Central Equity Trustinvesco.fgraphic.com/pdf/CETD0036pro.pdf · Central Equity Trust, Diversified...

41

Central Equity Trust Diversified Income Series 36 Central Equity Trust, Diversified Income Series 36 (the “Trust”), included in Van Kampen Unit Trusts, Series 992, is a unit investment trust that seeks capital appreciation and dividend income by investing in a portfolio of shares of common stocks of consumer cyclicals companies, consumer staples companies, energy companies, financial services companies, health care companies, industrials companies, real estate investment trusts, technology companies, telecommunications companies and utilities. Of course, we cannot guarantee that the Trust will achieve its objective. July 20, 2010 You should read this prospectus and retain it for future reference. The Securities and Exchange Commission has not approved or disapproved of the Units or passed upon the adequacy or accuracy of this prospectus. Any contrary representation is a criminal offense. Edward D. Jones & Co., L.P.

Transcript of Central Equity Trustinvesco.fgraphic.com/pdf/CETD0036pro.pdf · Central Equity Trust, Diversified...

Central Equity TrustDiversified Income Series 36

Central Equity Trust, Diversified Income Series 36 (the “Trust”), included in Van Kampen Unit Trusts, Series992, is a unit investment trust that seeks capital appreciation and dividend income by investing in a portfolio ofshares of common stocks of consumer cyclicals companies, consumer staples companies, energy companies,financial services companies, health care companies, industrials companies, real estate investment trusts,technology companies, telecommunications companies and utilities. Of course, we cannot guarantee that theTrust will achieve its objective.

July 20, 2010

You should read this prospectus and retain it for future reference.

The Securities and Exchange Commission has not approved or disapproved of the Unitsor passed upon the adequacy or accuracy of this prospectus.

Any contrary representation is a criminal offense.

Edward D. Jones & Co., L.P. INVESCO

Investment Objective. The Trust seeks capitalappreciation and dividend income.

Principal Investment Strategy. The Trust seeks toachieve its objective by investing in a portfolio of shares ofcommon stocks of consumer cyclicals companies,consumer staples companies, energy companies, financialservices companies, health care companies, industrialscompanies, real estate investment trusts (“REITs”),technology companies, telecommunications companies andutilities. The portfolio consists of securities selected byresearch analysts at Edward D. Jones & Co., L.P. (the“Underwriter”) and approved by the Sponsor. In selectingthe Securities, the following factors, among others, wereconsidered: dividend yield, dividend track record, dividendcoverage, earnings growth rates, dividend growth rates,regulatory climate and stock valuation. At the time theSecurities were selected, the Underwriter’s researchanalysts were currently covering all the issuers of theSecurities and had published favorable recommendationsfor each of them. There can be no assurance that suchcoverage will continue for any issuer during the life of theTrust or that the report on any such issuer will continue tobe favorable. A downgrade in an analyst’srecommendation for an issuer of Securities held by theTrust, or the termination of such coverage, could negativelyaffect the performance of the Trust.

Principal Risks. As with all investments, you can losemoney by investing in this Trust. The Trust also might notperform as well as you expect. This can happen forreasons such as these:

• Prices of the securities in the Trust willfluctuate. The value of your investment may fallover time.

• An issuer of Securities held by the Trust maybe unwilling or unable to declare dividends inthe future, or may reduce the level ofdividends declared. This could result in areduction in the value of your Units.

• The financial condition of an issuer ofSecurities held by the Trust may worsen orits credit ratings may drop, resulting in areduction in the value of your Units. This mayoccur at any point in time, including during the initialoffering period.

• The Trust is concentrated in securities issuedby companies in the industrials, financialservices, health care, utility, consumerstaples and energy industries. Negativedevelopments in these industries will affect thevalue of your investment more than would be thecase in a more diversified investment.

• The Trust may be more sensitive to changesin interest rates than the broader market.The Trust invests significantly in securities issued bycompanies in the financial services and utilityindustries, and, as a result of its expected higherdividend yield relative to the broader market, theTrust is expected to exhibit greater sensitivity tomovements in interest rates than the broadermarket.

• We do not actively manage the Trust. Exceptin limited circumstances, the Trust will hold, and, inconnection with sales of addit ional Units toinvestors continue to buy, the same securities evenif their market value declines.

2

Central Equity Trust

Fee Table

The amounts below are estimates of the direct and indirect expensesthat you may incur based on a $10 Public Offering Price per Unit. Actualexpenses may vary.

As a % ofPublic Amount

Offering Per 1,000Sales Charge Price Units_________ _________

Maximum sales charge 3.500% $350.000______ _____________ _______

As a % Amountof Net Per 1,000Assets Units_________ _________

Estimated Organization Costs 0.521% $50.000______ _____________ _______

Estimated Annual Expenses Trustee’s fee and operating expenses 0.208% $19.969Supervisory fee, bookkeeping

and administrative fees 0.042 4.000______ _______

Total 0.250% $23.969______ _____________ _______

Example

This example helps you compare the cost of the Trust with other unittrusts and mutual funds. In the example we assume that the expenses do notchange and that the Trust’s annual return is 5%. Your actual returns andexpenses will vary, potentially materially. Based on these assumptions, youwould pay the following expenses for every $10,000 you invest in Units of theTrust. These amounts are the same regardless of whether you sell yourinvestments at the end of a period or continue to hold your investment.

1 year $ 424

3 years 473

4 years (life of Trust) 499

The maximum sales charge is 3.50% of the Public Offering Price perUnit (equivalent to 3.627% of the aggregate value of Securities per Unit).A reduced sales charge applies to certain transactions. See “PublicOffering--Reducing Your Sales Charge”.

Essential Information

Unit Price at Initial Date of Deposit $10.0000

Initial Date of Deposit July 20, 2010

Mandatory Termination Date July 22, 2014

Estimated Net Annual Income* $0.26251 per Unit

Estimated Initial Distribution* $0.02 per Unit

Record Dates 10th day of March, June,September and December

Distribution Dates 25th day of March, June,September and December

CUSIP Number Cash – 92120Y420

Reinvest – 92120Y438

* As of close of business day prior to Initial Date of Deposit. The actualdistributions you receive will vary from the estimated amount due to changesin the Trust’s fees and expenses, in actual income received by the Trust,currency fluctuations and with changes in the Trust such as the acquisition orliquidation of securities. See “Rights of Unitholders--Estimated Distributions.”

3

Central Equity Trust

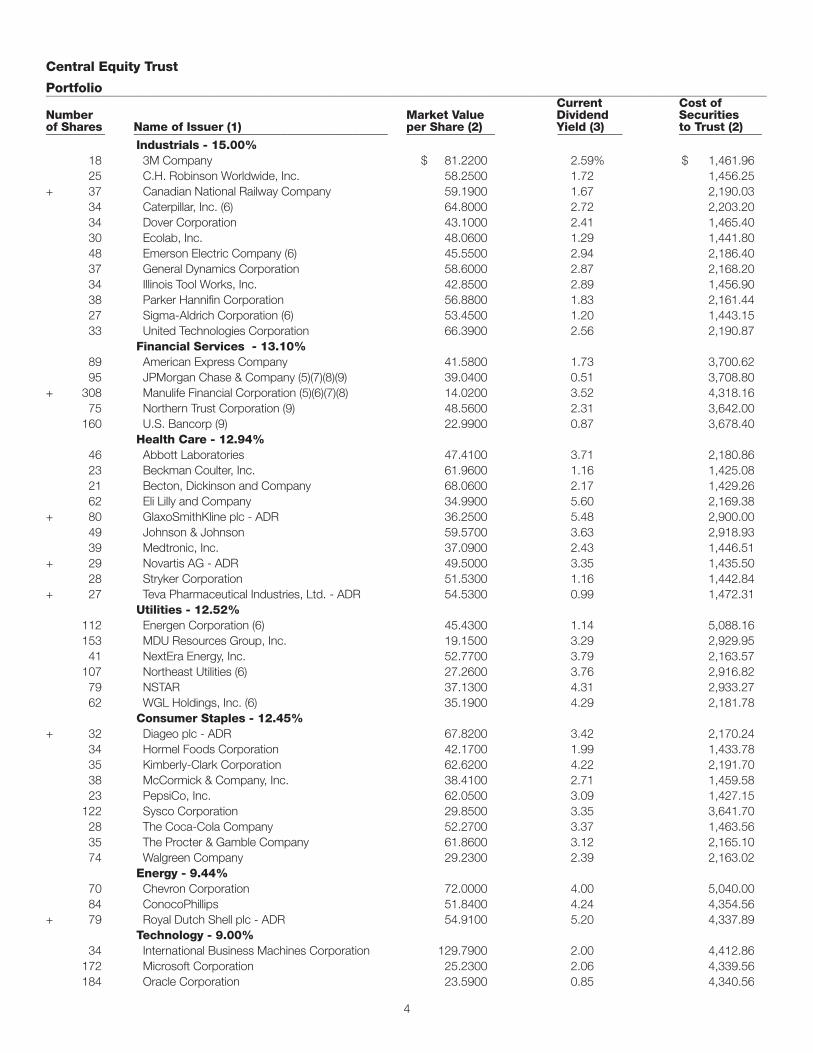

Portfolio__________________________________________________________________________________________________________________________Current Cost of

Number Market Value Dividend Securities of Shares Name of Issuer (1) per Share (2) Yield (3) to Trust (2) __________ ___________________________________________ _______________ ___________ ______________

Industrials - 15.00%18 3M Company $ 81.2200 2.59% $ 1,461.9625 C.H. Robinson Worldwide, Inc. 58.2500 1.72 1,456.25

+ 37 Canadian National Railway Company 59.1900 1.67 2,190.0334 Caterpillar, Inc. (6) 64.8000 2.72 2,203.2034 Dover Corporation 43.1000 2.41 1,465.4030 Ecolab, Inc. 48.0600 1.29 1,441.8048 Emerson Electric Company (6) 45.5500 2.94 2,186.4037 General Dynamics Corporation 58.6000 2.87 2,168.2034 Illinois Tool Works, Inc. 42.8500 2.89 1,456.9038 Parker Hannifin Corporation 56.8800 1.83 2,161.4427 Sigma-Aldrich Corporation (6) 53.4500 1.20 1,443.1533 United Technologies Corporation 66.3900 2.56 2,190.87

Financial Services - 13.10%89 American Express Company 41.5800 1.73 3,700.6295 JPMorgan Chase & Company (5)(7)(8)(9) 39.0400 0.51 3,708.80

+ 308 Manulife Financial Corporation (5)(6)(7)(8) 14.0200 3.52 4,318.1675 Northern Trust Corporation (9) 48.5600 2.31 3,642.00

160 U.S. Bancorp (9) 22.9900 0.87 3,678.40Health Care - 12.94%

46 Abbott Laboratories 47.4100 3.71 2,180.8623 Beckman Coulter, Inc. 61.9600 1.16 1,425.0821 Becton, Dickinson and Company 68.0600 2.17 1,429.2662 Eli Lilly and Company 34.9900 5.60 2,169.38

+ 80 GlaxoSmithKline plc - ADR 36.2500 5.48 2,900.0049 Johnson & Johnson 59.5700 3.63 2,918.9339 Medtronic, Inc. 37.0900 2.43 1,446.51

+ 29 Novartis AG - ADR 49.5000 3.35 1,435.5028 Stryker Corporation 51.5300 1.16 1,442.84

+ 27 Teva Pharmaceutical Industries, Ltd. - ADR 54.5300 0.99 1,472.31Utilities - 12.52%

112 Energen Corporation (6) 45.4300 1.14 5,088.16153 MDU Resources Group, Inc. 19.1500 3.29 2,929.9541 NextEra Energy, Inc. 52.7700 3.79 2,163.57

107 Northeast Utilities (6) 27.2600 3.76 2,916.8279 NSTAR 37.1300 4.31 2,933.2762 WGL Holdings, Inc. (6) 35.1900 4.29 2,181.78

Consumer Staples - 12.45%+ 32 Diageo plc - ADR 67.8200 3.42 2,170.24

34 Hormel Foods Corporation 42.1700 1.99 1,433.7835 Kimberly-Clark Corporation 62.6200 4.22 2,191.7038 McCormick & Company, Inc. 38.4100 2.71 1,459.5823 PepsiCo, Inc. 62.0500 3.09 1,427.15

122 Sysco Corporation 29.8500 3.35 3,641.7028 The Coca-Cola Company 52.2700 3.37 1,463.5635 The Procter & Gamble Company 61.8600 3.12 2,165.1074 Walgreen Company 29.2300 2.39 2,163.02

Energy - 9.44%70 Chevron Corporation 72.0000 4.00 5,040.0084 ConocoPhillips 51.8400 4.24 4,354.56

+ 79 Royal Dutch Shell plc - ADR 54.9100 5.20 4,337.89Technology - 9.00%

34 International Business Machines Corporation 129.7900 2.00 4,412.86172 Microsoft Corporation 25.2300 2.06 4,339.56184 Oracle Corporation 23.5900 0.85 4,340.56

4

5

Central Equity Trust

Portfolio (continued)__________________________________________________________________________________________________________________________Current Cost of

Number Market Value Dividend Securities of Shares Name of Issuer (1) per Share (2) Yield (3) to Trust (2) __________ ___________________________________________ _______________ ___________ ______________

Consumer Cyclicals - 8.53%36 Fortune Brands, Inc. $ 40.8100 1.86% $ 1,469.16

182 Lowe’s Companies, Inc. 19.9300 2.21 3,627.2673 Target Corporation 50.2300 1.99 3,666.7950 V.F. Corporation 72.7900 3.30 3,639.50

Telecommunications - 4.00%117 AT&T, Inc. 24.8800 6.75 2,910.96

+ 131 Vodafone Group plc - ADR 22.2200 5.58 2,910.82REITs - 3.02%

142 Realty Income Corporation 30.9900 5.56 4,400.58__________ _____________

3,855 $ 145,474.13__________ _______________________ _____________

See “Notes to Portfolio”.

6

Notes to Portfolio

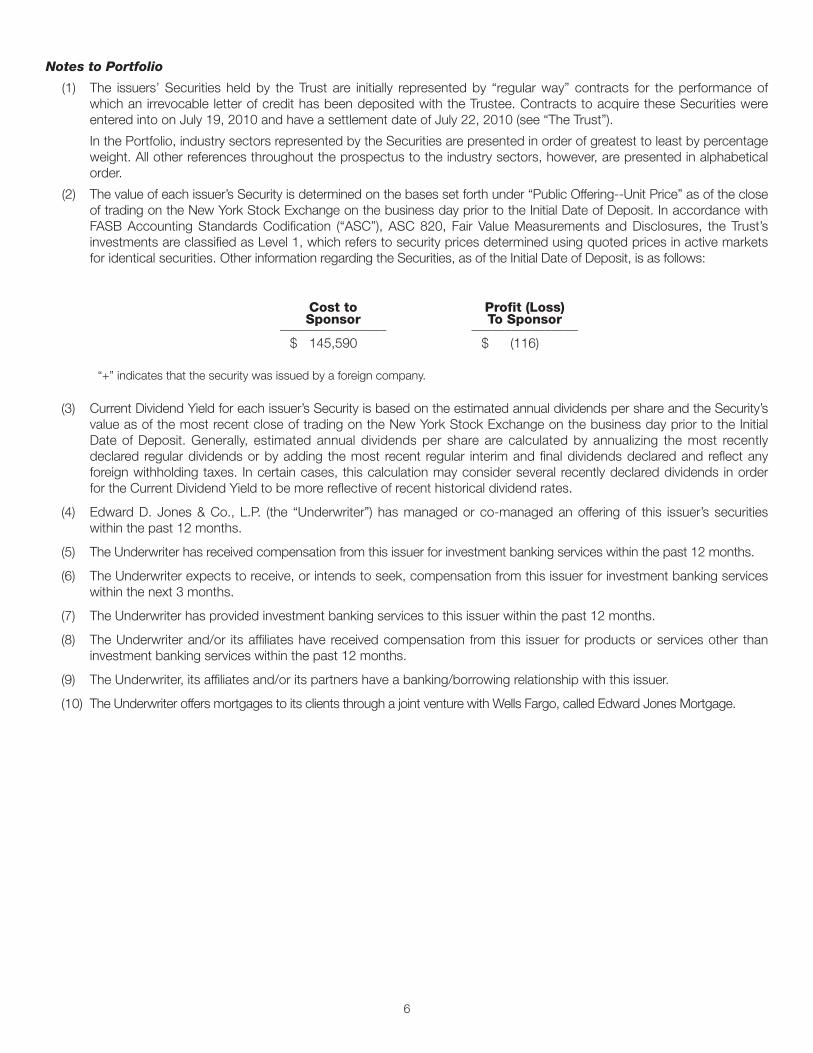

(1) The issuers’ Securities held by the Trust are initially represented by “regular way” contracts for the performance ofwhich an irrevocable letter of credit has been deposited with the Trustee. Contracts to acquire these Securities wereentered into on July 19, 2010 and have a settlement date of July 22, 2010 (see “The Trust”).

In the Portfolio, industry sectors represented by the Securities are presented in order of greatest to least by percentageweight. All other references throughout the prospectus to the industry sectors, however, are presented in alphabeticalorder.

(2) The value of each issuer’s Security is determined on the bases set forth under “Public Offering--Unit Price” as of the closeof trading on the New York Stock Exchange on the business day prior to the Initial Date of Deposit. In accordance withFASB Accounting Standards Codification (“ASC”), ASC 820, Fair Value Measurements and Disclosures, the Trust’sinvestments are classified as Level 1, which refers to security prices determined using quoted prices in active marketsfor identical securities. Other information regarding the Securities, as of the Initial Date of Deposit, is as follows:

Cost to Profit (Loss)Sponsor To Sponsor________________ ________________

$ 145,590 $ (116)

“+” indicates that the security was issued by a foreign company.

(3) Current Dividend Yield for each issuer’s Security is based on the estimated annual dividends per share and the Security’svalue as of the most recent close of trading on the New York Stock Exchange on the business day prior to the InitialDate of Deposit. Generally, estimated annual dividends per share are calculated by annualizing the most recentlydeclared regular dividends or by adding the most recent regular interim and final dividends declared and reflect anyforeign withholding taxes. In certain cases, this calculation may consider several recently declared dividends in orderfor the Current Dividend Yield to be more reflective of recent historical dividend rates.

(4) Edward D. Jones & Co., L.P. (the “Underwriter”) has managed or co-managed an offering of this issuer’s securitieswithin the past 12 months.

(5) The Underwriter has received compensation from this issuer for investment banking services within the past 12 months.

(6) The Underwriter expects to receive, or intends to seek, compensation from this issuer for investment banking serviceswithin the next 3 months.

(7) The Underwriter has provided investment banking services to this issuer within the past 12 months.

(8) The Underwriter and/or its affiliates have received compensation from this issuer for products or services other thaninvestment banking services within the past 12 months.

(9) The Underwriter, its affiliates and/or its partners have a banking/borrowing relationship with this issuer.

(10) The Underwriter offers mortgages to its clients through a joint venture with Wells Fargo, called Edward Jones Mortgage.

7

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Unitholders of Central Equity Trust, Diversified Income Series 36 (Van Kampen Unit Trusts, Series 992):

We have audited the accompanying statement of condition including the related portfolio of Central Equity Trust,Diversified Income Series 36 (included in Van Kampen Unit Trusts, Series 992) as of July 20, 2010. The statement ofcondition is the responsibility of the Sponsor. Our responsibility is to express an opinion on such statement ofcondition based on our audit.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (UnitedStates). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether thestatement of condition is free of material misstatement. The trust is not required to have, nor were we engaged toperform, an audit of its internal control over financial reporting. Our audit included consideration of internal control overfinancial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for thepurpose of expressing an opinion on the effectiveness of the trust’s internal control over financial reporting. Accordingly,we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts anddisclosures in the statement of condition, assessing the accounting principles used and significant estimates made by theSponsor, as well as evaluating the overall statement of condition presentation. Our procedures included confirmation withThe Bank of New York Mellon, Trustee, of cash or an irrevocable letter of credit deposited for the purchase of Securities asshown in the statement of condition as of July 20, 2010. We believe that our audit of the statement of condition providesa reasonable basis for our opinion.

In our opinion, the statement of condition referred to above presents fairly, in all material respects, the financialposition of Central Equity Trust, Diversified Income Series 36 (included in Van Kampen Unit Trusts, Series 992) as of July20, 2010, in conformity with accounting principles generally accepted in the United States of America.

/s/ GRANT THORNTON LLP

New York, New YorkJuly 20, 2010

8

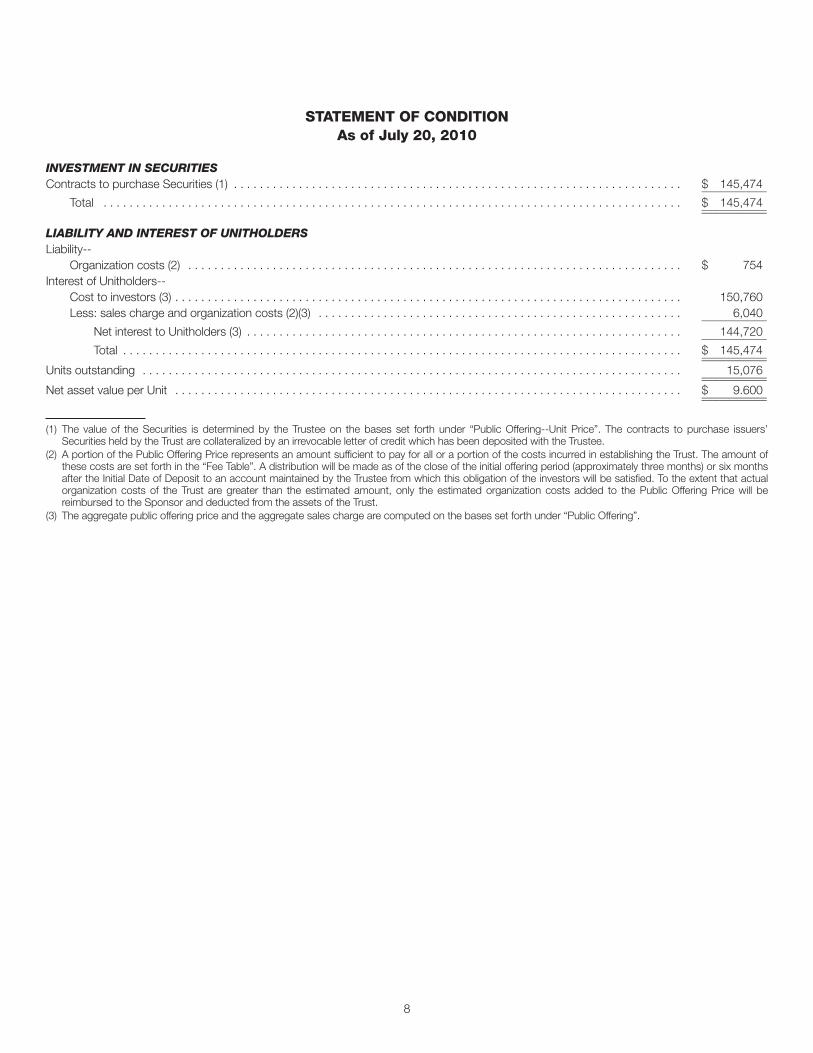

STATEMENT OF CONDITIONAs of July 20, 2010

INVESTMENT IN SECURITIESContracts to purchase Securities (1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 145,474___________

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 145,474______________________

LIABILITY AND INTEREST OF UNITHOLDERSLiability--

Organization costs (2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 754Interest of Unitholders--

Cost to investors (3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 150,760Less: sales charge and organization costs (2)(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,040___________

Net interest to Unitholders (3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 144,720___________Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 145,474______________________

Units outstanding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15,076______________________Net asset value per Unit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 9.600______________________

(1) The value of the Securities is determined by the Trustee on the bases set forth under “Public Offering--Unit Price”. The contracts to purchase issuers’Securities held by the Trust are collateralized by an irrevocable letter of credit which has been deposited with the Trustee.

(2) A portion of the Public Offering Price represents an amount sufficient to pay for all or a portion of the costs incurred in establishing the Trust. The amount ofthese costs are set forth in the “Fee Table”. A distribution will be made as of the close of the initial offering period (approximately three months) or six monthsafter the Initial Date of Deposit to an account maintained by the Trustee from which this obligation of the investors will be satisfied. To the extent that actualorganization costs of the Trust are greater than the estimated amount, only the estimated organization costs added to the Public Offering Price will bereimbursed to the Sponsor and deducted from the assets of the Trust.

(3) The aggregate public offering price and the aggregate sales charge are computed on the bases set forth under “Public Offering”.

THE TRUST

The Trust was created under the laws of the State of NewYork pursuant to a Trust Indenture and Trust Agreement (the“Trust Agreement”), dated the date of this prospectus (the“Initial Date of Deposit”), among Van Kampen Funds Inc., asSponsor, Van Kampen Asset Management, as Supervisor,and The Bank of New York Mellon, as Trustee.

The Trust offers the opportunity to purchase Unitsrepresenting proportionate interests in a portfolio of activelytraded equity securities. The Trust may be an appropriatemedium for investors who desire to participate in a portfolioof common stocks with greater diversification than theymight be able to acquire individually.

On the Initial Date of Deposit, the Sponsor depositeddelivery statements relating to contracts for the purchase ofthe issuers’ Securities, as defined in the last sentence of thisparagraph, and an irrevocable letter of credit in the amountrequired for these purchases with the Trustee. In exchangefor these contracts the Trustee delivered to the Sponsordocumentation evidencing the ownership of Units of theTrust. Unless otherwise terminated as provided in the TrustAgreement, the Trust will terminate on the MandatoryTermination Date and any remaining Securities will beliquidated or distributed by the Trustee within a reasonabletime. As used in this prospectus the term “Securities”means the securities (including contracts to purchase thesesecurities) listed in the “Portfolio” and any additionalsecurities deposited into the Trust.

Additional Units may be issued at any time by depositingin the Trust (i) additional Securities, (ii) contracts to purchaseSecurities together with cash or irrevocable letters of creditor (iii) cash (or a letter of credit or the equivalent) withinstructions to purchase additional Securities. As additionalUnits are issued by the Trust, the aggregate value of theSecurities may be increased and the fractional undividedinterest represented by each Unit will be decreased. TheSponsor may continue to make additional deposits into theTrust following the Initial Date of Deposit, provided that theadditional deposits will be in amounts which will maintain, asnearly as practicable, the same percentage relationshipamong the number of shares of each Security in the Trust’sportfolio as existed immediately prior to the subsequentdeposit. Investors may experience a dilution of theirinvestments and a reduction in their anticipated incomebecause of fluctuations in the prices of the Securitiesbetween the time of the deposit and the purchase of theSecurities and because the Trust will pay the associatedbrokerage or acquisition fees. Purchases and sales ofSecurit ies by the Trust may impact the value of theSecurities. This may especially be the case during the initialoffering of Units, upon Trust termination and in the course ofsatisfying large Unit redemptions.

Each Unit of the Trust initially offered represents anundivided interest in the Trust. At the close of the New YorkStock Exchange on the Initial Date of Deposit, the number

of Units may be adjusted so that the Public Offering Priceper Unit equals $10. The number of Units, fractionalundivided interest of each Unit in the Trust and theestimated distributions per Unit will increase or decrease tothe extent of any adjustment. To the extent that any Unitsare redeemed by the Trustee or additional Units are issuedas a result of additional Securities being deposited by theSponsor, the fractional undivided interest in the Trustrepresented by each unredeemed Unit will increase ordecrease accordingly, although the actual interest in theTrust will remain unchanged. Units will remain outstandinguntil redeemed upon tender to the Trustee by Unitholders,which may include the Sponsor, or until the termination ofthe Trust Agreement.

The Trust consists of (a) the Securit ies ( includingcontracts for the purchase thereof) listed under “Portfolio”as may continue to be held from time to time in the Trust, (b)any additional Securities acquired and held by the Trustpursuant to the provisions of the Trust Agreement and (c)any cash held in the related Income and Capital Accounts.Neither the Sponsor nor the Trustee shall be liable in anyway for any contract failure in any of the Securities.

OBJECTIVE AND SECURITIES SELECTION

The Trust seeks capital appreciation and dividend incomeby investing in a portfolio of shares of common stocks ofconsumer cyclicals companies, consumer staplescompanies, energy companies, f inancial services companies, health care companies, industrials companies,real estate investment trusts, technology companies,telecommunications companies and utilities. Please refer to“Portfolio” in Prospectus Part One for a presentation ofindustry sectors in order from greatest to least by percentageweight in your Trust. The portfolio consists of securitiesselected by research analysts at Edward D. Jones & Co., L.P.(the “Underwriter”) and approved by the Sponsor. Inselecting the Securities, the following factors, among others,were considered: dividend yield, dividend track record,dividend coverage, earnings growth rates, dividend growthrates, regulatory climate and stock valuation. At the time theSecurities were selected, the Underwriter’s research analystswere currently covering all the issuers of the Securities andhad published favorable recommendations for each of them.There can be no assurance that such coverage will continuefor any issuer of Securities held by the Trust during the life ofthe Trust or that the report on any such issuer will continue tobe favorable. A downgrade in an analyst’s recommendationfor an issuer of Securit ies held by the Trust, or thetermination of such coverage, could negatively affect theperformance of the Trust.

You should note that the selection criteria were applied tothe Securities for inclusion in the Trust as of the Initial Dateof Deposit. After this date, the Securities may no longermeet the selection criteria. Should a Security no longer meetthe selection criteria, we will generally not remove theSecurity from the portfolio.

A-1

Consumer Cyclicals. The Trust invests in companiesthat manufacture or sell products or services, the demandfor which is easi ly inf luenced by general economiccondit ions. Industr ies within this segment includeadvertising, auto parts, auto manufacturing, broadcasting,casinos, clothing and fabrics, consumer electronics,entertainment, footwear, furnishings and appliances, homeconstruction, lodging, publishing, recreational products andservices, restaurants, apparel retailers, broadline retailers,drug-based retailers, specialty retailers, tires and toys.These companies would be expected to perform well duringan improving economy but may lag during a decliningeconomy. Industries within this group that may holdpotential for above-average growth include niche retailing,entertainment and media. Many companies within thissector are becoming more dividends-focused, and mayincrease their dividends going forward.

Consumer Staples. The Trust invests in consumerstaples companies. Consumer staples is a relatively matureindustry, with growth in line with population growth. Recentwaves of consolidation in the industry have reduced thenumber of competitors, which has enabled product priceincreases in some sectors. Additionally, product innovationhas proven key to growth and should lead to above-industrygrowth rates for successful companies. The industry ischaracterized primarily by stable, high-profit margincompanies, several of which pay attractive dividends.

Energy. The Trust invests in energy companies. As theworld economy grows, energy use is also expected to rise.The companies that produce oil and natural gas are findingand developing new sources worldwide to satisfy thisgrowing need. Oil companies also refine crude oil into usefulproducts such as gasoline and jet fuel, as well as providethe raw materials for a wide variety of plastics. Investorsshould benefit from the diversity of their businesses, theirglobal reach, and their ability to find attractive opportunitiesin the changing energy marketplace.

Financial Services. The Trust invests in financialservices companies. As a large and integral part of theeconomy, financial services are like the oil that lubricates theeconomic engine. Nearly all consumers and businesses arecustomers of financial companies that provide services likesavings and investment products, loans, transaction andpayment processing, and insurance products that helpprotect against death and disaster. Secular drivers affectingfinancial-services business and profits include demographictrends and retirement needs, industry consolidation,technological advancements, and global izat ion ofeconomies and markets. Economic and interest-rate cyclescontinuously affect the shorter-term prospects for financialbusinesses. Financial companies generally exist in thebanking, consumer f inance, insurance, investmentmanagement and securities industries.

Health Care. The Trust invests in health carecompanies. These issuers include companies involved inadvanced medical devices and instruments, drugs and

biotec hnology, managed care, hospital management/healthservices and medical supplies. An aging population, newdrug development and product innovation should drivegrowth for this industry. Additionally, foreign demand forhealth care, particularly from developing nations, continuesto increase. The industry has historically grown at a ratefaster than the overall economy and that trend shouldcontinue. Research and development spending, supportedby strong demand, should lead to new products. Healthcare companies have traditionally paid part of earnings asdividends, which is expected to continue. Given the growthprospects for the industry, dividend growth should bemeaningful as well.

Industrials. The Trust invests in industrials companies.The industrials industry includes capital goods, commercialservices and transportation companies. Generally, growthprospects for the industry are tied to economic factors suchas consumer, business and government spending, U.S.Gross Domestic Product and exports to foreign nations. Theincreasingly global economy should increase the demandfor industrial products made by U.S. firms. Within capitalgoods, defense and electronics are some of the fastestgrowing areas, given the political support for highergovernment spending on defense init iat ives. Manyindustrials companies are well-established and havedemonstrated a track record of paying dividends andincreasing the amount of dividends paid over time.

Real Estate Investment Trusts. The Trust invests inreal estate investment trusts. A real estate investment trust, orREIT, is a company that buys, develops, finances and/ormanages income-producing real estate such as apartments,shopping centers, offices and warehouses. A REIT can be agood way to invest in commercial real estate. Compared totraditional direct investments in real estate, which may bedifficult to sell and value, REITs are traded on major stockexchanges, making them relatively liquid. REIT investors canalso gain the advantage of skilled management since REITmanagement teams tend to be experts within their specificproperty or geographic niches. Many believe that theattractive features of property ownership and stock ownershipare combined in this investment vehicle. REITs can provideinvestors with current income, as they are currently requiredto distribute 90% of taxable income annually, and can havethe potential for attractive returns. They have historically hadlow relative volatility and may provide inflation protection.

Technology. The Trust invests in technology companies.Technology companies generally include companiesinvolved in the development, design, manufacture and saleof computers, computer related equipment, computernetworks, communications systems, telecommunicationsproducts, electronic products, and other related products,systems and services. Technology is a cyclical industry,driven by corporate and consumer spending on technologyproducts, services and software. New technologies have thepotential to increase productivity and enable newapplications. Stable spending on traditional technology

A-2

platforms such as personal computers, plus spending onnew technologies, should enable the industry to grow fasterthan the economy. Several technology companies aregenerating substantial excess cash, which they have usedto begin paying dividends. These companies have thepotential to increase their dividends on a regular basis.

Telecommunications. The Trust invests intelecommunications companies. The emergence of a global,networked economy appears to be changing the face of thetelecommunications industry. Telecommunicationscompanies provide local, long distance and wirelesstelephone, as well as television and internet services andinformation systems, manufacture telecommunicationsproducts, and operate voice, data and telecommunicationsnetworks. Innovations, such as wireless and Internetapplications, are experiencing rapid demand. While theindustry is characterized by intense rivalry, heavy regulationand overcapacity in some markets, telecommunicationscompanies may be well-positioned to deliver these newtechnologies to consumers and businesses.

Utilities. The Trust invests in uti l i ty companies.Compared to the tradit ional government mandatedmonopolies, many states have pursued utility deregulation,which provides both opportunities and risk. While this couldprovide incremental growth for some, it may also increasethe level of competit ion for others. As a whole, thefundamentals of the utility sector have improved as thosecompanies that strayed in recent years into unrelatedbusinesses have generally refocused on their core businessof providing regulated electricity, natural gas and waterservice to their customers. This “return to basics” strategyhas helped increase cash flow, strengthen balance sheetsand solidify credit quality for many companies. It has alsoallowed many utilities to continue their long track records ofpaying dividends while providing increases in the dividendon a frequent and consistent basis.

Underwriter Activities. The Underwriter mayrecommend or effect transactions in the Securities in its dayto day brokerage activities. This may have an adverse effecton the prices of the Securities. This also may have animpact on the price the Trust pays for the Securities and theprice received upon Unit redemptions or Trust termination.From time to time, the Underwriter may engage in othertransactions with the issuers of the Securities. See “Notes toPortfolio” and “Trust Administration--Underwriter” for moreinformation regarding potential conflicts of interest arisingfrom such Underwriter activities.

RISK FACTORS

All investments involve risk. This section describes themain risks that can impact the value of your Units. Youshould understand these risks before you invest. If the valueof the Securities falls, the value of your Units will also fall. Wecannot guarantee that your Trust will achieve its objective orthat your investment return will be positive over any period.

Market Risk. Market risk is the risk that the value of thesecurities in your Trust will fluctuate. This could cause thevalue of your Units to fall below your original purchase price.Market value fluctuates in response to various factors.These can include changes in interest rates, inflation, thefinancial condition of a security’s issuer, perceptions of theissuer, or ratings on a security of the issuer. Even thoughyour Trust is supervised, you should remember that we donot manage your Trust. Your Trust will not sell a securitysolely because the market value falls as is possible in amanaged fund.

Interest Rate Risk. The Trust invests significantly insecurities issued by companies in the financial services andutilities industries, and, as a result of its expected higherdividend yield relative to the broader market, the portfolio isexpected to exhibit greater sensitivity to movements ininterest rates than the broader market.

Dividend Payment Risk. Dividend payment risk is therisk that an issuer of a security is unwilling or unable to paydividends on a security. Stocks represent ownershipinterests in the issuers and are not obligations of the issuers.Common stockholders have a right to receive dividends onlyafter the company has provided for payment of its creditors,bondholders and preferred stockholders. Common stocksdo not assure dividend payments. Dividends are paid onlywhen declared by an issuer’s board of directors at theirdiscretion, and the amount of any dividend may vary overtime. If dividends received by the Trust are insufficient tocover expenses, redemptions or other Trust costs, it may benecessary for the Trust to sell Securities to cover suchexpenses, redemptions or other costs. Any such sales mayresult in capital gains or losses to you. See “Taxation”.

Consumer Cyclicals. The Trust invests in consumercyclicals companies. The success of companies in theconsumer cyclicals sector depends heavily on consumerspending and disposable household income and is subjectto severe competition. General risks of these companiesinclude the general state of the economy, intensecompetition and consumer spending trends. A recessionaryeconomic climate with the consequent slowdown inemployment growth, less favorable trends in unemploymentor a marked deceleration in real disposable personal incomegrowth could result in significant pressure on both consumerwealth and consumer confidence, adversely affectingconsumer spending habits. A weak economy and its effecton consumer spending would likely hurt the consumercyclicals industry. The success of companies in theconsumer cyclicals segment is also strongly affected bychanges in demographics and consumer tastes.

Consumer Staples. The Trust invests in companiesthat manufacture or sell various consumer staples. Generalrisks of these companies include the general state of theeconomy, intense competition and consumer spendingtrends. Weakness in the banking or real estate industry, arecessionary economic climate with the consequentslowdown in employment growth, less favorable trends in

A-3

unemployment or a marked deceleration in real disposablepersonal income growth could result in significant pressureon both consumer wealth and consumer confidence,adversely affecting consumer spending habits. Furthermore,the failure to continue developing new products, lack of orreduced market acceptance of new and existing products,increased raw materials costs, an inability to raise prices,increased or changed regulation and product liability claimsor product recal ls could also adversely impact theperformance and stock prices of the issuers of Securities inthis industry group.

Energy. The Trust invests in energy companies. Energycompanies are subject to legislative or regulatory changes,adverse market conditions and/or increased competitionaffecting the energy sector. The prices of the securities ofenergy companies may fluctuate widely due to changes invalue and dividend yield, which depend largely on the priceand supply of energy fuels, international political eventsrelating to oil producing countries, energy conservation, thesuccess of exploration projects, and tax and othergovernmental regulatory policies.

Energy companies depend on their ability to find andacquire additional energy reserves. The exploration andrecovery process involves significant operating hazards andcan be very costly. An energy company has no assurancethat it will find reserves or that any reserves found will beeconomical ly recoverable. The industry also facessubstantial government regulation, including environmentalregulation. These regulations have increased costs andlimited production and usage of certain fuels. Furthermore,certain companies involved in the industry have also facedscrutiny for alleged accounting irregularities that may haveled to the overstatement of their financial results, and othercompanies in the industry may face similar scrutiny.

In addition, energy companies face risks related topolitical conditions in oil producing regions (such as theMiddle East), the actions of the Organization of PetroleumExporting Countries (OPEC), the price and worldwide supplyof oil and natural gas, the price and availability of alternativefuels, operating hazards, government regulation and thelevel of consumer demand. Political conditions of some oilproducing regions have been unstable in the past. Politicalinstability or war in these regions could have a negativeimpact on your investment. Oil and natural gas prices canbe extremely volatile. OPEC controls a substantial portion ofworld oil production. OPEC may take actions to increase orsuppress the price or availability of oil. Various domestic andforeign government authorities and international cartels alsoimpact these prices. Any substantial decline in these pricescould have an adverse effect on energy companies.

Financial Services. The Trust invests in banks,insurance companies and other financial services companies.Banks and their holding companies are especially subject tothe adverse effects of economic recession, volatile interestrates, portfolio concentrations in geographic markets and incommercial and residential real estate loans, and competition

from new entrants in their fields of business. In addition,banks and their holding companies are extensively regulatedat both the federal and state level and may be adverselyaffected by increased regulation.

The effects of the global financial crisis that began tounfold in 2007 continue to manifest in nearly all thesub-divisions of the financial services industry. Financiallosses and write downs among investment banks andsimilar institutions reached significant levels in 2008. Theimpact of these losses among traditional banks, investmentbanks, broker/dealers and insurers has forced a number ofsuch large institutions into either liquidation or combination,while drastically increasing the credit risk, and possibility ofdefault, of bonds issued by such institutions faced withthese troubles. Many of the institutions are having difficultyin accessing credit markets to finance their operations andin maintaining appropriate levels of equity capital. In somecases, U.S. and foreign governments have acted to bail outor provide support to select institutions, however the risk ofdefault by such issuers has nonetheless increasedsubstantially.

While the U.S. and foreign governments, and theirrespective government agencies, have taken steps toaddress problems in the financial markets and with financialinstitutions, there can be no assurance that the risksassociated with investment in financial services companyissuers will decrease as a result of these steps.

Banks face increased competition from nontraditionallending sources, as regulatory changes, such as theGramm-Leach-Bli ley Act f inancial services overhaullegislation, permit new entrants to offer various financialproducts. Technological advances such as the Internet allowthese nontraditional lending sources to cut overhead andpermit the more efficient use of customer data. Bankscontinue to face tremendous pressure from mutual funds,brokerage firms and other financial service providers in thecompetition to furnish services that were traditionally offeredby banks. Bank profitability is largely dependent on theavailability and cost of capital funds, and can fluctuatesignificantly when interest rates change or due to increasedcompetition.

Companies engaged in investment management andbrokerage activities are subject to volatility in their earningsand share prices that often exceeds the volatility of the equitymarket in general. Adverse changes in the direction of thestock market, investor confidence, the financial health ofcustomers, equity transaction volume, the level and directionof interest rates and the outlook of emerging markets couldadversely affect the financial stability, as well as the stockprices, of these companies. Economic conditions in the realestate markets have deteriorated and have had a substantialnegative effect upon banks because they generally have aportion of their assets invested in loans secured by realestate. Additionally, competitive pressures, includingincreased competition with new and existing competitors,the ongoing commoditization of traditional businesses and

A-4

the need for increased capital expenditures on newtechnology could adversely impact the profit margins ofcompanies in the investment management and brokerageindustries. Companies involved in investment managementand brokerage activities are also subject to extensiveregulation by government agencies and self-regulatoryorganizations, and changes in laws, regulations or rules, or inthe interpretation of such laws, regulations and rules, couldadversely affect the stock prices of such companies.

Companies involved in the insurance, reinsurance andrisk management industry underwrite, sell or distributeproperty, casualty and business insurance. Many factorsaffect insurance, reinsurance and risk managementcompany profits, including interest rate movements, theimposition of premium rate caps, a misapprehension of therisks involved in given underwritings, competition andpressure to compete globally, weather catastrophes or othernatural or man-made disasters and the effects of clientmergers. Already extensively regulated, insurancecompanies’ profits may be adversely affected by increasedgovernment regulation or tax law changes.

Health Care. The Trust invests in health care companies.These issuers include companies involved in advancedmedical devices and instruments, drugs and biotec hnology,managed care, hospital management/health services andmedical supplies. These companies face substantialgovernment regulation and approval procedures. Legislativeproposals concerning health care are proposed in Congressfrom time to time. These proposals span a wide range oftopics, including cost and price controls (which might includea freeze on the prices of prescription drugs), national healthinsurance, incentives for competition in the provision ofhealthcare services, tax incentives and penalties related tohealthcare insurance premiums and promotion of pre-paidhealthcare plans. The government could also reduce fundingfor health care related research. The Sponsor and theUnderwriter are unable to predict the effect of any of theseproposals, if enacted, on the issuers of Securities in the Trust.

Drug and medical products companies also face therisk of increasing competition from new products orservices, generic drug sales, termination of patentprotection for drug or medical supply products and the riskthat a product will never come to market. The researchand development costs of bringing a new drug or medicalproduct to market are substantial. This process involveslengthy government review with no guarantee of approval.These companies may have losses and may not offerproposed products for several years, if at all. The failure togain approval for a new drug or product or to maintainexist ing approval and related l i t igat ion can have asubstantial negative impact on a company and its stock.The goods and services of health care issuers are alsosubject to risks of product liability litigation.

Health care facility operators face risks related to demandfor services, the ability of the facility to provide requiredservices, confidence in the facility, management capabilities,

competition, efforts by insurers and government agencies tolimit rates, expenses, the cost and possible unavailability ofmalpractice insurance, and termination or restriction ofgovernment financial assistance (such as Medicare,Medicaid or similar programs).

Industrials. The Trust invests in industrials companies.General risks of industrials companies include the generalstate of the economy, intense competition, consolidation,domestic and international politics, excess capacity andconsumer spending trends. Capital goods companies mayalso be significantly affected by overall capital spending andleverage levels, economic cycles, technical obsolescence,delays in modernization, limitations on supply of keymaterials, labor relat ions, government regulat ions,government contracts and e-commerce initiatives.

Industrials companies may also be affected by factorsmore specific to their individual industries. Industrialmachinery manufacturers may be subject to declines incommercial and consumer demand and the need formodernization. Aerospace and defense companies may beinfluenced by decreased demand for new equipment,aircraft order cancellations, disputes over or ability to obtainor retain government contracts, labor disputes, changes ingovernment budget priorities, changes in aircraft-leasingcontracts and cutbacks in profitable business travel. Thenumber of housing starts, levels of public and non-residential construction including weakening demand fornew office and retail space, and overall constructionspending may adversely affect construction materials andequipment manufacturers.

Real Estate Investment Trusts. The Trust invests in REITs. Many factors can have an adverse impact on theperformance of a particular REIT, including its cash availablefor distribution, the credit quality of a particular REIT or thereal estate industry generally. The success of REITs dependson various factors, including the quality of propertymanagement, occupancy and rent levels, appreciation ofthe underlying property and the ability to raise rents onthose properties. Economic recession, over-building, tax lawchanges, environmental issues, higher interest rates orexcessive speculation can all negatively impact REITs andtheir future earnings and share prices.

Risks associated with the direct ownership of real estateinclude, among other factors,

• general U.S. and global as wel l as localeconomic conditions;

• decline in real estate values;

• possible lack of availability of mortgage funds;

• the financial health of tenants;

• over-building and increased competition fortenants;

• oversupply of properties for sale;

• changing demographics;

A-5

• changes in interest rates, tax rates and otheroperating expenses;

• changes in government regulations;

• changes in zoning laws;

• the ability of the owner to provide adequatemanagement, maintenance and insurance;

• faulty construction and the ongoing need forcapital improvements;

• the cost of complying with the Americans withDisabilities Act;

• regulatory and judicial requirements, includingrelating to liability for environmental hazards;

• natural or man-made disasters;

• changes in the perception of prospective tenantsof the safety, convenience and attractiveness ofthe properties;

• the ongoing financial strength and viability ofgovernment sponsored enterprises, such asFannie Mae and Freddie Mac;

• changes in neighborhood values and buyerdemand; and

• the unavailability of construction financing ormortgage loans at rates acceptable todevelopers.

Variations in rental income and space availability andvacancy rates in terms of supply and demand are additionalfactors affecting real estate generally and REITs in particular.Properties owned by a REIT may not be adequately insuredagainst certain losses and may be subject to significantenvironmental liabilities, including remediation costs.

You should also be aware that REITs may not bediversified and are subject to the risks of financing projects.The real estate industry may be cyclical, and, if the Trustacquires REIT Securities at or near the top of the cycle,there is increased risk of a decline in value of the REITSecurities and therefore the value of the Units. REITs arealso subject to defaults by borrowers and the market’sperception of the REIT industry generally.

Because of their structure, and the legal requirement thatthey distribute at least 90% of their taxable income toshareholders annually, REITs require frequent amounts ofnew funding, through both borrowing money and issuingstock. Thus, REITs historically have frequently issuedsubstantial amounts of new equity shares (or equivalents) topurchase or build new properties. This may have adverselyaffected REIT equity share market prices. Both existing andnew share issuances may have an adverse effect on theseprices in the future, especially when REITs continue to issuestock when real estate prices are relatively high and stockprices are relatively low.

Technology. The Trust invests in technologycompanies. Technology companies face risks related to

rapidly changing technology, rapid product obsolescence,cyclical market patterns and intense competition, evolvingindustry standards and frequent new product introductions.An unexpected change in technology can have a significantnegative impact on a technology company. The failure of atechnology company to introduce new products ortechnologies or keep pace with rapidly changingtechnology, can have a negative impact on the company’sresults. Technology stocks tend to experience substantialprice volatility and speculative trading. Announcementsabout new products, technologies, operating results ormarketing alliances can cause stock prices to fluctuatedramatically. At times, however, extreme price and volumefluctuations may occur in the Securities of companies inthis industry group that are unrelated to the operatingperformance of the company.

The market for certain products may have only recentlybegun to develop, is rapidly evolving or is characterized byan increase in suppliers. Key components of sometechnology products are available only from limited sources.This can impact the cost of and ability to acquire thesecomponents. Some technology companies service highlyconcentrated customer bases of only a limited number oflarge companies. Any failure to meet the standards of thesecustomers could result in a significant loss or reduction insales. Many products and technologies are incorporatedinto other products. As a result, some companies aresometimes highly dependent on the performance of othertechnology companies. We cannot guarantee that thesecustomers will continue to place additional orders or willplace orders in similar quantities as in the past.

The life cycle of a new technology product or servicetends to be short, resulting in volatile sales, earnings andstock prices for many technology companies. Additionally,with the rapid evolution of technologies, competitiveadvantages tend to be short lived and product pricingusually falls. Historically, many of the benefits from newtechnologies have gone to the consumer, as their creatorshave been unable to retain differentiation or pricing power.Some of the large technology companies have beeninvolved in antitrust litigation and may continue to be in thefuture. A slowdown in corporate or consumer spending ontechnology will likely hurt technology company revenues.Technology companies rely on international sales for ameaningful part of their revenues. Any economic slowdowncould hurt revenues.

Telecommunications. Because your Trust invests insecurities of issuers in the telecommunications industry, thevalue of the Units may be susceptible to factors affecting thetelecommunications industry. The telecommunications industryis subject to governmental regulation. For example, the UnitedStates government and state governments regulate permittedrates of return and the kinds of services that a company mayoffer. The products and services of telecommunicationscompanies may become outdated very rapidly. A company’sperformance can be hurt if the company fails to keep pace

A-6

with technological advances. These factors could affect thevalue of Units. Certain types of companies represented in aportfolio are engaged in fierce competition for a share of themarket of their products and may have higher costs, includingliabil it ies associated with the medical, pension andpostretirement expenses of their workforce, than theircompetitors. As a result, competitive pressures are intenseand the stocks are subject to rapid price volatility.

Several high-profile bankruptcies of large telecommunicationscompanies in the past have illustrated the potentially unstablecondition of the telecommunications industry. High debt loadsthat were accumulated during the industry growth spurt of the1990s caught up to the industry, causing debt and stockprices to trade at distressed levels for manytelecommunications companies and increasing the cost ofcapital for needed additional investment. At the same time,demand for some telecommunications services remainsweak, as several key markets are oversaturated and manycustomers can choose between several service providers andtechnology platforms. To meet increasing competition,companies may have to commit substantial capital,particularly in the formulation of new products and servicesusing new technologies. As a result, many companies havebeen compelled to cut costs by reducing their workforce,outsourcing, consolidating and/or closing existing facilitiesand divesting low selling product lines. Furthermore, certaincompanies involved in the industry have also faced scrutinyfor alleged accounting irregularities that may have led to theoverstatement of their financial results, and other companiesin the industry may face similar scrutiny. Moreover, somecompanies have begun the process of emerging frombankruptcy and may have reduced levels of debt and othercompetitive advantages over other telecommunicationscompanies. Due to these and other factors, the risk level ofowning the securities of telecommunications companies hasincreased substantially and may continue to rise.

Federal legislat ion governing the United Statestelecommunications industry may become subject to judicialreview and additional interpretation, which may adverselyaffect the companies whose securities are held by the Trust.Moreover, continued consolidation in this industry couldcreate integration expenses and delay, and consequentmanagement diversion of attention away from ongoingoperations and related risks, among other factors, couldresult in the failure of these companies to realize expectedcost savings or synergies.

Utilities. The Trust invests in utility companies. Manyutility companies, especially electric and gas and otherenergy related utility companies, are subject to variousuncertainties, including:

• risks of increases in fuel and other operatingcosts;

• restrictions on operations and increased costsand delays as a result of environmental, nuclearsafety and other regulations;

• regulatory restrictions on the ability to passincreasing wholesale costs along to the retailand business customer;

• coping with the general effects of energyconservation;

• technological innovations which may renderexisting plants, equipment or products obsolete;

• the effects of unusual, unexpected or normallocal weather, maturing markets and difficulty inexpanding to new markets due to regulatory andother factors;

• the potential impact of natural or man-madedisasters;

• difficulty obtaining adequate returns on investedcapital, even if frequent rate increases areapproved by public service commissions;

• the high cost of obtaining financing duringperiods of inflation;

• difficulties of the capital markets in absorbingutility debt and equity securities; and

• increased competition.

Any of these factors, or a combination of these factors,could affect the supply of or demand for energy, such aselectricity or natural gas, or water, or the ability of the issuersto pay for such energy or water which could adversely affectthe profitability of the issuers of the Securities and theperformance of the Trust.

Utility companies are subject to extensive regulation atthe federal and state levels in the United States. At thefederal level, the Federal Energy Regulatory Commission(the “FERC”), the Federal Trade Commission (the “FTC”),the Securities and Exchange Commission (the “SEC”), andthe Nuclear Regulatory Commission (the “NRC”) haveauthority to oversee electric and combination electric andgas utilities. The value of utility company stocks maydecline because governmental regulation affecting theutilities industry can change. This regulation may prevent ordelay the utility company from passing along cost increasesto its customers, which could hinder the utility company’sability to meet its obligations to its suppliers and could leadto the taking of measures, including the acceleration ofobligations or the institution of involuntary bankruptcyproceedings, by its creditors against such utility company.Furthermore, regulatory authorities, which may be subjectto political and other pressures, may not grant future rateincreases, or may impose accounting or operationalpolicies, any of which could adversely affect a company’sprofitability and its stock price.

Certain utility companies have experienced full or partialderegulation in recent years. These utility companies arefrequently more similar to industrial companies in that they aresubject to greater competition and have been permitted byregulators to diversify outside of their original geographic

A-7

regions and their traditional lines of business. Theseopportunities may permit certain utility companies to earnmore than their traditional regulated rates of return. Somecompanies, however, may be forced to defend their corebusiness and may be less profitable. Mergers in the utilityindustry may require approval from several federal and stateregulatory agencies, including the FERC, the FTC, and theSEC. These regulatory authorities could, as a matter of policy,reverse the trend toward deregulation and make consolidationmore difficult, or cause delay in the merger process, any ofwhich could cause the prices of these stocks to fall.

Foreign Issuers. The Trust may invest in stocks offoreign companies. These stocks involve additional risks thatdiffer from an investment in domestic stocks. These risksinclude the risk of losses due to future political andeconomic developments, international trade conditions,foreign withholding taxes and restrictions on foreigninvestments and exchange of securities. The Trust may alsoinvolve the risk that fluctuations in exchange rates betweenthe U.S. dollar and foreign currencies may negatively affectthe value of the stocks. The Trust may involve the risk thatinformation about the stocks is not publicly available or isinaccurate due to the absence of uniform accounting andfinancial reporting standards. In addition, some foreignsecurities markets are less liquid than U.S. markets. Thiscould cause the Trust to buy stocks at a higher price or sellstocks at a lower price than would be the case in a highlyliquid market. Foreign securities markets are often morevolatile and involve higher trading costs than U.S. markets,and foreign companies, securities markets and brokers arealso generally not subject to the same level of supervisionand regulation as in the U.S.

Certain stocks may be held in the form of AmericanDepositary Receipts (“ADRs”), Global Depositary Receipts(“GDRs”), or other similar receipts. ADRs and GDRsrepresent receipts for foreign common stock deposited witha custodian (which may include the Trustee). The ADRs inthe Trust, if any, trade in the U.S. in U.S. dollars and areregistered with the SEC. GDRs are receipts, issued byforeign banks or trust companies, or foreign branches ofU.S. banks, that represent an interest in shares of either aforeign or U.S. corporation. These instruments may notnecessarily be denominated in the same currency as thesecurities into which they may be converted. ADRs andGDRs generally involve the same types of risks as foreigncommon stock held directly. Some ADRs and GDRs mayexperience less liquidity than the underlying common stockstraded in their home market. The Trust may invest insponsored or unsponsored ADRs. Unlike a sponsored ADRwhere the depositary has an exclusive relationship with theforeign issuer, an unsponsored ADR may be created by adepositary institution independently and without thecooperation of the foreign issuer. Consequently, informationconcerning the foreign issuer may be less current or reliablefor an unsponsored ADR and the price of an unsponsoredADR may be more volatile than if it was a sponsored ADR.

Depositaries of unsponsored ADRs are not required todistribute shareholder communications received from theforeign issuer or to pass through voting rights to its holders.The holders of unsponsored ADRs generally bear all thecosts associated with establishing the unsponsored ADR,whereas the foreign issuers typically bear certain costs in asponsored ADR.

Legislation/Litigation. From time to time, variouslegislative initiatives are proposed in the United States andabroad which may have a negative impact on certain of theissuers whose Securities are held by the Trust. In addition,litigation regarding any of these issuers or of the industriesrepresented by these issuers may negatively impact theshare prices of their Securities, or on the tax treatment ofyour Trust or of your investment in the Trust. No one canpredict what impact any pending or threatened litigation willhave on the share prices of the Securities, which mayadversely affect the value of your Units.

No FDIC Guarantee. An investment in the Trust is nota deposit of any bank and is not insured or guaranteed bythe Federal Deposit Insurance Corporation or any othergovernment agency.

PUBLIC OFFERING

General. Units are offered at the Public Offering Pricewhich consists of the underlying value of the Securities, thesales charge, and cash, if any, in the Income and CapitalAccounts. The maximum sales charge assessed to eachUnitholder is 3.50% of the Public Offering Price (3.627% ofthe aggregate value of the Securities). A portion of thePublic Offering Price includes an amount of Securities to payfor all or a portion of the costs incurred in establishing theTrust, including the cost of preparing documents relating tothe Trust (such as the prospectus, trust agreement andclosing documents, federal and state registration fees, theinitial fees and expenses of the Trustee and legal and auditexpenses). In the event that Units continue to be offered onor after the first anniversary of the Initial Date of Deposit ofthe Trust, beginning on July 20, 2011, and on each July 20thereafter, the secondary market sales charge will bereduced by 0.5% to a minimum of 2.00%. The actual salescharge that may be paid by an investor may differ slightlyfrom the sales charges shown herein due to rounding thatoccurs in the calculation of the Public Offering Price and inthe number of Units purchased.

The minimum purchase is 200 Units but may vary byselling firm.

Reducing Your Sales Charge. The Sponsor offers avariety of ways for you to reduce the sales charge that youpay. It is your financial professional’s responsibility to alertthe Sponsor of any discount when you purchase Units.Before you purchase Units you must also inform yourfinancial professional of your qualification for any discount orof any combined purchases to be eligible for a reducedsales charge. You may not combine discounts.

A-8

Large Quantity Purchases. You can reduce your salescharge by increasing the size of your investment. If youpurchase the amount of Units shown in the table belowduring the initial offering period, the sales charge will beas follows:

Aggregate Units Purchased Sales Charge____________________________ ______________

Less than 2,500 . . . . . . . . . . . . . . . . . . . . . 3.50%2,500 - 24,999 . . . . . . . . . . . . . . . . . . . . . . 2.5025,000 - 99,999 . . . . . . . . . . . . . . . . . . . . 1.90100,000 or more . . . . . . . . . . . . . . . . . . . . 1.40

Except as described below, these quantity discountlevels apply only to purchases of Units made by the sameperson on a single day from a single broker-dealer. We applythese sales charges as a percent of the Public Offering Priceper Unit at the time of purchase. We also apply the differentpurchase levels on a Unit basis using a $10 Unit equivalent.For example, if you purchase between 2,500 and 24,999Units of the Trust, your sales charge will be 2.50% of yourPublic Offering Price per Unit.

For purposes of achieving these levels you may combinepurchases of Units of the Trust offered in this prospectuswith purchases of units of any other Van Kampen-sponsored unit investment trust in the initial offering period.In addition, Units purchased in the name of your spouse orchildren under 21 living in the same household as you willbe deemed to be additional purchases by you for thepurposes of calculating the applicable quantity discountlevel. The reduced sales charge levels wi l l a lso beapplicable to a trustee or other fiduciary purchasing Unitsfor a single trust, estate (including multiple trusts createdunder a single estate) or fiduciary account. To be eligible foraggregation as described in this paragraph, all purchasesmust be made on the same day through a single broker-dealer or selling agent. You must inform your broker-dealerof any combined purchases before your purchase to beeligible for a reduced sales charge.

Rollovers and Exchanges. During the initial offering periodof the Trust, unitholders of any Van Kampen-sponsored unitinvestment trusts and unitholders of unaffi l iated unitinvestment trusts may utilize their redemption or terminationproceeds from such a trust to purchase Units of the Trust atthe Public Offering Price per Unit less 1.00%. In order to beeligible for the sales charge discounts applicable to Unitpurchases made with redemption or termination proceedsfrom other unit investment trusts, the termination orredemption proceeds used to purchase Units of the Trustmust be derived from a transaction that occurred within 30days of your Unit purchase. In addition, the discounts willonly be available for investors that utilize the same financialprofessional (or a different financial professional withappropriate notification) for both the Unit purchase and thetransaction resulting in the receipt of the termination orredemption proceeds used for the Unit purchase. You maybe required to provide appropriate documentation or other

information to your financial professional to evidence youreligibility for these reduced sales charge discounts. Anexchange does not avoid a taxable event on the redemptionor termination of an interest in a trust.

Employees. Employees, officers and directors (includingtheir spouses and children under 21 living in the samehousehold, and trustees, custodians or fiduciaries for thebenefit of such persons) of Van Kampen Funds Inc. and itsaffiliates, and financial professionals and their affiliates maypurchase Units at the Public Offering Price less theapplicable dealer concession. All employee discounts aresubject to the policies of the related selling firm. Onlyemployees, officers and directors of companies that allowtheir employees to participate in this employee discountprogram are eligible for the discounts.

Distribution Reinvestments. We do not charge any salescharge when you reinvest distributions from your Trust intoadditional Units of your Trust.

Unit Price. The Public Offering Price of Units will varyfrom the amounts stated under “Essential Information” inaccordance with fluctuations in the prices of the underlyingSecurities in the Trust. The initial price of the Securities upondeposit by the Sponsor was determined by the Trustee. TheTrustee will generally determine the value of the Securitiesas of the Evaluation Time on each business day and willadjust the Public Offering Price of Units accordingly. The“Evaluation Time” is the close of trading on the New YorkStock Exchange on each Trust business day. The term“business day”, as used herein and under “Rights ofUnitholders--Redemption of Units”, means any day onwhich the New York Stock Exchange is open for regulartrading. The Public Offering Price per Unit will be effectivefor all orders received prior to the Evaluation Time on eachbusiness day. Orders received by the Sponsor prior to theEvaluation Time and orders received by authorized financialprofessionals prior to the Evaluation Time that are properlytransmitted to the Sponsor by the time designated by theSponsor, are priced based on the date of receipt. Ordersreceived by the Sponsor after the Evaluation Time, andorders received by authorized financial professionals afterthe Evaluation Time or orders received by such persons thatare not transmitted to the Sponsor until after the timedesignated by the Sponsor, are priced based on the date ofthe next determined Public Offering Price per Unit providedthey are received timely by the Sponsor on such date. It isthe responsibility of authorized financial professionals totransmit orders received by them to the Sponsor so they willbe received in a timely manner.

The value of Securities is based on the Securities’ marketprices when available. When a market price is not readilyavailable, including circumstances under which the Trusteedetermines that a Security’s market price is not accurate, aSecurity is valued at its fair value, as determined underprocedures established by the Trustee or an independentpricing service used by the Trustee. In these cases, theTrust’s net asset value will reflect certain Securities’ fair value

A-9

rather than their market price. With respect to Securitiesthat are primarily listed on foreign exchanges, the value ofthe Securities may change on days when you will not beable to purchase or sell Units. The value of any foreignSecurities is based on the applicable currency exchangerate as of the Evaluation Time. The Sponsor will provideprice dissemination and oversight services to the Trust.

During the initial offering period, part of the PublicOffering Price represents an amount that will pay the costsincurred in establishing the Trust. These costs include thecosts of preparing documents relating to the Trust (such asthe registration statement, prospectus, trust agreement andlegal documents), federal and state registration fees, theinitial fees and expenses of the Trustee and the initial audit.Your Trust will sell Securities to reimburse the Sponsor forthese costs at the end of the initial offering period or after sixmonths, if earlier. The value of your Units will decline whenthe Trust pays these costs.

In offering the Units to the public, neither the Sponsor norany broker-dealers are recommending any of the individualSecurities but rather the entire pool of Securities, taken as awhole, which are represented by the Units.

Unit Distribution. Units will be distributed to the publicby the Sponsor and the Underwriter at the Public OfferingPrice. Units repurchased in the secondary market, if any,may be offered by this prospectus at the secondary marketPublic Offering Price in the manner described above.

The Sponsor intends to qualify Units for sale in a numberof states. The Underwriter will be allowed a concession oragency commission in connection with the distribution ofUnits as described under “Sponsor and UnderwriterCompensation”.

In addit ion to the regular concession or agencycommission set forth in the table above, all broker-dealersand other selling firms will be eligible to receive additionalcompensation based on total initial offering period sales ofall eligible Van Kampen unit investment trusts during aQuarterly Period as set forth in the following table:

Initial Offering Period VolumeSales During Quarterly Period Concession______________________________ ____________

$2 million but less than $5 million . . . . . . . . 0.025%$5 million but less than $10 million . . . . . . . 0.050$10 million but less than $50 million . . . . . . 0.075$50 million or more . . . . . . . . . . . . . . . . . . 0.100

“Quarterly Period” means the following periods: January –March; April – June; July – September; and October –December. Broker-dealers and other selling firms will notreceive these additional volume concessions on the sale ofunits which are not subject to the transactional salescharge; however, such sales will be included in determiningwhether a firm has met the sales level breakpoints set forthin the table above. Secondary market sales of all unitinvestment trusts are excluded for purposes of thesevolume concessions. The Sponsor will pay these amounts

out of the transactional sales charge received on units withina reasonable time following each Quarterly Period. For atrust to be eligible for this additional compensation forQuarterly Period sales, the trust’s prospectus must includedisclosure related to this additional compensation; a trust isnot el igible for this addit ional compensation i f theprospectus for such trust does not include disclosurerelated to this additional compensation.

Any sales charge discount provided to investors will beborne by the selling broker-dealer or agent as indicatedunder “General” above. Notwithstanding anything to thecontrary herein, in no case shal l the total of anyconcessions, agency commissions and any additionalcompensation allowed or paid to any broker, dealer andother selling firms of Units with respect to any individualtransaction exceed the total sales charge applicable to suchtransaction. The Sponsor reserves the right to reject, inwhole or in part, any order for the purchase of Units and tochange the amount of the concession or agencycommission to dealers and others from time to time.

The Sponsor may provide, at its own expense and out ofits own profits, additional compensation and benefits tobroker-dealers and other selling firms who sell Units of thisTrust and the Sponsor’s other products. This compensationis intended to result in additional sales of the Sponsor’sproducts and/or compensate broker-dealers and otherselling firms for past sales. The Sponsor may make thesepayments for marketing, promotional or related expenses,including, but not limited to, expenses of entertaining retailcustomers and financial advisors, advertising, sponsorshipof events or seminars, obtaining shelf space in broker-dealerfirms and similar activities designed to promote the sale ofthe Trust and the Sponsor’s other products. Fees mayinclude payment for travel expenses, including lodging,incurred in connection with trips taken by invited registeredrepresentatives for meetings or seminars of a businessnature. These arrangements will not change the price youpay for your Units.