CEF Energy Info Day - European Commission · CEF Energy Info Day . ... Financing of PCI energy...

19

Cormac Murphy, New Products and Special Transactions 7/04/16 CEF Energy Info Day EIB Financial Instruments Brussels, 7 th April 2016

Transcript of CEF Energy Info Day - European Commission · CEF Energy Info Day . ... Financing of PCI energy...

Cormac Murphy, New Products and Special Transactions

7/04/16

CEF Energy Info Day

EIB Financial Instruments

Brussels, 7th April 2016

Financing of PCI energy projects

Generally financed by TSO’s on the corporate (regulated asset) balance sheet.

In more limited cases (given RAB etc. restrictions) financed on a project (SPV) basis with support from the TSO or potentially merchant risk.

Novel structures under development such as regulatory cap and floor mechanisms.

Need for CEF financial products that can support the different forms of financing but especially corporate/RAB balance sheet funding, which accounts for the bulk of investment.

Associated tool box of financial instruments from senior loans to credit enhancement and higher risk instruments to potential equity.

Need for a wide range of financial instruments for PCI’s in energy

7/04/16 2

EIB operations

7/04/16 3

EIB ‘higher-risk’ debt instruments under CEF/EFSI

4 European Investment Bank

EFSI-CEF Financial Instruments

Project Finance

Corporate

Credit enhancement Project Bonds

Credit enhancement Loans

Senior Loans

Hybrid Debt products

Capital markets

Banking market

Airports

Ports

TSOs

Products

Corporates

Corporate Bond Guarantees

Corporate Subordinated Debt

Transport Authorities

9/07/2015

Senior Loans Guarantees

Project Finance Borrowers

Project Financing

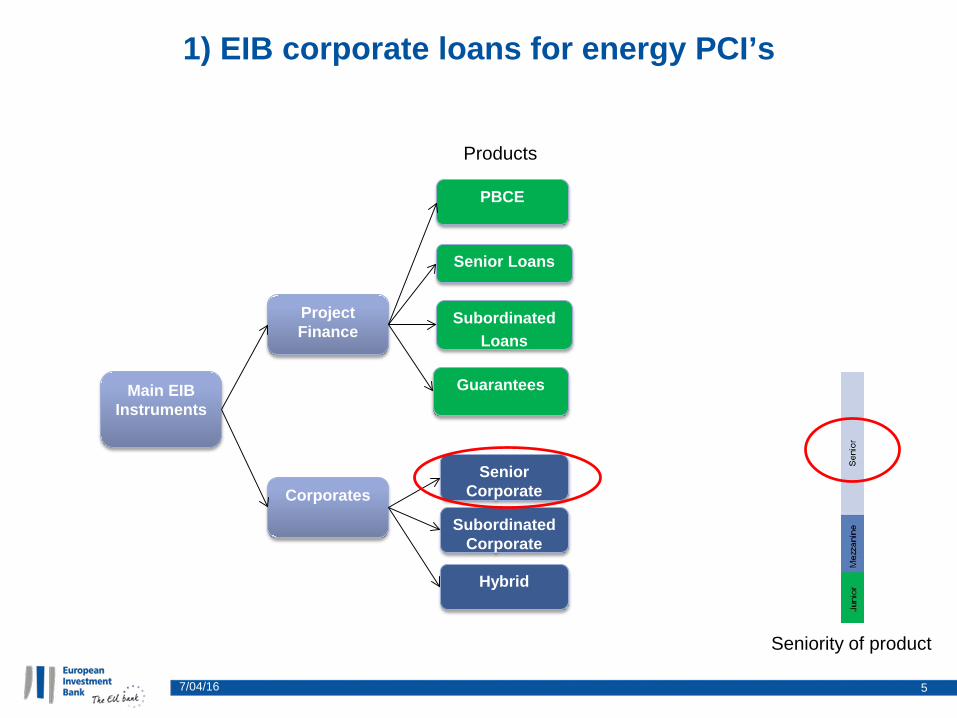

1) EIB corporate loans for energy PCI’s

Main EIB Instruments

Project Finance

Corporates

PBCE

Guarantees

Senior Corporate

Subordinated Corporate

Products

Senior Loans

Subordinated Loans

Hybrid

Seniority of product

7/04/16 5

2) EIB project finance loans

Main EIB Instruments

Project Finance

Corporates

PBCE /SDCE

Senior Corporate

Subordinated Corporate

Capital markets

Banking market

Products

Senior Loans

Subordinated Loans

Hybrid

Seniority of product

7/04/16 6

Project financing

Long term senior debt offered on a non-recourse project (SPV) basis

PPP/IPP type structures with underlying revenue source – potentially a regulatory income stream but also possibly merchant risk in well structured project

May also apply to large project based financing (e.g. LNG, pipelines), which use project financing techniques including long term supply/offtaker arrangements

Traditionally limited use of project financing by TSO’s given perceived complexity, costs and regulatory restrictions on ownership

7/04/2016 7 European Investment Bank

3) Credit enhancement

Main EIB Instruments

Project Finance

Corporates

PBCE /SDCE

Senior Corporate

Subordinated Corporate

Capital markets

Banking market

Products

Senior Loans

Subordinated Loans

Hybrid

Seniority of product

7/04/16 8

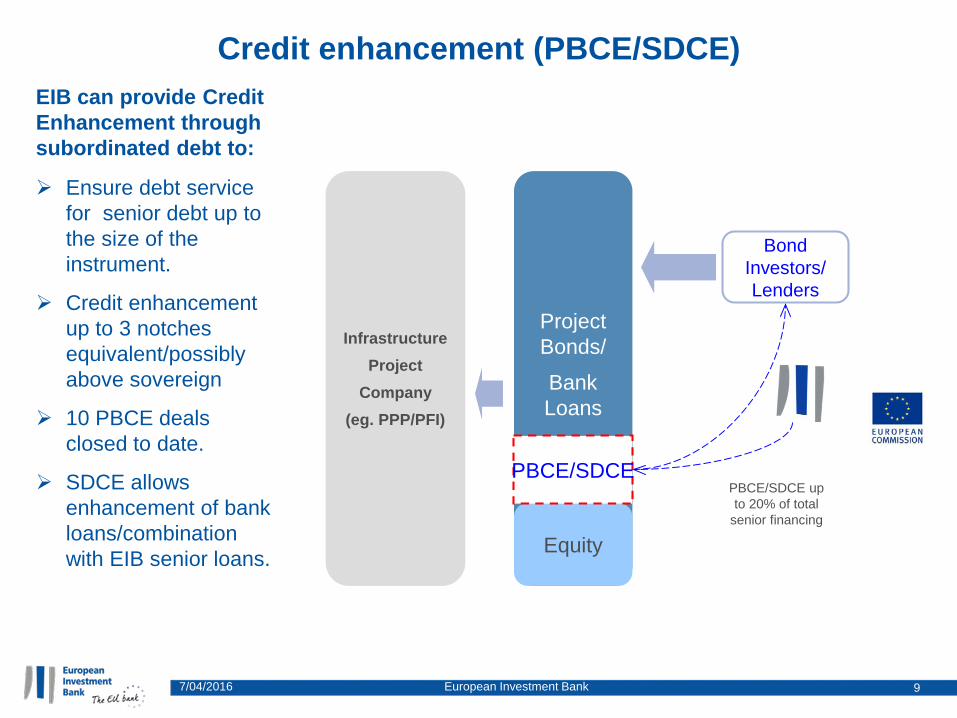

Credit enhancement (PBCE/SDCE) EIB can provide Credit Enhancement through subordinated debt to:

Ensure debt service for senior debt up to the size of the instrument.

Credit enhancement up to 3 notches equivalent/possibly above sovereign

10 PBCE deals closed to date.

SDCE allows enhancement of bank loans/combination with EIB senior loans.

Project Bonds/

Bank Loans

PBCE/SDCE up to 20% of total

senior financing

Infrastructure Project

Company (eg. PPP/PFI)

Equity

Bond Investors/ Lenders

PBCE/SDCE

9 7/04/2016 European Investment Bank

PBCE / SDCE

Enhancement of project bonds (PBCE):

Access to new funding sources to institutional investors.

Long tenors possible (e.g. 40 years for Calais harbour project).

Enhancement of senior loan (SDCE):

Total financing cost can be more economical (depending on the project).

Improves attractiveness for senior lenders (mitigates economic risk like ramp–up risk, demand risk, etc.).

7/04/2016 10 European Investment Bank

11

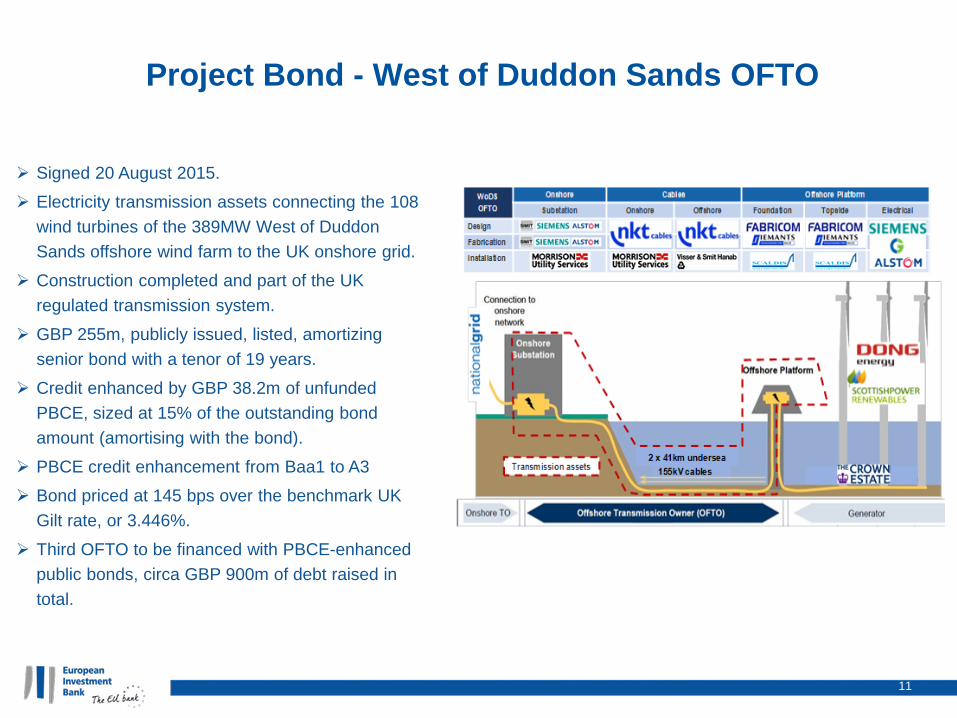

Project Bond - West of Duddon Sands OFTO

Signed 20 August 2015.

Electricity transmission assets connecting the 108 wind turbines of the 389MW West of Duddon Sands offshore wind farm to the UK onshore grid.

Construction completed and part of the UK regulated transmission system.

GBP 255m, publicly issued, listed, amortizing senior bond with a tenor of 19 years.

Credit enhanced by GBP 38.2m of unfunded PBCE, sized at 15% of the outstanding bond amount (amortising with the bond).

PBCE credit enhancement from Baa1 to A3

Bond priced at 145 bps over the benchmark UK Gilt rate, or 3.446%.

Third OFTO to be financed with PBCE-enhanced public bonds, circa GBP 900m of debt raised in total.

4) Corporate Subordinated Debt

Main EIB Instruments

Project Finance

Corporates

PBCE

Guarantees

Senior Corporate

Subordinated Corporate

Products

Senior Loans

Subordinated Loans

Hybrid

Seniority of product

7/04/16 12

3a) Corporate subordinated debt: Tailored product for Energy PCI’s: Hybrids

Main EIB Instruments

Project Finance

Corporates

PBCE

Guarantees

Senior Corporate

Subordinated Corporate

Capital markets

Banking market

Products

Senior Loans

Subordinated Loans

Hybrid

Seniority of product

7/04/16 13

zh

Case study: Hybrids for European utilities

Investment Rationale: Hybrid securities provide

benefits for both Corporate Issuers and Institutional Investors.

Hybrids equity recognition can be achieved in different proportions depending on the product structure.

The equity recognition provides flexibility and ratio protection for the issuer balance sheet.

Source : GS Hybrid presentation

The hybrids have become a common product for European utility corporates for credit ratio protection through equity content.

7/04/16 14

Hybrid bonds issued by European utilities

7/04/16 15

Why has the EIB developed a hybrid product? Utilities need to invest significant resources to maintain, expand and

interconnect the European Electricity and Gas markets.

In general, the construction phase of projects does not generate revenues and may put pressure on the corporate balance sheet.

Hybrids allow for an efficient financing alternative for projects during the construction period mitigating the debt exposure during this period.

The EIB mandates under the EFSI and CEF programs allow for higher risk taking approach.

More affordable financing for utilities type may accelerate the investment decision of utilities in new assets in line with the EFSI and CEF mandates.

EIB senior debt and hybrids products can be combined.

Hybrid offers a higher risk taking approach under EFSI/CEF with stronger credit counterparts that develop large infrastructure projects in the energy space.

7/04/16 16

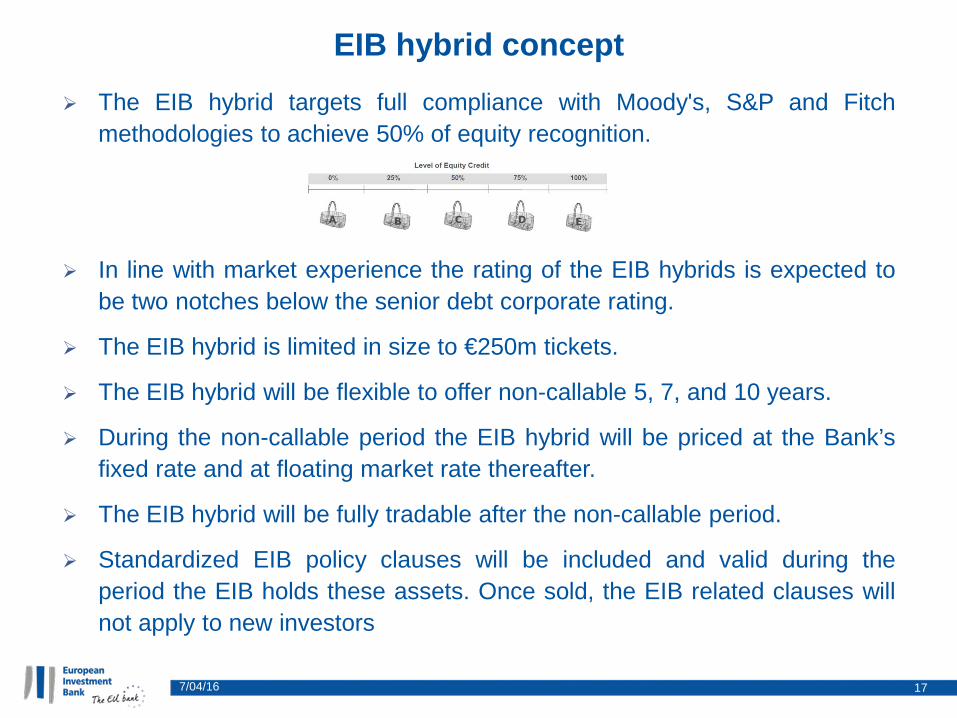

EIB hybrid concept The EIB hybrid targets full compliance with Moody's, S&P and Fitch

methodologies to achieve 50% of equity recognition.

In line with market experience the rating of the EIB hybrids is expected to be two notches below the senior debt corporate rating.

The EIB hybrid is limited in size to €250m tickets.

The EIB hybrid will be flexible to offer non-callable 5, 7, and 10 years.

During the non-callable period the EIB hybrid will be priced at the Bank’s fixed rate and at floating market rate thereafter.

The EIB hybrid will be fully tradable after the non-callable period.

Standardized EIB policy clauses will be included and valid during the period the EIB holds these assets. Once sold, the EIB related clauses will not apply to new investors

7/04/16 17

Investment rationale

EIB can provide hybrid securities as a complement to traditional lending for financing projects in the utility sector.

A hybrid product by giving partial equity recognition for 5-10 years provides flexibility/incentives for corporates who invest in projects with longer term (+ 5 years) payback cash flow.

As a balance sheet product, it also provides investment headroom beyond typical project based financing.

Can optimise WACC for issuers.

Additional issuance to match capex programme subject to corporate counterpart limits (currently €250M).

7/04/16 18