Case Study - Google Acquisition Plan

31

Modeling for M&A Deal Case Study: Google Acquisition Plan

-

Upload

rabismita-basu -

Category

Documents

-

view

133 -

download

0

Transcript of Case Study - Google Acquisition Plan

Modeling for M&A Deal

Case Study: Google Acquisition Plan

Part A

Google Business and Acquisition Plan

1.0 Introduction

Google is a global technology leader focused on improving the ways people connect with

information. Google maintains the largest, most comprehensive index of web sites and other

content and make this information freely available to anyone with an internet connection.

Google’s automated search technology helps people obtain nearly-instant access to relevant

information from our vast online index.

2.0 Revenue Source

Google’s revenue is generated almost entirely from advertising. Google’s advertising revenue is

generated each time an individual clicks on a Google web ad (“AdWords” program). In order to

increase the availability of Google search engine and expand the scope of its web

advertisements, Google have created “AdSense.” In this program, web publishers can place the

Google search box and targeted ads on their website in exchange for a percentage of the

AdWords advertising revenue. The AdSense program has been responsible for a large portion of

Google’s growth and accounted for 44% of advertising revenues in 2010

3.0 Competitors

Google face formidable competition in every aspect of its business, particularly from other

companies that seek to connect people with information on the web and provide them with

relevant advertising. Currently Google consider its primary competitors to be Microsoft and

Yahoo. Google held 45% of the US search market, Yahoo 28% and Microsoft 12%. They are

formidable opponents as both companies have had a presence in the web longer than Google and

both have tremendous financial and technical resources.

4.0 SWOT Analysis

Google strength is its strong brand, high quality product, financial resources and high caliber

employees. Google’s primary weakness is its lack of diversification. The usage of internet is

expanding and Google having first mover advantage is looking at it as an opportunity. The

convergence of internet and video related media is of particular interest to Google. However, in

recent times the competition is becoming fierce posing a threat before Google.

5.0 Mission/Vision

Google mission is to organize the world’s information and make it universally accessible and

useful.

� Google will do its best to provide the most relevant and useful search results possible, independent of financial incentives. Its search results will be objective and it will not accept payment for inclusion or ranking in them.

� It will do its best to provide the most relevant and useful advertising. Advertisements should not be an annoying interruption. If any element on a search result page is influenced by payment to Google, it will make it clear to its users.

� Google will never stop working to improve its user experience, its search technology and other important areas of information organization

6.0 Business Strategy

Google’s business strategy is based on its mission to organize all of the world’s information and

make it useful and universally accessible. Google primary business strategy is product

differentiation. Google’s search engine uses a unique formula to retrieve pertinent information

based on the user’s request. The formula gives Google users a more thorough and detailed

search then other search engines. The formula utilizes page rank and hypertext matching

technologies to determine the importance of a web site by analyzing the link structure of the

web.

Google AdWords product is its mechanism for differentiating Google from other internet

advertising competitors. AdWords was developed to allow advertisers to target a specific group

of prospected customers. It is beneficial to advertisers because it is an efficient way to target

customers and advertisers only pay when their advertisements are viewed.

7.0 Implementation Plan

Google has historically used acquisition as a method to accomplish its strategic objectives. Past

acquisitions have included Pyra Labs in 2003, Picasa, Inc. (a digital photo management

company) in 2004, Keyhole Corp (a digital and satellite mapping company) in 2003, and Urchin

software (a web analytics firm) in March 2005. The company created its search engine and the

majority of its other products through this strategy. As Google continues to grow and looks to

diversify its product line, it has become practical to incorporate acquisitions into its

implementation strategy.

8.0 Google Acquisition Objectives

Google’s objectives in pursuing an acquisition are as follows:

� First-mover advantages in convergence of media and technology � Product differentiation � Product diversification, overcoming weaknesses (e.g. reliance on one technology) � Increased advertising revenue � Expansion into new media markets � Expansion into new distribution channels

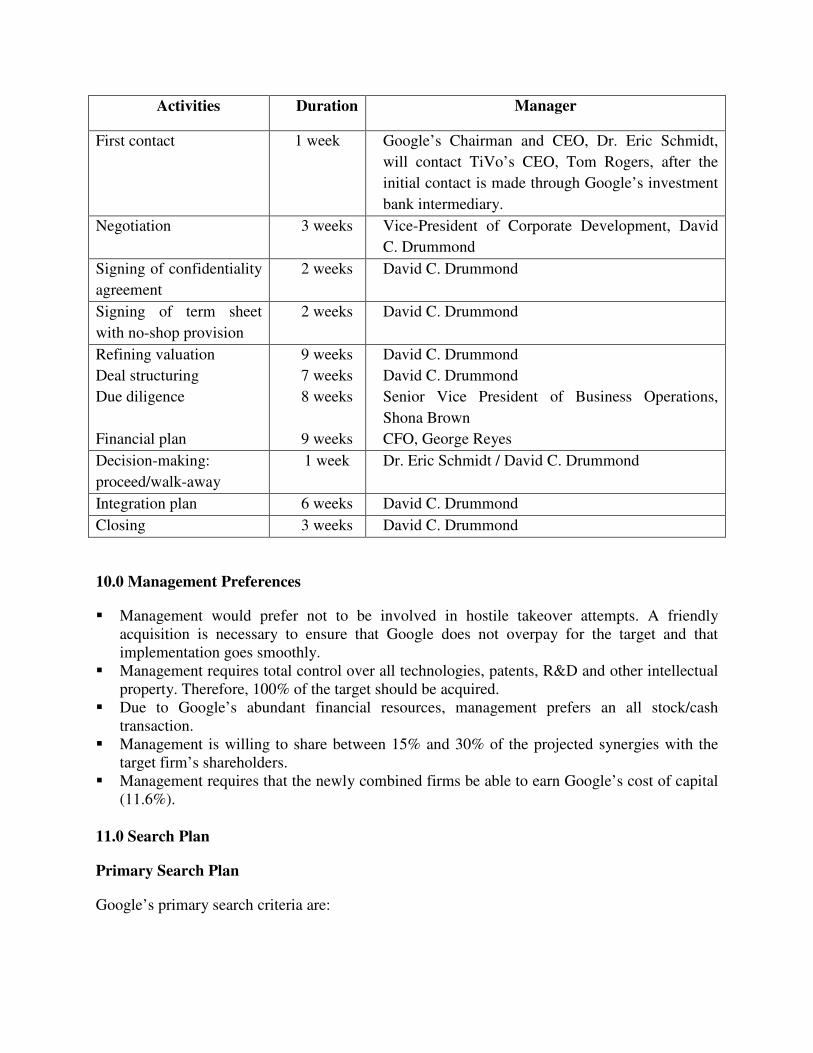

9.0 Timetable

Activities Duration Manager

First contact 1 week Google’s Chairman and CEO, Dr. Eric Schmidt,

will contact TiVo’s CEO, Tom Rogers, after the

initial contact is made through Google’s investment

bank intermediary.

Negotiation 3 weeks Vice-President of Corporate Development, David

C. Drummond

Signing of confidentiality

agreement

2 weeks David C. Drummond

Signing of term sheet

with no-shop provision

2 weeks David C. Drummond

Refining valuation

Deal structuring

Due diligence

Financial plan

9 weeks

7 weeks

8 weeks

9 weeks

David C. Drummond

David C. Drummond

Senior Vice President of Business Operations,

Shona Brown

CFO, George Reyes

Decision-making:

proceed/walk-away

1 week Dr. Eric Schmidt / David C. Drummond

Integration plan 6 weeks David C. Drummond

Closing 3 weeks David C. Drummond

10.0 Management Preferences

� Management would prefer not to be involved in hostile takeover attempts. A friendly acquisition is necessary to ensure that Google does not overpay for the target and that implementation goes smoothly.

� Management requires total control over all technologies, patents, R&D and other intellectual property. Therefore, 100% of the target should be acquired.

� Due to Google’s abundant financial resources, management prefers an all stock/cash transaction.

� Management is willing to share between 15% and 30% of the projected synergies with the target firm’s shareholders.

� Management requires that the newly combined firms be able to earn Google’s cost of capital (11.6%).

11.0 Search Plan

Primary Search Plan

Google’s primary search criteria are:

� The target must be in the Entertainment/ Media Distribution industry. � The target should have intellectual property assets in new entertainment technologies that

will help Google to introduce products that take advantage of opportunities related to media and technology convergence.

� The target’s value should not exceed $20 billion.

Search Strategy

The initial search generated the following list of potential candidates: TiVo, Cox Digital Cable,

Comcast Cable, Cisco (owner of Scientific Atlantic, a manufacturer of set- top boxes), and Echo

Star Communications.

Secondary Criteria

Google secondary criteria include:

� The target must have significant brand equity and market share. � The target should be a publicly traded company. � The target should be located near Google’s Mountain View, CA headquarters (west coast,

preferably in California).

12.0 Target Selection

TiVo has been selected as the acquisition target, chosen for its large market share, recognized

brand name, and numerous partnerships and licenses. The acquisition of TiVo would provide

Google the vehicle to expand into new media markets. Google is the leader in the internet

industry and TiVo is the leader in interactive television. Google can use TiVo’s expertise to

enter people’s homes through new mediums. Google’s profits are generated primarily from

advertising and TiVo offers technology that allows advertisers to deliver relevant, engaging

content and special offers in a more compelling way.

The acquisition will also serve as a diversification opportunity for Google. One of its primary

weaknesses is our lack of product diversification. A merger with TiVo allows Google to position

itself not just a search engine company, reducing dependence on a single technology. Also, it

would allow us to differentiate ourselves from our primary competitors (Yahoo and Microsoft),

similar to AOL’s goal to distinguish itself as the leader in online entertainment with their merger

with Time Warner. Google is number one in internet search and it would be easy to transfer

those competencies to the entertainment field. Acquiring TiVo will allow them to position

themselves as number one in several fields of information – internet, television, and

entertainment.

Internet and television, the two largest forms of media, are converging and an increasing number

of viewers are interested in technologies which bring them together. By acquiring TiVo, Google

has the opportunity to capitalize on significant first-mover advantages and establish itself as the

leader in interactive media. Other companies, such as Microsoft’s WebTV, have tried to

combine internet and TV but have failed. This is most likely due the fact that they are internet

companies expanding into an industry of which they have little knowledge. By using TiVo’s

expertise Google can branch into a new market with minimal risk. Google will benefit from

TiVo’s knowledge of producing premium set-top boxes, entering consumer’s homes through

television, and other relevant information

Google has been under increasing pressure to maintain growth rates. An acquisition of TiVo

would allow it to increase its connection with consumers, and its brand awareness and

recognition. Consumers would be exposed to the Google brand every time they turn on their

television or access the internet.

The financial performances as well as projections of Google are presented below.

Google Financial Performance and Projections

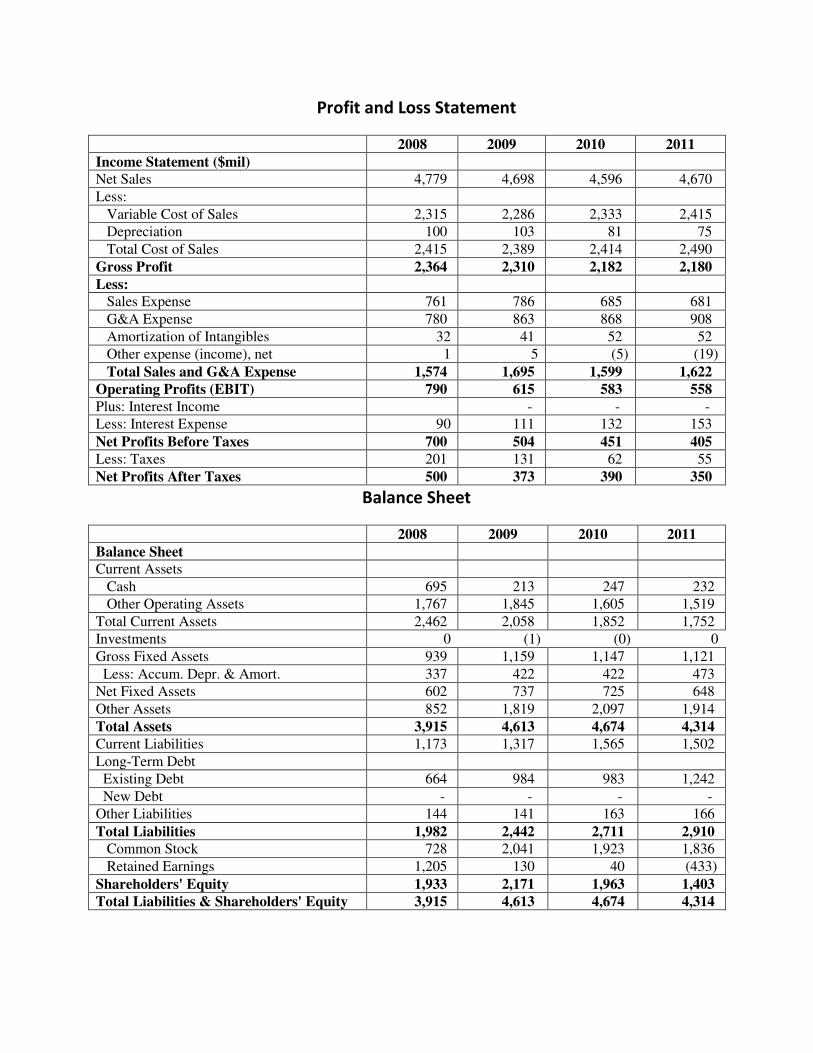

Profit and Loss Statement

2008 2009 2010 2011

Income Statement ($mil)

Net Sales 4,779 4,698 4,596 4,670

Less:

Variable Cost of Sales 2,315 2,286 2,333 2,415

Depreciation 100 103 81 75

Total Cost of Sales 2,415 2,389 2,414 2,490

Gross Profit 2,364 2,310 2,182 2,180

Less:

Sales Expense 761 786 685 681

G&A Expense 780 863 868 908

Amortization of Intangibles 32 41 52 52

Other expense (income), net 1 5 (5) (19)

Total Sales and G&A Expense 1,574 1,695 1,599 1,622 Operating Profits (EBIT) 790 615 583 558 Plus: Interest Income - - -

Less: Interest Expense 90 111 132 153

Net Profits Before Taxes 700 504 451 405 Less: Taxes 201 131 62 55

Net Profits After Taxes 500 373 390 350

Balance Sheet

2008 2009 2010 2011

Balance Sheet

Current Assets

Cash 695 213 247 232

Other Operating Assets 1,767 1,845 1,605 1,519

Total Current Assets 2,462 2,058 1,852 1,752

Investments 0 (1) (0) 0

Gross Fixed Assets 939 1,159 1,147 1,121

Less: Accum. Depr. & Amort. 337 422 422 473

Net Fixed Assets 602 737 725 648

Other Assets 852 1,819 2,097 1,914

Total Assets 3,915 4,613 4,674 4,314 Current Liabilities 1,173 1,317 1,565 1,502

Long-Term Debt

Existing Debt 664 984 983 1,242

New Debt - - - -

Other Liabilities 144 141 163 166

Total Liabilities 1,982 2,442 2,711 2,910 Common Stock 728 2,041 1,923 1,836

Retained Earnings 1,205 130 40 (433)

Shareholders' Equity 1,933 2,171 1,963 1,403 Total Liabilities & Shareholders' Equity 3,915 4,613 4,674 4,314

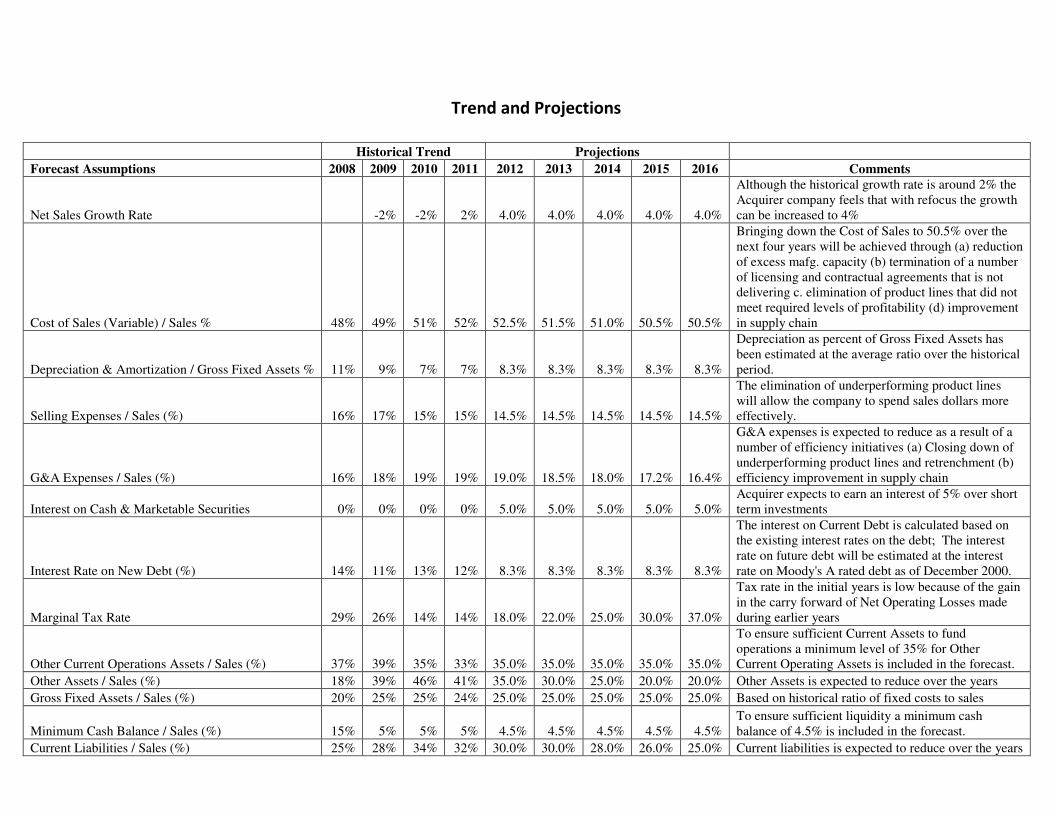

Trend and Projections

Historical Trend Projections

Forecast Assumptions 2008 2009 2010 2011 2012 2013 2014 2015 2016 Comments

Net Sales Growth Rate -2% -2% 2% 4.0% 4.0% 4.0% 4.0% 4.0%

Although the historical growth rate is around 2% the Acquirer company feels that with refocus the growth can be increased to 4%

Cost of Sales (Variable) / Sales % 48% 49% 51% 52% 52.5% 51.5% 51.0% 50.5% 50.5%

Bringing down the Cost of Sales to 50.5% over the next four years will be achieved through (a) reduction of excess mafg. capacity (b) termination of a number of licensing and contractual agreements that is not delivering c. elimination of product lines that did not meet required levels of profitability (d) improvement in supply chain

Depreciation & Amortization / Gross Fixed Assets % 11% 9% 7% 7% 8.3% 8.3% 8.3% 8.3% 8.3%

Depreciation as percent of Gross Fixed Assets has been estimated at the average ratio over the historical period.

Selling Expenses / Sales (%) 16% 17% 15% 15% 14.5% 14.5% 14.5% 14.5% 14.5%

The elimination of underperforming product lines will allow the company to spend sales dollars more effectively.

G&A Expenses / Sales (%) 16% 18% 19% 19% 19.0% 18.5% 18.0% 17.2% 16.4%

G&A expenses is expected to reduce as a result of a number of efficiency initiatives (a) Closing down of underperforming product lines and retrenchment (b) efficiency improvement in supply chain

Interest on Cash & Marketable Securities 0% 0% 0% 0% 5.0% 5.0% 5.0% 5.0% 5.0% Acquirer expects to earn an interest of 5% over short term investments

Interest Rate on New Debt (%) 14% 11% 13% 12% 8.3% 8.3% 8.3% 8.3% 8.3%

The interest on Current Debt is calculated based on the existing interest rates on the debt; The interest rate on future debt will be estimated at the interest rate on Moody's A rated debt as of December 2000.

Marginal Tax Rate 29% 26% 14% 14% 18.0% 22.0% 25.0% 30.0% 37.0%

Tax rate in the initial years is low because of the gain in the carry forward of Net Operating Losses made during earlier years

Other Current Operations Assets / Sales (%) 37% 39% 35% 33% 35.0% 35.0% 35.0% 35.0% 35.0%

To ensure sufficient Current Assets to fund operations a minimum level of 35% for Other Current Operating Assets is included in the forecast.

Other Assets / Sales (%) 18% 39% 46% 41% 35.0% 30.0% 25.0% 20.0% 20.0% Other Assets is expected to reduce over the years

Gross Fixed Assets / Sales (%) 20% 25% 25% 24% 25.0% 25.0% 25.0% 25.0% 25.0% Based on historical ratio of fixed costs to sales

Minimum Cash Balance / Sales (%) 15% 5% 5% 5% 4.5% 4.5% 4.5% 4.5% 4.5% To ensure sufficient liquidity a minimum cash balance of 4.5% is included in the forecast.

Current Liabilities / Sales (%) 25% 28% 34% 32% 30.0% 30.0% 28.0% 26.0% 25.0% Current liabilities is expected to reduce over the years

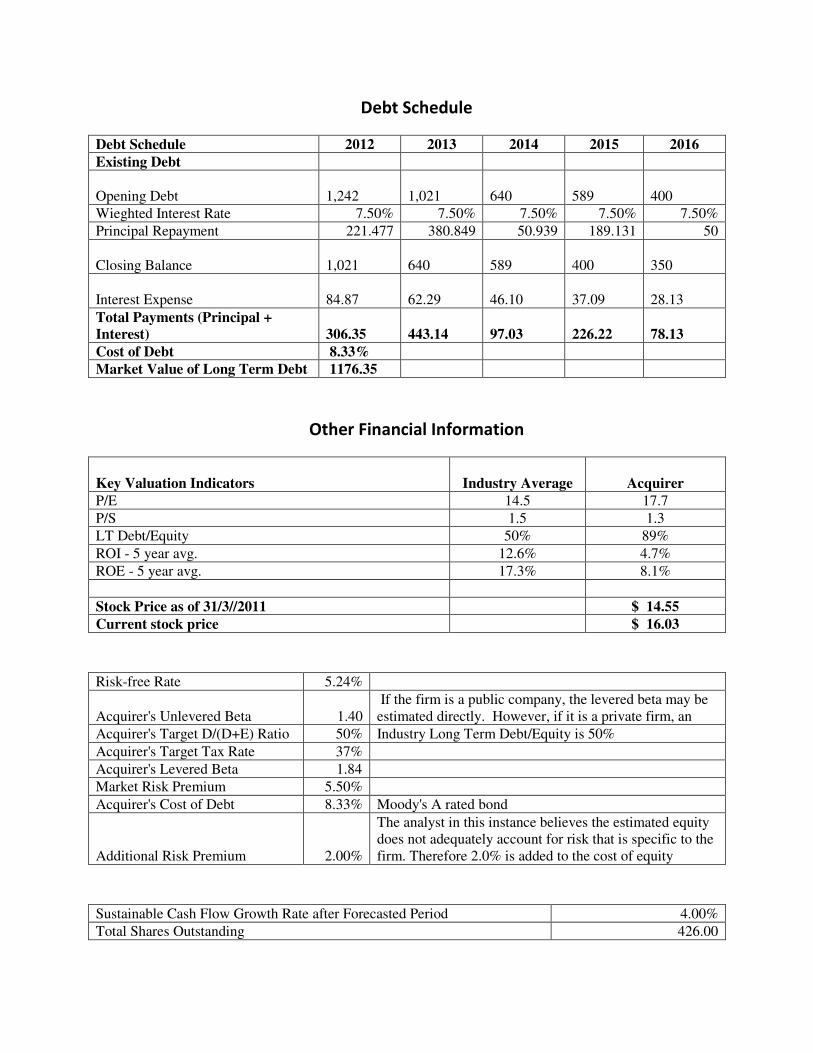

Debt Schedule

Debt Schedule 2012 2013 2014 2015 2016

Existing Debt

Opening Debt 1,242

1,021

640

589

400

Wieghted Interest Rate 7.50% 7.50% 7.50% 7.50% 7.50%

Principal Repayment 221.477 380.849 50.939 189.131 50

Closing Balance 1,021

640

589

400

350

Interest Expense 84.87

62.29

46.10

37.09

28.13

Total Payments (Principal + Interest)

306.35

443.14

97.03

226.22

78.13

Cost of Debt 8.33%

Market Value of Long Term Debt 1176.35

Other Financial Information

Key Valuation Indicators Industry Average Acquirer P/E 14.5 17.7

P/S 1.5 1.3

LT Debt/Equity 50% 89%

ROI - 5 year avg. 12.6% 4.7%

ROE - 5 year avg. 17.3% 8.1%

Stock Price as of 31/3//2011 $ 14.55

Current stock price $ 16.03

Risk-free Rate 5.24%

Acquirer's Unlevered Beta 1.40 If the firm is a public company, the levered beta may be estimated directly. However, if it is a private firm, an

Acquirer's Target D/(D+E) Ratio 50% Industry Long Term Debt/Equity is 50%

Acquirer's Target Tax Rate 37%

Acquirer's Levered Beta 1.84

Market Risk Premium 5.50%

Acquirer's Cost of Debt 8.33% Moody's A rated bond

Additional Risk Premium 2.00%

The analyst in this instance believes the estimated equity does not adequately account for risk that is specific to the firm. Therefore 2.0% is added to the cost of equity

Sustainable Cash Flow Growth Rate after Forecasted Period 4.00%

Total Shares Outstanding 426.00

Part B

Tivo the Target

1.0 Introduction

TiVo was developed by Jim Barton and Mike Ramsay through a corporation they named

"Teleworld" which was later renamed to TiVo, Inc. Though they originally intended to create a

home network device; it was redesigned as a device that records digitized video onto a hard disk.

They began the first public trials of the TiVo device and service in late 1998 in the San Francisco

Bay Area.

2.0 Tivo DVR

A TiVo DVR serves a function similar to a videocassette recorder, in that both allow a television

viewer to record programming for viewing at a later time. Unlike a videocassette recorder

(VCR), which uses removable magnetic tape cartridges, a TiVo DVR stores television programs

on an internal hard drive that can only be removed by disassembling the device? What

distinguishes TiVo from other DVRs is the sophisticated software written by TiVo Inc. that

automatically records programs — not only those the user specifically requests, but also other

material in which the user is likely to be interested. TiVo DVRs also implement a patented

feature TiVo calls "trick play," allowing the viewer to pause live television and rewind and

replay up to a half hour of recently viewed television. More recent TiVo DVRs can be connected

to a computer local area network, allowing the TiVo device to download information and even

video programs, music and movies from the Internet.

3.0 Functions

TiVo polls its network, receiving program information including description, regular and guest

actors, directors, genres, whether programs are new or repeats, and whether broadcast is in High

Definition (HD). Information is updated daily from Tribune Media Services. Users can select

individual programs to record or a "Season Pass" to record an entire season (or more). There are

options to record First Run Only, First Run and Repeats, or All Episodes. An episode is

considered "First Run" if aired within two weeks of that episode's initial air date. When user's

requests for multiple programs are conflicting, the lower priority program in the Season Pass

Manager is either not recorded or clipped where times overlap. The lower priority program will

be recorded if it is aired later. TiVo DVRs with two tuners record the top two priority programs.

TiVo pioneered recording programs based on household viewing habits; this is called TiVo

Suggestions. Users can rate programs from three "thumbs up" to three "thumbs down." TiVo

user ratings are combined to create a recommendation, based on what TiVo users with similar

viewing habits watch. For example, if a user likes American Idol, America's Got Talent and

Dancing with the Stars, then another TiVo user who watched just the American Idol might get a

recommendation for the other two shows.

A limited amount of space is available to store programs. When the space is full, the oldest

programs are deleted to make space for the newer ones; programs that users flag to not be

deleted are kept and TiVo Suggestions are always lowest priority. The recording capacity of a

TiVo HD DVR can be expanded with an external hard drive, which can add 65 additional hours

of HD recording space or up to 600 hours of standard definition video recording capacity.

When not recording specific user requests, the current channel is recorded for up to 30 minutes.

Dual-tuner models record two channels. This allows users to rewind or pause anything that has

been shown in the last thirty minutes — useful when viewing is interrupted. Shows already in

progress can be entirely recorded if less than 30 minutes have been shown. Unlike VCRs, TiVo

can record and play at the same time. A program can be watched from the beginning even if it's

in the middle of being recorded, which is something that VCRs cannot do. Some users take

advantage of this by waiting 10 to 15 minutes after a program starts (or is replayed from a

recording), so that they can fast forward through commercials. In this way, by the end of the

recording viewers are caught up with live television.

Unlike most DVRs, TiVo DVRs are easily connected to home networks, allowing users to

schedule recordings on TiVo's website (via TiVo Central Online), transfer recordings between

TiVo units (Multi-Room Viewing (MRV)) or to/from a home computer (TiVoToGo transfers),

play music and view photos over the network, and access third-party applications written for

TiVo's Home Media Engine (HME) API.

TiVo has added a number of broadband features, including integration with Amazon Video on

Demand, Jaman.com and Netflix Watch Instantly, offering users access to thousands of movie

titles and television shows right from the comfort of their couch. Additionally, broadband

connected to TiVo boxes can access digital photos from Picasa Web Albums or Photobucket.

Another popular feature is access to Rhapsody music through TiVo, allowing users to listen to

virtually any song from their living room. TiVo also teamed up with One True Media to give

subscribers a private channel for sharing photos and video with family and friends. They can also

access weather, traffic, Fandango movie listings (including ticket purchases), and music through

Live365. In the summer of 2008 TiVo announced the availability of YouTube videos on TiVo.

4.0 Subscription

The information that a TiVo DVR downloads regarding television schedules, as well as software

updates and any other relevant information is available through a monthly service subscription in

the United States. A different model applies in Australia where the TiVo media device is bought

for a one-off fee, without further subscription costs.

There are multiple types of Product Lifetime Service. For satellite enabled TiVo DVRS the

lifetime subscription remains as long as the account is active and does not follow a specific piece

of hardware. This satellite lifetime subscription cannot be transferred to another person. Toshiba

and Pioneer Tivo DVD recording equipped units include a "Basic Lifetime Subscription", which

is very similar to full lifetime, except only three days of the program guide is viewable and

search and Internet capabilities are not available, or at least limited. All units (except satellite but

including DVD units) are able to have "Product Lifetime Subscription" to the TiVo service

which covers the life of the TiVo DV, not the life of the subscriber. The Product Lifetime

Subscription accompanies the TiVo DVR in case of ownership transfer. TiVo makes no

warranties or representations as to the expected lifetime of the TiVo DVR (aside from the

manufacturer's Limited Warranty). In the past TiVo has offered multiple "Trade Up" programs

where you could transfer the Product Lifetime Subscription from an old unit to a newer model

with a fee. A Tivo can be used without a service agreement, but it will act more like a VCR in

that you can only do manual recordings. And the Tivo can't be connected to the Tivo service for

time or software updates or changes or Tivo will shut down the recording function.

5.0 Competitors

While its former main competitor, ReplayTV, had adopted a commercial-skip feature, TiVo

decided to avoid automatic implementation fearing such a move might provoke backlash from

the television industry. ReplayTV was sued over this feature as well as the ability to share shows

over the Internet, and these lawsuits contributed to the bankruptcy of SONICblue, their owner at

the time. Their new owner, DNNA, dropped both features in the final ReplayTV model, the

5500.

Other distributors' competing DVR sets include Comcast and Verizon, although both distribute

third-party hardware from manufacturers such as Motorola and the former Scientific Atlanta unit

of Cisco Systems with this functionality built-in. Verizon uses boxes fitted for FiOS, allowing

high-speed Internet access and other features.

As of January 2012, TiVo has approximately 2.3 million subscribers. Despite having gained

234,000 subscribers in the last quarter of 2011. This is down from a peak of 4.36 million in

January 2010.

6.0 Strategic Directions

Tivo has the first mover advantage and started with a lot of optimism. However, soon the

competition sets in and Tivo could not attain the growth it has forecasted. The market dynamics

have changed in recent times with change in technology and needs of the customer. The

convergence of internet and media has changed the way the contents were delivered. Tivo

management feels that they need to adapt to the changing market to continue to be in the race.

Tivo does not have enough resources in terms of finance and skill to upgrade itself into a web

based company. The other significant players in this segment have tied up with web based

companies or in the process of merging with them. Tivo got an initial offer from Google Inc. for

acquisition. The Board is considering the acquisition proposal from Google.

The financial performance and the projections is presented below.

Tivo Financial Performance and Projections

Profit and Loss Statement

2008 2009 2010 2011

Income Statement ($mil)

Net Sales 42 85 184 252

Less:

Variable Cost of Sales 25 49 103 141

Depreciation 1 3 5 9

Total Cost of Sales 26 52 108 150

Gross Profit 16 33 76 102

Less:

Sales Expense 6.30 13 28 38

G&A Expense 5.60 11 24 43

Amortization of Intangibles - - - -

Other expense (income), net 2) 0 1 (4) (15)

Total Sales and G&A Expense 12 25 47 66

Operating Profits (EBIT) 4 9 29 37

Plus: Interest Income - - 2 4

Less: Interest Expense 0 0 - -

Net Profits Before Taxes 3 8 30 40

Less: Taxes 1 2 8 12

Net Profits After Taxes 2.8 6 22 29

Balance Sheet

Historical Financials 2008 2009 2010 2011 Balance Sheet Current Assets

Cash 3 12 97 43

Other Operating Assets 12 16 61 86

Total Current Assets 15 29 158 129

Investments 0 0 (0) 0

Gross Fixed Assets 4 6 17 30

Less: Accum. Depr. & Amort. 1 2 5 11

Net Fixed Assets 3 4 12 19

Other Assets 26 26 64 101

Total Assets 44 59 233 249 Current Liabilities 12 15 44 42

Long-Term Debt

Existing Debt 6 6 0 1

New Debt - - - -

Other Liabilities 0 0 1 1

Total Liabilities 18 21 45 45 Common Stock 22 27 155 144

Retained Earnings 4 11 32 61

Shareholders' Equity 26 38 188 205

Total Liabilities & Shareholders' Equity 44 59 233 249

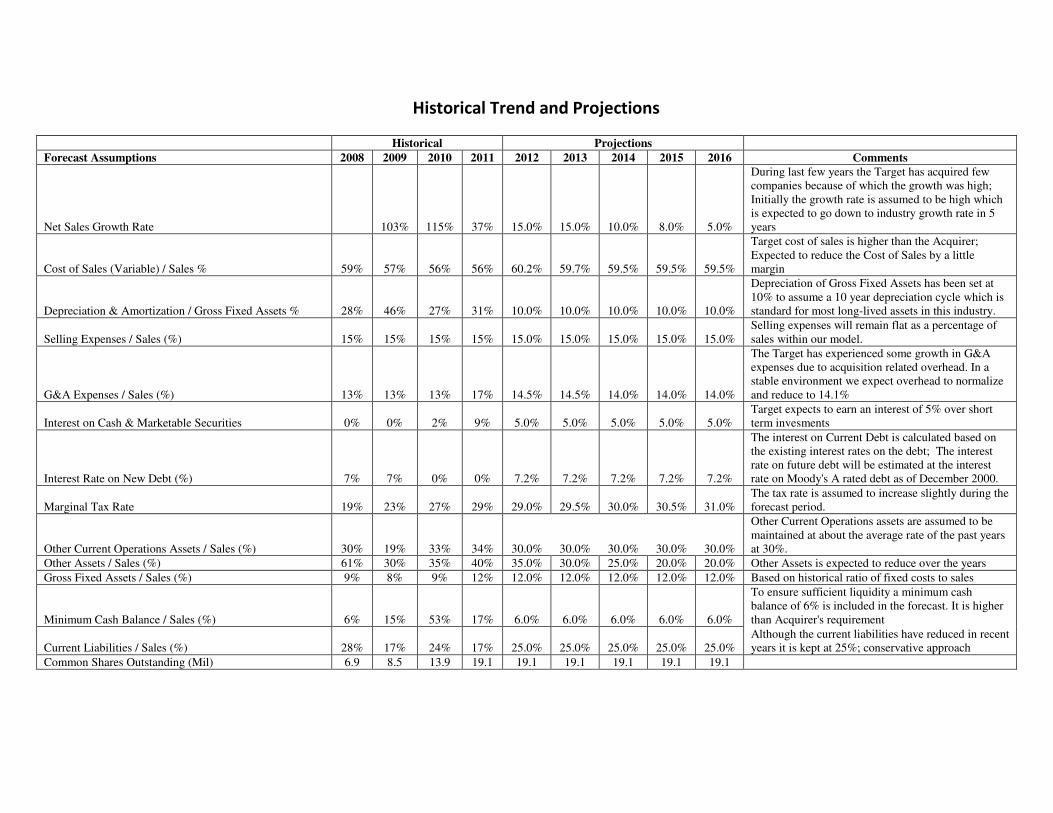

Historical Trend and Projections

Historical Projections

Forecast Assumptions 2008 2009 2010 2011 2012 2013 2014 2015 2016 Comments

Net Sales Growth Rate 103% 115% 37% 15.0% 15.0% 10.0% 8.0% 5.0%

During last few years the Target has acquired few companies because of which the growth was high; Initially the growth rate is assumed to be high which is expected to go down to industry growth rate in 5 years

Cost of Sales (Variable) / Sales % 59% 57% 56% 56% 60.2% 59.7% 59.5% 59.5% 59.5%

Target cost of sales is higher than the Acquirer; Expected to reduce the Cost of Sales by a little margin

Depreciation & Amortization / Gross Fixed Assets % 28% 46% 27% 31% 10.0% 10.0% 10.0% 10.0% 10.0%

Depreciation of Gross Fixed Assets has been set at 10% to assume a 10 year depreciation cycle which is standard for most long-lived assets in this industry.

Selling Expenses / Sales (%) 15% 15% 15% 15% 15.0% 15.0% 15.0% 15.0% 15.0% Selling expenses will remain flat as a percentage of sales within our model.

G&A Expenses / Sales (%) 13% 13% 13% 17% 14.5% 14.5% 14.0% 14.0% 14.0%

The Target has experienced some growth in G&A expenses due to acquisition related overhead. In a stable environment we expect overhead to normalize and reduce to 14.1%

Interest on Cash & Marketable Securities 0% 0% 2% 9% 5.0% 5.0% 5.0% 5.0% 5.0% Target expects to earn an interest of 5% over short term invesments

Interest Rate on New Debt (%) 7% 7% 0% 0% 7.2% 7.2% 7.2% 7.2% 7.2%

The interest on Current Debt is calculated based on the existing interest rates on the debt; The interest rate on future debt will be estimated at the interest rate on Moody's A rated debt as of December 2000.

Marginal Tax Rate 19% 23% 27% 29% 29.0% 29.5% 30.0% 30.5% 31.0% The tax rate is assumed to increase slightly during the forecast period.

Other Current Operations Assets / Sales (%) 30% 19% 33% 34% 30.0% 30.0% 30.0% 30.0% 30.0%

Other Current Operations assets are assumed to be maintained at about the average rate of the past years at 30%.

Other Assets / Sales (%) 61% 30% 35% 40% 35.0% 30.0% 25.0% 20.0% 20.0% Other Assets is expected to reduce over the years

Gross Fixed Assets / Sales (%) 9% 8% 9% 12% 12.0% 12.0% 12.0% 12.0% 12.0% Based on historical ratio of fixed costs to sales

Minimum Cash Balance / Sales (%) 6% 15% 53% 17% 6.0% 6.0% 6.0% 6.0% 6.0%

To ensure sufficient liquidity a minimum cash balance of 6% is included in the forecast. It is higher than Acquirer's requirement

Current Liabilities / Sales (%) 28% 17% 24% 17% 25.0% 25.0% 25.0% 25.0% 25.0% Although the current liabilities have reduced in recent years it is kept at 25%; conservative approach

Common Shares Outstanding (Mil) 6.9 8.5 13.9 19.1 19.1 19.1 19.1 19.1 19.1

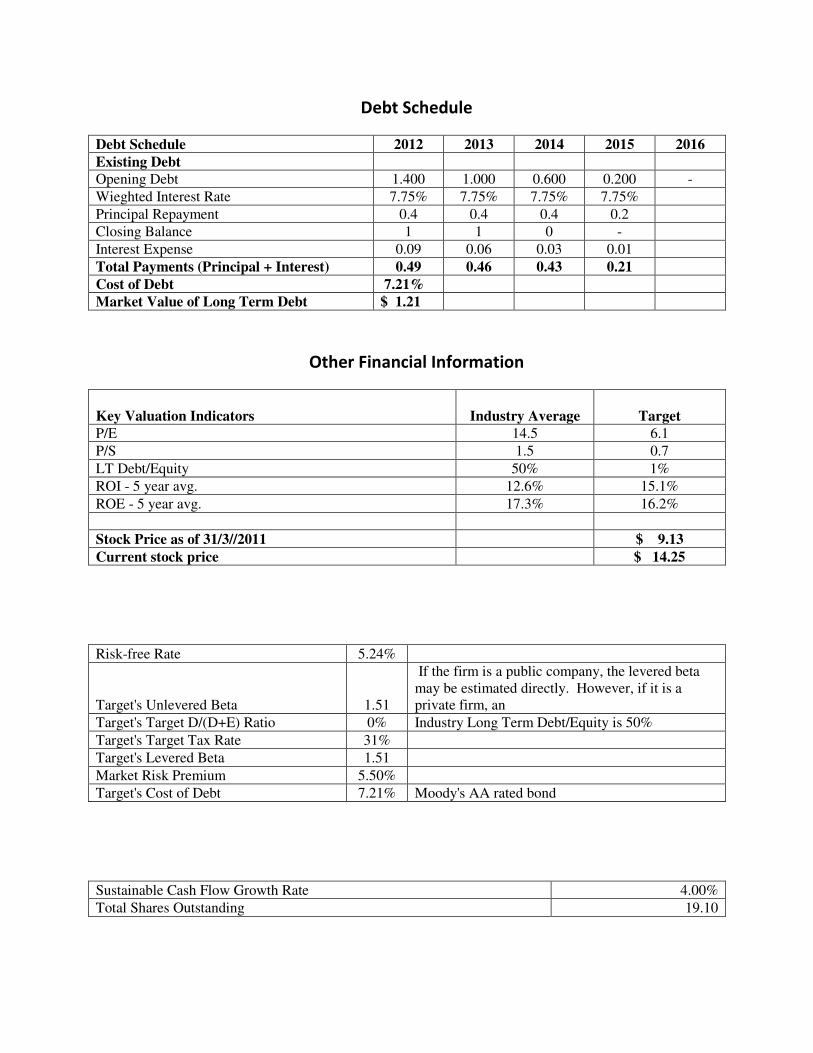

Debt Schedule

Debt Schedule 2012 2013 2014 2015 2016

Existing Debt

Opening Debt 1.400 1.000 0.600 0.200 -

Wieghted Interest Rate 7.75% 7.75% 7.75% 7.75%

Principal Repayment 0.4 0.4 0.4 0.2

Closing Balance 1 1 0 -

Interest Expense 0.09 0.06 0.03 0.01

Total Payments (Principal + Interest) 0.49 0.46 0.43 0.21

Cost of Debt 7.21%

Market Value of Long Term Debt $ 1.21

Other Financial Information

Key Valuation Indicators Industry Average Target P/E 14.5 6.1

P/S 1.5 0.7

LT Debt/Equity 50% 1%

ROI - 5 year avg. 12.6% 15.1%

ROE - 5 year avg. 17.3% 16.2%

Stock Price as of 31/3//2011 $ 9.13

Current stock price $ 14.25

Risk-free Rate 5.24%

Target's Unlevered Beta 1.51

If the firm is a public company, the levered beta may be estimated directly. However, if it is a private firm, an

Target's Target D/(D+E) Ratio 0% Industry Long Term Debt/Equity is 50%

Target's Target Tax Rate 31%

Target's Levered Beta 1.51

Market Risk Premium 5.50%

Target's Cost of Debt 7.21% Moody's AA rated bond

Sustainable Cash Flow Growth Rate 4.00%

Total Shares Outstanding 19.10

Part C

Expected Synergy from the Deal

1.0 Expected Gains from Restructuring and Control

Google could see a cross selling opportunity by acquiring Tivo. An acquisition of TiVo would

allow it to increase its connection with consumers, and its brand awareness and recognition.

Consumers would be exposed to the Google brand every time they turn on their television or

access the internet. On a conservative note, Tivo’s acquisition will help Google increase its

revenue by at least 2% every year.

Apart from the expected increase in revenue Google plans to close down the Head Office and

few other Zonal and Branch Offices of Tivo bring some reduction in redundancies and cost.

Google is currently heavily dependent on third parties to supply key elements of its internet

infrastructure including bandwidth providers, data centers etc. Acquisition of Tivo will help

Google in reducing a part of its dependencies on third part outsourcing. It plans to terminate

some of these contracts after acquisition and depend on the in house abilities of Tivo.

Google is very keen on retaining the core employees (electronics division working on the

product) of Tivo as it does not have the required expertise and skill to manage the products of

Tivo. Therefore, Google is planning to offer some additional pay to these core employees so as

to retain them.

Google have a very strong IT, Marketing and Finance division, therefore, it has planned to

retrench some of the employees working in Marketing and Finance division so as to reduce some

of the redundancies that would result after acquisition.

The details of expected synergy and cost reductions are presented below.

The expected synergy and its value are estimated in the following Tables. The category of expenses is also presented in the

Table.

1 The total annual savings of the closing of the Tivo's Head Office office will be:

(In millions) 2012 2013 2014 2015 2016 Expense Category

- Rent 250,000

0.13

0.25

0.25

0.25

0.25

50% COS/50% Sales Expense

- Elimination of 15 back office positions at $35,000 each

525,000

0.26

0.53

0.53

0.53

0.53 G&A

- Elimination of 10 professional positions at 90,000 each

900,000

0.45

0.90

0.90

0.90

0.90

50% COS/50% Sales Expense

2

As a result of the closure of the Tivo's Head Office Office the following additional expenses will be incurred in 2012: 2012 2013 2014 2015 2016 Expense Category

- 3 Months Rent 62,500 0.06 50% COS / 50% Sales Expense

- 1 Month's pay for back office positions 43,750 0.04 Integration Expense

- Average 3 months' pay for professional positions 225,000 0.23 Integration Expense

3 Termination of 3rd Party Equipment Outsourcing agreements 2012 2013 2014 2015 2016 Expense Category

3.00 9.00 12.00 12.00 12.50 100% COS

4) Termination of rental contracts: 2012 2013 2014 2015 2016

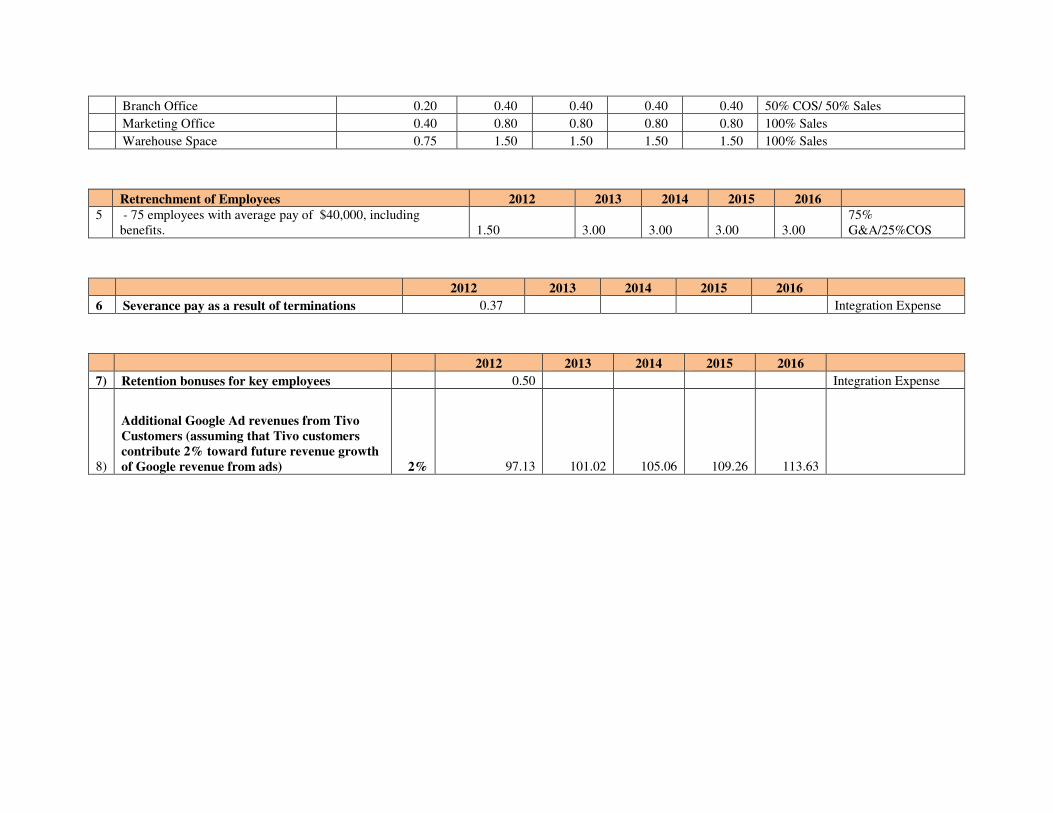

Zonal Headquarter 0.50 1.00 1.00 1.00 1.00 50% G&A/25% Sales/25% COS

Branch Office 0.20 0.40 0.40 0.40 0.40 50% COS/ 50% Sales

Marketing Office 0.40 0.80 0.80 0.80 0.80 100% Sales

Warehouse Space 0.75 1.50 1.50 1.50 1.50 100% Sales

Retrenchment of Employees 2012 2013 2014 2015 2016 5

- 75 employees with average pay of $40,000, including benefits.

1.50

3.00

3.00

3.00

3.00

75% G&A/25%COS

2012 2013 2014 2015 2016

6 Severance pay as a result of terminations 0.37 Integration Expense

2012 2013 2014 2015 2016

7) Retention bonuses for key employees 0.50 Integration Expense

8)

Additional Google Ad revenues from Tivo Customers (assuming that Tivo customers contribute 2% toward future revenue growth of Google revenue from ads) 2% 97.13 101.02 105.06 109.26 113.63

Part D

Structuring and Financing the Deal

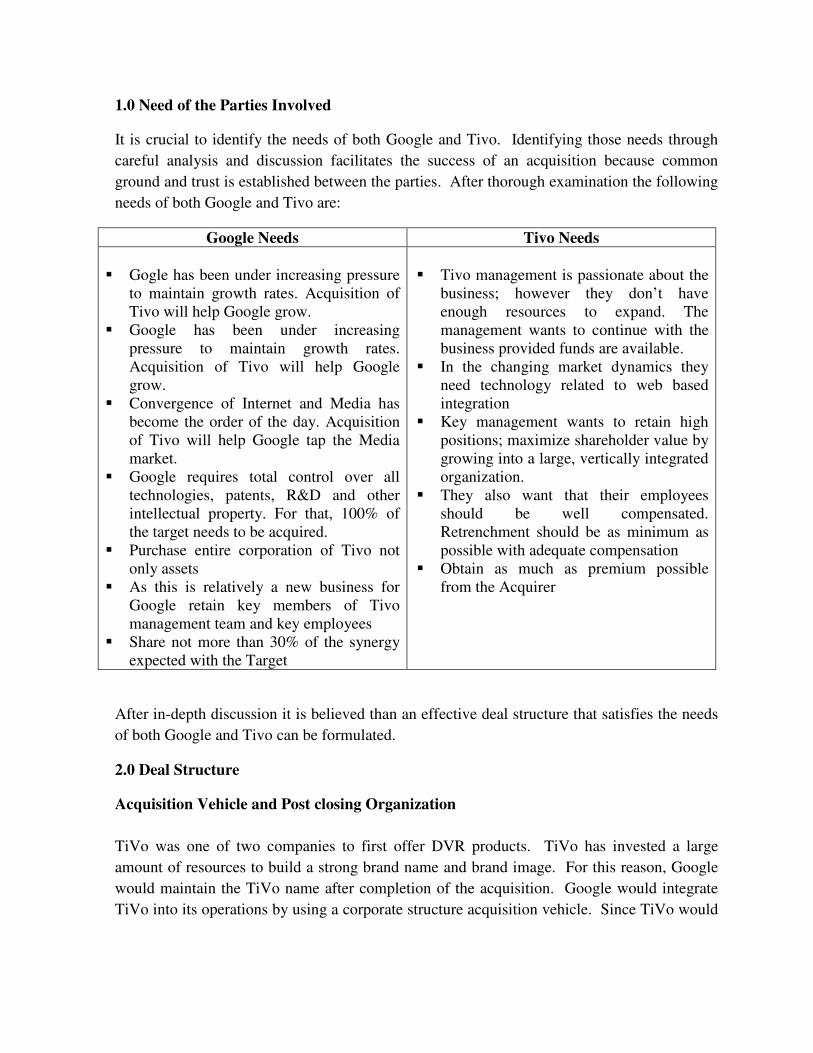

1.0 Need of the Parties Involved

It is crucial to identify the needs of both Google and Tivo. Identifying those needs through

careful analysis and discussion facilitates the success of an acquisition because common

ground and trust is established between the parties. After thorough examination the following

needs of both Google and Tivo are:

Google Needs Tivo Needs

� Gogle has been under increasing pressure to maintain growth rates. Acquisition of Tivo will help Google grow.

� Google has been under increasing pressure to maintain growth rates. Acquisition of Tivo will help Google grow.

� Convergence of Internet and Media has become the order of the day. Acquisition of Tivo will help Google tap the Media market.

� Google requires total control over all technologies, patents, R&D and other intellectual property. For that, 100% of the target needs to be acquired.

� Purchase entire corporation of Tivo not only assets

� As this is relatively a new business for Google retain key members of Tivo management team and key employees

� Share not more than 30% of the synergy expected with the Target

� Tivo management is passionate about the

business; however they don’t have enough resources to expand. The management wants to continue with the business provided funds are available.

� In the changing market dynamics they need technology related to web based integration

� Key management wants to retain high positions; maximize shareholder value by growing into a large, vertically integrated organization.

� They also want that their employees should be well compensated. Retrenchment should be as minimum as possible with adequate compensation

� Obtain as much as premium possible from the Acquirer

After in-depth discussion it is believed than an effective deal structure that satisfies the needs

of both Google and Tivo can be formulated.

2.0 Deal Structure

Acquisition Vehicle and Post closing Organization

TiVo was one of two companies to first offer DVR products. TiVo has invested a large

amount of resources to build a strong brand name and brand image. For this reason, Google

would maintain the TiVo name after completion of the acquisition. Google would integrate

TiVo into its operations by using a corporate structure acquisition vehicle. Since TiVo would

be integrated into Google at the time of acquisition, the post closing organization would be

the same as the acquisition vehicle.

Form of Acquisition and Payment

The form of acquisition would be for Google to purchase all of TiVo’s outstanding stock.

This would allow Google to gain control of all aspects of the company. Purchasing the assets

only would be more risky as it creates the possibility that Google will fail to purchase key

intellectual property or any other relevant assets provided by TiVo. Purchasing the entire

company through TiVo’s stock also presents risk as it would be assuming the cost TiVo is

incurring with the litigation it currently has with EchoStar. However, a Texas jury as already

sided with TiVo in the patent dispute and the case is currently in an appeals process where

Google feel TiVo will win. Google believes that TiVo is in a good position to win this

litigation and defend its valuable patents. In addition there is the possibility of discovering

unknown liabilities after the acquisition is completed, but Google expects that it’s due

diligence process will allow it to measure the possibility of this risk and it can account for this

during the negotiation process.

The most appropriate form of payment for TiVo is a stock-for-stock transaction. There is a

possibility of stock dilution but the expectation is that it will be small due to current amount

of Google’s shares outstanding.

Tax Considerations

Implementing a Type B stock-for-stock reorganization transaction would be beneficial to the

current shareholders of TiVo due to the transaction’s tax deferred status. This transaction

would give TiVo shareholders the ability to defer taxes until the converted shares have been

sold. In addition, Google stock has the potential for significant future capital gain.

3.0 Financing of the Deal

The TiVo acquisition would have no affect on the creditworthiness of Google. Considering

Google’s current market capitalization, cash position and expected future earnings, the TiVo

acquisition costs would not have a negative effect on Google’s financial stability. In addition,

Google’s financial success has allowed it to fund new projects and acquisitions through

retained earnings. Google has not used external funding to finance past acquisitions, but this

could change in the future.

Google is an extremely successful company. With the projected future growth of Google, net

income and revenue will grow at a high rate presenting the opportunity to acquire a company

for strategic reasons without significant negative effects on profitability.

Part E

Integration Plan

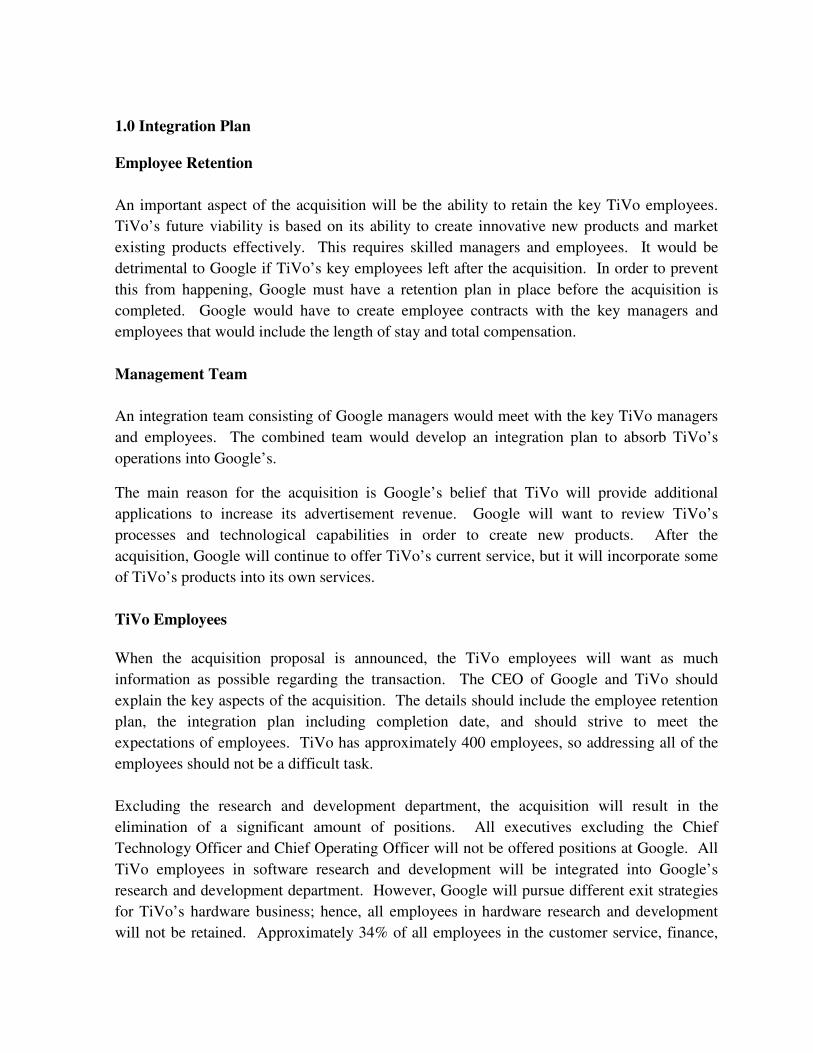

1.0 Integration Plan

Employee Retention

An important aspect of the acquisition will be the ability to retain the key TiVo employees.

TiVo’s future viability is based on its ability to create innovative new products and market

existing products effectively. This requires skilled managers and employees. It would be

detrimental to Google if TiVo’s key employees left after the acquisition. In order to prevent

this from happening, Google must have a retention plan in place before the acquisition is

completed. Google would have to create employee contracts with the key managers and

employees that would include the length of stay and total compensation.

Management Team

An integration team consisting of Google managers would meet with the key TiVo managers

and employees. The combined team would develop an integration plan to absorb TiVo’s

operations into Google’s.

The main reason for the acquisition is Google’s belief that TiVo will provide additional

applications to increase its advertisement revenue. Google will want to review TiVo’s

processes and technological capabilities in order to create new products. After the

acquisition, Google will continue to offer TiVo’s current service, but it will incorporate some

of TiVo’s products into its own services.

TiVo Employees

When the acquisition proposal is announced, the TiVo employees will want as much

information as possible regarding the transaction. The CEO of Google and TiVo should

explain the key aspects of the acquisition. The details should include the employee retention

plan, the integration plan including completion date, and should strive to meet the

expectations of employees. TiVo has approximately 400 employees, so addressing all of the

employees should not be a difficult task.

Excluding the research and development department, the acquisition will result in the

elimination of a significant amount of positions. All executives excluding the Chief

Technology Officer and Chief Operating Officer will not be offered positions at Google. All

TiVo employees in software research and development will be integrated into Google’s

research and development department. However, Google will pursue different exit strategies

for TiVo’s hardware business; hence, all employees in hardware research and development

will not be retained. Approximately 34% of all employees in the customer service, finance,

human resources, legal and marketing and sales departments will be retained. The employees

that are not retained will be given severance pay based on each employee’s job position and

length of service.

TiVo Customers and Suppliers

TiVo customers will need to be provided with assurances that their service will not be

disrupted in any way. TiVo should instruct customers about the short-term and long-term

implications of the acquisition. In the short-term TiVo will offer the same service it has

provided in the past. In the long-term customers will be provided with new and innovative

products and services.

Currently, TiVo’s DVR hardware is produced by third-party manufacturers. TiVo has

contracts with companies to manufacture and assemble the DVR. TiVo purchases the

components from a variety of vendors, but the three key suppliers are Amtek, Broadcom and

Remote Solutions. Amtek provides the chassis for the DVR’s, Broadcom supplies the

microprocessors and Remote Solutions provides the remote controls. These components are

sent to the platform manufacturers and assemblers located in China and Mexico. These

suppliers and manufacturers should be notified of the acquisition and how it will not disrupt

the current production of DVR’s. In the future, as Google incorporates TiVo’s services with

its own, management will reevaluate the viability of the hardware production unit. Exit

strategies that will minimize the effect on the hardware line of business will be considered,

such as a spin off or divestiture. The decision will depend on interest in the business by

potential suitors.

Key Integration Activities:

� Communication Program: CEO Dr. Eric Schmidt to address key issues with

employees, customers, and suppliers through regularly scheduled meetings throughout

the implementation process.

� Public Relations with Customers and Suppliers: Focus on customers, stay in contact to

make sure their needs are always satisfied.

� Restructure Advertising Contracts: Allow existing Google advertisers the option to

advertise their products through television as well as internet.

� Staffing Reorganization: Eliminate the majority of TiVo management positions. The

CTO and COO executives will be retained as they understand TiVo technology and

operations.

� Product Development Team: Structure team so that Google and TiVo employees play

an active part in creating a new product/technology that integrates Google and TiVo’s

strengths. Make sure that the team understands that their goal is creating a product that

combines search capabilities with entertainment.

� Headquarters Consolidation: Move TiVo employees to Google’s Headquarters. The

distance between TiVo’s headquarter and Google’s headquarters is a mere 8.4 miles. The

potential realized savings from closing the TiVo headquarters is approximately

$3,668,000.

� New Subscriber Campaign: Create hype about new product release to gain additional

Google/TiVo subscribers.

� New Product Release: Release to occur in early May. New product would incorporate

Google and TiVo’s strengths to converge media and technology. The new product would

keep the TiVo name but have Google based software upgrades. The test name for the

upgrades is currently the “Google Package.” The new product would link watch

consumers watch with Google AdWords.

� Website Redesign: Redesign Google’s Website to reflect its acquisition of TiVo. Redo

TiVo website to showcase new product. Create a website for the new product.

� Exit Hardware Production: Outsourcing to another hardware manufacturer, such as

Scientific Atlantic, will allow for significant cost savings.