. Jin Jiang will let more middle class people into the hotels by opening up afternoon teas and buffets.

In the past year, luxury consump-tion, including restaurants and hotels, has started to slow. Corpo-rate expenditures, particularly at state-owned companies, are also being reduced. How have Jin Jiang Group’s restaurants been affected by this?Jin Jiang is currently going through a transformation period. It is a pain-ful period of time since our revenue has suddenly dropped. Jin Jiang used to have more conferences and large meetings than it could organize at the end of every year. However, Jin Jiang now needs to fill the empty spaces that were used for those large meetings. This year, we are making progressive preparations to target the mass market, especially for the Chi-nese New Year’s eve dinner. A lot of large-sized hotels are going through the same transformation as well.

Is this transition caused by the slow-down in luxury consumption?Definitely. As high-end hotels, we have to respond to the changing market and make some popularized

designs and products. We try to not make customers feel tense in our res-taurants. Jin Jiang is opening its door to the entire market, not just high-class consumers.

Many restaurant operators complain of high staff turnover. How is your company affected by this?Yes, there are some labor-related problems at this stage. It has become more difficult for our restaurants to recruit waitresses since Chinese teenagers are not too familiar with this industry. But employees are still happy to work in high-end restau-rants. But it will become more dif-ficult for all restaurants and hotels to recruit employees.

What can you do about these labor-related problems?Jin Jiang is currently working on a vital project called ‘the central fac-tory.’ We now own several factories that do [food] deliveries because it is also difficult to recruit chefs. Thus, we deliver semi-finished products from these factories, which are also our central kitchens, to the restau-rants. We also invested in a produc-tion line that produces semi-finished food products in order to deliver to our other restaurant chains. We are able to reduce labor costs and elimi-nate nearly 90% of the [labor-related] troubles through these factories.

Some chefs at high-end Western hotels complain that affluent Chi-nese consumers often order plates of expensive food but never finish it. Is this your experience?Jin Jiang has always promoted the reduction of food waste, and we also contributed in the ‘empty plate’ action and ‘one serve per person’ activity. But it is hard to change this Chinese habit. We are only able to allow the customers to eat separately by dish-es in high-end Chinese restaurants

aagactsscr

Zhou Zhi Qiang

Q&A: HOSPITALIT Y

China Economic Review | March 2014 11

because it is more complicated for chefs to make them. In other res-taurants of ours, we encourage the employees to communicate with the customers and remind them when they order too much.

Do you think this culture of wasting food will change in the future?It will definitely change in the future, especially in the next generation. The post-1980s and 90s generation have adopted the cultures of ‘going Dutch’ and takeaways. They have become more westernized. However, elder customers might still feel embarrassed to pack leftover food home.

Following all these changes, how much potential do you think this industry still has?Chinese cuisine is one of the most popular cuisines in the world. How-ever, restaurants on the mainland have to upgrade due to the intense competition. Marketing strategy is just on the surface; what really mat-ters are the underlying details. Factors such as food safety and brand reputa-tion need adjustments. They still have a lot of spaces for us to explore and study. Therefore, the market for this industry is still massive. Also, since food is always a key part of the Chi-

nese culture and the living standard of Chinese is booming, the catering industry still has a lot of potential.

What do you think the trend of this industry will be like in the coming years?Many large-sized companies are starting up franchise food chains, and it will be the most prosperous sec-tor of the Chinese catering industry. Western and East-Asian brands are entering the Chinese market, there-fore the development of franchise res-taurants will be rapid.

Due to the changing age structure of China, an increasing amount of young people tend to dine out instead of making food at home. Thus the market for catering services within the neighborhood is also growing.

It will become more difficult to establish high-end restaurants in the future. This market is going to shrink. Expensive rents, low wages and inflation are all imposing threats upon the catering industry. The sizes of restaurants will decline in city cent-ers. The industry tends to become more professional, as there will be fewer large sized restaurants and more franchises. Restaurants will also set up more diversified services within one store.

Have you any plans to open hotels overseas? If so, where, and what is the driver for this overseas expan-sion?We started co-branding with a French company called Hotel du Louvre. This company owns an econ-omy hotel brand called Campanile. Each company offered 15 hotels for co-branding. We also have entered the hotel market in the Philippines, South Korea and Indonesia. We are responding to the changing market.

China has seen a massive build up of overseas hotel brands in recent years. What is your view on all this?Many overseas hotel brands have entered the Chinese market in recent years. However, since most of cus-tomers in the limited service mar-ket are local Chinese, therefore hotel brands such as Ibis are not as compet-itive as Chinese budget hotel brands. In contrast, luxury hotels are mostly dominated by overseas customers. Ibis is the popular foreign brand in China, however, it is developing at a slow rate due to the competitiveness of local hotel brands.

Marketplace services in the US such as Airbnb that match rooms in pri-vate homes with travelers are chal-lenging established hotels. Do you see something similar happening in China?There are some online businesses that are similar with Airbnb in China. In the long term, it challenges estab-lished hotels. However, Chinese peo-ple haven’t got used to marketplace services. The price of marketplace services is still higher in comparison to budget hotels. Their management systems are not as standardized as established hotels and their safety is still questionable.

These homes are usually for long-term [stays] while economy hotels are for short stays. Thus, the target markets for economy hotels and mar-ketplace services are quite different. These services currently don’t impact upon established hotels in China, but Jin Jiang Inn has been paying more attention to this sector. WHO’S COOKING?: Zhou, pictured front-center, says that even high-end Chinese establishments such

as Jin Jiang are fi nding it much more diffi cult to hire good service staff

Q&A: US-CHINA TRADE

Business as normal

Despite the fre-q u e n t u p s and downs in

the political relation-ship between Beijing and Washington, trade between the world’s two largest economies is booming. Away from Capitol Hill, officials at the US state level are forging deals to sell their goods to China and

bring Chinese investment the other way to create jobs and power the domestic economic recovery. They also want to build lasting ties to Asia, which has emerged from the financial crisis as the most important regional driver of global economic growth.

Behind the scenes are organiza-tions like Shanghai-based consultan-cy The Center of American States (CAS), which since 1996 has been building ties between China and states across the US. Ning Shao, CAS chief executive, tells China Economic Review that US firms must adjust as China becomes a “nor-mal” market and why we have to wait to see if re-shoring becomes a sus-tainable trend.

The relationship between the US and China has sometimes been tense. So how has that affected the bilateral trade relationship, in your view, and do you fear any kind of disruption in commercial ties between the US and China?Duties and other measures are dis-ruptive. For example, there was a Chinese company in Arizona that had to close because of such prob-lems. The public policy uncertainty in US-China trade is mutual; US invest-ments in China are also subject to public policy changes. I think you also have a view that a lot of Chinese companies are concerned when they enter the US market. But from a local

view, we don’t set policy. Typically all the policies are bilateral and fed-eral policies, so we all have to face the challenges of maximizing the oppor-tunity for Chinese investment to the United States and mitigate some of the risk by assisting them [Chinese firms] with the understanding of how the system works, and also sometimes hopefully avoid the policy constraints of foreign investment in each other.

Many people in the business com-munity in the US are unhappy about what they see as restrictive policies from China, in terms of export sub-sidies for example, or trade barriers. What are your views on that - do you see any of that changing in the medium-to-short term?In general, of course, we have to understand some of the changes are inevitable in terms of China becom-ing a normal market, because when you enjoyed the favorable policy when China opened the door and tried to attract investment, it really often put extremely favorable terms on the table just to attract foreign investment. You could presumably argue that some of the policy of course that was put on the table put Chinese companies at a disadvantage, because if the Chinese companies had to pay 30% tax, and the US firm had a 5% tax holiday.

So I think when we talk about a level field, we have to understand that the Chinese government is also being pushed on the other side by the Chi-nese companies, whether state-owned or private, to argue for a level field, which is called national treatment, so everybody should be treated fairly and freely, and instead of just treating international investment as a national policy.

So that’s sort of a general trend and some of the favorable incentive programs that China put in place as part of the reform are probably going to be gradually eased out, so China

will be more normal, just like the United States. So I think some of the issues you mentioned are, probably as a macro adjustment of the policy, from a longer-term perspective that is inevitable. China will have to be a normal market.

I also like to think positive. If you look at the larger picture, the positive side of the US-China relationship – trade, investment, tourism, educa-tion, all that – it far surpasses all the challenges that we have between the two. And therefore, we have to have a perspective. If you open a paper every day, of course you only see some of the trouble spots. But if you’re distracted with that then sometimes you’re not able to see the rest, because the mainstream overall relationship between the US and China has been very positive.

Several of the US states that you represent have seen huge increases in exports to China. What are the main sectors, and by how long and by how much can this growth con-tinue?It’s really hard sometimes to predict the future, but just look at Michigan. Governor [Rick] Snyder has come to China every year since he was elected governor [in 2011]. That’s unprece-dented, having one governor to come to one country every year. Michigan’s largest trade with China is still in the auto sector, chemicals and machin-ery sort of as a general category, and there are also some agricultural prod-ucts, aerospace products and parts having some comfortable growth, as well as semiconductors and electron-ics.

With the US, I think there are three things. One is technical prod-ucts and more advanced manufac-turing products are still enjoying a favorable advantage in China. Agri-cultural products, products that are applied to natural resources and effi-

As China becomes a more mature market, US fi rms will need to adjust

China Economic Review | March 201412

tsabtiCafg

Ning Shao

ciency, I think the US has one of the most efficient agricultural produc-tion and supply chain systems in the world. Another category would be the service industry, which typically is not on the bilateral numbers that we quote, but on the ground we’ve seen a lot of service firms that are coming to China, whether CPA, legal, design, and advisories and education.

What are your views about re-shor-ing, the trend of US firms moving manufacturing operations back home from China?The global supply chain is market-driven. It’s dictated by raw material supply, dictated by logistics, and some of course in the context of macro policy as well. The US is sort of beginning to gain its manufacturing advantage for several reasons. One is that, if you look at jobs that are com-ing back to the US market, they are being paid at a much lower rate than they have historically. The second

one, a lot of the jobs that are com-ing to the US market are driven by the need for access to cheaper energy and raw materials. Of course histori-cally China became an attraction for investment because of the cheaper labor or relatively affordable cheaper labor. As China is becoming a much more prosperous economy the cost of production rises and that considera-tion is no longer as important. I think we are seeing some manufacturing coming back, and also we’ve seen some Chinese manufacturing come to the US, so that’s a good sign. But how sustainable that trend really is, I think is for the future history to tell.

You’ve worked with partners in the government, private and non-profit sectors, so what kind of advice would you give to organizations in each of these different sectors about how to engage with China?Really, the bottom line is that China is such a fast-changing environment

for anyone to be in, and even for myself, who’s been doing this for a long time, so you have to be really adapting to the fast-changing envi-ronment, whether you’re operating on the government-to-government level, corporate level, not-for-profit or educational exchanges, understanding the changing landscape. Some of the changing priorities in the Chinese economy are opportunities.

We were just at a meeting and talking about the change in health-care. The reform of China will create a lot of opportunity for the US mar-ket in the overall healthcare sector. And just understanding that trend and leveraging what are the priori-ties for China, [which] has a five-year plan and then has a longer plan, understanding what the priorities for the Chinese economy will help not only business development but also help to align your resources with that of China’s. So that’s the smartest advice.

Q&A: US-CHINA TRADE

China Economic Review | March 2014 13

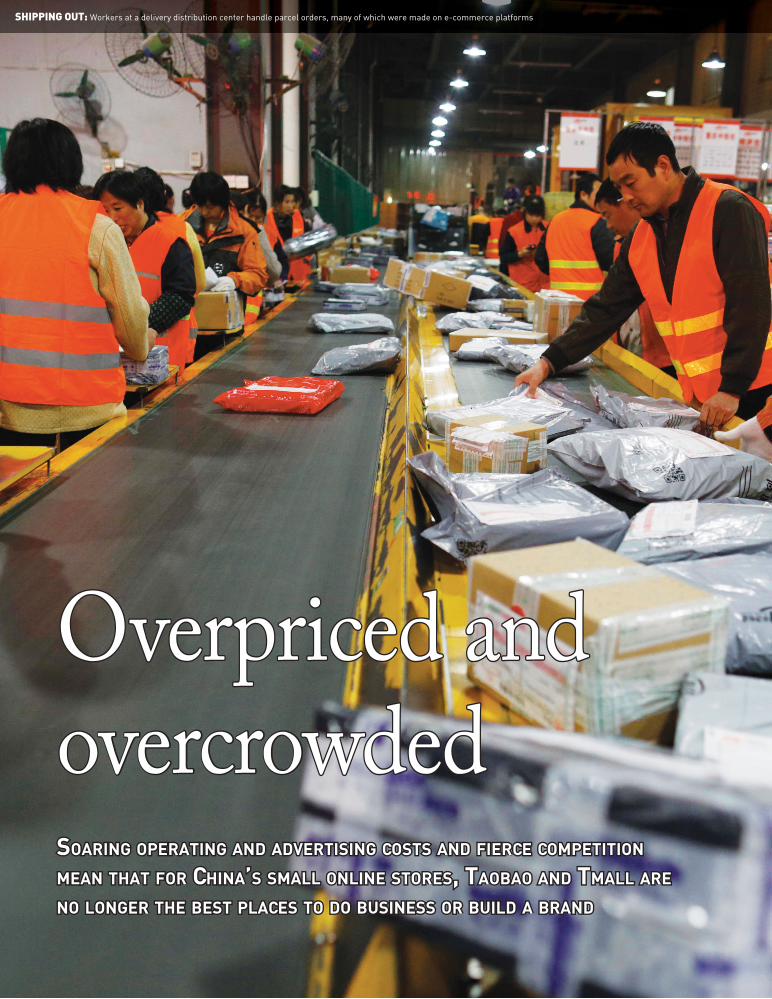

SOARING OPERATING AND ADVERTISING COSTS AND FIERCE COMPETITION SOARING OPERATING AND ADVERTISING COSTS AND FIERCE COMPETITION

MEAN THAT FOR CHINAMEAN THAT FOR CHINA’’S SMALL ONLINE STORES, TAOBAO AND TMALL ARE S SMALL ONLINE STORES, TAOBAO AND TMALL ARE

NO LONGER THE BEST PLACES TO DO BUSINESS OR BUILD A BRANDNO LONGER THE BEST PLACES TO DO BUSINESS OR BUILD A BRAND

Overpriced and Overpriced and overcrowdedovercrowded

SHIPPING OUT: Workers at a delivery distribution center handle parcel orders, many of which were made on e-commerce platforms

The hard figures don’t lie. When a company can attract 10 million unique views to its web-sites in a single minute, you know it’s serious

about business. When it posts a transaction value of US$5.7 billion in one day, you know it’s bringing in some serious cash.

Step forward Alibaba Group. The company’s Tmall and Taobao e-commerce platforms recorded an 83% year-on-year surge in transaction volume last November 11, the date of China’s annual “Sin-gle’s Day” online shopping extravaganza, coming off the back of a 260% surge a year earlier. The vol-ume of business on these sites – Tmall does mainly business-to-customer transactions while Taobao is largely business-to-business – is often described by industry watchers as “over the top” or “insane.”

Behind the mind-numbing figures is the myriad of shops and vendors doing business. The number of stores on the two platforms has grown from just over six million in late 2011 to more than nine mil-lion in October of last year. This huge number of vendors vying for customers has driven skyward the cost of advertising, while also producing a high degree of clutter from which the small players – which constitute the majority of the market – strug-gle to break free.

In the melee for shoppers, small Chinese brands are likely the biggest losers. While being increas-ingly priced out of ads, small retailers are often lost at sea among the multitude of similar shops on the mega sites and have few tools to build strong, enduring presences, experts and industry players told China Economic Review. But while many will look for a way off of the Alibaba platforms, for now they have few places to run to.

COVER STORY: SELLING ON TMALL

China Economic Review | March 2014 15

Branding hurts“They have hundreds of thousands of brands on the sites. As a small brand, it’s hard to get seen there with all that competition,” says Jil-lian Xin, the owner of online design-er-clothing platform Xinlelu.com.

Xin founded the site in 2012. Named after a street in Shanghai known for its small fashion bou-tiques, it serves as a platform for designer-clothing brands looking to market their goods on the mainland. For the some 50 global and Chi-nese brands on the site every sea-son, managing the customer’s shop-ping experience has become critical to branding. Xin said the platform tries to evoke a “boutique shopping experience” online, something that simply isn’t possible on Tmall right now.

“When someone’s looking at a minimalist-style dress and you have advertisements for Wangwang [soft-ware for the Alibaba platforms]

COVER STORY: SELLING ON TMALL

popping up on the screen, there’s just too much going on,” Xin said. But there’s more to it than just the refined image. Managing customer data can be another problem on the mega sites. Xin said brands operat-ing on Tmall might find it “difficult to know who your customers even are.”

That’s because Alibaba gives shop owners very little access to data con-cerning their businesses, says Patrick Deloy, executive director at e-com-merce consultancy Bluecom. Brands starting up on Tmall or Taobao will find it difficult to know who has been viewing their pages. Keeping track of and contacting past custom-ers can also be challenging.

In some cases, instead of online analytics furthering a brand’s under-standing of the market, the data is used by Alibaba itself for its own marketing and statistical purposes, Deloy said. There have even been cases where data have been sold from

one merchant to another, he noted.Although a brand may see high

sales volumes at certain times of the year, it isn’t necessarily forging last-ing business.

“If you’re a brand and you open a Tmall shop, you’re not going to build anything. You are actually kill-ing your brand,” said Cyril Drouin, chief executive at Bysoft, a consult-ing firm that advises brands that want to market online in China. “But you have to be there, because in terms of sale volume it’s absolutely amazing.”

‘Nothing to say’That’s the question brands on Taobao and Tmall are mulling now: Is the sales volume strong enough to justify the cost of staying there?

The price of online advertising in China during the past three years has climbed sharply. The increase is hard to quantify given the various forms of advertising that exist. In

OUR SECRET: Alibaba’s internet commerce platforms capture vast volumes of user data that they do not share easily with store owners

Cre

dit

: A

lib

ab

a

China Economic Review | March 201416

2012, online advertising revenues grew by more than 46%, hitting a value of US$12.3 billion, accord-ing to a report from Beijing-based iResearch. Some shop owners on Tmall say prices for certain kinds of advertising have more than doubled since 2012.

“There’s been a huge change in the past two years,” Zou Yini, the owner of a Taobao store that sells makeup, said of the cost of advertis-ing. Zou isn’t building a brand; she markets popular makeup products on her business-to-business site. But the difficulty of some brands to stay afloat is evident to her.

In the short life of Taobao, Zou is an old hand. When she opened her store three years ago there were so few competitors that she says she didn’t need to buy advertising. A year later, she had been crowded out as thousands of small stores began selling similar products. So she paid for an advertising cam-paign that distributed information over Sina Weibo, China’s version of twitter.

At that time, she paid between US$160 and US$320 for a simple Weibo package. Today, the same plan costs more than US$800, although the increasing popularity of the mirco-blogging service means that it now reaches far more people than it did when Zou started using it.

Zou said the ultra-high sales vol-ume during shopping holidays such as Single’s Day has buoyed the rate of return on her investment. After three years, her shop is well estab-lished. She’s less optimistic for new entrants into the market, though. The increasingly high costs coupled with superfluous vendors all selling similar items make Taobao a jungle for fledgling shops.

“The cost of acquiring new clients [online] in China is getting higher and higher every year. So they have less and less return on investment online,” Drouin said. On top of pricy ad rates, several fees come along with opening on an Alibaba platform. At Tmall, vendors pay deposits, setup fees, yearly fees and transaction fees.

COVER STORY: SELLING ON TMALL

Call them what you will, but e-commerce sites will lead online innovation in China

China’s mega online shopping plat-

forms might not be the best venue

for emerging brands to set up shop.

But Alibaba, along with peers such

as Dangdang and Jingdong, are mas-

ters of innovation. While China’s on-

line shopping universe may seem

crowded at present, it is, in the grand

scheme of things, in its infancy. The

companies, and the e-commerce

industry in general, will likely bring

forward some of China’s most inno-

vative products in the years to come.

In fact, they already are.

Alibaba founder Jack Ma is lead-

ing the way in e-innovation. So much

so that he has central bankers con-

cerned. Last year, Alibaba launched

Yu ’E Bao, an online fund that prom-

ises better returns than bank depos-

its. The fund had 49 million custom-

ers and US$40 billion in investments

as of mid-January, giving traditional

lenders a run for their money.

Jingdong Mall, a competitor to

Taobao and Tmall although much

smaller, is conducting fi nancial ex-

periments of its own. In February, the

company said it was trying a credit

system it calls “Baitiao.” Baitiao

will function like a credit card, giv-

ing customers limited lines of credit

although they will be restricted to

shopping on Jingdong’s e-commerce

universe. Credit cards have not

caught on in China mainly because

the interest rates they offer are

heavily regulated by the state. Jing-

dong may have a breakthrough on its

hands with Baitiao.

Innovation in China’s social media

is pulling along e-commerce as well.

Ad space on websites is expensive

but pushing along a brand’s name on

Sina Weibo, China’s version of Twit-

ter, is cheap and direct. Vendors and

brands that remain on the mega-mall

sites will increasing opt to access cli-

ents through this channel.

Social media may even help

change the face of China’s largest

e-markets. Meilishuo is one attempt

to personalize shopping on sites that

have become largely impersonal.

Translating roughly as “beauty talk,”

Meilishuo functions much like the

US’s Pinterest, where shoppers can

post their favorite brands and prod-

ucts, although the site is explicitly

“female only.” Last year, the founder

claimed the social media platform

had 32 million users, 80,000 of whom

used the site frequently.

Other major internet companies, such as Dangdang and Jingdong, have launched their own platforms for online businesses but Alibaba remains far and away king of the industry. “Now they [brands] have

one player and they are completely dependent on that player,” noted Drouin. “If Tmall decided to sud-denly raise fees, the brands would have nothing to say. They would just have to say ‘yes.’”

China Economic Review | March 2014 17

ECONOMICS & POLICY: URBANIZATION

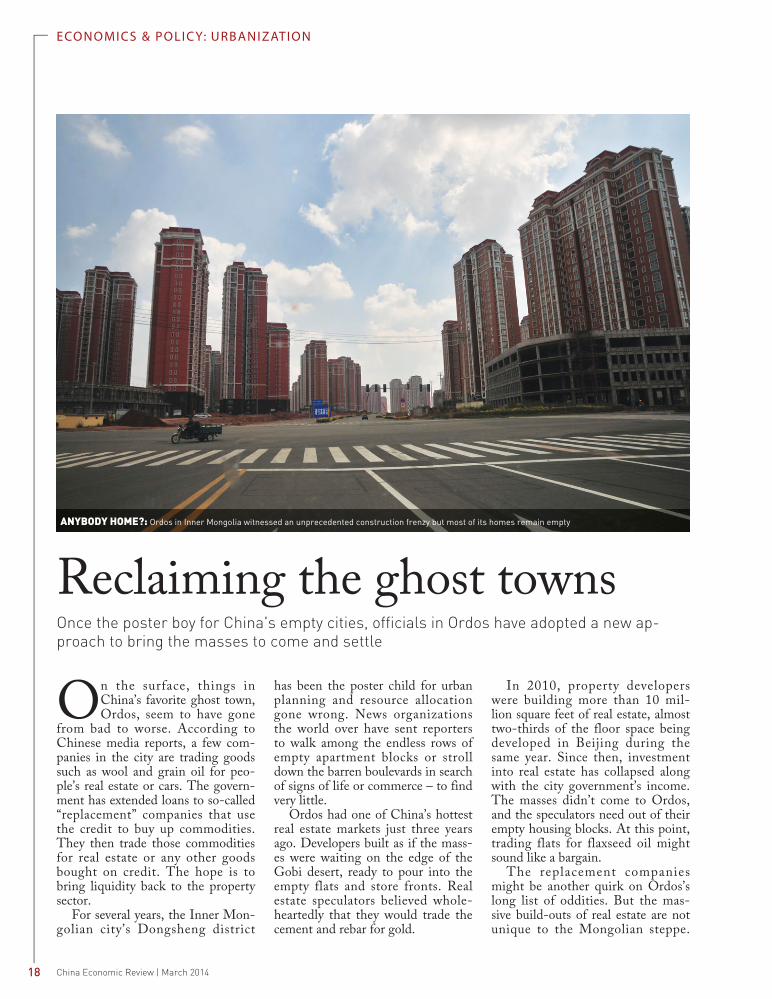

Once the poster boy for China's empty cities, offi cials in Ordos have adopted a new ap-proach to bring the masses to come and settle

On the surface, things in China’s favorite ghost town, Ordos, seem to have gone

from bad to worse. According to Chinese media reports, a few com-panies in the city are trading goods such as wool and grain oil for peo-ple’s real estate or cars. The govern-ment has extended loans to so-called “replacement” companies that use the credit to buy up commodities. They then trade those commodities for real estate or any other goods bought on credit. The hope is to bring liquidity back to the property sector.

For several years, the Inner Mon-golian city’s Dongsheng district

has been the poster child for urban planning and resource allocation gone wrong. News organizations the world over have sent reporters to walk among the endless rows of empty apartment blocks or stroll down the barren boulevards in search of signs of life or commerce – to find very little.

Ordos had one of China’s hottest real estate markets just three years ago. Developers built as if the mass-es were waiting on the edge of the Gobi desert, ready to pour into the empty flats and store fronts. Real estate speculators believed whole-heartedly that they would trade the cement and rebar for gold.

In 2010, property developers were building more than 10 mil-lion square feet of real estate, almost two-thirds of the floor space being developed in Beijing during the same year. Since then, investment into real estate has collapsed along with the city government’s income. The masses didn’t come to Ordos, and the speculators need out of their empty housing blocks. At this point, trading flats for flaxseed oil might sound like a bargain.

The replacement companies might be another quirk on Ordos’s long list of oddities. But the mas-sive build-outs of real estate are not unique to the Mongolian steppe.

Reclaiming the ghost townsANYBODY HOME?: Ordos in Inner Mongolia witnessed an unprecedented construction frenzy but most of its homes remain empty

China Economic Review | March 201418

Many cities across China are still adding amazing amounts of floor space, and with better planning, those places aren’t set to fall into the same ghost-town trap as Ordos.

Take Guiyang, the capital of Guizhou province, for example. Bar-clays Research recently visited the city and had some interesting notes on real estate developments in one the country’s poorest regions.

Between 2010 and 2016, the city will have 150 million square meters of property floor space under con-struction, according to the report. That’s enough space to house 3 mil-lion people in a city that only has a population of 4 million today. No more than a third of the people that will buy those houses currently live in Guiyang. Up to 60% of the flats will be filled by people from nearby counties.

Guizhou is one of China’s poor-est provinces. Per capita GDP there was just US$3,000 in 2012 versus

US$8,500 the same year in Guang-dong province to the southeast. The demand generated by urbanization is a force that will literally remake the provincial capital as the popu-lation nearly doubles in a span of six years. Migrants will settle into modern homes, take up modern jobs and earn modern wages (by China’s standards).

Barclays wasn’t in Guiyang to verify the success of the city’s urbani-zation process. The team was there inspecting the industries that are set to profit from such massive real estate projects, such as the manu-facturers of tires for big trucks. The city’s market may show some signs of a bubble, but with mainly poor migrants filling the new buildings, it also demonstrates effective urbaniza-tion planning, namely turning farm-ers into urban consumers.

The apartment blocks in Ordos won’t stay empty forever. People will eventually fill those flats – and

likely pay far more reasonable pric-es for them than they would have three years ago. But for the proc-ess to work smoothly, the govern-ment can’t rely on the “build-it-and-they-will-come” model. Much more important will be to give the people a reason to relocate to the edge of the desert.

Ordos is trying that now – albe-it not in time to save the specula-tors that originally rushed into the market. Fresh graduates who move to the city to set up businesses can receive free office space, utilities and internet connections. Instead of posh apartments, the city is building trade schools it hopes will usher in a new generation of entrepreneurs to the region.

Balanced planning should help Ordos officials run the ghosts out of town before the international media can post too many more stories and photo galleries depicting its lonely streets.

ECONOMICS & POLICY: URBANIZATION

China Economic Review | March 2014 19

For more information and online registration, visit:

url.topmba.mobi/cer2014

US $1.7 million in scholarships available to participants

Meet face-to-face with admissions directors from around the world

Network with alumni from top business schools

Get GMAT tips and advice straight from the source at GMAC seminar

Special section for EMBA programs

Women in Leadership event

TOPMBACONNECT 1-2-1

Emerging markets rose to prominence in the mainstream conscience lumped all togeth-

er. Individually, they were less attrac-tive and often considered too risky. That was helpful in raising their pro-file in global financial centers.

Such association is now looking like less of a good thing as serious economic turmoil in some developing nations has, in the eyes of investors, tarnished all of them with the same brush. Questions are now even being asked of China, the long-time poster boy for this group.

In December the US Federal Reserve started scaling back, or taper-

ing, its long running quantitative eas-ing program. Since then asset pur-chases have been trimmed to US$65 billion a month from US$85 billion, triggering widespread capital flight globally. The results have not been kind to places like Indonesia and Turkey and have amplified the uncer-tainty over emerging markets that first appeared last summer when talk of tapering turned serious.

Until now, China has looked largely stable. Many of the funda-mental issues causing pain elsewhere such as current account deficits and small supplies of foreign currency do not trouble Beijing. “The over-

all effect [of tapering] on China will probably be limited, as China has a current account surplus and the world’s largest foreign-exchange reserves,” Ivy Pan, a Hong Kong-based analyst with ABN Ambro, wrote in a research note.

But an increasingly anxious mar-ket is starting to ask deeper questions about the health of China. Some investors see the risks posed by taper-ing to exports and the local financial market as a trigger that could throw the whole economy off kilter.

Exports re-routedChinese exports to developing mar-

ECONOMICS & POLICY: QE3 TAPERING

RUNNING SCARED: Washington’s decision to scale back its asset-purchasing program has predictably led to an outfl ow of capital from emerging markets

Avoiding the tapering tideAlthough China is strong enough to fend of the rout hitting emerging markets, it must continue to reform to stay in strong shape againist future pressures

China Economic Review | March 201420

kets have boomed in recent years. As those places grew richer their emerg-ing middle classes sought a greater variety of consumer goods. Those regions now account for about 50% of the world economy and helped offset weak demand from rich nations in the years immediately following the financial crisis.

Giant container ships departing China for exotic destinations might soon be carrying much lighter car-goes. Since the beginning of Decem-ber, Argentina’s peso has fallen by about 20% versus the dollar while the Turkish lira is down around 8%, making imported goods much pricier. Interest-rate hikes by central banks in Ankara and Brasilia designed to stop foreign capital from fleeing will hurt the credit-driven consumer boom in those countries.

Dockers in Los Angeles and Port-land on the other hand can expect more work unloading vessels from Shanghai and Guangzhou. The Fed is tapering because American unem-ployment is falling below 7%, which indicates growth in economic activity. Stronger consumption in key devel-oped markets will offset a slowdown in Chinese exports elsewhere; roughly 20% of goods shipped from China are destined for the US compared to the 15% bound for emerging markets.

US consumers might soon be able to get more for their buck. “QE tapering could make the US dollar stronger, which would strengthen its purchasing power and import demand,” Cao Yongfu, an assistant research fellow at the China Acad-emy of Social Sciences, wrote in an opinion piece.

Money flowsOf potentially greater concern is financial stability in China as this is where risk has piled up. Taper-ing could inflict serious damage if it prompts a severe outflow of capital.

China faces the prospect of vola-tility from global capital movement. Investors might prefer to move their money to the US, where interest rates are expected to start rising, while the gradual economic recovery there makes it an attractive destination

overall, noted Cao. China recorded net capital outflows in 2012 after being a net recipient in the preceding three years.

Top officials in Beijing are cau-tious, asking Washington to consider the global implications of changes to its monetary actions. “We call on the US to work as a responsible major country and to be responsible for the spillover effect of its policy,” Zhu Guangyao, vice minister of finance, said in late December after a meeting with US officials.

Pressure is likely to mount in the short term and could seriously disrupt the business environment. Domestic monetary conditions are tight and the People’s Bank of China (PBOC) appears determined to keep a rein on things. January saw record credit expansion to which the central bank responded by unexpectedly draining liquidity from the market. Capital outflows will only add to the difficul-ties companies face in accessing vital financing.

Still, the broader impact of capital flows is unlikely to have anywhere near the damaging impact currently being felt in places like Jakarta. Cru-cially, China does not depend on short-term borrowing from overseas

to pay for what it spends, and has the means to deal with problems.

“The experience of the tapering scare back in middle part of this year [2013] suggests that the most vulner-able economies are those with sus-tained current account deficits and those that rely heavily on foreign cap-ital inflows to fund domestic growth,” JP Morgan chief China economist Zhu Haibin wrote in a note in Janu-ary. “From this perspective, China is indeed in a solid external position, which is why China was little affected by the previous tapering scare.”

Senior officials also have the ability to loosen domestic liquidity through their own means. One of these is scaling back the amount of money banks need to hold in reserve to inject more cash into the real economy. This is an oft-deployed monetary tool by the central bank. Strict capital account controls meanwhile prevent the rapid movement of money over borders.

If anything, top foreign exchange officials are bracing themselves for capital inflows this year. That would add to the massive US$138.8 billion current account and US$199.2 billion capital and financial account surpluses recorded in the first nine months

ECONOMICS & POLICY: QE3 TAPERING

PLAYING SAFE: China could see some foreign capital fl ow back to the US as the economic revoery there

gathers momentum and investors seek safer assets

Cre

dit

: P

erp

etu

al

tou

rist

China Economic Review | March 2014 21

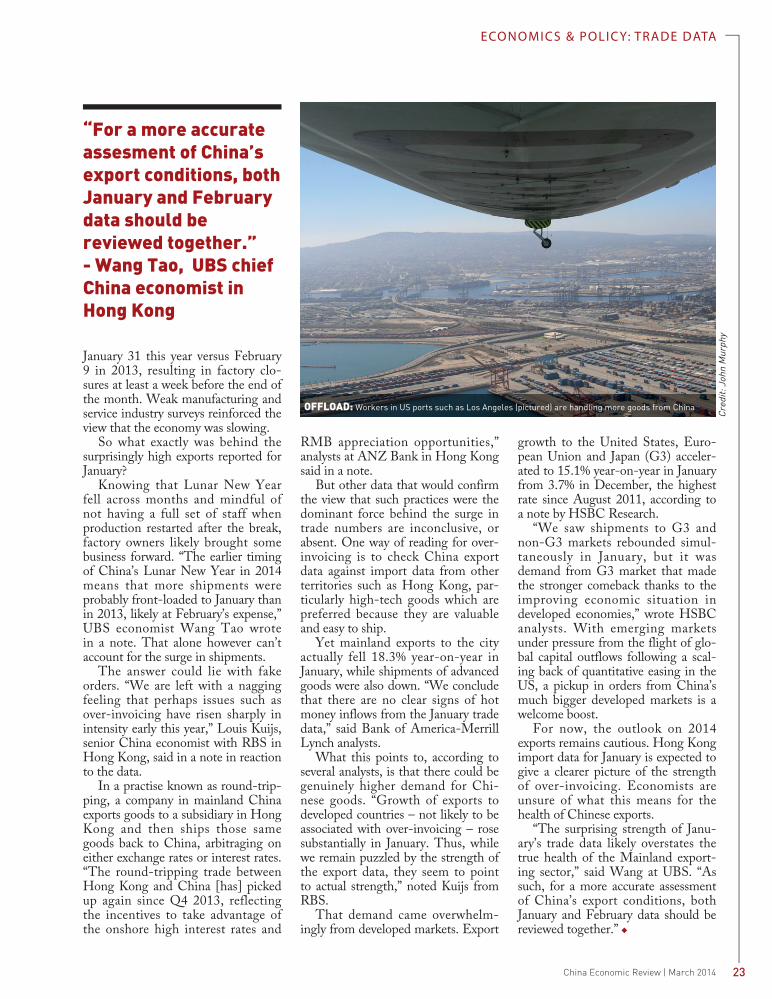

Widespread caution over Chinese economic data means that when num-

bers provide a positive surprise, loud grumbles from hardened skeptics run through the airwaves. January trade data would have had calmer observers toning the volume down.

Exports from China surged 10.1% from a year earlier despite overall predictions of at best flat growth or even a decline. Separate surveys of economists by Bloomberg and The Wall Street Journal had median export growth predictions of 0.1%. A Reu-ters’ poll put forward 2%.

Not long after China customs released the data on February 12, speculation was rife that the num-bers were indeed questionable, pos-sibly hinting at a recurrence of the over-invoicing that grossly distorted the same set of data a year earlier. At

that time, Chinese companies were caught inflating the value of exports to bypass currency controls and bring yuan into China.

Although that theory cannot be discounted completely – there is some evidence to support suspicions – the rosier take on the data is that demand for Chinese goods is coming back from developed markets. That is good for those who want China to hit the magic 7.5% GDP growth target this year and a welcome boost to the global economy overall.

Analysts' immediate reactions to the data were dominated by those two ideas.

Invoice trickery by traders last year led to a reported 25% rise in imports from the year prior, meaning the base figures for this January were extreme-ly high. Also, the seven-day nation-al Lunar New Year holiday started

ECONOMICS & POLICY: TRADE DATA

Not againQuestions about the reliability of Chinese trade data are back. This time though the numbers could be real

of 2013, bolstering China’s ability to withstand any stampede by inves-tors to the departure lounge.

Wealth of the nation“China’s economic fundamentals are much healthier than most other EMs and China is one of the least vul-nerable EM economies to US taper-ing in 2014,” Ma Jun, chief China economist at Deutsche Bank in Hong Kong, concluded in a recent note. Nevertheless, the country does face some risks from tapering and needs to be alert to the problems that can arise.

China is the world’s largest hold-er of US Treasury debt. It has been buying the paper to keep its currency weak and fuel global consumption of the goods it exports. But its hold-ings are now so vast that any decline in their value would be painful. This threat now looms as US interest rates are expected to pick up from the lows they have been at since 2009. In response, last December China con-ducted the biggest sale of such assets in nearly four years.

Advocates of liberal economic reforms see tapering as an oppor-tunity for China to get its house in order. They argue that emerging markets will see slower growth in the coming years while rich nations will take time to get back to full strength. Therefore, China needs to drive more growth internally and further secure itself against the possibility of external shocks.

“The end of monetary easing in the US will bring unprecedented financial risks to a China already fac-ing slowing growth. China has no choice but to reform its economy,” Hu Shuli, editor of the influential business magazine Century Weekly, wrote in an editorial.

Beijing is already moving in that direction, and needs to stick with it. “China is implementing the most aggressive structural reforms in dec-ades, while this determination is not seen in most other EMs due to political stalemate,” noted Ma. “China’s new reform program, espe-cially deregulation, would enhance the country’s growth potential and reduced macro risks.”

BACK IN BUSINESS: Chinese exports to the US, EU and Japan surged 15.1% year-on-year in January

in what could be a welcome sign that demand is returning in rich nations just as emerging markets falter

Cre

dit

: M

arc

oh

!

China Economic Review | March 201422

ECONOMICS & POLICY: TRADE DATA

January 31 this year versus February 9 in 2013, resulting in factory clo-sures at least a week before the end of the month. Weak manufacturing and service industry surveys reinforced the view that the economy was slowing.

So what exactly was behind the surprisingly high exports reported for January?

Knowing that Lunar New Year fell across months and mindful of not having a full set of staff when production restarted after the break, factory owners likely brought some business forward. “The earlier timing of China’s Lunar New Year in 2014 means that more shipments were probably front-loaded to January than in 2013, likely at February’s expense,” UBS economist Wang Tao wrote in a note. That alone however can’t account for the surge in shipments.

The answer could lie with fake orders. “We are left with a nagging feeling that perhaps issues such as over-invoicing have risen sharply in intensity early this year,” Louis Kuijs, senior China economist with RBS in Hong Kong, said in a note in reaction to the data.

In a practise known as round-trip-ping, a company in mainland China exports goods to a subsidiary in Hong Kong and then ships those same goods back to China, arbitraging on either exchange rates or interest rates. “The round-tripping trade between Hong Kong and China [has] picked up again since Q4 2013, reflecting the incentives to take advantage of the onshore high interest rates and

RMB appreciation opportunities,” analysts at ANZ Bank in Hong Kong said in a note.

But other data that would confirm the view that such practices were the dominant force behind the surge in trade numbers are inconclusive, or absent. One way of reading for over-invoicing is to check China export data against import data from other territories such as Hong Kong, par-ticularly high-tech goods which are preferred because they are valuable and easy to ship.

Yet mainland exports to the city actually fell 18.3% year-on-year in January, while shipments of advanced goods were also down. “We conclude that there are no clear signs of hot money inflows from the January trade data,” said Bank of America-Merrill Lynch analysts.

What this points to, according to several analysts, is that there could be genuinely higher demand for Chi-nese goods. “Growth of exports to developed countries – not likely to be associated with over-invoicing – rose substantially in January. Thus, while we remain puzzled by the strength of the export data, they seem to point to actual strength,” noted Kuijs from RBS.

That demand came overwhelm-ingly from developed markets. Export

growth to the United States, Euro-pean Union and Japan (G3) acceler-ated to 15.1% year-on-year in January from 3.7% in December, the highest rate since August 2011, according to a note by HSBC Research.

“We saw shipments to G3 and non-G3 markets rebounded simul-taneously in January, but it was demand from G3 market that made the stronger comeback thanks to the improving economic situation in developed economies,” wrote HSBC analysts. With emerging markets under pressure from the flight of glo-bal capital outflows following a scal-ing back of quantitative easing in the US, a pickup in orders from China’s much bigger developed markets is a welcome boost.

For now, the outlook on 2014 exports remains cautious. Hong Kong import data for January is expected to give a clearer picture of the strength of over-invoicing. Economists are unsure of what this means for the health of Chinese exports.

“The surprising strength of Janu-ary’s trade data likely overstates the true health of the Mainland export-ing sector,” said Wang at UBS. “As such, for a more accurate assessment of China’s export conditions, both January and February data should be reviewed together.”

OFFLOAD: Workers in US ports such as Los Angeles (pictured) are handling more goods from China

“For a more accurate assesment of China’s export conditions, both January and February data should be reviewed together.”- Wang Tao, UBS chief China economist in Hong Kong

Cre

dit

: J

oh

n M

urp

hy

China Economic Review | March 2014 23

ECONOMICS & POLICY: FOOD IMPORTS

Healthier serving

For years Beijing stressed that the country’s farmers must grow enough grain to feed the

masses. Measures enacted in 1996 called on China to produce 95% of its own grain. That policy reflected concerns rooted deeply in centuries of food instability and intermittent fam-ine in China’s long history.

The official outlook on how much grain the country must produce at home is changing, however. The State Council called for China to sta-bilize annual grain production at 550 million tons by 2020, far lower than the 602 million tons produced last year. The government will now turn its focus to the quality and safety of the domestic harvest.

But that doesn’t mean China has completely abandoned grain self-suf-ficiency. Agricultural policymakers are simply getting with the times.

Local media reported at the end of 2012 that Chinese self-sufficiency levels for rice, wheat, corn and soy-beans had fallen below 90%. Yet that figure was hotly contested by Chen Xiwen, director of China’s Rural Development Institute. When soy-beans are tossed out of the equation, Chen claimed, the country had main-tained its sacred 95% self-sufficiency rate. Soybeans are not counted as an edible grain.

China has the capacity to contin-ue producing enough edible grain, namely rice and wheat, to feed the

country through 2020, Jane Peng, a Shanghai-based grain and seed oil analyst at Rabobank International, told China Economic Review. Imports of corn and soybean, which are consumed by humans but mainly find use as animal feed, will increase as China continues to eat more meat.

Yet, the way Chinese people con-sume grain and meat is set to change in the coming years.

“The 95%-and-above self-suffi-ciency rate was posited in the 1990s. Under new circumstances, the con-notation of grain security is differ-ent from 10 to 20 years ago,” Cheng Guoqiang, secretary general of the State Council Development Research Center’s Academic Committee, was

A major change to agricultural policy underscores that top leaders acknowledgethe desire of their people to eat better quality food

FEELING FULL: Long-held concerns that China won’t be able to feed its people as it loses more arable land to urbanization may ease as it becomes clearer that

the surge in food consumption spurred by economic developments is starting to level out

Cre

dit

: S

teve

n G

itte

r

China Economic Review | March 201424

ECONOMICS & POLICY: FOOD IMPORTS

quoted by state media as comment-ing on the often-fierce debate over the amount of grain that China must produce at home.

That’s true. As a country gets rich-er, its consumption pattern changes. During the 1980s and 90s, when the country was still knee-deep in poverty -reduction efforts, a strong correla-tion existed between rising incomes and rising food – especially meat – consumption. However, as China continues to push most of its people further away from the breadline, its appetite for food will not necessarily rise in tandem.

“It’s a curve. There’s a ceiling for this consumption,” Peng said. “The higher the income does not indicate the more grain and meat we are going to eat.”

Around 2020, China’s average per capita income will hit US$10,000, Peng said, a mark that in other northeast Asian countries such as South Korea signified a change in the way people spent their money.

At that point in development, people begin emphasizing the quality of food over the quantity.

Setting the 2020 grain production target at 550 million tons and turning attention to the quality of food might be a sign that China’s agricultural sector, policy-wise one of its most conservative, is changing its hardline attitude. “I think that’s a very reason-able figure [for grain production] for 2020. The Chinese government has a good forecast for the future,” Peng said.

But producing rice safe enough for the Chinese people to eat in the next decade won’t be easy. Soil pollution has become a major challenge to the government’s self-sufficiency goals.

“In many places this kind of pollu-tion has already affected the ground water and the crop yield,” said Fu Zhenzhen, a grain analyst at Beijing Shennong Kexin Agribusiness Con-sulting in Beijing. “This problem has already become very serious.”

China has about 20% of the world’s arable land but accounts for 30% of global fertilizer use, or about 50 million tons in 2007, according to a report from Sustainalytics, a Singapore-based consultancy. Only 25-35% of the chemicals in the ferti-lizers can be absorbed by crops while the rest remains in the soil or flows into rivers. Last May, inspectors dis-covered rice with a high level of can-cer-causing cadmium in markets in the southern city of Guangzhou. The rice had been grown in a heavily pol-luted area in Hunan province and the incident underscored just how real are the daily concerns Chinese people have over the food they eat.

China may have the capacity to feed its people with home-grown grains. The question is whether Chinese will allow it in their bowls. Despite being the world’s biggest rice producer, China also became the world’s No. 1 rice importer in 2013, buying 3.4 million tons of the grain.

Those imports in part show that China’s appetite for quality – in this case potentially safer rice – is indeed growing. It’s encouraging that the government has recognized that quantity isn’t everything.

“The connotation of grain security [today] is different from 10 to 20 years ago.” - Cheng Guoqiang, secretary general of a State Council academic research committee

DIRTY CROPS: Above-average use of fertilizers on Chinese farms puts domestic crop yields at risk

Cre

dit

: P

ete

r P

ea

rso

n

China Economic Review | March 2014 25

BUSINESS: PROPERT Y BUBBLES

Th e cracks widen

Feng shui masters are telling fund managers to invest cau-tiously during the Year of the

Horse, China’s traditional lunar year that started on January 31. A famous Hong Kong fortune teller reported-ly said 2014, in the ancient 60-year zodiac cycle, represents “instability and disruption.”